Raising issues in emerging markets Inspiring reading on Responsible Investment from GES ® TWENTY years in uncharted waters Sustainable stock exchanges unchain financial markets ESG A share of the price – page 22 Investors highlight hidden conflict – page 34 Forgotten Europe in shade of crisis 2012 GES 1992-2012

mag.e.sine 2012

Mar 30, 2016

Inspiring reading on Responsible Investment from GES

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3 • MAG•E•SINE 2012 MAG•E•SINE 2012 • 3

Raising issues in emerging markets

I n s p i r i n g r e a d i n g o n R e s p o n s i b l e I n v e s t m e n t f r o m G E S ®

TWENTY yearsin uncharted waters

Sustainable stock exchanges unchain financial markets

ESG

A share of the price – page 22 Investors highlight hidden conflict – page 34

Forgotten Europe in shade of crisis

2012

GES 1992-2012

Preparing to celebrate GES’ 20th anniversary in 2012, the words of Danish philosopher Søren Kierkegaard crossed our minds: “Life can only be understood backwards, but it must be lived forwards.” For 20 years, we have merely kept our eyes on the horizon, navigating towards sustain-ability in what often felt like completely uncharted waters. GES’ anniversary provided a natural moment to lock back, not only at our own company his-tory but also at the history of Responsible Investment, two timelines that are occasionally intertwined in a way that we are proud and honoured of. And which may offer some guidance for the future route for anyone sailing in these waters, please see page 18.

When we started in 1992, Responsible Investment (RI) was almost per-ceived as a contradiction in itself (as well as our first company name Caring Capitalism). Today RI is well established and focus has shifted from ethical criteria and exclusion of companies to integration of ESG (environmental, social, governance) issues and engagement.

Therefore, we also find it an excellent timing to change our company name again – or more of refining it, in order to keep on signalling our forward-looking ambition. Thus, GES Investment Services is shortened to GES®, standing for Global Engagement Services which is our core business today and where we believe the future of RI is.

We hope you will find this magazine inspiring and that our paths will cross at some point.

Best regards,GES’ Team

Most of GES’ staff from four offices gathered at annual conference in September 2011 in Tenna, Switzerland.

34

20 Years1 9 9 2 - 2 0 1 2

4

26

MAG•E•SINE 2012 • 3

Raising ESG issues in emerging markets 4

Slowly taking the fast lane to Russian companies 11

Sustainable stock exchanges unchain financial markets 12

“Warsaw Stock Exchange educates Polish companies in CSR” 16

Twenty years in uncharted waters 18

A share of the price 22

“Engagement needs to be researched” 24

Forgotten Europe burgeons in shade of crisis 26

Sustainability part of the Megatrends investment compass 32

Investors highlight hidden conflict 34

Tax havens a rising challenge 38

contents

Magesine is produced by GES in cooperation with AD Reklambyrå. Publisher: Susanne Nyman. Cover: Energy Complex Building in Bangkok, Thailand. Photo: Palle Ellemann. Print: Centraltryckeriet Linköping, certified according to the official Nordic Ecolabel. Paper: Tom&Otto Gloss 250 g and Tom&Otto Silk 130 g, both certified according to the Forest Stewardship Council (FSC).

18

GES Kungsgatan 35, 111 56 Stockholm, Sweden

Phone +46 8 787 99 10

GES DenmarkVestergade 27, 1456 Copenhagen K, Denmark

Phone +45 30 86 03 70

GES PolandUl. Sikorskiego 27, 65-454 Zielona Gora, Poland

Phone +48 68 320 06 84

GES Switzerland Lavaterstrasse 75, 8002 Zurich, Switzerland

Phone +41 43 535 99 38

www.ges-invest.com

“The wind has turned and way-farers in Responsible Investment may today navigate along a steadier course aided by beacons from early explorers of these un-charted waters.”

Credit Suisse’ 3 Megatrends

32

22

4 • MAG•E•SINE 2012

Raising

issues in emerging markets

ESG

By Erik Alhøj, Managing Director, and Palle Ellemann,

Senior Consultant, GES Denmark

Not all rosy but with large potential for finan-cial returns, GES conducts engagement with emerging market companies based on a new concept developed together with Danish client Sydinvest. For many companies it is their first investor meeting ever on environmental, social and governance (ESG) issues.

While Europe and the US are struggling with his-torical financial and economic problems, the pic-ture is more promising for the emerging markets. Despite the negative global impact from the ongoing European debt crisis, investing in emerging market equities has given the best return to investors on all assets, except for gold, during the past ten years. And all the top ten fastest growing economies in the com-ing years are emerging market economies.

Many institutional investors, however, still consider the emerging economies significantly more risky to invest in than the developed economies. One reason

GES Denmark’s Managing Director Erik Alhøj in front of Energy Complex Building in Bangkok, Thailand, headquarters of PTT Exploration as well as the Ministry of Production and Energy.

MAG•E•SINE 2012 • 5

“We believe that emerging market investments will increase, also in the long term, because this is where the future growth potential is. With this trend, ESG will play a significant role.”

Niels Skovvart, Director at Sydinvest

is the relatively high risk related to ESG issues like bribery and corruption, pollution, child labour and dependent board members. These non-financial risks are more likely to materialise in the emerging econo-mies and the companies are generally less prepared to handle them in a constructive and transparent way.

But things are changing. Many emerging market companies are in the process of establishing policies, management and reporting systems for ESG issues. And they can be influenced in a very constructive way to build stronger ESG preparedness through active engagement from international institutional investors that own shares in the companies.

This is the starting point for an emerging market engagement project that GES has developed together with the Danish asset manager Sydinvest, who is one of the leading specialists in Denmark regarding emerg-ing market investing.

“The collaboration with GES has given us a unique insight to the challenges that emerging market com-panies are facing with regards to ESG. GES provides an up-to-date overview of the individual companies’ preparedness to handle these challenges. The input is important for our risk management of ESG issues on emerging markets”, says Niels Skovvart, Director at Sydinvest.

6 • MAG•E•SINE 2012

The emerging market engagement project started in 2009 with a portfolio of about 100 MSCI companies in Africa and the Middle East. It was later expanded to cover all Sydinvest’s four emerging market funds: Sydinvest Africa & Middle East, Sydinvest BRIC, Sydinvest Far East and Sydinvest Latin America. This portfolio of about 500 companies covers about half the total universe of large MSCI emerging market com-panies.

During the past 18 months, GES has visited about 80 companies in ten countries from these investor portfolios. Meetings have taken place in Mainland

China, Hong Kong, South East Asia, India, Mexico, Brazil, Egypt, South Africa and Russia. The compa-nies include some of the leading players in a variety of industries, such as mining, energy, food production, electronics and construction.

For many of these companies this has been the first investor meeting, where ESG issues have been dis-cussed in a constructive way. There are enormous differ-ences in the ESG preparedness and performance, but the vast majority appreciates the dialogue and shows sincere interest in improving and taking advantage of the input from the investor perspective.

Engagement tours around the world. Left and top right photos show Palle Ellemann, Senior Consultant at GES Denmark, overviewing Cape Town, South Africa. Right bottom photo is from Tiananmen Square, Beijing, China.

MAG•E•SINE 2012 • 7

Eleven per cent of the companies in the emerging market portfolios are committed to the UN Global Compact’s ten principles on environment, human rights and corruption, and 23 per cent comply (at least to some extent) with the Global Reporting Initiative’s (GRI) voluntary guidelines for sustainability reporting.

ESG reporting is a key challenge for most emerging market companies and the face-to-face meetings reveal always – without exceptions – new ESG information not published on the website or in the annual reports. It is not rare that sustainability reports are not trans-lated into English; this is particularly seen in China.

83 per cent of the emerging market companies publish information about corporate governance issues, which is often a requirement from local authorities or strong-ly encouraged by the local stock exchanges. The picture is completely different when it comes to other ESG information, where 72 per cent publish no or very little information on environmental issues and 76 per cent publish no or very little information on social issues.

