© TransGraph Consulting Pvt Ltd June 07 2012 “Economic crisis, Price volatility and Indonesian tax structure” – way forward By Nagaraj Meda, Managing Director, TransGraph Consulting Pvt Ltd Brands TransGraph TransGraph Research Consulting Technology Research Consulting Technology Commodities Currencies Commodities Currencies Malaysia – India POTS 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd SlideJune 07 2012

“Economic crisis, Price volatility and Indonesian tax structure” – way forward

By Nagaraj Meda,

Managing Director, TransGraph Consulting Pvt Ltd

BrandsTransGraphTransGraph Research Consulting TechnologyResearch Consulting Technology

Commodities CurrenciesCommodities Currencies

Malaysia –

India POTS 2012

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Global Economy and Currency outlook

2

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

US Economy –

Comparatively Better off than RoW

Industrial Production has been steady during the last 2 quarters while Unemployment rate – worrisomeOperation Twist shall come to an end on June 30 and speculations are growing over its extension. Persistent higher unemployment rate is worrying the policy makers, doors remain wide open for QE3 (extension of Operation Twist) keeping in view the Presidential elections (due on 6th Nov 2012).

US to do better than RoW (Rest of World) in terms of change in growth rates

3

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Sovereign debt concerns. High chances of Greece exiting the Euro Zone in coming couple of quartersSpain’s banking crisis came afresh sending tremors across the global financial markets.Changing political dynamics – towards anti austerity might lead to Partial implementation of austerity High unemployment – A major concernEuro Zone to go through recessionary pressures atleast for next 2‐3 quarters

4

EU Economy –

Worrying for the World

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Chinese economy cooling off as can be seen from the IP growth rates. Even during the Global Financial Crisis, IP growth was near 13%

The positive signals – Inflation cooling off, high possibility of stimulus (anywhere btw $200‐300 billion), interest rate cycle peaked so cut may be expected.

5

China –

Tremors in Growth Trajectory

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Preferred Elliott Wave Count on EURUSD Spot–

Long term

6

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Rupee depreciation causing ripples in the spine of policy makers and importersRising Inflation and declining IP Growth may change the investors’ perceptionIf recent numbers are any indication, GDP growth below 6.5% for 2012‐13 should not be a big surprise

7

India –

Traversing through Rough Phase

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Preferred Elliott wave Count on USDINR Spot–

Long term

8

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Indonesian Policy Revisions

9

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Revised Tax Structure –

In Brief

10

CPO export tax range has been revised to 7.5% to 22.5% (Earlier it was 1.5% to 25% based on CIF Rotterdam price ranges).The reference price (base export price) for crude palm oil will be calculated base on average prices at Rotterdam, Bursa Malaysia Derivatives or the Jakarta Bourse. (Earlier the same was based on mere CPO CIF Rotterdam prices) The export tax cap on palm oil Olein products (downstream) was cut to 13 percent (Earlier the same was 25 percent)

CIF Rot Price

($/ton)

Effective tax range ($/ton)

Earlier Revised Net tax change

750 ‐1000 22 ‐100 56‐135 36.4 ‐

38.5

1001‐1100 125 ‐165 150‐181.5 20.4 ‐

21.4

1100 ‐1150 192 ‐200 198 ‐207 5.5 ‐5.75

1150‐1250 230‐280 235‐262 ‐12

>1250 312.5 281.25 ‐31.25

In absolute terms, when CIF Rotterdam prices are reigning in the range of $ 750 ‐1000, industry shall end up paying a higher tax of $ 36‐38 With further increase in market and price volatility as the prices soar higher beyond MYR 3750 (>$1250/ton), industry players shall gain advantage from the present scenario by paying a lower tax of $30 from the

present levels

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 11

Global Palm –

In A Glimpse

In the next 3 Years, World shall be supplied with another 5MT of Palm Oil with

INDONESIA accounting for nearly 65% of this Growth

Always palm Supplies outpaced that of Demand resulting in a

continuous Stock Piling.As such Industry is inadvertently building

Supply Side Risk

With Such Supply Side Equation, lets’ now look at How the Demand Component transforms, Given the recent Indonesian Export Tax Revisions!!!

