Oilfield Services Newsletter | August 2016 Oil & Gas Team Duane Donner [email protected] Joe Brady [email protected] John Sullivan [email protected] John Ortstadt [email protected] Vaughn McCrary [email protected] Jackson Poe [email protected] Matt Roden [email protected] Recent Market Trends With another recent dive in oil prices to $40 a barrel on August 1, some were once again making a run for cover, but hope is not as fleeting this time around. Oil prices have recovered and the industry is showing more signs of a recovery as many industry leaders have called bottom and noted the worst is in the rear view mirror. David Lesar, CEO of Halliburton noted on their Q2 earnings call, “Despite these continuing headwinds, based on the recent improvements to North American activity, I believe that this second quarter will mark the trough for our earnings…Today our customers are thinking about growing their business again rather than being focused on survival.” With that said, we must hedge our thoughts using a notable quote from former oil executive Bill Dore’ Founder and former CEO of Global Industries Ltd., also Duane Donner’s father-in-law, “There are two types of people when it comes to predicting oil prices, those who don’t know, and those who know they don’t know.” Keeping that in mind, we will share an M&A update and some of the recent projections that Founders and Spears & Associates produced, in this August edition of the Oilfield Services Newsletter. Market Fundamentals Outlook OFS Newsletter | August 2016 Source: Mergers&Acquisitions “Dealmakers predict M&A in the energy industry will accelerate over the next 12 months, according to Mergers and Acquisitions’ Market Pulse, a forward- looking sentiment indicator” - Mergers&Acquisitions Improving Sentiment for Energy M&A The following chart can be viewed as a barometer for the outlook of M&A activity and conditions from the perspective of approximately 250 executives, collectively, from various private equity, investment banking, lending, and other advisory firms. Note that Energy, of all industries polled, has the most favorable 12-month outlook. 52.3 47.3 53.8 67.3 48 76.2 71.4 69.3 74.1 62.1 0 20 40 60 80 100 Energy Technology Healthcare Consumer Goods Manufacturing 3 - Month Forecast 12 - Month Forecast M&A Sentiment by Industry

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Oilfield Services Newsletter | August 2016

Oil & Gas Team

Duane [email protected]

John [email protected]

John [email protected]

Vaughn [email protected]

Jackson [email protected]

Matt [email protected]

Recent Market Trends

With another recent dive in oil prices to $40 a barrel on August 1, some were once againmaking a run for cover, but hope is not as fleeting this time around. Oil prices haverecovered and the industry is showing more signs of a recovery as many industry leadershave called bottom and noted the worst is in the rear view mirror. David Lesar, CEO ofHalliburton noted on their Q2 earnings call, “Despite these continuing headwinds, basedon the recent improvements to North American activity, I believe that this secondquarter will mark the trough for our earnings…Today our customers are thinking aboutgrowing their business again rather than being focused on survival.” With that said, wemust hedge our thoughts using a notable quote from former oil executive Bill Dore’Founder and former CEO of Global Industries Ltd., also Duane Donner’s father-in-law,“There are two types of people when it comes to predicting oil prices, those who don’tknow, and those who know they don’t know.” Keeping that in mind, we will share anM&A update and some of the recent projections that Founders and Spears & Associatesproduced, in this August edition of the Oilfield Services Newsletter.

Market Fundamentals OutlookOFS Newsletter | August 2016

Source: Mergers&Acquisitions

“Dealmakers predict M&A in the energy

industry will accelerate over the next 12

months, according to Mergers and

Acquisitions’ Market Pulse, a forward-looking sentiment

indicator”

- Mergers&Acquisitions

Improving Sentiment for Energy M&A

The following chart can be viewed as a barometer for the outlook of M&A activity andconditions from the perspective of approximately 250 executives, collectively, fromvarious private equity, investment banking, lending, and other advisory firms. Note thatEnergy, of all industries polled, has the most favorable 12-month outlook.

