Market Opportunities for New Diagnostics to Support Malaria Elimination Project DIAMETER (Diagnostics for Malaria Elimination Toward Eradication) Submitted to: The Bill & Melinda Gates Foundation March 26, 2014 MAILING ADDRESS PO Box 900922 Seattle, WA 98109 USA ADDRESS 2201 Westlake Avenue Suite 200 Seattle, WA 98121 USA TEL: 206.285.3500 FAX: 206.285.6619 www.path.org

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Market Opportunities for New Diagnostics to Support Malaria Elimination Project DIAMETER (Diagnostics for Malaria Elimination Toward Eradication) Submitted to: The Bill & Melinda Gates Foundation

March 26, 2014 MAIL ING ADDRESS PO Box 900922 Seattle, WA 98109 USA ADDRESS 2201 Westlake Avenue Suite 200 Seattle, WA 98121 USA TEL: 206.285.3500 FAX: 206.285.6619 www.path.org

Table of contents

Acronyms and abbreviations ...................................................................................................................... iii

Introduction .................................................................................................................................................. 1

Malaria elimination and diagnostics use ...................................................................................................... 2

The current malaria diagnostics market ....................................................................................................... 7

Country use of diagnostics for elimination and active use scenarios ......................................................... 21

The potential market for a new rapid infection detection test .................................................................... 30

Promoting investment and development of a healthy market .................................................................... 40

References .................................................................................................................................................. 47

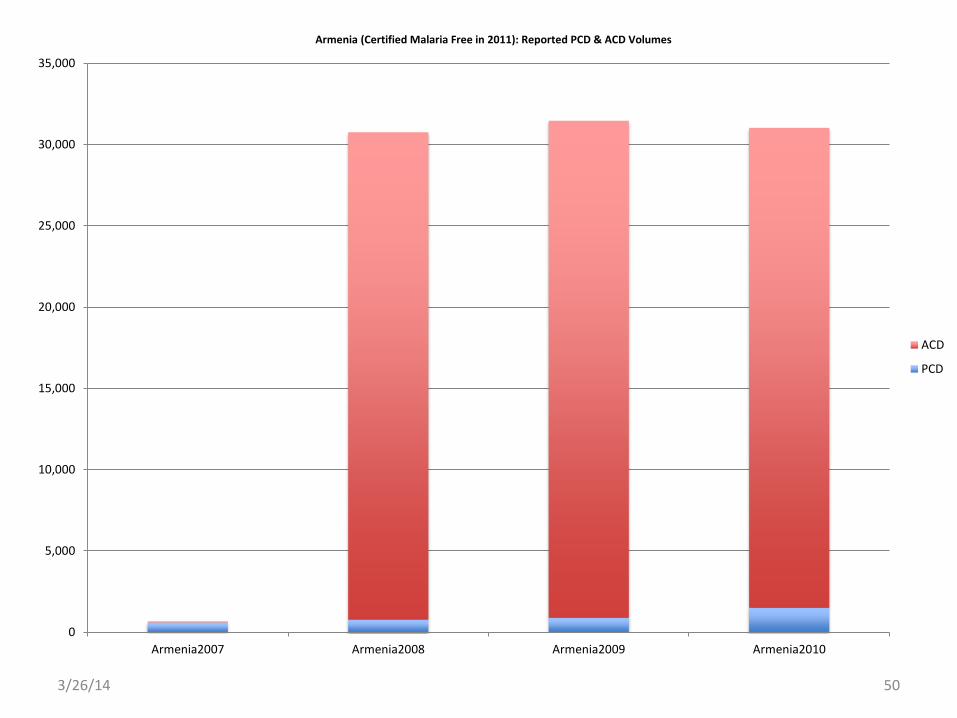

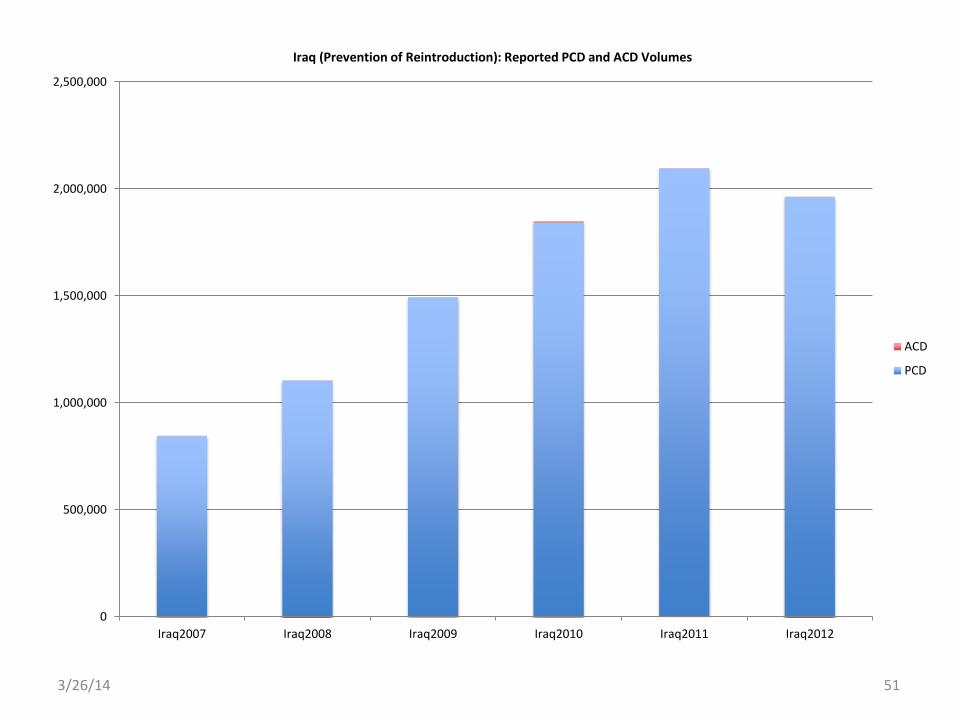

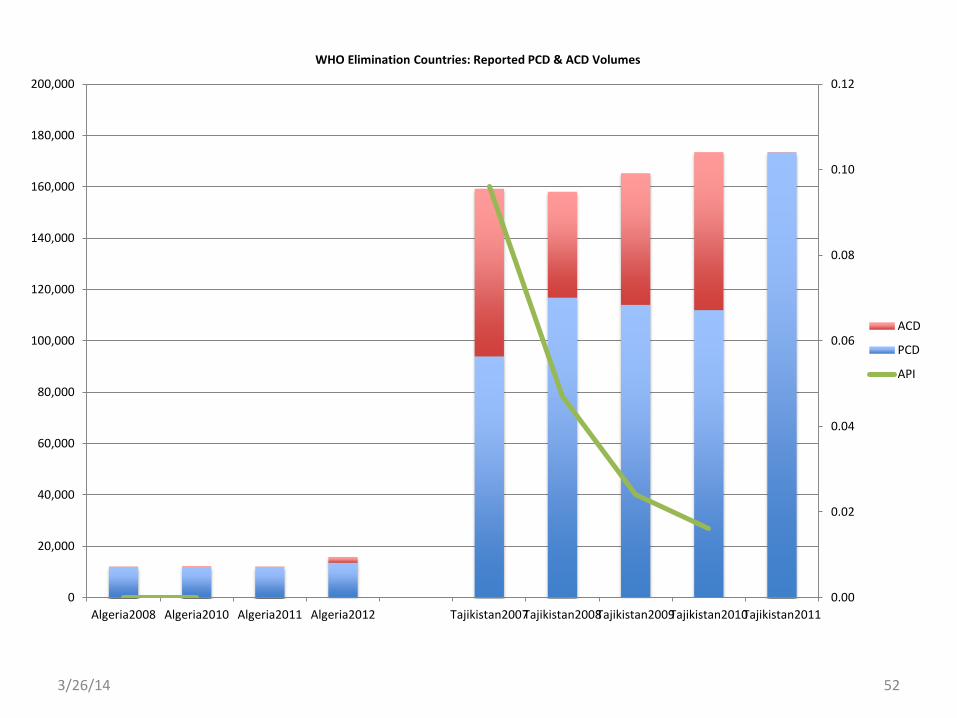

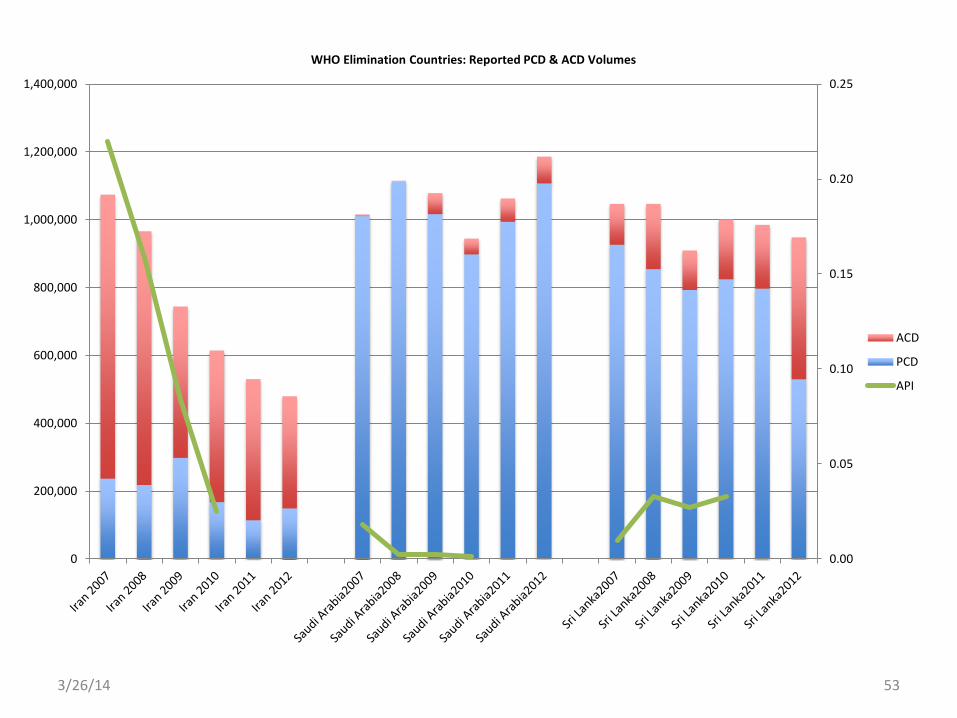

Annex I: Passive case detection and active infection detection testing volumes by country ..................... 49

Annex II: Market-sizing exercise ............................................................................................................... 61

Annex III: Role of the retail private sector in elimination countries ......................................................... 69

Annex IV: Financial background: Malaria-eliminating countries ............................................................. 70

Annex V: Experts interviewed ................................................................................................................... 71

ii

Acronyms and abbreviations

ACT artemisinin-based combination therapy AIDS Acquired Immune Deficiency Syndrome CDC US Centers for Disease Control and Prevention CHAI Clinton Health Access Initiative DIAMETER Diagnostics for Malaria Elimination Toward Eradication FDA US Food and Drug Administration FIND Foundation for Innovative New Diagnostics FTAT focused testing and treatment G6PD glucose-6-phosphate dehydrogenase deficiency Global Fund Global Fund to Fight AIDS, Tuberculosis and Malaria GPS Global Positioning System HIV human immunodeficiency virus HRP-II histidine-rich protein 2 ID infection detection IDT infection detection test IRS indoor residual spraying LAMP loop-mediated isothermal amplification MEG UCSF Malaria Elimination Group MOP Malaria Operational Plan MTAT mass testing and treatment PCD passive case detection PCR polymerase chain reaction PCW Positive Control Wells Pf Plasmodium falciparum pLDH Plasmodium lactate dehydrogenase PMI US President’s Malaria Initiative PQ prequalification Pv Plasmodium vivax QA quality assurance QC quality control LOD limit of detection R&D research and development RBM Roll Back Malaria RDT rapid diagnostic test SD Standard Diagnostics TDR WHO Special Programme for Research and Training in Tropical Diseases TPP target product profile UCSF University of California, San Francisco WHO World Health Organization

iii

Introduction

This report presents findings from a review of the market landscape conducted from December 2013 to February 2014 as part of PATH’s Project DIAMETER (Diagnostics for Malaria Elimination Toward Eradication). To date, evaluation of malaria diagnostics markets has been relatively limited, and where it is available, it is largely focused on passive case detection and on higher-burden countries.i This report aims to build on existing malaria diagnostics market work and to complement it by delving deeper into elimination and active use scenarios for malaria diagnostics. The report is structured as follows:

• Malaria elimination and diagnostics use: This section provides information on elimination countries and the role of diagnostics, including a review of current World Health Organization (WHO) guidance and trends shaping the research agenda.

• The current malaria diagnostics market: This section summarizes relevant aspects of the current microscopy and rapid diagnostic test (RDT) markets, drawing on existing work about the malaria diagnostics market.

• Country use of diagnostics for elimination and active use scenarios: This section considers use of and demand for diagnostics in elimination settings, with a focus on active use scenarios. It includes both qualitative and quantitative analyses.

• The potential market for a new rapid infection detection test: This section describes a market-sizing exercise that was undertaken for a new rapid infection detection test (IDT).

• Promoting investment and development of a healthy market: This section describes challenges and risks along the product development and market access pathway and describes some potential interventions to promote investment and development of a healthy market.

• Several annexes provide additional detail of the analyses conducted for this report and a list of experts interviewed.

The methodology undertaken is described at the start of each section. Generally, given the limited data available on malaria diagnostics markets, the methods for this report included identifying potential sources of data for analysis, desk review, and expert interviews. The available data on malaria diagnostics are limited (relative to other product categories, such as medicines), and even more limited for

i For example: • UNITAID. Malaria Diagnostics Technology and Market Landscape Updates. Geneva: World Health Organization; 2013. Available at:

http://www.unitaid.eu/en/resources/publications/technical-reports. • Wafula F, Agweyu A, Macintyre K. Regional and temporal trends in malaria commodity costs: an analysis of Global Fund data for 79

countries. Malaria Journal. 2013;12:466. • Zhao J, Lama M, Korenromp E, et al. Adoption of rapid diagnostic tests for the diagnosis of malaria: a preliminary analysis of the Global

Fund program data, 2005 to 2010. PLOS ONE. 2012;7(8):e43549. • USAID | DELIVER PROJECT. Price Analysis of Malaria Rapid Diagnostic Test Kits. Washington, DC: USAID | DELIVER PROJECT

Task Order 7; 2012. Available at: http://deliver.jsi.com/dlvr_content/resources/allpubs/logisticsbriefs/RDTPricAnal.pdf. • Frost LJ, Reich MR. Chapter 5: Malaria rapid diagnostic tests: access to diagnostics. In: Access: How do Good Health Technologies Get to

Poor People in Poor Countries? Cambridge: Harvard University Press; 2008.

1

eliminating countries.ii Therefore, for this report, we primarily relied on national malaria control program reporting to the WHO (published and unpublished information). Although many national programs do not completely or reliably report to the WHO, the assumption was made that, by definition, surveillance systems in countries pursuing elimination should be robust enough to produce reliable data. Given the time frame for this report, validation of the data and analyses with countries and experts was not possible. When reviewing the analyses and data in this report, it is important to keep in mind that many of the analyses presented are for a subset of countries, and therefore may not be completely representative of the global markets. Attempts were also made to identify analogous products and markets; however, none were identified. From an operational research perspective, malaria elimination is a rapidly evolving area, and currently many unanswered questions about optimal strategies are being explored. Likewise, WHO guidance on elimination is expected to be updated in 2014. The lack of consensus and guidance on optimal approaches makes analyzing the market and making predictions about the market size for a new diagnostic challenging. Evidence gaps and research questions that would impact the market have been highlighted in this report. Lastly, a note about defining elimination countries: The WHO characterizes all countries by program phase using a combination of epidemiological and operational criteria. In 2013, the WHO classified 19 countries as in the elimination or pre-elimination phase,iii with an additional seven countries in the prevention of reintroduction phase. The Malaria Elimination Group (MEG) at the University of California, San Francisco (UCSF) has a broader definition of “malaria-eliminating countries,” which is based on whether a country has adopted a strategy for elimination.1 Currently, this is a set of 38 countries. For this report, the UCSF MEG definition and set of countries is used, unless otherwise noted.

