l Equity Research l Important disclosures can be found in the Disclosures Appendix All rights reserved. Standard Chartered Bank 2011 http://research.standardchartered.com Malaysia | Emerging Companies - Healthcare 30 June 2011 KPJ Healthcare Berhad Steady and defensive OUTPERFORM (initiating coverage) PRICE as at 29 June 2011 MYR4.57 PRICE TARGET MYR5.00 Bloomberg code Reuters code KPJ MK KPJH.KL Market cap 12 month range MYR2,594m (US$855m) MYR3.18 - 4.72 EPS est. change n.a. We initiate coverage of KPJ Healthcare (KPJ) with an OUTPERFORM rating and a price target of MYR5.0 KPJ is the largest private hospital operator in Malaysia and is leveraged to the structural growth of healthcare spending in the country. We like KPJ for its market leadership, structural growth, and defensive qualities Although our 12m price target offers only 9% upside, we note that KPJ is highly defensive, outperformed the KLCI by 21% during the financial crisis, and our valuation on a DCF basis would be MYR6.59 per share Year end: Dec 2010 2011E 2012E 2013E Sales (MYRm) 1,655 1,920 2,179 2,473 EBIT (MYRm) 144 178 207 237 EBIT DA (MYRm) 203 247 277 324 Pretax profit (MYRm) 168 199 235 266 Earnings (MYRm) 119 139 164 186 Dilut ed EPS (MYR sen) 20. 3 21.2 25.0 28.3 DPS (MYR sen) 15. 0 8.5 10.0 11.3 Revenue growth ( %) 13. 6 16.1 13.5 13.4 EPS growth (%) -6.2 4.4 18.0 13.2 EBITDA margin (%) 12.3 12.9 12.7 13.1 EBIT margin (%) 8. 7 9.2 9.5 9.6 Net margin (%) 7. 2 7.2 7.5 7.5 Div payout (%) 73. 9 40.0 40.0 40.0 Book value / share (MYR) 1.37 1.52 1.70 1.92 Debt/ Equity (%) 46.3 41.5 37.0 32.9 ROE (%) 17. 0 17.1 18.0 18.1 ROCE (%) 11. 8 12.2 13.1 13.5 FCF (MYRm) 33 213 10 36 EV/EBITDA (x) 14.4 11.8 10.5 9.0 PBR (x) 3.3 3.0 2.7 2.4 PER (x) 22.5 21.6 18.3 16.1 Dividend yield (%) 3.3 1.9 2.2 2.5 Source: Company, Standard Chartered Research estimates Share price performance 3.2 3.4 3.6 3.8 4.0 4.2 4.4 4.6 4.8 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 KPJ Healthcare Berhad KUALA LUMPUR COMP INDEX (rebased) Share price (%) -1 mth -3 mth -12 mth Ordinary shares 7 24 41 Relative to Index 3 11 17 Relative to Sector - - - Major shareholder Johor Corp (41.9%) Free float 34% Average turnover (US$) 1,154,969 Leveraged to structural growth in private healthcare spending. The public healthcare system in Malaysia is highly stretched, with only 46% of overall healthcare sector expenditure but 74% of admissions. We expect a continued spillover into private healthcare especially with sustained growth in GDP per capita. Malaysia also has one of the fastest growing populations in Asia, and like most countries, an ageing population. In the last decade, private healthcare spending has grown at 16% p.a. Market leadership. KPJ operates the largest private hospital network in Malaysia with 20 hospitals and over 2,500 licensed beds. The closest competitors are Pantai and Columbia Asia, but they are much smaller with 10 and 9 hospitals respectively. KPJ focuses on community-based hospitals and targets opening 1-2 new hospitals per year as it continues to expand its network. Asset light. KPJ’s strategy is to offload profitable hospitals into Al-‘Aqar REIT (Not rated, last close MYR1.17, which it owns 49%. This allows KPJ to stay asset light and recycle its capital for future growth. Rental rate is based on a formula linked to the market value of the properties, but is stable as the maximum revision is 2% per year. Steady and defensive. Although near-term price appreciation appears limited, we believe KPJ’s defensive qualities will be appreciated in the current uncertain markets. In the last ten years, KPJ has compounded its earnings at 27% p.a. and grown earnings every year. During the financial crisis (from beginning 2008 to March 2009), KPJ’s shares outperformed KLCI by 21%. A potential catalyst for the stock may be the expected relisting of Parkway as Integrated Healthcare as it was privatised at PER27x forward earnings (based on our estimates). Source: Company, Bloomberg Stephen Hui [email protected] 65 6596 8514

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

l Equity Research l

Important disclosures can be found in the Disclosures Appendix All rights reserved. Standard Chartered Bank 2011 http://research.standardchartered.com

Malaysia | Emerging Companies - Healthcare 30 June 2011

KPJ Healthcare Berhad Steady and defensive

OUTPERFORM (initiating coverage) PRICE as at 29 June 2011

MYR4.57PRICE TARGET

MYR5.00

Bloomberg code Reuters codeKPJ MK KPJH.KL

Market cap 12 month rangeMYR2,594m (US$855m) MYR3.18 - 4.72

EPS est. change n.a.

We initiate coverage of KPJ Healthcare (KPJ) with an OUTPERFORM rating and a price target of MYR5.0

KPJ is the largest private hospital operator in Malaysia and is leveraged to the structural growth of healthcare spending in the country.

We like KPJ for its market leadership, structural growth, and defensive qualities

Although our 12m price target offers only 9% upside, we note that KPJ is highly defensive, outperformed the KLCI by 21% during the financial crisis, and our valuation on a DCF basis would be MYR6.59 per share

Year end: Dec 2010 2011E 2012E 2013ESales (MYRm) 1,655 1,920 2,179 2,473EBIT (MYRm) 144 178 207 237EBITDA (MYRm) 203 247 277 324Pretax profit (MYRm) 168 199 235 266Earnings (MYRm) 119 139 164 186Diluted EPS (MYR sen) 20.3 21.2 25.0 28.3DPS (MYR sen) 15.0 8.5 10.0 11.3Revenue growth (%) 13.6 16.1 13.5 13.4EPS growth (%) -6.2 4.4 18.0 13.2EBITDA margin (%) 12.3 12.9 12.7 13.1EBIT margin (%) 8.7 9.2 9.5 9.6Net margin (%) 7.2 7.2 7.5 7.5Div payout (%) 73.9 40.0 40.0 40.0Book value / share (MYR) 1.37 1.52 1.70 1.92Debt/ Equity (%) 46.3 41.5 37.0 32.9ROE (%) 17.0 17.1 18.0 18.1ROCE (%) 11.8 12.2 13.1 13.5FCF (MYRm) 33 213 10 36EV/EBITDA (x) 14.4 11.8 10.5 9.0PBR (x) 3.3 3.0 2.7 2.4PER (x) 22.5 21.6 18.3 16.1Dividend yield (%) 3.3 1.9 2.2 2.5

Source: Company, Standard Chartered Research estimates Share price performance

3.23.43.63.84.04.24.44.64.8

Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

KPJ Healthcare Berhad

KUALA LUMPUR COMP INDEX (rebased)

Share price (%) -1 mth -3 mth -12 mthOrdinary shares 7 24 41Relative to Index 3 11 17Relative to Sector - - -Major shareholder Johor Corp (41.9%)Free float 34%Average turnover (US$) 1,154,969

Leveraged to structural growth in private healthcare spending. The public healthcare system in Malaysia is highly stretched, with only 46% of overall healthcare sector expenditure but 74% of admissions. We expect a continued spillover into private healthcare especially with sustained growth in GDP per capita. Malaysia also has one of the fastest growing populations in Asia, and like most countries, an ageing population. In the last decade, private healthcare spending has grown at 16% p.a.

Market leadership. KPJ operates the largest private hospital network in Malaysia with 20 hospitals and over 2,500 licensed beds. The closest competitors are Pantai and Columbia Asia, but they are much smaller with 10 and 9 hospitals respectively. KPJ focuses on community-based hospitals and targets opening 1-2 new hospitals per year as it continues to expand its network.

Asset light. KPJ’s strategy is to offload profitable hospitals into Al-‘Aqar REIT (Not rated, last close MYR1.17, which it owns 49%. This allows KPJ to stay asset light and recycle its capital for future growth. Rental rate is based on a formula linked to the market value of the properties, but is stable as the maximum revision is 2% per year.

Steady and defensive. Although near-term price appreciation appears limited, we believe KPJ’s defensive qualities will be appreciated in the current uncertain markets. In the last ten years, KPJ has compounded its earnings at 27% p.a. and grown earnings every year. During the financial crisis (from beginning 2008 to March 2009), KPJ’s shares outperformed KLCI by 21%. A potential catalyst for the stock may be the expected relisting of Parkway as Integrated Healthcare as it was privatised at PER27x forward earnings (based on our estimates).

Source: Company, Bloomberg

Stephen Hui [email protected] 65 6596 8514

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 2

Contents

Investment highlights 3

Valuation 4

Peer comparison 8

Company overview 11

Structural drivers 15

Strong market position 18

Competitor analysis and positioning 21

High barriers to entry 23

Growth drivers 24

Healthcare education 26

REIT funds expansion 28

Group financials 30

Corporate information 35

Disclosures appendix 38

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 3

Investment highlights We initiate coverage of KPJ Healthcare with an OUTPERFORM rating and a price target of MYR5.0 per share, offering a potential total return of 11.6% (9.4% from share price appreciation, 2.2% from dividend yield). Our investment thesis is based on the following:

Structural growth. The Malaysian public healthcare system is highly stretched with only 46% of overall healthcare sector expenditure but 74% of admissions. As Malaysian household income steadily grows, we expect a spillover to private healthcare. From 2000 to 2008, Malaysian GDP per capita grew at 9% p.a. and private healthcare expenditure at 16% p.a.

Demographic drivers. Private healthcare expenditure is also driven by Malaysia’s growing and ageing population. According to Global Demographics, from 2010 to 2020, Malaysia’s population is expected to grow at 2% p.a. and the percentage of the population over 65 is expected to rise from 5% to 8%.

Market leadership. KPJ Healthcare is the leading private hospital operator in Malaysia with 20 hospitals and over 2,500 beds (as at end-2010). We estimate KPJ has a leading 20% share of private hospital beds in Malaysia and a leading 25% share of private inpatient admission. Over the eight years from 2000 to 2008, KPJ’s revenue share of the private healthcare market steadily increased from 2% to 7%.

