THE ACCOUNTING PROFESSION at WAR: Contributions during World War II Mark E. Jobe Middle Tennessee State University Dale L. Flesher University of Mississippi

Mark E. Jobe Middle Tennessee State University Dale L. Flesher University of Mississippi.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE ACCOUNTING PROFESSION at WAR: Contributions during

World War II

Mark E. JobeMiddle Tennessee State University

Dale L. FlesherUniversity of Mississippi

Great minds discuss ideas;

average minds discuss events;

small minds discuss people.

Eleanor Roosevelt

In early 1942, military matters were particularly bleak for the Allies.

“On the economic front . . . the Allies were still being worsted.” John D. Millett

Historical Background

“How shall the accounting profession convert to war?” John Carey – AIA Secretary April 13, 1942

◦ Relinquish the younger members to serve in uniform.

◦ Place the more experienced members in war agencies.

◦ “Facilitate production and efficient operation in war industries.”

Introduction

Private First Class Robert Raymond Sterling◦ Army Air Corps◦ Accounting Hall of Fame

Private Robert S. Lipson◦ Combat Engineer ◦ VP TSCPA 1971

Captain Charles Beasley◦ CPA Lybrand, Ross Bros., & Montgomery◦ USMC – Silver Star◦ 1st Battalion, 7th Marines Guadalcanal

Accountants in Uniformed Service

Commander Charles Printz◦U.S. Navy◦ Intelligence Pacific Theater◦ Received WVSCPA 50 year award

Lt. Colonel Howard W. Hinman◦ President OSCPA1938-1939◦ Awarded DSC, Silver Star, Bronze Star

Accountants in Uniformed Service

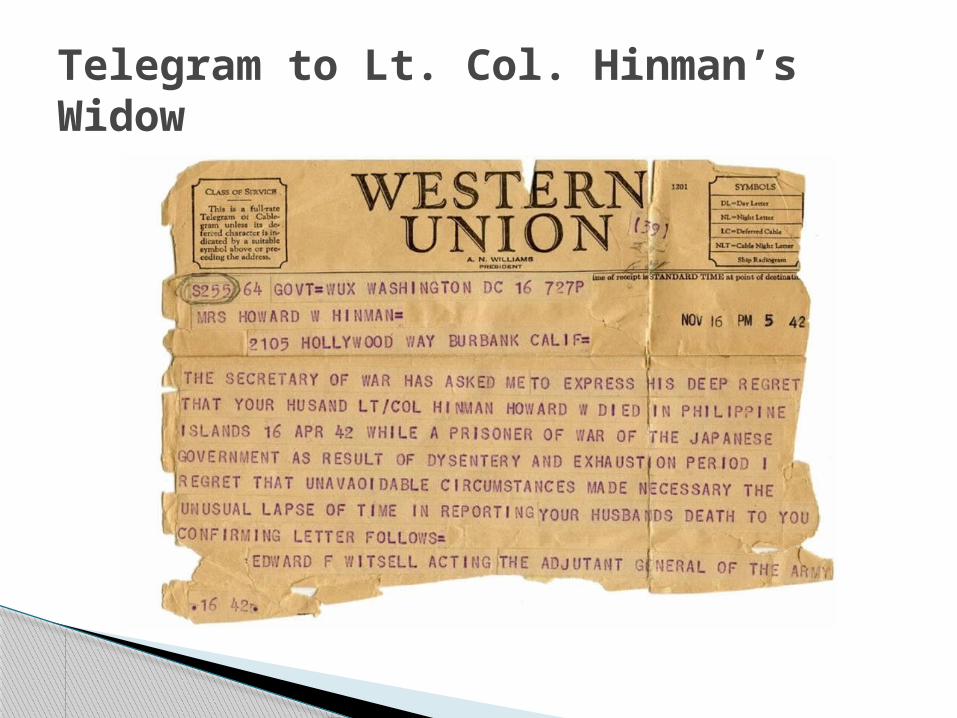

Lieutenant Colonel Howard W. Hinman

Telegram to Lt. Col. Hinman’s Widow

Captain Arthur Greenspan◦B-17 pilot 8th Air Force◦Flew 29 missions ◦Elected TSCPA Chairman of the Board 1986

Accountants in Uniformed Service

Lt. Arthur Greenspan

Office of Production Management

War Production Board

Office of Price Administration

Naval Department

Service in War Agencies

Established by Executive Order of the President - Jan. 7, 1941

Purpose – Coordinate the defense efforts of the nation’s industrial sector, ensure the supply of raw materials, formulate plans . . .

Office of Production Management

C. Oliver Wellington◦ President of the AIA 1940-1941

Maurice E. Peloubet ◦ Vice-President of the AIA 1940-1941

Ernest Seatree◦ The Senior partner of the European firm of Price Waterhouse & Co.