As global investments are increasingly flowing into emerging markets in search for the best return, this is positive news for the economic and social development of these economies but it is not an endeavour with-

Left: Malaysia’s capital Kuala Lumpur reaching for the sky. Right: GES visiting the Malaysian Stock Exchange.

out pitfalls and risks. Investors face a greater risk for losing the investment, because the market and regula-tory conditions can be unstable and there is a general challenge with lack of information and transparency about companies in the emerging markets. GES Risk Rating finds that about 35 per cent of the companies in emerging markets have an engagement challenge in terms of violations of international norms and conven-tions and/or a very low preparedness to handle high potential environmental and social risks.

GES supports investors in taking advantage of the opportunity in emerging market investments by addressing three main objectives with its ten-step emerging market engagement model (see next page):

1) Investors are provided with a comprehensive as-sessment of the most important ESG risks and the individual companies preparedness to handle these.

2) The assessment is used to identify the com-panies with the highest potential ESG risks and engage proactively and constructively with these companies to develop a more responsible and sustainable business approach. When the en-gagement effort succeeds and the companies build stronger ESG preparedness and perfor-mance, the financial risk-premium can be re-duced and the share price will increase to the benefit of the investor and the company.

3) Working to improve companies’ ESG performance with proactive engagement gives the investor a “license to operate” from its most important stake- holders.

Engagement results can be achieved with a consistent and collaborative approach, where the assessment must be based on a deep understanding of risk and prepared-ness on all levels – countries, industries and the market situation for specific companies. The ESG risks related to emerging market companies come from a variety of factors that investors have to take into account. 29 per cent of the emerging mar-ket companies analysed are located in countries with authoritarian regimes such as China and the Gulf countries. 66 per cent are located in countries with a high level of bribery and corruption, while 43 per cent are located in countries with a high environmental risk. Five per cent are located in countries with a high risk when it comes to peace and security.

The second layer of contextual risk is related to the industries where the companies in the emerging mar-ket portfolio operate. Mining and energy exploration are very important industries in many emerging mar-kets, but these industries also represent the highest potential environmental risks. Therefore, it is key for investors to consistently assess the mining and energy companies’ ESG preparedness and performance in order to manage the risks and select those companies with the lowest probability of experiencing major envi-ronmental incidents.

With regards to social issues, textile and food produc-tion shows a significant high potential risk. The Chi-nese milk scandal, where infant milk powder had been contaminated with the non-alimentary chemical melamine and led to the death of six infants and left about 300,000 people ill, is a clear example of a poten-tial risk materialising with a fatal result.

A significant part of the risk identified analysis is simply related to lack of information. About three out of four companies in the emerging market portfolios publish no or very little information on environmental and so-cial issues. In some cases it is a low-hanging fruit just to make sure that the companies report consistently about the policies, programs and systems in place for ESG, because this transparency is contributing to reducing the risks assessed by investors. Additionally, consistent disclosure is creating accountability and helping com-panies to identify opportunities for improvement and setting goals for future performance.

The best ESG preparedness is found in industries like paper and forestry, metals and mining, and energy, which corresponds with the industries with the highest potential environmental risks. On the other hand, the lowest ESG preparedness is found in industries like services, textiles, transportation and real estate.

From a geographical perspective, the Taiwanese com-panies in the emerging market portfolios tend to have the best environmental preparedness followed by companies in South Africa, Korea and India. Brazil, Mexico and other Latin American countries also have an environmental preparedness above average. In the opposite end of the scale, Nigerian and other African companies (except South Africa) tend to have the low-est environmental preparedness. Singaporean, Chinese and Middle East companies are also below average on environmental preparedness.

Continues on page 10.

8 • MAG•E•SINE 2012

MAG•E•SINE 2012 • 9

1. Screening for weapons - based on the GES Controversial screening model

2. Screening for ESG incidents - associations with violations of UN Global Compact prin-ciples, documented by GES Global Ethical Standard screening model

3. Rating of potential industry ESG risks - based on the GES Risk Rating model

4. Rating of the potential country risk - regarding democratic rights, civil liberties, bribery and corruption

5. Rating of the most material potential ESG Risks - based on GRI, Eurosif, IFC, etc.

6. Rating of the potential information risk regarding ESG - based on the GES Risk Rating model

7. Rating of the company preparedness and performance on ESG - based on the GES Risk Rating model

8. Rating of the engagement challenge - identifying the most important companies to influence

9. Active engagement - towards companies, associated with the highest potential ESG risk

10. Rating of Engagement Response - quality of the answer to GES’ dialogue efforts

10 steps for emerging market engagement

In August 2010, GES met with Fertilizantes Heringer for the first time in Sao Paolo, Brazil. The company is involved in the production, marketing and distribution of agricultural, macro-nutrients and micronutrients fertilizers under the Heringer brand name. As a relatively newly listed company (IPO in 2007), it had never encountered investors or analysts requiring information about ESG before and the Investor Relations officer could not provide GES with many answers to the questions about ESG. As a company in the chemical industry on an emerging market with low ESG preparedness, Fertilizantes Heringer was in the red box of the GES Risk Rating. However, the IR Officer brought the issue to the manage-ment of the company and then things started to develop quickly. Since the first meeting, GES has followed up with conference calls every six months with the company and today Fertilizantes

Heringer is no-longer a company scared of questions regard-ing ESG. The company acknowledges that it is still in an early phase of building a solid ESG preparedness and performance, but it has taken a very structured approach to working with ESG and the company is setting ambitious short and long-term goals. In the short term, the company intends to sign the UN Global Compact and the long-term goal is to join the Bovespa Sustain-ability Index. Additionally, Fertilizantes Heringer plans to report according to the Global Reporting Initiative. According to the company, working systematically with ESG and sustainability has had several positive effects, e.g. that large corporate clients have started commenting positively upon the development and it has been significantly easier for the company to obtain export loans from the financial sector due to the improved ESG profile.

Fertilizantes Heringer builds ESG preparedness

GES Risk Rating on Social Issues

Example of how GES rates a portfolio of 96 emerging market com-panies for preparedness and potential risks with regards to social issues like occupational health and safety, supply chain management, impact on the community, bribery and corruption. The companies in the top right and red corner with the high potential risk and the low preparedness are the target group for engagement. In the emerging market portfolios about 25 per cent of the companies fall into the red box for both the environmental as well as the social issues.

Since personal meetings are a distinguishing feature of GES’ engagement activities, a lot of resources are invested in visiting the companies. During the conver-sations and meetings, GES builds a relationship that allows us to ask the tough questions and respectfully offer advice and suggestions for improvements from an investor perspective. Draft meeting minutes are always shared with the company after the meetings. GES keeps the dialogue going with the company every six months with follow-up conference calls or visits.

The picture of conducting engagement on emerging markets is not all rosy. It takes hard work and persis-tency just to establish the dialogue with the companies, who often react with hesitation and suspicion to the meeting request. And some companies simply ignore or refuse the invitation for a dialogue. For the compa-nies not willing to engage into a dialogue, GES takes further steps of engagement to influence the direction of the company by e.g. :

• Contacting and possibly meeting top manage-ment/board members;

• Initiating/supporting/coordinating proxy voting and/or resolution with investor clients at annual general meeting;

• Bringing the case to UN PRI Clearinghouse in order to generate a stronger and more collective investor pressure.

But in most cases, the companies welcome the dialogue and the constructive feedback on how to improve the ESG preparedness and performance after the initial suspicion has been eliminated. The regular follow-ups contribute to building trust and lead to more open discussions on ESG challenges and solutions.

“We believe that emerging market investments will in-crease, also in the long term, because this is where the future growth potential is. With this trend, ESG will play a significant role,” says Niels Skovvart.

23 24

6 28

HIG

HS

TNR

DLO

W

HIGH STANDARD LOW

7 8

PO

TEN

TIAL R

ISK

PREPAREDNESS

10 • MAG•E•SINE 2012

11 • MAG•E•SINE 2012 MAG•E•SINE 2012 • 11

“Preparing for an engagement tour to Russia in December 2011, I reflected upon how very close Russia seems to be to us, but on the other hand quite far away. You cannot just buy a ticket and go to Russia, since there are a number of administrative obstacles.

