CA SRI LANKA CURRICULUM 2015 KE2 Management Accounting Information (English) Additional Study Support Material This document is designed to use as an additional study support material. Students are advised to refer the content in the study text and the additional study support material under each chapter. The students who have already purchased the “Executive Level KE2 – Management Accounting Information” study text are also advised to refer this study support material.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

C A S R I L A N K A C U R R I C U L U M 2 0 1 5

KE2 Management Accounting Information

(English)

A d d i t i o n a l S t u d y S u p p o r t M a t e r i a l

This document is designed to use as an additional study support material. Students are

advised to refer the content in the study text and the additional study support material

under each chapter. The students who have already purchased the “Executive Level KE2 –

Management Accounting Information” study text are also advised to refer this study

support material.

KE2 - Additional Study Support Material

2

All Rights Reserved

Contents KE2 Management Accounting Information Part A Fundamental Aspects of Cost Accounting

1 Introductory mathematics 3

4 Accounting for materials 14

6 Job, batch, contract and service costing 18

Part B Quantitative Aspects for Accounting

9 Normal distribution and sampling distributions 19

Part C Cost Accounting Systems

10 Accounting for overheads 28

11 Absorption, marginal and activity based costing 29

Part D Financial Mathematics for Business and Project Appraisal

Fundamentals

12 Financial mathematics for business 32

Part F Mathematics for Business Functions

16 Mathematics for business functions 34

Part G Budgeting and Forecasting

17 Budgetary control and budgetary systems 37

18 Forecasting and Preparing Budgets 44

KE2 - Additional Study Support Material

3

All Rights Reserved

Additional Practice Questions to Chapter 1

Introductory Mathematics

Heading 4: Percentages and Ratios (page 13)

Percentages in a business context (Learning Outcome 2.1.1)

1. If the price of a cosmetic product is reduced by 20%, sales volume increases by

30%. Calculate the change in total revenue.

A) 6% B) 12% C) 10% D) 4%

(2 marks) Solution:

Assume the original price is “p” and the original sales volume is “q”. Express the new price and the volume in terms of p and q respectively.

Original value Change New value Price 𝑝 decreases by 20% 0.80 𝑝 Volume 𝑞 increases by 30% 1.30 𝑞 Revenue 𝑝 × 𝑞 1.04 𝑝 × 𝑞

When revenue increases from 𝑝𝑞 to 1.04 𝑝𝑞 the increase would be 0.04𝑝𝑞 and so the percentage increase is 4%.

Change in total revenue = (1.04pq – pq) 100% = 4% Answer: D

2. The last month telephone cost of a company was Rs. 43,200, including VAT at

8%. It has been decided to allocate 50% of these telephone costs, excluding

VAT, to the Marketing Division and to allocate 25% of the remainder, excluding

VAT, to the Finance Division.

Compute the telephone costs to be allocated to the Finance Division.

(3 marks)

Solution:

In the question it has been stated that apportioning of telephone cost to the departments is excluding VAT and hence we need to work out the telephone cost excluding VAT.

KE2 - Additional Study Support Material

4

All Rights Reserved

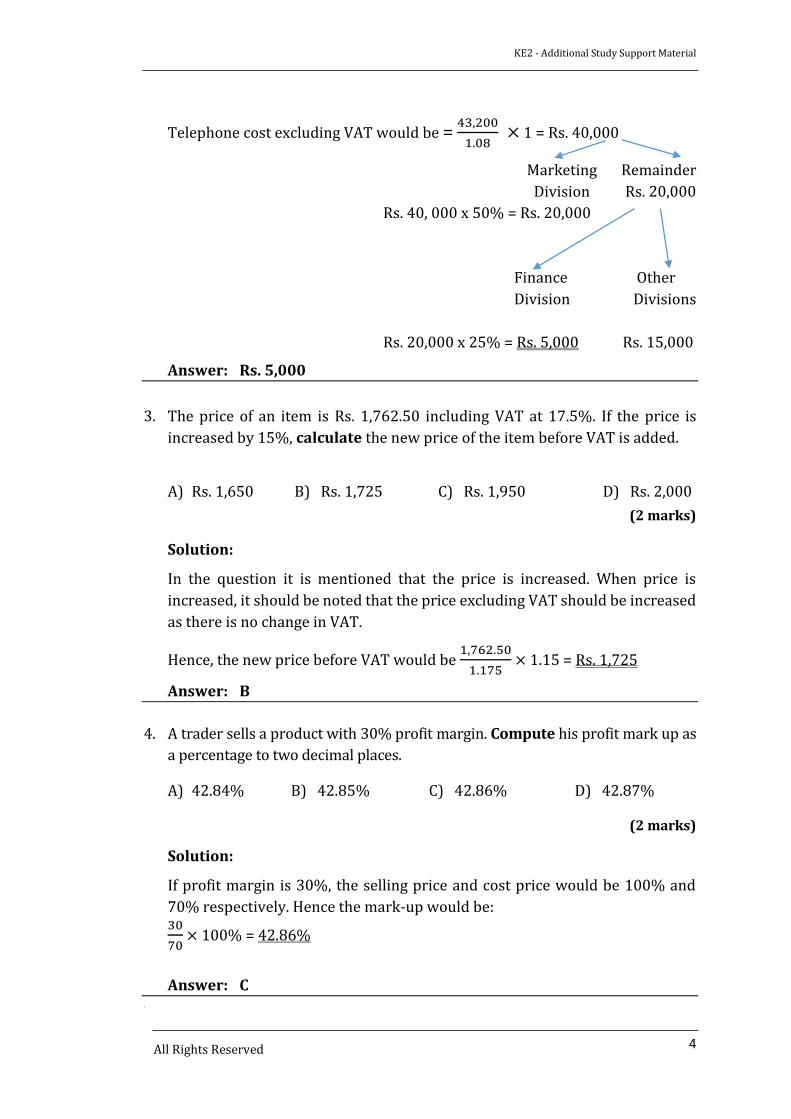

Telephone cost excluding VAT would be = 43,200

1.08 × 1 = Rs. 40,000

Marketing Remainder

Division Rs. 20,000

Rs. 40, 000 x 50% = Rs. 20,000

Finance Other

Division Divisions

Rs. 20,000 x 25% = Rs. 5,000 Rs. 15,000

Answer: Rs. 5,000

3. The price of an item is Rs. 1,762.50 including VAT at 17.5%. If the price is

increased by 15%, calculate the new price of the item before VAT is added.

A) Rs. 1,650 B) Rs. 1,725 C) Rs. 1,950 D) Rs. 2,000

(2 marks)

Solution:

In the question it is mentioned that the price is increased. When price is

increased, it should be noted that the price excluding VAT should be increased

as there is no change in VAT.

Hence, the new price before VAT would be 1,762.50

1.175 × 1.15 = Rs. 1,725

Answer: B

4. A trader sells a product with 30% profit margin. Compute his profit mark up as

a percentage to two decimal places.

A) 42.84% B) 42.85% C) 42.86% D) 42.87%

(2 marks)

Solution:

If profit margin is 30%, the selling price and cost price would be 100% and

70% respectively. Hence the mark-up would be: 30

70 × 100% = 42.86%

Answer: C \

KE2 - Additional Study Support Material

5

All Rights Reserved

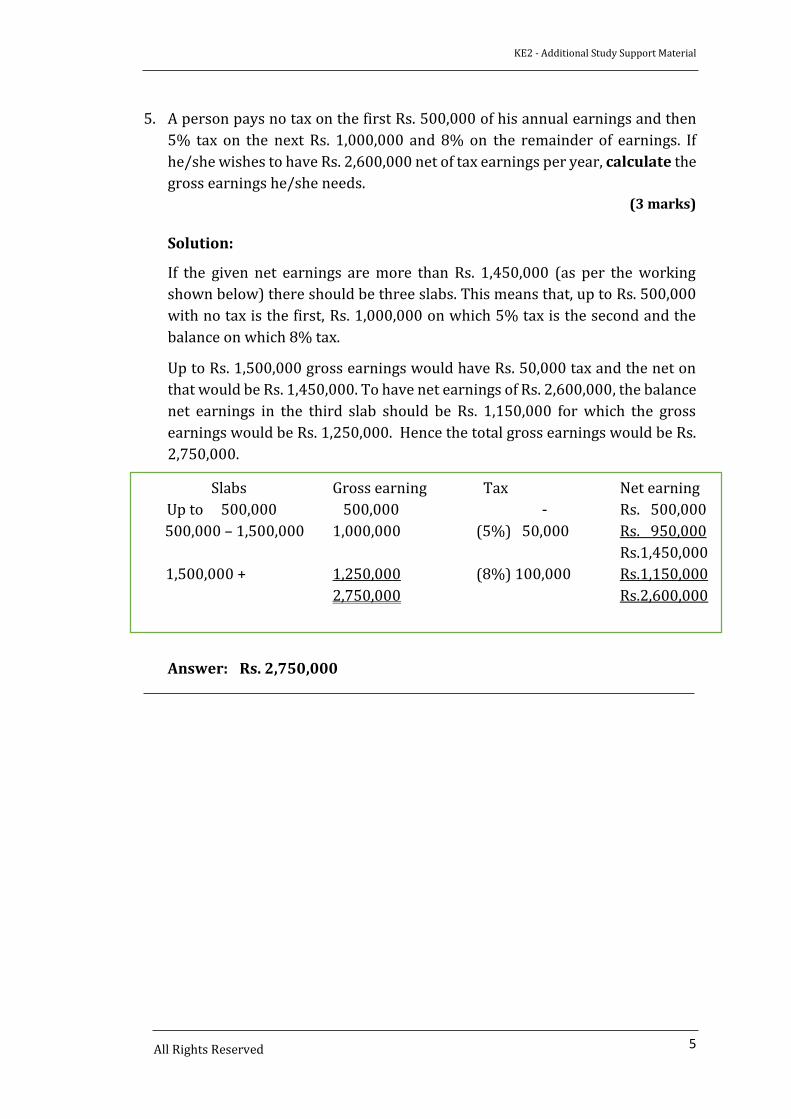

5. A person pays no tax on the first Rs. 500,000 of his annual earnings and then

5% tax on the next Rs. 1,000,000 and 8% on the remainder of earnings. If

he/she wishes to have Rs. 2,600,000 net of tax earnings per year, calculate the

gross earnings he/she needs.

(3 marks)

Solution:

If the given net earnings are more than Rs. 1,450,000 (as per the working

shown below) there should be three slabs. This means that, up to Rs. 500,000

with no tax is the first, Rs. 1,000,000 on which 5% tax is the second and the

balance on which 8% tax.

Up to Rs. 1,500,000 gross earnings would have Rs. 50,000 tax and the net on

that would be Rs. 1,450,000. To have net earnings of Rs. 2,600,000, the balance

net earnings in the third slab should be Rs. 1,150,000 for which the gross

earnings would be Rs. 1,250,000. Hence the total gross earnings would be Rs.

2,750,000.

Answer: Rs. 2,750,000

Slabs Gross earning Tax Net earning

Up to 500,000 500,000 - Rs. 500,000

500,000 – 1,500,000 1,000,000 (5%) 50,000 Rs. 950,000

Rs.1,450,000

1,500,000 + 1,250,000 (8%) 100,000 Rs.1,150,000

2,750,000 Rs.2,600,000

KE2 - Additional Study Support Material

6

All Rights Reserved

Heading 4: Percentages and Ratios (Page 13)

Percentages in a business context (Learning Outcome.2.1.1)

Chapter 6 , Heading 3: Batch costing (Page 214)

Specific and continuous order costing (Learning Outcome.1.4.2)

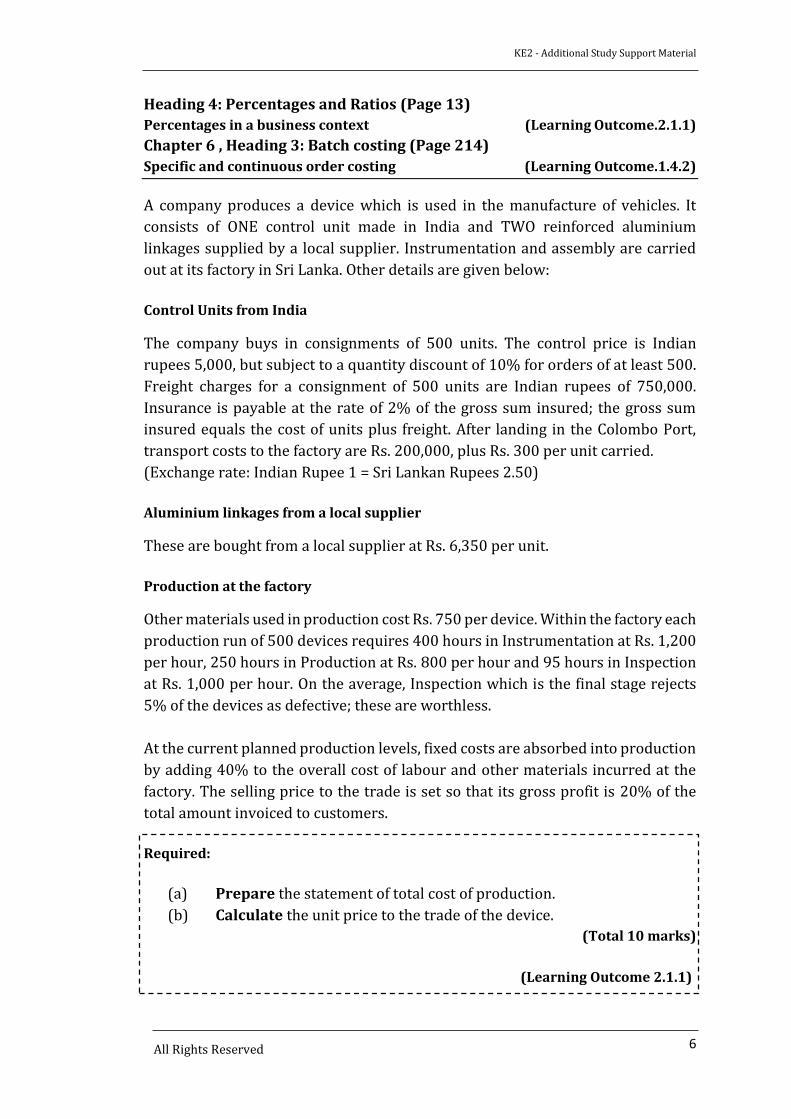

A company produces a device which is used in the manufacture of vehicles. It

consists of ONE control unit made in India and TWO reinforced aluminium

linkages supplied by a local supplier. Instrumentation and assembly are carried

out at its factory in Sri Lanka. Other details are given below:

Control Units from India

The company buys in consignments of 500 units. The control price is Indian

rupees 5,000, but subject to a quantity discount of 10% for orders of at least 500.

Freight charges for a consignment of 500 units are Indian rupees of 750,000.

Insurance is payable at the rate of 2% of the gross sum insured; the gross sum

insured equals the cost of units plus freight. After landing in the Colombo Port,

transport costs to the factory are Rs. 200,000, plus Rs. 300 per unit carried.

(Exchange rate: Indian Rupee 1 = Sri Lankan Rupees 2.50)

Aluminium linkages from a local supplier

These are bought from a local supplier at Rs. 6,350 per unit.

Production at the factory

Other materials used in production cost Rs. 750 per device. Within the factory each

production run of 500 devices requires 400 hours in Instrumentation at Rs. 1,200

per hour, 250 hours in Production at Rs. 800 per hour and 95 hours in Inspection

at Rs. 1,000 per hour. On the average, Inspection which is the final stage rejects

5% of the devices as defective; these are worthless.

At the current planned production levels, fixed costs are absorbed into production

by adding 40% to the overall cost of labour and other materials incurred at the

factory. The selling price to the trade is set so that its gross profit is 20% of the

total amount invoiced to customers.

