Logistics of empty marine containers March, 2007 S.J. Mol Master Thesis: TIL 5060 Transport, Infrastructure and Logistics, TU Delft

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Logistics of empty marine containers

March, 2007

S.J. Mol

Master Thesis: TIL 5060

Transport, Infrastructure and Logistics, TU Delft

Logistics of empty marine containers

A research on strategies for port planning, concerning the storage and flow of empty marine containers in

the port of Rotterdam

Final report

March, 2007

By: S.J. Mol

Stud.nr.: 9576648

E-mail: [email protected]

Master Thesis: TIL 5060

Transport, Infrastructure and Logistics, TU Delft

Graduation Committee:

Daily supervisors:

Chairman:

External supervisor:

Company:

J. C. van Ham M A (TPM faculty)

J. C. Rijsenbrij M Sc (3ME faculty)

G. P. van Wee M A PhD (TPM faculty)

C. Klaver M Sc (representative: A. Clijncke M Sc)

Witteveen+Bos, Rotterdam

'U Delft

Witteveen

Preface

The port of Rotterdam is one of the vital parts of the Dutch economy. Progressively more goods are transported in

marine containers. This large seaport supports the import, export and transhipment of containers (loaded and empty).

The transport, handling and storage of especially empty containers are the topic of this research.

Maasvlakte 2, a 1000 ha port expansion to be built in the North Sea starting in 2008, is being developed. The Rotterdam

Port Authority has the complicated task to determine a feasible strategy, regarding the spatial planning of empty depots,

towards 2040, when Maasvlakte 2 will be fully operational. Therefore, the characteristics of the logistics of empty marine

containers, their storage and their flow between the Maasvlakte 2, Port of Rotterdam and its hinterland, are of great

importance. The logistics of empty containers is an uncultivated topic. For that reason, getting insight in the effects of

possible strategies, proved to be a major challenge. In this report, I would like to share with you the knowledge of

empty containers logistics, as well as the process towards this understanding, which proved to be very complex. Since

this process sometimes was a struggle, I am very grateful to everybody, who helped to structure and depicts the

complex system. An introduction on this issue is presented in the first chapter, the methods of research and the further

structure of this report are explained in the second chapter.

This research has been executed as the Master Thesis Project of the master Transport Infrastructure and Logistics (TIL

Master) at the faculty of Technology, Policy and Management (TPM), of Civil Engineering and Geosciences (CITG) and of

Mechanical, Maritime and Materials Engineering (3ME), all part of Technical University Delft. Witteveen+Bos consulting

engineers commissioned the project. Similar to the background of the study program, the supervision was

multidisciplinary. The two daily supervisors Hans van Ham and Joan Rijsenbrij, both have their own expertise in the field

of port policies and economics respective container handling and logistic businesses. Their useful suggestions proved of

equal importance for this research and I thank them for their constructive discussions and comments. Also I would like

to thank Witteveen+Bos for their hospitality and for the guidance of course, by A. Clijncke and C. Klaver. In addition

many other experts have contributed to this research. Amongst them where Tom Dekker (Rotterdam Port Authority,

Business Developer depots and hinterland). Joop Mijland (APL, Director Network and Operations Europe) and Bert van

Wee (TUDelft, director TIL). And last but not least, I would like to thank my brother Joost and my friend Diana for their

support.

Rotterdam, January 2007

Fieke Mol

Executive summary

The aim of this research is to give insight in the effects of port planning strategies of the Rotterdam Port Authority

(RPA), regarding storage facilities for empty containers (empty depots) at the Port of Rotterdam (PoR).

Empty depots generate transport of empty containers (often by truck), and increasingly require port terrain. Given the

expected growth of trade volumes, the environmental regulations and the quality of the accessibiliy of the PoR requires

a planning strategy for empty depots.

In the allocation of storage areas for empty containers the RPA needs to decide upon the location, the quantity, the

dimensions of the required area, the related infrastructure (which impacts the accessibility of the port) and the lease

price of empty depot terrain.

There are conflicting interests of the RPA and the shipping companies regarding the aimed land use of the PoR for depot

terrain. A multi-actor approach is used to incorporate the different viewpoints. Storage facilities for empty containers are

of strategic importance to their direct clients; lease companies and shipping companies, the latter being the main user.

Transport operators are the indirect users of empty depots. The location and infrastructural connection of empty depots

affect their routing and fleet management.

The potential economic saving involved in the efficiency of empty container logistics by a larger use of inland storage (in

stead of storage at the port) is investigated. The need for storage facilities of empty containers in the port area is

derived from an analysis of the logistics of empty containers on different levels of scope. This is done by means of

literature study, interviews and application of the list extension method. This causal method indentifies the most

important influences on the demand for port depot terrain.

The imbalance in world trade causes a surplus of containers in North West Europe. Due to higher storage costs in the

Far East not all "match back" containers, are directly repositioned to the Far East. Another reason for storage in Europe

is the strong secondary container market. This gears the demand for empty depots in Europe and especially in the PoR,

since this is major transport node.

The organisational structure of the supply chain Is of great influence on the use of port depots. Shipping companies,

using merchant haulage, prefer to have the containers returned to the port for financial and organisational reasons.

Efficiency of hinterland transportation Is also important for transport operators, who try to maximize the occupation rate

of their vehicle fleet. Empty depots near ports enable more combinations trips.

The key determinants for quantification of future depot utilisation are ICT developments, type of haulage, empty deep-

sea transhipment and scale enlargements. An increase in ICT applications will reduce the demand for storage. A shift

towards merchant haulage would increases the need for storage in the port area. The empty throughput in the PoR is

growing slower than the throughput of full containers. Economies of scale positively influence the chance of matching a

container with cargo. The future number of depot arrivals are estimated on 2.1 to 2.4 million TEU in 2020 and on 2.7 to

3.2 million TEU in 2040. A higher price for depot services is an incentive for improvement of empty logistics, which

allows the dimensions of depots in the port area to be less than the demand resulting from an extrapolation of the

present situation.

This research offers a complete framework of the determinants of empty depots. Different strategy concepts regarding

empty depots are assessed on their performance in 2020 and 2040 regarding the criteria of the main parties involved, by

means of a multi criteria analysis.

It is recommended to allocate a substantial amount of empty depots behind the terminal as this supports a modal shift

and is logistically efficient. A limited part of the storage can be crowded out to inland terminals. Nevertheless, it is not

lucrative for the RPA to locate all empty depots behind the terminals at Maasvlakte 2 (MV2). The RPA should also

facilitate empty depots with a barge connection (to support modal shift) in the Waal-/Eemhaven area.

Logistics of empty containers

The RPA should use an adaptive, flexible policy to adjust the supply of depot terrain, as it complies with the need.

Regarding the planning process, it is favourable to plan depot terrain ahead. The RPA should reserve future depot

terrains at MV2 to avoid planning difficulties in later stages. During the starting phase of MV2 the RPA should find

temporary destinations for terrain that cannot be leased to depot operators yet. By restricting the duration of lease

contracts with depot operators (about five years) flexibility will be achieved in later phases.

Furthermore, it is advantageous to increase the depot prices, since this will stimulate the crowding out effect. Regarding

the prices of competing ports there is enough room for price increase.

Under conditions that the current average dwell time and the terrain productivity remain unchanged in the future, the

required space for empty depots varies from 100 to 113 ha in 2020 and 127 to 149 ha in 2040, for the entire PoR.

Currently there are 85 ha of depot terrain. If the current area remains available, there is a demand for an additional 15

to 28 ha empty depot terrain in 2020 and 42 to 64 ha for 2040 for the PoR.

Summary

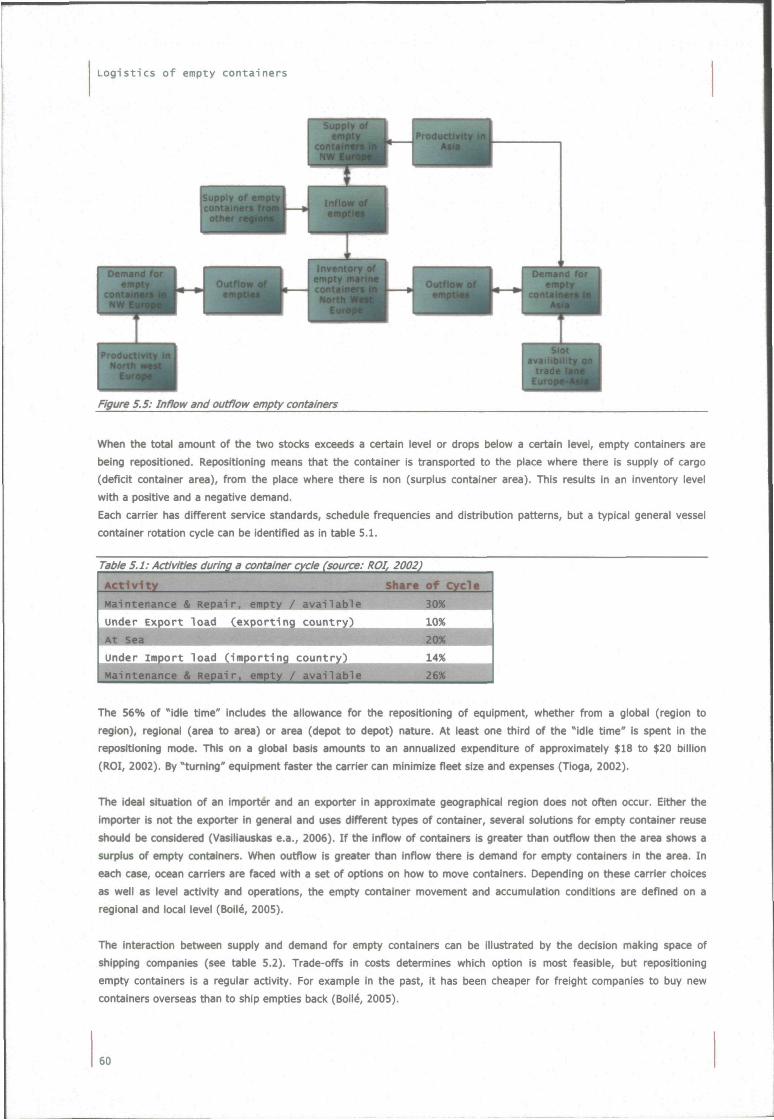

Introduction Due to mismatches in time and place, temporary storage of empty marine containers is inevitable. Imbalances and

fluctuations in trade cause an accumulation of empty containers at (amongst others) port areas. The inequity in cargo

flows has great impact on the Port of Rotterdam (PoR), as major European port. The flow of empty containers to and

from the PoR will increase, supported by the development of Maasvlakte 2 (MV2), a 1000 ha port expansion to be built

in the North Sea starting in 2008.

The aim of this research is to give insight in the effects of port planning strategies of the Rotterdam Port Authority

(RPA), regarding storage facilities for empty containers (empty depots) at the Port of Rotterdam (PoR).

In formulating the port planning strategy towards the spatial planning of empty depots, four points of interests can be

distinguished:

• Conflicting interests between RPA and shipping lines as container owners;

• Efficiency of empty container logistics;

• Environmental constraints

• Accessibility of the PoR;

Conflicting interests

The RPA prefers to use the available space in the port for commercial activities other than storing empty containers,

because this is more lucrative. Nevertheless, many empty containers are stored in empty depots located at the PoR.

Shipping companies as container owners prefer to have available empty containers in a buffer in port depots in order

to supply these when required to exporting companies.

Efficiency of empty container iogistics

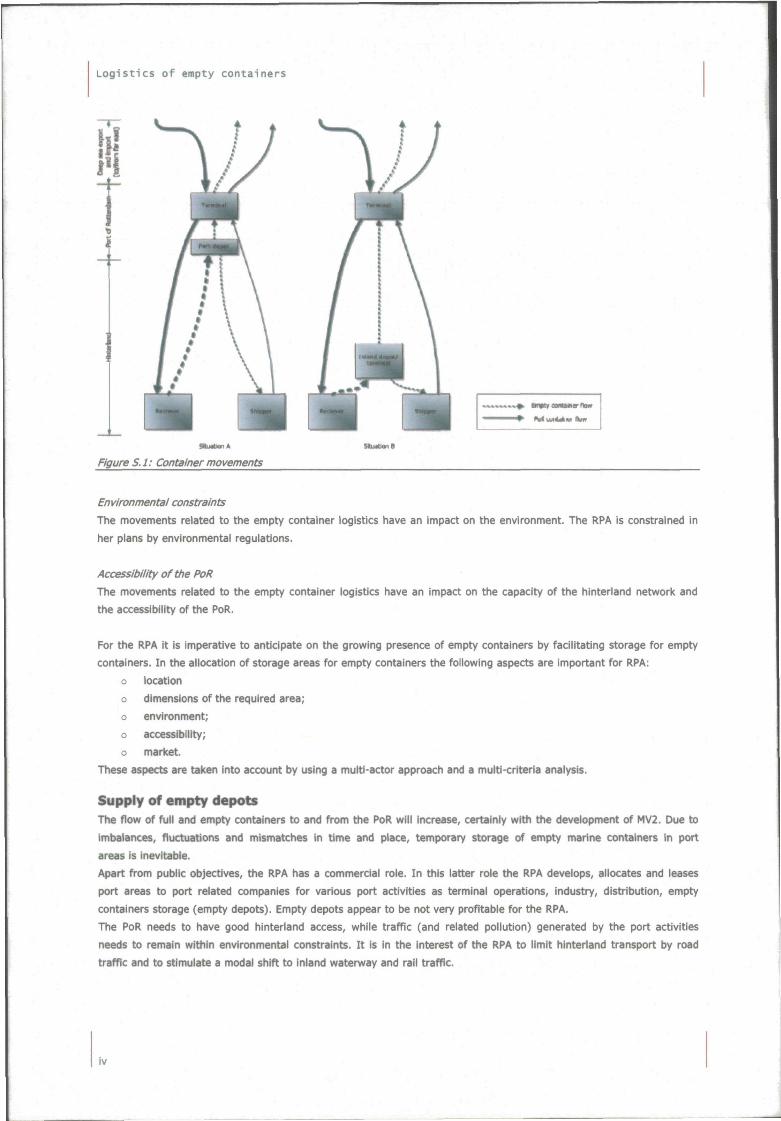

Economic savings can be reached with efficient empty container logistics. There seems to be an inefficiency regarding

the movements of empty containers. In case an inland depot is used for the storage of empty containers near the

market of receivers/shippers in the hinterland (see figure S.l, situation B), the travelling distance can be reduced.

Logistics of empty containers

T

Figure S.l: Container movements

Environmental constraints

The movements related to the empty container logistics have an impact on the environment. The RPA is constrained in

her plans by environmental regulations.

Accessibility of the PoR

The movements related to the empty container logistics have an impact on the capacity of the hinterland network and

the accessibility of the PoR.

For the RPA it is imperative to anticipate on the growing presence of empty containers by facilitating storage for empty

containers. In the allocation of storage areas for empty containers the following aspects are important for RPA:

o location

o dimensions of the required area; o environment;

o accessibility;

o market.

These aspects are taken into account by using a multi-actor approach and a multi-criteria analysis.

Supply of empty depots The flow of full and empty containers to and from the PoR will increase, certainly with the development of MV2. Due to

imbalances, fluctuations and mismatches in time and place, temporary storage of empty marine containers in port

areas is inevitable.

Apart from public objectives, the RPA has a commercial role. In this latter role the RPA develops, allocates and leases

port areas to port related companies for various port activities as terminal operations, industry, distribution, empty

containers storage (empty depots). Empty depots appear to be not very profitable for the RPA.

The PoR needs to have good hinterland access, while traffic (and related pollution) generated by the port activities

needs to remain within environmental constraints. It is in the interest of the RPA to limit hinterland transport by road

traffic and to stimulate a modal shift to inland waterway and rail traffic.

tv

Summary

The concepts are assessed on their performance in 2020 and 2040 regarding the criteria of the main parties involved,

by means of a multi criteria analysis. In first instance, the four concepts are assessed by the values of the RPA. Next,

the concepts are assessed to the criteria of the shipping companies.

The current policy can be corrected in order to create a better balance between supply and demand. Although it seems

advantageous to eliminate empty depots from the Waal-/Eemhaven area, it may have a negative effect on the trip

combinations. A depot behind the terminal is valuable, but can be kept minimal. Furthermore, there is a need for a

certain amount of depot terrain in the remaining part of the port, which is also in the interest of the RPA to supply.

It is feasible to allocate a substantial amount of empty depots behind the terminal and to offer storage at the Waal-

/Eemhaven. A limited part of the storage can be crowded out to inland terminals.

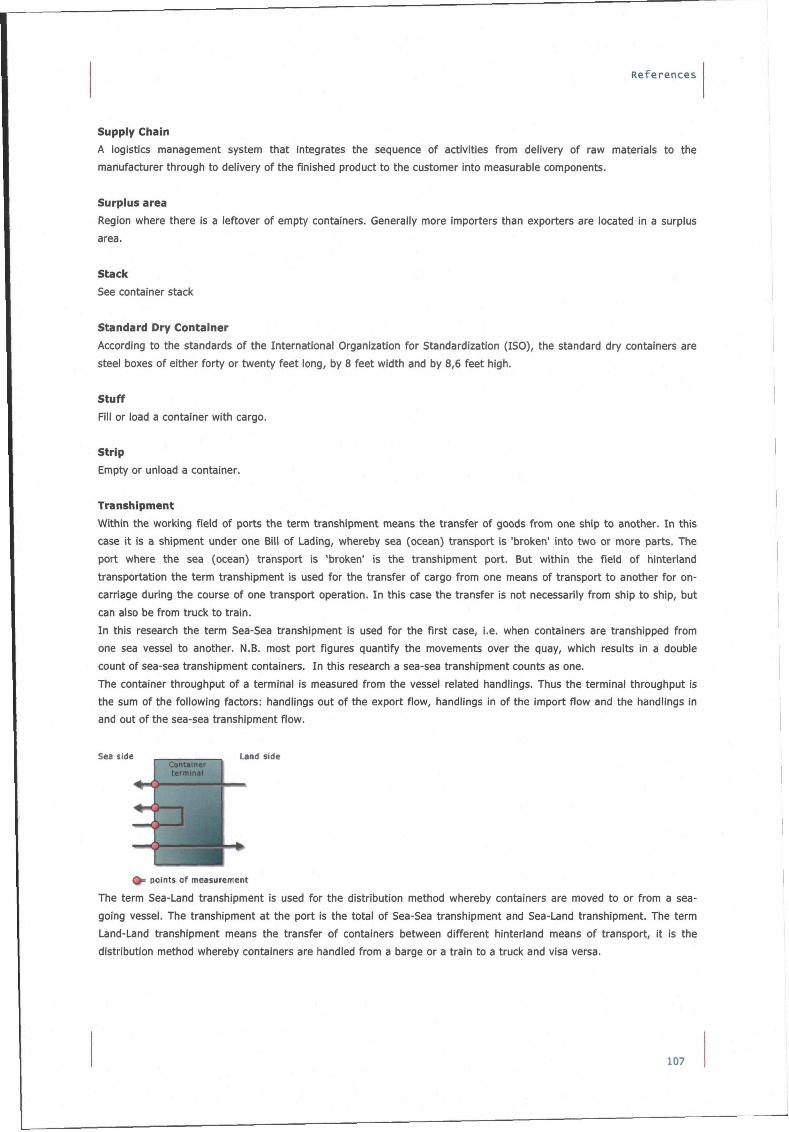

Conclusions The research results in the recommendation to facilitate empty depots with a barge connection In the Waal-/Eemhaven

area, to plan depot terrain ahead and to increase lease prices for depot areas. There is opportunity for improvement of

empty logistics, which allows the dimensions of depots in the port area to be less than the demand resulting from an

extrapolation of the present situation.

A modal shift in empty container transport can be achieved by locating empty depots behind terminals or by assigning

depots to land with a water connection. A connection of a depot with the terminal is logistically efficient. Nevertheless,

it is not lucrative for the RPA to locate all empty depots behind the terminals at MV2.

The analysis of the different allocations of depot terrains, confirmed that it is advantageous to allocate terrain in a

masterplan in order to prevent planning difficulties in later stages. This strategy results in lots, that are suitable for

empty container storage, due to their accessibility by different modalities and to logistical efficient location. Until the

empty depot volumes reach the maximal level of occupancy, there will be terrain that the RPA cannot lease to depot

operators yet, because the market for depot operators is insufficient at that moment. Therefore, it is lucrative and

recommendable for the RPA to find temporary destinations for terrain that will be used for empty depot in a later

stage.

It is advantageous to increase the depot prices, since this will stimulate the crowding out effect. Regarding the prices

of competing ports there is enough room for price increase.

Under conditions that the current average dwell time and the terrain productivity remain unchanged in the future, the

required space for empty depots varies from 100 to 113 ha in 2020 and 127 to 149 ha in 2040, for the entire PoR.

Currently there are 85 ha of depot terrain. If it is assumed that the current area remains available, the demand is for

an additional 15 to 28 ha empty depot terrain in 2020 and 42 to 64 ha for 2040 for the PoR.

The gradual growth of the future container flow, complicate the planning task of the RPA. Empty containers are in the

starting phase of a new terminal stored at the terminal. This retreats the moment at which a critical mass is reached

for depots behind future container terminals. Depot operators need a certain amount of depot arrivals to profitable

exploit a depot in highly competitive environment. Therefore, leasing terrain behind a new terminal to depot operators

in the starting phase is not achievable.

The RPA should use an adaptive, flexible policy to adjust the supply of depot terrain, as it complies with the need.

By restricting the duration of lease contracts with depot operators (about five years) flexibility will be achieved.

An interesting issue in this research is the identification of possibilities to relatively decrease the area for empty depots

at the PoR. It is likely that the storage of empty containers shifts towards inland depots. The tight supply of terrain

however may result in the following effects.

A reduction in supply may lead to less service to port users. The throughput of the port will decrease, as shipping

companies take refuge in other ports for their storage of empty containers.

Tight supply might be an incentive to further increase matchability, to a shift from merchant towards carrier haulage,

or to less dwell time by avoiding maintenance and repair in the port depots. Due to the complicated logistic market. It

is difficult to predict the future developments.

vii

Logistics of empty containers

To protect the competitive strength of the port, in case of tight supply, mitigating measures are needed to keep the

same level of service to the clients. Potential mitigating measures can compensate for the decrease in supply of depot

terrain. This new approach requires a commercially innovative attitude of the PoR towards empty container services.

The possibilities for mitigating measures were investigated, but both the RPA and the shipping companies are of the

opinion that those extra container services should originate independently as result of market dynamics.

Discussion The demand and supply of empty depots should be balanced in the future. Because of the dynamic environment,

monitoring is important.

Developments around the mega depot Maersk is planning to create should be followed. Maersk creates large

transhipment volumes in the PoR and is consequently responsible for a large part of the need for empty container

storage. When Maersk (in stead of depot operators) takes care of depot services at its terminal, there is less need for

depots elsewhere in the PoR.

The following aspects of the depot moves are of importance to refine the estimates of the future demand:

Type of container (distinction in reefer or standard and TEU or FEU)

Type of modality

Direction (towards MV or hinterland)

Dwell time

Price level of depot services

It is recommended that the RPA monitors the above-mentioned aspects, since an objective and multimodal approach Is

required.