Malaria elimination and diagnostics use

Malaria-eliminating countries An estimated 3.4 billion people, across 97 countries, were at risk of malaria in 2012.2 Since 2000, scale-up of malaria control efforts has contributed to tremendous reductions in the burden of malaria, and, as a result, has put malaria elimination within reach for many countries that have reduced transmission to low levels. Historically, there was a major effort to eliminate malaria during the Global Malaria Eradication Program beginning in the mid-1950s through the late 1970s. During this period, 68 countries became malaria free. In contrast, during the 30 years from 1979 to 2009, only ten countries became malaria free.3 Most recently, Armenia (2011), Morocco (2010), Turkmenistan (2010), and the United Arab Emirates (2007) were certified by the WHO as malaria free.

ii For example, the RDT Procurement Data Set analyzed by the Clinton Health Access Initiative (CHAI) and UNITAID includes about 388 million RDTs over several years and represents an estimated 50 percent of the global RDT market. The 34 malaria-eliminating countries (as defined by the UCSF MEG) represent about 1 percent of this data set. iii World Health Organization (WHO). World Malaria Report 2013. Geneva: WHO; 2013. WHO classifications by program phase are not entirely consistent (Table 8.2 is consistent with the country profiles). Table 8.2: 97 countries with ongoing transmission in 2013, 12 are in pre-elimination phase, 7 are in elimination phase. A further 7 are classified as being in the prevention of reintroduction phase. WHO pre-elimination countries: Argentina, Belize, Bhutan, Cabo Verde, Costa Rica, Democratic People’s Republic of Korea, Ecuador, El Salvador, Malaysia, Mexico, Paraguay, Republic of Korea. Elimination countries: Algeria, Azerbaijan, Iran, Saudi Arabia, Sri Lanka, Tajikistan, Turkey. Prevention of reintroduction countries: Egypt, Georgia, Iraq, Kyrgyzstan, Oman, Syrian Arab Republic, Uzbekistan. Recently certified malaria free: Armenia (2011), Morocco (2010), Turkmenistan (2010), and the United Arab Emirates (2007).

2

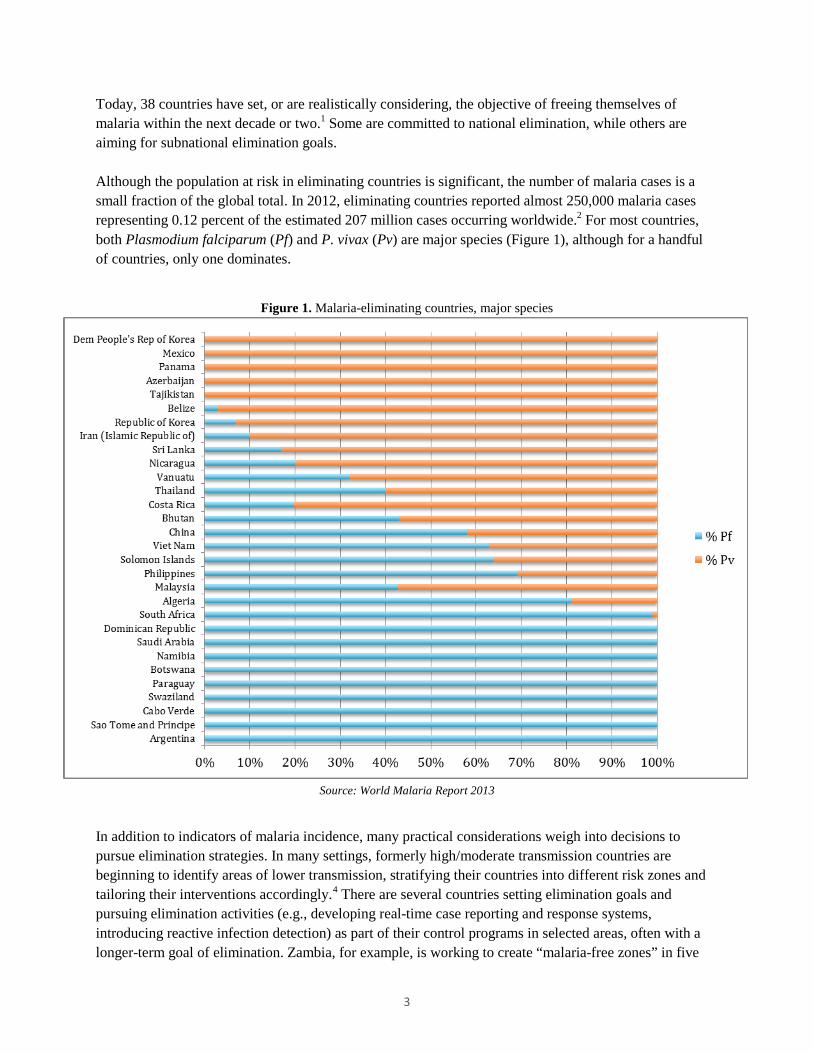

Today, 38 countries have set, or are realistically considering, the objective of freeing themselves of malaria within the next decade or two.1 Some are committed to national elimination, while others are aiming for subnational elimination goals. Although the population at risk in eliminating countries is significant, the number of malaria cases is a small fraction of the global total. In 2012, eliminating countries reported almost 250,000 malaria cases representing 0.12 percent of the estimated 207 million cases occurring worldwide.2 For most countries, both Plasmodium falciparum (Pf) and P. vivax (Pv) are major species (Figure 1), although for a handful of countries, only one dominates.

Figure 1. Malaria-eliminating countries, major species

Source: World Malaria Report 2013 In addition to indicators of malaria incidence, many practical considerations weigh into decisions to pursue elimination strategies. In many settings, formerly high/moderate transmission countries are beginning to identify areas of lower transmission, stratifying their countries into different risk zones and tailoring their interventions accordingly.4 There are several countries setting elimination goals and pursuing elimination activities (e.g., developing real-time case reporting and response systems, introducing reactive infection detection) as part of their control programs in selected areas, often with a longer-term goal of elimination. Zambia, for example, is working to create “malaria-free zones” in five

3

regions of the country by 2015. Likewise, the Tanzanian island of Zanzibar has strengthened reporting systems and is introducing active infection detection.

Diagnostics uses: passive detection, active detection, and laboratory testing There are three broad categories of diagnostics use scenarios in malaria: passive case detection, active infection detection, and laboratory testing. Within each of these categories, there are multiple use scenarios, which are described in a forthcoming publication by the DIAMETER team.5 The following is a brief summary of these uses. Passive case detection (PCD): All malaria programs rely on PCD, whereby the patient seeks care at a health facility or from a community health worker for symptoms of malaria. Microscopy and RDTs are primarily used for PCD testing, and, if these are of sufficiently high quality, they are considered adequate for detecting symptomatic cases of malaria. Active infection detection (ID): As countries move along the continuum from control to elimination, there is a shift in emphasis from detecting only clinical cases to actively seeking out and treating infections in order to reduce the malaria reservoir in the community, thereby driving down transmission. Within the active ID category, there are myriad approaches, many of which are focused on detecting malaria infection in asymptomatic individuals. Laboratory testing: Centralized laboratory testing complements PCD and active ID activities. A main role of centralized laboratory testing is to provide quality assurance (QA) and quality control (QC) of the diagnostics used for PCD and active ID. In addition, laboratory testing may support PCD by providing confirmation of questionable results or through monitoring response to treatment. Genotyping also becomes important, as countries need to determine whether a case is locally acquired or imported. Often, central laboratories employ microscopy and molecular methods.

WHO guidance The WHO provides normative guidance on malaria diagnosis and surveillance for elimination settings in several documents, including the Guidelines for the Treatment of Malaria (second edition; 2010), the Malaria Elimination Field Manual for Low and Moderate Endemic Countries (2007), and the Disease Surveillance for Malaria Elimination: Operational Manual (2012).iv A brief summary of WHO guidance pertaining to diagnostics is below.

Passive case detection

• WHO guidance for PCD is very clear: prompt diagnosis is recommended for all patients with suspected malaria. Before proceeding to the elimination phase, 100 percent of suspected cases should be confirmed, including those in the private sector.

iv Community-Based Reduction of Malaria Transmission was not reviewed, as it is no longer considered to be a relevant document. According to Andrea Bosman (February 2014), the WHO is considering an evidence review group for late 2014 to reconsider this document and the 2007 Elimination Manual, as well as to review research in this area and map priority areas for more work.

4

• Microscopy is the WHO’s preferred technology for diagnosing malaria from the start of the pre-elimination program. Microscopy is preferred to RDTs for its ability to speciate and provide information on density and gametocytes, and due to the limitations of RDTs (persistent antigenemia, limit of detection [LOD] for P. vivax). The WHO recommends that when an RDT is used to guide treatment, a slide is also made and read as soon as possible.

• Access to free testing and treatment in both the public and private sectors is recommended.

Active infection detection

• There is no guidance on when to begin active ID activities, although they are an expected element of elimination programs. Reactive ID would likely begin during the pre-elimination phase as part of case investigations. During the elimination phase, 100 percent of cases are investigated.

Laboratory testing

• An operational QA system for microscopy is a precondition to proceeding to the elimination phase. It is expected that all positive and a proportion of negative slides (usually 10 percent) are re-checked. In addition, laboratories should participate in a national external QA network.

• Genotyping is recommended from the start of a pre-elimination program onward. In general, while WHO guidance is available, a one-size-fits-all approach is not possible in malaria elimination, and many decisions are left to the discretion of the national program, based on local conditions and local expertise. In addition, providing definitive guidance is challenging due to the limited evidence base on the effectiveness of many elimination activities, as well as a lack of evidence on optimal strategies for implementation.

Unanswered research questions and implications for diagnostics markets There is much to be learned about optimizing elimination strategies; as best practices are defined, the demand for malaria diagnostics could vary widely. Among the unanswered questions are several related to the use of diagnostics in malaria elimination settings, as well as questions around targeting hotspots and the potential of mass campaign strategies for reducing the burden of malaria more generally. Important trends in program implementation and research priorities include:

• Understanding the dynamics of sub-patent, asymptomatic infections in transmission. Understanding the role of sub-patent, asymptomatic infections and their contribution to ongoing malaria transmission is a priority for diagnostics and malaria elimination. In theory, the systematic identification and treatment of asymptomatic individuals should reduce disease transmission by reducing the parasite reservoir in the community. However, the relationship between parasitemia and transmission is not well understood; and, therefore, the optimal LOD for a test aimed at detection of infections is uncertain.

• Optimizing active infection detection strategies. Although active ID strategies, in particular reactive ID, are widely used, implementation varies widely, both in policy and in practice, and there is little evidence on the effectiveness of these interventions.6,7,8 In particular, there is a need for

5

operational research on the optimal implementation protocols (e.g., number of households to screen, events that trigger reactive ID) that would efficiently and effectively identify infections. Given new evidence suggesting that asymptomatic, sub-patent parasitemia may contribute significantly to transmission, there is likely to be a trend toward screening all individuals, regardless of symptoms. However, there are practical limitations associated with this, both with respect to the LOD of current field-deployable diagnostics and in terms of the capacity of programs to test large numbers of people.

• Targeting interventions to achieve higher impact and improve resource utilization. Evidence suggests that increased targeting of hotspots may have a more dramatic impact on transmission than broadly applied efforts.9 Therefore, diagnostics combined with new technologies (Global Positioning System [GPS], mapping programs, communications technologies) should allow for rapid production of finer-resolution maps that can be used to target interventions, thereby improving resource utilization. These new technologies are already being leveraged to support targeting of interventions,10 and the continued adoption of these technologies and improvements in their application are anticipated in the coming years. With respect to diagnostics markets, the impact is twofold. First, the identification of foci of transmission and, at a finer resolution, hotspotsv and hotpops,vi will require broad use of highly sensitive diagnostics, linked to strong surveillance and mapping systems. Second, in elimination settings, a more targeted approach implies that activities may be undertaken in a targeted manner and on a smaller scale as opposed to routine use of mass campaigns. Such an approach would be consistent with the general pressure on resources (both human and financial) that often constrains malaria programs.

• Improving the evidence base for malaria transmission and incidence. Although there has been substantial progress in reducing incidence and transmission of malaria in many areas, the evidence base is imprecise and incomplete in many areas, in particular for many African countries.2,11 In most countries, surveillance systems are not strong enough to develop stratified malaria maps of the country that would allow for tailoring of approaches.2 One of the near-term research and programmatic goals therefore is to improve the available information on malaria through strengthening surveillance, use of new GPS/mapping and communication technologies, and through modeling. Having a better evidence base would in turn inform country decision-making around timelines for elimination (these may be very long term in some countries, while others may decide to pursue spatially targeted elimination) and around adoption of new tactics.

• Strategies for reducing transmission to very low levels in endemic countries, thereby accelerating elimination. With malaria eradication on the global agenda again, there is increasing interest in the possibility of accelerating elimination of malaria in more moderate transmission countries. Unconventional tactics are being explored, including revisiting the role of approaches such as mass testing and treatment (MTAT) and mass drug administration for burden reduction.12,13,14,15,16 At the same time, an evidence gap exists for endemic countries that have significantly lowered transmission levels through high coverage of vector control and case management interventions, but have not yet reached the very low levels of transmission required to seriously consider elimination. While there are many unanswered questions around elimination more generally, countries that have rapidly reduced transmission will likely face a unique set of challenges given the potential for

v Hotspots, also referred to as foci, are large or small geographically clustered populations identified as having comparatively higher levels of transmission. Hotspots occur at every level of transmission and therefore are fractal in nature.5 vi Hotpops are demographically clustered populations of malaria incidence. Within an elimination context, hotpops are often associated with travel history and occupation.5

6

resurgence, and the road map for these countries is uncertain. Current research, such as that led by the Malaria Control and Elimination Partnership in Africa in Zambia and Senegal and the national program in Zanzibar, includes testing approaches like reactive ID and MTAT in these settings.

The current malaria diagnostics market

This section of the report focuses on the malaria diagnostics market broadly, with the aim to present relevant highlights as context for further understanding of the potential market for a new rapid IDT. It is not specific to eliminating-country markets unless otherwise noted.

