ALEXANDER SCHRÖDER/SVEN GROSS Low Cost Airlines and Coach Tourism – Threats and Opportunities for German Tour Operators in: Groß, S./Schröder, A. (Eds.): Handbook of Low Cost Airlines - Strategies, Bu- siness Processes and Market Environment, Berlin 2007, pp. 249-261 1 Introduction 2 Coach Tour Operators and Low Cost Airlines 2.1 Tour Operating Market Situation in Germany 2.2 Low Cost Airlines from a Coach Tour Operator’s Point of View 3 Coach Tour Operators and Low Cost Airlines 3.1 Using Airlines for the Tour Operating Business 3.2 Opportunities for using Low Cost Services for Coach Tourism and General Tour Operating Purposes 3.3 Selected Implications 4 Conclusions Abstract: The present paper gives a survey of the particularities when using airline ser- vices for (coach) tour purposes. The “low cost airline” product is examined with respect to its properties and in relationship to the tour operating business. It is the aim to demonstrate that the new services offered by low cost airlines on the tourist market create, on the one hand, a new competitive situation for tour operators. On the other hand, however, these services offer numerous opportunities to cooperatively improve each partner’s own prod- ucts and to establish new attractive trips on the market. Keywords: Medium-sized Coach Tour Operators, Coach Travel Market, Business and Distribution Model, Cooperation with Low Cost Airlines, Competition from Low Cost Airlines, Coach Tourism

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ALEXANDER SCHRÖDER/SVEN GROSS

Low Cost Airlines and Coach Tourism –

Threats and Opportunities for German Tour Operators

in: Groß, S./Schröder, A. (Eds.): Handbook of Low Cost Airlines - Strategies, Bu-

siness Processes and Market Environment, Berlin 2007, pp. 249-261

1 Introduction

2 Coach Tour Operators and Low Cost Airlines

2.1 Tour Operating Market Situation in Germany

2.2 Low Cost Airlines from a Coach Tour Operator’s Point of View

3 Coach Tour Operators and Low Cost Airlines

3.1 Using Airlines for the Tour Operating Business

3.2 Opportunities for using Low Cost Services for Coach Tourism and General Tour

Operating Purposes

3.3 Selected Implications

4 Conclusions

Abstract: The present paper gives a survey of the particularities when using airline ser-

vices for (coach) tour purposes. The “low cost airline” product is examined with respect to

its properties and in relationship to the tour operating business. It is the aim to demonstrate

that the new services offered by low cost airlines on the tourist market create, on the one

hand, a new competitive situation for tour operators. On the other hand, however, these

services offer numerous opportunities to cooperatively improve each partner’s own prod-

ucts and to establish new attractive trips on the market.

Keywords: Medium-sized Coach Tour Operators, Coach Travel Market, Business and

Distribution Model, Cooperation with Low Cost Airlines, Competition from Low Cost

Airlines, Coach Tourism

Alexander Schröder/Sven Gross

1 Introduction

The low cost airlines have established themselves during the last few years as a

new competitor for coach tourism. The fact that the new market situation hereby

created is being strongly discussed within the branch, is indicated, e.g., by different

workshops and conferences as well as by articles in periodicals, press releases and

statements on the subject of “low cost carriers”.1 However, not only risks for the

coach tourism business are being underlined, but also new market potentials and

additional opportunities if coach tour operators react to these market developments

by, e.g., creating new products and marketing strategies.

Anyway, the growing acceptance of low cost airlines by consumers is a general

challenge for coach tour operators to which they have to face up. The (coach) tour

operators have to adjust themselves to the changes on the European flight market

by developing suitable strategies. The strong sides of a coach round-trip may be

combined with the advantages of the services offered by low cost airlines. If these

new, attractive offers are introduced on the market, both coach tour operators and

low cost airlines can benefit from them. The conditions for such a strategy and the

opportunities for its implementation are the subject of what shall be discussed

below.

2 Coach Tour Oerators and Low Cost Airlines

2.1 Tour Operating Market Situation in Germany

On average over several years, the coach, being the most important means of

transport for holiday trips (of more than 5 days duration), always held a market

share of about 10% in Germany during the last 20 years (see figure 1). The airplane

in particular was able to gain more market shares over the last few decades. After a

short “slump” following the September 11, 2001 attacks, the airplane has regained

more importance again as a means of transport for holiday trips while the soaring

growth rates of low cost airlines played a major role in this respect.

