MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE Taxation & eCommerce Chapter 6 Forder & Quirk

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE Taxation & eCommerce Chapter 6 Forder & Quirk.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Taxation & eCommerce

Chapter 6 Forder & Quirk

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Overview Developments in the taxation of electronic

commerce. Analysis of the design principles that shape

existing and new taxes on electronic transactions.

How Australia taxes and administers eCommerce

ATO response to eCommerce International response to eCommerce

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Initial Responses eCommerce was too insignificant to have a

major effect taxation Initially Internet was left tax fee Some wanted the Internet to be a tariff free zone Concern that countries with normal tax regimes

would lose tax revenue to tax havens

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Initial Responses Others argued to have a “bit tax.” To remove all taxes from Internet transactions

would heavily discriminate against non-electronic trading.

To impose a new tax on information also goes against the principles of taxation because it is highly discriminatory.

A bit tax would be almost impossible to implement using current technology.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Initial Responses How taxpayers could use the Internet and just

how widespread e-commerce could grow. Australia was one of he first countries to look

seriously at the impact of e-commerce on the tax system.

Australia released a report in 1997 then a second in December 1999.

Some people argue to have no taxes on e-commerce.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Initial Responses Developed countries strongly favour not

imposing any new taxes on e-commerce. The USA passed the Internet Tax Freedom Act

in 1998 that prohibits new taxes on the Internet. The World Trade Organisation aims to make the

Internet a tariff-free zone. The existing tax rules need to change to cope

with e-commerce.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Tax Design Basic principles need to be complied with when

introducing new or changing existing taxes. Members of the OECD agreed to try to base any

changes to their taxation of e-commerce on international cooperation and agreement.

The OECD agreed that five traditional principles should apply to any tax changes.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Tax Design These principles are:

1. Neutrality2. Efficiency3. Certainty and Simplicity4. Effectiveness and Fairness5. Flexibility.

Principles of the ATO:1. Neutrality2. The minimisation of compliance and administration

costs3. Privacy.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The Australian Tax Environment The Australian taxes that e-commerce is most

likely to affect are: Income tax Pay-as-you-go (PAYG) tax GST Withholding taxes.

Tax problems arising from e-commerce: Effectiveness of the GST.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

GST Payable at point of each sale in the supply chain Vendor collects GST and sends it to ATO GST not payable on sales that occur outside Australia Vendor can claim credit for GST on previous sales in

supply chain (input tax credit) Some items are GST free e.g. fresh food, medicine etc. Input Tax Credits can be claimed by Vendor on a GST

free sale (i.e. Vendor gets a refund) Some sales are Input Taxed Sales e.g. bank account

fees, interest, superannuation. life insurance Input Tax Credits cannot be claimed by Vendor on an

