Maban Host Community Food Security & Livelihood Assessment Maban County, Upper Nile State, South Sudan Project Title: Improve food and nutrition security through better agricultural practices, enhanced livestock health and strengthened resilience to external shocks Presented to European Commission Date of Publication: 9/1/2015 ACTED HQ 33, rue Godot de Mauroy 75009 Paris,France Tel: +33 1 42653333 [email protected] ACTED South Sudan, Juba Hai Malakal Opposite MSF Belgium Juba, Central Equatoria

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Maban Host Community Food

Security & Livelihood Assessment

Maban County, Upper Nile State,

South Sudan

Project Title:

Improve food and nutrition security through better agricultural practices,

enhanced livestock health and strengthened resilience to external shocks

Presented to European Commission

Date of Publication:

9/1/2015

ACTED HQ

33, rue Godot de Mauroy

75009 Paris,France

Tel: +33 1 42653333

ACTED South Sudan, Juba

Hai Malakal

Opposite MSF Belgium

Juba, Central Equatoria

ACTED – Maban Host Community Food Security & Livelihoods Assessment

1

Table of Contents

Executive Summary ................................................................................................................... 3

Background ................................................................................................................................ 5

Methodology .............................................................................................................................. 6

Survey Findings ......................................................................................................................... 6

Village Assessment Questionnaire ............................................................................................. 6

Demographic Profile ............................................................................................................... 6

Livelihoods & Food Security ................................................................................................... 8

Market Assessment Questionnaire ............................................................................................15

Market Demographic Profile ..................................................................................................15

Focus Group Discussion Findings .............................................................................................22

Kula 1 & 2 ..............................................................................................................................22

Pakaji East ............................................................................................................................24

Participatory Seasonal Calendar ...............................................................................................25

Conclusion ................................................................................................................................25

Recommendations ....................................................................................................................26

Annexes ....................................................................................................................................27

Annex I, Survey Questionnaire – Market Assessment ...........................................................27

Annex II, Survey Questionnaire – Village Assessment ..........................................................32

Table of Figures Figure 1 - Village Assessment Distribution ................................................................................. 6 Figure 2 - Household Occupation ............................................................................................... 7 Figure 3 - Livestock Type Owned by Households ...................................................................... 8 Figure 4 - Reported Livestock Deaths due to Untreated Disease ............................................... 8 Figure 5 - Main Water Source for Livestock ............................................................................... 9 Figure 6 - Common Crops Produced .........................................................................................10 Figure 7 - Common Months for Sale of Agro-Pastoral Produce to be Sold ................................10 Figure 8 - Reasons for Market Inaccessibility ............................................................................11 Figure 9 - Village Reliable Water Source...................................................................................12 Figure 10 - Identified NGOs Working in Host Community ..........................................................13 Figure 11 - Services Offered in Village Vicinity ..........................................................................13 Figure 12 - Services Identified as Useful if Offered in Maban ....................................................14 Figure 13 - Diversity of Market Traders Nationality ....................................................................15 Figure 14 - Types of Shops Found Within the Market................................................................16 Figure 15 - Items Sold During Dry Season & Rainy Season ......................................................17 Figure 16 - Source of Goods Sold in Bunj .................................................................................18 Figure 17 - Methods of Transport by Season ............................................................................18 Figure 18 - Challenges Identified to Purchasing More Local Products .......................................19

ACTED – Maban Host Community Food Security & Livelihoods Assessment

2

Figure 19 - External Shocks Identified by Vendors as Affecting their Business .........................20 Figure 20 - Length of Time Business was Affected by External Shocks ....................................21 Figure 21 - Distance of Market to Vendors Household ..............................................................22

Table 1 - Types of External Shocks Experienced in Past 12 Months .........................................20

ACTED – Maban Host Community Food Security & Livelihoods Assessment

3

Executive Summary

Project title: Improve food and nutrition security through better agricultural practices, enhanced livestock

health and strengthened resilience to external shocks

Donor &

project

duration:

European Commission – 36 months

Date of survey: September 1st – September 6th, 2015

Survey

objective: To assess the food security and resiliency of the host community villages in Maban County

Specific

objectives:

Determine current trends in agro-pastoral production

Assess community participation & coping mechanisms during external shocks & identify

which shocks have occurred over last 12 months

Identify the current trends of the market and those who utilize it

Identify potential challenges and opportunities in project implementation

Determine levels of access to water & its relation to food security for villages

Location: Maban County, Upper Nile State, South Sudan

Sample

methodology

& data

collection tool:

Convenience sampling was utilized in all of the 14 host community villages for the village

assessment questionnaire to ensure coverage of all communities relevant to project activities.

81 respondents provides us with at least 90% confidence level and 10% margin of error.

The market assessment utilized convenience sampling in Bunj to survey 101 vendors to

ensure 95% confidence level and 10% margin of error. Due to the close proximity of vendors

in the market, the AMEU field team would conduct an interview and skip one vendor to

eliminate collaboration or bias in the answers.

Community mobilization for the focus group discussions was conducted with the assistance

and cooperation of the food security & livelihoods department. Villages were targeted based

on their proximity to the market and to each other to determine issues that concern villages

throughout Maban County, both FGDs were conducted in villages targeted for this project

Findings

Summary:

Village Assessment

79% (n=64) of respondents stated that they own livestock or animals of some type

A large portion of households (53% n=34) had reported livestock deaths due to disease of

some sort in the past year

56% (n=45) stated less than a quarter own other types of livestock which is consistent with

the heavy reliance on household crop husbandry and only a small amount have livestock

72% (n=58) of respondents suggested that their main source of food was their own

agricultural production with only 23% (n=19) of respondents identifying with the market.

A large majority also reported that for all agro-pastoral crops they do not commonly sell

them in the market and most are only consumed at the household level

77% (n=62) only rely on human labour to transport goods into the market

ACTED – Maban Host Community Food Security & Livelihoods Assessment

4

Slaughter slabs were largely identified as being far away from most of the respondents with

23% (n=19) claiming it was too far to travel regularly to the site and 35% (n=28) stating

they did not know where a slaughter slab was located

53% (n=34) of respondents with livestock stated in the past year their livestock were

vaccinated by ICRC or VSF and 65% (n=22) of these respondents claimed they paid

between 50-100SSP for the vaccination service.

43% (n=35) of respondents stated it was too expensive to pay for veterinary services or

medicine and another 11% (n=9) claimed they were using local medicines as an alternative

Market Assessment

Most of the items sold in Bunj were sourced from either the local economy and producers,

as well as Juba, or Sudan with Ethiopia and Uganda represented slightly lower

During the rainy season, the percentage of vendors claiming they use road transport

significantly falls from 71% (n=72) to 44% (n=44)

Approximately 56% (n=57) of traders surveyed purchase either agro-pastoral products or

crafted items from the local producers to re-sell in their shops inside Bunj market

44% (n=44) of respondents stated that they only sold products that came from the

production of their own household

Only 42% (n=42) of respondents stated that they have experienced external shocks that

have effected their business in the past 12 months

Many identified primarily the economic shocks and the devaluation of the South Sudanese

Pound as the main shocks of the past 12 months (52% n=22). Others suggested conflict

(26% n=11). Only 15% (n=6) of respondents stated that livestock or agricultural disease

had effected them

71% (n=30) of those who had their business impacted by external shocks stated that higher

prices was the main effect for them. 57% (n=24) of the vendors claimed that the increase

in the product prices was an extreme increase. 93% (n=39) of vendors effected by external

shocks claimed they had to close for a month or less

ACTED – Maban Host Community Food Security & Livelihoods Assessment

5

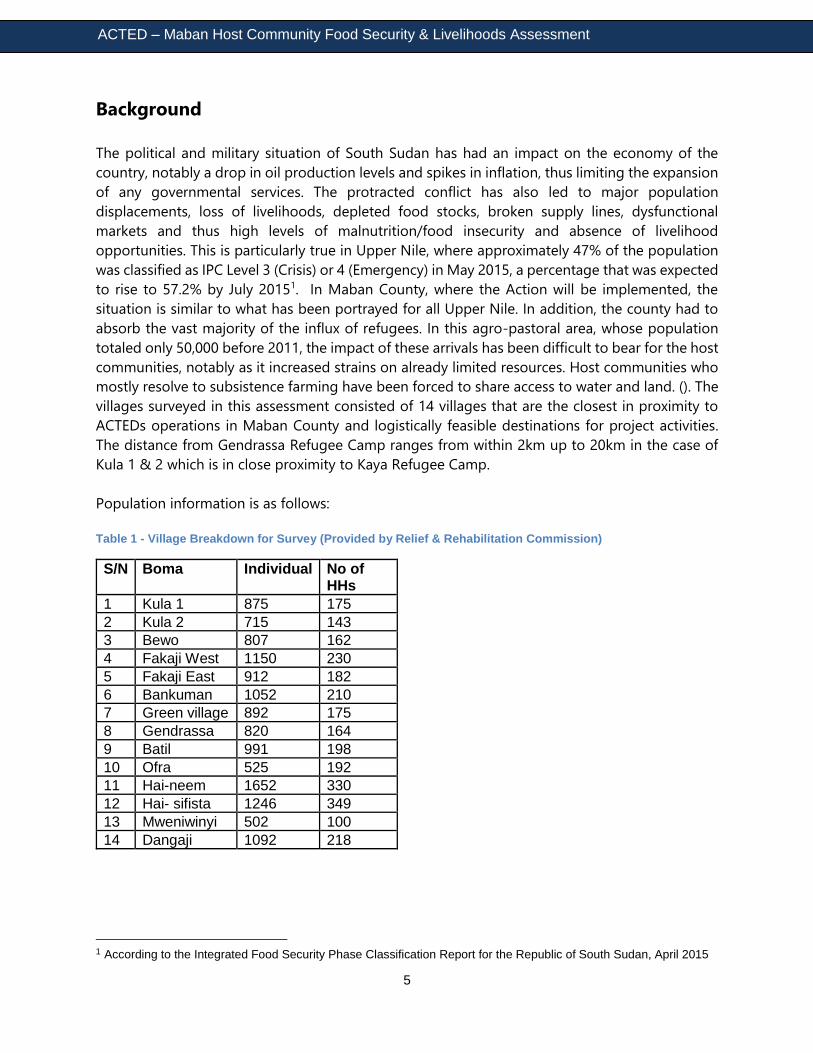

Background

The political and military situation of South Sudan has had an impact on the economy of the

country, notably a drop in oil production levels and spikes in inflation, thus limiting the expansion

of any governmental services. The protracted conflict has also led to major population

displacements, loss of livelihoods, depleted food stocks, broken supply lines, dysfunctional

markets and thus high levels of malnutrition/food insecurity and absence of livelihood

opportunities. This is particularly true in Upper Nile, where approximately 47% of the population

was classified as IPC Level 3 (Crisis) or 4 (Emergency) in May 2015, a percentage that was expected

to rise to 57.2% by July 20151. In Maban County, where the Action will be implemented, the

situation is similar to what has been portrayed for all Upper Nile. In addition, the county had to

absorb the vast majority of the influx of refugees. In this agro-pastoral area, whose population

totaled only 50,000 before 2011, the impact of these arrivals has been difficult to bear for the host

communities, notably as it increased strains on already limited resources. Host communities who

mostly resolve to subsistence farming have been forced to share access to water and land. (). The

villages surveyed in this assessment consisted of 14 villages that are the closest in proximity to

ACTEDs operations in Maban County and logistically feasible destinations for project activities.

The distance from Gendrassa Refugee Camp ranges from within 2km up to 20km in the case of

Kula 1 & 2 which is in close proximity to Kaya Refugee Camp.