Required:

(a) Prepare the statement of total cost of production.

(b) Calculate the unit price to the trade of the device.

(Total 10 marks)

(Learning Outcome 2.1.1)

KE2 - Additional Study Support Material

7

All Rights Reserved

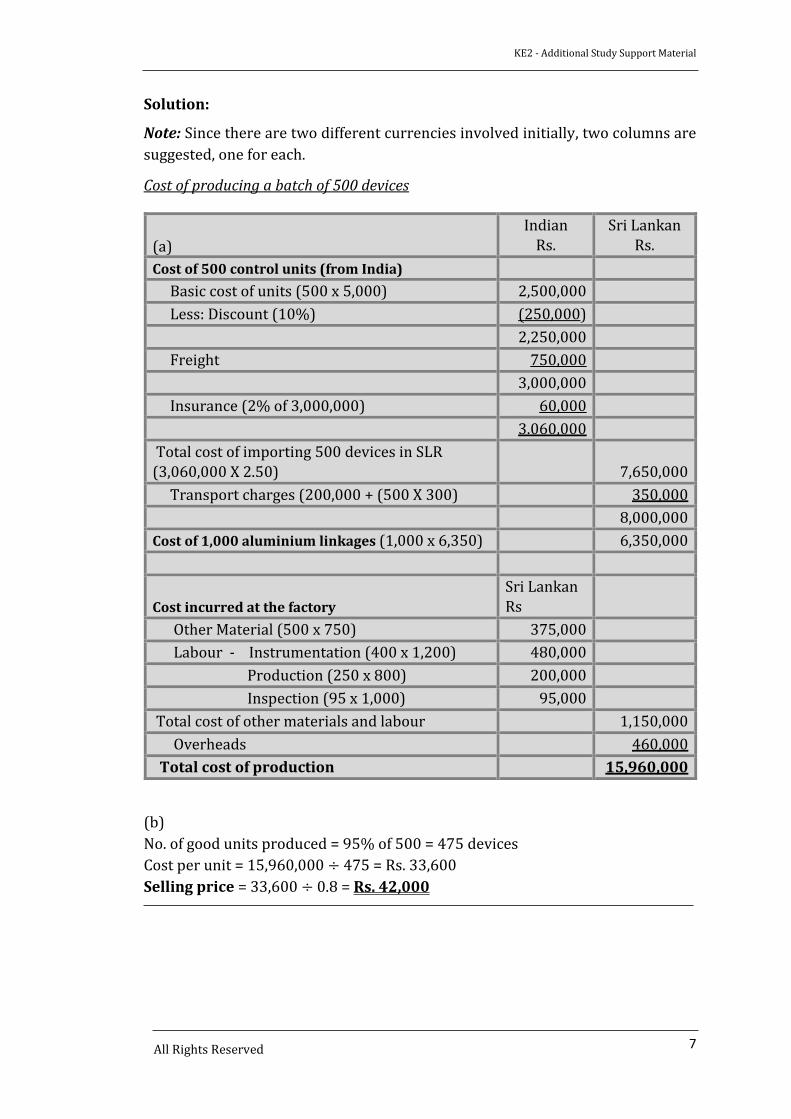

Solution:

Note: Since there are two different currencies involved initially, two columns are

suggested, one for each.

Cost of producing a batch of 500 devices

(b)

No. of good units produced = 95% of 500 = 475 devices

Cost per unit = 15,960,000 ÷ 475 = Rs. 33,600

Selling price = 33,600 ÷ 0.8 = Rs. 42,000

(a)

Indian Rs.

Sri Lankan Rs.

Cost of 500 control units (from India)

Basic cost of units (500 x 5,000) 2,500,000

Less: Discount (10%) (250,000)

2,250,000

Freight 750,000

3,000,000

Insurance (2% of 3,000,000) 60,000

3.060,000

Total cost of importing 500 devices in SLR (3,060,000 X 2.50) 7,650,000

Transport charges (200,000 + (500 X 300) 350,000

8,000,000

Cost of 1,000 aluminium linkages (1,000 x 6,350) 6,350,000

Cost incurred at the factory

Sri Lankan Rs

Other Material (500 x 750) 375,000

Labour - Instrumentation (400 x 1,200) 480,000

Production (250 x 800) 200,000

Inspection (95 x 1,000) 95,000

Total cost of other materials and labour 1,150,000

Overheads 460,000

Total cost of production 15,960,000

KE2 - Additional Study Support Material

8

All Rights Reserved

Heading 6: Errors (page 28)

Variations under addition, subtraction, multiplication

and division (Learning Outcome 2.2.1)

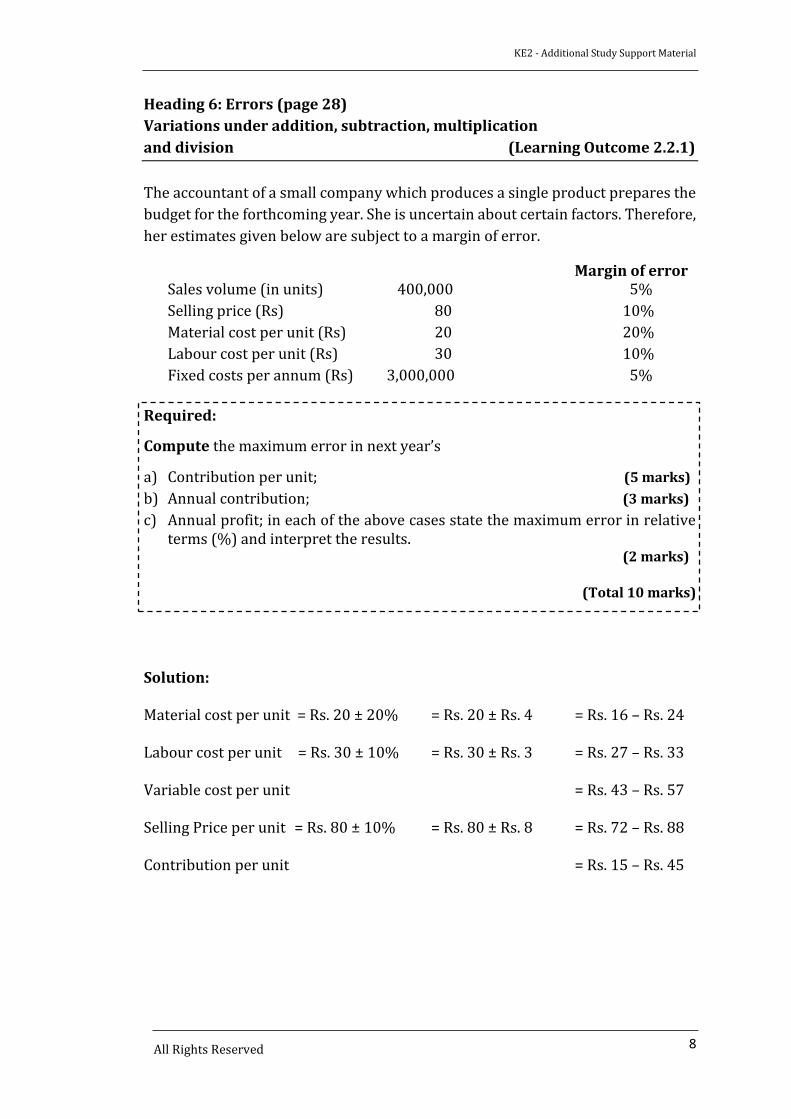

The accountant of a small company which produces a single product prepares the

budget for the forthcoming year. She is uncertain about certain factors. Therefore,

her estimates given below are subject to a margin of error.

Margin of error Sales volume (in units) 400,000 5%

Selling price (Rs) 80 10%

Material cost per unit (Rs) 20 20%

Labour cost per unit (Rs) 30 10%

Fixed costs per annum (Rs) 3,000,000 5%

Required:

Compute the maximum error in next year’s

a) Contribution per unit; (5 marks)

b) Annual contribution; (3 marks)

c) Annual profit; in each of the above cases state the maximum error in relative terms (%) and interpret the results.

(2 marks)

(Total 10 marks)

Solution:

Material cost per unit = Rs. 20 ± 20% = Rs. 20 ± Rs. 4 = Rs. 16 – Rs. 24

Labour cost per unit = Rs. 30 ± 10% = Rs. 30 ± Rs. 3 = Rs. 27 – Rs. 33

Variable cost per unit = Rs. 43 – Rs. 57

Selling Price per unit = Rs. 80 ± 10% = Rs. 80 ± Rs. 8 = Rs. 72 – Rs. 88

Contribution per unit = Rs. 15 – Rs. 45

KE2 - Additional Study Support Material

9

All Rights Reserved

a) The contribution per unit can also be expressed as follows:

Contribution per unit = Rs. 15 - Rs. 45 = Rs. 30 ± Rs. 15 = Rs. 30 ± 50%

Interpretation: When the selling price is subject to ± 10% error and the

material and labour cost per unit is subject to errors of ± 20%

and ± 10% respectively then contribution per unit will be

subject to an error of ± 50%.

b) Sales Volume = 400,000 ± 5% = 400,000 ± 20,000

= [380,000 – 420,000] units

Contribution per unit = [Rs. 15 – Rs. 45]

Hence total contribution would be between = Rs. 5,700,000 – Rs. 18,900,000

= Rs. 12,000,000 ± 6,900,000

= Rs. 12,000,000 ± 57.5%

The maximum error in total contribution would be 57.5%.

Interpretation: When the sales volume is subject to ± 5% error and the

contribution per unit is subject to an error of ±50% error,

the maximum error in the total contribution would be ±

57.5%.

c) Total contribution is [Rs. 5,700,000 – Rs. 18,900,000]

Fixed overhead = Rs. 3,000,000 ± 5%

= Rs. 3,000,000 ± Rs. 150,000

= Rs. 2,850,000 – Rs. 3,150,000

Hence, annual profit would be [Rs. 2,550,000 - Rs. 16,050,000]. This could be

expressed as Rs. 9,000,000 ± Rs. 7,050,000 = Rs. 9,000,000 ± 78.3%

Interpretation: When all the variations happen in the factors as

mentioned in the question the profit will be subject to a

maximum error of ± 78.3%.

KE2 - Additional Study Support Material

10

All Rights Reserved

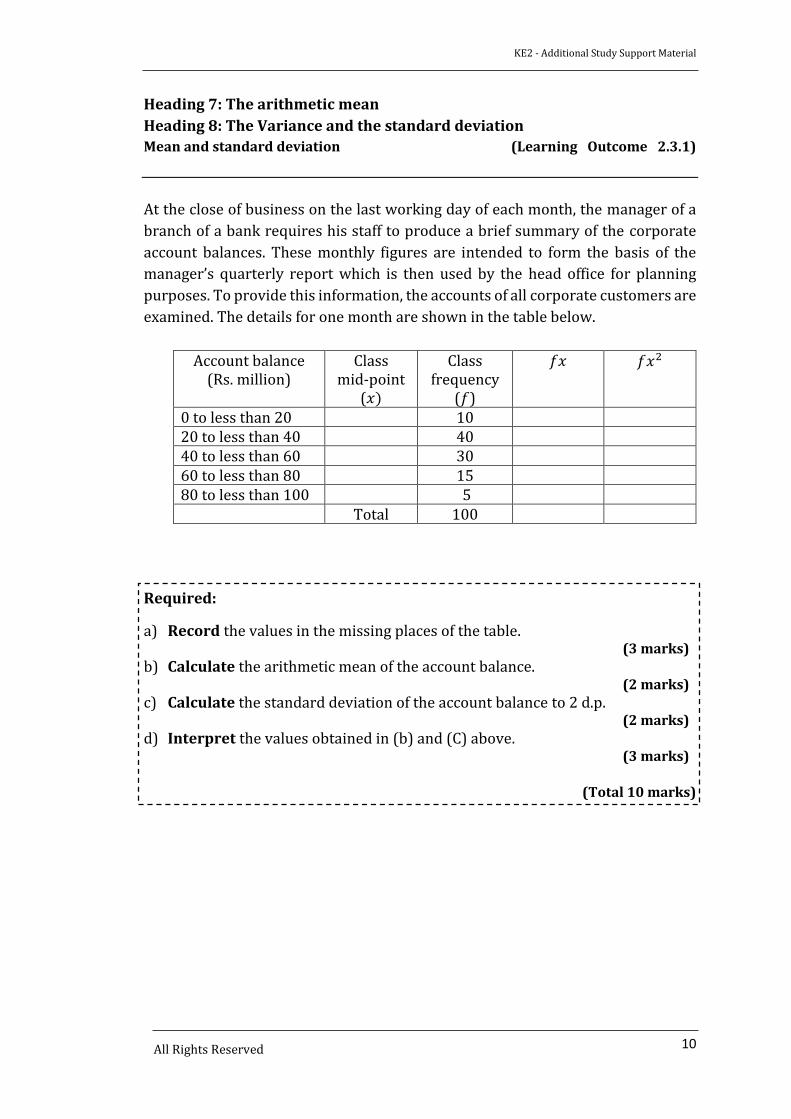

Heading 7: The arithmetic mean

Heading 8: The Variance and the standard deviation

Mean and standard deviation (Learning Outcome 2.3.1)

At the close of business on the last working day of each month, the manager of a

branch of a bank requires his staff to produce a brief summary of the corporate

account balances. These monthly figures are intended to form the basis of the

manager’s quarterly report which is then used by the head office for planning

purposes. To provide this information, the accounts of all corporate customers are

examined. The details for one month are shown in the table below.

Account balance (Rs. million)

Class mid-point

(𝑥)

Class frequency

(𝑓)

𝑓𝑥 𝑓𝑥2

0 to less than 20 10 20 to less than 40 40 40 to less than 60 30 60 to less than 80 15 80 to less than 100 5

Total 100

Required:

a) Record the values in the missing places of the table. (3 marks)

b) Calculate the arithmetic mean of the account balance. (2 marks)

c) Calculate the standard deviation of the account balance to 2 d.p. (2 marks)

d) Interpret the values obtained in (b) and (C) above. (3 marks)

(Total 10 marks)

KE2 - Additional Study Support Material

11

All Rights Reserved

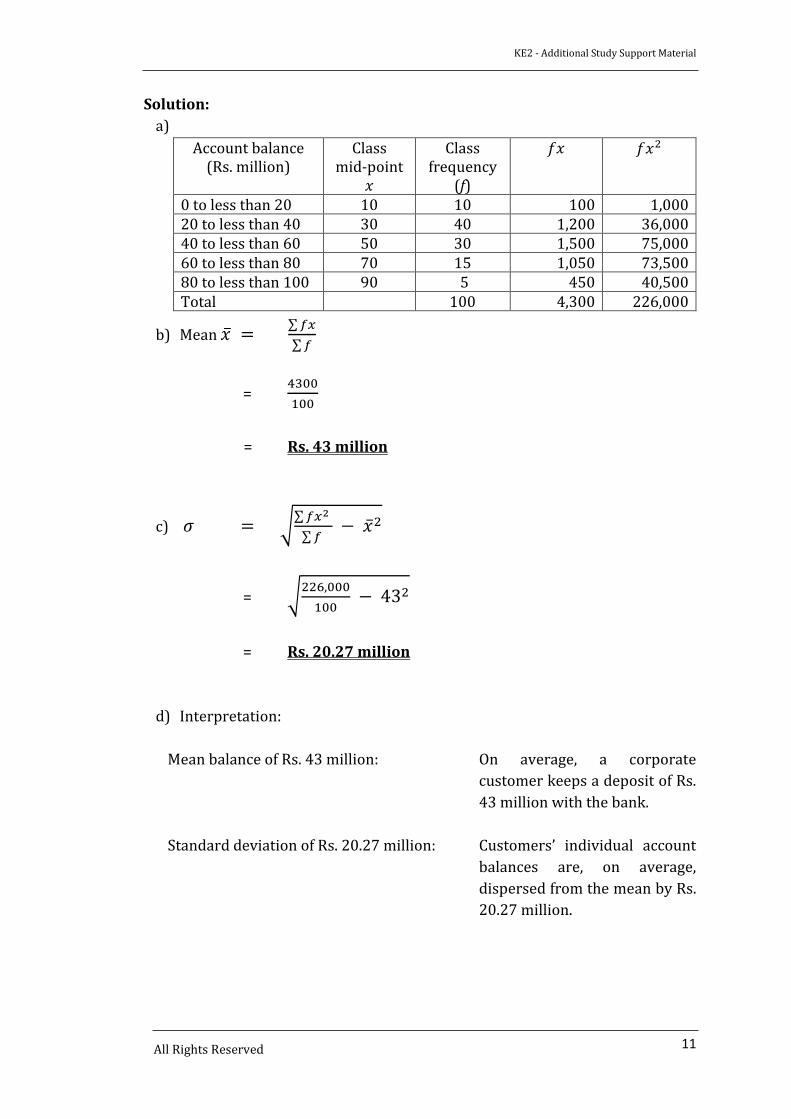

Solution:

a)

Account balance (Rs. million)

Class mid-point

𝑥

Class frequency

(f)

𝑓𝑥 𝑓𝑥2

0 to less than 20 10 10 100 1,000 20 to less than 40 30 40 1,200 36,000 40 to less than 60 50 30 1,500 75,000 60 to less than 80 70 15 1,050 73,500 80 to less than 100 90 5 450 40,500 Total 100 4,300 226,000

b) Mean �̅� = ∑ 𝑓𝑥

∑ 𝑓

= 4300

100

= Rs. 43 million

c) 𝜎 = √∑ 𝑓𝑥2

∑ 𝑓 − �̅�2

= √226,000

100 − 432

= Rs. 20.27 million

d) Interpretation:

Mean balance of Rs. 43 million: On average, a corporate

customer keeps a deposit of Rs.

