LUMA partners The State of DIGITAL VIDEO Terence Kawaja

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LUMA partners

The State of DIGITAL VIDEO

Terence Kawaja

The Rise of Digital Video

Hours

29%

Source: eMarketer, comScore

U.S. Digital Video Proper6es Ranked by Unique Video Viewers

Average Time Spent per Day with Digital Video by Device in U.S.

YouTube Has Dominated the Rise of Digital Video

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8

2011 2012 2013 2014 2015

Tablet Smartphone Desktop Other

But Now It’s Not the Only Game in Town

Facebook Auto-Play Videos are Ubiquitous

75% From Mobile

4 Billion Daily Views

Mobile Apps Bring Live Content to Your Fingertips

Snapchat Has Built Mobile-First Advertising

Publishers Are Making Video Too

There Just Isn’t Enough Supply!

Display Ad CPM $1.90

Video Ad CPM $24.60

Source: ZenithOptimedia, Note: Average CPM

$2.9%

$4.2%

$6.0%

$7.8%

$9.5%

$0.0%

$1.0%

$2.0%

$3.0%

$4.0%

$5.0%

$6.0%

$7.0%

$8.0%

$9.0%

$10.0%

2012% 2013% 2014% 2015% 2016%

CAGR:&34%

&

CAGR:&172%

&

Source: eMarketer

$ billions

ProgrammaAc Video Digital Video

Digital Video Spend Continues to Rise

Source: eMarketer

$ billions

ProgrammaAc Video Digital Video TV

$0.0$

$10.0$

$20.0$

$30.0$

$40.0$

$50.0$

$60.0$

$70.0$

$80.0$

2012$ 2013$ 2014$ 2015$ 2016$

$64.5 $66.4 $68.5 $70.6 $73.8

But is Still Only a Fraction of the TV Market

Traditional Digital vs.

Traditional Digital vs.

100 : 1

19 Buckets 36 ~ 100 Companies ~ 400

$150 billion Total Spend $6 billion $1.5 Billion $ / Company $15 Million

Traditional TV vs. Digital Video Players

100 : 1

Market Cap: $2 Trillion Cash: $530 Billion

5x Cash

New Entrants Have Plenty of Money to Build or Buy

Screens

Delivery

Content

2008 Was So Simple: Traditional & Digital Silos

Delivery

Screens

Content

Second Screen Chromecast / Airplay

Partnerships “Netflix + Disney”

Convergence Begins with Device Proliferation

OTT/CTV

Delivery

Screens

Content Partnerships “Netflix + Disney”

Facebook Drones?

TV Economics

Content Channels Media MVPDs Device / UI

9,000+ Channels

CONSUMER

CTV

Devices

OTT

UI

Traditional TV Content Model

Content Channels Media MVPDs Device / UI

CONSUMER

Programs Networks Channel Bundles

“Must Carry” & Broadcast Content

Traditional TV Content Model

Content Channels Media MVPDs Device / UI

Tier 1 Cable and Broadcast Content

M A R K E T E R

CPG Upfronts $30BB

$40BB Spot and Scatter TV ads

$6.3BB Comcast bundles in sports content

C O N S UM E R Affiliate Fees

$40BB

Retrans Fees

$80BB Subscriptions

Traditional TV Content Model

Bundling Enables Pre-Funding of Content

10% Support 100%

Bundling Enables Pre-Funding of Content

Final Late Night Episode

Evolution of Top Rated Show

Most Viewed Episode

1993

1990

1992

80MM

52MM

38MM

Traditional TV Content Model

Final Late Night Episode

Evolution of Top Rated Show

Most Viewed Episode

1993

2007

1990

2013

1992

2009

80MM

30MM

52MM

8MM

4MM

38MM

Cross channel devices killed the television star!

Media Channels MVPDs Content Device / UI

CONSUMER

“Just broadband only, thanks!”

Subscription content on license

Discrete content

“Made for web” content

“I forget what channel it’s on I just stream it”

“Artist to Consumer”

Digital Opens Different Distribution & Content Strategies

Big $$$ A18-49 Reach

Incremental Budget

A25-54 Reach

Paying 30-50% more for .5-1% more reach?!

TRP

Source: Needham & Co. , Nielsen

Incremental Cost Per Reach Point

Incremental is Increasingly Expensive on TV!

eMarketer Digital Video Spend Projection

$0 $0

Source: eMarketer

eMarketer TV Spend Projection

Yet TV Dollars aren’t Slowing…

TV is Definitely Not Hurting Yet

Leslie Moonves, CEO

3 Year Compensation:

$186 Million

2014 Revenue >

Cracks In The Wall

Slack in Demand for Upfront Buys

OTT Options are Growing

$50-‐$70

$8

$9

$20

$99/year

$15

$6

Average Basic Cable Packages ~$120

Source: NPD Group

$15 Stream

Programmatic Platforms Targeting Technology Attribution / Analytics Low-Cost Production