To receive an entry visa, you need to prepare all docu-ments required, such as an invitation, special insur-ance accepted by Russian authorities, visa application filled in only with black ball pen and then apply for the visa in person or via an agent at the Russian embassy. Therefore, you should be very patient while waiting and be prepared for that you might not be able to travel to Russia in the exact time you planned.

Furthermore, arranging meetings with Russian com-panies was not as easy as I had expected. Many emails sent, follow-up calls with explanations of who we are,

why we want to meet, what we would like to ask. Very often the companies were concerned to meet with us, since they did not have any formal policies regarding environmental, social and governance (ESG) issues. Due to that, I had to be very tactful to convince them that the main purpose of the meeting is not to judge them but to learn about their opinion on Corporate Social Responsibility (CSR) and future plans regard-ing this issue.

After all, the companies appeared to be very open for a dialogue with us and showed some interest in imple-menting ESG issues into their operations. In many cases we found out that the companies are aware that CSR is becoming increasingly significant for the glob-al economy and that they are willing to comply with international standards to meet investors’ demands.

What might be surprising is that communication in English was not a problem. However, it was very use-ful for me to know the local language, especially when we had to get to the companies’ headquarters, pass the security control or move by public transport. Due to heavy traffic in Moscow, where there are about four million cars on the streets, it was much faster to get to the meeting by subway instead of taxi. Unfortunately, metro is not so friendly for foreigners, since all signs are written in Cyrillic.

In general, GES’ engagement tour opened doors for us that I hope will help us continue our dialogue with the companies in order to support them in developing ESG programmes and policies.”

slowly Taking the fast lane to Russian companiesBy Paulina Kurkiewicz, Research Analyst at GES Poland

Research Analyst Paulina Kurkiewicz from GES Poland at Red Square in Moscow.

Sustainable stock exchanges unchain financial

markets

While the “Occupy Wall Street” movement has attracted massive attention for its protests outside stock exchanges all over the world, it is less well known that another movement towards more responsible business practices is already on its way inside some of these buildings. And emerging markets are paving the way.

12 • MAG•E•SINE 2012

By Fredric Nyström, Engagement Coordinator and Key Account Manager at GES

MAG•E•SINE 2012 • 13

Financial markets have great transformational power to accelerate the transition towards more sustain-able business practices and value creation. The basic hypothesis behind the powerful trend of Responsible Investment is that environmental, social and gover-nance (ESG) factors in an economy, sector or com-pany, play an increasingly important part in enhancing or eroding shareholder value through good corporate governance. Responsible investment is slowly but surely rising up the agenda of other stakeholders who play a key role in shaping the investment climate: leg-

islators, policy-makers, regulators, multilateral agencies and the professional bodies that set accounting and auditing standards.

Some of the more important actors in this develop-ment are the stock exchanges – the actual place where buyers and sellers meet. In 2008, members of the World Federation of Exchanges (WFE) transacted over USD 80 trillion, connecting thousands of in-vestors and companies. Through their listing require-ments, stock exchanges can affect some of the busi-ness operations and practices of the companies that seek to use the exchange as a forum to access capital from global retail and institutional investors. There is an increased awareness among exchange management that exchanges do have a responsibility to encourage greater corporate responsibility on sustainability issues and many have already begun to implement initia-tives. These range from the introduction of sustainable investment indexes to listing requirements demanding sustainability reporting.

Whilst understanding the limitations of mandate and scope of the exchanges to assess materiality of ESG risk for its listed entities, there is still potential

for exchanges to do more, including strengthening requirements for general ESG reporting and, poten-tially, introducing requirements for a forward-looking non-binding shareholder resolution on sustainability strategy at the annual general meeting. Many stock exchanges have taken innovative steps to anticipate and respond to these new opportunities, both as regulatory bodies as well as trading platforms. However, there is a gap between the good examples and the less good ones.

What a stock exchange can do:• Facilitate that the market efficiently meets the

new ESG-related information needs of investors, analysts and companies;

• Introduce investors and issuers to one another on the theme of sustainability excellence;

• Raise ESG awareness and standards among listed companies by introducing additional listing requirements;

• Promote good corporate governance;• Promote good ESG disclosure;• Create trading products geared to specific sustain-

able investment niches.

By addressing environmental and social aspects in their operations, corporations can reduce risks and costs as well as better take advantage of and develop business opportunities. Thus, addressing these issues contrib-utes to the sustainable value creation that investors see as fundamental to the future financial return. Listing requirements are the set of conditions imposed by a stock exchange upon companies that want to be listed on that exchange. Such conditions sometimes include minimum number of shares outstanding, minimum market capitalisation and minimum annual income. There are, though, several examples from different parts of the world where exchanges enhance those criteria to include even ESG. It is important to stress that these requirements are currently introduced on a comply-or-explain basis, but it is reasonable to believe that this will shift toward mandatory requirements as time changes. Companies from the western hemisphere are com-peting in increasingly global markets, not least with companies from the emerging economies of the “new world”. This competition is growing ever tougher, and there are signs that Europe is beginning to fall behind. Many of the CSR/ESG initiatives by stock exchanges we are seeing around the world are initi-

Fredric Nyström, Engagement Coordinator and Key Account Manager at GES, takes a new perspective on Wall Street, New York.

14 • MAG•E•SINE 2012

ated by exchanges in emerging markets. In addition to the highlighted examples (next page) from the stock exchanges in Malaysia, Australia and South Africa, the stock exchanges in Mexico, Colombia and Singapore shall also be mentioned. This development means that global investors in the long run will be more interested in emerging market companies since they will eventu-ally be well-run with better corporate governance than their western peers. It would not be surprising if, with

in five-ten years, companies in the West and the US will be overtaken by emerging markets companies when it comes to CSR and top of the line corporate governance. This thesis is supported by a study from GES in September 2010. The reason is that many exchanges in emerging markets today require or are working actively to promote CSR and ESG disclosure through listing requirements and the like.

The increased sustainability awareness among interna-tional stock exchanges has to been seen in the light of the balancing they have to do between attracting new companies and new listing requirements. Increased requirements might keep companies away from the exchanges and they will to a larger extent seek new capital outside the exchanges. This is already a reality in Europe and the US where introductions on the stock exchanges have decreased over the last ten years. The overarching social role that the exchanges have to play is to supply growing companies with capital. Compa-nies that grow contribute to a higher degree of employ-ment and increased economic welfare. During the sec-ond half of the 20th century many of the multinational companies with the most well known brands have been living in symbiosis with the exchanges that have pro-vided them with capital and made it possible for them to conquer the world, with increased economic welfare

as a positive consequence. So, stock exchanges that do not play an active role in the society might in the future play a peripheral role, which will hurt the economic development.

What is there to do for an investor? Many of the stock exchanges are by themselves listed entities; therefore, asset owners and managers could and should have a constructive dialogue with managers at the stock

exchanges in which they are invested around issues of long-termism, business model and competitive pres-sure. Institutional investors can through active engage-ment with stock exchanges on issues of sustainability increase transparency and ESG disclosure by corpora-tions, and hence improve the investable environment.

Stock exchanges that do not play an active role in the society might in the future play a peripheral role, which will hurt the economic development.

It would not be surprising if, within five-ten years, companies in the West and the US will be overtaken by emerging markets companies when it comes to CSR and top of the line corporate governance. This thesis is supported by a study from GES in September 2010.

15 • MAG•E•SINE 2012

Examples of stock exchange initiatives within sustainability:

MalaysiaMalaysian public listed companies are required to include a description of the CSR activities or practices undertaken, on a comply-or-explain basis. The requirement is an extension of the CSR Framework for voluntary reporting launched in 2006. The framework, focusing on four dimensions: marketplace, workplace, environment and community, is a guide for companies to understand and implement CSR into their business operations and encourage reporting. The framework aims primarily to maintain market integrity and inves-tor protection. Bursa Malaysia places a strong emphasis on CSR in its own business and is proactive in raising CSR standards in Malaysia’s public listed companies.