43 million with the bank.

Standard deviation of Rs. 20.27 million: Customers’ individual account

balances are, on average,

dispersed from the mean by Rs.

20.27 million.

KE2 - Additional Study Support Material

12

All Rights Reserved

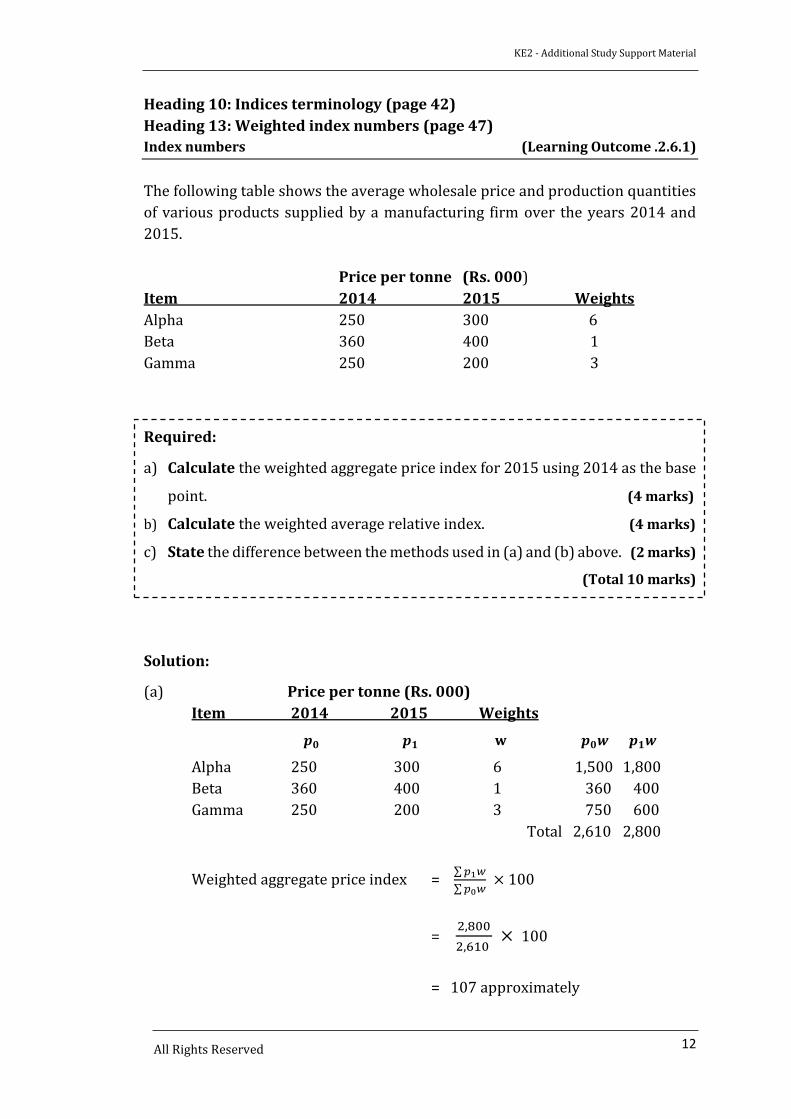

Heading 10: Indices terminology (page 42)

Heading 13: Weighted index numbers (page 47)

Index numbers (Learning Outcome .2.6.1)

The following table shows the average wholesale price and production quantities

of various products supplied by a manufacturing firm over the years 2014 and

2015.

Price per tonne (Rs. 000)

Item 2014 2015 Weights

Alpha 250 300 6

Beta 360 400 1

Gamma 250 200 3

Required:

a) Calculate the weighted aggregate price index for 2015 using 2014 as the base

point. (4 marks)

b) Calculate the weighted average relative index. (4 marks)

c) State the difference between the methods used in (a) and (b) above. (2 marks)

(Total 10 marks)

Solution:

(a) Price per tonne (Rs. 000)

Item 2014 2015 Weights

𝒑𝟎 𝒑𝟏 w 𝒑𝟎𝒘 𝒑𝟏𝒘

Alpha 250 300 6 1,500 1,800

Beta 360 400 1 360 400

Gamma 250 200 3 750 600

Total 2,610 2,800

Weighted aggregate price index = ∑ 𝑝1𝑤

∑ 𝑝0𝑤 × 100

= 2,800

2,610 × 100

= 107 approximately

KE2 - Additional Study Support Material

13

All Rights Reserved

The overall increase in prices, using the standard weights given, between

2014 and 2015, is approximately 7% (107% - 100%).

b) Price relative weights

𝑰 = 𝒑𝟏

𝒑𝟎 × 100 w I × w

Alpha 300

250 × 100 = 120 6 720

Beta 400

360× 100 = 111 1 111

Gamma 200

250 ×100 = 80 3 240

10 1,071

Weighted average of price relative = 1,071

10 = 107 (approximately)

The overall increase in prices, using the standard weights provided,

between 2014 and 2015, is approximately 7%.

c) The difference between weighted aggregate method and the weighted

average method is, the weights are provided first and then the index is

calculated. Whereas with the weighted average method, the index is

calculated first and then the weights are provided.

Both show the overall increase in prices, taking the weights given into

account.

KE2 - Additional Study Support Material

14 All Rights Reserved

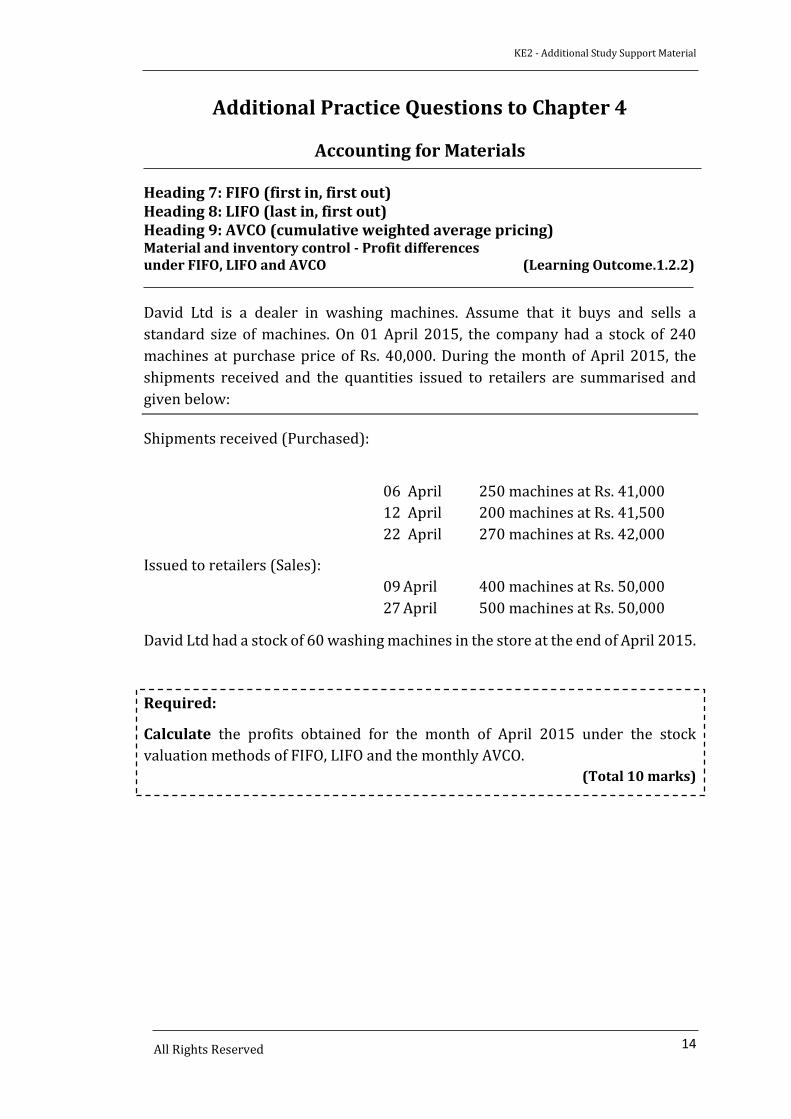

Additional Practice Questions to Chapter 4

Accounting for Materials

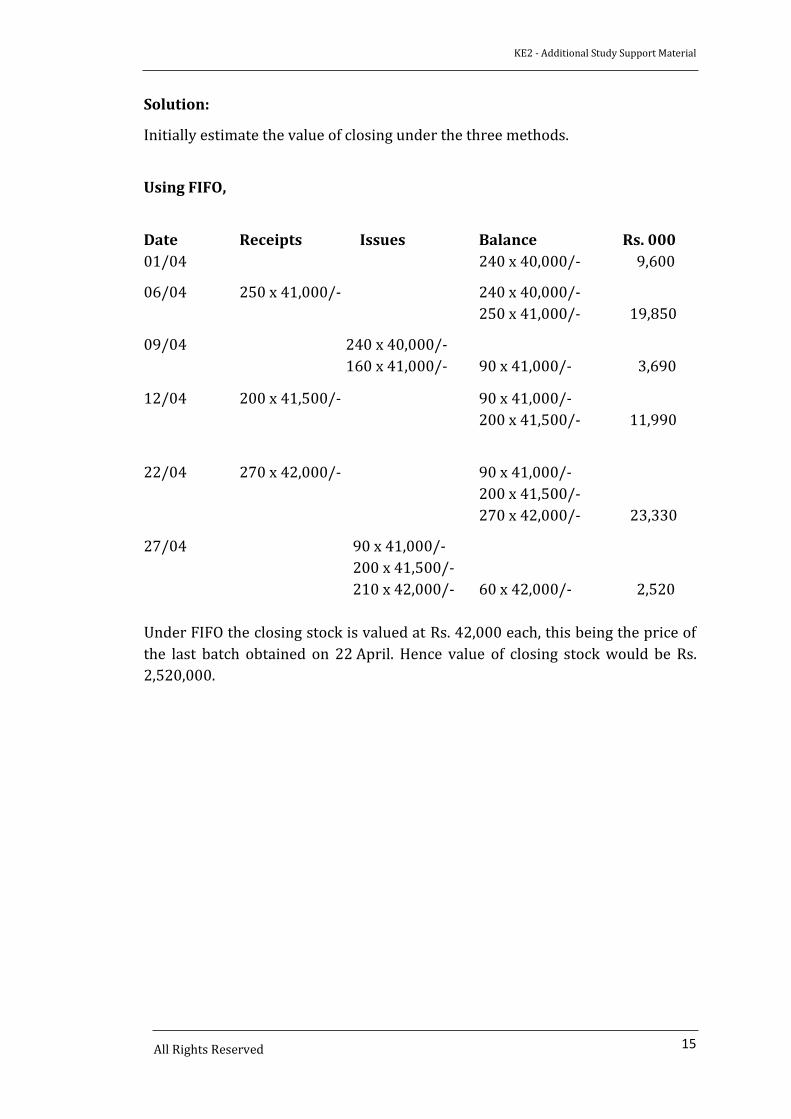

Heading 7: FIFO (first in, first out)Heading 8: LIFO (last in, first out)Heading 9: AVCO (cumulative weighted average pricing)Material and inventory control - Profit differences under FIFO, LIFO and AVCO (Learning Outcome.1.2.2)

David Ltd is a dealer in washing machines. Assume that it buys and sells a

standard size of machines. On 01 April 2015, the company had a stock of 240

machines at purchase price of Rs. 40,000. During the month of April 2015, the

shipments received and the quantities issued to retailers are summarised and given below:

Shipments received (Purchased):

06 April 250 machines at Rs. 41,000

12 April 200 machines at Rs. 41,500

22 April 270 machines at Rs. 42,000

Issued to retailers (Sales):

09 April 400 machines at Rs. 50,000

27 April 500 machines at Rs. 50,000

David Ltd had a stock of 60 washing machines in the store at the end of April 2015.

Required:

Calculate the profits obtained for the month of April 2015 under the stock

valuation methods of FIFO, LIFO and the monthly AVCO.

(Total 10 marks)

KE2 - Additional Study Support Material

15 All Rights Reserved

Solution:

Initially estimate the value of closing under the three methods.

Using FIFO,

Date Receipts Issues Balance Rs. 000

01/04 240 x 40,000/- 9,600

06/04 250 x 41,000/- 240 x 40,000/-

250 x 41,000/- 19,850

09/04 240 x 40,000/-

160 x 41,000/- 90 x 41,000/- 3,690

12/04 200 x 41,500/- 90 x 41,000/-

200 x 41,500/- 11,990

22/04 270 x 42,000/- 90 x 41,000/-

200 x 41,500/-

270 x 42,000/- 23,330

27/04 90 x 41,000/-

200 x 41,500/-

210 x 42,000/- 60 x 42,000/- 2,520

Under FIFO the closing stock is valued at Rs. 42,000 each, this being the price of

the last batch obtained on 22 April. Hence value of closing stock would be Rs.

2,520,000.

