March 2006 Silvio de Carvalho Executive Director Roadshow

March 2006 Silvio de Carvalho Executive Director Roadshow.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

March 2006

Silvio de CarvalhoExecutive Director

Roadshow

2

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

Agenda

3

Brazilian Macroeconomic Scenario

Floating exchange rate and outstanding adjustment in external

accounts

Monetary policy: inflation expectation and growth

Fiscal policy: accomplishment of fiscal targets, even without IMF

surveillance

Credit expansion: public sector crowding out

Baseline scenario

Brazil: towards investment grade

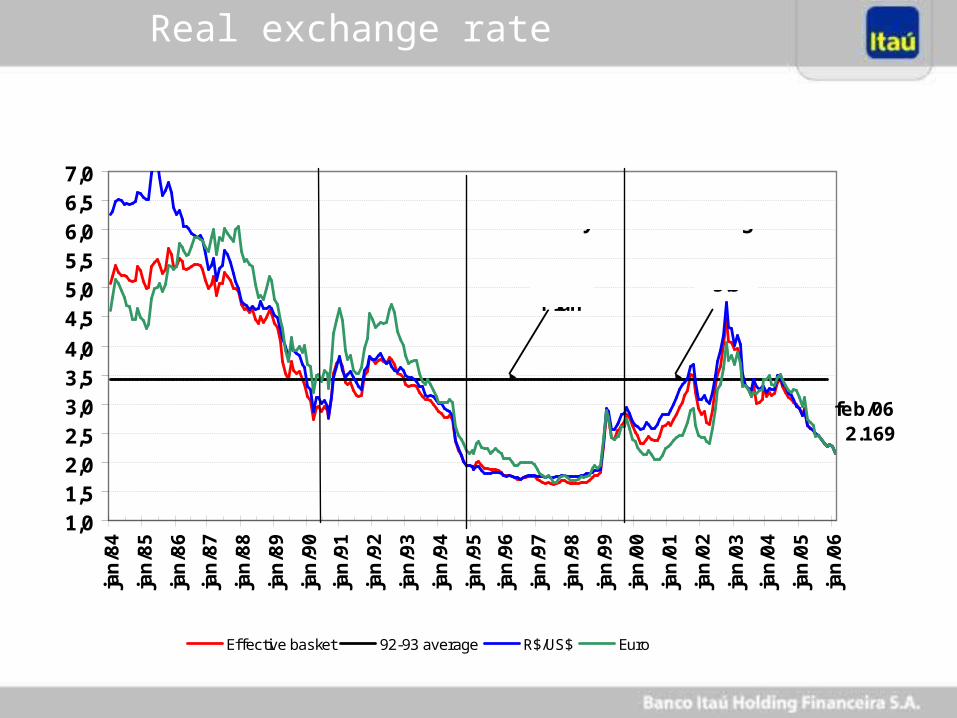

Real exchange rate

feb/06 2.169

1,0

1,52,02,5

3,03,54,0

4,55,05,5

6,06,57,0

jan

/84

jan

/85

jan

/86

jan

/87

jan

/88

jan

/89

jan

/90

jan

/91

jan

/92

jan

/93

jan

/94

jan

/95

jan

/96

jan

/97

jan

/98

jan

/99

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

Effective basket 92-93 average R$/US$ Euro

Collor-ItamarPeriod

Peggedcurrency

Floatingexchange rate

RealPlan

3.5

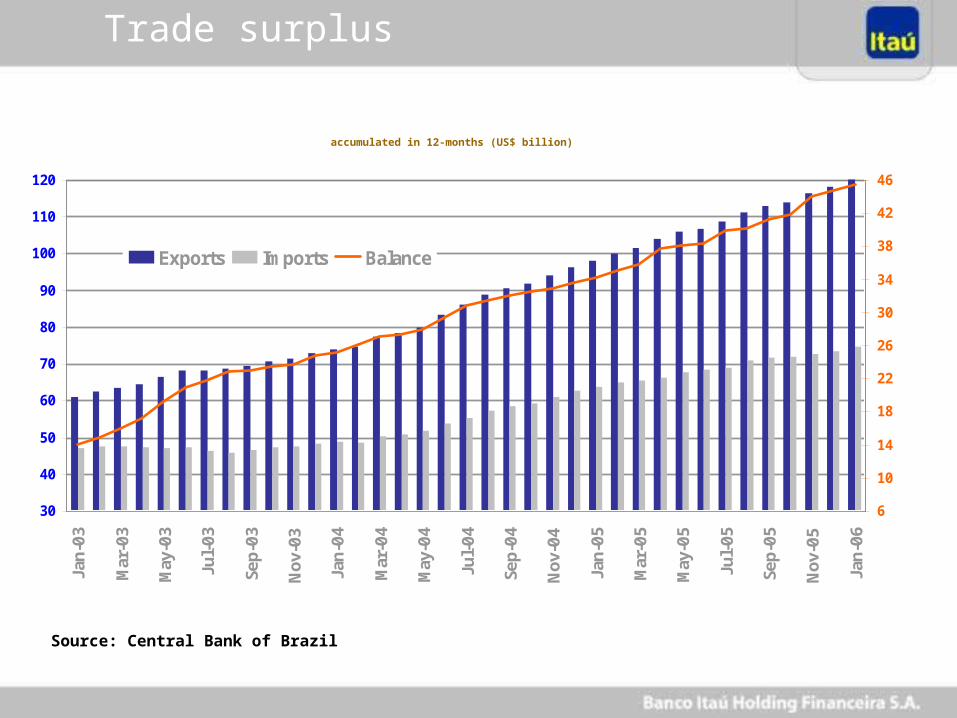

Trade surplus

accumulated in 12-months (US$ billion)

Source: Central Bank of Brazil

30

40

50

60

70

80

90

100

110

120

Jan-

03

Mar

-03

May

-03

Jul-03

Sep-

03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-04

Sep-

04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-05

Sep-

05

Nov

-05

Jan-

06

6

10

14

18

22

26

30

34

38

42

46

Exports Imports Balance

6

0

2

4

6

8

10

12

14

16

18Ja

n-99

Apr-

99Ju

l-99

Oct

-99

Jan-

00Ap

r-00

Jul-

00O

ct-0

0Ja

n-01

Apr-

01Ju

l-01

Oct

-01

Jan-

02Ap

r-02

Jul-

02O

ct-0

2Ja

n-03

Apr-

03Ju

l-03

Oct

-03

Jan-

04Ap

r-04

Jul-

04O

ct-0

4Ja

n-05

Apr-

05Ju

l-05

Oct

-05

Jan-

06Ap

r-06

Jul-

06O

ct-0

6

0

2

4

6

8

10

12

14

16

18

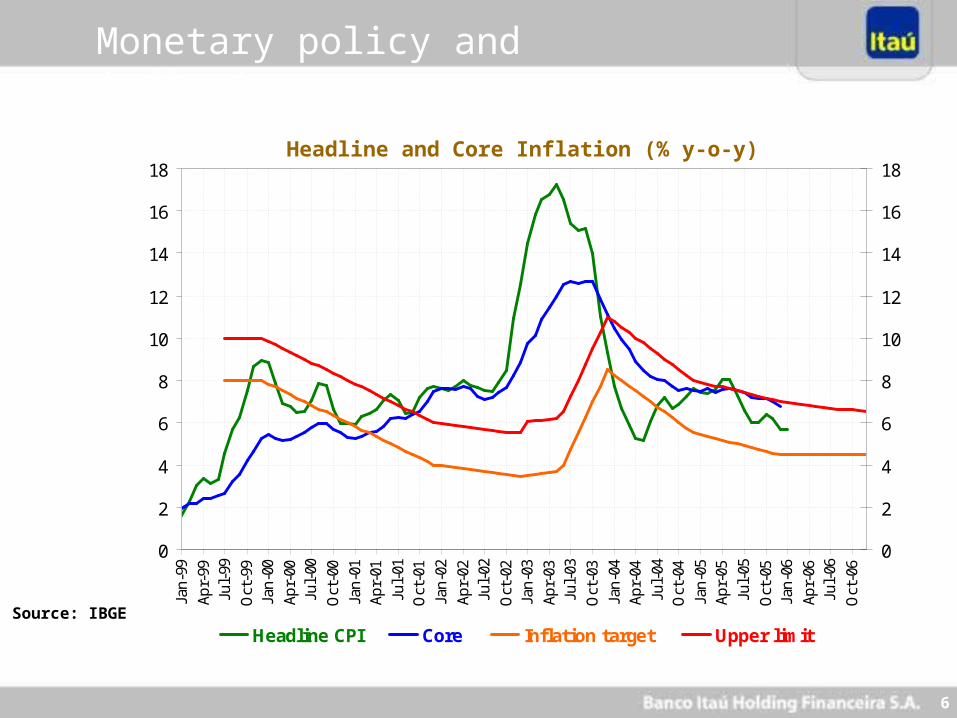

Headline CPI Core Inflation target Upper limit

Monetary policy and inflation

Source: IBGE

Headline and Core Inflation (% y-o-y)

7

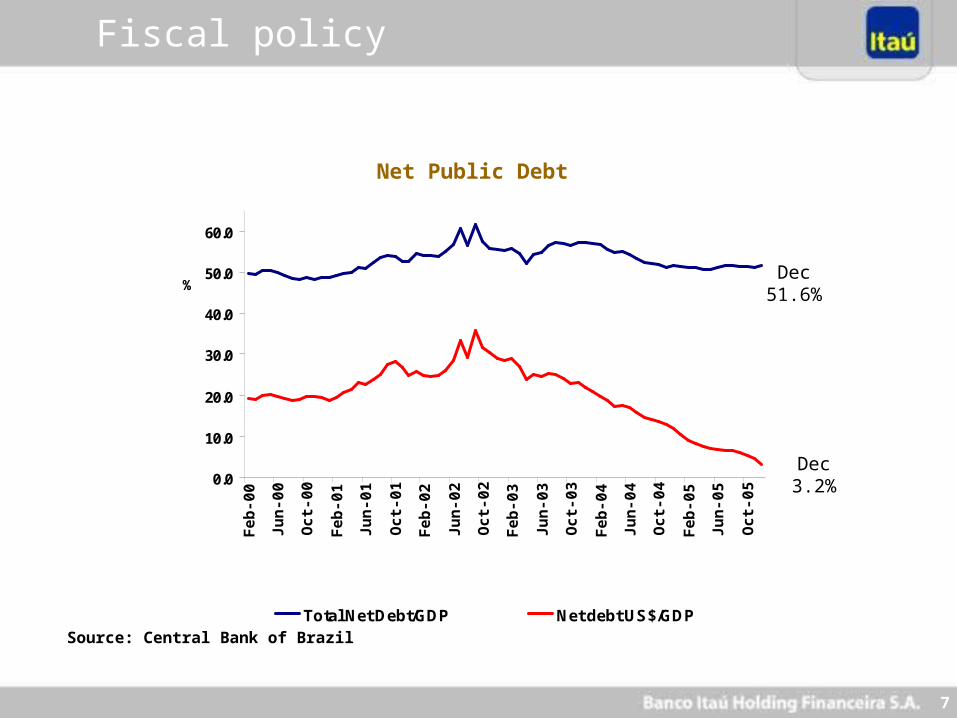

Fiscal policy

Source: Central Bank of Brazil

Net Public Debt

Dec 51.6%

Dec 3.2%0.0

10.0

20.0

30.0

40.0

50.0

60.0F

eb-0

0

Jun

-00

Oct

-00

Feb

-01

Jun

-01

Oct

-01

Feb

-02

Jun

-02

Oct

-02

Feb

-03

Jun

-03

Oct

-03

Feb

-04

Jun

-04

Oct

-04

Feb

-05

Jun

-05

Oct

-05

Total Net Debt/GDP Net debt US$/GDP

%

8

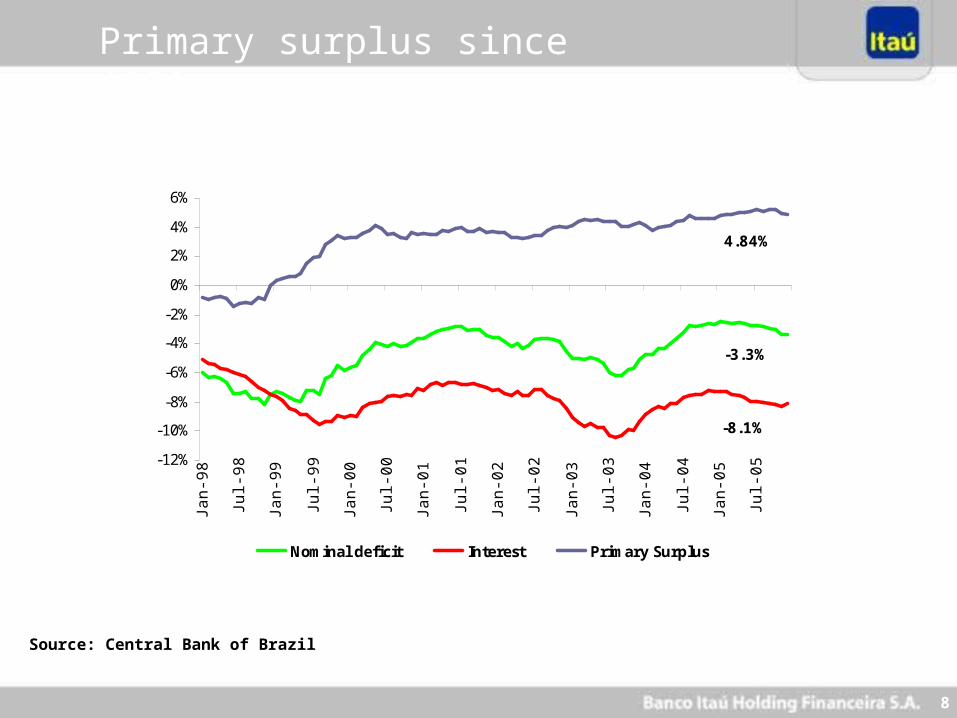

Primary surplus since 1998

Source: Central Bank of Brazil

-3.3%

-8.1%

4.84%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%Ja

n-9

8

Jul-

98

Jan-9

9

Jul-

99

Jan-0

0

Jul-

00

Jan-0

1

Jul-

01

Jan-0

2

Jul-

02

Jan-0

3

Jul-

03

Jan-0

4

Jul-

04

Jan-0

5

Jul-

05

Nominal deficit Interest Primary Surplus

9

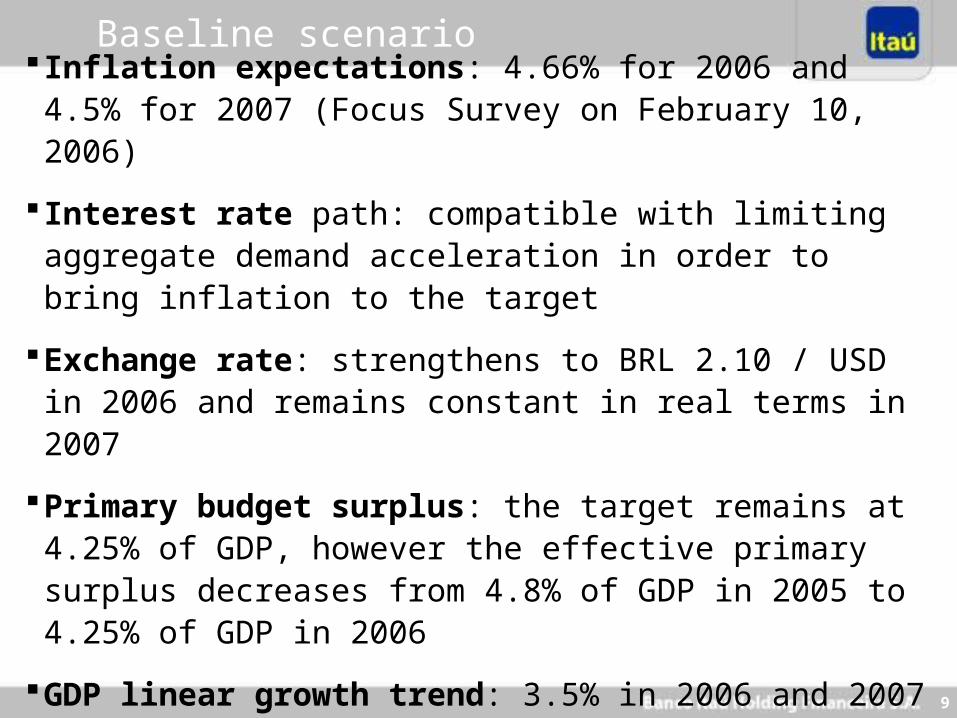

Inflation expectations: 4.66% for 2006 and 4.5% for 2007 (Focus Survey on February 10, 2006)