Global Palm Oil Scenario ‐ In a Nut Shell (MT)

20

25

30

35

40

45

50

55

2001‐02 2003‐04 2005‐06 2007‐08 2009‐10 2011‐12e

2

2.5

3

3.5

4

4.5

5

5.5

6Stocks Production Consumption

S-D Gap Intact Stocks on Continuous Rise

Risk is Inbuilt

Source: USDA ; Year ‐ Oct ‐ Sep

Way Forward ‐ Palm Oil Supply Projections (MT)

28.8

25.4

23.6

20.518.0

17.6 17.318.2 18.7

19.4

15

17

19

21

23

25

27

29

31

2007‐08 2008‐09 2009‐10 2010‐11 2011‐12e 2012‐13 2013‐14 2014‐15

Indones ia Malays ia

Source: USDA, TG Research; Year ‐Oct ‐ Sept

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 12

Futuristic Impact : Global Palm Trade

Ultimately, Olein

to CPO spreads will be squeezed may be permanently towards 20-25$/ton range or even lower (very often) making refining industry unviable elsewhere

How Does Global Exports* Of CPO and Olein

Change?

2011 By 2014 Absolute Change

CPO Olein CPO Olein CPO Olein

Indonesia 9.52 7.48 7.97 11.01 ‐1.55 3.53

Malaysia 3.48 14.48 ?? ?? ?? ??

Others 4.1 ‐‐ 4.48 ‐‐ 0.38 ‐‐

By

changing

tax

structure,

Indonesia

targets

to

tilt

its

crude

to

finished

export

ratio

from

currently

estimated

56:44

to

40:60

by

2015.

By

2014,

world

shall

face

an

extra

Olein

supplies

of

3.53

MT

while

that

of

CPO

will

be

squeezed

by

1.55

MT

from Indonesia.

Hence, Indonesia will now switch to push strategy w.r.t. OleinIndonesia currently has a Refining Capacity of 22.2 MT (2011)

and is currently operating at 50% Utilization rates

Source: GAPKI, TG Projections

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Implications to Stake Holders

13

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 14

Malaysian refining industry shall now have intensified competition as Indonesia attempts to create market for itself.

More than pure refining industry, high degree value added industries viz. Specialty fats, Oleo Chemicals of Malaysia need to share its clientele base with the new supplier.Depreciation of MYR against USD from 2.99 to 3.2 (by 7%) since Mar’12 has temporarily rescued Malaysian Refining industry.

Indian Olein industry cannot compete with foreign originating cheaper oil.Vanaspati or modernly called IE fat industry shall have squeezed supply of feed stock – so in long‐run the industry shall become non‐economicalSpecialty fats and Oleo industries that are in nurturing stage too shall need policy support as higher feed stock prices might curtail their profitsAs such consolidation shall pick‐up pace apart from operating rates falling down sharply.

Indonesia Export tax restructuring –

Effects could be Seismic in nature

These are few to state, while given palm industry’s sheer size, ripple effects could be uncountable`

MALAYSIA INDIA

In addition, nations like Netherlands, Egypt, Saudi Arabia which are sole CPO importers too face similar crisis of their domestic refining industry.Countries like China who are RBD Olein importers have a price advantage with Indonesia’s competitive price quotes

Processing Cost MYR 75/ton Processing Cost INR 20/10 Kg

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

India

15

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 16

India –

Backbone for world palm industry

Since

2005,

Indian

Palm

consumption

grew

@

CAGR

of

16%

vs.

its

cumulative

veg.

oil

demand surge of 2.9%

Against

China

– 4%

of

palm

vs.

5.1%

total veg. oils

Of

the

total

world

palm

incremental

consumption of 15.8 MT, India accounted

for 29%.

Source: USDA, MPOB & TG Research; All units in MT

Hypothetically,

if

Indian

consumption

grew

only

by

10%,

then

global

stocks

could

have

been higher by another 2.2. MT.

Else

Industry

as

such

might

have

shown

lopsided

growth

Leading Palm Oil Importers -2005-06

India11%

China19%

Other42%

EU-2716%

Pakistan7%

Malaysia3%

Egypt2%

Source: USDA, TG Research

Leading Palm Oil Importers -2010-11

Egypt3%Malaysia

4%

Pakistan6%

EU-2714%

Other37%

China17%

India19%

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Policy driven Indian palm demand

17

World Palm industry should be thankful to Indian policy makers for opening a great market

for ever growing SE Asian palm producers

Indian Palm Import Trends ‐ CPO to Olein Mix (% share)

