IN VESTO R P R E S E N TATIO N 1H 2016 FINANCIALRESULTS published on August24, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INVESTOR PRESENTATION

1H 2016 FINANCIAL RESULTS published on August 24, 2016

2

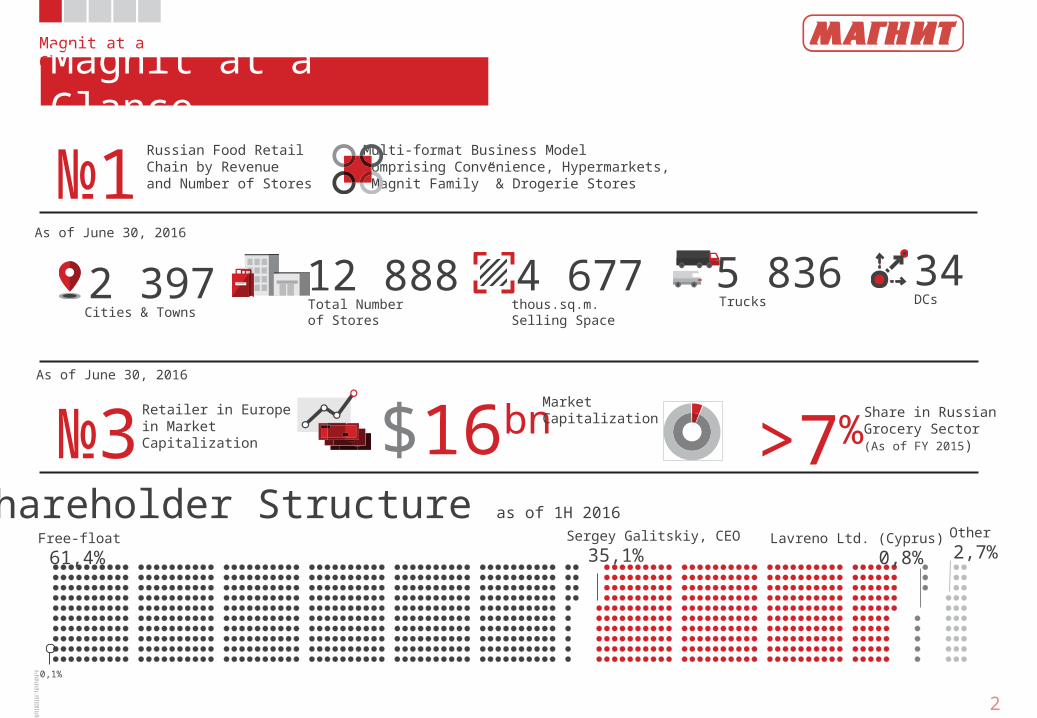

Magnit at a GlanceMagnit at a Glance

Source: Company, Thomson Reuters, Company’s calculations based on IFRS accounts for 1H2016

2 397Cities & Towns

№1Russian Food RetailChain by Revenueand Number of Stores

12 888Total Numberof Stores

4 677thous.sq.m.Selling Space

34DCs

5 836Trucks

Multi-format Business ModelComprising Convenience, Hypermarkets,“Magnit Family” & Drogerie Stores

№3Retailer in Europein MarketCapitalization $16bnMarket

Capitalization >7%Share in RussianGrocery Sector (As of FY 2015)

Shareholder Structure as of 1H 2016

61,4%Free-float

35,1%Sergey Galitskiy, CEO

0,8%Lavreno Ltd. (Cyprus)

