1 Macroprudential indicators of the financial sector December 2015 Macroeconomic risk indicators ............................................................................................... 3 1 Manufacturing Purchasing Managers’ Index (PMI) in selected economies ....................... 3 2 Services Purchasing Managers’ Index (PMI) in selected economies.................................. 3 3 Consumer confidence indicators in the United States ......................................................... 3 4 Economic sentiment indicators in the euro area .................................................................. 3 5 Unemployment rates in selected economies ....................................................................... 3 6 Consumer price inflation in selected economies ................................................................. 3 7 Industrial production indices in selected economies ........................................................... 4 8 Retail sales indices in selected economies .......................................................................... 4 9 General government balances of EU countries in 2014 (%) ............................................... 4 10 Gross government debt of EU countries in the third quarter of 2015 (%) ........................ 4 Financial market risk indicators ............................................................................................. 4 11 Price commodity indices ................................................................................................... 4 12 Exchange rate indices ........................................................................................................ 4 13 Equity indices .................................................................................................................... 5 14 Share price indices of the parent institutions of the five largest domestic banks .............. 5 15 Yield curve slopes in selected economies ......................................................................... 5 16 Volatility of equity indices ................................................................................................ 5 17 CDS spread indices ........................................................................................................... 5 18 CDSs of the parent institutions of the largest Slovak banks ............................................. 5 19 Three-month rates and the OIS spread .............................................................................. 6 20 Inflation-linked swap prices .............................................................................................. 6 21 Credit spreads on 5-year government bonds issued by lower-rated countries .................. 6 22 Credit spreads on 5-year government bonds issued by selected central European countries and Germany........................................................................................................... 6 Corporate credit risk indicators ............................................................................................. 6 23 Exports and the business environment .............................................................................. 6 24 Exports and corporate sales ............................................................................................... 6 25 Sales in selected sectors compared with their level for the period 06/2007 to 06/2008 ... 7 26 Corporate loans and sales .................................................................................................. 7 27 Interest rate spreads on new loans to NFCs ...................................................................... 7 28 Non-performing loans and default rates ............................................................................ 7 29 Loans at risk ...................................................................................................................... 7 30 Debt-service burden and its components........................................................................... 7 31 Commercial real estate: price and vacancy rates in the office segment ............................ 8 32 Commercial real estate: sales in the residential segment (new flats) ................................ 8

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Macroprudential indicators of the financial sector

December 2015

Macroeconomic risk indicators ............................................................................................... 3

1 Manufacturing Purchasing Managers’ Index (PMI) in selected economies ....................... 3

2 Services Purchasing Managers’ Index (PMI) in selected economies.................................. 3

3 Consumer confidence indicators in the United States ......................................................... 3

4 Economic sentiment indicators in the euro area .................................................................. 3

5 Unemployment rates in selected economies ....................................................................... 3

6 Consumer price inflation in selected economies ................................................................. 3

7 Industrial production indices in selected economies ........................................................... 4

8 Retail sales indices in selected economies .......................................................................... 4

9 General government balances of EU countries in 2014 (%) ............................................... 4

10 Gross government debt of EU countries in the third quarter of 2015 (%) ........................ 4

Financial market risk indicators ............................................................................................. 4

11 Price commodity indices ................................................................................................... 4

12 Exchange rate indices ........................................................................................................ 4

13 Equity indices .................................................................................................................... 5

14 Share price indices of the parent institutions of the five largest domestic banks .............. 5

15 Yield curve slopes in selected economies ......................................................................... 5

16 Volatility of equity indices ................................................................................................ 5

17 CDS spread indices ........................................................................................................... 5

18 CDSs of the parent institutions of the largest Slovak banks ............................................. 5

19 Three-month rates and the OIS spread .............................................................................. 6

20 Inflation-linked swap prices .............................................................................................. 6

21 Credit spreads on 5-year government bonds issued by lower-rated countries .................. 6

22 Credit spreads on 5-year government bonds issued by selected central European

countries and Germany ........................................................................................................... 6

Corporate credit risk indicators ............................................................................................. 6

23 Exports and the business environment .............................................................................. 6

24 Exports and corporate sales ............................................................................................... 6

25 Sales in selected sectors compared with their level for the period 06/2007 to 06/2008 ... 7

26 Corporate loans and sales .................................................................................................. 7

27 Interest rate spreads on new loans to NFCs ...................................................................... 7

28 Non-performing loans and default rates ............................................................................ 7

29 Loans at risk ...................................................................................................................... 7

30 Debt-service burden and its components........................................................................... 7

31 Commercial real estate: price and vacancy rates in the office segment ............................ 8

32 Commercial real estate: sales in the residential segment (new flats) ................................ 8

2

33 Comparison of corporate balance sheets and sales ........................................................... 8

34 Liabilities of non-financial corporations ........................................................................... 8

Household credit risk indicators ............................................................................................. 8

35 Household indebtedness in Slovakia and in selected countries (%) ................................. 8

36 Changes in household financial assets .............................................................................. 8

37 Number of unemployed by income category .................................................................... 9

38 Employment in selected sectors - index ............................................................................ 9

39 Expected employment in selected sectors - index ............................................................. 9

40 Real wages in selected sectors - index .............................................................................. 9

41 The consumer confidence index and its components ........................................................ 9

42 Non-performing household loans ...................................................................................... 9

43 Loan-to-value (LTV) ratio ............................................................................................... 10

44 Housing affordability index............................................................................................. 10

Market risk and liquidity risk indicators ............................................................................. 10

45 Value at Risk for investments in different types of financial instruments ...................... 10

46 Sensitivity to different risk types in the banking sector .................................................. 10

47 Sensitivity to different risk types in the sector of PFMC funds ...................................... 11

48 Sensitivity to different risk types in the SPMC funds sector .......................................... 11

49 Sensitivity to different risk types in the collective investment sector ............................. 11

50 Sensitivity of insurers' assets to different risk types ....................................................... 11

51 Loan-to-deposit ratio ....................................................................................................... 11

52 Liquid asset ratio ............................................................................................................. 11

53 Impact of the stress test scenarios on PFMC managed pension funds ............................ 12

54 Impact of the stress test scenarios on payout SPMC managed distribution supplementary

pension funds ........................................................................................................................ 12

55 Impact of the stress test scenarios on collective investment funds ................................. 12

56 Impact of the stress test scenarios on the assets of insurance companies ....................... 12

57 Additional expenses that the insurance sector would incur under the stress test scenarios

.............................................................................................................................................. 12

58 Impact of the stress test scenarios on the assets of unit-linked insurance funds ............. 12

General note:

'Index: 31 December 2015 = 1' means that the given index was normalized so that its value on the specified

date (31 December 2015) was equal to 1.