52.347.3

53.8

67.3

48

76.271.4 69.3

74.1

62.1

0

20

40

60

80

100

Energy Technology Healthcare Consumer Goods Manufacturing

3 - Month Forecast 12 - Month Forecast

M&A Sentiment by Industry

Oilfield Services Newsletter | August 2016

Market Fundamentals Outlook

“Dealmakers predict M&A in the energy

industry will accelerate over the

next 12 months, according to Mergers and

Acquisitions’ Market Pulse, a forward-looking sentiment

indicator”

“We have won 8 of the last 8 bids for

projects, raising our prices for each

subsequent project.”- OFS CEO (Former

Founders client)

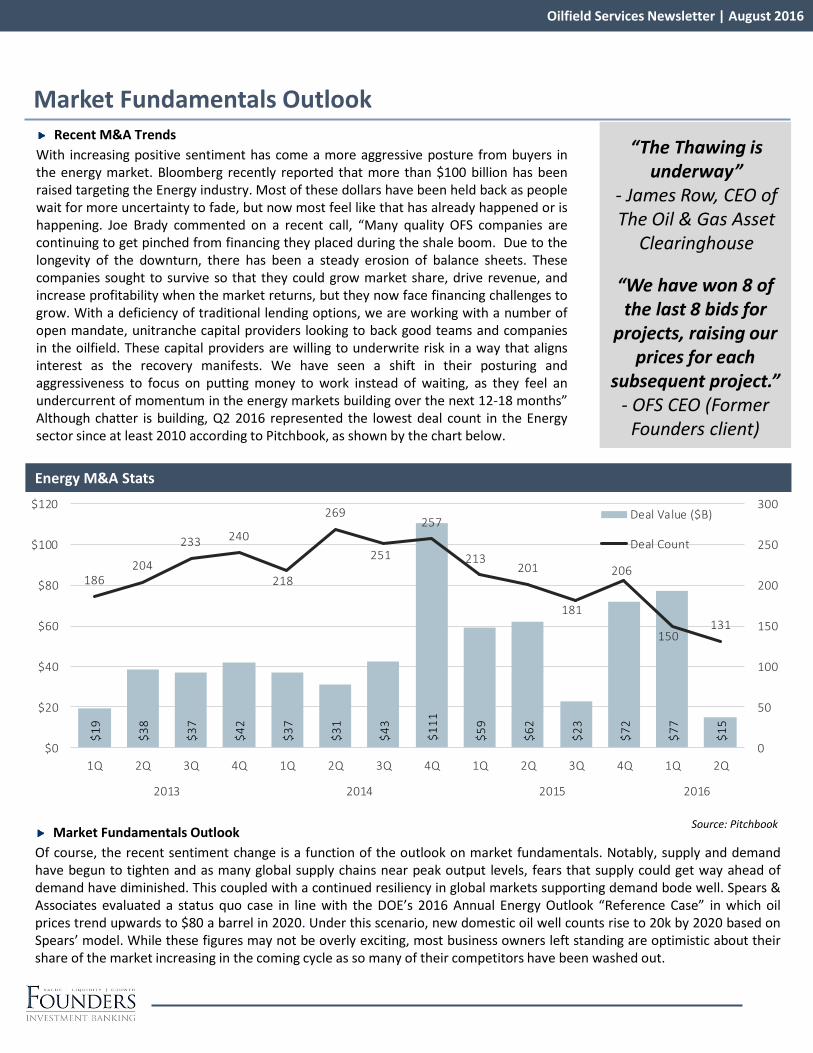

Recent M&A Trends

With increasing positive sentiment has come a more aggressive posture from buyers inthe energy market. Bloomberg recently reported that more than $100 billion has beenraised targeting the Energy industry. Most of these dollars have been held back as peoplewait for more uncertainty to fade, but now most feel like that has already happened or ishappening. Joe Brady commented on a recent call, “Many quality OFS companies arecontinuing to get pinched from financing they placed during the shale boom. Due to thelongevity of the downturn, there has been a steady erosion of balance sheets. Thesecompanies sought to survive so that they could grow market share, drive revenue, andincrease profitability when the market returns, but they now face financing challenges togrow. With a deficiency of traditional lending options, we are working with a number ofopen mandate, unitranche capital providers looking to back good teams and companiesin the oilfield. These capital providers are willing to underwrite risk in a way that alignsinterest as the recovery manifests. We have seen a shift in their posturing andaggressiveness to focus on putting money to work instead of waiting, as they feel anundercurrent of momentum in the energy markets building over the next 12-18 months”Although chatter is building, Q2 2016 represented the lowest deal count in the Energysector since at least 2010 according to Pitchbook, as shown by the chart below.

