ADVANCE CONNECT Strengthen Opportunities, strategies, and risks MEDIA PARTNER: MERGERS & ACQUISITIONS MASTERCLASS

M&a Masterclass Presentation Slides

Oct 26, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ADVANCECONNECTStrengthen

Opportunities, strategies, and risks

MEDIA PARTNER:

MERGERS & ACQUISITIONS MASTERCLASS

AGENDA

Chair: Mark Paganin SF Fin, Partner, Clayton Utz

>> M&A megatrends: assessing the opportunities in the domestic and international markets- Richie Baston, Director, Azure Capital

>> Innovations in M&A deal strategies, business models and techniques- Aaron Hood, Executive Director, Catalyst Investment Managers

>> A snap-shot view of the regulatory developments and impact on deal approval- Russell Philip, Partner, Corrs Chambers Westgarth

AGENDA cont…

>> 10:10am Networking & refreshment break

>> Linking due diligence to the value of the deal- Roger Port SF Fin, Partner, PwC

>> Panel discussion: identifying the hot sectors and the top sources of deal flow- Aaron Hood, Executive Director, Catalyst Investments- Russell Philip, Partner, Corrs Chambers Westgarth- Roger Port SF Fin, Partner, PwC

>> 12:00pm Event Close

Richie Baston, Director, Azure Capital

M&A megatrends: assessing the opportunities in the domestic and international markets

M&A megatrends: assessing the opportunities in the domestic and

international markets

7

Today’s Themes…

1. Mega Capex Cycle

2. Funding Challenges Driving Earlier Exits for Independent Miners

3. Food Security as a Driver for Agricultural Activity

88

Committed Capex in Australia

At the end of October 2011, there were 102 projects at advanced stage of development with a record capital expenditure of $231.8 billion (74% y.o.y increase).

Source: BREE, Mi ning Industr y Maj or Pr ojec ts ( October 2011).

New Capital Expenditure (2010-11 dollars)

Projected Capex§Oct 10: $A133bn, 10% of GDP (1% pa net addition)§May 11: $A173bn, 13% of GDP (1¼% pa addition)§Oct 11: $A232bn. 17% of GDP (1½-2% of GDP pa addition) §Formidable list of projects awaiting approval/ feasibility ($A224bn)

99

Advanced Minerals & Energy Projects (1/2)

Source: BREE, Mi ning Industr y Maj or Pr ojec ts ( October 2011).

1010

Advanced Minerals & Energy Projects (2/2)

Mostly in petroleum, mostly in WA…

Source: BREE, Mi ning Industr y Maj or Pr ojec ts ( October 2011).

Value of advanced projects by commodity Value of advanced projects by state

11

Project Owners LocationProject Capex (A$bn)

FirstProd.

Macedon BHP B, Apache Exmouth Basin, WA

1.4 2013

GorgonChevron, Shell, ExxonMobil, Osa ka Gas, Tokyo Gas, Chubu

Barrow Island, WA 35 2014

Pluto 2 & 3 WoodsideCarnarvon Basin, WA 20 2015

Prelude Shell Browse Basin, WA 12 2016

Wheatstone Chevron, Apache, KUFPEC, Shell

Carnarvon Basin, WA

29 2016

BrowseWoodside, BP, Chevron, BHP B, Shell

Browse Basin, WA 38 2017

Ichthys Inpex, Total Browse Basin, WA. NT processing

34 2017

SunriseWoodside, ConocoPhill ips, Shell, Osaka Ga s

Bonaparte Basin, NT 14 2017

WA-390-P Hess Carnarvon Basin, WA

N/A N/A

Source: ABARE: Miner als and Energ y D evelopment Projects R eport, C ompany Announcements.

Hydrocarbon Industry: Planned Capital Expenditure

A small number of oil & gas projects account for a large percentage of the planned capital expenditure in Western Australia.

1212

Resulting Revenue Impact

Resource service companies are performing very strongly with mining, marine and civil contractors being the standout performers.

Source: Company Announcements , Azur e Anal ysis , March 2012.

Mining services companies – HY on HY growth PE firms sniffing around mining services

1313

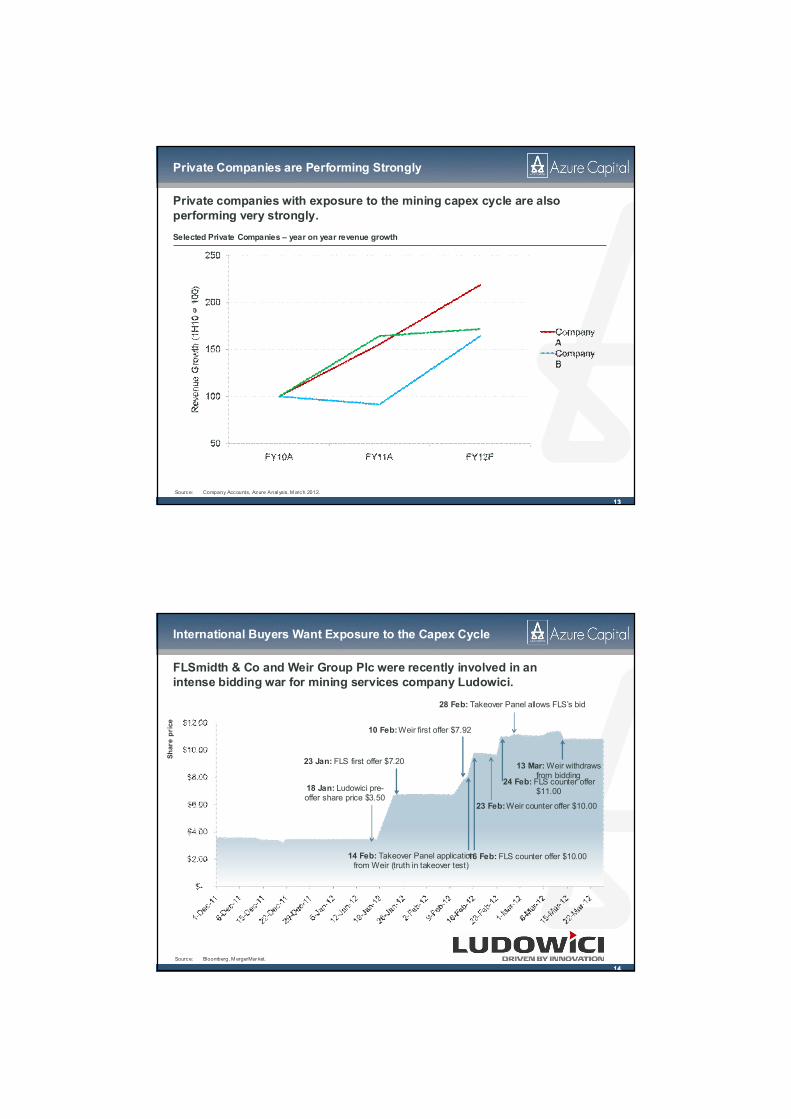

Private Companies are Performing Strongly

Private companies with exposure to the mining capex cycle are also performing very strongly.

Source: Company Accounts, Azure Anal ysis, M arch 2012.

Selected Private Companies – year on year revenue growth

1414

International Buyers Want Exposure to the Capex Cycle

FLSmidth & Co and Weir Group Plc were recently involved in an intense bidding war for mining services company Ludowici.

Source: Bloomberg, M ergerMar ket.

Shar

e pr

ice

18 Jan: Ludowici pre-offer share price $3.50

23 Jan: FLS first offer $7.20

10 Feb: Weir first offer $7.92

14 Feb: Takeover Panel application from Weir (truth in takeover test)

16 Feb: FLS counter offer $10.00

24 Feb: FLS counter offer $11.00

23 Feb: Weir counter offer $10.00

28 Feb: Takeover Panel allows FLS’s bid

13 Mar: Weir withdraws from bidding

15

Private Equity Activity – Services Companies

Date PE Firm Target

Nov 2011

Dec 2011

Dec 2010

§ Professional services provider to the offshore oil and gas industry

§ Provider of equipment of underground mine communication and tracking

§ Provides crushing and screening products and services to the mineral resources industry

§ Provider of hire equipment for heavy earthmoving

§ Spec ialised equipment & fuel services to mining, construction, agriculture & transport industries

§ Supplier of hire equipment to the mining, construction and industrial industries

Mar 2011

Mar 2011

Dec 2010

Target Description

§ Remote facilit ies management & accommodation services to the resources sector

Feb 2012

Source: MergerMar ket.