Access to malaria diagnosticsvii

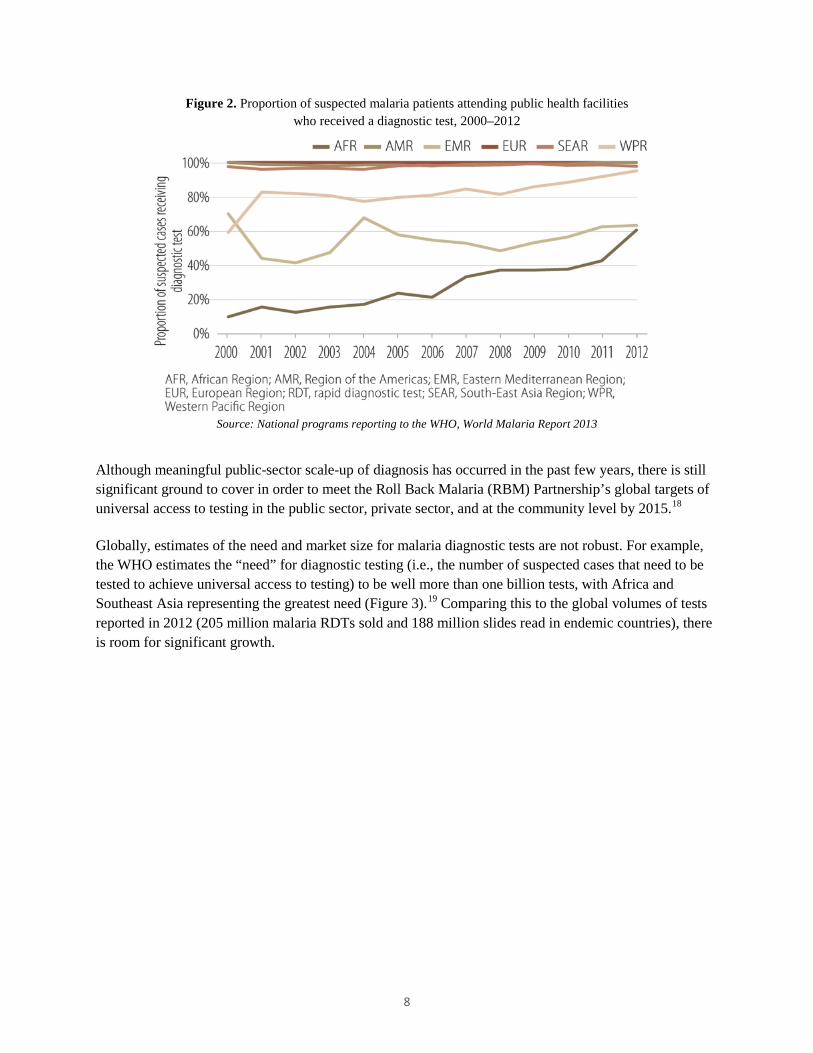

There has been a steady increase in the number of diagnostic tests performed globally in recent years, as indicated by the growth in public-sector testing rates (Figure 2) and in the growth in the malaria RDT market (Figure 5). While testing rates in the public sector have grown steadily, to 64 percent globally in 2012, the African (61 percent of suspected cases tested), Southeast Asian (56 percent, excluding India, where testing rates are high), and Eastern Mediterranean (63 percent) regions lag behind. In many countries, the private sector plays an important role in care of fevers and provision of malaria drugs, yet diagnostic testing in this sector is minimal in the majority of countries. Much of the recent growth in testing is driven by the release in 2010 of the revised WHO Guidelines for the Treatment of Malaria,17 which for the first time recommended that all suspected cases of malaria receive a diagnostic test before treatment.

vii This section draws on World Malaria Report 2013 unless otherwise noted.

7

Figure 2. Proportion of suspected malaria patients attending public health facilities who received a diagnostic test, 2000–2012

Source: National programs reporting to the WHO, World Malaria Report 2013

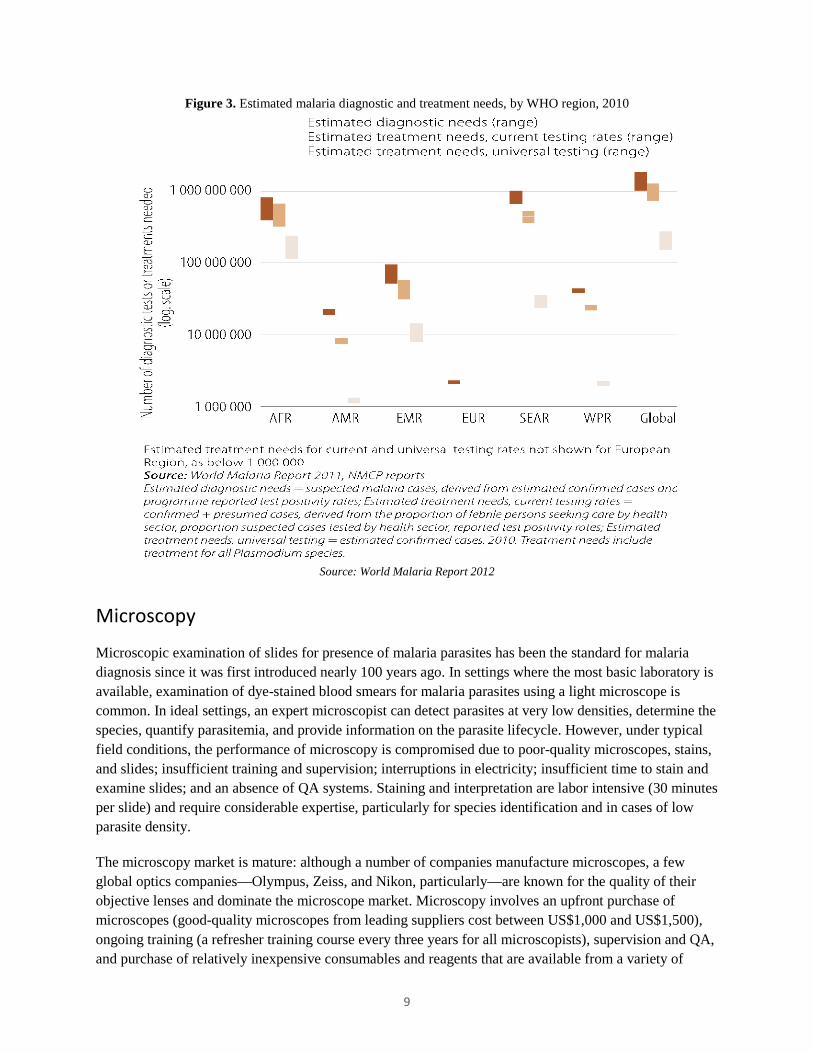

Although meaningful public-sector scale-up of diagnosis has occurred in the past few years, there is still significant ground to cover in order to meet the Roll Back Malaria (RBM) Partnership’s global targets of universal access to testing in the public sector, private sector, and at the community level by 2015.18 Globally, estimates of the need and market size for malaria diagnostic tests are not robust. For example, the WHO estimates the “need” for diagnostic testing (i.e., the number of suspected cases that need to be tested to achieve universal access to testing) to be well more than one billion tests, with Africa and Southeast Asia representing the greatest need (Figure 3).19 Comparing this to the global volumes of tests reported in 2012 (205 million malaria RDTs sold and 188 million slides read in endemic countries), there is room for significant growth.

8

Figure 3. Estimated malaria diagnostic and treatment needs, by WHO region, 2010

Source: World Malaria Report 2012

Microscopy

Microscopic examination of slides for presence of malaria parasites has been the standard for malaria diagnosis since it was first introduced nearly 100 years ago. In settings where the most basic laboratory is available, examination of dye-stained blood smears for malaria parasites using a light microscope is common. In ideal settings, an expert microscopist can detect parasites at very low densities, determine the species, quantify parasitemia, and provide information on the parasite lifecycle. However, under typical field conditions, the performance of microscopy is compromised due to poor-quality microscopes, stains, and slides; insufficient training and supervision; interruptions in electricity; insufficient time to stain and examine slides; and an absence of QA systems. Staining and interpretation are labor intensive (30 minutes per slide) and require considerable expertise, particularly for species identification and in cases of low parasite density.

The microscopy market is mature: although a number of companies manufacture microscopes, a few global optics companies—Olympus, Zeiss, and Nikon, particularly—are known for the quality of their objective lenses and dominate the microscope market. Microscopy involves an upfront purchase of microscopes (good-quality microscopes from leading suppliers cost between US$1,000 and US$1,500), ongoing training (a refresher training course every three years for all microscopists), supervision and QA, and purchase of relatively inexpensive consumables and reagents that are available from a variety of

9

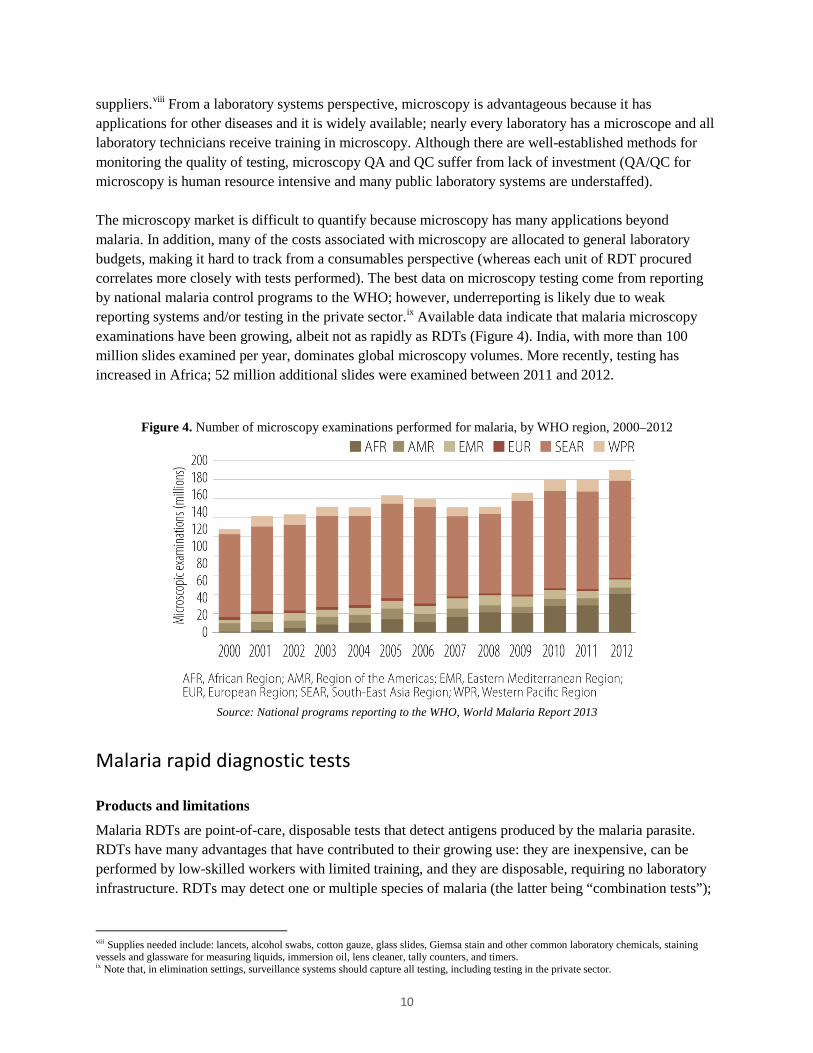

suppliers.viii From a laboratory systems perspective, microscopy is advantageous because it has applications for other diseases and it is widely available; nearly every laboratory has a microscope and all laboratory technicians receive training in microscopy. Although there are well-established methods for monitoring the quality of testing, microscopy QA and QC suffer from lack of investment (QA/QC for microscopy is human resource intensive and many public laboratory systems are understaffed). The microscopy market is difficult to quantify because microscopy has many applications beyond malaria. In addition, many of the costs associated with microscopy are allocated to general laboratory budgets, making it hard to track from a consumables perspective (whereas each unit of RDT procured correlates more closely with tests performed). The best data on microscopy testing come from reporting by national malaria control programs to the WHO; however, underreporting is likely due to weak reporting systems and/or testing in the private sector.ix Available data indicate that malaria microscopy examinations have been growing, albeit not as rapidly as RDTs (Figure 4). India, with more than 100 million slides examined per year, dominates global microscopy volumes. More recently, testing has increased in Africa; 52 million additional slides were examined between 2011 and 2012.

Figure 4. Number of microscopy examinations performed for malaria, by WHO region, 2000–2012

Source: National programs reporting to the WHO, World Malaria Report 2013

Malaria rapid diagnostic tests

Products and limitations

Malaria RDTs are point-of-care, disposable tests that detect antigens produced by the malaria parasite. RDTs have many advantages that have contributed to their growing use: they are inexpensive, can be performed by low-skilled workers with limited training, and they are disposable, requiring no laboratory infrastructure. RDTs may detect one or multiple species of malaria (the latter being “combination tests”);

viii Supplies needed include: lancets, alcohol swabs, cotton gauze, glass slides, Giemsa stain and other common laboratory chemicals, staining vessels and glassware for measuring liquids, immersion oil, lens cleaner, tally counters, and timers. ix Note that, in elimination settings, surveillance systems should capture all testing, including testing in the private sector.

10

however, only performance for P. falciparum has been extensively evaluated.x While the LODxi for RDTs is thought to be adequate for clinical case management, they do not reliably detect asymptomatic infections. With respect to performance, prior to 2009, it was difficult to determine the performance of RDTs: hundreds of small studies (manufacturer and independent) had been conducted; however, poor study design and reporting made it difficult to appreciate RDT performance. In 2009, the WHO completed the first round of product testing for malaria RDTs. This evaluation, a landmark for the market, directly compared the performance of dozens of tests and concluded that, while the quality of products on the market varies, there are many commercially available RDTs that perform as well as, if not better than, operational microscopy.xii Subsequently, three additional rounds of testing have been completed and a fifth is underway. Malaria RDTs have many limitations, including:

• Availability. For common use scenarios, a variety of high-performing products are available; however, in some categories, product selection is limited or improvements are needed (e.g., for P. falciparum, Plasmodium lactate dehydrogenase [pLDH]-based tests for regions where histidine-rich protein 2 [HRP-II] deletion is common; improvement in the LOD for P. vivax).

• Switching between different brands. Between manufacturers, there are differences in the format of the RDT, labeling, components included in the test kit, and in the test procedures. Although the extent of operator error caused by these differences has not been systematically documented, these differences present challenges to operators and to national programs. Given the decentralized nature of testing and the need to train and supervise thousands of operators, there is scope for improving RDTs so as to make them more user friendly and to reduce the programmatic burden of switching tests. The RBM Partnership is currently supporting a task force composed of implementers, policymakers, and manufacturers that is considering opportunities to ease switching and to improve the quality of test kits overall.

• Quality control. Practical technologies for RDT QC do not exist and are inadequate where they do exist. Suitable replacements for human-derived specimens (i.e., heat-stable recombinant antigens) are in development but have yet to come to market. For example, heat-stable quality controls for use at the point of service are not available. Controls in developmentxiii have yet to come to market and/or be extensively evaluated.

• Heat stability. Based largely on anecdotal evidence, experts suggest that heat stability is not an issue for high-performing RDTs. However, there is significant concern among users in the field about heat stability, especially since field conditions exceed manufacturer storage recommendations. Large-scale

x For example, the panels used in the WHO product evaluation are primarily P. falciparum panels, with limited P. vivax testing; P. ovale and P. malariae are not evaluated. Similarly, the 2011 Cochrane review of RDTs looked only at P. falciparum trials. xi Typical evaluation thresholds are 100 to 200 parasites/µl and considered adequate for symptomatic cases. xii The WHO Product Testing Programme is co-sponsored by the Foundation for Innovative New Diagnostics (FIND), the WHO Special Programme for Research and Training in Tropical Diseases (TDR), and the WHO Global Malaria Programme. Testing is performed at the US Centers for Disease Control and Prevention (CDC). Reports from the WHO product testing of malaria RDTs include: Malaria Rapid Diagnostic Test Performance: Results of WHO Product Testing of Malaria RDTs: Round 1 (2008); Round 2 (2009); Round 3 (2010-11); Round 4 (2012). Geneva: WHO. xiii FIND has been working to develop recombinant-based Positive Control Wells (PCWs) for several years, and trials in Uganda and Laos were just completed. The WHO is expected to review data from the PCW trials in 2014 and make recommendations about their use. Some RDT manufacturers are developing/have controls, but these have not been extensively evaluated.

