Paul K. Wotton, Ph.D. President and Chief Executive Officer March 2011 AMEX: AIS

March2011 ais investorpresentation

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Paul K. Wotton, Ph.D.President and Chief Executive Officer

March 2011

AMEX: AIS

Page 2

2

This presentation may contain forward-looking statements which are made pursuant to the safeharbor provisions of Section 21E of the Securities Exchange Act of 1934 and the Private SecuritiesLitigation Reform Act of 1995. Investors are cautioned that statements which are not strictlyhistorical statements, including, without limitation, statements regarding the plans, objectives andfuture financial performance of Antares Pharma, constitute forward-looking statements which involverisks and uncertainties. The Company’s actual results may differ materially from those anticipated inthese forward-looking statements based upon a number of factors, including anticipated operatinglosses, uncertainties associated with research, development, testing and related regulatoryapprovals, unproven markets, future capital needs and uncertainty of additional financing,competition, uncertainties associated with intellectual property, complex manufacturing, high qualityrequirements, dependence on third-party manufacturers, suppliers and collaborators, lack of salesand marketing experience, loss of key personnel, uncertainties associated with market acceptanceand adequacy of reimbursement, technological change, and government regulation. For a moredetailed description of the risk factors associated with the Company, please refer to the Company’speriodic reports filed with the U.S. Securities and Exchange Commission from time to time, includingits Annual Report on Form 10-K for the year ended December 31, 2009. Undue reliance should notbe placed on any forward-looking statements, which speak only as of the date of this presentation.The Company undertakes no obligation to update any forward-looking information contained in thispresentation.

Safe Harbor Statement

Page 3

3

Investment Highlights

• Leader in fast growing self administered injection technology with one

product marketed (Tjet for Human Growth Hormone)

