Initiating Coverage FC Research Analyst: Amanda Lokugamage SRI LANKA ROYAL CERAMICS LANKA PLC STRONG BUY RCL.N0000 Sep 2016 “Glazed Performance” Current Price: LKR 120.5 Fair Value: LKR 200.0 Royal Ceramic Lanka PLC, leader in high quality surface covering and bath- ware in Sri Lanka with subsidiaries providing a diversified product portfolio. RCL’s earnings is expected to grow at a CAGR of c.13% FY16-FY19E surpassing c.LKR 4.0Bn in FY18E and c.LKR 4.3Bn in FY19E. RCL is expected to grow its earnings mainly driven by the incline in its revenue streams coupled with the efficient management of operational costs. FC Research expect RCL to provide a return of 82% at LKR 200.0. STRONG BUY Construction sector boom driven revenue: RCL’s revenue is expected to grow at a c.CAGR of 14% over FY16-19E to reach c.LKR 36.9Bn in FY18E as opposed to LKR 24.9Bn registered in FY16 on the back of the growth in the construction sector primarily driven by the increased demand for housing and residential property led by rising urbanization and the boom in the tourism industry deriving from the increase in the number of tourist arrivals result in an increased demand for tourist accommodation. Increased volumes to Improve Margins and Earnings: Economies of scale deriving from increased volumes coupled with comparatively lower commodity prices to reduce the overall cost of sales thus record it at c.LKR 20.0Bn in FY18E with a CAGR of 14% over FY16-FY18E leading to an increase in RCL earnings to c.LKR 4.3Bn (CAGR of 17% over FY16-FY18E) while improving GP, EBIT and NP margins in FY18E to 39%, 21% and 12% respectively. RCL to provide 82% return over 18-months period: FC Research expect RCL to achieve a fair value of LKR 200.0 providing a total return of 82% (Dividend yield 16%) over 18-month period. [DCF based LKR 141.2 and PER based LKR 253.1] Risks associated: Given the nature of the business model of the company RCL is exposed to the risk resulting from the fluctuations in exchange rates and the changes in the government policies. Figure 1: RCL Price Volume Graph Disclosure on Shareholding: First Capital Group and its affiliates holds 246,842 shares in RCL. Neither First Capital Group nor its affiliates have traded in the shares in the three trading days prior to this document, and will not trade in the shares for three trading days following the issue of this document. P/E 31 March FY15 FY16 FY17E FY18E FY19E Revenue (LKR Mn) 22,379 24,905 27,130 32,623 36,902 Net Profit (LKR Mn) 2,135 2,934 3,093 4,006 4,285 EPS (LKR) 19.3 26.5 27.9 36.2 38.7 YoY % Growth 132% 37% 5% 30% 7% Valuations PER (X) 6.3 4.5 4.3 3.3 3.1 PBV (X) 1.1 0.9 0.8 0.7 0.6 Dividend Yield (%) 4.1% 6.6% 7.0% 9.0% 9.6% NAVPS 107.2 132.1 151.6 176.9 204.0 DPS (LKR) 5.0 8.0 8.4 10.8 11.6 Payout Ratio 26% 30% 30% 30% 30% KEY DATA Share Price (LKR) Average Daily Volume (Shares) 42,792 Average Daily Turnover 4,907,740 110.8 13,350 Price Performance (%) 1 mth 3 mths 12mths RCL -2.6% 4.2% -0.8% ASPI -2.5% 2.3% -9.3% 51.0% 13.8% 3.2% 2.5% 1.8% Market Capitalisation (LKR mn) 120.50 52w High/Low (LKR) 97.0/125.0 Issued Share Capital (Shares mn) Public Holdings 47.5% Major Shareholders as at 30th June 2016 Vallibel One PLC Employee Provident Fund HSBC Intl Nom Ltd - BBH- Grandeur Peak Emerging Mkts Sri Lanka Insurance Corporation Ltd - General Fund Employee Trust Fund Board

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Initiating Coverage

FC Research Analyst: Amanda Lokugamage

SRI LANKA

ROYAL CERAMICS LANKA PLC STRONG BUY

RCL.N0000 Sep 2016

“Glazed Performance”

Current Price: LKR 120.5 Fair Value: LKR 200.0

Royal Ceramic Lanka PLC, leader in high quality surface covering and bath-

ware in Sri Lanka with subsidiaries providing a diversified product portfolio.

RCL’s earnings is expected to grow at a CAGR of c.13% FY16-FY19E surpassing

c.LKR 4.0Bn in FY18E and c.LKR 4.3Bn in FY19E. RCL is expected to grow its

earnings mainly driven by the incline in its revenue streams coupled with the

efficient management of operational costs. FC Research expect RCL to provide

a return of 82% at LKR 200.0. STRONG BUY

Construction sector boom driven revenue: RCL’s revenue is expected to grow

at a c.CAGR of 14% over FY16-19E to reach c.LKR 36.9Bn in FY18E as opposed to

LKR 24.9Bn registered in FY16 on the back of the growth in the construction

sector primarily driven by the increased demand for housing and residential

property led by rising urbanization and the boom in the tourism industry

deriving from the increase in the number of tourist arrivals result in an increased

demand for tourist accommodation.