0,1%

As of June 30, 2016

As of June 30, 2016

2,7%Other

Magnit at a GlanceKey Metrics

3

Source: Company’s estimates and calculations

522bn 14,7 %5,01%

NetMargin

9,89%

EBITDAMargin

1,1Net debt/LTM EBITDA

1000-1100 80 1200

P= Revenue growth Y-o-Y

Guidance for FY2016

Figures for 1H 2016

14-16%Sales Growth Rub

10-10,5%EBITDA Margin

67bnCapex Rub

New Convenience Stores

New Hypermarkets

New Drogerie Stores

4

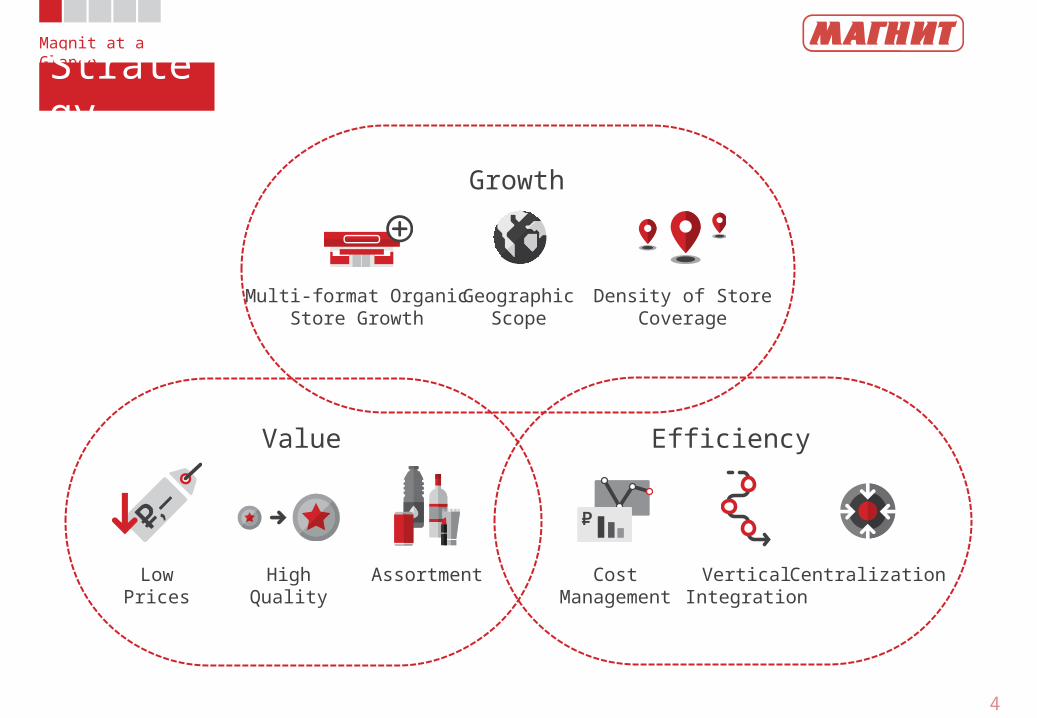

Magnit at a GlanceStrategy

Growth

Value Efficiency

Multi-format OrganicStore Growth

GeographicScope

Density of StoreCoverage

LowPrices

HighQuality

Assortment CostManagement

VerticalIntegration

Centralization

5

65

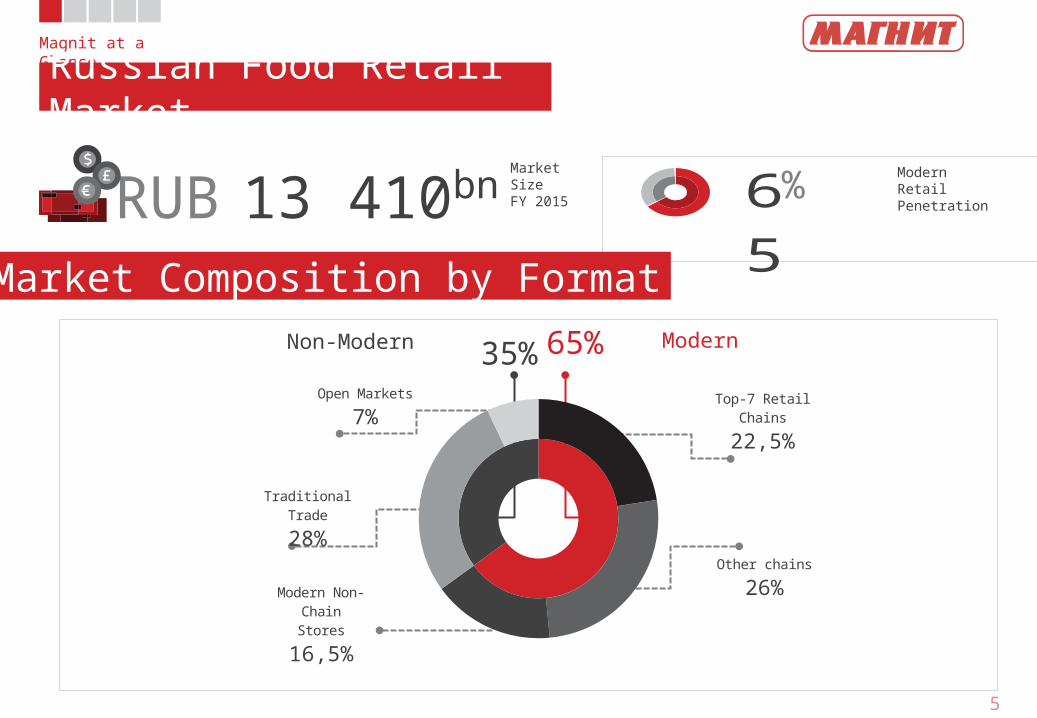

Magnit at a GlanceRussian Food Retail Market

Market Composition by FormatRUB 13 410bn Market

SizeFY 2015 % Modern

RetailPenetration

Non-Modern Modern

Source: INFOLine, as of December 31, 2015

65%

35%

Top-7 Retail Chains

22,5%

Modern Non-ChainStores

16,5%

Other chains26%

Traditional Trade28%

Open Markets7%

6

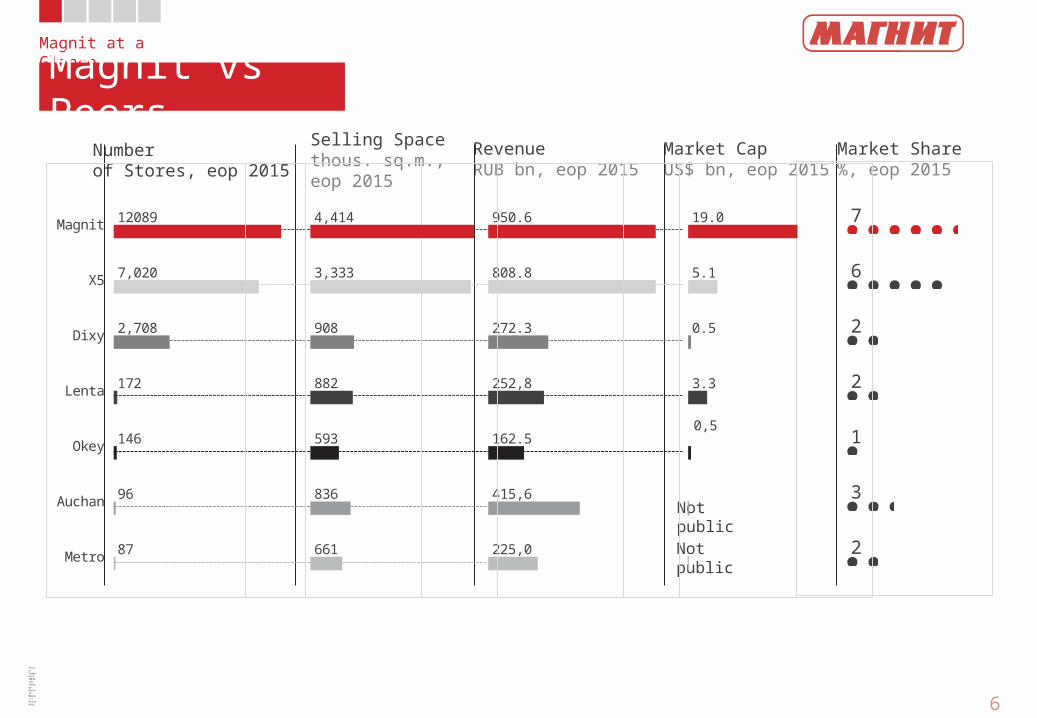

Magnit at a GlanceMagnit vs Peers

Source: Companies, INFOLine, Thomson Reuters, Magnit’s Estimates

Numberof Stores, eop 2015

Selling Spacethous. sq.m., eop 2015

RevenueRUB bn, eop 2015

Market CapUS$ bn, eop 2015

Market Share%, eop 2015

7

6

2

2

1

3

2

Not public

Not public

950.6

808.8

272.3