VIII

Table of contents

PREFACE i

SUMMARY i i i

L I S T OF FIGURES 5

L I S T OF TABLES 7

1 | I N T R O D U C T I O N ON EMPTY CONTAINER LOGISTICS 9

1.11 IMBALANCES I N TRADE LANES 10

1.21 CONTAINER TRANSPORT AND STORAGE 12

1.3| ALLOCATION OF DEPOTS IN THE PORT 13

1.4| PORT DEPOT REQUIREMENTS 13

2 | RESEARCH FRAMEWORK 15

2.11 LITERATURE 15

2.2| SCOPE 16

2.3| RESEARCH QUESTIONS 17

2.4| RESEARCH METHODS 18

2.51 BOOKMARK 19

3 | PORT PLANNING AND EMPTY DEPOTS. . . . 2 1

3.11 PORT DEVELOPMENT 22

3.21 COMPETITIVE STRENGTH 23

3.31 ENVIRONMENTAL IMPACT AND ACCESSIBILITY 25

3.41 PLANNING POLICY 27

3.51 DESIGN SPACE 28

3.61 ALLOCATING EMPTY DEPOTS 30

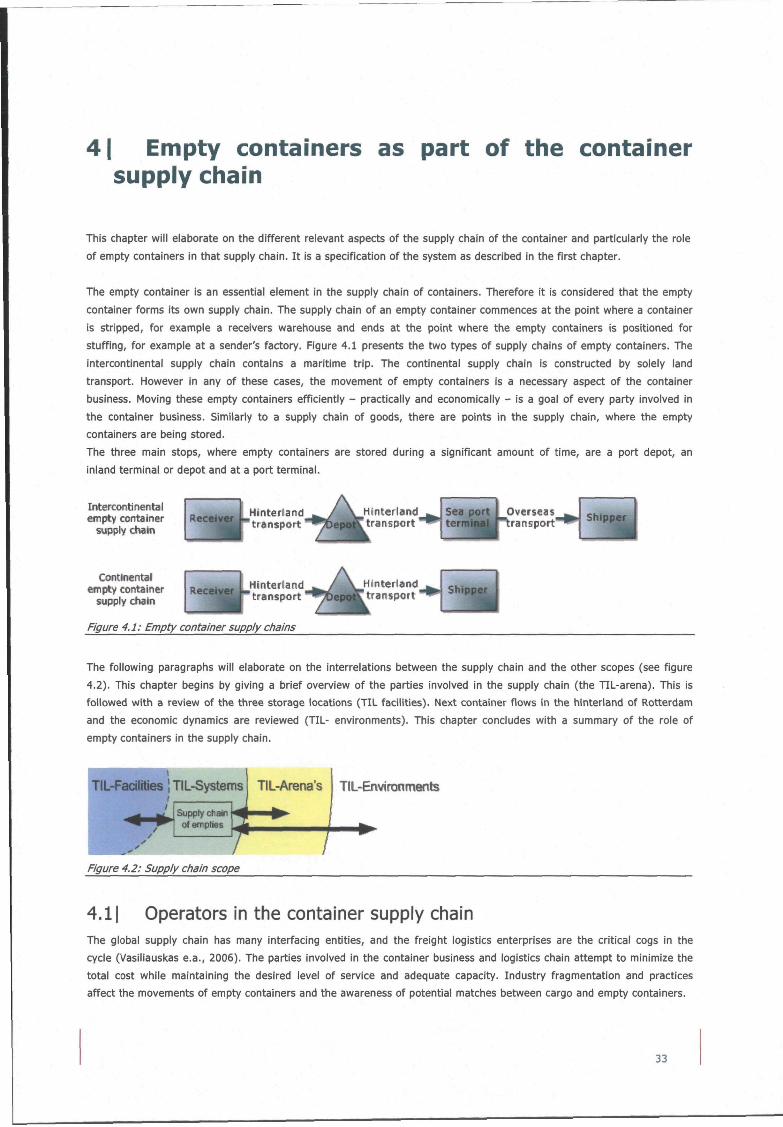

4 | EMPTY CONTAINERS AS PART OF THE CONTAINER SUPPLY C H A I N 33

4.11 OPERATORS I N THE CONTAINER SUPPLY CHAIN 33

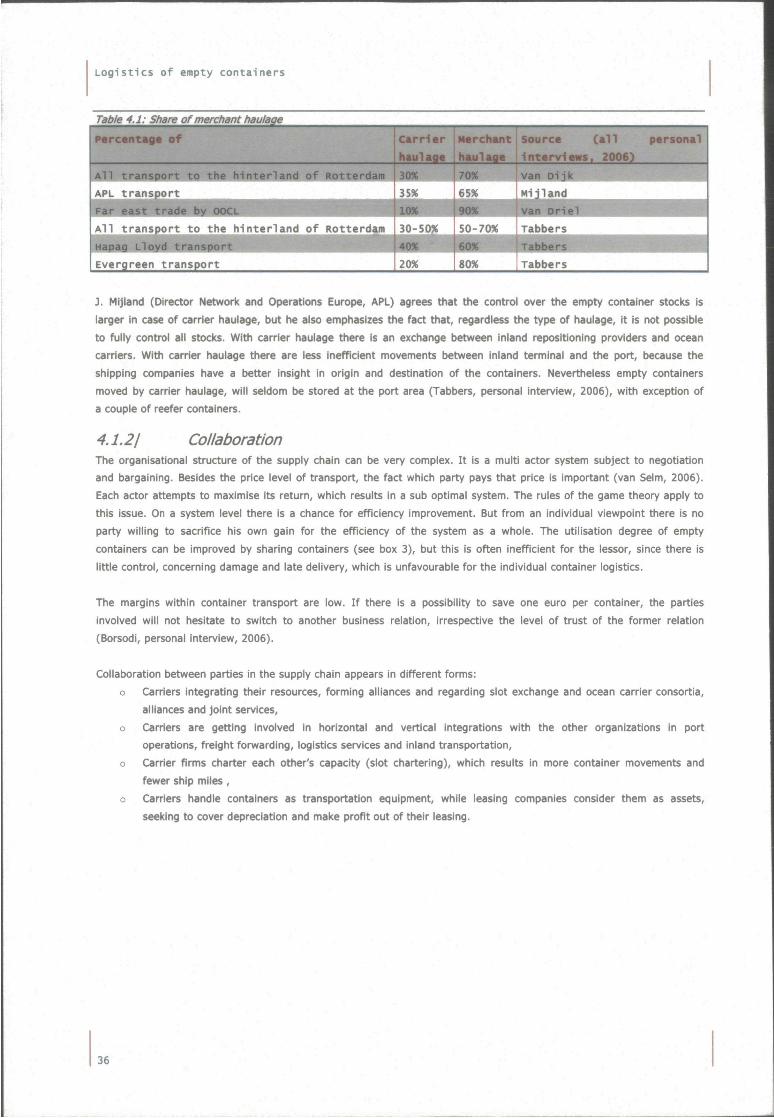

4.1.11 Merchant versus Carrier Haulage 35

4.1.21 Collaboration 36

4.21 EMPTY CONTAINERS AT SEA PORT CONTAINER TERMINAL 39

4.2.11 Storage at the terminal 40

4.2.21 Connection terminal with depot 40

4.31 EMPTY CONTAINERS AT PORT DEPOTS 41

4.3.11 Port depot function 42

4.3.21 Depot business 44

4.3.31 Lease depots 44

4.41 EMPTY CONTAINERS AT INLAND TERMINALS 46

4.4.11 Inland terminal function 46

4.4.21 Substitute for port depots 46

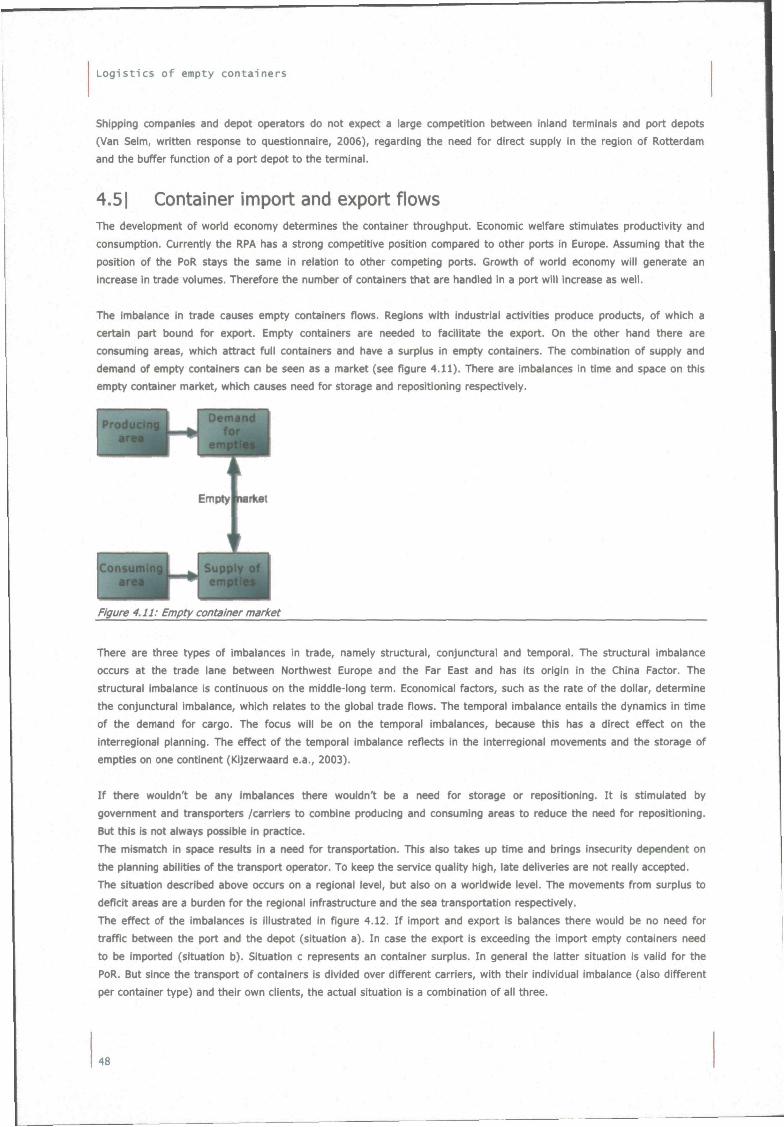

4.51 CONTAINER IMPORT AND EXPORT FLOWS 48

4.5.11 Commodity and origin and destination of empties 49

Logistics of empty containers