Population information is as follows:

Table 1 - Village Breakdown for Survey (Provided by Relief & Rehabilitation Commission)

S/N Boma Individual No of HHs

1 Kula 1 875 175

2 Kula 2 715 143

3 Bewo 807 162

4 Fakaji West 1150 230

5 Fakaji East 912 182

6 Bankuman 1052 210

7 Green village 892 175

8 Gendrassa 820 164

9 Batil 991 198

10 Ofra 525 192

11 Hai-neem 1652 330

12 Hai- sifista 1246 349

13 Mweniwinyi 502 100

14 Dangaji 1092 218

1 According to the Integrated Food Security Phase Classification Report for the Republic of South Sudan, April 2015

ACTED – Maban Host Community Food Security & Livelihoods Assessment

6

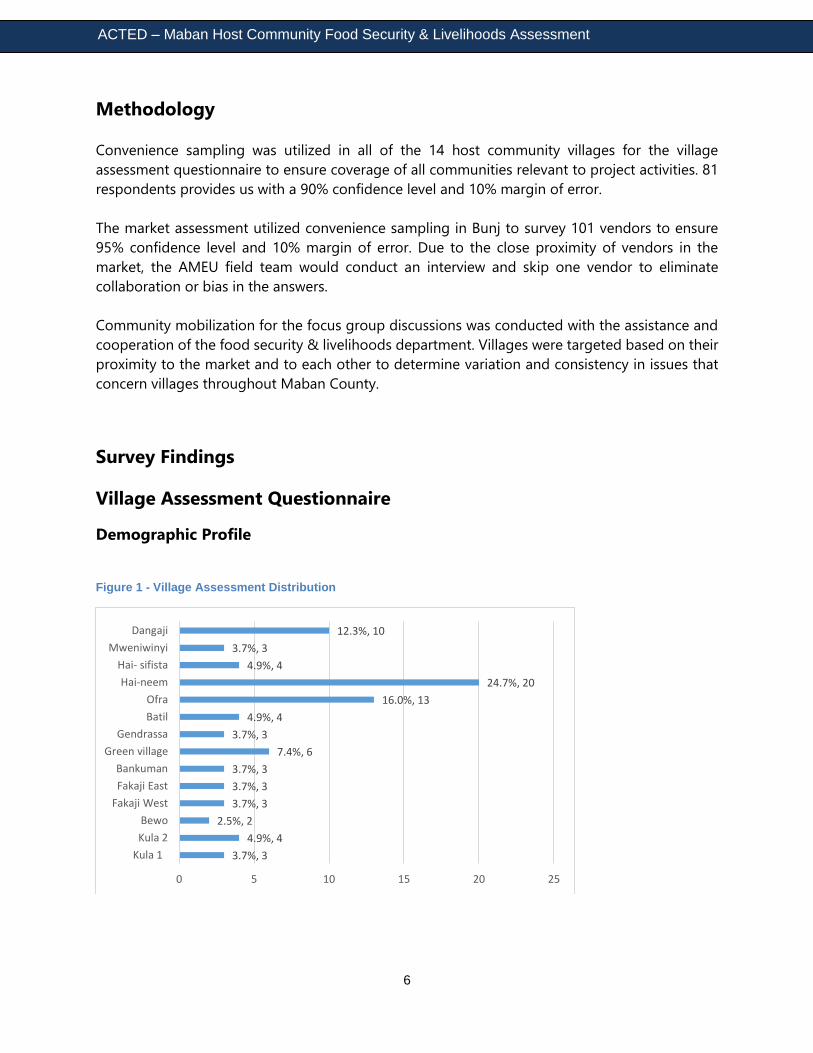

Methodology

Convenience sampling was utilized in all of the 14 host community villages for the village

assessment questionnaire to ensure coverage of all communities relevant to project activities. 81

respondents provides us with a 90% confidence level and 10% margin of error.

The market assessment utilized convenience sampling in Bunj to survey 101 vendors to ensure

95% confidence level and 10% margin of error. Due to the close proximity of vendors in the

market, the AMEU field team would conduct an interview and skip one vendor to eliminate

collaboration or bias in the answers.

Community mobilization for the focus group discussions was conducted with the assistance and

cooperation of the food security & livelihoods department. Villages were targeted based on their

proximity to the market and to each other to determine variation and consistency in issues that

concern villages throughout Maban County.

Survey Findings

Village Assessment Questionnaire

Demographic Profile

Figure 1 - Village Assessment Distribution

3.7%, 3

4.9%, 4

2.5%, 2

3.7%, 3

3.7%, 3

3.7%, 3

7.4%, 6

3.7%, 3

4.9%, 4

16.0%, 13

24.7%, 20

4.9%, 4

3.7%, 3

12.3%, 10

0 5 10 15 20 25

Kula 1

Kula 2

Bewo

Fakaji West

Fakaji East

Bankuman

Green village

Gendrassa

Batil

Ofra

Hai-neem

Hai- sifista

Mweniwinyi

Dangaji

ACTED – Maban Host Community Food Security & Livelihoods Assessment

7

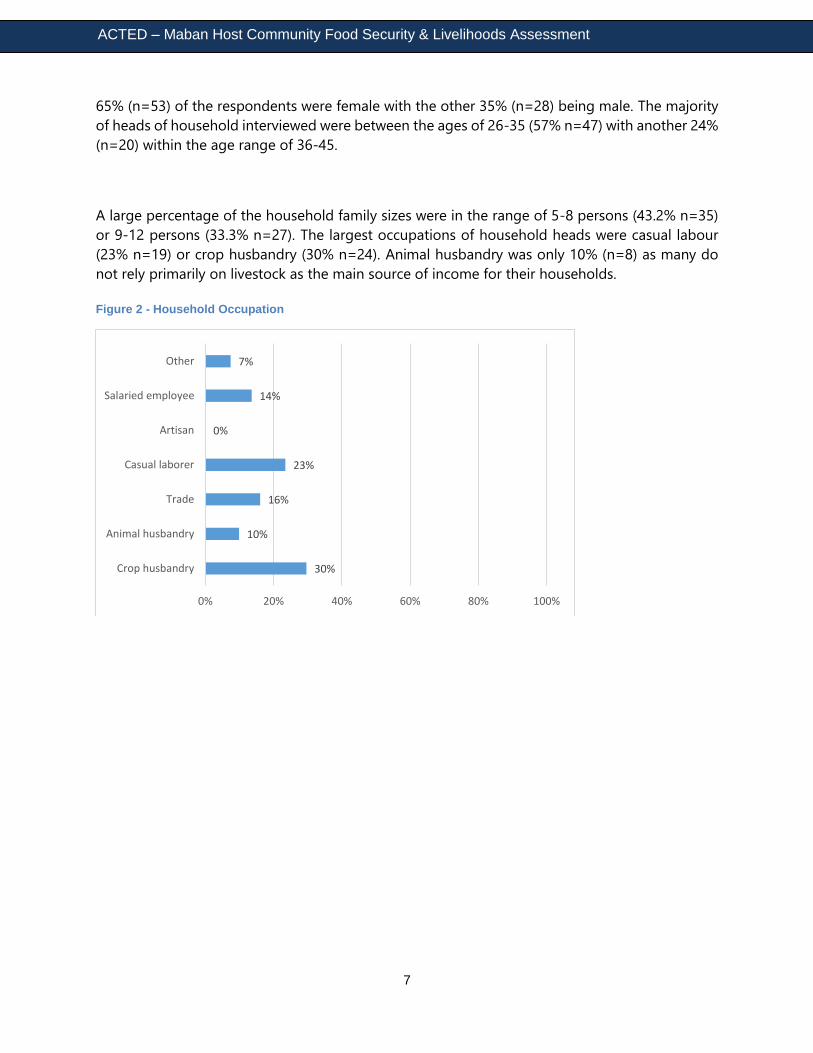

65% (n=53) of the respondents were female with the other 35% (n=28) being male. The majority

of heads of household interviewed were between the ages of 26-35 (57% n=47) with another 24%

(n=20) within the age range of 36-45.

A large percentage of the household family sizes were in the range of 5-8 persons (43.2% n=35)

or 9-12 persons (33.3% n=27). The largest occupations of household heads were casual labour

(23% n=19) or crop husbandry (30% n=24). Animal husbandry was only 10% (n=8) as many do

not rely primarily on livestock as the main source of income for their households.

Figure 2 - Household Occupation

30%

10%

16%

23%

0%

14%

7%

0% 20% 40% 60% 80% 100%

Crop husbandry

Animal husbandry

Trade

Casual laborer

Artisan

Salaried employee

Other

ACTED – Maban Host Community Food Security & Livelihoods Assessment

8

Livelihoods & Food Security

79% (n=64) of respondents stated that they own livestock or animals of some type. The most

common livestock types owned by households are goats (80% n=51), pigs (86% n=55), and

chickens (77% n=49).

Figure 3 - Livestock Type Owned by Households

Cattle was only owned by 17% (n=11) of the respondents. Most of the respondents stated that

they owned between 11-20 cattle, goats, or sheep (36% n=23) with another 31% (n=20) stating

1-5 animals, and 19% (n=12) between 6-10 animals. For poultry, (58% n=37), most of the

respondents owned 1-10 chickens or ducks per household. Another 23% (n=15) of respondents

did not own any poultry.

Figure 4 - Reported Livestock Deaths due to Untreated Disease

17%

80%

2%

86%

77%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cattle Goats Sheep Pigs Chicken Donkey

2%

53%

23%

13%

2%

8%

0% 20% 40% 60% 80% 100%

None died from disease

1-5 animals

6-10 animals

11-15 animals

16-20 animals

20 or more

ACTED – Maban Host Community Food Security & Livelihoods Assessment

9

A large portion of households (53% n=34) had reported livestock deaths due to disease of some

sort in the past year. Additionally a large majority of households (56% n=36) slaughter 1-5 animals

for their own household consumption in a month. 52% (n=33) of households have sold 1-5

animals this month alone. This may be slightly higher, according to some respondents spoken to

in the focus group discussions, due to the concerns over lack of rain over the past few months

which continues to delay crop growth and harvesting. 78% (n=63) of respondents stated that less

than a quarter of the residents in their community own cattle specifically. 56% (n=45) stated less

than a quarter own other types of livestock which is consistent with the data reporting heavy

reliance on household crop husbandry and only a small amount, allegedly, have livestock

regularly. This also indicates that perceptions of livestock ownership amongst community

members is much lower than reported by the household owners themselves. 63% (n=40) of

respondents stated that the grazing and waterhole they use for their livestock is relatively close

to their household averaging 10-20 minutes’ walk, with another 28% (n=18) claiming 30-40

minutes on average. As shown in figure 5 below, there are still a large number of households

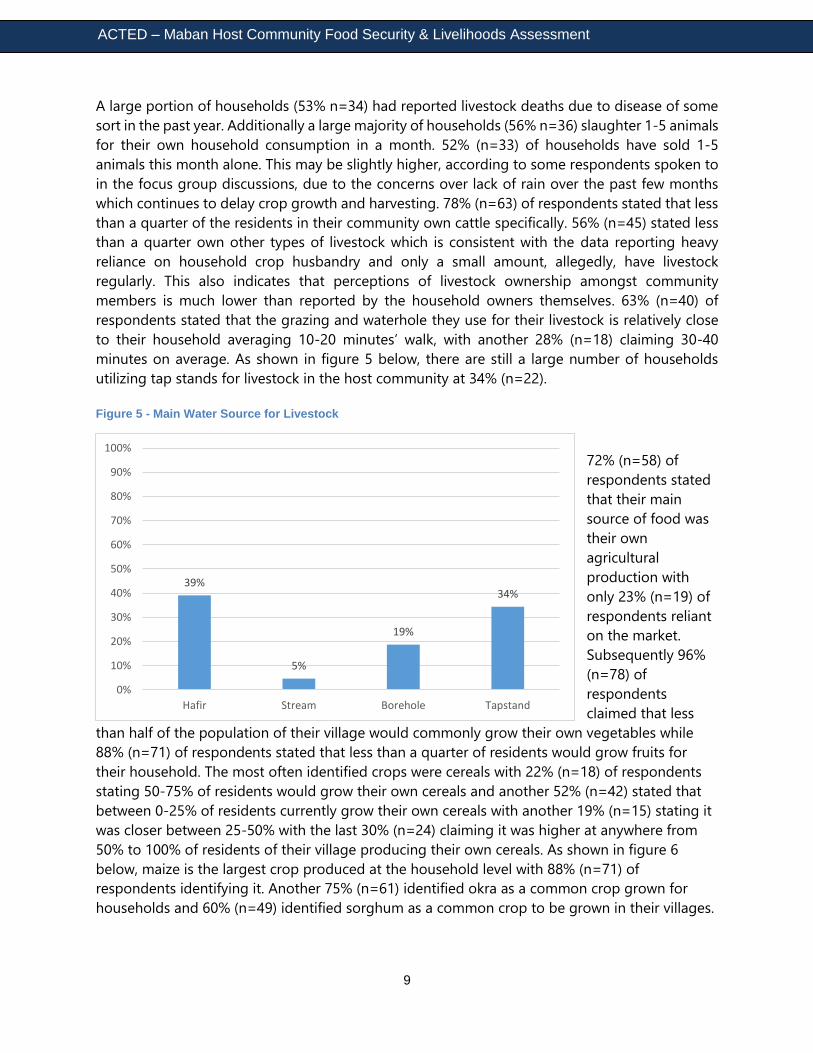

utilizing tap stands for livestock in the host community at 34% (n=22).