93 85 83 78

24

15 17 22

0

20

40

60

80

100

2002‐03 2005‐06 2008‐09 2011‐12e

CPO RBD

Higher Tari ffs Period

Nov ‐ Oct

MT

Indian Palm Import Trends ‐ CPO to Olein Mix

01234

5678

2002‐03 2005‐06 2008‐09 2011‐12e

RBD CPO Total Palm

Nov‐Oct

Policy Driven Demand Curve Shifts during 2008

MT

Indian Import Scenario ‐

2011‐12

CPO RBD Olein

Nov‐Apr 2.49 (15) 0.92 (89)

Nov‐Oct* 5.78 (7.6) 1.62 (50)

* TG Estimates; Units in MT; (y‐o‐y % change)

Constructive

policy

change

of

Zero

duty

on

CPO

and

just

7.5%

on

Olein

during

2008

has

come

to

the

rescue

of

palm

trade,

while

the

current

Indonesian

policy is restricting the opportunities.

So

far

Indian

Imports

have

already

replicated

the

repercussions

with

RBD

Olein

imports

so

far

recorded 89% higher on yearly basis

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Inflation –

A Check for Edible Oil Import Policies

18

Tremors

in

growth

rate

of

Indian

Economy,

coupled

with

relatively

higher

inflation

during

the

recent past shall keep a tab on policy revisions of Indian edible oil industry in the near term

Now let us look at Anatomy of Indian Edible oil Consumption and Chief problems of Indian Industry!!!

5.0

6.0

7.0

8.0

9.0

10.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2007‐08 2008‐09 2009‐10 2010‐11 2011‐12

Annual Inflation Rate (WPI)

GDP Growth RateSource: RBI

Indian GDP and Inflation Trend

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Anatomy of Edible Oil Consumption Patterns

Hinterland of Kandla

Palm oil 33%

Soy oil 25%

Mustard oil 22%

Cottonseed oil 6%

GNO 4%

Hinterland of Haldia

Palm oil 31%

Soy oil 11%

Mustard oil 41%

Hinterland of JNPT +

Mangalore

Palm oil 36%

Soy oil 23%

Cottonseed oil 7%

GNO 9%

Sun oil 14%

Hinterland of Kakinada

Palm oil 38%

Soy oil 11%

Cottonseed oil 12%

GNO 12%

Sun oil 12%

Hinterland of Chennai

Palm oil 49%

GNO 4%

Sun oil 16%

19

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Indian Refining Industry -

South based refiners are bad hit

20

Capacity Utilization Across Hinterlands

Hinterland Kandla Haldia JNPT

and

Mangalore

Kakinada

+ 60%

of k’patnam

Chennai + 40%

Krishnapatnam

Total

palm

Refining

capacity

(TPD)

9562 5695 4680 6750 4600

Per

Year

(300 days) MMT

2.869 1.709 1.404 2.025 1.380

CPO

arriving

at

port (MMT)

1.824 1.088 0.953 0.74 0.57

Utilization 64% 64% 68% 37% 41%Source: SEA of India and TG field survey (2010)

With

Krishnapatnam

coming

in,

South

Indian

operating

rates

dropped

precipitously

and

with

Indonesian

tax

changes, the industry could be

pushed to “Un‐viable”

West & East based refiners too

shall undergo stress tests.

This happens for two reasons

1.

LOW CAPACITY UTILIZATION ‐

Already suffering with low capacity utilization and so if these rates further reduce,

it is only killing

2.

ABSENCE OF DOWNSTREAM INDUSTRIES ‐

Value addition stops mostly at Olein

level, hence leveraging from high

profit making specialty fats, vanaspati

and refining of other edible oils is absent

Our Study shows that, Indian players earn very high double digit

margins in value added downstream products while the same would be mere 2% in RBD olein

refining

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Indian Refining Industry -

West & East based refiners are better placed

21

Why??

Highly leveraged due to multi oil refining avenues

These regions account for 75% of biscuit & confectionary industries and more than 80% of Vanaspati (vegetable oil hard fat) making. 80% of the feedstock used in these industries is stearin.

80% of Oleo industry is located in North and West India providing good scope for offloading byproducts

Hence, those CPO refiners who don’t have high end value addition facilities in place, will be FIRST to hit. While drilling it region wise, South Indian units are badly effected.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Indian Price Spreads

22

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 23

Olein

–

CPO spread squeezing will be the biggest pain point for the industry

Now

the

industry

is

worried

that,

in

the

rush

of

market making, Indonesia will pressurize Olein

prices

and hence the spreads between the oils will become

a “Permanent Business Risk”.

Typically Indian industry will now turn more speculative –

i.e. emphasize more on price views to ensure margins required to run the business units –

like the case of Indian soy crush industry or industry players will move up the chain.