Defensive community-based strategy. KPJ operates hospitals in communities of over 200k where it is typically the main hospital in the area. KPJ believes this creates strong customer loyalty and limits competition as it would be very difficult for a competitor to enter the market. The Ministry of Health’s guideline of a minimum distance of 20km between private hospitals also precludes competitors from entering KPJ’s communities.

High barriers to entry. Doctors are in shortage in Malaysia and KPJ has an established relationship with the largest panel of doctors. As KPJ also has the largest network of hospitals, it is the key beneficiary of Malaysia’s Private Healthcare Facilities and Services Act.

Secular growth. KPJ plans to open 1-2 hospitals per year in Malaysia over the next five years. The overall occupancy of the group’s hospitals is about 70% so there is further room to drive patient volume at existing hospitals. In addition, in the last five years, average revenue per patient has compounded at 7% p.a.

Asset-light expansion. KPJ set up Al-‘Aqar KPJ REIT (Al-‘Aqar REIT) in 2006 and owns 49%. KPJ’s strategy is to offload profitable hospitals into Al-’Aqar REIT and recycle its capital for future growth. Rental rate has a maximum revision of 2% per year. Since the establishment of Al-’Aqar REIT in 2006, KPJ’s net gearing has fallen from 57% to 23% at end-2010.

Reasonable valuations. KPJ is trading on PER18x 2012E while the average valuation of peers is at PER20x 2012E. We believe that for investors with a long time horizon, a discounted cash flow reflects the future growth of the group’s cash flows. Our discounted cash flow model shows a fair value of MYR6.59 per share.

High M&A valuations. We note that for industry participants, valuations paid for acquisitions in Asian hospitals are high. Parkway was privatised at PER31x forward earnings; Thomson was acquired at PER27x forward earnings. A potential future catalyst for KPJ’s stock may be the expected relisting of Parkway as Integrated Healthcare.

Steady and defensive. In the last ten years, KPJ has compounded its earnings at 27% p.a. and has grown its revenues and earnings every year. In 2010-2013E, we expect an earnings CAGR of 16%. During the financial crisis (from beginning 2008 to March 2009), KPJ’s shares were down by 19% and outperformed the KLCI by 21%.

Key risks. As KPJ is owned by Johor Corp, it is a government-linked corporation and may be used to advance the national agenda. However, KPJ has a good track record with all hospitals in Malaysia currently profitable.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 4

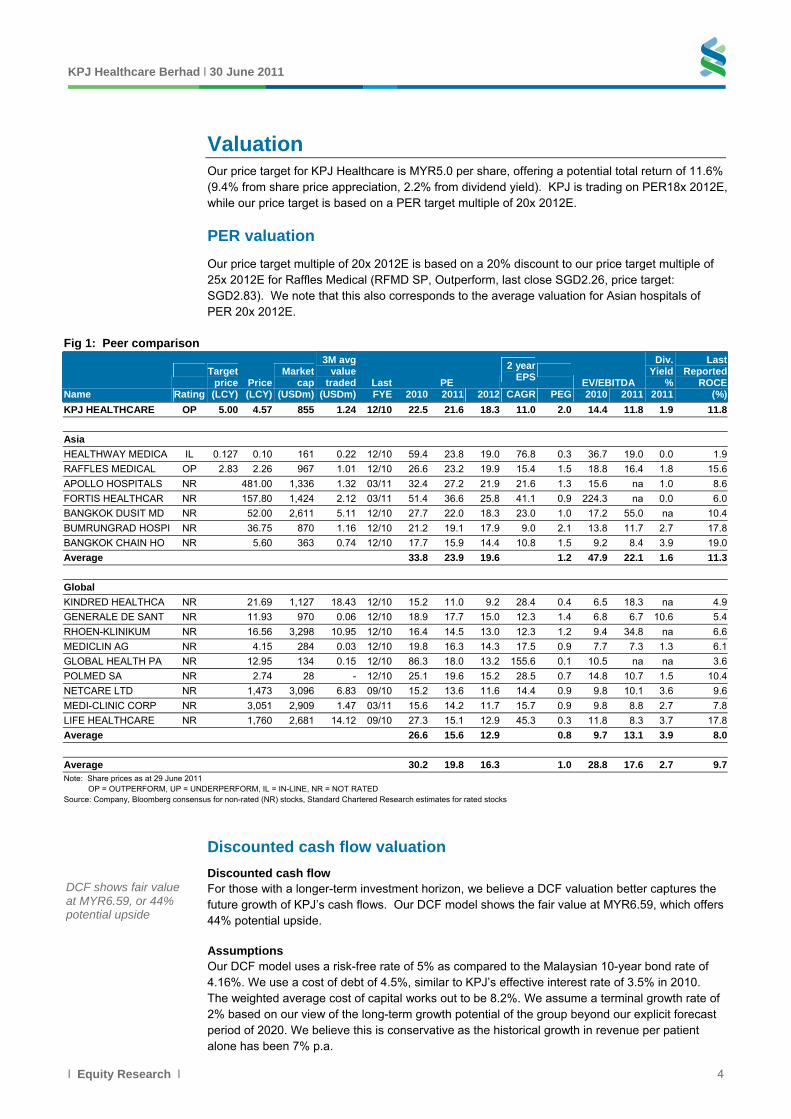

Valuation Our price target for KPJ Healthcare is MYR5.0 per share, offering a potential total return of 11.6% (9.4% from share price appreciation, 2.2% from dividend yield). KPJ is trading on PER18x 2012E, while our price target is based on a PER target multiple of 20x 2012E.

PER valuation

Our price target multiple of 20x 2012E is based on a 20% discount to our price target multiple of 25x 2012E for Raffles Medical (RFMD SP, Outperform, last close SGD2.26, price target: SGD2.83). We note that this also corresponds to the average valuation for Asian hospitals of PER 20x 2012E.

Fig 1: Peer comparison

Target

price Price Market

cap

3M avg value

traded Last PE

2 year EPS

EV/EBITDA

Div. Yield

%

Last Reported

ROCEName Rating (LCY) (LCY) (USDm) (USDm) FYE 2010 2011 2012 CAGR PEG 2010 2011 2011 (%)

KPJ HEALTHCARE OP 5.00 4.57 855 1.24 12/10 22.5 21.6 18.3 11.0 2.0 14.4 11.8 1.9 11.8

Asia

HEALTHWAY MEDICA IL 0.127 0.10 161 0.22 12/10 59.4 23.8 19.0 76.8 0.3 36.7 19.0 0.0 1.9

RAFFLES MEDICAL OP 2.83 2.26 967 1.01 12/10 26.6 23.2 19.9 15.4 1.5 18.8 16.4 1.8 15.6

APOLLO HOSPITALS NR 481.00 1,336 1.32 03/11 32.4 27.2 21.9 21.6 1.3 15.6 na 1.0 8.6

FORTIS HEALTHCAR NR 157.80 1,424 2.12 03/11 51.4 36.6 25.8 41.1 0.9 224.3 na 0.0 6.0

BANGKOK DUSIT MD NR 52.00 2,611 5.11 12/10 27.7 22.0 18.3 23.0 1.0 17.2 55.0 na 10.4

BUMRUNGRAD HOSPI NR 36.75 870 1.16 12/10 21.2 19.1 17.9 9.0 2.1 13.8 11.7 2.7 17.8

BANGKOK CHAIN HO NR 5.60 363 0.74 12/10 17.7 15.9 14.4 10.8 1.5 9.2 8.4 3.9 19.0

Average 33.8 23.9 19.6 1.2 47.9 22.1 1.6 11.3

Global

KINDRED HEALTHCA NR 21.69 1,127 18.43 12/10 15.2 11.0 9.2 28.4 0.4 6.5 18.3 na 4.9

GENERALE DE SANT NR 11.93 970 0.06 12/10 18.9 17.7 15.0 12.3 1.4 6.8 6.7 10.6 5.4

RHOEN-KLINIKUM NR 16.56 3,298 10.95 12/10 16.4 14.5 13.0 12.3 1.2 9.4 34.8 na 6.6

MEDICLIN AG NR 4.15 284 0.03 12/10 19.8 16.3 14.3 17.5 0.9 7.7 7.3 1.3 6.1

GLOBAL HEALTH PA NR 12.95 134 0.15 12/10 86.3 18.0 13.2 155.6 0.1 10.5 na na 3.6

POLMED SA NR 2.74 28 - 12/10 25.1 19.6 15.2 28.5 0.7 14.8 10.7 1.5 10.4

NETCARE LTD NR 1,473 3,096 6.83 09/10 15.2 13.6 11.6 14.4 0.9 9.8 10.1 3.6 9.6

MEDI-CLINIC CORP NR 3,051 2,909 1.47 03/11 15.6 14.2 11.7 15.7 0.9 9.8 8.8 2.7 7.8

LIFE HEALTHCARE NR 1,760 2,681 14.12 09/10 27.3 15.1 12.9 45.3 0.3 11.8 8.3 3.7 17.8

Average 26.6 15.6 12.9 0.8 9.7 13.1 3.9 8.0

Average 30.2 19.8 16.3 1.0 28.8 17.6 2.7 9.7Note: Share prices as at 29 June 2011 OP = OUTPERFORM, UP = UNDERPERFORM, IL = IN-LINE, NR = NOT RATED Source: Company, Bloomberg consensus for non-rated (NR) stocks, Standard Chartered Research estimates for rated stocks

Discounted cash flow valuation

Discounted cash flow For those with a longer-term investment horizon, we believe a DCF valuation better captures the future growth of KPJ’s cash flows. Our DCF model shows the fair value at MYR6.59, which offers 44% potential upside.

Assumptions Our DCF model uses a risk-free rate of 5% as compared to the Malaysian 10-year bond rate of 4.16%. We use a cost of debt of 4.5%, similar to KPJ’s effective interest rate of 3.5% in 2010. The weighted average cost of capital works out to be 8.2%. We assume a terminal growth rate of 2% based on our view of the long-term growth potential of the group beyond our explicit forecast period of 2020. We believe this is conservative as the historical growth in revenue per patient alone has been 7% p.a.

DCF shows fair value at MYR6.59, or 44% potential upside

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 5

Included REIT injections In our free cash flow calculation, we have included expected future proceeds from disposals of hospitals into Al-’Aqar REIT as this is a core part of KPJ’s strategy. We have estimated the GFA of future hospitals and assumed a value based on a valuation of MYR2,142 per square meter, a 20% discount to the average valuation of the past four tranches of injections into Al-’Aqar REIT.

Premium to PER valuation Our DCF valuation is significantly higher than our PER-based valuation, due to the strong expected future cash flow and steady compounding of earnings. We expect KPJ to compound earnings at 16% p.a. over 2010-2013E. The business has a negative working capital with payables days more than offsetting receivable and inventory days.

