Looking over the Horizon A Review of Trends in Residential Brokerage REAL Trends Consulting

Looking over the Horizon A Review of Trends in Residential Brokerage REAL Trends Consulting.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Looking over the Horizon

A Review of Trends in Residential Brokerage

REAL Trends Consulting

Looking over the Horizon

The Housing Market

Change in Consumers

The Brokerage Challenge

The Brokerage Opportunity

The Housing Market

Inventory currently running at 11-12 months

Shadow inventory adds from 4-6 months of additional supply

The Housing Market

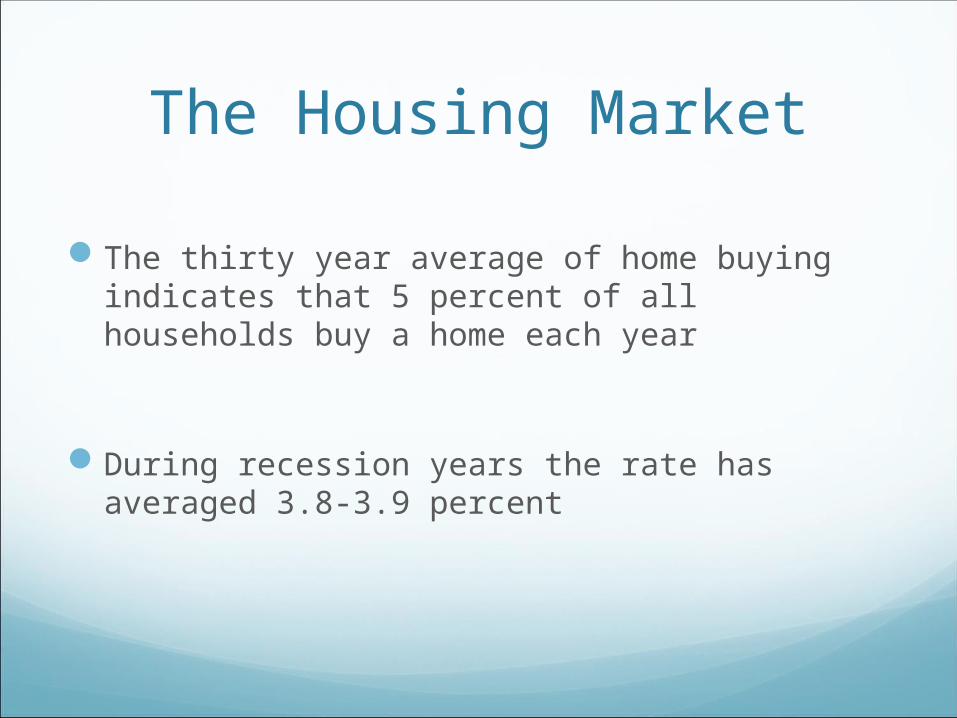

The thirty year average of home buying indicates that 5 percent of all households buy a home each year

During recession years the rate has averaged 3.8-3.9 percent

The Housing Market

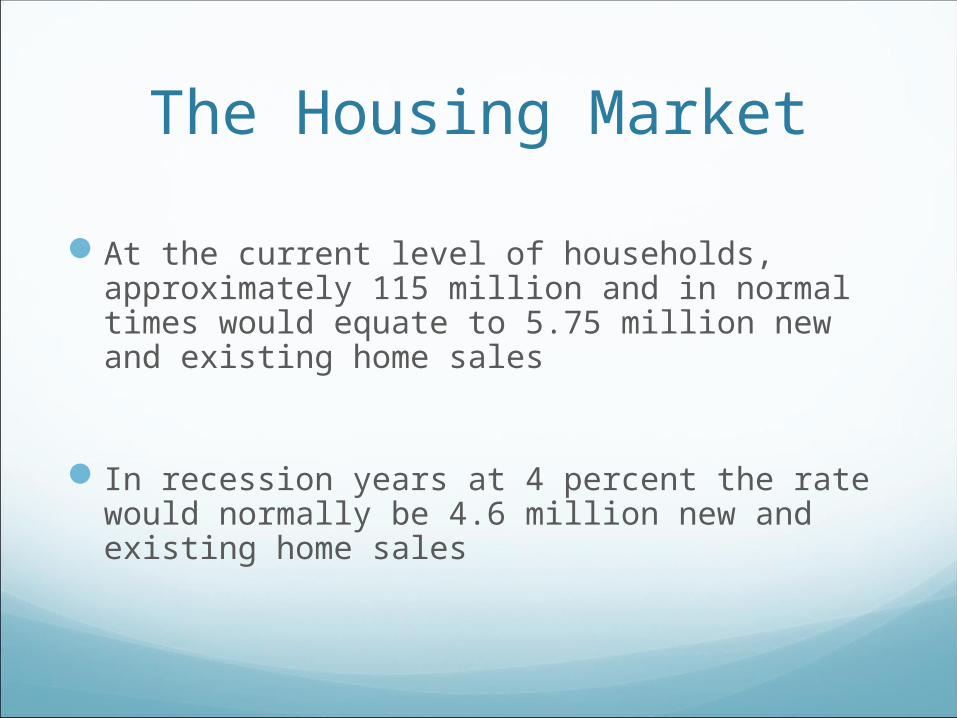

At the current level of households, approximately 115 million and in normal times would equate to 5.75 million new and existing home sales