Input Taxed Sale

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

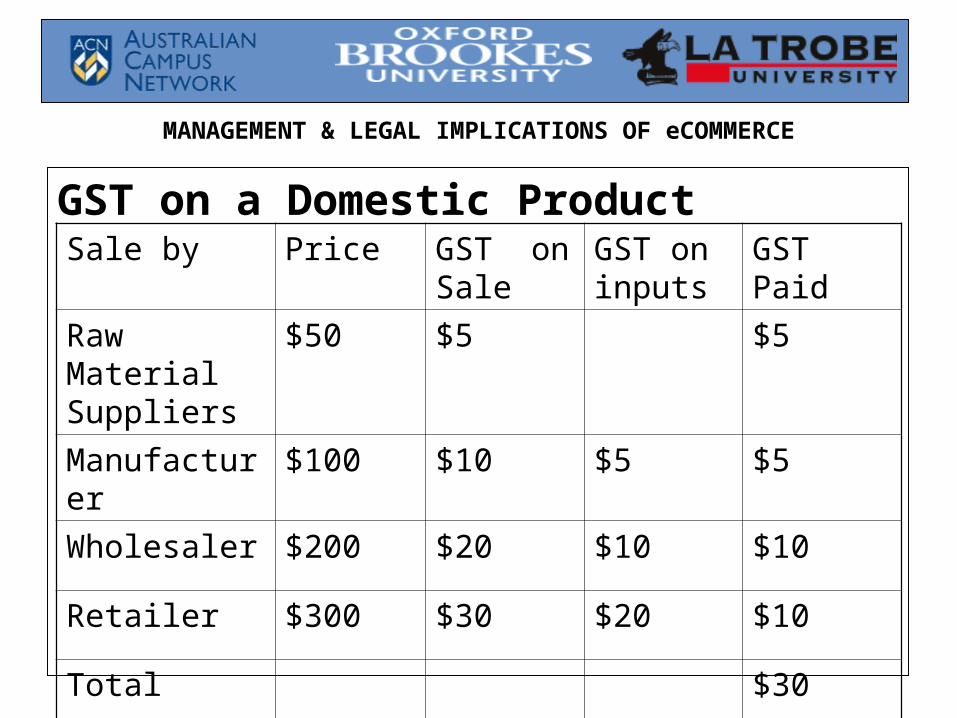

GST on a Domestic ProductSale by Price GST on

SaleGST on inputs

GST Paid

Raw Material Suppliers

$50 $5 $5

Manufacturer $100 $10 $5 $5

Wholesaler $200 $20 $10 $10

Retailer $300 $30 $20 $10

Total $30

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

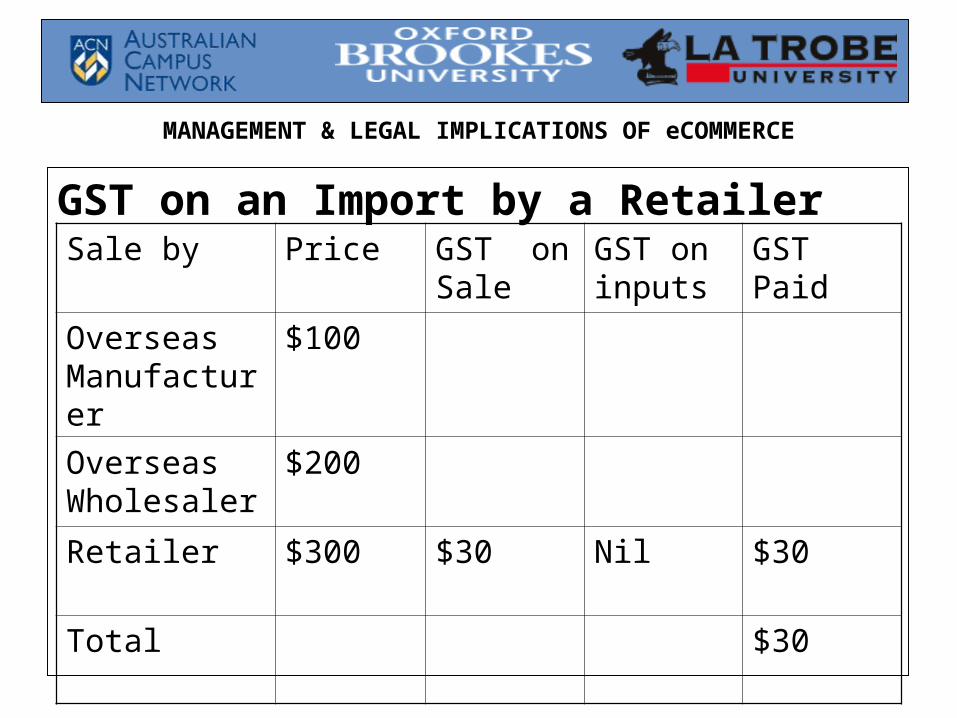

GST on an Import by a RetailerSale by Price GST on

SaleGST on inputs

GST Paid

Overseas Manufacturer

$100

Overseas Wholesaler

$200

Retailer $300 $30 Nil $30

Total $30

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

