Manchester Monitor Quarterly Decline in unemployment continues Increase in business start-ups Service sector expected to drive growth Visitor economy buoyant House prices on the rise Crime volumes increase www.neweconomymanchester.com [email protected] January 2015 Forecasting Greater Manchester’s Future Prospects

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Manchester Monitor Quarterly

Decline in unemployment continues

Increase in business start-ups

Service sector expected to drive growth

Visitor economy buoyant

House prices on the rise

Crime volumes increase

January 2015

Forecasting Greater Manchester’s

Future Prospects

1 | Manchester Monitor – January 2015

This issue of the Manchester Monitor Quarterly includes a

detailed feature on the latest results from the 2014 edition

of the Greater Manchester Forecasting Model (GMFM). The

focus is on which sectors are expected to lead Greater

Manchester’s (GM) employment growth over the next

decade, which industries will contribute towards increased

economic output and how the conurbation’s occupational

structure will change up to 2024.

From an employment perspective, business, financial &

professional services and the cultural & creative industries

are expected to be the largest contributors to jobs growth in

GM over the next decade – with almost 88,000 new

opportunities being created in the these sectors. The long-

term decline in manufacturing employment is still evident,

although manufacturing’s contribution towards economic

output is expected to grow considerably up to 2024 as the

sector becomes ever more productive in order to remain

globally competitive. Analysis of GM’s sector specialisation

reveals that it is performing well in traditional industries, and

also in a number of sub-sectors associated with business,

financial and professional services.

The latest Business Demography dataset released by the

Office for National Statistics (ONS) shows there was a sharp

rise in the number of start-ups in GM between 2012 and

2013. There were 14,705 new businesses started in GM in

2013, a substantial increase of 3,850 (35.5%) on the 10,855

business births in 2012. Business deaths in GM were

recorded at 10,005 in 2013, an annual decline of 510 (4.9%).

For the third year in succession, the number of births

exceeded the number of deaths and this means that net

change in GM in 2013 was 4,700. GM’s business start-up

rate has increased over time. In 2013 there were 84 new

business starts per 10,000 resident working age population,

up from 55 in 2009. The 2013 figure was also virtually in line

with the UK average of 85 new starts per 10,000 working

age residents.

Turning to look at the regular data on the labour market, the

latest unemployment figures from the Department for Work

and Pensions (DWP) show further reductions in the number

of people claiming Jobseeker’s Allowance (JSA) in GM.

Current JSA data show that around 38,100 people – or 2.2%

of the working age population – were claiming JSA in GM in

November 2014. This represents a decrease of 27,300

(41.7%) when compared with the figure 12 months

previously. Looking at a combined estimate for both JSA and

Universal Credit (UC) claimants, the number of people

claiming JSA or UC in GM in November 2014 was 45,400,

representing an annual decline of 32.9%. This is less than

the 41.7% decline for JSA claimants, although it still

represents a substantial fall over 12 months and highlights

the ongoing economic recovery.

The visitor economy in GM continues to perform well, with

hotel occupancy rates recorded at 83.6% for GM and 87.1%

for Manchester city centre for November 2014. When

December figures are released, they are expected to show

that 2014 was the strongest performing year to date in terms

of occupancy levels. There are also encouraging signs for

2015, with Manchester hosting 40 national and international

conferences that are expected to bring 34,000 delegates to

the city and generate £61million for the local economy.

Manchester Airport handled more than 2 million passengers

in October 2014, 128,200 (6.8%) more than 12 months

previously. With passenger numbers close to reaching 22

million on a rolling 12 month basis, a figure not achieved

since 2007, it was reported in December that the Airport is

aiming to double the annual number of passengers by 2036.

The latest data from the Land Registry show that the average

house in GM cost £108,400 in November 2014, an increase

of 4.5% (£4,600) from this time last year, but slightly below

the annual rise of 7.1% (£11,700) in house prices for England

& Wales. In terms of properties sold, house sales in GM grew

by 16.4% (418) between September 2013 and 2014. This is

proportionally more than in the North West and nationally,

where house sales have risen 10.0% and 5.0% respectively

on an annual basis.