South AfricaThe First King Report on Corporate Governance was published in 1994 by the Insti-tute of Directors in response to the increasing concern over corporate failures and the perceived need for a formal code of corporate governance. The First King Report sought to assist companies and their directors by providing a comprehensive set of principles and guidelines to codify, clarify and (in certain circumstances) expand upon the common law principles of corporate governance. The King Code requires the board to act in the best interest of the company and to act as a focal point for and custodian of corporate gover-nance by ensuring that the company is a responsible corporate citizen and is perceived as such, acknowledging that strategy, risk, performance and sustainability are inseparable. The listing requirements of the Johannesburg Stock Exchange have since a number of years been amended to mandate compliance with the First King Code. The corporate governance code based on the King Report asks the entities for integrated reporting, meaning that the compulsory reporting should convey adequate information regarding the company’s financial and sustainability performance.

AustraliaThe listing rules at the Australian Securities Exchange require companies to disclose, on a comply-or-explain basis, to which extent the company has followed the recommendations set by the ASX Corporate Governance Council. Environmental and sustainability risks are factors that are recommended for considerations. Each company need to determine the material business risks it faces. A company shall not only take into account its legal obli-gation but also consider reasonable expectations of its stakeholders. Companies should establish policies for the oversight and management of material business risks and dis-close a summary of those policies.

GES Risk Rating* for Bursa Malaysia:E b- (c+)S c+ (c+)G a- (a-)

GES Risk Rating* for Australian Securities Exchange:E c+ (c+)S c+ (c+)G a (a-)

GES Risk Rating* for Johannesburg Stock Exchange:E b- (c+)S b- (c+)G a- (a-)

* GES Risk Rating assesses the company’s preparedness and performance on environmental, social and governance (ESG) issues, with “a” being top-rating and “c-” being the poorest. Here, the rating of the company operating the exchange is compared with the industry average of the world’s twelve leading stock exchange operators, indicated within parenthesis.

Bursa Malaysia

Johannesburg Stock Exchange

Australian Securities Exchange

MAG•E•SINE 2012 • 15

Phot

o Lai

Sen

g Sin

/Sca

npix

Phot

o Sip

hiw

e Sib

eko/

Reu

ters/S

canp

ix

Phot

o Will

iam

West

/AFP

/Sca

npix

16 • MAG•E•SINE 2012

“Warsaw Stock Exchange educates POLISH COMPANIES IN CSR”Five questions to Tomasz Wiśniewski, Chairman of the Warsaw Stock Exchange (WSE) Index Committee, which in 2009 launched the first index of responsible and sustainable companies in Central-Eastern Europe, the RESPECT index.

Tomasz Wiśniewski, Chairman of the Warsaw Stock Exchange Index Committee

MAG•E•SINE 2012 • 17

By Martin Pitura, Managing Director of GES Poland

1. Why does WSE provide a sustainability index?The RESPECT Index project has two main objectives. The first is to attract the investors’ attention to the com-panies in the index and to encourage them to take the environmental, social and governance (ESG) criteria into account in their investment decisions. The second objective is to motivate companies to become more involved in Corporate Social Responsibility (CSR) by identifying leaders in the areas examined.

2. What response have you received since start?After three editions of the RESPECT Index, I find a noticeable increase in Polish companies’ activity in the areas of CSR and I believe that this is partly a result of the educational role of the index. In financial terms, it shows a higher return rate than other indices. At the end of 2011, the index had risen by 23.02 per cent since it was launched in November 2009.

3. Do you have plans for further development?Producing the latest edition of the index, we conducted the first research in Poland addressed at institutional investors in order to diagnose the level of account-ability of ESG factors in investment decisions. We plan to repeat this research in the middle of 2012. We also intend to conduct workshops aimed at analysts, to bring them closer to the subject of CSR and ESG factors.

4. What are the biggest challenges for you to continue with this?The biggest challenge is building the awareness and the education process in CSR and SRI (Socially Respon-sible Investment) in Poland. Unfortunately, our market still lacks the companies that conduct CSR activities on a regular and effective basis.

5. How would you predict the status of sustainability issues on the WSE in ten years?The high standards of corporate governance create a strong foundation for the development of SRI in Poland. Recent years have shown that also other ESG factors are increasingly being taken into account in institutions’ and individual parties’ investment deci-sions. With a continued promotion from e.g. the RESPECT Index and the Polish Ministry of Econ-omy’s assigned working groups* for SRI and CSR, I hope that in coming years all these initiatives will bring us closer to the level of countries such as France, the Netherlands or Denmark. * Including representatives from e.g. Warsaw Stock Exchange and GES Poland.

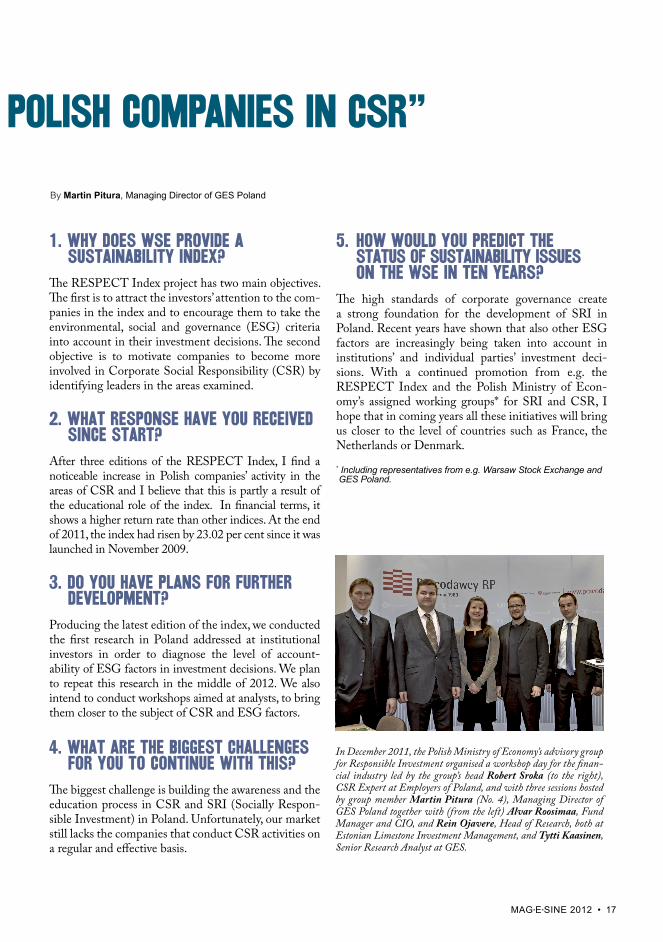

In December 2011, the Polish Ministry of Economy’s advisory group for Responsible Investment organised a workshop day for the finan-cial industry led by the group’s head Robert Sroka (to the right), CSR Expert at Employers of Poland, and with three sessions hosted by group member Martin Pitura (No. 4), Managing Director of GES Poland together with (from the left) Alvar Roosimaa, Fund Manager and CIO, and Rein Ojavere, Head of Research, both at Estonian Limestone Investment Management, and Tytti Kaasinen, Senior Research Analyst at GES.

“Warsaw Stock Exchange educates POLISH COMPANIES IN CSR”

18 • MAG•E•SINE 2012

twenty years in

By Susanne Nyman, Founder and Communications Director of GES

UNCHARTED WATERSThe wind has turned and wayfarers in Responsible Investment may today navigate along a steadier course aided by beacons from early explorers of these uncharted waters. GES has plotted some of the ground gained during its 20 years of sailing, which provides an indispensable guide for the financial industry’s future route.

MAG•E•SINE 2012 • 19

Early exploration within what we today call Responsible Investment (RI) started long time ago; many refer to the US Quakers as the first

explorers. They practiced RI as early as in the 16th century, based on their beliefs in human equality and nonviolence. And in the 18th century, John Wesley, a Church of England cleric and founder of the Methodist movement, outlined his basic tenets of RI: not to harm your neighbour through your business practices and to avoid industries like tanning and chemical production, which can harm the health of workers.