Interest rate path: compatible with limiting aggregate demand acceleration in order to bring inflation to the target

Exchange rate: strengthens to BRL 2.10 / USD in 2006 and remains constant in real terms in 2007

Primary budget surplus: the target remains at 4.25% of GDP, however the effective primary surplus decreases from 4.8% of GDP in 2005 to 4.25% of GDP in 2006

GDP linear growth trend: 3.5% in 2006 and 2007

Baseline scenario

10

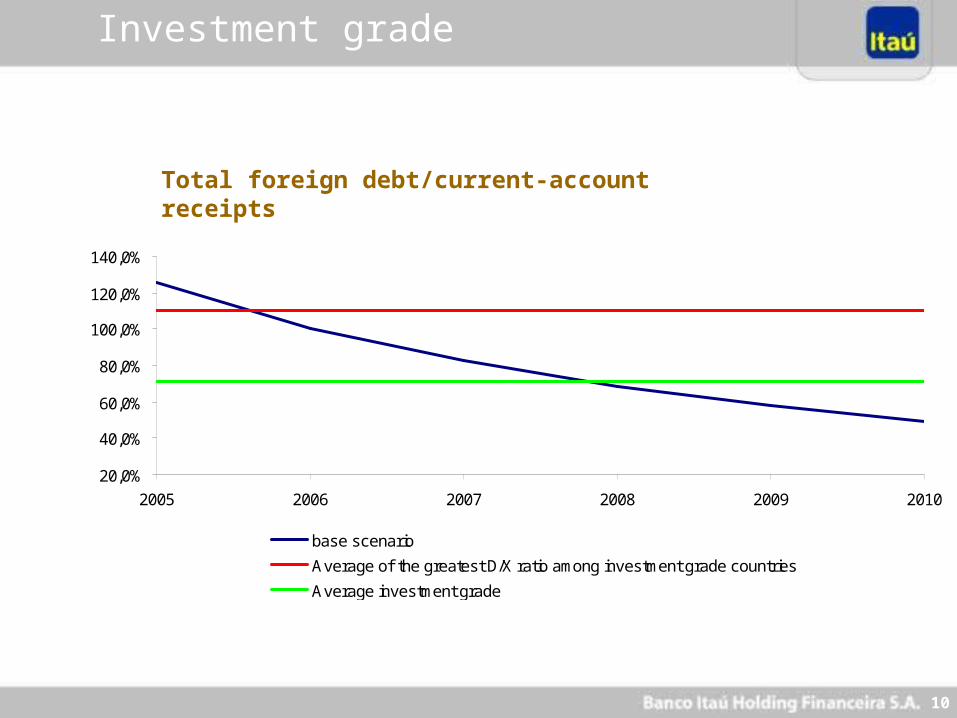

Investment grade

Total foreign debt/current-account receipts

20,0%

40,0%

60,0%

80,0%

100,0%

120,0%

140,0%

2005 2006 2007 2008 2009 2010

base scenario

Average of the greatest D/X ratio among investment grade countries

Average investment grade

11

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

Agenda

12

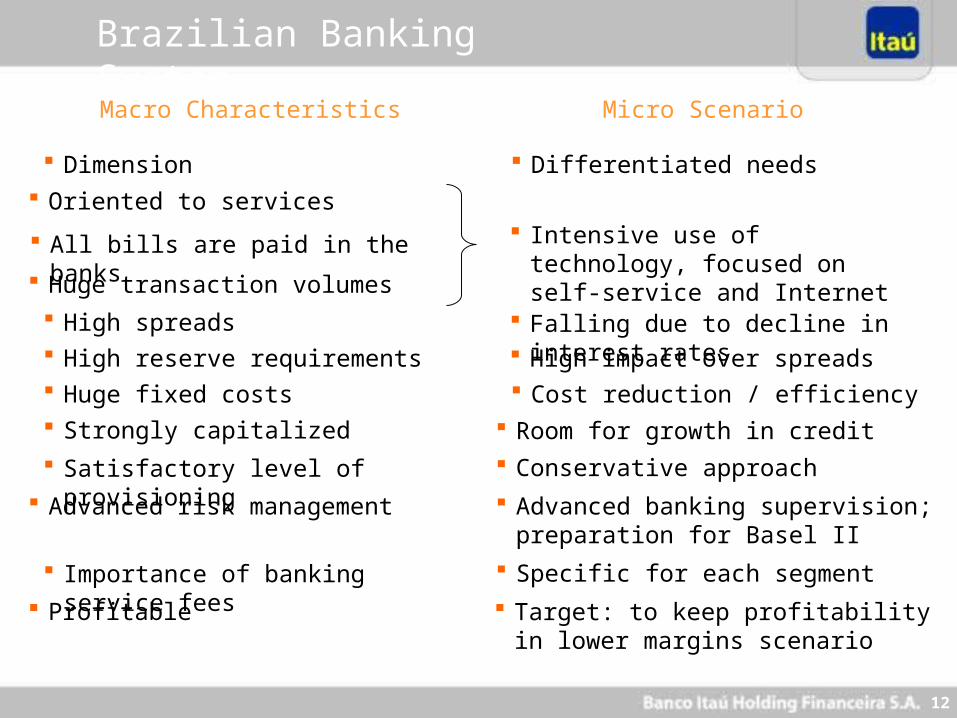

Brazilian Banking System

Macro Characteristics Micro Scenario

Huge fixed costs Cost reduction / efficiency Strongly capitalized Room for growth in credit Satisfactory level of provisioning Conservative approach

Advanced risk management Advanced banking supervision; preparation for Basel II

Importance of banking service fees Specific for each segment

Profitable Target: to keep profitability in lower margins scenario

Oriented to services Intensive use of technology, focused

on self-service and Internet All bills are paid in the banks

Huge transaction volumes

High spreads Falling due to decline in interest rates

Dimension Differentiated needs

High reserve requirements High impact over spreads

13

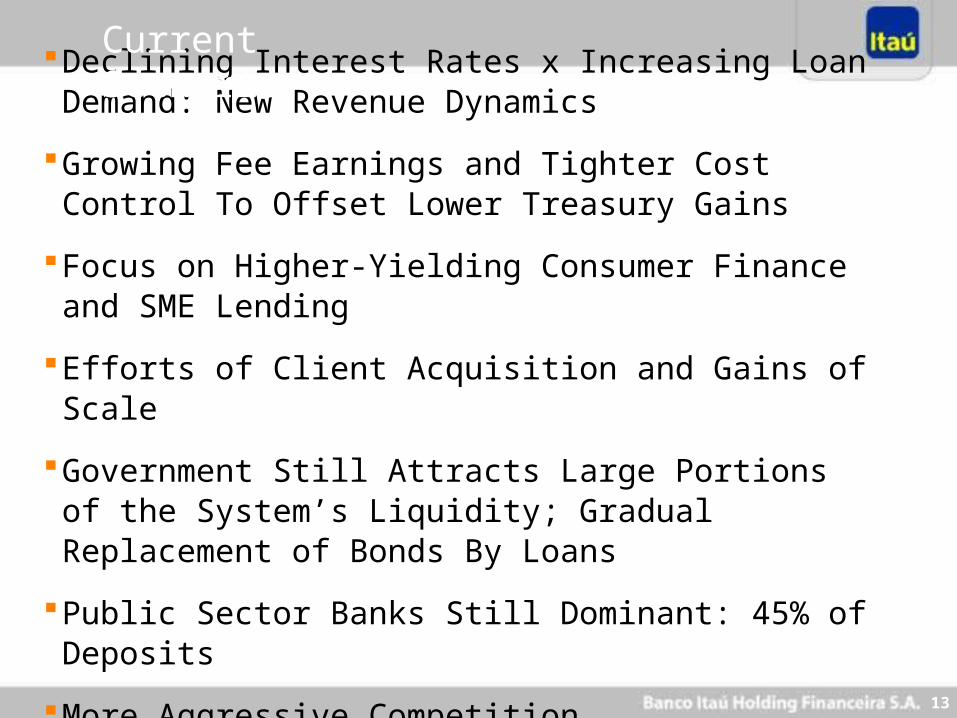

Declining Interest Rates x Increasing Loan Demand: New Revenue Dynamics

Growing Fee Earnings and Tighter Cost Control To Offset Lower Treasury Gains

Focus on Higher-Yielding Consumer Finance and SME Lending

Efforts of Client Acquisition and Gains of Scale

Government Still Attracts Large Portions of the System’s Liquidity; Gradual Replacement of Bonds By Loans

Public Sector Banks Still Dominant: 45% of Deposits

More Aggressive Competition

Current Scenario

14

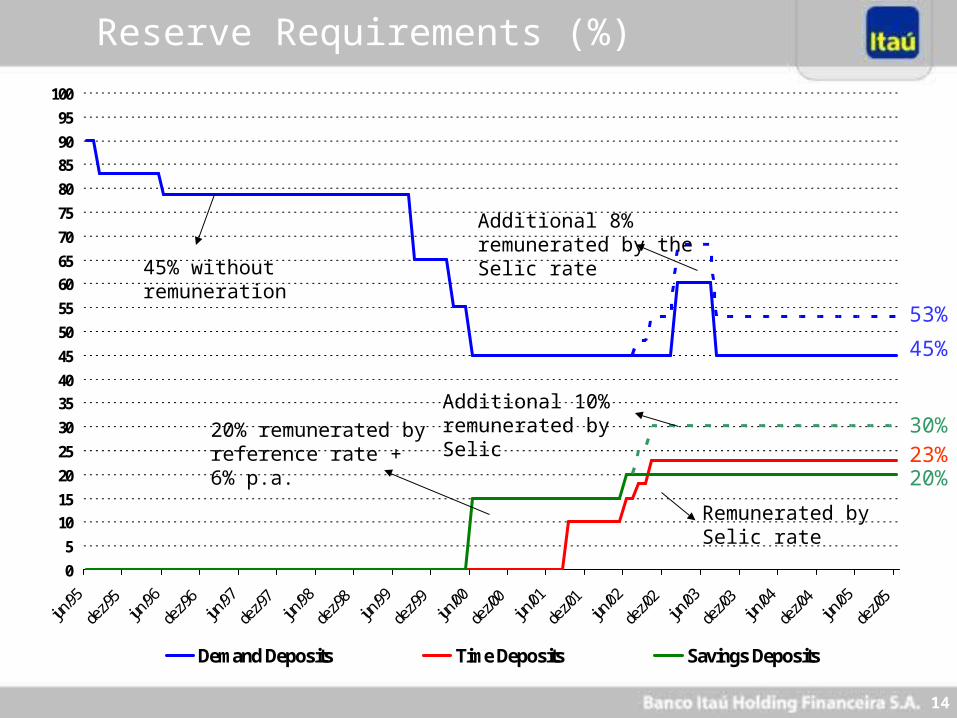

Reserve Requirements (%)

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

jun/95

dez/9

5jun

/96

dez/9

6jun

/97

dez/9

7jun

/98

dez/9

8jun

/99

dez/9

9jun

/00

dez/0

0jun

/01

dez/0

1jun

/02

dez/0

2jun

/03

dez/0

3jun

/04

dez/0

4jun

/05

dez/0

5

Demand Deposits Time Deposits Savings Deposits

53%

30%23%

45%

20%

Additional 8% remunerated by the Selic rate

20% remunerated by reference rate + 6% p.a.

Additional 10% remunerated by Selic

Remunerated by Selic rate

45% without remuneration

15

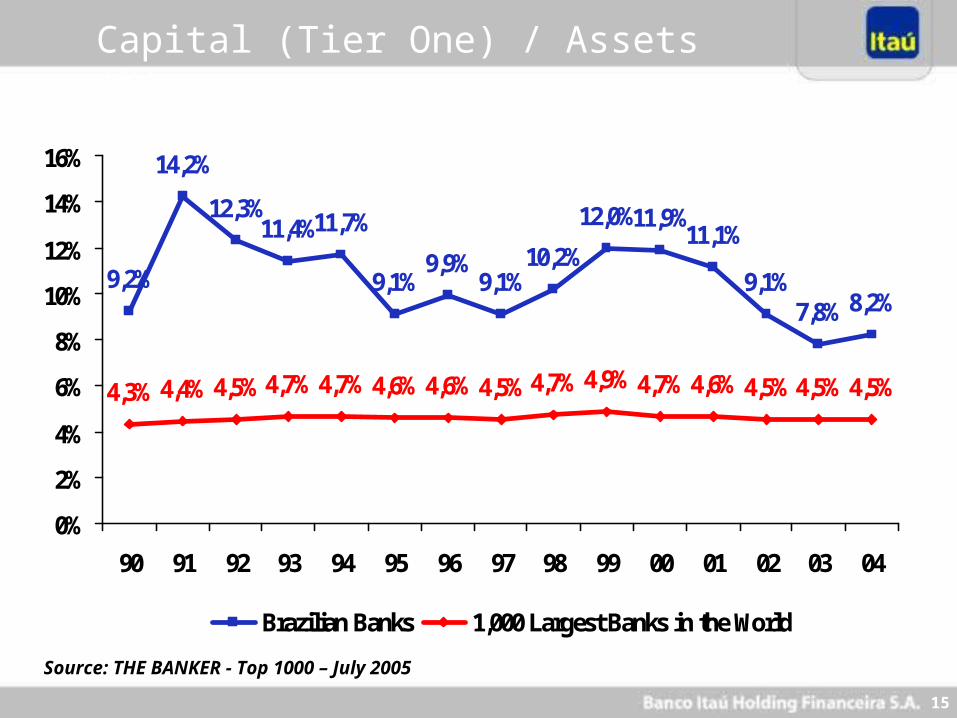

Capital (Tier One) / Assets (%)

9,2%

14,2%

12,3%11,4%11,7%

9,1%9,9%

9,1%10,2%

12,0%11,9%11,1%

9,1%7,8% 8,2%

4,3% 4,4% 4,5% 4,7% 4,7% 4,6% 4,6% 4,5% 4,7% 4,9% 4,7% 4,6% 4,5% 4,5% 4,5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

Brazilian Banks 1,000 Largest Banks in the World

Source: THE BANKER - Top 1000 – July 2005

16

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

Agenda

17

Ownership Structure - Dec/05

ESA Family: 33.67%

• Common Shares: 60.64%

• Preferred Shares: 17.15%

Free Float: 66.33%

• Common Shares: 39.36%

• Preferred Shares: 82.85%

Itaúsa

Banco Itaú Holding Financeira S.A.