Increased volumes to Improve Margins and Earnings: Economies of scale

deriving from increased volumes coupled with comparatively lower commodity

prices to reduce the overall cost of sales thus record it at c.LKR 20.0Bn in FY18E

with a CAGR of 14% over FY16-FY18E leading to an increase in RCL earnings to

c.LKR 4.3Bn (CAGR of 17% over FY16-FY18E) while improving GP, EBIT and NP

margins in FY18E to 39%, 21% and 12% respectively.

RCL to provide 82% return over 18-months period: FC Research expect RCL to

achieve a fair value of LKR 200.0 providing a total return of 82% (Dividend yield

16%) over 18-month period. [DCF based LKR 141.2 and PER based LKR 253.1]

Risks associated: Given the nature of the business model of the company RCL

is exposed to the risk resulting from the fluctuations in exchange rates and the

changes in the government policies.

Figure 1: RCL Price Volume Graph

Disclosure on Shareholding:

First Capital Group and its affiliates holds 246,842

shares in RCL. Neither First Capital Group nor its

affiliates have traded in the shares in the three

trading days prior to this document, and will not

trade in the shares for three trading days following

the issue of this document.

P/E 31 March FY15 FY16 FY17E FY18E FY19E

Revenue (LKR Mn) 22,379 24,905 27,130 32,623 36,902

Net Profit (LKR Mn) 2,135 2,934 3,093 4,006 4,285

EPS (LKR) 19.3 26.5 27.9 36.2 38.7

YoY % Growth 132% 37% 5% 30% 7%

Valuations

PER (X) 6.3 4.5 4.3 3.3 3.1

PBV (X) 1.1 0.9 0.8 0.7 0.6

Dividend Yield (%) 4.1% 6.6% 7.0% 9.0% 9.6%

NAVPS 107.2 132.1 151.6 176.9 204.0

DPS (LKR) 5.0 8.0 8.4 10.8 11.6

Payout Ratio 26% 30% 30% 30% 30%

KEY DATA

Share Price (LKR)

Average Daily Volume (Shares) 42,792

Average Daily Turnover 4,907,740

110.8

13,350

Price Performance (%) 1 mth 3 mths 12mths

RCL -2.6% 4.2% -0.8%

ASPI -2.5% 2.3% -9.3%

51.0%

13.8%

3.2%

2.5%

1.8%

Market Capitalisation (LKR mn)

120.50

52w High/Low (LKR) 97.0/125.0

Issued Share Capital (Shares mn)

Public Holdings 47.5%

Major Shareholders as at 30th June 2016

Vallibel One PLC

Employee Provident Fund

HSBC Intl Nom Ltd - BBH- Grandeur Peak Emerging Mkts

Sri Lanka Insurance Corporation Ltd - General Fund

Employee Trust Fund Board

FC Research

2

“Glazed Performance”

1.1 Introduction

Monopoly power of the tile sector: RCL, established in 1990, engages in manufacturing and sale of floor tiles, wall tiles and other ceramic products while having diversified into financial services and plantations. Through a series of acquisitions, the company presently holds the monopoly position in the tile sector, controlling c.60%-70% of the tile market. Operational and segmental review: RCL markets its tiles at a premium price under the brand name “Rocell” through a network of over 50 showrooms and 450 dealers island wide. The ISO 9001:2008 certified company operates two factories in Horana and Eheliyagoda, with capacities of 11,000 and 6,000 square meters of tiles per day respectively. In FY16 company generated 6% of its revenue from exports to Europe, North America, Australia and several parts of Asia. Royal ceramics employs c.10,000 employees and has a market capitalization of LKR 14Bn. SWOT analysis:

Strengths Monopoly power Brand equity

Opportunities Boost in the construction sector Better technology

Weaknesses Heavily concentrated on tile

and construction sector related products

Threats Possible delays in government

lead construction drive Competition from imports

RCL’s price has moved in line with ASPI. The downward trend in the share price during Sep 2015 – Mar 2016 reflects the overall slowdown in the market owing to the investors’ wait-and-see approach prior to the important government policies are accounted. Post Mar 2016, along with the recommencing of the major construction projects, the share has started to gain ground which we expect to continue.

4,500

5,000

5,500

6,000

6,500

7,000

7,500

80

90

100

110

120

130

140

150

160

RCL (LHS) ASPI (RHS)

67%

9%

6%

10%

7% 1%

Tiles and associated products Aluminium Products

Sanitaryware Packaging Material

Plantation Paints and other

Figure 2: Revenue sources of RCL

Source: Company Annual Reports

Figure 3: ASPI vs RCL

FC Research

3

“Glazed Performance”

1.3 Tile sector overview

Tile sector: Sri Lanka provides evidence for richly crafted ceramics dating back several centuries. The country is gifted with natural mineral deposits such as kaolin, ball clay, feldspar, silica quartz and dolomite which is a major factor strengthening the local manufacturing of tiles. Skilled workforce is abundant at a competitive labor cost. The locally manufactured tiles are reputed for its superior quality and is sold at a premium price, catering the upper end of the market. Tiles (floor tiles and wall tiles) are featured in several varieties such as glazed vs. unglazed and ceramic vs. porcelain. Import and export performance: The locally manufactured tiles account for c.60%-70% while imported tiles comprise c.30%-40% of the market. The imported tiles are primarily coming from India and China and is subject to CESS and other import taxes. Sri Lanka exports its locally manufactured tiles to United States, Australia, Canada, Japan, UK and several other European countries.

