CHAPTER 1- INTRODUCTION 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 1-

INTRODUCTION

1

11 INTRODUCTION TO ORGANIZATION

111 HISTORY

The Karvy group was formed in 1983 at Hyderabad India Karvy ranks among the

top player in almost all the fields it operates Karvy Computershare Limited is Indiarsquos largest

Registrar and Transfer Agent with a client base of nearly 500 blue chip corporates managing

over 2 crore accounts Karvy Stock Brokers Limited member of National Stock Exchange of

India and the Bombay Stock Exchange ranks among the top 5 stock brokers in India With

over 600000 active accounts it ranks among the top 5 Depositary Participant in India

registered with NSDL and CDSL Karvy Comtrade Member of NCDEX and MCX ranks

among the top 3 commodity brokers in the country Karvy Insurance Brokers is registered as

a Broker with IRDA and ranks among the top 5 insurance agent in the country Registered

with AMFI as a corporate Agent Karvy is also among the top Mutual Fund mobilizer with

over Rs 5000 crores under management Karvy Realty Services which started in 2006 has

quickly established itself as a broker who adds value in the realty sector Karvy Global offers

niche off shoring services to clients in the US Karvy has 575 offices over 375 locations

across India and overseas at Dubai and New York Over 9000 highly qualified people staff

Karvy

112 ORGANIZATION

Karvy was started by a group of five chartered accountants in 1979 The partners

decided to offer other than the audit services value added services like corporate advisory

services to their clients The first firm in the group Karvy Consultants Limited was

incorporated on 23rd July 1983 In a very short period it became the largest Registrar and

Transfer Agent in India This business was spun off to form a separate joint venture with

Computershare of Australia in 2005 Karvyrsquos foray into stock broking began with marketing

IPOs in 1993 Within a few years Karvy began topping the IPO procurement league tables

and it has consistently maintained its position among the top 5 Karvy was among the first

few members of National Stock Exchange in 1994 and became a member of The Stock

Exchange Mumbai in 2001 Dematerialization of shares gathered pace in mid-90s and Karvy

2

was in the forefront educating investors on the advantages of dematerializing their shares

Today Karvy is among the top 5 Depositary Participant in India

While the registry business is a 5050 Joint Venture with Computershare of Australia

we have equity participation by ICICI Ventures Limited and Barings Asia Limited in Karvy

Stock Broking Limited

Karvy has always believed in adding value to services it offers to clients A top-notch

research team based in Mumbai and Hyderabad supports its employees to advise clients on

their investment needs With the information overload today Karvyrsquos team of analysts help

investors make the right calls be it equities mf insurance On a typical working day Karvy

Has more than 25000 investors visiting our 575 offices

Publishes broadcasts at least 50 buy sell calls

Attends to 10000+ telephone calls

Mails 25000 envelopes containing Annual Reports dividend cheques advises

allotment refund advises

Executes 150000+ trades on NSE BSE

Executes 50000 debit credit in the depositary accounts

Advises 3000+ clients on the investments in mutual funds

113 SERVICES OFFERED

KARVY Stock Broking Limited one of the cornerstones of the KARVY edifice flows freely

towards attaining diverse goals of the customer through varied services It creates a plethora

of opportunities for the customer by opening up investment vistas backed by research-based

advisory services Here growth knows no limits and success recognizes no boundaries

Helping the customer create waves in his portfolio and empowering the investor completely

is the ultimate goal KARVY Stock Broking Limited is a member of

National Stock Exchange (NSE)

Bombay Stock Exchange (BSE)

3

Hyderabad Stock Exchange (HSE)

Karvy Com trade Limited an ISO 90012000 certified company is another venture of the

prestigious Karvy group With our well established presence in the multifarious facets of the

modern Financial services industry from stock broking to registry services it is indeed a

pleasure for us to make foray into the commodities derivatives market which opens yet

another door for us to deliver our service to our beloved customers and the investor public at

large

At Karvy Insurance Broking Limited we provide both life and non-life insurance products to

retail individuals high net-worth clients and corporates With the opening up of the insurance

sector and with a large number of private players in the business we are in a position to

provide tailor made policies for different segments of customers In our journey to emerge as

a personal finance advisor we will be better positioned to leverage our relationships with the

product providers and place the requirements of our customers appropriately with the product

providers With Indian markets seeing a sea change both in terms of investment pattern and

attitude of investors insurance is no more seen as only a tax saving product but also as an

investment product By setting up a separate entity we would be positioned to provide the

best of the products available in this business to our customers

Our wide national network spanning the length and breadth of India further supports these

advantages Further personalized service is provided here by a dedicated team committed in

giving hassle-free service to the clients

Deepening of the Financial Markets and an ever-increasing sophistication in corporate

transactions has made the role of Investment Bankers indispensable to organizations seeking

professional expertise and counseling in raising financial resources through capital market

apart from Capital and Corporate Restructuring Mergers amp Acquisitions Project Advisory

and the entire gamut of Financial Market activities

4

Karvy Investor Services Limited (lsquoKISLrsquo) a SEBI registered Merchant Banker has emerged

as a leading Investment Banking entity in the country with over a decade of experience KISL

has built its reputation by capitalizing on its qualified professionals who have successfully

executed a large number of complex and unique transactions

Our quality professional team and our work-oriented dedication have propelled us to offer

value-added corporate financial services and act as a professional navigator for long term

growth of our clients who include leading corporates State Governments Foreign

Institutional Investors public and private sector companies and banks in Indian and global

markets

We have also emerged as a trailblazer in the arena of relationships both at the customer and

trade levels because of our unshakable integrity seamless service and innovative solutions

that are tuned to meet varied needs Our team of committed industry specialists having

extensive experience in capital markets further nurtures this relationship

Credentials

Emerging as a leading Investment Banker with a strong support from its Group entities in

Research Stock Broking Institutional Sales and Retail Distribution

Strong team of more than 25 qualified professionals operating from six cities Hyderabad

Mumbai Delhi Kolkata Chennai and Bangalore apart from two overseas offices at New

York (USA) and Dubai

One of the largest retail distribution networks with over 584 branches in over 389

citiestowns

Excellent Institutional Sales Desk

Karvy Realty (India) Limited (KRIL) is promoted by the Karvy Group Indiarsquos largest

financial services group The group carries forward its legacy of trust and excellence in

5

investor and customer services delivered with passion and the highest level of quality that

align with global standards

Karvy Realty (India) Limited is engaged in the business of real estate and property services

offering

Buying selling renting of properties

Identifying valuable investments opportunities in the real estate sector

Facilitating financial support for real estate and investments in properties

Real estate portfolio advisory services

KRIL is your personal real estate advisor guiding and hand holding you through real estate

transactions and offering valuable investment opportunities Building on the KARVY brand

as a leading industry benchmark for world class customer servicing and quality standards

KRIL brings to investors a reputation of reliability dependability and honesty Our

understanding of the needs and preferences of our clients and our teams of qualified realty

professionals help us to establish fruitful relationships with buyers and sellers of properties

alike

A single stop shop for realty services offering

Transacting Options Choose to buy sell or rent properties (residential and

commercial)

Investing Options Give your investments a good opportunity with properties

marketed by KRIL

Financing Options Get unmatched deals for financing your investment

Research Options We undertake valuation and feasibility studies area analysis and

customized analysis on behalf of clients

6

KRIL has ongoing relations with builders and developers across the country which will help

you place your investments in the most genuine properties for a good value appreciation at

the right place and at the right price KRIL is committed to the guiding principles of

quality timely service delivery fair pricing transparency and integrity

Karvy Computershare Private Limited is a joint venture between Computershare

Australia and Karvy Consultants Limited India in the registry management services industry