252,8

162.5

415,6

225,0

Magnit

X5

Dixy

Lenta

Okey

Auchan

Metro

12089

7,020

2,708

172

146

96

87

4,414

3,333

908

882

593

836

661

19.0

5.1

0.5

3.3

0,5

7

2 588Drogerie Stores 92 511 658 745 237 238107

9 902Convenience Stores

228Hypermarkets

170Magnit Family

34Distribution Centers

6 44 33 52 12 11

8 63 38 64 15 3010

3581684 2667 2961 972 895

365

Operational OverviewGeographical Coverage

Source: Company, as of June 30, 2016

2 397Cities& Towns

7 FederalRegions

North Caucasu

sSouthern Volga North

WestUrals SiberiaCentral

8 10 8 3

8

Operational OverviewLogistics System

Source: Company, as of June 30, 2016

12 888Total Numberof Stores

1 351thous.sq.m.Warehousing Space

34DCs

5 836Trucks

Central

Volga

Southern

Urals

North Caucasus

North West

Siberia

10

8

8

3

1

2

2

3684

3957

2293

1179

462

826

487

283,871

310,387

142,533

Centralization Ratio%

90

10

92

8

Convenience Stores

1H2016

73

27

80

20

HypermarketsDelivered from DC

Delivered from supplier

Delivered from DC

Delivered from supplier

9

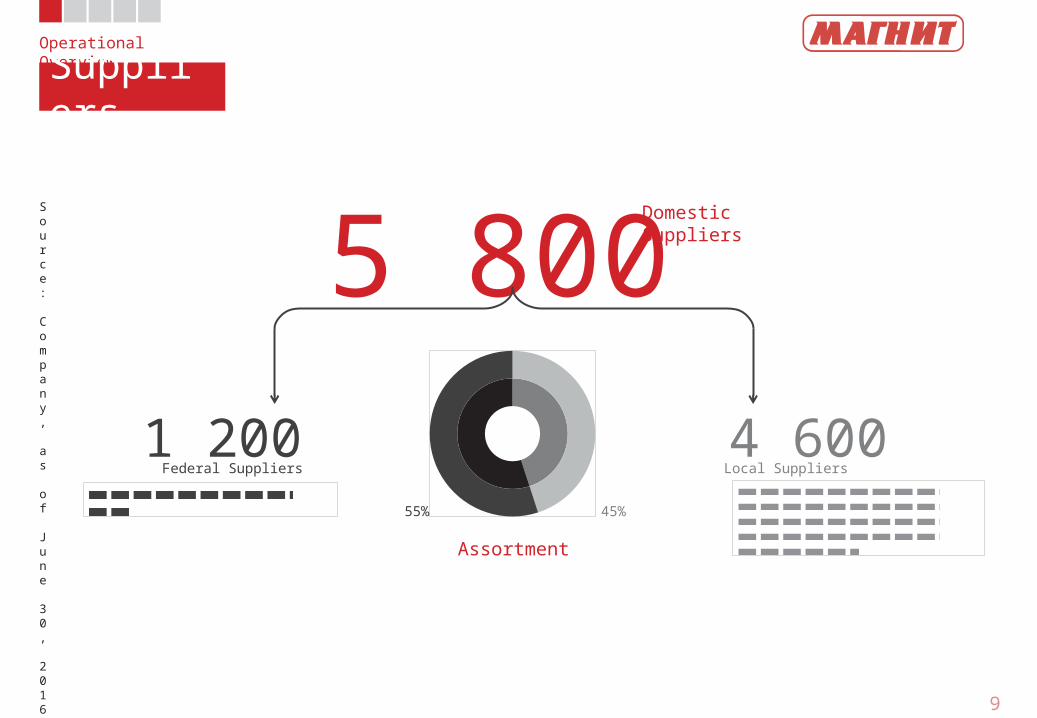

Operational OverviewSuppliers

Source: Company, as of June 30, 2016

5 800DomesticSuppliers

4 600Local Suppliers

1 200Federal Suppliers

Assortment55% 45%

10

Operational OverviewDirect Import

Source: Company, Direct Import – as of December 31, 2015; Private Label – as of June 30, 2016

