2009 Annual Results Presentation 25 th March 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2009 Annual Results Presentation 25th March 2010

25th March 2010 | Page 1

Forward looking statements

This presentation may contain forward-looking statements and information that both represents management's current expectations or beliefs concerning future events and are subject to known and unknown risks and uncertainties.

A number of factors could cause actual results, performance or events to differ materially from those expressed or implied by

these forward-looking statements.

25th March 2010 | Page 2

Agenda

Progress against strategy Simon Lockett

2009 financial results Tony Durrant

Operations update Neil Hawkings

Exploration update Andrew Lodge

Summary Simon Lockett

25th March 2010 | Page 3

2009 highlights

• 21% increase in production and 23% increase in reserves and resources

• Continuing good progress on development projects

– Chim Sao, Gajah Baru on track for 2011

• Acquisitions in UK and Vietnam successfully integrated

• Five successes out of nine exploration and appraisal wells

• Strong cash flow, despite lower average commodity prices

• Record profits after tax of US$113 million

25th March 2010 | Page 4

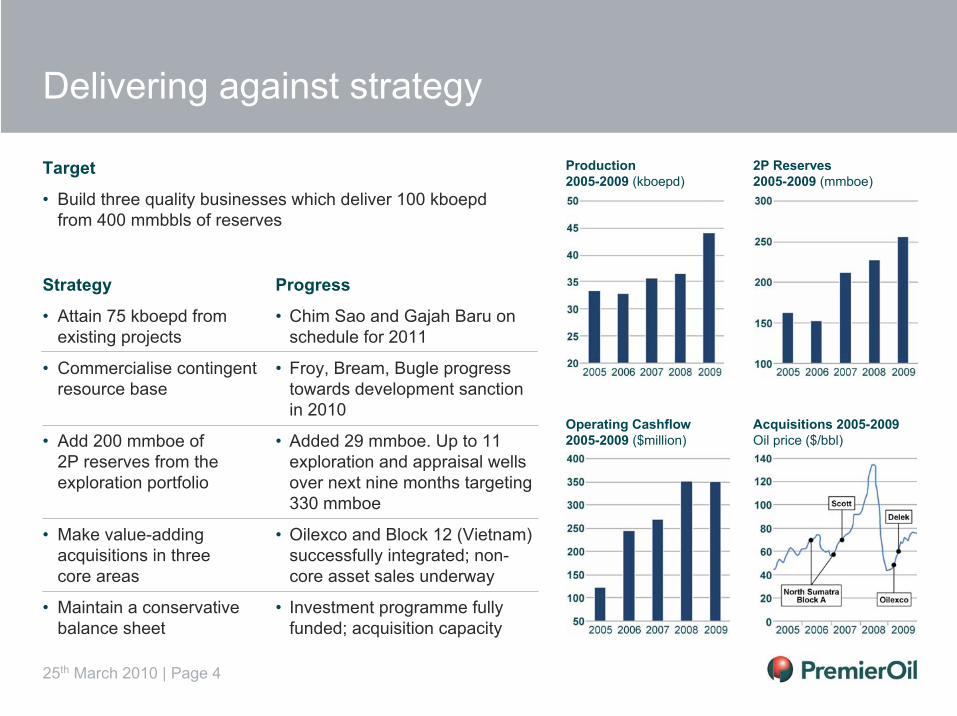

Delivering against strategy

Progress

• Chim Sao and Gajah Baru on schedule for 2011

• Froy, Bream, Bugle progress towards development sanction in 2010

• Added 29 mmboe. Up to 11 exploration and appraisal wells over next nine months targeting 330 mmboe

• Oilexco and Block 12 (Vietnam) successfully integrated; non-core asset sales underway

• Investment programme fully funded; acquisition capacity

Strategy

• Attain 75 kboepd from existing projects

• Commercialise contingent resource base

• Add 200 mmboe of2P reserves from the exploration portfolio

• Make value-adding acquisitions in threecore areas

• Maintain a conservative balance sheet

Production2005-2009 (kboepd)

Target

• Build three quality businesses which deliver 100 kboepdfrom 400 mmbbls of reserves

Operating Cashflow2005-2009 ($million)

2P Reserves2005-2009 (mmboe)

Acquisitions 2005-2009Oil price ($/bbl)

25th March 2010 | Page 5

2009 financial results

25th March 2010 | Page 6

Production and income statement

Working Interest Production (kboepd)Entitlement Interest Production (kboepd)Realised oil price ($/bbl)Realised gas price ($/mcf)

Sales and other operating revenuesCost of salesGross profitExcess of fair value over purchase considerationExploration/New BusinessGeneral and administration costsOperating profit Financial ItemsProfit before taxationTaxationProfit after tax

12 months to31 Dec 2008

12 months to31 Dec 2009

36.531.894.5

6.6

$m655

(318)337

-(59)(17)262

16278

(179)98

44.240.266.3

5.2

$m621

(361)260

6(77)(18)170(90)

8033

113

Average gas pricing ($/mcf)2009 2008

Singapore $11.0 $15.2Pakistan $3.2 $3.5

Average Brent oil price was $61.7/bbl(2008: $97.3/bbl)

Operating costs per barrel ($/bbl)2009 2008

UK $23.2 $20.6Indonesia $10.0 $8.6Pakistan $1.9 $1.5Group $12.2 $9.5

Includes non-cash mark to market adjustment on hedging of $61.1 million (pre-tax)

Tax credit arises due to UK tax allowances acquired with Oilexco

Highlights

25th March 2010 | Page 7

Hedging

• Policy unchanged: secure cashflows via floors or forwards to fund investment programme even at low oil prices

• 2009 ImpactNo cash payments under collars

$Cash premia paid (Oilexco-related) 12.5Mark-to-market movement 48.6Charge to income statement 61.1

Outlook

• 41% liquids 2010 - 2012 has collar of $49 - $84/bbl

• 22% Indonesian gas 2010 - 1H 2013 has collarof $47 - $94/bbl

• 1.3 mmbbls 2010 production sold forward at average $76/bbl

25th March 2010 | Page 8

Overseas

UK

PRT

CT

Prior period revisions

Current charge

Deferred tax credits

Tax charge for the year

12 months to31 Dec 2008

$m

12 months to31 Dec 2009

$m

111.6

34.0

47.5

(0.2)