On the crime front, the latest data from GM Police show an

increase of 8.2% (14,800) in the number of reported crimes

in the year ending December 2014, to 194,400 reported

offences. Within this total, victim-based crimes (stealing,

criminal damage & arson, violence and sexual offences) saw

175,200 cases recorded over the same period, representing

an annual increase of 8.3%. The latest figures from GM Fire

& Rescue Service show a 24.3% reduction in the total

volume of deliberate fires in GM for the 12 months to

December 2014.

Monitor FocusForecasting Greater Manchester’s Future Prospects

Manchester Monitor – January 2015 | 2

Monitor Dashboard

Jobseeker’s Allowance (JSA) claimants

41.7%since last year

Number of businesses started in GM in 2013

14,705new jobs forecast to be

created over next ten years

House Prices

4.5%

since November 2013

Airport Passengers

6.8%

since October 2013

Hotel Occupancy

1.0%pts

since November 2013

Crime

8.2%

since December 2013

3 | Manchester Monitor – January 2015

JSA Claimants

Around 2.2% of the resident working age population in GM

were claiming JSA in November. The rate remains marginally

higher than the North West (2.1%) and Great Britain (2.0%).

The number of male JSA claimants in GM fell on a monthly

basis by 8.3% (2,200) to 24,200, and similarly, female

claimants fell by 9.5% (1,500) over the month to 13,900. On

an annual basis both male and female claimants continue to

decrease – down by 18,500 (43.3%) and 8,700 (38.6%)

respectively.

Long-term JSA claimants (6 months+) in GM in November

2014 were 17,400, representing an annual decline of 42.8%

(13,000). This was above the regional (38.8%) and national

falls (36.2%).

Youth unemployment (JSA claimants aged 16-24) in GM fell

on an annual basis between November 2013 and 2014,

decreasing by approximately 8,900 (54.0%) to 7,600.

Universal Credit

Data sourced from the Department for Work and Pensions

(DWP) show that there were 10,400 people claiming UC in

November 2014. These people are not included in JSA

claimant count statistics, meaning that analysing the

unemployment outlook based purely on trends in JSA

claimants may look more flattering than it actually is.

At a UK level, the DWP data show that around 70.0% of

people claiming UC are not in employment. Assuming similar

trend in GM and that these people would otherwise be

claiming JSA in the absence of UC would add 7,300 people

to the JSA figure for GM. This gives a combined JSA/UC

total of over 45,400 in November 2014.