3

Macroeconomic risk indicators

1 Manufacturing Purchasing Managers’

Index (PMI) in selected economies

2 Services Purchasing Managers’ Index

(PMI) in selected economies

Source: Bloomberg. Note: PMI (Purchasing Managers’ Index) is an indicator of the economic health of the manufacturing or service sector: an index value of more than 50 represents expansion, while a value of below 50 represents contraction.

Source: Bloomberg. Note: PMI (Purchasing Managers’ Index) is an indicator of the economic health of the manufacturing or service sector: an index value of more than 50 represents expansion, while a value of below 50 represents contraction.

3 Consumer confidence indicators in the

United States

4 Economic sentiment indicators in the euro

area

Source: Bloomberg. Note: The chart refers to US consumer confidence indices produced by two different institutions.

Source: Bloomberg. Notes: ESI is the Economic Sentiment Indicator compiled by the European Commission. ZEW represents the economic sentiment indicator compiled by a private company ZEW (Zentrum für Europäische Wirtschaftsforschung).

5 Unemployment rates in selected economies 6 Consumer price inflation in selected

economies

Source: Eurostat, Bureau of Labor Statistics. Note: Seasonally adjusted.

Source: Eurostat, Bureau of Labor Statistics. Note: Year-on-year percentage changes in the consumer price indices.

30

35

40

45

50

55

60

65

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Euro area United States China

30

35

40

45

50

55

60

65

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Euro area United States

20

40

60

80

100

120

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Conference Board Consumer Confidence Index

University of Michigan Consumer Sentiment Index

-80

-60

-40

-20

0

20

40

60

80

60

70

80

90

100

110

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

ESI ZEW (right-hand scale)

3%

5%

7%

9%

11%

13%

15%

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Euro area United States Slovakia

-1%

0%

1%

2%

3%

4%

5%

1.10

5.10

9.10

1.11

5.11

9.11

1.12

5.12

9.12

1.13

5.13

9.13

1.14

5.14

9.14

1.15

5.15

9.15

1.16

Euro area United States Slovakia

4

7 Industrial production indices in selected

economies

8 Retail sales indices in selected economies

Source: Eurostat, US Federal Reserve. Notes: Rebalanced (average: 2007 = 100). Seasonally adjusted.

Source: Eurostat, US Department of Commerce. Notes: Rebalanced (average 2007 = 100). Seasonally adjusted.

9 General government balances of EU

countries in 2014 (%)

10 Gross government debt of EU countries in

the third quarter of 2015 (%)

Source: Eurostat. Note: Balance is expressed as a percentage of GDP.

Source: Eurostat. Note: Gross government debt is expressed as a percentage of shares of GDP.

Financial market risk indicators

11 Price commodity indices (31. 12. 2014 = 1) 12 Exchange rate indices (31. 12. 2013 = 1)

Source: Bloomberg, NBS.

Source: Bloomberg, NBS.

80

90

100

110

120

130

140

150

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Euro area United States Slovakia Germany

90

95

100

105

110

115

120

125

1.07

7.07

1.08

7.08

1.09

7.09

1.10

7.10

1.11

7.11

1.12

7.12

1.13

7.13

1.14

7.14

1.15

7.15

1.16

Euro area United States Slovakia Germany

-10

-8

-6

-4

-2

0

2

Cyp

rus

Por

tuga

lS

pain

Bul

garia

UK

Cro

atia

Slo

veni

aIr

elan

dF

ranc

eG

reec

eP

olan

dF

inla

ndB

elgi

umIta

lyS

lova

kia

Aus

tria

Eur

o ar

eaH

unga

ryN

ethe

rland

sM

alta

Cze

ch R

epub

licS

wed

enLa

tvia

Rom

ania

Lith

uani

aG

erm

any

Est

onia

Luxe

mbo

urg

Den

mar

k

020406080

100120140160180

Gre

ece

Ital

yP

ortu

gal

Cyp

rus

Bel

gium

Irel

and

Spa

inF

ranc

eE

uro

area UK

Cro

atia

Aus

tria

Slo

veni

aH

unga

ryG

erm

any

Mal

taN

ethe

rland

sF

inla

ndS

lova

kia

Pol

and

Sw

eden

Den

mar

kC

zech

Rep

ublic

Lith

uani

aR

oman

iaLa

tvia

Bul

garia

Luxe

mbo

urg

Est

onia

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1.1.2010 1.1.2011 1.1.2012 1.1.2013 1.1.2014 1.1.2015 1.1.2016

Brent oil price index

Gold price index

0.7

0.8

0.9

1.0

1.1

1.2

1.1.20071.1.20081.1.20091.1.20101.1.20111.1.20121.1.20131.1.20141.1.20151.1.2016

USD / EURCZK / EURHUF / EUR

5

13 Equity indices (31. 12. 2014 = 1) 14 Share price indices of the parent

institutions of the five largest domestic banks

(31. 12. 2014 = 1)

Source: Bloomberg, NBS. Source: Bloomberg, NBS.

15 Yield curve slopes in selected economies

(p. p.)