192.9

(13.6)

179.3

Group taxation position

73.0

23.2

(23.4)

(24.6)

48.2

(81.3)

(33.1)

Allowances acquired

Carried back to 2008

Utilised in 2009

Premier allowances brought forward

Recognised as deferred tax asset

Currently unrecognised

Tax allowances carried forward

UK Tax Allowance Position at 31 Dec 2009

$m

1199

(47)

(59)

37

1130

875

275

1130

Outlook• Significant UK carry forward of allowances• UK cash taxes not anticipated until at least 2014

25th March 2010 | Page 9

Cash flow

Cash flow from operations

Taxation

Operating cash flow

Capital expenditure

(Acquisitions)/disposals

Finance charges, net

Pre-licence expenditure

Net cash flow

12 months to31 Dec 2009

$m2009 2008

Development

Exploration

Estimated Capex split ($m)12 months to31 Dec 2008

$m127

90

217

195

108

303

Operating cashflow Capex

Asia

MEP

Estimated 2009 Regional Capex split ($m)

143

26

134

47

97

204North Sea

303348

555

(203)

352

(217)

3

-

(16)

122

419

(71)

348

(303)

(643)

(55)

(20)

(673)

Outlook• Forecast full-year 2010 spend of $400m (development) and $150m (exploration)

25th March 2010 | Page 10

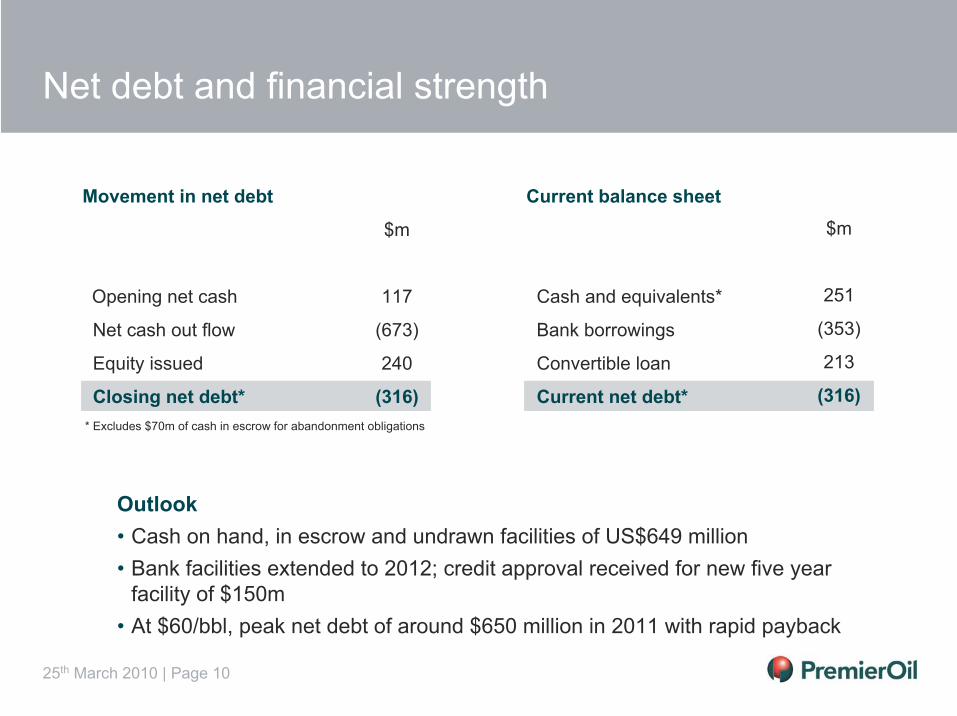

Net debt and financial strength

$m

117

(673)

240

(316)

Movement in net debt

Opening net cash

Net cash out flow

Equity issued

Closing net debt*

Outlook• Cash on hand, in escrow and undrawn facilities of US$649 million• Bank facilities extended to 2012; credit approval received for new five year

facility of $150m• At $60/bbl, peak net debt of around $650 million in 2011 with rapid payback

* Excludes $70m of cash in escrow for abandonment obligations

$m

251

(353)

213

(316)