People MonitorDecline in unemployment continues

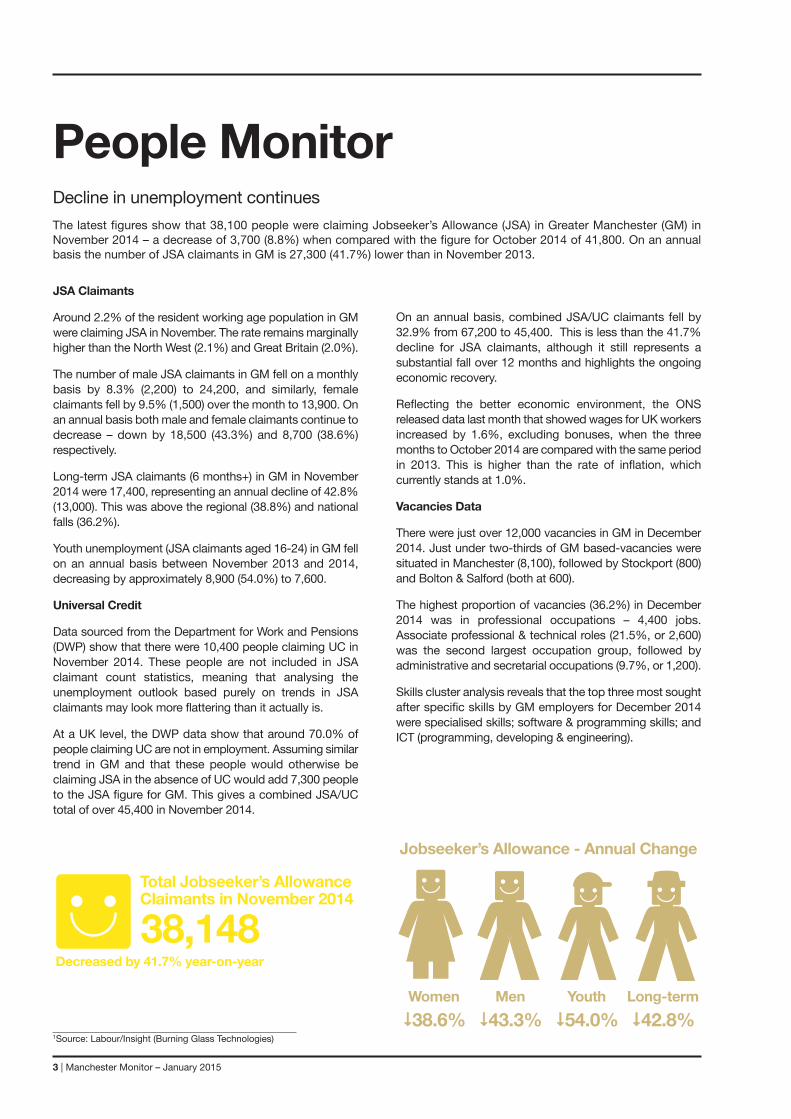

The latest figures show that 38,100 people were claiming Jobseeker’s Allowance (JSA) in Greater Manchester (GM) inNovember 2014 – a decrease of 3,700 (8.8%) when compared with the figure for October 2014 of 41,800. On an annualbasis the number of JSA claimants in GM is 27,300 (41.7%) lower than in November 2013.

Total Jobseeker’s Allowance Claimants in November 2014

38,148Decreased by 41.7% year-on-year

Jobseeker’s Allowance - Annual Change

Women

$38.6%

Men

$43.3%

Youth

$54.0%

Long-term

$42.8%1Source: Labour/Insight (Burning Glass Technologies)

On an annual basis, combined JSA/UC claimants fell by

32.9% from 67,200 to 45,400. This is less than the 41.7%

decline for JSA claimants, although it still represents a

substantial fall over 12 months and highlights the ongoing

economic recovery.

Reflecting the better economic environment, the ONS

released data last month that showed wages for UK workers

increased by 1.6%, excluding bonuses, when the three

months to October 2014 are compared with the same period

in 2013. This is higher than the rate of inflation, which

currently stands at 1.0%.

Vacancies Data

There were just over 12,000 vacancies in GM in December

2014. Just under two-thirds of GM based-vacancies were

situated in Manchester (8,100), followed by Stockport (800)

and Bolton & Salford (both at 600).

The highest proportion of vacancies (36.2%) in December

2014 was in professional occupations – 4,400 jobs.

Associate professional & technical roles (21.5%, or 2,600)

was the second largest occupation group, followed by

administrative and secretarial occupations (9.7%, or 1,200).

Skills cluster analysis reveals that the top three most sought

after specific skills by GM employers for December 2014

were specialised skills; software & programming skills; and

ICT (programming, developing & engineering).

Manchester Monitor – January 2015 | 4

There were 14,705 new businesses started in GM in 2013, a

substantial increase of 3,850 (35.5%) on the 10,855 business

births in 2012. At a UK level, the number of business births

increased by 28.5% from 270,000 to 346,000.

As noted by ONS, the rise coincides with the new Pay As

You Earn (PAYE) Real Time Information (RTI) system, which

was rolled out across businesses during 2013. Nonetheless,

the increase in start-ups is a positive sign that the economy

is continuing in its recovery from the downturn.

Business deaths in GM were recorded at 10,005 in 2013, an

annual decline of 510 (4.9%). For the third year in

succession, the number of births exceeded the number

of deaths and this means that net change in GM in 2013

was 4,700.

GM’s business start-up rate has increased over time. In 2013

there were 84 new business starts per 10,000 resident

working age population, up from 55 in 2009. The 2013 figure

was also virtually in line with the UK average of 85 new starts

per 10,000 resident working age population.

The ONS Business Demography dataset also provides

information on survival rates of firms and this reveals that:

• The 1-year survival rate of firms started in 2012 in GM is

91.9%, slightly above the UK average of 91.2% and

also London (89.7%).

• The 5-year survival rate for companies in GM (those

started in 2008) is 38.7%, which is below the UK average

of 41.3%, but higher than London (37.1%).

Increase in business start-ups

The latest Business Demography dataset released by the Office for National Statistics (ONS) shows there was a sharp rise in thenumber of start-ups in GM between 2012 and 2013. The number of business failures in the conurbation in recent years has remainedbroadly consistent, while start-ups have been increasing over the last three years.

