Making financial markets work for the poor Remittances from South Africa to SADC Geoff Orpen 26 March 2015

Making financial markets work for the poor Remittances from South Africa to SADC Geoff Orpen 26 March 2015.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Making financial markets work for the poor

Remittances from South Africa to SADC

Geoff Orpen26 March 2015

About FinMark Trust and its focus areas

• Independent trust formed in April 2002• Initial and core funding from the UKAid• Mission: “Making Financial Markets Work for the Poor”• Aim: Facilitating and catalysing development around access to financial services• How: move beyond data production, with an increased focus on being a catalyst to

systemic change in financial inclusion by providing support to transformation at a country level

Savings

Credit SMME access

Cross cutting themes:

Focus areas

Information and Research Support

Consumer Financial Empowerment

Financial Policy and Regulation

Housing Finance

Micro-insurance

Regional Financial Integration

Retail payments systems

Rural / agricultural finance

2

Coverage of our regional work

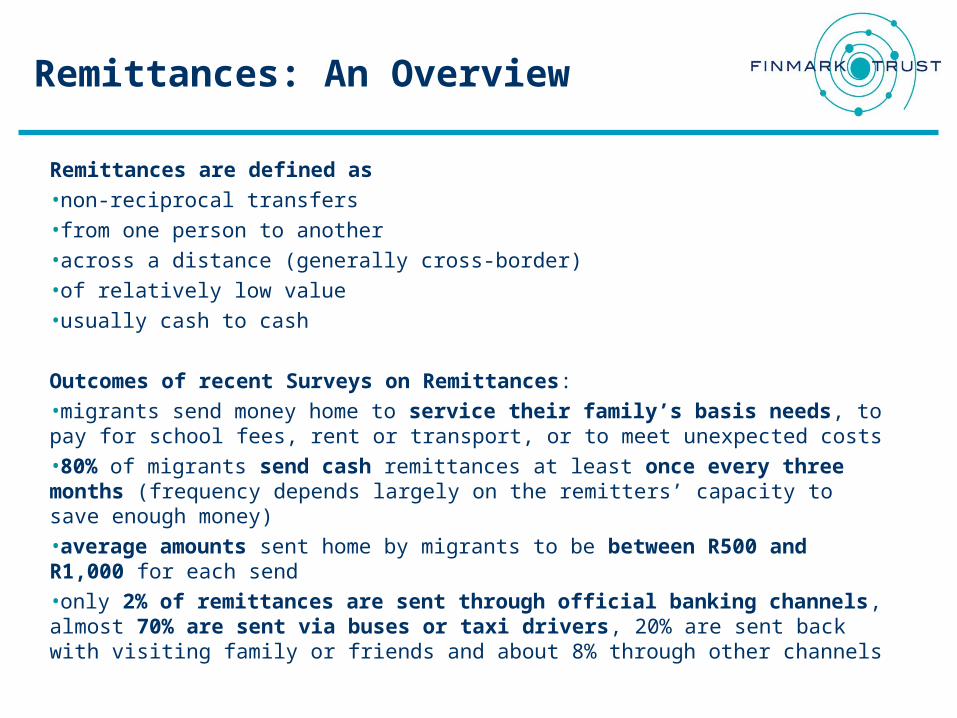

Remittances: An Overview

Remittances are defined as •non-reciprocal transfers •from one person to another •across a distance (generally cross-border) •of relatively low value •usually cash to cash

Outcomes of recent Surveys on Remittances:•migrants send money home to service their family’s basis needs, to pay for school fees, rent or transport, or to meet unexpected costs •80% of migrants send cash remittances at least once every three months (frequency depends largely on the remitters’ capacity to save enough money) •average amounts sent home by migrants to be between R500 and R1,000 for each send •only 2% of remittances are sent through official banking channels, almost 70% are sent via buses or taxi drivers, 20% are sent back with visiting family or friends and about 8% through other channels