Free Float: 51.59%

• Common Shares: 11.16%

• Preferred Shares: 99.99%

Total: 48.41%• Commom Shares: 88.84%• Preferred Shares: 0.01%

18

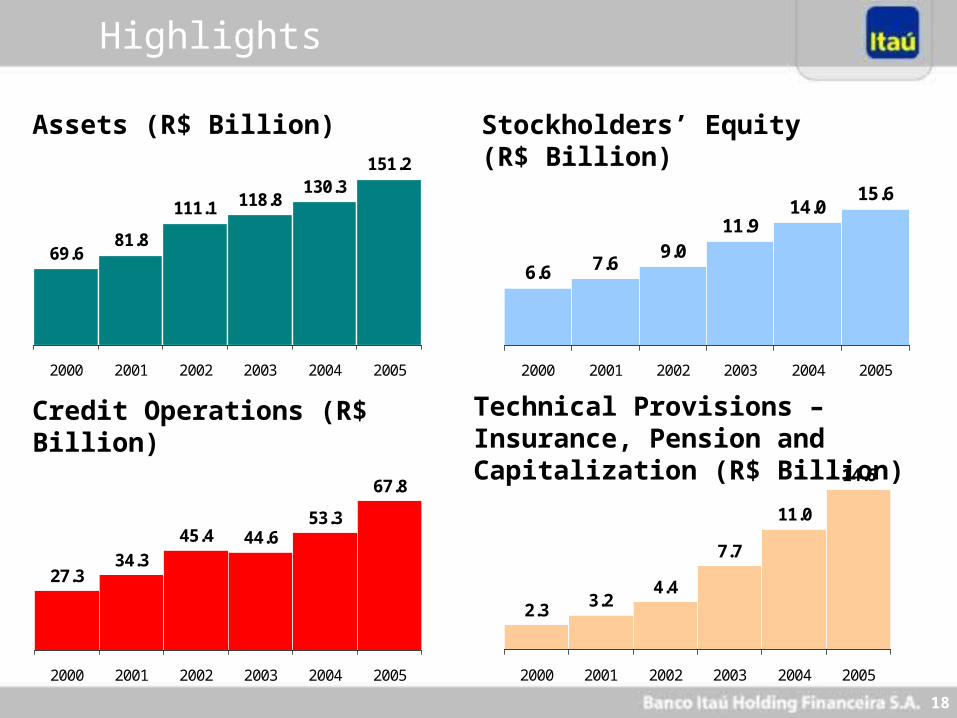

69.681.8

151.2130.3

118.8111.1

2000 2001 2002 2003 2004 2005

27.334.3

45.4 44.653.3

67.8

2000 2001 2002 2003 2004 2005

6.6 7.69.0

11.914.0

15.6

2000 2001 2002 2003 2004 2005

Highlights

Assets (R$ Billion)

Credit Operations (R$ Billion)

Stockholders’ Equity (R$ Billion)

2.3 3.24.4

7.7

11.0

14.6

2000 2001 2002 2003 2004 2005

Technical Provisions – Insurance, Pension and Capitalization (R$ Billion)

19

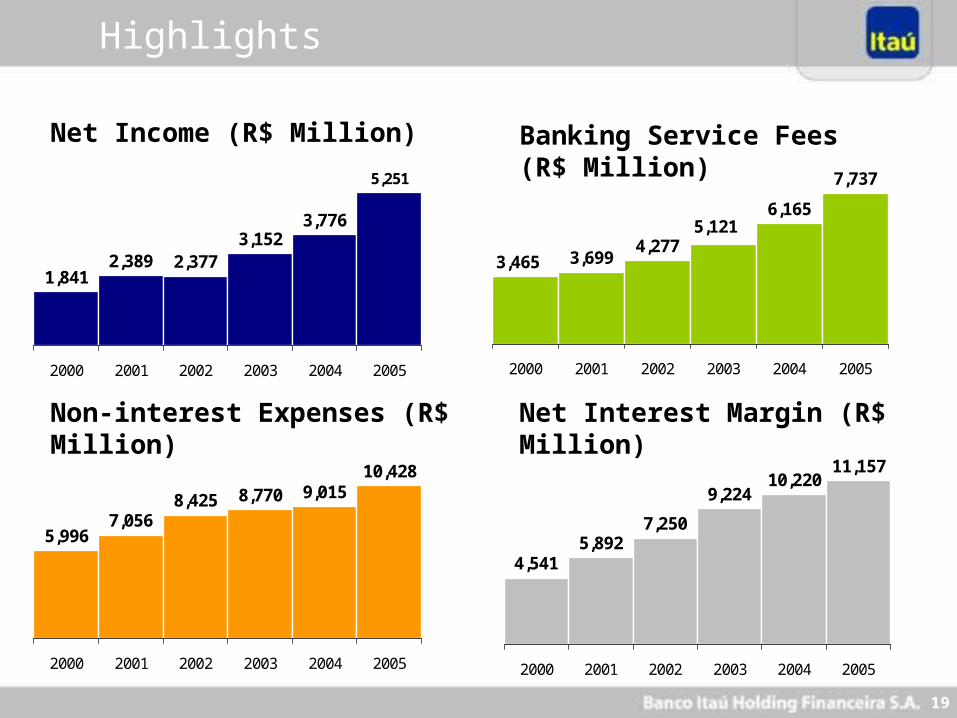

11,15710,220

9,224

7,2505,892

4,541

2000 2001 2002 2003 2004 2005

1,841

3,7763,152

5,251

2,3772,389

2000 2001 2002 2003 2004 2005

7,056

8,770 9,0158,425

5,996

10,428

2000 2001 2002 2003 2004 2005

3,6994,277

6,165

7,737

3,465

5,121

2000 2001 2002 2003 2004 2005

Net Income (R$ Million)

Non-interest Expenses (R$ Million)

Banking Service Fees (R$ Million)

Net Interest Margin (R$ Million)

Highlights

20

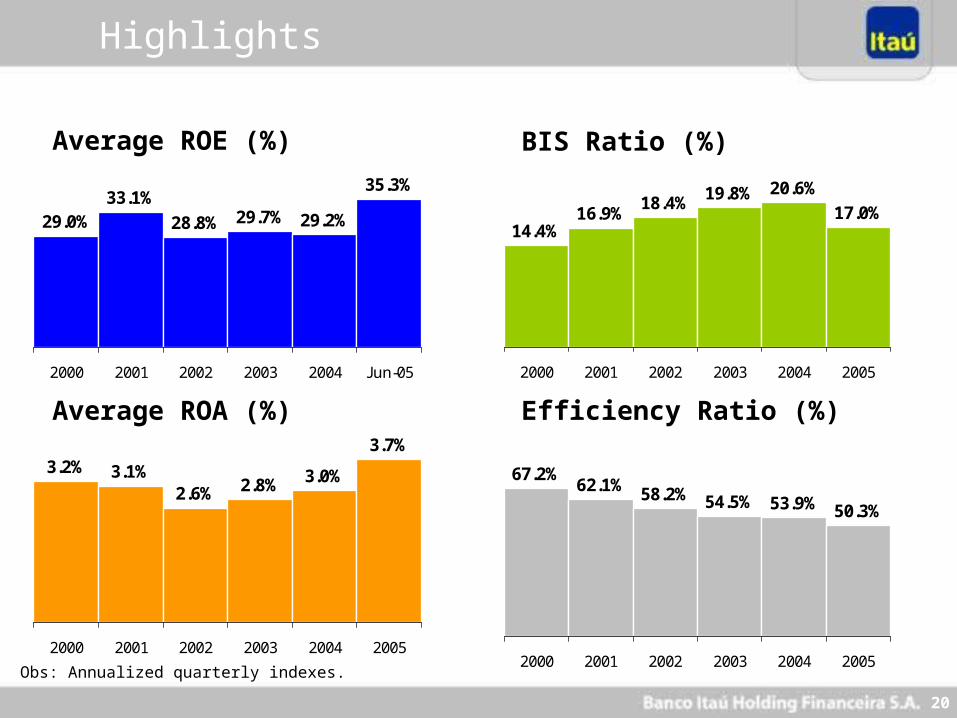

29.0%33.1%

28.8% 29.7% 29.2%

35.3%

2000 2001 2002 2003 2004 Jun-05

3.2% 3.1%2.6% 2.8% 3.0%

3.7%

2000 2001 2002 2003 2004 2005

14.4%16.9%

18.4% 19.8% 20.6%

17.0%

2000 2001 2002 2003 2004 2005

67.2%62.1% 58.2% 54.5% 53.9% 50.3%

2000 2001 2002 2003 2004 2005Obs: Annualized quarterly indexes.

Average ROE (%)

Average ROA (%)

BIS Ratio (%)

Efficiency Ratio (%)

Highlights

21

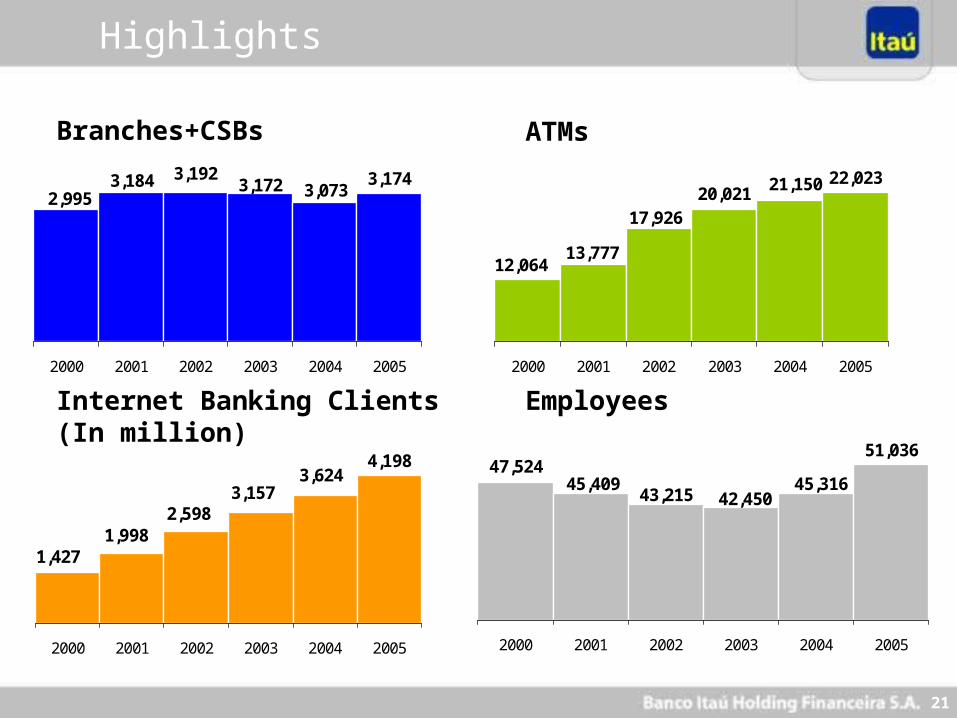

3,1743,0733,172

3,1923,1842,995

2000 2001 2002 2003 2004 2005

3,6243,157

2,5981,998

1,427

4,198

2000 2001 2002 2003 2004 2005

22,02320,021 21,150

17,926

13,77712,064

2000 2001 2002 2003 2004 2005

42,45045,316

43,21545,409

47,52451,036

2000 2001 2002 2003 2004 2005

Branches+CSBs

Internet Banking Clients (In million)