11

% Shareof Revenue611PL

SKUsM 84% FoodItems

Private Label

9 % InternationalDirect Import 757Open

Contracts

11

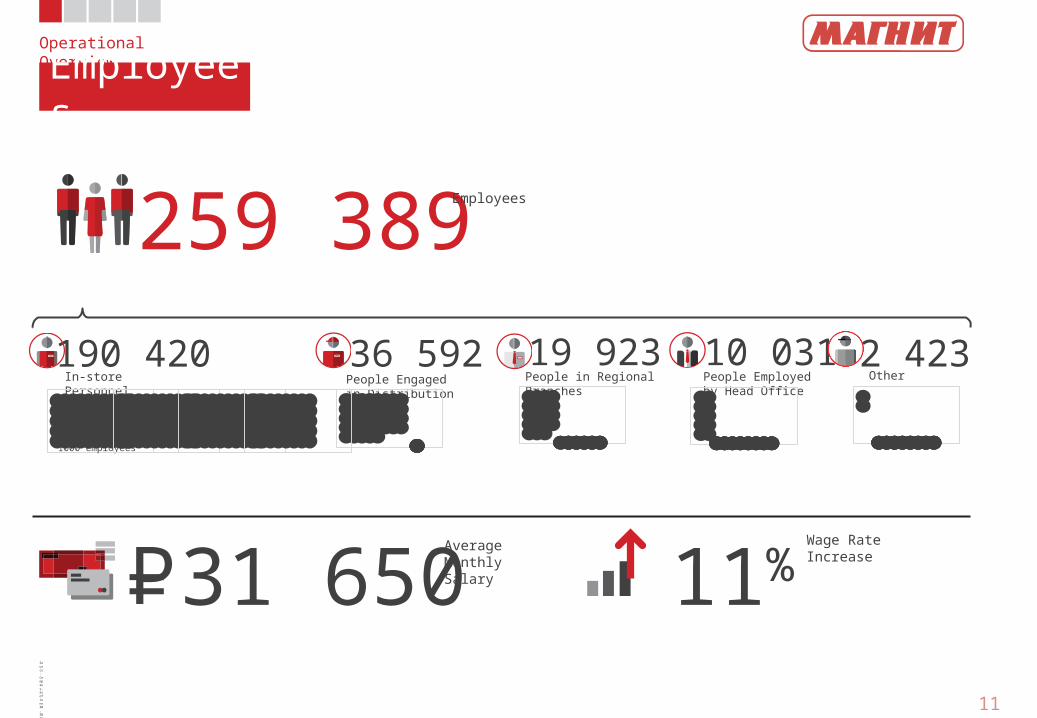

Operational OverviewEmployees

Source: Company, as of June 30, 2016

259 389Employees

31 650AverageMonthlySalary 11% Wage Rate

Increase P=

190 420In-storePersonnel

36 592People Engagedin Distribution

19 923People in RegionalBranches

10 031People Employedby Head Office

1000 employees

2 423Other

12

Operational OverviewCompetitive Attributes

43-45 % of FamilyBudgetSpent on Food

Location Quality(of Products)

Assortment Reliability AtmospherePrices

5 000 People —MinimumPopulation

(1 500–1 600 Families)

4 000-9 500 MonthlyFamily FoodBudgetP=

Overlap “Good”Cannibalization

Magnit #1

Magnit #2500m

Competitor #1 Competitor #2

Competitor #3

500m

Sales Catchment Area

Source: Company’s Estimates

Convenience Store

14

Operational OverviewConvenience Store

Source: Company, as of June 30, 2016

457

sq.m.Total

327

sq.m.Selling Space

89% Food

11% Non-food

25% Owned

75% Leased

Format Description Key Operational Statistics OpeningSize of the Store Average Ticket Payback