CNF Olein

–

CPO spread is quoting around 20$/ton.Narrowed Spreads with the advent of Indonesian Tax revisions

0

20

40

60

80

100

120

140

Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12

RBD‐CPO spread (CNF India)$/ton

‐1500

‐1000

‐500

0

500

1000

1500

2000

2500

Jun‐11 Aug‐11 Oct‐11 Dec‐11 Feb‐12 Apr‐12

Indian Soybean Crush Margins (INR/ton)

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Current Market Fundamentals -

Outlook

24

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Global Weather –

In a Glimpse

Rapeseed belts of EU, Delta tracts of US (which is yet to plant soybeans) and Indian KharifSeason (Which accounts for nearly 60% of Indian oilseed production) remain watchful in 1‐2 months.

Alarming for Oilseed Crops

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

US Spring Crops –Looming Dryness for Jun-July Months

Weather models forecast for persisting dry conditions with above normal temperatures for Jun‐July.Dryness in Southern belts to augment worries over planting soybeans post Winter Wheat Harvest.

*Water availability to Agriculture

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

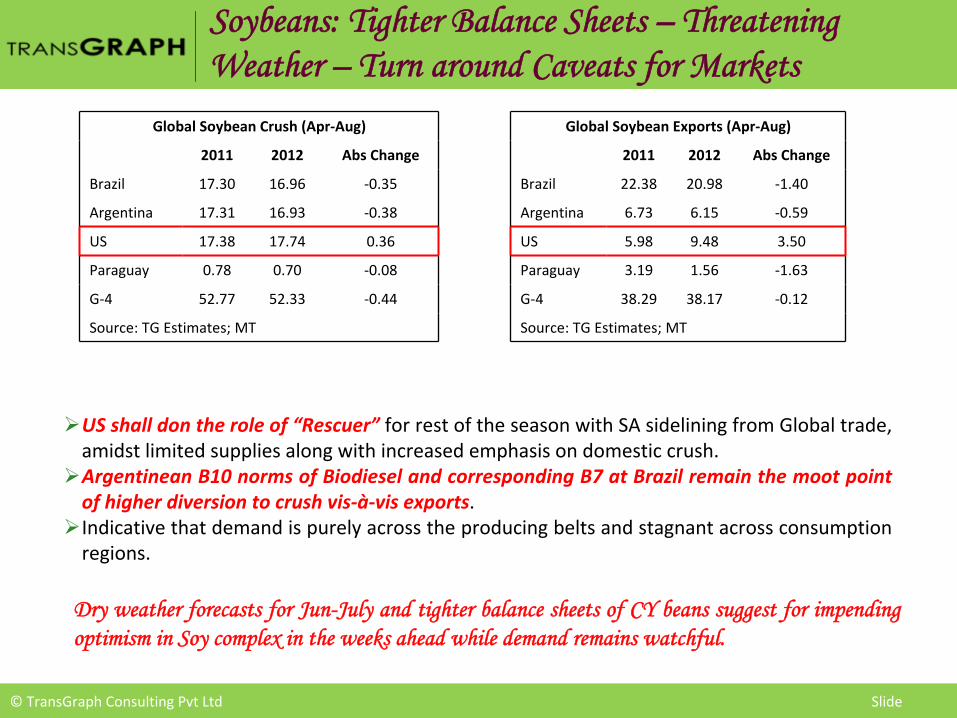

Soybeans: Tighter Balance Sheets –

Threatening Weather –

Turn around Caveats for Markets

US shall don the role of “Rescuer” for rest of the season with SA sidelining from Global trade, amidst limited supplies along with increased emphasis on domestic crush.Argentinean B10 norms of Biodiesel and corresponding B7 at Brazil remain the moot point of higher diversion to crush vis‐à‐vis exports.Indicative that demand is purely across the producing belts and stagnant across consumption regions.