However, people have always discussed what is right and wrong with regards to ownership, so in that aspect there is nothing new under the sun. Historically, dis-cussions used to concern physical ownership of land, estate, cattle, etc., like in the examples above. But the new thing is that it today concerns an abstract share ownership that has become very large and widespread among both institutions and individuals.

During the latest two decades, excursions in RI have intensified tremendously and spread all over the world, thereby conquering new territory and drawing a more comprehensive map. GES has identified some of the most important stages of this voyage, both internal and external, occasionally intertwined, see foldout chart on the next page. A mapping exercise well worth doing and sharing, believes Magnus Furugård, Founder and President of GES:

“Looking backwards like this, it is encouraging to dis-cover what can be achieved in the long term although you sometimes do not see it in your everyday work. And for your future navigation it is invaluable, since you have to know where you come from in order to lay out a reli-able course. We are honoured of having sailed these wa-ters with so many visionary pioneers. Some are unfortu-nately not with us anymore - like Dame Anita Roddick, Founder of The Body Shop, and Joan Bavaria, Founder of Trillium Asset Management and environmental coalition CERES - but they have left clear cardinal marks for others to follow. And we do hope for more companions since a constantly updated chart is to the benefit of all wayfarers.”

Taking an overall view of the development the last 20 years, three main stages can be distinguished: steered by consumers until the mid ’90s, jointly by companies and consumers until the early ’00s and then increasingly also by investors.

In the early-mid ’90s, the development of envi-ronmental and social responsibility was mainly driv-en by consumer activism, occasionally quite stormy with boycotts and campaigns. These were sparked by media revelations but also by NGOs and other entities

20 • MAG•E•SINE 2012

gathering information about companies like Interfaith Center on Corporate Responsibility and Council on Economic Priorities. As the targets were often com-panies within food and commodities, these naturally were among the first to act by developing policies and experimenting with social audits. This paved the way for the development of structured business information necessary for investors to be able to act later on.

Two of the most highlighted boycotts were directed against Shell for its plans to sink the outdated Brent Spar oil plat-form in the North Sea and for alleged association to the Ni-gerian military regime’s ex-ecution of environmental activist Ken Saro Viwa. Not only did it make Shell ad-dress environmental and so-cial responsibility, but subse-quently also numerous other international companies that still today refer to these boy-cotts as a wake-up call for business in general.

“The big hurdle for active consumers during this era was the limited range of choice and price; there were very few alternatives to conventional products and those available were very expensive,” recalls Magnus Furugård.

“Companies’ major problem was that they did not have control of their supply chains and were often fooled by contractors who e.g. hid child labour when controls occurred. The companies realised they had to build their own administration for control but this was not easy since it threatened to increase costs. There was also a general lack of knowledge and awareness within the companies’ organisations regarding social issues and thus they could not see how to integrate them with ex-isting goals. Independent certification companies could

not assist them either as they did not have the compe-tence to assure quality in such immaterial aspects.”

In the late ’90s, more companies started to realise that they had to extend the environmental responsi-bility many had started to take in the 80’s to include social aspects. The initial motive to satisfy stakehold-ers matured into an understanding of the embedded risks and opportunities and how proactive conscious-ness could be made a competitive advantage. However, there were big variations in the terminology – business ethics, corporate social responsibility (CSR), corporate citizenship, etc. – as well as in the interpretation of what this responsibility included and thus an increas-ing demand for an international benchmark, which

the establishment of the UN Global Com-pact and its principles for environment, labour and human rights be-came an answer to.

A breakthrough for RI came around the millennium shift, when political initiatives in several countries turned the focus towards investment. The UK government piloted this development by making it mandatory for pen-sion funds to disclose if they had an investment policy including ethical,

social or environmental considerations. Although it did not oblige them to adopt such a policy, the req-uisite to state whether or not they had one, made the possible lack obvious and consequently increased de-mand for RI services.

During the early ’00s, investors increasingly joined forces in voting on environmental and social share-holder resolutions, especially in the US, as well as in initiatives like the Institutional Investors Group on Climate Change (2001) and the Equator Principles (2003), developed by private sector banks.

“The new law requirements in various countries made asset owners and pension funds explore how they could apply this on all of their operations, instead of just a small part as previously. The value-driven criteria that had dominated the market so far became

GES’ Founders Magnus Furugård and Susanne Nyman in Bay of Kotor, Montenegro, and Stockholm archipelago, Sweden.

A big challenge for the financial industry at this time – which partly remains today - was that they did not have the knowledge and competence for RI internally, often re-sulting in price being more important than quality in purchase of services.

MAG•E•SINE 2012 • 21

less attractive, because these were not universal among people and meant excluding entire industries. Instead of this absolute view on what was responsible, RI took on a more relative view making UN Global Compact’s principles a universal basis for criteria. Some also start-ed to explore if there was a financial link,” comments Magnus Furugård.

As RI became an integrated part of investors’ whole operations, quality demand on analysis increased; investors had to be accountable both towards their clients and towards the companies. To address the need to “watch the watch dogs”, a number of initiatives were taken. For instance, the Swedish Foundation for Strategic Environmental Research, Mistra, published an annual evaluation of service providers and some of these started the development of a Voluntary Quality Stan-dard for Sustainability and Responsibility Research.

At the same time criticism accumulated against the increased anonymous institutional ownership, which allegedly failed to take responsibility. Even large inves-tors realised that they were too small to have an impact on their own and therefore started to collaborate.

“A big challenge for the financial industry at this time – which partly remains today - was that they did not have the knowledge and competence for RI inter-nally, often resulting in price being more important than quality in purchase of services. Another hurdle was that the way portfolio managers worked was hard to combine with RI considerations. They saw it as sole-ly cost creating, not income driving. A third challenge for investors was - and still is - to make a long-term commitment,” says Magnus Furugård.

In the mid-late ’00s, RI entered the main fairway when the UN Principles for Responsible Investment (PRI) attracted a large number of signatories from the financial industry. The acronym ESG (environmen-tal, social and governance) became the new compass together with company engagement, thereby mov-ing away from exclusion strategies. The BP disaster in the Mexican Gulf in April 2010 brought ESG risks to the attention of mainstream investors, as well as the Japanese nuclear disaster in March 2011. corpo-rate governance became more closely linked to the E and S and the overall concept of RI, when excessive bonuses caused uproar and the financial crisis emerged. Politicians became increasingly active in regulation efforts and the European Commission prepared to present a “legislative proposal” on corporate disclosure of extra-financial information in the first half of 2012…

“The massive adherence to PRI created a common platform for all investors and service providers which is a major success, however the latest development of making PRI a corporation and deleting its UN link changes the relationship for investors since it is not independent or universal anymore,” comments Magnus Furugård.

Nevertheless, it is quite clear that integration of ESG in financial analysis and integration of engagement in ownership responsibility will be a natural part of the financial industry’s future route. But in the horizon Magnus Furugård spots three major challenges:

“One big challenge lies in handling extractive industries. It is not a sustainable business, but cannot be avoided since they often generate large returns. All exploitation of natural resources that are limited - fossile fuels, land, water, etc. - will oblige the inves-tor to make sure that investments are sustainable and responsible.”

“Investors should also keep an eye on the issues of democracy and freedom of speech. We have only seen the start of a democratisation of the world: in the Arab region, Burma, Latin America, Russia, ex-Soviet states. It will be extremely important for companies to navigate right and act responsibly in these instable markets and for investors to be informed of their operations.”

“Finally, the harsh upwind of the financial crisis might turn into a favourable downwind for RI since it has made many realise that the solution lies within sustainable, responsible and long-term investment. But to reach this, it is very important that the world’s decision makers aim for the same waypoints at the 20th anniversary of the UN Earth Summit in Rio de Janeiro on June 20-22, 2012. They agreed on quite good documents in 1992, so now it is a matter of imple-mentation. For this, we need good governance on both political and investor level and it would be most benefi-cial if the conference could come up with some strong incitements for this.”

The harsh upwind from the financial crisis might turn into a more favourable down-wind for RI since it has made many realise that the solution lies within sustainable, responsible and long-term investment.

UK think tank and consultancy SustainAbility introduces the term Triple Bottom Line, thereby wid-ening corporations’ traditional focus on performance to include environmental, social and financial aspects.