4.5.21 Size of empty container flow 51

4.61 ROLE OF EMPTY PORT DEPOTS IN THE SUPPLY CHAIN 52

S| EMPTY CONTAINER MANAGEMENT 55

5.11 STOCK MANAGEMENT 55

5.21 FORECASTING OF EMPTY CONTAINER DEMAND 58

5.31 REPOSITIONING 59

5.3.11 International repositioning 62

5.3.21 Port of Rotterdam as empty container hub 63

5.3.3! Repositioning strategies 63

5.4| TRANSPORT OPERATIONS 63

5.4.11 Matchability 64

5.4.21 Hinterland routing 64

5.51 CONTAINER MANAGEMENT AND EMPTY DEPOTS 66

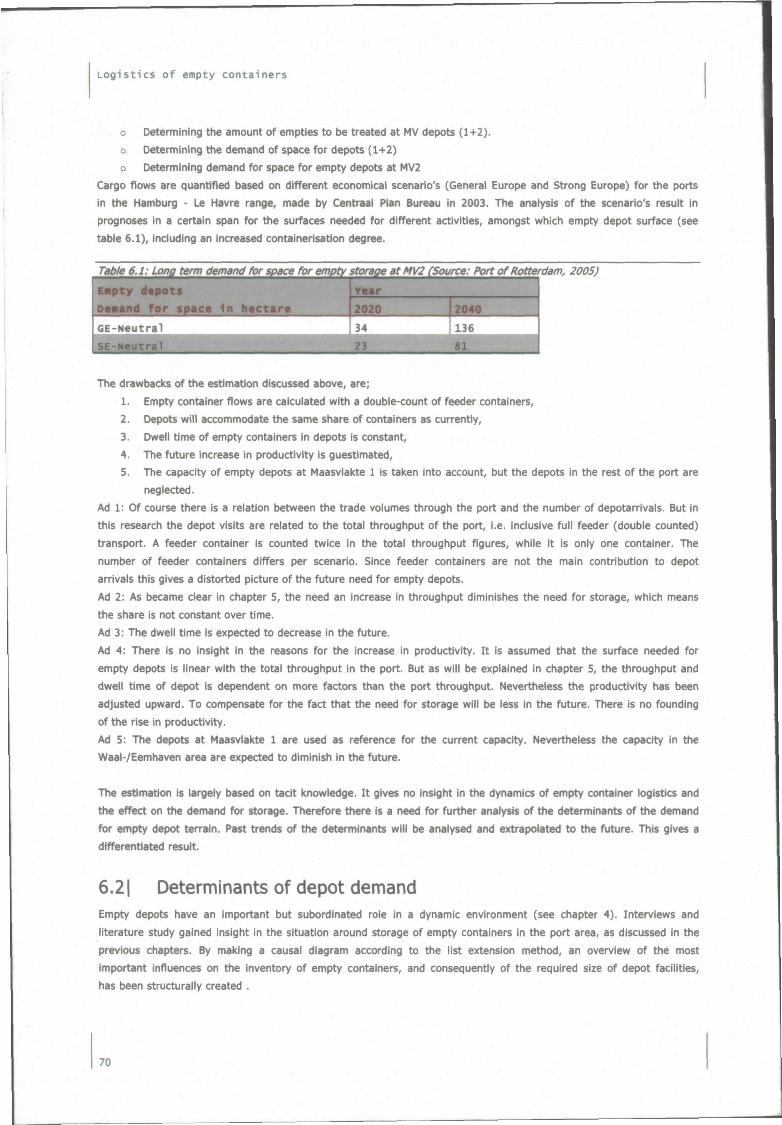

61 EMPTY DEPOTS: THE BALANCE BETWEEN PORT PLANNING AND CONTAINER MANAGEMENT 69

6.1| PRELIMINARY LAND USE ESTIMATES 69

6.2| DETERMINANTS OF DEPOT DEMAND 70

6.3| FUTURE CONDITIONS AND DEMAND 71

6.4| EFFECTS OF TIGHT SUPPLY 72

6.51 BALANCING 74

71 EVALUATION OP EMPTY DEPOT DESIGN CONCEPTS 77

7.11 CONSTRAINTS AND POINTS OF DEPARTURE 77

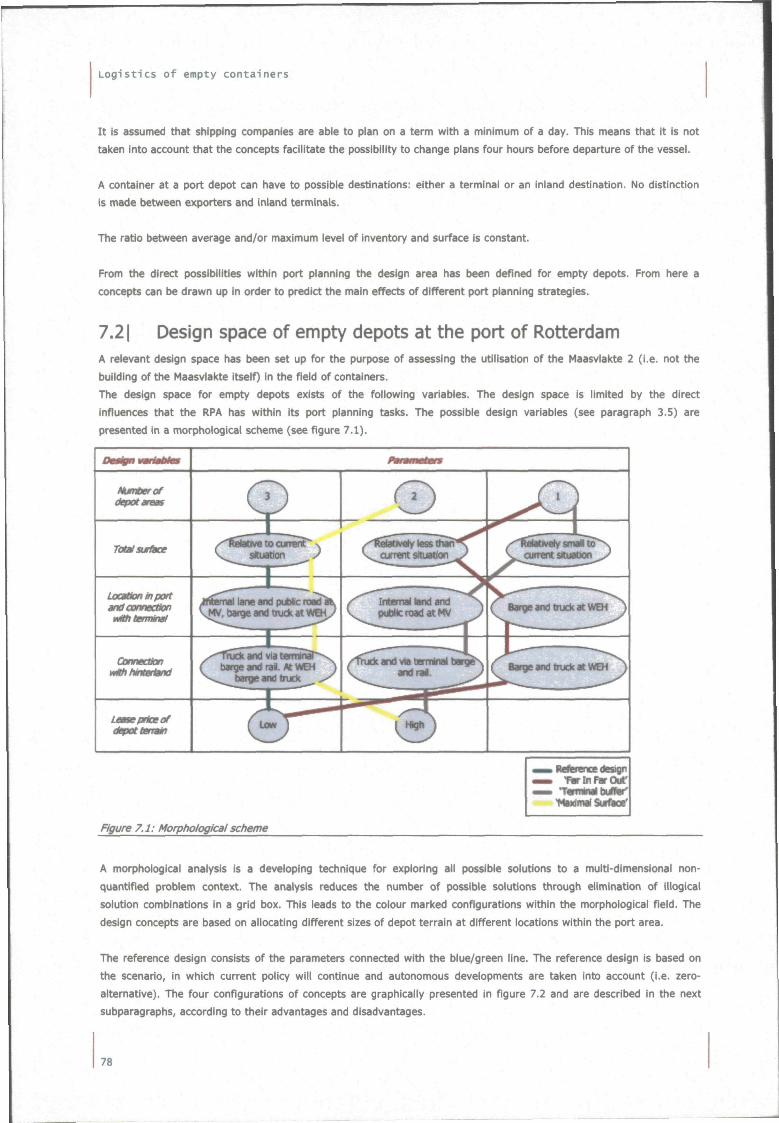

7.2| DESIGN SPACE OF EMPTY DEPOTS AT THE PORT OF ROTTERDAM 78

7.31 ASSESSMENT FRAMEWORK FOR EMPTY DEPOT DESIGNS 83

7.41 COMPARISON OF CONCEPTS 83

7.4.11 Availability 83

7.4.21 Transport performance 84

7.4.3! Trip combinations 85

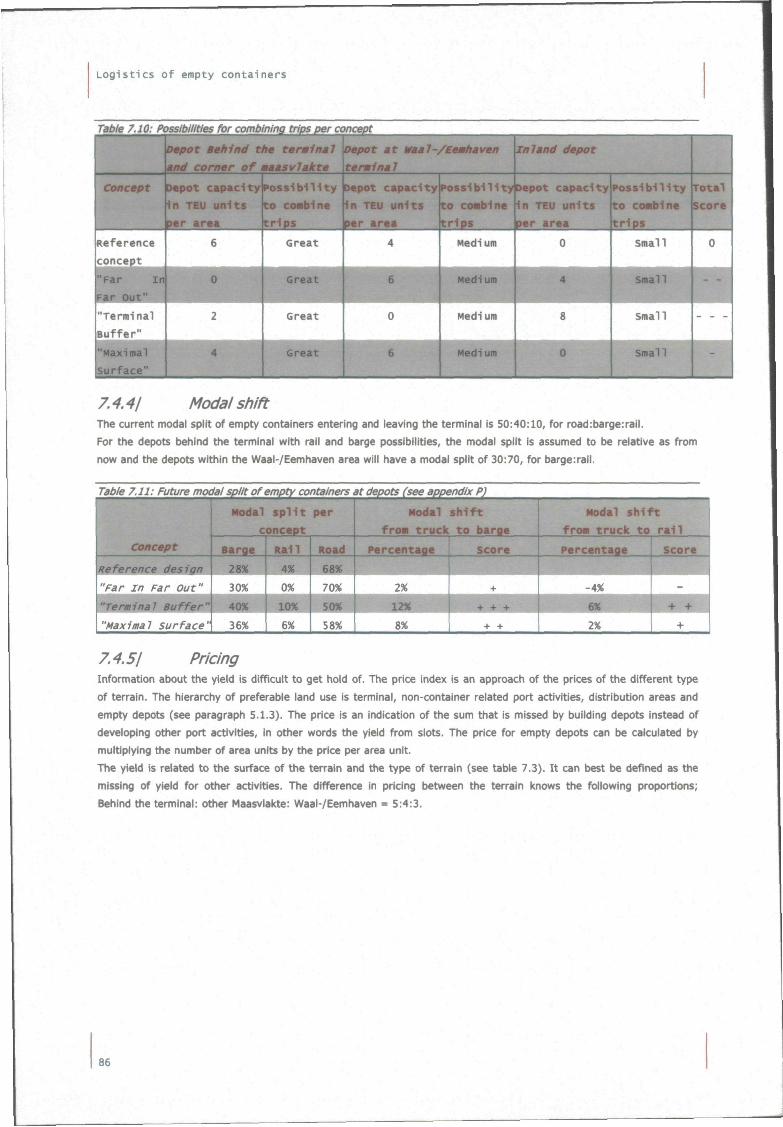

7.4.41 Modal shift 86

7.4.5! Pricing 86

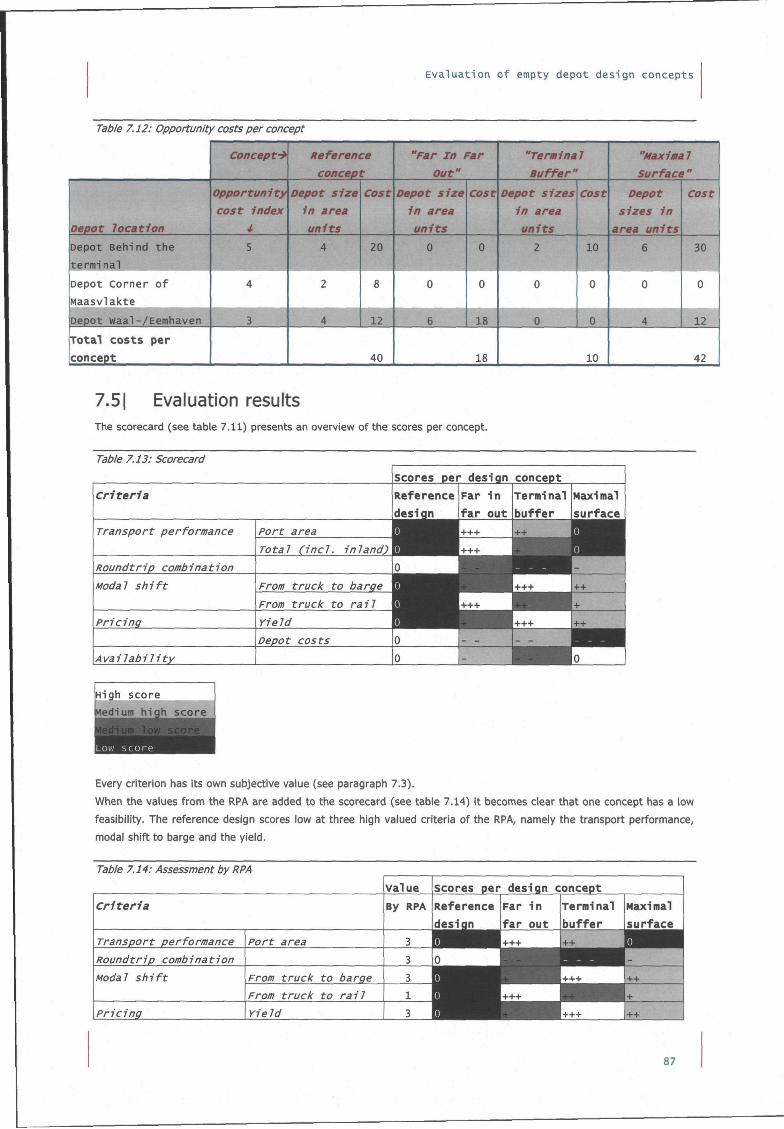

7.5! EVALUATION RESULTS 87

81 CONCLUSIONS AND RECOMMENDATIONS 89

EPILOGUE 93

REFERENCES 95

GLOSSARY 103

APPENDICES 109

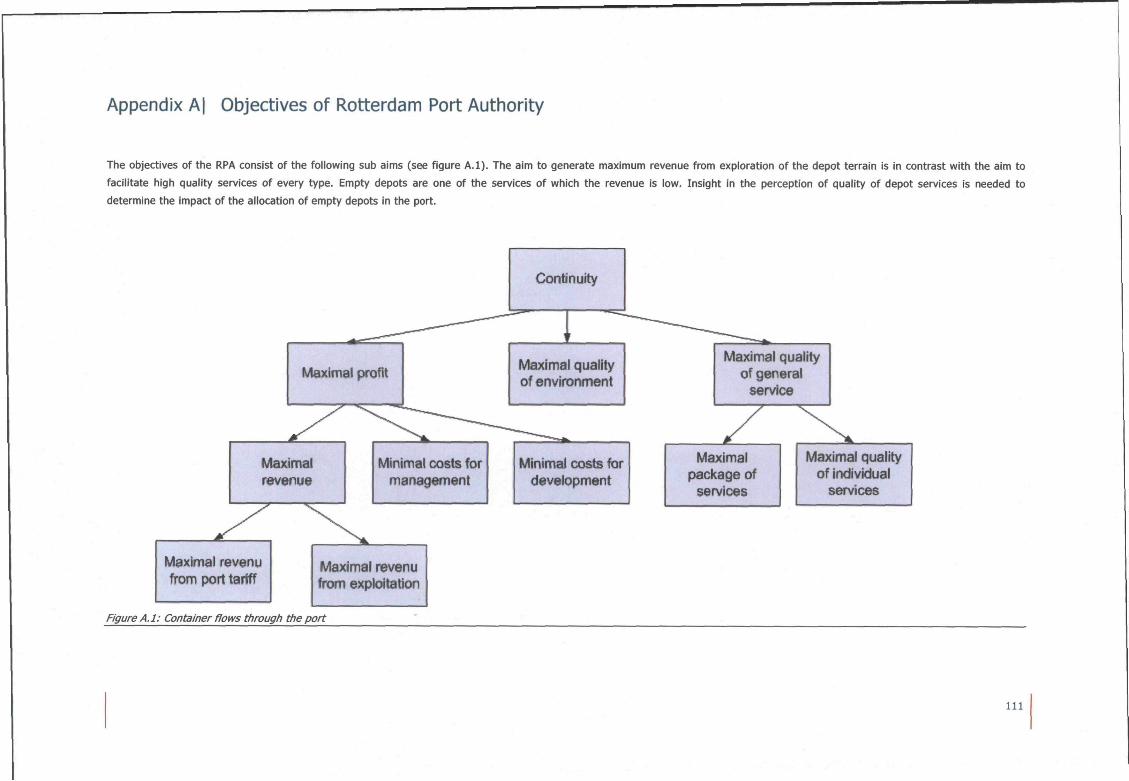

APPENDIX A | OBJECTIVES OF ROTTERDAM PORT AUTHORITY I l l