Global Soybean Crush (Apr‐Aug)

2011 2012 Abs Change

Brazil 17.30 16.96 ‐0.35

Argentina 17.31 16.93 ‐0.38

US 17.38 17.74 0.36

Paraguay 0.78 0.70 ‐0.08

G‐4 52.77 52.33 ‐0.44

Source: TG Estimates; MT

Global Soybean Exports (Apr‐Aug)

2011 2012 Abs Change

Brazil 22.38 20.98 ‐1.40

Argentina 6.73 6.15 ‐0.59

US 5.98 9.48 3.50

Paraguay 3.19 1.56 ‐1.63

G‐4 38.29 38.17 ‐0.12

Source: TG Estimates; MT

Dry weather forecasts for Jun-July and tighter balance sheets of CY beans suggest for impending optimism in Soy complex in the weeks ahead while demand remains watchful.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Palm Complex –

Disappointing FFB Yields; OER close to Normality

28

FFB reduction – a major contributor for production decline so far in 2012.Seasonal Recovery on cards for Q2‐Q3.Thus, monthly CPO output at Malaysia to improve towards 1.48‐1.5 MT in June‐July. (1.27 MT in April’12)Overall Malaysian CPO output for 2012 to stay close to 18.5 MT, down by 2% Y‐o‐Y while Indonesian CPO output might remain 5‐6% higher around 25.8 MT.

TG Estimates

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Global Veg. Oil B/S –

Stunted Supply Growth to Eat away the Carry-in for Next Season

29

Rich supplies of Palm from SE Asia during 2011 (11.3% higher production from Malaysia and 10% from Indonesia) translated into ample carry‐in for 2012 season.Lower availability of Rapeseed and Soy oils to augur the demand for palm oil during 2012.Global veg oil stocks to steeply plunge towards 10.2 MT, 12.5% drop on yearly basis

Global Veg. Oil S'n'D Dynamics (MT)

4.4

1.4

3.0 2.62.30.9

2.72.0

0.5

‐0.7

0.5

‐0.6

‐0.1

2.1

‐0.1

1.7

8.1

4.2

6.86.2

‐2.0

0.0

2.0

4.0

6.0

8.0

2010‐11 2011‐12e 2010‐11 2011‐12e

Incrementa l Suppl ies Incrementa l Demand

Palm oil Soy oil Rape oil Sun oil Total

Falling Supplies while relatively firm demand to eat away into stocks

Source: TG Research, USDA

Global Edible Oil Stocks (MT)

1.5

4.2

4.7

4.7

4.2

2.43.03.03.8

0.60.91.1

0.5

1.31.7

0.7

10.211.7

12.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2006‐07 2007‐08 2008‐09 2009‐10 2010‐11 2011‐12e

0

2

4

6

8

10

12

14

Palm oi l Soy oi l Rape oi l Sun oi l Tota l

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Indian Kharif

Crop Prospects –

2012-13

30

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

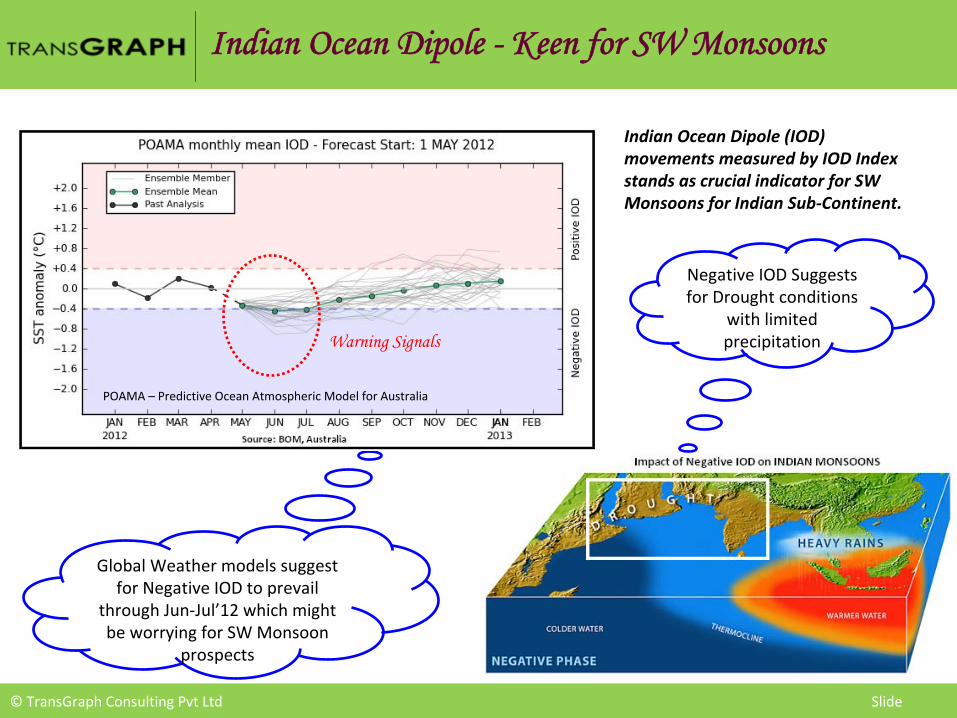

Indian Ocean Dipole -

Keen for SW Monsoons

Indian Ocean Dipole (IOD)

movements measured by IOD Index

stands as crucial indicator for SW

Monsoons for Indian Sub‐Continent.