KE2 - Additional Study Support Material

16 All Rights Reserved

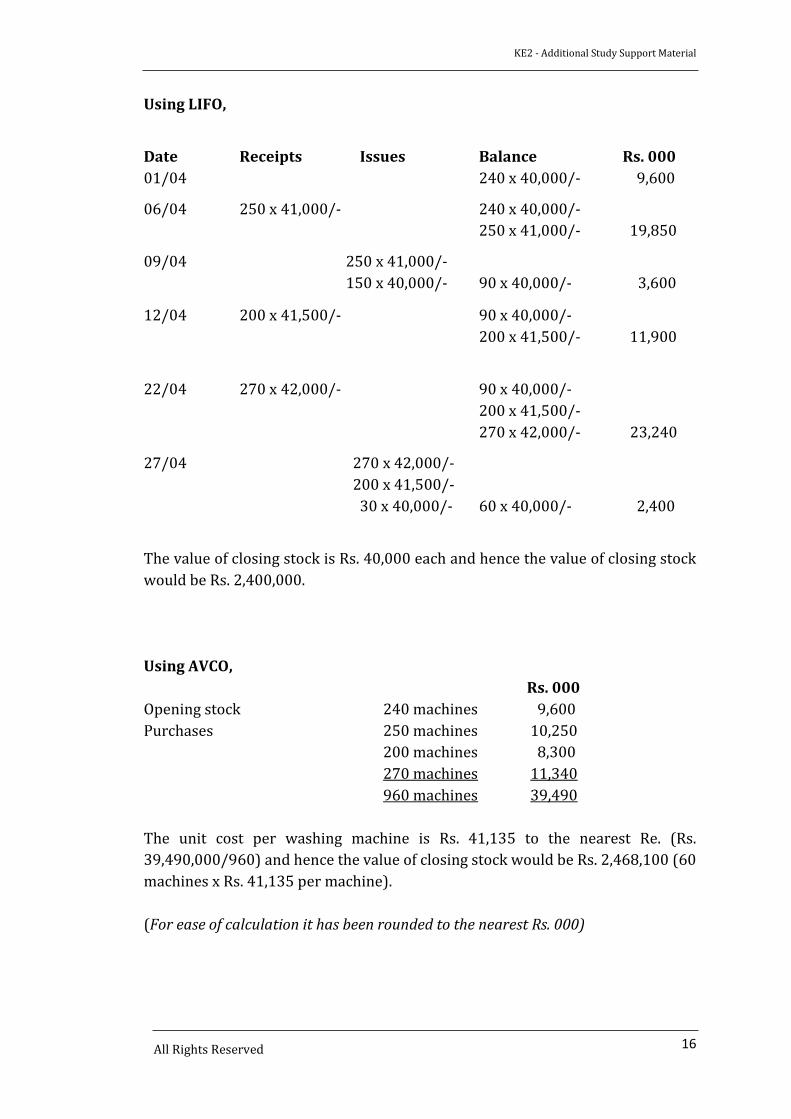

Using LIFO,

Date Receipts Issues Balance Rs. 000

01/04 240 x 40,000/- 9,600

06/04 250 x 41,000/- 240 x 40,000/-

250 x 41,000/- 19,850

09/04 250 x 41,000/-

150 x 40,000/- 90 x 40,000/- 3,600

12/04 200 x 41,500/- 90 x 40,000/-

200 x 41,500/- 11,900

22/04 270 x 42,000/- 90 x 40,000/-

200 x 41,500/-

270 x 42,000/- 23,240

27/04 270 x 42,000/-

200 x 41,500/-

30 x 40,000/- 60 x 40,000/- 2,400

The value of closing stock is Rs. 40,000 each and hence the value of closing stock

would be Rs. 2,400,000.

Using AVCO,

Rs. 000

Opening stock 240 machines 9,600

Purchases 250 machines 10,250

200 machines 8,300

270 machines 11,340

960 machines 39,490

The unit cost per washing machine is Rs. 41,135 to the nearest Re. (Rs.

39,490,000/960) and hence the value of closing stock would be Rs. 2,468,100 (60

machines x Rs. 41,135 per machine).

(For ease of calculation it has been rounded to the nearest Rs. 000)

KE2 - Additional Study Support Material

17 All Rights Reserved

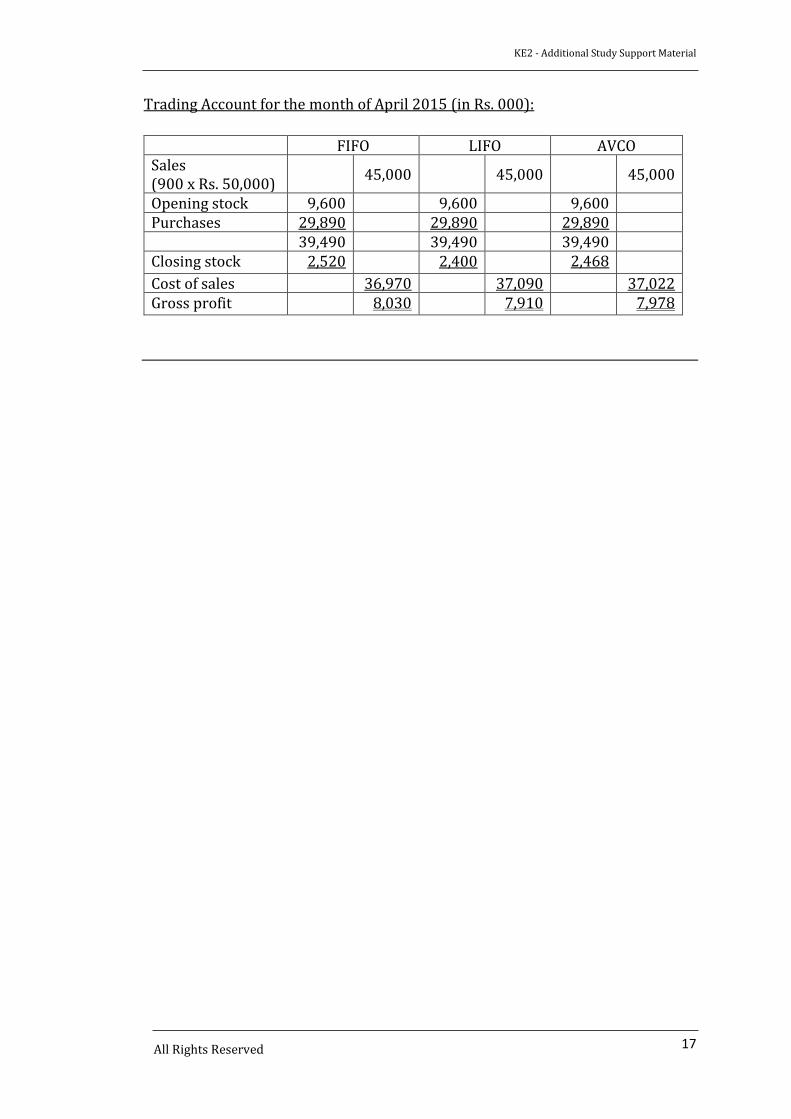

Trading Account for the month of April 2015 (in Rs. 000):

FIFO LIFO AVCO Sales (900 x Rs. 50,000)

45,000 45,000 45,000

Opening stock 9,600 9,600 9,600

Purchases 29,890 29,890 29,890

39,490 39,490 39,490

Closing stock 2,520 2,400 2,468

Cost of sales 36,970 37,090 37,022

Gross profit 8,030 7,910 7,978

KE2 - Additional Study Support Material

18

All Rights Reserved

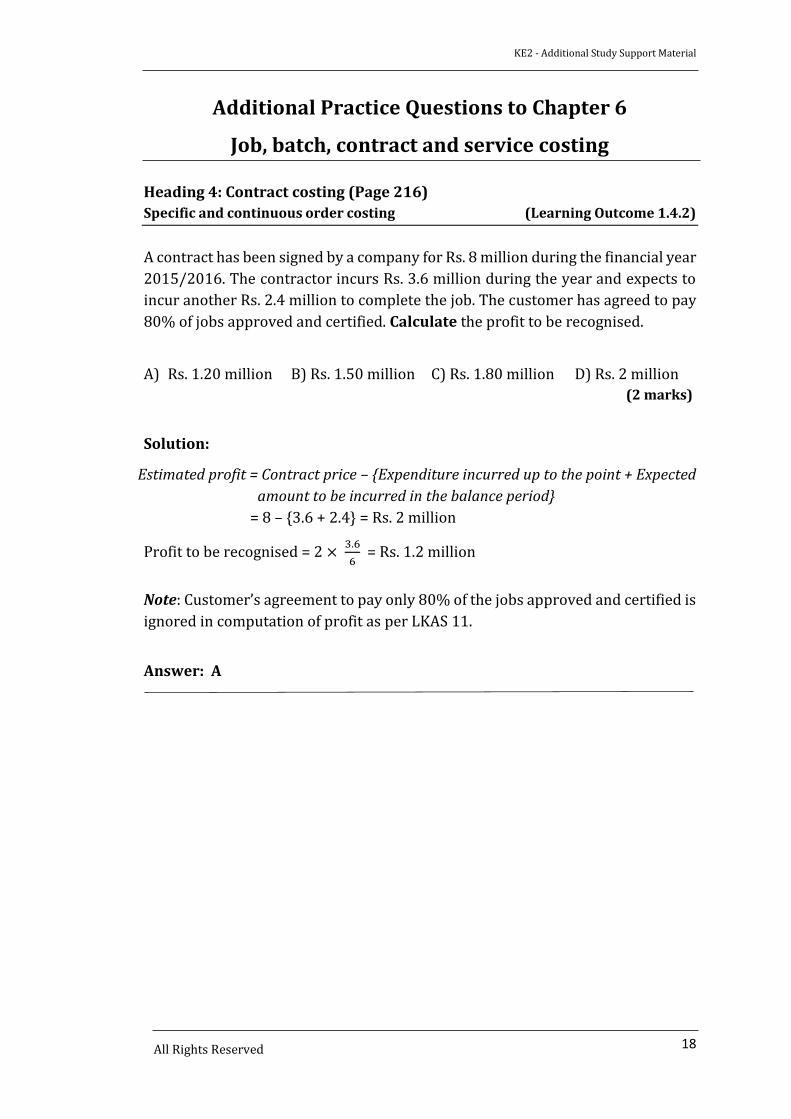

Additional Practice Questions to Chapter 6

Job, batch, contract and service costing

Heading 4: Contract costing (Page 216)

Specific and continuous order costing (Learning Outcome 1.4.2)

A contract has been signed by a company for Rs. 8 million during the financial year

2015/2016. The contractor incurs Rs. 3.6 million during the year and expects to

incur another Rs. 2.4 million to complete the job. The customer has agreed to pay

80% of jobs approved and certified. Calculate the profit to be recognised.

A) Rs. 1.20 million B) Rs. 1.50 million C) Rs. 1.80 million D) Rs. 2 million

(2 marks)

Solution:

Estimated profit = Contract price – {Expenditure incurred up to the point + Expected

amount to be incurred in the balance period}

= 8 – {3.6 + 2.4} = Rs. 2 million

Profit to be recognised = 2 × 3.6

6 = Rs. 1.2 million

Note: Customer’s agreement to pay only 80% of the jobs approved and certified is

ignored in computation of profit as per LKAS 11.

Answer: A

KE2 - Additional Study Support Material

19

All Rights Reserved

Additional Practice Questions to Chapter 9

Normal Distribution and Sampling Distributions

Sub Heading 6.4: Estimation of parameters: Confidence intervals (Page 325)

Sampling technique – Confidence interval (Learning Outcome 2.5.1)

1. The Municipal Council of a city is considering how it should change a derelict

site to a peoples’ leisure centre. Three proposals have been put forward by its

board members, for which the Council decides to ascertain people’s opinion

through a sample survey. The sample includes 900 people of the city

population. Preferences expressed by the sample are as follows:

Number of people

Public Park 360

Performing Art Centre 240

Cricket Ground 300

Required:

i) Calculate the confidence interval

&

ii) Interpret the results in each case in the situations given below.

a) The proportion of the city population that prefers the Cricket Ground at

95% level.

(5 marks)

b) The number of the city population that prefers the Performing Art Centre

at 99% level, assuming a city population of 500,000 people.

(5 marks)

(Total 10 marks)

Solution:

a) i. Confidence interval for population proportion at any given level is

𝑃 = 𝑝 ± 𝑍 × 𝑆𝐸𝑃

The proportion of people in the sample who prefer Cricket Grounds is 300

900 = ⅓.

𝑝 = ⅓ SEP =√⅓×⅔

900 = 0.0157 (approx.) and at 95% level Z = 1.96

𝑃 = 𝑝 ± 𝑍 × 𝑆𝐸𝑃

KE2 - Additional Study Support Material

20

All Rights Reserved

P = ⅓ ± 1.96 × 0.0157

Hence, P = 0.303 – 0.364

P = 30.3% - 36.4%

ii.Interpretation: We are 95% certain that between 30.3% and 36.4% of the

city population prefer a Cricket Ground built in that land.

b) 𝑖. 𝑃 = 𝑝 ± 𝑍 × 𝑆𝐸𝑃

The proportion of people in the sample that prefers Performing Art Centre

is 240

900 =

4

15.

𝑝 = 4

15 SEP =√

4

15 ×

11

15

900 = 0.0147 (approx.) and at 99% level Z = 2.58

𝑃 = 𝑝 ± 𝑍 × 𝑆𝐸𝑃

P = 4

15 ± 2.58 × 0.0147

Hence, P = 0.2287 – 0.3046

P = 22.87% - 30.46%

So, the number of people in the city population that prefers Performing Art

Centre is as follows:

= (22.87% - 30.46%) × 500,000

= 114,350 – 152,300

ii.Interpretation: We are 99% sure that between 114,350 and 152,300 in the city

population go for Performing Art Centre.

KE2 - Additional Study Support Material

21

All Rights Reserved

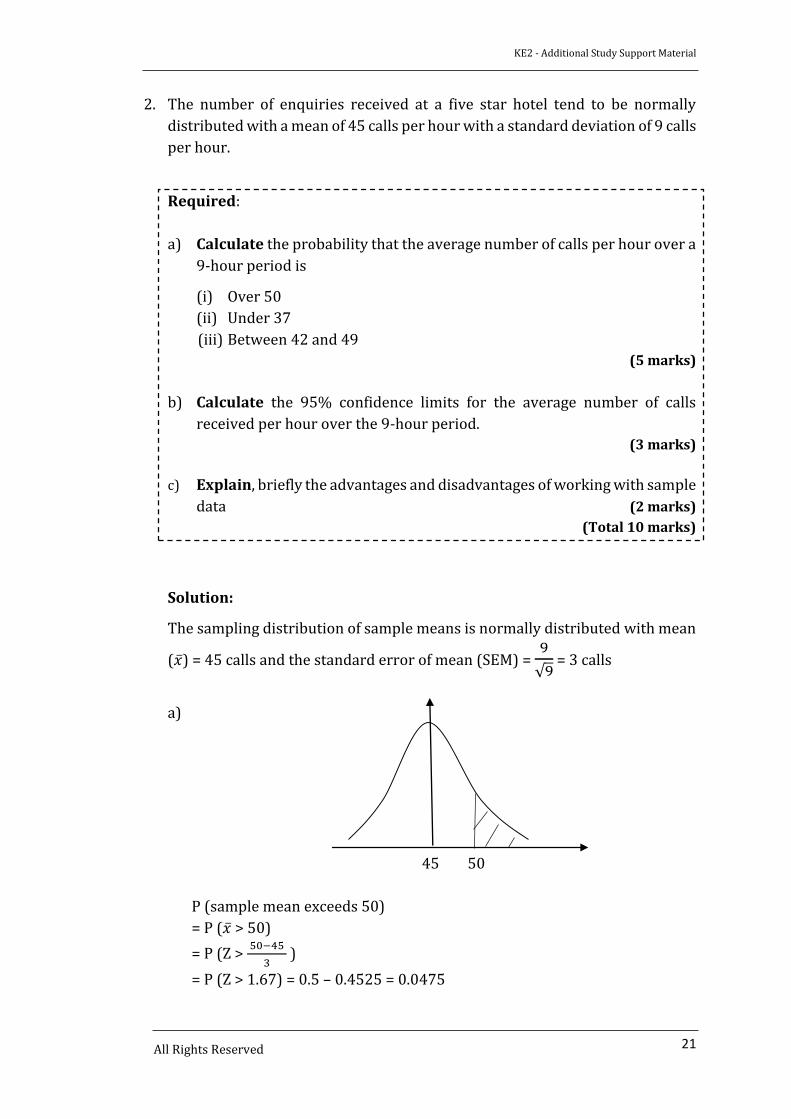

2. The number of enquiries received at a five star hotel tend to be normally

distributed with a mean of 45 calls per hour with a standard deviation of 9 calls

per hour.