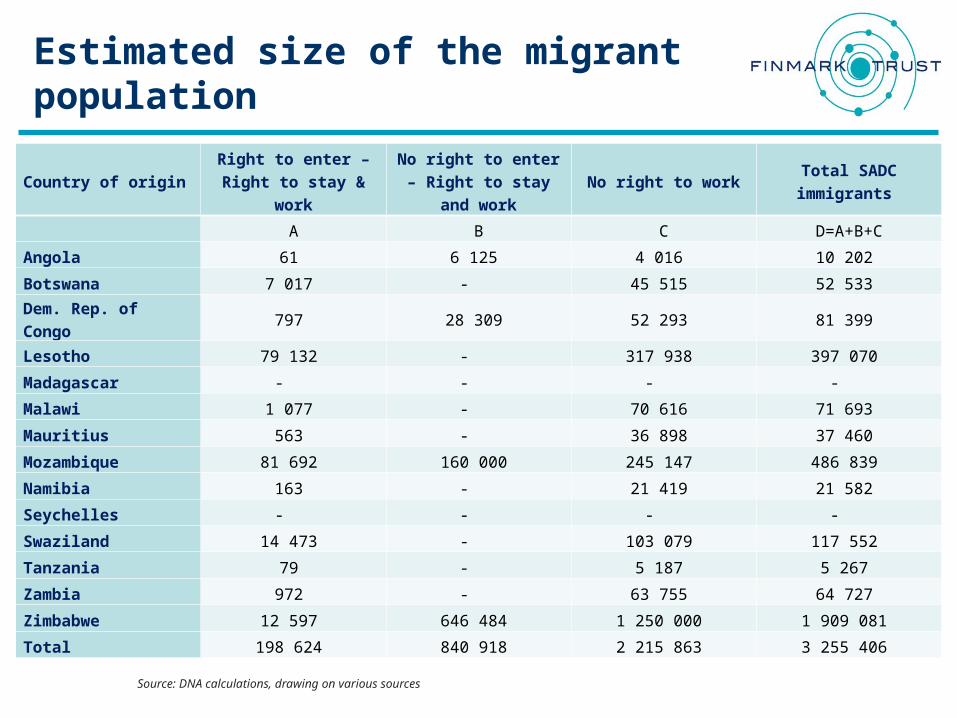

Estimated size of the migrant population

Country of originRight to enter – Right to stay &

work

No right to enter – Right to stay and

workNo right to work

Total SADC immigrants

A B C D=A+B+C

Angola 61 6 125 4 016 10 202

Botswana 7 017 - 45 515 52 533

Dem. Rep. of Congo

797 28 309 52 293 81 399

Lesotho 79 132 - 317 938 397 070

Madagascar - - - -

Malawi 1 077 - 70 616 71 693

Mauritius 563 - 36 898 37 460

Mozambique 81 692 160 000 245 147 486 839

Namibia 163 - 21 419 21 582

Seychelles - - - -

Swaziland 14 473 - 103 079 117 552

Tanzania 79 - 5 187 5 267

Zambia 972 - 63 755 64 727

Zimbabwe 12 597 646 484 1 250 000 1 909 081

Total 198 624 840 918 2 215 863 3 255 406

Source: DNA calculations, drawing on various sources

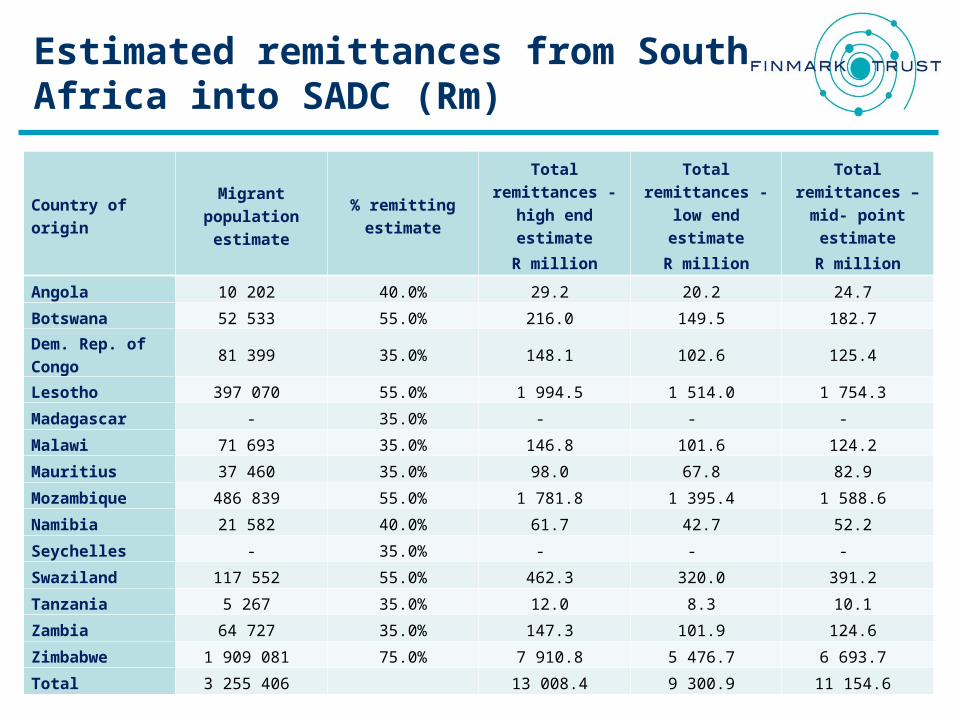

Estimated remittances from South Africa into SADC (Rm)