11

studies of heat stability in conditions of use have not been conducted. In addition, heat stability testing by manufacturers during the design phase of product development was often minimal. If/when quality controls for RDTs come to market, they might alleviate concerns about heat stability.

• Issues with the HRP-II antigen. There are two issues related to the HRP-II antigen, the most commonly used detection method in RDTs. First, HRP-II antigens can persist in the blood for several weeks after successful treatment. In practice, this complicates the diagnosis of fever and should be part of provider training on RDTs. Second, HRP-II polymorphisms may affect the performance of RDTs. To date, deletion of HRP-II has been extensively documented in the Amazon region of South America, and in these areas, HRP-II-based tests are not recommended.

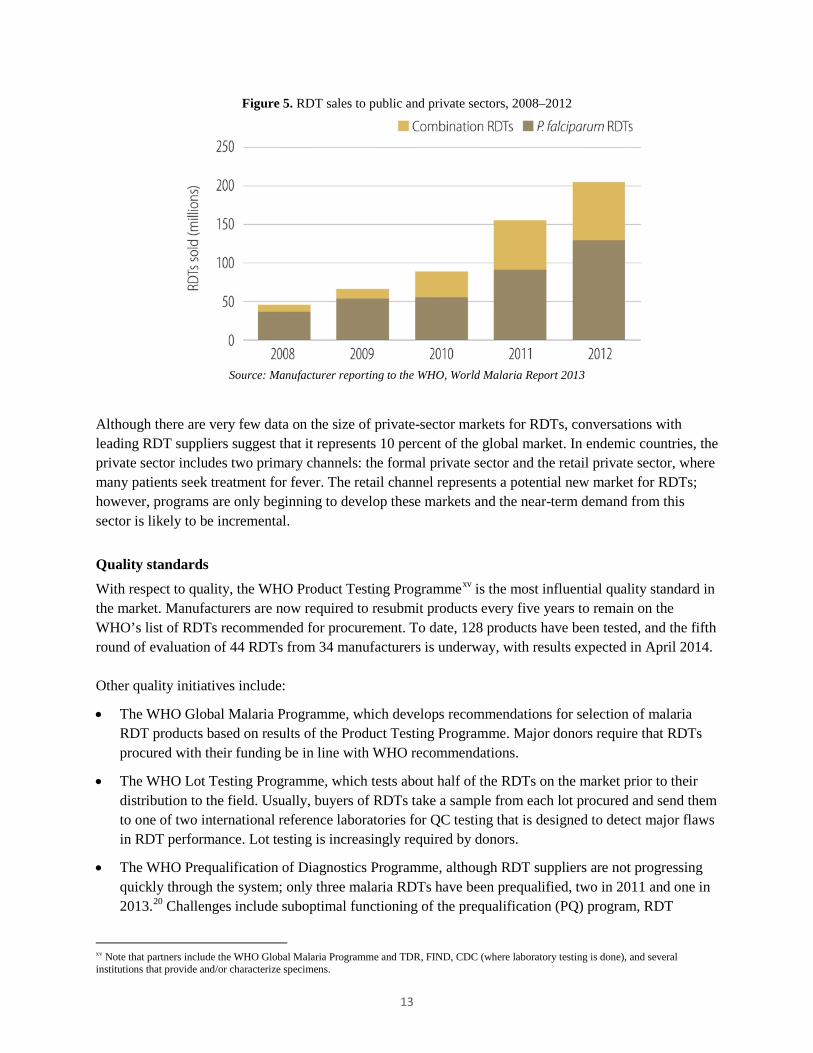

RDT market size and growthxiv

The malaria RDT market has been growing rapidly, from 45 million tests sold in 2008 to 205 million in 2012 (Figure 5). Although the total volume of tests has increased, the market value has not grown as rapidly due to declining unit prices. Currently, the market value is estimated to be in the $70 to $80 million range. While RDTs are sold globally, growth of demand is driven by increasingly larger orders from the African public sector, where it is not uncommon to see 5 to 10 million tests per year procured by high-volume countries. While some countries have scaled up use of diagnostics nationally, most have a ways to go. Donors, primarily the Global Fund to Fight AIDS, Tuberculosis and Malaria (Global Fund) and the US President’s Malaria Initiative (PMI), have enabled recent growth in the RDT market, and continued growth is largely contingent upon the availability of funding. However, recent changes to the grant-making process and fundraising challenges at the Global Fund may negatively impact malaria diagnostics budgets in the coming years. (A review of the donor landscape is included later in this report.)

xiv Unless otherwise noted, this section draws on UNITAID’s 2013 Malaria Diagnostics Technology and Market Landscape Updates.

12

Figure 5. RDT sales to public and private sectors, 2008–2012

Source: Manufacturer reporting to the WHO, World Malaria Report 2013

Although there are very few data on the size of private-sector markets for RDTs, conversations with leading RDT suppliers suggest that it represents 10 percent of the global market. In endemic countries, the private sector includes two primary channels: the formal private sector and the retail private sector, where many patients seek treatment for fever. The retail channel represents a potential new market for RDTs; however, programs are only beginning to develop these markets and the near-term demand from this sector is likely to be incremental.

Quality standards

With respect to quality, the WHO Product Testing Programmexv is the most influential quality standard in the market. Manufacturers are now required to resubmit products every five years to remain on the WHO’s list of RDTs recommended for procurement. To date, 128 products have been tested, and the fifth round of evaluation of 44 RDTs from 34 manufacturers is underway, with results expected in April 2014. Other quality initiatives include:

• The WHO Global Malaria Programme, which develops recommendations for selection of malaria RDT products based on results of the Product Testing Programme. Major donors require that RDTs procured with their funding be in line with WHO recommendations.

• The WHO Lot Testing Programme, which tests about half of the RDTs on the market prior to their distribution to the field. Usually, buyers of RDTs take a sample from each lot procured and send them to one of two international reference laboratories for QC testing that is designed to detect major flaws in RDT performance. Lot testing is increasingly required by donors.

• The WHO Prequalification of Diagnostics Programme, although RDT suppliers are not progressing quickly through the system; only three malaria RDTs have been prequalified, two in 2011 and one in 2013.20 Challenges include suboptimal functioning of the prequalification (PQ) program, RDT

xv Note that partners include the WHO Global Malaria Programme and TDR, FIND, CDC (where laboratory testing is done), and several institutions that provide and/or characterize specimens.

13

supplier inexperience with stringent regulatory systems, and weaknesses in manufacturing quality systems. It is notable that PQ status has no impact on procurement, and that of the three tests that have been prequalified, two are from one of the leading RDT market suppliers while the other has essentially no market share.

The current WHO Product Testing and Lot Testing Programmes for malaria RDT QC are expensive and complex due primarily to their reliance on human-derived specimens. In the near term, these programs will continue to operate normally; however, several changes to streamline operations and reduce costs are anticipated. The major change is a transition to recombinant antigen testing panels, which depends on successful research and development (R&D) that has been underway for several years. It is expected that these recombinant antigen panels will be available for manufacturer purchase and to country programs for lot testing at national reference laboratories.

Demand

Product selection in the public sector is generally conducted through a formalized process involving a committee of local experts and stakeholders established by the national malaria control program that develops a set of specifications and a short list of RDTs eligible for procurement. The main drivers of product selection are price, a product’s ability to meet minimum performance thresholds as demonstrated by the WHO Product Testing Programme, ease of use (including differences from the currently used RDT), and lead time. Generally, this process occurs every few years, as once an RDT has been selected and rolled out, programs prefer to continue using it for a couple of years to avoid the programmatic costs of switching RDTs. Procurement is typically conducted through a tender process that is run by the country or outsourced to agents. The most commonly used RDT, by volume, is the P. falciparum-only test; however, combination tests are also common and more countries reported procuring a combination test in 2012 than a P. falciparum-only test. Among the combination tests, procurement data analysis suggests that the P. falciparum/pan tests are most common.xvi Competitive procurement practices may lead to frequent switching of RDTs to obtain the lowest price, although this is often in conflict with the programmatic desire to stay with the same RDT due to the costs and effort associated with switching RDTs (e.g., retraining of health care workers, publication of new job aids). Analysis of procurement data suggests that the majority of countries have experience with multiple RDTs: half of countries switched test types between 2010 and 2013 (mostly from a P. falciparum-only test to a combination test), and 72 percent switched brands since 2010, often resulting in lower pricing.xvi

Donor landscape

The Global Fund and US PMI have been the primary funders of malaria diagnostic test procurement, and, as such, their policies have significant influence on demand for RDTs. Other important stakeholders affecting the malaria diagnostics market include the donors: the Bill & Melinda Gates Foundation, World Bank, UK Department for International Development, and UNITAID. These donors intervene at various

xvi In Q4 2013, malaria RDT procurement data analysis was conducted by CHAI in collaboration with the author of this report. The data set analyzed includes Global Fund and PMI procurement data. In total, 656 transactions representing more than 388 million RDTs were analyzed, representing 41 percent to 58 percent of the global RDT market in 2010–2013. The analysis is unpublished; however, some of it, referenced in this report, is included in the forthcoming 2013 UNITAID Malaria Diagnostics Market Landscape Update report.

14

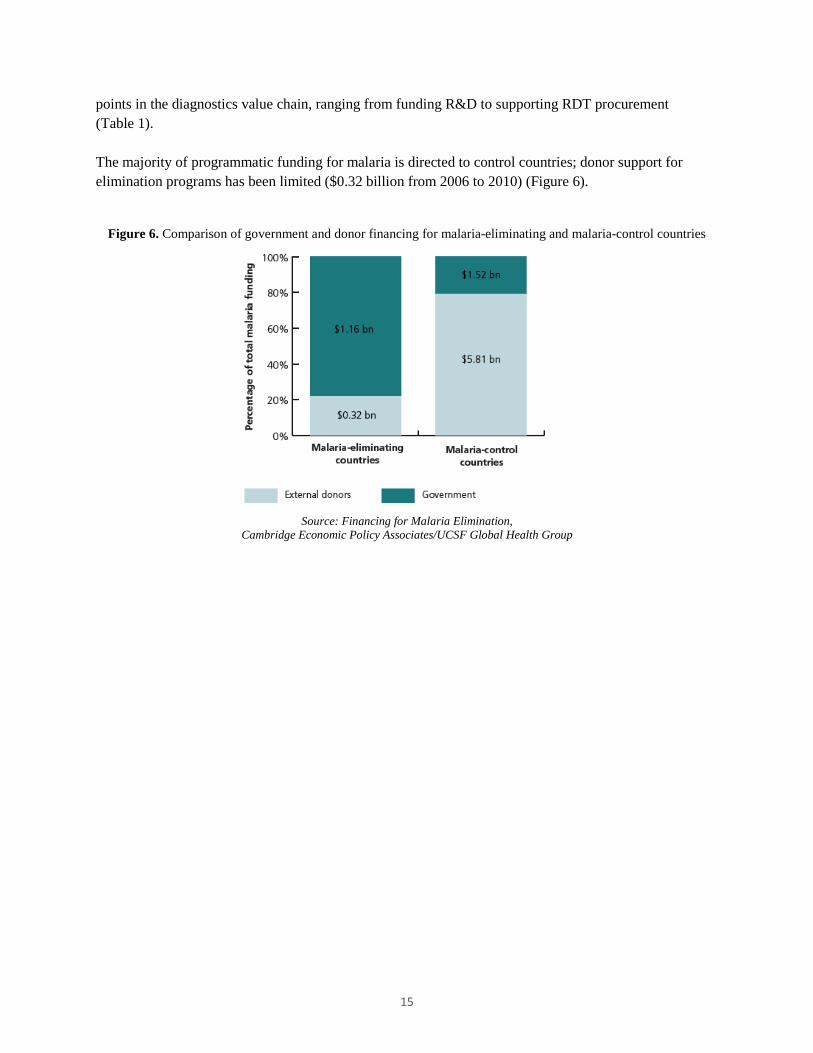

points in the diagnostics value chain, ranging from funding R&D to supporting RDT procurement (Table 1). The majority of programmatic funding for malaria is directed to control countries; donor support for elimination programs has been limited ($0.32 billion from 2006 to 2010) (Figure 6).

Figure 6. Comparison of government and donor financing for malaria-eliminating and malaria-control countries

Source: Financing for Malaria Elimination,

Cambridge Economic Policy Associates/UCSF Global Health Group

15

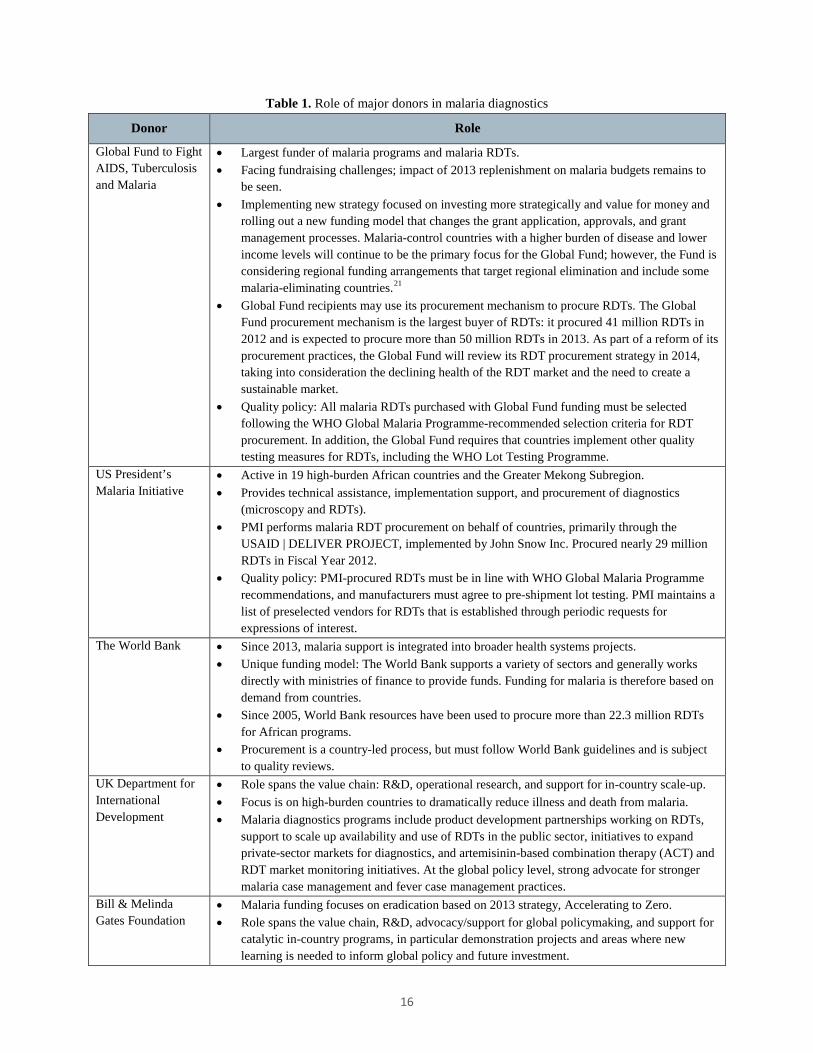

Table 1. Role of major donors in malaria diagnostics

Donor Role

Global Fund to Fight AIDS, Tuberculosis and Malaria

• Largest funder of malaria programs and malaria RDTs. • Facing fundraising challenges; impact of 2013 replenishment on malaria budgets remains to

be seen. • Implementing new strategy focused on investing more strategically and value for money and

rolling out a new funding model that changes the grant application, approvals, and grant management processes. Malaria-control countries with a higher burden of disease and lower income levels will continue to be the primary focus for the Global Fund; however, the Fund is considering regional funding arrangements that target regional elimination and include some malaria-eliminating countries.21

• Global Fund recipients may use its procurement mechanism to procure RDTs. The Global Fund procurement mechanism is the largest buyer of RDTs: it procured 41 million RDTs in 2012 and is expected to procure more than 50 million RDTs in 2013. As part of a reform of its procurement practices, the Global Fund will review its RDT procurement strategy in 2014, taking into consideration the declining health of the RDT market and the need to create a sustainable market.