Computershare Australia is the worldrsquos largest and only global share registry providing

financial market services and technology to the global securities industry Karvy Corporate

and Mutual Fund Share Registry and Investor Services business Indias No 1 Registrar and

Transfer Agent and rated as Indias Most Admired Registrar for its overall excellence in

volume management quality processes and technology driven services

Karvy Global Services is a knowledge services company We provide specialist resources to

extend in house analyst teams in driving clear business results We serve investment banks

insurance providers brokerages hedge funds research agencies and life settlement providers

across the United States Middle East and Europe Our clients have found our cost

advantage ability to scale efforts and specialist knowledge regarding emerging markets to be

a strong advantage in the new fast and unpredictable world Our areas of focus include

equity and industry research commodity research credit analytics technology-based

workflow solutions insurance policy and portfolio valuation and other specialized services

Incorporated in 2004 we are backed by over 25 years of experience through Indiarsquos largest

financial services company the Karvy Group We are headquartered in New York and have

our primary delivery center in Hyderabad India We encourage you to contact us to evaluate

your research or outsourcing needs

As the flagship company of the KARVY Group KARVY Consultants Limited has always

remained at the helm of organizational affairs pioneering business policies work ethic and

channels of progress Having emerged as a leader in the registry business the first of the

businesses that we ventured into we have now transferred this business into a joint venture

7

with Computershare Limited of Australia the worldrsquos largest registrar With the advent of

depositories in the Indian capital market and the relationships that we have created in the

registry business we believe that we were best positioned to venture into this activity as a

Depository Participant We were one of the early entrants registered as Depository Participant

with NSDL (National Securities Depository Limited) the first Depository in the country and

then with CDSL (Central Depository Services Limited) Today we service over seven lakh

customer accounts in this business spread across over 540 citiestowns in India and are

ranked amongst the largest Depository Participants in the country With a growing secondary

market presence we have transferred this business to KARVY Stock Broking Limited

(KSBL) our associate and a member of NSE BSE and HSE

114 ORGANIZATION

Karvy was started by a group of five chartered accountants in 1979 The partners decided to

offer other than the audit services value added services like corporate advisory services to

their clients The first firm in the group Karvy Consultants Limited was incorporated on 23rd

July 1983 In a very short period it became the largest Registrar and Transfer Agent in India

This business was spun off to form a separate joint venture with Computershare of Australia

in 2005 Karvyrsquos foray into stock broking began with marketing IPOs in 1993 Within a few

years Karvy began topping the IPO procurement league tables and it has consistently

maintained its position among the top 5 Karvy was among the first few members of National

Stock Exchange in 1994 and became a member of The Stock Exchange Mumbai in 2001

Dematerialization of shares gathered pace in mid-90s and Karvy was in the forefront

educating investors on the advantages of dematerializing their shares Today Karvy is among

the top 5 Depositary Participant in India While the registry business is a 5050 Joint Venture

with Computershare of Australia we have equity participation by ICICI Ventures Limited

and Barings Asia Limited in Karvy Stock Broking Limited Karvy has always believed in

adding value to services it offers to clients A top-notch research team based in Mumbai and

Hyderabad supports its employees to advise clients on their investment needs With the

8

information overload today Karvyrsquos team of analysts help investors make the right calls be it

equities mf insurance On a typical working day Karvy

Has more than 25000 investors visiting our 575 offices

Publishes broadcasts at least 50 buy sell calls

Attends to 10000+ telephone calls

12 INTRODUCTION TO COMMODITY MARKET

Commodity markets are markets where raw or primary products are exchanged These raw

commodities are traded on regulated commodities exchanges in which they are bought and

sold in standardized contracts

Commodity market is an important constituent of the financial markets of any country It is

the market where a wide range of products viz precious metals base metals crude oil

energy and soft commodities like plam oil coffee etc are traded It is important to develop a

vibrant active and liquid commodity market This will help investors hedge their commodity

risk take speculative positions in commodities and exploit arbitrage opportunities in the

market

Different types of commodities traded

World-over one will find that a market exists for almost all the commodities known to us

These commodities can be broadly classified into the following categories

Precious metals Gold Silver Platinum etc

Other metals Nickel Aluminum Copper etc

Agro-Based commodities Wheat Corn Cotton Oils Oilseeds

Soft commodities Coffee Cocoa Sugar etc

Live-Stock Live cattle Pork bellies etc

Energy Crude oil Natural Gas Gasoline etc

9

10

121 COMMODITIES AND COMMODITY MARKET IN INDIA

India a commodity based economy where two-third of the one billion population depends on

agricultural commodities surprisingly has an under developed commodity market Unlike the

physical market futures markets trades in commodity are largely used as risk management

(hedging) mechanism on either physical commodity itself or open positions in commodity

stock

For instance a jeweler can hedge his inventory against perceived short-term downturn in gold

prices by going short in the future markets

The article aims at know how of the commodities market and how the commodities traded on

the exchange The idea is to understand the importance of commodity derivatives and learn

about the market from Indian point of view In fact it was one of the most vibrant markets till

early 70s Its development and growth was shunted due to numerous restrictions earlier Now

with most of these restrictions being removed there is tremendous potential for growth of

this market in the country

History

Though in recent years organized commodity markets have come into limelight however we

have a long history of commodity markets It is believed that the establishment of Bombay

Cotton Trade Association Ltd in 1875 marks the beginning of organized futures Commodity

market in India Further while in 1900 futures trading in oilseeds was organized

In India with the setting up of Gujarati Vyapari Mandali the same in Raw Jute and Jute

Goods began in Calcutta with the establishment of the Calcutta Hessian Exchange Ltd in

1919 Futures market in Bullion began at Mumbai in 1920 and following the trend similar

Markets also came up in various other key cities of the country Over the years futures

Trading in various other commodities like pepper turmeric potato sugar and gur etc also

begun After independence Forward Contracts (Regulation) Act 1952 was enacted to

regulate commodity futures markets and Forward Markets Commission was also set up

However in the seventies most of the registered associations became inactive as futures

trading in the commodities for which they were registered came to be either suspended or

prohibited altogether With the gradual withdrawal of the government from various sectors in

the post-liberalization era the need has been felt that various operators in the commodities

market is provided with a mechanism to perform the economic functions of price discovery

and risk management Consequently the Government issued notifications on 142003

permitting futures trading in the commodities

11

122 COMMODITY

A commodity may be defined as an article a p

roduct or material that is bought and sold It can be classified as every kind of movable

property except Actionable Claims Money amp Securities

Commodities actually offer immense potential to become a separate asset class for market-

savvy investors arbitrageurs and speculators Retail investors who claim to understand the

equity markets may find commodities an unfathomable market But commodities are easy to

understand as far as fundamentals of demand and supply are concerned Retail investors

should understand the risks and advantages of trading in commodities futures before taking a

leap Historically pricing in commodities futures has been less volatile compared with equity

and bonds thus providing an efficient portfolio diversification option

In fact the size of the commodities markets in India is also quite significant Of the countrys

GDP of Rs 13 20730 crore (Rs 132073 billion) commodities related (and dependent)

industries constitute about 58 per cent

Currently the various commodities across the country clock an annual turnover of Rs 1