In recession years at 4 percent the rate would normally be 4.6 million new and existing home sales

The Housing Market

The market is currently running just under the 5 percent rate. Near record low interest rates, extraordinary pricing and the strength of the investor market are keeping the rate higher than would be expected

The Housing Market

These are the forecasts for 2011

Existing New Total

NAR 5.123M .350M 5.473M

Fannie 5.011M .350M 5.361M

RT 4.990M .350M 5.340M

The Housing Market

Projections therefore expect lower unemployment, continuation of affordable mortgage rates and continued growth in the economy.

Not full recovery but measurable

The Housing MarketWild cards

Rising mortgage rates/tightening of credit

Either flood of/or tightening of foreclosure inventory

Economy slides or doesn't recover

Tax hikes to cover state/city deficits

Immigration due to unemployment shrinks further

The Housing Market

Joint Center for Housing Studies at Harvard indicates that 1.1 to 1.3 million new households per year through 2020

Additional stimulus from Gen X and Millennial households who are now living home

The Housing Market

Investors will continue to be >20 percent of all sales for several years

Second home/retirement home sales are .300M per year first half of decade sliding in second half of decade

Changes with Consumers

The Millenials are marrying later, marrying not at all and are delaying entry into housing purchase market

Of the new households that will be created in the next decade fully 71 percent will be minority households

Changes with Consumers

Between 1/5th and 1/4th of all owner occupied households currently have either negative or no equity in their homes

The Boomers and the Millenials are both seeking similar housing – low maintenance smaller more urban quarters

Changes with Consumers

So two groups representing over 70 percent of all potential homebuyers are moving away from suburban housing and crowding into condominiums, townhomes, lofts and apartments

And Generation X, the smallest of the generations, is left to purchase the suburban two story homes

Changes with Consumers

The homeownership rate was 66.5 percent in the fourth quarter of 2010

The homeownership rate peaked at 69.2 percent in 2004

The last time the rate was at 66.5 was 1999

Changes with Consumers

Singles make up an increasing share of all homebuyers. Homeownership rates for single women are higher than for single men (focused on their big screens not homes!)

The Brokerage Challenge

The rate of home sales will likely resume its 30 year average of 5 percent

From the current level and with 1.2 million new households created each year, then home sales will grow roughly at 50-55,000 additional home sales each year

The Brokerage Challenge

That represents roughly 1 percent growth in home sales each year for the next decade

Prices are expected to resume long term trends of 3-4 percent per year with higher levels in certain markets

The Brokerage Challenge

The average commission rate declined from 1991 to 2005 to 5.02 percent then reversed upwards through 2009 to 5.36 percent

We expect it to remain there for a year or two then begin to soften as sales professionals go back to competing for listings

The Brokerage Challenge

The gross margin for brokerage firms has declined for the past twenty years.

The rate in 1990 was 36 percent and in 2009 it was 26.8 percent nationally (lower in western region)

The Brokerage ChallengeCompetition from 1)RE/MAX, 2) Keller Williams

and 3) Virtual and Freedom Brokerage firms has driven competition for sales professionals to new heights

There are no apparent reasons for this to continue (In Canada where such trends are 5-10 years ahead of U.S. gross margins are 17-18 percent)

The Brokerage Challenge

The competition has moved to:

Lead Generation and Capture

Technology platforms

Recruiting systems

Educational programs and training

The Brokerage Challenge

The significant growth in core services (mortgage, title and other settlement) has reached maturity for most firms.

Capture rates do have room to grow but for most firms it is limited

The Brokerage Opportunity

An estimated 60-65 million homes will be bought and sold in the next ten years

The total commission revenue from such sales will between $450 billion and $550 billion

The Brokerage Opportunity

The market is segmenting by type of brokerage

Traditional graduated commission

100 % commission

Capped Company Dollar

Virtual/Freedom Brokerage

The Brokerage Opportunity

There are profitable brokerage firms in each different model

Generally the higher the retained gross margin the more success in core services

The Brokerage Opportunity

Research indicates the following:

20 percent of the agents do 60 percent of the business when comparing only those doing business at all

The Brokerage Opportunity

General keys to success

Pick a model

Execute ruthlessly

Bet that technology and content will be of equal value in the future, not just the technology

Related Documents