Feb 2012 § Marine services for the oil & gas industr ies

16

Today’s Themes…

1. Mega Capex Cycle

2. Funding Challenges Driving Earlier Exits for Independent Miners

3. Food Security as a Driver for Agricultural Activity

17

Equity Issues

Metals and mining company equity issuance over A$10m (2006-2012 YTD)

Late 2010 and early 2011 were reasonably strong for equity issuance in the metals and mining sector. 2H2011 was weak whilst 1H2012 is off to cautious start.

Source: ThomsonOne, primary and secondary issuances included.

18

Securing Funding: Continuing Post-GFC Volatility

Market volatility: Equities, FX, Credit

Source: NAB Global Markets Research, Reuters EcoWin

00 01 02 03 04 05 06 07 08 09 10 11 12

Bas

is p

oin

t

0100200300400500600700800900

10001100

Bas

is p

oin

t

-100-50

050

100150200250300350400450

US corporate default insurance, left

Emerging market sovereign default

insurance, right

Pe

rcen

t

0

10

20

30

40

50

60

70

80

90

"Fear index" (S&P 500 volatility VIX index)

AUD/USD, 1m, implied volatility (%)

Greek-Euro crises I & II

GFC

19

Securing Funding: Junior Resource Companies

...further explanation of scarcity of funding …

Capex Blow-outs (A$b)

Karara (Gindalbie)

Sino Iron (CITIC)

Capital Expenditure

§ Independent mining companies with large capex requirements continue to have difficulty in obtaining funding – without a first class asset

§ Economic uncertainty, and the recent volatility in commodity markets have reduced the banks’ willingness to lend, particularly European banks

§ Dramatic costs blow outs on major projects result in risk aversion – especially for those without a track record

2020

Commodity Prices

5 year trading range, spot price & consensus forecasts (real)

% of Current Spot Price

Most commodity prices are still a long way short of historical highs, with the exception of iron ore, coking coal, copper and gold.

1. Based on 2 year tradi ng range onl y.Source: Bloomberg as at 27 M ar 2012, Energ y & M etals C onsensus Forecasts Januar y 2012 Report.

Current spot pr ice5 year trading rangeConsensus long term real price

1 1

21

The Mining Value Creation Curve

Seed

Speculation (Higher Risk)

Investment Analysis

Revaluation (Lower Risk)

Discovery JORC Resource

PFS

DFSFinancing

Construction

Commence Operations

Steady State

Indi

cativ

e Va

lue

(% o

f NPV

)

100%

50%

25%

75%

Time

JORC Reserve

Public Equity Equity / Project Finance

21

22

The Mining Value Creation Curve

Seed

Speculation (Higher Risk)

Investment Analysis

Revaluation (Lower Risk)

Discovery JORC Resource

PFS

DFSFinancing

Construction

Commence Operations

Steady State

Indi

cativ

e Va

lue

(% o

f NPV

)

100%

50%

25%

75%

Time

JORC Reserve

Public Equity Equity / Project Finance

22

Pre-GFC

• Paladin – Kayalekera (2009), Langer Heinrich (2006)

• Mirabela – Santa Rita (2009)• Anvil – Kinsevere (2009)• Lynas – Mt Weld (2008)• FMG – Cloudbreak (2006)• Equinox – Lumwana (2006)

Prior to the GFC, companies had more opportunities to independently develop projects.

23

The Mining Value Creation Curve

Seed

Speculation (Higher Risk)

Investment Analysis

Revaluation (Lower Risk)

Discovery JORC Resource

PFS

DFSFinancing

Construction

Commence Operations

Steady State

Indi

cativ

e Va

lue

(% o

f NPV

)

100%

50%

25%

75%

Time

JORC Reserve

Public Equity Equity / Project Finance

23

Post-GFC

African Iron

Giralia

Extract ResourcesChalice Gold Mines

AuroxPhillips River

CitadelMantra

FerrausMeridian Minerals

Riversdale

… however, post GFC, companies are finding it harder to fund project development. We see a trend of companies existing earlier.

24

Historical and Forecast Free Cash Flow – Majors

BHP Billiton

Operating Cash Flow Capex Forecast Operating Cash Flow Forecast Capex

Source: RBC Capital Markets: Commodity Assumption Rev ision, Mar 2012.

Net cash f low

Rio Tinto Xstrata

The hugely cash generative majors are choosing to re-invest into own operations, capital management strategies and some major Tier 1 assets where available.

25

Historical and Forecast Free Cash Flow – Mid Tiers

OZ Minerals

Operating Cash Flow Capex Forecast Operating Cash Flow Forecast Capex

Source: RBC Capital Markets: Australia Div ersif ied Metals & Mining, Mar 2012.

Net cash f low

Western Areas Mount Gibson

Mid tier companies with operating assets (= strong cash generation ability) are well positioned to acquire second tier assets and accelerate growth of target companies.

26

Recent Iron Ore Acquisitions in Africa by Chinese (1/2)

Date Acquirer Target Value (US$) Stake

Jan 2010

Mar 2010

$244m

$68m

12.5% (company)

60%

Bong Mining Project

Mar 2010 $1,350m up to 45%

Simandou Mining Project

Chinese Railway Materials Tonkolili Iron Ore Project

Source: RBC.

Strategics remain a very important alternative funding source – e.g. African iron ore investment by Chinese groups – show comfort in managing geopolitical risk.

27

Recent Iron Ore Acquisitions in Africa by Chinese (2/2)

Jul 2010

Aug 2010

$1,500m

$1,240m

25%

Earn-in agreement

(up to 50%)

Kalia Iron Project

Tonkolili Iron Ore Project Shandong Iron & Steel

Source: RBC.

Date Acquirer Target Value (US$) Stake

28

Today’s Themes…

1. Mega Capex Cycle

2. Funding Challenges Driving Earlier Exits for Independent Miners

3. Food Security as a Driver for Agricultural Activity

29

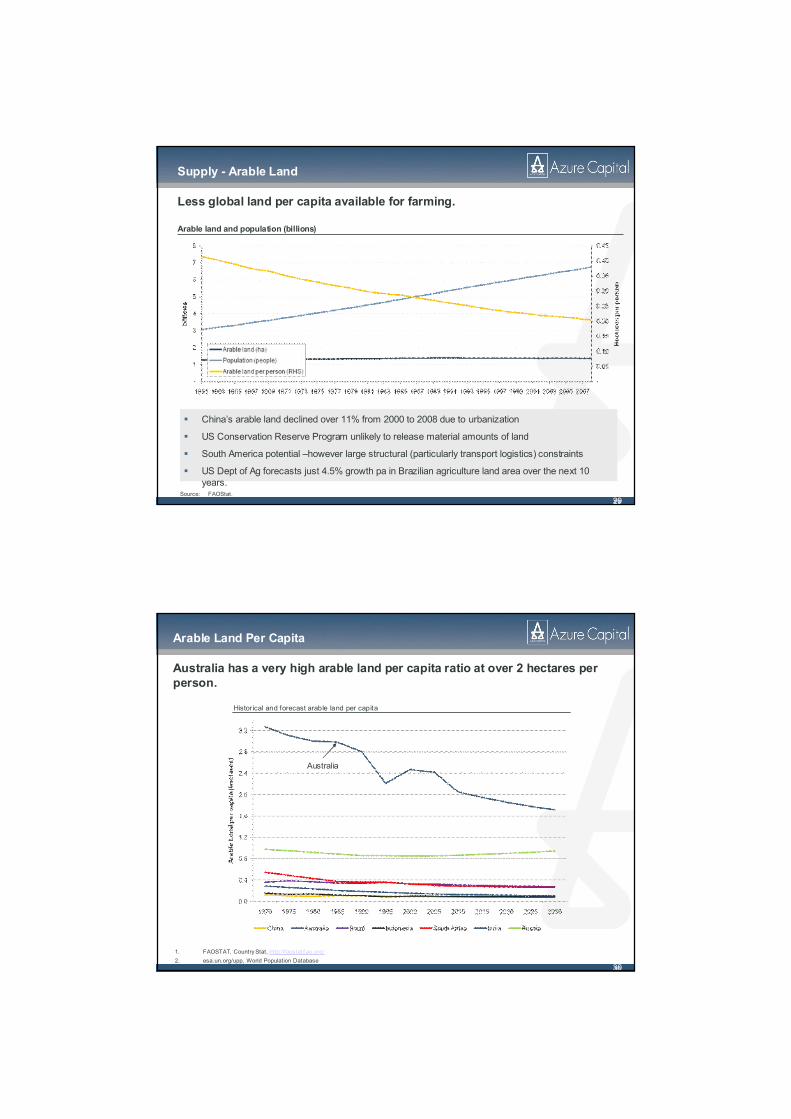

Supply - Arable Land

Less global land per capita available for farming.