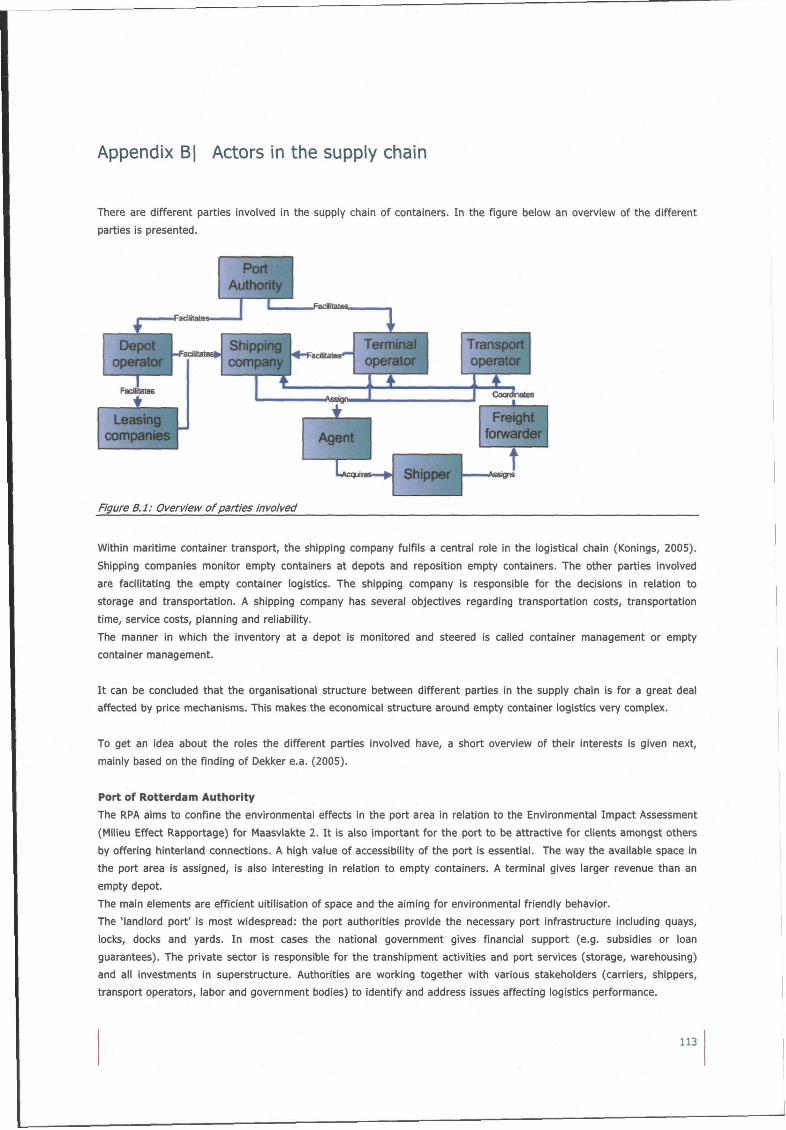

APPENDIX B! ACTORS IN THE SUPPLY CHAIN 113

APPENDIX C! COMBINATION OF TRIPS 115

APPENDIX D! FUTURE EMPTY DEEP SEA THROUGHPUT 119

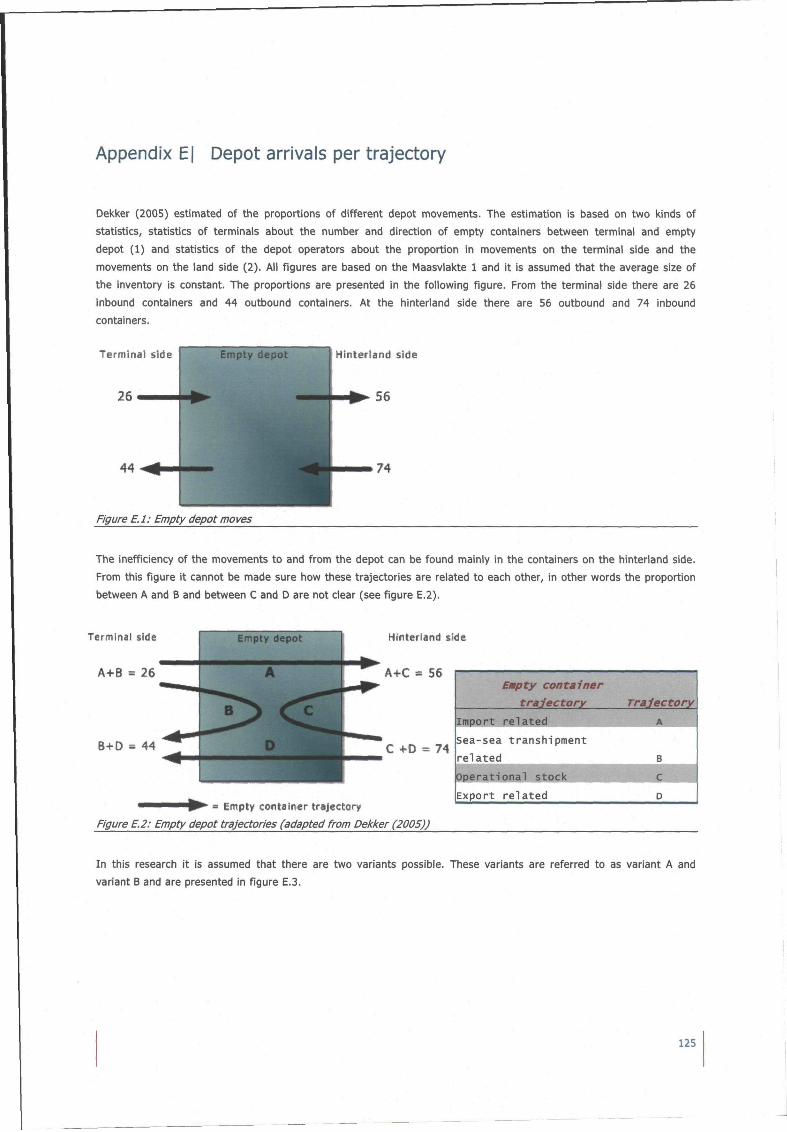

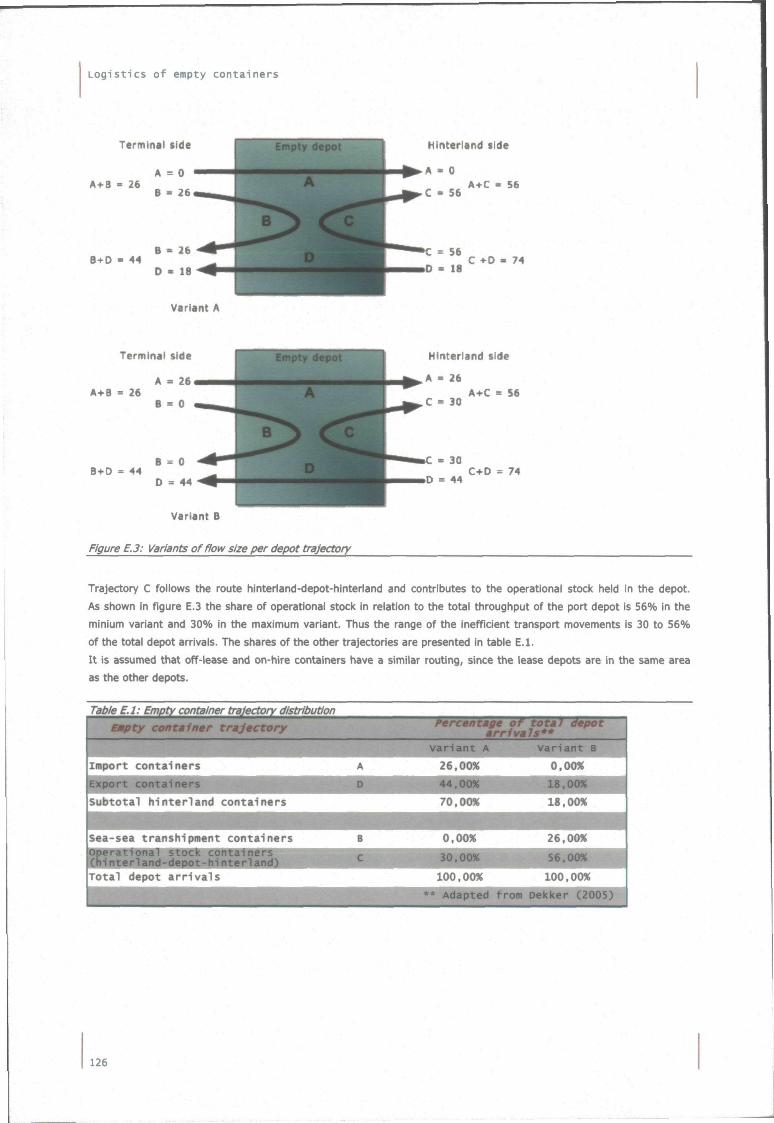

APPENDIX E| DEPOT ARRIVALS PER TRAJECTORY 125

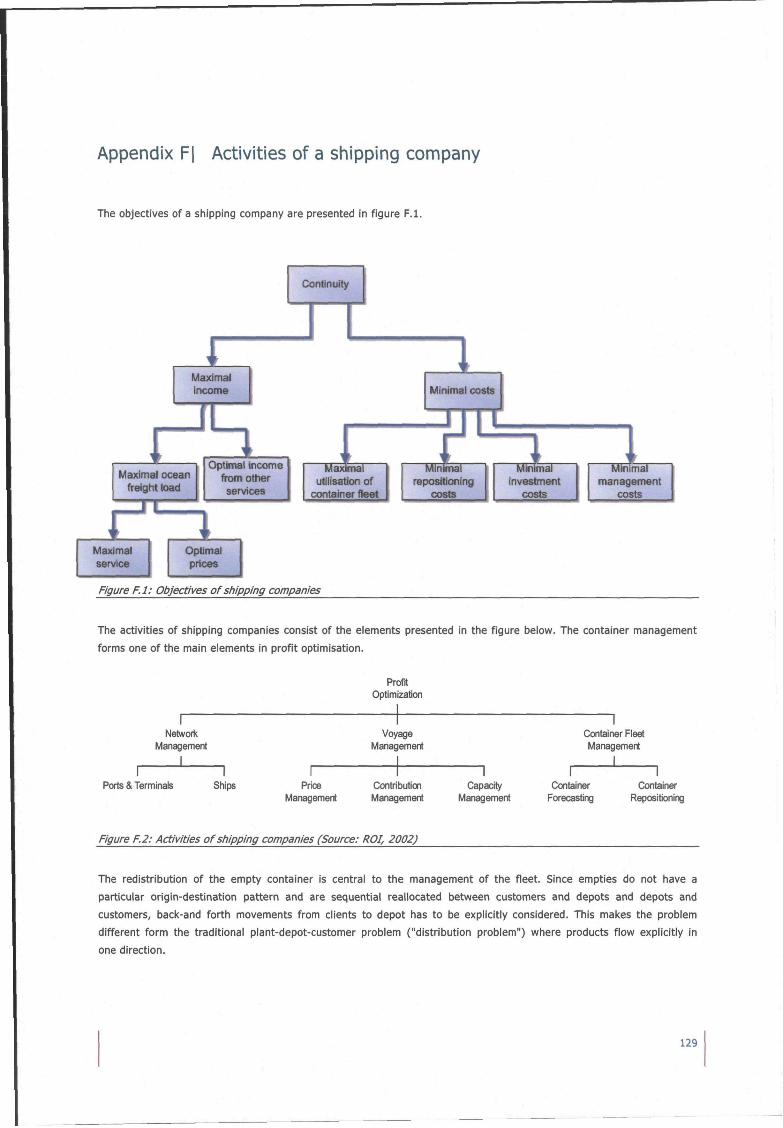

APPENDIX F| ACTIVITIES OF A SHIPPING COMPANY 129

APPENDIX G! POSITIONING ALGORITHM 131

2

Table pf contents

APPENDIX H | REPOSITIONING STRATEGIES 133

APPENDIX I! TRANSPORT AND LOGISTICS TERMINOLOGY 135

APPENDIX J! LIST EXTENSION 137

APPENDIX K| FUTURE EMPTY DEPOT ARRIVALS 145

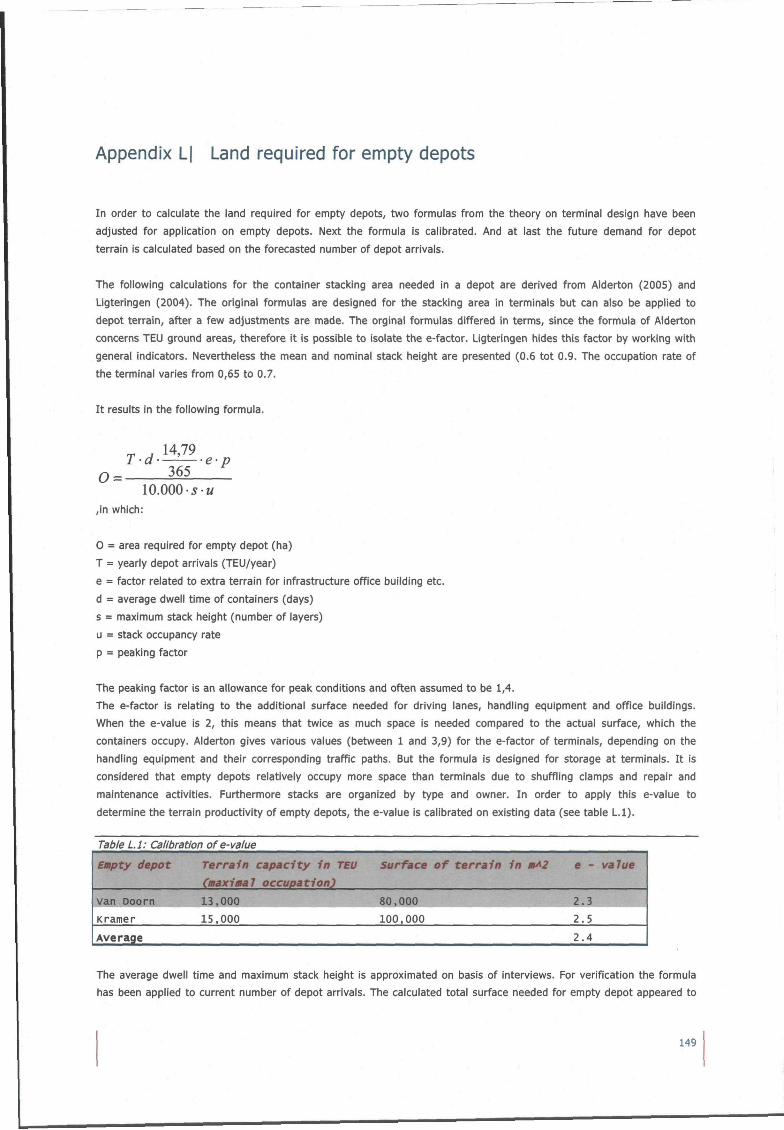

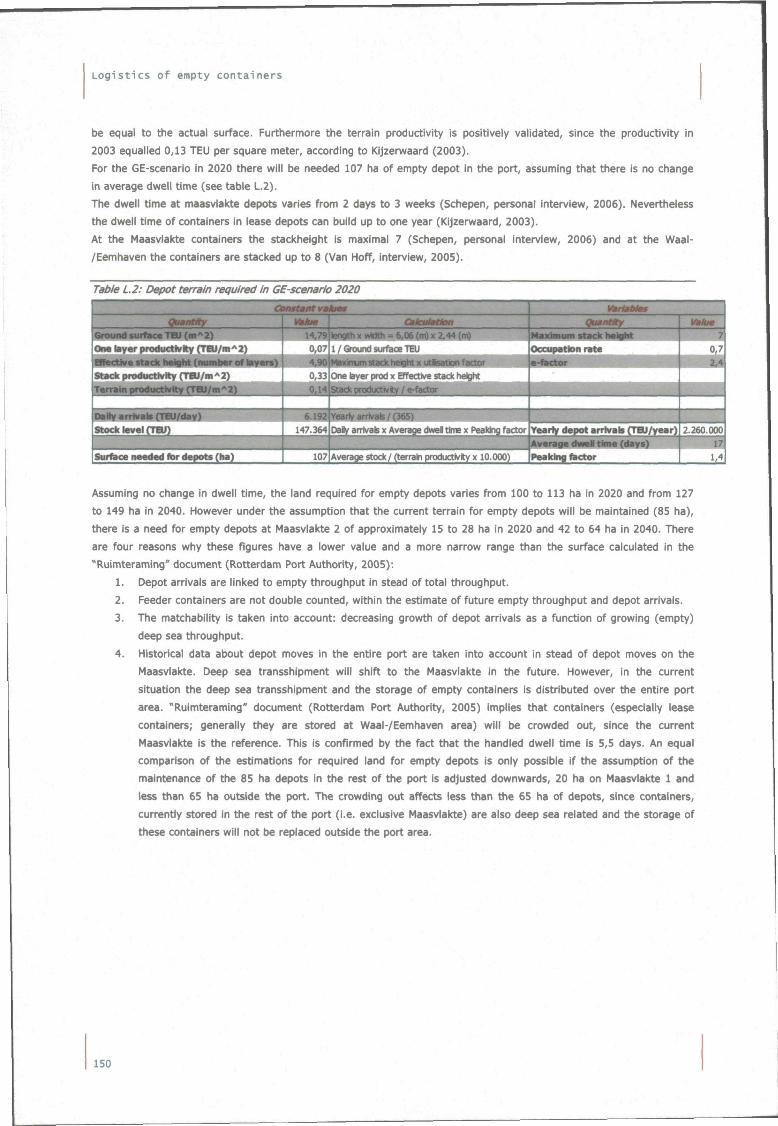

APPENDIX L| LAND REQUIRED FOR EMPTY DEPOTS 149

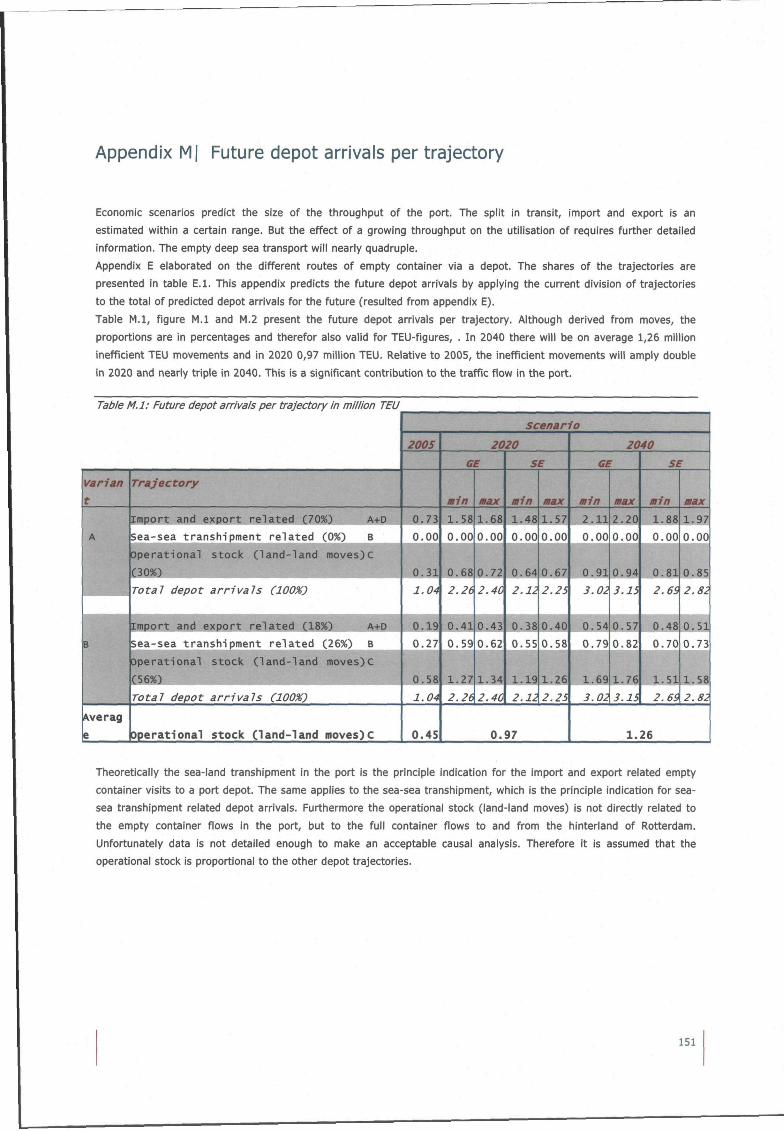

APPENDIX M! FUTURE DEPOT ARRIVALS PER TRAJECTORY 151

APPENDIX N| TRENDS 153

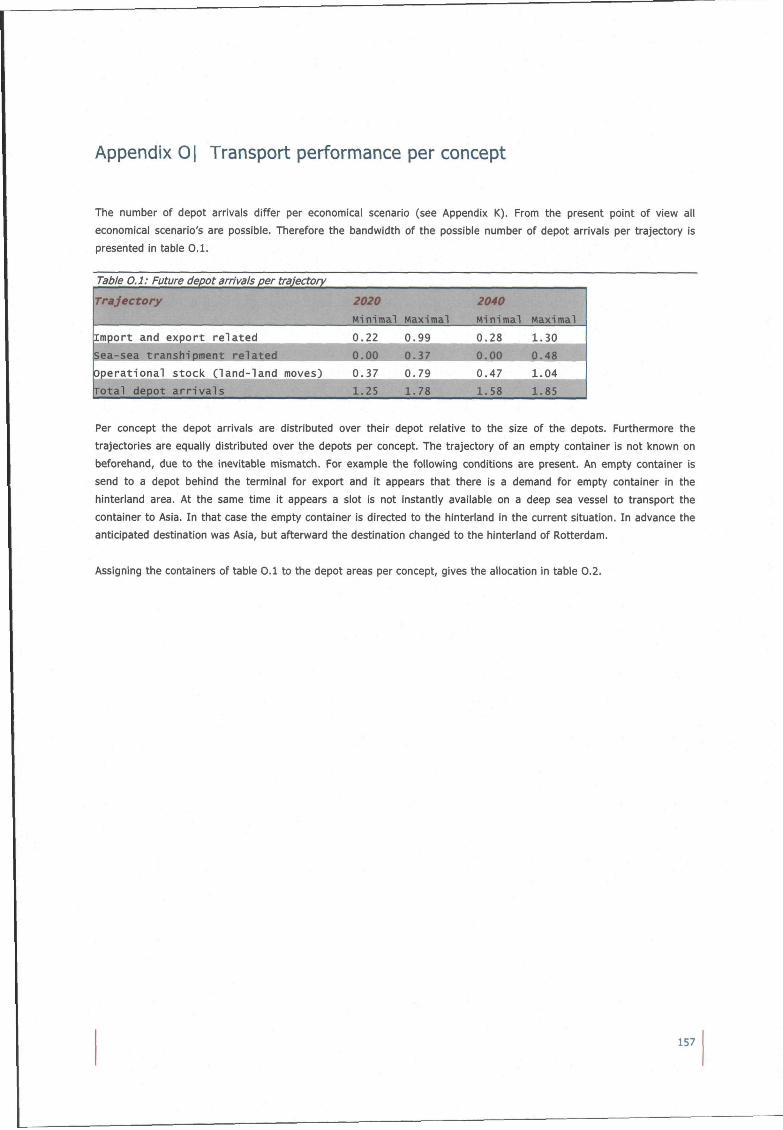

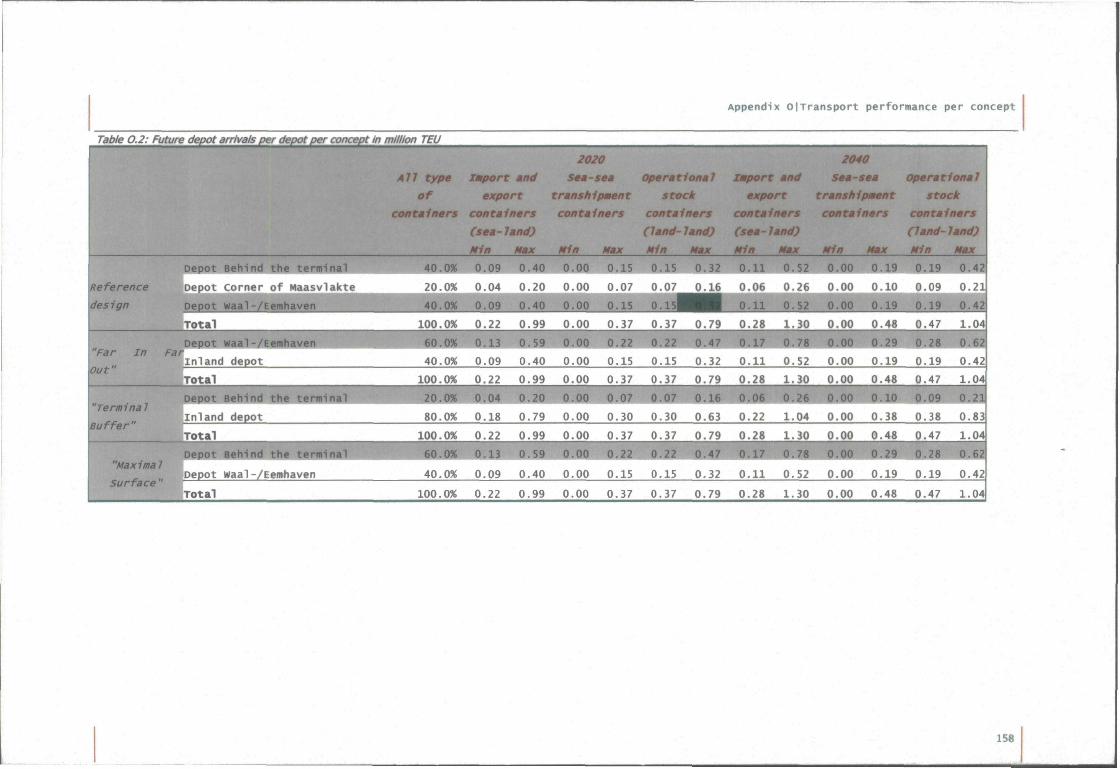

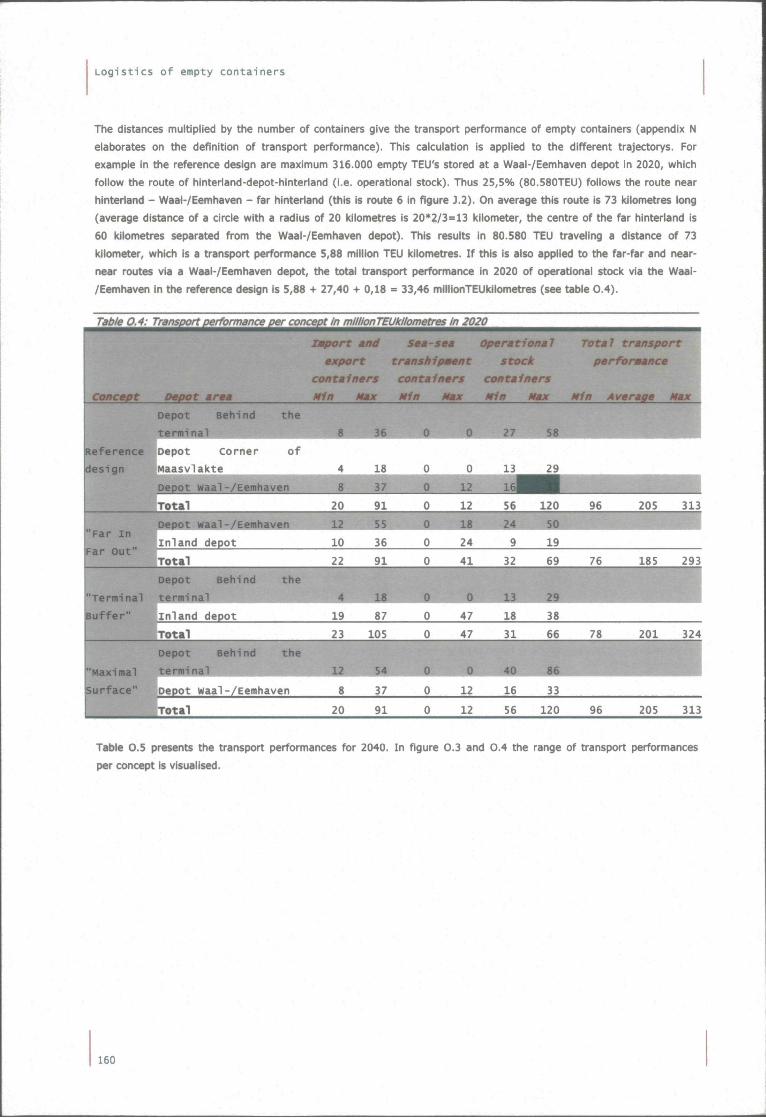

APPENDIX 0 | TRANSPORT PERFORMANCE PER CONCEPT 157

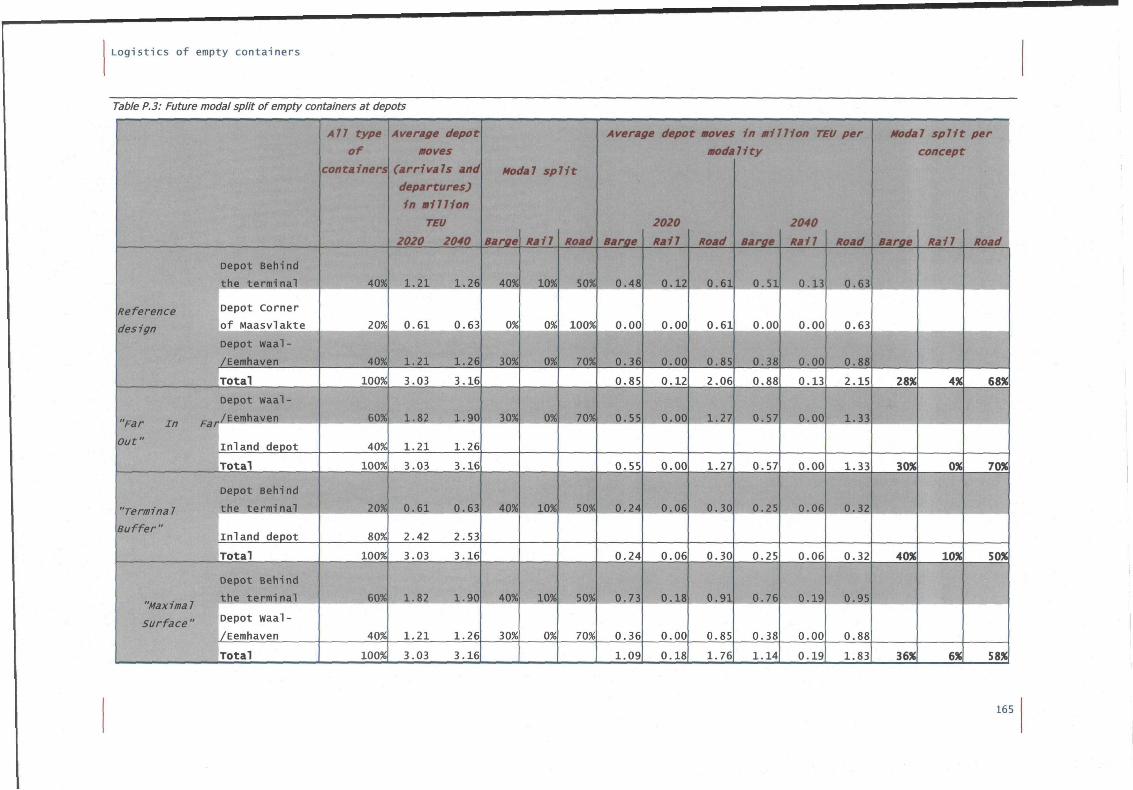

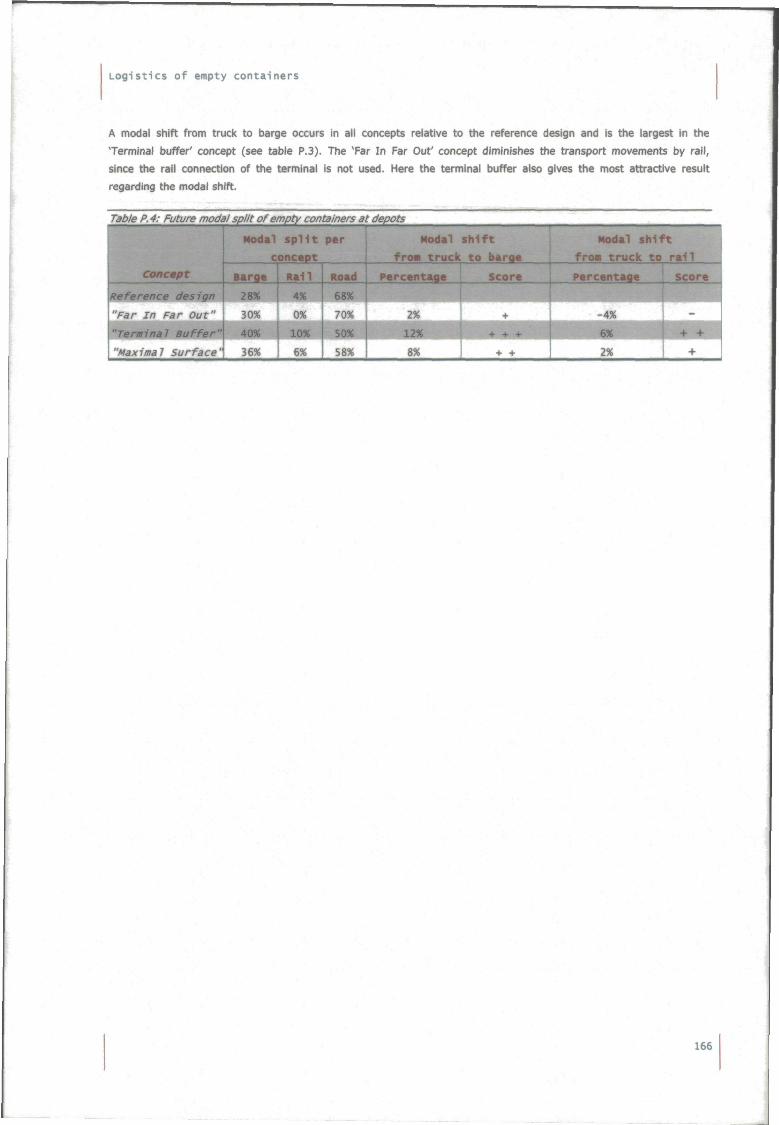

APPENDIX P! MODAL SPLIT PER CONCEPT 164

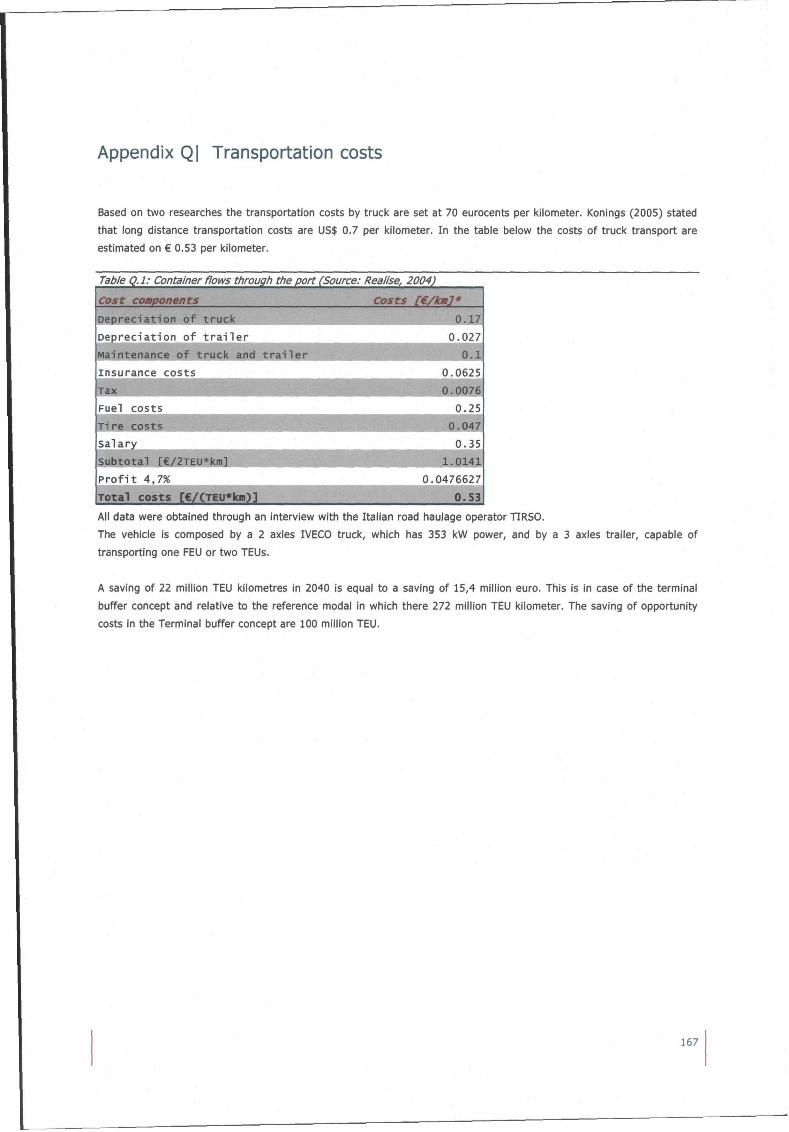

APPENDIX Q! TRANSPORTATION COSTS 167

3

Logistics of empty containers

List of figures

FIGURE S . l : CONTAINER MOVEMENTS iv

FIGURE l . l : SIGNIFICANT PORTS I N EUROPE (SOURCE: PORT OF ROTTERDAM, 2 0 0 6 A ) 10

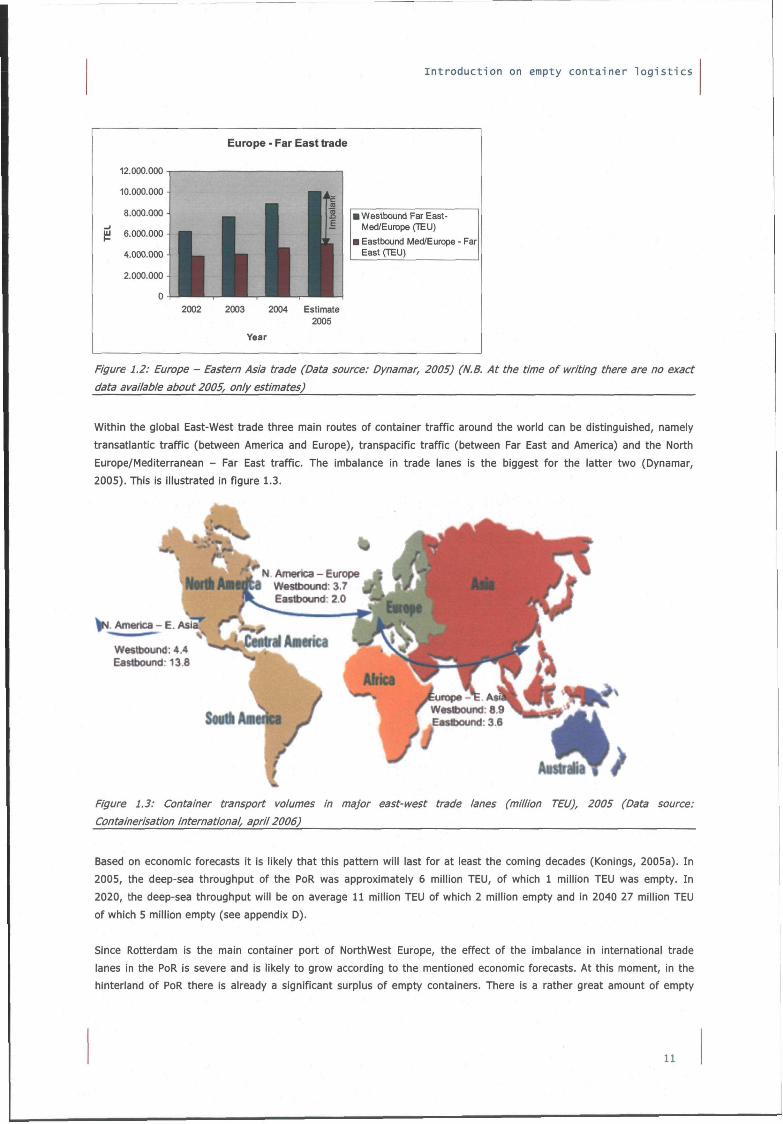