Integrated Workflow

Premium Content Brand Relationships

Convergence of Two Worlds

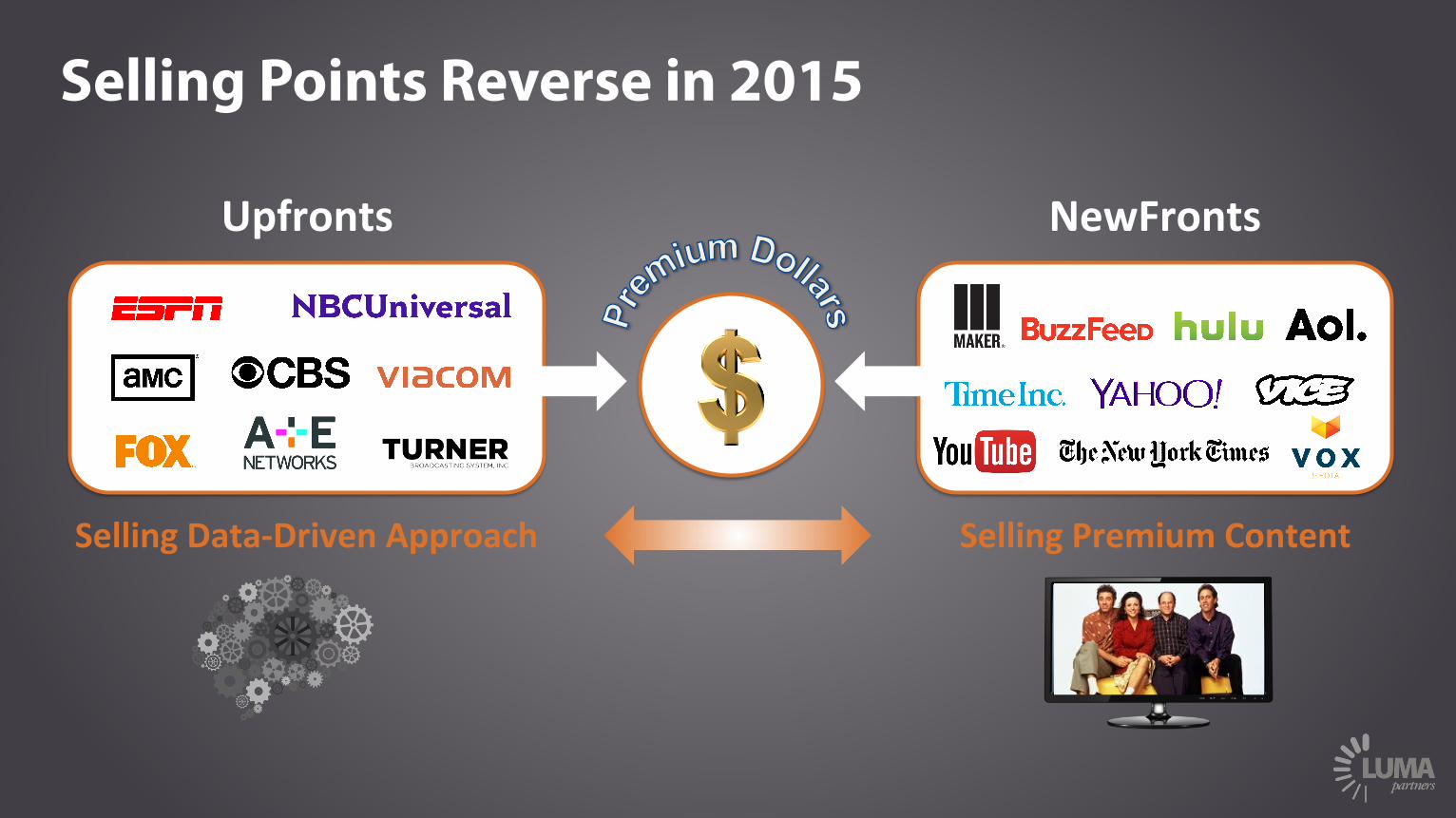

Selling Points Reverse in 2015

Upfronts NewFronts

Selling Premium Content Selling Data-‐Driven Approach

Selling Points Reverse in 2015

Selling Data-‐Driven Approach Selling Premium Content

Upfronts NewFronts

Now TV is Being Aggressive with Data

Credit Card Data

Subscriber Data Target Audience

Yogurt Buyers

Frozen Snack Buyers

Wireless Data Users

Inspired by WSJ

Digital is Increasing Investment in Original Content

Everyone is geVng in on the game

?

New Tier 1 Shows Backed with Tier 1 Talent

$0 $0

(1) Assumes 7.5% of TV Spend Shifts to Digital Source: eMarketer

eMarketer Digital Video Spend Projection eMarketer TV Spend Projection

Digital Dollars Could Double

Perception vs. Reality in Addressable TV

Linear TV Programma6c TV

Percep6on

Reality

Linear TV Addressable Linear TV

Video On Demand (VOD)

Over The Top (OTT)

Digital Video

Programma6c TV

WARNING: LUMA Decks Usually Call for More M&A

Convergent TV via M&A

CONTENT

DISTRIBUTION

MONETIZATION

Media

31 Video Deals in the Last 2 Years

Digital Video Has a Very Bright Future

1. Preferred Consumer Media 2. Continued Device 3. New Content Formats 4. Ad Inventory Shortage 5. TV Demand Shift 6. Strategic Exit Opportunities

New York | San Francisco | Palo Alto

Access. Insights. Execution.

LUMA partners

Thank you! @tkawaja

Related Documents