Figure 5 - Main Water Source for Livestock

72% (n=58) of

respondents stated

that their main

source of food was

their own

agricultural

production with

only 23% (n=19) of

respondents reliant

on the market.

Subsequently 96%

(n=78) of

respondents

claimed that less

than half of the population of their village would commonly grow their own vegetables while

88% (n=71) of respondents stated that less than a quarter of residents would grow fruits for

their household. The most often identified crops were cereals with 22% (n=18) of respondents

stating 50-75% of residents would grow their own cereals and another 52% (n=42) stated that

between 0-25% of residents currently grow their own cereals with another 19% (n=15) stating it

was closer between 25-50% with the last 30% (n=24) claiming it was higher at anywhere from

50% to 100% of residents of their village producing their own cereals. As shown in figure 6

below, maize is the largest crop produced at the household level with 88% (n=71) of

respondents identifying it. Another 75% (n=61) identified okra as a common crop grown for

households and 60% (n=49) identified sorghum as a common crop to be grown in their villages.

39%

5%

19%

34%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hafir Stream Borehole Tapstand

ACTED – Maban Host Community Food Security & Livelihoods Assessment

10

Figure 6 - Common Crops Produced

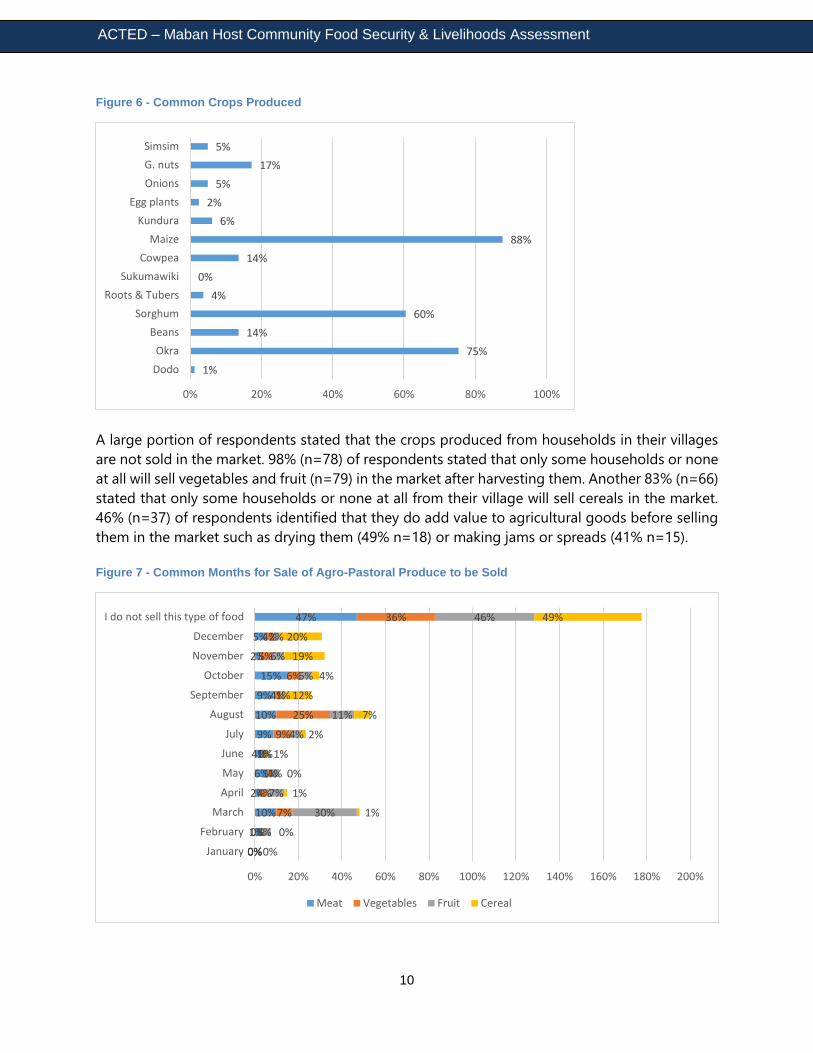

A large portion of respondents stated that the crops produced from households in their villages

are not sold in the market. 98% (n=78) of respondents stated that only some households or none

at all will sell vegetables and fruit (n=79) in the market after harvesting them. Another 83% (n=66)

stated that only some households or none at all from their village will sell cereals in the market.

46% (n=37) of respondents identified that they do add value to agricultural goods before selling

them in the market such as drying them (49% n=18) or making jams or spreads (41% n=15).

Figure 7 - Common Months for Sale of Agro-Pastoral Produce to be Sold

1%

75%

14%

60%

4%

0%

14%

88%

6%

2%

5%

17%

5%

0% 20% 40% 60% 80% 100%

Dodo

Okra

Beans

Sorghum

Roots & Tubers

Sukumawiki

Cowpea

Maize

Kundura

Egg plants

Onions

G. nuts

Simsim

0%

1%

10%

2%

6%

4%

9%

10%

9%

15%

2%

5%

47%

0%

0%

7%

4%

1%

1%

9%

25%

4%

6%

5%

4%

36%

0%

6%

30%

7%

4%

0%

4%

11%

1%

5%

6%

2%

46%

0%

0%

1%

1%

0%

1%

2%

7%

12%

4%

19%

20%

49%

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 200%

January

February

March

April

May

June

July

August

September

October

November

December

I do not sell this type of food

Meat Vegetables Fruit Cereal

ACTED – Maban Host Community Food Security & Livelihoods Assessment

11

As you can see in Figure 7 above, a large majority also reported that for all agro-pastoral crops

they do not commonly sell them in the market and most are only consumed at the household

level. However there were some notable months such as August, December, and November for

cereals and August for vegetables as well. January and February were not reported at all for any

produce sold. Only 67% (n=54) of respondents suggested that the closest market to their village

was easily accessible for themselves and their family members. As Figure 8 shows, distance was a

strong factor in the lack of access on a regular basis to the closest markets with lack of transport

obviously adding to the stress of village isolation. Subsequently a majority (74% n=60) of

respondents identified their villages as being below average for economic opportunity and status

compared to other villages in Maban County.

Figure 8 - Reasons for Market Inaccessibility

77% (n=62) only rely on human labour to transport goods into the market with nobody identifying

any other method of transport. Another 14% (n=11) stated they do not take products to the

market. Slaughter slabs were largely identified as being far away from most of the respondents

with 23% (n=19) claiming it was too far to travel regularly to the site and 35% (n=28) stating they

did not know where a slaughter slab was located. According to the AMEU field team the only

slaughter slab is located near Bunj and therefore a large portion of respondents who live in villages

further away would have no realistic means of using the slab and would generally have little idea

of where it is located. Many of the villages would easily take several hours at minimum to walk

their livestock to the slab and then transport of the product back to the village would be nearly

impossible. 28% (n=23) stated it was in their village, however this was more highly reported in

those villages close to Bunj as they have a much closer proximity to each other and have relatively

equal access to a slaughter slab near the town. 38% (n=31) of respondents claimed that the

government inspected the animals being slaughtered in this way but whether they have witnessed

government authorities performing this activity themselves is still to be determined. A majority of

animal carcasses were burned (48% n=39) with another 37% (n=30) disposing of the carcass away

from the household.

56%

15%

30%

Distance Bad road during rainy season Lack of transport

ACTED – Maban Host Community Food Security & Livelihoods Assessment

12

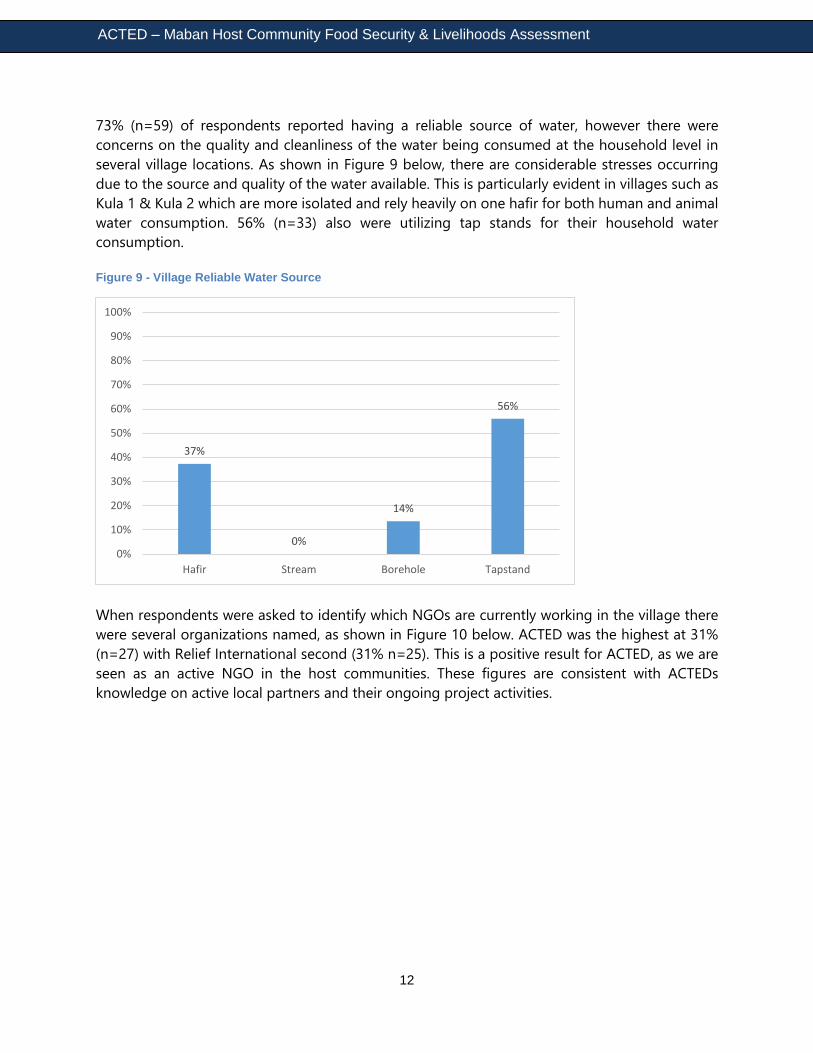

73% (n=59) of respondents reported having a reliable source of water, however there were

concerns on the quality and cleanliness of the water being consumed at the household level in

several village locations. As shown in Figure 9 below, there are considerable stresses occurring

due to the source and quality of the water available. This is particularly evident in villages such as

Kula 1 & Kula 2 which are more isolated and rely heavily on one hafir for both human and animal

water consumption. 56% (n=33) also were utilizing tap stands for their household water

consumption.

Figure 9 - Village Reliable Water Source

When respondents were asked to identify which NGOs are currently working in the village there

were several organizations named, as shown in Figure 10 below. ACTED was the highest at 31%

(n=27) with Relief International second (31% n=25). This is a positive result for ACTED, as we are

seen as an active NGO in the host communities. These figures are consistent with ACTEDs

knowledge on active local partners and their ongoing project activities.