ATMs

Employees

Highlights

22

11,879

15,027

2,229

15,560

9,036

7,578

6,6425,907

4,198

3,3372,857

880

3,152

181

3,776

5,251

2,389

1,8411,869

721592

343

3820

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

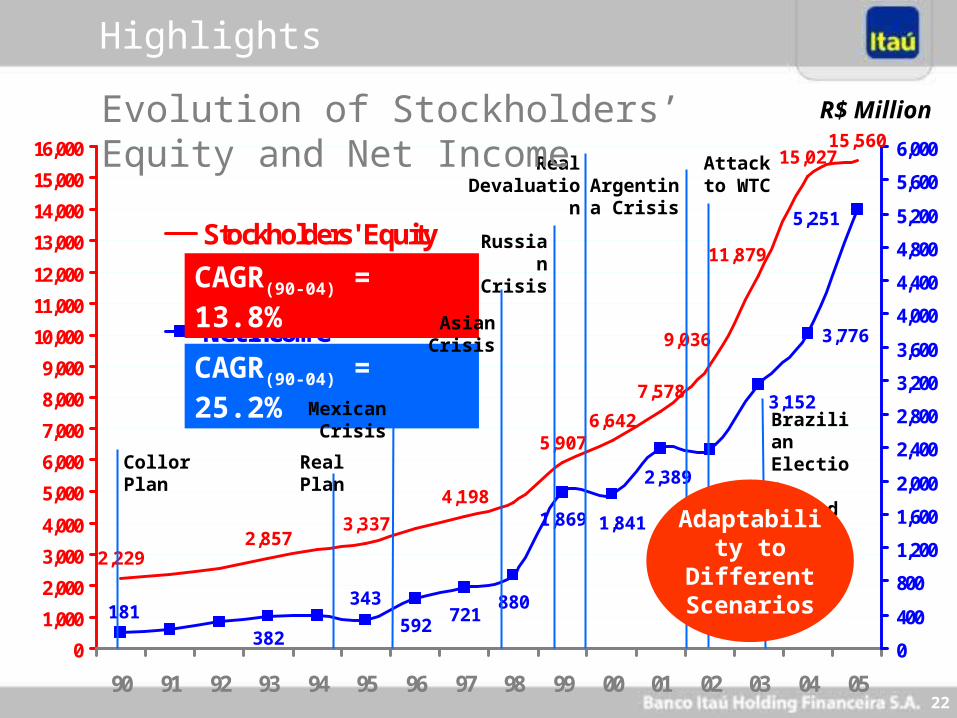

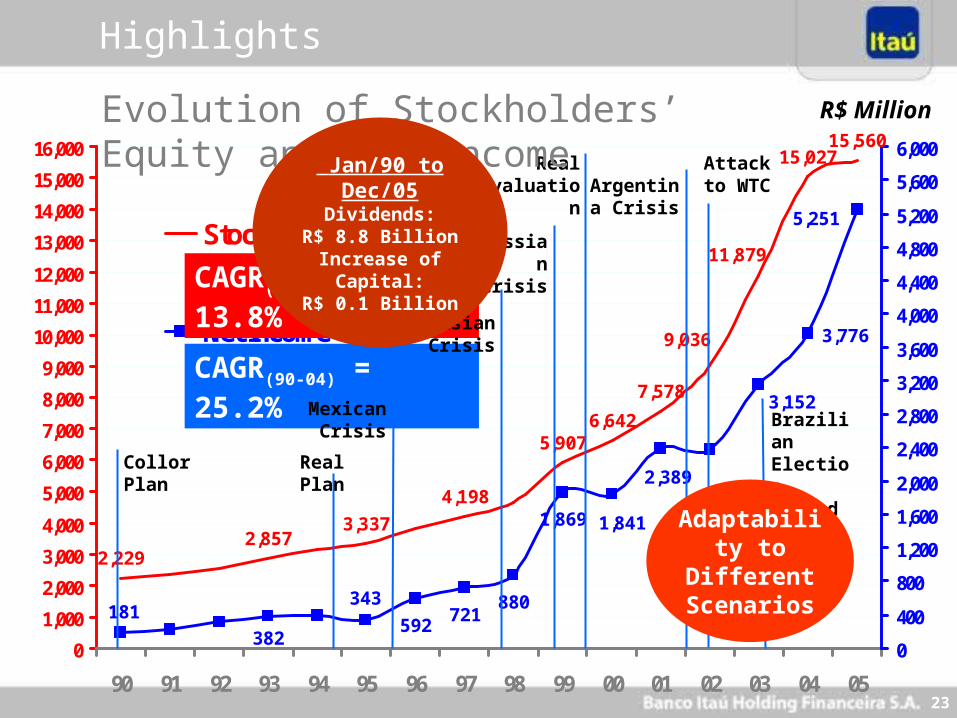

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

4,000

4,400

4,800

5,200

5,600

6,000

Stockholders' Equity

Net Income

CAGR(90-04) = 13.8%

CAGR(90-04) = 25.2%

Real Plan

Mexican Crisis

Asian Crisis

Russian Crisis

Real Devaluation Argentina

Crisis

Collor Plan

Attack to WTC

Brazilian Election Period

R$ Million

Adaptability to Different

Scenarios

Evolution of Stockholders’ Equity and Net Income

Highlights

23

11,879

15,027

2,229

15,560

9,036

7,578

6,6425,907

4,198

3,3372,857

880

3,152

181

3,776

5,251

2,389

1,8411,869

721592

343

3820

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

4,000

4,400

4,800

5,200

5,600

6,000

Stockholders' Equity

Net Income

CAGR(90-04) = 13.8%

CAGR(90-04) = 25.2%

Real Plan

Mexican Crisis

Asian Crisis

Russian Crisis

Real Devaluation Argentina

Crisis

Collor Plan

Attack to WTC

Brazilian Election Period

R$ Million

Adaptability to Different

Scenarios

Evolution of Stockholders’ Equity and Net Income

Highlights

Jan/90 to Dec/05Dividends:

R$ 8.8 BillionIncrease of Capital:

R$ 0.1 Billion

24

Agenda

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

25

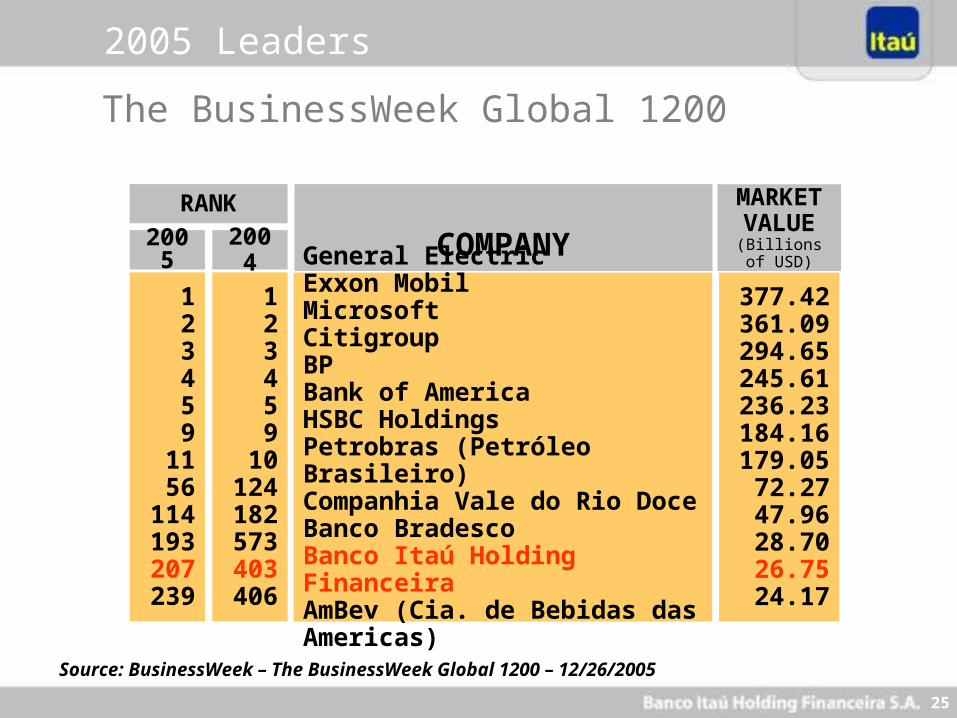

2005 Leaders

Source: BusinessWeek – The BusinessWeek Global 1200 – 12/26/2005

RANK

123459

1156

114193207239

2005

123459

10124182573403406

2004 COMPANY

General ElectricExxon MobilMicrosoftCitigroupBPBank of AmericaHSBC HoldingsPetrobras (Petróleo Brasileiro)Companhia Vale do Rio DoceBanco BradescoBanco Itaú Holding FinanceiraAmBev (Cia. de Bebidas das Americas)

377.42361.09294.65245.61236.23184.16179.0572.2747.9628.7026.7524.17

MARKET VALUE

(Billions of USD)