Market Fundamentals Outlook

Of course, the recent sentiment change is a function of the outlook on market fundamentals. Notably, supply and demandhave begun to tighten and as many global supply chains near peak output levels, fears that supply could get way ahead ofdemand have diminished. This coupled with a continued resiliency in global markets supporting demand bode well. Spears &Associates evaluated a status quo case in line with the DOE’s 2016 Annual Energy Outlook “Reference Case” in which oilprices trend upwards to $80 a barrel in 2020. Under this scenario, new domestic oil well counts rise to 20k by 2020 based onSpears’ model. While these figures may not be overly exciting, most business owners left standing are optimistic about theirshare of the market increasing in the coming cycle as so many of their competitors have been washed out.

“The Thawing is underway”

- James Row, CEO of The Oil & Gas Asset

Clearinghouse

Energy M&A Stats

Source: Pitchbook

$1

9

$3

8

$3

7

$4

2

$3

7

$3

1

$4

3

$1

11

$5

9

$6

2

$2

3

$7

2

$7

7

$1

5

186204

233 240

218

269

251

257

213201

181

206

150131

0

50

100

150

200

250

300

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2013 2014 2015 2016

Deal Value ($B)

Deal Count

Oilfield Services Newsletter | August 2016

Market Fundamentals Outlook

3

Recent M&A Activity

Conclusion

Improving market fundamentals have given many industry constituents hope that conditions will significantly improve in thenext 12 months, but as we recently wrote about in our last newsletter – projections are quite prone to error. Hopefully theindustry consensus is more right than wrong this time around. If you still remain hopeless, we would like to point you to arecent article by Richard Spears of Spears & Associates that we thoroughly enjoyed – The Boom of 2017.

Source: CapitalIQ

Domestic Oil Production and New Oil Wells

Source: Spears & Associates, EIA

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2012 2013 2014 2015 2016E 2017P 2018P 2019P 2020P

(Wel

l Co

un

t)

(Mil

lio

ns

of B

arr

els

per

Da

y)

Lower - 48 Onshore Alaska Offshore New Domestic Oil Wells

Announced Date

Target Buyers / InvestorsTransaction Value ($M)

7/28/2016 GRS Inc. National Oilwell Varco, Inc. -

7/28/2016 DJ Oilfield Services Co., Ltd. National Oilwell Varco, Inc. -

7/18/2016 Ulterra Drilling Technologies, L.P. American Securities -

7/14/2016 Managed Pressure Operations LLC AFGlobal Corporation $75.00

7/13/2016 Redneck Oilfield Services Ltd. Strad Energy Services Ltd. $6.77

7/1/2016 AmSpec Services, LLC Olympus Partners; Olympus Growth Fund VI, L.P. -

6/2/2016 Omron Oilfield & Marine, Inc. Schlumberger Limited -

6/1/2016 Trican Well Service Ltd., Completion Tools BusinessDreco Energy Services ULC; National Oilwell Varco Norway AS; National Oilwell Varco Eurasia, LLC

$40.90

5/19/2016 FMC Technologies, Inc. Technip SA $5,269.02

5/11/2016 FMC Technologies, Inc., North American Wireline Assets Reliance Oilfield Services, LLC -

4/28/2016 Team Oil Tools, Inc., Wholesale Completion Packer Business Forum Energy Technologies, Inc. -

4/13/2016 Davy Crockett's Oilfield Services Ltd. Hallmark Tubulars Ltd. -

3/10/2016 Tolteq Group, LLC National Oilwell Varco, Inc. -

3/9/2016 Marlin Services LLC Gulf Coast Specialty Energy Services, LLC -

2/22/2016 Industrial Action Services, Inc. RelaDyne, Inc. -

Oilfield Services Newsletter | August 2016

Trading Statistics

4

FOUNDERS INVESTMENT BANKING, LLC

Public Comparables

(In millions, except per share data)

Stock Price % of 52-Week Market Enterprise 2016P Enterprise Value / 2017P Enterprise Value /

Ticker Company Name 8/18/16 High Low Cap Value Revenue EBITDA 2016 Revenue 2016 EBITDA Revenue EBITDA 2017 Revenue 2017 EBITDA

Integrated Equipment & Service Providers

NYSE: SLB Schlumberger Limited $ 83.86 99.9% 140.7% $ 116,623.6 $ 127,458.6 $ 29,163.0 $ 6,783.8 4.4x 18.8x $ 33,208.2 $ 8,265.6 3.8x 15.4x

NYSE: HAL Halliburton Company $ 46.46 99.5% 168.1% $ 40,006.8 $ 49,799.8 $ 15,971.0 $ 2,012.9 3.1x 24.7x $ 19,075.9 $ 3,277.5 2.6x 15.2x