___________________ 1 Such as at the German Travel Association (DRV) conference held during the Cologne Work-

shop of the International Coach Tourism Federation (RDA), at RDA general meetings, press

conferences and in press releases, at the coach tourism day and in articles published in the

“Omnibusrevue” and “busplaner” periodicals.

Low Cost Airlines and Coach Tourism – Threats and Opportunities

Figure 1: Choice of transport modes for main holiday trips over a time basis

Source: F.U.R. 2006

According to calculations made by the German Federal Statistical Office (Sta-

tistisches Bundesamt), the number of passengers on long-distance coach tours in

2005 dropped by 1.8% to 71 million travellers, compared to the previous year. Ac-

cording to the same source, 56 million or nearly 4/5 of all tourists travelled on

coaches hired by tour operators (Hired coach service2). This segment registered a

slight increase (2.1%). On the other hand, the number of travellers who participated

in trips offered by coach operators (excursion tours3) fell considerably. Compared

to 2004, there is a drop by 16.4% to 12 million customers.

As far as holiday destination trips4 are concerned, 2.2 million customers used

the coach option, which corresponds to a decline in the number of passengers by

3.6%. The service of carriage5 dropped particularly sharply for trips abroad and

from abroad (-6.8%), while for trips inside Germany, the service of carriage

decreased only by 1.9% (cf. Statistisches Bundesamt 2006).

___________________ 2 Hired coach service: Purpose, destination and program of the trip are determined by the

customer. 3 Excursion tours: The coach operator determines the purpose, destination and program for all

participants (e.g. day trips). 4 Holiday destination trips: Trips which are offered and carried out by carriers for a total charge

including outward and return journey as well as accommodation with or without meals (e.g.

holiday trip to Spain). 5 Service of carriage: Product of the number of people transported and the travelling distance.

In 2005, this figure amounted to about 5.6 thousand million person-kilometres.

Car

45%

Airplane37%

10%Coach

6% Train

0

10

20

30

40

50

60

70

1960 1970 1974 1978 1982 1986 1990 1994 1998 2000 2002 2004 2005

Alexander Schröder/Sven Gross

For the German coach tour operators, these figures indicate, besides other factors

such as the general economic situation, also a certain impact created by low cost

airlines. There is a certain relationship between the fall in excursions and holiday

destination trips as well as between the decreasing number of trips abroad and the

services offered by low cost airlines. Consequently, the latter should be considered

as a new competitor for coach tour operators. This conclusion is supported by opin-

ion polls made by the International Coach Tourism Federation (RDA, e.g. RDA

trend analysis) and the “busplaner” magazine.

According to the RDA trend analysis, about 50% of the questioned coach tour

operators held the opinion in 2003 that low cost airlines should be considered as

competitors. 24% believed that these airlines act as general competitors while 18%

saw the competitive situation only with respect to common destination areas. 55%

of the tour operators did not see any urgent need for action, while 21% said that

they would cancel the such destination areas from their program, and 16% declared

their intention to highlight even more the strong points of the coach as a means of

transport (cf. Geiger 2003, p. 28).