The BusinessWeek Global 1200

26

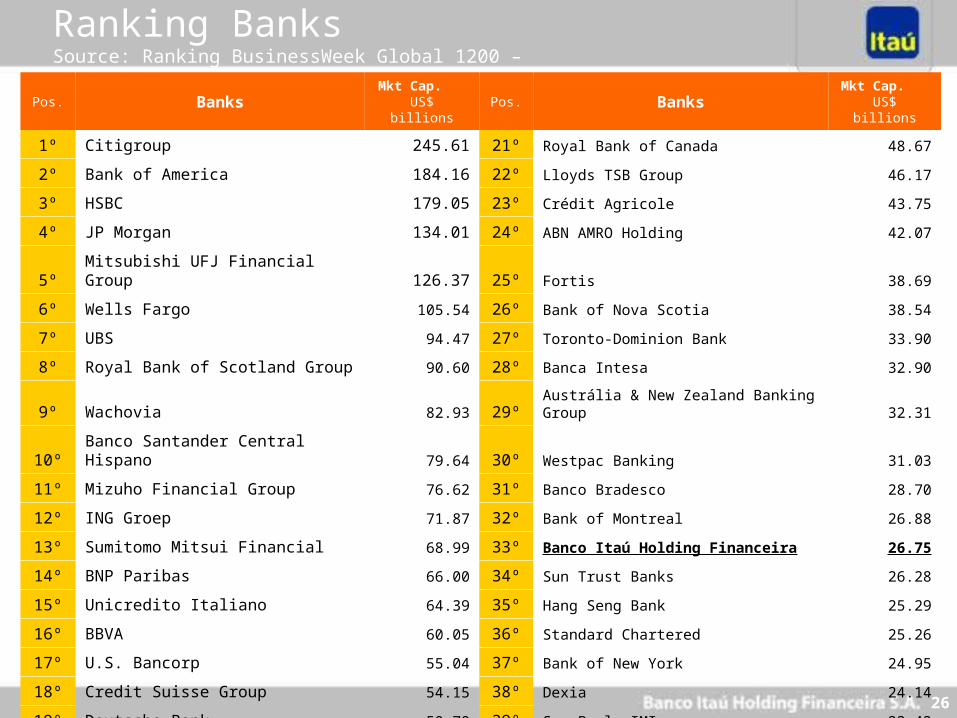

Ranking Banks Source: Ranking BusinessWeek Global 1200 – 12/26/2005

Pos. BanksMkt Cap. US$

billionsPos. Banks

Mkt Cap. US$ billions

1º Citigroup 245.61 21º Royal Bank of Canada 48.67

2º Bank of America 184.16 22º Lloyds TSB Group 46.17

3º HSBC 179.05 23º Crédit Agricole 43.75

4º JP Morgan 134.01 24º ABN AMRO Holding 42.07

5º Mitsubishi UFJ Financial Group 126.37 25º Fortis 38.69

6º Wells Fargo 105.54 26º Bank of Nova Scotia 38.54

7º UBS 94.47 27º Toronto-Dominion Bank 33.90

8º Royal Bank of Scotland Group 90.60 28º Banca Intesa 32.90

9º Wachovia 82.93 29º Austrália & New Zealand Banking Group 32.31

10º Banco Santander Central Hispano 79.64 30º Westpac Banking 31.03

11º Mizuho Financial Group 76.62 31º Banco Bradesco 28.70

12º ING Groep 71.87 32º Bank of Montreal 26.88

13º Sumitomo Mitsui Financial 68.99 33º Banco Itaú Holding Financeira 26.75

14º BNP Paribas 66.00 34º Sun Trust Banks 26.28

15º Unicredito Italiano 64.39 35º Hang Seng Bank 25.29

16º BBVA 60.05 36º Standard Chartered 25.26

17º U.S. Bancorp 55.04 37º Bank of New York 24.95

18º Credit Suisse Group 54.15 38º Dexia 24.14

19º Deutsche Bank 50.70 39º San Paolo-IMI 22.42

20º Société Générale 49.44 40º Canadian Imperial Bank of Commerce 22.36

27

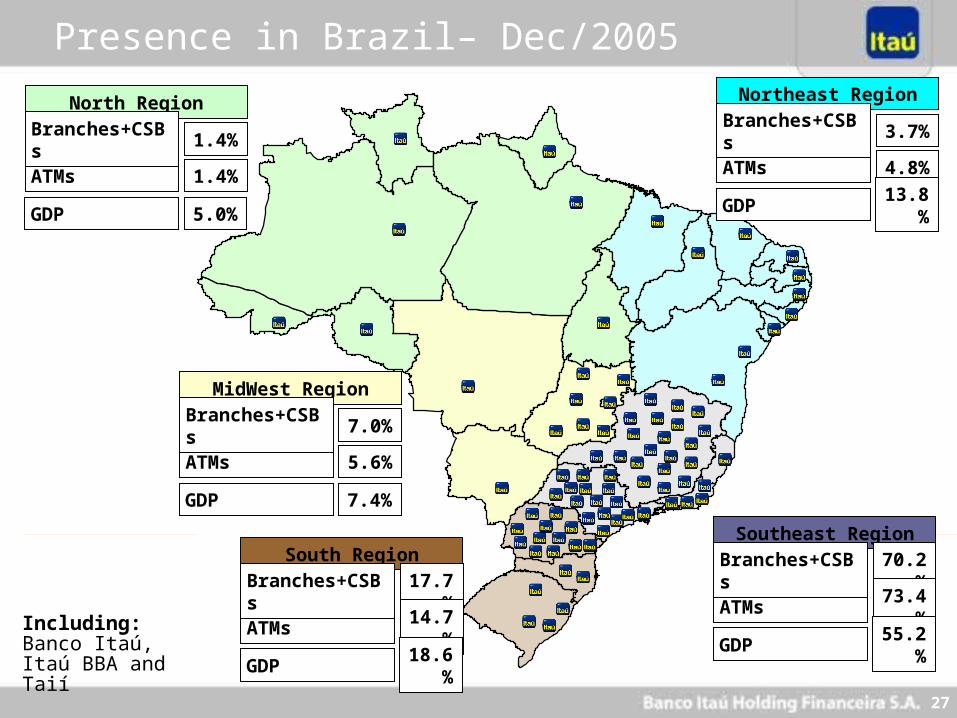

Presence in Brazil– Dec/2005

Including: Banco Itaú, Itaú BBA and Taií

ATMs

North Region

Branches+CSBs 1.4%

1.4%

GDP 5.0%

ATMs

MidWest Region

Branches+CSBs 7.0%

5.6%

GDP 7.4%

ATMs

South Region

Branches+CSBs 17.7%

14.7%

GDP 18.6%

ATMs

Southeast Region

Branches+CSBs 70.2%

73.4%

GDP 55.2%

ATMs

Northeast Region

Branches+CSBs 3.7%

4.8%

GDP 13.8%

28

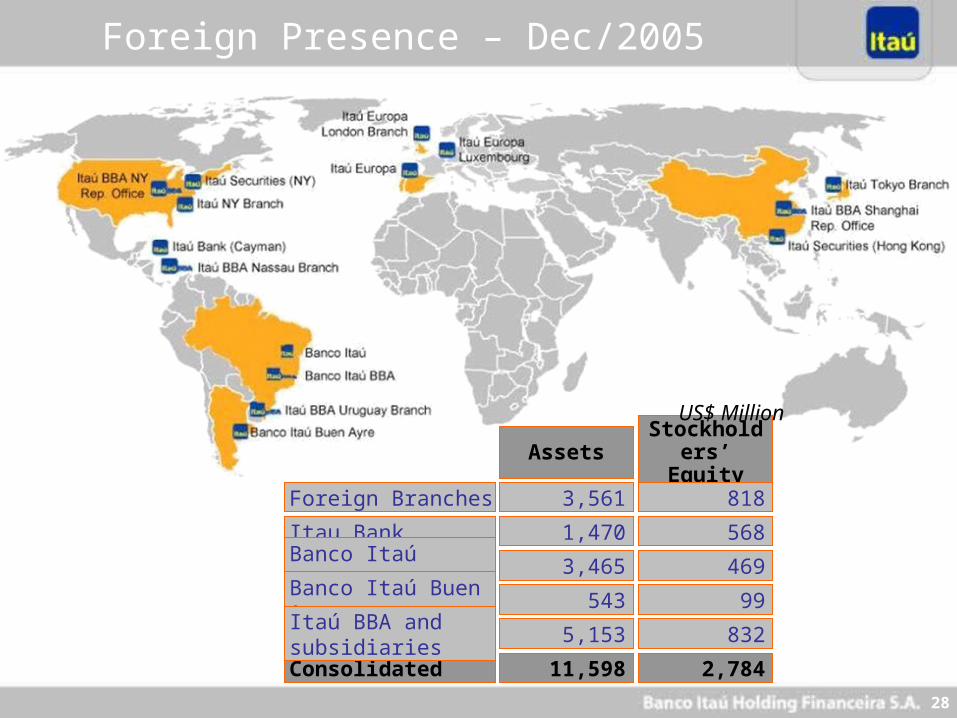

Foreign Presence – Dec/2005

Itau Bank 1,470 568

Banco Itaú Europa 3,465 469

Consolidated 11,598 2,784

Assets Stockholders’ Equity

Foreign Branches 3,561 818

Banco Itaú Buen Ayre 543 99

Itaú BBA and subsidiaries 5,153 832

US$ Million

29

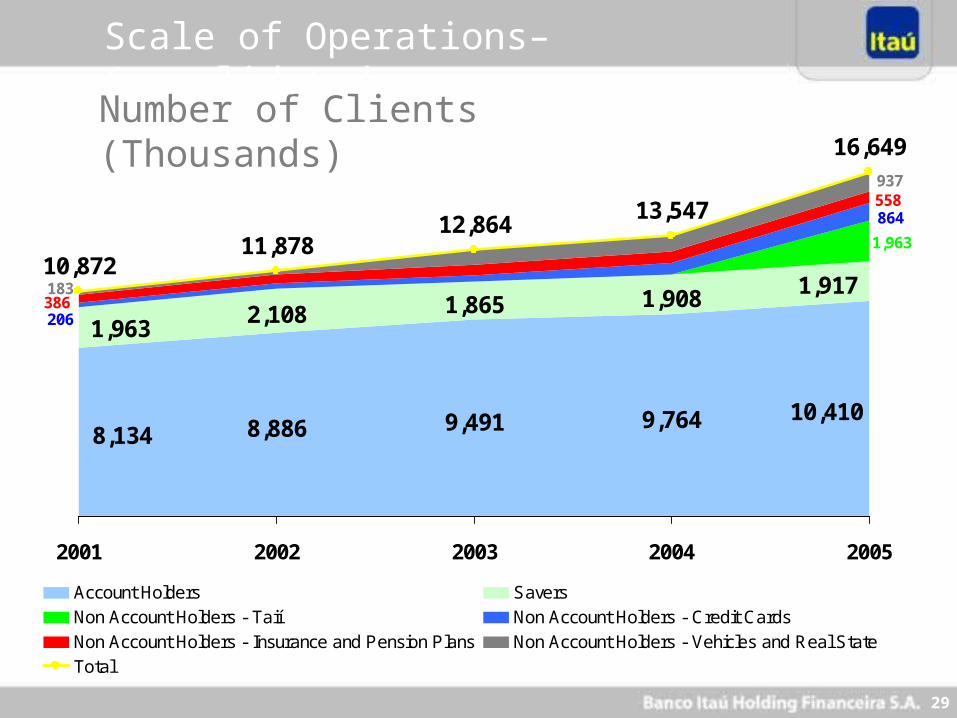

Number of Clients (Thousands)

Scale of Operations– Consolidated

8,886 9,491 9,764

2,108 1,865 1,908

10,4108,134

1,917

1,963

1,963

864

206

558

386

937

183

11,87812,864

13,547

16,649

10,872

2001 2002 2003 2004 2005

Account Holders Savers

Non Account Holders - Taií Non Account Holders - Credit Cards

Non Account Holders - Insurance and Pension Plans Non Account Holders - Vehicles and Real State

Total

30

Agenda

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

31

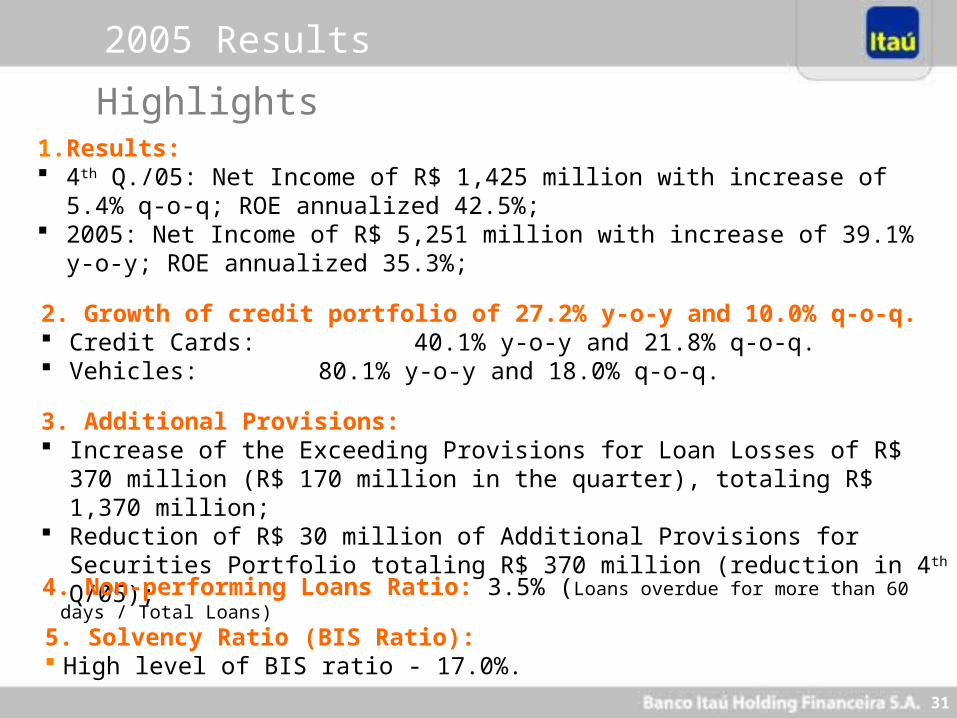

Highlights

3. Additional Provisions: Increase of the Exceeding Provisions for Loan Losses of R$ 370 million (R$ 170

million in the quarter), totaling R$ 1,370 million; Reduction of R$ 30 million of Additional Provisions for Securities Portfolio totaling

R$ 370 million (reduction in 4th Q/05);

1. Results: 4th Q./05: Net Income of R$ 1,425 million with increase of 5.4% q-o-q; ROE

annualized 42.5%; 2005: Net Income of R$ 5,251 million with increase of 39.1% y-o-y; ROE

annualized 35.3%;

4. Non-performing Loans Ratio: 3.5% (Loans overdue for more than 60 days / Total Loans)

2. Growth of credit portfolio of 27.2% y-o-y and 10.0% q-o-q. Credit Cards: 40.1% y-o-y and 21.8% q-o-q. Vehicles: 80.1% y-o-y and 18.0% q-o-q.

5. Solvency Ratio (BIS Ratio): High level of BIS ratio - 17.0%.

2005 Results

32

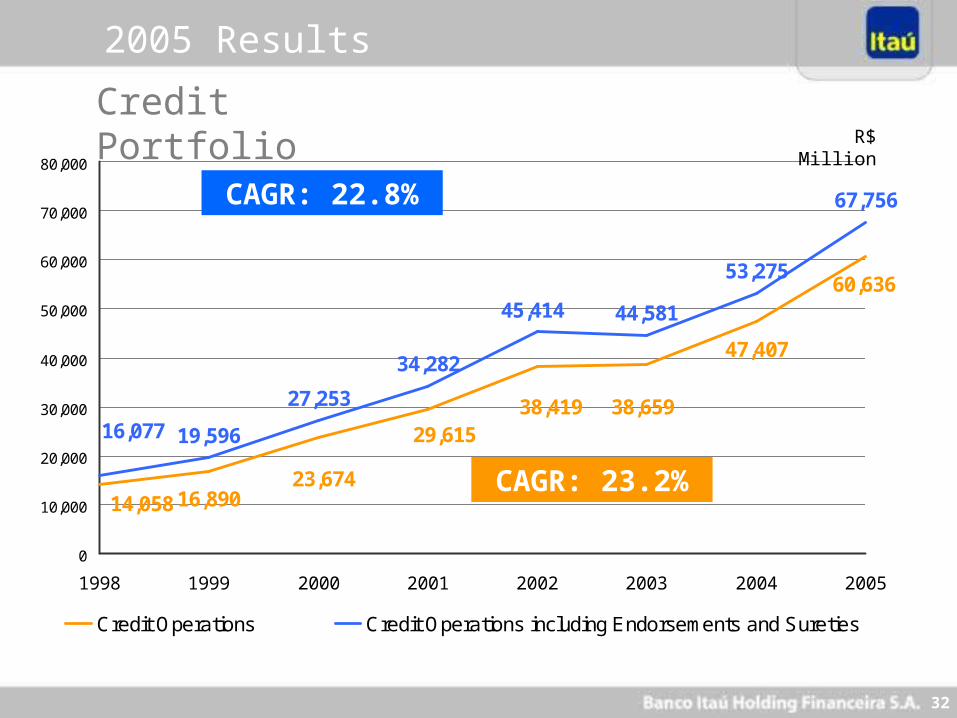

16,890

47,407

60,636

19,596

27,253

34,282

44,581

53,275

67,756

38,419 38,65929,615

23,67414,058

16,077

45,414

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1998 1999 2000 2001 2002 2003 2004 2005

Credit Operations Credit Operations including Endorsements and Sureties

CAGR: 22.8%

CAGR: 23.2%

R$ Million

Credit Portfolio

2005 Results

33

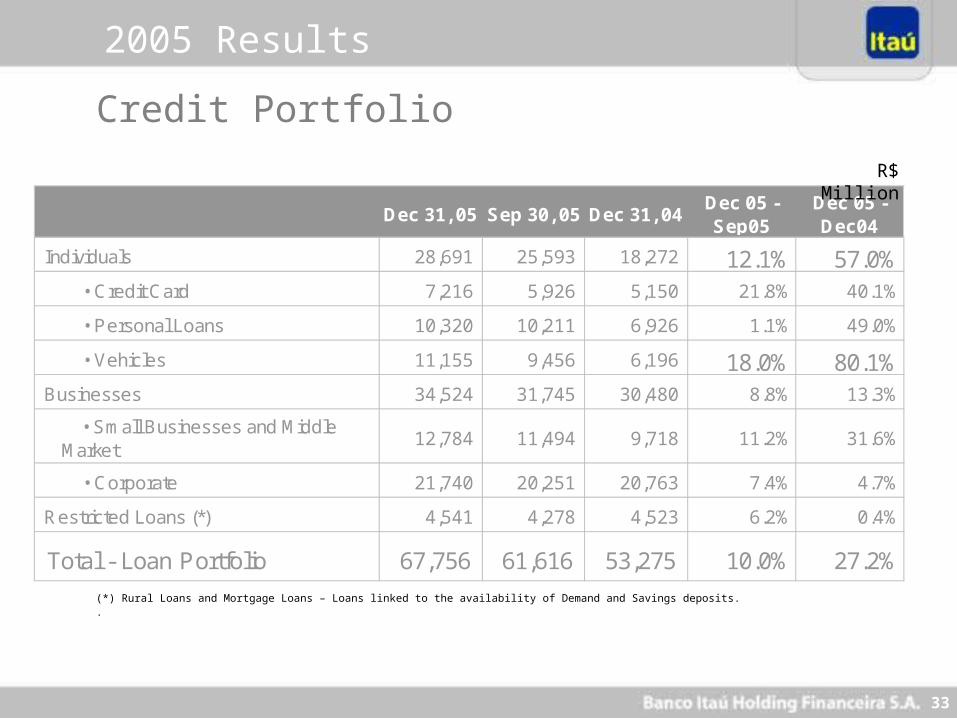

Dec 31, 05 Sep 30, 05 Dec 31, 04Dec 05 - Sep05

Dec 05 - Dec04

Individuals 28,691 25,593 18,272 12.1% 57.0% • Credit Card 7,216 5,926 5,150 21.8% 40.1%

• Personal Loans 10,320 10,211 6,926 1.1% 49.0%

• Vehicles 11,155 9,456 6,196 18.0% 80.1%Businesses 34,524 31,745 30,480 8.8% 13.3%

• Small Businesses and Middle Market

12,784 11,494 9,718 11.2% 31.6%

• Corporate 21,740 20,251 20,763 7.4% 4.7%

Restricted Loans (*) 4,541 4,278 4,523 6.2% 0.4%

Total - Loan Portfolio 67,756 61,616 53,275 10.0% 27.2%

(*) Rural Loans and Mortgage Loans – Loans linked to the availability of Demand and Savings deposits..

Credit Portfolio

R$ Million

2005 Results

34

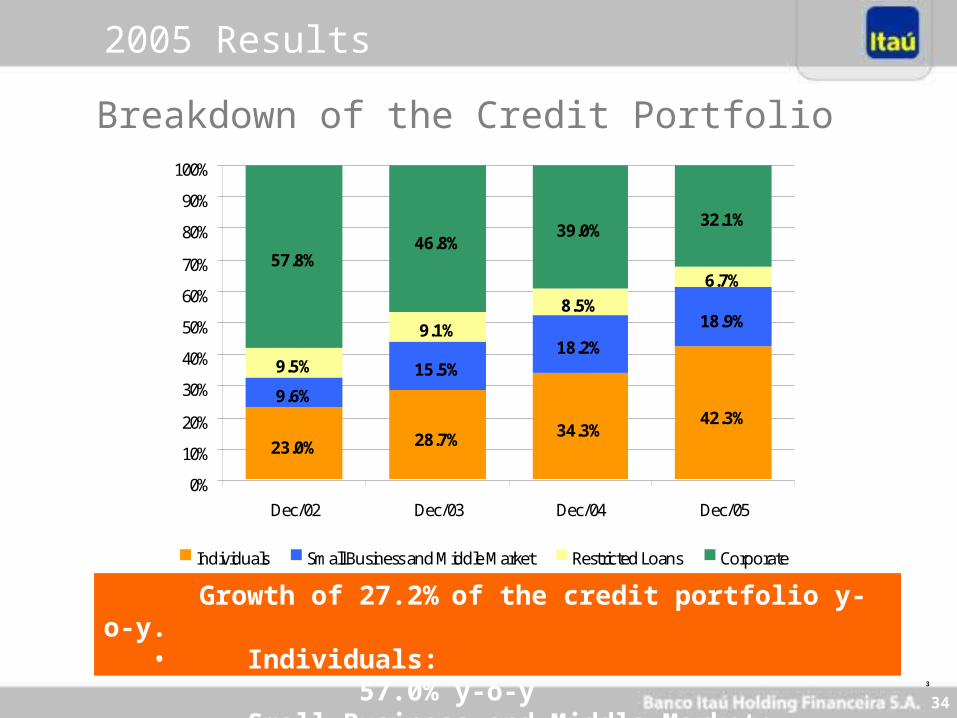

Growth of 27.2% of the credit portfolio y-o-y.• Individuals: 57.0% y-o-y• Small Business and Middle Market: 31.6% y-o-y