NYSE: BHI Baker Hughes Incorporated $ 52.05 89.4% 138.5% $ 22,272.3 $ 21,471.3 $ 9,940.6 $ 326.9 2.2x 65.7x $ 11,146.8 $ 1,281.1 1.9x 16.8x

NYSE: WFT Weatherford International plc $ 5.91 51.4% 125.5% $ 5,296.3 $ 12,141.3 $ 5,913.0 $ 346.1 2.1x 35.1x $ 6,727.8 $ 890.4 1.8x 13.6x

Min $ 5.91 51.4% 125.5% $ 5,296.3 $ 12,141.3 $ 5,913.0 $ 326.9 2.1x 18.8x $ 6,727.8 $ 890.4 1.8x 13.6x

Median $ 49.26 94.4% 139.6% $ 31,139.5 $ 35,635.5 $ 12,955.8 $ 1,179.5 2.6x 29.9x $ 15,111.3 $ 2,279.3 2.3x 15.3x

Mean $ 47.07 85.0% 143.2% $ 46,049.7 $ 52,717.7 $ 15,246.9 $ 2,367.4 2.9x 36.1x $ 17,539.7 $ 3,428.6 2.5x 15.3x

Max $ 83.86 99.9% 168.1% $ 116,623.6 $ 127,458.6 $ 29,163.0 $ 6,783.8 4.4x 65.7x $ 33,208.2 $ 8,265.6 3.8x 16.8x

Equipment & Technology

NYSE: NOV National Oilwell Varco, Inc. $ 36.09 84.7% 140.2% $ 13,628.7 $ 15,315.7 $ 7,309.5 $ 270.2 2.1x 56.7x $ 7,611.2 $ 600.7 2.0x 25.5x

NYSE: FTI FMC Technologies, Inc. $ 28.55 79.5% 128.0% $ 6,441.6 $ 6,708.9 $ 4,655.6 $ 533.5 1.4x 12.6x $ 4,427.0 $ 547.7 1.5x 12.2x

NYSE: OII Oceaneering International, Inc. $ 29.29 60.9% 115.6% $ 2,872.2 $ 3,271.3 $ 2,395.3 $ 378.2 1.4x 8.6x $ 2,249.7 $ 334.3 1.5x 9.8x

NYSE: DRQ Dril-Quip, Inc. $ 58.64 84.5% 120.0% $ 2,203.1 $ 1,711.4 $ 542.1 $ 144.0 3.2x 11.9x $ 419.9 $ 77.0 4.1x 22.2x

NYSE: OIS Oil States International Inc. $ 33.15 90.3% 154.6% $ 1,702.0 $ 1,734.2 $ 688.0 $ 47.3 2.5x 36.7x $ 744.5 $ 77.5 2.3x 22.4x

NYSE: FET Forum Energy Technologies, Inc. $ 18.41 95.3% 220.7% $ 1,681.7 $ 1,941.4 $ 600.2 $ (24.2) 3.2x N/A $ 733.8 $ 50.1 2.6x 38.7x

Min $ 18.41 60.9% 115.6% $ 1,681.7 $ 1,711.4 $ 542.1 $ (24.2) 1.4x N/A $ 419.9 $ 50.1 1.5x 9.8x

Median $ 31.22 84.6% 134.1% $ 2,537.7 $ 2,606.4 $ 1,541.7 $ 207.1 2.3x 12.2x $ 1,497.1 $ 205.9 2.2x 22.3x

Mean $ 34.02 82.5% 146.5% $ 4,754.9 $ 5,113.8 $ 2,698.5 $ 224.8 2.3x 7.7x $ 2,697.7 $ 281.2 2.3x 21.8x

Max $ 58.64 95.3% 220.7% $ 13,628.7 $ 15,315.7 $ 7,309.5 $ 533.5 3.2x 56.7x $ 7,611.2 $ 600.7 4.1x 38.7x

Service Providers

NYSE: SPN Superior Energy Services, Inc. $ 18.36 92.6% 222.5% $ 2,785.2 $ 3,833.2 $ 1,504.0 $ 119.2 2.5x 32.2x $ 1,850.2 $ 282.1 2.1x 13.6x

NYSE: FI Frank's International N.V. $ 12.75 70.3% 112.3% $ 1,991.6 $ 1,630.5 $ 491.8 $ 13.0 3.3x 125.0x $ 482.8 $ 40.2 3.4x 40.6x