Fig 2: DCF valuation MYRm 2010 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

EBIT 144 178 207 237 266 304 324 351 399 421 445

EBIT (1-tax) 108 133 155 178 199 228 243 263 299 316 334

(+) Depreciation and amort. 59 70 70 87 104 116 135 147 141 155 169

(-) Change in working capital 31 39 1 (0) (1) 1 1 1 1 1 1

(-) Net capital expenditure (228) (11) (203) (213) (149) (234) (155) 72 (171) (179) (89)

Unlevered free cash flow (30) 231 24 52 154 110 224 483 270 292 415

Present Value of FCF's 222 21 43 117 77 145 290 150 149 196

Terminal value 6,829

2012E WACC assumptions

DCF of operations 1,409 Risk-free rate 5.00%

NPV of the terminal value 3,231 Cost of debt 4.50%

Fair value of the operations 4,641 Equity risk premium 4.50%

Net cash/(debt) (224) Tax rate 25%

Minorities (99) Target debt to firm value 15%

Equity value 4,318 Equity beta 0.90

Shares outstanding 656 Cost of debt (after tax) 3.38%

Fair value per share (MYR) 6.59 Cost of equity 9.05%

Current price * 4.57 WACC 8.20%

Upside/(downside) 44% Terminal growth rate 2.00% * Price as at 29 June 2011 Source: Company, Standard Chartered Research estimates

Fig 3: Sensitivity of fair value WACC

7.2% 7.7% 8.2% 8.7% 9.2%

1.0% 7.10 6.43 5.86 5.36 4.93

1.5% 7.60 6.84 6.20 5.64 5.17

2.0% 8.19 7.32 6.59 5.97 5.44

2.5% 8.91 7.88 7.04 6.34 5.75 Ter

min

al g

row

th

3.0% 9.80 8.57 7.59 6.78 6.11 Source: Company, Standard Chartered Research estimates

Fig 4: Upside/downside from current price WACC

7.2% 7.7% 8.2% 8.7% 9.2%

1.0% 55% 41% 28% 17% 8%

1.5% 66% 50% 36% 24% 13%

2.0% 79% 60% 44% 31% 19%

2.5% 95% 73% 54% 39% 26%Ter

min

al g

row

th

3.0% 114% 88% 66% 48% 34%Source: Company, Standard Chartered Research estimates

Future REIT injections valued at 20% discount to historical average of past four tranches

DCF valuation reflects strong cash flow and steady compounding

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 6

Historical valuation

In the last 5 years, KPJ has traded in the range of PER 4x to 19x on 12-month forward earnings. KPJ’s share price has rallied 11% since the beginning of May.

Fig 5: PER band chart M

YR

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

19x

12x

10x

8x

6x

16x

14x

4x

* Priced as at 29 June 2011 Source: Company, Bloomberg, Standard Chartered Research estimates

During the financial crisis (from beginning 2008 to March 2009), KPJ’s shares were down by 19% and outperformed the KLCI by 21%.

Fig 6: KPJ’s share price performance relative to KLCI

50%

65%

80%

95%

110%

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09

KPJ MK rebased KLCI rebased

Source: Bloomberg

Historically, KPJ traded at very low valuations as the market overlooked its growth prospects

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 7

Merger and acquisition valuation

Key M&A deals in both Singaporean and Malaysian hospital sectors have been executed in an implied PER range of 23x-32x over the last 6 years. Our target PER20x 2012E is at a 30% discount to the average PER multiple of 29x. We believe the high industry acquisition multiples reflect the steady growth, high predictability, and strong cash flow generation of the businesses.

Previous acquisition valuation: Pantai Holdings. Khazanah and Parkway Holdings acquired Pantai Holdings in 2006 at

PER23x 2005 net profit. Khazanah and Parkway formed a 51:49 joint venture for the acquisition.

Apollo Hospitals. (APHS IN, Not rated, last close INR483.1) In 2005, Khazanah paid INR1,925m (USD44.2m) for a 13.2% stake in Apollo Hospitals of India. This translates to PER32x 3/2006 net profit.

Parkway Holdings (unlisted). In 2010, Khazanah Nasional Bhd increased its stake in Parkway Holdings in a deal valued at SGD2.8bn at an implied PER27x.

Thomson Medical (unlisted). Sasteria Pte Ltd gained full control over Thomson Medical with two deals in Nov 2010 and Jan 2011. The initial deal was valued at SGD202m, at PER27x, and the final deal was valued at SGD292m, translating to PER26x.

Integrated Healthcare (unlisted). Mitsui acquired a 30% stake in Integrated Healthcare Holdings from Khazanah Nasional Bhd for a sum of MRY3.3bn. Integrated Healthcare’s holdings include Parkway Hospitals and Pantai Hospitals.

Fig 7: Historical M&A deals and valuation

Deal

valueNet

profit Date Target Acquirer Description Currency (m) (m) Year Valuation

8-May-11 Integrated Healthcare Mitsui & Co Ltd Minority purchase MYR 3,300 Na na na

24-Jan-11 Thomson Medical Centre Sasteria Pte Ltd Company takeover SGD 292 19 2011E PER26x 2011E profit

24-Nov-10 Parkway Holdings Khazanah Nasional Additional stake to obtain control SGD 2,841 162 2011E PER27x 2011E profit

9-Nov-10 Thomson Medical Centre Sasteria Pte Ltd Acquisition of minority SGD 202 19 2011E PER27x 2011E profit

14-May-08 Parkway Holdings Khazanah Nasional Additional stake SGD 532 119 2009 PER27x 2009 profit

27-Nov-06 Pantai Holdings Bhd Khazanah Nasional Additional stake to obtain control MYR 868 63 2005 PER23x 2005 profit

3-Aug-05 Apollo Hospitals Khazanah Nasional Minority purchase INR 1,925 457 3/2006 PER32x 3/2006 profitSource: Bloomberg, Standard Chartered Research estimates

Major M&A deals at an implied PER of 11x-56x

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 8

Peer comparison KPJ’s margins and average revenue per bed are lower than the sector average as it is less leveraged to high-end specialist healthcare. However, KPJ’s ROCE is similar to the sector average due to its asset-light model with disposal of properties to Al-’Aqar REIT.

Gross margin KPJ’s reported gross margin of 31% in FY2010 is close to the sector average of 38% (only for the peers in the below chart). However, a more accurate reflection of KPJ’s margins would be to exclude consultation revenue as KPJ only retains 5-10% as a hospital management fee. If we exclude the fees paid to consultants from the total revenue, KPJ’s adjusted margin improves to 42% for 2010. (We assume fees paid to consultants to be 92.5% of consultation income.)

Fig 8: Gross margin FY2010

0%

10%

20%

30%

40%

50%

Ave

rage

Tho

mso

nM

edic

al

Ban

gkok

Dus

itM

edic

al

KP

JH

ealth

care

-A

djus

ted

Bum

rung

rad

Hos

pita

l

Ban

gkok

Cha

inH

ospi

tals

KP

JH

ealth

care

-R

epor

ted

Note: Average excludes KPJ Healthcare’s adjusted margin Source: Companies, Bloomberg

Net margins KPJ’s net margin of 7.2% in FY2010 is at the lower end of the sector and below the Asian hospitals average of 12.2%. However, KPJ’s adjusted margin was 9.9% in 2010, closer to the sector average.

Fig 9: Net margins FY2010

0%

3%

6%

9%

12%

15%

18%

21%

Ave

rage

Tho

mso

nM

edic

al

Raf

fles

Med

ical

Ban

gkok

Cha

inH

ospi

tals

Bum

rung

rad

Hos

pita

l

Par

kway

KP

JH

ealth

care

-A

djus

ted

Ban

gkok

Dus

itM

edic

al

For

tisH

ealth

care

KP

JH

ealth

care

-R

epor

ted

Apo

lloH

ospi

tals

Note: Average excludes KPJ Healthcare’s adjusted margin Source: Companies, Bloomberg

KPJ’s gross margin of 31% is close to the sector average of 35%

KPJ’s net margin dragged down by lower EBIT per licensed bed

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 9

ROCE KPJ’s ROCE of 12% in FY2010 is equal to the Asian Hospital sector average despite lower gross and net margins. This is mainly due to the asset-light nature of the business with most of its hospitals owned by the KPJ Al-‘Aqar REIT.

Fig 10: ROCE FY2010

0%

5%

10%

15%

20%

Ave

rage

Ban

gkok

Cha

inH

ospi

tals

Bum

rung

rad

Hos

pita

l

Raf

fles

Med

ical

Tho

mso

nM

edic

al

KP

JH

ealth

care

Ban

gkok

Dus

itM

edic

al

Apo

lloH

ospi

tals

For

tisH

ealth

care

Source: Companies, Bloomberg

Number of licensed beds KPJ has over 2,500 beds in 20 hospitals as of June 2011. Apollo Hospitals is one of the largest in the region in terms of number of licensed beds with over 8,500 beds in 54 hospitals.

Fig 11: Number of licensed beds as at June 2011

0

1,500

3,000

4,500

6,000

7,500

9,000

Ave

rage

Apo

lloH

ospi

tals

Ban

gkok

Dus

itM

edic

al

Par

kway

For

tisH

ealth

care

KP

JH

ealth

care

-R

epor

ted

Ban

gkok

Cha

inH

ospi

tals

Bum

rung

rad

Hos

pita

l

Raf

fles

Med

ical

Num

ber

of li

cens

ed b

eds

Source: Companies, Google Finance

Revenue per licensed bed KPJ’s average revenue per licensed bed is significantly below Raffles Medical and Parkway as it is less leveraged to high-end specialist care. KPJ’s revenue per licensed bed is similar to Bangkok Dusit Medical (BGH TB, Not rated, last close THB52.00), perhaps because both have a strategy of building a network of hospitals across the country. In contrast, Bumrungrad (BH TB, Not rated, last close THB36.75) and Raffles Medical have the highest revenue per licensed bed as they focus on one flagship hospital in the city centre and are more focused on high-end care. This difference in strategy is also reflected in average operating profit per licensed bed with Bumrungrad and Raffles Medical at the top, and KPJ at a very similar level to Bangkok Dusit Medical.