Store Ownership Structure

Sales MixTraffictickets/sq.m./day

Sales Densitysales/sq.m./year

LFL 1H2016 –1H2015,%

243,80P=$3,47

245 306P=$4 024

-0,36 AverageTicket, RUB

2,21 Traffic

1,85 Sales

2,7

3 years

If Leased

If Owned

Cost of New Storeper sq.m. of Total Space, thousand RUB

Time to Maturity

6 months

4-6 years

Owned 35-105Leased 10-19

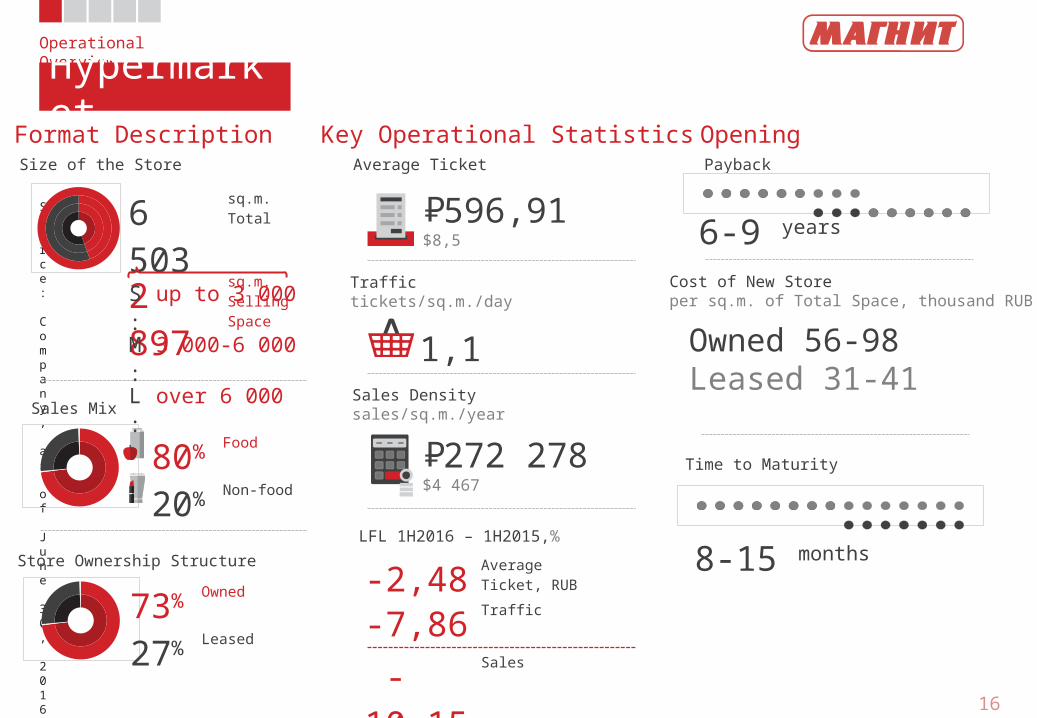

Hypermarket

16

Operational OverviewHypermarket

Source: Company, as of June 30, 2016

80% Food

20% Non-food

73% Owned

27% Leased

Format Description Key Operational StatisticsSize of the Store Average Ticket

Store Ownership Structure

Sales Mix

Traffictickets/sq.m./day

Sales Densitysales/sq.m./year

LFL 1H2016 – 1H2015,%

596,91P=$8,5

272 278P=$4 467

1,1

6 503

sq.m.Total

2 897

sq.m.Selling Space

-2,48 AverageTicket, RUB

-7,86 Traffic

-10,15

Sales

OpeningPayback

6-9 years

Cost of New Storeper sq.m. of Total Space, thousand RUB

Owned 56-98Leased 31-41

8-15 months

Time to Maturity

S: up to 3 000M:

3 000-6 000

L: over 6 000

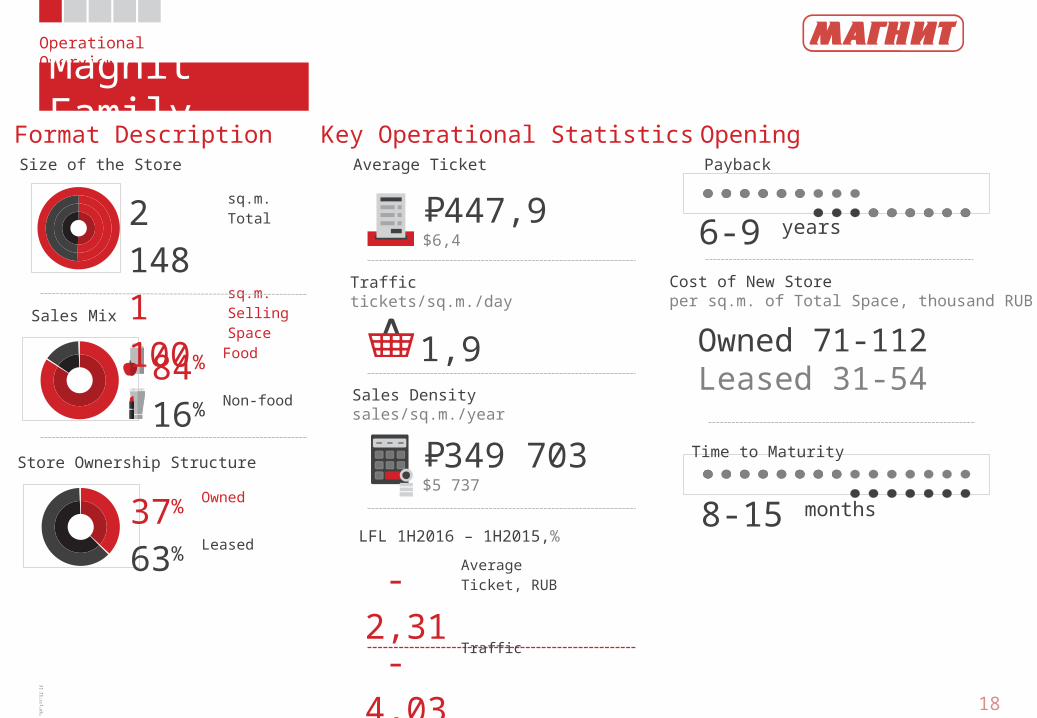

Magnit Family

18

Operational OverviewMagnit Family

Source: Company, as of June 30, 2016

2 148

sq.m.Total

1 100

sq.m.Selling Space

84% Food

16% Non-food

37% Owned

63% Leased

Format Description Key Operational Statistics OpeningSize of the Store Average Ticket Payback