TSX: ESI Ensign Energy Services Inc. $ 6.00 72.4% 162.5% $ 918.9 $ 1,439.1 $ 673.6 $ 138.7 2.1x 10.4x $ 830.7 $ 171.4 1.7x 8.4x

TSX: CFW Calfrac Well Services Ltd. $ 2.72 70.0% 327.4% $ 313.9 $ 947.3 $ 592.4 $ (16.6) 1.6x N/A $ 826.7 $ 50.4 1.1x 18.8x

TSX: TCW Trican Well Service Ltd. $ 1.84 84.8% 701.5% $ 353.9 $ 527.8 $ 261.4 $ (36.3) 2.0x N/A $ 445.2 $ 34.5 1.2x 15.3x

NasdaqGS: TESO Tesco Corporation $ 7.45 76.3% 145.4% $ 345.7 $ 245.0 $ 129.6 $ (34.0) 1.9x N/A $ 162.7 $ (15.3) 1.5x N/A

NYSE: BAS Basic Energy Services, Inc. $ 0.69 12.3% 113.1% $ 29.5 $ 947.7 $ 510.9 $ (40.0) 1.9x N/A $ 687.0 $ 32.8 1.4x 28.9x

NYSE: RES RPC Inc. $ 16.21 96.3% 191.8% $ 3,526.4 $ 3,385.1 $ 667.4 $ (57.4) 5.1x N/A $ 1,035.5 $ 96.7 3.3x 35.0x

NYSE: TTI TETRA Technologies, Inc. $ 6.67 70.7% 144.4% $ 618.3 $ 1,580.0 $ 750.2 $ 131.1 2.1x 12.1x $ 883.0 $ 188.9 1.8x 8.4x

Min $ 0.69 12.3% 112.3% $ 29.5 $ 245.0 $ 129.6 $ (57.4) 1.6x N/A $ 162.7 $ (15.3) 1.1x N/A

Median $ 6.67 72.4% 162.5% $ 618.3 $ 1,439.1 $ 592.4 $ (16.6) 2.1x N/A $ 826.7 $ 50.4 1.7x 15.3x

Mean $ 8.08 71.7% 235.7% $ 1,209.3 $ 1,615.1 $ 620.2 $ 24.2 2.5x 2.0x $ 800.4 $ 98.0 1.9x 17.0x

Max $ 18.36 96.3% 701.5% $ 3,526.4 $ 3,833.2 $ 1,504.0 $ 138.7 5.1x 125.0x $ 1,850.2 $ 282.1 3.4x 40.6x

Offshore Drillers

NYSE: RIG Transocean Ltd. $ 10.62 61.8% 138.6% $ 3,880.5 $ 10,266.5 NA NA N/A N/A $ 3,112.0 $ 1,166.4 3.3x 8.8x

NYSE: ESV Ensco plc $ 8.99 47.5% 124.0% $ 2,710.0 $ 5,822.3 $ 2,602.3 $ 1,221.6 2.2x 4.8x $ 2,012.1 $ 818.1 2.9x 7.1x

NYSE: DO Diamond Offshore Drilling, Inc. $ 20.31 76.0% 143.3% $ 2,785.9 $ 4,990.2 $ 1,639.6 $ 686.4 3.0x 7.3x $ 1,579.2 $ 679.7 3.2x 7.3x

NYSE: NE Noble Corporation plc $ 6.50 44.4% 104.7% $ 1,580.9 $ 5,610.1 $ 2,104.8 $ 942.7 2.7x 6.0x $ 1,499.7 $ 575.8 3.7x 9.7x

NYSE: RDC Rowan Companies plc $ 14.45 66.2% 135.4% $ 1,812.3 $ 3,696.3 $ 1,731.7 $ 798.6 2.1x 4.6x $ 1,422.9 $ 566.0 2.6x 6.5x

Min $ 6.50 44.4% 104.7% $ 1,580.9 $ 3,696.3 $ 1,639.6 $ 686.4 2.1x 4.6x $ 1,422.9 $ 566.0 2.6x 6.5x

Median $ 10.62 61.8% 135.4% $ 2,710.0 $ 5,610.1 $ 1,918.3 $ 870.6 2.5x 5.4x $ 1,579.2 $ 679.7 3.2x 7.3x