KPJ’s sector-average margin of 12% is due to the asset-light nature of operations

KPJ is the fifth largest hospital in the region in terms of licensed beds

KPJ’s closest peer is perhaps Bangkok Dusit as both build nationwide networks

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 10

Fig 12: Revenue per licensed bed in FY2010

0

100

200

300

400

500

600

Ave

rage

Bum

rung

rad

Hos

pita

l

Raf

fles

Med

ical

Par

kway

KP

JH

ealth

care

-R

epor

ted

Ban

gkok

Dus

itM

edic

al

KP

JH

ealth

care

-A

djus

ted

For

tisH

ealth

care

Ban

gkok

Cha

inH

ospi

tals

Apo

lloH

ospi

tals

US

D (

'000

)

Note: Bumrungrad, Raffles Medical, Bangkok Dusit and Apollo are based on segmental revenue while others are based on total revenue Source: Companies, Bloomberg

Fig 13: Operating profit per licensed bed in FY2010

0

20

40

60

80

100

120

Ave

rage

Bum

rung

rad

Hos

pita

l

Raf

fles

Med

ical

Par

kway

Ban

gkok

Dus

itM

edic

al

Ban

gkok

Cha

inH

ospi

tals

KP

JH

ealth

care

For

tisH

ealth

care

Apo

lloH

ospi

tals

US

D (

'000

)

Note: Raffles Medical, and Apollo are based on segmental operating profit while others are based on total operating profit Source: Companies, Bloomberg

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 11

Company overview KPJ Healthcare Berhad is the leading private healthcare provider in Malaysia with 20 hospitals and over 2,500 beds. KPJ is part of Johor Corporation, a corporate linked to the Johor State Government. KPJ is the leading private hospital operator in Malaysia by number of hospitals, beds, and number of affiliated doctors. KPJ also owns 49% of Al-’Aqar REIT, a separately listed entity to allow KPJ to dispose of its hospitals into.

History

KPJ Healthcare commenced operations in 1981 with its first hospital in Johor. KPJ was listed on the Bursa Malaysia on 29 November 1994 and was the first healthcare company to be listed on the Main Board of Bursa Malaysia. In 2006, KPJ established Al-’Aqar REIT and to date has injected 4 tranches of properties into the REIT.

Business segments

KPJ discloses its segmental revenue by hospital income, consultation income, sale of pharmaceutical, medical and surgical products, and other hospital income.

Hospital Income – 2010: 38.6% of revenue Hospital Income grew by 22% p.a over 2000-2010 to MYR638m in 2010 from MYR84m in 2000. This was driven by an increase in number of hospitals to 21 in 2010 from two in 2000. The number of inpatients rose to 222,758 in 2010 from 28,484 in 2000, growing at 23% p.a.

Consultation Income – 2010: 29.6% of revenue Consultation income grew by 28% p.a. over 2000-2010 to MYR490m in 2010 from MYR40m in 2000. This was mainly attributable to an increase in number of medical consultants from 95 in 2000 to 750 in 2010; and growth in number of outpatients by 24% p.a. over the period.

Sale of pharmaceutical, medical and surgical products – 2010: 30.7% of revenue Revenue from the sale of pharmaceutical, medical and surgical products increased to MYR507m in 2010 from MYR5m in 2002, growing at 58% p.a. over 2002-2010.

Other hospital income – 2010: 1.1% of revenue The other hospital income segment includes income from clinic rental, laboratory test fees, investment income and others. Other hospital income grew by 39% p.a. over 2000-2010 to MYR19m in 2010 from MYR1m in 2000.

Revenue breakdown

The 2010 revenue breakdown was 38.6% hospital income, 29.6% consultation income, 30.7% sale of pharmaceutical, medical and surgical products; and other hospital income 1.1%.

Fig 14: Revenue breakdown in 2010

Hospital Income 38.6%

Consultation Income 29.6%

Sale of pharmaceutical, medical and surgical products 30.7%

Other hospital income 1.1%

Legend: segments listed clockw ise from top

Source: Company

Hospital income accounted for 38.6% of total revenue in 2010

KPJ was the first healthcare company to be listed on the Main Board of Bursa Malaysia

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 12

We also show adjusted revenue breakdown excluding 92.5% of consultation income as KPJ provides centralised collection for its specialist doctors. This adjusted revenue is more reflective of KPJ’s actual income.

Fig 15: Adjusted revenue breakdown in 2010

Hospital Income 53.1%

Consultation Income 3.1%

Sale of pharmaceutical, medical and surgical products 42.2%

Other hospital income 1.6%

Legend: segments listed clockw ise from top

Note: The consultation income excludes the revenue received on behalf of consultants Source: Company

Geographic breakdown

KPJ generates most of its revenue from the operation of hospitals in Malaysia, which accounted for 92.6% of total revenue in 2010. Assuming all support services are based in Malaysia, Malaysia accounted for 99.8% of the total revenue of KPJ Healthcare in 2010.

Fig 16: Geographic breakdown in 2010

Operating of specialist hospitals - Malaysia 92.6%

Operating of specialist hospitals - Indonesia 0.2%

Support services 7.2%

Legend: segments listed clockw ise from top

Source: Company

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 13

Porter’s five forces

Fig 17: Malaysian private healthcare industry: Porter’s five competitive forces model Malaysia has a tight supply of

specialist doctors so their bargaining power is high. KPJ is relatively well positioned to peers as it already has the largest panel of specialist doctors and has an established working system with doctors (centralised collection, etc).

KPJ sources medical equipment from the few manufacturers globally but enjoys economies of scale as the group centralises purchasing.

The healthcare sector in Malaysia is highly regulated (by the Private Healthcare Facilities and Services Act) and regulatory approval is required to set up a private hospital.

Due to the limited supply of specialist doctors, hospital groups with a strong reputation and established systems (centralised collection and billing) have an edge in recruiting doctors.

The Ministry of Health recommends a 20km distance between private hospitals and this largely precludes new entrants into communities with an existing private hospital.

Suppliers Potential entrants

Bargaining power of suppliers

HIGH

Threat of new entrants

MEDIUM Industry competitors

Rivalry among existing firms

MEDIUM

Substitutes Buyers

Threat of substitute products

LOW

Bargaining power of buyers

MEDIUM

Public healthcare is an alternative, but it only receives 46% of the sector expenditure while accepting 74% of admissions. As a result, the public healthcare system is highly stretched and we expect those who can afford it to shift to private healthcare.

For medical tourism, Thailand and Singapore are more popular medical tourism destinations, but medical tourism is a small portion of Malaysia’s private healthcare market (for KPJ it is about 6%).

There are several hospital operators

with sizeable networks in Malaysia, with KPJ having the largest (20) followed by Pantai (10) and Columbia Asia (9).

However, due to the Ministry of Health’s recommendation of zoning with a 20km distance between private hospitals, direct competition is limited.

Conventional economics also may not apply to healthcare due to ‘information asymmetry’ (doctors have superior knowledge to their patients).

For the private healthcare market, patients are generally less sensitive to pricing as they seek the best healthcare service provider.

As KPJ operates community hospitals where it is generally the main hospital for the community, it seeks to be the first hospital of choice for its patients.

Adapted from: Porter 1980 p.4. Source: Company, Standard Chartered Research

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 14

SWOT

Fig 18: SWOT analysis – KPJ Healthcare

Strengths

Market leadership – KPJ Healthcare is the largest private hospital operator in Malaysia with 20 hospitals and over 2,500 beds (as at end-2010). We estimate KPJ has a leading 20% share of private hospital beds in Malaysia and a leading 25% share of private inpatient admission.

Strong relationship with doctors – In 2010, KPJ healthcare had 750 medical consultants, which translates to a 7% share of private doctors in Malaysia. KPJ has an established and reputable system in place for centralised payment and billing, helping it in recruitment of doctors.

Brand and reputation – As the largest private hospital operator in Malaysia, KPJ has an established reputation. For example, its Damansara hospital is regarded as one of the best in Malaysia.

Private nursing college – KPJ has its own nursing college. As nurses are in short supply, this gives KPJ a competitive advantage in sourcing nurses.

Strong parent – KPJ’s parent, Johor Corporation, is one of Malaysia’s leading conglomerates and provides potential synergies with KPJ. For example, for its upcoming Iskandar hospital, KPJ’s sister company, Johor Land, will build and own the hospital while KPJ will lease.

Weaknesses

Failure in overseas expansion – KPJ has failed to manage the operation of its hospitals in Bangladesh and Saudi Arabia.

Accreditation – While 10 of KPJ’s 20 hospitals in Malaysia have obtained Malaysian Society for Quality in Health (MSQH) accreditation, none of KPJ’s hospitals have obtained JCI accreditation. This limits KPJ’s ability to attract medical tourists, although three of its hospitals are currently seeking accreditation.

Government link – As KPJ is ultimately owned by the state of Johor, KPJ may be used to advance a national agenda to the detriment of minority shareholders. However, to date KPJ has had a good track record with all hospitals in Malaysia profitable.

Opportunities

Structural growth of private healthcare. With the public healthcare system highly stretched (46% of the sector expenditure but 74% of the admissions), we expect Malaysians who can afford it to shift to private healthcare. In addition, Malaysia has a rapidly growing and ageing population.

Healthcare insurance – The rise in income levels and public awareness has led to increased demand for healthcare insurance as customers seek medical and health protection.

Potential for medical tourism – The Malaysia government has plans to spur growth in the medical tourism market. Although we have not factored in robust growth, this could be significant if successful.

Healthcare education – KPJ’s nursing college is currently still small with a capacity for 2,500 while Masterskill has over 18,000 students. KPJ has plans to expand the capacity of its college to 10,000 in 5 years.

Threats

Increasing competition – More aggressive expansion and competition from existing players such as Parkway and Columbia Asia may hurt KPJ. However, we note that each has slightly different positioning.

Shortage of healthcare professionals – There is a lack of qualified doctors and nurses to cater to the growing demand for healthcare services.

Insurance companies are negotiating for more discounts – Along with growth and increasing penetration of health insurance, insurance companies are negotiating for bigger discounts with private healthcare providers.