Country of origin

Migrant population estimate

% remitting estimate

Total remittances -

high end estimate

R million

Total remittances -

low end estimate

R million

Total remittances –

mid- point estimate

R million

Angola 10 202 40.0% 29.2 20.2 24.7

Botswana 52 533 55.0% 216.0 149.5 182.7

Dem. Rep. of Congo

81 399 35.0% 148.1 102.6 125.4

Lesotho 397 070 55.0% 1 994.5 1 514.0 1 754.3

Madagascar - 35.0% - - -

Malawi 71 693 35.0% 146.8 101.6 124.2

Mauritius 37 460 35.0% 98.0 67.8 82.9

Mozambique 486 839 55.0% 1 781.8 1 395.4 1 588.6

Namibia 21 582 40.0% 61.7 42.7 52.2

Seychelles - 35.0% - - -

Swaziland 117 552 55.0% 462.3 320.0 391.2

Tanzania 5 267 35.0% 12.0 8.3 10.1

Zambia 64 727 35.0% 147.3 101.9 124.6

Zimbabwe 1 909 081 75.0% 7 910.8 5 476.7 6 693.7

Total 3 255 406 13 008.4 9 300.9 11 154.6

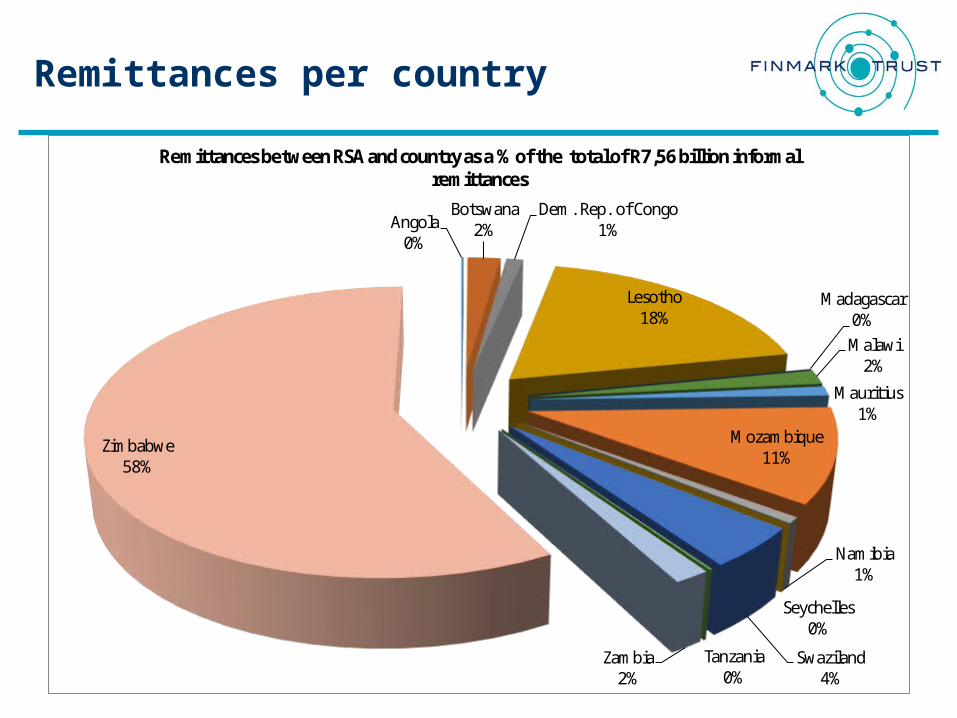

Remittances per country

Angola0%

Botswana2%

Dem. Rep. of Congo1%

Lesotho18%

Madagascar0%Malawi

2%

Mauritius1%

Mozambique11%

Namibia1%

Seychelles0%

Swaziland4%

Tanzania0%

Zambia2%

Zimbabwe58%

Remittances between RSA and country as a % of the total of R7,56 billion informal remittances