Breakdown of the Credit Portfolio

3

23.0% 28.7% 34.3%42.3%

9.6%

15.5%18.2%

18.9%

9.5%

9.1%

8.5%

57.8%46.8%

39.0%32.1%

6.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec/02 Dec/03 Dec/04 Dec/05

Individuals Small Business and Middle Market Restricted Loans Corporate

2005 Results

35

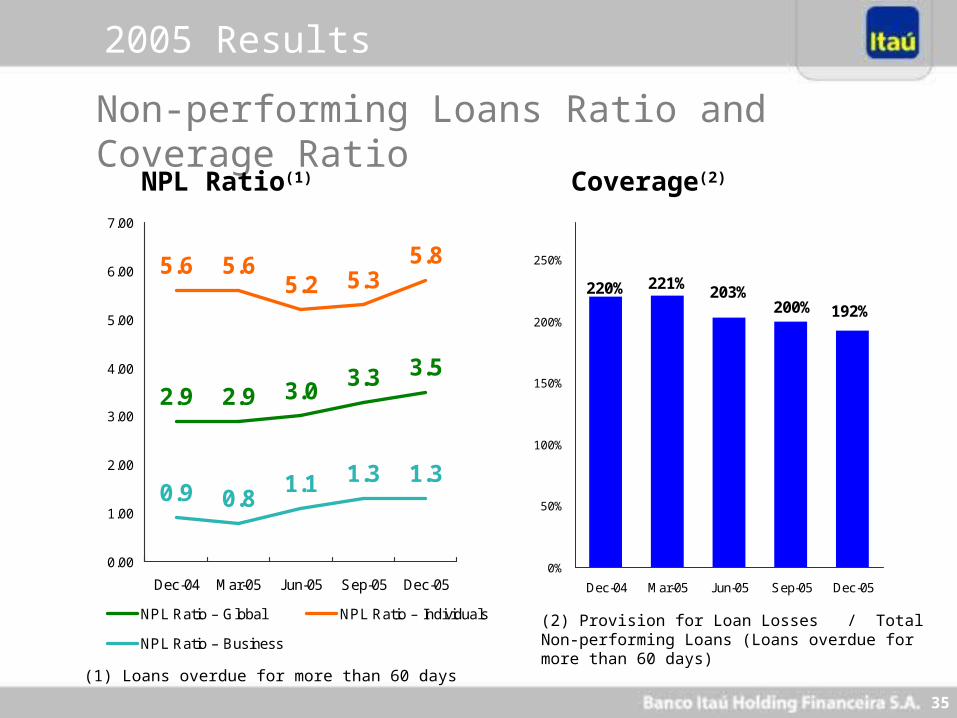

3.53.33.02.92.9

5.6 5.6 5.85.2 5.3

0.9 0.81.1 1.3 1.3

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Dec-04 Mar-05 Jun-05 Sep-05 Dec-05

NPL Ratio – Global NPL Ratio – Individuals

NPL Ratio – Business

192%200%203%

221%220%

0%

50%

100%

150%

200%

250%

Dec-04 Mar-05 Jun-05 Sep-05 Dec-05

Non-performing Loans Ratio and Coverage Ratio

NPL Ratio(1) Coverage(2)

(2) Provision for Loan Losses / Total Non-performing Loans (Loans overdue for more than 60 days)

(1) Loans overdue for more than 60 days

2005 Results

36

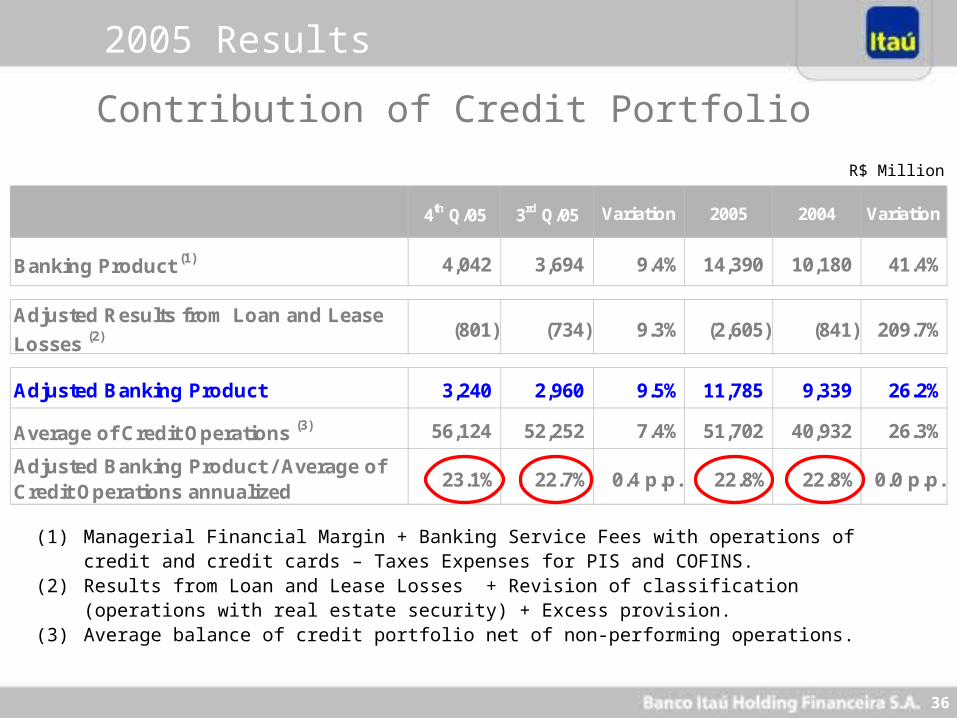

4th Q/05 3rd Q/05 Variation 2005 2004 Variation

Banking Product (1) 4,042 3,694 9.4% 14,390 10,180 41.4%

Adjusted Results from Loan and Lease

Losses (2) (801) (734) 9.3% (2,605) (841) 209.7%

Adjusted Banking Product 3,240 2,960 9.5% 11,785 9,339 26.2%

Average of Credit Operations (3) 56,124 52,252 7.4% 51,702 40,932 26.3%

Adjusted Banking Product / Average of Credit Operations annualized

23.1% 22.7% 0.4 p.p. 22.8% 22.8% 0.0 p.p.

R$ Million

Contribution of Credit Portfolio

(1) Managerial Financial Margin + Banking Service Fees with operations of credit and credit cards – Taxes Expenses for PIS and COFINS.

(2) Results from Loan and Lease Losses + Revision of classification (operations with real estate security) + Excess provision.

(3) Average balance of credit portfolio net of non-performing operations.

2005 Results

37

R$ Million

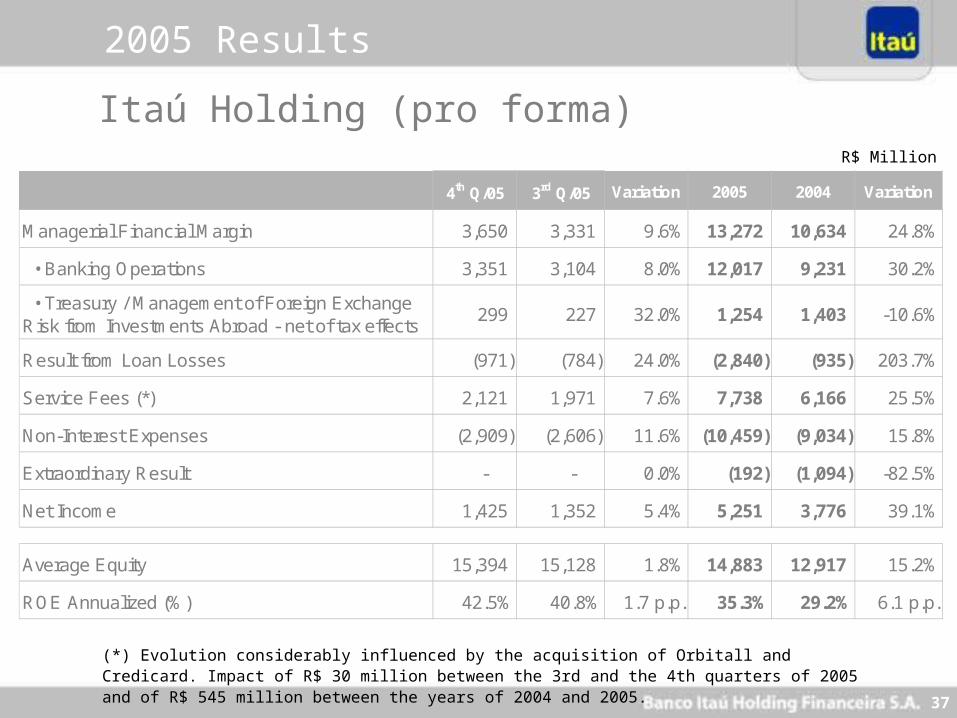

Itaú Holding (pro forma)

(*) Evolution considerably influenced by the acquisition of Orbitall and Credicard. Impact of R$ 30 million between the 3rd and the 4th quarters of 2005 and of R$ 545 million between the years of 2004 and 2005.

4th Q/05 3rd Q/05 Variation 2005 2004 Variation

Managerial Financial Margin 3,650 3,331 9.6% 13,272 10,634 24.8%

• Banking Operations 3,351 3,104 8.0% 12,017 9,231 30.2%

• Treasury / Management of Foreign Exchange Risk from Investments Abroad - net of tax effects

299 227 32.0% 1,254 1,403 -10.6%

Result from Loan Losses (971) (784) 24.0% (2,840) (935) 203.7%

Service Fees (*) 2,121 1,971 7.6% 7,738 6,166 25.5%

Non-Interest Expenses (2,909) (2,606) 11.6% (10,459) (9,034) 15.8%

Extraordinary Result - - 0.0% (192) (1,094) -82.5%

Net Income 1,425 1,352 5.4% 5,251 3,776 39.1%

Average Equity 15,394 15,128 1.8% 14,883 12,917 15.2%

ROE Annualized (%) 42.5% 40.8% 1.7 p.p. 35.3% 29.2% 6.1 p.p.

2005 Results

38

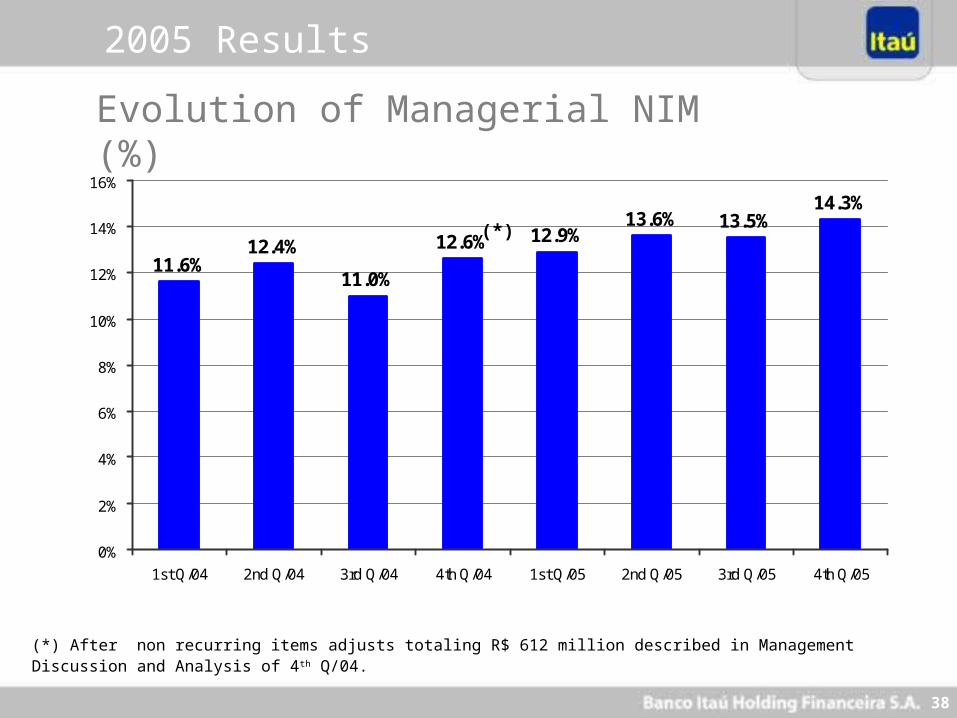

Evolution of Managerial NIM (%)

12.4%13.5%

14.3%

11.6%11.0%

12.6%13.6%

12.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1st Q/04 2nd Q/04 3rd Q/04 4th Q/04 1st Q/05 2nd Q/05 3rd Q/05 4th Q/05

(*)

(*) After non recurring items adjusts totaling R$ 612 million described in Management Discussion and Analysis of 4 th Q/04.

2005 Results

39

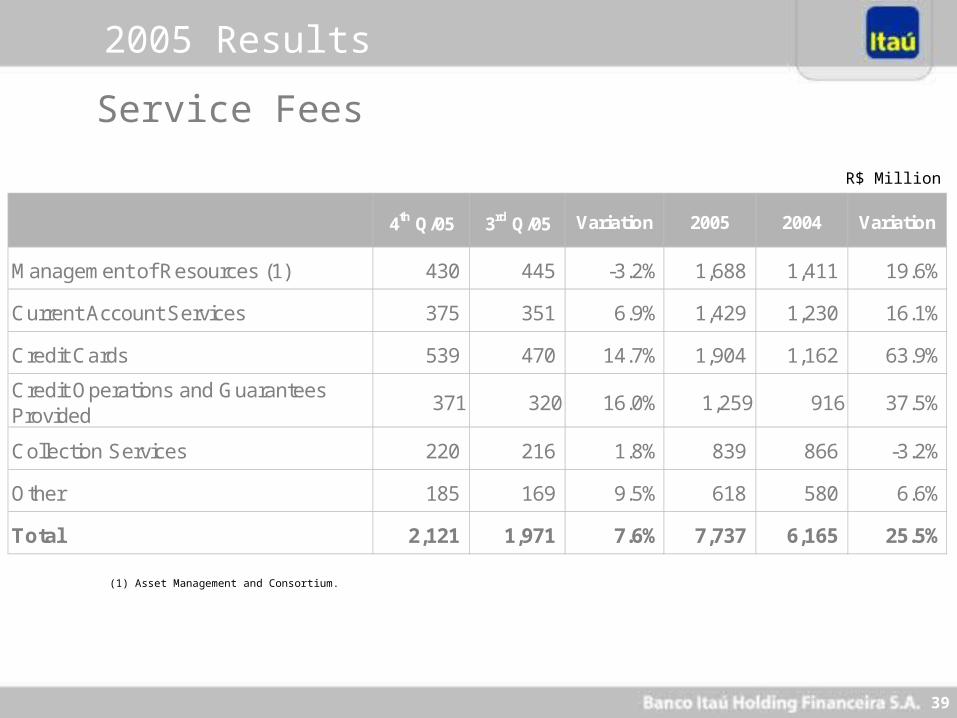

R$ Million

(1) Asset Management and Consortium.