9,520 9,310 10,595 10,855

14,705

12,070 10,605

9,595 10,515 10,005

-2,550 -1,295

1,000 340

4,700

-4,000

0

4,000

8,000

12,000

16,000

2009 2010 2011 2012 2013

Births Deaths Net Change

Business MonitorBusiness births and deaths in GM, 2009-13

5 | Manchester Monitor – January 2015

Results from the latest release of the GM Forecasting Model

(GMFM – December 2014) give an indication of expected

long-term trends in the economy. GMFM is produced by

Oxford Economics for New Economy on behalf of the 10 GM

local authorities, and this month’s quarterly feature provides

more detailed analysis of the forecasts. The focus is on

identifying sectors which are expected to lead employment

growth, the industries which will contribute towards

increased economic output and how the conurbation’s

occupational structure will change up to 2024.

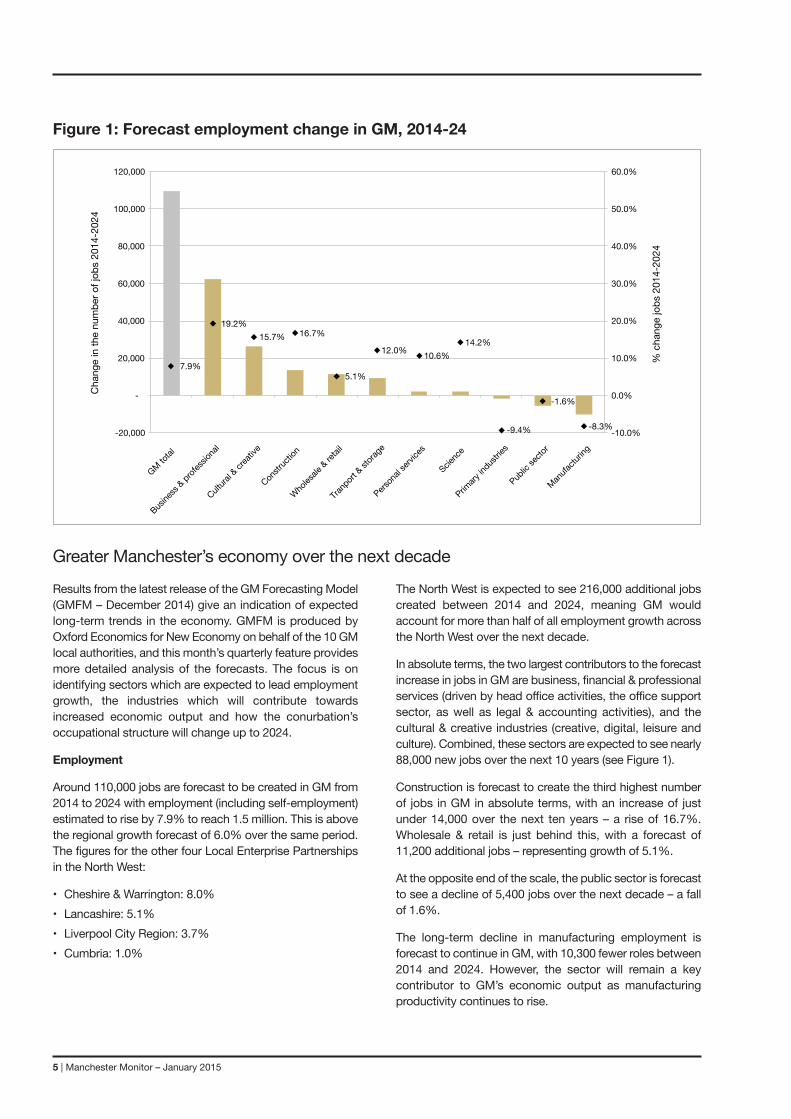

Employment

Around 110,000 jobs are forecast to be created in GM from

2014 to 2024 with employment (including self-employment)

estimated to rise by 7.9% to reach 1.5 million. This is above

the regional growth forecast of 6.0% over the same period.