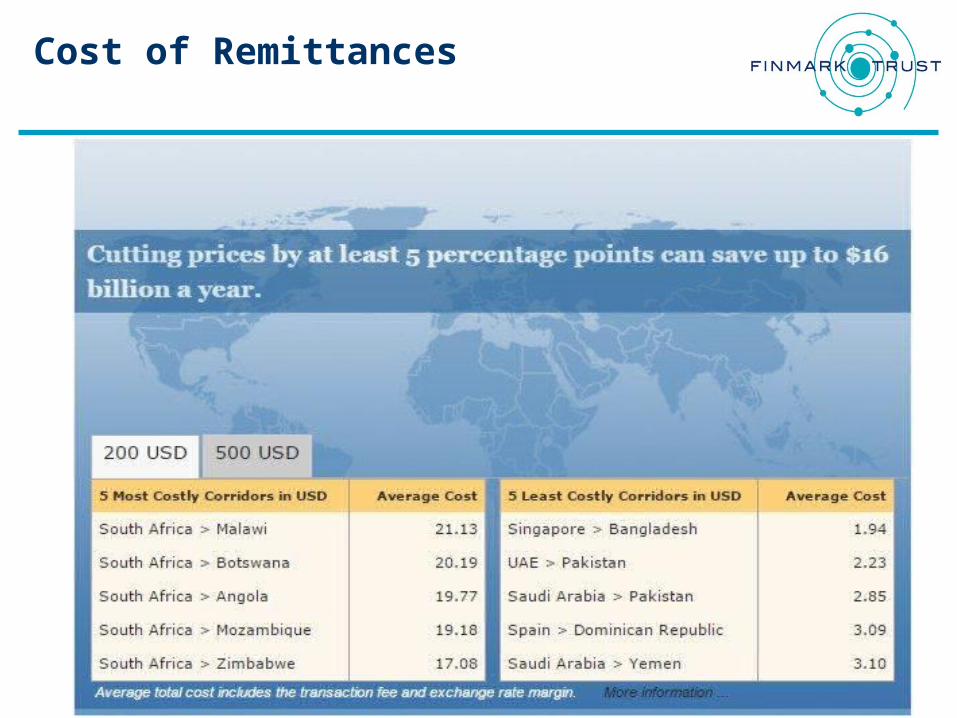

Cost of Remittances

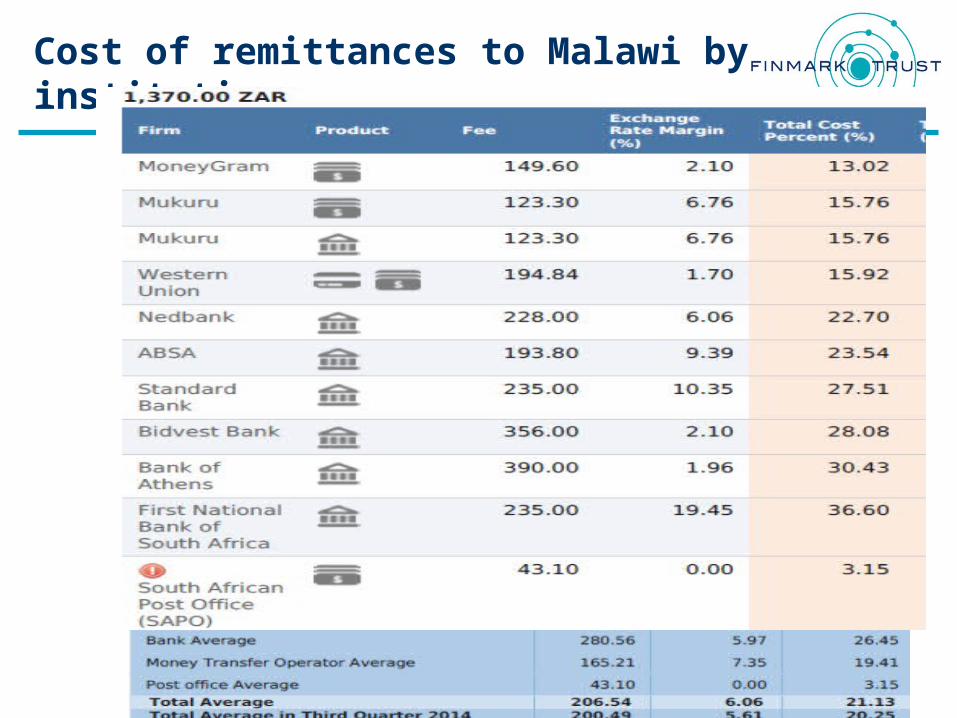

Cost of remittances to Malawi by institution

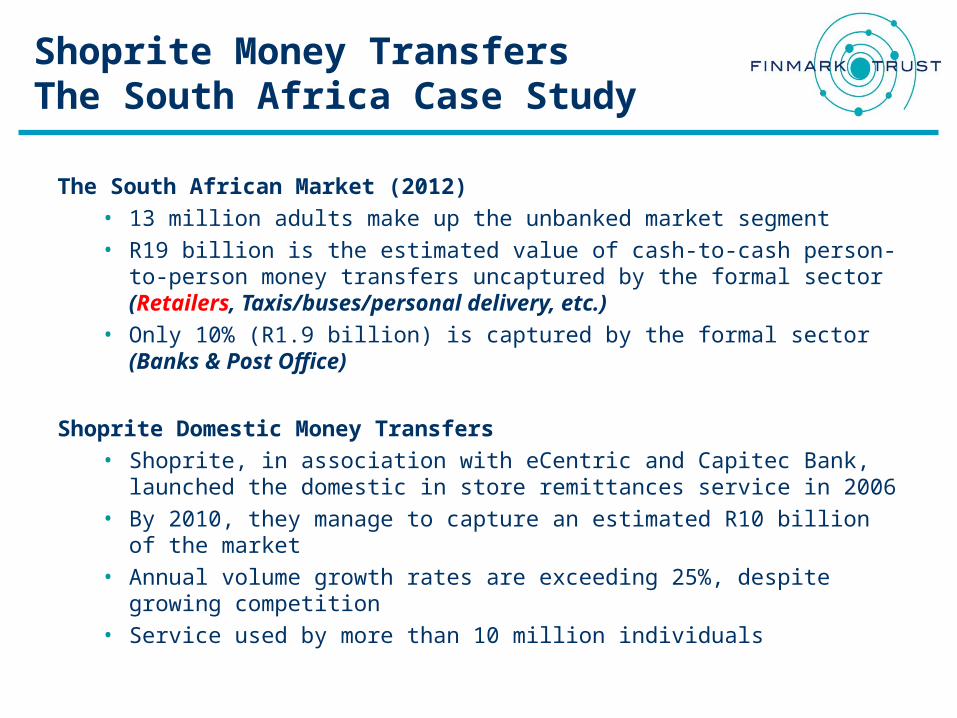

Shoprite Money Transfers The South Africa Case Study

The South African Market (2012) • 13 million adults make up the unbanked market segment • R19 billion is the estimated value of cash-to-cash person-to-

person money transfers uncaptured by the formal sector (Retailers, Taxis/buses/personal delivery, etc.)