• Quality policy: All malaria RDTs purchased with Global Fund funding must be selected following the WHO Global Malaria Programme-recommended selection criteria for RDT procurement. In addition, the Global Fund requires that countries implement other quality testing measures for RDTs, including the WHO Lot Testing Programme.

US President’s Malaria Initiative

• Active in 19 high-burden African countries and the Greater Mekong Subregion. • Provides technical assistance, implementation support, and procurement of diagnostics

(microscopy and RDTs). • PMI performs malaria RDT procurement on behalf of countries, primarily through the

USAID | DELIVER PROJECT, implemented by John Snow Inc. Procured nearly 29 million RDTs in Fiscal Year 2012.

• Quality policy: PMI-procured RDTs must be in line with WHO Global Malaria Programme recommendations, and manufacturers must agree to pre-shipment lot testing. PMI maintains a list of preselected vendors for RDTs that is established through periodic requests for expressions of interest.

The World Bank • Since 2013, malaria support is integrated into broader health systems projects. • Unique funding model: The World Bank supports a variety of sectors and generally works

directly with ministries of finance to provide funds. Funding for malaria is therefore based on demand from countries.

• Since 2005, World Bank resources have been used to procure more than 22.3 million RDTs for African programs.

• Procurement is a country-led process, but must follow World Bank guidelines and is subject to quality reviews.

UK Department for International Development

• Role spans the value chain: R&D, operational research, and support for in-country scale-up. • Focus is on high-burden countries to dramatically reduce illness and death from malaria. • Malaria diagnostics programs include product development partnerships working on RDTs,

support to scale up availability and use of RDTs in the public sector, initiatives to expand private-sector markets for diagnostics, and artemisinin-based combination therapy (ACT) and RDT market monitoring initiatives. At the global policy level, strong advocate for stronger malaria case management and fever case management practices.

Bill & Melinda Gates Foundation

• Malaria funding focuses on eradication based on 2013 strategy, Accelerating to Zero. • Role spans the value chain, R&D, advocacy/support for global policymaking, and support for

catalytic in-country programs, in particular demonstration projects and areas where new learning is needed to inform global policy and future investment.

16

Donor Role

UNITAID • Funds market-based approaches to increasing access to health products. • Malaria programs include support for ACT and long-lasting insecticide-treated net scale-up

and to the Affordable Medicines Facility - malaria; $10 million to the Foundation for Innovative New Diagnostics to support the WHO Product and Lot Testing Programmes; more than $30 million to Population Services International to support the development of private-sector markets for RDTs in five endemic countries.

• Market intelligence projects include ACT, RDT, and raw materials forecasting, support for ACT watch, and work to better understand the supply of raw materials for ACTs and RDTs.

RDT pricing

With respect to prices, malaria RDTs are relatively inexpensive tests, and intense competition has led to pricing declines (Figure 7). For example, in 2010, the weighted average public-sector price was $0.49 for P. falciparum RDTs and $0.68 for P. falciparum/pan tests. In 2013, average prices were $0.32 for P. falciparum RDTs and $0.38 for P. falciparum/pan tests. Wide variation in pricing is common, with competitive bids usually resulting in lower pricing.

Figure 7. Weighted average test prices by year for P. falciparum-only and combination RDTs

Source: Procurement Data Analysis 2009–2013, UNITAID/Clinton Health Access Initiative (forthcoming)

While suppliers continue to drive prices lower through competitive bidding, the sustainability of low prices is concerning. Low prices represent strategic attempts by RDT suppliers to capture and penetrate new markets, as well as efforts to use inventory and ensure capacity utilization (e.g., avoid costs associated with shutting down production). However, current pricing appears to be approaching the cost of goods and contributes to the declining attractiveness of the market.

Market share

Analysis of procurement data suggests that market share has been shifting significantly in the past five years; in 2010 and 2011, shifts toward products with higher performance in the WHO Product Testing

17

Programme occurred. More recently, the market has been consolidating around three suppliers: Access BIO, Alere™ (Standard Diagnostics), and Premier Medical Corporation Limited (Figure 8). These companies’ tests are among the highest-performing products in the WHO Product Testing Programme (as of Round 4; several are undergoing mandatory retesting in Round 5, and results are expected in early 2014). However, they are not able to obtain a price premium.

Figure 8. Malaria RDT market share, based on procurement data

Source: Procurement Data Analysis 2009–2013, UNITAID/Clinton Health Access Initiative (forthcoming)

The consolidation of the market is in contrast with the large number of companies with malaria RDTs in their portfolios. The malaria RDT market seems to attract many players due to its rapid growth and the large “need” for tests, the relative ease of developing a product, and the low regulatory requirements in comparison to other diagnostic tests. However, recent price declines have made the market unattractive, and at least one formerly dominant supplier has reduced malaria RDT production capacity and exited the public-sector market. Other companies appear to be targeting niche market segments and/or rounding out their portfolio of rapid test products, but not actively marketing malaria tests. Barriers to entry have also emerged, hindering participation in the largest market segment, the public sector. Among the barriers: participation in WHO product testing, which can take two years; economies of scale; working capital and capacity to deliver large public-sector orders rapidly; local product registration; and WHO PQ, which is not yet required but is a lengthy process that may be prioritized in the future.

Supply

Of the leading companies, there is only one multinational diagnostics company, Alere, controlling several RDT brands, the largest being Standard Diagnostics (SD Bioline). Other suppliers tend to be small companies; some focus almost exclusively on the global malaria RDT market, while others have modest-sized lateral flow test businesses and/or reagent businesses. Some companies that manufacture and market their own product also perform manufacturing of complete unlabeled RDTs or components of RDTs for other suppliers. The degree of automation and vertical integration varies (Table 2).

18

Table 2. Characteristics of leading malaria RDT suppliers

Company Location Notes

Access BIO Headquarters: New Jersey Manufacturing: primarily New Jersey, new facility in Ethiopia; however, problems meeting WHO requirements have delayed scale-up of production. (Possible contract manufacturing in Korea.)

• Small business, primary focus on malaria RDTs; recently became listed on the Korean stock exchange.

• HRP-II sourced from National Bioproducts Institute (South Africa); pLDH business acquired from Flow in 2011.

• Moderately automated facility (New Jersey). • R&D: Active in G6PD test development;

fluorescent RDT in development is currently on hold.

• Supplies Premier Medical Corporation Limited with raw materials for tests.

Alere – Standard Diagnostics (SD)

Headquarters: Korea Manufacturing: for leading brand, primarily Korea (WHO-prequalified facility); also has facility in India. Other brands have facilities worldwide.

• Multinational public company focused on point-of-care testing.

• Alere controls many malaria RDT brands, including Binax (USA), Orgenics (Israel), Vision/Clearview (South Africa), Abon (China); SD (Korea) is the vast majority of volumes. After many years of acquisitions and hands-off management, Alere is increasingly focused on integration of disparate businesses.

• SD has highly automated production facility in Korea and in-house monoclonal production.

• R&D: QC for RDTs is in development. • Only major WHO PQ supplier, although had

Notice of Concern issued in 2012 (mainly due to issues with HIV RDTs). Company has addressed WHO concerns.

Premier Medical Corporation Limited

Headquarters: New Jersey, India Manufacturing: India

• Has several RDTs in their portfolio. • Assembly-only operation; sources strips from

Access BIO (possibly other companies since 2013). In terms of manufacturing, malaria RDTs are made to order, and suppliers generally do not maintain significant inventories of finished goods. Although production capacity is generally not considered to be a limiting factor in this market, managing logistics to meet tight delivery time frames requires significant effort on the part of manufacturers. The major components of test kits are commodities, largely sourced from Asia and costing $0.005 to $0.03 each, with the plastic cassette and foil pouch generally costing the most. With the exception of nitrocellulose, other membranes, and monoclonal antibodies, there are several suppliers of components. Quality nitrocellulose and membranes are available from a limited number of suppliers; RDT manufacturers typically work with one primary supplier. Currently, monoclonal antibodies are available from a limited number of commercial sources or are produced in house by a few RDT manufacturers. Estimates of the cost of monoclonal antibody per test vary, as manufacturers use different quantities and combinations of antibodies depending on the product. Assuming a commercial source of antibody is used,

19

the antibody cost for RDTs ranges from $0.02 to $0.09 per test, with the multi-line combination tests and smaller production runs having a higher cost per test. In addition to the components, labor is a major cost. Demand growth, decreasing RDT prices, and rising labor costs have contributed to increasing levels of automation, although the degree of automation varies.

Summary and implications for innovation

Although the pricing declines have enabled greater access to testing, in light of current market conditions, the malaria diagnostics market is increasingly unhealthy. The market is characterized by competition on price, the ability to deliver rapidly, and meeting minimum quality standards. While demand is likely to continue to increase as malaria-control countries continue to scale diagnostic testing in the public sector, other market segments, such as the private sector, will take time to mature. These dynamics have important implications for RDT quality and for innovation. With respect to quality, market conditions put RDT quality at risk. The market conditions also limit the business incentives for new product development at a time when improvements to existing RDTs as well as development of new technologies to address unmet needs are needed. The current downward trend in pricing for malaria RDTs generally contrasts with the business principles of introducing a new product, as the malaria market may be unwilling to pay a premium for new products, unless their value is perceived to be substantially better than today’s RDTs, and companies are therefore unlikely to recapture their R&D investment through price premiums. While there are a number of products in the pipeline for malaria, many have stalled due to lack of pull from the market and a general lack of R&D funding for malaria diagnostics.

20

Country use of diagnostics for elimination and active use scenarios

Use of diagnostics for malaria elimination

As a starting point for evaluating the opportunity for new diagnostics to support elimination, an understanding of current and future diagnostics policies and uses in malaria-eliminating countries is necessary. Additionally, existing work on malaria diagnostics markets has largely focused on PCD markets; in this report, active uses are also investigated. This section is structured in two parts: the first summarizes qualitative analysis of policy and diagnostic test use across a range of countries, and the second summarizes analysis of diagnostic testing volume data reported by national programs to the WHO.

Qualitative analysis: trends in diagnostics use

To gain a better appreciation for current use of malaria diagnostics, we undertook a desk review, supplemented by reports from field visits and interviews.

xviii

xvii The focus of the review was malaria-eliminating countries (ten countries), although a handful of other endemic countries where malaria elimination strategies might be considered in the medium term were also included (six countries). A summary of key themes and findings is below.

Passive case detection

• There is room for improvement in PCD. Testing rates are generally high; however, many countries have included plans to strengthen case confirmation. Several report that clinical diagnosis (approximately 20 percent; in some instances, higher) is still practiced, particularly in remote communities and/or at the periphery. In part, a reliance on microscopy, especially outside of Africa, means that diagnostic coverage is insufficient at the lower levels of the system. In some instances, treatment is given empirically and a smear is taken and transported to another facility for results. In Africa, where RDTs are more commonly used, stockouts are reported.

• Across most countries, diagnostic coverage in the more remote communities and at the lower levels of the health system is a challenge. In some places, community health worker and village health worker programs using RDTs have been/are being scaled up.

• In general, RDTs are more commonly used for routine diagnosis in settings where malaria diagnosis has only recently been scaled up (primarily in African countries). In the majority of malaria-eliminating countries, microscopy is the primary mode of diagnosis and RDT use is minimal. Outside of Africa, RDTs are often considered to be a “back-up for emergency use,” for “outbreak response,” and for use in “remote areas.” In these settings, when an RDT is performed, it is used to guide patient management and often a slide is made and sent to the laboratory for confirmation.

xvii See Annex V for a list of experts interviewed. Sources consulted include: the Asia Pacific Malaria Elimination Network Country Partner Strategy and Intervention Matrices, PATH DIAMETER Country Trip Reports, PMI Malaria Operational Plans (MOPs), UCSF Global Health Group and World Health Organization Case Studies, and other limited publications from the literature. xviii Malaria-eliminating countries reviewed include: Bhutan, China, Namibia, North Korea, Philippines, Solomon Islands, Sri Lanka, Swaziland, Thailand, and Vietnam (Greater Mekong Subregion multi-country PMI MOP only). Malaria-control countries include: Angola, Ethiopia, Indonesia, Myanmar (Greater Mekong Subregion multi-country PMI MOP only), Zambia, and Zanzibar.

21

• In the countries reviewed, RDTs were frequently purchased with funds from the Global Fund or PMI, as opposed to government budgets. Constraints cited by end-users include poor speciation and inability to quantify parasite density. Although this may not be critical for initial patient management, it is relevant when monitoring response to treatment, which is commonly done in programs concerned about drug resistance.

• Parallel systems, whereby the national malaria control program sets up dedicated clinics (sometimes called “enhanced” or “activated” PCD), are not common, but are in place in a few countries. Often, these clinics yield the most positive cases (compared to other passive and active systems).

• Overall, there is little mention of the private sector and its role in PCD. In some countries, given poor treatment-seeking behavior, this sector is likely to play an important role in malaria case management.

• Follow-up of patients who test positive at regular intervals to ensure response to treatment is common in Asian countries, particularly in areas where drug resistance is a concern.

Active infection detection

• Use of periodic (every two to three years), nationally representative surveys was reported for about half of the countries reviewed, while others rely on reporting through the PCD systems, complemented by smaller-scale surveys of high-risk areas (focused testing and treatment, or FTAT). Surveys are conducted using a variety of technologies (often a combination), including RDT, microscopy, and molecular methods (primarily polymerase chain reaction [PCR] and piloting of loop-mediated isothermal amplification [LAMP]). A few countries are using serology or are planning to use serology to identify foci and hotspots/hotpops.

• Most of the malaria-eliminating countries reviewed, and a few others (e.g., Indonesia, Zambia, and Zanzibar), are performing some form of active ID targeting high-risk areas and/or populations. Among the more commonly reported activities are reactive ID (usually community index case as opposed to mobile); FTAT; border screening (often mentioned as planned, not yet implemented); and time-location screening of mobile populations, including migrant workers, military, and returning workers. Mobile clinics and “mass blood surveys” are commonly reported. In general, given the lack of standardization in the language used to describe active ID activities, it is difficult to categorize the activities reported.

• Reactive ID is common and reported by most elimination countries; however, there is a large variety in how it is implemented. This is consistent with a recent paper summarizing survey results from active ID in Asia Pacific countries.7 Variation occurs in the triggers for active ID (e.g., all cases, or just those that originated locally), whether only febrile individuals are tested or if all individuals are tested, and in the number of households screened around each index case (e.g., only members of the index household, five to ten homes surrounding the index home, an entire village, or a 100-m to 1-km radius around a household). In some instances, travel companions are also followed up and screened. In practice, experts suggest that the number of tests performed for each index case is likely to be 10 to 100.