16 Volatility of equity indices

Source: Bloomberg, NBS. Notes: The yield curve slope is expressed as the difference between the yield to maturity on 10-year and 3-month government bonds. p. p. – percentage points

Source: Bloomberg.

17 CDS spread indices (b. p.)

18 CDSs of the parent institutions of the

largest Slovak banks (b. p.)

Source: Bloomberg, NBS. Note: b. p. – basis points

Source: Bloomberg, NBS. Note: b. p. – basis points

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4 EUROSTOXX

NIKKEI

S&P 500

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1.1.2010 1.1.2011 1.1.2012 1.1.2013 1.1.2014 1.1.2015 1.1.2016

UniCreditKBCErste BankRZBIntesa

-2

-1

0

1

2

3

4

5

Germany

United States0

20

40

60

80

100

VIX

VSTOXX

0

50

100

150

200

250

300

350

400

iTraxx Europe 5Y

iTraxx SeniorFinancials 5Y

0

100

200

300

400

500

600

700

1.1.

2007

1.1.

2008

1.1.

2009

1.1.

2010

1.1.

2011

1.1.

2012

1.1.

2013

1.1.

2014

1.1.

2015

1.1.

2016

Max. - min. CDS spreads of parent banks

iTraxx Senior Financials 5Y

6

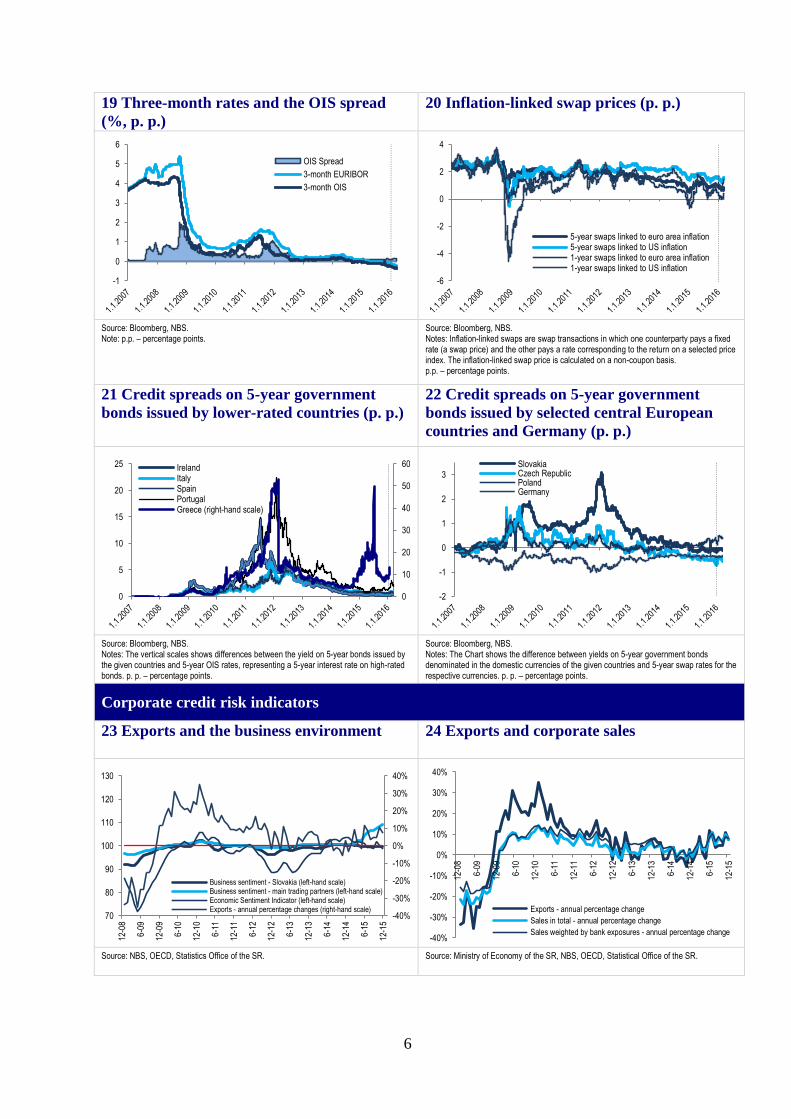

19 Three-month rates and the OIS spread

(%, p. p.)

20 Inflation-linked swap prices (p. p.)

Source: Bloomberg, NBS. Note: p.p. – percentage points.

Source: Bloomberg, NBS. Notes: Inflation-linked swaps are swap transactions in which one counterparty pays a fixed rate (a swap price) and the other pays a rate corresponding to the return on a selected price index. The inflation-linked swap price is calculated on a non-coupon basis. p.p. – percentage points.

21 Credit spreads on 5-year government

bonds issued by lower-rated countries (p. p.)

22 Credit spreads on 5-year government

bonds issued by selected central European

countries and Germany (p. p.)

Source: Bloomberg, NBS. Notes: The vertical scales shows differences between the yield on 5-year bonds issued by the given countries and 5-year OIS rates, representing a 5-year interest rate on high-rated bonds. p. p. – percentage points.

Source: Bloomberg, NBS. Notes: The Chart shows the difference between yields on 5-year government bonds denominated in the domestic currencies of the given countries and 5-year swap rates for the respective currencies. p. p. – percentage points.

Corporate credit risk indicators

23 Exports and the business environment

24 Exports and corporate sales

Source: NBS, OECD, Statistics Office of the SR. Source: Ministry of Economy of the SR, NBS, OECD, Statistical Office of the SR.