Service Fees

4th Q/05 3rd Q/05 Variation 2005 2004 Variation

Management of Resources (1) 430 445 -3.2% 1,688 1,411 19.6%

Current Account Services 375 351 6.9% 1,429 1,230 16.1%

Credit Cards 539 470 14.7% 1,904 1,162 63.9%

Credit Operations and Guarantees Provided

371 320 16.0% 1,259 916 37.5%

Collection Services 220 216 1.8% 839 866 -3.2%

Other 185 169 9.5% 618 580 6.6%

Total 2,121 1,971 7.6% 7,737 6,165 25.5%

2005 Results

40

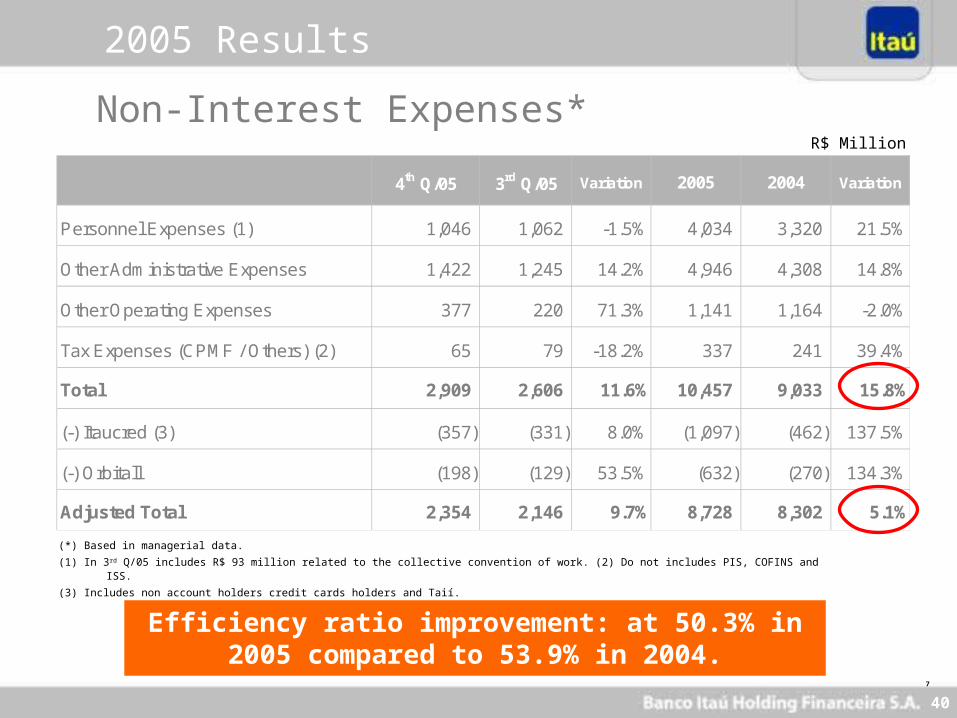

4th Q/05 3rd Q/05 Variation 2005 2004 Variation

Personnel Expenses (1) 1,046 1,062 -1.5% 4,034 3,320 21.5%

Other Administrative Expenses 1,422 1,245 14.2% 4,946 4,308 14.8%

Other Operating Expenses 377 220 71.3% 1,141 1,164 -2.0%

Tax Expenses (CPMF / Others) (2) 65 79 -18.2% 337 241 39.4%

Total 2,909 2,606 11.6% 10,457 9,033 15.8%

(-) Itaucred (3) (357) (331) 8.0% (1,097) (462) 137.5%

(-) Orbitall (198) (129) 53.5% (632) (270) 134.3%

Adjusted Total 2,354 2,146 9.7% 8,728 8,302 5.1%

R$ Million

(*) Based in managerial data.

(1) In 3rd Q/05 includes R$ 93 million related to the collective convention of work. (2) Do not includes PIS, COFINS and ISS.

(3) Includes non account holders credit cards holders and Taií.

Non-Interest Expenses*

Efficiency ratio improvement: at 50.3% in 2005 compared to 53.9% in 2004.

7

2005 Results

41

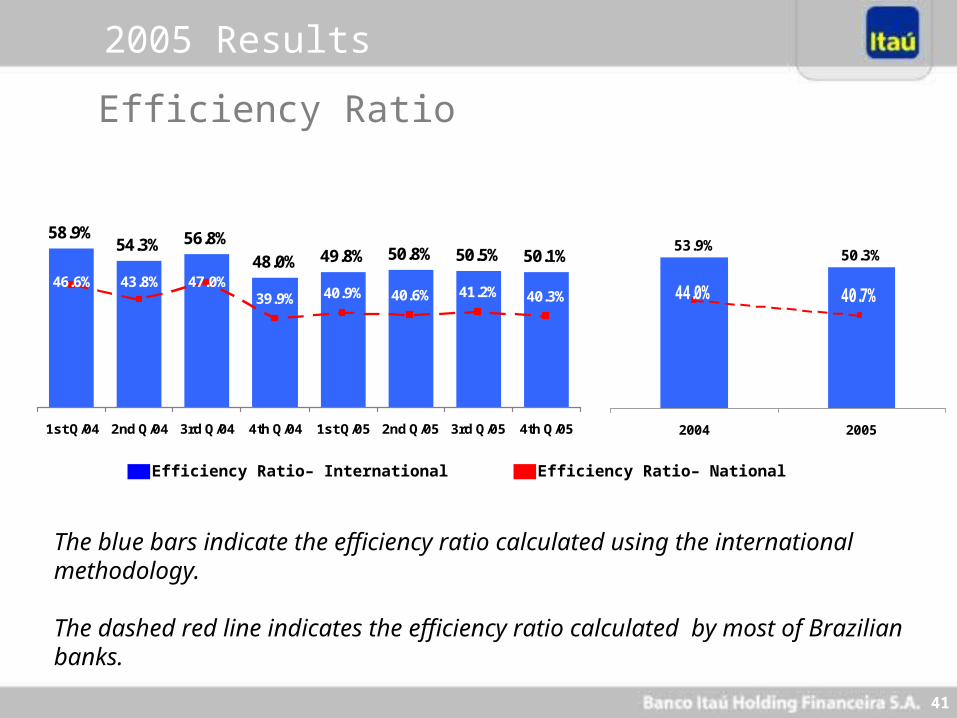

53.9%50.3%

2004 2005

44.0% 40.7%

58.9%54.3% 56.8%

48.0% 49.8% 50.8% 50.5% 50.1%

1st Q/04 2nd Q/04 3rd Q/04 4th Q/04 1st Q/05 2nd Q/05 3rd Q/05 4th Q/05

46.6% 43.8% 47.0%39.9% 41.2% 40.3%40.6%40.9%

Efficiency Ratio– International

Efficiency Ratio

The blue bars indicate the efficiency ratio calculated using the international methodology.

The dashed red line indicates the efficiency ratio calculated by most of Brazilian banks.

Efficiency Ratio– National

2005 Results

42

(*) Values differ from the one published in note “Market Value” because they are net of the additional provision for securities.

Conservative Accounting Practices

SecuritiesAdjust. market value

Additional Provision

Total

Additional Provision for Loan Losses (PDD)

Financial Instruments: Market vs. Recorded Value(*)

R$ 435 million

R$ 370 million

R$ 3,6 billion

12/31/05

R$ 1,37 billion

R$ 1,4 billion

R$ 733 million

R$ 400 million

R$ 3,8 billion

12/31/04

R$ 1,0 billion

R$ 1,67 billion

R$ 758 million

R$ 545 million

R$ 3,7 billion

12/31/03

R$ 906 million

R$ 1,5 billion

2005 Results

43

Agenda

Brazilian Economy

Brazilian Banking System

Highlights Itaú

Itaú´s Positioning

2005 Results

Strategy

44

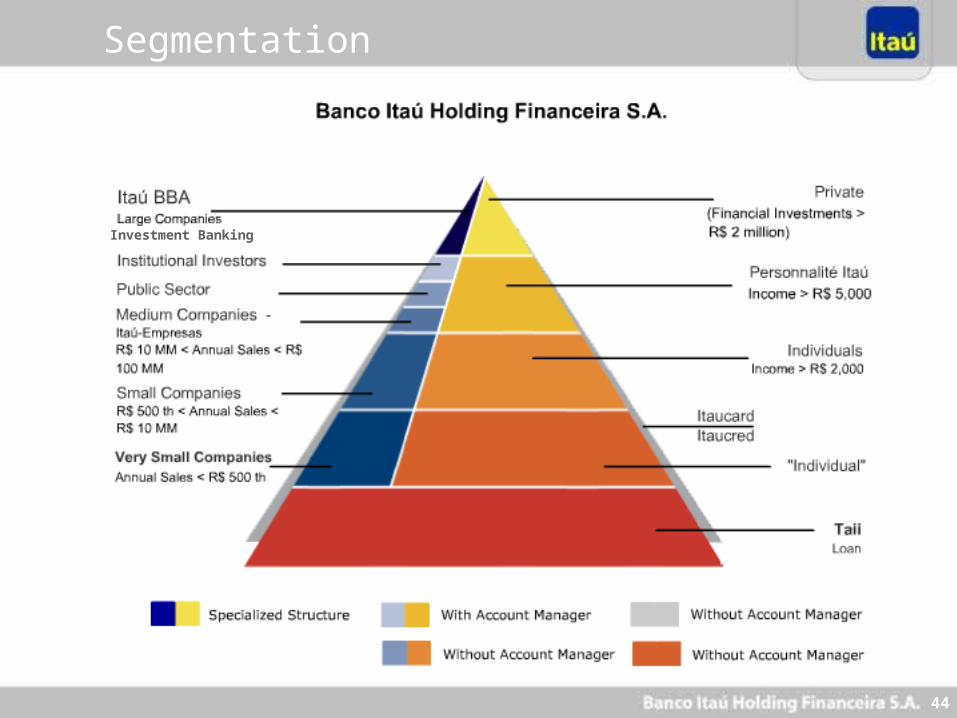

Segmentation

Investment Banking

45

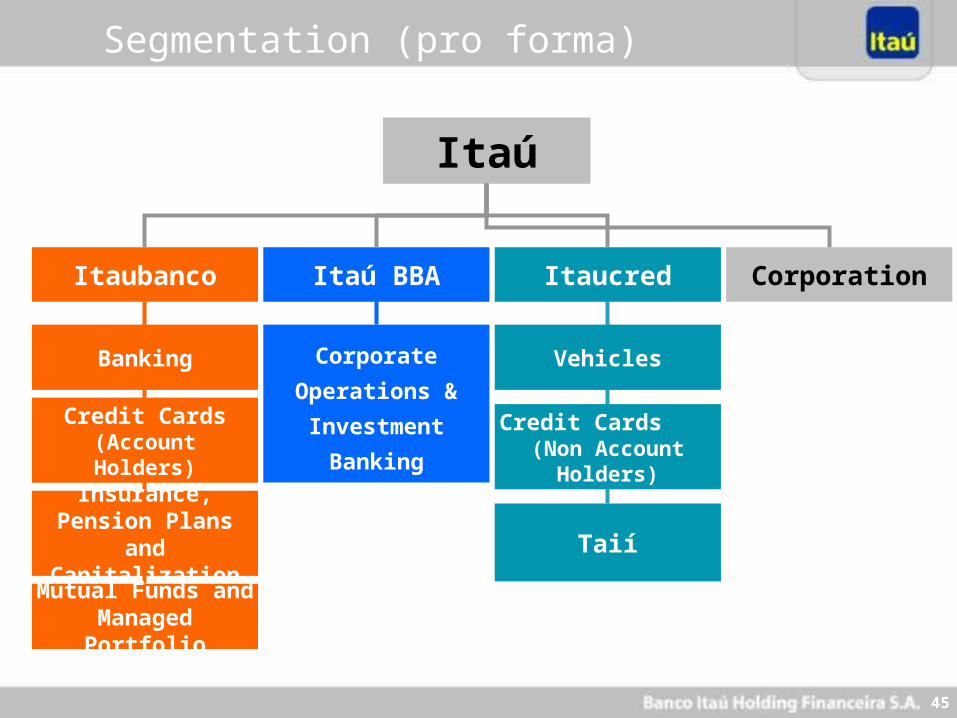

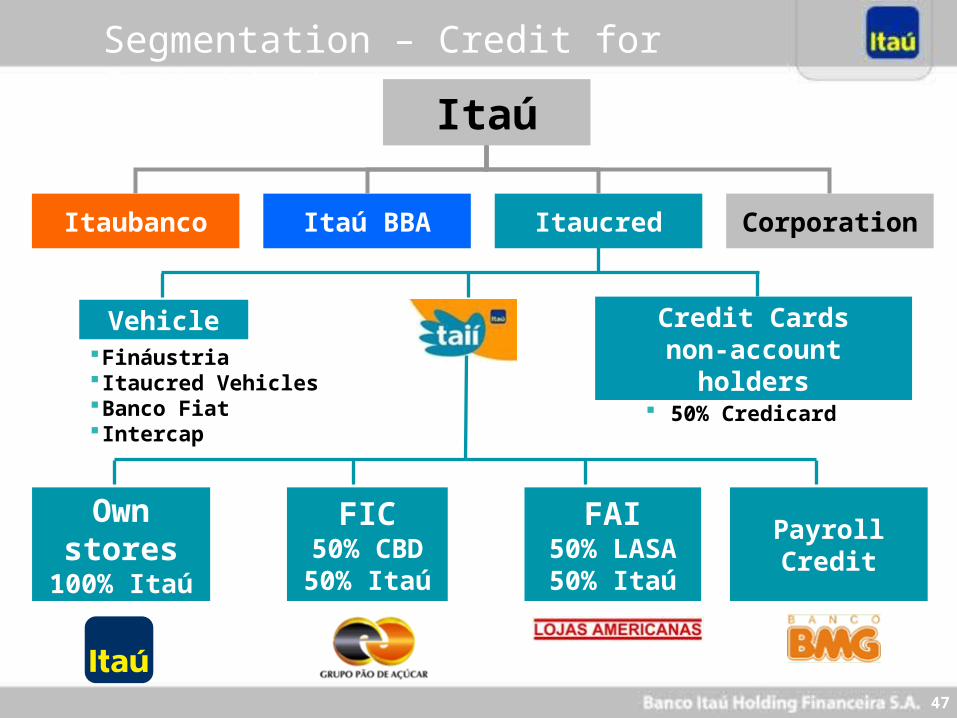

Itaú

ItaucredItaú BBAItaubanco

Banking

Credit Cards (Account Holders)

Insurance, Pension Plans

and CapitalizationMutual Funds and Managed

Portfolio

Corporation

Corporate

Operations &

Investment

Banking

Vehicles

Credit Cards (Non Account

Holders)