• Many programs are focused on limiting imported malaria. Strategies reported include use of mobile clinics in border areas and in areas where migrant workers reside. It is also common to require screening of foreign workers in order to receive a work permit. Island nations that are eliminating

22

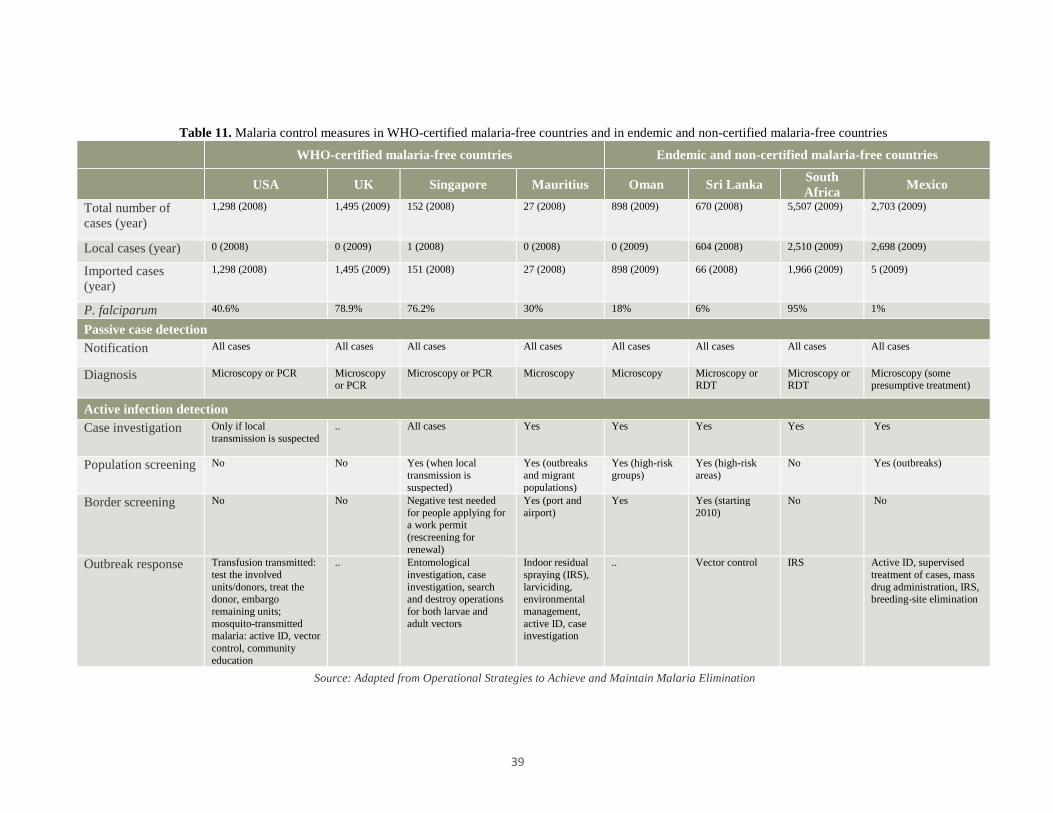

malaria (e.g., Sri Lanka, Solomon Islands) screen at airports and ports or are planning to establish screening in these locations. Mauritius, which is malaria free, relied on an intensive passenger screening program at airports and ports to eliminate malaria and continues to screen tens of thousands of passengers each year as part of its program to prevent reintroduction.22

• MTAT was mentioned by only two countries (Solomon Islands and Zambia). FTAT is more common.

• In general, available resources limit the magnitude of active ID operations. The cost of the diagnostic test is often minimal compared to the other costs involved in these activities, such as salaries and per diems, maintenance of vehicles and boats, and fuel. Dealing with seasonality can also be challenging from a resource perspective: staff are fully occupied during the malaria season, but may be idle or reallocated to other areas of the health system during the rest of the year.

• The technologies employed include a mix of microscopy, RDTs, and molecular methods. Outside of Africa, microscopy is often the primary diagnostic. For example, among the Asia Pacific countries responding to a survey, all used microscopy for reactive ID and many used it in combination with RDTs and PCR.7 It is not uncommon (although it may not be policy) for health workers to transport a microscope to the community being screened to avoid loss to follow-up.

• Several programs that have access to molecular methods have an appreciation for the large reservoir of asymptomatic infections and are recognizing the limitations of microscopy and RDTs for detecting such infections.

• There is scope for refining and optimizing active ID programs, especially in light of practical realities and resources. PATH field teams and experts report that implementation frequently deviates from policy, largely due to resource constraints (e.g., human resources, availability of transport, supplies, weather) resulting in low coverage or compromised sampling. Often, decision-making is delegated to the local level (e.g., in which village to implement FTAT, what radius to cover in reactive ID); however, it is not always clear that the necessary expertise is available at this level, and again decisions are often based on operational constraints.

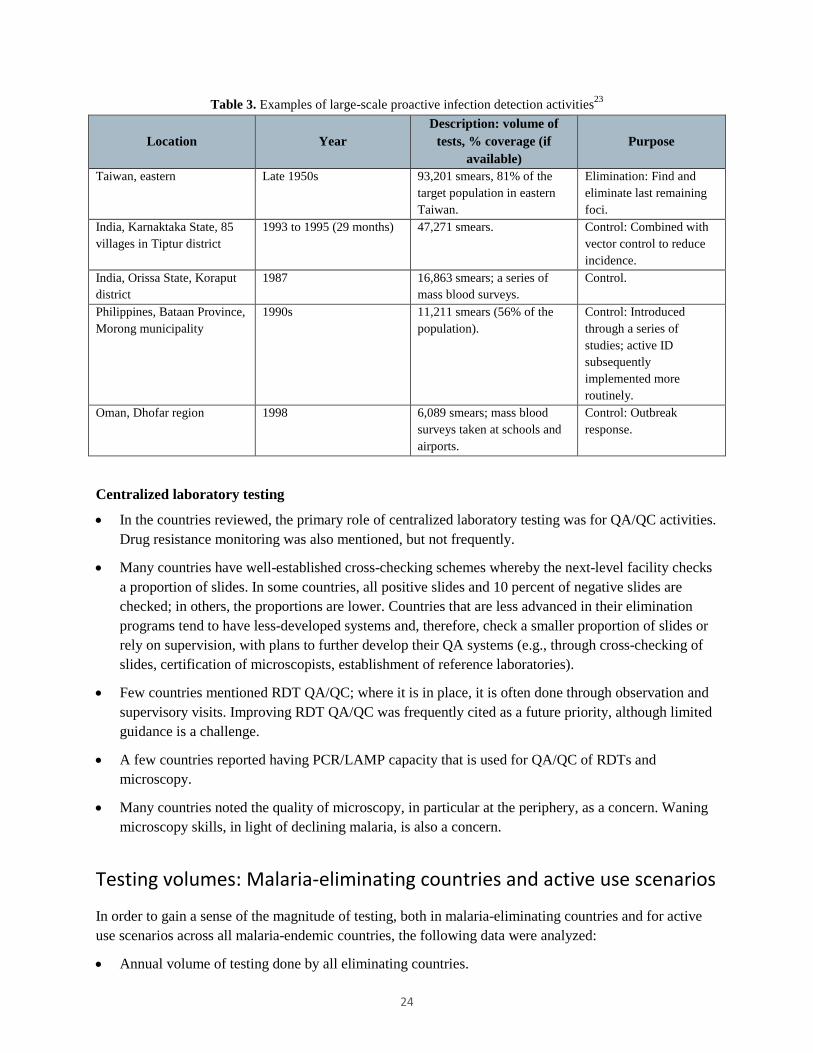

Large-scale proactive infection detection operations

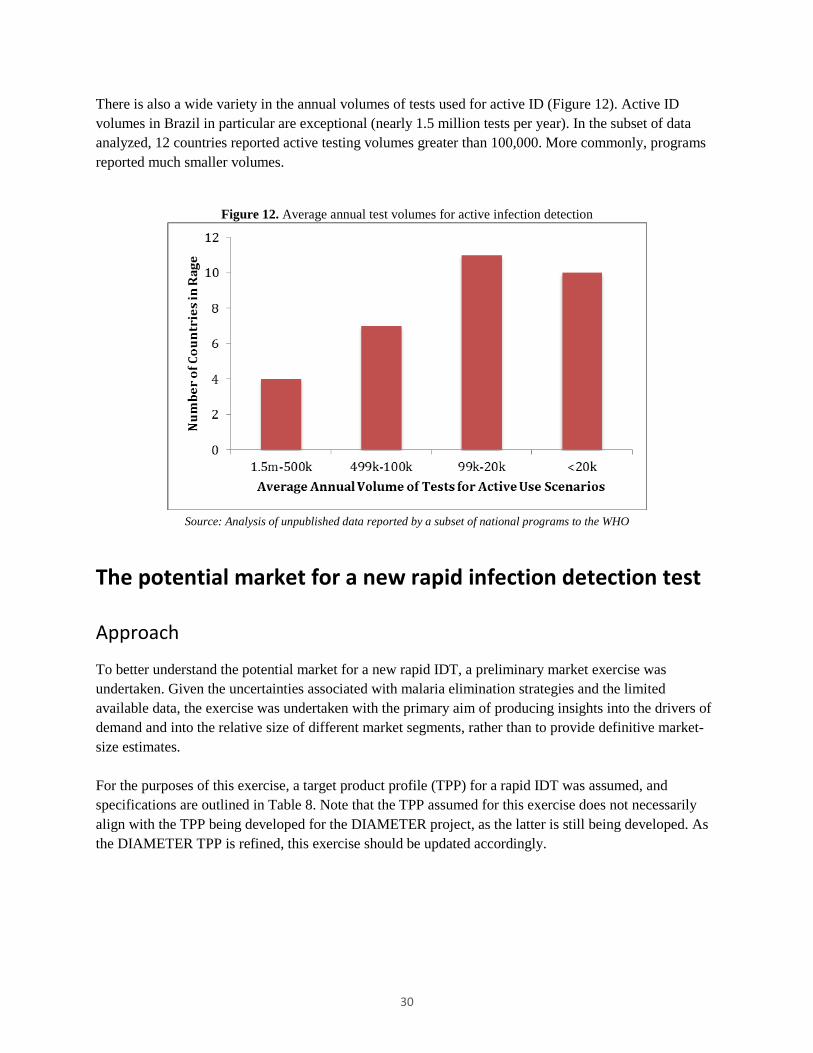

To improve the understanding of active ID, we reviewed Aggressive Active Case Detection: A Malaria Control Strategy Based on the Brazilian Model,23 a publication describing proactive ID strategies. The publication includes an in-depth discussion of Brazil’s malaria program, whereby the Ministry of Health has been using a model of “aggressive active case detection” in which most members of a community are tested and treated for malaria on a monthly basis. Brazil uses RDTs and microscopy for this work, and it continues to report exceptionally high volumes of active ID today (nearly 1.5 million tests per year). Other examples of large-scale active ID often include periodic (e.g., monthly) visits to communities where residual transmission occurs, often called “mass blood surveys.” Historically, these activities have been conducted largely using microscopy. The scale is generally in the tens of thousands, and these are undertaken at the district level (Table 3). Not all of these examples were successful; success was associated with simultaneous vector control work, and with populations whose movement is relatively limited (or well tracked) and that were amenable to routine screening. Mauritius, Morocco, Turkey, and Southern China have also undertaken proactive screening on a large scale.22,23,24,25

23

Table 3. Examples of large-scale proactive infection detection activities23

Location Year Description: volume of

tests, % coverage (if available)

Purpose

Taiwan, eastern Late 1950s 93,201 smears, 81% of the target population in eastern Taiwan.

Elimination: Find and eliminate last remaining foci.

India, Karnaktaka State, 85 villages in Tiptur district

1993 to 1995 (29 months) 47,271 smears. Control: Combined with vector control to reduce incidence.

India, Orissa State, Koraput district

1987 16,863 smears; a series of mass blood surveys.

Control.

Philippines, Bataan Province, Morong municipality

1990s 11,211 smears (56% of the population).

Control: Introduced through a series of studies; active ID subsequently implemented more routinely.

Oman, Dhofar region 1998 6,089 smears; mass blood surveys taken at schools and airports.

Control: Outbreak response.

Centralized laboratory testing

• In the countries reviewed, the primary role of centralized laboratory testing was for QA/QC activities. Drug resistance monitoring was also mentioned, but not frequently.

• Many countries have well-established cross-checking schemes whereby the next-level facility checks a proportion of slides. In some countries, all positive slides and 10 percent of negative slides are checked; in others, the proportions are lower. Countries that are less advanced in their elimination programs tend to have less-developed systems and, therefore, check a smaller proportion of slides or rely on supervision, with plans to further develop their QA systems (e.g., through cross-checking of slides, certification of microscopists, establishment of reference laboratories).

• Few countries mentioned RDT QA/QC; where it is in place, it is often done through observation and supervisory visits. Improving RDT QA/QC was frequently cited as a future priority, although limited guidance is a challenge.

• A few countries reported having PCR/LAMP capacity that is used for QA/QC of RDTs and microscopy.

• Many countries noted the quality of microscopy, in particular at the periphery, as a concern. Waning microscopy skills, in light of declining malaria, is also a concern.