-1

0

1

2

3

4

5

6

OIS Spread

3-month EURIBOR

3-month OIS

-6

-4

-2

0

2

4

5-year swaps linked to euro area inflation5-year swaps linked to US inflation1-year swaps linked to euro area inflation1-year swaps linked to US inflation

0

10

20

30

40

50

60

0

5

10

15

20

25 IrelandItalySpainPortugalGreece (right-hand scale)

-2

-1

0

1

2

3SlovakiaCzech RepublicPolandGermany

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

70

80

90

100

110

120

130

12-0

8

6-09

12-0

9

6-10

12-1

0

6-11

12-1

1

6-12

12-1

2

6-13

12-1

3

6-14

12-1

4

6-15

12-1

5

Business sentiment - Slovakia (left-hand scale)Business sentiment - main trading partners (left-hand scale)Economic Sentiment Indicator (left-hand scale)Exports - annual percentage changes (right-hand scale)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

12-0

8

6-09

12-0

9

6-10

12-1

0

6-11

12-1

1

6-12

12-1

2

6-13

12-1

3

6-14

12-1

4

6-15

12-1

5

Exports - annual percentage change

Sales in total - annual percentage change

Sales weighted by bank exposures - annual percentage change

7

25 Sales in selected sectors compared with

their level for the period 06/2007 to 06/2008

26 Corporate loans and sales

Source: Statistical Office of the SR. Source: NBS, Statistical Office of the SR.

27 Interest rate spreads on new loans to

NFCs

28 Non-performing loans and default rates

Source: NBS, European Banking Federation. Note: The spread is defined as the difference between the monthly EURIBOR rate and the average rate on new loans in the respective category.

Source: NBS. Notes: Data on the right-hand scale are in EUR mil. Default rates refer to the number/volume of loans re-categorised as defaulted to the number/volume of non-defaulted loans at the beginning of the period under review.

29 Loans at risk 30 Debt-service burden and its components

Source: NBS. Note: The chart shows the interquartile range.

Source: NBS, SO SR. Note: Data on the right-hand scale are in EUR mil.

20%

45%

70%

95%

120%

12-08 12-09 12-10 12-11 12-12 12-13 12-14 12-15

Corporate sector in total IndustryConstruction Trade and motor vehicle salesHotels and restaurants -25%

-15%

-5%

5%

15%

12-0

8

6-09

12-0

9

6-10

12-1

0

6-11

12-1

1

6-12

12-1

2

6-13

12-1

3

6-14

12-1

4

6-15

12-1

5

Total sales - annual percentage change

Year-on-year growth in loans from domestic banks to non-financial corporations

-1%

0%

1%

2%

3%

4%

5%

6%

12-0

9

6-10

12-1

0

6-11

12-1

1

6-12

12-1

2

6-13

12-1

3

6-14

12-1

4

6-15

12-1

5

EURIBOR 1MLoans of up to and including €0.25 million Loans of more than €0.25 million, up to and including €1 million Loans of more than €1 million

-150

-100

-50

0

50

100

150

200

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%12

-08

6-09

12-0

9

6-10

12-1

0

6-11

12-1

1

6-12

12-1

2

6-13

12-1

3

6-14

12-1

4

6-15

12-1

5

Th

ou

san

ds

Change in the amount of NPL - m/m (right-hand scale)Default rates (amount of loans)Default rates (number of loans)Ratio of non-performing loans

0%

2%

4%

6%

8%

10%

3.11

6.11

9.11

12.1

1

3.12

6.12

9.12

12.1

2

3.13

6.13

9.13

12.1

3

3.14

6.14

9.14

12.1

4

3.15

6.15

9.15

Average Median

0

25

50

75

100

125

150

-8%

-6%

-4%

-2%

0%

2%

4%

1-08 7-08 1-09 7-09 1-10 7-10 1-11 7-11 1-12 7-12 1-13 7-13 1-14 7-14 1-15 7-15

Interest rate (left-hand scale)Loans (left-hand scale)Sales (left-hand scale)Debt-service burden - domestic loans - indexDebt-service burden at 2008 rates - domestic loans - indexDebt burden-service - total loans - indexDebt-service burden at 2008 rates - total loans - index