Negative IOD Suggests

for Drought conditions

with limited

precipitation

Global Weather models suggest

for Negative IOD to prevail

through Jun‐Jul’12 which might

be worrying for SW Monsoon

prospects

POAMA – Predictive Ocean Atmospheric Model for Australia

Warning Signals

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 32

Kharif

Plantings –

Soybean and GN to Steal the Show

Price Realization (% Change) during Mar‐May’12 vs.

same period LY – MINOR CEREALS

Higher prices realizations for oilseeds to translate into higher acreages this yearCotton to lose some acres to better performing Soybeans and GNPulses and cereals to face stiff competition from oilseeds owing to poor returns.

Price Realization (% Change) during Mar‐May’12 vs.

same period LY – PULSES

Price Realization (% Change) during Mar‐May’12 vs.

same period LY – OILSEEDS

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 33

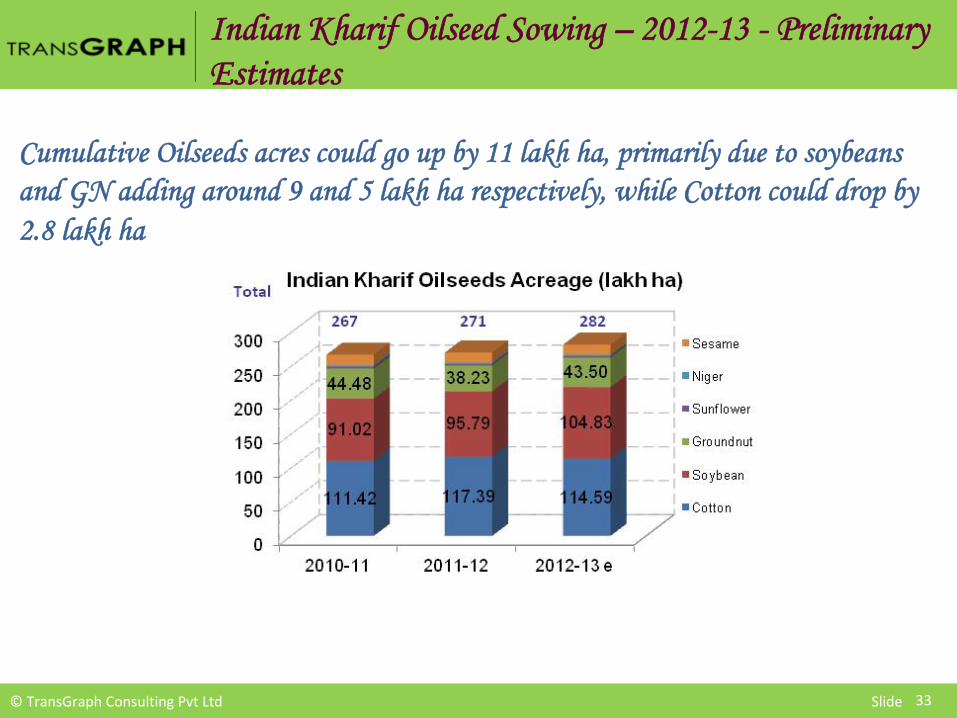

Indian Kharif

Oilseed Sowing –

2012-13 -

Preliminary Estimates

Cumulative Oilseeds acres could go up by 11 lakh

ha, primarily due to soybeans and GN adding around 9 and 5 lakh

ha respectively, while Cotton could drop by

2.8 lakh

ha

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

BMD CPO Futures Cont, MYR/MT, Elliott Wave

34

BMD Palm oil futures prices are retracing back upon honoring a crucial level at MYR 3620. According to Elliott wave analysis prices are running as the Primary wave C of Cycle wave 2. Although initial gains are expected, potential of such gains could remain limited above MYR 3300/3350. Subsequently prices could extend lower towards MYR 2500 remains open in the coming 2-3 months ahead of turning higher.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

BMD CPO Futures Cont, MYR/MT, Elliott Wave Count…(Short term)

35

Prices to bounce initially to 3200 MYR and shall turn to bearish mode towards 2750 and eventually to 2500 MYR in long-run. However, in the event of unexpected stimulus packages from US and EU, prices could stench short-term bounce to MYR 3350/3400 and turn lower from there