40000 crore (Rs 1400 billion) With the introduction of futures trading the size of the

commodities market grows many folds here on

123 COMMODITY MARKET

Commodity market is an important constituent of the financial markets of any country It is

the market where a wide range of products viz precious metals base metals crude oil

energy and soft commodities like palm oil coffee etc are traded It is important to develop a

vibrant active and liquid commodity market This would help investors hedge their

commodity risk take speculative positions in commodities and exploit arbitrage opportunities

in the market

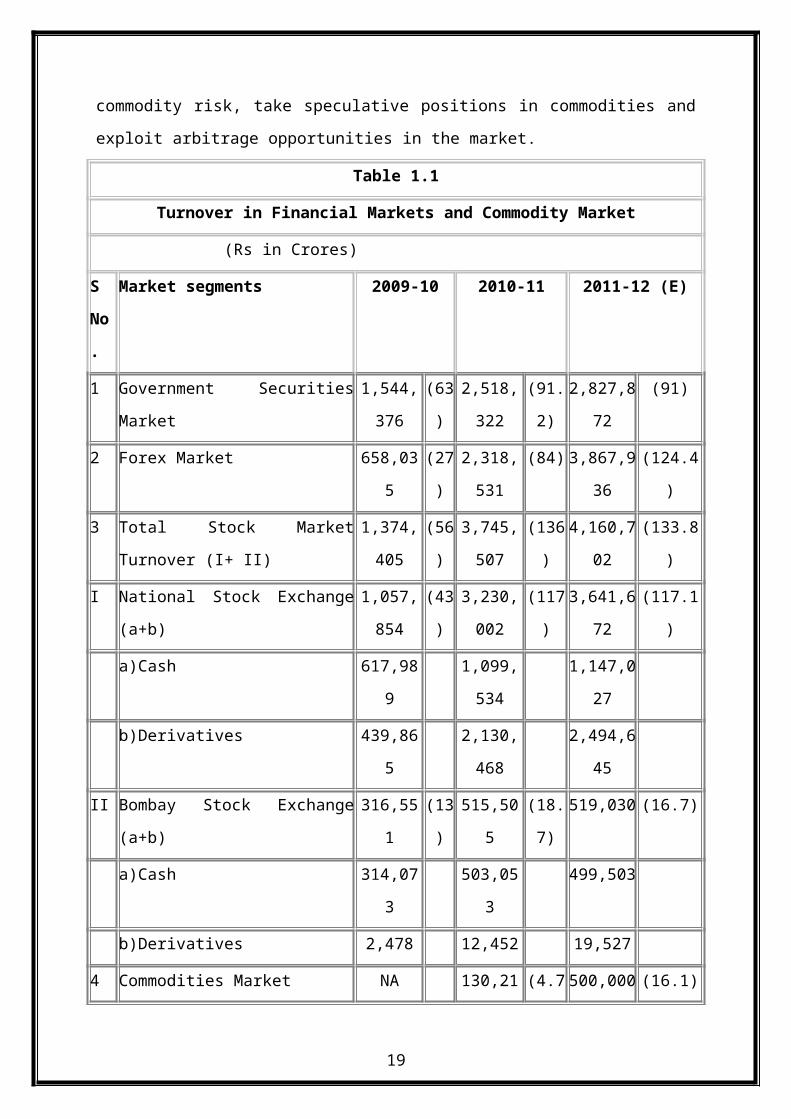

Table 11

Turnover in Financial Markets and Commodity Market

(Rs in Crores)

S

No

Market segments 2009-10 2010-11 2011-12 (E)

1 Government Securities Market 1544376 (63) 2518322 (912) 2827872 (91)

2 Forex Market 658035 (27) 2318531 (84) 3867936 (1244)

12

3 Total Stock Market Turnover (I+ II) 1374405 (56) 3745507 (136) 4160702 (1338)

I National Stock Exchange (a+b) 1057854 (43) 3230002 (117) 3641672 (1171)

a)Cash 617989 1099534 1147027

b)Derivatives 439865 2130468 2494645

II Bombay Stock Exchange (a+b) 316551 (13) 515505 (187) 519030 (167)

a)Cash 314073 503053 499503

b)Derivatives 2478 12452 19527

4 Commodities Market NA 130215 (47) 500000 (161)

Note Fig in bracket represents percentage to GDP at market prices

Source SEBI Bulletin

Different types of commodities traded

World-over one will find that a market exits for almost all the commodities known to us

These commodities can be broadly classified into the following

Precious Metals Gold Silver Platinum etc

Other Metals Nickel Aluminum Copper etc

Agro-Based Commodities Wheat Corn Cotton Oils Oilseeds

Soft Commodities Coffee Cocoa Sugar etc

Live-Stock Live Cattle Pork Bellies etc

Energy Crude Oil Natural Gas Gasoline etc

Different segments in Commodities market

The commodities market exits in two distinct forms namely the Over the Counter (OTC)

market and the Exchange based market Also as in equities there exists the spot and the

derivatives segment The spot markets are essentially over the counter markets and the

participation is restricted to people who are involved with that commodity say the farmer

processor wholesaler etc Derivative trading takes place through exchange-based markets

with standardized contracts settlements etc

Leading commodity markets of world

13

Some of the leading exchanges of the world are New York Mercantile Exchange (NYMEX)

the London Metal Exchange (LME) and the Chicago Board of Trade (CBOT)

Leading commodity markets of India

The government has now allowed national commodity exchanges similar to the BSE amp NSE

to come up and let them deal in commodity derivatives in an electronic trading environment

These exchanges are expected to offer a nation-wide anonymous order driven screen based

trading system for trading The Forward Markets Commission (FMC) will regulate these

exchanges

Consequently four commodity exchanges have been approved to commence business in this

regard They are

Multi Commodity Exchange (MCX) located at Mumbai

National Commodity and Derivatives Exchange Ltd (NCDEX) located at Mumbai

National Board of Trade (NBOT) located at Indore

National Multi Commodity Exchange (NMCE) located at Ahmedabad

Regulatory Framework

The commodity exchanges are governed and regulated under FORWARDS CONTRACTS

(REGULATION) ACT 1952 by the FORWARDS MARKET COMMISSION (FMC)

Which is an apex regulatory body for the commodities and futures market on the lines of

securities and exchange board of India (SEBI) for the securities market operations The

commodity exchanges are granted approval by FMC under the overall aegis of the Ministry

Of Consumer Affairs Food and Public Distribution Government of India All commodities

and future contracts traded on the exchange are required to be approved by the FMC along

14

MAIN COMMODITY EXCHANGES OF INDIA

with their contract specification which describes the quantity quality and place of the

commodities traded

The Indian commodities market stands out quiet tall among the global markets for a variety

of factors And the reasons for the same are not difficult to understand

Supply Worldrsquos leading producers of 17 agro commodities

Demand Worlds largest consumer of edible oils GOLD

GDP driver Primarily an AGRAIRIAN ECONOMY

Captive market Agro Products are consumed locally

Waiting to explode Value of production around Rs 300000 crore and expected

future market potential around Rs 3000000 crore (this is assuming a conservative

multiplier 10 times which was 20 times and also assuming that all commodities have

futures market over a period of time as the markets mature )

124 OVERVIEW OF COMMODITIES EXCHANGES IN INDIA

Forward Markets Commission (FMC) headquartered at Mumbai is a regulatory authority

which is overseen by the Ministry of Consumer Affairs and Public Distribution Govt of

India It is a statutory body set up in 1953 under the Forward Contracts (Regulation) Act

1952

The Act Provides that the Commission shall consist of not less then two but not exceeding

four members appointed by the Central Government out of them being nominated by the