37%

0%

14%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hafir Stream Borehole Tapstand

ACTED – Maban Host Community Food Security & Livelihoods Assessment

13

Figure 10 - Identified NGOs Working in Host Community

Figure 11 - Services Offered in Village Vicinity

The largest service identified was health (67% n=54) and food security (35% n=28). 56% (n=45)

of respondents also mentioned that there were animal health services located in the area of their

village. However it was also noted that several village members had been trained in the use of

animal health but no longer could obtain medicine or tools to perform the work. 43% (n=35) of

livestock owners stated that they could not access drugs at any point in time with others

suggesting it is sometimes available in the open market (17% n=14) or by the veterinary pharmacy

(19% n=15). These may have been offered in the past but it was noted by many respondents that

drugs for animal health were generally not offered consistently. 53% (n=34) of respondents with

livestock stated in the past year their livestock were vaccinated by ICRC or VSF and 65% (n=22) of

6%

12%

4%

33%

2%

31%

23%

0% 20% 40% 60% 80% 100%

Medair

MSF

LWF

ACTED

DRC

Relief International

None

67%

5%

20%

35%

4%

4%

0% 20% 40% 60% 80% 100%

Health

Education

WASH

Food Security & Livelihoods (incomegeneration, food security, vocational…

Protection for women, children, elderly

Early childhood development

ACTED – Maban Host Community Food Security & Livelihoods Assessment

14

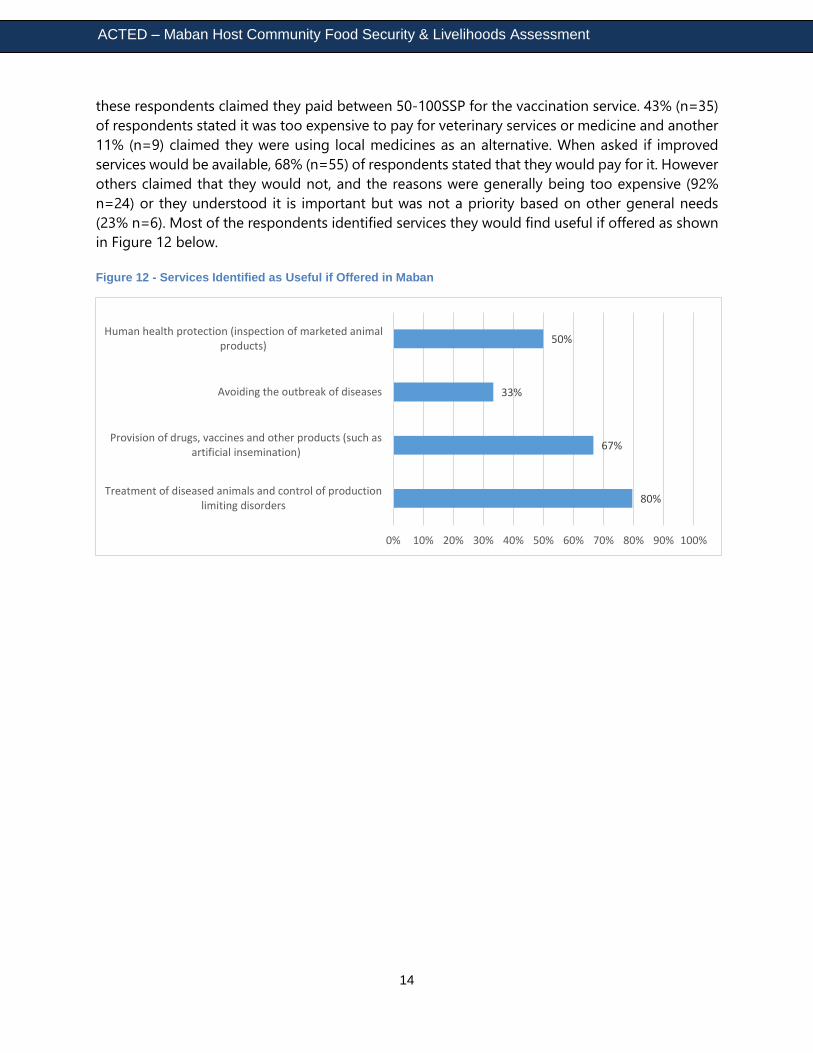

these respondents claimed they paid between 50-100SSP for the vaccination service. 43% (n=35)

of respondents stated it was too expensive to pay for veterinary services or medicine and another

11% (n=9) claimed they were using local medicines as an alternative. When asked if improved

services would be available, 68% (n=55) of respondents stated that they would pay for it. However

others claimed that they would not, and the reasons were generally being too expensive (92%

n=24) or they understood it is important but was not a priority based on other general needs

(23% n=6). Most of the respondents identified services they would find useful if offered as shown

in Figure 12 below.

Figure 12 - Services Identified as Useful if Offered in Maban

80%

67%

33%

50%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Treatment of diseased animals and control of productionlimiting disorders

Provision of drugs, vaccines and other products (such asartificial insemination)

Avoiding the outbreak of diseases

Human health protection (inspection of marketed animalproducts)

ACTED – Maban Host Community Food Security & Livelihoods Assessment

15

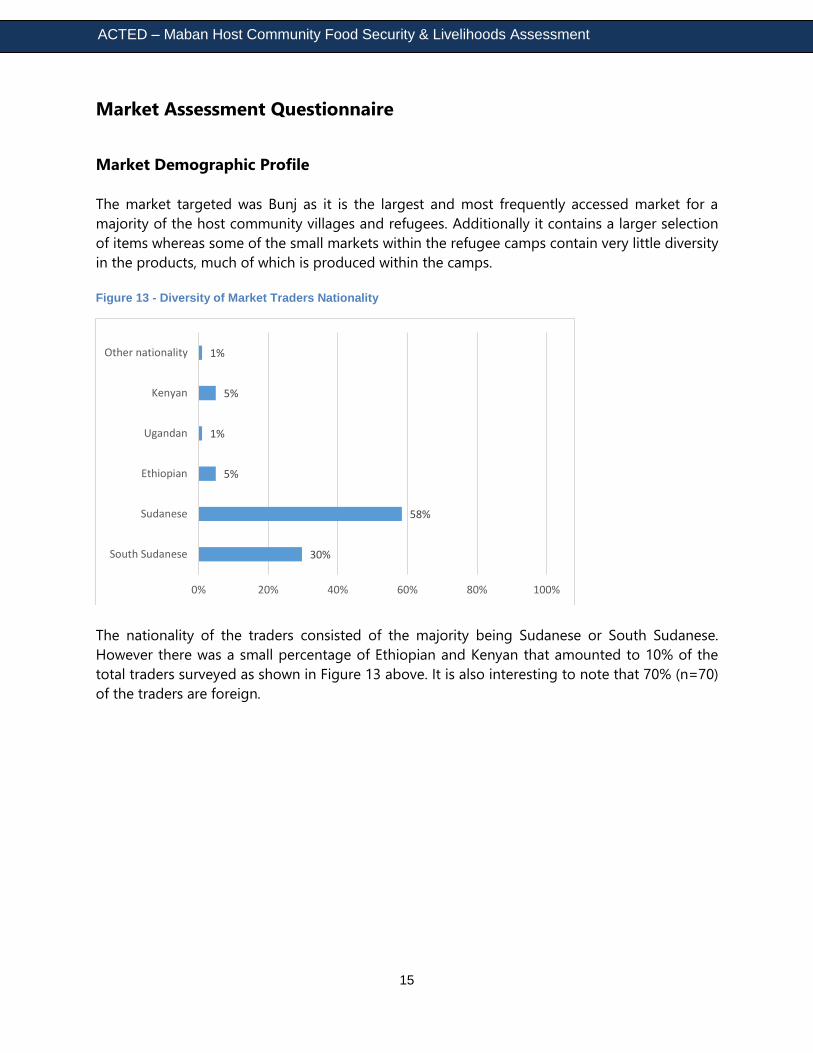

Market Assessment Questionnaire

Market Demographic Profile

The market targeted was Bunj as it is the largest and most frequently accessed market for a

majority of the host community villages and refugees. Additionally it contains a larger selection

of items whereas some of the small markets within the refugee camps contain very little diversity

in the products, much of which is produced within the camps.

Figure 13 - Diversity of Market Traders Nationality

The nationality of the traders consisted of the majority being Sudanese or South Sudanese.

However there was a small percentage of Ethiopian and Kenyan that amounted to 10% of the

total traders surveyed as shown in Figure 13 above. It is also interesting to note that 70% (n=70)

of the traders are foreign.

30%

58%

5%

1%

5%

1%

0% 20% 40% 60% 80% 100%

South Sudanese

Sudanese

Ethiopian

Ugandan

Kenyan

Other nationality

ACTED – Maban Host Community Food Security & Livelihoods Assessment

16

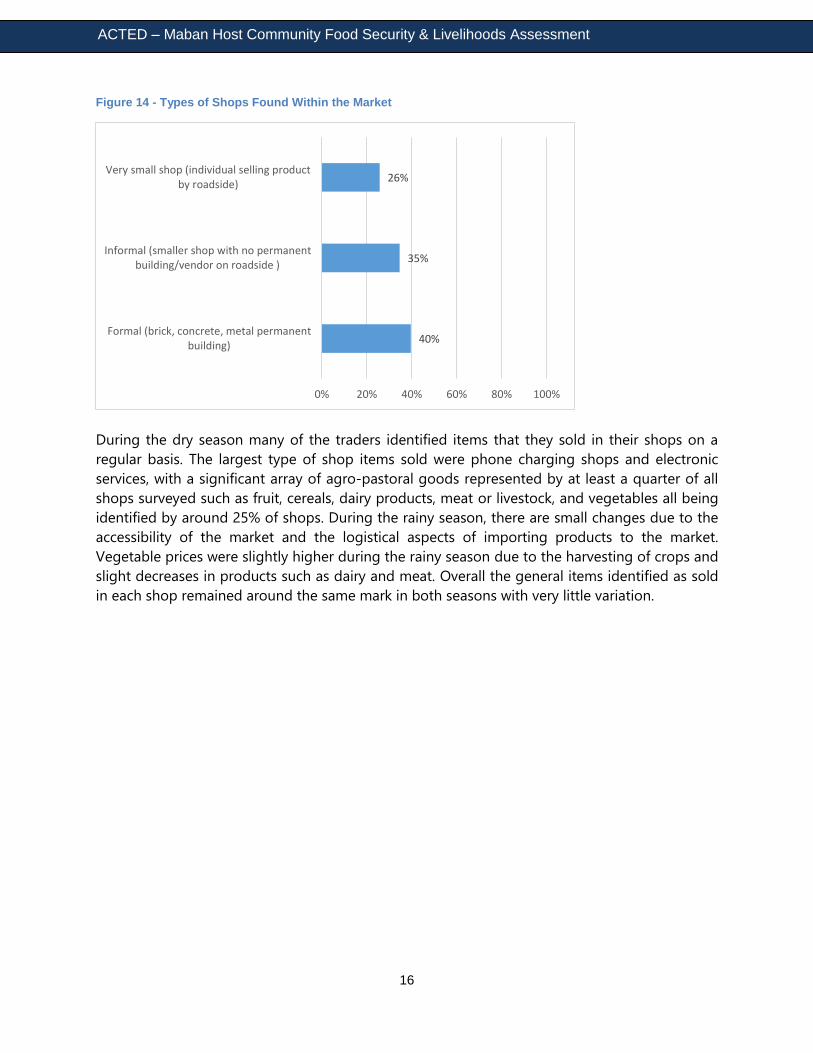

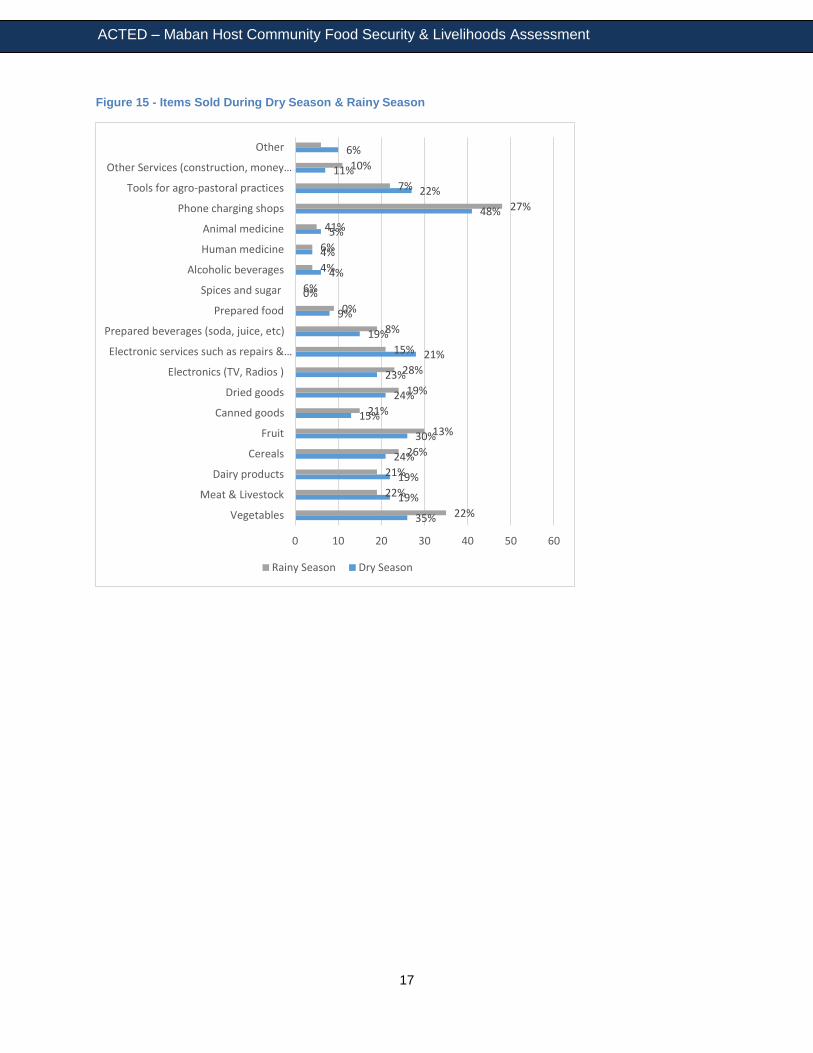

Figure 14 - Types of Shops Found Within the Market

During the dry season many of the traders identified items that they sold in their shops on a

regular basis. The largest type of shop items sold were phone charging shops and electronic

services, with a significant array of agro-pastoral goods represented by at least a quarter of all

shops surveyed such as fruit, cereals, dairy products, meat or livestock, and vegetables all being

identified by around 25% of shops. During the rainy season, there are small changes due to the

accessibility of the market and the logistical aspects of importing products to the market.