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

BMD CPO Futures Cont, Cycle Analysis

36

In BMD CPO futures prices a 4-year cyclicality is been observed as shown above. According to the same come Oct’12 prices are likely to place a major bottom and enter a fresh bull run.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

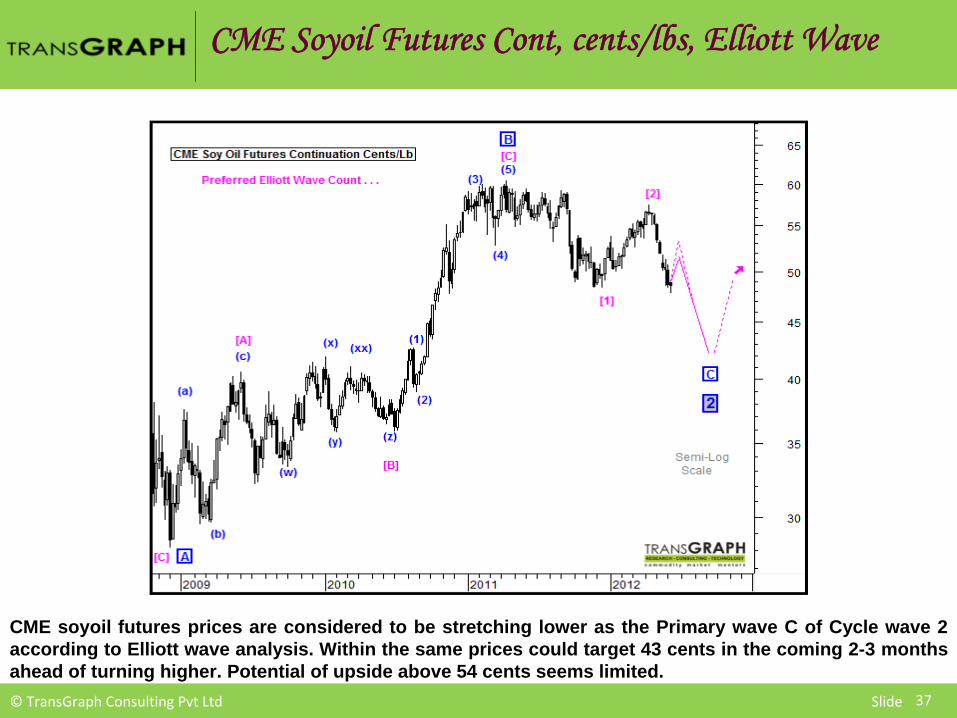

CME Soyoil

Futures Cont, cents/lbs, Elliott Wave

37

CME soyoil futures prices are considered to be stretching lower as the Primary wave C of Cycle wave 2 according to Elliott wave analysis. Within the same prices could target 43 cents in the coming 2-3 months ahead of turning higher. Potential of upside above 54 cents seems limited.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 38

NCDEX Soy Oil Futures Cont, INR/10 Kg

NCDEX Soy Oil Futures prices have witnessed a setback from INR 790 and weakened towards INR 710 finding follow through selling. Possibility of initial gains towards INR 760 could be seen ahead of such extended weakness in the coming month. In the medium term extended weakness towards INR 650 shall remain open.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 39

NCDEX Soybean Futures Cont, INR/Qtl.

NCDEX Soybean futures prices are forming a triangle while hovering mixed within INR 3250-3450 as the overall weakness from the May’12 high of INR 3785 is intact. While the existing consolidation is seen as an upside correction , prices upon a retest of INR 3450 shall attract good renewed selling pressure to turn lower and prompt extension of the underlying weakness towards INR 3000 and lower in the coming months.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 40

MCX CPO Futures prices are hovering near INR 540 after weakening from the May’12 high of INR 635 exhibiting a weak tone. Owing to the oversold short term oscillators possibility of minor gains towards INR 580 remains open ahead of extended weakness towards INR 500 in the coming months.