• ProducesthefirstSwedishSocialAuditforCSRpioneerandretailerICA–Fokus.

• Ethical fundmanager Working Assets enters Inc. magazine’s list of 500 fastest-growing US compa-nies, success partly built on client activism towards companies.

• StudytourforIKEAtosub-suppliersinIndia,Ne-pal andPakistan aftermedia revelations aboutchildlabourintherugindustry,resultingincom-panywidesocialresponsibilitycommitment.

• Internationalbusinessleaders’ network Caux Round Table launches the world’s first ethical business code “Principles for Business”.

• RenamedCaringCompany,startsfirstNordiccommercial newsletter on business ethics,Etik&Affärer,andco-foundsGlobalPartnersfor Corporate Responsibility Research withe.g.CEP.

• Starbucksbreaksice in coffee and agricultural industry by adopting a code of conduct on work-ing conditions for growers.

• IntroducesFairTradeconceptinSwedenwithcoffeeindustryreportfortheSwedishSocietyforNatureConservation.

• Right Livelihood Award (“Alternative Nobel Prize”) granted to US-based Council on Economic Priorities (CEP) for groundbreaking consumer information on company ethics, e.g. bestseller “Shopping for a better world”.

• ProducessectorreportforSwedishCoopontheenvi-ronmentalandsocialimpactsofthecoffeeindustry.

• LeviStrauss&Co. follows the examples of Nike and Reebok in 1992 by developing first code of conduct in its industry, and further demonstrates its commitment by discontinuing working with contractors in China and Burma because of human rights violations.

• Co-founds Social Venture Network (SVN) EuropeandSwedish business network FSA, FöretagmedSocialtAnsvar,inspiredbye.g.SVN.

• Two pioneers in CSR develop audits with measur-able indicators: Ben & Jerry’s presents a Social Report developed by New Economics Foundation (UK); The Body Shop presents “The Values Report”, weighing a couple of kilos and consisting of several booklets includ-ing environmental, social and animal rights reports.

• Screening assignment for first Swedish ethicalfundwithhumanandlabourrightscriteria,WASA U-hjälpsfond,lateracquiredbyLänsförsäkringar.

• Tobacco divestment wave among US state pension funds and unparalleled USD368.5 bil-lion settlement after claims from around 20 states against tobacco companies for compen-sation for health care.

• SA8000labourstandard launched by Council on Economic Priorities (CEP), developed with its partner CaringCompany and IKEA in reference group.

•OECDaddsenvironment, labour and human rights to updated Guide-lines for Multinational Enterprises.

• Australiaintroduceslaw for all fund providers to state if they have an ethical policy or not, and explicitly on labour conditions.

• FoundationofAsRia, The Association for Sustainable & Responsible Investment in Asia.

• OpensDanishofficeandsetsupengagementserviceGESActiveforSwedishnationalpensionfundAP1.

• Auniqueconstellation of six Swedish NGOs and Danske Bank start Humanix index funds with sharpened environmental, social and ethical criteria, screened by CaringCompany.

• UKimplements new law for pension funds to disclose if they consider ethical, social or environmental issues in their invest-ments. France and Germany adopt similar laws, while Swe-den makes it mandatory for national pension funds to take environmental and ethical considerations into account.

• GlobalReportingInitiative (GRI) releases first full version of voluntary guidelines for sustainability reporting.

• Co-founds global SiRi Group (Sustainable Investment ResearchInternational),abusinesscollaborationbetweenelevenleadingcompanies.

• Shell’s social report “Profits and principles – does there have to be a choice” marks a turn point in stake-holder dialogue after massive boycotts.

•Assists Swedish KPA Pension with integrationof environmental and social responsibility in all operations, includingcapitalmanagement, therebybecomingfirstpensioncompanyofferingonlyethi-calinvestments.

• USSecurities and Exchange Commission (SEC) re-tracts criticised “Cracker Barrel rule”, which since 1992 had disallowed shareholder resolutions on labour issues.

•ConsultedbytheSwedishParliamentaryCommitteeonFinanceoninternationalpracticeofintegrationofenvironmentalandsocialissuesininvestments.

•UNestablishesGlobalCompact to gather companies’ sup-port for nine principles on environment, labour and human rights. (Corruption principle added in 2004.)

•CaliforniaPublicEmployeesRetirementSystem, CalPers, begins to support labour resolutions aside from traditional corporate governance resolutions.

•Submits proposal to UK Social Investment Forum - togetherwithotherScandinavianmembers-toformEuro-peanSIF,resultinginfoundationofEurosifin2001.

20 milestones for Responsible Investment (and GES)

• UNEarthSummit in Rio calls for an expanded perspective on environmental issues - “sustain-ability” - which also includes social issues. • Company founded asCaringCapitalism -nameinspiredbythephilosophyofUSicecreammakerBen&Jerry’sHomemadeInc.,apioneerinsocialentrepreneurship.

1992

1995

1996

1997

1998

1999

2000

2001

19931994•

MAG•E•SINE 2012 • 2

• UN Convention against Corruption becomes the first legally binding international anti- corruption instrument.

• Advances norm-based screening serviceGlobalEthicalStandard®intomarketleader.

• UN sets up The Kimberley Process, a certi-fication scheme aiming to prevent so-called blood diamonds, fuelling conflict in West Africa, from entering the mainstream market.

• RenamedGESInvestmentServices.

•UNlaunchesthePrinciples for Responsible Invest-ment, PRI, which advocates engagement as a key method/tool.

• Engagement success with Marriott regardingpreventionofchildsextourism.

• AwardedbriefbySwedishFirst-FourthAPfunds’newjointEthicalCouncilforscreeningandcoor-dinationofengagementactivities.

• TheKyotoProtocol to the UN Framework Convention on Climate Change enters into force.• EUproclaims2005 “the European year of CSR” setting off a

four-year campaign to build partnerships between companies, investors, governments and civil society.

• EngagementsuccesswithCoca-Colainturn-aroundcaseonlabourconditionsinColombia.

• SetsupGESEngagementForum,anunprecedentedclientinterfaceforactiveownership.

• UNGlobalCompact and UN Environment Programme launch “Caring for Climate” aimed at advancing the role of business in addressing climate change.

• Sets upBurmaEngagement Service on demandfromtheChurchofSwedenandpensioninsurancecompaniesFolksam(Sweden)andKLP(Norway).

•Rio+20-UnitedNationsConference on Sustainable Develop-ment and 20th anniversary of first Earth Summit in Rio.

• Celebrates 20th anniversary and presentsmajor upgradetoGESEngagementForum3.0,introducinga360companyperspective.

• OECDupdates Guidelines for Multinational Enterprises with tougher standards on e.g. remuneration, human rights abuse and company re-sponsibility for supply chains.

• WinsIPE-TBLIESGLeadersAwardfor“BestESGconsulting/researchhouse”basedone.g.“itsuniqueandnoteworthyclient-focusedplat-formGESEngagementForum”.

• Polishgovernmentpresents a series of recommendations from its advi-sory group on Responsible Investment, including GES, on how to promote this development in Poland.

• Rio+10, UN Earth Summit in Johannesburg, enlarges target group from producers and consumers to investors.

• Recordsupportfor environmental and social resolutions at US AGMs: 16 resolutions to 14 companies were supported by 18,9-34 percent. Climate change emerging hot issue. Increasing support from public pension funds.

• Co-founds European Corporate Governance Service(ECGS)togetherwithfiveotherresearchcompanies.

• EuropeanVoluntaryQualityStandard for Sustainability and Responsibility Research certifies first seven research groups, including GES.

• OpensSwissoffice.• UNClimateChangeConference in Copenhagen fails to reach

a global agreement on CO2 reductions, but sparks off several investor initiatives around the world calling on and committing to higher ambitions.

• Presents study identifyingmajor opportunities in climate engagementwithrealestate.

2009

• Norwegianparliamentadopts ethical invest-ment guidelines for the Petroleum fund.

•EstablishesPolishoffice.