Vegetable prices were slightly higher during the rainy season due to the harvesting of crops and

slight decreases in products such as dairy and meat. Overall the general items identified as sold

in each shop remained around the same mark in both seasons with very little variation.

40%

35%

26%

0% 20% 40% 60% 80% 100%

Formal (brick, concrete, metal permanentbuilding)

Informal (smaller shop with no permanentbuilding/vendor on roadside )

Very small shop (individual selling productby roadside)

ACTED – Maban Host Community Food Security & Livelihoods Assessment

17

Figure 15 - Items Sold During Dry Season & Rainy Season

35%

19%

19%

24%

30%

15%

24%

23%

21%

19%

9%

0%

4%

4%

5%

48%

22%

11%

6%

22%

22%

21%

26%

13%

21%

19%

28%

15%

8%

0%

6%

4%

6%

41%

27%

7%

10%

0 10 20 30 40 50 60

Vegetables

Meat & Livestock

Dairy products

Cereals

Fruit

Canned goods

Dried goods

Electronics (TV, Radios )

Electronic services such as repairs &…

Prepared beverages (soda, juice, etc)

Prepared food

Spices and sugar

Alcoholic beverages

Human medicine

Animal medicine

Phone charging shops

Tools for agro-pastoral practices

Other Services (construction, money…

Other

Rainy Season Dry Season

ACTED – Maban Host Community Food Security & Livelihoods Assessment

18

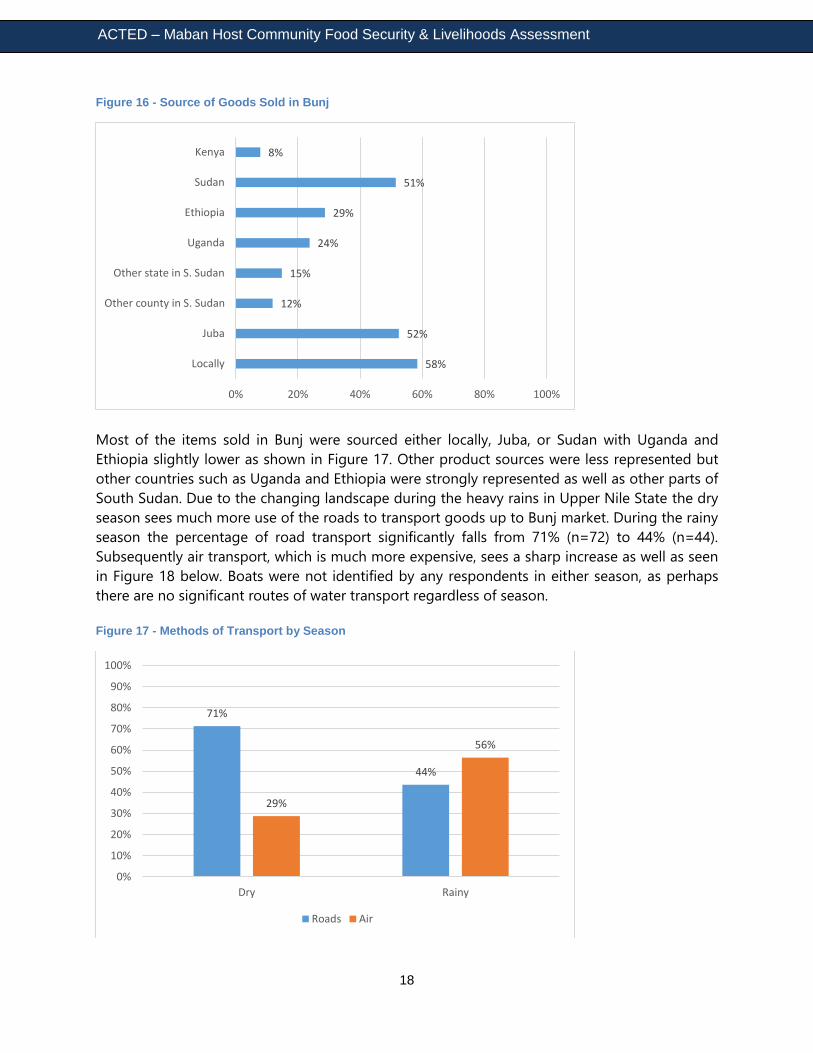

Figure 16 - Source of Goods Sold in Bunj

Most of the items sold in Bunj were sourced either locally, Juba, or Sudan with Uganda and

Ethiopia slightly lower as shown in Figure 17. Other product sources were less represented but

other countries such as Uganda and Ethiopia were strongly represented as well as other parts of

South Sudan. Due to the changing landscape during the heavy rains in Upper Nile State the dry

season sees much more use of the roads to transport goods up to Bunj market. During the rainy

season the percentage of road transport significantly falls from 71% (n=72) to 44% (n=44).

Subsequently air transport, which is much more expensive, sees a sharp increase as well as seen

in Figure 18 below. Boats were not identified by any respondents in either season, as perhaps

there are no significant routes of water transport regardless of season.

Figure 17 - Methods of Transport by Season

58%

52%

12%

15%

24%

29%

51%

8%

0% 20% 40% 60% 80% 100%

Locally

Juba

Other county in S. Sudan

Other state in S. Sudan

Uganda

Ethiopia

Sudan

Kenya

71%

44%

29%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dry Rainy

Roads Air

ACTED – Maban Host Community Food Security & Livelihoods Assessment

19

Approximately 56% (n=57) of traders surveyed purchase either agro-pastoral products or crafted

items from the local producers to re-sell in their shops inside Bunj market. The other 44% (n=44)

respondents stated that they only sold products that came from the production of their own

household. Therefore there is a strong mix of both traders and those who are utilizing the market

to sell products directly from their household’s agricultural and pastoral production. Out of those

vendors who purchase local products they overwhelmingly sold local raw vegetables or prepared

goods such as cooked food, spiced or prepared local products. Only 4% (n=2) of these vendors

identified livestock as a purchase.

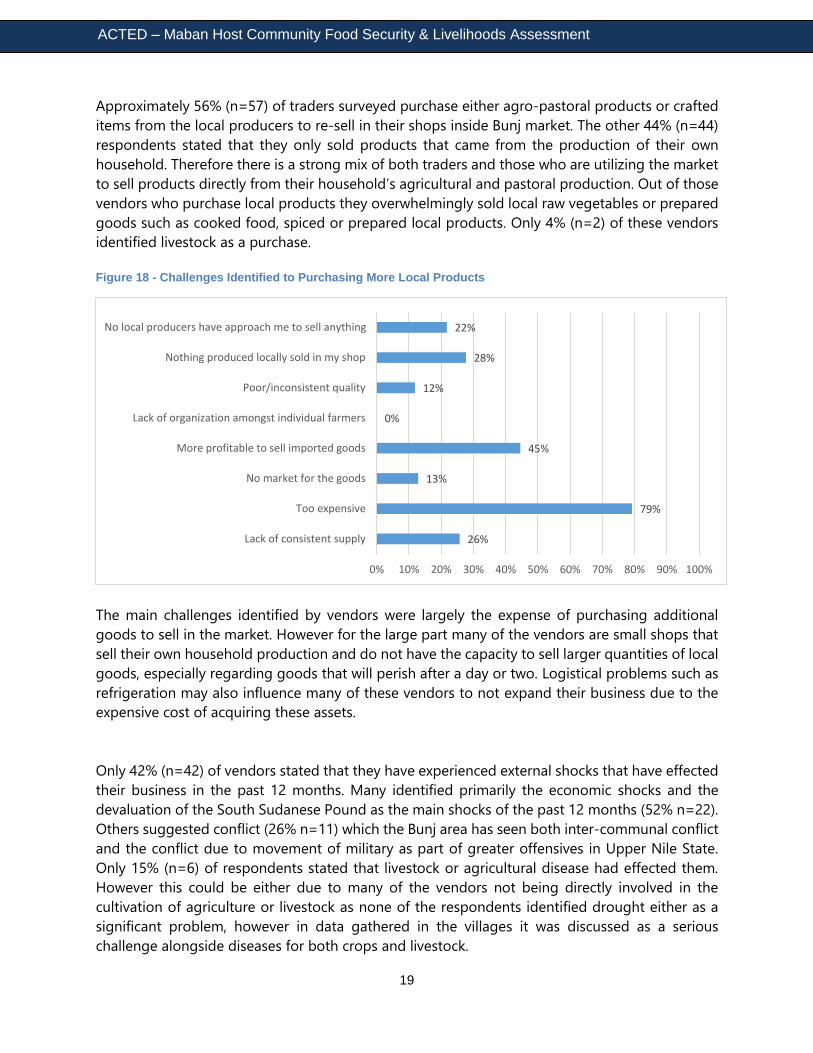

Figure 18 - Challenges Identified to Purchasing More Local Products

The main challenges identified by vendors were largely the expense of purchasing additional

goods to sell in the market. However for the large part many of the vendors are small shops that

sell their own household production and do not have the capacity to sell larger quantities of local

goods, especially regarding goods that will perish after a day or two. Logistical problems such as

refrigeration may also influence many of these vendors to not expand their business due to the

expensive cost of acquiring these assets.

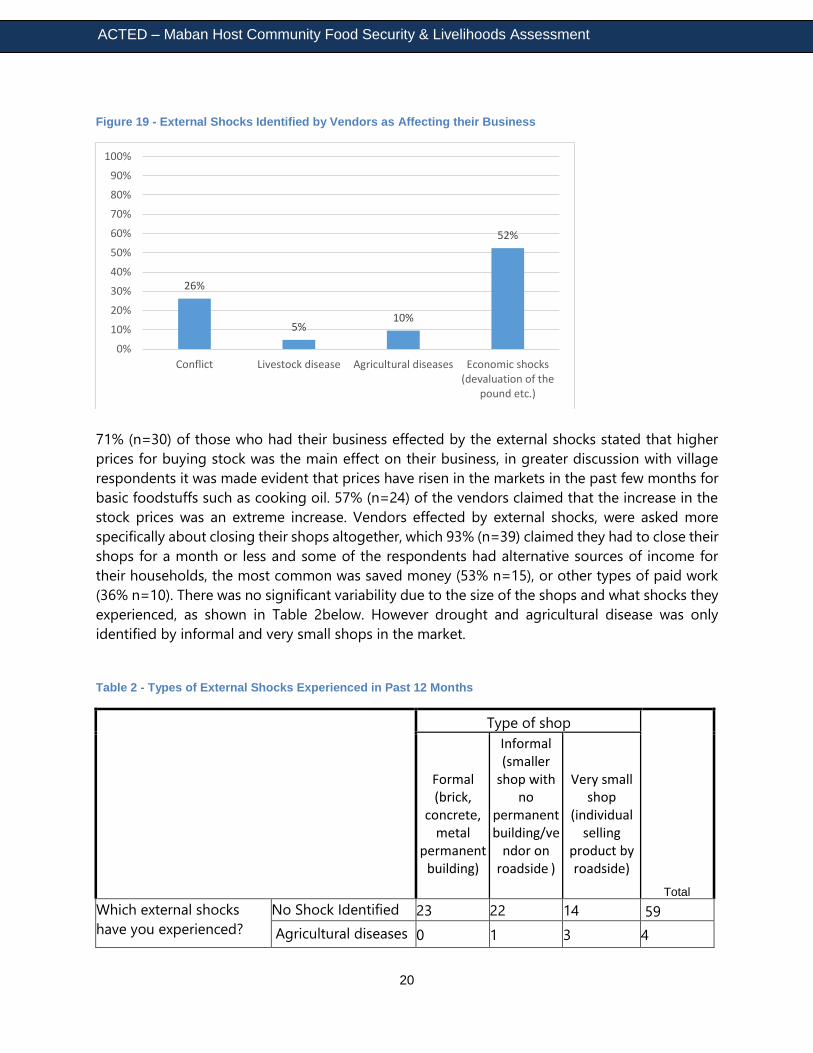

Only 42% (n=42) of vendors stated that they have experienced external shocks that have effected

their business in the past 12 months. Many identified primarily the economic shocks and the

devaluation of the South Sudanese Pound as the main shocks of the past 12 months (52% n=22).