Monopoly lead by Royal Ceramics: The local tile manufacturing is dominated by the cluster of companies lead by Royal ceramics (Figure 2). They have the majority of market share in both wall tiles as well as floor tiles (Figure 4).

100

300

500

700

900

1,100

1,300

2011 2012 2013 2014 2015

LKR

-M

n

Source: Royal Ceramics Annual Report Note: Non-ceramic businesses are excluded

Figure 6: Monopoly lead by RCL

Figure 4: Manufactured Vs. imported

Locally manufactured Imported

60% - 70%

30% - 40%

Figure 5: Export performance

Source: Central Bank of Sri Lanka

Royal Ceramics PLC (RCL.N0000)

Lanka Ceramic PLC (CERA) (77%)

Lanka Walltiles PLC (LWL)

(62%)

Lanka Tiles PLC (TILE)

(68%)

Royal Porcelain (Pvt) Ltd) (100%)

Rocell Bathware Ltd (61%)

Rocell (Pty) Ltd (100%)

Swissteck Ceylon PLC (PARQ)

Source: Company Annual Report, FC Research Estimates

FC Research

4

“Glazed Performance”

Major tile manufacturers in the consortium other than RCL

Lanka Walltiles PLC (LWL): LWL is a subsidiary of RCL and produces wall tiles for more economic users. LWL has a production capacity of c.2.3Mn square meters per annum. The ISO 13006 certified company employs c.500 employees and has a market capitalization of LKR 6Bn.

Lanka Tiles PLC (TILE.N0000): TILE caters the floor tile segment and has a capacity of c.3Mn square meters of tile per annum. TILE employs c.500 employees and has a market capitalization of LKR 6Bn.

63%56%

37%44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RCL Group Other

Figure 7: Market shares in wall tiles and floor tiles

40%

23%

Source: Company Annual Report

-

1,000

2,000

3,000

4,000

5,000

6,000

Revenue Net profit

Figure 8: Company revenues and profits

Source: Company Annual Reports

FC Research

5

“Glazed Performance”

2.0 Construction sector boom driven revenue

A

Revenue to grow by 20%: RCL’s revenue is expected to grow at a CAGR of

c.14% over FY16-19E to reach c.LKR 36.9Bn in FY19E on the back of increased

demand resultant to the boom witness in the construction sector. Tiles and

associated products coupled with sanitary-ware is expected to generate

c.LKR 20.3Bn to contribute c.75% while Aluminium products segment is

expected to generate c.LKR 2.7Bn contributing c.10% of RCL’s total revenue

in FY17E primarily driven by the increased volumes created by the improved

demand.

2.1 Construction sector boom driven volume

All segments to boost demand: A boom in all segments of the construction

sector namely government led mega infrastructure development projects,

sky scrapers, mega hotel and tourism accommodation projects, residential

property and condominium apartment projects, integrated projects, etc.

coupled with the boom in the real estate segment have collectively

contributed to the increase in demand for building materials (e.g.: cement,

cables, floor tiles, wall tiles, sanitary-ware and aluminium products, etc…)

which in turn result in an increase in volumes for RCL which has a diversified

product portfolio through its subsidiary/ associate companies consisting of

floor tiles, wall tiles, sanitary-ware and aluminium products.

GDP growth supported by Construction: Country’s GDP registered a YoY

growth of 4.5% and 4.8% in 2014 and 2015 respectively while the same is

expected to record a growth of c. 5.5% and c. 6.3% in 2016E and 2017E

respectively where the contribution from construction sector was recorded

at 7.5% and 7.4% in 2014 and 2015 primarily driven by the government’s

heavy investment into mega infrastructure development projects. Currently

Figure 9: Revenue Growth

Figure 10: Construction as a % of GDP

0%

5%

10%

15%

20%

25%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Re

ven

ue

Gro

wth

(Yo

Y)R

eve

nu

e -

LKR

(M

n)

Revenue Growth (YoY)

Source: Company Annual Reports and FC Research Estimates

FC Research

6

“Glazed Performance”