• Growing revenues from product sales and royalties up 54% over 2009

• Diverse portfolio of marketed and late-stage products

• Anturol for overactive bladder: NDA Filed in 2010 and fully owned

• Proprietary VIBEX MTX in clinical trial, expect rapid path forward with

NDA targeted for 2012

• Broad multi product partnership with Teva

• One of two Libigel Phase 3 efficacy trials completed enrollment

• Decreasing cash burn - More than one year’s cash on hand

Page 4

4

Advanced Product Portfolio based on Strong IP

Self Injector Products ATD Gel Products

Anturol®

Page 5

5

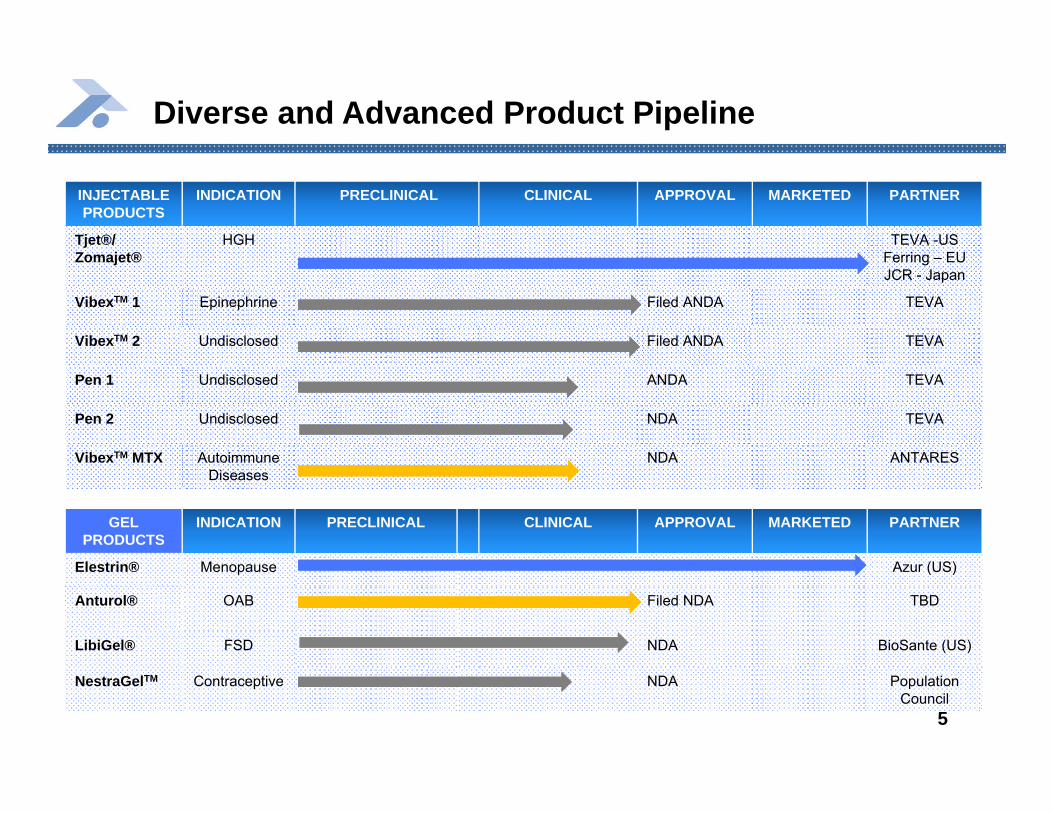

INJECTABLE PRODUCTS

INDICATION PRECLINICAL CLINICAL APPROVAL MARKETED PARTNER

Tjet®/Zomajet®

HGH TEVA -USFerring – EUJCR - Japan

VibexTM 1 Epinephrine Filed ANDA TEVA

VibexTM 2 Undisclosed Filed ANDA TEVA

Pen 1 Undisclosed ANDA TEVA

Pen 2 Undisclosed NDA TEVA

VibexTM MTX AutoimmuneDiseases

NDA ANTARES

GEL PRODUCTS

INDICATION PRECLINICAL CLINICAL APPROVAL MARKETED PARTNER

Elestrin® Menopause Azur (US)

Anturol® OAB Filed NDA TBD

LibiGel® FSD NDA BioSante (US)

NestraGelTM Contraceptive NDA Population Council

wedDiverse and Advanced Product Pipeline

Page 6

6

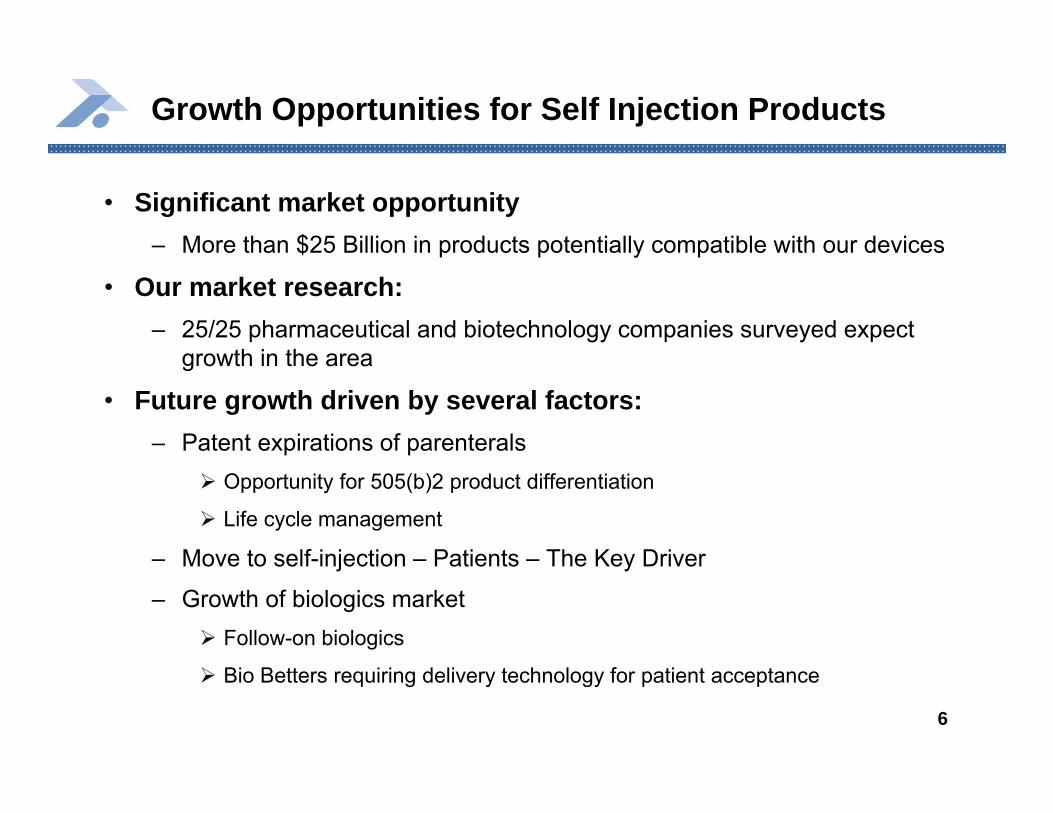

• Significant market opportunity– More than $25 Billion in products potentially compatible with our devices