Arable land and population (billions)

§ China’s arable land declined over 11% from 2000 to 2008 due to urbanization

§ US Conservation Reserve Program unlikely to release material amounts of land

§ South America potential –however large structural (particularly transport logistics) constraints

§ US Dept of Ag forecasts just 4.5% growth pa in Brazilian agriculture land area over the next 10 years.

Source: FAOStat.29

30

Arable Land Per Capita

Australia has a very high arable land per capita ratio at over 2 hectares per person.

1. FAOSTAT, Country Stat, http://faostat.f ao.org/2. esa.un.org/upp, World Population Database

Histor ical and forecast arable land per capita

Australia

30

31

Commodity Prices

1. Indexed to 100 (Jan 1983) (real)Source: Bloomberg as at 22 Nov ember 2010 using S&P GSCI.

Global agriculture prices have historically moved with other commodities but have yet to reach the recent levels achieved by metals and energy.

Agriculture vs. all commodit ies1

31

32

Agricultural Land

The Australian agricultural land market is larger than the commercial property market exceeding A$300 billion in 2010.

Land values by use 20101

1. ABS, National Accounts 2010.

Rural values by state (AUD 2010)1

Pastoral

Wheat –sheep

High rainfall

NSW $113bn

TAS $7bn

WA $29bn SA

$25bn

NT $600m

QLD $63bn

VIC/ACT $68bn

A$ billion

$2,829

$306

$291

$190

$3,614

ResidentialRuralCommercialOtherTotal

32

33

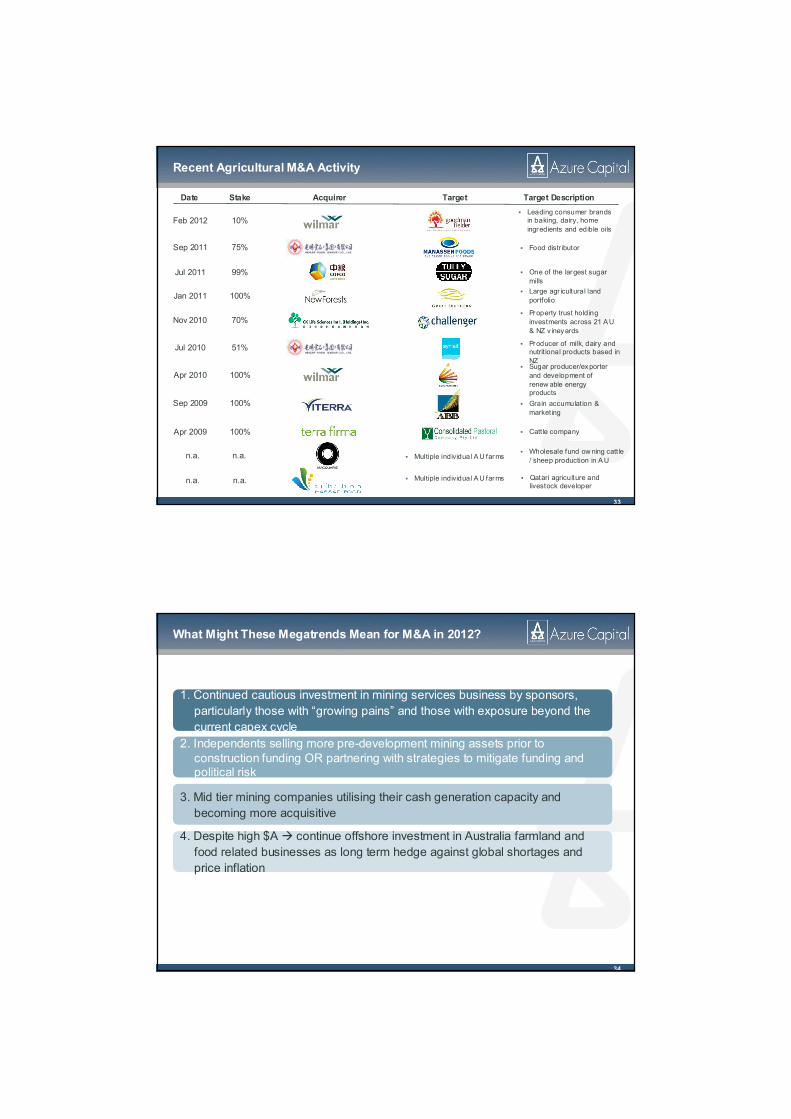

Recent Agricultural M&A Activity

Date Acquirer Target Target DescriptionStake

Feb 2012§ Leading consumer brands

in baking, dairy, home ingredients and edible oils

10%

§ Sugar producer/exporter and development of renew able energy products

Apr 2010 100%

§ Grain accumulation & marketing

Sep 2009 100%

Sep 2011 § Food distr ibutor75%

§ One of the largest sugar mills

Jul 2011 99%

§ Property trust holding investments across 21 A U & NZ v ineyards

70%Nov 2010

§ Producer of milk, dairy and nutrit ional products based in NZ

51%Jul 2010

§ Large agr icultural land portfolio100%Jan 2011

§ Cattle companyApr 2009 100%

§ Wholesale fund ow ning catt le / sheep production in A U

§ Qatari agriculture and livestock developer

§ Multiple individual A U farms

§ Multiple individual A U farmsn.a. n.a.

n.a. n.a.

34

What Might These Megatrends Mean for M&A in 2012?

1. Continued cautious investment in mining services business by sponsors, particularly those with “growing pains” and those with exposure beyond the current capex cycle

2. Independents selling more pre-development mining assets prior to construction funding OR partnering with strategies to mitigate funding and political risk

3. Mid tier mining companies utilising their cash generation capacity and becoming more acquisitive

4. Despite high $A à continue offshore investment in Australia farmland and food related businesses as long term hedge against global shortages and price inflation

Azure Capital Limited ACN 107 416 106

PO Box Z5340Perth Western Australia 6831

Level 34 Exchange Plaza2 The Esplanade Perth Western Australia 6000

Phone: +61 8 6263 0888Fax: +61 8 6263 0878

Aaron Hood, Executive Director, Catalyst Investment Managers

Innovations in M&A deal strategies, business models and techniques

M&A MasterclassPerthMarch 2012

catalyst

38

Home & Decor Holdings (HDH) – Established in December 2010

Bhagw an M arine - Acquired in M arch 2012

• HDH acquired specia lty retailers Adairs and Dusk

• Dusk is based in Perth and is Australia’s leading specialty retailer of candles, home fragrance & giftw are products, w ith over 70 stores at acquisition

• Value creation w ill be driven by Australia w ide store roll out in both concepts, plus increasingly selling higher margin ow n brands

• HDH may look to acquire other specialty retail businesses in the home and decor segment in Australasia

• Bhagw an M arine is the pre-eminent provider of vessels and marine personnel to the Oil & Gas industry in Australia

• The business currently operates in excess of 50 vessels, has a presence in key port locations in WA, NT and Qld and has a blue chip customer base

• Catalyst acquired a minority interest in M arch 2012 and provided growth capital to expand the vessel fleet. The founding Kannikoski family continue to hold a majority shareholding

• The Kannikoski family w ere seeking a partner that could help strengthen the balance sheet to ensure the business remains market leader, ahead of an eventual IPO

Introduction to Catalyst

Catalyst is currently investing its 8th buyout fund and has in excess of A$1b under management. We currently have 2 investments managed from its Perth office.