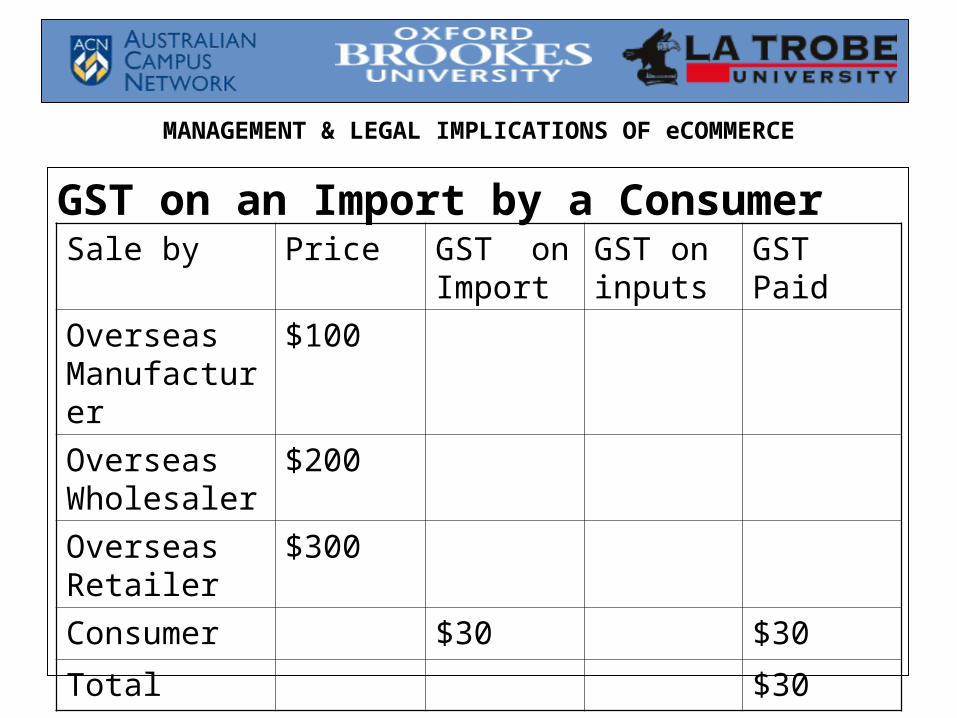

GST on an Import by a ConsumerSale by Price GST on

ImportGST on inputs

GST Paid

Overseas Manufacturer

$100

Overseas Wholesaler

$200

Overseas Retailer

$300

Consumer $30 $30

Total $30

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

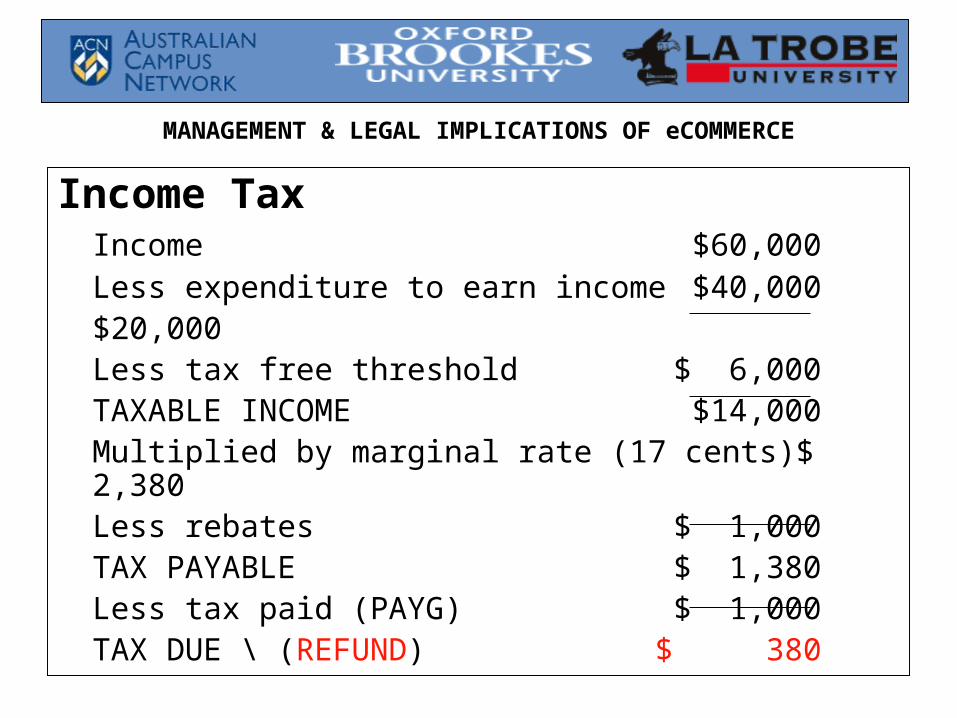

Income TaxIncome $60,000Less expenditure to earn income $40,000

$20,000Less tax free threshold $ 6,000TAXABLE INCOME $14,000Multiplied by marginal rate (17 cents) $ 2,380Less rebates $ 1,000TAX PAYABLE $ 1,380Less tax paid (PAYG) $ 1,000TAX DUE \ (REFUND) $ 380