In another opinion poll conducted by the periodical “busplaner” in autumn

2005, almost 60% of the people questioned already named the low cost airlines as

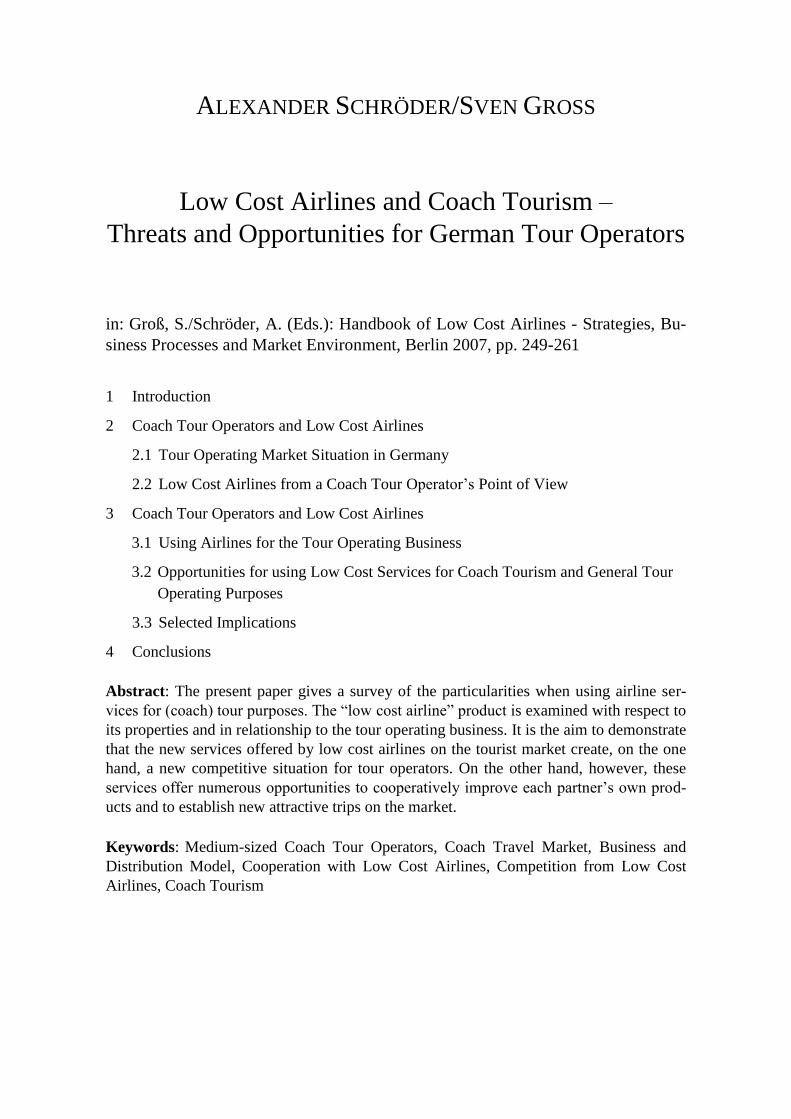

being the most important competitor for coach tour operators (see figure 2).

Another interesting point is the fact that low cost airlines are considered to be

bigger rival than any competitors from the field of coach tourism business. Railway

companies which are often regarded as one of the hardest competitors, remains

below 10%. All other competitors mentioned also stay below or around 10%,

except the big tour operator groups (22%).

Figure 2: Competitors of coach tour operators (n=45)

Source: Geiger 2005, p. 40

0 10 20 30 40 50 60

Figures in %

Internet

Tour sale in supermarket

Railway

Tour sale on TV

All-Inclusive providers

Flight carriage providers

Big tour operator groups

Other tour operators

Low cost carriers

Low Cost Airlines and Coach Tourism – Threats and Opportunities

The biggest danger caused by low cost airlines to coach tour operators concerns

one of their “prides and joys”: the city tour. Since, in Europe, low cost airlines

serve mostly airports between economic centers providing large numbers of pas-

sengers and a high demand potential, their services can also be easily used by tour-

ist travellers (primarily for weekend or short holiday trips).

Another risk factor for coach tour operators occurs when consumers start com-

paring prices. They wonder why they should pay, e.g., for a trip to Paris much more

if they go by coach if they can get there – seemingly – much cheaper by plane.

Provided fair costing and pricing, coach tour operators are absolutely unable to

compete with prices offered by low cost airlines, e.g. for trips to European big cit-

ies. Nevertheless, coach tour operators have to accept being rated against the low

base prices of low cost airlines. However, not all customers are aware of the fact

that tickets are sold at different prices and that there are extra charges (e.g. safety

fees and airport taxes) in most cases. The advertised low cost tickets account only

for a small part of the low cost airlines’ offer. When sold in the process of the

booking procedure, their price mostly increases to the level of what established air-

lines, such as Lufthansa, charge. This low-price ticket portion varies according to

the airline from about 10% to up to 70% (Ryanair) of all seats available. In most

cases, it covers about 20-30% (cf. Ramm 2002, p. 10). As soon as this ticket alloca-

tion is sold, the price goes up mostly in steps and may reach or even go beyond the

prices of established airlines (cf. Groß/Schröder 2005, pp. 58-61).