Required:

a) Calculate the probability that the average number of calls per hour over a

9-hour period is

(i) Over 50

(ii) Under 37

(iii) Between 42 and 49

(5 marks)

b) Calculate the 95% confidence limits for the average number of calls

received per hour over the 9-hour period.

(3 marks)

c) Explain, briefly the advantages and disadvantages of working with sample

data (2 marks)

(Total 10 marks)

Solution:

The sampling distribution of sample means is normally distributed with mean

(�̅�) = 45 calls and the standard error of mean (SEM) = 9

√9 = 3 calls

a)

45 50

P (sample mean exceeds 50)

= P (�̅� > 50)

= P (Z > 50−45

3 )

= P (Z > 1.67) = 0.5 – 0.4525 = 0.0475

KE2 - Additional Study Support Material

22

All Rights Reserved

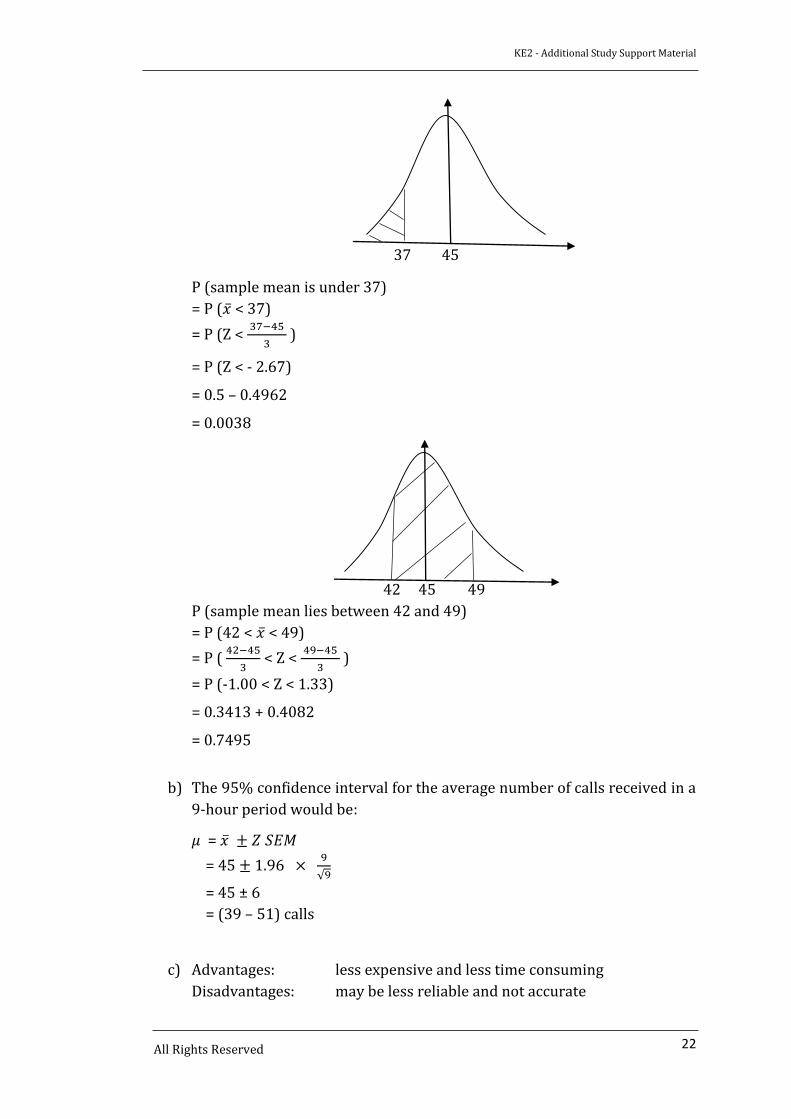

37 45

P (sample mean is under 37)

= P (�̅� < 37)

= P (Z < 37−45

3 )

= P (Z < - 2.67)

= 0.5 – 0.4962

= 0.0038

42 45 49

P (sample mean lies between 42 and 49)

= P (42 < �̅� < 49)

= P ( 42−45

3 < Z <

49−45

3 )

= P (-1.00 < Z < 1.33)

= 0.3413 + 0.4082

= 0.7495

b) The 95% confidence interval for the average number of calls received in a

9-hour period would be:

𝜇 = �̅� ± 𝑍 𝑆𝐸𝑀

= 45 ± 1.96 × 9

√9

= 45 ± 6

= (39 – 51) calls

c) Advantages: less expensive and less time consuming

Disadvantages: may be less reliable and not accurate

KE2 - Additional Study Support Material

23

All Rights Reserved

Sub Heading- 7.2 Breakeven analysis

Page No. 329

The word “point” needs to be corrected as “Profit”. Corrected profit/volume

chart is given below.

Profit

KE2 - Additional Study Support Material

24

All Rights Reserved

Sub Heading 6.4: Estimation of parameters: Confidence intervals (Page 325)

Sampling technique – Confidence interval (Learning Outcome 2.5.1)

Chapter 18

Forecasting for budgeting (Learning Outcome 7.2.2)

Lankan Automobiles PLC

Lankan Automobiles PLC operates a chain of garages in three major cities,

Colombo, Kandy and Galle. The company’s business include car hire, servicing,

repairs and petrol sales. It operates for 50 weeks a year, closing for one week in

December from Christmas to New Year and another one week in April for Sinhala

& Tamil New Year.

Car Servicing Departments

Lankan Automobiles PLC is concerned about the number of errors which seems to

be made on customers’ service bills in the pricing of replacement items such as oil

filters, engine oil, brake shoes, fan and A/C belts etc. The car servicing

departments of the three garages in Colombo, Kandy and Galle had an internal

audit last week. The internal audit included 100% investigation on 10% of its

invoices in the last month.

Some of the findings of the internal audit were as follows:

Colombo Kandy Galle

Number of invoices checked 144 64 49

Number of items on invoices 444 135 90

Number of items with error 40 15 10

Average (mean) value of error +Rs. 800 +Rs. 200 - Rs. 120

Standard deviation Rs. 84 Rs. 40 Rs. 35

(A plus mean value shows over charging and a minus under charging)

Hire Cars

Two types of fleets are used for this service, Maruti Suzuki Swift (S) and Maruti

Suzuki Ritz (R).

The new vehicle of both types cost the same. The company has 5 cars of each type.

The Management Accountant of the firm has already obtained a relationship

between the age (X) of a vehicle in months and its market value (Y) in Rs. million

for each type of fleet using the least squares method of regression analysis. Given

below are age and market value of each vehicle of each type.

KE2 - Additional Study Support Material

25

All Rights Reserved

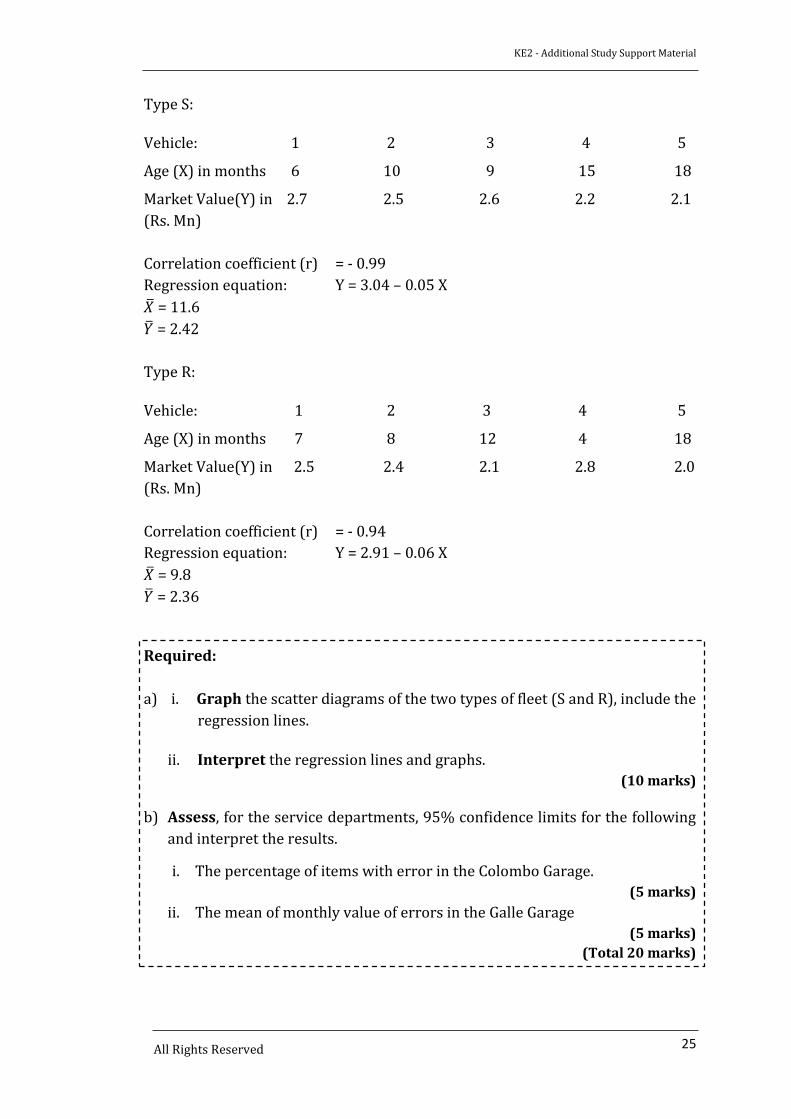

Type S:

Vehicle: 1 2 3 4 5

Age (X) in months 6 10 9 15 18

Market Value(Y) in 2.7 2.5 2.6 2.2 2.1

(Rs. Mn)

Correlation coefficient (r) = - 0.99

Regression equation: Y = 3.04 – 0.05 X

�̅� = 11.6

�̅� = 2.42

Type R:

Vehicle: 1 2 3 4 5

Age (X) in months 7 8 12 4 18

Market Value(Y) in 2.5 2.4 2.1 2.8 2.0

(Rs. Mn)

Correlation coefficient (r) = - 0.94

Regression equation: Y = 2.91 – 0.06 X

�̅� = 9.8

�̅� = 2.36

Required:

a) i. Graph the scatter diagrams of the two types of fleet (S and R), include the

regression lines.

ii. Interpret the regression lines and graphs.

(10 marks)

b) Assess, for the service departments, 95% confidence limits for the following

and interpret the results.

i. The percentage of items with error in the Colombo Garage.

(5 marks)

ii. The mean of monthly value of errors in the Galle Garage

(5 marks)

(Total 20 marks)

KE2 - Additional Study Support Material

26

All Rights Reserved

Solution:

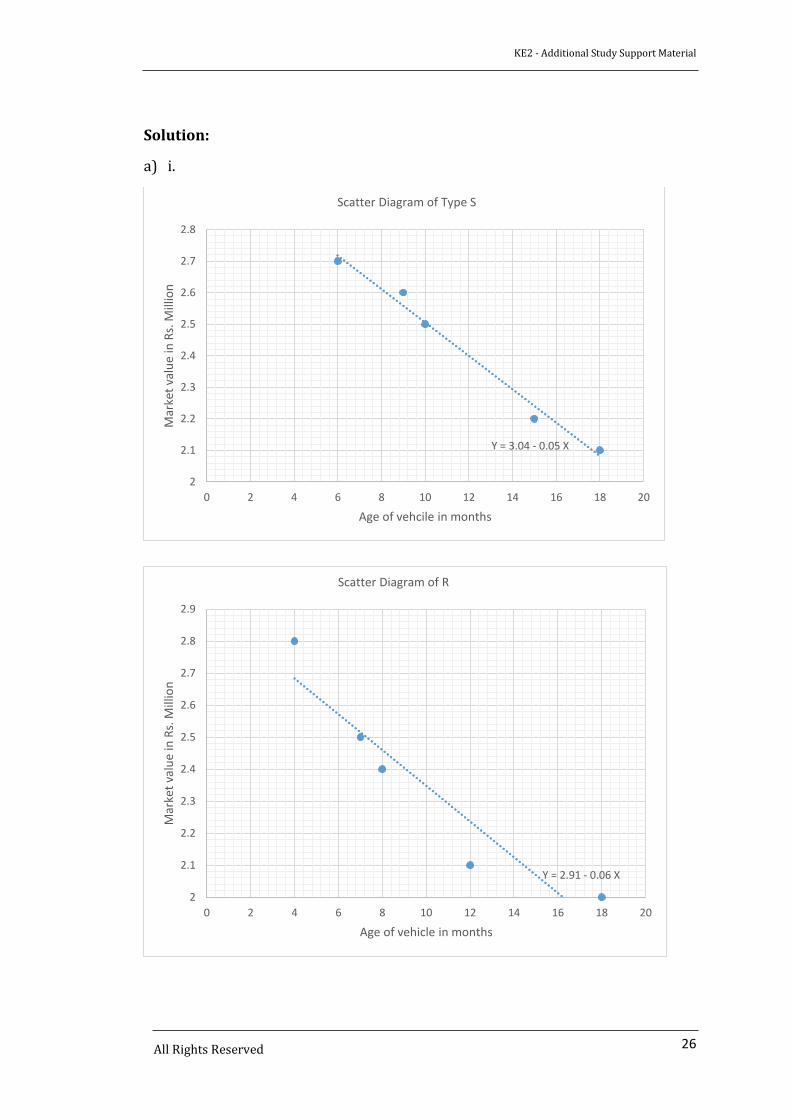

a) i.

Y = 3.04 - 0.05 X

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

0 2 4 6 8 10 12 14 16 18 20

Mar

ket

valu

e in

Rs.

Mill

ion

Age of vehcile in months

Scatter Diagram of Type S

Y = 2.91 - 0.06 X

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

0 2 4 6 8 10 12 14 16 18 20

Mar

ket

valu

e in

Rs.