Source: Company. Standard Chartered Research

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 15

Structural drivers

Growing population

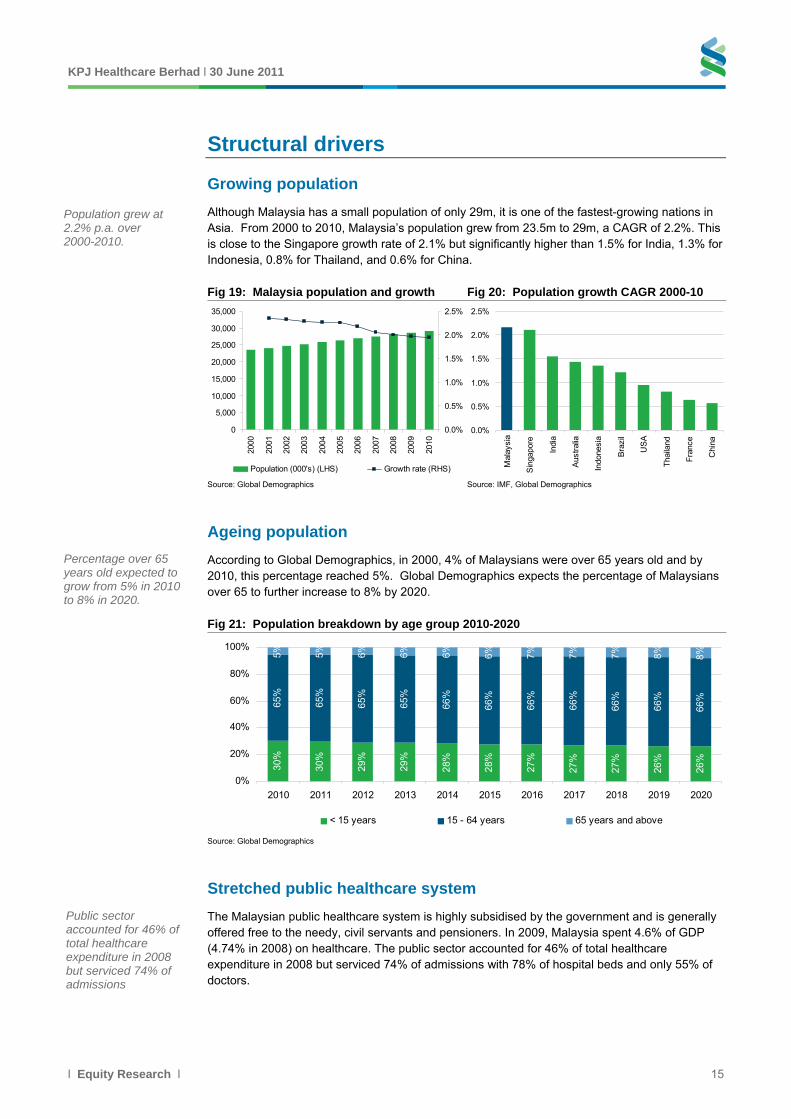

Although Malaysia has a small population of only 29m, it is one of the fastest-growing nations in Asia. From 2000 to 2010, Malaysia’s population grew from 23.5m to 29m, a CAGR of 2.2%. This is close to the Singapore growth rate of 2.1% but significantly higher than 1.5% for India, 1.3% for Indonesia, 0.8% for Thailand, and 0.6% for China.

Fig 19: Malaysia population and growth Fig 20: Population growth CAGR 2000-10

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Population (000's) (LHS) Growth rate (RHS)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Mal

aysi

a

Sin

gapo

re

Indi

a

Aus

tral

ia

Indo

nesi

a

Bra

zil

US

A

Tha

iland

Fra

nce

Chi

na

Source: Global Demographics Source: IMF, Global Demographics

Ageing population

According to Global Demographics, in 2000, 4% of Malaysians were over 65 years old and by 2010, this percentage reached 5%. Global Demographics expects the percentage of Malaysians over 65 to further increase to 8% by 2020.

Fig 21: Population breakdown by age group 2010-2020

30%

30%

29%

29%

28%

28%

27%

27%

27%

26%

26%

65%

65%

65%

65%

66%

66%

66%

66%

66%

66%

66%

5% 5% 6% 6% 6% 6% 7% 7% 7% 8% 8%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

< 15 years 15 - 64 years 65 years and above

Source: Global Demographics

Stretched public healthcare system

The Malaysian public healthcare system is highly subsidised by the government and is generally offered free to the needy, civil servants and pensioners. In 2009, Malaysia spent 4.6% of GDP (4.74% in 2008) on healthcare. The public sector accounted for 46% of total healthcare expenditure in 2008 but serviced 74% of admissions with 78% of hospital beds and only 55% of doctors.

Public sector accounted for 46% of total healthcare expenditure in 2008 but serviced 74% of admissions

Population grew at 2.2% p.a. over 2000-2010.

Percentage over 65 years old expected to grow from 5% in 2010 to 8% in 2020.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 16

Fig 22: Public-Private sector distribution of resources and workload - 2008

55%

78%

74%

46%

45%

22%

26%

54%

Doctors *

Hospital beds

Admissions

Hospital expenditure

Public Private

22,087 doctors

53,118 hospital beds

MYR18bn

2.95m admissions

* Total number of doctors excluding housemen Source: Ministry of Health

Private healthcare gaining share

In 2000, 53% of healthcare spending was on public healthcare but the private sector has been steadily gaining share. By 2008, public healthcare only accounted for 46% of sector spending. From 2000 to 2008, private healthcare grew at 16% p.a. while public healthcare grew at 13% p.a.

Fig 23: Public and Private healthcare expenditure in Malaysia

Fig 24: Number of doctors in Malaysia

53%

59%

59%

54%

50%

44%

45%

44%

46%

47%

46%

47%

45%

50%

56%

56%

56%

54%

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Public healthcare expenditure Private healthcare expenditure

39%

40%

40%

34%

61%

60%

60%

66%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009

Private doctors Public doctors

Source: Ministry of Health Source: Ministry of Health

Fig 25: Public healthcare expenditure Fig 26: Private healthcare expenditure

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

2000 2001 2002 2003 2004 2005 2006 2007 2008

MY

Rm

-10%

0%

10%

20%

30%

40%

Public healthcare expenditure (LHS) Growth (RHS)

CAGR 2000-08 13%

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

MY

Rm

-5%

5%

15%

25%

35%

45%

Private healthcare expenditure (LHS) Growth (RHS)

CAGR 2000-08 16%

Source: Ministry of Health Source: Ministry of Health

Growing household income

Malaysia’s GDP per capita grew at 6.2% p.a. over 2000 to 2009 to reach USD6,950 in 2009, according to the International Monetary Fund (IMF). It dropped in 2009 due to the impact of the global recession on Malaysia. In 2008, GDP per capita stood at USD8,143. The IMF expects Malaysia’s GDP per capita to grow at 7% p.a. over 2009 to 2015.

GDP per capita of USD6,950 in 2009

Private healthcare compounded at 16% p.a. from 2000-2008.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 17

Fig 27: Malaysia’s GDP per capita

0

2,000

4,000

6,000

8,000

10,000

12,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

E

2011

E

2012

E

2013

E

2014

E

2015

E

US

D

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Malaysia's GDP per capita (LHS) Grow th rate (RHS)

Source: IMF

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 18

Strong market position

Leading market share

KPJ is the largest private hospital operator in Malaysia with 20 hospitals and growing. KPJ has the leading share of the market by every category from number of hospitals and number of beds, to admissions.

Hospitals. KPJ has 20 hospitals in Malaysia while the closest competitors, Pantai and Columbia Asia, only have 10 and 9, respectively.

Beds. KPJ has a 20% share of private hospital beds in Malaysia. (KPJ has over 2500 licensed beds as at June 2011 while there were 12,216 private hospital beds as of 2009).

Share of medical consultants. At end-2010, KPJ had a 7% share of private doctors and a 2% share of total doctors in Malaysia. (This share is dragged down by the number of general practitioners as KPJ does not operate in the family clinic space.)

Inpatient admissions. In 2009, KPJ had a 25% share of private hospital admissions and a 7% share of total nationwide admissions (both public and private).

Fig 28: Share of private hospital beds Fig 29: Share of private medical consultants

KPJ Healthcare 20%

Pantai 14%

Columbia Asia 4%

Prince Court 2%

Tropicana 2%

Others 58%

Legend: segments listed clockwise from top

KPJ Healthcare 7%

Pantai 5%

Columbia Asia 1%

Tropicana 0%

Others 93%

Legend: segments listed clockwise from top

Note: Number of licensed beds as of June 2011, Private hospital beds for 2009 as reported by Ministry of Health Source: Companies, Ministry of Health

Note: Number of consultants as of June 2011, Private medical consultants for 2009 as reported by Ministry of Health Source: Companies, Ministry of Health

Fig 30: Share of private inpatient admissions - 2009

Fig 31: Share of private outpatient admissions - 2009

KPJ Healthcare 25%

Others 75%

Legend: segments listed clockwise from top

KPJ Healthcare 69%

Others 31%

Legend: segments listed clockwise from top

Source: Company, Ministry of Health Source: Company, Ministry of Health

KPJ has a 20% share of private hospital beds, 7% share of private doctors, and 25% share of private hospital admissions

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 19

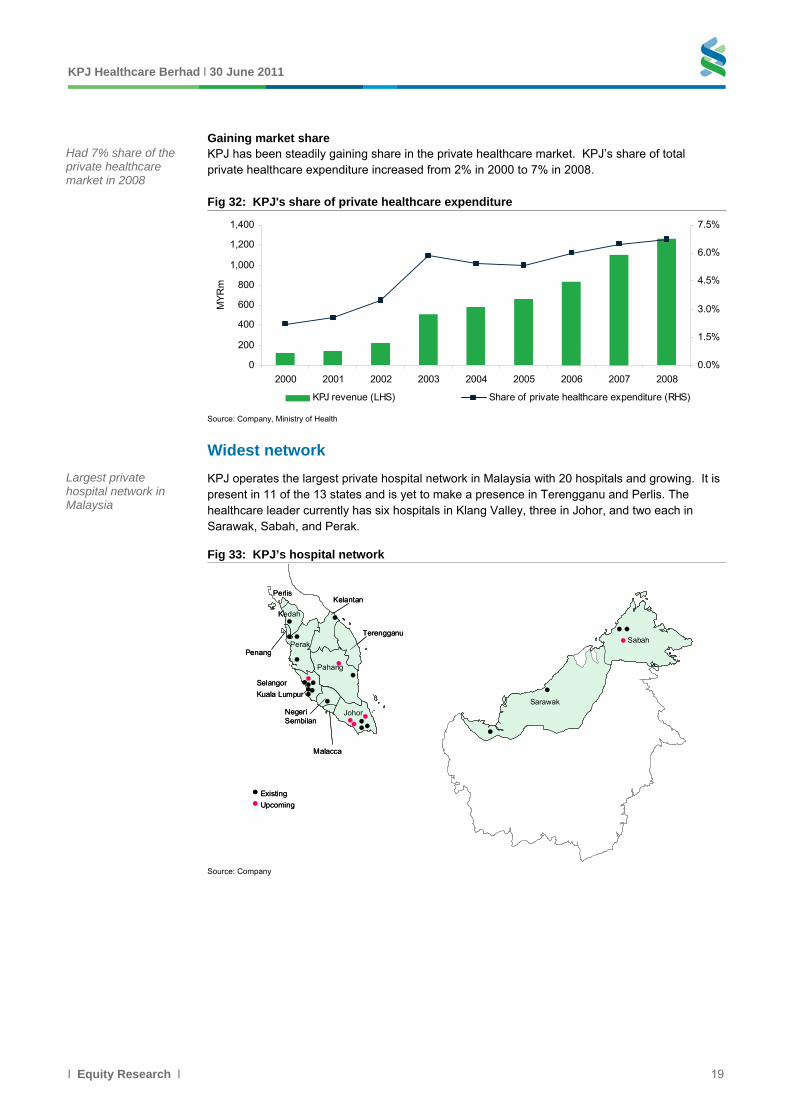

Gaining market share KPJ has been steadily gaining share in the private healthcare market. KPJ’s share of total private healthcare expenditure increased from 2% in 2000 to 7% in 2008.