8

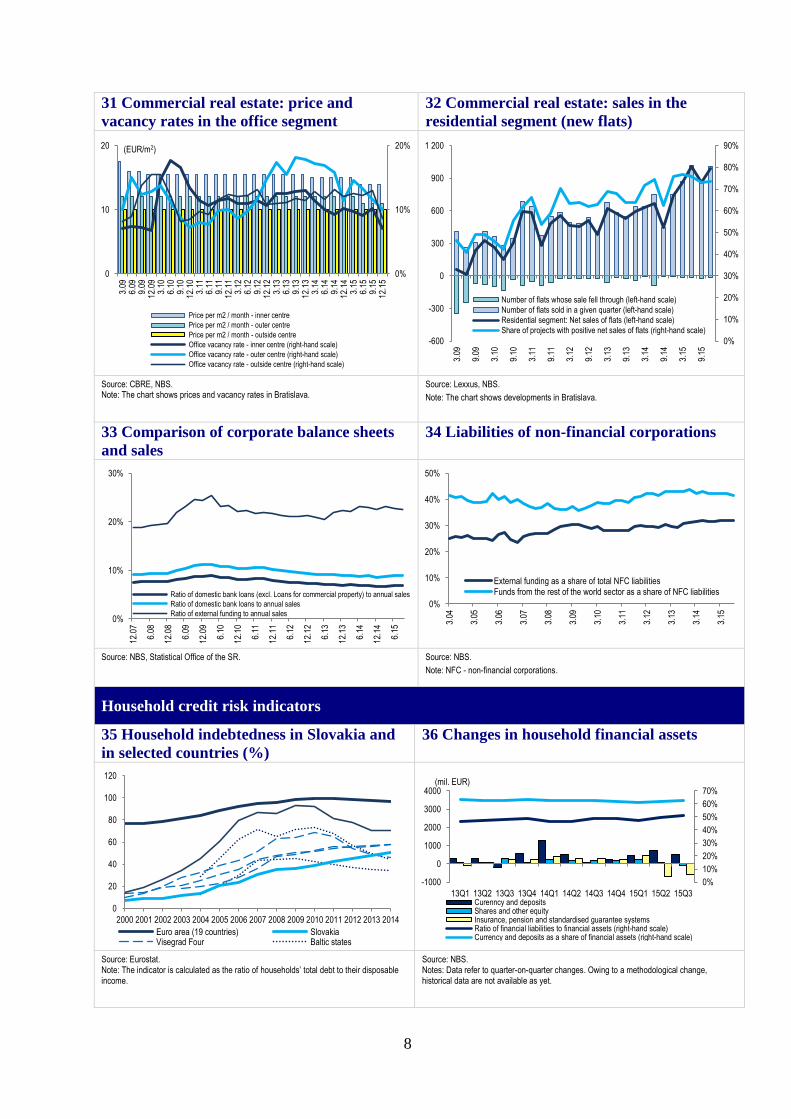

31 Commercial real estate: price and

vacancy rates in the office segment

32 Commercial real estate: sales in the

residential segment (new flats)

Source: CBRE, NBS. Note: The chart shows prices and vacancy rates in Bratislava.

Source: Lexxus, NBS.

Note: The chart shows developments in Bratislava.

33 Comparison of corporate balance sheets

and sales

34 Liabilities of non-financial corporations

Source: NBS, Statistical Office of the SR. Source: NBS.

Note: NFC - non-financial corporations.

Household credit risk indicators

35 Household indebtedness in Slovakia and

in selected countries (%)

36 Changes in household financial assets

Source: Eurostat. Note: The indicator is calculated as the ratio of households’ total debt to their disposable income.

Source: NBS. Notes: Data refer to quarter-on-quarter changes. Owing to a methodological change, historical data are not available as yet.

0%

10%

20%

0

10

20

3.09

6.09

9.09

12.0

93.

106.

109.

1012

.10

3.11

6.11

9.11

12.1

13.

126.

129.

1212

.12

3.13

6.13

9.13

12.1

33.

146.

149.

1412

.14

3.15

6.15

9.15

12.1

5

Price per m2 / month - inner centre

Price per m2 / month - outer centre

Price per m2 / month - outside centre

Office vacancy rate - inner centre (right-hand scale)

Office vacancy rate - outer centre (right-hand scale)

Office vacancy rate - outside centre (right-hand scale)

(EUR/m2)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-600

-300

0

300

600

900

1 200

3.09

9.09

3.10

9.10

3.11

9.11

3.12

9.12

3.13

9.13

3.14

9.14

3.15

9.15

Number of flats whose sale fell through (left-hand scale)

Number of flats sold in a given quarter (left-hand scale)

Residential segment: Net sales of flats (left-hand scale)

Share of projects with positive net sales of flats (right-hand scale)

0%

10%

20%

30%

12.0

7

6.08

12.0

8

6.09

12.0

9

6.10

12.1

0

6.11

12.1

1

6.12

12.1

2

6.13

12.1

3

6.14

12.1

4

6.15

Ratio of domestic bank loans (excl. Loans for commercial property) to annual sales

Ratio of domestic bank loans to annual sales

Ratio of external funding to annual sales0%

10%

20%

30%

40%

50%

3.04

3.05

3.06

3.07

3.08

3.09

3.10

3.11

3.12

3.13

3.14

3.15

External funding as a share of total NFC liabilitiesFunds from the rest of the world sector as a share of NFC liabilities

0

20

40

60

80

100

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Euro area (19 countries) SlovakiaVisegrad Four Baltic states

0%

10%

20%

30%

40%

50%

60%

70%

-1000

0

1000

2000

3000

4000

13Q1 13Q2 13Q3 13Q4 14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3

Th

ou

san

ds

Curenncy and depositsShares and other equityInsurance, pension and standardised guarantee systemsRatio of financial liabilities to financial assets (right-hand scale)Currency and deposits as a share of financial assets (right-hand scale)

(mil. EUR)

9

37 Number of unemployed by income

category

38 Employment in selected sectors - index

Source: Central Office of Labour, Social Affairs and Family of the SR. Notes: Left-hand and right-hand scales: Numbers of job seekers are in thousands. Household income categories – categorisation based on the KZAM employment classification and KZAM income data; it consists of three categories: higher-income category (income of over €800 per month) – legislators, senior officials and managers, scientists, professionals, technicians, health professionals, and teaching professionals; middle-income category (income between €600 and €800 per month) – office workers, craft and skilled workers, processors, and plant and machinery operators; lower-income category (income of up to €600) – service and retail workers, agricultural and forestry workers, auxiliary and unskilled workers.

Source: Statistical Office of the SR. Note: Year-on-year changes.

39 Expected employment in selected sectors -

index

40 Real wages in selected sectors - index

Source: Statistical Office of the SR.

Source: Statistical Office of the SR. Note: HICP - Harmonised Index of Consumer Prices, change on the same period of the previous year.

41 The consumer confidence index and its

components

42 Non-performing household loans

Source: Statistical Office of the SR. Source: NBS.

Note: Left-hand scale: ratio of non-performing household loans to total household loans.

0

20

40

60

80

100

120

0

2

4

6

8

10

12

I.07

X.0

7V

II.08

IV.0

9I.1

0X

.10

VII.

11IV

.12

I.13

X.1

3V

II.14

IV.1

5I.

16 I.07

X.0

7V

II.08

IV.0

9I.1

0X

.10

VII.

11IV

.12

I.13

X.1

3V

II.14

IV.1

5I.

16

Th

ou

san

ds

Higher-income category Medium-income category

Lower-income category

Inflow of job seekers Number of job seekers

80

85

90

95

100

105

110

I.10

IV.1

0

VII.

10

X.1

0

I.11

IV.1

1

VII.

11

X.1

1

I.12

IV.1

2

VII.

12

X.1

2

I.13

IV.1

3

VII.

13

X.1

3

I.14

IV.1

4

VII.