Current balance sheet

Cash and equivalents*

Bank borrowings

Convertible loan

Current net debt*

25th March 2010 | Page 11

Operations update

25th March 2010 | Page 12

Operations highlights

• Oilexco integration complete

• GSA2 project sanction

• Chim Sáo acquisition

• Chim Sáo project sanction

25th March 2010 | Page 13

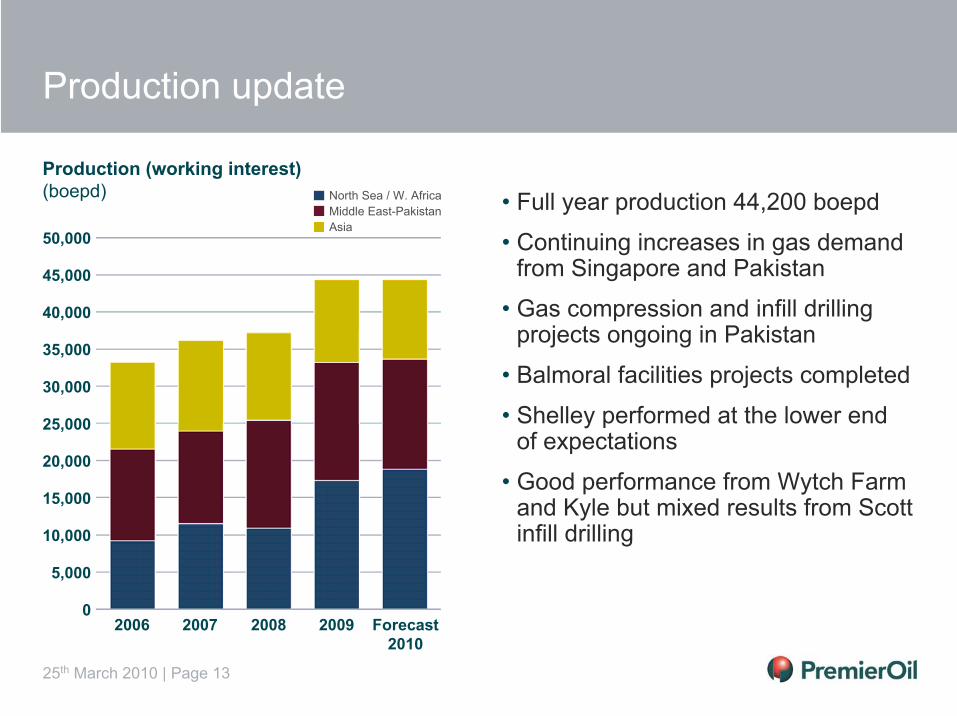

Production update

50,000

Production (working interest)(boepd)

30,000

25,000

10,000

5,000

02006 2007 2008

15,000

20,000

35,000

North Sea / W. AfricaMiddle East-PakistanAsia

2009

40,000

45,000

Forecast2010

• Full year production 44,200 boepd

• Continuing increases in gas demand from Singapore and Pakistan

• Gas compression and infill drilling projects ongoing in Pakistan

• Balmoral facilities projects completed

• Shelley performed at the lower endof expectations

• Good performance from Wytch Farm and Kyle but mixed results from Scott infill drilling

25th March 2010 | Page 14

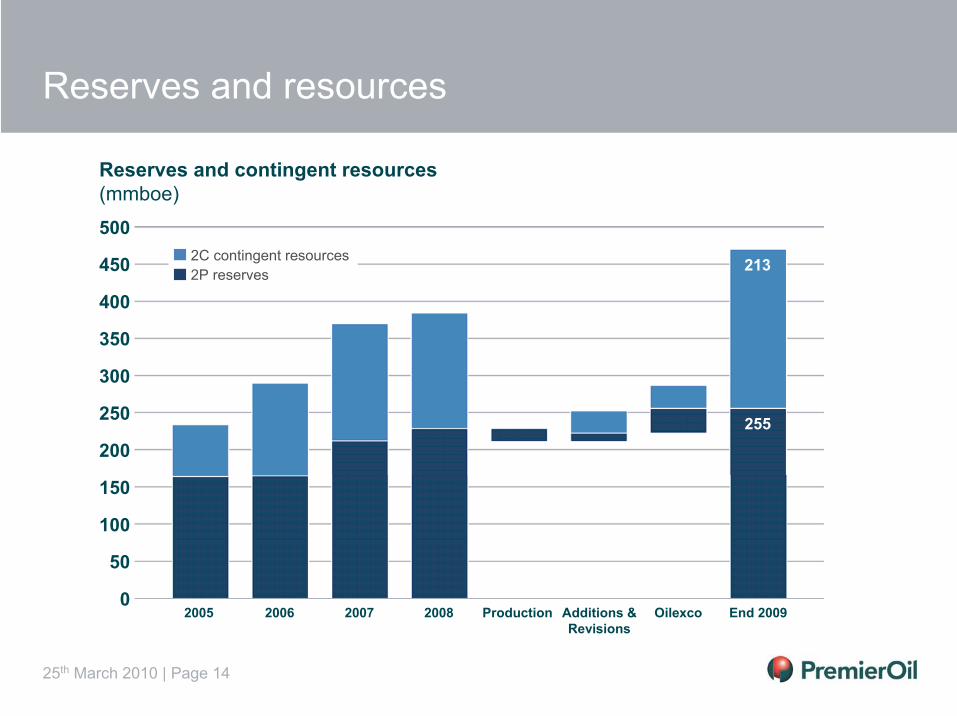

Reserves and resources

500

2005

450

400

350

0

150

200

250

300

2006 2007

100

50

Reserves and contingent resources (mmboe)