Furthermore, many customers are not aware of the fact that certain low cost

airlines often use secondary airports frequently located far away from their place of

residence or destination area, thus adding quite significant costs and extra time to

the bill. On the other hand, a high-quality coach tour provides a door to door home

pick-up service and a comfortable journey to the accommodation facility. There are

no extra charges for travellers, and the higher time expenditure involved is

compensated by good comfort (e.g. when 4- or 5-star coaches are used). Besides,

there is also the opportunity to combine a longer ride to the destination area with an

(for the traveller) interesting program or even overnight stop-over stays.

Finally, looking at the general market situation, it should be noted that the

target group of low cost airlines is no longer made up of only younger, well earning

and well trained customers. Services offered by the “low cost carriers” are more

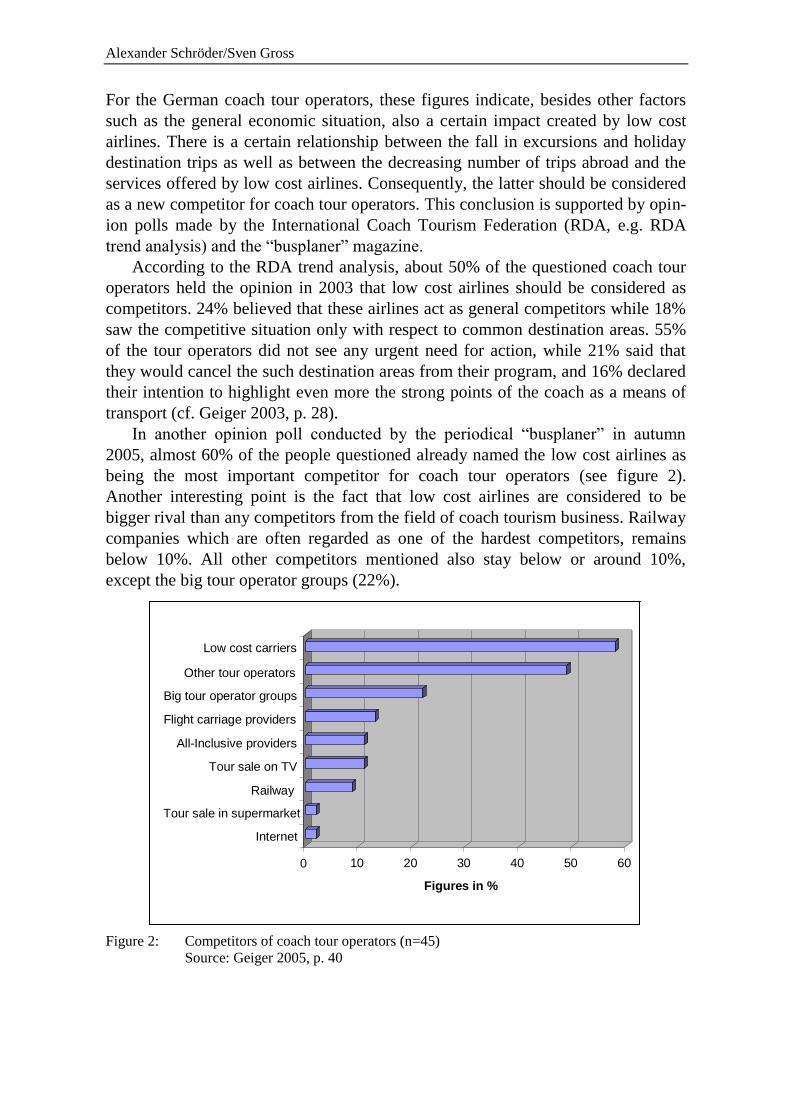

and more used also by older people. The example of Hapag Lloyd Express (HLX)

is very illustrative in this respect: While in 2002, the over 50 year old were still

underrepresented compared to their part of the total population, they account for

almost the same share in 2004 (see table 1). For the coach tourism operators, this

means that one of their main target groups has moved more “into the line of fire” of

low cost airlines, thus increasing the danger to them.

Alexander Schröder/Sven Gross

Age 2002 German population 2004

under 34 years 35.6% 30.1% 32.0%

35-49 years 42.3% 36.1% 38.4%

50+ years 22.1% 33.8% 29.6%

Table 1: Customers of low cost airlines are getting older – the example of HLX

Source: Kurth 2004

2.2 Low Cost Airlines from a Coach Tour Operator’s Point of View

The segment of low cost airlines registered high growth rates in the last few years.