14

X.1

4

I.15

IV.1

5

VII.

15

X.1

5

Manufacturing Construction

Wholesale trade Retail trade

Accomodation Transportation and storage

-60

-40

-20

0

20

40

I.08

V.0

8

IX.0

8

I.09

V.0

9

IX.0

9

I.10

V.1

0

IX.1

0

I.11

V.1

1

IX.1

1

I.12

V.1

2

IX.1

2

I.13

V.1

3

IX.1

3

I.14

V.1

4

IX.1

4

I.15

V.1

5

IX.1

5

I.16

Services Industry Trade Construction

98

100

102

104

106

85

90

95

100

105

110

I.09

V.0

9

IX.0

9

I.10

V.1

0

IX.1

0

I.11

V.1

1

IX.1

1

I.12

V.1

2

IX.1

2

I.13

V.1

3

IX.1

3

I.14

V.1

4

IX.1

4

I.15

V.1

5

IX.1

5

I.16

HICP (righ-hand scale)IndustryConstructionWholesale trade except for motor vehiclesRetail trade except for motor vehicles

-60

-30

0

30

60

90

I.08

V.0

8

IX.0

8

I.09

V.0

9

IX.0

9

I.10

V.1

0

IX.1

0

I.11

V.1

1

IX.1

1

I.12

V.1

2

IX.1

2

I.13

V.1

3

IX.1

3

I.14

V.1

4

IX.1

4

I.15

V.1

5

IX.1

5

I.16

Consumer confidence indexExpected financial situation of householdsExpected economic situation in SlovakiaExpected unemploymentExpected household savings

-90

-60

-30

0

30

60

90

120

150

0

2

4

6

8

10

I.09

IV.0

9V

II.09

X.0

9I.1

0IV

.10

VII.

10X

.10

I.11

IV.1

1V

II.11

X.1

1I.1

2IV

.12

VII.

12X

.12

I.13

IV.1

3V

II.13

X.1

3I.1

4IV

.14

VII.

14X

.14

I.15

IV.1

5V

II.15

X.1

5

Upper and lower quartiles of the non-performing loan (NPL) ratioWeighted average of the NPL ratioMonth-on-month changes in the amount of NPLs (right-hand scale)

(%) (mil. EUR)

(mil. EUR)

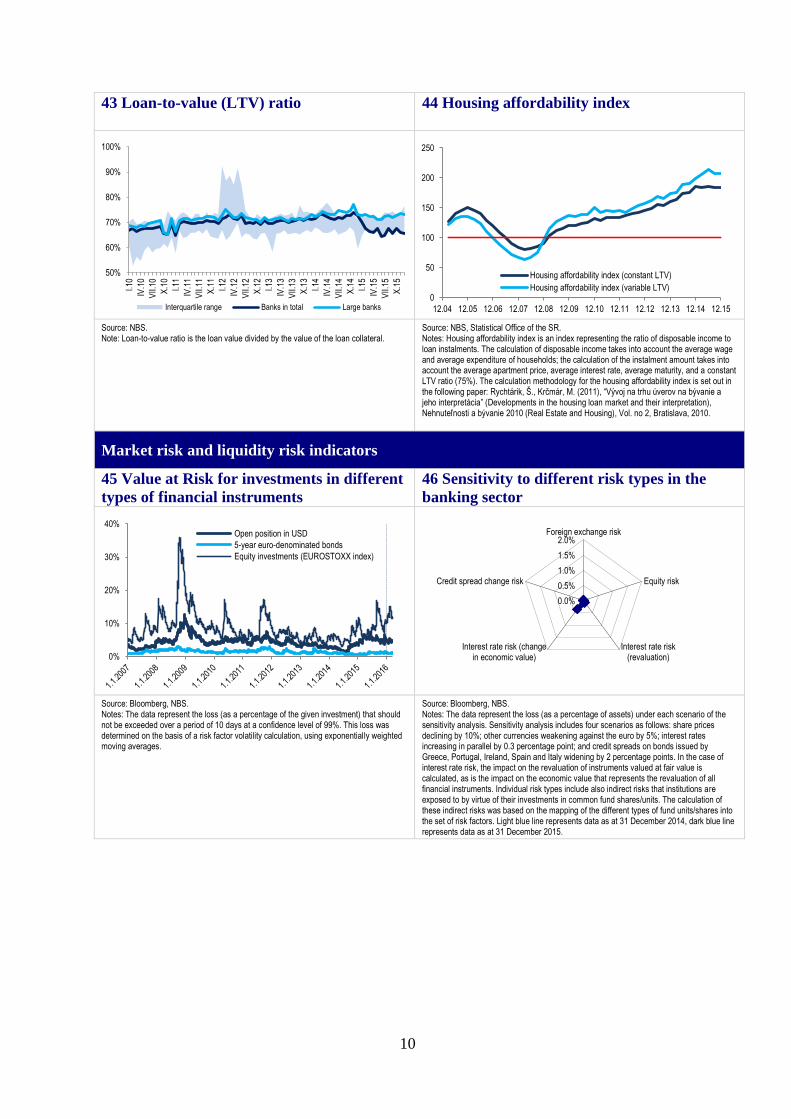

10

43 Loan-to-value (LTV) ratio 44 Housing affordability index

Source: NBS. Note: Loan-to-value ratio is the loan value divided by the value of the loan collateral.

Source: NBS, Statistical Office of the SR. Notes: Housing affordability index is an index representing the ratio of disposable income to loan instalments. The calculation of disposable income takes into account the average wage and average expenditure of households; the calculation of the instalment amount takes into account the average apartment price, average interest rate, average maturity, and a constant LTV ratio (75%). The calculation methodology for the housing affordability index is set out in the following paper: Rychtárik, Š., Krčmár, M. (2011), “Vývoj na trhu úverov na bývanie a jeho interpretácia” (Developments in the housing loan market and their interpretation), Nehnuteľnosti a bývanie 2010 (Real Estate and Housing), Vol. no 2, Bratislava, 2010.