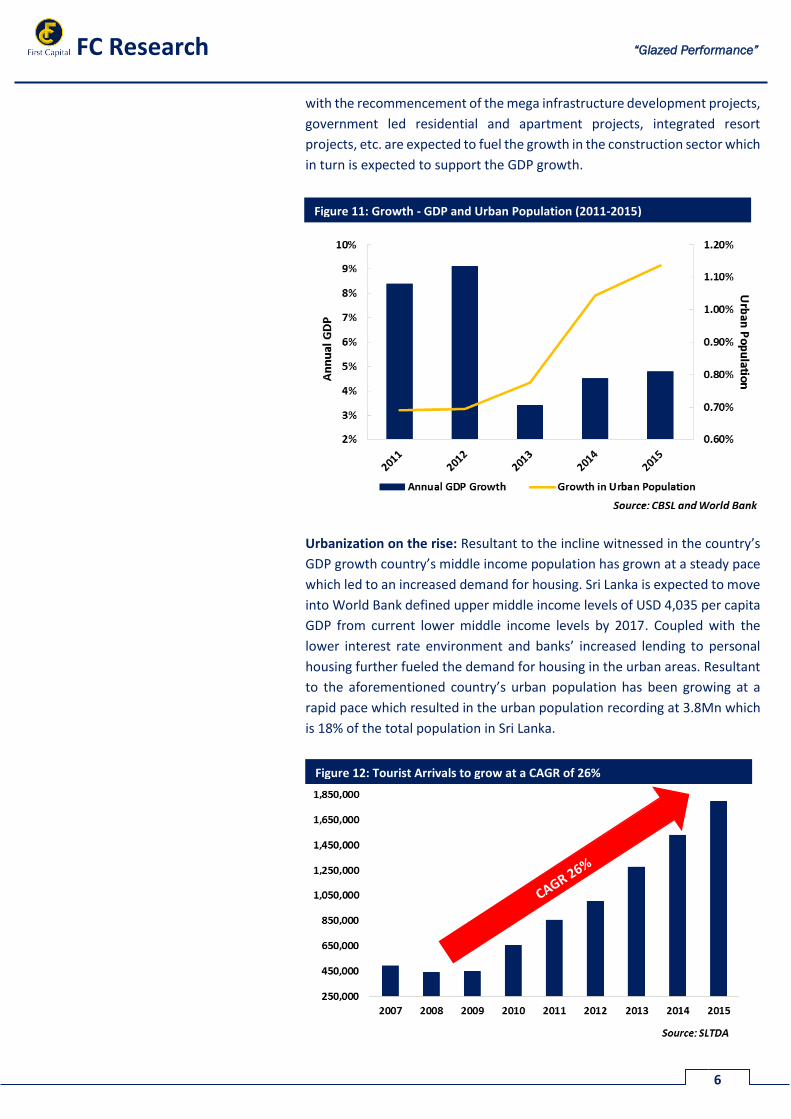

with the recommencement of the mega infrastructure development projects,

government led residential and apartment projects, integrated resort

projects, etc. are expected to fuel the growth in the construction sector which

in turn is expected to support the GDP growth.

Urbanization on the rise: Resultant to the incline witnessed in the country’s

GDP growth country’s middle income population has grown at a steady pace

which led to an increased demand for housing. Sri Lanka is expected to move

into World Bank defined upper middle income levels of USD 4,035 per capita

GDP from current lower middle income levels by 2017. Coupled with the

lower interest rate environment and banks’ increased lending to personal

housing further fueled the demand for housing in the urban areas. Resultant

to the aforementioned country’s urban population has been growing at a

rapid pace which resulted in the urban population recording at 3.8Mn which

is 18% of the total population in Sri Lanka.

Figure 11: Growth - GDP and Urban Population (2011-2015)

Figure 12: Tourist Arrivals to grow at a CAGR of 26%

FC Research

7

“Glazed Performance”

Growth in Tourism led accommodation: Since the eradication of war in 2009

Sri Lanka’s tourist arrivals have been growing at an accelerated rate to reach

1.8Mn by end 2015 with a YoY growth of 18% (1.5Mn in 2014) at a CAGR of

26% from 2009-15. Tourist arrivals are expected to reach 2.2Mn by end 2016

with a YoY growth of 22%. To accommodate the increased number of tourists

an estimated 50,000 rooms are required which is more than twice the current

capacity thus country witness more investments going into tourism led

construction specially in the informal segment which creates more demand

for tiles and associated products, sanitary-ware, aluminium product and

paints and allied products. Revenue from tile and associated products and

sanitary-ware is expected to register a YoY growth of 9% to reach c.LKR 20.2

while c.LKR aluminium products was recorded at LKR 2.2Mn accounting for

9% of the total RCL revenue of LKR 24.9Bn in FY16. Revenue from Aluminum

products is expected to grow at a CAGR of c.21% over FY16-19E to reach c.LKR

3.8Bn in FY19E.

Products to cater every segment: RCL group has a wide array of products

consisting of premium quality products marketed under Rocell brand and

more affordable surface covering (e.g. Wall tiles, floor tiles, etc.) and sanitary-

ware manufactured and marketed by Lanka Ceramic PLC, Lanka Walltiles PLC

and Lanka Tiles PLC, etc. RCL is well positioned itself to cater the different

income segments of the population through its wide array of product

portfolio. Swisstek Aluminium Limited is in the view of introducing aluminium

proprietary system for high rise and commercial buildings.

2.2 Increase Demand met by Enhanced Capacity:

During the FY16 in-line with its strategic expansion plan RCL invested LKR

1.9Bn on purchasing, upgrading plant and machinery, revamping showroom

network and adopting new technology in several of its subsidiary and

associate companies with the view of enabling to cater to the increase in

demand. LKR 189Mn was invested in Lanka Walltiles PLC to enhanced

manufacture capabilities, LKR 205Mn was invested in Swisstek Aluminium

Limited to increase capacity to 450MT per month from previous 300MT per

month with the aim of increasing the capacity by additional 500MT per

month.

FC Research

8

“Glazed Performance”

3.0 Increased volumes to Improve Margins and Earnings

RCL’s Earnings to improve: Economies of scale deriving from increased

volumes coupled with comparatively lower commodity prices to reduce the

overall cost of sales thus recording it at c.LKR 20.0Bn in FY18E with a CAGR of

14% over FY16-FY18E thus increasing RCL earnings to c.LKR 4.3Bn (CAGR of

17% over FY16-FY18E) while improving GP, EBIT and NP margins in FY18E to

39%, 21% and 12% respectively.