Central Government to be the Chairman thereof Currently Commission comprises three

members among whom Dr Kewal Ram IES is acting as Chairman and Smt Padma

Swaminathan CSS and Dr (Smt) Jayashree Gupta CSS are the Members of the

Commission

The list of exchanges that has been allowed to trade in commodities are

1 Bhatinda Om amp Oil Exchange Ltd Batinda

2 The Bombay Commodity Exchange Ltd Mumbai

3 The Rajkot Seeds oil amp Bullion Merchants` Association Ltd

4 The Kanpur Commodity Exchange Ltd Kanpur

15

5 The Meerut Agro Commodities Exchange Co Ltd Meerut

6 The Spices and Oilseeds Exchange Ltd

7 Ahmedabad Commodity Exchange Ltd

8 Vijay Beopar Chamber Ltd Muzaffarnagar

9 India Pepper amp Spice Trade Association Kochi

10 Rajdhani Oils and Oilseeds Exchange Ltd Delhi

11 National Board of Trade Indore

12 The Chamber Of Commerce Hapur

13 The East India Cotton Association Mumbai

14 The Central India Commercial Exchange Ltd Gwaliar

15 The East India Jute amp Hessian Exchange Ltd

16 First Commodity Exchange of India Ltd Kochi

17 Bikaner Commodity Exchange Ltd Bikaner

18 The Coffee Futures Exchange India Ltd Bangalore

19 Esugarindia Limited

20 National Multi Commodity Exchange of India Limited

21 Surendranagar Cotton oil amp Oilseeds Association Ltd

22 Multi Commodity Exchange of India Ltd

23 National Commodity amp Derivatives Exchange Ltd

24 Haryana Commodities Ltd Hissar

25 e-Commodities Ltd

125 NCDEX AND MCX

The two main exchanges in India facilitating commodity trading are NCDEX and MCX

National Commodity amp Derivatives Exchange Limited

16

NCDEX is a public limited company incorporated on April 23 2003 under the Companies

Act 1956 It has commenced its operations on December 15 2003 National Commodity amp

Derivatives Exchange Limited (NCDEX) is a professionally managed online multi

commodity exchange promoted by ICICI Bank Limited (ICICI Bank) Life Insurance

Corporation of India (LIC) National Bank for Agriculture and Rural Development

(NABARD) and National Stock Exchange of India Limited (NSE) Punjab National Bank

(PNB) CRISIL Limited Indian Farmers Fertilizer Cooperative Limited (IFFCO) and

Canara Bank by subscribing to the equity shares have joined the initial promoters as

shareholders of the Exchange Started with an authorized capital of Rs50crores ICICI

BANK LIC NABARD and NSE hold the maximum share in the share capital (15

each)NCDEX is located in Mumbai and offers facilities to its members in more than

390centers throughout India The reach will gradually be expanded to more centers NCDEX

is the only commodity exchange in the country promoted by national level institutions

NCDEX is a nation-level technology driven on-line commodity exchange with an

independent Board of Directors and professionals not having any vested interest in

commodity markets

NCDEX currently facilitates trading of thirty six commodities - Cashew Castor Seed

Chana Chilli Coffee Cotton Cotton Seed Oilcake Crude Palm Oil Expeller Mustard Oil

Gold Guar gum Guar Seeds Gur Jeera Jute sacking bags Mild Steel Ingot Mulberry

Green Cocoons Pepper Rapeseed - Mustard Seed Raw Jute RBD Palmolein Refined Soy

Oil Rice Rubber Sesame Seeds Silk Silver Soy Bean Sugar Tur Turmeric Urad (Black

Matpe) Wheat Yellow Peas Yellow Red Maize amp Yellow Soybean Meal At subsequent

phases trading in more commodities would be facilitated

Currently NCDEX has 700 members at 470 locations across the country The exchange saw

400 growth in the first year of its operations and expects 200 in the second year also

According to the latest news NCDEX plans to roll out more contracts like contracts in nickel

tin and mentha oil

17

Multi Commodity Exchange of India Limited (MCX)

MCX an independent multi commodity exchange has permanent recognition from

Government of India for facilitating online trading clearing and settlement operations for

commodity futures markets across the country It was inaugurated in November 2003 by Mr

Mukesh Ambani It is headquartered in Mumbai The key shareholders of MCX are Financial

Technologies (India) Ltd State Bank of India NABARD NSE HDFC Bank State Bank of

Indore State Bank of Hyderabad State Bank of Saurashtra SBI Life Insurance Co Ltd

Union Bank of India Bank Of India Bank Of Baroda Canara Bank Corporation Bank

MCX offers futures trading in the following commodity categories Agri Commodities

Bullion Metals- Ferrous amp Non-ferrous Pulses Oils amp Oilseeds Energy Plantations Spices

and other soft commodities

Today MCX is offering spectacular growth opportunities and advantages to a large cross

section of the participants including Producers Processors Traders Corporate Regional

Trading Centers Importers Exporters Cooperatives and Industry Associations

In a significant development National Stock Exchange of India Ltd (NSE) countryrsquos largest

exchange and National Bank for Agriculture and Rural Development (NABARD) countryrsquos

premier agriculture development bank announced their strategic participation in the equity of

MCX on June 15 2005 This new partnership of NSE and NABARD with MCX makes MCX

consortium the largest distribution network across the country

MCX is an ISO 90012000 online nationwide multi commodity exchange It has over 900+

members spread across 500+ centers across the country with more than 750+VSATs and

leased line connections and 5000+ trading terminals that provide a transparent robust and

trustworthy trading platform in more than 50 commodity futures contract with a wide range

of commodity baskets which includes metals energy and agriculture commodities Exchange

has pioneered major innovations in Indian commodities market which has become the

industry benchmarks subsequently

18

MCX is the only Exchange which has got three international tie- ups which is with Tokyo

Commodity Exchange (TOCOM) the 250 year old Baltic Freight Exchange London Dubai

Metals amp Commodity Centre (DMCC) amp Dubai Gold amp Commodity Exchange (DGCX) the

strategic initiative of Government of Dubai MCX has to its credit setting up of the National

spot exchange (NSEAP) which connects all India APMC markets thereby contributing in the

implementation of Government of Indiarsquos vision to create a common Indian market

The trading system of MCX is state- of-the -art new generation trading platform that permits

extremely cost effective operations at much greater efficiency The Exchange Central System

is located in Mumbai which maintains the Central Order Book Exchange Members located

across the country are connected to the central system through VSAT or any other mode of

communication as may be decided by the Exchange from time to time The controls in the

system are system driven requiring minimum human intervention The Exchange Members

places orders through the Traders Work Station (TWS) of the Member linked to the

Exchange which matches on the Central System and sends a confirmation back to the

Member

Settlement Exchange maintains electronic interface with its Clearing Bank All Members of

the Exchange are having their Exchange operations account with the Clearing Bank

All debits and credits are affected electronically through such accounts only All contracts on

maturity are for delivery MCX specifies tender and delivery periods A seller or a short open

position holder in that contract may tender documents to the

Exchange expressing his intention to deliver the underlying commodity Exchange would

select from the long open position holder for the tendered quantity Once the buyer is

identified seller has to initiate the process of giving delivery and buyer has to take delivery

according to the delivery schedule prescribed by the Exchange Players involve d in

commodities trading like commodity exchanges financial institutions and banks have a

feeling that the markets are not being fully exploited Education and regulation are the main

impediments to the growth of commodity trading Producers farmers and Agri- based

companies should enter into formal contracts to hedge against losses The use of commodity

exchanges will create more trading opportunities result in an integrated market and better

price discoveries

19

MCX and NCDEX Membership

There shall be different classes of membership along with associated rights and privileges

which will include trading cum clearing membership and institutional clearing members to

start with MCX and NCDEX would also include other membership classes as may be

defined by the Exchange from time to time The different membership classes of MCX and