Market risk and liquidity risk indicators

45 Value at Risk for investments in different

types of financial instruments

46 Sensitivity to different risk types in the

banking sector

Source: Bloomberg, NBS. Notes: The data represent the loss (as a percentage of the given investment) that should not be exceeded over a period of 10 days at a confidence level of 99%. This loss was determined on the basis of a risk factor volatility calculation, using exponentially weighted moving averages.

Source: Bloomberg, NBS. Notes: The data represent the loss (as a percentage of assets) under each scenario of the sensitivity analysis. Sensitivity analysis includes four scenarios as follows: share prices declining by 10%; other currencies weakening against the euro by 5%; interest rates increasing in parallel by 0.3 percentage point; and credit spreads on bonds issued by Greece, Portugal, Ireland, Spain and Italy widening by 2 percentage points. In the case of interest rate risk, the impact on the revaluation of instruments valued at fair value is calculated, as is the impact on the economic value that represents the revaluation of all financial instruments. Individual risk types include also indirect risks that institutions are exposed to by virtue of their investments in common fund shares/units. The calculation of these indirect risks was based on the mapping of the different types of fund units/shares into the set of risk factors. Light blue line represents data as at 31 December 2014, dark blue line represents data as at 31 December 2015.

50%

60%

70%

80%

90%

100%

I.10

IV.1

0

VII.

10

X.1

0

I.11

IV.1

1

VII.

11

X.1

1

I.12

IV.1

2

VII.

12

X.1

2

I.13

IV.1

3

VII.

13

X.1

3

I.14

IV.1

4

VII.

14

X.1

4

I.15

IV.1

5

VII.

15

X.1

5

Interquartile range Banks in total Large banks0

50

100

150

200

250

12.04 12.05 12.06 12.07 12.08 12.09 12.10 12.11 12.12 12.13 12.14 12.15

Housing affordability index (constant LTV)

Housing affordability index (variable LTV)

0%

10%

20%

30%

40%Open position in USD

5-year euro-denominated bonds

Equity investments (EUROSTOXX index)

0.0%

0.5%

1.0%

1.5%

2.0%Foreign exchange risk

Equity risk

Interest rate risk(revaluation)

Interest rate risk (changein economic value)

Credit spread change risk

11

47 Sensitivity to different risk types in the

sector of PFMC funds

48 Sensitivity to different risk types in the

SPMC funds sector

Source: Bloomberg, NBS. Notes: The data represent the loss (as a percentage of NAV) under each scenario of the sensitivity analysis. The sensitivity analysis is described in the note to chart 46. Light blue line represents data as at 31 December 2014, dark blue line represents data as at 31 December 2015.

Source: Bloomberg, NBS. Notes: The data represent the loss (as a percentage of NAV) under each scenario of the sensitivity analysis. The sensitivity analysis is described in the note to chart 46. Light blue line represents data as at 31 December 2014, dark blue line represents data as at 31 December 2015.

49 Sensitivity to different risk types in the

collective investment sector

50 Sensitivity of insurers' assets to different

risk types

Source: Bloomberg, NBS. Notes: The data represent the loss (as a percentage of NAV) under each scenario of the sensitivity analysis. The sensitivity analysis is described in the note to chart 46. Light blue line represents data as at 31 December 2014, dark blue line represents data as at 31 December 2015.

Source: Bloomberg, NBS. Notes: The data represent the percentage decline in the value of assets under each scenario of the sensitivity analysis. The sensitivity analysis is described in the note to chart 46. Light blue line represents data as at 31 December 2014, dark blue line represents data as at 31 December 2015.

51 Loan-to-deposit ratio 52 Liquid asset ratio

Source: NBS.

Source: NBS.

0.0%

0.5%

1.0%

1.5%

2.0%Foreign exchange risk

Equity risk

Interest rate risk(revaluation)

Interest rate risk(change in economic

value)

Credit spread changerisk

0.0%

0.5%

1.0%

1.5%

2.0%Foreign exchange risk

Equity risk

Interest rate risk(revaluation)

Interest rate risk(change in economic

value)

Credit spread changerisk

0.0%

0.5%

1.0%

1.5%

2.0%Foreign exchange risk

Equity risk

Interest rate risk(revaluation)

Interest rate risk(change in economic

value)

Credit spread changerisk

0.0%

0.5%

1.0%

1.5%

2.0%Foreign exchange risk

Equity risk

Interest rate risk(revaluation)

Interest rate risk (changein economic value)

Credit spread changerisk

0%

20%

40%

60%

80%

100%

Loan-to-deposit ratio

Loan-to-deposit ratio (excluding mortgage bonds issued)

Loan-to-deposit ratio (retail sector)