3.1 Economies of Scale through increased volumes: Adhering to the

strategic expansion plan RCL’s investment of LKR 1.9Bn during FY16 resulted

in increased capacity of RCL and its subsidiary and associate companies

which is expected to increase overall manufacture volumes enabling the

company to enjoy economies of scale leading to a reduction in cost of sales

to c.LKR 20.0Bn in FY18E with a CAGR of c. 10% over FY15-FY18E in

comparison to revenue of c.LKR 32.6Bn recorded in FY18E (CAGR of 13%

over FY15-FY18E) is expected to improve the bottom line while widening the

margins.

3.2 Access to raw material at lower cost: Basic raw materials used in RCL to

form the body of the tiles are Feldspar, Ball clay, Dolomite and Silica sand.

Most of these materials are used in their raw state, as mined. These

materials are generally homogenized to ensure consistency in composition.

RCL has invested in mining lands to ensure the access of raw material at

lower costs. RCL’s subsidiary Lanka Ceramics PLC is primarily focused onto

mining and processing of raw material for tiling and ceramic industry. During

FY16 company’s accumulated production was recorded at 68,000MT of raw

clay as the country’s largest supplier.

Further, company has secured steady supply of clay by investing in two

mining lands in Owala and Meetiyagoda for 7 years and 5 years respectively

while entering into an operating lease agreement with ball clay land owners

in Dediyawala.

Figure 13: Revenue, GP, EBIT and NP Margins (FY14-FY19E)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

12,000

17,000

22,000

27,000

32,000

37,000

42,000

Revenue GP Margin EBIT Margin NP Margin

Source: Company Annual Reports and FC Research Estimates

Re

ven

ue

-LK

R (

Mn

)

Margin

s

FC Research

9

“Glazed Performance”

3.3 Better cost management strategies: RCL group in a bid to improve

accessibility to its products appointed new franchise dealers, upgrading

existing showrooms, revamping dealer network and strengthening its global

presence by opening 4 showrooms in Australia with the aim to expand into

Pakistan and Maldives. Company introduced lean management systems

along with investment into upgrading machinery resulted in cost savings of

LKR 12.0Mn during 4QFY16. Further, LKR 45Mn was invested in expansion

and LKR 12.0Mn was invested in a firewood boiler which is expected to bring

down the energy cost in Uni Dil Packaging Limited while company continued

to invest in the diversification of its plantation sector.

FC Research

10

“Glazed Performance”

4.0 RCL to provide 82% return

RCL Earnings CAGR of 13% FY16-18E: We expect a fair value of LKR 200.0

based on RCL’s earnings of c.LKR 4.3Bn in FY19E (CAGR of 13% over FY16-

19E). In FY18E RCL is expected to reach a net profit of LKR 4.0Bn, growing by

a CAGR of c.17% over FY16-18E. At the current price forward PER is expected

to be 7.0x by FY17E and FY18E.

4.1 RCL Total Return of 82%

Fair Value of LKR 200.0: Based on the company’s value as at March 2018 FC

Research expects a fair value of LKR 200.0 for RCL providing a total return of

82% at current price levels of LKR 120.5. The RCL target price of LKR 200.0 is

based on the average price of LKR 141.2 via DCF valuations and LKR 253.1 via

PER based. On an annualized basis RCL is expected to provide a return of 49%

with a fair value of LKR 200.0 at current price level of LKR 120.5.

Figure 14: Earnings to grow at a CAGR of 14% over FY16-FY19E

P/E 31 March FY15 FY16 FY17E FY18E FY19E

Revenue (LKR Mn) 22,379 24,905 27,130 32,623 36,902

Net Profit (LKR Mn) 2,135 2,934 3,093 4,006 4,285

EPS (LKR) 19.3 26.5 27.9 36.2 38.7

YoY % Growth 132% 37% 5% 30% 7%

Valuations

PER (X) 6.3 4.5 4.3 3.3 3.1

PBV (X) 1.1 0.9 0.8 0.7 0.6

Dividend Yield (%) 4.1% 6.6% 7.0% 9.0% 9.6%

NAVPS 107.2 132.1 151.6 176.9 204.0

DPS (LKR) 5.0 8.0 8.4 10.8 11.6

Payout Ratio 26% 30% 30% 30% 30%

15,000

20,000

25,000

30,000

35,000

40,000

FY16 FY17E FY18E FY19E

FY16 FY17E FY18E FY19E

Source: Company Annual Reports and FC Research Estimates

FC Research

11

“Glazed Performance”

FY17E: For FY17E we expect a fair value of LKR 170.0 for RCL based on average

price of LKR 154.3 via DCF valuations and LKR 195.4 via PER based valuations

providing a total return of 48% (capital gain 41% and dividend yield 7%) at

current market price of LKR 120.5.

Dividend Yield of 16%: FC Research expects a DPS of LKR 19.2 for FY18E

resulting in a dividend yield of 16% over a period of 18 months for RCL.