• Only 10% (R1.9 billion) is captured by the formal sector (Banks & Post Office)

Shoprite Domestic Money Transfers • Shoprite, in association with eCentric and Capitec Bank,

launched the domestic in store remittances service in 2006 • By 2010, they manage to capture an estimated R10 billion of the

market • Annual volume growth rates are exceeding 25%, despite growing

competition • Service used by more than 10 million individuals

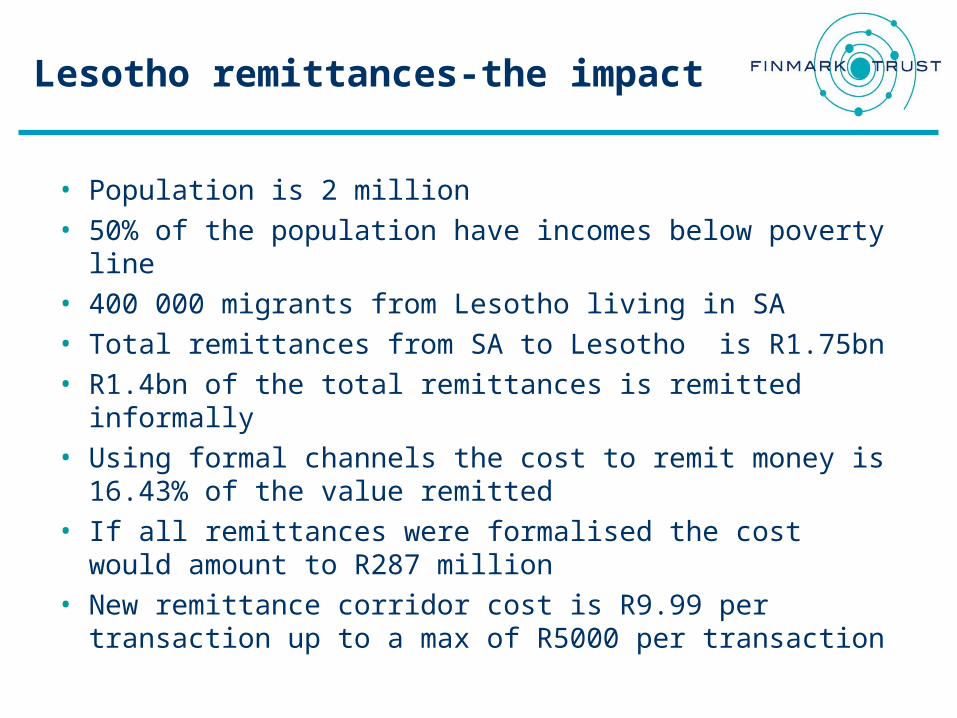

Lesotho remittances-the impact

• Population is 2 million• 50% of the population have incomes below poverty

line• 400 000 migrants from Lesotho living in SA• Total remittances from SA to Lesotho is R1.75bn• R1.4bn of the total remittances is remitted informally• Using formal channels the cost to remit money is

16.43% of the value remitted• If all remittances were formalised the cost would

amount to R287 million• New remittance corridor cost is R9.99 per transaction

up to a max of R5000 per transaction

Shoprite - Money Markets

“Money Market” service stations offer a comprehensive range of financial services and products to the Group’s customers through dedicated in-store service counters: •utility bill payments •bus and airline tickets •basic insurance policies •tickets for major sporting and cultural events •travel packages •MONEY TRANSFERS

Shoprite estimates more than 50% of its clients make use of the counter while in the store