Production Additions &Revisions

Oilexco End 20092008

2C contingent resources2P reserves 213

255

25th March 2010 | Page 1525th March 2010 |

• WHP jacket being installed in April

• ENSCO 107 drilling rig contracted and mobilising in June

• Platform topsides to be installed in July

• FPSO conversion underway – vessel in Keppel shipyard

• Project overall 65.8% complete at end March

• Premier equity 53.125%

Chim Sáo – on schedule for first oil in July 2011

25th March 2010 | Page 16

• Wellhead platform jacket progressing well

• Rig tender complete and drilling starts in September

• Wellhead platform to be installed in September

• Central Processing Platform construction underway

• Overall project 43% complete

• Premier equity 28.67%

Gajah Baru – on schedule for October 2011

25th March 2010 | Page 17

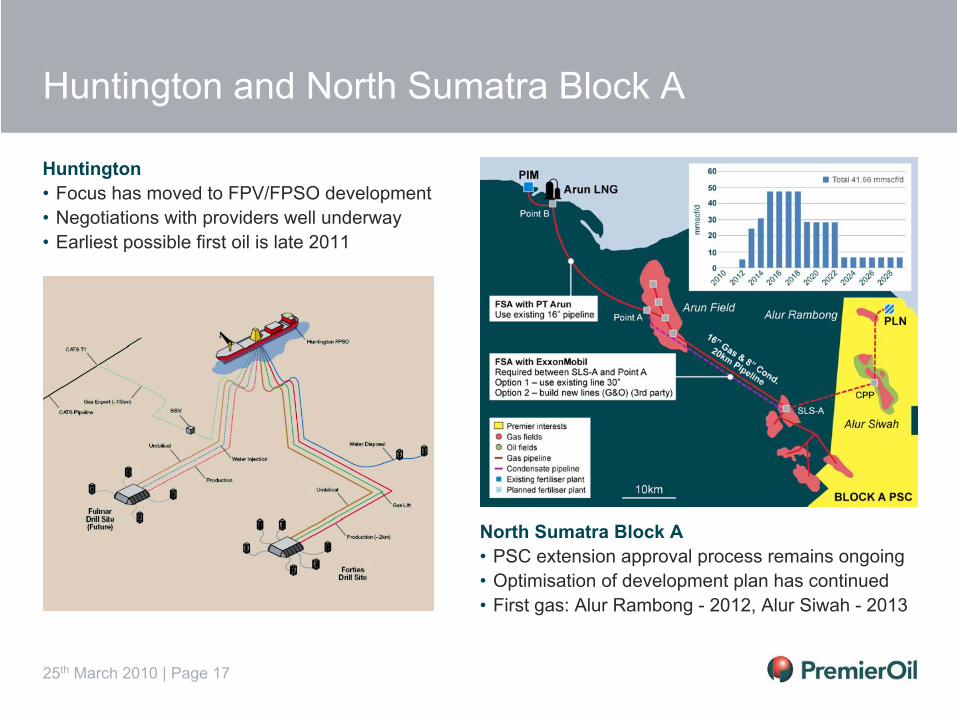

North Sumatra Block A• PSC extension approval process remains ongoing• Optimisation of development plan has continued• First gas: Alur Rambong - 2012, Alur Siwah - 2013

Huntington and North Sumatra Block A

Huntington• Focus has moved to FPV/FPSO development• Negotiations with providers well underway• Earliest possible first oil is late 2011

25th March 2010 | Page 18

Appraised development portfolio targeting 2013

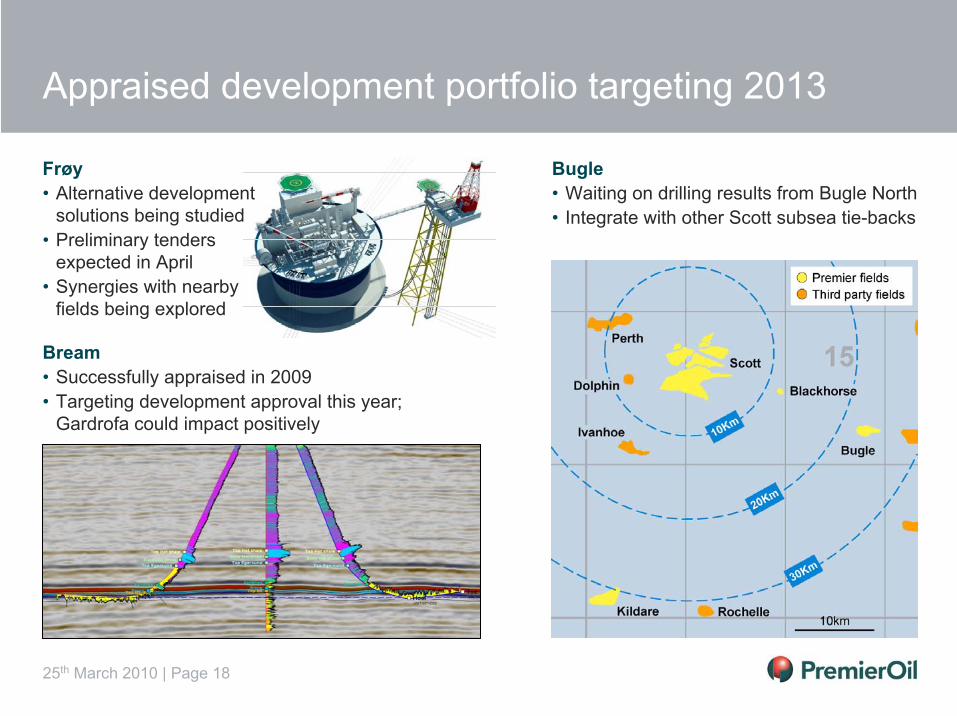

Frøy• Alternative development

solutions being studied• Preliminary tenders

expected in April• Synergies with nearby

fields being explored

Bugle• Waiting on drilling results from Bugle North• Integrate with other Scott subsea tie-backs

Bream• Successfully appraised in 2009• Targeting development approval this year;

Gardrofa could impact positively

25th March 2010 | Page 19

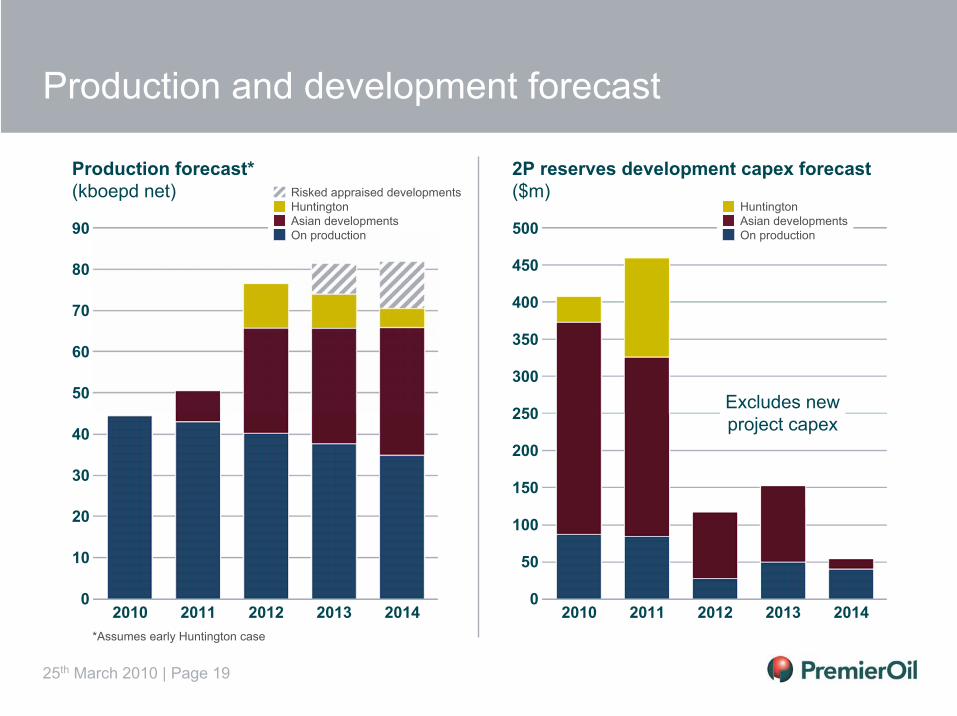

Production and development forecast

90

Production forecast*(kboepd net)