• Our market research: – 25/25 pharmaceutical and biotechnology companies surveyed expect

growth in the area

• Future growth driven by several factors:– Patent expirations of parenterals

Opportunity for 505(b)2 product differentiation

Life cycle management

– Move to self-injection – Patients – The Key Driver

– Growth of biologics marketFollow-on biologics

Bio Betters requiring delivery technology for patient acceptance

Growth Opportunities for Self Injection Products

Page 7

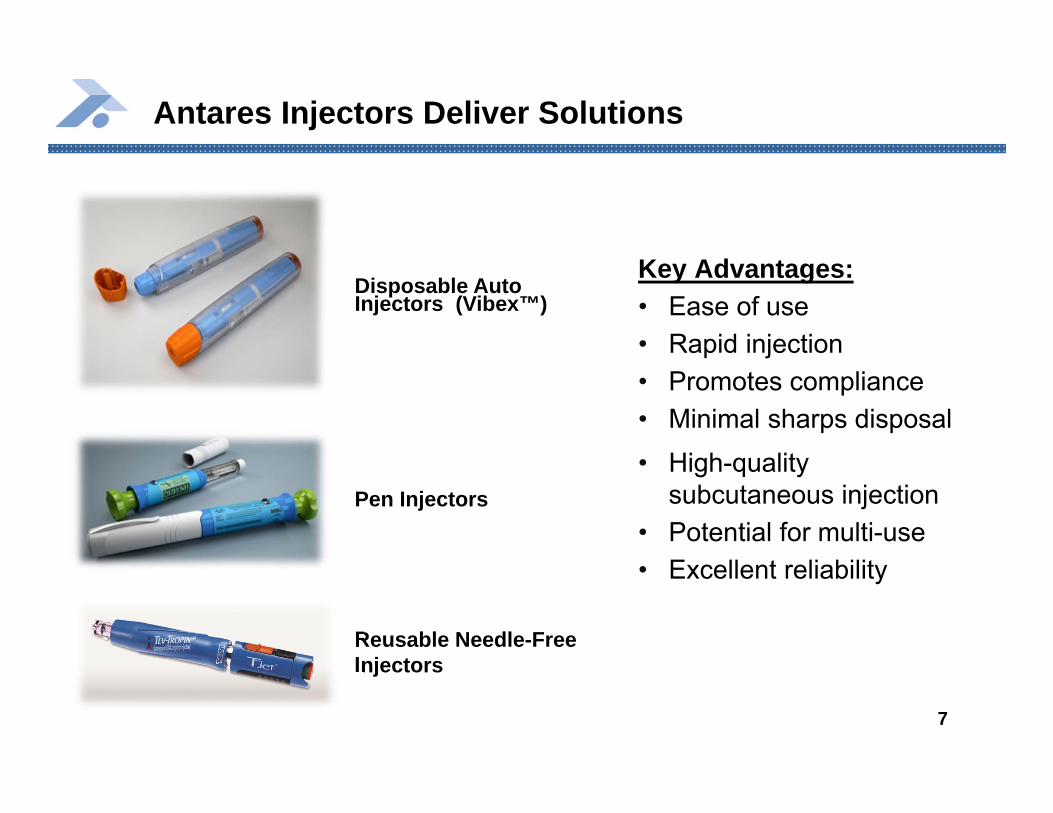

7

Key Advantages:• Ease of use• Rapid injection• Promotes compliance• Minimal sharps disposal• High-quality

subcutaneous injection• Potential for multi-use• Excellent reliability

Antares Injectors Deliver Solutions

Disposable Auto Injectors (Vibex™)

Pen Injectors

Reusable Needle-Free Injectors

Page 8

8

• Strong, international marketing partner– Top-seller of injectables with more than 125 products marketed worldwide