FIGURE 1.2: EUROPE - EASTERN A S I A TRADE (DATA SOURCE: DYNAMAR, 2005) (N.B. AT THE TIME OF WRITING THERE

ARE NO EXACT DATA AVAILABLE ABOUT 2005, ONLY ESTIMATES) 11

FIGURE 1.3: CONTAINER TRANSPORT VOLUMES I N MAJOR EAST-WEST TRADE LANES (MILLION TEU), 2005 (DATA

SOURCE: CONTAINERISATION INTERNATIONAL, APRIL 2006) 11

FIGURE 1,4: TRANSPORTATION CONCEPTS 12

FIGURE 1.5: WHERE DIFFERENT REQUIREMENTS MEET 14

FIGURE 2 . 1 : MSc-TIL SCOPES OF ATTENTION (ADAPTED FROM LUDEMA, 2005) 17

FIGURE 2.2: STRUCTURE OF RESEARCH 18

FIGURE 2 .3 : STRUCTURE OF CHAPTERS 19

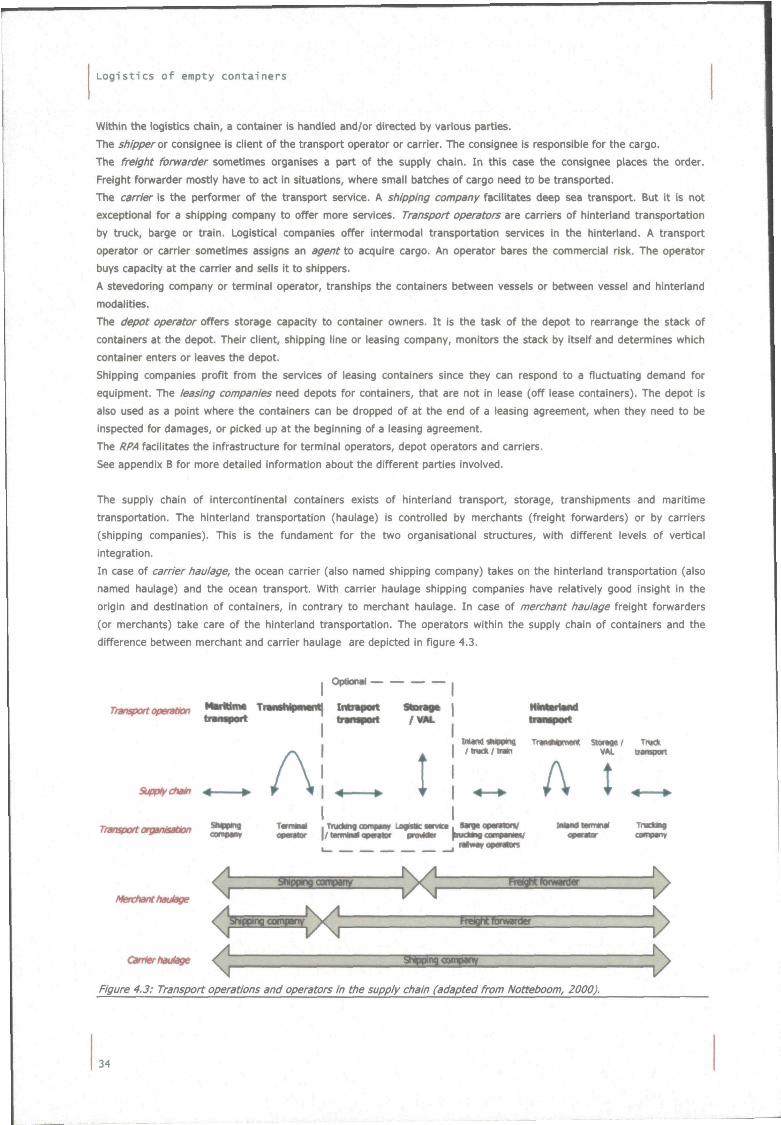

FIGURE 3 . 1 : PORT PLANNING SCOPE 21

FIGURE 4 . 1 : EMPTY CONTAINER SUPPLY CHAINS 33

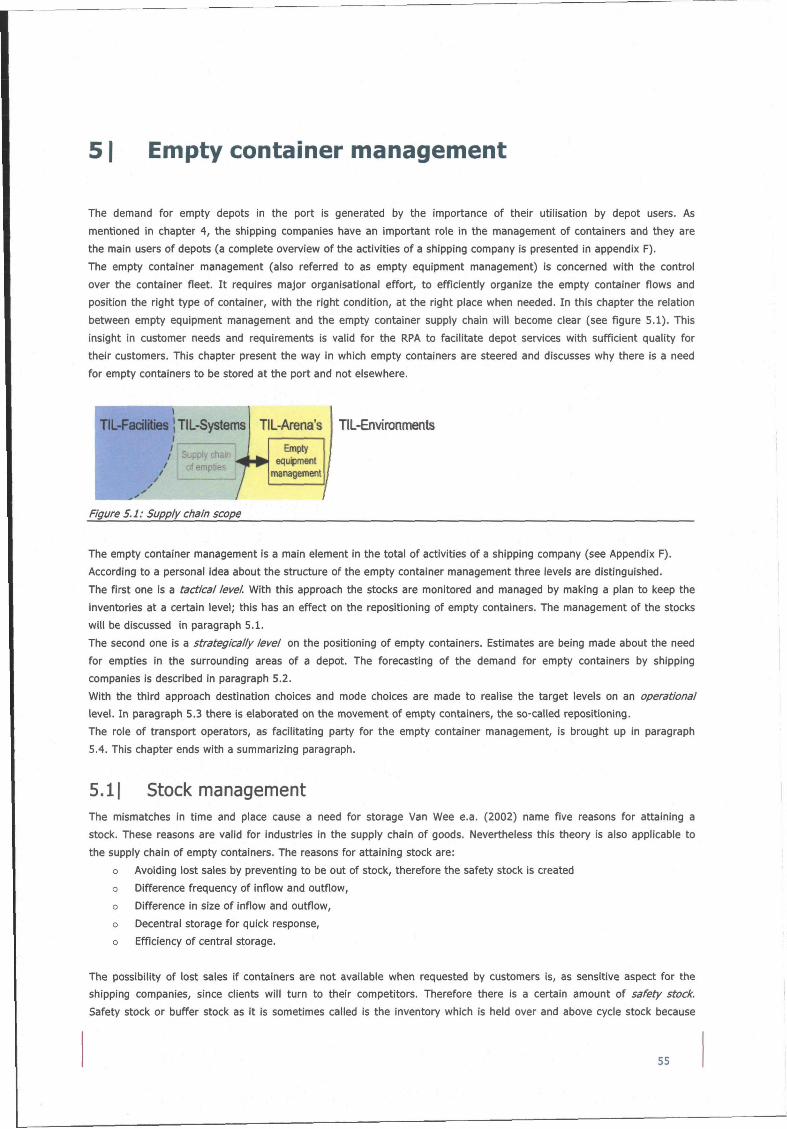

FIGURE 4 .2 : SUPPLY CHAIN SCOPE 33

FIGURE 4 .3 : TRANSPORT OPERATIONS AND OPERATORS I N THE SUPPLY CHAIN (ADAPTED FROM NOTTEBOOM, 2000) 34

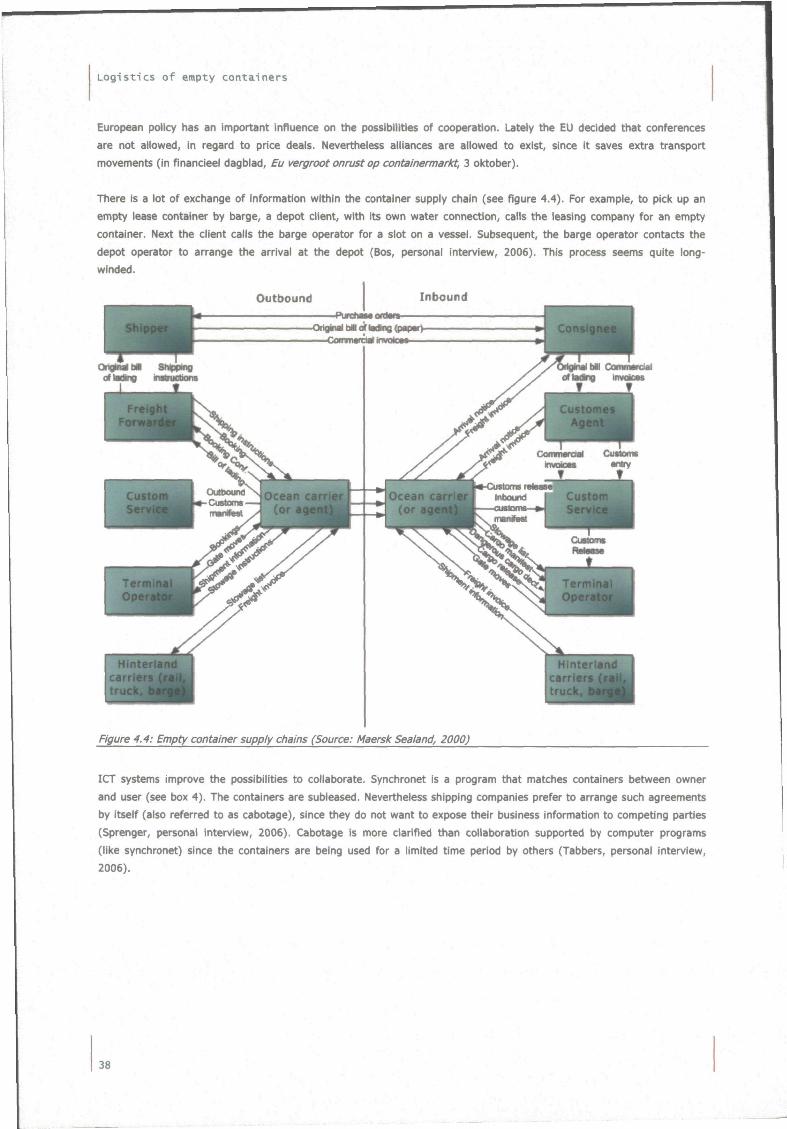

FIGURE 4 .4 : EMPTY CONTAINER SUPPLY CHAINS (SOURCE: MAERSK SEALAND, 2000) 38

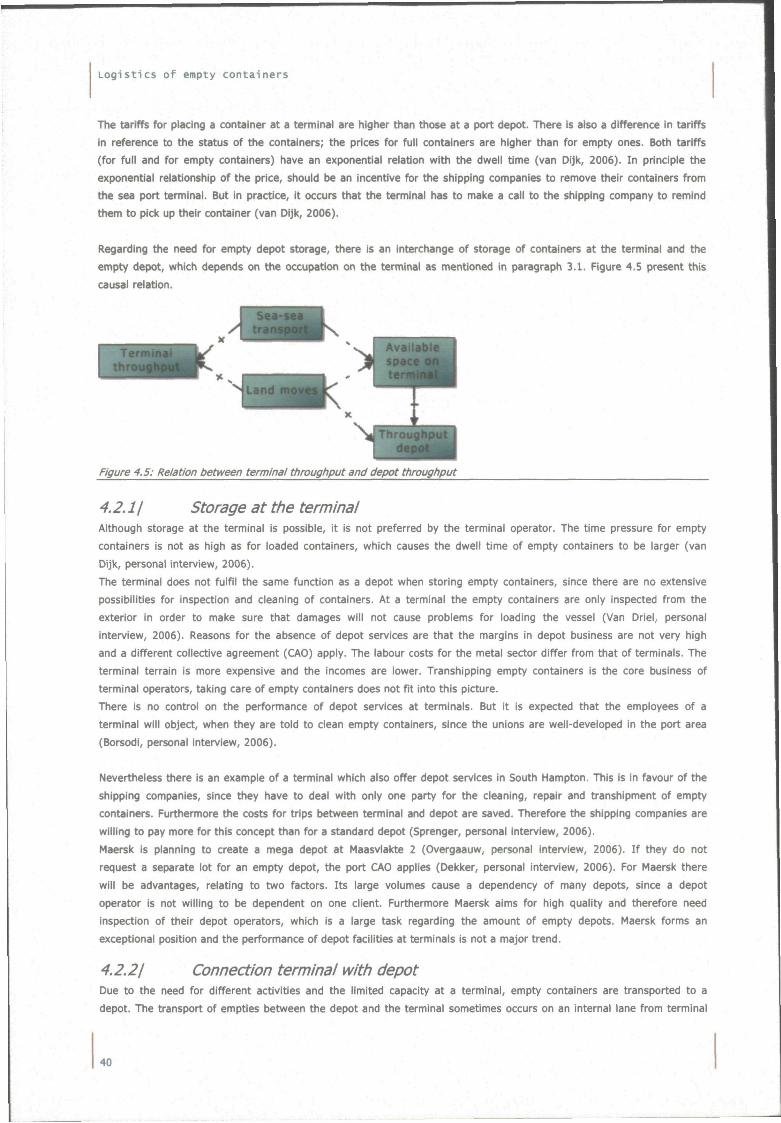

FIGURE 4 .5 : RELATION BETWEEN TERMINAL THROUGHPUT AND DEPOT THROUGHPUT 40

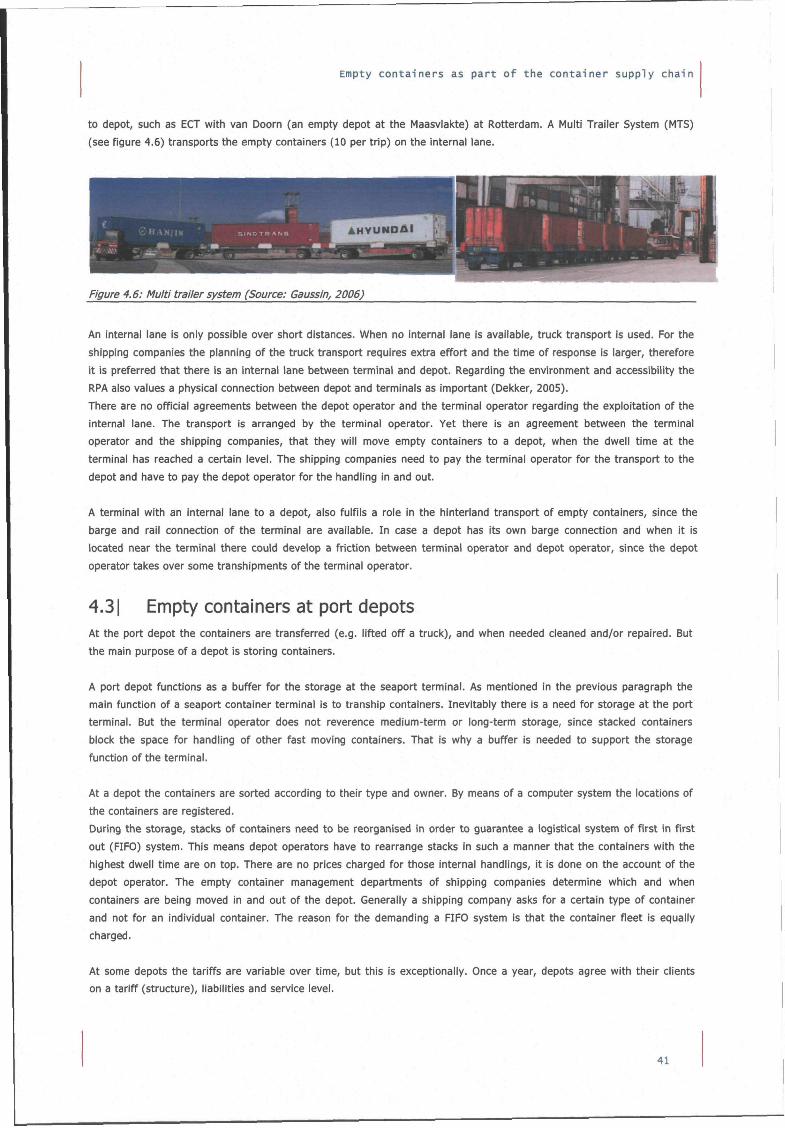

FIGURE 4 .6 : MULTI TRAILER SYSTEM (SOURCE: GAUSSIN, 2006) 41

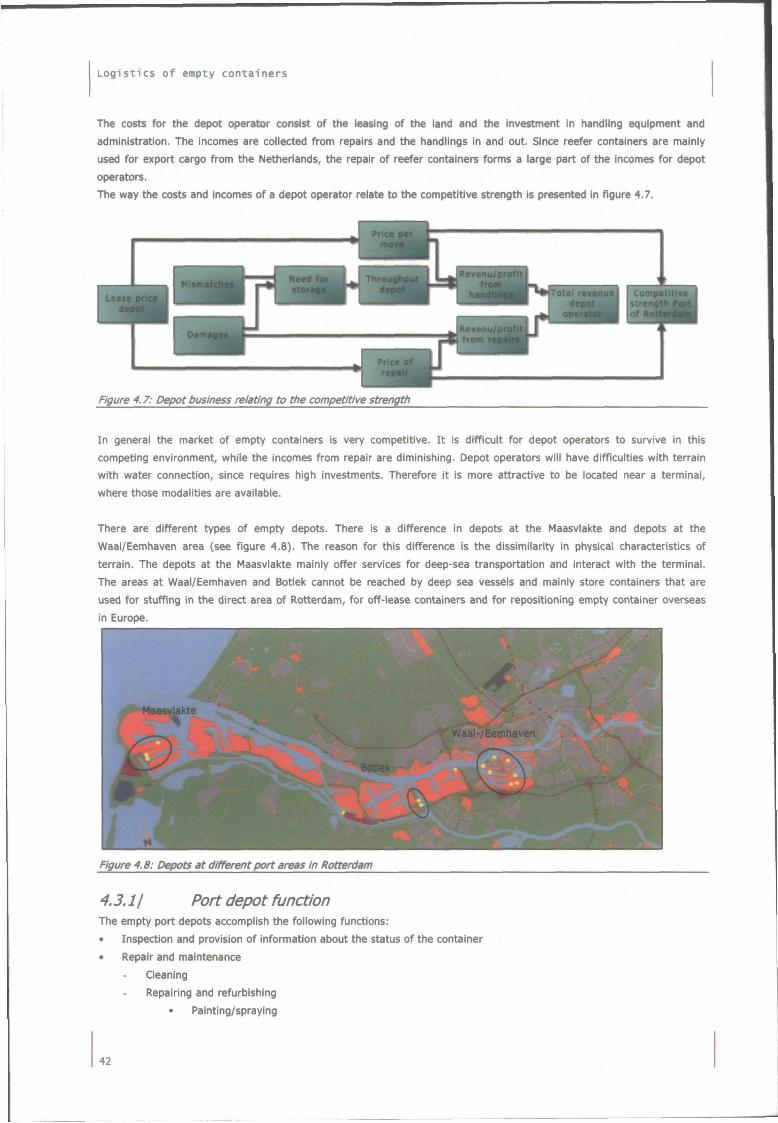

FIGURE 4 .7 : DEPOT BUSINESS RELATING TO THE COMPETITIVE STRENGTH 42

FIGURE 4 .8 : DEPOTS AT DIFFERENT PORT AREAS I N ROTTERDAM 42

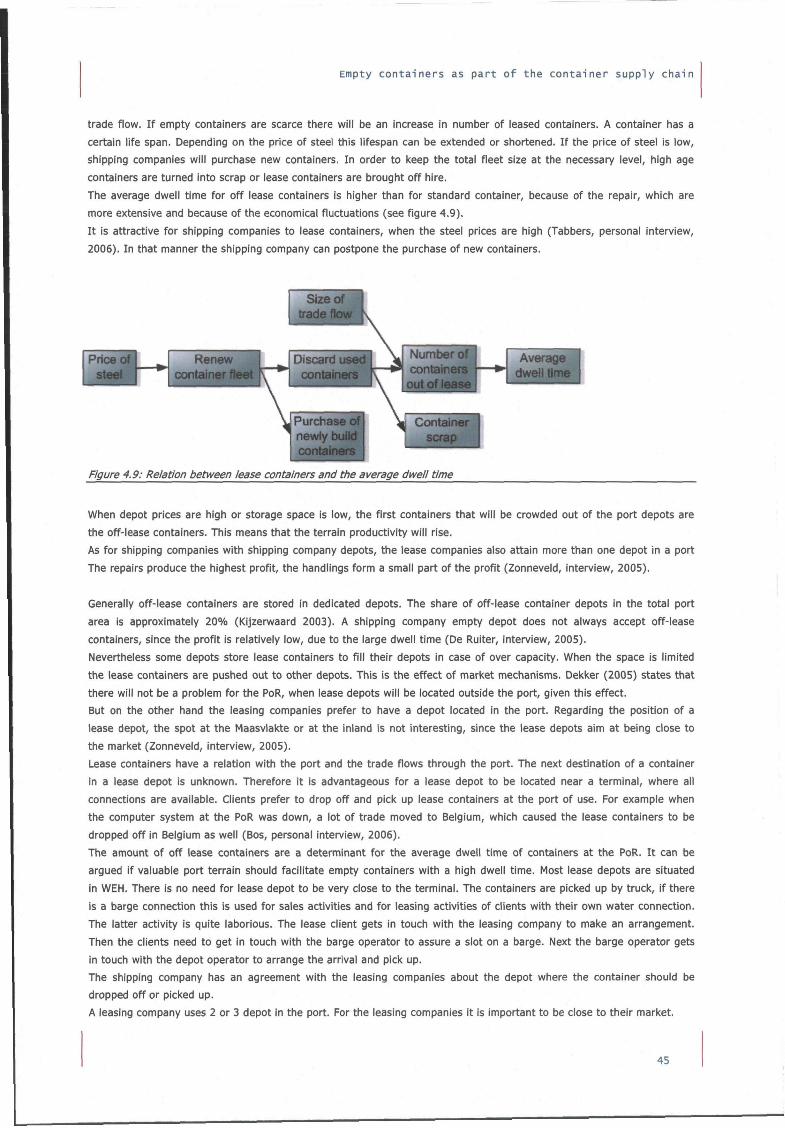

FIGURE 4 .9 : RELATION BETWEEN LEASE CONTAINERS AND THE AVERAGE DWELL TIME 45