Installed 642 new service points to meet demand

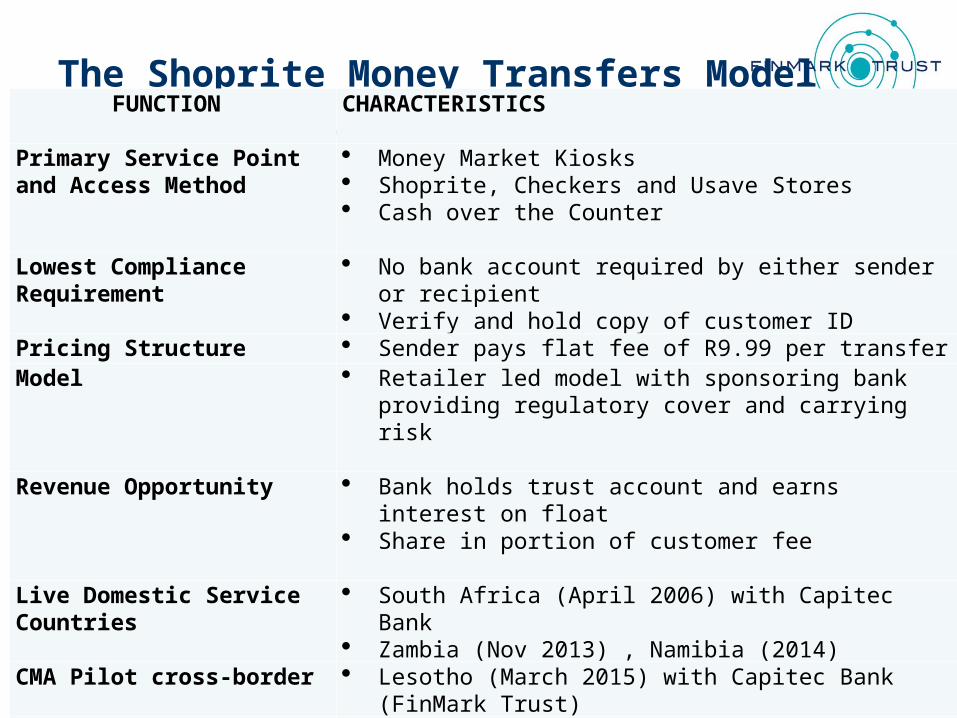

The Shoprite Money Transfers Model FUNCTION CHARACTERISTICS

Primary Service Point and Access Method

Money Market Kiosks Shoprite, Checkers and Usave Stores Cash over the Counter

Lowest Compliance Requirement

No bank account required by either sender or recipient

Verify and hold copy of customer ID Pricing Structure Sender pays flat fee of R9.99 per transfer Model Retailer led model with sponsoring bank providing

regulatory cover and carrying risk

Revenue Opportunity Bank holds trust account and earns interest on float

Share in portion of customer fee

Live Domestic Service Countries

South Africa (April 2006) with Capitec Bank Zambia (Nov 2013) , Namibia (2014)

CMA Pilot cross-border Lesotho (March 2015) with Capitec Bank (FinMark Trust)

Domestic and Cross-border under application

Swaziland, with Standard Bank and FinMark Trust

Potential Angola, Nigeria, Botswana, Ghana, Malawi, Mozambique, Nigeria, Tanzania, Uganda, Zimbabwe with Standard Bank