• Tev-Tropin® Tjet® (reusable) hGH– U.S. rights, over $1 billion market, launched August 2009, device sales

with strong margins, royalty on product sales - mid to high single digit %

• Two Vibex™ (auto injector, single shot disposables) products – Epinephrine (N.A. rights) & an undisclosed product (U.S rights)– $250+ million markets– Device sales with strong margins, royalty on product sales – mid-to-high

single digit %

• Two pen injectors (disposables) products– Undisclosed products, NA, EU and Asia rights– $1.6 billion market for both products– Transfer price plus margin on device sales, royalty on product sales - high

single digit-to-mid teens percentage

Teva and Antares: Our Broad Collaboration

Multiple agreements for diverse products with nearly $3 billion in U.S. sales

Page 9

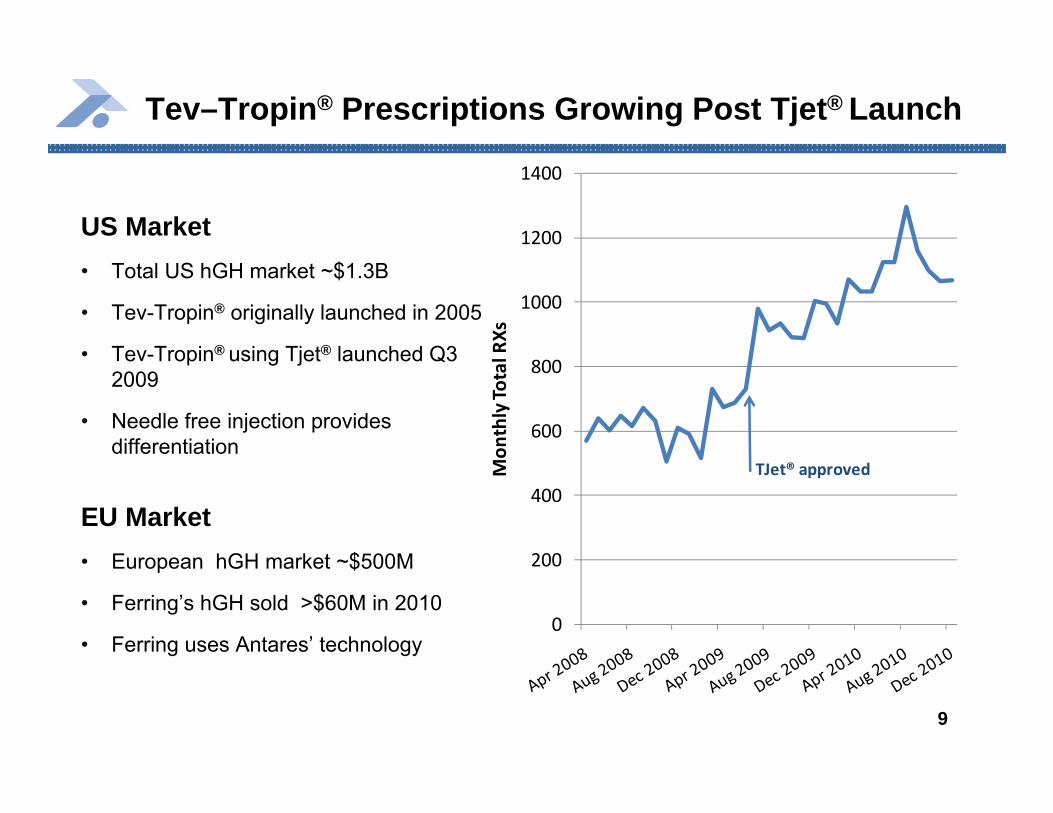

9

US Market• Total US hGH market ~$1.3B

• Tev-Tropin® originally launched in 2005

• Tev-Tropin® using Tjet® launched Q3 2009

• Needle free injection provides differentiation

EU Market• European hGH market ~$500M

• Ferring’s hGH sold >$60M in 2010

• Ferring uses Antares’ technology

Tev–Tropin® Prescriptions Growing Post Tjet® Launch

0

200

400

600

800

1000

1200

1400

Mon

thly To

tal R

XsTJet® approved

Page 10

10

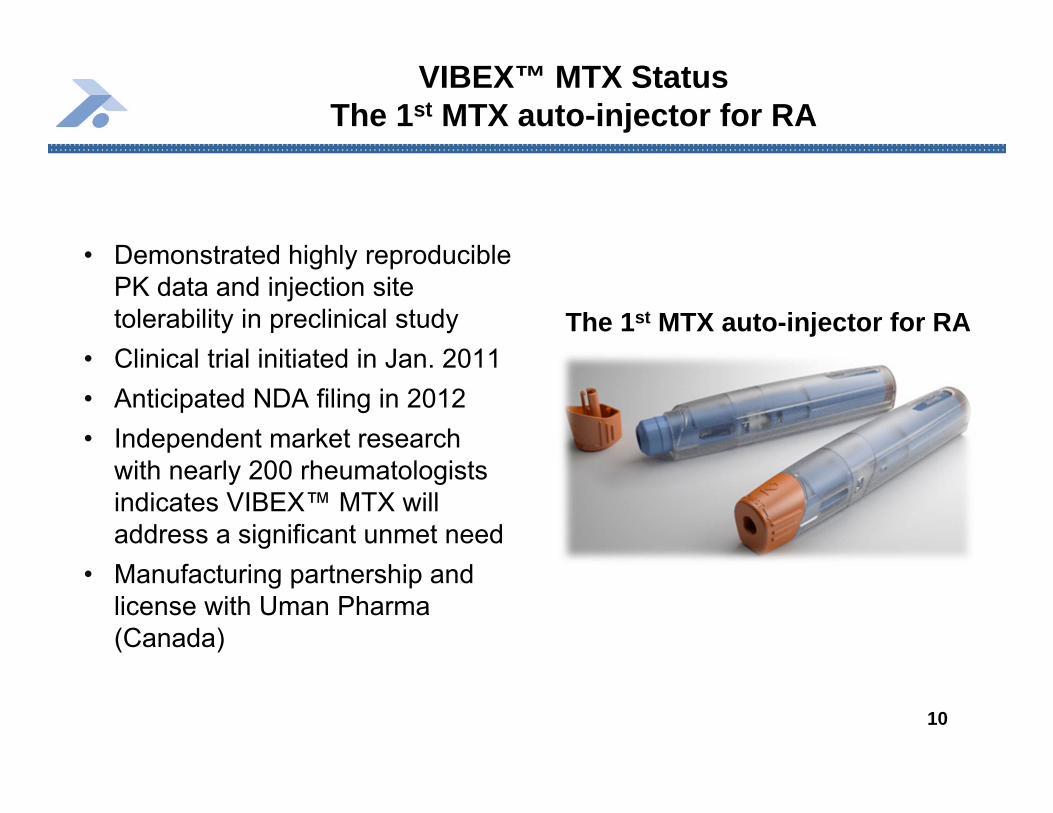

VIBEX™ MTX StatusThe 1st MTX auto-injector for RA