Fig 32: KPJ's share of private healthcare expenditure

0

200

400

600

800

1,000

1,200

1,400

2000 2001 2002 2003 2004 2005 2006 2007 2008

MY

Rm

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

KPJ revenue (LHS) Share of private healthcare expenditure (RHS)

Source: Company, Ministry of Health

Widest network

KPJ operates the largest private hospital network in Malaysia with 20 hospitals and growing. It is present in 11 of the 13 states and is yet to make a presence in Terengganu and Perlis. The healthcare leader currently has six hospitals in Klang Valley, three in Johor, and two each in Sarawak, Sabah, and Perak.

Fig 33: KPJ’s hospital network

Sabah

Sarawak

Terengganu

Pahang

Johor

Malacca

Negeri Sembilan

Selangor

Perak

Kelantan

Penang

Kedah

Perlis

Kuala Lumpur

Upcoming

Existing

Sabah

Sarawak

Terengganu

Pahang

Johor

Malacca

Negeri Sembilan

Selangor

Perak

Kelantan

Penang

Kedah

Perlis

Kuala Lumpur

Upcoming

Existing

Source: Company

Largest private hospital network in Malaysia

Had 7% share of the private healthcare market in 2008

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 20

Current hospital details

10 of the hospitals in Malaysia have obtained Malaysian Society for Quality in Health (MSQH) certification while 7 are ISO certified. Currently, Ampang Puteri Hospital and Seremban Specialist Hospital are working towards Joint Commission International (JCI) accreditation.

Fig 34: KPJ Hospitals

No. Name of hospital State Year of build /

acquisitionBuilt /

AcquiredNumber of

beds Accreditations

Malaysia 1 KPJ Johor Specialist Hospital Johor 1981 Built 200 MSQH2 Puteri Specialist Hospital Johor 1993 Acquired 146 3 Kluang Utama Specialist Hospital Johor 2008 Acquired 40 4 KPJ Ampang Puteri Specialist Hospital Selangor 1995 Built 217 ISO 9001:2000, MSQH 5 KPJ Damansara Specialist Hospital Selangor 1997 Built 158 ISO 9001:2000, MSQH 6 KPJ Selangor Specialist Hospital Selangor 2006 Acquired 169 ISO 9001:2000, MSQH 7 KPJ Kajang Specialist Hospital Selangor 2006 Acquired 110 MSQH8 KPJ Tawakkal Specialist Hospital Selangor 1984 Built 147 ISO 9001:20009 Sentosa Medical Centre Selangor 2006 Acquired 135 10 KPJ Perdana Specialist Hospital Kelantan 2002 Built 83 MSQH11 Kedah Medical Centre Kedah 1991 Acquired 98 ISO 9001:2000, MSQH 12 KPJ Seremban Specialist Hospital Negeri Sembilan 2004 Built 130 MSQH13 KPJ Ipoh Specialist Hospital Perak 1989 Acquired 250 ISO 9001:2000, MSQH 14 Taiping Medical Centre Perak 2008 Acquired 46 15 KPJ Penang Specialist Hospital Penang 1985 236 MSQH16 Kuantan Specialist Hospital Pahang 1990 Acquired 72 ISO 900217 Kuching Specialist Hospital Sarawak 2003 Built 80 18 Sibu Specialist Medical Centre Sarawak 2011 Acquired 50 19 Kota Kinabalu Specialist Hospital Sabah 2005 Acquired 43 20 Sabah Medcial Centre Sabah 2010 Acquired 95 Total number of beds - Malaysia 2,505 Indonesia 21 RS Bumi Serpong Damai 2010 60 22 RS Medika Permata Hijau 1995 80 Total number of beds - Indonesia 140 Total number of beds 2,645 Source: Company

Upcoming hospitals

KPJ is planning to invest MYR250m over the next two years on four key new projects which should expand the total KPJ network of hospitals to 24 by the end of 2013. It is also building a new hospital to replace Sabah Medical Centre, which should be completed by 2012. The company has also announced plans to build a 400-bed specialist hospital in Iskandar in Johor.

Fig 35: Upcoming hospitals Hospital Name Location Status Year of completion No. of beds

Bandar Baru Klang Specialist Hospital Selangor New 2011 200

Muar Specialist Hospital Johor New 2012 90

Pasir Gudang Specialist Hospital Johor New 2012 90

Tanjung Lumpur, Kuantan - Preliminary Pahang New 2013 90

New Sabah Medical Centre Sabah Replacement 2012 95

Iskandar Specialist Hospital Johor New na 400Source: Company, Business Times

10 of the 20 hospitals have MSQH certification

Four new projects in progress at a cost of MYR250m, and a fifth on the pipeline

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 21

Competitor analysis and positioning

Operation comparison

KPJ is the largest private hospital operator in Malaysia with 20 hospitals and over 2,500 licensed beds across Malaysia. Its closest competitor, Pantai has 10 hospitals and 1,739 beds while Columbia Asia has 9 hospitals and 444 beds.

Fig 36: Hospital operator comparison KPJ Pantai Columbia Asia Sime Darby Prince Court Tropicana

Number of Hospitals 20 10 9 1 1 2

Number of Beds 2,505 1,739 444 393 300 204

Number of specialist doctors 750 500 112 160 na 50

Number of nurses 8,000 1,800 na na na naSource: Companies' websites as at 31 May 2011

Fig 37: Number of private hospitals by operator

Fig 38: Number of licensed beds by operator

20

10 9

20

2

4

6

8

10

12

14

16

18

20

KPJhealthcare

Pantai Columbia Asia Tropicana

Num

ber

of h

ospi

tals

2505

1739

444204

0

300

600

900

1,200

1,500

1,800

2,100

2,400

2,700

KPJhealthcare

Pantai ColumbiaAsia

Tropicana

Num

ber

of li

cens

ed b

eds

Source: Companies Source: Companies, Ministry of Health

Positioning comparison

KPJ is positioned as a mid-tier hospital, with an average charge of MYR234 per single-bed room (ranging from MYR100 to MYR368 per single-bed room as of May 2011). Pantai hospitals are higher end with an average rate of MYR317 per single-bed room while Columbia Asia appears to be positioned lower with an average rate of MYR160 per single-bed room. KPJ’s closest peer in terms of positioning may be Prince Court at MYR203 per single-bed room.

Fig 39: Average charges of the hospitals 2010 KPJ Pantai Columbia Asia Prince Court Tropicana

Avg. charge per single bed room 234 317 160 203 250

Avg. charge per double bedded room 140 149 110 na 130

Avg. charge per suite 621 959 na 800 455Note: Average of all the hospitals Source: Companies' websites as at 31 May 2011

KPJ is the largest hospital operator in Malaysia with 20 hospitals and over 2,500 licensed beds

KPJ is positioned as a mid-tier hospital

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 22

Fig 40: Average charge per single bed room

0

50

100

150

200

250

300

350

Pantai Tropicana KPJ Prince Court Columbia Asia

MY

R

Note: Average of all the hospitals Source: Companies' websites as at 31 May 2011

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 23

High barriers to entry The private healthcare sector in Malaysia is difficult to enter as there are several high barriers to entry.

Private Healthcare Facilities and Services Act

Regulates construction of new hospitals The Private Healthcare Facilities and Services Act was announced in 1998 but enforced in 2006 and regulates all private healthcare facilities and services in Malaysia. The act requires approval to be granted before a new private healthcare facility can be established.

Zoning restricts competition As specified in the act, when deciding whether to grant approval for a new private healthcare facility, the body will assess “the extent to which the healthcare facilities or services are already available in an area.” The intention of the act is to encourage healthcare resources to be spread out across the country, otherwise healthcare providers would all focus on the wealthier Klang Valley region. But as KPJ operates community-based hospitals, the act has helped limit direct competition. The typical requirement is that there is a 20km distance between private hospitals.

Exception for specialist hospitals The exception to the 20km zoning requirement is if a group builds a new private centre of excellence. A centre of excellence refers to a medical centre with a specialty in a particular field such as cardiology. Going forward, KPJ may explore building centres of excellence.

Doctors

KPJ has strong relationship with its specialist doctors A significant barrier to entry in the private hospital sector is the difficulty in securing private specialists. KPJ’s consultant specialists pay a one-time practising rights fee of MYR25k-MYR50k in order to practice at KPJ’s hospitals. The practising rights fee is refunded upon death or retirement.

Doctors are in shortage According to the Malaysian government’s economic transformation programme, there is a significant shortage of specialist doctors in several key areas – in particular, anaesthesiology, cardiology, and plastic surgery.

Fig 41: Shortage of specialist doctors -Anaesthesiology

Fig 42: Shortage of specialist doctors - Cardiology

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2010 2020

Demand Supply Shortfall

0

100

200

300

400

500

600

700

2010 2020

Demand Supply Shortfall

Source: Economic Transformation Program Source: Economic Transformation Program

Established centralised collection and billing KPJ also has a well-established centralised system in place for collection and billing. KPJ collects the consultant’s income and pays the doctor twice a month. KPJ charges the doctors 5-10% of their income as a hospital management fee.

The act requires minimum distance of 20km between private hospitals

Malaysia is short of doctors and KPJ has established relationship with large team of doctors

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 24

Growth drivers

Network expansion

Further room for growth KPJ operates community-based hospitals in areas with a population over 200k. KPJ’s hospitals are typically the largest (and often the only) hospital for the community. We estimate there are 40 communities in Malaysia with a population over 200k. Considering KPJ, Pantai, and Columbia Asia’s networks, we estimate there are 19 communities where KPJ could establish a presence.