Mill

ion

Age of vehicle in months

Scatter Diagram of R

KE2 - Additional Study Support Material

27

All Rights Reserved

ii. Interpretation:

If we notice the two scatter diagrams, we can notice that the relationship between

age and market value is stronger for type S than type R as the points are closer to

the regression lines and also the value of r shows it. The regression line of type S

{Y = 3.04 + 0.05 X} indicates that a brand new vehicle of this type would cost

Rs. 3,040,000 and the market value drops by Rs. 50,000 every month. Similarly the

regression line of type R {Y = 2.91 – 0.06 X} shows that a brand new vehicle of this

type would cost Rs. 2,910,000 and the market value drops by Rs. 60,000 every

month.

b)

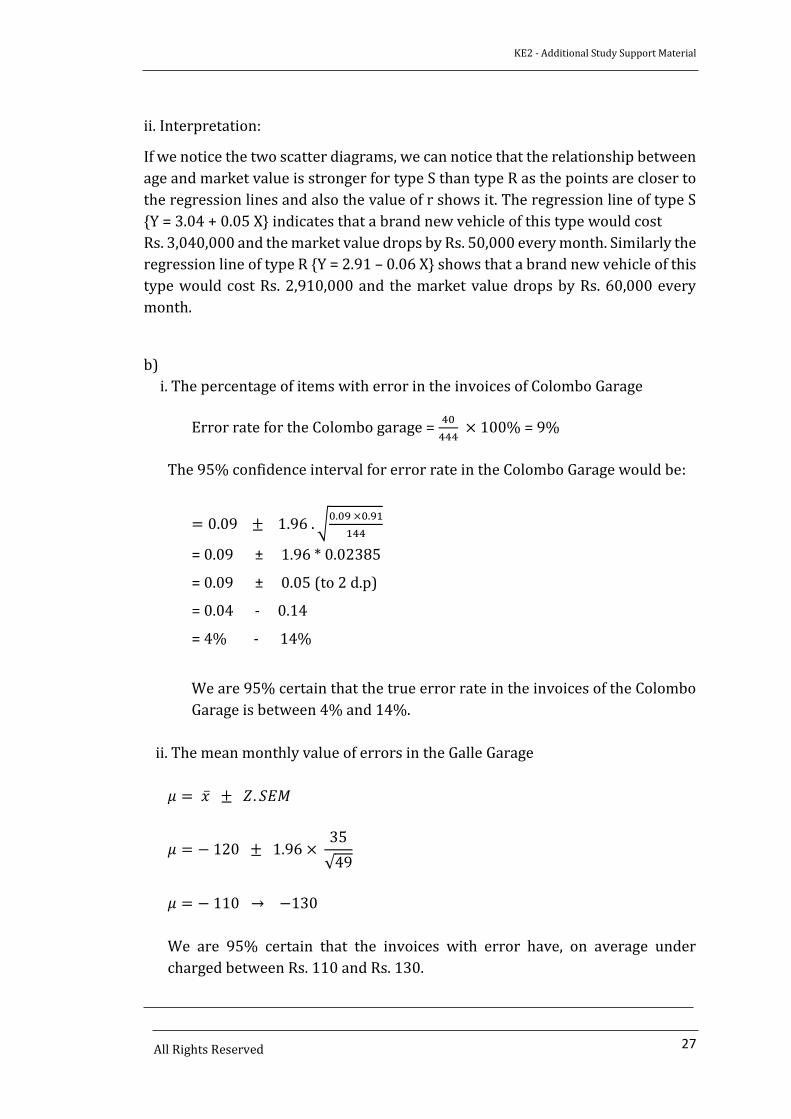

i. The percentage of items with error in the invoices of Colombo Garage

Error rate for the Colombo garage = 40

444 × 100% = 9%

The 95% confidence interval for error rate in the Colombo Garage would be:

= 0.09 ± 1.96 . √0.09 ×0.91

144

= 0.09 ± 1.96 * 0.02385

= 0.09 ± 0.05 (to 2 d.p)

= 0.04 - 0.14

= 4% - 14%

We are 95% certain that the true error rate in the invoices of the Colombo

Garage is between 4% and 14%.

ii. The mean monthly value of errors in the Galle Garage

𝜇 = �̅� ± 𝑍. 𝑆𝐸𝑀

𝜇 = − 120 ± 1.96 × 35

√49

𝜇 = − 110 → −130

We are 95% certain that the invoices with error have, on average under

charged between Rs. 110 and Rs. 130.

KE2 - Additional Study Support Material

28

All Rights Reserved

Additional Contents to Chapter 10

Accounting for Overheads

Heading 7: Over and under absorption of overheads (Page 364)

Absorption costing and marginal costing – Accounting of under/over-absorbed

overheads (Learning Outcome 3.1.2)

The accounting treatment of under/over absorption of overheads could be done

in one of the following ways:

a) Using supplementary rates:

It is calculated by dividing the under or over absorbed amount by the amount

absorbed and expressed as a percentage. Under absorption is adjusted by the

plus percentage and over absorption by the minus percentage.

b) By writing off to the Costing P & L Account:

The amount of under or over-absorption at the end of the accounting period is

transferred to the Costing Profit and Loss Account. Since the under or over

absorbed is transferred directly to Costing P & L, it will distort the value of

stock by the amount of under or over-absorption of overheads.

c) Under or over absorption will be taken in the accounts in to the subsequent

Year.

KE2 - Additional Study Support Material

29

All Rights Reserved

Additional Contents to Chapter 11

Absorption, marginal and activity based costing

Heading 7: Calculating product costs using ABC (Page 389) The steps involved in ABC (Learning Outcome 3.2.2)

An ABC system would be developed by analysing the causes of overhead costs as

a function of the support activities carried out within the organisation. These cost

drivers are then used to apportion costs in a meaningful way to the different

products produced in a multi-product organisation.

Steps involved with ABC approach:

Let us explain the steps with activity based costing approach taking a simple

example given below:

Example:

A company produces four products, AYE, BEE, CEE and DEE. The standard cost

card of the 4 products is shown below:

AYE BEE CEE DEE

Rs Rs Rs Rs

Material 1,200 1,500 800 1,000

Labour (at Rs. 600 per hour) 1,800 1,500 900 1,200

Production overhead absorbed 1,500 1,250 750 1,000

Standard cost per unit 4,500 4,250 2,450 3,200

Quantity produced (in units) 8,000 6,000 10,000 5,000

In the above cost card, production overhead has been absorbed on the basis of

labour hours.

The accountant of the firm is keen to introduce ABC since there is great diversity

in the product range. He has identified only two major cost pool for production

overhead. They are Machine set-ups and quality assurance for which the cost

drivers are identified as purchase orders and number of batches produced. The

cost associated with the above cost pools are as follows:

Quality assurance Rs. 12,000,000

Machine set-up Rs. 20,000,000

Rs. 32,000,000

KE2 - Additional Study Support Material

30 All Rights Reserved

Further relevant information on the four products are as follows:

AYE BEE CEE DEE

Number of purchase orders 800 700 900 600

Number of batches produced 80 40 80 50

Required:

Calculate the activity based standard cost of production per unit for the four

products.

Solution:

If we consider the steps mentioned in Chapter 11, heading 7

Step 1: Identify the major production related activities and the cost of

these activities

In this example the production related activities are quality assurance and machine set-up.

Step 2: Identify the cost drivers. It provides an explanation of the size of

the cost pool.

The cost drivers for the two production related activities have been

identified as number of purchase orders and number of batches

produced.

Step 3: Record the cost of each activity into cost pools

Cost pools are quality assurance and machine set-ups for which the

amounts are Rs. 12 million and Rs. 20 million.

Step 4: Charge support overheads to products on the basis of their usage of

the activity.

Calculate a cost driver rate for each activity cost pool in the same

way as an overhead is calculated with the traditional approach and

then use the rates to products to arrive at an activity based product

cost.

Cost driver rate:

- Quality assurance = 𝑅𝑠.12,000,000

3,000 𝑜𝑟𝑑𝑒𝑟𝑠= Rs. 4,000

- Machine set-up = 𝑅𝑠.20,000,000

250 𝑠𝑒𝑡−𝑢𝑝𝑠= Rs. 80,000

KE2 - Additional Study Support Material

31 All Rights Reserved

AYE BEE CEE DEE

Rs. Rs. Rs. Rs. Quality assurance

𝑅𝑠.4,000 × 800

8,000400

𝑅𝑠.4,000 ×700

6,000467

𝑅𝑠.4,000 × 900

10,000360

𝑅𝑠.4,000 × 600

5,000480

Machine set-up 𝑅𝑠. 80,000 ×80

8,000 800

𝑅𝑠. 80,000 ×40

6,000 533

𝑅𝑠. 80,000 ×80

10,000 640

𝑅𝑠. 80,000 ×50

5,000 800

1,200 1,000 1,000 1,280

AYE BEE CEE DEE

Rs. Rs. Rs. Rs.

Material 1,200 1,500 800 1,000

Labour (at Rs. 600 per hour) 1,800 1,500 900 1,200

Activity based production overhead 1,200 1,000 1,000 1,280

Standard cost per unit 4,200 4,000 2,700 3,480

KE2 - Additional Study Support Material

32 All Rights Reserved

Additional Practice Questions to Chapter 12

Financial Mathematics for Business

Amortisation Schedule (Learning Outcome 4.1.1)

An Amortisation Schedule is a statement which shows the outstanding amount

of a loan, period by period. The amount of repayment can be either calculated in

which case every repayment from the first to the final is the same and it covers the

principal amount and the interest, or as agreed by the two parties in which case

every payment is the same except for the final payment which is the balance due

on the loan at the end.

Question: Spotlight PLC is a firm which deals with N-Computing. N-computing is where one server machine is used by more than one users at a time through N-Computing units, thus it reduces the power consumption and the capital cost. ABC Ltd, a small company, wishes to buy an 8-user N-computing set for Rs. 250,000. ABC Ltd has agreed to pay a deposit of Rs. 100,000 and to set off the balance payment by instalments of Rs. 50,000 per year, payable at the end of each year. Interest is charged on the outstanding balance at 10% per year.

Required:

a) Draw up a schedule of the payments until the debt is paid off.

(3 marks)

b) State the number of full payments of Rs. 35,000 is made and the value of the

final payment

(1 marks)

c) State the amount paid in total for the computer

(1 marks)

ABC Ltd is facing a financial crisis at present and therefore is unable to pay a big

annual instalment of Rs. 50,000 for the next four years. Spotlight PLC has decided

to help ABC Ltd to obtain the N-computing units immediately but pay for it after 4

years with no interest.

ABC Ltd management has requested the Accountant to open a reserve fund

account so that it can deposit a fixed amount every quarter for 16 quarters, the

first one now.

The reserve fund will earn compound interest of 2% per quarter. At the end of 4

years ABC Ltd can withdraw the whole amount and settle the due.

d) Calculate the amount of quarterly deposits.

(5 marks)

(Total 10 marks)

KE2 - Additional Study Support Material

33 All Rights Reserved

Solution:

a)

Year Amount at the

Beginning

(Rs.)

Interest

payable

(Rs.)

Installments

(Rs.)

Amount at

the end

(Rs.)

1 150,000 15,000 (50,000) 115,000

2 115,000 11,500 (50,000) 76,500

3 76,500 7,650 (50,000) 34,150

4 34,150 3,415 (37,565) NIL

b) There are 3 full payments of Rs. 50,000 and the final payment is Rs. 37,565.

c) Total amount paid for the computer,

Rs. 100,000 + (3 * Rs. 50,000) + Rs. 37,565 = Rs. 287,565

d) Assume that each quarterly investment deposit is Rs. A then

250,000 = 𝐴 × 1.02 × (1.0216 − 1)

(1.02 − 1)

A = (250,000 ×0.02)

{1.02 ×(1.0216−1)}

A = Rs. 13,150 (approx.)

KE2 - Additional Study Support Material

34 All Rights Reserved

Additional Practice Questions to Chapter 16

Mathematics for Business Functions

Heading 8: The profit-maximising price/output level

Average cost minimisation (Learning Outcome 6.2.1)

1. On a certain ferry it has been observed that the running costs per km, C are

directly proportional to the square of the sailing speed. It can be considered as

C = 𝑘 × 𝑥2, where k is a constant and 𝑥 is the sailing speed. From experience

and it is known that C = Rs. 27,000 per km when the speed is 30 km per hour.

In addition, there are other costs of Rs. 1,000 per hour, regardless of the ferry

speed. Every week the ferry makes 10 journeys of 81 km up and down.

Required

Assess the following requirements:

a) A mathematical expression for the cost of a journey of 60 km at 𝑥 km per

hour in terms of 𝑥.

(4 marks)

b) The most economical sailing speed for the ferry and the total cost for that

journey at that speed.

(6 marks)

(Total 10 marks)

Solution:

a) Total weekly cost = Running costs + Other costs

To estimate the running cost, the constant k should be identified. This is

possible from the equation C = 𝑘 × 𝑥2

27,000 = k (900), and hence, k = 30

This implies running costs are = 30 𝑥2

Other costs depend upon the sailing time. When the ferry sails at

𝑥 𝑘𝑚 𝑝𝑒𝑟 ℎ𝑜𝑢𝑟 time taken for a journey (up and down) would be 81

𝑥 hours

and so other costs per journey = 81,000

𝑥

Therefore weekly other costs would be810,000

𝑥

Total weekly costs (C) = 30 𝑥2 + 810,000

𝑥

KE2 - Additional Study Support Material

35 All Rights Reserved

C = 30 𝑥2 + 810,000

𝑥

𝑑𝐶

𝑑𝑥= 30𝑥 –

810,000

𝑥2

At turning points, 𝑑𝐶

𝑑𝑥 = 0 and so 30𝑥 –

810,000

𝑥2= 0

This implies that 30 𝑥3 = 810,000

𝑥3 = 27,000

𝑥 = 30 km per hour

The turning point is minima as 𝑑2𝐶

𝑑𝑥> 0

Hence, the most economical speed is 30 km per hour.

When 𝑥 = 30 total weekly cost would be 30 (302) + 810,000

30= Rs. 54,000 per week.

2. Covering L.O 6.2.1

a) The costs of a company consist of variable costs, semi-variable costs

and fixed costs. The relationship of capacity utilisation to costs can be

expressed as:

AC = 125 U + 32

𝑈2 + 300 where AC is the average cost per unit in Rs.

and U is the capacity utilisation proportion.

Required

Calculate the percentage capacity utilisation which will give the least

cost per unit.

(5 marks)

b) The cost of producing a product is described by the function givenbelow.

C = 1280 − 560 𝑥 + 0.2𝑥2 (in Rs. 000)

i. Calculate the level of production which minimises the averagecost.

(3 marks) ii. Calculate the cost of producing the 151st unit.

(2 marks) (Total 10 marks)

b) Minimise the total weekly costs:

KE2 - Additional Study Support Material

36 All Rights Reserved

Solution:

a) AC = 125 U + 32

𝑈2 + 3

𝑑𝐴𝐶

𝑑𝑈 = 125 -

64

𝑈3

At turning point 125 - 64

𝑈3 = 0 𝑈3 = 0.512

Hence, at the minimum point of AC, U = 0.8 as 𝑑2𝐴𝐶

𝑈2 is always positive.

The average cost is minimised when 80% of the capacity is utilised.

b) (i) Since the cost function is C = 1,280 − 560 𝑥 + 0.2𝑥2 , the average cost

function would be:

AC = 1,280

𝑥 - 560 + 0.2 𝑥

𝑑𝐴𝐶

𝑑𝑥= -

1,280

𝑥2 + 0.2

At turning points 𝑑𝐴𝐶

𝑑𝑥= 0. This implies -

1,280

𝑥2 + 0.2 = 0

0.2𝑥2 = 1,280

𝑥 = 80 Units is the minima as the second derivative is positive.

(ii) MC = - 1,280

𝑥2 + 0.2

When 𝑥 = 150 MC = - 1,280

1502 + 0.2 = 0.143 (3 dp)

Cost of producing the 151st unit equals Rs. 143 (approx.)