Store Ownership Structure

Sales MixTraffictickets/sq.m./day

Sales Densitysales/sq.m./year

LFL 1H2016 – 1H2015,%

447,9P=$6,4

349 703P=$5 737

1,9

6-9 years

Cost of New Storeper sq.m. of Total Space, thousand RUB

Owned 71-112Leased 31-54

8-15 months

-2,31

AverageTicket, RUB

-4,03

Traffic

-6,25

Sales

Time to Maturity

Drogerie Store

20

Operational OverviewDrogerie Store

Source: Company, as of June 30, 2016

290

sq.m.Total

229

sq.m.Selling Space

100% Non-food

13% Owned

87% Leased

Format Description Key Operational Statistics OpeningSize of the Store Average Ticket Payback

Store Ownership Structure

Sales MixTraffictickets/sq.m./day

Sales Densitysales/sq.m./year

LFL 1H2016 – 1H2015,%

305,3P=$4,4

114 924P=$1 885

10,86

AverageTicket, RUB

-4,00 Traffic

6,42 Sales

0,9

3 years

If Leased

If Owned

Cost of New Storeper sq.m. of Total Space, thousand RUB

Time to Maturity

6 months

Owned 20-70Leased 9-16

4-6 years

21

80%20%

Sizeof the Store

sq.m.

AverageTicket

TrafficTickets/

sq.m./day

DensitySales/

sq.m./year

SalesMix

LFL 1H2016-1H2015

%

Store Owner-

ship Structure

PaybackYears

Cost of New Store

per sq.m.of Total Space

Timeto Maturity

Months

• Total• Selling Space

• Food• Non-food

• Av.ticket• Traffic/ Sales

• Owned• Leased

13%

87%

37%

63%

73%27%

25%75%

Operational OverviewFormat Summary

Source: Company, as of June 30, 2016; * Excludes selling space designated for leases

Hypermarket

DrogerieStore

MagnitFamily

327

2897*6 503

290

Owned RUB 35-

105kLeased

RUB 10-19k2,7

0,9

1,9

P.243,8$3,5

P.596,9$8,5

P.305,3$4,4

P.447,9$6,4

P.245 306$4 024

P.272 278$4 467

P. 114 924$1 885

P.349 703$5 737

89%11%

Conveniencestore

6

8-15

6

8-15

3 (if leased)

6-9

3 (if leased)

6-9

4-6 (if owned)

4-6 (if owned)

OwnedRUB 56-98k

LeasedRUB 31-41k

OwnedRUB 20-70k

LeasedRUB 9-16k

OwnedRUB 71-112k

LeasedRUB 31-54k8

4%16%

1

-0.36

-2.48

10.86

-2.31

2.21

-7.86

-4.00

-4.03

1.85

-10.15

6.42

-6.25

22

Financial OverviewSummary P&L

SG&A is presented net of Depreciation & Amortization (except for Depreciation of production fixed assets which was included in the Cost of sales)Source: Company’ s calculations based on IFRS accounts for 1H2015 – 1H2016Please note: there may be small variations in calculation of totals , subtotals, and/ or percentage change due to rounding of decimals

RUB MN 1H2015 1H2016 1H2015 / 1H2016Y-o-Y Growth

Net sales 454,808.63 521,527.57 14.7%

Cost of sales (327,748.22) (379,464.58) 15.8%

Gross profit 127,060.41 142,062.99 11.8%

Gross margin, % 27.94% 27.24%

SG&A (79,406.25) (92,661.97) 16.7%

Other income, net 937.45 2,138.69 128.1%

EBITDA 48,627.66 51,599.85 6.1%

EBITDA margin,% 10.69% 9.89%

Depreciation & Amortization (10,033.63) (12,101.38) 20.6%

EBIT 38,594.03 39,498.47 2.3%

Net finance costs (5,865.82) (6,853.38) 16.8%

Profit before tax 32,728.21 32,645.09 -0.3%

Taxes (7,462.55) (6,537.85) -12.4%

Effective tax rate 22.80% 20.03%

Net income 25,265.66 26,107.24 3.3%

Net margin, % 5.56% 5.01%

23

1H2014 1H2015 1H2016

2025 26

1H2014 1H2015 1H2016

349455 522

Financial OverviewRevenue & Costs

Source: Company’s calculations based on IFRS accounts for 1H2014-1H20161H2014 1H2015 1H2016

0

5

10

15

20

25

3027.8 27.9 27.2

10.5 10.7 9.9

5.6 5.6 5

Revenue DynamicsRUB bn

Net Income DynamicsRUB bn

Margin DynamicsSG&A Expense StructureRevenue — 522 RUB bn

GrossMargin

EBITDAMargin

NetMargin

%

+30,3%

11,5% -0,5%

+14,7%+29,0%

+3,3%

LFLLFL

Sales Growth, RUB

Sales Growth, RUB

2,07 (0,42) ― Packaging & Raw Materials1,84 (0,37) ― Repair & Maintenance

50,08 (10,05) ― Payroll & Related Taxes1,56 (0,31) ― Taxes, Other than Income Tax

