March 2015

March 2015. 2 BUSINESS COMPOSITION Rm turnover 2014 % Animal Feed1 24134,8 Layers1 08730,5 Broilers1 08130,4 Africa1524,3 Quantum Foods3 561100.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

March 2015

2BUSINESS COMPOSITION

Rm turnover 2014

%

Animal Feed 1 241 34,8

Layers 1 087 30,5

Broilers 1 081 30,4

Africa 152 4,3

Quantum Foods 3 561 100

3NOVA FEEDS

Malmesbury

52%

George

14%

Pretoria

34%

42% sales to external market

CAGR for external sales volumes for period 2010-2014 is 6.7%

Leading supplier of diary feed in Western Cape

Ability to “pass though” raw material price changes

Superior technical input with custom mixes are key success factors

4NULAID EGGS

GP

Parents

Hatchery

BREEDING COMMERCIAL

Rearing

Laying

SALES

Pack Station

Ungraded

Liquid Egg

Integrated business from grand parent level to pack stations

Quantum Foods sell the equivalent of over 1 billion eggs per annum

90% of eggs sold are produced by own farms

One of only three suppliers of pullets

Geographical spread of farms

Nulaid brand commands a premium

Day old pullet sales

Point of lay sales

Transfer Transfer

5BROILER BUSINESS

GP

Parents

Hatchery

BREEDING COMMERCIAL

Rearing

Sales to

Others

Own

Abattoir

Significant re-engineering to stop losses

• Exit Eastern Cape market

• Closure of two abattoirs

• Live bird supply agreement in Western Cape

Western Cape business essentially a livestock farming business

Gauteng business remain fully integrated

560 000 broilers per week Western Cape

250 000 broilers per week Gauteng

Retail

&

WholesaleTransfer

6AFRICA OUTSIDE SOUTH AFRICA

Significant contributor to profits during 2013 and 2014

ZAMBIA

• Broiler and layer breeding• Commercial egg farm in

Copperbelt• Feed mixing plant

UGANDA

• Broiler and layer breeding• Feed mixing plant

7SUCCESS FACTORS

Commodity prices

• Maize (refer to slide 11)

• Soybean meal

ZAR/US$

• Exchange rate (refer to slide 12)

Egg prices

• Egg cycle of supply and demand (refer to slide 13)

• Feed prices

Broiler meat prices

• Trade regime

• Domestic supply and demand

• Feed prices

1

2

3

4

Economic factors

8OPERATIONAL FACTORS

Feed Conversion Ratio ( FCR ) both layers and broilers

Eggs per hen housed

Lowest cost of production throughout value chains

Disease status of national flocks

1

2

3

4

9

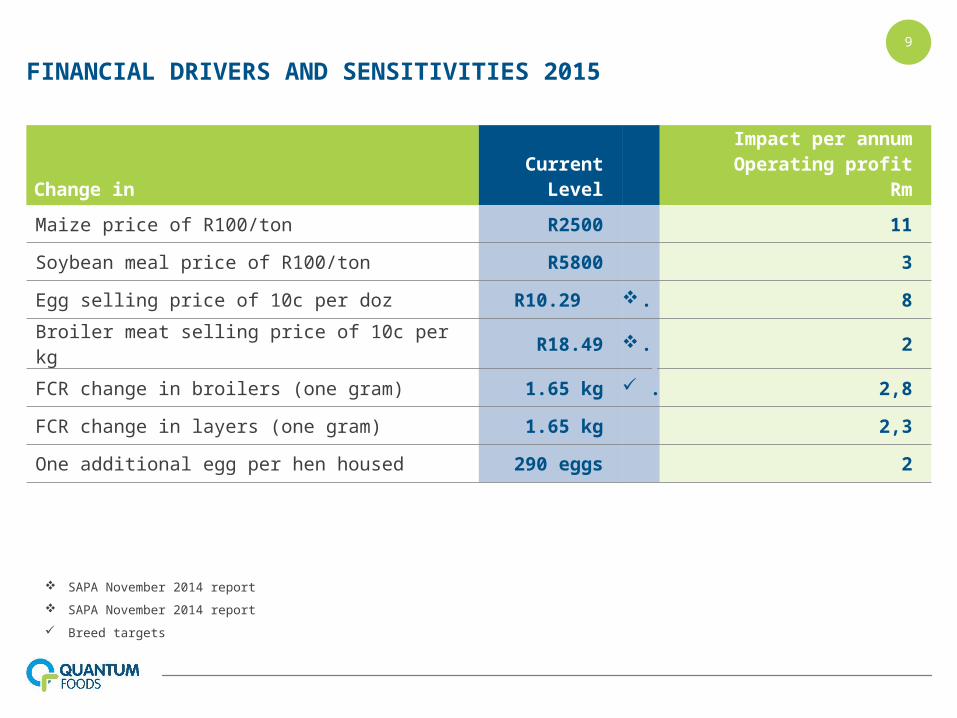

FINANCIAL DRIVERS AND SENSITIVITIES 2015

Change inCurrent

Level

Impact per annumOperating profit

Rm

Maize price of R100/ton R2500 11

Soybean meal price of R100/ton R5800 3

Egg selling price of 10c per doz R10.29 . 8

Broiler meat selling price of 10c per kg R18.49 . 2

FCR change in broilers (one gram) 1.65 kg . 2,8

FCR change in layers (one gram) 1.65 kg 2,3

One additional egg per hen housed 290 eggs 2

SAPA November 2014 report

SAPA November 2014 report

Breed targets

10STRATEGY

1. Western Cape de-risking of boiler business

2. Review Hartebees abattoir

3. Improve Customer and Product mix in Egg business

4. Increase Africa geographic footprint

Reducing cyclicality

1

1. Improvement of farm operations• Broiler FCR close to optimum• Layer FCR and eggs per hen

housed can improve by at least 2.5%

2. Cost efficiency in pack stations

3. Consolidated supply chain efforts

4. Utilize import opportunities for maize

5. Pack station project KZN

1. Organic growth in feed business

2. Acquisitive growth in feed business

3. “Off balance sheet” growth in egg business

4. Growth in current Africa operations

5. Grow the layer livestock business

Improve margins Grow selected markets

2 3

11ECONOMIC FACTORS: MAIZE

0

500

1000

1500

2000

2500

3000

3500

Yellow Maize (Safex)

R/t

on

2010 2011 2012 2013

R1,278

R1,672

R2,380

R2,264

2010 - 2014 Reporting period: Oct - Sep2015 Reporting period: Oct - Febr

R2,377

2014 2015

R2,069

-15.70%

+30.80%

+42.34

-4.87%

+5.03%

-12.98%

12ECONOMIC FACTORS: EXCHANGE RATE

5.5

6

6.5

7

7.5

8

8.5

9

9.5

10

10.5

11

11.5

12

ZAR vs US$

Rand

2010 2011 2012 2013

R7.4865

R6.9697

R8.0729

R9.2888

2014

R10.6037

R11.3085

-17.39%

-6.90%

+15.83%

+15.06%

+14.16%

+6.65%

2015

13

Source: SAPA

Thank you

Related Documents

![Accelerometer: Understanding Acceleration Opportunities ......tractors and learned models [26, 51, 101, 132]. The feature vectors are sent to Feed1, which calculates and returns a](https://static.cupdf.com/doc/110x72/5f46f6dffef9262e03429cd9/accelerometer-understanding-acceleration-opportunities-tractors-and-learned.jpg)