The figures for the other four Local Enterprise Partnerships

in the North West:

• Cheshire & Warrington: 8.0%

• Lancashire: 5.1%

• Liverpool City Region: 3.7%

• Cumbria: 1.0%

The North West is expected to see 216,000 additional jobs

created between 2014 and 2024, meaning GM would

account for more than half of all employment growth across

the North West over the next decade.

In absolute terms, the two largest contributors to the forecast

increase in jobs in GM are business, financial & professional

services (driven by head office activities, the office support

sector, as well as legal & accounting activities), and the

cultural & creative industries (creative, digital, leisure and

culture). Combined, these sectors are expected to see nearly

88,000 new jobs over the next 10 years (see Figure 1).

Construction is forecast to create the third highest number

of jobs in GM in absolute terms, with an increase of just

under 14,000 over the next ten years – a rise of 16.7%.

Wholesale & retail is just behind this, with a forecast of

11,200 additional jobs – representing growth of 5.1%.

At the opposite end of the scale, the public sector is forecast

to see a decline of 5,400 jobs over the next decade – a fall

of 1.6%.

The long-term decline in manufacturing employment is

forecast to continue in GM, with 10,300 fewer roles between

2014 and 2024. However, the sector will remain a key

contributor to GM’s economic output as manufacturing

productivity continues to rise.

Greater Manchester’s economy over the next decade

7.9%

19.2% 15.7% 16.7%

5.1%

12.0% 10.6% 14.2%

-9.4%

-1.6%

-8.3% -10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-20,000

-

20,000

40,000

60,000

80,000

100,000

120,000

GM total

Busines

s & prof

ession

al

Cultural

& creat

ive

Constr

uction

Wholes

ale & re

tail

Tranp

ort & sto

rage

Person

al serv

ices

Science

Primary

indust

ries

Public

sector

Manufac

turing

% c

hang

e jo

bs 2

014-

2024

Chan

ge in

the

num

ber o

f job

s 201

4-20

24

Figure 1: Forecast employment change in GM, 2014-24

Manchester Monitor – January 2015 | 6

Gross Value Added

GM’s gross value added (GVA) currently stands at £54.7bn

and is forecast to grow by 31.6% (£17.3bn) to £72bn in

2024. The forecasts suggest that business, financial and

professional services will experience the largest rise in

economic output from 2014 to 2024 at £7.3bn – growing

from £15.5bn to £22.9bn.

It is important to note that while manufacturing is forecast

to see a fall in total employment, its importance to GM in

terms of economic output is still expected to grow, with its

GVA contribution increasing by £2bn from 2014 to 2024.

In order to establish GM’s economic strengths, Figure 2

looks at sectors in more detail and provides a specialisation

index (SI), which is calculated by dividing the share of GVA

in a particular sector in GM by the UK share. A value below

1 for a sector means that relatively, its GVA in GM is

lower than in the UK, while a value of above 1 shows

a concentration. High values on the index can be

regarded as a potential indication for the existence of

agglomeration/urbanisation economies, i.e. external benefits

to firms based on their geographic co-location in an area.

The highest degree of specialisation is observed in the

textiles sector, with an SI of 3.5 (not shown on the chart),

meaning the sector’s GVA in GM is 3.5 times higher than UK

average. Textiles falls within the wider manufacturing sector,

which has an SI of 1.2. Legal & accounting (1.4), office

support (1.3), water & air transport (1.3), postal services (1.3),

insurance (1.2), and employment services (1.2) also exhibit

stronger concentrations in GM than in the national average.

Manufacturing

Construction

Wholesale Retail

Water & air transport Postal & courier

Accommodation

Food & beverage services Publishing & Broadcasting

ICT

Financial services

Insurance

Real estate

Legal and accounting Head offices

Advertising & market research

Employment activities Office support

Public administration

Education

Health

Culture & Sports

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1.4 1.5

Sect

oral

% o

f GM

's GV

A

Index of Specialisation

Architecture & Engineering

Figure 2: Specialisation Index for Greater Manchester 2014

7 | Manchester Monitor – January 2015

Occupational Structure

In line with results from the 2013 GMFM, the forecasts for

2014 again suggest that an increasing number of roles will

be created at both the high and low ends of the skills

spectrum in GM over the next 10 years.

For higher-skilled roles, managerial & senior official roles in

GM are forecast to grow by 6.7% over the next 10 years, as

well as for associate professional & technical occupations.