KE2 - Additional Study Support Material

37 All Rights Reserved

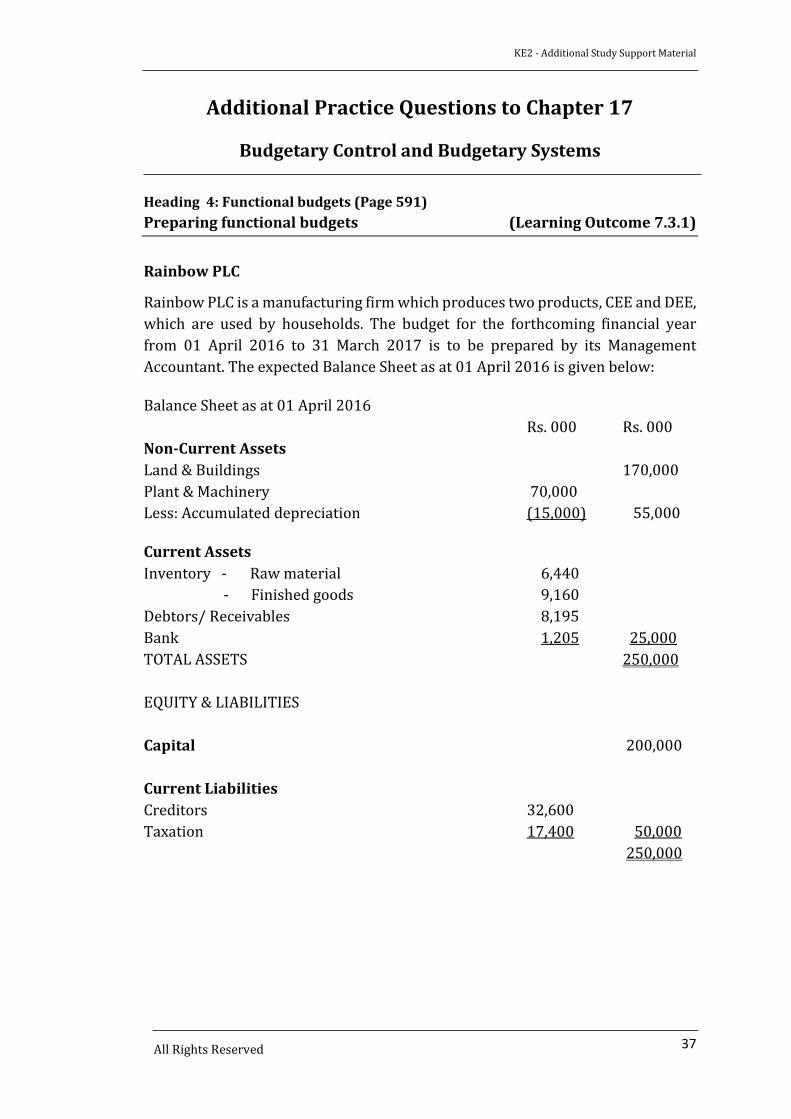

Additional Practice Questions to Chapter 17

Budgetary Control and Budgetary Systems

Heading 4: Functional budgets (Page 591)

Preparing functional budgets (Learning Outcome 7.3.1)

Rainbow PLC

Rainbow PLC is a manufacturing firm which produces two products, CEE and DEE,

which are used by households. The budget for the forthcoming financial year

from 01 April 2016 to 31 March 2017 is to be prepared by its Management

Accountant. The expected Balance Sheet as at 01 April 2016 is given below:

Balance Sheet as at 01 April 2016

Rs. 000 Rs. 000

Non-Current Assets

Land & Buildings 170,000

Plant & Machinery 70,000

Less: Accumulated depreciation (15,000) 55,000

Current Assets

Inventory - Raw material 6,440

- Finished goods 9,160

Debtors/ Receivables 8,195

Bank 1,205 25,000

TOTAL ASSETS 250,000

EQUITY & LIABILITIES

Capital 200,000

Current Liabilities

Creditors 32,600

Taxation 17,400 50,000

250,000

KE2 - Additional Study Support Material

38 All Rights Reserved

Further information is given below:

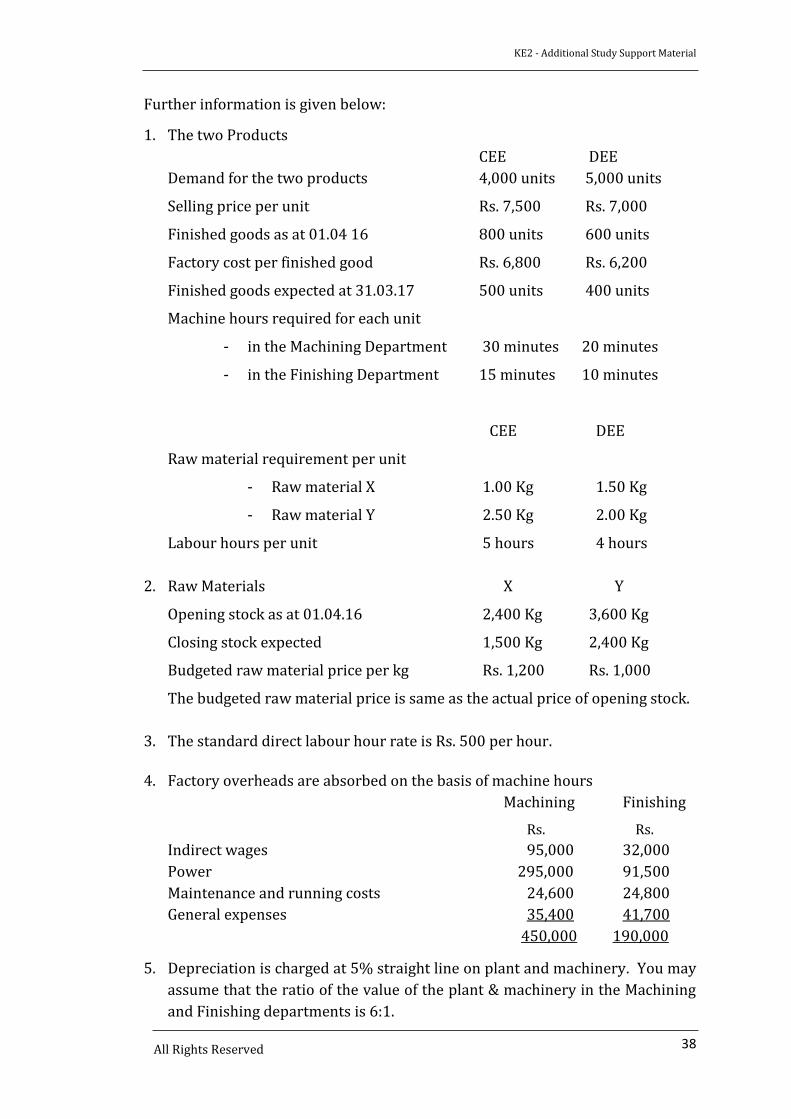

1. The two Products

CEE DEE

Demand for the two products 4,000 units 5,000 units

Selling price per unit Rs. 7,500 Rs. 7,000

Finished goods as at 01.04 16 800 units 600 units

Factory cost per finished good Rs. 6,800 Rs. 6,200

Finished goods expected at 31.03.17 500 units 400 units

Machine hours required for each unit

- in the Machining Department 30 minutes 20 minutes

- in the Finishing Department 15 minutes 10 minutes

CEE DEE

Raw material requirement per unit

- Raw material X 1.00 Kg 1.50 Kg

- Raw material Y 2.50 Kg 2.00 Kg

Labour hours per unit 5 hours 4 hours

2. Raw Materials X Y

Opening stock as at 01.04.16 2,400 Kg 3,600 Kg

Closing stock expected 1,500 Kg 2,400 Kg

Budgeted raw material price per kg Rs. 1,200 Rs. 1,000

The budgeted raw material price is same as the actual price of opening stock.

3. The standard direct labour hour rate is Rs. 500 per hour.

4. Factory overheads are absorbed on the basis of machine hours

Machining Finishing

Rs. Rs.

Indirect wages 95,000 32,000

Power 295,000 91,500

Maintenance and running costs 24,600 24,800

General expenses 35,400 41,700

450,000 190,000

5. Depreciation is charged at 5% straight line on plant and machinery. You may

assume that the ratio of the value of the plant & machinery in the Machining

and Finishing departments is 6:1.

KE2 - Additional Study Support Material

39 All Rights Reserved

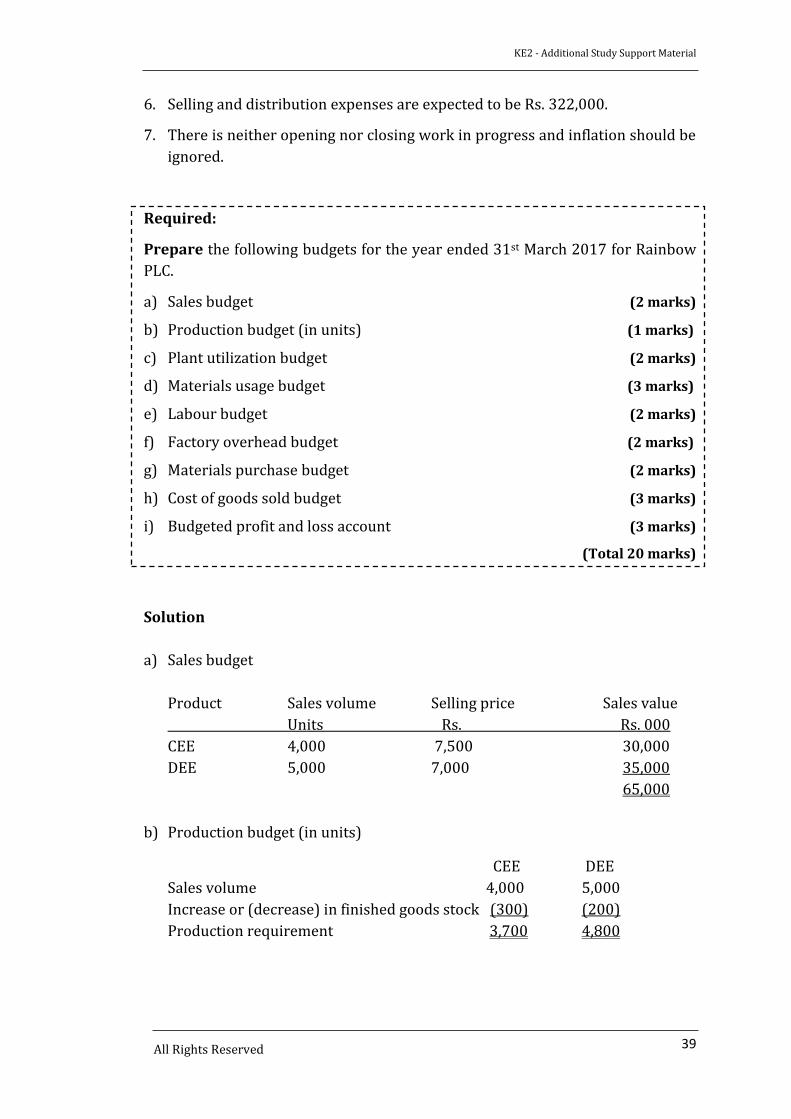

6. Selling and distribution expenses are expected to be Rs. 322,000.

7. There is neither opening nor closing work in progress and inflation should be

ignored.

Required:

Prepare the following budgets for the year ended 31st March 2017 for Rainbow

PLC.

a) Sales budget (2 marks)

b) Production budget (in units) (1 marks)

c) Plant utilization budget (2 marks)

d) Materials usage budget (3 marks)

e) Labour budget (2 marks)

f) Factory overhead budget (2 marks)

g) Materials purchase budget (2 marks)

h) Cost of goods sold budget (3 marks)

i) Budgeted profit and loss account (3 marks)

(Total 20 marks)

Solution

a) Sales budget

Product Sales volume Selling price Sales value

Units Rs. Rs. 000

CEE 4,000 7,500 30,000

DEE 5,000 7,000 35,000

65,000

b) Production budget (in units)

CEE DEE

Sales volume 4,000 5,000

Increase or (decrease) in finished goods stock (300) (200)

Production requirement 3,700 4,800

KE2 - Additional Study Support Material

40 All Rights Reserved

c) Plant utilization budget

Products Units Machining Finishing

Hours Total Hours Total

per unit hours per unit hours

CEE 3,700 ½ 1,850 ¼ 925

DEE 4,800 ⅓ 1,600 ⅙ 800

3,450 1,725

d) Materials usage budget

Raw material X Raw material Y

Required for production Kg Kg

CEE 1.0 kg × 3,700 3,700 2.5 kg × 3,700 9,250

DEE 1.5 kg × 4,800 7,200 2.0 kg × 4,800 9,600

10,900 18,850

e) Labour budget

Product Production Hours Total Rate per Total labour

Units Per unit hours hour cost (Rs. 000)

CEE 3,700 5 18,500 500/- 9,250

DEE 4,800 4 19,200 500/- 9,600

18,850

f) Factory overhead budget

Machining Finishing

Rs.000 Rs.000

As per allocated and apportioned 450 190

Depreciation (5%) 3,000 500

3,450 690

Total machine hours [As per above (c)] 3,450 hours 1,725 hours

Absorption rate per machine hour Rs. 1,000 Rs. 400

KE2 - Additional Study Support Material

41 All Rights Reserved

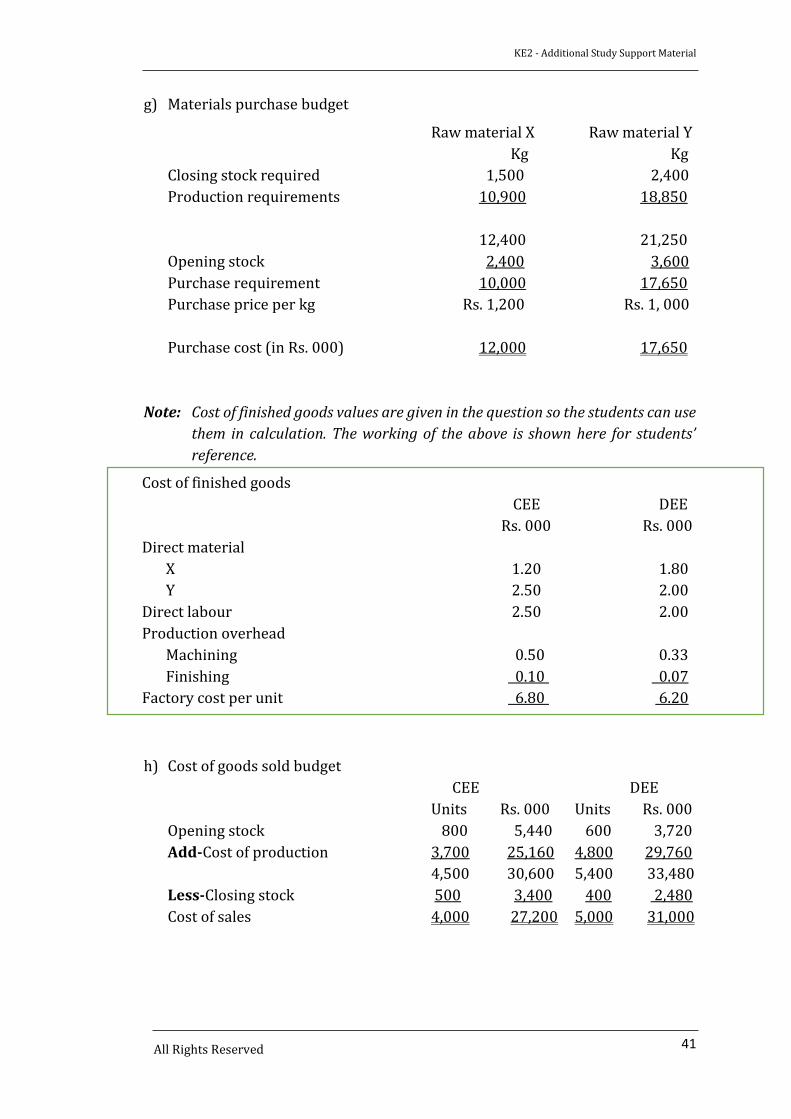

g) Materials purchase budget

Raw material X Raw material Y

Kg Kg

Closing stock required 1,500 2,400

Production requirements 10,900 18,850

12,400 21,250

Opening stock 2,400 3,600

Purchase requirement 10,000 17,650

Purchase price per kg Rs. 1,200 Rs. 1, 000

Purchase cost (in Rs. 000) 12,000 17,650

Note: Cost of finished goods values are given in the question so the students can use

them in calculation. The working of the above is shown here for students’

reference.

h) Cost of goods sold budget

CEE DEE

Units Rs. 000 Units Rs. 000

Opening stock 800 5,440 600 3,720

Add-Cost of production 3,700 25,160 4,800 29,760

4,500 30,600 5,400 33,480

Less-Closing stock 500 3,400 400 2,480

Cost of sales 4,000 27,200 5,000 31,000

Cost of finished goods

CEE DEE

Rs. 000 Rs. 000

Direct material

X 1.20 1.80

Y 2.50 2.00

Direct labour 2.50 2.00

Production overhead

Machining 0.50 0.33

Finishing 0.10 0.07

Factory cost per unit 6.80 6.20

KE2 - Additional Study Support Material

42 All Rights Reserved

i) Budgeted profit and loss account

CEE DEE Total

Rs. 000 Rs. 000 Rs. 000

Sales 30,000 35,000 65,000

Less: Cost of sales 27,200 31,000 58,200

Gross profit 2, 800 4,000 6,800

Less: Selling & Administration expenses 322

Net profit before taxation 6,478

Note: There will be no under or over absorbed production overhead in a budgeted

profit or loss account.