Taií

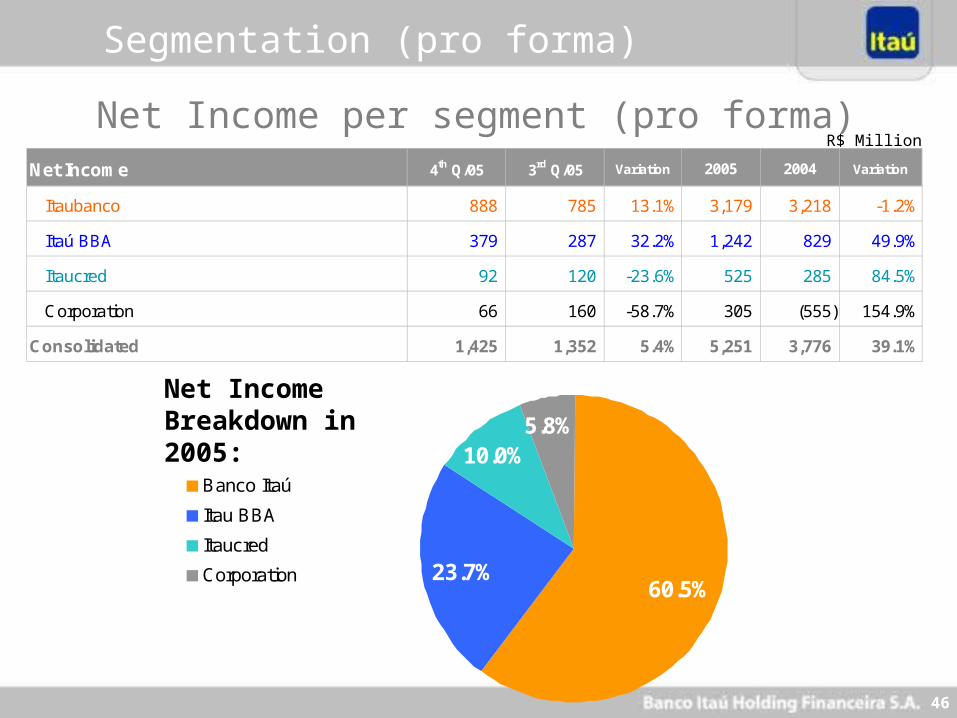

Segmentation (pro forma)

46

Net Income 4th Q/05 3rd Q/05 Variation 2005 2004 Variation

Itaubanco 888 785 13.1% 3,179 3,218 -1.2%

Itaú BBA 379 287 32.2% 1,242 829 49.9%

Itaucred 92 120 -23.6% 525 285 84.5%

Corporation 66 160 -58.7% 305 (555) 154.9%

Consolidated 1,425 1,352 5.4% 5,251 3,776 39.1%

R$ MillionNet Income per segment (pro forma)

23.7%

10.0%5.8%

60.5%

Banco Itaú

Itau BBA

Itaucred

Corporation

Net Income Breakdown in 2005:

Segmentation (pro forma)

47

Itaú

CorporationItaucredItaú BBAItaubanco

FIC50% CBD50% Itaú

FAI50% LASA50% Itaú

Own stores

100% Itaú

Payroll Credit

FináustriaItaucred VehiclesBanco FiatIntercap

Vehicle Credit Cardsnon-account

holders 50% Credicard

Segmentation – Credit for Individuals

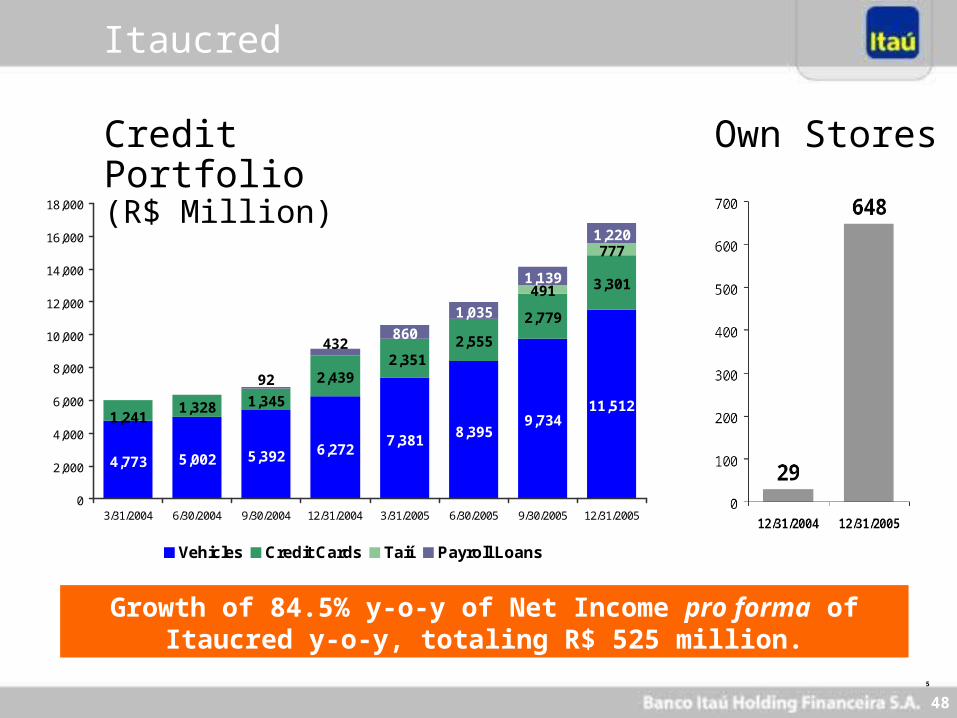

48

5,002

9,73411,5121,328 1,345

2,439

2,555

2,779

3,301491

777

860

1,035

1,139

1,220

4,773 5,392 6,2728,395

7,381

2,351

1,241

92

432

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

3/31/2004 6/30/2004 9/30/2004 12/31/2004 3/31/2005 6/30/2005 9/30/2005 12/31/2005

Vehicles Credit Cards Taií Payroll Loans

Growth of 84.5% y-o-y of Net Income pro forma of Itaucred y-o-y, totaling R$ 525 million.

Credit Portfolio (R$ Million)

Own Stores

5

Itaucred

49

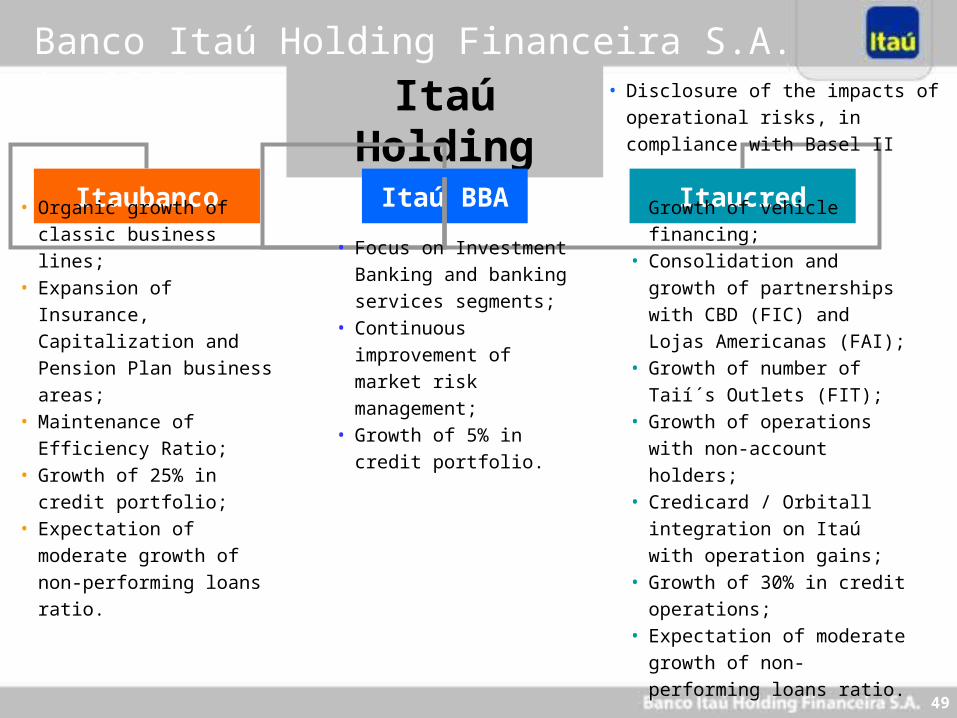

Itaú Holding

ItaucredItaú BBAItaubanco

• Organic growth of classic

business lines;• Expansion of Insurance,

Capitalization and Pension

Plan business areas;• Maintenance of Efficiency

Ratio;• Growth of 25% in credit

portfolio; • Expectation of moderate

growth of non-performing

loans ratio.

• Focus on Investment

Banking and banking

services segments;• Continuous improvement

of market risk

management;• Growth of 5% in credit

portfolio.

• Growth of vehicle financing;• Consolidation and growth of

partnerships with CBD (FIC)

and Lojas Americanas (FAI);• Growth of number of Taií´s

Outlets (FIT);• Growth of operations with non-

account holders;• Credicard / Orbitall integration

on Itaú with operation gains;• Growth of 30% in credit

operations;• Expectation of moderate

growth of non-performing loans

ratio.

• Disclosure of the impacts of operational

risks, in compliance with Basel II

Banco Itaú Holding Financeira S.A. in 2006

50

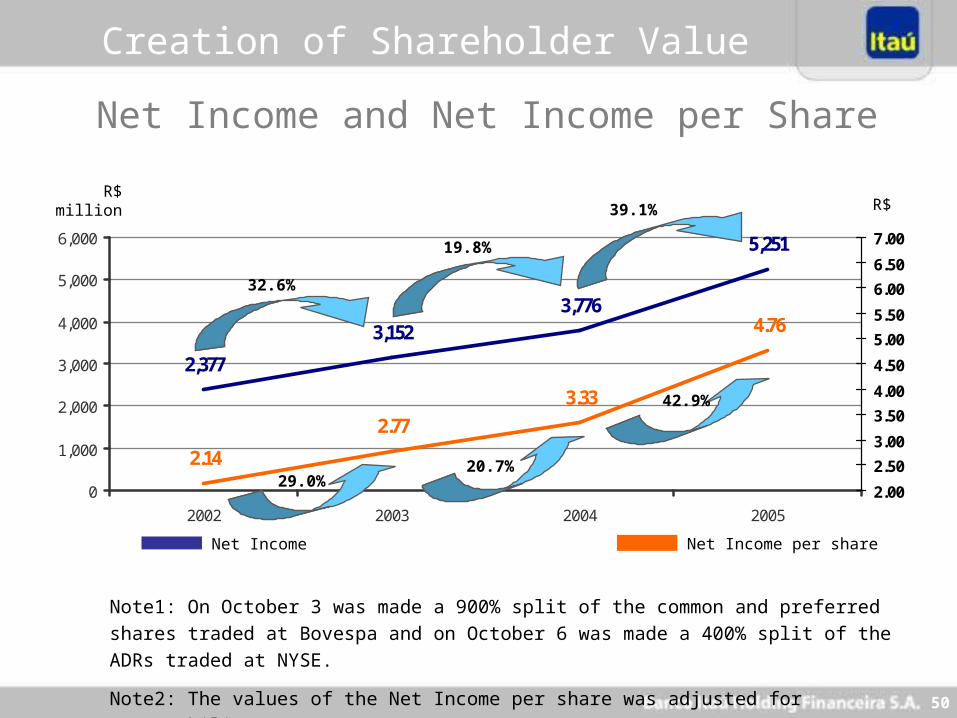

R$

3,1523,776

5,251

2,377

3.33

4.76

2.77

2.14

0

1,000

2,000

3,000

4,000

5,000

6,000

2002 2003 2004 2005

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

Net Income per shareNet Income

R$ million

Note1: On October 3 was made a 900% split of the common and preferred shares traded at

Bovespa and on October 6 was made a 400% split of the ADRs traded at NYSE.

Note2: The values of the Net Income per share was adjusted for comparability purposes.

Net Income and Net Income per Share

19.8%

39.1%

20.7%

42.9%

29.0%

32.6%

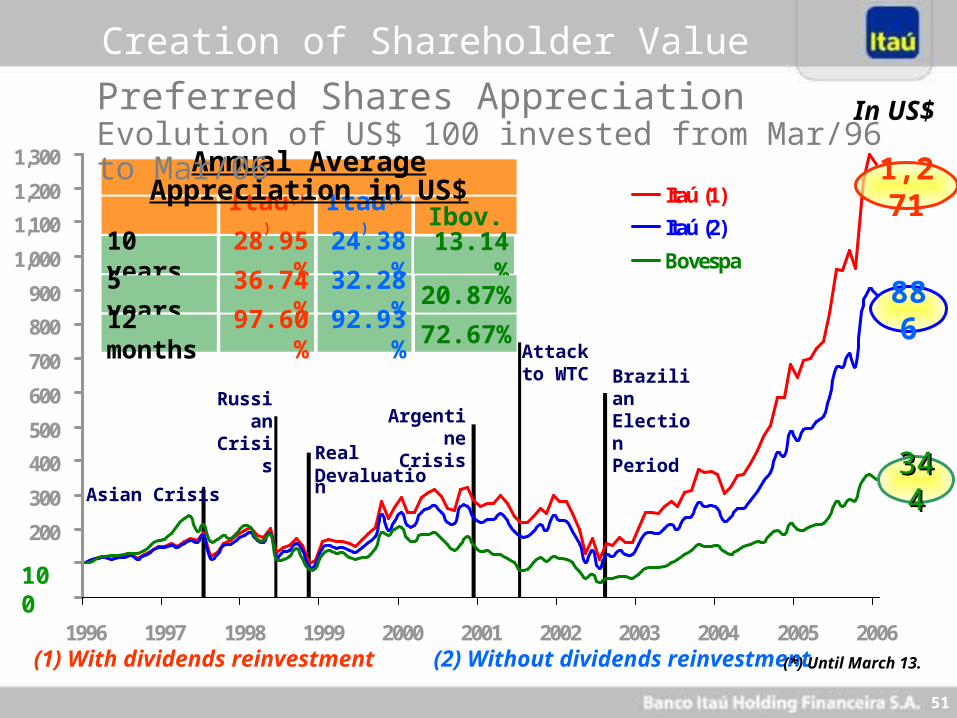

Creation of Shareholder Value

51

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Itaú (1)

Itaú (2)

Bovespa

In US$

100

Itaú(1) Itaú(2) Ibov.

10 years 28.95% 24.38% 13.14%

5 years 36.74% 32.28% 20.87%

12 months 97.60% 92.93% 72.67%

Annual Average Appreciation in US$

Preferred Shares AppreciationEvolution of US$ 100 invested from Mar/96 to Mar/06

Asian Crisis

Russian Crisis

Real Devaluation

Argentine Crisis

Attack to WTC

Brazilian Election Period

(1) With dividends reinvestment (2) Without dividends reinvestment

Creation of Shareholder Value

886

344344

1,271

(*) Until March 13.

March 2006

Silvio de CarvalhoExecutive Director

Roadshow

Related Documents