0

0.5

1

1.5

2

2.5

3

12-09 12-10 12-11 12-12 12-13 12-14 12-15

Banking sector - median

Retail banks - median

Weighted average

12

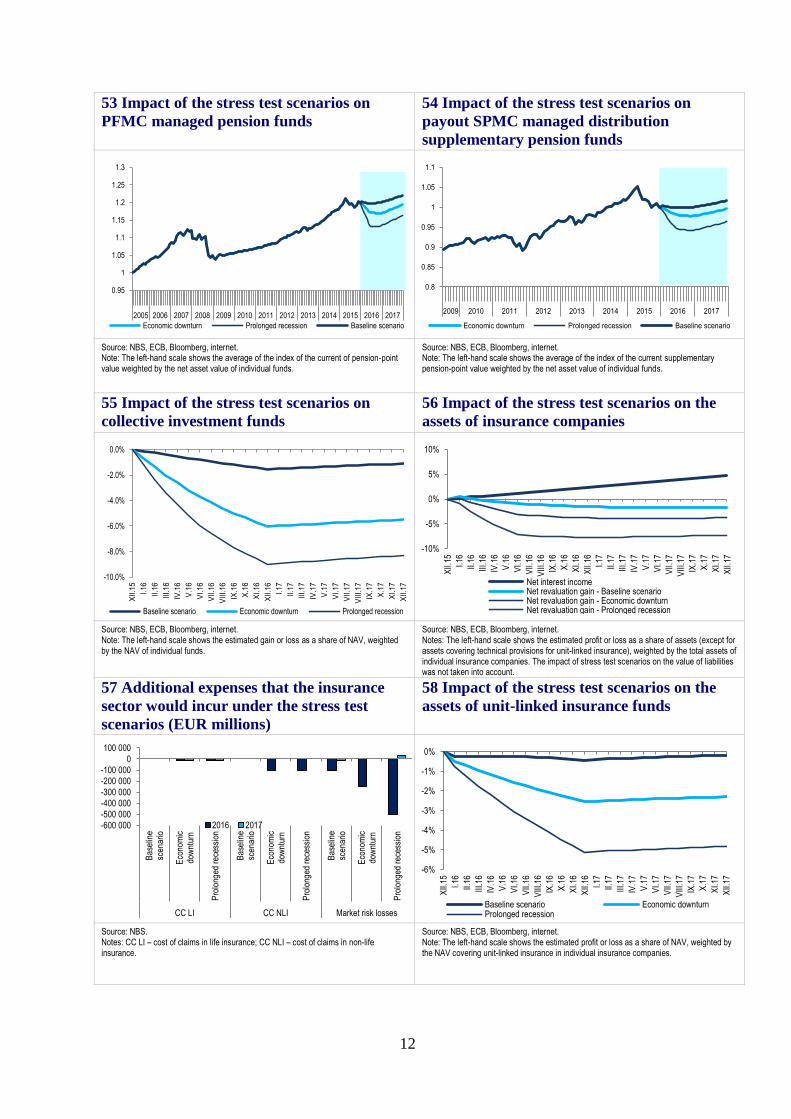

53 Impact of the stress test scenarios on

PFMC managed pension funds

54 Impact of the stress test scenarios on

payout SPMC managed distribution

supplementary pension funds

Source: NBS, ECB, Bloomberg, internet. Note: The left-hand scale shows the average of the index of the current of pension-point value weighted by the net asset value of individual funds.

Source: NBS, ECB, Bloomberg, internet. Note: The left-hand scale shows the average of the index of the current supplementary pension-point value weighted by the net asset value of individual funds.

55 Impact of the stress test scenarios on

collective investment funds

56 Impact of the stress test scenarios on the

assets of insurance companies

Source: NBS, ECB, Bloomberg, internet. Note: The left-hand scale shows the estimated gain or loss as a share of NAV, weighted by the NAV of individual funds.

Source: NBS, ECB, Bloomberg, internet. Notes: The left-hand scale shows the estimated profit or loss as a share of assets (except for assets covering technical provisions for unit-linked insurance), weighted by the total assets of individual insurance companies. The impact of stress test scenarios on the value of liabilities was not taken into account.

57 Additional expenses that the insurance

sector would incur under the stress test

scenarios (EUR millions)

58 Impact of the stress test scenarios on the

assets of unit-linked insurance funds

Source: NBS. Notes: CC LI – cost of claims in life insurance; CC NLI – cost of claims in non-life insurance.

Source: NBS, ECB, Bloomberg, internet. Note: The left-hand scale shows the estimated profit or loss as a share of NAV, weighted by the NAV covering unit-linked insurance in individual insurance companies.

0.95

1

1.05

1.1

1.15

1.2

1.25

1.3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Economic downturn Prolonged recession Baseline scenario

0.8

0.85

0.9

0.95

1

1.05

1.1

2009 2010 2011 2012 2013 2014 2015 2016 2017

Economic downturn Prolonged recession Baseline scenario

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

XII

.15

I.16

II.1

6

III.1

6

IV.1

6

V.1

6

VI.

16

VII

.16

VII

I.1

6

IX.1

6

X.1

6

XI.

16

XII

.16

I.17

II.1

7

III.1

7

IV.1

7

V.1

7

VI.

17

VII

.17

VII

I.1

7

IX.1

7

X.1

7

XI.

17

XII

.17

Baseline scenario Economic downturn Prolonged recession

-10%

-5%

0%

5%

10%X

II.15 I.16

II.16

III.1

6

IV.1

6

V.1

6

VI.1

6

VII.

16

VIII

.16

IX.1

6

X.1

6

XI.1

6

XII.

16 I.17

II.17

III.1

7

IV.1

7

V.1

7

VI.1

7

VII.

17

VIII

.17

IX.1

7

X.1

7

XI.1

7

XII.

17

Net interest incomeNet revaluation gain - Baseline scenarioNet revaluation gain - Economic downturnNet revaluation gain - Prolonged recession

-600 000

-500 000

-400 000

-300 000

-200 000

-100 000

0

100 000

Bas

elin

esc

enar

io

Eco

nom

icdo

wnt

urn

Pro

long

ed r

eces

sion

Bas

elin

esc

enar

io

Eco

nom

icdo

wnt

urn

Pro

long

ed r

eces

sion

Bas

elin

esc

enar

io

Eco

nom

icdo

wnt

urn

Pro

long

ed r

eces

sion

CC LI CC NLI Market risk losses

2016 2017

-6%

-5%

-4%

-3%

-2%

-1%

0%

XII.

15 I.16

II.16

III.1

6

IV.1

6

V.1

6

VI.1

6

VII.

16

VIII

.16

IX.1

6

X.1

6

XI.1

6

XII.

16 I.17

II.17

III.1

7

IV.1

7

V.1

7

VI.1

7

VII.

17

VIII

.17

IX.1

7

X.1

7

XI.1

7

XII.

17

Baseline scenario Economic downturnProlonged recession

Related Documents