7

39

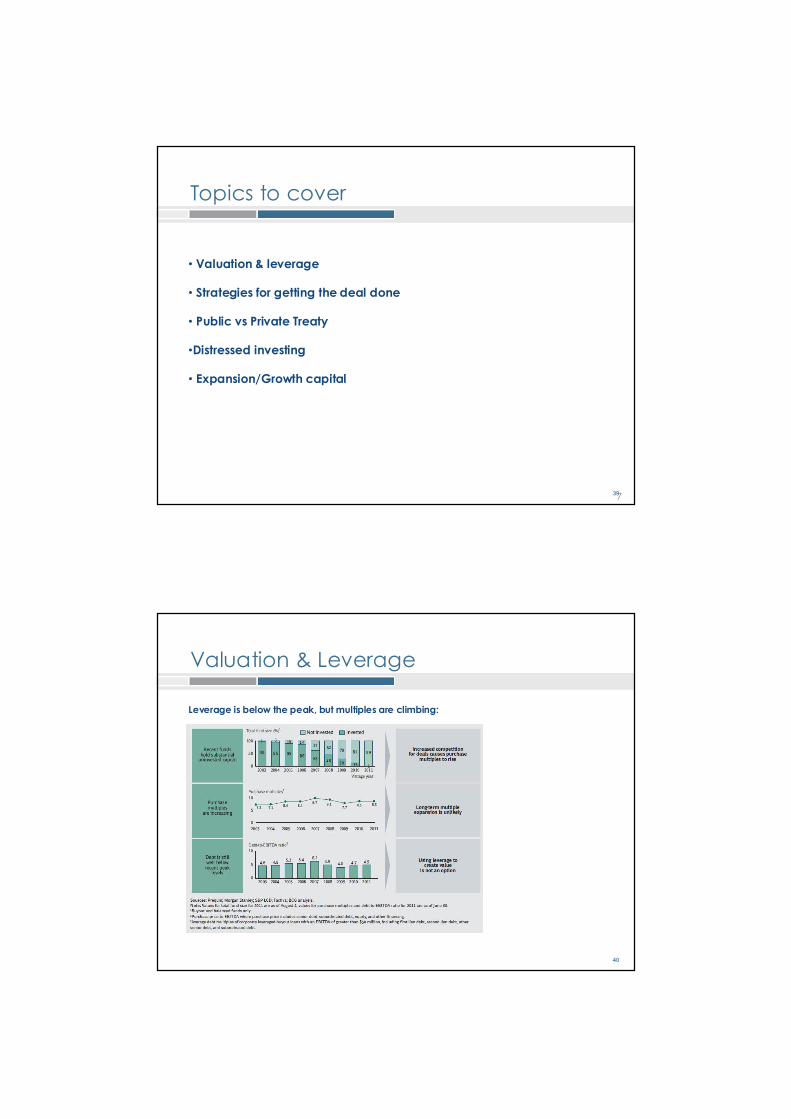

Topics to cover

• Valuation & leverage

• Strategies for getting the deal done

• Public vs Private Treaty

•Distressed investing

• Expansion/Growth capital

7

40

Valuation & Leverage

Leverage is below the peak, but multiples are climbing:

41

Valuation Expectations

Firms pay for growth ...

ASPAC is not expecting strong growth however ...

42

Strategies for getting the deal done

• It is not about financing or debt arrangement anymore (and never should have been)

• You have to find good businesses

• Funding will follow

• Local knowledge, self generated origination and relationships are the key

• Family businesses and divisions of corporates are still the best sources

43

Private vs. Public

• P2Ps are difficult to complete & quite rare in practice

• Catalyst has completed 2 out of 38 transactions

• The failure rate is quite high

• Emotional & powerful shareholders (e.g Flight Centre & Qantas)

• Attracts counter-bidders (e.g PearlStreet,

• Directors take a different course (e.g Fosters, Orica, Perpetual etc)

44

Special Situations / Distressed Investing

What is it:

“Special situations” investors look at businesses in financial distress as opportunities for turning the business around outside insolvency by contributing new capital and reviving management. The influx of new funding has the potential to facilitate a restructure of Australian debt outside of formal insolvency.

Who is involved:

• Specialist turn-around funds

• Hedge funds

• Debt traders / Principal desks of Investment Banks

45

“Loan to own”

46

Distressed Investing – Long Process

47

Expansion/Growth Capital Experience

Morris Corporation - Acquired in De cember 2011 Bhagw an M arine - Acquired in M arch 2012

• Morris Corporation is Australia's leading specialist provider of catering, accommodation and facilities management services to the remote fly-in fly-out (FIFO) resources industry

• The business provides both outsourced facil ities management services for FIFO camp ow ners, as well as operating a portfolio of company ow ned and operated sites in the Bowen Basin and Pilbara regions

• Catalyst acquired a 49% interest in M orris in December 2011 to support the business as it pursues an array of growth opportunities

• The ex isting shareholders w ere looking for a partner that could provide assistance in “corporatisation” as w ell as capital to pursue further build , ow n operate camp developments

• Bhagw an M arine is the pre-eminent provider of vessels and marine personnel to the Oil & Gas industry in Australia

• The business currently operates in excess of 50 vessels, has a presence in key port locations in WA, NT and Qld and has a blue chip customer base

• Catalyst acquired a minority interest in M arch 2012 and provided growth capital to expand the vessel fleet. The founding Kannikoski family continue to hold a majority shareholding

• The Kannikoski family w ere seeking a partner that could help strengthen the balance sheet to ensure the business remains market leader, ahead of an eventual IPO

Catalyst currently has 2 investments in its current fund defined as “Growth/Expansion Deals”

7

Catalyst Investment Managers Pty LimitedLevel 9, 151 Macquarie Street Sydney NSW 2000Level 4, 91-93 Flinders Lane Melbourne VIC 3000

Level 17, Exchange Plaza , 2 The Esplanade Perth 6000

www.catalystinvest.com.au

Russell Philip, Partner, Corrs Chambers Westgarth

A snap-shot view of the regulatory developments and impact on deal approval

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL FINSIA M&A Masterclass

28 March 2012

Presenter:

Russell PhilipPartner

6426630/2

5129 March 2012

INTRODUCTION

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

52

INTRODUCTION

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

CURRENT REGULATORY ISSUES

5329 March 2012

OVERVIEW OF THE AUSTRALIAN REGULATORY ENVIRONMENT

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

54

THE AUSTRALIAN REGULATORY ENVIRONMENT

• Takeovers of publicly listed Australian companies, and unlisted Australian companies with more than 50 members, are regulated under Chapter 6 of the Corporations Act

• Mixture of ‘black letter’ and ‘fuzzy letter’ law

• ASIC and the Takeovers Panel are the principal regulators in this field

• If the target is listed on ASX, the ASX Listing Rules also apply

• Other regulatory bodies may become involved, depending upon the industry sector, the effect of the acquisition on competition and whether the bidder is a foreign person

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

55

REGULATORY FRAMEWORK: CORPORATIONS ACT

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 28 March 2012

• Responsible for administration of the Australian Corporations Act• Broad powers to enforce, modify the provisions of, and grant exemptions

from, the Corporations Act• Publishes Regulatory Guides setting out its policy in exercising powers

• Responsible for administration of the Australian Corporations Act• Broad powers to enforce, modify the provisions of, and grant exemptions

from, the Corporations Act• Publishes Regulatory Guides setting out its policy in exercising powers

• A peer review body, which is the main forum for resolving takeover disputes until the bid period has ended

• Makes declarations of "unacceptable circumstances“ and wide ranging consequential orders

• Issues Guidance Notes as to how it will exercise these powers• Power to decide appeals from ASIC’s decisions on modifications and

exemptions concerning takeovers

• A peer review body, which is the main forum for resolving takeover disputes until the bid period has ended

• Makes declarations of "unacceptable circumstances“ and wide ranging consequential orders