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

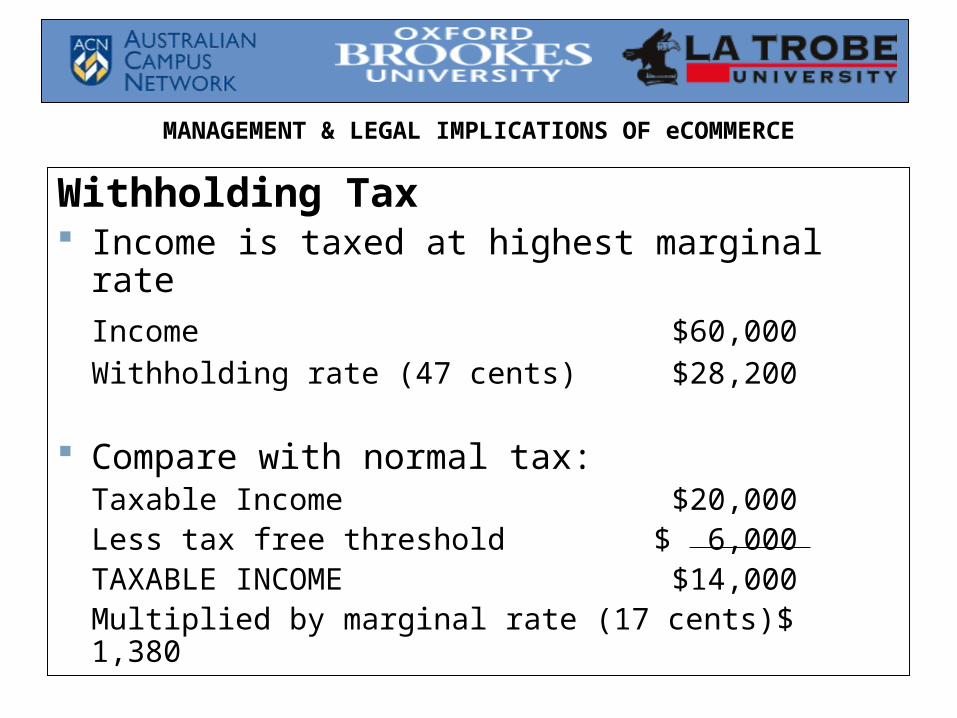

Withholding Tax Income is taxed at highest marginal rate

Income $60,000

Withholding rate (47 cents) $28,200

Compare with normal tax:Taxable Income $20,000Less tax free threshold $ 6,000TAXABLE INCOME $14,000Multiplied by marginal rate (17 cents) $ 1,380

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

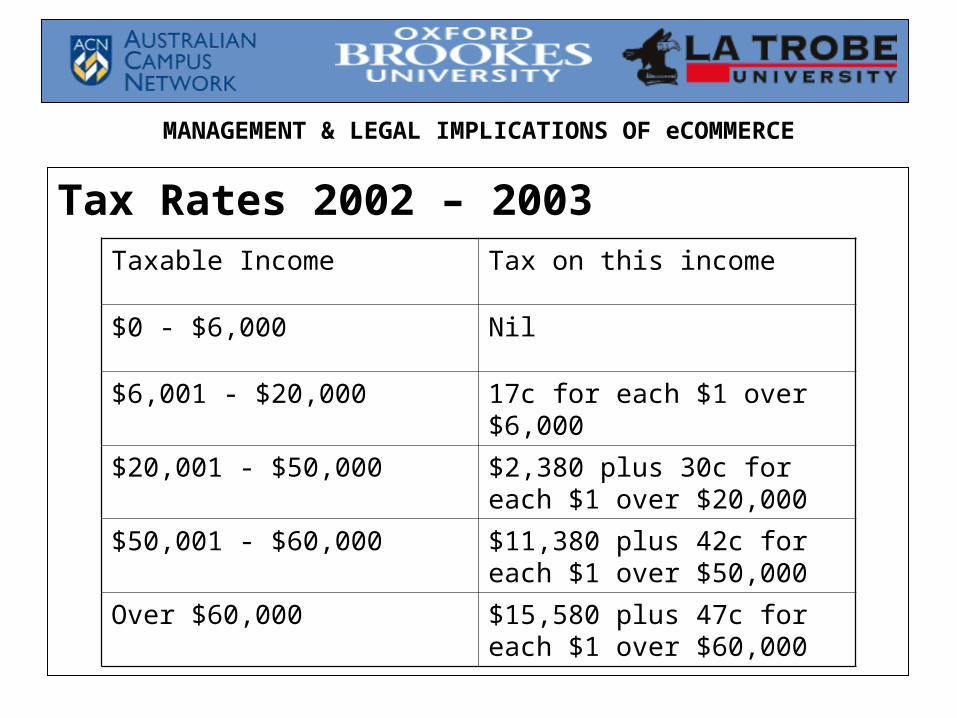

Tax Rates 2002 – 2003Taxable Income Tax on this income

$0 - $6,000 Nil

$6,001 - $20,000 17c for each $1 over $6,000

$20,001 - $50,000 $2,380 plus 30c for each $1 over $20,000

$50,001 - $60,000 $11,380 plus 42c for each $1 over $50,000

Over $60,000 $15,580 plus 47c for each $1 over $60,000

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Tax Challenges for eCommerce One transaction may consist of many separate