This is followed by professional roles at 5.9% (see Figure 3).

At the lower end of the skills spectrum, personal services are

forecast to rise by 7.3%, followed by elementary

occupations (5.5%) and then sales & customer roles (5.3%).

Intermediate level occupations are expected to either show

a smaller increase or decline between 2014 and 2024.

Skilled trades as well as administrative and secretarial roles

are forecast to grow by 1.5%, while process, plant &

machine operative roles are forecast to decline by 1.7%,

which is consistent with the forecast for a decline in the

numbers of jobs in manufacturing.

The trends suggested by GMFM continue to indicate that

the GM labour market is being reshaped and that jobs are

being created at the top and bottom of the skills scale, while

those in the middle tier are being squeezed. This could have

implications for the distribution of income of the GM working

population.

5.5%

5.3%

7.3%

-1.7%

1.5%

1.5%

6.7%

5.9%

6.7%

Elementary

Sales & customer service

Personal service

Process, plant & machine operatives

Skilled trades

Administrative & secretarial

Associate professional & technical

Professional

Managers and senior officials

Fore

cast

Cha

nge

in Oc

cupa

tions

in G

M, 2

014-

24 (%

)

Intermediate Skill

High Skill

Low Skill

Figure 3: Forecast Change in GM’s Occupational Structure, 2014–24

Summary

From an employment perspective, business, financial and

professional services (driven both by head office activities,

the office support sector as well as legal & accounting), and

the cultural & creative industries are expected to be the

largest contributors to jobs growth in GM over the next 10

years – with almost 88,000 new opportunities being created

in the two sectors. In addition, they are expected to see GVA

grow by more than £9.6bn over the next decade.

Analysis of GM’s sector specialisation reveals that while it is

performing well in traditional industries, and also in a number

of sub-sectors associated with business, financial and

professional services.

The long-term decline in manufacturing employment is still

evident, although the sector’s contribution towards

economic output is expected to grow considerably to 2024,

due to increases in productivity.

The 2014 GMFM results also suggest that an increasing

number of roles in the conurbation will be created at the

higher and lower ends of the skills ladder in GM over the next

10 years, with fewer at intermediate levels. This is likely to

impact on the type of job opportunities that become

available in GM and significantly, on the level of qualifications

people need in order to access them.

Manchester Monitor – January 2015 | 8

Place MonitorVisitor economy remains buoyant

The hotel occupancy indicator continues to perform well and with one set of figures still to come for December, 2014 is

looking like it will be the strongest performing year on record. In addition to strong hotel occupancy levels, the latest monthly

data from the Civil Aviation Authority show passenger numbers are still growing at Manchester Airport.

% represents year-on-year change

Airport passenger numbers (+6.8%)

2,007,549

Hotel Occupancy

The average hotel occupancy rate in Manchester city centre

was recorded at 87.1% in November 2014, consistent with

the same month last year.

Weekend occupancy in the city centre reached the highest

on record for the month at 93.9%, a 1.2 percentage point

increase on the November 2013 figure of 92.7%. The

weekday average occupancy in the city centre was 83.0%,

comparable with the 83.2% recorded for November 2013.

For GM as a whole, average occupancy rates in November

were 83.6%, a rise of 1 percentage point compared to 2013.

Key dates for hotel occupancy in the city centre during

November were:

• 15 November – occupancy of 99% was achieved on the

opening weekend of the Christmas markets, John Bishop

performed at the Manchester Arena and a number of

exhibitions were hosted in the city.

• 29 November – 99% occupancy was also recorded when

Manchester United played at Old Trafford, Enrique Iglesias

performed at the Manchester Arena and the National

Cycling Centre hosted a BMX track event.

• 25 November – 99% was reached when the Etihad

Stadium hosted a UEFA Champions League match and

Manchester Central hosted a 900-delegate conference

relating to the energy sector.

When December figures are released, they are expected to

show that 2014 was the strongest performing year to date

in terms of occupancy levels. There are also encouraging

signs for 2015, with Manchester hosting 40 national and

international conferences that are expected to bring 34,000

delegates to the city and generate £61million for the local

economy. Events include the Conservative Party Conference

and Soccerex Global Convention.