Fig 43: Communities with population over 200k No. of hospitals by operator Districts

State District Population ('000) 2010

KPJ Healthcare Pantai

Columbia Asia

without any presence

Johor Bahru 1,464 2 - 1

Batu Pahat 406 - 1 -

Muar 398 - - - √

Kluang 317 1 - -

Kota Tinggi 252 - - - √

Johor

Segamat 209 - - - √

Kuala Muda 428 - - 1

Kota Setar 423 1 - -

Kulim 251 - - - √

Kedah

Kubang Pasu 230 - - - √

Kota Bharu 509 1 - - Kelantan

Pasir Mas 211 - - - √

Melaka Melaka Tengah 475 - 1 -

N. Sembilan Seremban 469 1 - 1

Pahang Kuantan 416 1 - -

Timur Laut 524 - - - √

S.P. Tengah 387 - - - √

S.P. Utara 310 1 - -

Pulau Pinang

Barat Daya 216 - - - √

Kinta 852 1 1 -

Larut & Matang 341 1 - 1

Manjung 239 - - - √

Perak

Hilir Perak 233 - - - √

Perlis Perlis 240 - - - √

Petaling 1,509 2 - 3

Hulu Langat 1,150 1 1 1

Klang 833 - 1 -

Gombak 681 - - - √

Kuala Langat 242 - - - √

Selangor

Kuala Selangor 202 1 - -

Terengganu K. Terengganu 341 - - - √

Kuala Lumpur Kuala Lumpur 1,722 2 3 -

Kuching 600 1 - -

Miri 281 1 - 1

Sibu 258 - - - √

Sarawak

Bintulu 200 - - 1

Sandakan 454 - - - √

Kota Kinabalu 436 2 - -

Tawau 402 - - - √

Sabah

Lahad Datu 213 - - - √

Total number of districts without any hospitals by key operators 19 Source: Department of Statistics, Malaysia; Standard Chartered Research estimates

At least 19 more communities where KPJ could open a hospital

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 25

Growth in patient volume

Robust volume growth From 2005 to 2010, KPJ’s annual inpatient and outpatient volume both grew by 14% p.a. (annual inpatients from 117,539 to 222,758; annual outpatients from 1,162,585 to 2,196,769).

Fig 44: Number of inpatients Fig 45: Number of outpatients

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,00020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0%

20%

40%

60%

80%

100%

120%

140%

Number of in-patients (LHS) YoY growth (RHS)

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2,250,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0%

20%

40%

60%

80%

100%

120%

140%

160%

Number of out-patients (LHS) YoY growth (RHS)

Source: Company Source: Company

Growth in revenue per patient

Room to drive revenue intensity From 2005 to 2010, KPJ’s average revenue per inpatient grew at 7% p.a from MYR2,035 to MYR2,865. Before it was privatised, Parkway’s average revenue per inpatient for its Singapore hospitals was SGD5,660/MYR13,867 for 2009. Parkway is clearly much more focused on high-end-specialist care, but we believe the vast differential between the two (KPJ is at a 79% discount to Parkway) reflects the opportunity for KPJ to move up the value chain.

Fig 46: KPJ’s hospital revenue per inpatient Fig 47: Revenue per inpatient- KPJ vs. Parkway FY2010

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 2010

MY

Rm

-10%

-5%

0%

5%

10%

15%

20%

Hospital income per in-patient (LHS) YoY growth (RHS)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

KPJ Parkway

Source: Company Source: Companies

Total number of inpatients grew at 14% p.a. in 2005-10

Hospital income per inpatient grew at 7% p.a. in 2005-10.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 26

Healthcare education KPJ established its own nursing college in 1991. Today, the nursing school is called KPJ International College of Nursing with the main campus at Kotai Seriemas, Nilai, Negeri Sembilan.

Strategic importance

Shortage of nurses in Malaysia KPJ’s involvement in nursing education is strategically important due to the chronic shortage of nursing staff in Malaysia. According to the World Health Organization (WHO), Malaysia has only 27 nurses per 10k population compared to 59 in Singapore and a global average of 30. KPJ College gives KPJ a competitive advantage in securing nurses for its hospitals.

Fig 48: Nurse density per 10K population

0

10

20

30

40

50

60

Singapore Global average Malaysia Indonesia Thailand South East AsiaRegion

Per

10k

pop

ulat

ion

Source: WHO - World Health Statistics 2011

Growing the business

Campus expansion KPJ College’s campus currently has a capacity of up to 2,500 students. The group plans to expand this capacity to 5,000 students in 3 years and 10,000 in 5 years. The main campus is at Nilai, Negeri Sembilan, with a branch campus in Johor Bahru in the South. A new branch campus in the North in Bukit Mertajam will open in 2011.

Highly profitable business

High-margin business According to KPJ management, KPJ College generates revenues of about MYR35m with a net margin of about 20%.

Comparison with Masterskill Masterskill is the only listed comparable for the education business in Malaysia. In 2010, Masterskill had about 18,400 students and generated revenue of MYR316m and a net profit of MYR102m. The business is highly profitable, with a net profit margin of 32%, and generates a return on equity of 20%. The business also appears to be highly scalable as Masterskill has compounded revenue and earnings at 36% and 26% in the last 4 years.

Fig 49: Masterskill – summary financials MYRm 2007 2008 2009 2010 CAGR 2007-10

Revenue 127 203 273 316 36%

Net profit 51 72 97 102 26%

Net margin 41% 36% 36% 32%

ROE 42% 37% 33% 20% Source: Masterskill Education Group Bhd

Masterskill had 18k students and generated MYR102m of net profit in 2010

Vertical integration into nursing college gives KPJ strategic advantage.

College capacity to grow from 2,500 to 10,000 in 5 years

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 27

High regulatory risk One of the key risks for the education business is government regulation. Taking Masterskill as an example, about 95% of its students are financed by the Malaysian government’s PTPTN student loan scheme. Any changes to the size and terms of the loans could significantly affect demand for courses. For KPJ College, about half of the students are funded by PTPTN while the other half is funded by scholarships from KPJ’s hospitals.

Most students dependent on government funding

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 28

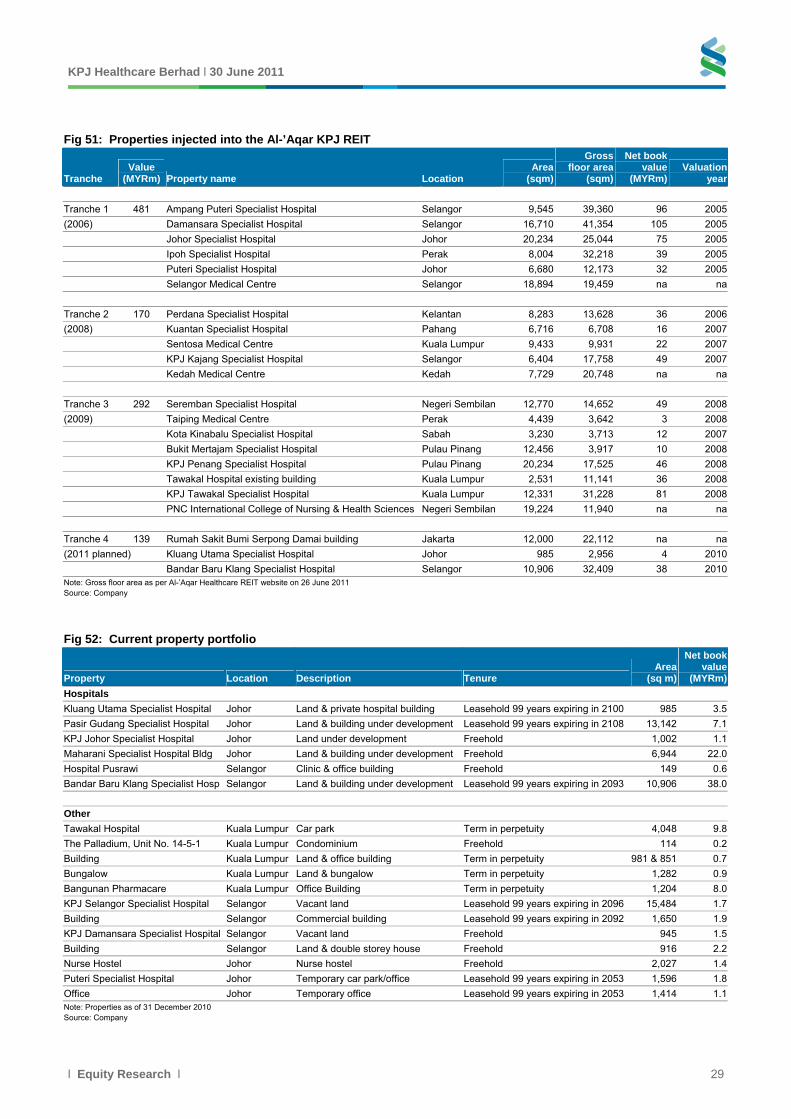

REIT funds expansion KPJ set up the Al-’Aqar KPJ REIT (Al-’Aqar REIT) in 2006 to allow the group to become asset-light. Al-’Aqar REIT was the first healthcare REIT in Asia and the first Islamic REIT in the world. Today, KPJ owns 49% of Al-‘Aqar KPJ REIT.

Asset-light expansion

KPJ sees the Al-’Aqar REIT as a key part of its strategy for expansion as it allows it to free up cash flow to fund further growth. Below are some key highlights of Al-’Aqar REIT:

Al-’Aqar REIT was listed on 10 August 2006

Tranche 1 (2006): 6 properties were injected into the REIT and KPJ raised MYR481m

Tranche 2 (2008): 5 properties were injected for MYR170m.

Tranche 3 (2009): 8 properties were injected for MYR292m.

Tranche 4 (planned 2011): Shareholders have approved injection of 3 properties for MYR139m

Revision of rental rate

The rental that KPJ pays to Al-’Aqar REIT is based on a fixed formula as per below:

(10-year MGS + 238 bps) x market value of the properties

Minimum rental of MYR33m per annum

Maximum 2% increment over the preceding year’s rental amount.

Rental as percentage of revenue The rental amount paid to Al-’Aqar REIT from 2006 to 2010 translated to MYR27-73m p.a. The rate has been steadily rising from 1.6% of revenue in 2006 (only for 6 months from the date of establishment) to 4.4% of revenue in 2010, corresponding with the number of properties injected into the REIT.