Mean $ 12.17 59.2% 129.2% $ 2,553.9 $ 6,077.1 $ 2,019.6 $ 912.3 2.5x 5.7x $ 1,925.2 $ 761.2 3.1x 7.9x

Max $ 20.31 76.0% 143.3% $ 3,880.5 $ 10,266.5 $ 2,602.3 $ 1,221.6 3.0x 7.3x $ 3,112.0 $ 1,166.4 3.7x 9.7x

Land Drillers

NYSE: HP Helmerich & Payne, Inc. $ 64.67 92.0% 161.6% $ 6,988.6 $ 6,564.4 $ 1,525.6 $ 438.6 4.3x 15.0x $ 1,414.3 $ 362.5 4.6x 18.1x

NYSE: NBR Nabors Industries Ltd. $ 10.31 83.6% 209.1% $ 2,921.6 $ 6,176.0 $ 2,239.6 $ 595.9 2.8x 10.4x $ 2,504.6 $ 680.7 2.5x 9.1x

NasdaqGS: PTEN Patterson-UTI Energy Inc. $ 21.17 95.7% 193.6% $ 3,127.6 $ 3,744.8 $ 878.9 $ 192.1 4.3x 19.5x $ 1,203.9 $ 255.1 3.1x 14.7x

NYSE: PES Pioneer Energy Services Corp. $ 3.76 74.5% 395.7% $ 243.1 $ 616.1 $ 272.4 $ 15.5 2.3x 39.8x $ 377.6 $ 45.5 1.6x 13.5x

Min $ 3.76 74.5% 161.6% $ 243.1 $ 616.1 $ 272.4 $ 15.5 2.3x 10.4x $ 377.6 $ 45.5 1.6x 9.1x

Median $ 15.74 87.8% 201.4% $ 3,024.6 $ 4,960.4 $ 1,202.2 $ 315.4 3.5x 17.2x $ 1,309.1 $ 308.8 2.8x 14.1x

Mean $ 24.98 86.4% 240.0% $ 3,320.2 $ 4,275.3 $ 1,229.1 $ 310.5 3.4x 21.1x $ 1,375.1 $ 336.0 3.0x 13.8x

Max $ 64.67 95.7% 395.7% $ 6,988.6 $ 6,564.4 $ 2,239.6 $ 595.9 4.3x 39.8x $ 2,504.6 $ 680.7 4.6x 18.1x

Source: CapitalIQ

Oilfield Services Newsletter | August 2016

Recent Trends

5

Crude Oil (NYMEX: CL)

Domestic Oil and Natural Gas Rig Count

Domestic Crude Oil Production

Source: CapitalIQ, EIA

200

250

300

350

400

450

500

550

600

650

700

(Rig

Co

un

t)

250

255

260

265

270

275

280

285

290

295

300

(Mill

ion

s o

f Bar

rels

)

$20

$30

$40

$50

$60

$70

$80

$90

$100

(Pri

ce p

er B

arre

l)

Oilfield Services Newsletter | August 2016

Domestic Oil Trends

6

Notable Trends2012 2013 2014 2015 2016E 2017P 2018P 2019P 2020P

Avg. Oil Price

Avg. Rig Count

New Wells Drilled

Production (M b/d)

$94.18 $98.02 $93.22 $48.59 $42.20 $52.25 $62.00 $70.00 $80.00

1,335 1,334 1,485 728 380 500 630 810 965

New Wells Drilled per Rig

31,425 32,150 33,150 19,250 8,650 11,100 13,300 17,000 20,000

5.2 6.1 7.3 7.9 6.9 7.4 7.4 7.7 8.0

23.5 24.1 22.3 26.4 22.8 22.2 22.1 21.0 20.7

Source: CapitalIQ, EIA, Spears & Associates

Domestic New Oil Well Count and Production

Crude Oil Price and Rig Count

$-

$20

$40

$60

$80

$100

$120

0

200

400

600

800

1,000

1,200

1,400

1,600

(Pri

ce p

er B

arre

l)

(Rig

Co

un

t)

Rig Count Oil Price

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

1

2

3

4

5

6

7

8

9

(New

Wel

ls D

rille

d)

(Pro

du

ctio

n -

M b

/d)

Production (M b/d) New Wells Drilled

Oilfield Services Newsletter | August 2016

Domestic Natural Gas Trends

7

Notable Trends2012 2013 2014 2015 2016E 2017P 2018P 2019P 2020P

Avg. Nat. Gas Price

Avg. Rig Count

New Wells Drilled

Production (Mcf/d)