Airport Passenger Numbers

Manchester Airport handled more than 2 million passengers

in October 2014, 128,200 (6.8%) more than 12 months

previously. The annual growth was higher than that

experienced by Birmingham (5.8%) and Heathrow (0.4%),

while Stansted (16.8%) and Gatwick (7.8%) experienced

higher year-on-year rises in passenger numbers.

With passengers numbers close to reaching 22 million on a

rolling 12 month basis, a figure not achieved since 2007, it

was reported in December that the Airport is aiming to

double the annual number of passengers by 2036.

In the shorter term, a number of new routes should help

support growth at the Airport. This includes the launch of the

first non-stop direct flight to China (Hong Kong), operated

by Cathay Pacific, which began last month.

Increased frequencies on existing routes have also been

announced, including:

• An increased capacity of 8,000 seats in the summer

between Manchester and North America on Virgin routes

to and from Orlando and Las Vegas.

• An increased number of flights per week from February on

the Manchester to Doha route operated by Qatar Airways.

• An increased capacity of 48,000 seats per year on the

Emirates service to Dubai

IMPORTANT NOTE: The source of the hotel occupancy data referenced in this newsletter is STR Global Ltd.

Republication or other reuse of this data without the express written permission of STR Global is strictly prohibited.

Hotel occupancy (city centre) (0% pts)

87.1%Flights (1.5%)

14,803Hotel occupancy (GM) (+1.0% pts)

83.6%

9 | Manchester Monitor – January 2015

Housing Monitor

House prices on the rise again

House prices in GM have grown year-on-year, based on analysis of the latest data sourced from the Land Registry. The

cost of a property in GM increased more than in the North West as a whole, but at a lower rate than in England & Wales.

The average property in GM cost £108,400 in October 2014,

up slightly on the previous month’s figure of £108,300. On

an annual basis, the average cost of a property in GM is

4.5% (£4,600) higher than it was in October 2013. This

means that year-on-year prices in GM have now risen for 13

consecutive months.

The annual increase in GM was above the 3.1% rise in the

North West, however it was below the increase for England

and Wales of 7.1%. Nationally, the cost of an average

property now stands at £176,600.

All GM districts except for Tameside recorded annual

increases in house prices from November 2013-14. On a

relative basis, Trafford (9.8%) and Salford (7.8%)

experienced the highest rises.

House sales data from the Land Registry show that there

were a total of 2,964 properties sold in GM in September

2014, an increase of 418 units (16.4%) over the same period

a year earlier. This was a higher figure than across England

and Wales (5.0%), and well above the regional increase of

10.0%.

Nationally, figures released by Halifax reveal that the number

of first-time buyers climbing on to the property ladder rose

by more than a fifth in 2014 to a seven-year high. In its

review, Halifax said the number of buyers joining the UK

property market for the first time jumped by 22% to 326,500

in 2014, following a 23% increase in 2013.

Looking ahead, the Centre for Economics and Business

Research (CEBR) has forecast that house prices will fall by

0.6% across Britain this year. CEBR said factors such as the

threat of higher interest rates, the May general election will

send the market into reverse in 2015 – including in London.

9.8%

5.0%

3.6% 4.5%

2.8%

7.8%

3.5% 4.5%

-1.2%

3.0% 3.3%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

£-

£50,000

£100,000

£150,000

£200,000

£250,000

Traffo

rd

Stockp

ort

Bury

GM

Manches

ter

Salford

Wigan

Rochd

ale

Tamesi

de Bolt

on

Oldham

Average House Price, November 2014 % change, November 2013-November 2014

Average house prices and % change in GM boroughs, 2013-14

Manchester Monitor – January 2015 | 10

Crime Monitor

28,211

3,105

27,834

38,027

4,455

28,956

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Violence Sexual Offences Criminal Damage & Arson