Others suggested conflict (26% n=11) which the Bunj area has seen both inter-communal conflict

and the conflict due to movement of military as part of greater offensives in Upper Nile State.

Only 15% (n=6) of respondents stated that livestock or agricultural disease had effected them.

However this could be either due to many of the vendors not being directly involved in the

cultivation of agriculture or livestock as none of the respondents identified drought either as a

significant problem, however in data gathered in the villages it was discussed as a serious

challenge alongside diseases for both crops and livestock.

26%

79%

13%

45%

0%

12%

28%

22%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Lack of consistent supply

Too expensive

No market for the goods

More profitable to sell imported goods

Lack of organization amongst individual farmers

Poor/inconsistent quality

Nothing produced locally sold in my shop

No local producers have approach me to sell anything

ACTED – Maban Host Community Food Security & Livelihoods Assessment

20

Figure 19 - External Shocks Identified by Vendors as Affecting their Business

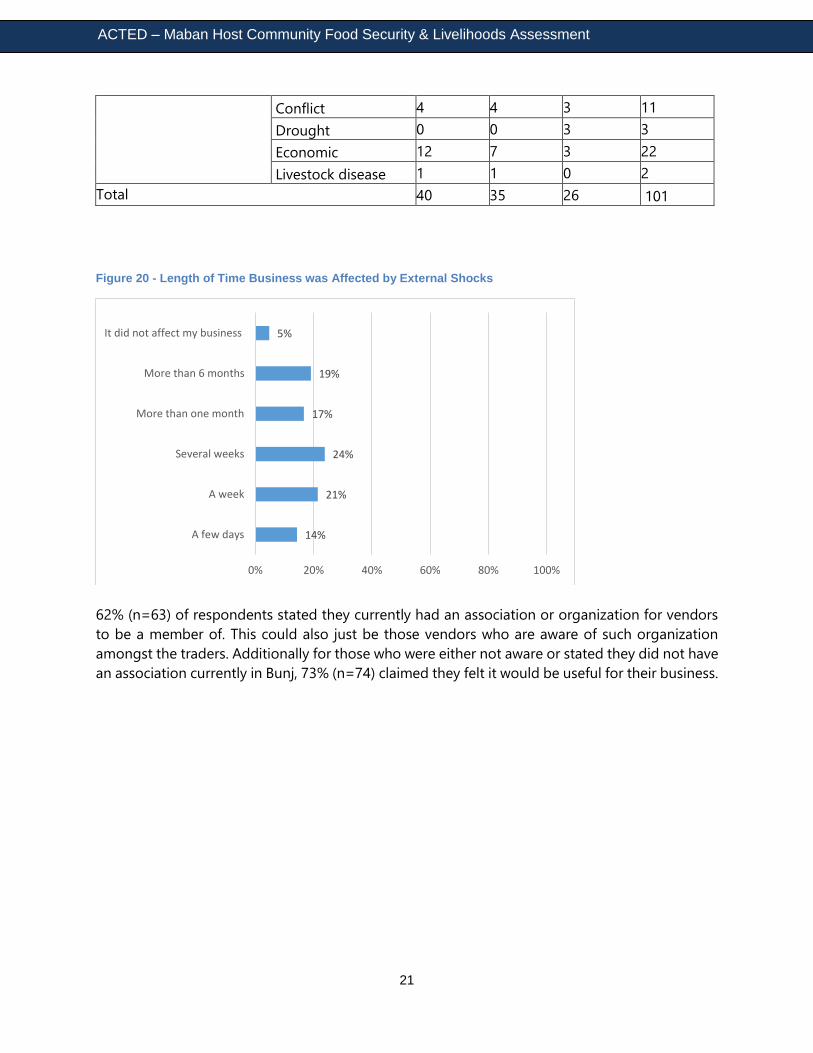

71% (n=30) of those who had their business effected by the external shocks stated that higher

prices for buying stock was the main effect on their business, in greater discussion with village

respondents it was made evident that prices have risen in the markets in the past few months for

basic foodstuffs such as cooking oil. 57% (n=24) of the vendors claimed that the increase in the

stock prices was an extreme increase. Vendors effected by external shocks, were asked more

specifically about closing their shops altogether, which 93% (n=39) claimed they had to close their

shops for a month or less and some of the respondents had alternative sources of income for

their households, the most common was saved money (53% n=15), or other types of paid work

(36% n=10). There was no significant variability due to the size of the shops and what shocks they

experienced, as shown in Table 2below. However drought and agricultural disease was only

identified by informal and very small shops in the market.

Table 2 - Types of External Shocks Experienced in Past 12 Months

Type of shop

Total

Formal (brick,

concrete, metal

permanent building)

Informal (smaller

shop with no

permanent building/ve

ndor on roadside )

Very small shop

(individual selling

product by roadside)

Which external shocks

have you experienced?

No Shock Identified 23 22 14 59

Agricultural diseases 0 1 3 4

26%

5%10%

52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Conflict Livestock disease Agricultural diseases Economic shocks(devaluation of the

pound etc.)

ACTED – Maban Host Community Food Security & Livelihoods Assessment

21

Conflict 4 4 3 11

Drought 0 0 3 3

Economic 12 7 3 22

Livestock disease 1 1 0 2

Total 40 35 26 101

Figure 20 - Length of Time Business was Affected by External Shocks

62% (n=63) of respondents stated they currently had an association or organization for vendors

to be a member of. This could also just be those vendors who are aware of such organization

amongst the traders. Additionally for those who were either not aware or stated they did not have

an association currently in Bunj, 73% (n=74) claimed they felt it would be useful for their business.

14%

21%

24%

17%

19%

5%

0% 20% 40% 60% 80% 100%

A few days

A week

Several weeks

More than one month

More than 6 months

It did not affect my business

ACTED – Maban Host Community Food Security & Livelihoods Assessment

22

Figure 21 - Distance of Market to Vendors Household

The distance of travel from households to the Bunj market for vendors was spread across the

board with the large majority living within a 1 hour walk of the market. However there was 16%

(n=16) respondents who stated they walked for more than one hour at least. Some of the more

isolated villages would generally travel up to a day to reach Bunj on foot and would not regularly

do business in the market without improved transportation, this corresponds to the comments

above by villagers where generally Bunj market is only accessible for those villages bordering the

market. 94% (n=95) of the respondents claimed their access to the market was at least average

with 77% (n=78) rating access to the market from their household as extremely good or very

good. This implies that most of the vendors surveyed in Bunj are not from the more isolated

villages in Maban and much of the vendors reside within a small radius of the market.

Focus Group Discussion Findings

Kula 1 & 2

FGD Background

The focus groups attracted a large number of both men & women from the communities Kula 1

& Kula 2 which came together to discuss the challenges faced by both villages due to their

relatively close proximity to each other. Kula 1 & 2 faced significant challenges due to their

isolation from the largest market Bunj, and consequently even ten kilometres roughly from the

closest small market in Kaya Refugee Camp or nearby Offra. Therefore the villages are not in as

close proximity to the refugee camps as other host community villages are. Generally if they do

not access the Kaya refugee camp market it will take about a day travel both ways either to Bunj

40%

21%

24%

11%

5%

0% 20% 40% 60% 80% 100%

Less than 10 minutes’ walk

11-30 minutes’ walk

31 minutes – 1 hour walk

1-2 hours walk

More than 2 hours walk

ACTED – Maban Host Community Food Security & Livelihoods Assessment

23

or Jamam without access to a vehicle. Therefore the hafir and water supply are solely utilized by

their villages and other smaller villages in the area.

Community Challenges

Community members identified several distinct challenges, when asked about the main concerns

that they experience on a day-to-day basis: Water, Food (seeds), human & animal health,

education, & agricultural support (e.g. grinding mills).

Community members expressed serious concern over the annual drought that has occurred for

the past several months in Maban. This has significantly affected crop production with huge

depletion of food stocks without replenishment. If the crops do not grow well enough due to the

drought there will be significant food insecurity in the area. Some community members claimed

they had witnessed crops being infested by insects and they could not prevent this. Coping

mechanisms were identified such as the selling of timber, in the form of firewood or charcoal,

from nearby forests to ensure an income for households. This has contributed to the deforestation

of the region and long term will reinforce the challenges related to drought. Livestock was also

identified to have suffered some ailments such as diarrhea by pastoralists in the community. Most

of the members of the community only had around 2-5 livestock on average each and so when

they sold livestock for money or food in the market due to lack of agricultural production it is a

severe loss of assets for a household, however this would be a very severe coping mechanism for

many households and would not occur until there was a clear and sustained drought and crops

have not produced by September or October during which initial crop harvest should take place

according to the community. Members of the community discussed that there was a grinding mill

provided to the community but the community lacks the technical knowledge for its maintenance

as well as the capacity to replace parts when they fall into disrepair, however the FSL technical

team identified the machine as a high quality brand when it was shown to the ACTED team.

Water was the main issue highlighted for these communities, as they were now obtaining water

for both animal and human consumption from a hafir that was built previously by ACTED solely

for the host community. There were previous attempts to construct functioning tap stands in Kula

1 by OXFAM however they have ceased to function properly and require maintenance. Some

community members explained that there were functioning tap stands but there was both a lack

of technical knowledge for maintenance on the motor as well as a lack of material for replacement

in case parts broke. Therefore it would seem more self-sustaining approaches would be useful in

the more remote villages for the provision of water. Additionally the community members brought

up that the tap stand attracted other villages further out to come utilize their water supply which

could not provide enough water for both their own households and the other villages.

The community brought up the fact that they had high capacity to mobilize as a community when

they were facing challenges and often worked together to resolve the problems identified above.

However after they discussed as a community they noted there is little capacity through official

government channels to resolve any of these issues so they have reported several times to the

ACTED – Maban Host Community Food Security & Livelihoods Assessment

24

commissioner through the local Sheikh. The villagers seemed to be slightly discouraged by both

the actions of NGOs and local authorities up until this point. They noted both failed projects by

NGOs in their village, as well as, no feedback from local authorities. To be realistic the government

has very little presence in the area and therefore any action on their behalf would not satisfy the

communities material requirements yet they also stressed it would be useful to receive feedback

on where the reports from the local community leaders have been sent.

Pakaji East

Pakaji East is located between Gendrassa Refugee Camp and Bunj market on the main road. It is

closer in proximity to Bunj and therefore has slightly better opportunities to profit from the

market. However it shared very similar challenges to Kula 1 & 2 regarding food security and water.

Community Challenges

The community claimed that there was only one small hand pump for the community which was

not sufficient for the population in the area. Additionally the lack of rain was also noted as a

serious problem in this community with seeds planted and a lack of rain threatening to spoil early

and healthy crop harvest. Additionally they have been the target of thefts for livestock in the past

and tension has grown between other communities and their own.

Coping mechanisms for Pakaji East were similar with many households cutting trees and selling it

as firewood or charcoal in Bunj market. There were only a handful of community members

employed in other income generating activities and therefore relied heavily on their own

agricultural and livestock production. Livestock was fairly small scale for most households with

only around 2-5 livestock and therefore most of the households were relying more on the

agricultural crops they produced. Whenever they had problems to discuss as a community they

would raise the issue to their Sheikh and he would then be in charge of reporting the issue to the

commissioner and local authorities. This, however, is similar to the case of Kula in which local

government lacks the capacity to do anything about the grievances.

The community members claimed that some individuals were trained as CAHW (Community

Animal Health Workers) through an NGO project but that they lacked any capability to obtain

drugs to treat animals in the area on a regular basis. Additionally they had been targeted for a

grinding mill but the project never materialized and it created tension between the community

and the organization involved as the community had been instructed to build a structure that is

still there and once it was completed the project activity was not concluded. Therefore they remain

skeptical of project activities in their community, however community mobilization and their

willingness to work together to achieve results that benefit all of their community members

seemed incredibly high due to the activities they had reported collaborating on in the past such

as the construction of shelters, granaries, and the planting and maintenance of a pilot tree nursery

project and in some cases such as the grinding mill shelter they took strong initiative and followed

up several times as a community with the NGO at their office to no avail. They were interested,

ACTED – Maban Host Community Food Security & Livelihoods Assessment

25

however, in pursuing the idea of cooperation with ACTED and have also been working with the

FSL team on a pilot project for tree nursery and have responded well and mentioned this in the

discussion as useful.