The 1st MTX auto-injector for RA

• Demonstrated highly reproducible PK data and injection site tolerability in preclinical study

• Clinical trial initiated in Jan. 2011• Anticipated NDA filing in 2012• Independent market research

with nearly 200 rheumatologists indicates VIBEX™ MTX will address a significant unmet need

• Manufacturing partnership and license with Uman Pharma(Canada)

Page 11

11

VIBEX™ MTX: Rheumatoid Arthritis (RA) Market Overview

• 2.1 million RA patients in the U.S.

• Methotrexate (MTX) is standard of care, used in majority of RA patients

• 5.3 million RX for MTX in 2010, and growing

– 70% of RX are for RA

• 30% to 60% of patients don’t tolerate oral MTX & can do better on injection

• Concentrated prescriber base: 3000 Rheumatologists

70%

9%

20%

Arthritis

Psoriasis

Other Conditions

US Methotrexate Prescription Breakdown

Page 12

12

The VIBEX™ MTX Advantage

• Clinical benefits– Removes variable absorption of oral MTX – Enables higher dose titration– Better efficacy vs. oral MTX– Better tolerability vs. oral MTX

• Convenience– 3-easy steps—easy to teach patients – Hidden needle reduces patient apprehension, supports compliance– Fast, complete and comfortable

• Safety– Avoids dosing errors and inadvertent exposure to cytotoxic agent– Locking needle shield reduces risk of accidental needle sticks