50

40

20

10

02010 2011

30

60

20142012 2013

70

80

Risked appraised developmentsHuntingtonAsian developmentsOn production

2P reserves development capex forecast($m)

500

300

250

150

50

02010 2011

200

350

20142012 2013

400

450

HuntingtonAsian developmentsOn production

100

*Assumes early Huntington case

Excludes new project capex

25th March 2010 | Page 20

Exploration update

25th March 2010 | Page 21

2009 Exploration highlights

• 29 mmboe added; finding cost <$4/boe

• Nine exploration and appraisal wells drilled, 55% success rate

– Success on key exploration wells Grosbeak, Cá Rồng Đỏ

– Successful Bream appraisal

• New acreage captured in UKand Egypt

• Central North Sea databasefrom Oilexco integrated

• Exploration strategy redefined

25th March 2010 | Page 22

• Premier began exploring in 1986, initially via entry into SE Asia

• To date Premier has discovered net 800 mmboe at an overall commercial success rate of 22%

• The commercial discoveries have been made in two basin types:1) Rifts: Southeast Asia and Norway2) Frontal Fold-belts: Pakistan

• The success rate in these basin types is ~40%

• Since 2000 the exploration success has been dominated by Rift Basin exploration in Asia and latterly in Norway

• 200 mmboe net reserves additions are targettedover the next five years

Exploration – Historic performance and future target

1000

Premier Discoveries 1986-2009 (net mmboe)

500

400

200

100

01985 1990

300

600

700

1995 2000 2005 2010

Cumulative annual discoveriesHistoric performance

800

900

2015

Cumulative annual discoveriesHistoric performanceFuture target

25th March 2010 | Page 23

Add 200 mmboe bookable net reserves by 2015 from unrisked portfolio of >1bnboe

Exploration – Targets

2010-2012• Unrisked prospect resource: 780 mmboe• Risked resource target: 144 mmboe• 12 Exploration and appraisal wells planned

in 2010• Material prospects targeted• Drilling candidates from existing portfolio

2012 to 2014• Resource additions must come from the lead

inventory maturation and success case follow up • Unrisked lead resource: 786 mmboe• Risked resource target: 78 mmboe• New ventures are required to secure the

2013/14 delivery and ensure longer term growth

250

200

100

50

02010 2011

150

300

2012 2013 2014

350

500Lead inventory - unriskedLead inventory - riskedProspect inventory - unriskedProspect inventory - riskedCum risked additions

Global exploration:Forecast resource additions (mmboe)

400

450

25th March 2010 | Page 24

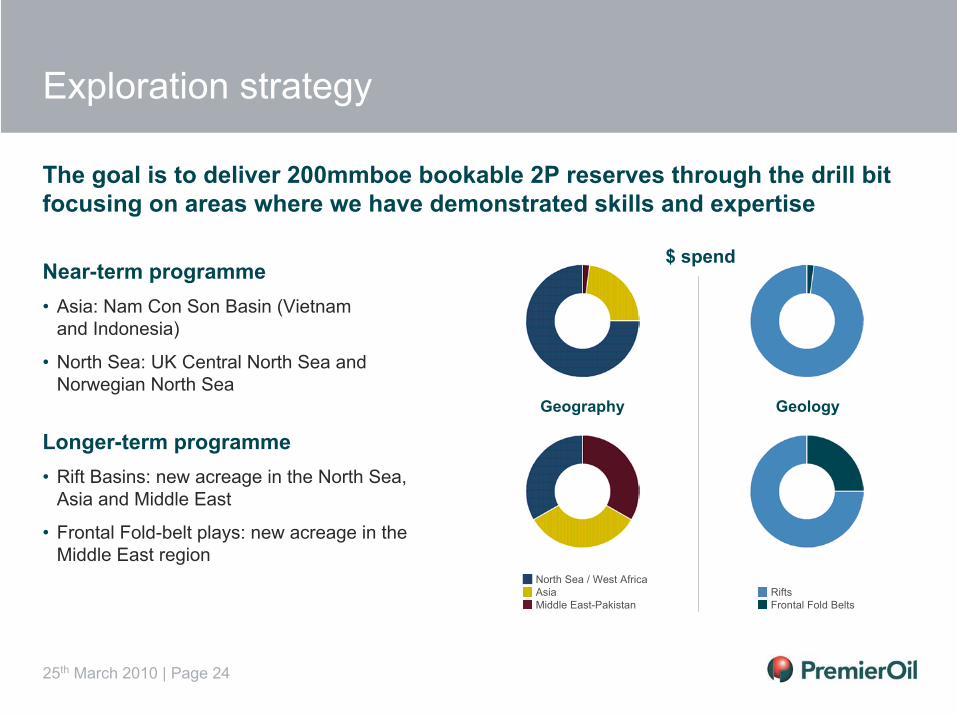

Exploration strategy

Longer-term programme• Rift Basins: new acreage in the North Sea,

Asia and Middle East

• Frontal Fold-belt plays: new acreage in the Middle East region

The goal is to deliver 200mmboe bookable 2P reserves through the drill bitfocusing on areas where we have demonstrated skills and expertise

North Sea / West AfricaAsiaMiddle East-Pakistan

Geography Geology

RiftsFrontal Fold Belts

Near-term programme• Asia: Nam Con Son Basin (Vietnam

and Indonesia)