11,50 (2,31) ― Deprecation & Amortization

25,81 (5,18) ― Rent & Utilities

3,00 (0,60) ― Other

in SG&A,% in Revenue, %

2,51 (0,50) ― Advertising

1,63 (0,33) ― Bank Services20%

104 703 RUB mn

24

GM1H2014

Trading Margin Transport Losses GM1H2015

Trading Margin Transport Losses GM1H2016

15171921232527293133

27.83 27.94 27.24-0.42 -0.11 -0.60 -0.160.64 0.06

Financial OverviewGross Margin Bridge

Source: Company’s calculations

EBITDA Margin Bridge

% of Sales

% of Sales

+11 b.p. -70 b.p.

+22 b.p. -80 b.p.

02468

1012 10.47 10.69 9.890.11 0.59 0.09

0.43 0.09 0.210.29 0.22 0.06 0.7 0.75 0.04 0.04

25

49,065

36,336

11,551

-5,777

-2,239-5,735 -4,755

-24 434

-351 -19 299

1 972

Financial OverviewFree Cash Flow

Source: Company’s calculations based on IFRS accounts for 1H2015-1H2016

Working Capital AnalysisThe Average Days Payable to Suppliers is 38 Days.

Inventory Management Days is 57 Days

Working Capital: RUB 34 258 mn as of 30.06.2016

RUB mn1H 2015

1H 2016

Adjusted for loss from disposal of PPE, provision for doubtful receivables, foreign exchange loss, gain on disposal of subsidiary Calculated as

additions + transfers of PP&E during the respective period

Does not include cash flow from financing activities

Adjusted

EBITDA

Change in

Working ca

pital

Net Interest

Expense Ta

xes

Paid OCF

Capex

Other Cash

Flow

from In

vesti

ng

Activit

iesFC

F

Paym

ent of D

ividents

Other Cash

Flow

from Fi

nancing

Activit

ies

CF

51,182

23,519

2,374

-3,505

-16,964

-6,796 -3,903 -21 018

-127 -20 982

15 102

26

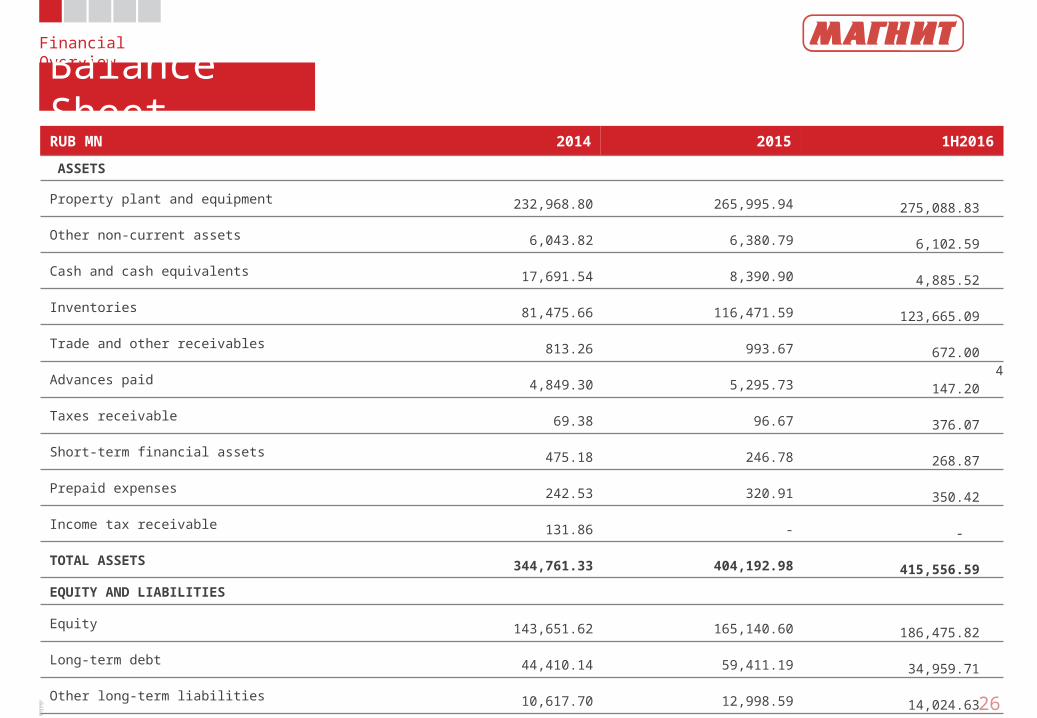

Financial OverviewBalance Sheet

Source: Company’ s calculations based on IFRS accounts for FY2014 - 1H2016Please note: there may be small variations in calculation of totals , subtotals, and/or percentage change due to rounding of decimals