Office of Production Management

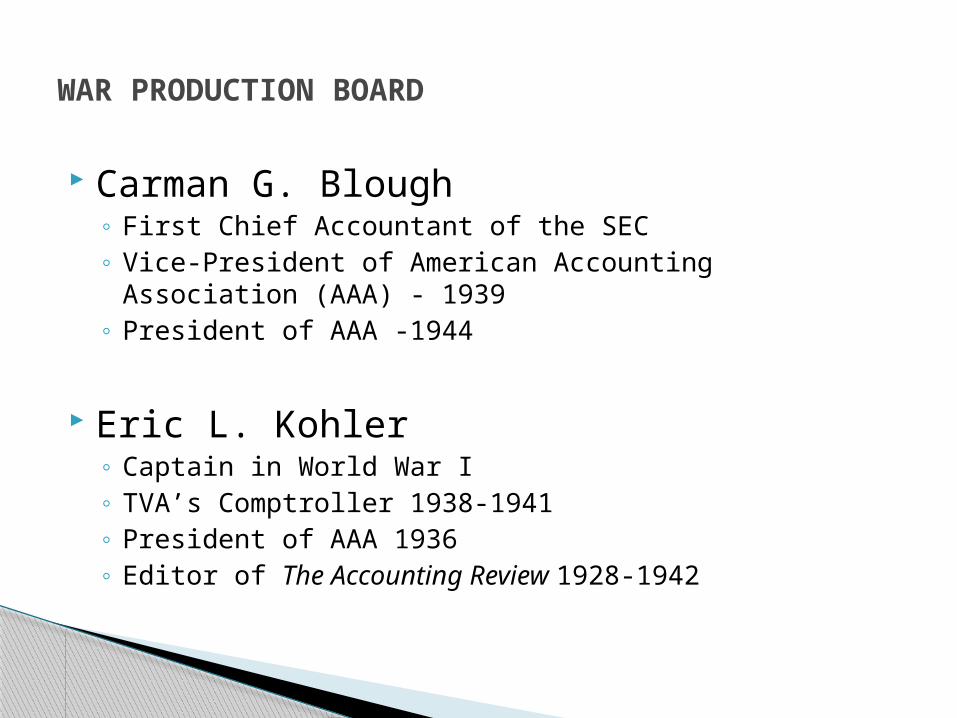

Carman G. Blough◦ First Chief Accountant of the SEC◦ Vice-President of American Accounting Association (AAA)

- 1939◦ President of AAA -1944

Eric L. Kohler◦ Captain in World War I◦ TVA’s Comptroller 1938-1941◦ President of AAA 1936◦ Editor of The Accounting Review 1928-1942

WAR PRODUCTION BOARD

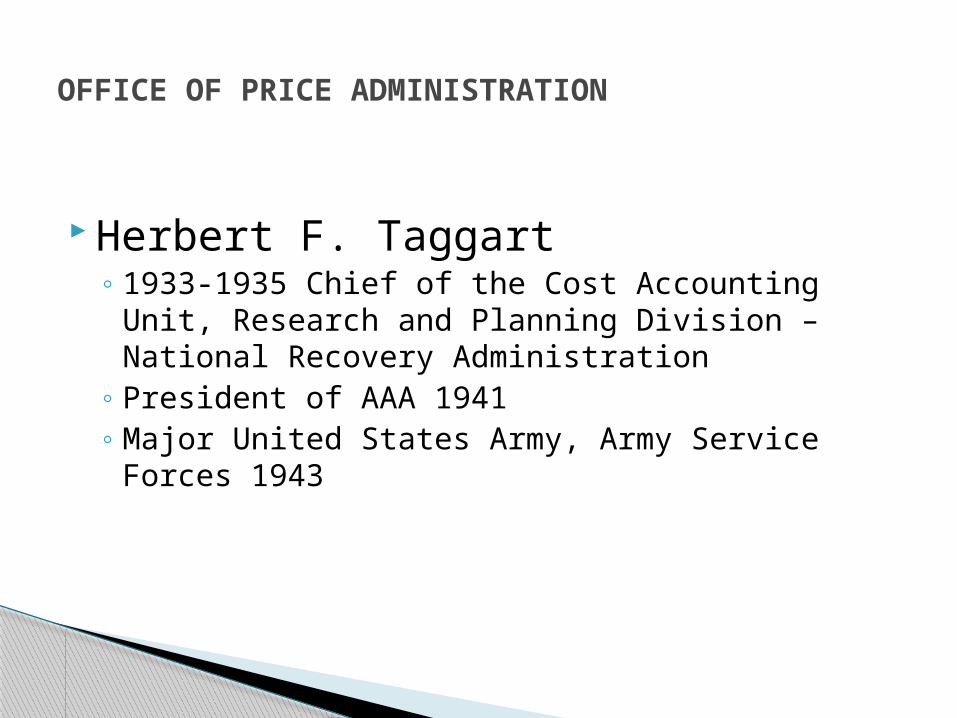

Herbert F. Taggart◦ 1933-1935 Chief of the Cost Accounting Unit,

Research and Planning Division – National Recovery Administration

◦ President of AAA 1941◦ Major United States Army, Army Service Forces

1943

OFFICE OF PRICE ADMINISTRATION

Commander George P. Auld◦ Naval Chief Accounting Officer 1915-1918◦ Accountant General of the Inter-Allied Reparations

Commission 1920-1924◦ Partner at Haskins&Sells1930-41◦ Chief of the Cost and Audit Branch of the Office of

Procurement and Material, Navy Department 1942

Paul Grady◦ Partner Arthur Andersen & Co.◦ Accounting Hall of Fame◦ Partner Price, Waterhouse & Co.