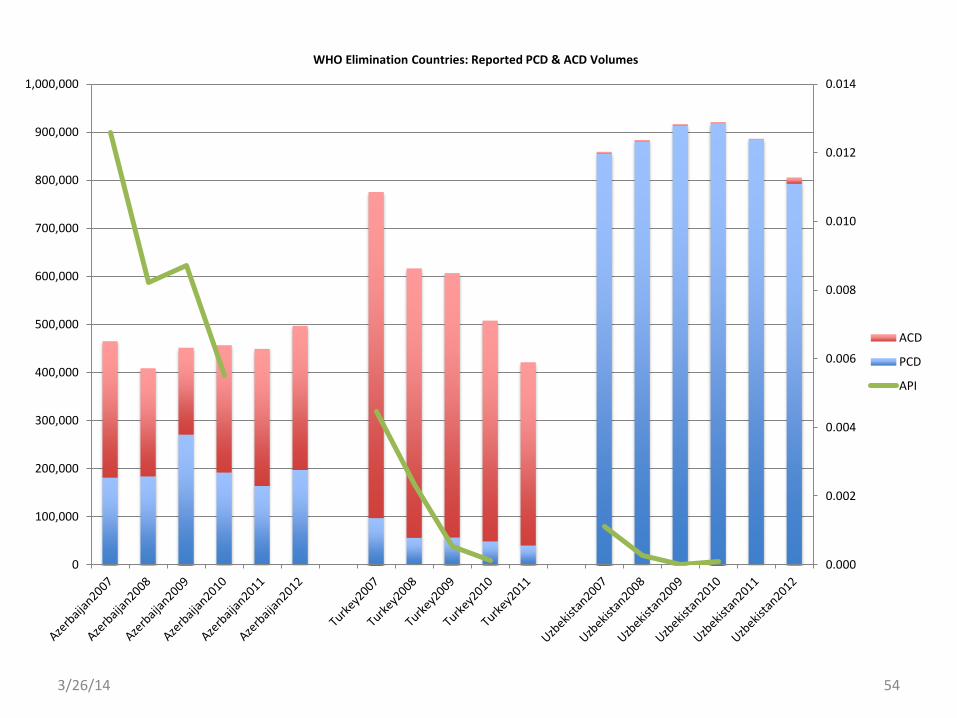

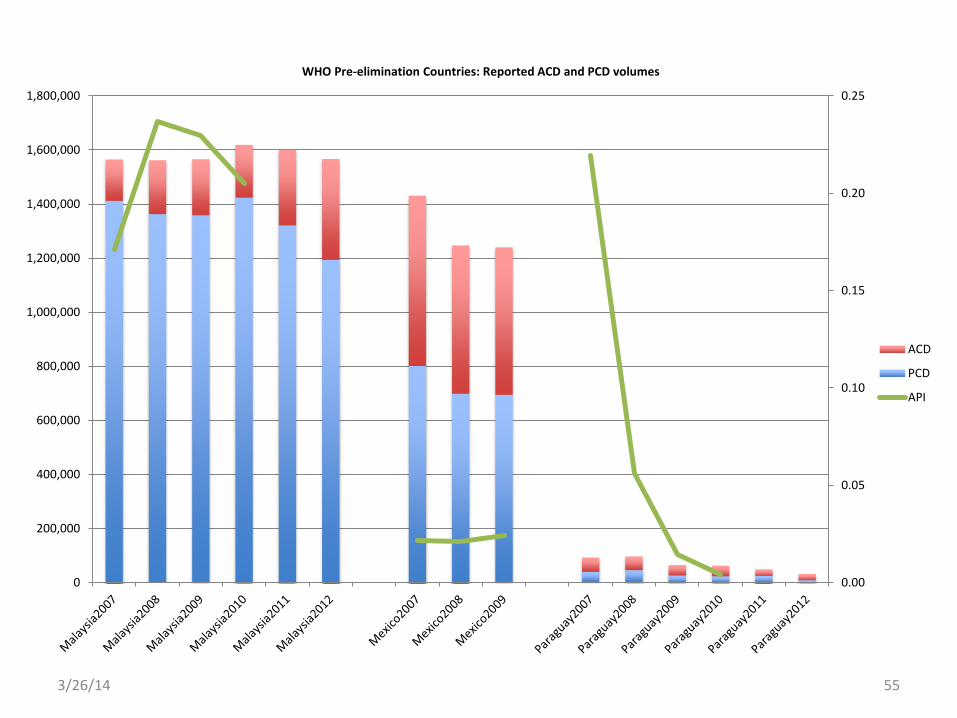

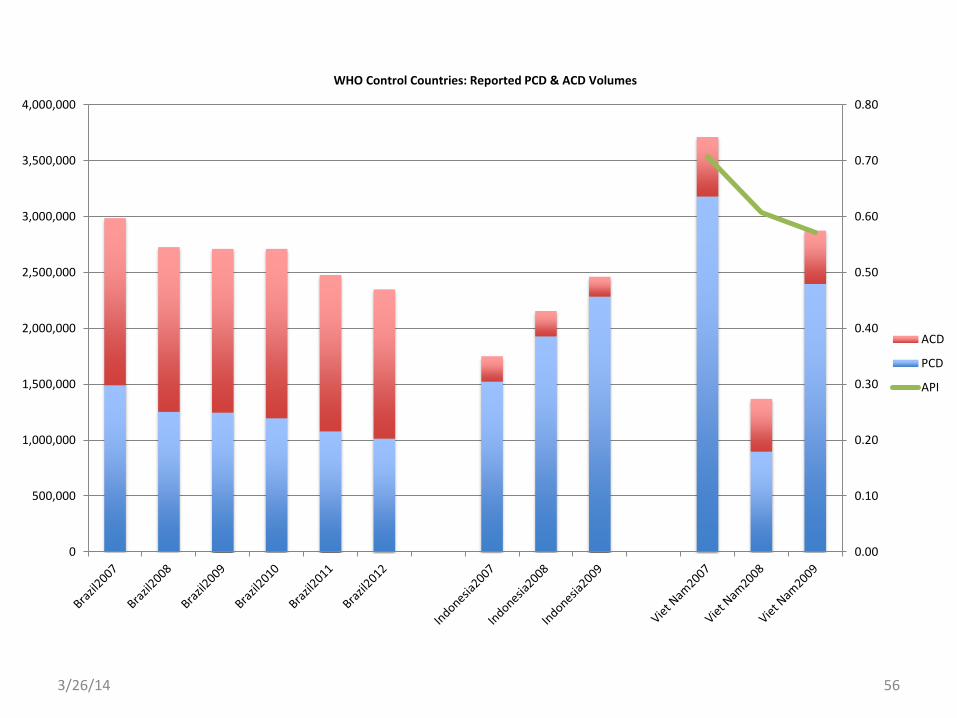

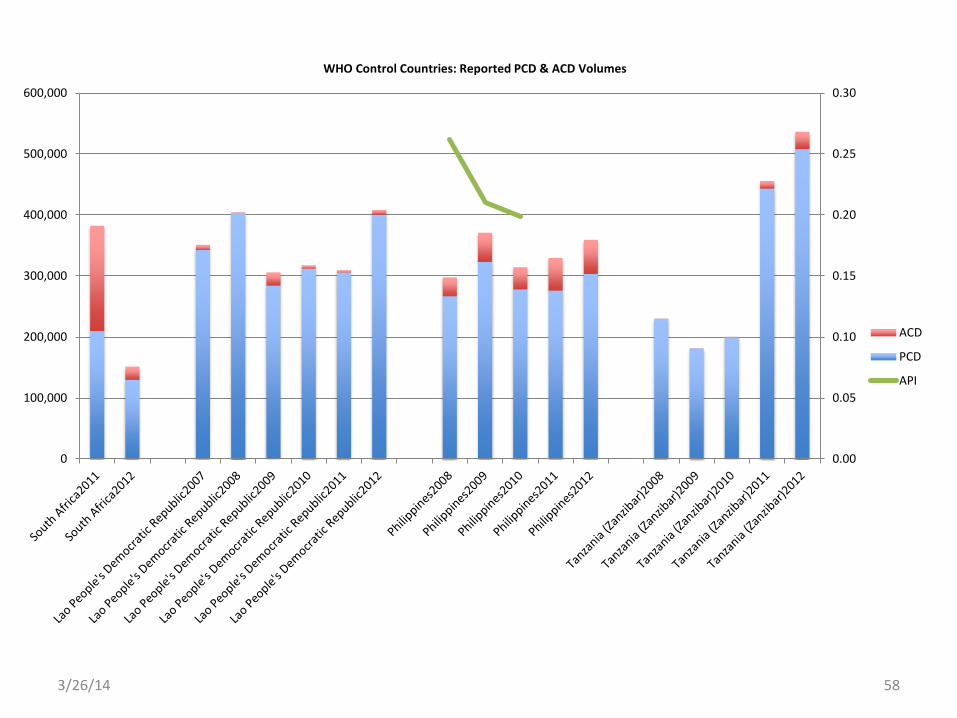

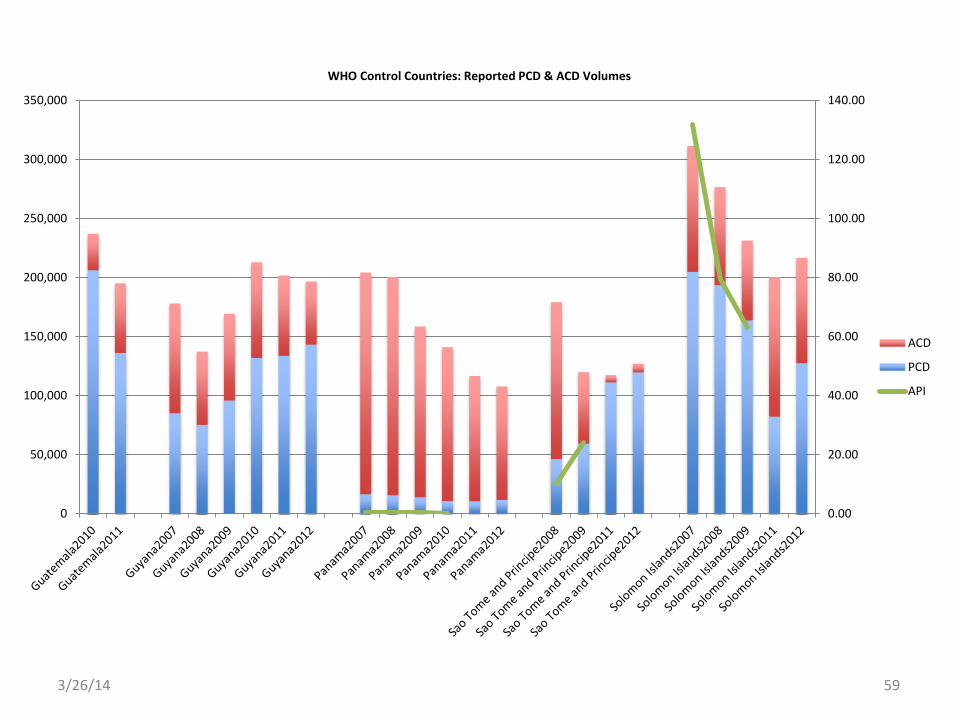

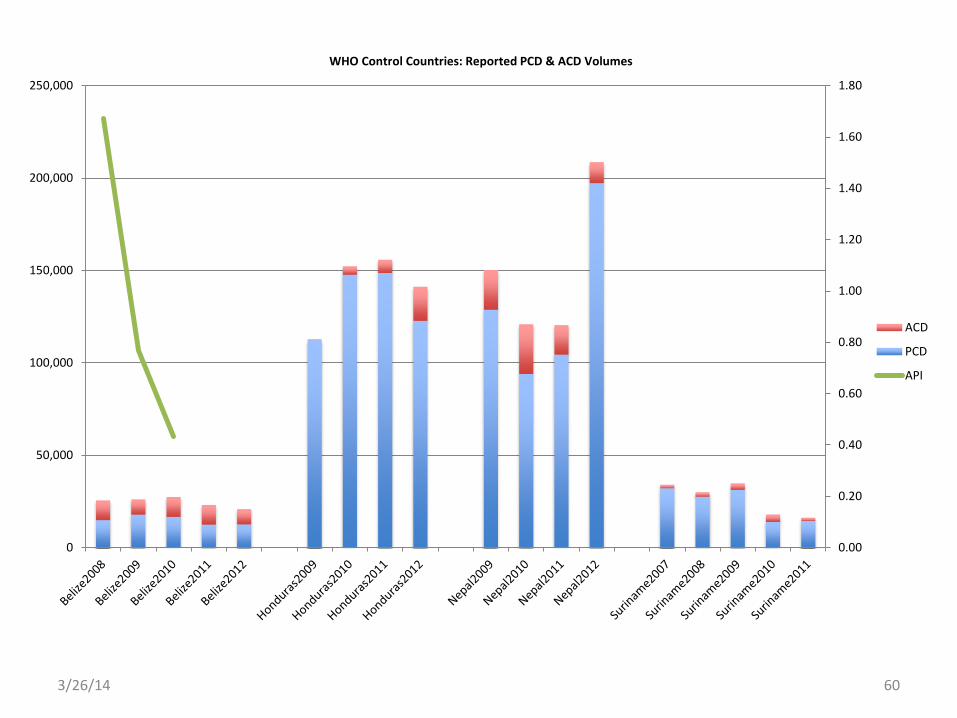

Testing volumes: Malaria-eliminating countries and active use scenarios

In order to gain a sense of the magnitude of testing, both in malaria-eliminating countries and for active use scenarios across all malaria-endemic countries, the following data were analyzed:

• Annual volume of testing done by all eliminating countries.

24

• Number of malaria-endemic countries with policies for active use.

• Breakdown in test volumes between PCD and active ID. The data sets analyzed are described below; all are derived from national reporting to the WHO. It is possible that countries did not follow reporting guidance; however, it would be impractical to validate all of the data provided. Selected validation of the data (e.g., high-volume countries) might, however, lend more confidence to the analysis, but was not performed given the timelines for this project.