KE2 - Additional Study Support Material

43 All Rights Reserved

Heading 13: Rolling budgets (Page 626) Budgeting – Rolling budgets (Learning Outcme.7.1.2)

A rolling budget is a new, revised set of financial plans for the next accounting

period used to replace the prior one in a continuous budgeting system. In other

words, it’s a newly updated budget that takes the place of the old version when it

expires.

Explain the steps involved in preparing rolling budgets by giving an example of

your own.

The process of preparing a rolling budget can be explained using an example given

below:

Assume that a company has prepared a budget for the year 2016 (January –

December) by the end of 2015. It has been broken down into suitable periods (for

instance quarterly). At the end of first quarter, (31 March 2016), a comparison is

made between that quarter’s actual and the budget. The variations between the

two is analysed and the necessary corrective measures are taken into account for

the remaining period of the year. Then the first quarter of 2016 budget will be

dropped and a budget for a further quarter (first quarter of 2017) will be added

to the budget, making the budget for 4 quarters from April 2016 to March 2017.

This process will be repeated at the end of every new quarter. If a shorter period

(for example monthly) is considered it will be comparatively more tedious.

State the advantages and disadvantages of rolling budgets.

Advantages:

More accurate

Up to date

Always a budget is available for one year that extends in to the future

The impact of uncertainty would be small as it concerns with short

periods

It becomes a budget which is concerned with current developments

Disadvantages:

When budgetary targets keep on changing, it may demotivate the

employees

Since more time will be spent on preparing budgets, time available for

control over actual results and other important matters may get

curtailed

More expensive

time consuming

KE2 - Additional Study Support Material

44 All Rights Reserved

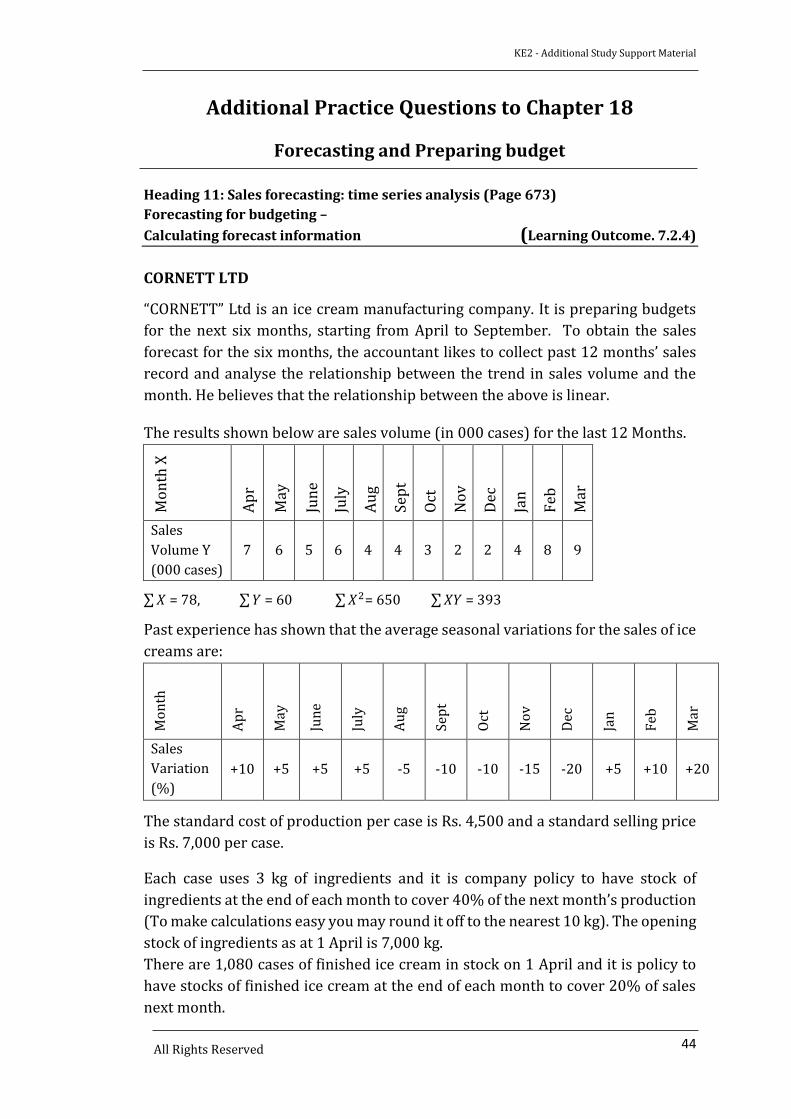

Additional Practice Questions to Chapter 18

Forecasting and Preparing budget

Heading 11: Sales forecasting: time series analysis (Page 673)

Forecasting for budgeting –

Calculating forecast information (Learning Outcome. 7.2.4)

CORNETT LTD

“CORNETT” Ltd is an ice cream manufacturing company. It is preparing budgets

for the next six months, starting from April to September. To obtain the sales

forecast for the six months, the accountant likes to collect past 12 months’ sales

record and analyse the relationship between the trend in sales volume and the

month. He believes that the relationship between the above is linear.

The results shown below are sales volume (in 000 cases) for the last 12 Months.

Mo

nth

X

Ap

r

May

Jun

e

July

Au

g

Sep

t

Oct

No

v

Dec

Jan

Feb

Mar

Sales

Volume Y

(000 cases)

7 6 5 6 4 4 3 2 2 4 8 9

∑ 𝑋 = 78, ∑ 𝑌 = 60 ∑ 𝑋2= 650 ∑ 𝑋𝑌 = 393

Past experience has shown that the average seasonal variations for the sales of ice

creams are:

Mo

nth

Ap

r

May

Jun

e

July

Au

g

Sep

t

Oct

No

v

Dec

Jan

Feb

Mar

Sales

Variation

(%)

+10 +5 +5 +5 -5 -10 -10 -15 -20 +5 +10 +20

The standard cost of production per case is Rs. 4,500 and a standard selling price

is Rs. 7,000 per case.

Each case uses 3 kg of ingredients and it is company policy to have stock of

ingredients at the end of each month to cover 40% of the next month’s production

(To make calculations easy you may round it off to the nearest 10 kg). The opening

stock of ingredients as at 1 April is 7,000 kg.

There are 1,080 cases of finished ice cream in stock on 1 April and it is policy to

have stocks of finished ice cream at the end of each month to cover 20% of sales

next month.

KE2 - Additional Study Support Material

45

All Rights Reserved

Required:

a) Calculate the least squares regression equation for the trend in sales volume,

assuming the relationship between the sales volume and month is linear.

(4 marks)

b) Calculate the sales forecast for the quarter (April – June), assuming the

multiplicative (or proportional) model of a time series. (For ease of calculations

you may round it off to the nearest 10 cases)

(3 marks)

c) Prepare a production budget (in cases) for the quarter (April – June).

(5 marks)

d) Prepare ingredients purchase budget for the quarter (April – June).

(5 marks)

e) Assess the budgeted gross profit for the quarter (April-June).

(3 marks)

(Total 20 marks)

Solution:

a) If the least square regression equation of Sales volume on month is

𝑌 = 𝑎 + 𝑏 𝑋, then the regression coefficients a and b are given as follows:

b = 𝑛×∑ 𝑋𝑌− ∑ 𝑋×∑ 𝑌

𝑛×∑ 𝑋2− (∑ 𝑋)2

b = {(12×393)−(78 ×60)}

{(12×650)− 782}

b = 0.02

Interpretation: b = 0.02 indicates that, on average, the trend in sales volume

increases by 20 cases every month

Hence, “a” would be 𝑎 = 𝑌 ̅ − 𝑏 × �̅�

𝑎 = 60

12 − 0.02 ×

78

12

𝑎 = 4.87

Interpretation: 𝑎 = 4.87 indicates that the sales volume in March last year

were 4,870 cases.

Therefore the TREND in sales volume is given by:

𝑇𝑟𝑒𝑛𝑑 = 4.87 + 0.02 𝑋

KE2 - Additional Study Support Material

46

All Rights Reserved

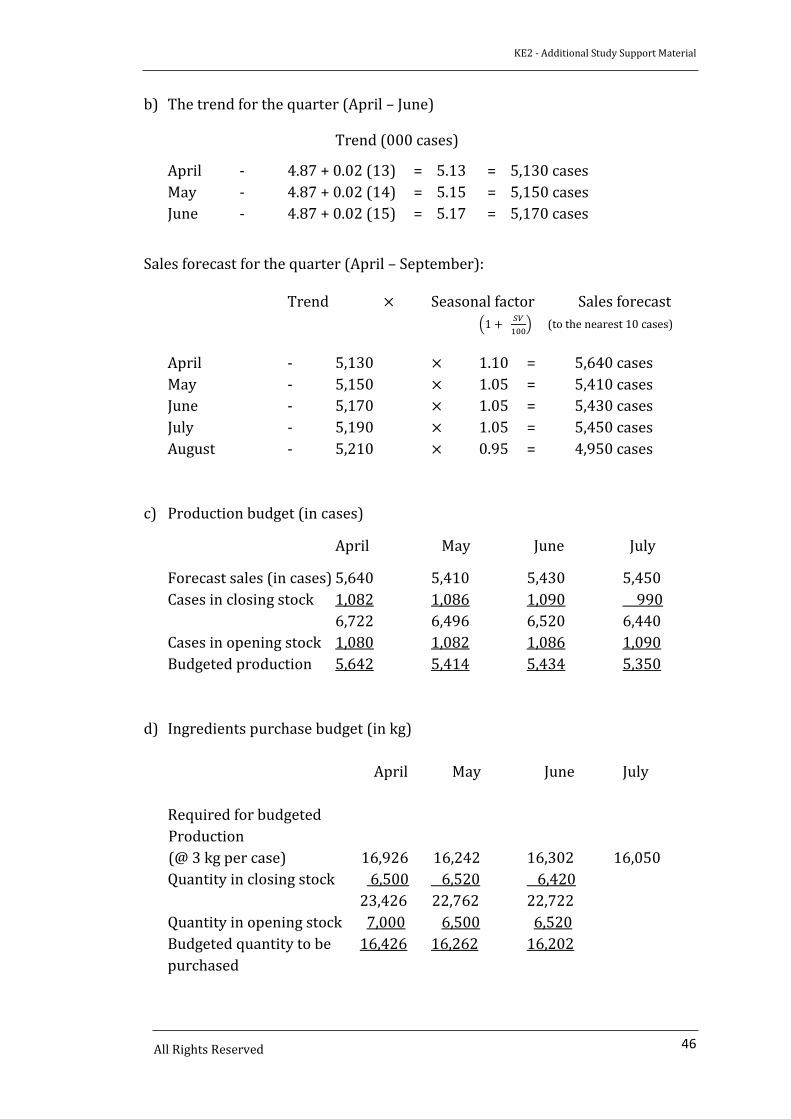

b) The trend for the quarter (April – June)

Trend (000 cases)

April - 4.87 + 0.02 (13) = 5.13 = 5,130 cases

May - 4.87 + 0.02 (14) = 5.15 = 5,150 cases

June - 4.87 + 0.02 (15) = 5.17 = 5,170 cases

Sales forecast for the quarter (April – September):

Trend × Seasonal factor Sales forecast

(1 + 𝑆𝑉

100) (to the nearest 10 cases)

April - 5,130 × 1.10 = 5,640 cases

May - 5,150 × 1.05 = 5,410 cases

June - 5,170 × 1.05 = 5,430 cases

July - 5,190 × 1.05 = 5,450 cases

August - 5,210 × 0.95 = 4,950 cases

c) Production budget (in cases)

April May June July

Forecast sales (in cases) 5,640 5,410 5,430 5,450

Cases in closing stock 1,082 1,086 1,090 990

6,722 6,496 6,520 6,440

Cases in opening stock 1,080 1,082 1,086 1,090

Budgeted production 5,642 5,414 5,434 5,350

d) Ingredients purchase budget (in kg)

April May June July

Required for budgeted

Production

(@ 3 kg per case) 16,926 16,242 16,302 16,050

Quantity in closing stock 6,500 6,520 6,420

23,426 22,762 22,722

Quantity in opening stock 7,000 6,500 6,520

Budgeted quantity to be 16,426 16,262 16,202

purchased

KE2 - Additional Study Support Material

47

All Rights Reserved

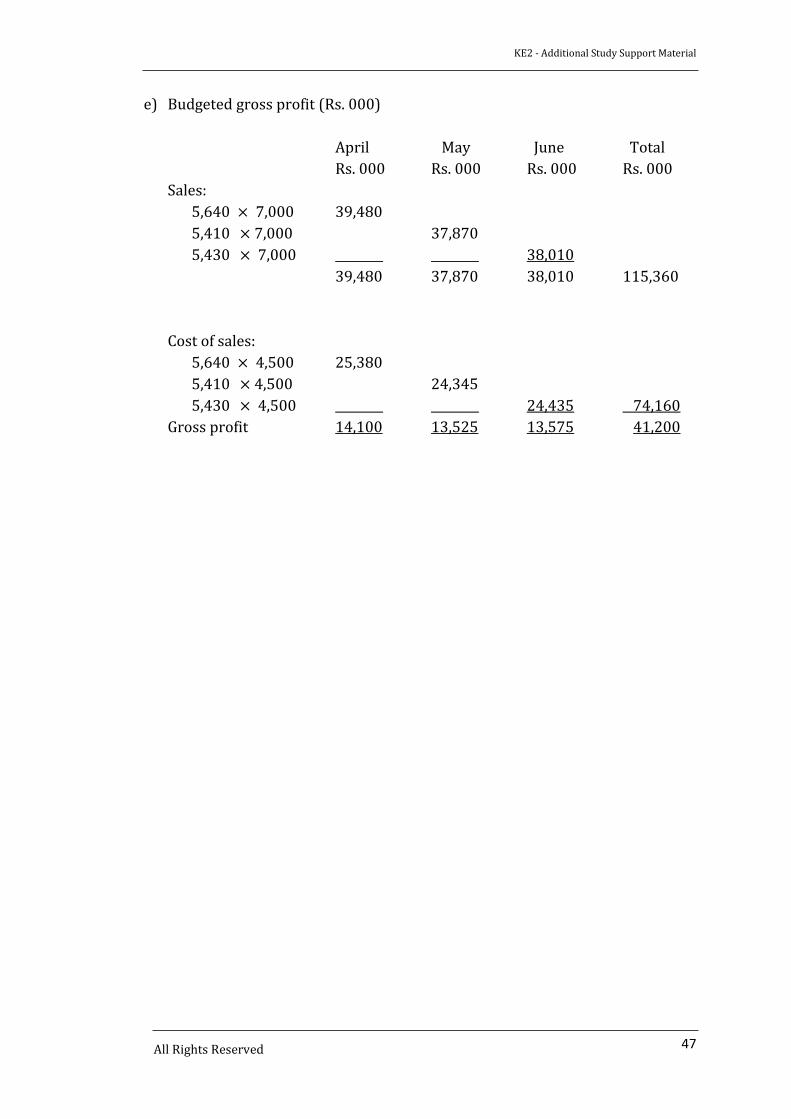

e) Budgeted gross profit (Rs. 000)

April May June Total

Rs. 000 Rs. 000 Rs. 000 Rs. 000

Sales:

5,640 × 7,000 39,480

5,410 × 7,000 37,870

5,430 × 7,000 38,010

39,480 37,870 38,010 115,360

Cost of sales:

5,640 × 4,500 25,380

5,410 × 4,500 24,345

5,430 × 4,500 24,435 74,160

Gross profit 14,100 13,525 13,575 41,200

Related Documents