• AdoptionofConvention on Cluster Munitions impels pension funds, particularly government-sponsored schemes, to exclude companies linked to the manufacture of cluster bombs.

• USSIF and investors establish Emerging Markets Disclosure Project to assess and improve corporate environmental, social and governance reporting in emerging markets.

•EngagementsuccesseswithGoldcorpregardinghumanrightsinGuatemalaandwithSodexoconcerninginhumaneconditionsfordetainees.

•CoordinatesnewNordicEngagementCooperation(NEC)betweenpensioninsurancecompaniesFolksam(Sweden),Ilmarinen(Finland)andKLP(Norway).

• NorwegianGovernmentPensionFund adopts new en-gagement guidelines moving away from criticised exclu-sion strategy, in order to enhance its shareholder influence.

• EngagementsuccesswithG4Sonlabourrights.• UK’sFinancialReportingCouncil presents Stewardship

Code for institutional investors, encouraging them to e.g. disclose voting policies and report on voting.

• Extends engagement services to voting and local expertiseinAsiabyformingstrategicpartnershipswithManifestandSIRIS.

2012

2003

2007

2002

2006

2005

2004

2010

2008

2011

22 • MAG•E•SINE 2012

SIRP (Sustainable Investment Research Platform) started in 2006, funded by Mistra (the Foundation for Strategic Environmental Research in Sweden), and involves fifteen European universities and research institutions lead by Professor Lars Hassel at Umeå School of Business in Sweden. The program’s objective is “to find out how sustainable investment practices can create added value for institutional investors and iden-tify barriers to mainstreaming such practices”.

Based on data from e.g. GES, SIRP has conducted about ten studies within the research area Sustain-able investments and markets. Another 15 projects have been conducted within the research areas Sus-tainable companies and ratings, Incentive systems and Fiduciary responsibility. Although the studies within investments vary a lot in choice of topic and method, they can roughly be grouped into three main sub areas: Value relevance studies, Incident studies and Portfolio studies (see fact box on page 14).

Focusing on the first category, Natalia Semenova, post-doctoral researcher and lecturer in accounting at Åbo Akademi University in Finland, conducted different aspects of Value relevance studies for her doctoral dis-sertation in June 2011. Thereby she could sum up six years of research by concluding:

“Contemporary research provides evidence that environmental and some dimensions of social performance - supplier and community rela-tions - are valued by the stock market beyond financial fundamentals in annual accounts. In general, there is a positive but weak price premium, but the varying results indicate there might be a price dif-ference depending on company size and industry.”

This inspired Natalia Semenova to further inves-tigate the asymmetry in pricing on environmental performance. She chose the E focus “because the ef-fect of environmental performance is more industry-specific when comparing with the reputational effect of reporting, which is independent of industry risk. And GES Risk Rating data allows differentiating these effects on market value”.

a share of the price – ESG found to be part of stock market value

Albert Einstein may have been right saying: “Not everything that counts can be counted, and not everything that can be counted counts”. But in order to spur the increasing inter-est in Responsible Investment, academic researchers within the SIRP program have spent six years to search for evidence that company management of environmental, social and governance (ESG) issues is rewarded by the financial markets. And they have found some, but to various degrees.

By Susanne Nyman, Communications Director of GES

Natalia Semenova, postdoctoral re-searcher and lecturer in accounting at Åbo Akademi University, Finland

MAG•E•SINE 2012 • 23

The results were presented in a separate working paper to the PRI Academic Network conference in Sigtuna, Swe-den, in September 2011, highlighting three main findings:

1) A stronger positive relation for large and mid-sized companies in low-risk industries.

2) A less strong but positive relation for large and mid-sized companies in medium-risk industries.

3) A strong negative relation for large and mid-sized companies in high-risk, more regulated industries.

The first-mentioned positive finding supports the so-called Porter hypothesis on the business value of beyond-compliance environmental performance: In low risk industries with lower environmental regula-tion, such as CO2 tax, there is more room for voluntary corporate responsibility that seems to pay-off. If a large company is less financially constrained, especially in markets less influenced by regulation, this adds further to its market value in a positive way.

Finding No. 3 on a negative relation surprised Nata-lia Semenova most. Obviously, the capital markets are more likely to monitor environmental performance in polluting industries that have more frequent nega-

tive events (environmental incidents) and are subject to specific environmental legislative actions (costly sanctions, penalties or taxes). But it would be very discouraging if for example an oil company puts efforts in improving its environmental performance and then is “punished” with a lower market value. On the other hand, an ESG leader in high impact industries has to be profitable which can indicate that voluntary over-spending in corporate responsibility is costly and not rewarded by the market.

Natalia Semenova thinks further research might add some nuances to this contradictory conclusion:

“It would be interesting to study what effect changes in environmental performance, rather than explicit levels of it, have on market value. Constant improvements could be valued differently than one time efforts to raise a company’s environmental standards.”

Another factor of importance for the pricing is risk. Environmental leaders show lower credit risks and higher credit ratings. Lenders seem to consider environmental performance in their decisions because it can reduce regulatory and reputational risks steaming from costly future shocks such as sanctions and scan-dals. Therefore, the environmental leaders are expected

Research by SIRP provides evidence that the financial markets are learning to price ESG factors.

24 • MAG•E•SINE 2012

to pay lower interest rates on their bank loans and to receive higher credit standings, irrespective of industry.

Also, environmental leaders show lower cost of equity capital or return required by shareholders. As a result, they can increase market value by a lower rate of return or discount rate that investors apply to their expected future earnings. For example, if a company by investing in environmental performance reduces the probability of an environmental incident, then a reduced risk will enhance the market value. An environmentally lag-ging company has to offer higher returns to investors as a compensation for higher incremental risks that are related to ESG.

Another vital contributor to the RI development would be further academic research on portfolio selec-tion, believes Natalia Semenova. Since studies show there is no financial benefit from excluding companies, active portfolio management should pay more atten-tion to positive selection criteria and integration of ESG. With numerous investors having signed the

Principles for Responsible Investment, many are ask-ing: when does it pay off?

Out of the three ESG aspects, she suggests more research on the S as well as on another E, Engagement:

“The social aspects are not well researched and I think it would be interesting to study for instance employer relations and customer relations in European markets, where the pressure for companies is potentially stronger. I also have a feeling that we need to improve corporate governance in companies to get them to improve E and S. Although G has been researched quite a lot separately it has not been studied within the ESG framework.”

“Engagement is an area where research is lacking, especially since more and more investors are moving into it and it is a key feature in Responsible Investment according to the PRI. But engagement is today like a “black box” because we cannot readily measure the effect of this process,” says Natalia Semenova.

1. How would you briefly describe the overall result of the SIRP program? I would make the following conclusions of ESG impli-cations on company and portfolio levels: Back-testing over time indicates that ESG is priced on company level and that market imperfections cannot continue to provide abnormal risk-adjusted returns based on publicly available ESG rankings. Privately acces-sible information on company fundamentals - e.g. by engagement - and errors in market expectations de-rived from sustainability or intangible ESG factors need to be exploited by research and practice.

2. What impact has the SIRP program had on the RI development?One important role of the academic research has been to critically provide research support to the RI and ESG movements in the value chain in the finan-

cial markets. This has been accomplished by targeting asset owners and managers, financial and ESG analysts, company management and auditing firms.

3. How will you round up the program in 2012 when it ends? Research projects will be active in delivering out-comes during the whole year. In the spring, we plan to organise practitioner-targeted workshops in Paris, Milan and London in partnership with the local finance industry. After the summer, a synthesis of the outcomes of the program will be launched at a work-shop.

4. What will happen after that – any plans on continuation? We are a diversified academic research network con-nected to leading universities in Europe and active

5 questions to Professor Lars Hassel at Umeå School of Business in Sweden, who has lead the Sustainable Investment Research Platform, SIRP, since 2006.