• North Sea: UK Central North Sea and Norwegian North Sea

$ spend

25th March 2010 | Page 25

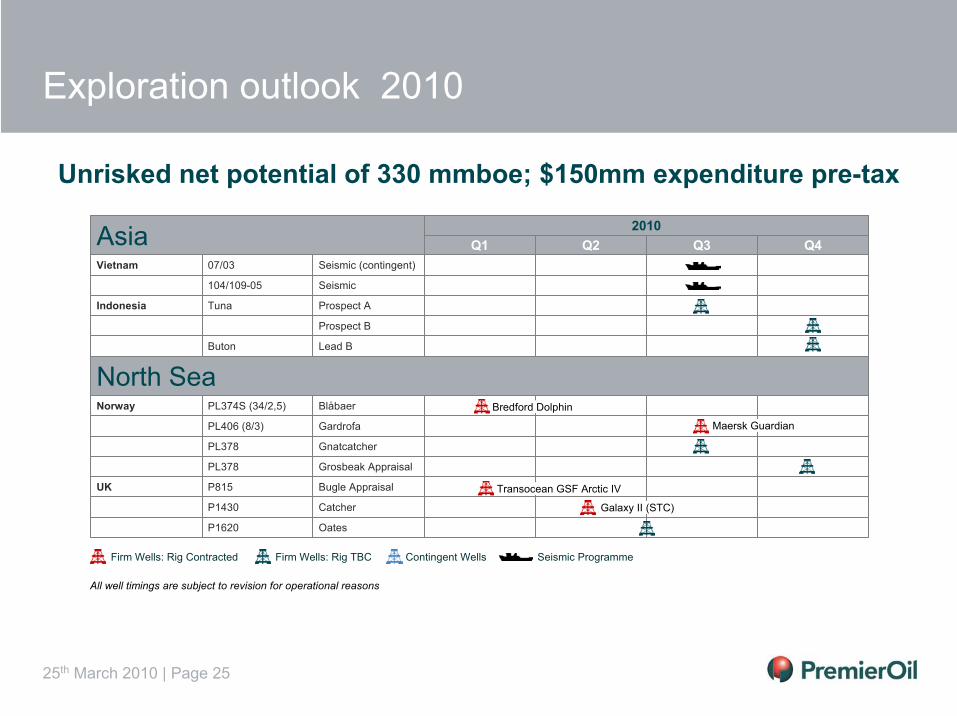

Exploration outlook 2010

Contingent WellsFirm Wells: Rig Contracted Firm Wells: Rig TBC Seismic Programme

All well timings are subject to revision for operational reasons

Unrisked net potential of 330 mmboe; $150mm expenditure pre-tax

BlåbaerPL374S (34/2,5)Norway

OatesP1620

CatcherP1430

Bugle AppraisalP815UK

Grosbeak AppraisalPL378

GnatcatcherPL378

GardrofaPL406 (8/3)

North SeaLead BButon

Prospect B

Prospect ATunaIndonesia

Seismic104/109-05

Seismic (contingent)07/03Vietnam

Q4Q3Q2Q12010Asia

Transocean GSF Arctic IV

Galaxy II (STC)

Maersk Guardian

Bredford Dolphin

25th March 2010 | Page 26

• Active 2010 programme targeting40-150 mmboe net to Premier:

Gnatcatcher

Moth/Lacewing

Gardrofa

Blåbaer

Bugle Appraisal

Bream

Oates

Catcher

Premier’s rift basin expertise is being applied to the North Sea

Exploration – North Sea

Exploration Drilling

10-25 mmboeGrosbeak

7-39 mmboeBugle

Appraisal Drilling18-33 mmboeCatcher

25-107 mmboeOates

15-115 mmboeGardrofa

31-60 mmboeGnatcatcher

15-75 mmboeBlåbaer

Gross PotentialProspect

• Prospect maturation and new venture activity in preparation for 2011 drilling

25th March 2010 | Page 27

Exploration – Norway – Greater Luno

Greater Luno (Pl 359)• Premier 30% equity• Operated by Lundin• Well status: plugged and abandoned with minor shows• Pre-drill risk: reservoir presence and effectiveness• Post Drill analysis

– No Jurassic Reservoir present– No effective reservoir in Basement– Demonstrates lateral seal to Hinault lead– Hinault under evaluation for future drilling

16/4-5 Well Location

Greater Luno

Hinault

25th March 2010 | Page 28

Blåbaer

Blåbaer (PL374)• Premier 15% equity• Operated by BG• Reserves estimate 15-30-75 mmboe• Well status: oil discovered in primary target,

being appraised via sidetrack drilling• Jordbaer project moving forward, also

operated by BG

Exploration – Norway – Blåbaer

C.I. 10m

Sidetrack

2 Km2 Km

25th March 2010 | Page 29

Exploration – UK – Bugle Appraisal

Bugle North (P815)• Premier 50%• Operated by Nexen• Well costs equally shared between 15/23d and 15/23c partnerships• High value near field exploration opportunity• Gross reserves estimate 7-17-39 mmboe• Adjacent Bugle discovery flowed 7,398 bopd and 9.06 mmscfd gas• Well Status: drilling

Galley

Dirk

S

BCU

15/23d Bugle North15/23d-13,13Z

N

Base Galley

Inline-2273 ThinMan Impedance Volume 1 Km

Bugle North

25th March 2010 | Page 30

Exploration – UK – Oates

Oates (P1620)• Premier 50% equity and operator• Reserve estimate 25-65-107 mmboe• Amplitude supported stratigraphic trap• Low to moderate risk for oil and gas• Drilling planned June 2010• Follow up potential exists at Bowers

(10-65 mmboe unrisked reserves)

Oates

Bowers

Forties Isopach Map

OatesNW SE

Amplitude Bloom on Far Stacks

25th March 2010 | Page 31

Exploration – Norway – Bream, Gardrofa

Bream (PL 406)• Brent age oil discovered 1971, close to Yme Field• In 2009,17/12-4 and its sidetracks wells appraised

this discovery, testing 2,516 boepd• Operated by BG, Premier equity 20%• Estimated reserves 39-50-63 mmboe• Plan of development under review

Gardrofa (PL407)• Premier’s first operated licence in Norway• Premier equity 40%• Untested trap flanking a Salt dome feature• Estimated reserves 15-70-115 mmboe• Moderate risk for oil• Well planned for August 2010