• Issues Guidance Notes as to how it will exercise these powers• Power to decide appeals from ASIC’s decisions on modifications and

exemptions concerning takeovers

• Primary responsibility under the Act for schemes of arrangement• Only ASIC and certain other government authorities can commence Court

proceedings between announcement and end of bid period • Panel may refer a question of law to the Court - this does not happen very

often

• Primary responsibility under the Act for schemes of arrangement• Only ASIC and certain other government authorities can commence Court

proceedings between announcement and end of bid period • Panel may refer a question of law to the Court - this does not happen very

often

ASICASIC

TAKEOVERSPANEL

TAKEOVERSPANEL

COURTSCOURTS

56

SECURITIES MARKETSECURITIES MARKET

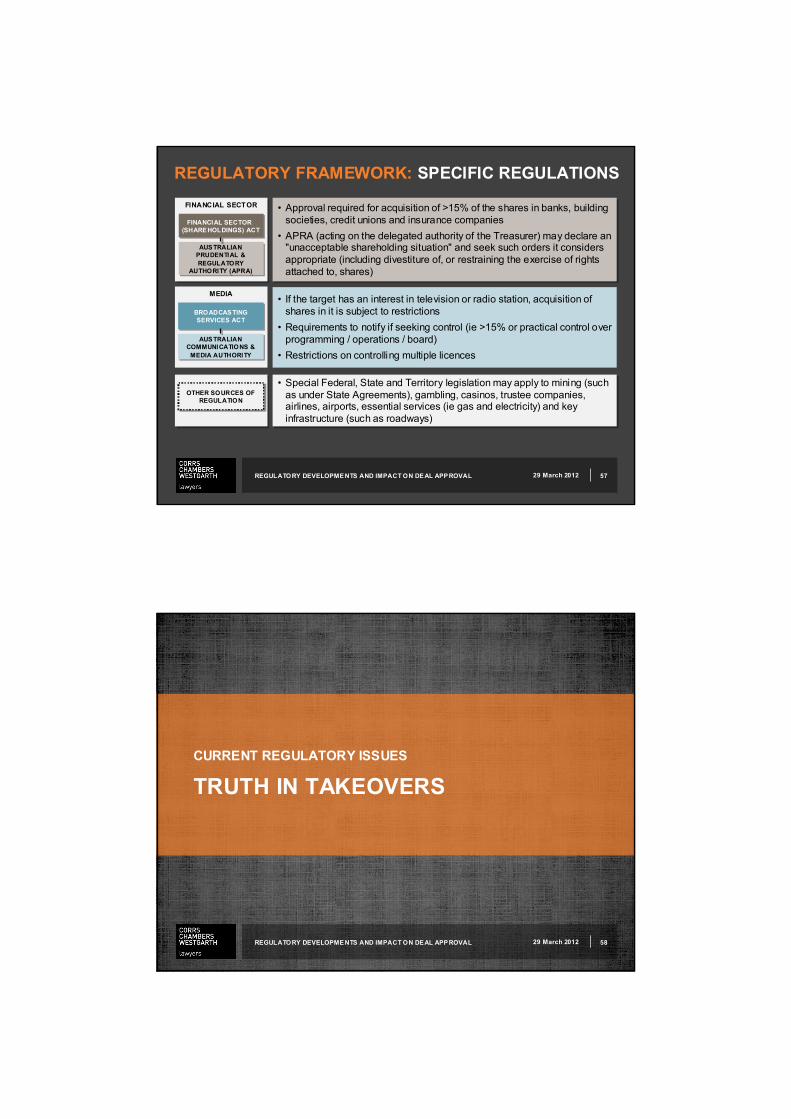

REGULATORY FRAMEWORK: SPECIFIC REGULATIONS

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

• ASX Listing Rules will apply if bidder or target is listed, ie continuous disclosure, 15% threshold, related party provisions etc

• ASX is responsible for ensuring compliance with ASX Listing Rules• ASIC is responsible for market supervision and ensuring compliance with

ASIC Market Integrity Rules

• ASX Listing Rules will apply if bidder or target is listed, ie continuous disclosure, 15% threshold, related party provisions etc

• ASX is responsible for ensuring compliance with ASX Listing Rules• ASIC is responsible for market supervision and ensuring compliance with

ASIC Market Integrity Rules

• Foreign entities may need to obtain prior approval from the Federal Treasurer, through FIRB

• Approval is compulsory for any direct investment of >10% by a foreign government or their related entities, irrespective of size and also in some sensitive areas (ie media)

• Foreign entities may need to obtain prior approval from the Federal Treasurer, through FIRB

• Approval is compulsory for any direct investment of >10% by a foreign government or their related entities, irrespective of size and also in some sensitive areas (ie media)

ASX LISTING RULESASX LISTING RULES

ASIC MARKET INTEGRITY RULES

ASIC MARKET INTEGRITY RULES

FOREIGN INV ESTM ENT

FOREIGN ACQUISITIONS AND

TAKEOVERS ACT

FOREIGN ACQUISITIONS AND

TAKEOVERS ACT

FOREIGN INVESTMENT REVIEW BOARD (FIRB)FOREIGN INVESTMENT REVIEW BOARD (FIRB)

• M&A prohibited if likely to substantially lessen competition in a market• Parties to voluntarily notify or can be compelled by ACCC• Contravention may result in injunctions to prevent closing, or penalties

and divestiture orders for completed transactions.

• M&A prohibited if likely to substantially lessen competition in a market• Parties to voluntarily notify or can be compelled by ACCC• Contravention may result in injunctions to prevent closing, or penalties

and divestiture orders for completed transactions.

COMPETITION

COMPETITION AND CONSUMER ACT

COMPETITION AND CONSUMER ACT

AUSTRALIAN COMPETITION AND

CONSUMER COMMISSION (ACCC)

AUSTRALIAN COMPETITION AND

CONSUMER COMMISSION (ACCC)

57

FINANCIAL SECTORFINANCIAL SECTOR

REGULATORY FRAMEWORK: SPECIFIC REGULATIONS

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

• Approval required for acquisition of >15% of the shares in banks, building societies, credit unions and insurance companies

• APRA (acting on the delegated authority of the Treasurer) may declare an "unacceptable shareholding situation" and seek such orders it considers appropriate (including divestiture of, or restraining the exercise of rights attached to, shares)

• Approval required for acquisition of >15% of the shares in banks, building societies, credit unions and insurance companies

• APRA (acting on the delegated authority of the Treasurer) may declare an "unacceptable shareholding situation" and seek such orders it considers appropriate (including divestiture of, or restraining the exercise of rights attached to, shares)

• If the target has an interest in television or radio station, acquisition of shares in it is subject to restrictions

• Requirements to notify if seeking control (ie >15% or practical control over programming / operations / board)

• Restrictions on controlling multiple licences

FINANCIAL SECTOR (SHAREHOLDINGS) ACT

FINANCIAL SECTOR (SHAREHOLDINGS) ACT

AUSTRALIAN PRUDENTIAL & REGULATORY

AUTHORITY (APRA)

AUSTRALIAN PRUDENTIAL & REGULATORY

AUTHORITY (APRA)

MEDIA

BROADCASTING SERVICES ACT

BROADCASTING SERVICES ACT

AUSTRALIAN COMMUNICATIONS &

MEDIA AUTHORITY

AUSTRALIAN COMMUNICATIONS &

MEDIA AUTHORITY

• Special Federal, State and Territory legislation may apply to mining (such as under State Agreements), gambling, casinos, trustee companies, airlines, airports, essential services (ie gas and electricity) and key infrastructure (such as roadways)

• Special Federal, State and Territory legislation may apply to mining (such as under State Agreements), gambling, casinos, trustee companies, airlines, airports, essential services (ie gas and electricity) and key infrastructure (such as roadways)

OTHER SOURCES OF REGULATION

OTHER SOURCES OF REGULATION

5829 March 2012

CURRENT REGULATORY ISSUES

TRUTH IN TAKEOVERS

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

59

TRUTH IN TAKEOVERS

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

"The Panel considers the truth in takeovers policy to be a fundamental tenet of the Australian takeovers regime and unwarranted departures by takeovers participants from statements they make to the market are to be taken very seriously"

Market participants should be held to their

best and final statements

Market participants should be held to their

best and final statements

"A bidder cannot depart from a no increase statement even if it

compensates those who have sold on-market"

"A bidder cannot depart from a no increase statement even if it

compensates those who have sold on-market"

A compensation policy would allow a bidder to press holders into accepting early by using a no

increase statement and improve the consideration later only if necessary for the bid to succeed

A compensation policy would allow a bidder to press holders into accepting early by using a no

increase statement and improve the consideration later only if necessary for the bid to succeed

Summit Resources

Rather than “shoot the shareholder” by not allowing Rinker shareholders to retain the increased consideration (ie trying to unscramble the egg), ASIC instead requested that the Panel allow affected shareholders to be compensated.