Participatory Seasonal Calendar

Month

January

February

March

April

May

June July

August

September

October

November

December

Rainfall season

Dry season Rainfall season Dry Season

Crop Calendar

Feasting duration

Harvesting Long term Sorghum

Land Preparation: Land opening & Digging

Planting Maize &Millet

Planting Long term Sorghum and Wedding rest of Crops

Harvesting Maize and Cow peas

Food Gaps

Access from previous season and copping strategy

Early fast maturing crops and vegetables

Lean Season (Hunger gap)

Food Availability

Livestock Calendar

Limited pasture and water. Livestock Migration and returns end of May

Pastures Increased Livestock Disease prevalence.

Conclusion

The above report highlights many shared challenges that are faced throughout Maban County by

the host community villages. Food insecurity remains a real threat due to the lack of alternative

income opportunities for residents in Maban. Many are solely reliant on their household’s

production of agriculture and livestock and therefore systems need to be improved so that there

is less seasonal stress on the community’s means of livelihood. Isolation from the market is a real

source of stress for many of the villages in Maban County and products coming to the market are

a limited selection of imports and local produce. There is no consistent access to medicine for

both humans and animals and consequently livestock disease is left untreated in many cases. Crop

disease has also been highly reported and little technical knowledge was present in the

communities to identify and prevent further damage.

ACTED – Maban Host Community Food Security & Livelihoods Assessment

26

Recommendations

Project interventions have to consider the local capacity to acquire materials due to the

isolation of many villages in question. Low maintenance and sustainable approaches are

more advisable.

Water has been identified as a serious issue in many of the villages. The food insecurity in

the villages has been intensified by the lack of adequate water provision for both animals

and humans.

Interventions focused on training should take into consideration the local seasonal

calendar for any project activities to ensure they are effectively presented to ensure

optimal knowledge transfer.

ACTED – Maban Host Community Food Security & Livelihoods Assessment

27

Annexes

Annex I, Survey Questionnaire – Market Assessment

Hello, my name is ___________________ and I am helping ACTED collect information to help us gain a better understanding of the living situation in your community.

I would like to ask you some questions about your Market

The survey is confidential and any answers you provide will remain private.

The questionnaire does not have "good" or "bad" answers. You do not have to answer if

you do not want to. You may decline to answer any questions or stop the interview at any time. It will take around 20-30 minutes to complete.

Do you agree to let me ask you these questions?

Basic data

1. Date of interview

2. Name of interviewer

Background data Skip Logic

3. Market name a) Bunj b) Batil

All

4. Nationality of Vendor a) South Sudanese b) Sudanese c) Ethiopian d) Ugandan e) Kenyan f) Other nationality

All

5. Type of shop a) Formal (brick, concrete, metal permanent building)

b) Informal (smaller shop with no permanent building/vendor on roadside)

c) Very small vendors (individual selling product as roadside)

All

Market Data

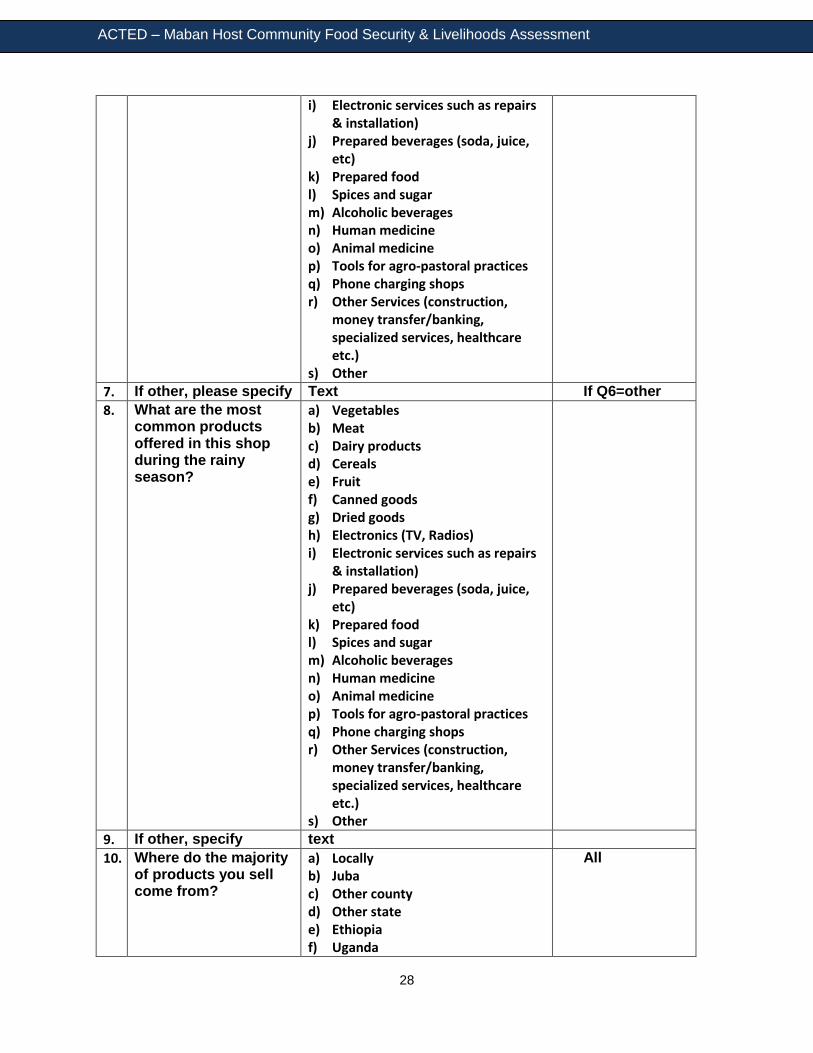

6. What are the most common products offered in this shop during the dry season?

a) Vegetables b) Meat c) Dairy products d) Cereals e) Fruit f) Canned goods g) Dried goods h) Electronics (TV, Radios)

All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

28

i) Electronic services such as repairs & installation)

j) Prepared beverages (soda, juice, etc)

k) Prepared food l) Spices and sugar m) Alcoholic beverages n) Human medicine o) Animal medicine p) Tools for agro-pastoral practices q) Phone charging shops r) Other Services (construction,

money transfer/banking, specialized services, healthcare etc.)

s) Other

7. If other, please specify Text If Q6=other

8. What are the most common products offered in this shop during the rainy season?

a) Vegetables b) Meat c) Dairy products d) Cereals e) Fruit f) Canned goods g) Dried goods h) Electronics (TV, Radios) i) Electronic services such as repairs

& installation) j) Prepared beverages (soda, juice,

etc) k) Prepared food l) Spices and sugar m) Alcoholic beverages n) Human medicine o) Animal medicine p) Tools for agro-pastoral practices q) Phone charging shops r) Other Services (construction,

money transfer/banking, specialized services, healthcare etc.)

s) Other

9. If other, specify text

10. Where do the majority of products you sell come from?

a) Locally b) Juba c) Other county d) Other state e) Ethiopia f) Uganda

All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

29

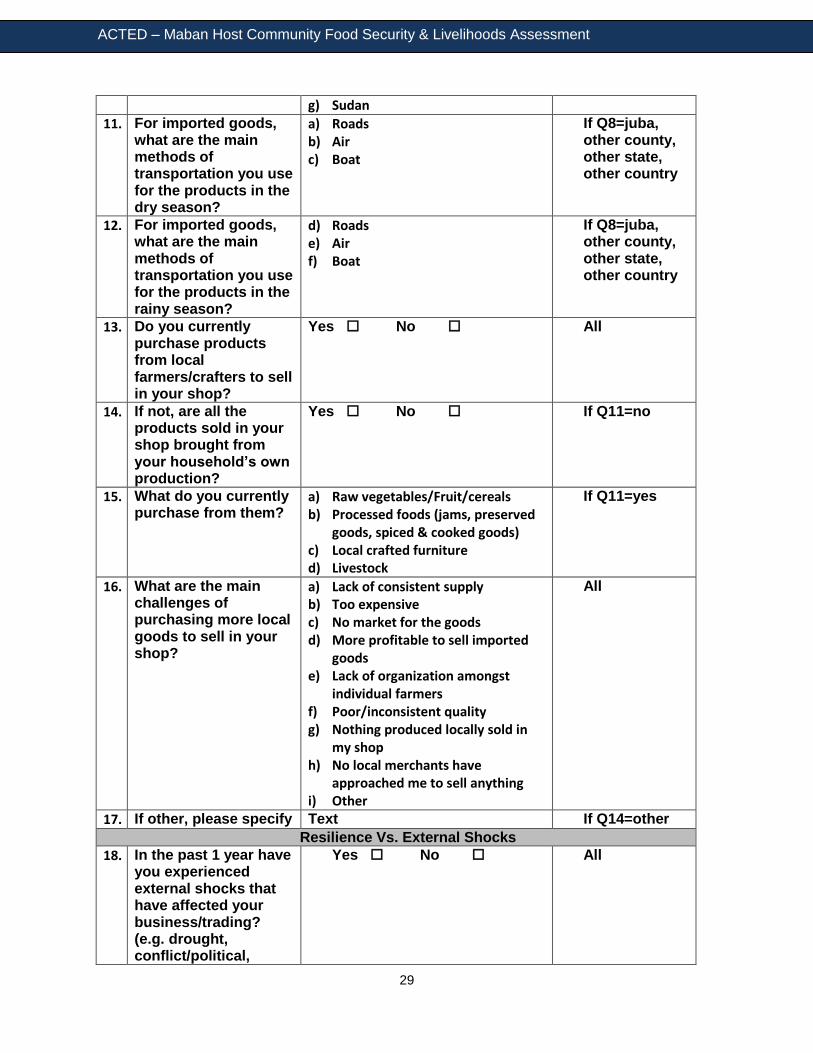

g) Sudan

11. For imported goods, what are the main methods of transportation you use for the products in the dry season?

a) Roads b) Air c) Boat

If Q8=juba, other county, other state, other country

12. For imported goods, what are the main methods of transportation you use for the products in the rainy season?

d) Roads e) Air f) Boat

If Q8=juba, other county, other state, other country

13. Do you currently purchase products from local farmers/crafters to sell in your shop?

Yes No All

14. If not, are all the products sold in your shop brought from your household’s own production?

Yes No If Q11=no

15. What do you currently purchase from them?

a) Raw vegetables/Fruit/cereals b) Processed foods (jams, preserved

goods, spiced & cooked goods) c) Local crafted furniture d) Livestock

If Q11=yes

16. What are the main challenges of purchasing more local goods to sell in your shop?

a) Lack of consistent supply b) Too expensive c) No market for the goods d) More profitable to sell imported

goods e) Lack of organization amongst

individual farmers f) Poor/inconsistent quality g) Nothing produced locally sold in

my shop h) No local merchants have

approached me to sell anything i) Other

All

17. If other, please specify Text If Q14=other

Resilience Vs. External Shocks

18. In the past 1 year have you experienced external shocks that have affected your business/trading? (e.g. drought, conflict/political,

Yes No All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

30

livestock disease, flooding, human disease 1outbreaks, etc.)

19. Which ones have you experienced?

a) Drought b) Conflict c) Livestock disease d) Flooding e) Agricultural diseases f) Economic shocks (devaluation of

the pound, etc.)

If Q16=yes

20. How did this effect your business?

a) Less customers b) More customers c) Less products available d) Higher prices to purchase products

If Q16=yes

21. How did this change product prices?

a) Extreme increase b) Large increase c) Stayed the same d) Large decrease e) Extreme decrease

If Q16=yes

22. How did this change product availability?

a) No products available for purchase/import

b) Very few products available for purchase/import

c) Stayed the same d) Longer transport time e) Other

If Q16=yes

23. If other, specify Text If Q20=other

24. Did you have to locate new sources of products to bring your products to market?

Yes No If Q16=yes

25. Did you have to change your methods of transport?

Yes No

26. How long, would you estimate, your business was affected significantly by the external shocks? (e.g. closing shop, product price increase, product availability, etc.)

a) A few days b) A week c) Several weeks d) More than one month e) More than 6 months but continues

to affect my business f) More than 6 months but it has

returned to normal g) It did not affect my business

If Q16=yes

27. Has there been any point where you could not operate your shop for an extended period

a) 1 week b) 2 weeks c) 1 month d) More than 1 month

If Q16=yes

ACTED – Maban Host Community Food Security & Livelihoods Assessment

31

of time due to an external shock?