Their European market share grew from about 2% (1999) to 16% in 2004, and will,

according to estimates, cover about one-fourth of the European air traffic market by

2010 (cf. McKinsey & Company 2005).

Figure 3: European flight market share

Source: McKinsey & Company 2005

However, figure 3 also shows that the growth rate will slow down, resulting in a

further shake-outs and consolidations on the European low cost flight market. What

started with the takeover of Buzz by Ryanair or of Go by easyJet, and with the

insolvencies of certain other airlines on the European market, continued in 2006

with the buyout of dba by Air Berlin. Likewise, TUI’s decision to merge Hapag

Lloyd Express with the sister company Hapagfly (formerly Hapag Lloyd Flug) to

the common brand TUIfly in January 2007, is also an indication of further

consolidations on the European flight market.

Development of Market Shares

75% 72%66% 62% 60%

23%21%

18%18% 16%

7%16% 20% 24%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1998 2001 2004 2007E 2010E

Network Carrier Charter Airlines Low Cost Airlines

Low Cost Airlines and Coach Tourism – Threats and Opportunities

The services offered by the low cost airlines have changed the market. As has been

demonstrated, the services offered by the low cost airlines are in competition with

the tour operators business, such as for city tours or holiday destination trips. But

the inexpensive offers have also created a large number of new and low cost flight

connections to touristically interesting destinations, forcing the established airlines

to also offer lower prices on the market.

3 Coach Tour Oerators and Low Cost Airlines

3.1 Using Airlines for the Tour Operating Business

Until now, coach tour operators have been using the airlines’ flight services

according to the following classic pattern: purchase of ticket allocations at group

fares before the seasonal start or as an optional booking in connection with the

catalogue program preparation. When the option deadline was due, the required

quantities of tickets were firmly purchased (firm sale) or cancelled without any

extra charges according to the booking situation. There was a relatively small risk

for the tour operator although the number of flight trips purchased by a single

coach tour operator was comparatively small.

Considering the different business models applied by low cost airlines, the

following categorization can be established from the coach tour operators’ point of

view.

Low Cost Business Model “in the narrowest Sense”

The Ryanair airline is one of the companies which apply (almost) all elements of

the business model as far as strategic planning (e.g. choice of secondary airports,

outsourcing, aircraft procurement, etc.) and operational implementation (e.g.

minimisation of turnaround times, almost complete abandonment of free services,

etc.) is concerned, and it may, thus, be conceived as a low cost business model “in

the narrowest sense” of the term. From the (coach) tour operators’ point of view,

these offers hardly bear any interest. The destination airports are in most cases

located far away from the destination area properly speaking and generate high

transfer costs (e.g. Barcelona: airport at Reus or Girona, Hamburg: airport at

Lübeck). Group tours or tour operator rates have not (yet) been on offer. Ticket

allocations, optional bookings or cancellations are not possible, and rebooking or

change of name is subject to high charges.6 The services offered are strictly end

customer-orientated, and when booking is done, the full price must be paid (e.g. by

credit card) and the precise name must be given (firm booking).

___________________ 6 Rebooking is possible at a charge of £ 17/€ 25 (through www.ryanair.de) or of £ 30/€ 45

(through Ryanair’s central booking office) per person and simple flight as well as against

payment of the price difference between the originally paid fare and the lowest flight fare at

the point of the rebooking procedure. Name changes can be made at a charge of £ 45/€ 65 per

personal name (cf. www.ryanair.com).

Alexander Schröder/Sven Gross

Low Cost Business Model “in the narrow sense”

The easyJet business model is different in some points. The served airports are of

the large-size type, centrally located, but subject to frequent delays and higher

charges, and the company publishes its own in-flight magazine. Consequently, this

strategy may be categorized as a low cost business model “in the narrow sense” of

the term. It also allows optional booking or cancellation of flights. However, tour

operators may register with easyJet and book flights by using a company credit

card (cf. http://www.easyjet.de: easyJetb2b), while a firm sale of tickets with name

identification is also applied here.