Sep-13 Sep-14

+24.8%

+43.5%

+4.0%

Victim based crime December 2013 - December 2014

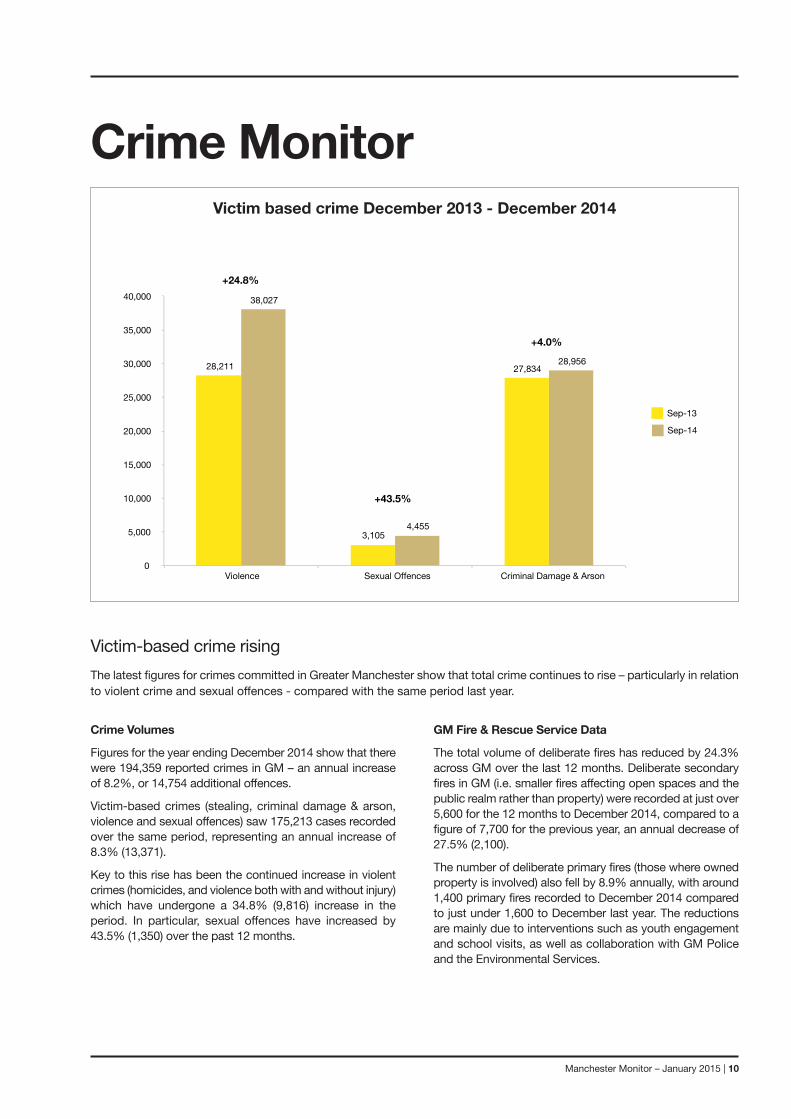

Victim-based crime rising

The latest figures for crimes committed in Greater Manchester show that total crime continues to rise – particularly in relation

to violent crime and sexual offences - compared with the same period last year.

Crime Volumes

Figures for the year ending December 2014 show that there

were 194,359 reported crimes in GM – an annual increase

of 8.2%, or 14,754 additional offences.

Victim-based crimes (stealing, criminal damage & arson,

violence and sexual offences) saw 175,213 cases recorded

over the same period, representing an annual increase of

8.3% (13,371).

Key to this rise has been the continued increase in violent

crimes (homicides, and violence both with and without injury)

which have undergone a 34.8% (9,816) increase in the

period. In particular, sexual offences have increased by

43.5% (1,350) over the past 12 months.

GM Fire & Rescue Service Data

The total volume of deliberate fires has reduced by 24.3%

across GM over the last 12 months. Deliberate secondary

fires in GM (i.e. smaller fires affecting open spaces and the

public realm rather than property) were recorded at just over

5,600 for the 12 months to December 2014, compared to a

figure of 7,700 for the previous year, an annual decrease of

27.5% (2,100).

The number of deliberate primary fires (those where owned

property is involved) also fell by 8.9% annually, with around

1,400 primary fires recorded to December 2014 compared

to just under 1,600 to December last year. The reductions

are mainly due to interventions such as youth engagement

and school visits, as well as collaboration with GM Police

and the Environmental Services.

11 | Manchester Monitor – January 2015

T: +44 (0)161 237 4446 [email protected]

New EconomyChurchgate House56 Oxford StreetManchester M1 6EU

A company limited by guarantee registered in England no. 5678007.

Registered Office MPSL, PO Box 532, Manchester Town Hall, M60 2LA

Related Documents