4.2 Discounted Cash flow Valuation

Expeceted RCL Price FY17E FY18E

DCF Valuations based Target Price 154.3 141.2

PER based Target Price 195.4 253.1

Average Target Price 174.8 197.2

Target Price (Rounded Up) 170.0 200.0

RCL

Return FY17E FY18E

Target Price 170.0 200.0

Current Price 120.5 120.5

Capital Gain (LKR) 49.5 79.5

Dividend(LKR) 8.4 19.2

Capital Gain % 41% 66%

Dividend Yield % 7% 16%

Total Return % 48% 82%

Annualised Return % 48% 49%

COE (Ke)

Rf 11%

Rm 18%

β 1.07

Ke=Rf m-Rf) 18%

Valuations FY17E FY18E

Enterprise Value 25,423 23,530

Debt (-) 10,522 10,464

Cash (+) 2,189 2,580

Total Value of Equity 17,090 15,647

No. of Shares 111 111

Value of Equity per Share 154 141

WACC

Ke 18%

Kd (1-t) 9%

D/E Assumption 40 /60

Terminal Growth (% ) 3%

WACC 14%

FY17E

154 12% 13% 14% 15% 16%

1% 127.4 127.4 127.4 127.4 127.4

2% 139.7 139.7 139.7 139.7 139.7

3% 154.3 154.3 154.3 154.3 154.3

4% 171.5 171.5 171.5 171.5 171.5

5% 192.5 192.5 192.5 192.5 192.5

WACC

Terminal

Growth

(%)

FY18E

141 12% 13% 14% 15% 16%

1% 114.4 114.4 114.4 114.4 114.4

2% 126.7 126.7 126.7 126.7 126.7

3% 141.2 141.2 141.2 141.2 141.2

4% 158.5 158.5 158.5 158.5 158.5

5% 179.4 179.4 179.4 179.4 179.4

WACC

Terminal

Growth

(%)

FC Research

12

“Glazed Performance”

4.3 Average PER of 7.0x

RCL price has been trading between 3.0x – 9.0x bands during the last 24

months. We expect RCL to trade at a PER of 7.0x on FY17E earnings. By FY17E

RCL’s EPS is expected to reach LKR 36.2. At 7.0x earnings, the price for RCL

stands at LKR 253.1.

5.0 Investment Risks

Change in Government Policy: At the 2016 Budget proposal government’s

decision the downwards revision of the import related duties on several

items including tiles and sanitary-ware will have an adverse impact on RCL’s

subsidiaries; Lanka Walltiles PLC and Lanka Tiles PLC. On the same budget

proposal Government’s decision to remove the tile and sanitary-ware sector

from BOI negative list will result in industry’s protected status being removed

exposing RCL to the threat of new players entering the market.

Exchange Rate Risk: RCL’s contribution from exports was recorded at 5% of

gross revenue with LKR 1.5Bn in FY16. Fluctuations in the USD exchange rate

would have an impact on the revenue as company exports to Australia while

securing dealerships in four continents with the view of entering Pakistan and

Maldives markets by opening stores. Fluctuation in Euro exchange rate is

likely to impact the cost of sales given RCL imports raw material from Europe.

Figure 15: PE Band Graph PER based Valuation FY17E FY18E

Earnings (LKR 'Mn) 3,093 4,006

No. of Shares ('Mn) 111 111

EPS 27.9 36.2

Expected Average PER 7.0 7.0

Price at 7.0x Earnings 195.4 253.1

FC Research

13

“Glazed Performance”

Appendix 1 – Recommendation Criteria

*1 Year T Bill rate as of 14-09-2016 - 10.39%

Appendix 2 – Income Statement

Categorization Company Category

Strong Buy Buy Hold Sell

Grade A S&P SL20 Companies

T.Bill + 10% & Above

T.Bill + 5% & Above

T.Bill + 1% & Above

Below T.Bill + 1%

Grade B Rest of the Companies

T.Bill + 13% & Above

T.Bill + 8% & Above

T.Bill + 3% & Above

Below T.Bill + 3%

Grade C Companies less than LKR 1Bn Market Cap

T.Bill + 16% & Above

T.Bill + 11% & Above

T.Bill + 6% & Above

Below T.Bill + 6%

Profit & Loss Statement

P/E 31 March FY15 FY16 FY17E FY18E FY19E

Revenue 22,379 24,905 27,130 32,623 36,902

Cost of sales (15,071) (15,348) (16,921) (19,985) (23,417)

Gross profit 7,308 9,557 10,209 12,638 13,485

Other income 236 191 125 151 170

Distribution cost (2,443) (3,243) (3,527) (4,078) (4,428)

Administrative expenses (1,319) (1,399) (1,523) (1,899) (2,225)

EBIT 3,782 5,106 5,285 6,813 7,003

Finance income 2 69 78 74 60

Finance cost (971) (823) (915) (860) (703)

Share of Associate company's Profits 831 1,356 1,518 1,701 1,905

Profit before tax 3,644 5,708 5,967 7,728 8,265

Income tax expense (577) (1,616) (1,671) (2,164) (2,314)

Profit for the period 3,067 4,092 4,296 5,564 5,951

Non controlling interest 932 1,157 1,203 1,558 1,666

Equityholders of Royal Ceramic Lanka PLC 2,135 2,934 3,093 4,006 4,285

EPS 19.3 26.5 27.9 36.2 38.7

Source: Company Annual Reports and FC Research Estimates

FC Research

14

“Glazed Performance”