Low Cost Business Model “in the broader sense”

Companies such as HLX, Germanwings or Air Berlin are examples for the business

model ”in the broader sense” of the term. HLX and Germanwings accept group

bookings and allow inquiries without any obligations for 10-189 persons (HLX) or

for groups of at least 10 persons (Germanwings). If the offer is accepted, a firm

quantity of tickets has to be booked at the customer’s own risk. The names of

passengers may be changed free of charge and as often as desired until 2 or 4 days

before departure. Afterwards, no more changes are allowed (Germanwings), or

changes may be made between 48 to 2 hours before departure through the

company’s service center at a charge of 25 Euros per person (HLX) (cf.

www.hlx.de; www.germanwings.de, as of December 2006).

Air Berlin implemented its business system primarily through the application of

yield and lean management with resulting cost savings and high occupancy rates.

Furthermore, a major role is played by focussing on customer loyality, which is

achieved mainly through the offer of additional services (such as catering included

in the fare) and the use of a frequent flyer scheme. Besides direct sale through the

Internet, distribution is also ensured by travel agents and tour operators. Air Berlin

has included in its group section the opportunity to reserve options for groups at

special prices. Booked flights may be cancelled subject to time-depending charges7,

leaving the risk not only with the tour operator.

Some charter airlines may also be included in the “broader sense” business

model. Having adopted certain elements of the low cost business model (e.g.

Condor), they are increasing the sale of single seats to compensate for the erosion

of the tour operator business. This mixed model is aimed at both the tour operators

(classic charter business) and the single ticket sale by means of the low cost pricing

system in order to increase occupancy rates and to reduce dependence on the tour

operating business. Adjustments to the new market conditions are made by offering

tickets at one-way prices, adapting fares to the booking situation and reducing the

optional ticket possibilities. The lower the fares are, the tighter get the option

deadlines.

___________________ 7 Current cancellation charges are between 20% (21 days before departure) and 50% (1 day be-

fore departure) and amount at least to 25 Euros (company information, as of December 2006).

Low Cost Airlines and Coach Tourism – Threats and Opportunities

Consequently, there are several opportunities for tour operators to use the low cost

airlines. In most cases, the different business or distribution models of the low cost

airlines are used in a blend while the actual number of occasions depends, among

other factors, on the services provided by the low cost airlines in the tour operator’s

“catchment area”. Similarly, information on expected demand plays a major role

for tour operators. The more precise the demand forecasts for a running season are,

the less risks are involved for firmly purchasing low cost ticket allocations.8 But it

should not be forgotten either that the established airlines (e.g. Lufthansa) also pro-

vide favorable offers for group tours.

3.2 Opportunities for using Low Cost Services for Coach Tourism and

general Tour Operating Purposes

As far as the practical application is concerned, there are a number of opportunities

in relationship with the different travel schemes used by coach tour operators (see

comments on terms in chapter 2.1). These opportunities and any related problems

will be demonstrated in the following section. Chapter 3.3 then covers the

implications for tour operators and airlines.

Low cost airlines may be used as shuttle services for coach round-trips. This

can be done in combination with optional coach transport to the point of departure,

e.g. to Spain or Greece. The customer may choose between transport by coach or

plane to and from the point of departure (transport alternative). The tour operator

uses his own round-trip coach for the whole round-trip.

Another opportunity is the combination of coach and plane transport to the

point of departure for two interlinked tours (plane/coach option). All travellers of

tour no. 1 go to the destination area by coach and embark there on the local round-

trip. On the last day, travellers of tour no. 1 fly home again, and the customers of

the follow-up tour no. 2 fly to the destination area. Then, the round-trip (tour no. 2)

is carried out on site, and at its end customers return home by coach. However, this

system bears the danger of a much bigger demand for the tour including return

transport by plane (tour no. 1) than for the other tour with return transport by coach

(tour no. 2).9 But this problem may be solved through pricing by offering, e.g., tour

no. 1 at a higher rate.

___________________ 8 For the airlines which allow firm bookings without indication of name.

9 Experience has shown that customers of round-trips to far-away destination areas consider it

important to get quickly back to their homes. This desire is matched by the return transport by

plane (tour no. 1).