Rinker / CEMEX

The Panel ordered market participants depart from unqualified intention statements, as to hold them to such statements would result in unacceptable circumstances

MYOB

60

FLSMIDTH SIGNS MIA AND INCREASES OFFER PRICE TO $10.00 IN LINE WITH UNDERTAKING

CASE STUDY

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

FLSMIDTH GIVES INDICATIVE NON-BINDING SCHEME PROPOSAL TO LUDOWICI ($7.20)

THE AUSTRALIAN REPEATS THE REUTERS ARTICLE

FLSMIDTH RETRACTS STATEMENT AND RESERVES RIGHT TO INCREASE PRICE

WEIR MAKES TAKEOVERS PANEL APPLICATION

FLSMIDTH INCREASES OFFER PRICE TO $11.00

FLSMIDTH CEO RESPONDS “NO”WHEN ASKED WHETHER HE WOULD CONSIDER RAISING THE BID PRICE OF $7.20 (REUTERS ARTICLE)

WEIR GIVES INDICATIVE NON-BINDING SCHEME PROPOSAL TO LUDOWICI ($7.92)

PANEL ACCEPTS FLSMIDTHUNDERTAKING ALLOWING INCREASED OFFER SUBJECT TO OUTCOME OF PANEL PROCEEDINGS

WEIR GIVES BINDING PROPOSAL FOR $10.00 SUBJECT TO PANEL DECLARING UNACCEPTABLE CIRCUMSTANCES IN RELATION TO FLSMIDTH PROPOSAL

PANEL DECL ARES UNACCEPTABLE CIRCUMSTANCES, AND REQUIRES COMPENSATION

LUDOWICI RECOMMENDS FLSMIDTH’S OFFER

• NO INCREASE WITHOUT DISCLAIMER

• NO MI A WITHOUT CONDITION PRECEDENT

VS

61

PRICING CHART (ASX: LDW)

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

62

SO WHERE TO FROM HERE?

• The decision in Ludowici has left the market in an even greater state of uncertainty – the Panel had the opportunity to put its foot down, but chose not to foreclose on a potential auction

• Is the real policy 'best price wins‘, and that compensation for departing from a ‘best and final’ statement is just a cost to be factored into doing a deal?

• Ludowici shareholders have resoundingly benefitted in this case... but at what cost to market integrity?

• Is it time to change the policy?

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

6329 March 2012

CURRENT REGULATORY ISSUES

ENFORCING THIRD PARTY RIGHTS TRIGGERED ON A TAKEOVER

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

64

CROWN JEWEL DEFENCES

• An arrangement with a third party concerning the company’s key assets which is triggered in the event of a takeover bid

• Common examples include:• Pre-emptive rights exercisable upon a change of control in joint venture agreements• Accelerated repayment obligations under debt facilities if a change of control occurs• Termination of leasing arrangements if a change of control occurs

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

65

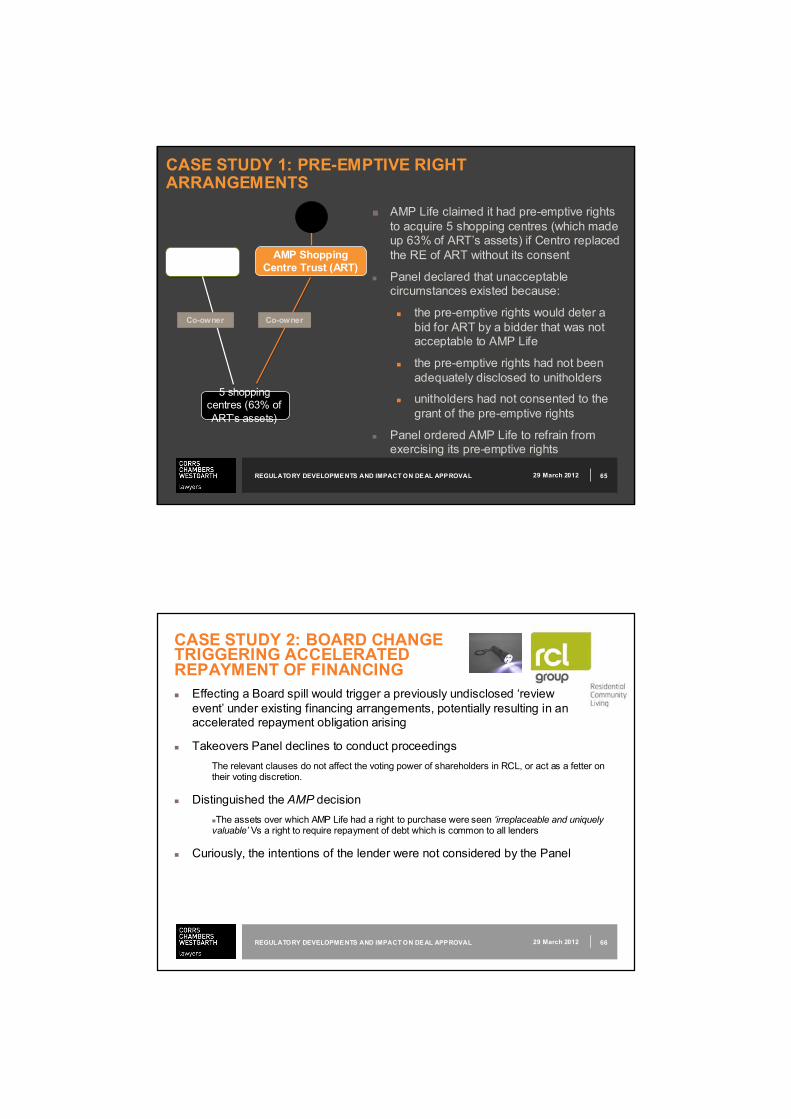

CASE STUDY 1: PRE-EMPTIVE RIGHT ARRANGEMENTS

■ AMP Life claimed it had pre-emptive rights to acquire 5 shopping centres (which made up 63% of ART’s assets) if Centro replaced the RE of ART without its consent

n Panel declared that unacceptable circumstances existed because:

n the pre-emptive rights would deter a bid for ART by a bidder that was not acceptable to AMP Life

n the pre-emptive rights had not been adequately disclosed to unitholders

n unitholders had not consented to the grant of the pre-emptive rights

n Panel ordered AMP Life to refrain from exercising its pre-emptive rights

AMP Shopping Centre Trust (ART)

5 shopping centres (63% of ART’s assets)

AMP Life

Co-ownerCo-owner Co-ownerCo-owner

RE

29 March 2012 REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

66

CASE STUDY 2: BOARD CHANGE TRIGGERING ACCELERATED REPAYMENT OF FINANCINGn Effecting a Board spill would trigger a previously undisclosed ‘review

event’ under existing financing arrangements, potentially resulting in an accelerated repayment obligation arising

n Takeovers Panel declines to conduct proceedingsThe relevant clauses do not affect the voting power of shareholders in RCL, or act as a fetter on their voting discretion.

n Distinguished the AMP decision nThe assets over which AMP Life had a right to purchase were seen ‘irreplaceable and uniquely valuable’ Vs a right to require repayment of debt which is common to all lenders

n Curiously, the intentions of the lender were not considered by the Panel

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

67

WHERE DOES THIS LEAVE US?n Whether third parties can enforce rights triggered

on a takeover bid is likely to depend upon:n the nature of the rights themselves and their likely effect on control

n whether they have been disclosed to target shareholders previously, and the nature of that disclosure

n whether target shareholders have consented to the grant of the third party rights

n Is it fair that the Panel can deny an innocent third party the ability to enforce their contractual rights?

n How do third parties protect their rights?

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

6829 March 2012

CURRENT REGULATORY ISSUES

PRODUCTION TARGETS

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL

69

DISCLOSURE OF PRODUCTION TARGETS

n What is a production target?

n How do they fit within JORC?

n If they are just a target, how can they be misleading?

n What is all the fuss about?

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

70

RECAP ON THE JORC CODE

• Figure 1, JORC. General relationship between Exploration Results, Mineral Resource s and Ore Re serve s

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

71

FORWARD LOOKING STATEMENTS AND PROSPECTIVE FINANCIAL INFORMATION

n Production targets are clearly forward looking

n Need a reasonable basis for making forward looking statementsn Producing assets

n Development assets

n Greenfields exploration assets

n Disclosure of supporting information to enable users to assess relevance and reliability

n Is a disclaimer enough?