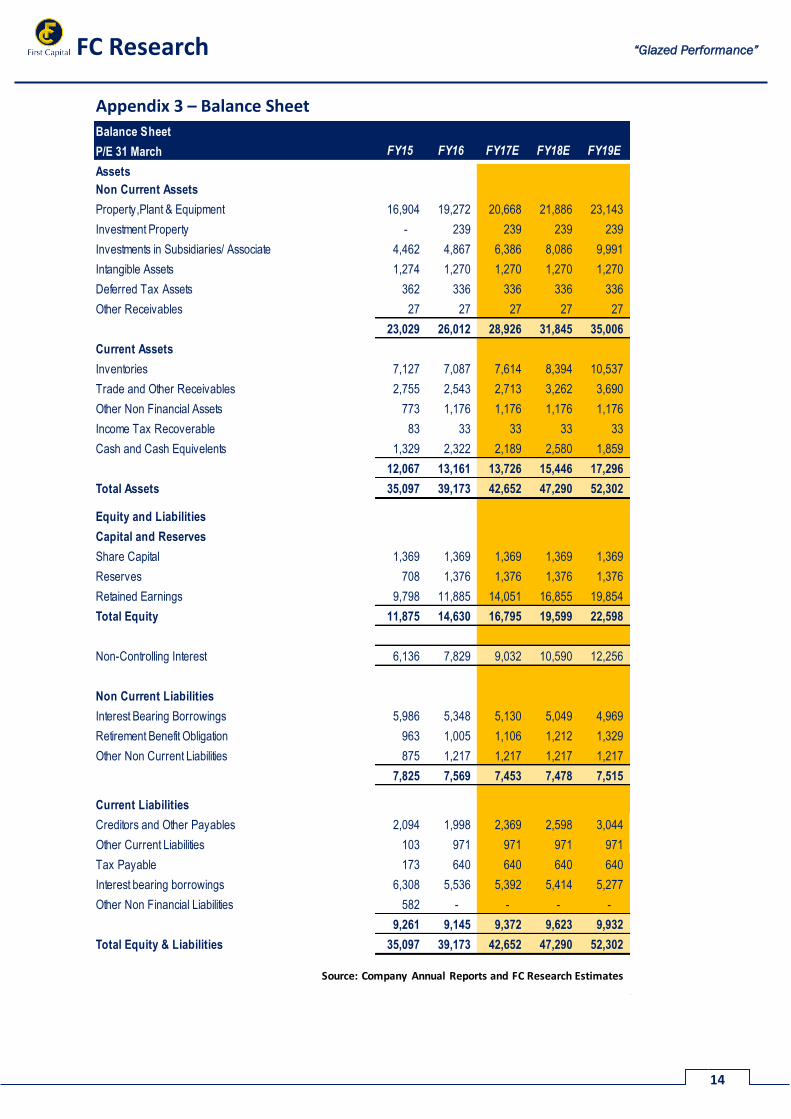

Appendix 3 – Balance Sheet

Balance Sheet

P/E 31 March FY15 FY16 FY17E FY18E FY19E

Assets

Non Current Assets

Property,Plant & Equipment 16,904 19,272 20,668 21,886 23,143

Investment Property - 239 239 239 239

Investments in Subsidiaries/ Associate 4,462 4,867 6,386 8,086 9,991

Intangible Assets 1,274 1,270 1,270 1,270 1,270

Deferred Tax Assets 362 336 336 336 336

Other Receivables 27 27 27 27 27

23,029 26,012 28,926 31,845 35,006

Current Assets

Inventories 7,127 7,087 7,614 8,394 10,537

Trade and Other Receivables 2,755 2,543 2,713 3,262 3,690

Other Non Financial Assets 773 1,176 1,176 1,176 1,176

Income Tax Recoverable 83 33 33 33 33

Cash and Cash Equivelents 1,329 2,322 2,189 2,580 1,859

12,067 13,161 13,726 15,446 17,296

Total Assets 35,097 39,173 42,652 47,290 52,302

Equity and Liabilities

Capital and Reserves

Share Capital 1,369 1,369 1,369 1,369 1,369

Reserves 708 1,376 1,376 1,376 1,376

Retained Earnings 9,798 11,885 14,051 16,855 19,854

Total Equity 11,875 14,630 16,795 19,599 22,598

Non-Controlling Interest 6,136 7,829 9,032 10,590 12,256

Non Current Liabilities

Interest Bearing Borrowings 5,986 5,348 5,130 5,049 4,969

Retirement Benefit Obligation 963 1,005 1,106 1,212 1,329

Other Non Current Liabilities 875 1,217 1,217 1,217 1,217

7,825 7,569 7,453 7,478 7,515

Current Liabilities

Creditors and Other Payables 2,094 1,998 2,369 2,598 3,044

Other Current Liabilities 103 971 971 971 971

Tax Payable 173 640 640 640 640

Interest bearing borrowings 6,308 5,536 5,392 5,414 5,277

Other Non Financial Liabilities 582 - - - -

9,261 9,145 9,372 9,623 9,932

Total Equity & Liabilities 35,097 39,173 42,652 47,290 52,302

Source: Company Annual Reports and FC Research Estimates

FC Research

15

“Glazed Performance”