“Engagement needs to be researched”

MAG•E•SINE 2012 • 25

Portfolio studiesResearchers in the SIRP network have been able to contribute to the alpha puzzle in two ways: they have extended the traditional knowledge of the risk/return implications of integrating ESG factors into equity portfolio management and contributed theoretically by highlighting the different RI segments and related differences in financial outcomes. The values-driven investors shun the controversial industries by sacrific-ing returns while the profit-seeking responsible inves-tors hunt superior financial returns in best-in-class portfolios. In relation to this, it has been shown that mispricing is not likely to continue in the alpha-seek-ing segment when the market learns to price ESG factors. With mainstreaming ESG, mispricing lead-ing to superior returns will fade out and the inves-tors will need exclusive, not publicly available ESG information linked to financial fundamentals of the company, in order to be able to exploit market imper-fections and create abnormal returns.

Incident studiesSIRP researchers have used event study method-ology to analyse whether bad news in the form of environmental incidents affect company value nega-tively. The studies have used GES Alert Service data provided weekly to clients with news briefings on recently reported company incidents that violate international norms on ESG. This systemized pro-cess singles out news of special investor concern, which often takes long before being highlighted in mainstream media or disappear in the abundant news flow. In an international sample it is found that environmental incidents are generally associated with the loss of value. For European firms, the loss is statistically significant and the magnitude of the abnormal returns should be of economic significance to corporations and investors.

Latest results...

Unethical board poor E

One of SIRP’s most recent research projects to be pre-

sented in 2012 looks at the relation between corporate

governance – the role of the board – and the sustainability

of the company. Why are there environmental leaders and

laggards? Why do the ratings differ between companies?

Findings indicate that environmental performance is not

only determined by the company’s financial resources and

by the industry where it operates, but also by the structure

of the board and the personal characteristics of the board

members. By focusing on past criminal convictions, suspi-

cions of crimes, records of non-payment and bankruptcy

history, the researchers create an ethical compass of the

board. The results show a negative relation between the

past unethical risk behaviour of board members and the

environmental performance of the company. “Hence, firms

with higher proportion of risk prone unethical board mem-

bers seem to focus less on the environmental implications

of the business,” concludes Lars Hassel.

within the PRI Academic Network. The network has a momentum and research will continue.

5. What kind of research is still missing? In addition to the already mentioned areas of social issues and engagement (see previous arti-cle), research is also needed on the organisational levels. I am not sure that the financial institutions have the knowledge, skills, incentives and ’time’ to really integrate ESG into decisions making. Another important area concerns the systemic changes that are needed in the financial markets: What sort of regulatory frameworks could sup-port a more long term and more sustainable view to such an extent that it eliminates much of the short-term trading that creates volatility?

“Engagement needs to be researched”

26 • MAG•E•SINE 2012

Despite two world economic crises and an outdated perspective on Eastern Europe among mainstream investors, Estonian Limestone New Europe Fund has proven that their high-conviction investment strategy works. And when the light returns to the financial markets, they hope their three years of outperformance will make “any rational investor” realise where the best growth potential is.

Forgotten Europe burgeons in shade of crisis

L aunched in 2008, Limestone New Europe Fund was the first fund applying environmental, social and governance (ESG) analysis on investments

in Eastern Europe - or New Europe, a term increas-ingly preferred in the region. Three years later the fund presented remarkable results outperforming its bench-mark, STOXX EU Enlarged Total Return by 15.6 per cent: -20.6 per cent compared to -36.1 per cent.

“As institutional investors often consider three years to be the minimum proof of meaningful performance history, we believe that we have now proved that our high-conviction investment strategy works even dur-ing times of very high pressure,” says Alvar Roosimaa, Fund Manager and CIO of Limestone Investment Management, an independent specialist Eastern Eu-rope equity funds manager based in Tallinn, Estonia.

The fund’s investment universe comprises of approxi-mately 250 companies operating in Eastern Euro-pean countries except Russia. Based on ESG risk ratings provided by GES, the fund seeks to engage with companies to improve poor ratings rather than elimi-nate future potential investment targets. However, it avoids investing in equities of companies that receive significant revenues from producing alcoholic bever-ages, tobacco, military weapons or are involved in the gambling business.

The key to success is finding how to bridge the so-called ‘information gap’ between what is reported to the public and what actually happens inside the com-panies. Alvar Roosimaa emphasises the importance of research and information gathering for better risk management and full integration of the sustainability considerations into investment decision making:

By Susanne Nyman, Communications Director of GES

“It has taken 300 company meetings combined with research from GES to successfully bridge the informa-tion gap. We are pleased to have demonstrated that sustainable investing in Eastern Europe is possible.”

103%

Slovenia

Eurozone 17 100%

Poland

70%

Eurozone 17 100%

Estonia

68%Eurozone 17 100%

Bulgaria

47%

Eurozone 17 100%

Romania

44%

Eurozone 17 100%

Hungary

69%

Eurozone 17 100%

Serbia

40%

Eurozone 17 100%

Czech Republic

91%

Eurozone 17 100%

Croatia

Eurozone 17 100%

65%

Lithuania

Eurozone 17 100%

63%

MAG•E•SINE 2012 • 27

Example of “room to grow” in Eastern Europe, according to Limestone. GDP (PPP) per capita 2011 for ten countries included in their New Europe Fund in com-parison with the equivalent average of the 17 Eurozone countries (100 per cent). Source: Northern Star/Limestone Sustainability Yearbook 2011

28 • MAG•E•SINE 2012

According to Limestone, New Europe has shown sur-prisingly strong recovery from the two crises. Already in spring 2009, the fund turned around more signifi-cantly than its benchmark and has kept the leading distance ever since. And while the world was hold-ing its breath during most of the spring and summer 2011 over Eurozone and US debt, news from Eastern

Europe grew constantly more positive, not least from the Southern part which is the most neglected by investors:

• The European Council concluded that Croatia is ready to become the 28th member of the Euro-pean Union.

• Moody’s raised the credit rating of Bulgaria as a consequence of its balanced budget and low levels of public debt.

• The European Bank for Reconstruction and Development revised upward its forecast for Romanian economic growth.

• Serbia made a giant leap towards EU accession when it caught the last missing war criminals and handed them over to the International Court of Justice in The Hague.

Which burgeoning companies in these emerging mar-kets that are most suitable for an investor to cultivate, varies considerably within the region. Usually the financial industry, banks, is the first winner in expanding countries. The second harvest depends if the mar-ket cycle is in an export or consump-tion phase. And ultimately, it depends on what is available on the local stock market, explains Rein Ojavere, Head of Research at Limestone:

“For example, Estonia and Slovenia have very strong export companies but they are not on the stock market so you can not buy shares in them.”

Although the fund was created on direct client demand and has received very good recognition from investors, it has not managed to attract a proportionate amount of capital - yet, due to the paralysing economic crisis.

“These have been the worst three years to market an ESG fund in Eastern Eu-rope. Risk taking in all areas has been put on hold, but as soon as the situation turns normal again we hope that any rational investor will realise that Eastern Europe has a lot of opportunities to of-fer,” says Alvar Roosimaa.

The stabilisation of the Eurozone is therefore the single most important factor for the future of Lime-stone New Europe Fund. But a second challenge is mainstream investors’ view on Eastern Europe, or even lack of view.

“It is interesting to question the prevalent perspective on European equities, because this only encompasses

New and old highway in Vojvodina, Serbia known as corridor 10.

Cargo ship sail into Port of Varna-West, Bulgaria, to be loaded with containers.

MAG•E•SINE 2012 • 29

Construction of the Ada bridge over the Sava river in Belgrade, Serbia. The bridge opened on January 1, 2012, and is the longest single-pylon cable-stayed bridge in the world.

If there is one clear message to learn from the financial crisis that has rocked the world for the better part of last four years, it is that change is needed…there are signs everywhere that the current Western financial model is not entirely sustainable…it is not only possible to do things differently but it is also nec-essary in order to survive and prosper in these turbulent times. The world is full of opportunities.

30 • MAG•E•SINE 2012

Old Europe for most investors. We try to widen their view by asking: why not look at Eastern/New Europe?” says Paavo Põld, Head of Business Development at Lime-stone.

Sooner or later, they are convinced that the perspective will change, empowered by their own track record as well as official statistics revealing that for the first time ever the general investment risks are lower in Eastern Europe than in Western.