Naval Department

Rear Admiral N. Loyall McLaren◦ President of the AIA 1941◦ Managing Partner of McLaren and Goode◦ President of California Society of CPAs – 1928◦ Vice-president of the AIA 1935,1936

Naval Department

“The war has brought forth many opportunities for general services to business and government in connection with procurement, renegotiation of excess profits, and termination of war contracts. The need for constructive accounting services in the government will not be lessened with the close of the war.”

Paul Grady - April 1945

War Agency Summary

Aviation Industry◦ A critical industry

Magnesium Production◦ A vital war material

Contract Renegotiation◦ A vexing audit process

Service on the Home Front

Lockheed Aircraft Corporation◦ Vega Aircraft Corporation Plant –L.A.◦ This marked the first U.S. effort to mass produce

large aircraft with assembly line production methods.

Problem◦ “It soon became apparent that the proposed

system was not providing information such as the scheduling of material to meet production requirements, the amount on order, when it was promised, usage to date, and spoilage factors.”

AVIATION

Herman E. Ward◦ Manager at Arthur Young & Company (Now E&Y)

◦ Investigated the problem and reported that the machine system was insufficient for the task.

◦ Provided a general description of what was lacking in the current system and suggested the types of records that would be necessary.

◦ Lockheed requested that Arthur Young & Co. design and implement a robust material control system – the job fell to Herman Ward.

AVIATION

Germany produced an estimated 25,000 tons in 1940 while the best America could muster was 6,500 tons that year.

Basic Magnesium Incorporated (BMI).◦ 1.75 miles long and .75 miles wide.◦ Construction alone required 13,000 employees.◦ Largest such magnesium plant in the world.◦ Gave rise to the town of Henderson, Nevada.

MAGNESIUM

Dixon Fagerberg, Jr.◦Arizona CPA◦1938-39 Chair of the ASCPA◦Designed the magnesium process-cost system in a five-week marathon session.

MAGNESIUM

BMI turned out 56,000 tons per year and “supplied one-fourth of the magnesium that was used in the incendiary bombs dropped by the Allies in World War II.”

TIME Feb. 1943: that since 1939, when the annual U.S. production was a paltry 3,350 tons, magnesium production had increased “nearly 100 times.” ◦Basic Magnesium, which utilized an

“electrolytic process” at their “gargantuan plant near Las Vegas.”

MAGNESIUM

April 28, 1942, Congress signed the Sixth Supplemental National Defense Appropriation Act.◦ Controversial Section 403.◦ Applied to approximately 85,000 manufacturers.◦ Required contractors to maintain adequate

records so that excess profits could be determined.

RENEGOTIATION

First, “there was no measure or definition of normal or excessive profits in the War Profits Control Law.” Walter Staub

Second, it was disruptive to operations.

Finally, it created financial uncertainty. “We are in the peculiar position of doing the greatest business in our history and selling our goods without knowing the price we are getting. . . . Any quarterly or six-month financial report of a large corporation engaged in war production is nothing more than a forecast.” -- Irving S. Olds

RENEGOTIATION PROBLEMS

Rear-Admiral N. Loyall McLaren

◦ “if the contractor’s independent accountant is a man of stature and experience . . . it is very helpful,. . . the independent accountants have been most helpful in developing important factors in the case that might otherwise have been overlooked.”

◦ “The best combination is the comptroller or chief accountant, plus the independent auditor if he has the requisite familiarity with the case.”

RENEGOTIATION

“a great deal of importance attaches itself in the minds of the entire . . . Navy Price Adjustment Board as to whether or not the contractor submits audited figures” in preliminary filings.

“the tendency on the part of the members of the board where a war contractor has no auditor is very definitely to look upon the case with a somewhat jaundiced eye.”

War Department Price Adjustment Board recovered $1,866,000,000 in excess profits for the year ended May 1, 1943.

RENEGOTIATION

“Without American production the United Nations (Allies) could never have won the war.”◦Joseph Stalin - Soviet Premier◦Tehran Conference, November 1943

One War Won

Accountants played important roles in strengthening, designing, and implementing the internal controls, processes, and procedures of America’s war-time defense industries.

This aid helped American industry to turn the tide in the armaments race.

Home Front Summary

Questions

Related Documents