NCDEX for the present are as under

Trading-Cum-Clearing Member

Trading-Cum-Clearing Member means a personcorporate who is admitted by the Exchange

as the member conferring upon them a right to trade and clear through the clearing house of

the Exchange as a Clearing Member

Moreover the Member may be allowed to make deals for himself as well as on behalf of his

clients and clear and settle such deals only

Institutional Clearing Member

Institutional Clearing Member means a person who is admitted by the Exchange as a Clearing

Member of the Exchange and the Clearing House of the Exchange and who shall be allowed

to only clear and settle trades on account of Trading-Cum ndashClearing Members

The Market Rules

The Market of the Exchange would be provided with the following framework to trade on

MCX and NCDEX

They would be required to register with the Exchange on payment of a membership fee

and on compliance of their registration requirements

Trading limit could be obtained by the Exchange Members on payment of a deposit

which is called as a Margin Deposit

They would be provided the software for trading on the exchange

They would be connected to the central system of MCX and NCDEX inn Mumbai

through a VSAT

The members have to maintain account with an approved Clearing Bank of MCX and

NCDEX which would provide the Electronic Fund Transfer facility between the

Members and the Exchange through which the daily receipts and payments of margin and

mark-to-margins would be accomplished

20

The Trading Mechanism

How Trading would take place on MCX and NCDEX

The trading system of MCX and NCDEX is state of the art new generation trading platform

that permits extremely cost effective operations at much greater efficiency The Exchange

Central System is located in Mumbai which will maintain the Central order book Exchange

members could be located anywhere in the country and would be connected to Central system

through VSAT or any other mode of communications may be decided by the Exchange from

time to time The exchange members would place orders through the Traders Workstation

(TWS) of the member linked to the Exchange which shall match on the Central System and

send a confirmation back to the member

Clearing and Settlement Mechanism

How MCX and NCDEX propose to Clear and Settle

The clearing and settlement system of Exchange is system driven and rules based

Clearing Bank Interface

Exchange will maintain electronic interface with its clearing bank All members need to have

their Exchange operation account with such clearing bank All debits and credits will be

affected through such accounts only

Delivery and Final Settlement

All contracts on maturity are for delivery MCX and NCDEX would specify a tender amp

delivery period For example such periods can be from 8 th working day till the 15th day of the

month-where 15th is the last trading day of the contract month ndashas tender ampor delivery

period A seller or a short open position holder in that contract may tender documents to the

Exchange expressing his intention to deliver the underlying commodity Exchange would

select from the long open position for the tendered quantity Once the buyer is identified

seller has to initiate the process of giving delivery amp buyer has to take delivery according to

the delivery schedule prescribed by the exchange

Limitations of forward markets

Forward markets world-wide are affected by several problems

Lack of centralization of trading

Illiquidity and Counterparty risk

21

In the first two of these the basic problem is that of too much edibility and generality The

forward market is like a real estate market in that any two consenting adults can form

contracts against each other This often makes them design terms of the deal which are very

convenient in that specific situation but makes the contracts non-tradable

Counterparty risk arises from the possibility of default by any one party to the transaction

When one of the two sides to the transaction declares bankruptcy the other suffers Even

when forward markets trade standardized contracts and hence avoid the problem of

illiquidity still the counterparty risk remains a very serious issue

126 COMMODITY DERIVATIVES

Derivatives as a tool for managing risk first originated in the commodities markets They

were then found useful as a hedging tool in financial markets as well In India trading in

commodity futures has been in existence from the nineteenth century with organized trading

in cotton through the establishment of Cotton Trade Association in 1875 Over a period of

time other commodities were permitted to be traded in futures exchanges Regulatory

constraints in 1960s resulted in virtual dismantling of the commodities future markets It is

only in the last decade that commodity future exchanges have been actively encouraged

However the markets have been thin with poor liquidity and have not grown to any

significant level In this chapter we look at how commodity derivatives differ from financial

derivatives We also have a brief look at the global commodity markets and the commodity

markets that exist in India

Difference between commodity and financial derivatives

The basic concept of a derivative contract remains the same whether the underlying happens

to be a commodity or a financial asset However there are some features which are very

peculiar to commodity derivative markets In the case of financial derivatives most of these

contracts are cash settled Even in the case of physical settlement financial assets are not

bulky and do not need special facility for storage Due to the bulky nature of the underlying

assets physical settlement in commodity derivatives creates the need for warehousing

Similarly the concept of varying quality of asset does not really exist as far as financial

underlying are concerned

However in the case of commodities the quality of the asset underlying a contract can vary

largely This becomes an important issue to be managed We have a brief look at these issues

22

Futures

Futures markets were designed to solve the problems that exist in forward markets A futures

contract is an agreement between two parties to buy or sell an asset at a certain time in the

future at a certain price But unlike forward contracts the futures contracts are standardized

and exchange traded To facilitate liquidity in the futures contracts the exchange specifies

certain standard features of the contract It is a standardized contract with standard underlying

instrument a standard quantity and quality of the underlying instrument that can be delivered

(or which can be used for reference purposes in settlement) and a standard timing of such

Settlement A futures contract may be offset prior to maturity by entering into an equal and

opposite transaction More than 99 of futures transactions are offset this way

The standardized items in a futures contract are

Quantity of the underlying

Quality of the underlying

The date and the month of delivery

The units of price quotation and minimum price change

Location of settlement

Futures terminology

Spot price The price at which an asset trades in the spot market

Futures price The price at which the futures contract trades in the futures market

Contract cycle The period over which a contract trades The commodity futures contracts on

the NCDEX have one-month two-months and three-month expiry cycles which expire on the

20th day of the delivery month Thus a January expiration contract expires on the 20th of

January and a February expiration contract ceases trading on the 20th of February On the

next trading day following the 20th a new contract having a three-month expiry is introduced

for trading

Expiry date It is the date specified in the futures contract This is the last day on which the

contract will be traded at the end of which it will cease to exist

23

Delivery unit The amount of asset that has to be delivered less than one contract For

instance the delivery unit for futures on Long Staple Cotton on the NCDEX is 55 bales The

delivery unit for the Gold futures contract is 1 kg

Basis Basis can be defined as the futures price minus the spot price There will be a different

basis for each delivery month for each contract In a normal market basis will be positive

This reflects that futures prices normally exceed spot prices

Cost of carry The relationship between futures prices and spot prices can be summarized in

terms of what is known as the cost of carry This measures the storage cost plus the interest

that is paid to finance the asset less the income earned on the asset

Initial margin The amount that must be deposited in the margin account at the time a futures

contract is first entered into is known as initial margin

Marking-to-market (MTM) In the futures market at the end of each trading day the

margin account is adjusted to re ect the investorrsquos gain or loss depending upon the futures

closing price This is called markingndashtondashmarket Maintenance margin This is somewhat

lower than the initial margin This is set to ensure that the balance in the margin account

never becomes negative

Introduction to options

In this section we look at another interesting derivative contract namely options Options are

fundamentally different from forward and futures contracts An option gives the holder of the

option the right to do something The holder does not have to exercise this right In contrast

in a forward or futures contract the two parties have committed themselves to doing

something Whereas it costs nothing (except margin requirements) to enter into a futures

contract the purchase of an option requires an upndashfront payment

Option terminology

Commodity options Commodity options are options with a commodity as the underlying