Fig 50: Rental expenses

0

50

100

150

200

250

2006 2007 2008 2009 2010

MY

R

0.0%

0.5%1.0%

1.5%

2.0%2.5%

3.0%

3.5%

4.0%4.5%

5.0%

Average rental rate per sqm % of KPJ revenue (RHS)

Note: Rent paid refers to the gross rental income of Al-’Aqar KPJ REIT, Number of sqm is adjusted for timing of injection into REIT Source: Companies

Property portfolio

KPJ has injected 19 hospitals into the Al-’Aqar REIT as at June 2011 and three more are in the pipeline planned for injection in 2011 in tranche 4 for total proceeds of MYR139m.

Maximum 2% increment from preceding year rental.

Rental paid to REIT equivalent to 4.4% of revenue in 2010

19 of the 20 existing hospitals injected into Al-Aqar REIT

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 29

Fig 51: Properties injected into the Al-’Aqar KPJ REIT

Tranche Value

(MYRm) Property name Location Area

(sqm)

Gross floor area

(sqm)

Net book value

(MYRm)Valuation

year

Tranche 1 481 Ampang Puteri Specialist Hospital Selangor 9,545 39,360 96 2005

(2006) Damansara Specialist Hospital Selangor 16,710 41,354 105 2005

Johor Specialist Hospital Johor 20,234 25,044 75 2005

Ipoh Specialist Hospital Perak 8,004 32,218 39 2005

Puteri Specialist Hospital Johor 6,680 12,173 32 2005

Selangor Medical Centre Selangor 18,894 19,459 na na

Tranche 2 170 Perdana Specialist Hospital Kelantan 8,283 13,628 36 2006

(2008) Kuantan Specialist Hospital Pahang 6,716 6,708 16 2007

Sentosa Medical Centre Kuala Lumpur 9,433 9,931 22 2007

KPJ Kajang Specialist Hospital Selangor 6,404 17,758 49 2007

Kedah Medical Centre Kedah 7,729 20,748 na na

Tranche 3 292 Seremban Specialist Hospital Negeri Sembilan 12,770 14,652 49 2008

(2009) Taiping Medical Centre Perak 4,439 3,642 3 2008

Kota Kinabalu Specialist Hospital Sabah 3,230 3,713 12 2007

Bukit Mertajam Specialist Hospital Pulau Pinang 12,456 3,917 10 2008

KPJ Penang Specialist Hospital Pulau Pinang 20,234 17,525 46 2008

Tawakal Hospital existing building Kuala Lumpur 2,531 11,141 36 2008

KPJ Tawakal Specialist Hospital Kuala Lumpur 12,331 31,228 81 2008

PNC International College of Nursing & Health Sciences Negeri Sembilan 19,224 11,940 na na

Tranche 4 139 Rumah Sakit Bumi Serpong Damai building Jakarta 12,000 22,112 na na

(2011 planned) Kluang Utama Specialist Hospital Johor 985 2,956 4 2010

Bandar Baru Klang Specialist Hospital Selangor 10,906 32,409 38 2010Note: Gross floor area as per Al-’Aqar Healthcare REIT website on 26 June 2011 Source: Company

Fig 52: Current property portfolio

Property Location Description Tenure Area

(sq m)

Net book value

(MYRm)

Hospitals

Kluang Utama Specialist Hospital Johor Land & private hospital building Leasehold 99 years expiring in 2100 985 3.5

Pasir Gudang Specialist Hospital Johor Land & building under development Leasehold 99 years expiring in 2108 13,142 7.1

KPJ Johor Specialist Hospital Johor Land under development Freehold 1,002 1.1

Maharani Specialist Hospital Bldg Johor Land & building under development Freehold 6,944 22.0

Hospital Pusrawi Selangor Clinic & office building Freehold 149 0.6

Bandar Baru Klang Specialist Hosp Selangor Land & building under development Leasehold 99 years expiring in 2093 10,906 38.0

Other

Tawakal Hospital Kuala Lumpur Car park Term in perpetuity 4,048 9.8

The Palladium, Unit No. 14-5-1 Kuala Lumpur Condominium Freehold 114 0.2

Building Kuala Lumpur Land & office building Term in perpetuity 981 & 851 0.7

Bungalow Kuala Lumpur Land & bungalow Term in perpetuity 1,282 0.9

Bangunan Pharmacare Kuala Lumpur Office Building Term in perpetuity 1,204 8.0

KPJ Selangor Specialist Hospital Selangor Vacant land Leasehold 99 years expiring in 2096 15,484 1.7

Building Selangor Commercial building Leasehold 99 years expiring in 2092 1,650 1.9

KPJ Damansara Specialist Hospital Selangor Vacant land Freehold 945 1.5

Building Selangor Land & double storey house Freehold 916 2.2

Nurse Hostel Johor Nurse hostel Freehold 2,027 1.4

Puteri Specialist Hospital Johor Temporary car park/office Leasehold 99 years expiring in 2053 1,596 1.8

Office Johor Temporary office Leasehold 99 years expiring in 2053 1,414 1.1Note: Properties as of 31 December 2010 Source: Company

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 30

Group financials

Income statement

Fig 53: Income statement MYRm FY2006 FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E FY2013E

Group Revenue 831 1,108 1,267 1,456 1,655 1,920 2,179 2,473

Cost of goods sold (589) (781) (899) (1,037) (1,151) (1,335) (1,515) (1,712)

Gross profit 243 327 368 419 504 586 665 760

Selling, general, & admin. (152) (205) (229) (244) (313) (351) (399) (444)

Other income 17 13 16 12 12 13 13 14

EBITDA 108 136 155 187 203 247 279 330

Depreciation & amortisation (33) (43) (42) (46) (59) (70) (70) (87)

EBIT 75 93 114 140 144 178 209 243

Finance costs (20) (20) (19) (17) (14) (16) (16) (16)

Finance income - - - 3 7 6 11 9

Associates 5 12 19 19 30 32 33 35

Pretax profit 60 85 114 145 168 199 237 272

Zakat - - - (1) (1) (2) (2) (2)

Taxation (19) (7) (25) (29) (40) (50) (59) (67)

Minorities (0) (4) (4) (4) (7) (9) (10) (11)

Net profit 41 74 86 111 119 139 166 192

Net profit (adjusted) 41 74 86 111 119 139 164 186Source: Company, Standard Chartered Research estimates

Revenue

From 2000 to 2010, KPJ compounded its revenues at 29% p.a.. KPJ recorded exceptional growth of 129% in 2003 given it was the first full operational year following the completion of its corporate restructuring exercise undertaken in 4Q2002. For the restructuring, KPJ added 12 specialist hospitals and 5 support companies compared to only 2 hospitals at the beginning of 2002. We expect revenue to grow by 14% p.a. over the next three years to reach MYR2,473m in 2013E.

Fig 54: Revenue and revenue growth

0

500

1,000

1,500

2,000

2,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

MY

Rm

0%

20%

40%

60%

80%

100%

120%

140%

Hospital Consultation

Pharmaceutical, medical & surgical products Other hospital income

Rvenue grow th (RHS)

Source: Company, Standard Chartered Research estimates

Profitability

Stable EBIT margin Over the last six years, KPJ reported an average EBIT margin of 8.9%. However, we expect EBIT margin to gradually improve to 9.6% in 2013E from 8.7% in 2010 as KPJ continues to gain economies of scale, and occupancy levels increase for the group.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 31

Fig 55: EBIT margin

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

MY

Rm

0%

2%

4%

6%

8%

10%

EBIT (LHS) EBIT margin (RHS)

Source: Company, Standard Chartered Research estimates

Remarkable net profit growth From 2005 to 2010, KPJ’s net profit grew 29% p.a. We expect the group’s net profit to continue to grow at 16% p.a. over 2010-2013E as the group continues to expand its hospital network (1-2 per year) and average revenue per patient grows at 7% p.a. from 2011 to 2013.

Fig 56: Net profit and growth

0

25

50

75

100

125

150

175

200

2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

MY

Rm

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Net prof it (LHS) Net profit grow th (RHS)

Source: Company, Standard Chartered Research estimates

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 32

Balance sheet

Fig 57: Balance sheet MYRm FY2006 FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E FY2013E

Assets

Property, plant & equipment 512 464 304 447 537 478 610 736

Goodwill & intangibles 101 100 110 116 136 136 136 136

Associates 180 167 227 239 307 339 373 408

Others 54 164 295 144 150 150 150 150

Long term assets 847 895 936 946 1,131 1,104 1,269 1,430

Cash & cash equivalents 95 100 106 144 197 362 315 287

Inventories 22 27 30 30 42 46 52 58

Receivables 131 153 195 243 298 307 348 395

Others 7 29 11 9 12 12 12 12

Total current assets 255 310 342 426 550 727 727 752

Total assets 1,102 1,205 1,278 1,372 1,680 1,831 1,996 2,182

Liabilities and Equity

Payables 173 210 236 261 308 359 408 461

Short term debt 52 91 114 95 399 399 399 399

Others 26 17 2 1 18 18 18 18

Current liabilities 251 318 352 356 725 776 824 878

Long term debt 323 307 268 303 37 37 37 37

Deferred income tax 31 14 19 23 41 41 41 41

Others 10 10 11 13 14 14 14 14

Total liabilities 615 650 650 695 817 868 916 969

Minorities 45 46 48 45 95 103 113 125

Shareholders funds 443 509 581 632 769 860 967 1,088

Total liabilities and equity 1,102 1,205 1,278 1,372 1,680 1,831 1,996 2,182Source: Company, Standard Chartered Research estimates

Fig 58: Assets – 1Q2011 Fig 59: Liabilities - 1Q2011

Fixed assets 33%

Other non-curr. Assets 35%

Receivables 18%

Inventories 3%

Cash 10%

Other curr. Assets 1%

Legend: segments listed clockwise from top

Creditors 17%

Total debt 24%

Other liabilities 7%

Equity 52%

Legend: segments listed clockwise from top

Source: Company Source: Company

Fixed assets accounted for only 33% of KPJ’s total assets in 1Q2011 reflecting the asset-light nature of the operations given the injection of hospitals into the Al-’Aqar REIT. KPJ’s capital structure was equally balanced between liabilities (48%) and equity (52%) at the end of 1Q2011.

Debt KPJ’s net gearing steadily decreased from 78% in 2005 to 23% in 2010 due to the strong cash flow of the business, particularly with the setup of Al-’Aqar REIT in 2006 allowing the group to dispose of its hospitals into the REIT.

KPJ Healthcare Berhad l 30 June 2011

l Equity Research l 33

Fig 60: Total debt and net gearing

0

50

100

150

200

250

300

350

400

450

2002 2003 2004 2005 2006 2007 2008 2009 2010

MY