MCX CPO Futures Continuation, INR/10Kg

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Markets Last Closing (June 6,2012)

Price outlook (3-4 months)

BMD Palm Oil Futures, MYR/MT 3003 2940-3350-2500

CME Soy Oil Futures, Cents/lb 48.5 48-53-43

NYMEX Crude Oil, USD/bbl 85.11 80-92-75

NCDEX Soy Oil Futures, INR/10kg 731.60 720-760-650

NCDEX Soybean Futures, INR/Qtl 3379.50 3260-3470-2900

MCX CPO Futures, INR/10Kg 551.50 540-580-500

Price Outlook (4-6 Months)

The global oil and oil seed complex is likely to maintain the current underlying weakness in the medium term while weather vagaries could prompt minor upside potential in the short term.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide 42

So finally how Indonesia policies impact industry in the wake of my weak price outlook

It will be double wammy…..For Indonesian CPO Sellers

• As prices fall and incidental tax will be high in lower price brackets – much to shell-out to Govt.

For Malaysia and India• Indonesia vendors will resort to more aggressive selling of Olein and that is killing for refining industries in both these nations.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide

Road Ahead -

TransGraph

Perspectives

43

It is only matter of time, counter-intuitive policy revisions are bound to come, especially India and Malaysia could react Following are the likely policy changes possible.By Malaysia:1.Could initiate a dialogue with Indonesia2.lift the export quota ceiling of CPO and employ similar tax structures followed by Indonesia on CPO –

level playing field

By India:1.Logically, base import price could be revised from $484/ton to 950/1000$ per ton. It will double the

incidental tax ensuring margin making scope for the refiners

a)

If this happens, Olein

prices will shoot higher tentatively translating into demand destruction2.Could initiate a dialogue with Indonesia3.Or Origin shift to Central America in the longer run

Overall the source countries priorities in order are1.

Find markets for the palm oil2.

Find market for the refined products to ensure development of industry.There

should

be

balance

and

source

countries

can

not

risk

the

first

point

at

the

cost

of

second

point. The balance between export ratio of products and materials in the soybean industry at

countries like USA should be observed by Indonesia.

© TransGraph Consulting Pvt Ltd Slide© TransGraph Consulting Pvt Ltd Slide44

Thank you for your attention

www.transgraph.com

Transgraph Consulting Pvt Limited

TransGraph Consulting Pvt. Ltd.# 6-3-655 / 2/1, III Floor, A.P. Civil Supplies Bhavan Lane, Somajiguda, Hyderabad –

82,Tel: +91-40-30685001-04: Facsimile: +91-40-30685002

E-mail: [email protected]; mktg@ transgraph.comwww.transgraph.com

LEGAL INFORMATION

This document is the whole property of Transgraph Consulting Private Limited, Hyderabad, India (hereafter “TransGraph”).

The following acts are strictly prohibited:Reproduction and/or forwarding for sale or any other usesPosting on any communication mediumTransmittal via the Internet

Terms of usageUpon receipt of this document either directly or indirectly, it is understood that the user will and must fully comply with the other terms and conditions of TransGraph. By accepting this document the user agrees to be bound by the foregoing limitations.

This publication is prepared by TransGraph and protected by copyright laws. Unless otherwise noted in the Service Agreement, the entire contents of this publication are copyrighted by TransGraph, and may not be reproduced, stored in another retrieval system, posted on any communication medium, or transmitted in any form or by any means without prior written consent of TransGraph. Unauthorized reproduction or distribution of this publication, or any portion of it, may result in severe civil and criminal penalties, and will be prosecuted to the maximum extent necessary to protect the rights of TransGraph.

The information and opinions contained in this report have been obtained from sources TransGraph believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete and it should not be relied upon as such.

This report does not constitute a prospectus or other offering document or an offer or solicitation to buy or sell any assets (commodities, currencies, etc) or other investment. Information and opinions contained in the report are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient; they are subject to change without any notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Any views expressed reflect the current views of the analysts, which do not necessarily correspond to the opinions of TransGraph or its affiliates. Opinions expressed may differ from views set out in other documents, including research, published by TransGraph.

Any reference to past performance should not be taken as an indication of future performance. No member in the public related to TransGraph accepts any liability whatsoever for any direct or consequential loss arising from any use of material contained in this report.

Analyst CertificationEach analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the analyst's views about any and all of the factors and assets (commodities, currencies, etc) named in this report, and (ii) no part of the analyst's compensation is directly or indirectly, related to the execution of the specific recommendations or views expressed herein.

Copyright © TransGraph Consulting Private Limited, Hyderabad, India.

Prepared by Consulting Team – TransGraphRegistered Office: 6‐3‐655/2/1, AP Civil Supplies Bhavan Lane, Somajiguda, Hyderabad – 500082 INDIA Phone: +91 40 30685000 04 | E mail: services@transgraph com | Internet: www transgraph com

45

Related Documents