For instance a gold options contract would give the holder the right to buy or sell a specified

quantity of gold at the price specified in the contract

24

Stock options Stock options are options on individual stocks Options currently trade on

over 500 stocks in the United States A contract gives the holder the right to buy or sell shares

at the specified price

Buyer of an option The buyer of an option is the one who by paying the option premium

buys the right but not the obligation to exercise his option on the seller writer

Writer of an option The writer of a call put option is the one who receives the option

premium and is thereby obliged to sell buy the asset if the buyer exercises on him

There are two basic types of options call options and put options

Call option A call option gives the holder the right but not the obligation to buy an asset by

a certain date for a certain price

Put option A put option gives the holder the right but not the obligation to sell an asset by a

certain date for a certain price

Option price Option price is the price which the option buyer pays to the option seller It is

also referred to as the option premium

Expiration date The date specified in the options contract is known as the expiration date

the exercise date the strike date or the maturity

Strike price The price specified in the options contract is known as the strike price or the

exercise price

American options American options are options that can be exercised at any time upto the

expiration date Most exchange-traded options are American

European options European options are options that can be exercised only on the expiration

date itself European options are easier to analyze than American options and properties of

an American option are frequently deduced from those of its European counterpart

In-the-money option An in-the-money (ITM) option is an option that would lead to positive

cash flow to the holder if it were exercised immediately A call option on the index is said to

25

be in-the-money when the current index stands at a level higher than the strike price (ie spot

price strike price) If the index is much higher than the strike price the call is said to be deep

ITM In the case of a put the put is ITM if the index is below the strike price

(At-the-money option An at-the-money (ATM) option is an option that would lead to zero

cash flow if it were exercised immediately An option on the index is at-the-money when the

current index equals the strike price (ie spot price = strike price)

Out-of-the-money option An out-of-the-money (OTM) option is an option that would lead to

a negative cash flow it was exercised immediately A call option on the index is out-of-the-

money when the current index stands at a level which is less than the strike price (ie spot

price strike price) If the index is much lower than the strike price the call is said to be deep

OTM In the case of a put the put is OTM if the index is above the strike price )

Intrinsic value of an option The option premium can be broken down into two components

ndash intrinsic value and time value The intrinsic value of a call is the amount the option is ITM

if it is ITM If the call is OTM its intrinsic value is zero Putting it another way the intrinsic

value of a call is I Similarly Q which means the intrinsic value of a call is the greater of 0 or

9 I K is the strike price Q ie the greater of 0 or 9 C is the spot price the intrinsic value of a

put is 0

Time value of an option The time value of an option is the difference between its premium

and its intrinsic value Both calls and puts have time value An option that is OTM or ATM

has only time value

127 WORKING OF COMMODITY MARKET

Physical settlement

Physical settlement involves the physical delivery of the underlying commodity typically at

an accredited warehouse The seller intending to make delivery would have to take the

commodities to the designated warehouse and the buyer intending to take delivery would

have to go to the designated warehouse and pick up the commodity This may sound simple

but the physical settlement of commodities is a complex process The issues faced in physical

settlement are enormous There are limits on storage facilities in different states There are

restrictions on interstate movement of commodities Besides state level octroi and duties have

26

an impact on the cost of movement of goods across locations The process of taking physical

delivery in commodities is quite different from the process of taking physical delivery in

financial assets We take a general overview at the process of physical settlement of

commodities Later on we will look into details of how physical settlement happens on the

NCDEX

Delivery notice period

Unlike in the case of equity futures typically a seller of commodity futures has the option to

give notice of delivery This option is given during a period identified as lsquodelivery notice

periodrsquo Such contracts are then assigned to a buyer in a manner similar to the assignments to

a seller in an options market However what is interesting and different from a typical options

exercise is that in the commodities market both positions can still be closed out before expiry

of the contract The intention of this notice is to allow verification of delivery and to give

adequate notice to the buyer of a possible requirement to take delivery These are required by

virtue of the act that the actual physical settlement of commodities requires preparation from

both delivering and receiving members

Typically in all commodity exchanges delivery notice is required to be supported by a

warehouse receipt The warehouse receipt is the proof for the quantity and quality of

commodities being delivered Some exchanges have certified laboratories for verifying the

quality of goods In these exchanges the seller has to produce a verification report from these

laboratories along with delivery notice Some exchanges like LIFFE accept warehouse

receipts as quality verification documents while others like BMFndashBrazil have independent

grading and classification agency to verify the quality

In the case of BMF-Brazil a seller typically has to submit the following documents

A declaration verifying that the asset is free of any and all charges including fiscal debts

related to the stored goods A provisional delivery order of the good to BMampF (Brazil)

issued by the warehouse A warehouse certificate showing that storage and regular insurance

have been paid

Assignment

Whenever delivery notices are given by the seller the clearing house of the exchange

identifies the buyer to whom this notice may be assigned Exchanges follow different

27

practices for the assignment process One approach is to display the delivery notice and allow

buyers wishing to take delivery to bid for taking delivery Among the international

exchanges BMF CBOT and CME display delivery notices Alternatively the clearing

houses may assign deliveries to buyers on some basis Exchanges such as COMMEX and the

Indian commodities exchanges have adopted this method

Any seller buyer who has given intention to deliver been assigned a delivery has an option

to square off positions till the market close of the day of delivery notice After the close of

trading exchanges assign the delivery intentions to open long positions Assignment is done

typically either on random basis or firstndashinndashfirst out basis In some exchanges (CME) the

buyer has the option to give his preference for delivery location The clearing house decides

on the daily delivery order rate at which delivery will be settled Delivery rate depends on the

spot rate of the underlying adjusted for discount premium for quality and freight costs The

discount premium for quality and freight costs are published by the clearing house before

introduction of the contract The most active spot market is normally taken as the benchmark

for deciding spot prices Alternatively the delivery rate is determined based on the previous

day closing rate for the contract or the closing rate for the day

Delivery

After the assignment process clearing house exchange issues a delivery order to the buyer

The exchange also informs the respective warehouse about the identity of the buyer The

buyer is required to deposit a certain percentage of the contract amount with the clearing

house as margin against the warehouse receipt The period available for the buyer to take

physical delivery is stipulated by the exchange Buyer or his authorized representative in the

presence of seller or his representative takes the physical stocks against the delivery order

Proof of physical delivery having been affected is forwarded by the seller to the clearing

house and the invoice amount is credited to the sellerrsquos account In India if a seller does not

give notice of delivery then at the expiry of the contract the positions are cash settled by price

difference exactly as in cash settled equity futures contracts

Warehousing

One of the main differences between financial and commodity derivatives are the need for

warehousing In case of most exchangendashtraded financial derivatives all the positions are cash

settled Cash settlement involves paying up the difference in prices between the time the

28

contract was entered into and the time the contract was closed For instance if a trader buys

futures on a stock at Rs100 and on the day of expiration the futures on that stock close

Rs120 he does not really have to buy the underlying stock All he does is take the difference

of Rs20 in cash Similarly the person who sold this futures contract at Rs100 does not have

to deliver the underlying stock All he has to do is pay up the loss of Rs20 in cash

In case of commodity derivatives however there is a possibility of physical settlement