$2.75 $3.73 $4.32 $2.62 $2.35 $3.13 $3.25 $3.40 $3.60

534 368 318 219 105 140 180 220 255

New Wells Drilled per Rig

9,500 7,800 7,150 4,850 2,450 3,450 4,375 6,000 7,750

767.5 772.5 823.8 864.2 NA NA NA NA NA

17.8 21.2 22.5 22.2 23.3 24.6 24.3 27.3 30.4

Natural Gas Price and Rig Count

Source: CapitalIQ, EIA, Spears & Associates

Domestic Natural Gas Production

$- $1 $2 $3 $4 $5 $6 $7 $8 $9 $10

0

200

400

600

800

1,000

1,200

1,400

1,600

(Pri

ce p

er M

BTU

)

(Rig

Co

un

t)

Rig Count Natural Gas Price

0

100

200

300

400

500

600

700

800

900

1,000

(Gro

ss W

ith

dra

wal

s -M

cf/d

)

Oilfield Services Newsletter | August 2016

Trends by Basin

8

YTD Change in Rig Count

Current Natural Gas and Oil Rig Count

Oil Production Natural Gas Production

0 1 2 3 5 9 14 14 18 24 27 32 36

110

196

0

50

100

150

200

250

(Rig

Co

un

t)

0.0

0.5

1.0

1.5

2.0

2.5

(Pro

du

ctio

n -

M b

/d)

Sep-15 Sep-16

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000(P

rod

uct

ion

-M

cf/d

)

Sep-15 Sep-16

-1 -1 -6 -9 -2 -6 -11 -1 -5 -17 -26 -6 -40 -55 -21

-60

-50

-40

-30

-20

-10

0

(Rig

Co

un

t)

Oilfield Services Newsletter | August 2016

Offshore Trends

9

Crude Oil Price and Rig Count

Source: CapitalIQ, EIA, Spears & Associates

Offshore U.S. Production

Notable Trends2012 2013 2014 2015 2016E 2017P 2018P 2019P 2020P

Avg. Oil Price

Avg. Rig Count

Wells Drilled

Production (M b/d)

$94.18 $98.02 $93.22 $48.59 $42.20 $52.25 $62.00 $70.00 $80.00

24 38 41 26 NA NA NA NA NA

Wells Drilled per Rig

375 440 450 275 210 275 350 400 430

1.3 1.3 1.4 1.6 1.7 1.9 2.0 2.1 2.2

15.6 11.5 10.9 10.6 NA NA NA NA NA

$-

$20

$40

$60

$80

$100

$120

0

5

10

15

20

25

30

35

40

45

(Pri

ce p

er B

arre

l)

(Rig

Co

un

t)

Rig Count Crude Oil Price

0.0

0.5

1.0

1.5

2.0

2.5

(Pro

du

ctio

n -

M b

/d)