RUB MN 2014 2015 1H2016 ASSETS Property plant and equipment 232,968.80 265,995.94 275,088.83 Other non-current assets 6,043.82 6,380.79 6,102.59 Cash and cash equivalents 17,691.54 8,390.90 4,885.52 Inventories 81,475.66 116,471.59 123,665.09 Trade and other receivables 813.26 993.67 672.00 Advances paid 4,849.30 5,295.73 4 147.20 Taxes receivable 69.38 96.67 376.07 Short-term financial assets 475.18 246.78 268.87 Prepaid expenses 242.53 320.91 350.42 Income tax receivable 131.86 - - TOTAL ASSETS 344,761.33 404,192.98 415,556.59 EQUITY AND LIABILITIES Equity 143,651.62 165,140.60 186,475.82 Long-term debt 44,410.14 59,411.19 34,959.71 Other long-term liabilities 10,617.70 12,998.59 14,024.63 Trade and other payables 66,794.61 88,372.22 73,498.37 Short-term debt 51,256.67 44,817.12 85,207.60 Dividends payable 14,372.03 16,993.86 7.10 Other current liabilities 13,658.56 16,459.40 21,383.36 TOTAL EQUITY AND LIABILITIES 344,761.33 404,192.98 415,556.59

27

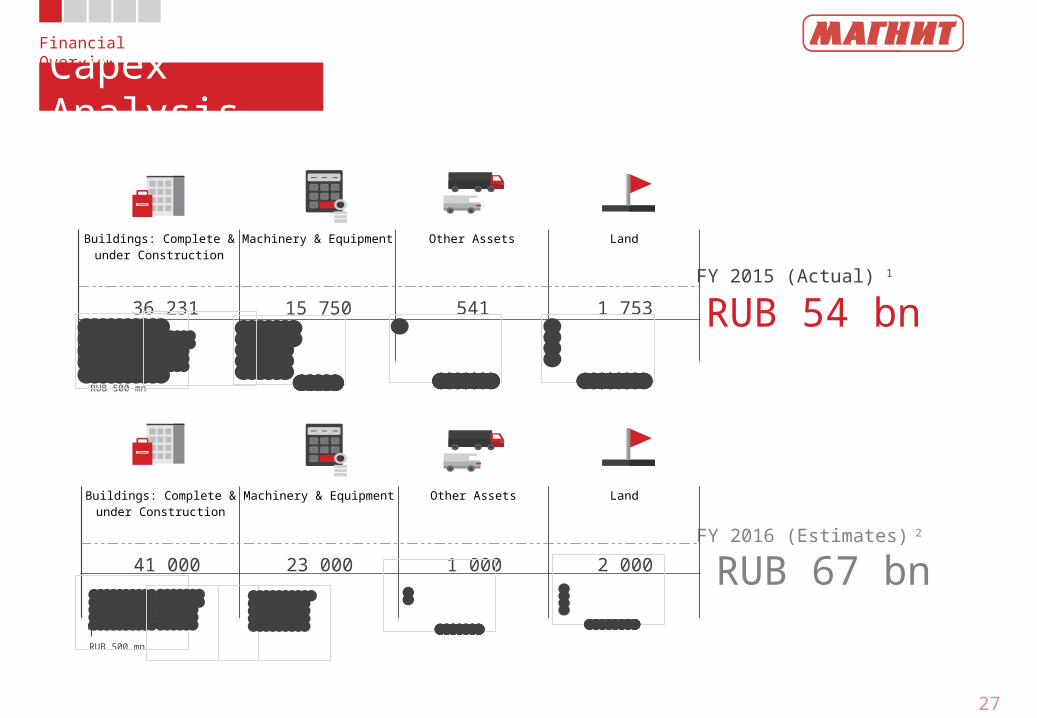

Financial OverviewCapex Analysis

1 CAPEX for 1H2016 amounts to RUB 21,018 mn2 Source: Company’s calculations based on IFRS accounts for FY2015, Company’s Estimates for FY2016

Buildings: Complete & under Construction

Machinery & Equipment Other Assets Land

36 231 15 750 541 1 753FY 2015 (Actual) 1

RUB 54 bn

FY 2016 (Estimates) 2

RUB 67 bn

RUB 500 mn

Buildings: Complete & under Construction

Machinery & Equipment Other Assets Land

41 000 23 000 1 000 2 000

RUB 500 mn

Source: Company’s calculations based on IFRS accounts for FY2014-1H2016 28

2014 2015 1H2016

95,667104,228

120,167

77,975

95,837

115,28244,410 59,411 34,960

Net DebtLong-term Debt%

Financial OverviewDebt Burden

2014 2015 1H20160.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0 12.9

8.77.5

2014 2015 1H20160

0.5

1

1.5

2

0.9 0.91.1

Debt Level Dynamics RUB mn

Credit Metrics Credit ProfileEBITDA / Finance Expenses

Net Debt / LTM EBITDA

The Company Hasan Impeccable Credit HistoryCollaboration withthe Largest BanksLow Debt Burden:Net Debt / LTM EBITDA Ratio of 1,1

No Currency Risk: 100%of Debt is Rub DenominatedMatching Revenue StructureInsignificant Interest Rate Risk:Interest Payments are Madeat Fixed Rates Primarily

53,6%43,0%

70,9%

29% of Debt is Long-termApproximately 59%of LT Debt is Rub Bonds

29

Contact InformationContact InformationTimothy PostHead of Investor Relations

+7 (961) [email protected]://ir.magnit.com

15/2 Solnechnaya StreetKrasnodar, 350072Russian Federation

Related Documents