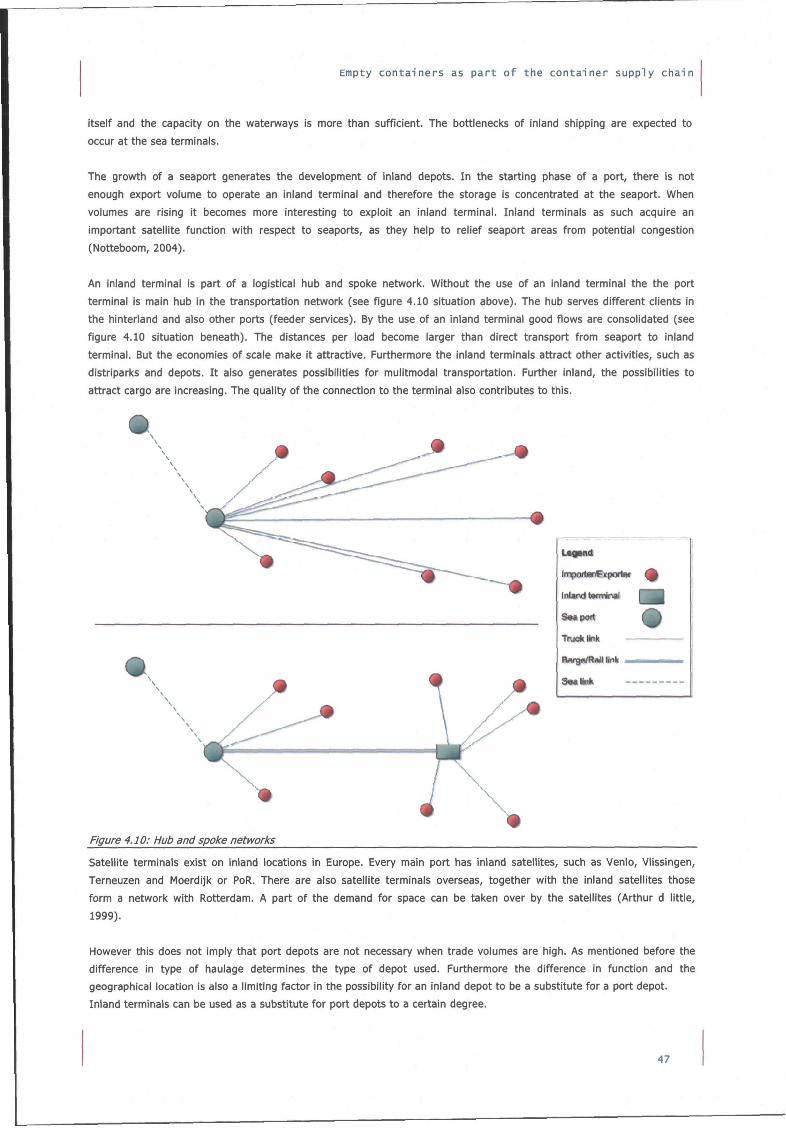

FIGURE 4 .10 : HUB AND SPOKE NETWORKS 47

FIGURE 4 . 1 1 : EMPTY CONTAINER MARKET 48

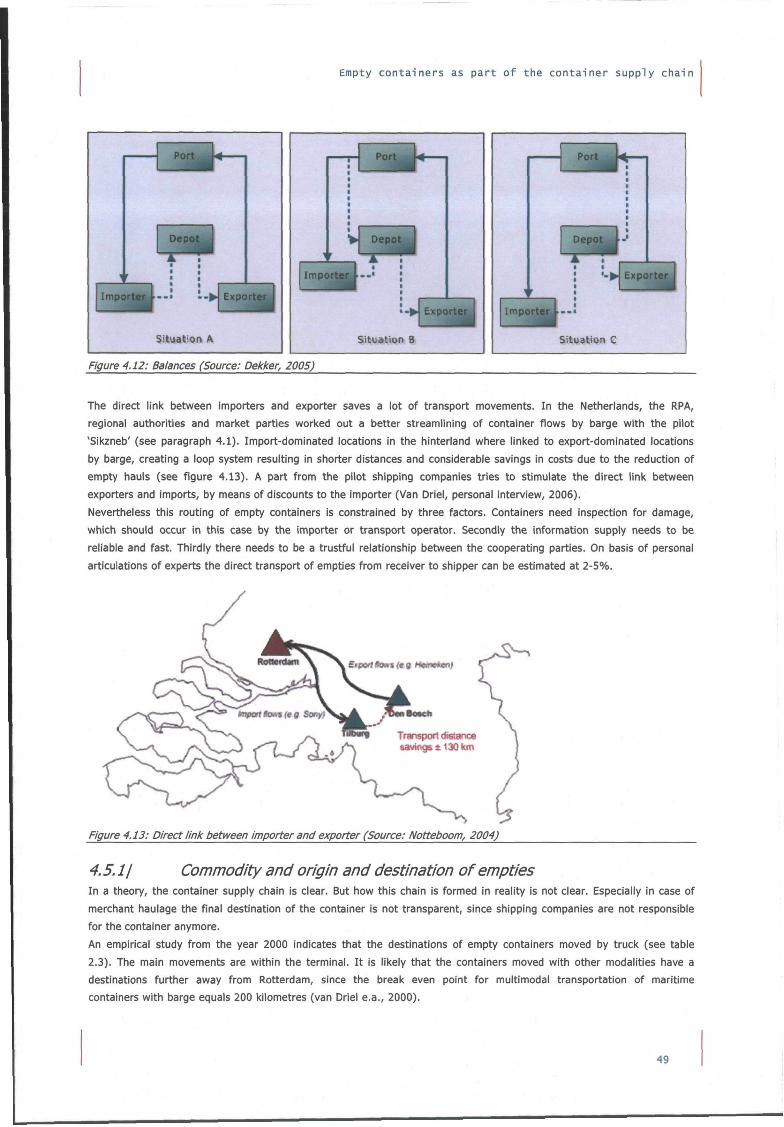

FIGURE 4 .12: BALANCES (SOURCE; DEKKER, 2005) 49

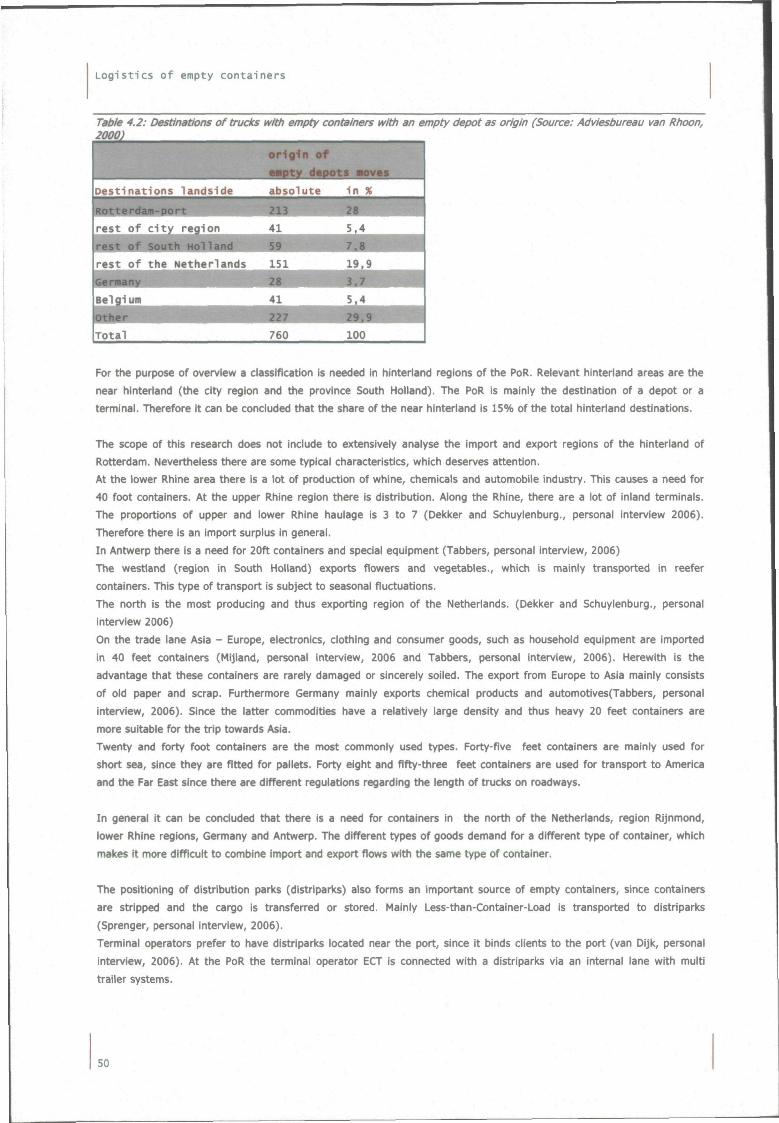

FIGURE 4 .13: DIRECT LINK BETWEEN IMPORTER AND EXPORTER (SOURCE; NOTTEBOOM, 2004) 49

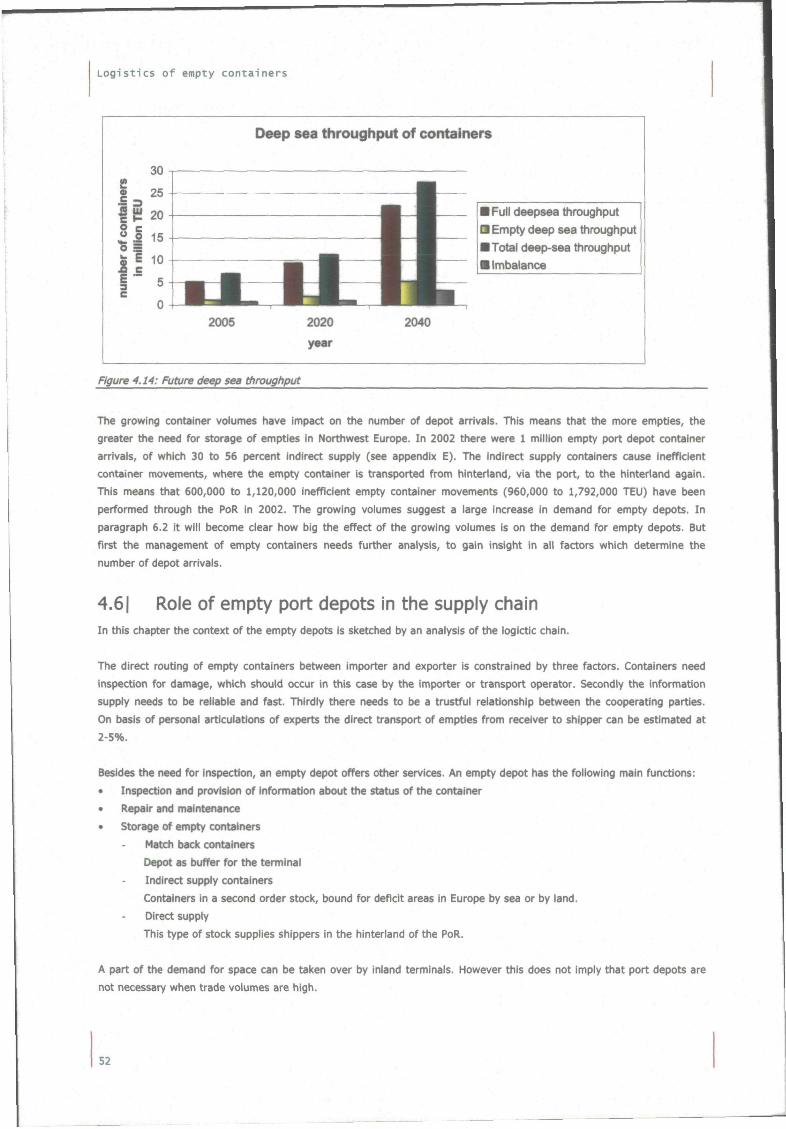

FIGURE 4 .14 : FUTURE DEEP SEA THROUGHPUT 52

FIGURE 5 . 1 : SUPPLY CHAIN SCOPE 55

FIGURE 5.2; SAW TOOTH DIAGRAM (ADAPTED FROM: COVENTRY UNIVERSITY, 1999) 56

FIGURE 5.3: DEVELOPMENT OF THE INVENTORY LEVEL AT A DEPOT 56

FIGURE 5.4: TYPES OF CONTAINER STOCKS 58

FIGURE 5.5; INFLOW AND OUTFLOW EMPTY CONTAINERS 60

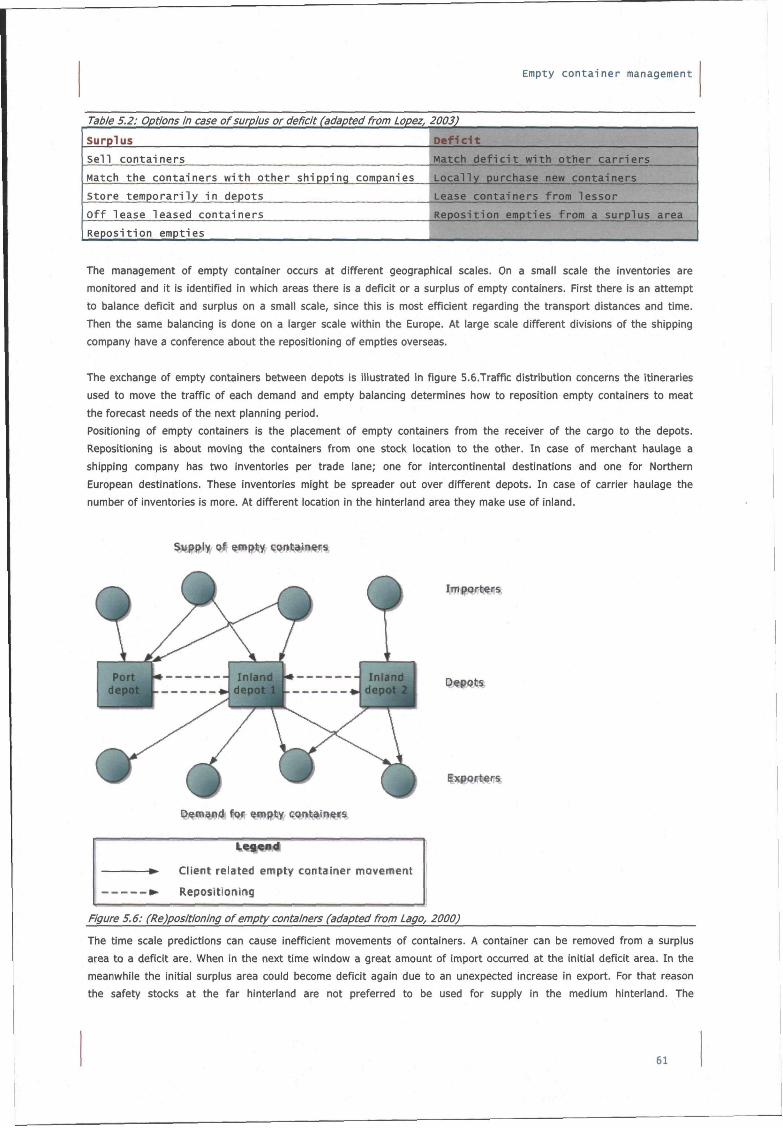

FIGURE 5.6: (RE)POSITIONING OF EMPTY CONTAINERS (ADAPTED FROM LAGO, 2000) 61

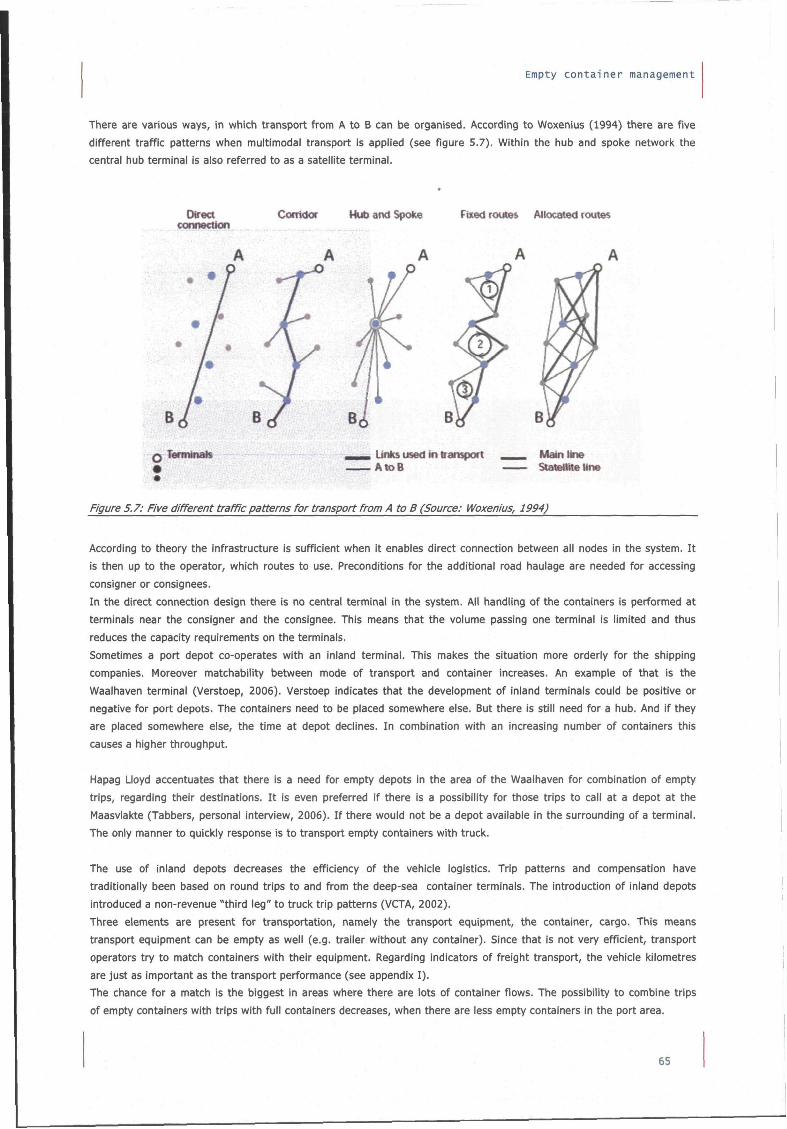

FIGURE 5.7: FIVE DIFFERENT TRAFFIC PATTERNS FOR TRANSPORT FROM A TO B (SOURCE: WOXENIUS, 1994) 65

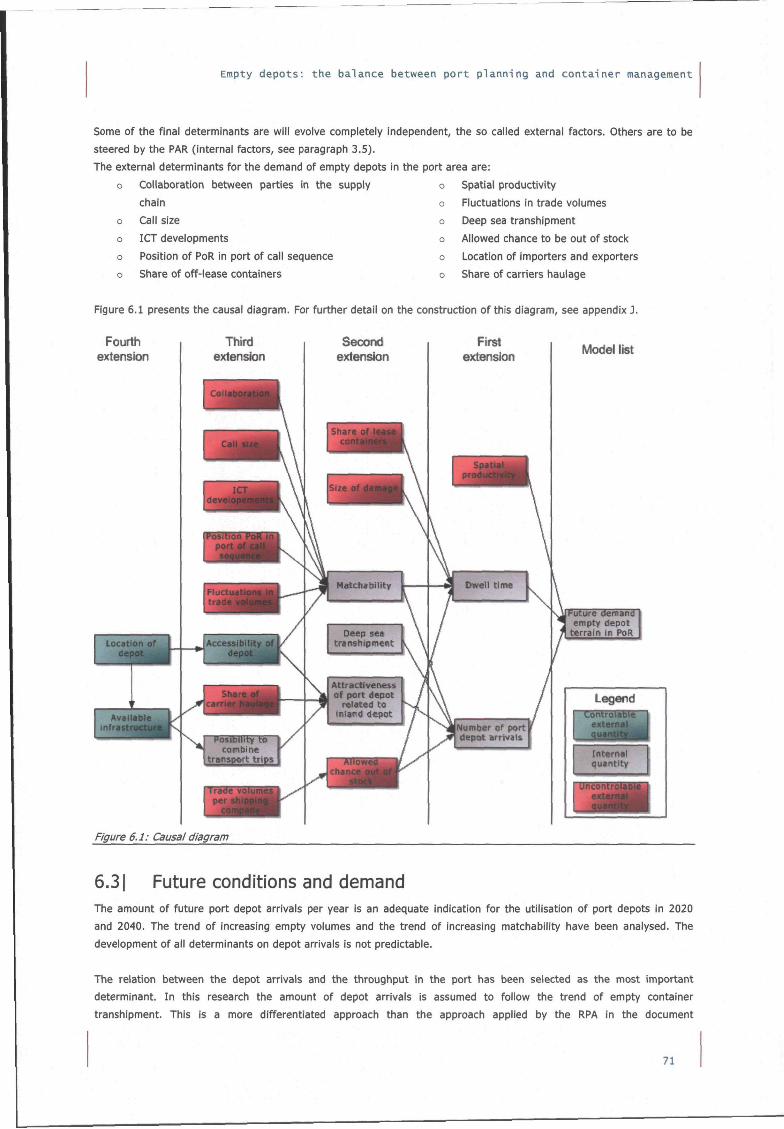

FIGURE 6 . 1 : CAUSAL DIAGRAM 71

FIGURE 6.2: INCREASING DEPOT PRODUCTIVITY (SOURCE: BOILÉ, 2005) 72

FIGURE 7 . 1 : MORPHOLOGICAL SCHEME 78

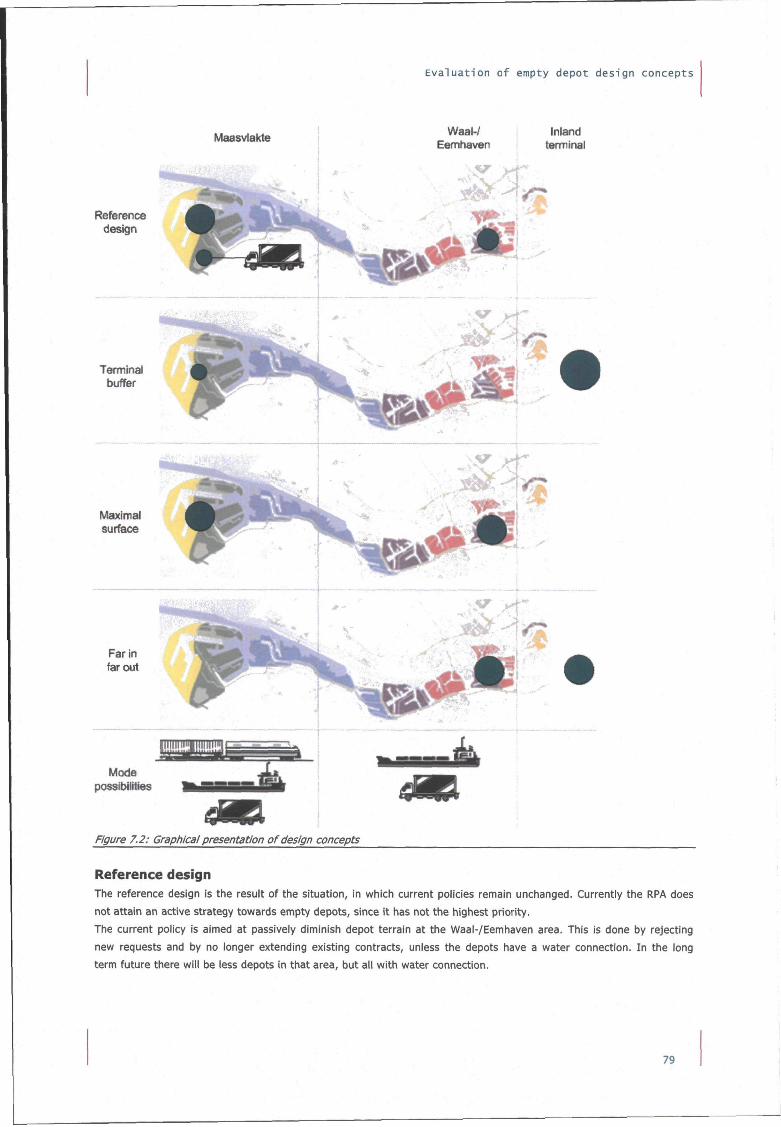

FIGURE 7.2: GRAPHICAL PRESENTATION OF DESIGN CONCEPTS 79

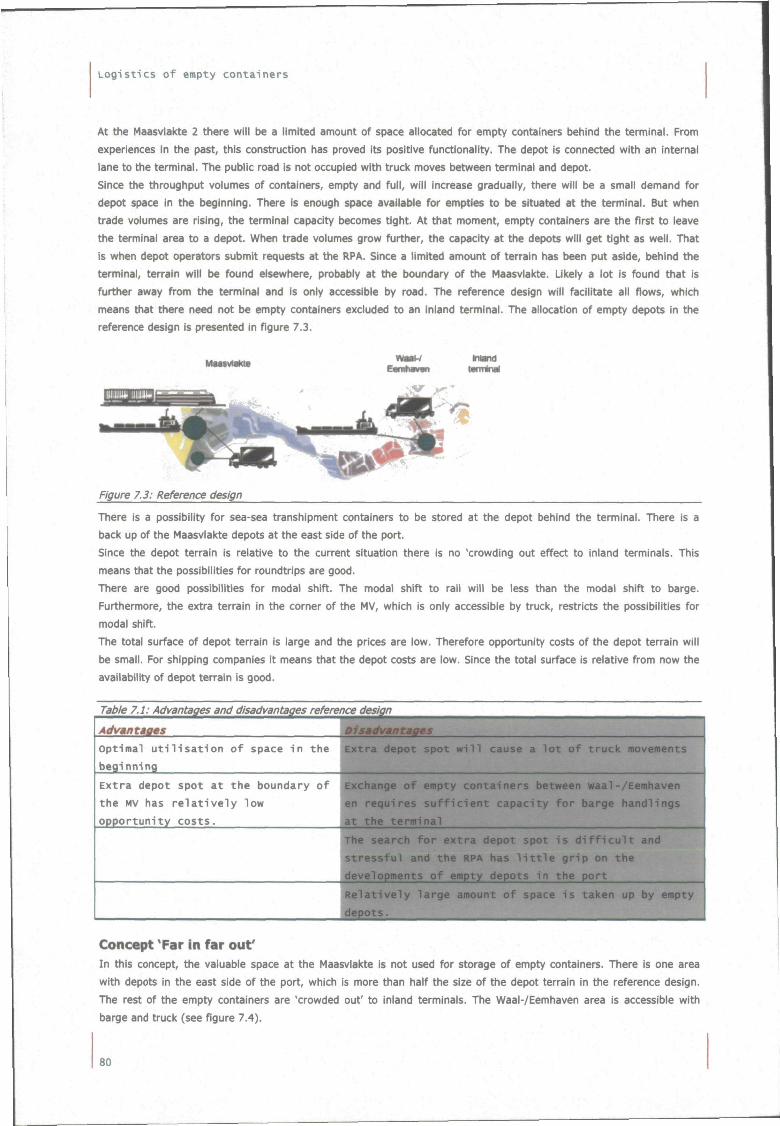

FIGURE 7.3: REFERENCE DESIGN 80

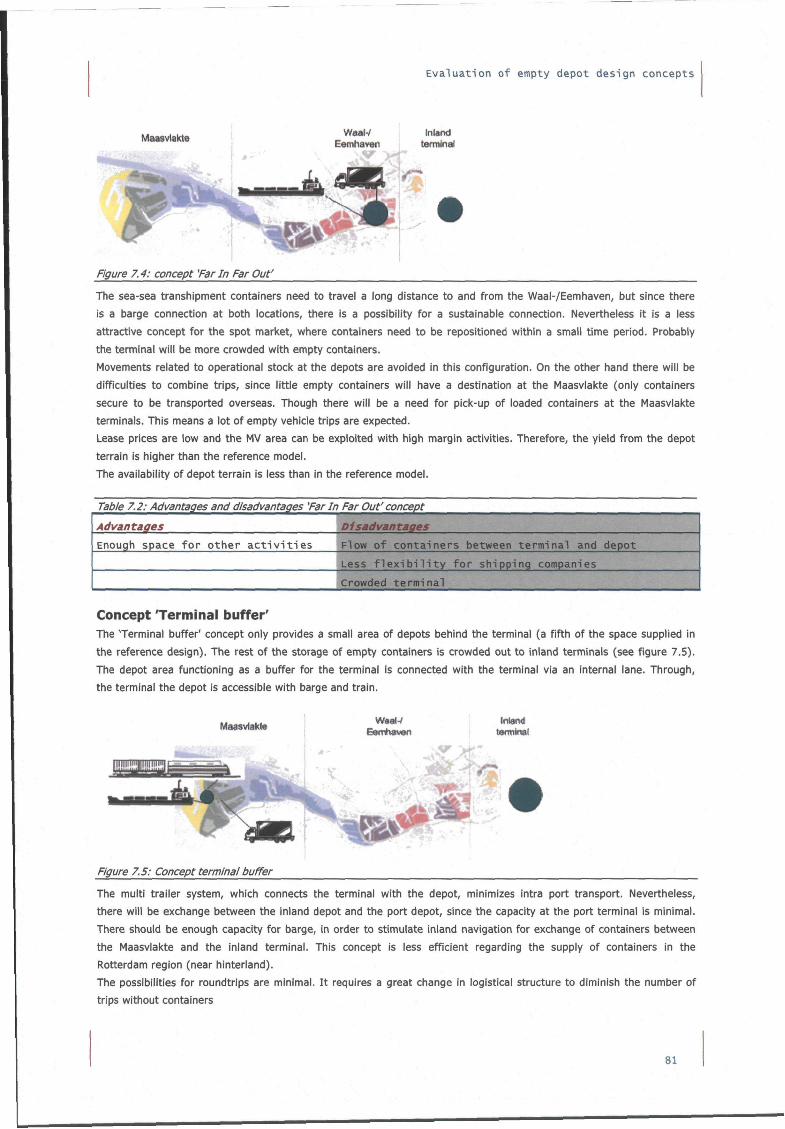

FIGURE 7.4: CONCEPT'FAR I N FAR OUT' 81

FIGURE 7.5: CONCEPT TERMINAL BUFFER 81