Alexander Schröder/Sven Gross

On the other hand, it is also conceivable to produce pure flight trips. For this pur-

pose, there is the possibility of using a local round-trip coach or of posting own

coaches in the destination area. Additionally, it is possible to organize a flight

transfer from A to B within the destination area. For example, a low cost airline

may be used for returning passengers after a round-trip in Italy.10

In order to comply with the new regulation on driving times and rest periods11

of the European Union, tour operators may use the possibility of transporting the

replacement drivers for low costs to/from the destination area.

For package tours including a stay at an on-site hotel, e.g. on the Italian island

of Ischia, low cost airlines may be used as feeder service instead of a shuttle bus12.

During weak seasonal periods such as in winter, (price-)attractive low cost flight

trips including hotel accommodation to suitable destination areas may be

integrated, thus generating new sales revenues.

In the field of coach hire service, an obvious approach consists in using low

cost flights when programs for particular groups (i.e. excluding catalogue tours) are

conceived. In this case, it is an advantage that the group size is mostly known at the

booking time and that, consequently, flights can be booked with a relatively small

risk.

Many coach tour operators also run their own travel agencies or offer tours for

individual customers. For them, specific offers including low cost flights, accom-

modation, transfer and/or on-site services may be designed.

From the (coach) tour operators’ perspective, some of the following problems

might occur when these opportunities are implemented:

– Catalogue preparation: In most cases, fares and flight schedules are not yet

available when the catalogue is published; however, this is a general problem in

the tour operator business.

– System of prices and conditions: Fares go up with increasing ticket purchase

quantity per flight (e.g. Ryanair or easyJet) or flights must be firmly booked

(e.g. HLX, Germanwings). If the tour is cancelled by the customer, cancellation

charges of tour operators13 do often not cover the costs for firmly booked low

cost flights.

___________________ 10

There a such offers by the Italian Volareweb.com for flights from the south of Italy to Milano. 11

The new regulation will come into force on 11 April 2007. It includes the stipulation that a

coach driver has to observe his weekly rest period of at least 24 hours already after six days of

round-trips and holiday resort trips, and that he has to rest for 45 hours after another six days. 12

I.e. that the tour operator uses a regular transfer bus for transfering customers to the holiday

site and back again. 13

According to the General Business Conditions of the tour operator Eberhardt TRAVEL, the

cancellation charges for a withdrawal up to four week before departure amount to 5% of the

total tour price or at least 30 Euros.

Low Cost Airlines and Coach Tourism – Threats and Opportunities

– Liability: The liability of the low cost airlines is limited to the flight fare in

most cases. If the flight had been sold under package tour arrangements, the

tour operator will be held responsible for the entire tour. If the customer cannot

start off on his journey due to flight cancellations, the tour operator has to

refund the tour price and pay compensation for lost holiday time.

– Image and quality problem: In certain cases, the low (advertised) fares are

conceived by customers as being due to lacking or bad safety standards.

Similarly, missing free-of-charge extra services such as catering,

newspapers/periodicals or the smaller seat distance are often interpreted as

lower quality and not accepted by all customers.14

3.3 Selected Implications

From the above-mentioned opportunities and risks arises the need to act for both

coach tour operators and low cost airlines. A number of opportunities for

integrating low cost airline services into the catalogue program was demonstrated.

In this respect, the following points may be implemented:

When the flight offer is being planned and the low cost airline services are

integrated, it should always be checked what the total costs are, taking into account

taxes, fees or fuel charges as well as any additional transfer costs in case of remote

airports. The low cost offers should only be used for selected tours by considering

the value for money aspect. It is still important to compare prices to the offers

provided by conventional airlines since they have a great number of attractive

group fares.

If the offers allow it, tour operators should possibly concentrate on a minimum

number of airlines in order to increase their long-term bargaining power allowing

them to obtain better conditions. The still high competition pressure on the

European low cost market may also be used for bargaining to obtain better

conditions. However, airlines such as Ryanair or easyJet have hardly been willing

to engaged themselves in such business talks. In this respect, better conditions are

provided by HLX or Germanwings (group bookings with firm sale) or by the tour

operating-orientated Air Berlin offering optional booking opportunities.

For catalogue tours, customers usually expect firm prices. Integrating low cost

flights (such as provided by easyJet) into the catalogue prices allows to come up

with an average price similar to the price system applied by low cost airlines, in

order to make up for price differences between the various flights.