9/1-1 Gardrofa Prospect Well Location

Success at Gardrofa will lead to a new core area for Premier in Norway

25th March 2010 | Page 32

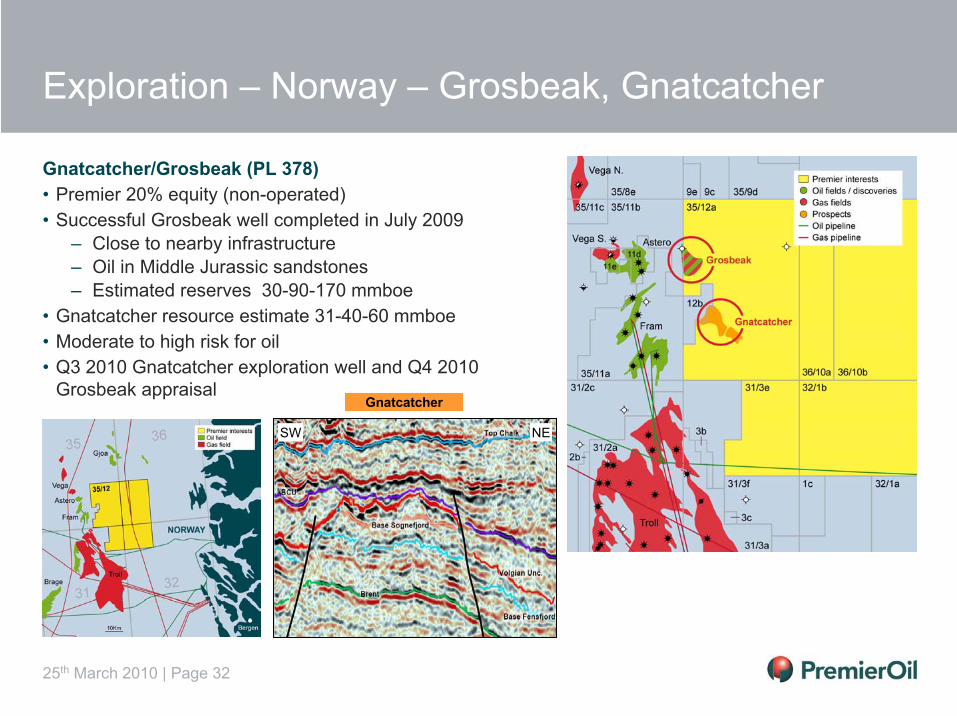

Exploration – Norway – Grosbeak, Gnatcatcher

Gnatcatcher/Grosbeak (PL 378)• Premier 20% equity (non-operated)• Successful Grosbeak well completed in July 2009

– Close to nearby infrastructure– Oil in Middle Jurassic sandstones– Estimated reserves 30-90-170 mmboe

• Gnatcatcher resource estimate 31-40-60 mmboe• Moderate to high risk for oil• Q3 2010 Gnatcatcher exploration well and Q4 2010

Grosbeak appraisalGnatcatcher

SW NE

25th March 2010 | Page 33

Exploration – Indonesia – Tuna

Singa / Kuda Laut Cacing Laut Gajah Laut Utara

Tuna PSC• Premier 65% equity• Target equity pre-drill 40%• Numerous drillable prospects being defined on 3D• Reserves estimate 30-100-200 mmboe, per

prospect• Moderate risk for oil and gas• 2 wells planned for Q3 / Q4 2010

25th March 2010 | Page 34

South Darag• Premier 100%, subject to government approvals• Located in the Gulf of Suez rift basin, close to

existing production facilities• Three year initial term• Planned exploration drilling in 2013• Block wide resource potential: 50-250 mmboe• Three leads identified with 30-100 mmbo potential• Moderate risk for oil

SW

New Business/Exploration – Egypt – South Darag

NE

25th March 2010 | Page 35

North Sea• UK: Four exploration wells planned including

appraisal of Moth and testing of the deeperTriassic Lacewing prospect

• Norway: Drilling dependent on 2010 results

SE Asia• Vietnam: Block 07/03 - CRD Appraisal and an

additional exploration well• Vietnam: 104-109/5 - Commitment well• Indonesia: Near field exploration wells in

Natuna A and NSBA, further drilling on Tuna

Middle East Pakistan• Pakistan: One near field exploration well

West Africa• Congo: Contingent well on the Ida prospect

New ventures• Actively pursuing new opportunities for 2011 drilling

Exploration – 2011 Outlook

12 Exploration & appraisal wells are planned,targeting net 250 mmboe of unrisked resource potential

Firm wellsContingent wells

25th March 2010 | Page 36

Summary

25th March 2010 | Page 37

Delivering against strategy

Progress

• Chim Sao and Gajah Baru on schedule for 2011

• Froy, Bream, Bugle progress towards development sanction in 2010

• Added 29 mmboe. Up to 11 exploration and appraisal wells over next nine months targeting 330 mmboe

• Oilexco and Block 12 (Vietnam) successfully integrated; non-core asset sales underway

• Investment programme fully funded; acquisition capacity

Strategy

• Attain 75 kboepd from existing projects

• Commercialise contingent resource base

• Add 200 mmboe of2P reserves from the exploration portfolio

• Make value-adding acquisitions in threecore areas

• Maintain a conservative balance sheet

Production2005-2009 (kboepd)

Target

• Build three quality businesses which deliver 100 kboepdfrom 400 mmbbls of reserves

Operating Cashflow2005-2009 ($million)

2P Reserves2005-2009 (mmboe)

Acquisitions 2005-2009Oil price ($/bbl)