transactions Each separate transaction may be subject to

different countries tax regimes Each separate transaction may be separately

taxed Different taxes can apply to each separate

transactions See hypotheticals on pp 156, 157 & 163 of

Forder & Quirk

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

ATO Strategies Revenue impacts

Monitoring

Service Integration Improved information Interactive self help Software

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

ATO Strategies (cont.) Jurisdiction

International agreements

Administration Automation

Detection Move to Consumption Tax (GST) International cooperation

Research & Development

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

ATO Use of Internet The ATO foresees the that e-commerce is not

expected to have a significant impact on tax revenues for the next few years.

The ATO does not want to be caught out unprepared so has developed a comprehensive action plan.

ATO is taking advantage of electronic technologies. Making paying tax easier Detecting tax avoidance

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Paying Tax Made Easier ATO sees opportunities for improving its

services. Implementing Tax Reform:

Education Documentation online Facilitating payment Promoting electronic record keeping Improving ATO efficiency

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Improving Taxpayer Service: The Internet is the major medium being used by the

ATO to improve taxpayer service. Over 75% of income tax returns are lodged

electronically. Using the Internet to help the taxpayer. Businesses can register and get their Australian

Business Number instantly.

Improving ATO efficiency and best practice: Improvements in efficiency will cut costs for the ATO

and for taxpayers.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

E-Grant The Diesel and Alternative Fuels Grants

Scheme. Transport operators currently have to fill in about

70 to 80 pages of forms each year to get their money.

E-Grant is set to end all the paperwork. Truckies will soon be able to receive their

payment directly from the ATO.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Listening to the Community Make the tax experience better. Listening to what people need. The aim is not to change the law. The aim is to change the way of their business

by complying with the law.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Detecting Tax Avoidance Data collection from taxpayers

ABN TFN

Data exchange Government Departments AUSTRAC Other governments

Data modelling Detect transactions which are likely to be associated

with tax evasion

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The International Tax Environment Consumption Taxes

Is tax collected in vendor or buyers jurisdiction? GST will apply if supply connected to Australia Importation is taxable but GST not collected if:

Arrive by post and value less than $1,000; or Value less than $250.

If imported by a consumer, the consumer pays the GST

How do you detect intangible supplies? Negligible impact detected so far

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The International Tax Environment Income Tax:

Based on residence of taxpayer and\or source of income

How to determine when an electronic presence is enough to establish a taxable base in a country? OECD uses the concept of permanent rental\

ownership of a server Uncertainty is created in the application of traditional

source rules, income characterisation, apportionment, the application of traditional residence rules, transfer pricing and avoidance.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The International Tax Environment Income Tax (cont.)

Double taxation agreements avoid a taxpayer paying income tax twice One country is given primary taxing rights; or Taxpayer can rebate tax paid in one country

against tax payable in other country Use of tax havens

Transfer pricing

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The International Tax Environment The OECD response to e-commerce:

Informal round table discussion between business and government.

The formation of technical advisory groups (TAG’s). Areas the TAG’s deal with:

Technology Professional data access Consumption taxes Business profits Income characterisation.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The International Tax Environment International Tax Administration:

There has been a focus on improving the administration of tax at the international level.

The Internet facilitates the automatic exchange of information in a standard format.

The Internet can overcome political, technical and language barriers.

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

The ATO’s International Involvement Heavy involvement in International Tax forums

especially the OECD. Development of international guidelines. International consideration of the impact of

growth in e-commerce. Guidelines for the exchange of data

Privacy and security concerns

MANAGEMENT & LEGAL IMPLICATIONS OF eCOMMERCE

Conclusion Some tax avoidance is possible using

eCommerce No real difference to tax avoidance in traditional

commerce eCommerce improves tax authorities ability to

prevent and detect avoidance eCommerce reduces businesses cost of

compliance with tax obligations

Related Documents