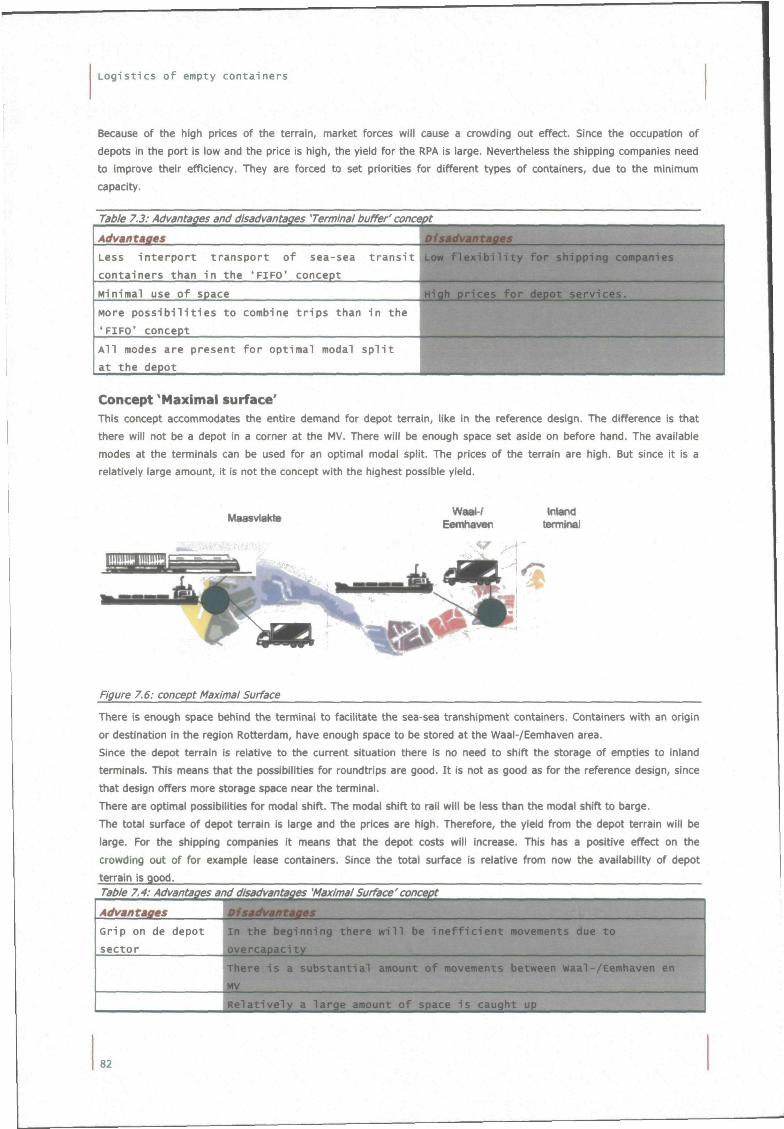

FIGURE 7.6: CONCEPT MAXIMAL SURFACE 82

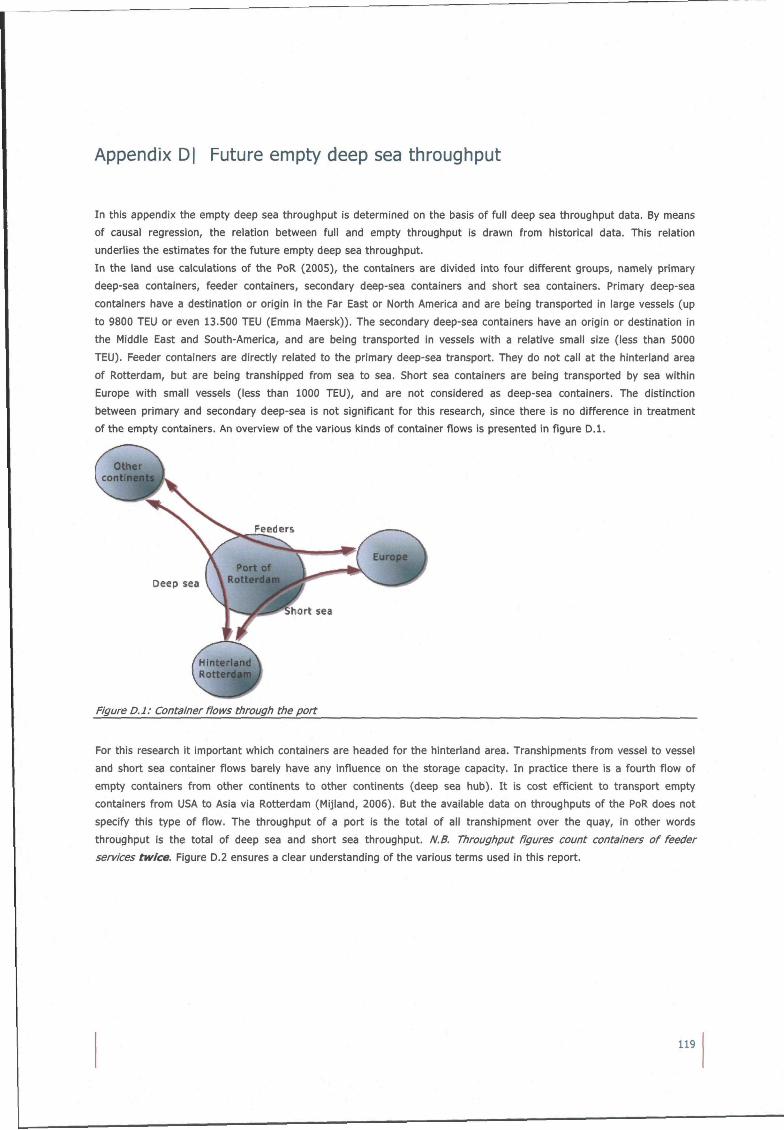

FIGURE A . l : CONTAINER FLOWS THROUGH THE PORT i l l

FIGURE B . l : OVERVIEW OF PARTIES INVOLVED 113

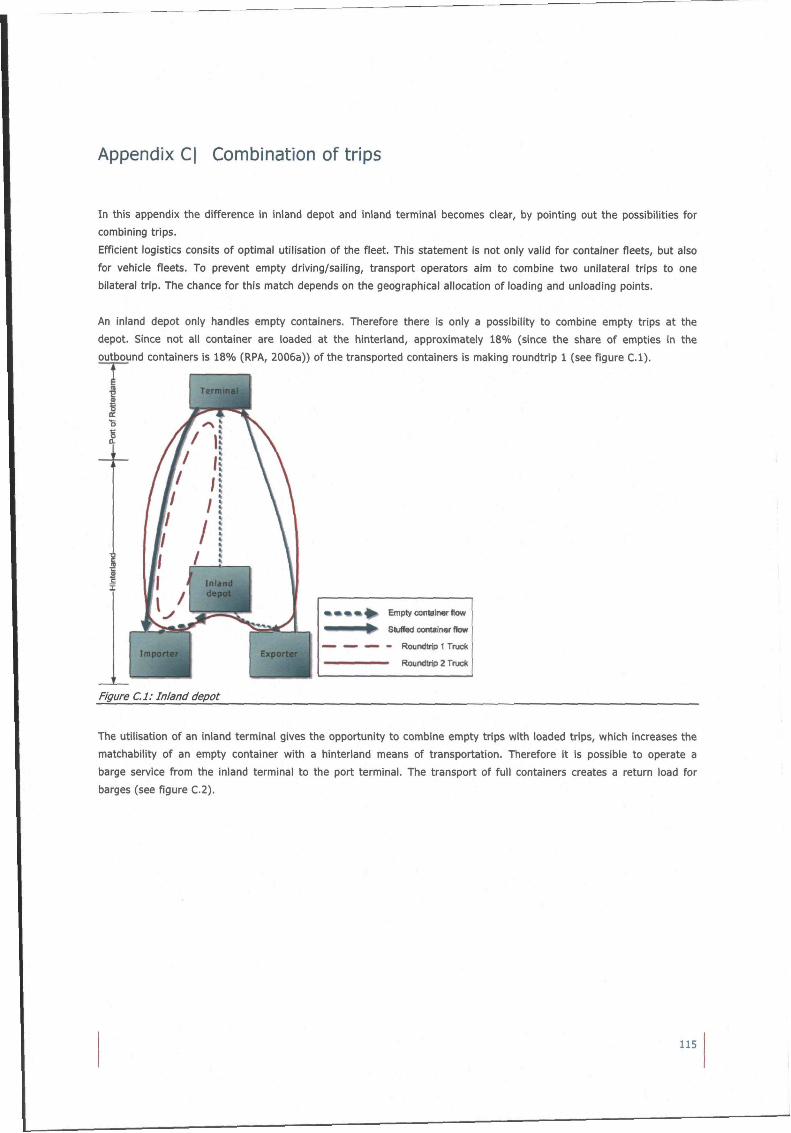

FIGURE C . l ; INLAND DEPOT 115

5

L o g i s t i c s o f empty c o n t a i n e r s

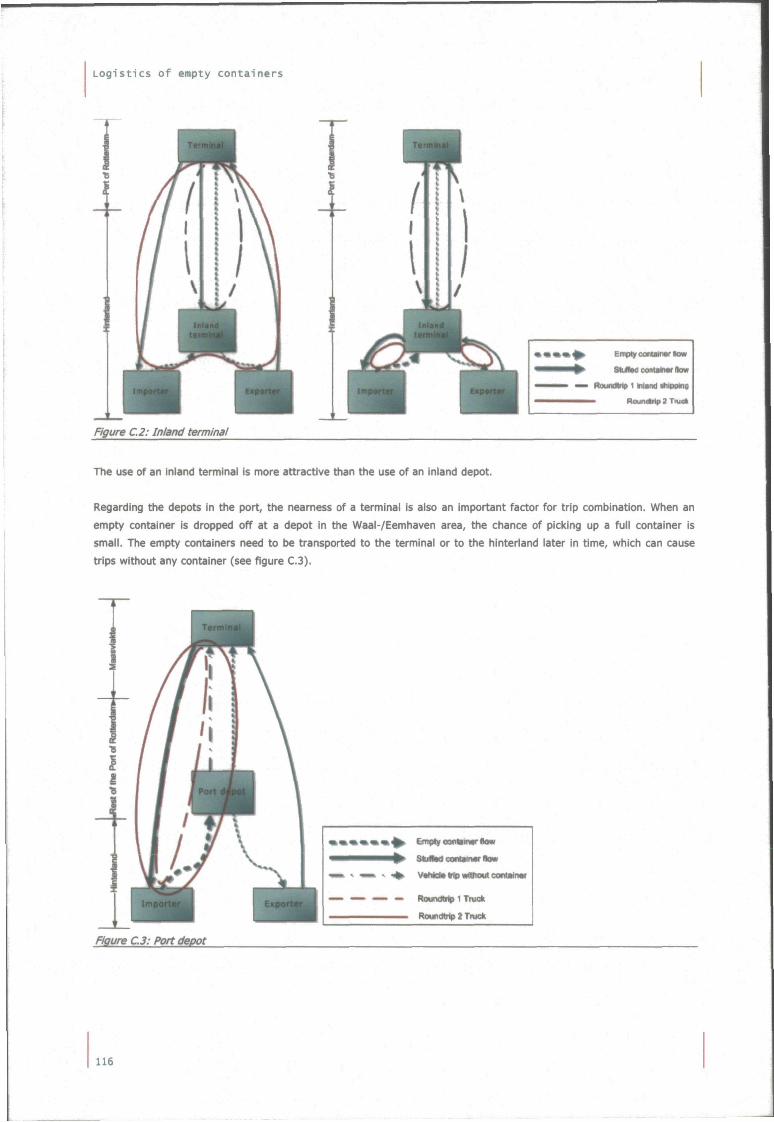

FIGURE C.2: INLAND TERMINAL 116

FIGURE c . 3 : PORT DEPOT 116

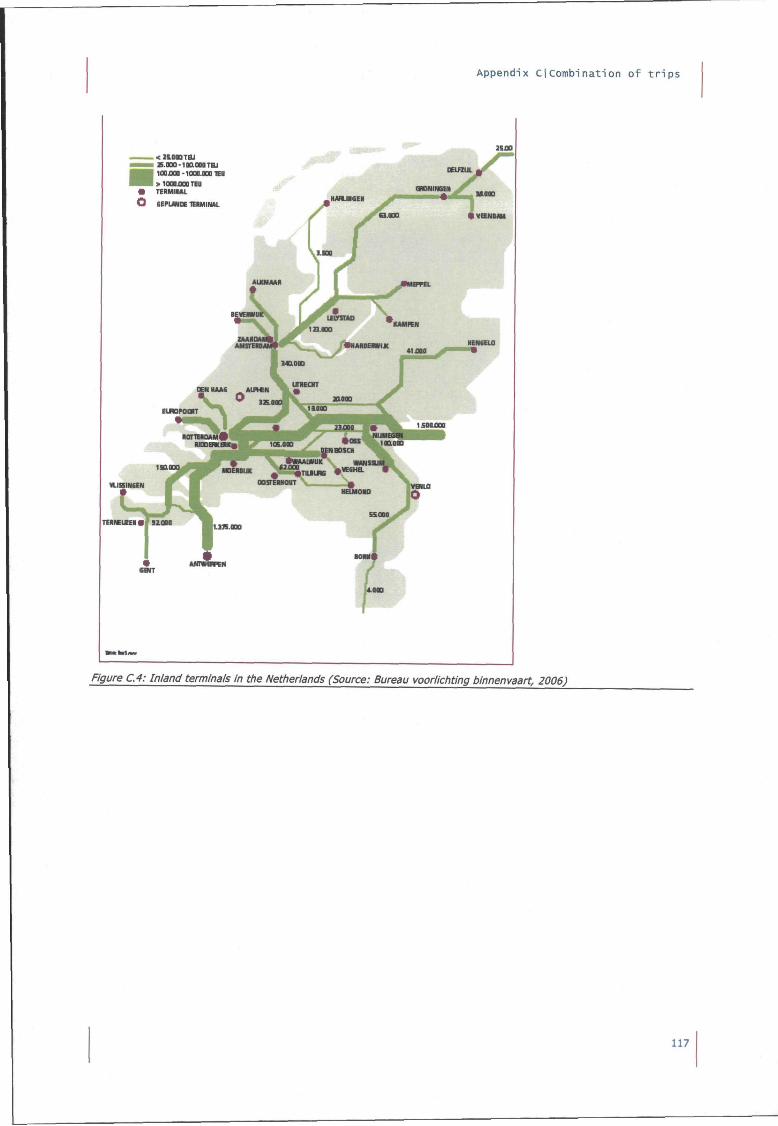

FIGURE C . 4 : INLAND TERMINALS I N THE NETHERLANDS (SOURCE: BUREAU VOORLICHTING BINNENVAART, 2006) 117

FIGURE D . l ; CONTAINER FLOWS THROUGH THE PORT 119

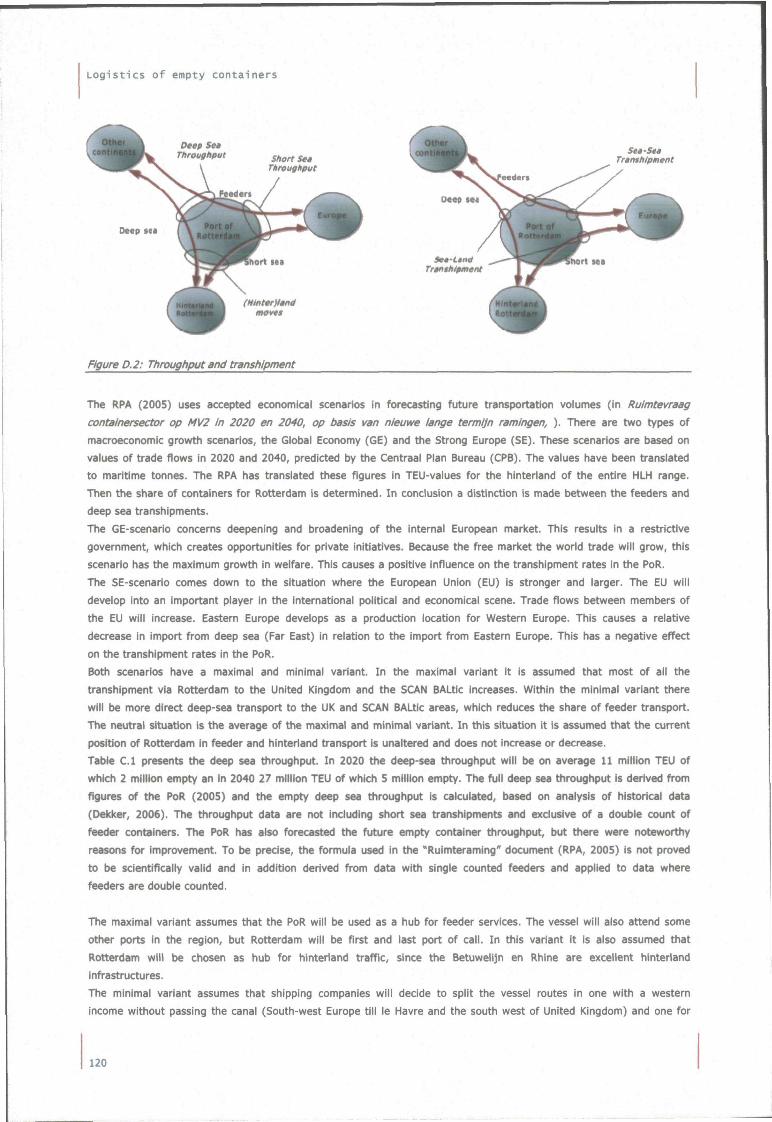

FIGURE D.2: THROUGHPUT AND TRANSHIPMENT 120

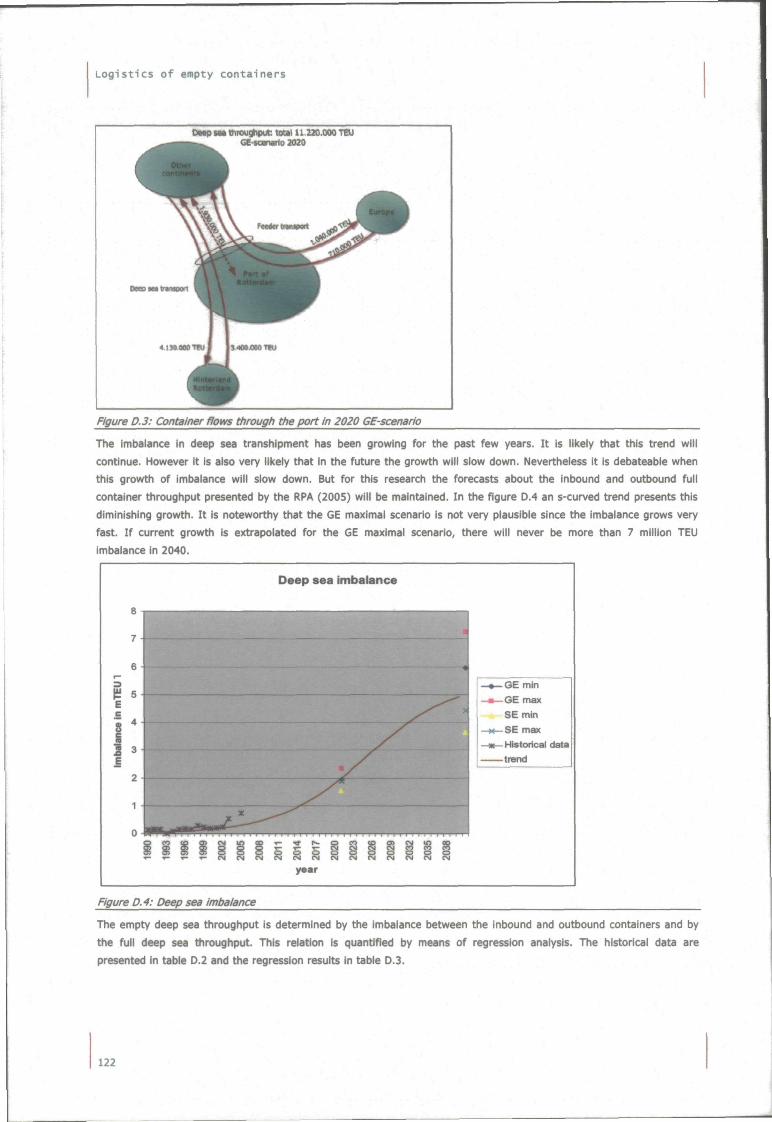

FIGURE D.3: CONTAINER FLOWS THROUGH THE P O R T I N 2020 GE-SCENARIO 122

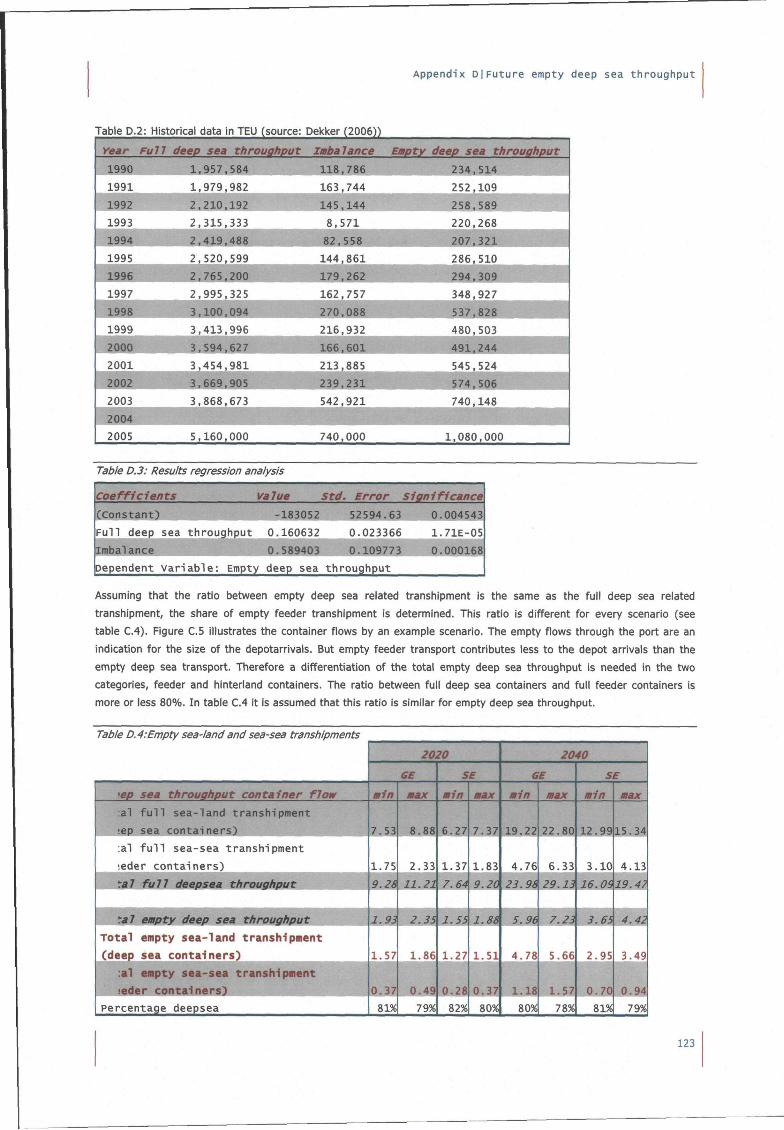

FIGURE D . 4 : DEEP SEA IMBAUNCE 122

FIGURE D . 5 : EMPTY CONTAINER FLOWS THROUGH THE PORT I N 2020 GE-SCENARIO 124

FIGURE D . 6 : FUTURE DEEP SEA THROUGHPUT 124

FIGURE E . l : EMPTY DEPOT MOVES 125

FIGURE E . 2 : EMPTY DEPOT TRAJECTORIES (ADAPTED FROM DEKKER (2005)) 125

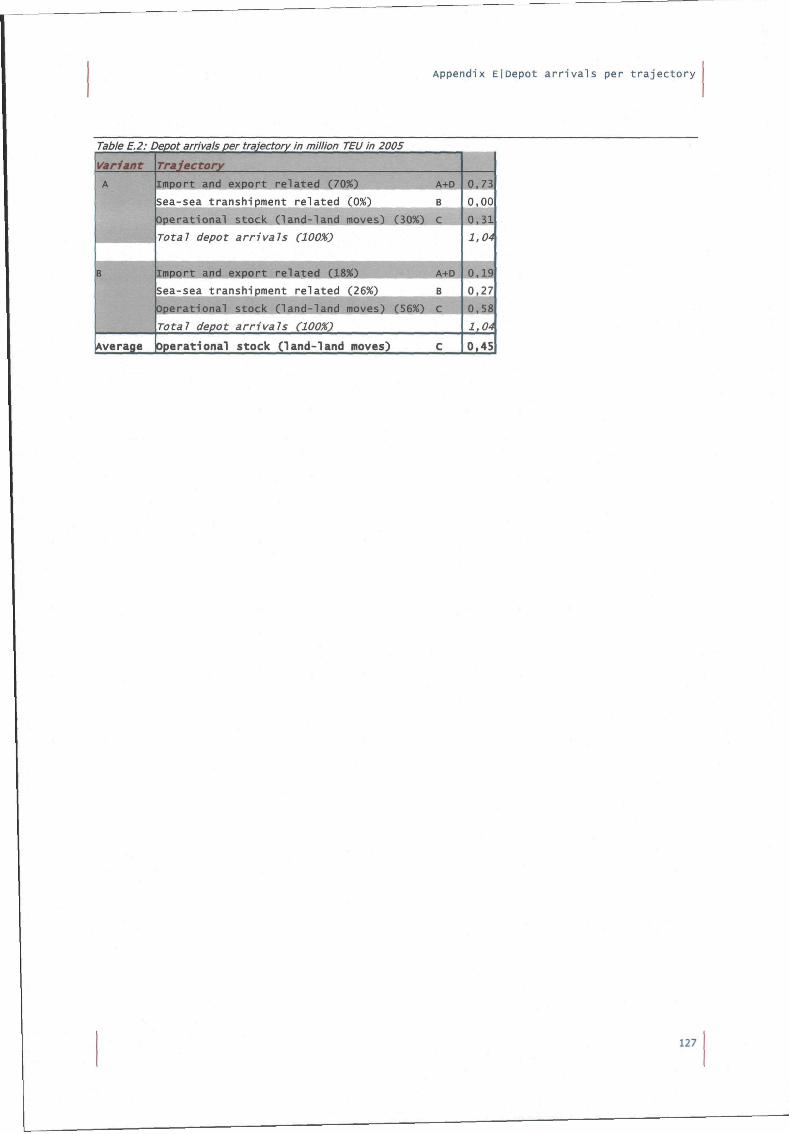

FIGURE E . 3 : VARIANTS OF FLOW SIZE PER DEPOT TRAJECTORY 126

FIGURE G . l : ALGORITHM 132

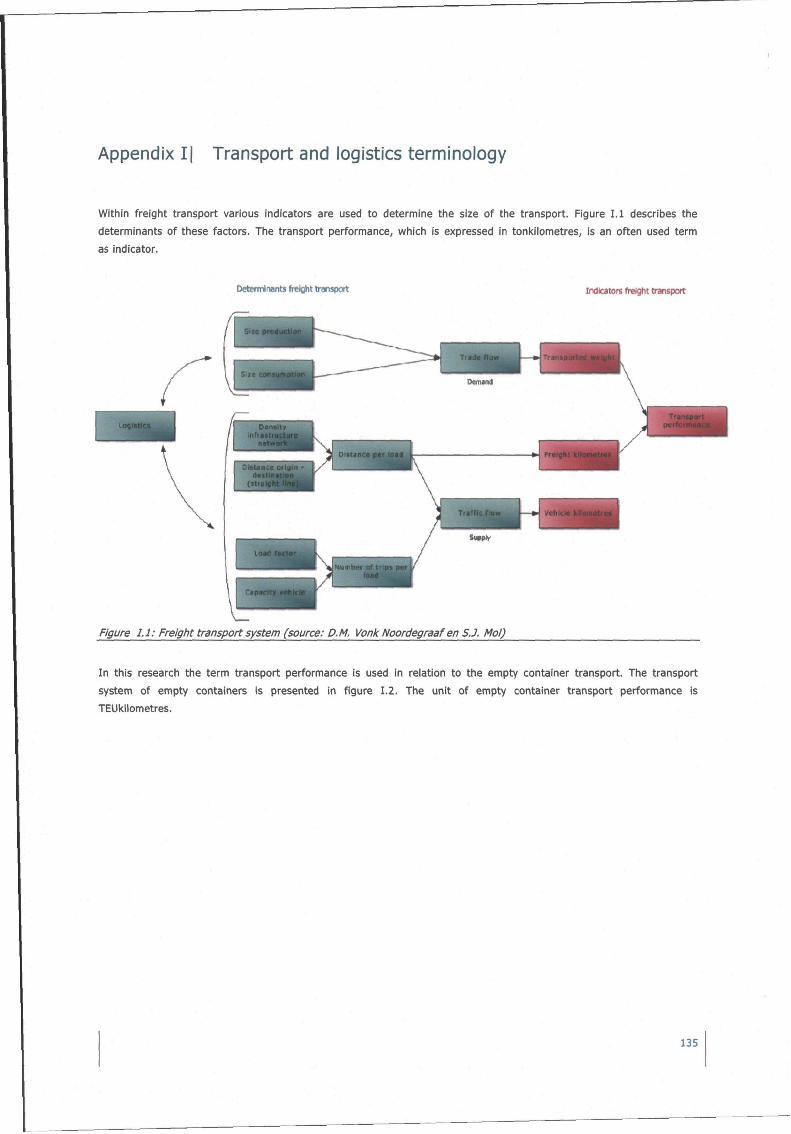

FIGURE l . l : FREIGHT TRANSPORT SYSTEM (SOURCE: D.M. VONK NOORDEGRAAF EN S . J . MOL) 135

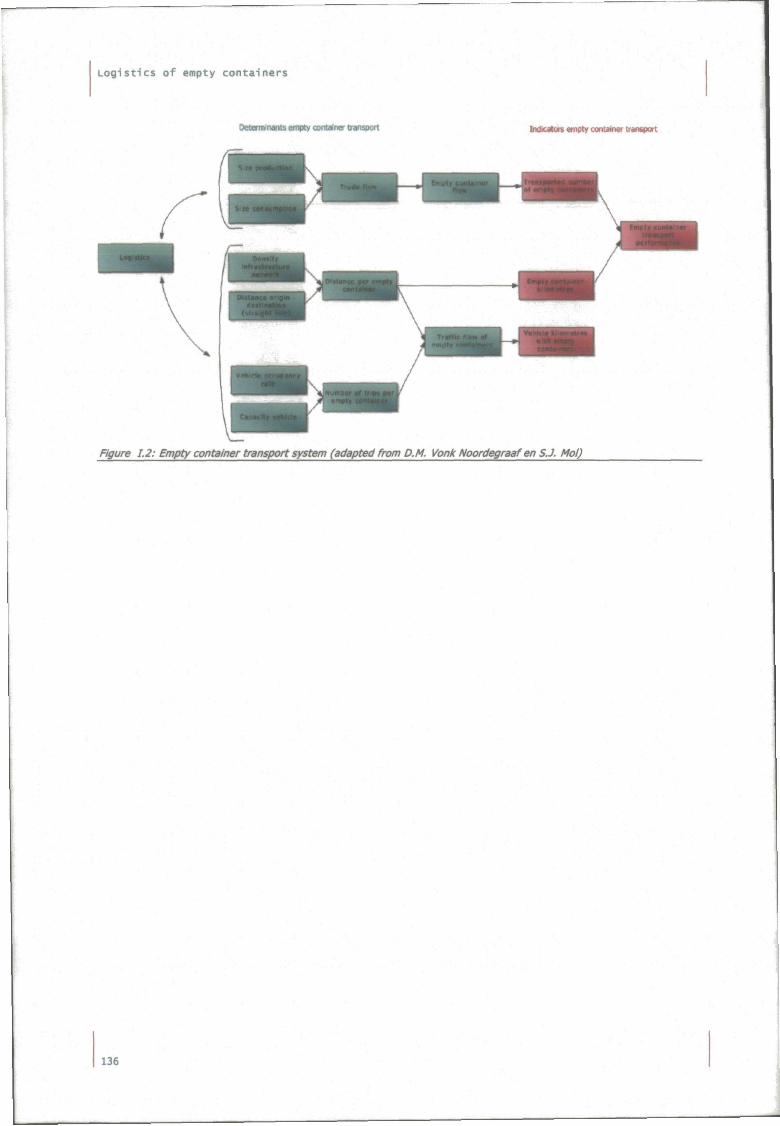