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

72

WATCH THIS SPACE!

n The outcome of the ASX review should provide significant clarity on what is acceptable regarding disclosure of production targetsn Expected late 2012

n The ability to provide such information, and extent of accompanying disclosure, is likely to depend upon confidence levels in economically extracting the ore from the ground

n Until further guidance is available, extreme caution should be exercised in disclosing production targets

REGULATORY DEVELOPMENTS AND IMPACT ON DEAL APPROVAL 29 March 2012

73

PROFILE

QualificationsMasters of Laws, University of Sydney (2004)Bachelor of Laws / Bachelor of Commerce, University of Western Australia (1997)Graduate Diploma in Applied Finance and Investment with FINSIA

Career SummaryRussell specialises in advising public and private companies on a wide range of corporate transactions, including

regulated and unregulated mergers and acquisitions, foreign investment matters, equity and hybrid fundraisings, corporate reconstructions, capital management and general corporate and compliance matters. He has significant experience in the mining, mining services, technology and financial services industries.

Russell is the course facilitator for the Australian Institute of Company Directors in ‘The Board’s role in M&A transactions’, and is a guest lecturer at the University of Western Australia on corporate law related matters.

Russell PhilipPartner

Tel +61 8 9460 1673Mob 0400 299 098

January 2012

30 Minutes, recommence workshop at 10.40am

Networking refreshment break

Roger Port SF Fin, Partner, PwC

Linking due diligence to the value of the deal

Linking Due Diligence to the Value of the Deal

Presentation to Finsia M&A Workshop

Roger Port

28 March 2012

pwc.com.au

PwC

Agenda

Deal Readiness

Value Drivers

Vendor Due Diligence

77March 2012FINSIA

PwC

Deal Readiness

FINSIA78

March 2012

PwC

Why does M&A consistently fail to meet its objectives?

It is consistently reported that the majority of M&A transactions fail to add value for shareholders:

• “70% of acquirers better off if acquisitions not undertaken”

• “83% of mergers produced no net shareholder value benefit”

• “two thirds of merged groups perform well below industry average”

There is no easy answer to the question – some possible reasons include:

• poorly defined strategy or overly optimistic objectives

• inadequate transaction due diligence

• bad management and ineffective post acquisition execution

• changes in market conditions and competition

FINSIA79

March 2012

PwC

Is it any surprise that M&A regularly fails? – the M&A context is often complex

FINSIA80

March 2012

Actions of competitors

Limited time

Incomplete information

Ego

Risk appetite

Access to M&A skills

Integration issues

Changing market conditions

Management incentives

Availability and cost of finance

Organisational culture

Shareholder requirements

Management distraction

Clash of cultures

PwC

Linking due diligence to the value of the deal

A standard checklist approach fails to reflect the unique characteristics of each company and each deal

Effective due diligence requires an understanding of internal situation, capabilities and strategy, and a tailored and realistic assessment of the keys to realising value from the deal

Deal readiness and preparation is critical as time and information is often limited, and major decisions need to be made quickly

Multi-disciplinary skills are required to contribute to a successful due diligence investigation – valuation, commercial, financial, legal and technical

An overriding value focus is critical to the effectiveness of the due diligence process

FINSIA81

March 2012

PwC

What is due diligence?

Investigation of a target based on a sound understanding of the acquirer’s current strategy, situation, skill base and vulnerabilities

Investigation of value assumptions which assists to explain the value proposition and provides effective input into the final investment decision

Provides insight into potential deal breakers, significant risks and commercial issues

Considers the post acquisition integration plan and realisation of material synergy benefits

FINSIA82

March 2012

PwC

Deal readiness

Many companies are consistently underprepared for M&A activity –whether they are a potential target or an acquirer

M&A is a skill that must be developed

Experience suggests that frequent M&A participants have better prospects of success – some empirical evidence to this effect

An incomplete transaction can be a valuable learning experience, which can inform corporate strategy including future M&A transactions

Deal readiness activities can inform corporate strategy, lead to greater understanding of value drivers and improve the resilience of thebusiness

Deal readiness can be considered from a buyer and a sellers perspective

FINSIA83

March 2012

PwC

Deal readiness – divestment framework

• Divestment strategy and enhanced business planning should be undertaken early to achieve the optimum divestment result

• Common consequencesof being under-prepared are:

- significant value can be lost due to a valuation discount being applied by the buyer to offset perceived ‘unknowns’ or ‘risks’; or

- a buyer is deterred due to perceived risks associated with the opportunity, thereby reducing competitive tension in the process.

Stage 1 Strategic

Options Review

Stage 2 Preparing

Business for Sale

Stage 3Transaction

Execution

Divestment Framework

Determi ne shar ehold er objecti ves

Transaction op tions analysi s

Assess valu e and buyer uni ver se

Establish preferr ed strategy

Prepare d etail ed strategic plan

Opti mise bus ines s operation s

Sanitise f inancial/l egal/tax records

Oth er sharehol der plann ing

(e.g. tax)

Strateg y & planning

Deal & market anal ysis

Transaction process & negotiation

Settlemen t and compl etio n

84

PwC

Barriers to entry

• Strength of br ands and rel ated intellectual property

• Scal e of operations and rel ati ve effici ency

• Production know how• Strength of dis tribution networ ks• Sal es r elationships and s trength

of cus tomer contracts

Su pply Characteristics

• Level of concentr ation and flexi bility of suppl y

• Generic vs . specialised natur e of inputs

• Market based vs . neg oti ated prici ng of inputs

• Nature of any suppl y contrac ts ( pricing, tenure)

Key In dustry Play ers

• Level of competiti on / concentr ati on and conduc t of players

• Competitors as potenti al acquirers (and extent of any synergies and consolidati on benefits )

• Over all industr y gr owth and trends

• Over all industr y margins and retur ns

Alternatives

• Existence of any alter nati ve products and ser vices

• New technol ogical devel opments and other innovati ons

Cu stomer Characteristics

• Level of concentr ation (and thus r eliance)

• Spr ead of channels and routes to mar ket

• Customer sticki ness• Nature of any customer

relati onshi ps and/or contrac ts

• Market tr ends

Key Influencing Factors (examples): Other Key Factors

Internal Factors

• Future earni ngs and cash flow profil e (including opportuni ties and risks)

• Bal ance sheet compositi on

• Strength of manag ement team and gover nance s truc tur e

• Organisati onal capabiliti es & culture

• Simplicity of ownership struc ture

• Potenti al for oper ational impr ovement (and/or synergies)

• Ability to retai n key employees

• Lack of percei ved liabilities fr om historical events

• Quality of sys tems and processes(IT, accounti ng, contract variations)

• Extent of any sur plus assets and liabilities

Ext ernal Factors

• Comparabl e company trading and historic industr y transacti on multipl es

• State of debt and eq uity mar kets

• Impact of any potenti al reg ulator y chang es

Deal readiness – review of value drivers

85

PwC

Maximising value from deal readiness

Demon stratin g the strengths and potent ial of the Busine ss is key t o value maximisation

+

_

Shar

ehol

der

valu

e

Exceed inve stor / buyer

expectations

Active management to realise the

value from deal readine ss activitie s and

planning

…and to minimise

the impactof potential

risks and process

complexit ies

The Business

Lack of confidentiality Delay s in

agreein g terms and condition s

Incomplete / poor quality of

information Concealment of issue s

Lack of focus in managin g the

business durin g the sale / se ll-down proce ss

Strict timetable

Competit ive tension

Prepare for and pre-empt

like ly quest ion s/

issues

Identify growth option s for inve stors /

buyers

Quantify valuable

synergie s for key trade

buyers

Effective negotiat ion

with attention to detail

Ti ght Pr ocess

Be P r epa r ed

86

PwC

Value Drivers

FINSIA87

March 2012

PwC

Value driver decision tree

FINSIA88

March 2012

Cor porateValue

Equity value

Dis counts

Enterpr is e value

Tax rate

Working c apita l

Fixed capi tal

Rev enue

Cas h cos ts

Weighted Av erageCost of Capi tal

Compet itive advantage per iod

Minority

Gov ernance

Size

Marketabil ity/liquidity

Overhang

Debt

Produc t base

Price

Volumes

Sel lingConv ersionResource acquisitionOverhead

Tax ratesInternal capital structureIncent ives

Receiv ablesInventor iesCreditors

InnovationMarketingPeopleProcess

Interest ra tesMarket riskSyst ematic risk correlationGear ing

duration of competitive advanta ge

spec if ic r is ks

Existing productsNew products

Customer va lue proposi tionCompet itive ten sion

Demand –-- c onsumer sentimentCapacity

Cor porateValue

Equity value

Dis counts

Enterpr is e value

Tax rate

Working c apita l

Fixed capi tal

Rev enue

Cas h cos ts

Weighted Av erageCost of Capi tal

Compet itive advantage per iod

Minority

Gov ernance

Size

Marketabil ity/liquidity

Overhang

Debt

Produc t base

Price

Volumes

Sel lingConv ersionResource acquisitionOverhead

Tax ratesInternal capital structureIncent ives

Receiv ablesInventor iesCreditors

InnovationMarketingPeopleProcess

Interest ra tesMarket riskSyst ematic risk correlationGear ing

duration of competitive advanta ge

spec if ic r is ks

Existing productsNew products

Customer va lue proposi tionCompet itive ten sion

Demand –-- c onsumer sentimentCapacity

PwC

Weighted average cost of capital assessment

Accurate cost of capital assessment is critical to target evaluation and transaction pricing