___________________ 14

For example, customers of a tour operator refused to fly the ”low cost airline” easyJet and

cancelled the tour when they received the travel documents.

Alexander Schröder/Sven Gross

In order to solve the cancellation problem, the tour operator’s T&Cs may be ad-

justed accordingly by adding under the “cancellation by the customer” paragraph

an additional clause for tours “including booking of a low cost airline flight”.15

For a round-trip with optional arrival transfer to the point of departure, the coach

round-trip shall be offered in the catalogue without transfer service so that the cus-

tomer may book the low cost flight at the daily price.

The image problem of low cost airlines occurring to some extent may be

improved upon by tour operators by informing potential customer about the

business model of low cost airlines, thus reducing any possible safety concerns.16

In order to maintain a certain quality level for the customers, a departure service for

groups may be provided at departure airports. This may be ensured by the tour

guide or staff of the (coach) tour operator. These services can include a collective

check-in or catering services for the customers (provided by partner organisations

at the airport).

Similarly, the opportunities available in the incoming business sector should be

used as well. Holiday-maker groups who used to travel on a local coach to their

destination area, fly low cost today. For these target groups, attractive offers may

be conceived in order to boost the incoming business.

On a long-term basis, low cost airlines should also adapt themselves to the

changing market conditions. Similarly to certain charter airlines which have come

closer to the business model of low cost airlines, the latter should take advantage of

the opportunities arising from the cooperation with tour operators. Above a certain

number of tickets sold by the tour operator, conditions should be adjusted to the

requirements of the tour operator and additional staff, such as a key account

manager, should be employed. This would allow to strengthen the ties between the

tour operator and the airline. Other forms of cooperation such as transfer service

from or to the airport, matching of groups for round-trips etc., could be considered

together with the local tour operator. Such cooperation is already being practised

with car hire companies and hotels.

___________________ 15

For example, besides the general cancellation charges for package tours, the tour operator

Eberhardt TRAVEL has included in his T&Cs special terms with higher costs for sea tours

and river cruises. 16

Other arguments include the fact that low cost airlines have very young fleets (e.g. easyJet)

and that there is no way to achieve savings in the safety area because of the stringent regula-

tions applicable to all airlines (cf. for more details Groß/Schröder 2005, pp. 43f.).

Low Cost Airlines and Coach Tourism – Threats and Opportunities

4 Conclusions

As has been demonstrated, services provided by low cost airlines have created a

new competitive situation for coach tourism, mainly leading to a drop in demand

for trips provided by coach tour operators. For the future, further growth of the low

cost market and corresponding impacts on coach tourism can be expected.

However, the services provided by low cost airlines do not only bear risks, but also

a number of opportunities for (coach) tour operators. The design of new, innovative

products allowing to combine the conventional coach round-trip with the low cost

services, offers new sales opportunities. However, processes and techniques

applied by tour operators sofar must be better geared to the new conditions.

Similarly, low cost airlines should adjust their business systems in some points in

order to suit the needs of tour operators.

Bibliography F.U.R. – Forschungsgemeinschaft Urlaub und Reisen: RA 2005 – Die Reiseanalyse 2005 – Be-

richtsband; Kiel 2006

FVW International: Jeder zehnte Sitz zum Schnäppchenpreis, 2003, No. 22, p. 80

Geiger, M.: Preiskampf über den Wolken; In: busplaner 2003, No. 9, pp. 28-30

Geiger, M.: Quo vadis Bustouristik?; In: busplaner 2005, No. 10, p. 40

Groß, S./Schröder, A.: Low Cost Airlines in Europa – eine marktorientierte Betrachtung von Bil-

ligfliegern; Dresden 2005

Kurth, W.: Stimulanz der Nachfrage schafft Wachstum – Das Marktpotential der Niedrigpreis-

Airlines; Bensberg 2004

McKinsey (Ed.): Business Breakfast – Billigflieger in Europa; 2005, www.mckinsey.de

Ramm, T.: Germanisch fliegen; In: Touristik Report, 2002, No. 20, p. 10

Statistisches Bundesamt: Fernreisen mit Omnibussen 2005: Rückgang bei Fahrgastzahlen; Pres-

semitteilung December 27, 2006, http://www.destatis.de/presse/deutsch/pm2006/

p5430191.htm

15

Related Documents