Which means that if the seller chooses to hand over the commodity instead of the difference

in cash the buyer must take physical delivery of the underlying asset This requires the

exchange to make an arrangement with warehouses to handle the settlements The efficacy of

the commodities a settlement depends on the warehousing system available Most

international commodity exchanges used certified warehouses (CWH) for the purpose of

handling physical settlements

Such CWH are required to provide storage facilities for participants in the commodities

markets and to certify the quantity and quality of the underlying commodity The advantage

of this system is that a warehouse receipt becomes good collateral not just for settlement of

exchange trades but also for other purposes too In India the warehousing system is not as

efficient as it is in some of the other developed markets Central and state government

controlled warehouses are the major providers of Agrindashproduce storage facilities Apart from

these there are a few private warehousing being maintained However there is no clear

regulatory oversight of warehousing services

Quality of underlying assets

A derivatives contract is written on a given underlying Variance in quality is not an issue in

case of financial derivatives as the physical attribute is missing When the underlying asset is

a commodity the quality of the underlying asset is of prime importance There may be quite

some variation in the quality of what is available in the marketplace When the asset is

specified it is therefore important that the exchange stipulate the grade or grades of the

commodity that are acceptable Commodity derivatives demand good standards and quality

assurance certification procedures A good grading system allows commodities to be traded

by specification

Currently there are various agencies that are responsible for specifying grades for

Commodities For example the Bureau of Indian Standards (BIS) under Ministry of

29

Consumer Affairs specifies standards for processed agricultural commodities whereas

AGMARK under the department of rural development under Ministry of Agriculture is

responsible for promulgating standards for basic agricultural commodities Apart from these

there are other agencies like EIA which specify standards for export oriented commodities

How does a Commodity Futures Exchange help in Price Discovery

Unlike the physical market a futures market facilitates offsetting the trades without changing

physical goods until the expiry of a contract

As a result futures market attracts hedgers for risk management and encourages considerable

external competition from those who possess market information and price judgment to trade

as traders in these commodities While hedgers have long-term perspective of the market the

traders or arbitragers prefer an immediate view of the market However all these users

participate in buying and selling of commodities based on various domestic and global

parameters such as price demand and supply climatic and market related information

These factors together result in efficient price discovery allowing large number of buyers

and sellers to trade on the exchange MCX is communicating these prices all across the globe

to make the market more efficient and to enhance the utility of this price discovery function

Price Risk Management Hedging is the practice of off-setting the price risk inherent in any

cash market position by taking an equal but opposite position in the futures market This

technique is very useful in case of any long-term requirements for which the prices have to be

firmed to quote a sale price but to avoid buying the physical commodity immediately to

prevent blocking of funds and incurring large holding costs

How does a seller tender delivery to a buyer

Sellers at MCX intimate the exchange at the beginning of the tender period and get the

delivery quality certified from empanelled quality certification agencies They also submit the

documents to the Exchange with the details of the warehouse within the city chosen as a

delivery center Sellers are free to use any warehouse as they are responsible for the goods

until the buyer picks up the delivery which is a practice followed in the commodities market

globally

30

Seller would receive the money from the exchange against the goods delivered which

happens when the buyer has confirmed its satisfaction over quality and picked up the

deliveries within stipulated time

MCX has tied up with State Level Warehousing Corporations of Karalla Gujarat Tamil

Nadu and Uttar Pradesh and is in the process of finalizing the arrangements with CWC and

other State level Warehousing Corporations

How settlement happens at the end of the contract

A contract has a life cycle of one month or longer At MCX two weeks before the expiry of a

contract the contract enters into a tender period At the start of the tender period both the

parties must state their intentions to give or receive delivery based on which the parties are

supposed to act or bear the penal charges for any failure in doing so

Those who do not express their intention to give or receive delivery at the beginning of tender

period are required to square-up their open positions before the expiry of the contract In case

they do not their positions are closed out at due date rate The links to the physical market

through the delivery process ensures maintenance of uniformity between spot and futures

prices

Charges

Members are liable to pay transaction charges for the trade done through the exchange during

the previous month The important provisions are listed below The billing for the all trades

done during the previous month will be raised in the succeeding month

1 Rate of charges The transaction charges are payable at the rate of Rs6 per Rs one Lakh

trade done This rate is subject to change from time to time

2 Due date The transaction charges are payable on the 7th day from the date of the bill

every month in respect of the trade done in the previous month

3 Collection process NCDEX has engaged the services of Bill Junction Payments Limited

(BJPL) to collect the transaction charges through Electronic Clearing System

4 Registration with BJPL and their services Members have to fill up the mandate form

and submit the same to NCDEX NCDEX then forwards the mandate form to BJPL BJPL

sends the logndashin ID and password to the mailing address as mentioned in the registration

form The members can then log on through the website of BJPL and view the billing amount

31

and the due date Advance email intimation is also sent to the members Besides the billing

details can be viewed on the website upto a maximum period of 12 months

5 Adjustment against advances transaction charges In terms of the regulations members

are required to remit Rs50 000 as advance transaction charges on registration The

transaction charges due first will be adjusted against the advance transaction charges already

paid as advance and members need to pay transaction charges only after exhausting the

balance lying in advance transaction

6 Penalty for delayed payments If the transaction charges are not paid on or before the due

date a penal interest is levied as specified by the exchange

Finally the futures market is a zero sum game ie the total number of long in any contract

always equals the total number of short in any contract The total number of outstanding

contracts (long short) at any point in time is called the ldquoOpen interestrdquo This Open interest

figure is a good indicator of the liquidity in every contract

Regulatory framework

At present there are three tiers of regulations of forwardfutures trading system in India

namely government of India Forward Markets Commission (FMC) and commodity

exchanges The need for regulation arises on account of the fact that the benefits of futures

markets accrue in competitive conditions Proper regulation is needed to create competitive

conditions In the absence of regulation unscrupulous participants could use these leveraged

contracts for manipulating prices This could have undesirable in hence on the spot prices

thereby affecting interests of society at large Regulation is also needed to ensure that the

market has appropriate risk management system In the absence of such a system a major

default could create a chain reaction The resultant financial crisis in a futures market could

create systematic risk Regulation is also needed to ensure fairness and transparency in

trading clearing settlement and management of the exchange so as to protect and promote

the interest of various stakeholders particularly nonndashmember users of the market

Rules governing commodity derivatives exchanges

The trading of commodity derivatives on the NCDEX is regulated by Forward Markets

Commission (FMC) Under the Forward Contracts (Regulation) Act 1952 forward trading in

commodities notified under section 15 of the Act can be conducted only on the exchanges

which are granted recognition by the central government (Department of Consumer Affairs

Ministry of Consumer Affairs Food and Public Distribution) All the exchanges which deal

32

with forward contracts are required to obtain certificate of registration from the FMC

Besides they are subjected to various laws of the land like the Companies Act Stamp Act

Contracts Act Forward Commission (Regulation) Act and various other legislations which

impinge on their working

1 Limit on net open position as on the close of the trading hours Some times limit is also

imposed on intrandashday net open position The limit is imposed operatorndashwise and in some

cases also memberndash wise

2 Circuitndashfilters or limit on price actuations to allow cooling of market in the event of abrupt

upswing or downswing in prices

3 Special margin deposit to be collected on outstanding purchases or sales when price moves

up or down sharply above or below the previous day closing price By making further

purchasessales relatively costly the price rise or fall is sobered down This measure is

imposed only on the request of the exchange

4 Circuit breakers or minimummaximum prices These are prescribed to prevent futures

prices from falling below as rising above not warranted by prospective supply and demand

factors This measure is also imposed on the request of the exchanges

5 Skipping trading in certain derivatives of the contract closing the market for a specified

period and even closing out the contract These extreme measures are taken only in

emergency situations

Besides these regulatory measures the FC(R) Act provides that a clientrsquos position cannot be

appropriated by the member of the exchange except when a written consent is taken within

three days time The FMC is persuading increasing number of exchanges to switch over to

electronic trading clearing and settlement which is more customerndashfriendly The FMC has

also prescribed simultaneous reporting system for the exchanges following open outndashcry

system

These steps facilitate audit trail and make it difficult for the members to indulge in

malpractices like trading ahead of clients etc The FMC has also mandated all the exchanges

following open outcry system to display at a prominent place in exchange premises the