Oilfield Services Newsletter | August 2016

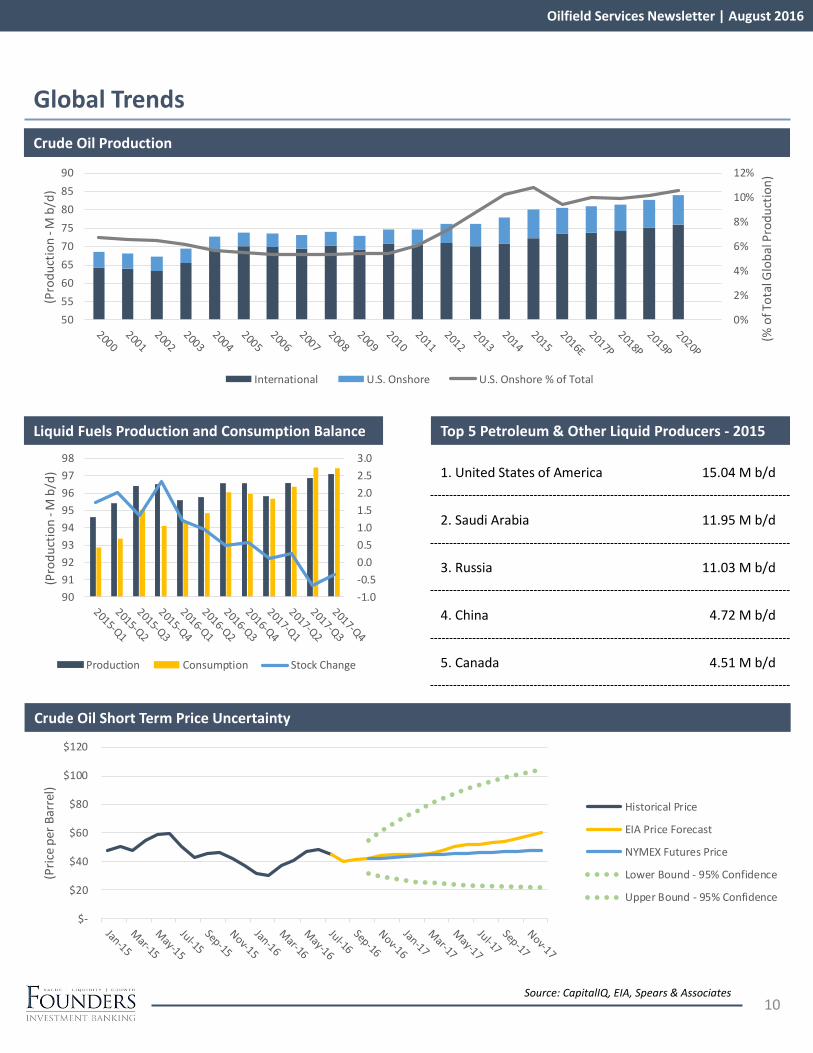

Global Trends

10

Crude Oil Production

Source: CapitalIQ, EIA, Spears & Associates

Crude Oil Short Term Price Uncertainty

Liquid Fuels Production and Consumption Balance Top 5 Petroleum & Other Liquid Producers - 2015

1. United States of America 15.04 M b/d

2. Saudi Arabia 11.95 M b/d

3. Russia 11.03 M b/d

4. China 4.72 M b/d

5. Canada 4.51 M b/d

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

90

91

92

93

94

95

96

97

98

(Pro

du

ctio

n -

M b

/d)

Production Consumption Stock Change

$-

$20

$40

$60

$80

$100

$120

(Pri

ce p

er B

arre

l)

Historical Price

EIA Price Forecast

NYMEX Futures Price

Lower Bound - 95% Confidence

Upper Bound - 95% Confidence

0%

2%

4%

6%

8%

10%

12%

50

55

60

65

70

75

80

85

90

(% o

f To

tal G

lob

al P

rod

uct

ion

)

(Pro

du

ctio

n -

M b

/d)

International U.S. Onshore U.S. Onshore % of Total

Oilfield Services Newsletter | August 2016

Contact

For more information, visit www.foundersib.com, call us at 205.949.2043, or contact the oil and gas team directly by email:

About Founders Investment Banking

11

people make all the difference

meet the founders investment banking TEAM

Founders Investment Banking (Founders) is a merger, acquisition & strategic advisory firm serving middle-market companies.

Founders’ focus is on oil and gas, industrials, software, internet, digital media and healthcare companies located nationwide,

as well as companies based in the Southeast across a variety of industries. Founders’ Skilled professionals, proven expertise

and process-based solutions help companies access growth capital, make acquisitions, and/or prepare for and execute

liquidity events to achieve specific financial goals. In order to provide securities-related services discussed herein, certain

principals of Founders are licensed with M&A Securities Group, Inc. or Founder M&A Advisory, LLC, both members FINRA &

SiPC. Founders M&A Advisory is a wholly owned subsidiary of Founders. M&A Securities Group and Founders are not

affiliated entities. For more information, visit www.foundersib.com.

Duane P. Donner, II, Managing Director [email protected]

John W. Sullivan, Vice [email protected]

Vaughn R. McCrary, [email protected]

Matt Roden, [email protected]

Joe H. Brady, III, [email protected]

John F. Ortstadt, Business [email protected]

Jackson Poe, [email protected]

In order to provide securities-related services discussed herein, certain principals of Founders are licensed with M&A Securities Group, Inc. or Founders M&A Advisory, LLC, both members FINRA & SiPC. M&A Securities Group and Founders are unaffiliated entities. Founders M&A Advisory is a wholly owned subsidiary of Founders.

BIRMINGHAM2204 Lakeshore Drive, Suite 425

Birmingham, AL 35209-8855Phone: 205.949.2043

Fax: 205.871.0010

DALLAS5605 N. MacArthur Blvd, Suite 1000

Irving, TX 75038Phone: 214.295.1055

Fax: 214.295.1047

Related Documents