2012 testing volumes in malaria-eliminating countries

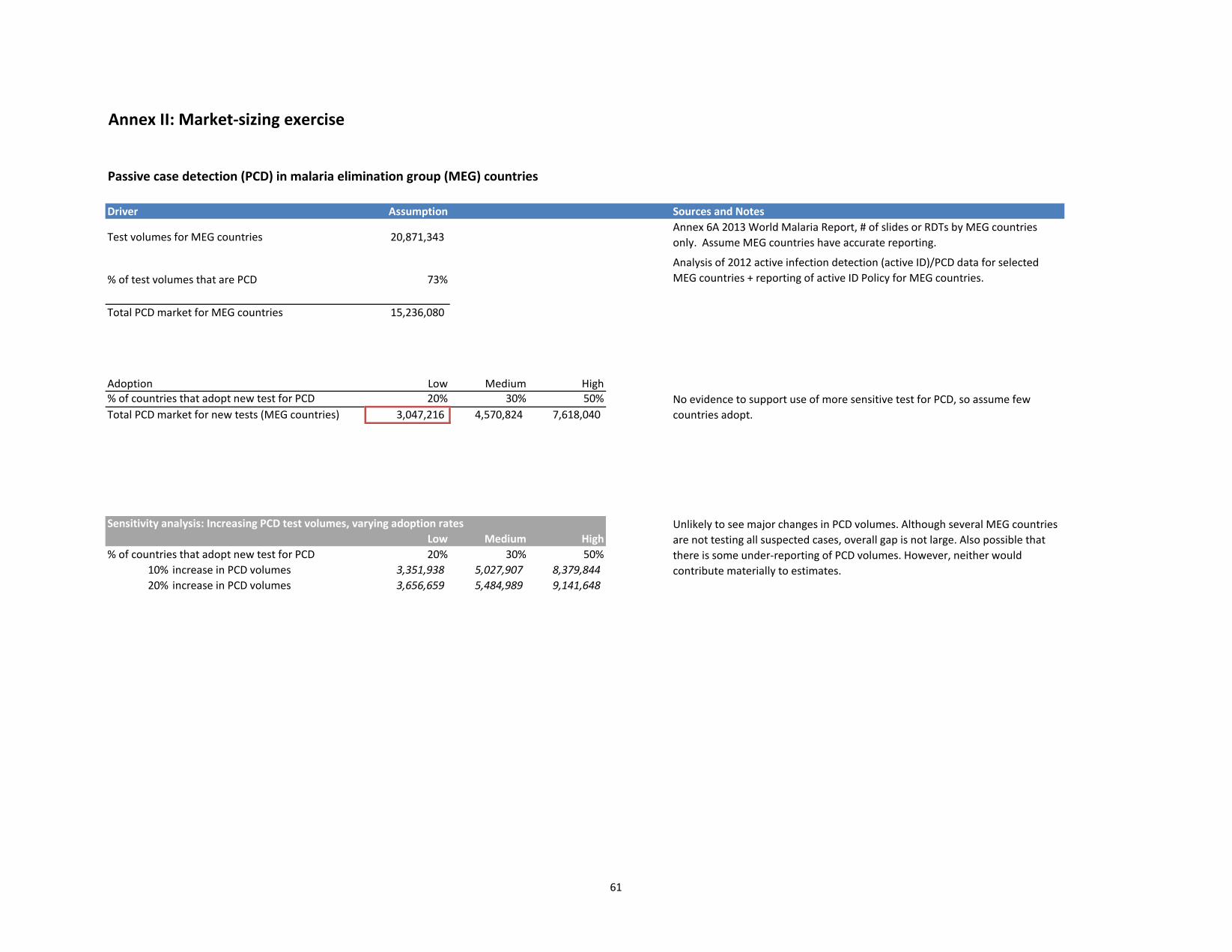

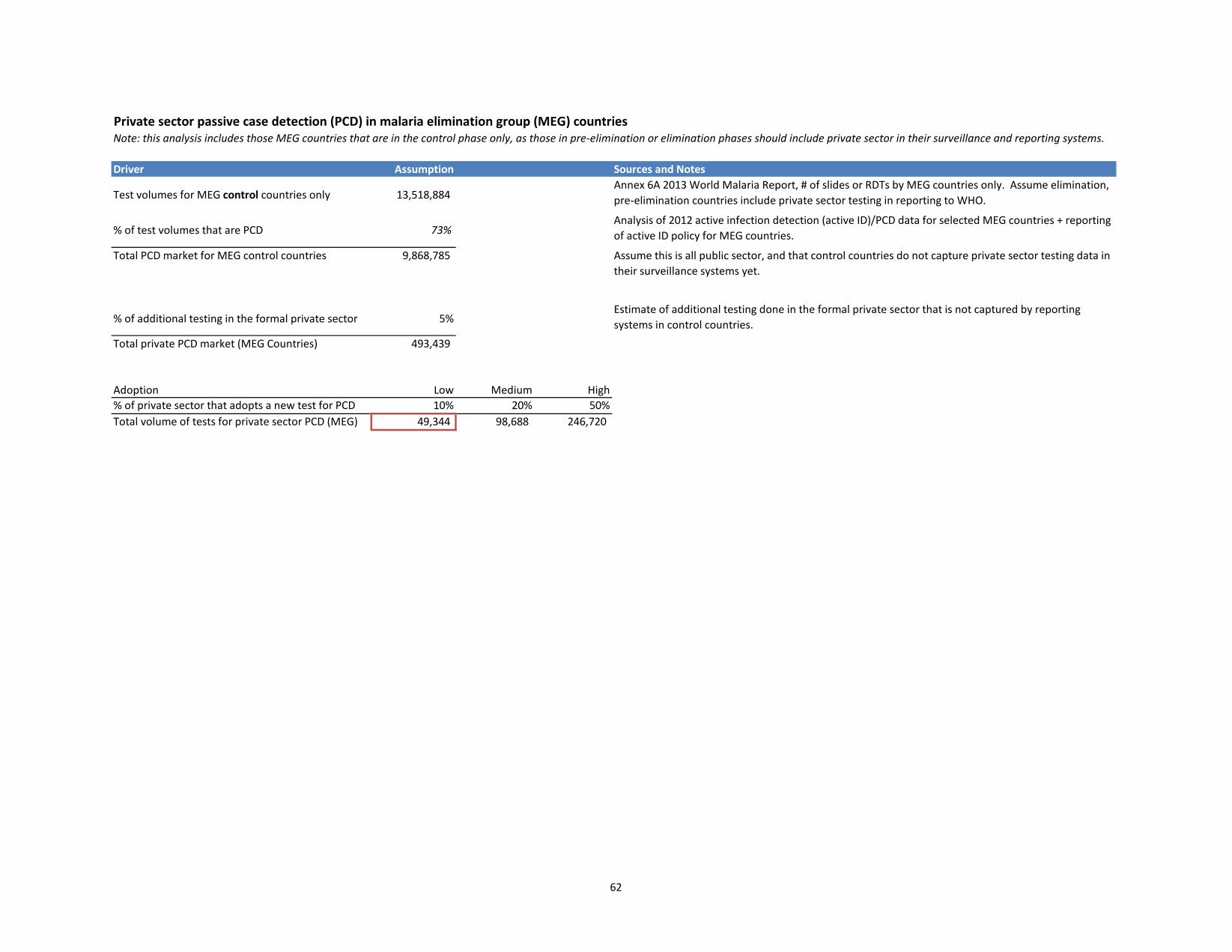

Data reported by national programs to the WHO on diagnostic testing volumes in 2012 were analyzed (specifically, Annex 6A of the 2013 World Malaria Report). While this data set is not reliable for high-burden countries due to weak reporting, countries considering elimination, by definition, have stronger reporting systems in place; and, therefore, the reported testing volumes should be reasonably accurate.xix In 2012, malaria-eliminating countries performed 20.9 million diagnostic tests (both PCD and active ID) (Table 4). Overall, the eliminating countries represented an estimated 5 percent of the global diagnostics market in 2012.xx

xix Of 103 countries that submitted data to the WHO, 62 countries representing 15 percent of the global burden are considered to have adequate reporting systems. The 34 malaria-eliminating countries are among these countries. The reported data for 41 higher-incidence countries, representing the remaining 85 percent of the global burden, are not sufficiently complete or consistent.2 xx Eliminating countries are 8.6 percent of the total volume of tests reported by endemic countries globally using data from Annex 6a of World Malaria Report 2013. However, while the total volume of tests performed in eliminating countries is likely accurate, the contribution of eliminating countries to the global total is over-represented due to poor reporting of testing in high-volume countries. Using a more accurate estimate for the denominator of 393 million tests (205 million RDTs + 188 million slides) performed globally suggests that 5 percent is a more reasonable estimate.

25

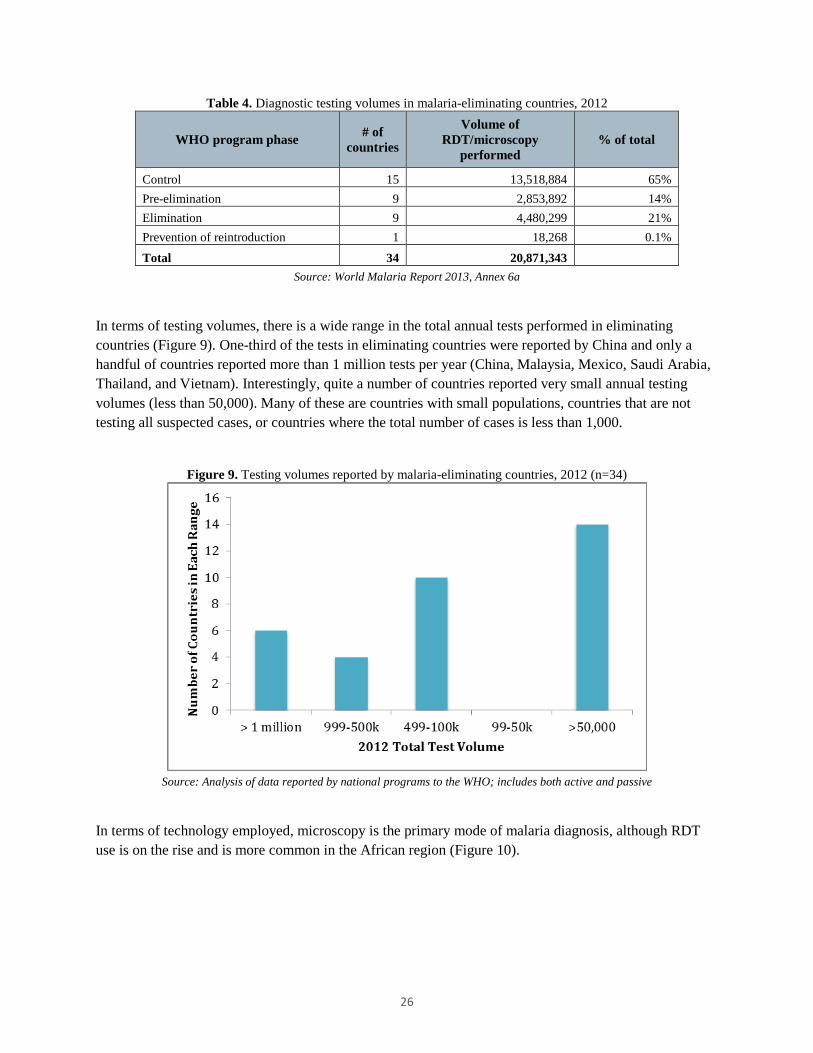

Table 4. Diagnostic testing volumes in malaria-eliminating countries, 2012

WHO program phase # of countries

Volume of RDT/microscopy

performed % of total

Control 15 13,518,884 65% Pre-elimination 9 2,853,892 14% Elimination 9 4,480,299 21% Prevention of reintroduction 1 18,268 0.1%

Total 34 20,871,343 Source: World Malaria Report 2013, Annex 6a

In terms of testing volumes, there is a wide range in the total annual tests performed in eliminating countries (Figure 9). One-third of the tests in eliminating countries were reported by China and only a handful of countries reported more than 1 million tests per year (China, Malaysia, Mexico, Saudi Arabia, Thailand, and Vietnam). Interestingly, quite a number of countries reported very small annual testing volumes (less than 50,000). Many of these are countries with small populations, countries that are not testing all suspected cases, or countries where the total number of cases is less than 1,000.

Figure 9. Testing volumes reported by malaria-eliminating countries, 2012 (n=34)

Source: Analysis of data reported by national programs to the WHO; includes both active and passive

In terms of technology employed, microscopy is the primary mode of malaria diagnosis, although RDT use is on the rise and is more common in the African region (Figure 10).

26

Figure 10. Proportion of RDTs versus microscopy, 2010 and 2012, by WHO region

EMRO = Eastern Mediterranean Regional Office; SEARO = South-East Asia Regional Office; WPRO = Western Pacific Regional Office

Source: Analysis of unpublished data reported by national programs to the WHO;xxi includes both active and passive

Policies for active use scenarios (all malaria-endemic countries)

Figure 11 and Table 5 summarize data on active use scenarios reported by countries and published in the 2013 World Malaria Report. Given the magnitude of countries, these data were not validated and it is possible that countries did not interpret WHO reporting guidelines correctly. In summary, many countries have policies for reactive ID (42) and proactive ID (38), as well as for MTAT (30). Additionally, many countries in the control phase have adopted strategies that are generally considered to be elimination tactics. The data also indicate that even among eliminating countries, there is variety in the tactics employed.

xxi Analysis based on unpublished data reported by national programs to the WHO (data set described below in the section comparing active ID and PCD volumes), supplemented by additional information where available (e.g., WHO data were compared to Global Fund RDT procurement data available for 14 eliminating countries and RDT volumes adjusted upward where relevant).

27

Figure 11. Countries reporting active use scenarios to the WHO

*ACD = active case detection (referred to as “active infection detection” in this report)

Source: Analysis of policy reporting by national programs to the WHO, published in World Malaria Report 2013 (Country Profiles)

Table 5. Percentage of countries reporting active use scenarios to the WHO, by program phase

Control Pre-elimination Elimination Prevention of reintroduction

Active ID for case investigation (reactive) 33% 82% 67% 100% Active ID at the community level of febrile cases (proactive) 32% 55% 78% 0%

Mass screening is undertaken 28% 45% 22% 100% Source: Analysis of policy reporting by national programs to the WHO,

published in World Malaria Report 2013 (Country Profiles)

Comparing passive and active infection detection volumes (subset of malaria-endemic countries)

In order to gain a sense of the magnitude of passive and active diagnostic test volumes, and how these change as programs progress toward elimination, an unpublished data set of 648 entries, covering 2007 through 2012 for 108 countries (provided by the WHO), was analyzed. As part of annual reporting to the WHO, national programs from endemic countries report the total volumes of diagnostic tests performed, breaking out volumes according to PCD and active ID. In order to create a subset of countries that reported both active and passive volumes, the data were cleaned as follows: (1) countries that did not report any active ID volumes were excluded (62 percent of the total data entries); and (2) testing volumes for the remaining countries were reviewed for consistency and anomalies that may have resulted from misinterpretation of the reporting guidelines (excluding an additional 14 percent of data entries). The final set of data analyzed comprised 24 percent of the original set, representing 32 countries (157 entries). For the countries included in this data set, the data have been treated in the way countries are asked to report; however, it is possible that some countries do not follow reporting guidance. Additional validation of the data with countries and experts might be informative, although this was not possible given the timelines for this project. For example, some countries did not report active ID volumes every year, and it would be interesting to know if this was an oversight in reporting or if there was indeed a gap in active ID.

28

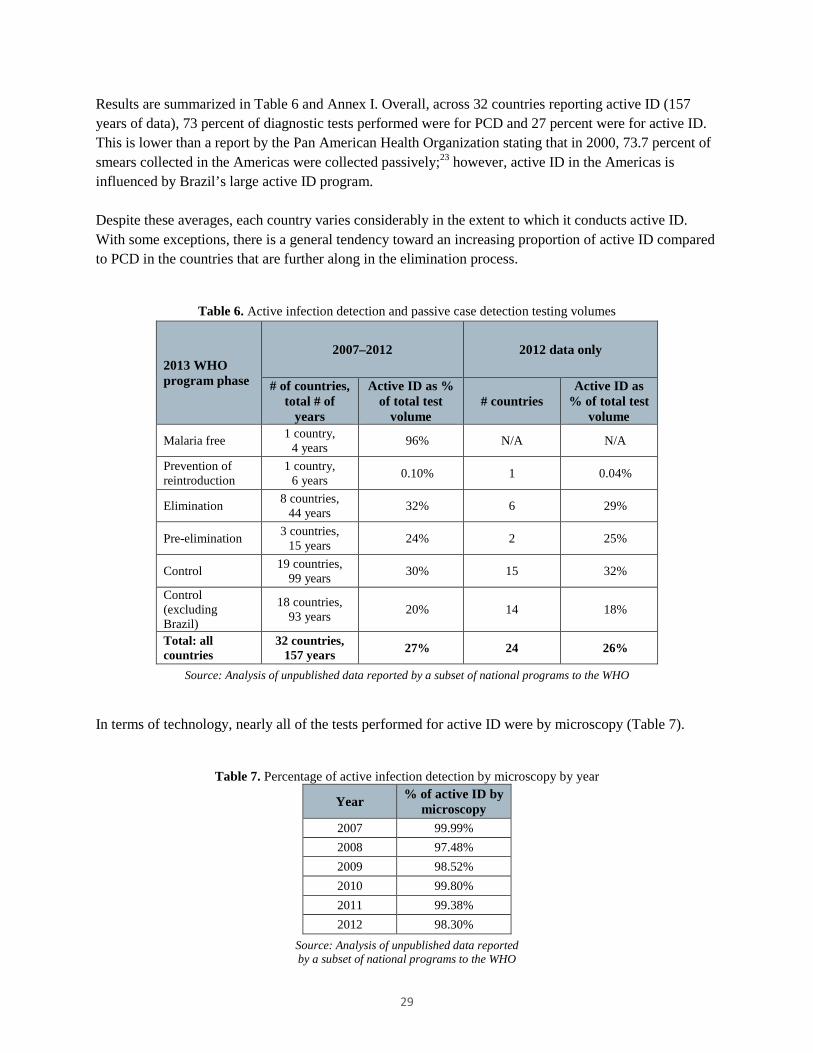

Results are summarized in Table 6 and Annex I. Overall, across 32 countries reporting active ID (157 years of data), 73 percent of diagnostic tests performed were for PCD and 27 percent were for active ID. This is lower than a report by the Pan American Health Organization stating that in 2000, 73.7 percent of smears collected in the Americas were collected passively;23 however, active ID in the Americas is influenced by Brazil’s large active ID program. Despite these averages, each country varies considerably in the extent to which it conducts active ID. With some exceptions, there is a general tendency toward an increasing proportion of active ID compared to PCD in the countries that are further along in the elimination process.

Table 6. Active infection detection and passive case detection testing volumes

2013 WHO program phase

2007–2012 2012 data only

# of countries, total # of

years

Active ID as % of total test

volume # countries

Active ID as % of total test

volume

Malaria free 1 country, 4 years 96% N/A N/A

Prevention of reintroduction

1 country, 6 years 0.10% 1 0.04%

Elimination 8 countries, 44 years 32% 6 29%

Pre-elimination 3 countries, 15 years 24% 2 25%

Control 19 countries, 99 years 30% 15 32%

Control (excluding Brazil)

18 countries, 93 years 20% 14 18%

Total: all countries

32 countries, 157 years 27% 24 26%