33

name address telephone number of the officer of the commission who can be contacted for

any grievance The website of the commission also has a provision for the customers to make

complaint and send comments and suggestions to the FMC Officers of the FMC have been

instructed to meet the members and clients on a random basis whenever they visit exchanges

to ascertain the situation on the ground instead of merely attending meetings of the board of

directors and holding discussions with the officendashbearers

Rules governing intermediaries

In addition to the provisions of the Forward Contracts (Regulation) Act 1952 and rules

framed there under exchanges are governed by its own rules and bye laws (approved by the

FMC) In this section we have brief look at the important regulations that govern NCDEX

For the sake of convenience these have been divided into two main divisions pertaining to

trading and clearing The detailed bye laws rules and regulations are available on the

NCDEX home page

Trading

The NCDEX provides an automated trading facility in all the commodities admitted for

dealings on the spot market and derivative market Trading on the exchange is allowed only

through approved workstation(s) located at locations for the office(s) of a trading member as

approved by the exchange If LAN or any other way to other workstations at any place

connects an approved workstation of a trading Member it shall require an approval of the

exchange

Each trading member is required to have a unique identification number which is provided by

the exchange and which will be used to log on (sign on) to the trading system A trading

ember has a non-exclusive permission to use the trading system as provided by the exchange

in the ordinary course of business as trading member He does not have any title rights or

interest whatsoever with respect to trading system its facilities software and the information

provided by the trading system

For the purpose of accessing the trading system the member will install and use equipment

and software as specified by the exchange at his own cost The exchange has the right to

inspect equipment and software used for the purposes of accessing the trading system at any

34

time The cost of the equipment and software supplied by the exchange installation and

maintenance of the equipment is borne by the trading member

Trading members and users

Trading members are entitled to appoint (subject to such terms and conditions as may be

specified by the relevant authority) from time to time -

1048576 Authorized persons

1048576 Approved users

Trading members have to pass a certification program which has been prescribed by the

exchange In case of trading members other than individuals or sole proprietorships such

certification program has to be passed by at least one of their directors employees partners

members of governing body Each trading member is permitted to appoint a certain number

of approved users as noticed from time to time by the exchange The appointment of

approved users is subject to the terms and conditions prescribed by the exchange Each

approved user is given a unique identification number through which he will have access to

the trading system An approved user can access the trading system through a password and

can change the password from time to time The trading member or its approved users are

required to maintain complete secrecy of its password Any trade or transaction done by use

of password of any approved user of the trading member will be binding on such trading

member Approved user shall be required to change his password at the end of the password

expiry period

Trading days

The exchange operates on all days except Saturday and Sunday and on holidays that it

declares from time to time Other than the regular trading hours trading members are

provided a facility to place orders off-line ie outside trading hours These are stored by the

system but get traded only once the market opens for trading on the following working day

The types of order books trade books price a limit matching rules and other parameters

pertaining to each or all of these sessions are specified by the exchange to the members via its

circulars or notices issued from time to time Members can place orders on the trading system

during these sessions within the regulations prescribed by the exchange as per these bye

laws rules and regulations from time to time

35

Trading hours and trading cycle

The exchange announces the normal trading hours open period in advance from time to time

In case necessary the exchange can extend or reduce the trading hours by notifying the

members Trading cycle for each commodity derivative contract has a standard period

during which it will be available for trading

Contract expiration

Derivatives contracts expire on a predetermined date and time up to which the contract is

available for trading This is notified by the exchange in advance The contract expiration

period will not exceed twelve months or as the exchange may specify from time to time

Trading parameters

The exchange from time to time specifies various trading parameters relating to the trading

system Every trading member is required to specify the buy or sell orders as either an open

order or a close order for derivatives contracts The exchange also prescribes different order

books that shall be maintained on the trading system and also specifies various conditions on

the order that will make it eligible to place it in those books

The exchange specifies the minimum disclosed quantity for orders that will be allowed for

each commodity derivatives contract It also prescribes the number of days after which Good

Till Cancelled orders will be cancelled by the system It specifies parameters like lot size in

which orders can be placed price steps in which orders shall be entered on the trading

system position limits in respect of each commodity etc

Failure of trading member terminal

In the event of failure of trading memberrsquos workstation and or the loss of access to the

trading system the exchange can at its discretion undertake to carry out on behalf of the

trading member the necessary functions which the trading member is eligible for Only

requests made in writing in a clear and precise manner by the trading member would be

considered The trading member is accountable for the functions executed by the exchange on

its behalf and has to indemnity the exchange against any losses or costs incurred by the

exchange

36

In the event of failure of trading memberrsquos workstation and or the loss of access to the

trading system the exchange can at its discretion undertake to carry out on behalf of the

trading member the necessary functions which the trading member is eligible for Only

requests made in writing in a clear and precise manner by the trading member would be

considered The trading member is accountable for the functions executed by the exchange on

its behalf and has to indemnity the exchange against any losses or costs incurred by the

exchange

Trade operations

Trading members have to ensure that appropriate confirmed order instructions are obtained

from the constituents before placement of an order on the system They have to keep relevant

records or documents concerning the order and trading system order number and copies of

the order confirmation slip modification slip must be made available to the constituents

The trading member has to disclose to the exchange at the time of order entry whether the

order is on his own account or on behalf of constituents and also specify orders for buy or sell

as open or close orders Trading members are solely responsible for the accuracy of details of

orders entered into the trading system including orders entered on behalf of their constituents

Trades generated on the system are irrevocable and `locked in The exchange specifies from

time to time the market types and the manner if any in which trade cancellation can be

effected Where a trade cancellation is permitted and trading member wishes to cancel a

trade it can be done only with the approval of the exchange

Margin requirements

Subject to the provisions as contained in the exchange byelaws and such other regulations as

may be in force every clearing member in respect of the trades in which he is party to has to

deposit a margin with exchange authorities

The exchange prescribes from time to time the commodities derivative contracts the

settlement periods and trade types for which margin would be attracted The exchange levies

initial margin on derivatives contracts using the concept of Value at Risk (VaR) or any other

concept as the exchange may decide from time to time The margin is charged so as to cover

one day loss that can be encountered on the position on 99 of the days Additional margins

may be levied for deliverable positions on the basis of VaR from the expiry of the contract

37

till the actual settlement date plus a mark Up for default The margin has to be deposited

with the exchange within the time notified by the exchange The exchange also prescribes

categories of securities that would be eligible for a margin deposit as well as the method of

valuation and amount of securities that would be required to be deposited against the margin

amount

The procedure for refund adjustment of margins is also specified by the exchange from time

to time The exchange can impose upon any particular trading member or category of trading

member any special or other margin requirement On failure to deposit margins as required

under this clause the exchangeclearing house can withdraw the trading facility of the trading

member After the pay-out the clearing house releases all margins

Margins for trading in futures

Margin is the deposit money that needs to be paid to buy or sell each contract The margin

required for a futures contract is better described as performance bond or good faith money

The margin levels are set by the exchanges based on volatility (market conditions) and can be

changed at any time The margin requirements for most futures contracts range from 2 to

15 of the value of the contract

In the futures market there are different types of margins that a trader has to maintain At

this stage we look at the types of margins as they apply on most futures exchanges

Initial margin The amount that must be deposited by a customer at the time of entering into