Appendix 4 – Cash flow Statement

Cashflow Statement

P/E 31 March FY15 FY16 FY17E FY18E FY19E

PBT 3,644 5,708 5,967 7,728 8,265

Dividend Income (0) (3) - - -

Depreciation & Amortization 1,167 1,265 1,306 1,508 1,742

Interest Expense 969 754 837 786 643

(Profit) on sale of ST Investments - (11) - - -

(Profit)/Loss on sale of PPE (35) 23 - - -

Provision for defined benefit plans - 168 192 206 226

Profit Share of Investment in associate (831) (1,356) (1,518) (1,701) (1,905)

(Profit)/loss on Disposal of Subsidiary - 109 - - -

Other 287 - - - -

Operating Profit / (Loss) before Working Capital Changes 5,200 6,657 6,783 8,526 8,972

(Increase)/Decrease in Inventory (398) (49) (527) (779) (2,144)

(Increase)/Decrease in Receivables 502 206 (170) (549) (428)

Increase/(Decrease) in Payables 62 (114) 371 229 446

Other 260 (252) - - -

Net Change in Working Capital 425 (209) (326) (1,100) (2,125)

Cash Generated from Operation 5,625 6,448 6,456 7,427 6,846

Inerest paid (959) (806) (915) (860) (703)

Defined Benefit Obligations (79) (88) (90) (100) (109)

Tax Paid (202) (672) (1,671) (2,164) (2,314)

Cash from operations 4,384 4,882 3,781 4,304 3,721

Investing activities

Fixed and Intangible Assets (1,462) (1,877) (2,702) (2,726) (2,999)

Proceeds from Sale of Property, Plant & Equipment 41 74 - - -

Interest and Dividend received 108 234 78 74 60

Acquisition of Investments (67) - - - -

Proceeds from Sale of Short Term investments - 76 - - -

Cash from investments (1,381) (1,493) (2,624) (2,652) (2,939)

Fiancing Activities

Proceeds From Interest Bearing Loans & Borrowings (1,665) (941) (362) (59) (217)

Capital Repayments under Finance Lease Liabilities (33) (6) - - -

Dividend Paid (670) (931) (928) (1,202) (1,285)

Other 8 18 - - -

Cash from financing (2,361) (1,860) (1,290) (1,260) (1,503)

Net Foreign Exchange Differences (4) (2) - - -

Net cash during the year 639 1,528 (133) 391 (721)

Net cash at beginning (1,419) (780) 748 615 1,006

Net cash at end (780) 748 615 1,006 285

Balance sheet Cash Balance 1,329 2,322 2,189 2,580 1,859

Bank overdraft (2,109) (1,575) (1,575) (1,575) (1,575)

Source: Company Annual Reports and FC Research Estimates

347 1/1, Dr. Colvin R. De Silva Mawatha,

Colombo 2

Sales Desk: +94 11 2145 000

Fax: +94 11 5736 264

HEAD OFFICE BRANCHES

347 1/1, Negombo

Dr. Colvin R. De Silva Mawatha, No.72A, 2/1,

Colombo 2 Old Chilaw Road,

Negombo

Sales Desk: +94 11 2145 000

Fax: +94 11 5736 264 Tel: +94 31 2233 299

SALES BRANCHES

CEO http://www.firstcapital.lk/investment-bank-about-us/leadership/Jaliya Wijeratne +94 70 2910 042 Negombo

Priyanka Anuruddha +94 70 2910 035

Colombo Priyantha Wijesiri +94 70 2910 036

Damian Le Grand +94 70 2910 032

Nishantha Mudalige +94 70 2910 041

Isuru Jayawardana +94 70 2910 034

Anushka Buddhika +94 70 2910 030

Gamini Hettiarachchi +94 70 2910 039

Thushara Abeyratne +94 70 2910 037

RESEARCH

Dimantha Mathew +94 11 2145 016 Amanda Lokugamage +94 11 2145 015

Atchuthan Srirangan +94 11 2145 017 Michelle Weerasinghe +94 11 2145 018

Hansinee Beddage +94 11 2145 018

FIRST CAPITAL GROUP http://www.firstcapital.lk/investment-bank-about-us/leadership/

HEAD OFFICE BRANCHES

No. 2, Deal Place, Matara Kurunegala Kandy

Colombo 3 No. 24, 1/3, 2nd Floor, No. 6, 1st Floor, No.213-215,

Tel: +94 11 2639 898 Lakshman Cooray Building, Union Assurance Building, Peradeniya Road,

Anagarika Dharmapala Mawatha, Rajapihilla Mawatha, Kandy

Matara Kurunegala

Tel: +94 41 2222 988 Tel: +94 37 2222 930 Tel: +94 81 2236 011

Disclaimer:This Review is prepared and issued by First Capital Equities (Pvt) Ltd. and is based on information available in the public domain, internally developed and other sources

believed to be correct. Although all reasonable care has been taken to ensure that the contents of this document are accurate, First Capital Equities (Pvt) Ltd and its Directors

and employees, are not responsible for its accuracy, usefulness and reliability and disclaim liability for any loss suffered by the use of information contained herein.

First Capital Equities (Pvt) Ltd may act as a Broker in the investments which are the subject of this document or any related investments and may have acted on or have used

the information contained in this document, or the research or analysis on which it is based, before its publication.

First Capital Equities (Pvt) Ltd

Related Documents