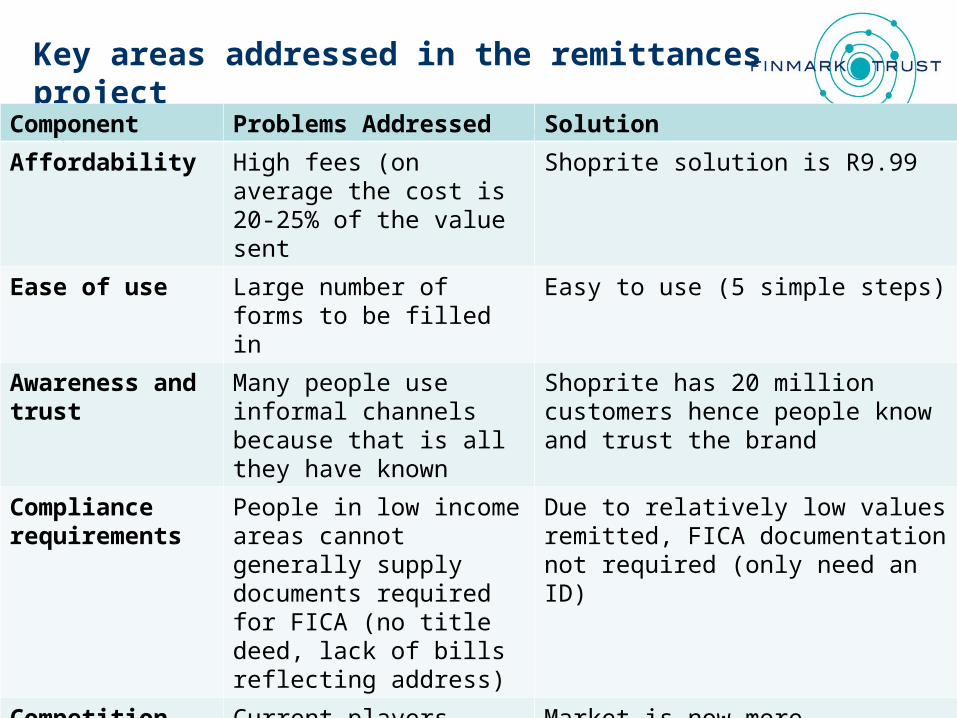

Key areas addressed in the remittances project

Component Problems Addressed Solution

Affordability High fees (on average the cost is 20-25% of the value sent

Shoprite solution is R9.99

Ease of use Large number of forms to be filled in

Easy to use (5 simple steps)

Awareness and trust

Many people use informal channels because that is all they have known

Shoprite has 20 million customers hence people know and trust the brand

Compliance requirements

People in low income areas cannot generally supply documents required for FICA (no title deed, lack of bills reflecting address)

Due to relatively low values remitted, FICA documentation not required (only need an ID)

Competition Current players monopolise the remittance space hence can almost charge what they want to.

Market is now more competitive and diversified

Financial Inclusion

Financial sector excludes the poor to a large degree

Migrant families are introduced to financial services

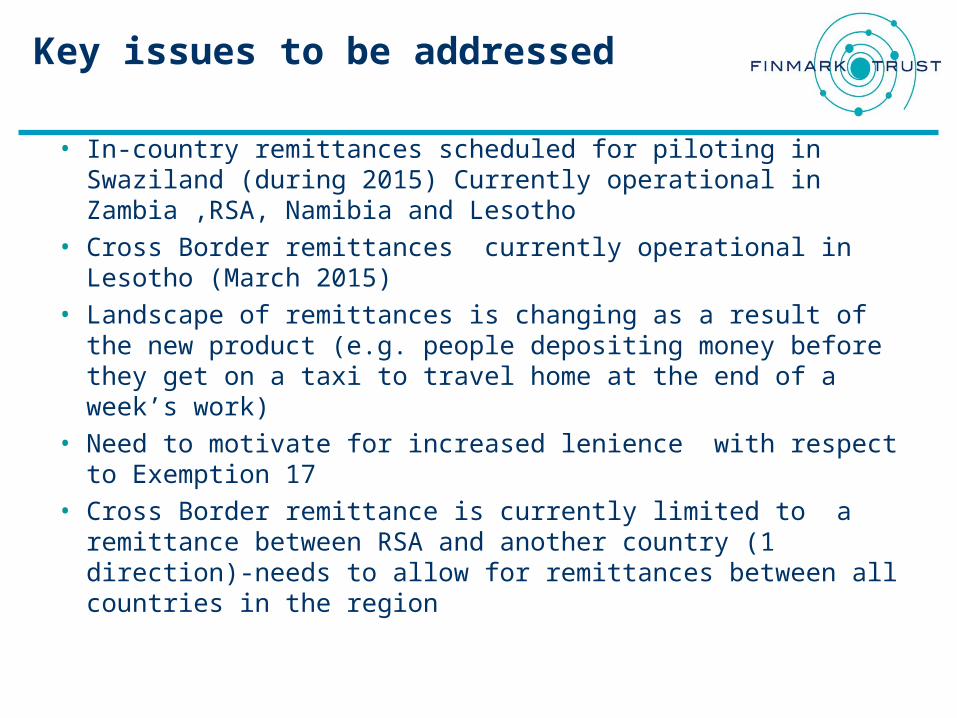

Key issues to be addressed

• In-country remittances scheduled for piloting in Swaziland (during 2015) Currently operational in Zambia ,RSA, Namibia and Lesotho

• Cross Border remittances currently operational in Lesotho (March 2015)

• Landscape of remittances is changing as a result of the new product (e.g. people depositing money before they get on a taxi to travel home at the end of a week’s work)

• Need to motivate for increased lenience with respect to Exemption 17

• Cross Border remittance is currently limited to a remittance between RSA and another country (1 direction)-needs to allow for remittances between all countries in the region

Making financial markets work for the poor

Thank you

Related Documents