Page 13

13

Commercial/Advanced Transdermal Gel Portfolio

Anturol®

FDA Approved Delivery Technology

Page 14

1414

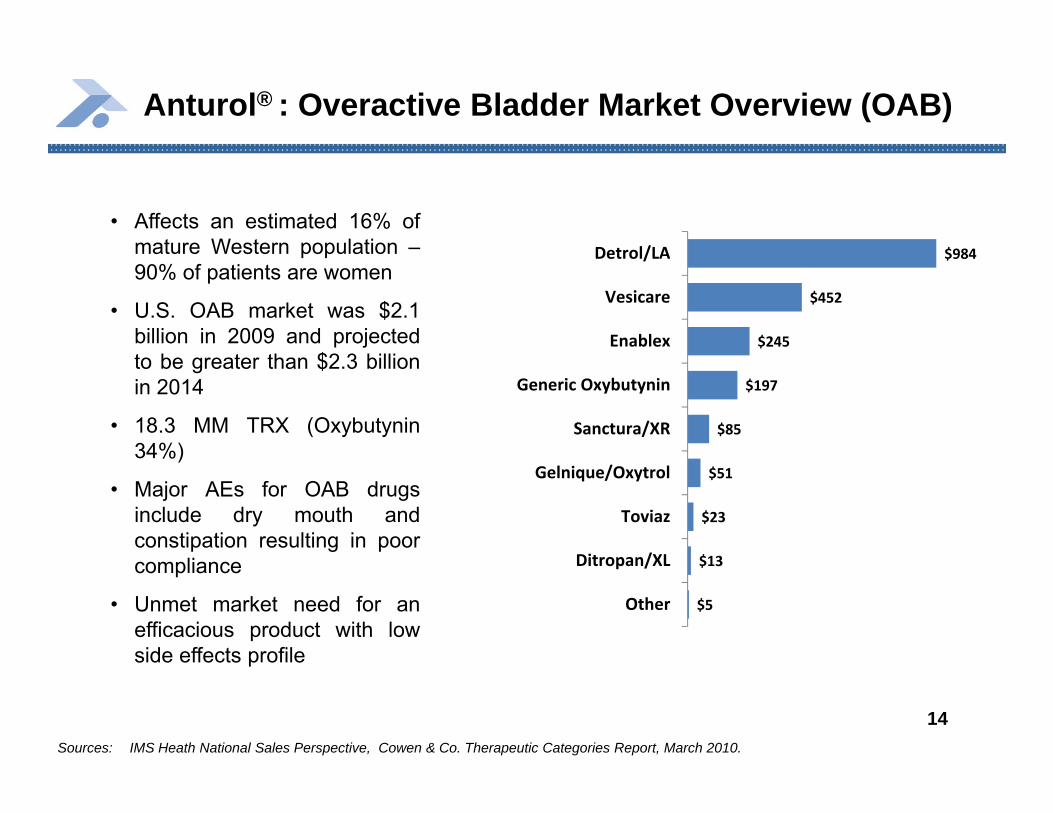

Anturol® : Overactive Bladder Market Overview (OAB)

• Affects an estimated 16% ofmature Western population –90% of patients are women

• U.S. OAB market was $2.1billion in 2009 and projectedto be greater than $2.3 billionin 2014

• 18.3 MM TRX (Oxybutynin34%)

• Major AEs for OAB drugsinclude dry mouth andconstipation resulting in poorcompliance

• Unmet market need for anefficacious product with lowside effects profile

Sources: IMS Heath National Sales Perspective, Cowen & Co. Therapeutic Categories Report, March 2010.

$984

$452

$245

$197

$85

$51

$23

$13

$5

Detrol/LA

Vesicare

Enablex

Generic Oxybutynin

Sanctura/XR

Gelnique/Oxytrol

Toviaz

Ditropan/XL

Other

Page 15

15

• First & Only Titratable Once-Daily Transdermal Treatment for OAB• 2 pumps for 56mg dose or 3 pumps for 84mg dose

• Gel Dries Quickly and Clearly in less than 2 minutes, leaving no odor or residue feel

• Urge Incontinence Reduced by first week and sustained throughout 12-week study for both dosage strengths - 56 mg (p<0.028) and 84mg (p<0.033) vs placebo

• Efficacy comparable to market leader & newer oral OAB drugs

• Good compliance• 2.9% of patients on Anturol Gel discontinued due dermal side effects which were

mild and transient

• Well-Tolerated by most patients • Dry mouth in 11.5% of patients , less than 1% of patients on Anturol Gel

discontinued due to dry mouth• Constipation in 2.6% of patients vs. 1.5% with placebo• Low incidence of dizziness and fatigue comparable to placebo (<2%)