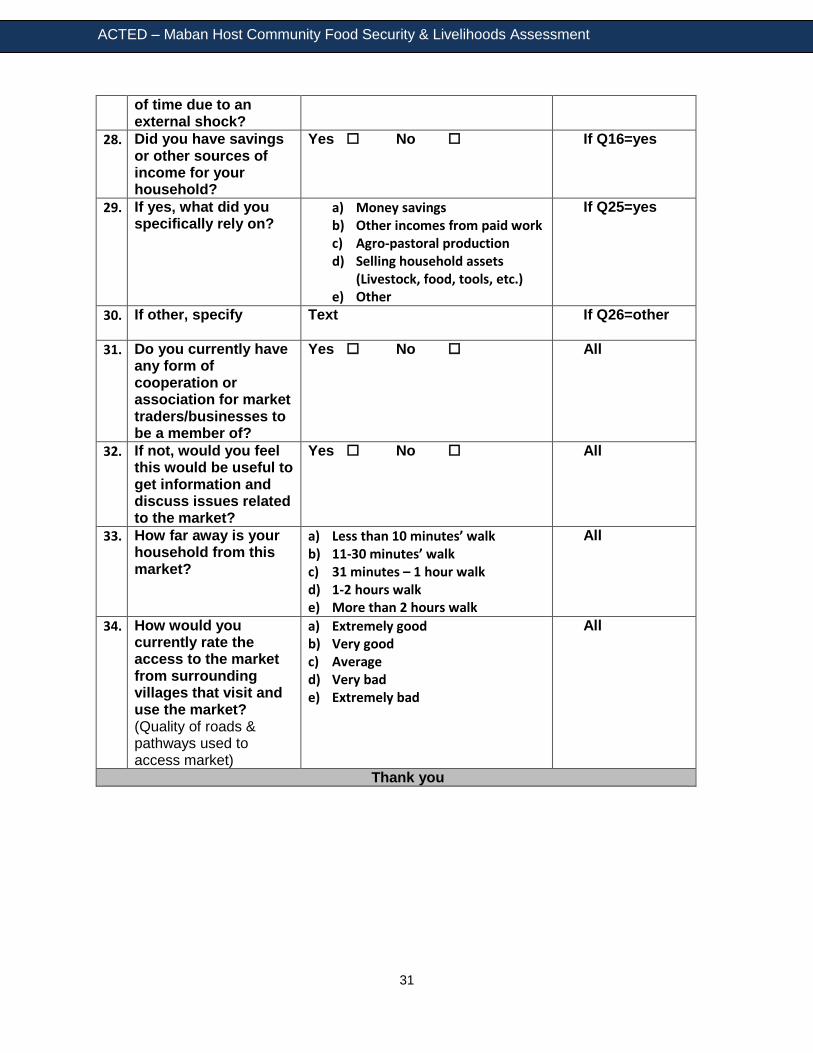

28. Did you have savings or other sources of income for your household?

Yes No If Q16=yes

29. If yes, what did you specifically rely on?

a) Money savings b) Other incomes from paid work c) Agro-pastoral production d) Selling household assets

(Livestock, food, tools, etc.) e) Other

If Q25=yes

30. If other, specify Text If Q26=other

31. Do you currently have any form of cooperation or association for market traders/businesses to be a member of?

Yes No All

32. If not, would you feel this would be useful to get information and discuss issues related to the market?

Yes No All

33. How far away is your household from this market?

a) Less than 10 minutes’ walk b) 11-30 minutes’ walk c) 31 minutes – 1 hour walk d) 1-2 hours walk e) More than 2 hours walk

All

34. How would you currently rate the access to the market from surrounding villages that visit and use the market? (Quality of roads & pathways used to access market)

a) Extremely good b) Very good c) Average d) Very bad e) Extremely bad

All

Thank you

ACTED – Maban Host Community Food Security & Livelihoods Assessment

32

Annex II, Survey Questionnaire – Village Assessment

Hello, my name is ___________________ and I am helping ACTED collect information to help us gain a better understanding of the living situation in your community.

I would like to ask you some questions about your household & village food security &

livelihoods

The survey is confidential and any answers you provide will remain private.

The questionnaire does not have "good" or "bad" answers. You do not have to answer if you do not want to. You may decline to answer any questions or stop the interview at any

time. It will take around 20-30 minutes to complete.

Do you agree to let me ask you these questions?

Basic data

35. Date of interview

36. Name of interviewer

Background data Skip Logic

37. Village name a) Kula 1 b) Kula 2 c) Bewo d) Fakaji West e) Fakaji East f) Bankuman g) Green village h) Gendrassa i) Batil j) Ofra k) Hai-neem l) Hai- sifista m) Mweniwinyi n) Dangaji

All

38. Sex of respondent Male Female All

39. What is your age? a) 15-25 b) 26-35 c) 36-45 d) 45 or older

All

40. Number of people living in your household including yourself?

a) 1-4 b) 5-8 c) 9-12 d) 13-16 e) 16 or more

All

41. Are you the head of the HH?

Yes No All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

33

42. If not, what is the gender of your HH head?

Male Female If Q7=no

43. What is the age of the household head?

a) 15-25 b) 26-35 c) 36-45 d) 45 or older

All

44. What is the occupation of the household head?

a) Crop husbandry b) Animal husbandry c) Trade d) Casual laborer e) Artisan f) Salaried employee g) Other

All

45. If other, specify text If Q10=other

Agriculture & Livestock

46. Does your household own livestock or animals?

Yes No All

47. What type of animals does this household own?

a) Cattle b) Goats c) Sheep d) Pigs e) Chicken f) Donkey g) Camel h) Dogs i) Rabbits j) Horse

If Q12=yes

48. What is the number of livestock owned for the last 6 months by estimate? (Including cattle, goats, sheep, pigs, donkeys)

a) 1-10 b) 11-20 c) 21-30 d) 31-40 e) 41-50 f) 50 or more

If Q12=yes

49. What about chickens and ducks and other smaller animals in the past six months?

a) 1-10 b) 11-20 c) 21-30 d) 31-40 e) 41-50 f) 50 or more

If Q12=yes

50. What is the number animals that died due to diseases in the last 12 months?

a) 1-5 b) 6-10 c) 11-15 d) 16-20 e) 20+

If Q12=yes

51. The number of animals slaughtered

a) 1-5 If Q12=yes

ACTED – Maban Host Community Food Security & Livelihoods Assessment

34

for HH consumption for the past month?

b) 6-10 c) 11-15 d) 16-20 e) 20+

52. What is the number of animals sold per month from your household?

a) 1-5 b) 6-10 c) 11-15 d) 16-20 e) 20+

If Q12=yes

53. What percentage of households in this village own cattle would you estimate?

a) 0-25% b) 26-50% c) 51-75% d) 76-100%

If Q12=yes

54. What percentage of households in this village raise other types of livestock (goats, chickens, etc.)

a) 0-25% b) 26-50% c) 51-75% d) 76-100%

If Q12=yes

55. How far is water /grazing point from your community?

a) 10-20min b) 30-40min c) 50-60min d) More than 60mins e) Don’t know

If Q12=yes

56. What is the main source of water for livestock?

a) Hafir b) Stream c) Borehole d) Tapstand

If Q12=yes

57. What is the largest source of food for this household?

a) Own farm b) Gathered & wild foods c) Market d) WFP ration

All

58. What percentage of households in this village grow their own vegetables would you estimate?

a) 0-25% b) 26-50% c) 51-75% d) 76-100%

All

59. What percentage of households in this village grow their own fruits would you estimate?

a) 0-25% b) 26-50% c) 51-75% d) 76-100%

All

60. What percentage of households in this village grow their own cereals would you estimate?

a) 0-25% b) 26-50% c) 51-75% d) 76-100%

All

61. What are the most common vegetables/fruits/grain

a) Dodo b) Okra c) Beans

All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

35

s /legumes/oil crops grown in this village?

d) Sorghum e) Roots & Tubers f) Sukumawiki g) Cowpea h) Maize i) Kundura j) Egg plants k) Onions l) G. nuts m) Simsim

62. How many households who grow their own vegetables/fruits/cereals, would you say, sell them in the market?

a) Almost everyone b) Many households c) Some households d) Almost nobody

All

63. Does anyone who sells vegetables/fruits, add value to them in any way before selling? (i.e. dry them, make jams, prepare them in any way)

Yes No All

64. If yes, what do they do to add value?

a) Dry them b) Make jams or spreads c) Preserve them in jars/containers

for longer shelf life d) Spice/flavor them before selling

If Q29=yes

65. What month of the year do you sell a majority of your food produce?

a) January b) February c) March d) April e) May f) June g) July h) August i) September j) October k) November l) December m) I do not sell food produce

All

66. Is the closest large market easily accessible for you or your family members?

Yes No All

67. If not, what is the largest reason why?

a) Distance b) Bad road during rainy season c) Lack of transport

If Q32=no

ACTED – Maban Host Community Food Security & Livelihoods Assessment

36

68. What means of transport do you usually use to take your products and inputs to and from market

a) Donkey cart b) Bicycle c) Motorcycle d) Human labor e) Other vehicle types f) I do not take products to the

market

All

69. Where is the closest slaughter slab for livestock?

a) In this village b) In a nearby village c) In a village far away d) Too far to travel regularly

All

70. How often would you say people use it?

a) Once every day b) Once every other day c) Once every week d) Once every 2 weeks e) Once a month f) Almost never

All

71. Are the animals slaughtered on these slabs inspected before human consumption?

Yes No All

72. If yes, who inspects them?

a) Gov’t vet personnel b) CAHWs c) Other authority

If Q37=yes

73. How do you dispose of animal carcasses?

a) Burning b) Burying c) Throw away from household d) Other method

All

74. Besides agro-pastoral, what other livelihoods activities do you have in your village?

a) Trading of goods b) Vocational trades (metal work,

electro-mechanic, baking, etc.) c) Other services/business ventures

(beekeeping, soap making, other crafts & supply manufacturing)

d) None of the above

All

75. Does your village have a reliable source of water?

Yes No All

76. If yes, what type of water source is it?

a) Borehole b) Stream/river c) Tap stand d) Hafir

If Q41=yes

Service Assessment

77. How would you rate the economic status in this village compared to others villages in Maban?

a) Far above average b) Above Average c) Average d) Below Average e) Far below average

All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

37

78. What NGOs are working in this village?

a) Medair b) MSF c) LWF d) ACTED e) DRC f) Relief International g) Other

All

79. If other, specify Text If Q44=other

80. What services do they provide to you or your village?

a) Health b) Education c) WASH d) Food Security & Livelihoods

(income generation, food security, vocational training, etc.)

All

81. Are there any animal health services offered in your village or the surrounding area?

Yes No All

82. If yes, what services do they provide?

a) Treatment of diseased animals and control of production limiting disorders

b) Provision of drugs, vaccines and other products (such as artificial insemination)

c) Avoiding the outbreak of diseases d) Human health protection

(inspection of marketed animal products)

e) Other services

If Q47=yes

83. How do you access drugs for your animals?

a) Veterinary pharmacy b) Open market c) MARF d) I cannot access drugs or do not

know how

All

84. Have your household animals been vaccinated/de-wormed?

Yes No All

85. If no, why? a) Lack of vaccines b) Lack of service providers c) Lack of money d) Other

If Q50=no

86. If other, specify Text If Q51=other

87. If yes, Which organization or group vaccinated your animals?

a) MARF b) VSF c) ICRC d) FAO

If Q50=yes

ACTED – Maban Host Community Food Security & Livelihoods Assessment

38

88. Did you pay for the vaccination/treatment of your animals

Yes No If Q50=yes

89. If yes, how much did you pay?

a) 50-100 SSP b) 150-200 SSP c) 250-300 SSP d) 400-500 SSP e) 500 or more SSP

If Q54=yes

90. Are there Baytaris(CAHWs) working in your community?

Yes No All

91. Are there other animal health services not provided that you feel would be extremely useful?

Yes No All

92. If yes, which ones? f) Treatment of diseased animals and control of production limiting disorders

g) Provision of drugs, vaccines and other products (such as artificial insemination)

h) Avoiding the outbreak of diseases i) Human health protection

(inspection of marketed animal products)

j) Other services

If Q57=yes

93. Do people in your village currently pay for any veterinary services?

Yes No All

94. What are some common reasons people do not want to pay for veterinary services?

a) Too expensive b) Don’t believe it will help

productivity c) Nothing useful is available d) Local medicine or herbs are

available instead e) Other

All

95. If other, specify text If Q60=other

96. If better veterinary services were available in the area, do you feel people would pay for them? (Improved services would be more access

Yes No All

ACTED – Maban Host Community Food Security & Livelihoods Assessment

39

to medicine, knowledgeable veterinary health care workers who can properly diagnosis and treat common illnesses)

97. If no, what are the main reasons why you feel people would still not pay?

a) Too expensive b) Not informed of benefits c) Understand benefits but feel there

are more important things to spend income on

d) Other

All

98. If other, specify text If Q63=other

Thank you

Related Documents