Cost of capital is a key component of the value equation and whether shareholder value is enhanced

Some acquirers underestimate the true cost of capital, or have poorly developed frameworks for accurate and robust assessment

Weighted average cost of capital (nominal or real, after tax basis) needs to be effectively linked to cashflow assessment

Topical current issue – low bond rates and how to incorporate into cost of capital assessment – low bond rates do not necessarily mean reduced risk of equity investment

FINSIA89

March 2012

PwC

Quality of earnings

• Objective of quality of earnings analysis is to provide a sound basis for the assessment of sustainable future earnings or cashflows

Reported earnings can incorporate the impact of many factors:

• Effect of changes in market conditions

• Changes in profitability as volumes, costs and prices change

• Relative bargaining power of customers and suppliers

• Effect of discontinued operations

• Acquisition or commencement of new businesses

• Private owner and related party transactions

• One-off transactions and incidence of disputes and variations

• Changes in accounting policies and practice

FINSIA90

March 2012

PwC

Quality of earnings

Earnings trends can be obscured without specific recognition andunderstanding of these factors

Robust assessment of recent earnings provides effective insights into the key value drivers of significance to the target business

The impact of changes in volumes, prices and costs should be analysed

Reported earnings and EPS impact of the acquisition likely to be critical for most buyers

FINSIA91

March 2012

PwC

Working capital and cashflows

Focus on value: Working capital impacts price and funding

FINSIA92

March 2012

(8 ,00 0)

(6 ,00 0)

(4 ,00 0)

(2 ,00 0)

-

2,0 00

4,0 00

6,0 00

8,0 00

1 0,0 00

1-Mar-11

13-Mar-11

15-Mar-11

17-Mar-11

19-Mar-11

21-Mar-11

23-Mar-11

25-Mar-11

27-Mar-11

29-Mar-11

31-Mar-11

31-Mar-11

2-Apr-11

4-Apr-11

6-Apr-11

8-Apr-11

10-Apr-11

12-Apr-11

24-Apr-11

26-Apr-11

28-Apr-11

30-Apr-11

30-Apr-11

2-May-11

4-May-11

6-May-11

8-May-11

10-May-11

12-May-11

14-May-11

16-May-11

18-May-11

20-May-11

22-May-11

24-May-11

3-Jun-11

5-Jun-11

7-Jun-11

9-Jun-11

11-Jun-11

13-Jun-11

15-Jun-11

17-Jun-11

29-Jun-11

30-Jun-11

1-Jul-11

3-Jul-11

5-Jul-11

7-Jul-11

9-Jul-11

11-Jul-11

13-Jul-11

15-Jul-11

17-Jul-11

19-Jul-11

21-Jul-11

23-Jul-11

25-Jul-11

27-Jul-11

29-Jul-11

8-Aug-11

10-Aug-11

12-Aug-11

14-Aug-11

16-Aug-11

Net cash movement fro m 1 M arch 2011 to 16 Au gust 2011

No r ma lised ne t ca sh mo ve me nt Ow ne r in ject ion s/withd raw als int o bu sine ss Cum ul ativ e n et c ash mo vem ent

PwC

Composition and quality of assets and liabilities

Traditional financial due diligence has focussed on assets and liabilities on the balance sheet

Forecast cashflows and transaction price likely to imply a substantially different value for the underlying assets and liabilities of the target

Substantial values for intangible assets are often paid, particularly in the services sector – compare net tangible assets per share and price paid per share

Prominent intangible assets can include:

• Customer contracts and relationships

• Brands

• Franchise agreements

• Goodwill (location, assembled workforce, know-how, excess capacity, growth)

FINSIA93

March 2012

PwC

Composition and quality of assets and liabilities

• Due diligence on these intangible assets is likely to require a multi-disciplinary approach (beyond traditional balance sheet due diligence) covering:

• Management of customer contracts and customer engagement

• Brand management and marketing effectiveness

• Workforce retention and integration/cultural fit issues

• Cost of excess capacity and strategies for growth

• An accurate picture of these intangible assets (and effective management of these assets post acquisition) is likely to be critical to the acquisition strategy

• A preliminary purchase price allocation exercise will highlight the intangible asset values and the potential profile of amortisation affecting the reported earnings in future years

FINSIA94

March 2012

PwC

Post acquisition synergy benefits

Due diligence on material synergy benefits is required pre-acquisition –simple high level identification is not enough

High level pre-acquisition estimates of synergy benefits, cost to achieve and time taken are often too optimistic

Development of a synergy realisation plan is essential if these are material to the transaction – the management team charged with achieving the synergies needs to be closely involved in this due diligence work in the pre-acquisition phase

Cultural issues need attention and careful but decisive management

The cost of delay in the realisation of synergy benefits is high – speed over precision is likely to be better

FINSIA95

March 2012

PwC

Vendor Due Diligence

FINSIA96

March 2012

PwC

Vendor due diligence – rationale

• Assists a vendor to maintain control over the sale process and the release of information to potential bidders

• Facilitates competitive tension between bidders as bidders can be brought up to speed very quickly

• Independent review provides confidence in the robustness of dataand reduces the likelihood of any surprises arising from bidders

• Opportunity for the vendor to review and assess upsides and riskareas to optimise negotiating position

• Mitigates attempts by bidders to use due diligence and exclusivity period to negotiate better terms

• An integrated vendor due diligence report provides the vendor with a unique opportunity to have input into the bidder’s view of the commercial, strategic and financial position of the business

FINSIA97

March 2012

PwC

Vendor due diligence – advantages

Vendors

• Minimises disruption to the underlying business and its management as there is only one full scope due diligence process

• Allows management early ownership to address any diligence issues

• Facilitates management’s understanding of the sale process

Purchasers

• Can aid in saving time, cost and aggravation through a detailed independent view of the business

• Confidence in the basis for offers and underpins the financing process

• Better due diligence outcome as it is less rushed and the team has better access to the business

• Better use of buyer’s time in exclusivity phase

FINSIA98

March 2012

PwC

Vendor due diligence – disadvantages

• Preparation of a vendor due diligence report takes time which might delay the start of a sale process

• The time involved in preparation may potentially distract management from day-to-day operations

• The vendor incurs the cost of the vendor due diligence report regardless of whether or not a sale is realised

• Further due diligence will still be required (although on a limited basis)

• Confidentiality may be compromised by providing such a detailed report earlier than normal in the transaction timeline

FINSIA99

March 2012

Thank you

Roger PortEmail: [email protected]

PANEL DISCUSSIONIdentifying the hot sectors and the top sources of deal flow

Chair: Mark Paganin SF Fin, Partner, Clayton Utz

» Aaron Hood, Executive Director, Catalyst Investments» Russell Philip, Partner, Corrs Chambers Westgarth» Roger Port SF Fin, Partner, PwC

Chair’s closing remarksMark Paganin SF Fin, Partner, Clayton Utz

Upcoming West Australian Events

YFP WHO’S IN THE ROOM? – Networking cocktails29 March 2012

YFP INSIDE THE BOARDROOM – Ashurst 4 April 2012

YFP INSIDE THE BOARDROOM – Bankwest 2 May 2012

LEADERSHIP LUNCHEON – Hon Christian Porter MLA 22 June 2012

Related Documents