Anturol - Strong Product Profile

Page 16

16

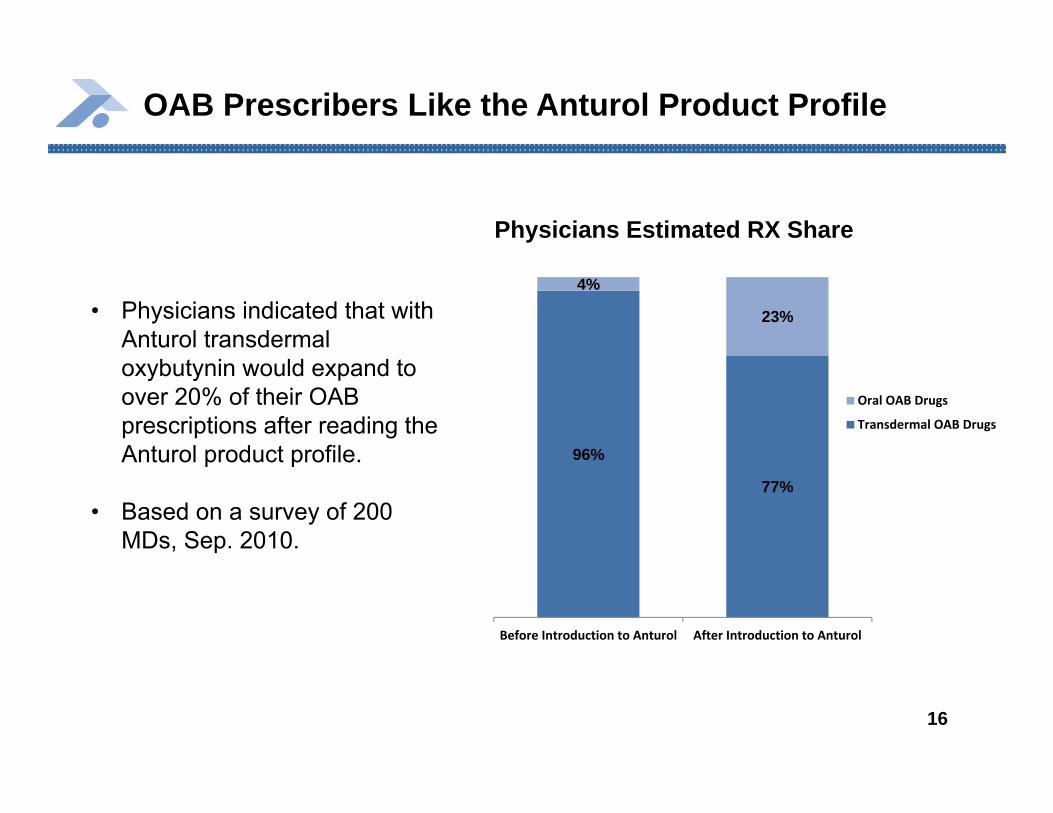

• Physicians indicated that with Anturol transdermal oxybutynin would expand to over 20% of their OAB prescriptions after reading the Anturol product profile.

• Based on a survey of 200 MDs, Sep. 2010.

OAB Prescribers Like the Anturol Product Profile

96%

77%

4%

23%

Before Introduction to Anturol After Introduction to Anturol

Oral OAB Drugs

Transdermal OAB Drugs

Physicians Estimated RX Share

Page 17

17

17

• Phase 3 trial successfully met primary end point in July 2010

• NDA Filed December 2010

• Open Label extension safety trial completed successfully

• Awaiting FDA acceptance of application following NDA user

fee waiver receipt February 8, 2011

• Currently in talks with several potential partners

Anturol Update

Page 18

18

• Indication: hypoactive sexual desire disorder (HSDD)in menopausal women

• Currently in Phase 3 testing

• Enrollment completed in one of two efficacy studies

• Physician survey shows significant unmet medical need and market opportunity already exists

• BioSante reported favorable unblinded safety data on use of testosterone in women for FSD

• Antares owns international licensing rights in significant territories (e.g. EU) and all manufacturing