25th March 2010 | Page 38

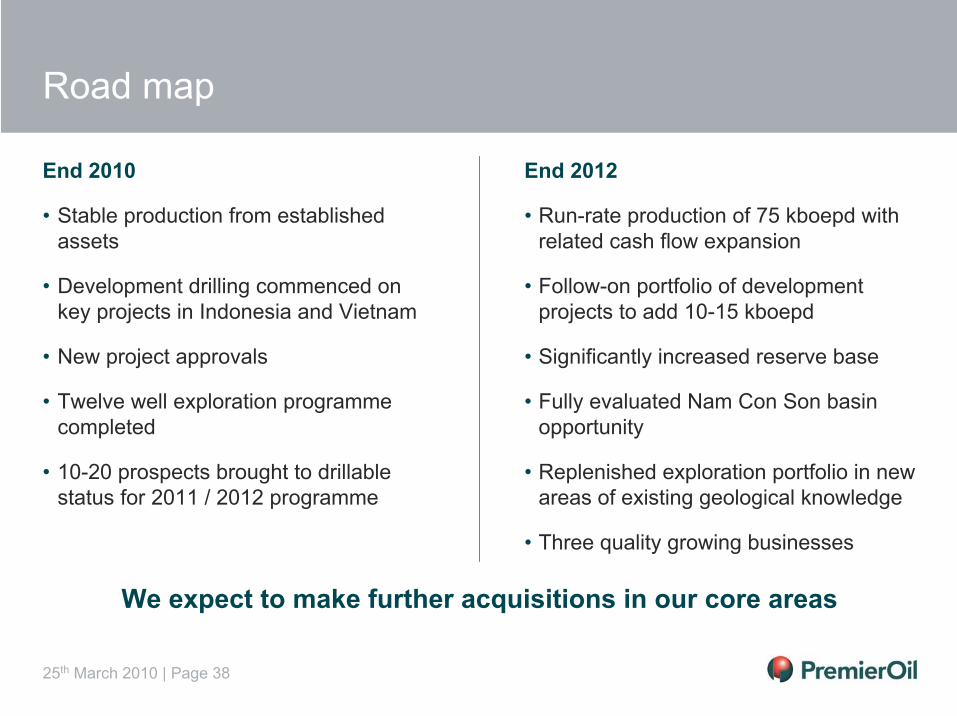

Road map

End 2012

• Run-rate production of 75 kboepd with related cash flow expansion

• Follow-on portfolio of development projects to add 10-15 kboepd

• Significantly increased reserve base

• Fully evaluated Nam Con Son basin opportunity

• Replenished exploration portfolio in new areas of existing geological knowledge

• Three quality growing businesses

End 2010

• Stable production from established assets

• Development drilling commenced on key projects in Indonesia and Vietnam

• New project approvals

• Twelve well exploration programme completed

• 10-20 prospects brought to drillable status for 2011 / 2012 programme

We expect to make further acquisitions in our core areas

25th March 2010 | Page 39

Appendix

25th March 2010 | Page 40

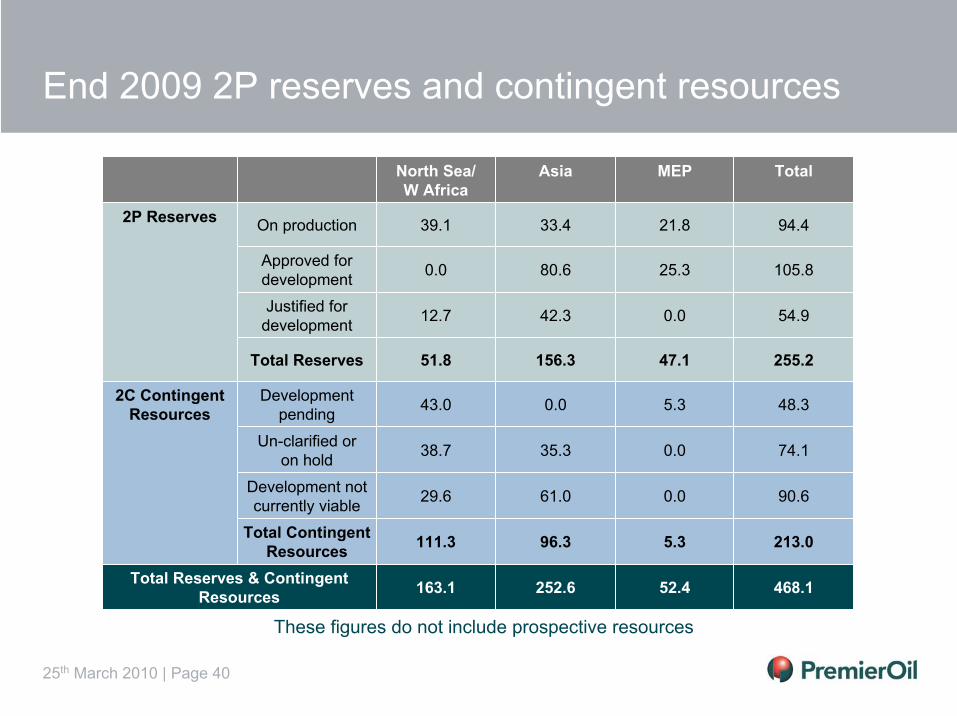

End 2009 2P reserves and contingent resources

468.152.4252.6163.1Total Reserves & Contingent Resources

2C Contingent Resources

2P Reserves

48.35.30.043.0Development pending

74.10.035.338.7Un-clarified oron hold

90.60.061.029.6Development not currently viable

213.05.396.3111.3Total Contingent Resources

47.1

0.0

25.3

21.8

MEP

156.3

42.3

80.6

33.4

Asia

255.251.8Total Reserves

54.912.7Justified for development

105.80.0Approved for development

94.439.1On production

TotalNorth Sea/W Africa

These figures do not include prospective resources

25th March 2010 | Page 41

Exploration – Indonesia – Buton

meters

‘B’

Buton PSC• Premier equity 30%• Japex operator• Lead B reserve estimates 35-100-300 mmboe• High risk for oil, in fold belt theme• Prospect maturation ongoing• Drilling planned Q4 2010 / Q1 2011

Lead BNW SE

0 5000

25th March 2010 | Page 42

Exploration – UK – Catcher

2 Km

Catcher (P1430)• Premier equity 50%, target equity 35% pre-drill• Encore operator• Reserves estimates 18-25-33 mmboe• High risk for oil• Drilling planned April 2010

CatcherWTop Cromarty depth Map E

Balder

Chalk

Top Cromarty

Phase Change

2 Km

Blocks28/9 & 10c

25th March 2010 | Page 43www.premier-oil.com 25th March 2010

Related Documents