• NDA filing planned for 2011

• BioSante guidance: $2B addressable market

LibiGel® Phase 3 Program Partnered with BioSante

Page 19

19

Elestrin® : Convenient, Flexible Dosing, Effective

Page 20

20

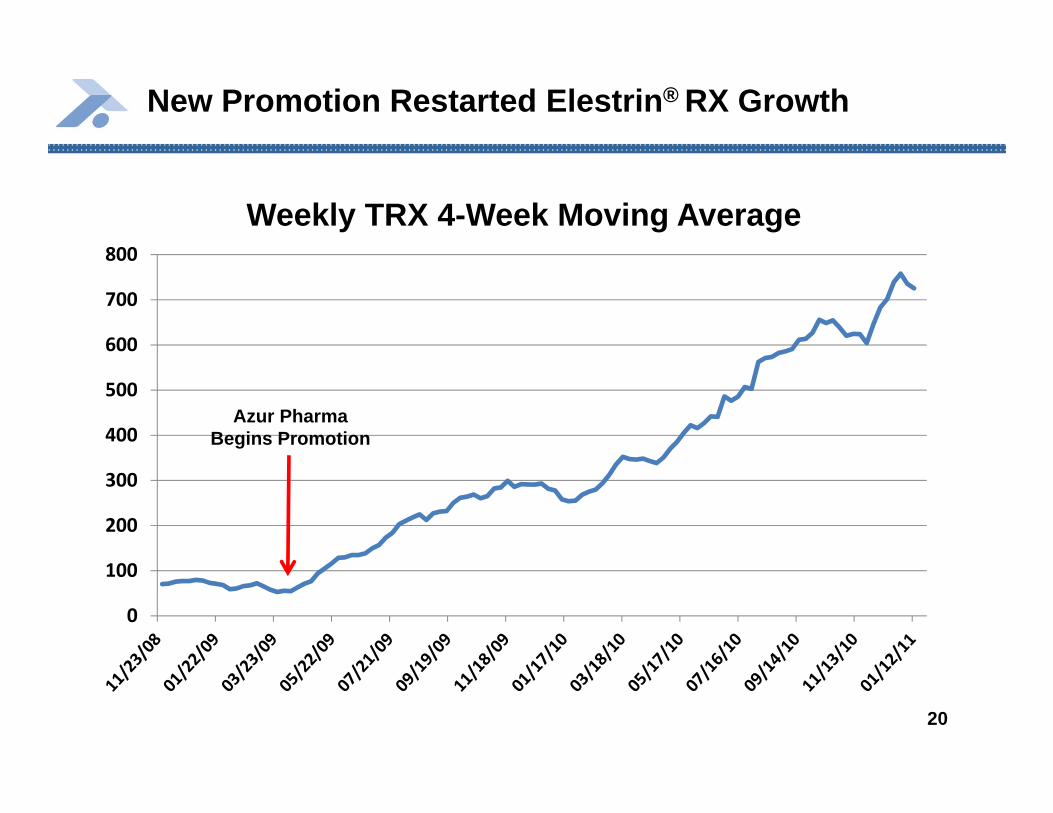

New Promotion Restarted Elestrin® RX Growth

0

100

200

300

400

500

600

700

800

Weekly TRX 4-Week Moving Average

Azur PharmaBegins Promotion

Page 21

21

• Indication: contraception• Featured Extensively in Media

- October 2010• Successfully completed Phase 2

Trial (three separate doses givenfor 21 days) induced ovulation suppression

• Product well tolerated with no serious adverse events reported and no instances of skin irritation

• Nestorone® has no androgenic effects but is not orally active –ideally suited to gel administration

• Potentially attractive contraceptive option as both the formulation and active drugs are designed to reduce adverse events which can lead to discontinuation with other forms of reversible contraceptive products − 31% of women discontinue oral contraceptives use after 6

months, and 44% within 12 months*

NestraGel™: Partnered with the Population Council

**National Survey of Family Growth, CDC

Page 22

22

Financial Overview

• Strong cash positionAs of December 31st 2010, cash /cash equivalents of $9.8 million

$1.50 Warrants/Options exercised - $5 Million in Q1 2011

• Growing revenue base2008 total revenues were $4.6 Million

2009 total revenues of $8.3M (47% over 2008)

2010 Revenues $12.8 Million (54% over 2009)

• Reducing burn rateCash burn in 2010 was approximately $3.7 million

Paul K. Wotton, Ph.D.President and Chief Executive Officer

March 2011

AMEX: AIS

Related Documents