FIGURE 1.2: EMPTY CONTAINER TRANSPORT SYSTEM (ADAPTED FROM D.M. VONK NOORDEGRAAF EN S.J. MOL) 136

FIGURE J . l : INITIAL QUANTITY LIST 138

FIGURE J.2: SPATIAL PRODUCTIVITY 139

FIGURE J.3: MATCHABIUTY 139

FIGURE J.4: DEEP SEA TRANSHIPMENT 140

FIGURE J.5: QUANTITY LIST 141

FIGURE J.6: U S T EXTENSION 143

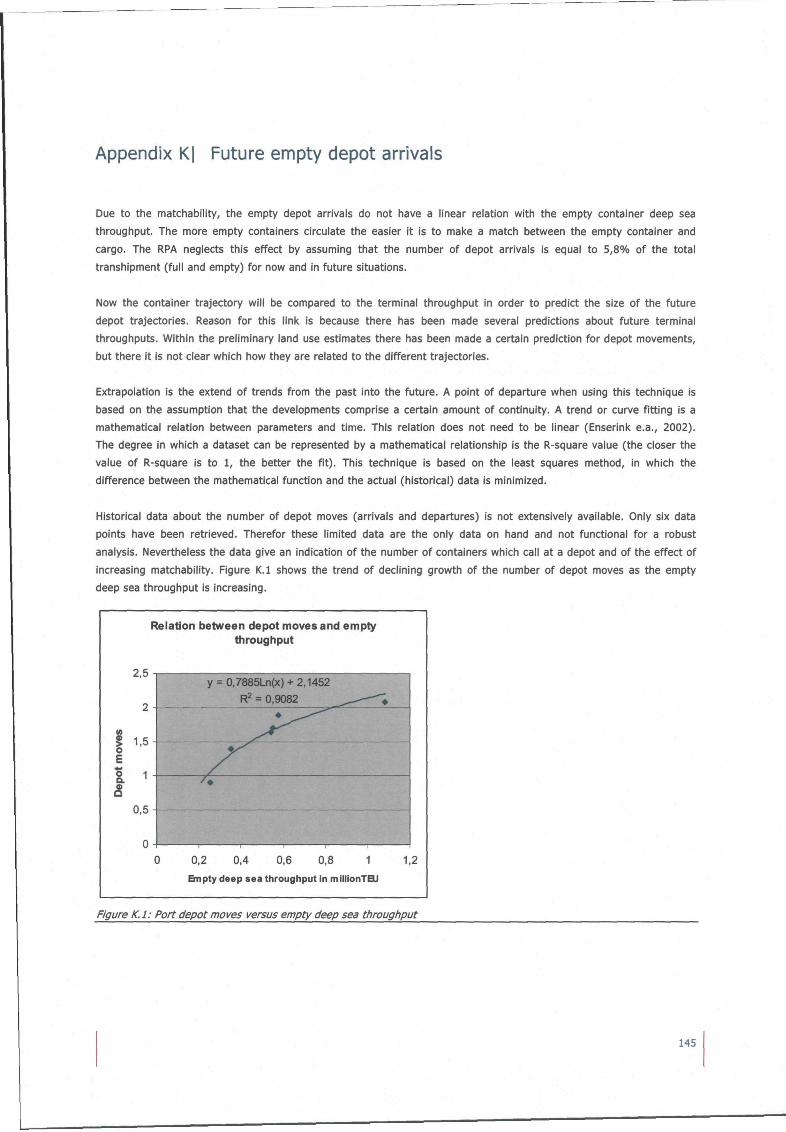

FIGURE K . l : PORT DEPOT MOVES VERSUS EMPTY DEEP SEA THROUGHPUT 145

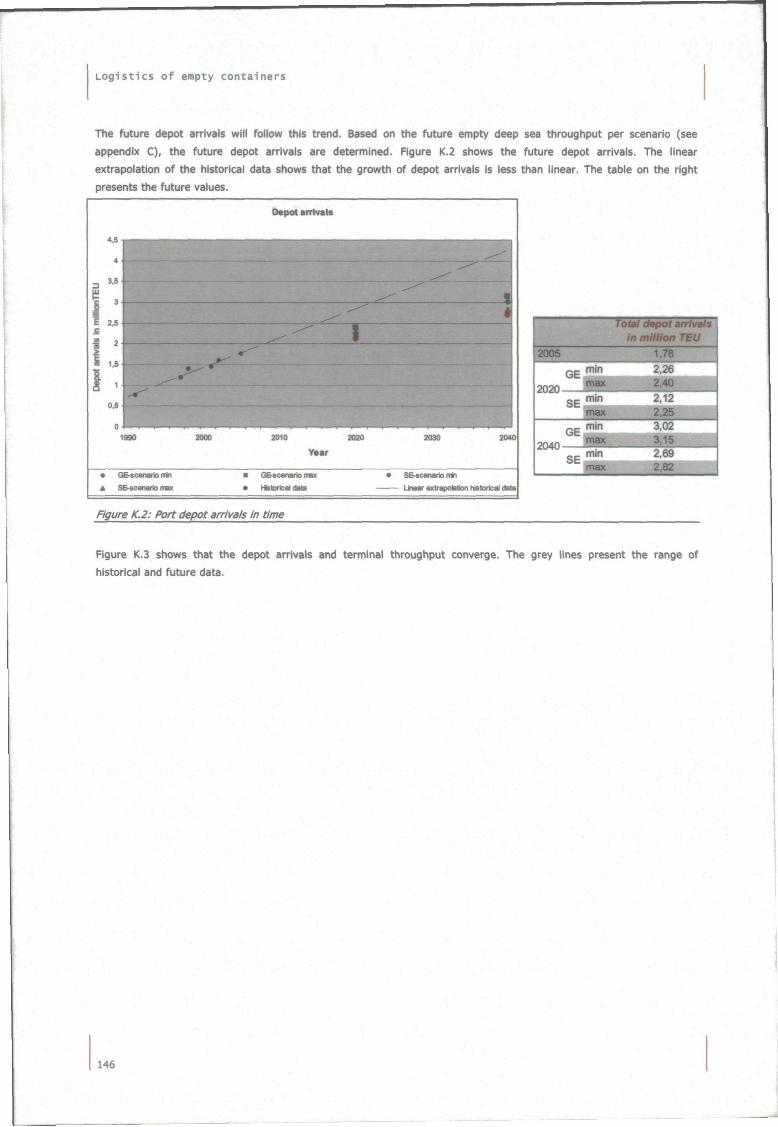

FIGURE K . 2 ; PORT DEPOT ARRIVALS I N TIME 146

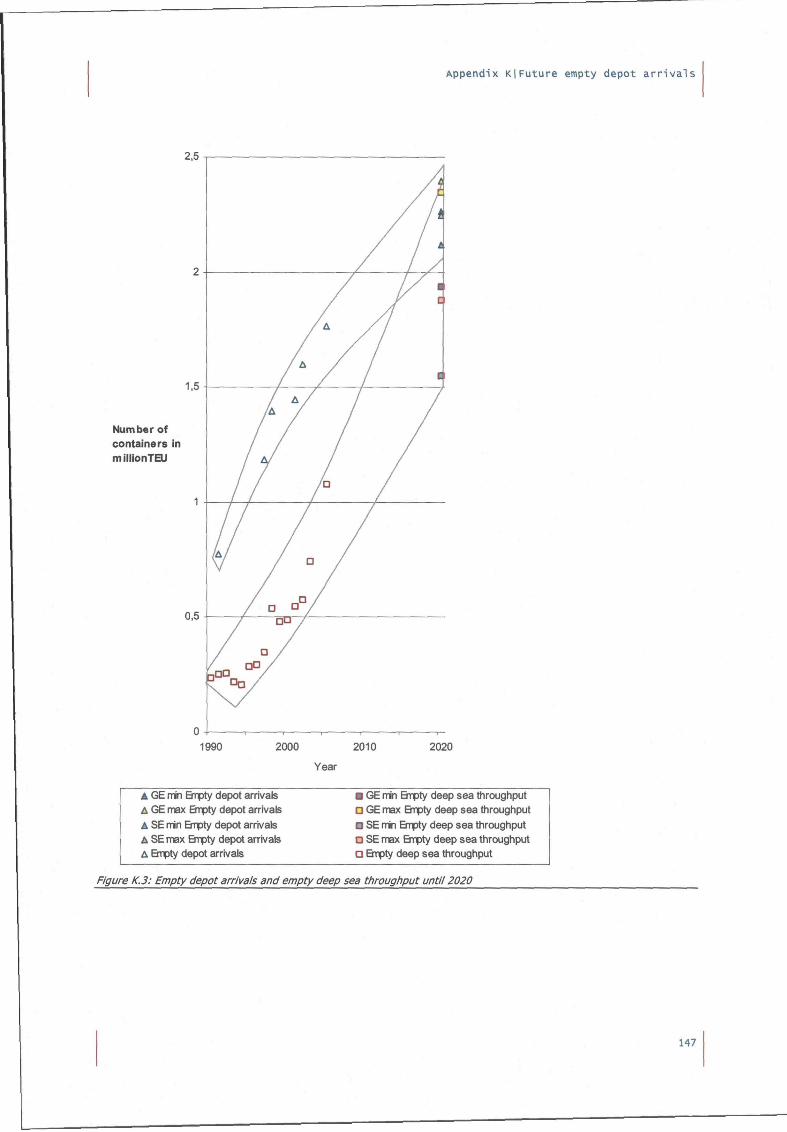

FIGURE K . 3 : EMPTY DEPOT ARRIVALS AND EMPTY DEEP SEA THROUGHPUT UNTIL 2020 147

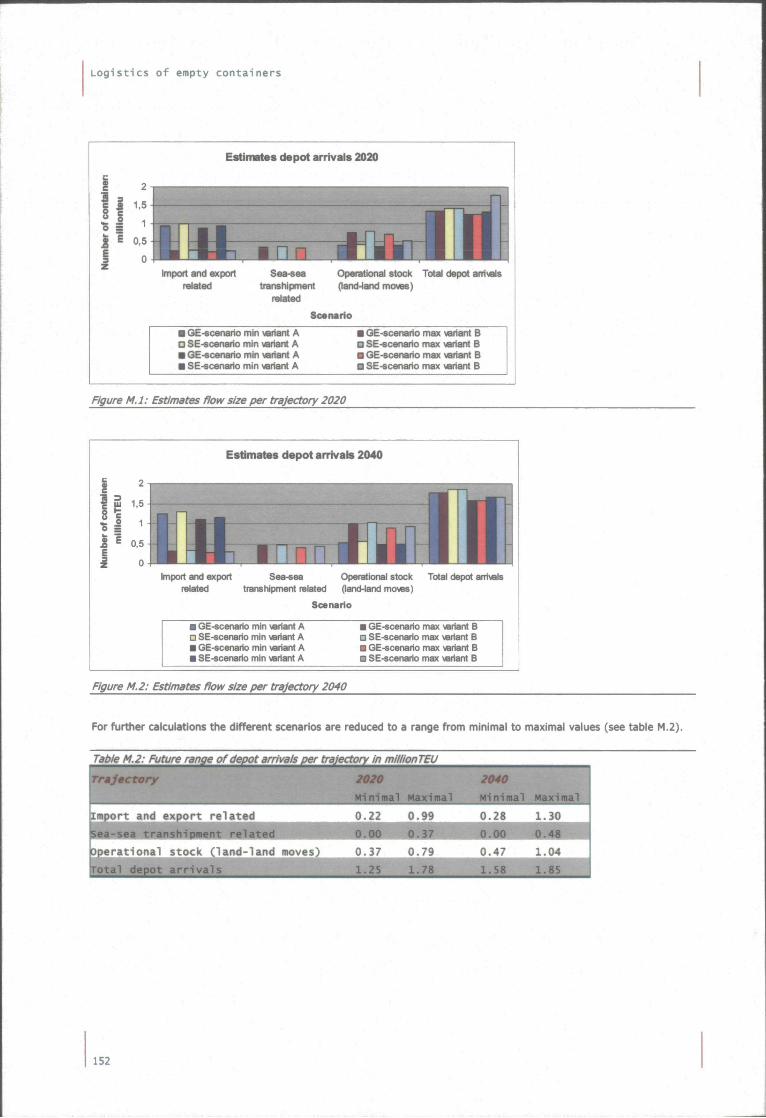

FIGURE M . l : ESTIMATES FLOW SIZE PER TRAJECTORY 2020 152

FIGURE M . 2 ; ESTIMATES FLOW SIZE PER TRAJECTORY 2040 152

FIGURE N . I : CONTAINER FLOWS THROUGH THE PORT (SOURCE:

HTTP://INFORMATIE.BINNENVAART.NL/VERVOERGOED.PHP) 154

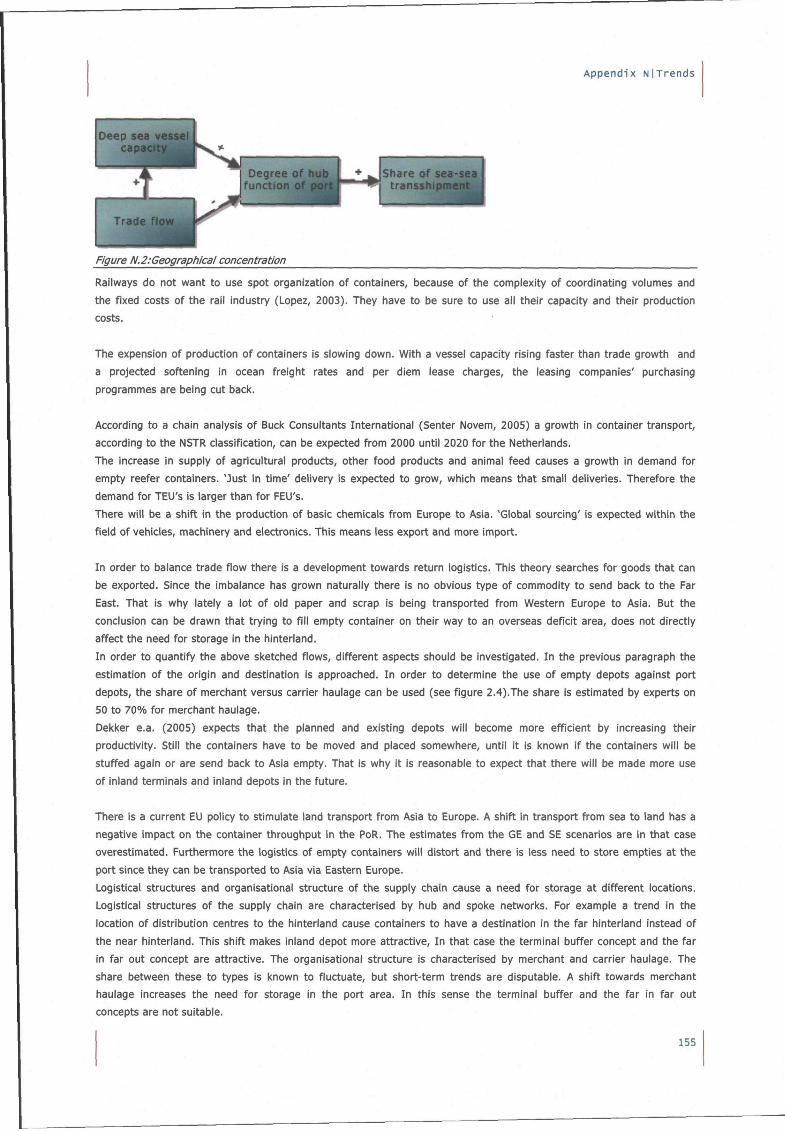

FIGURE N.2:GEOGRAPHICAL CONCENTRATION 155

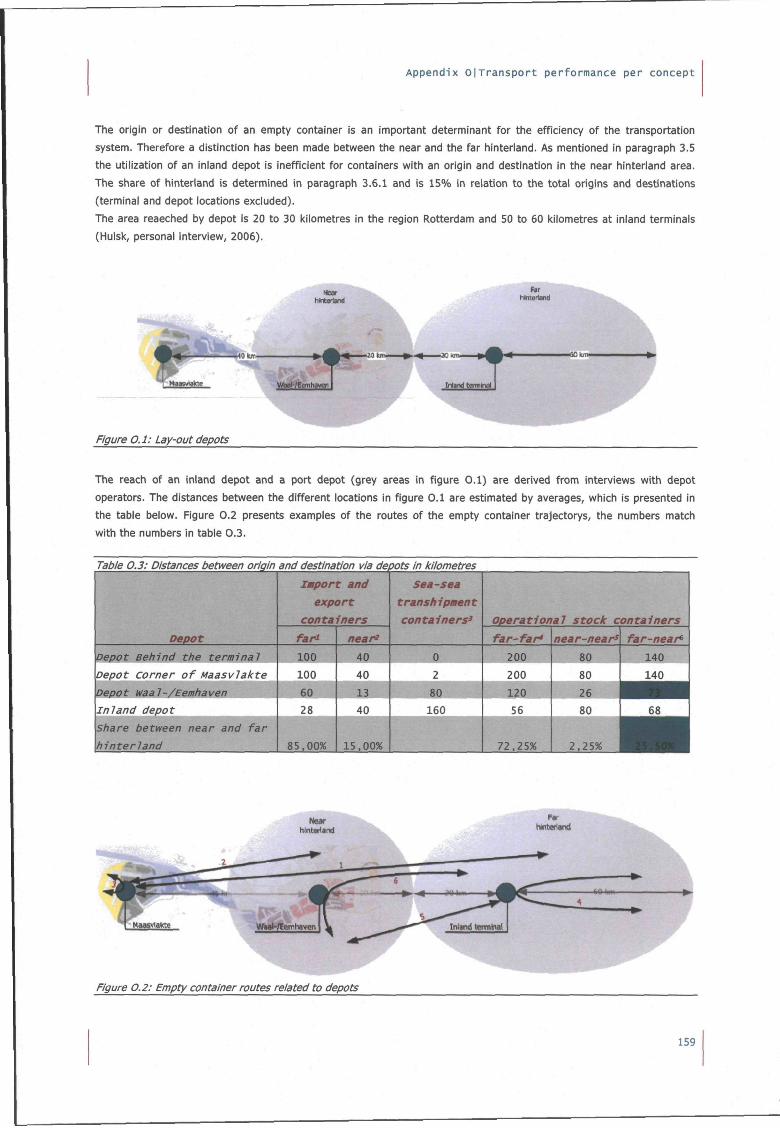

FIGURE 0 . 1 : LAY-OUT DEPOTS 159

FIGURE 0 . 2 : EMPTY CONTAINER ROUTES RELATED TO DEPOTS 159

FIGURE 0 . 3 : TRANSPORT PERFORMANCE 2020 162

FIGURE 0 . 4 : TRANSPORT PERFORMANCE 2040 162

6

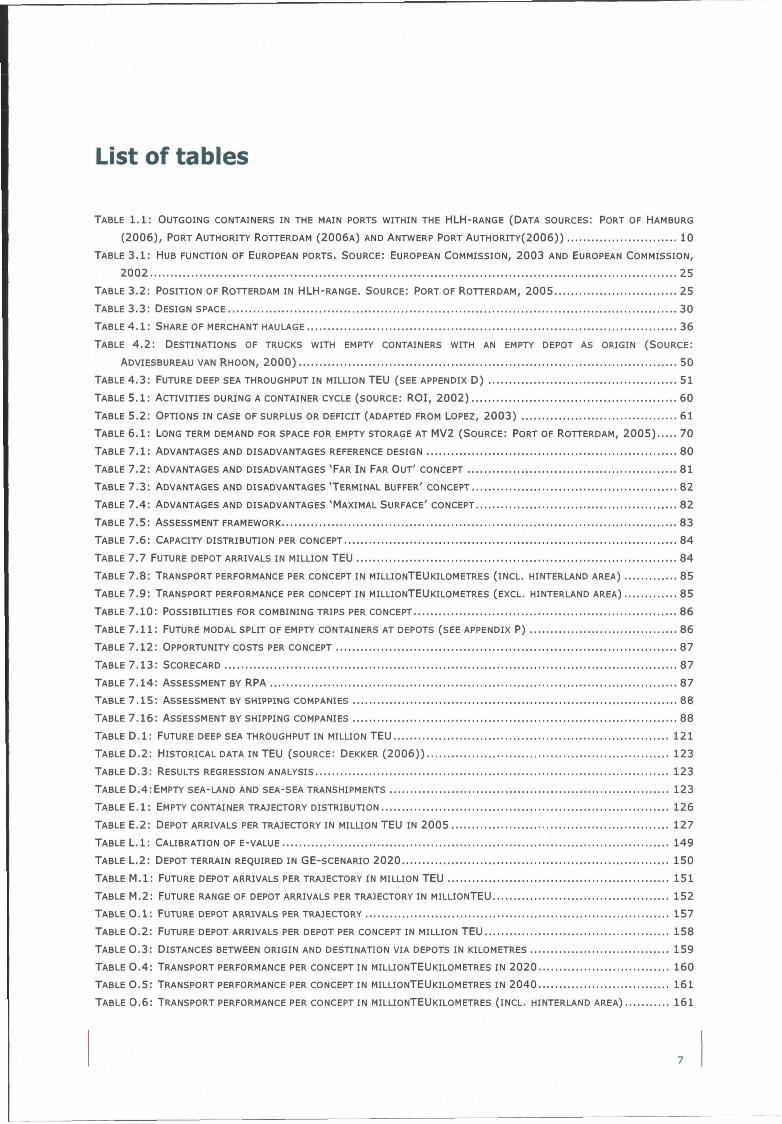

List of tables

TABLE 1 .1 : OUTGOING CONTAINERS I N THE MAIN PORTS WITHIN THE HLH-RANGE (DATA SOURCES: PORT OF HAMBURG

(2006), PORT AUTHORITY ROTTERDAM ( 2 0 0 6 A ) AND ANTWERP PORT A U T H O R I T Y ( 2 0 0 6 ) ) 10

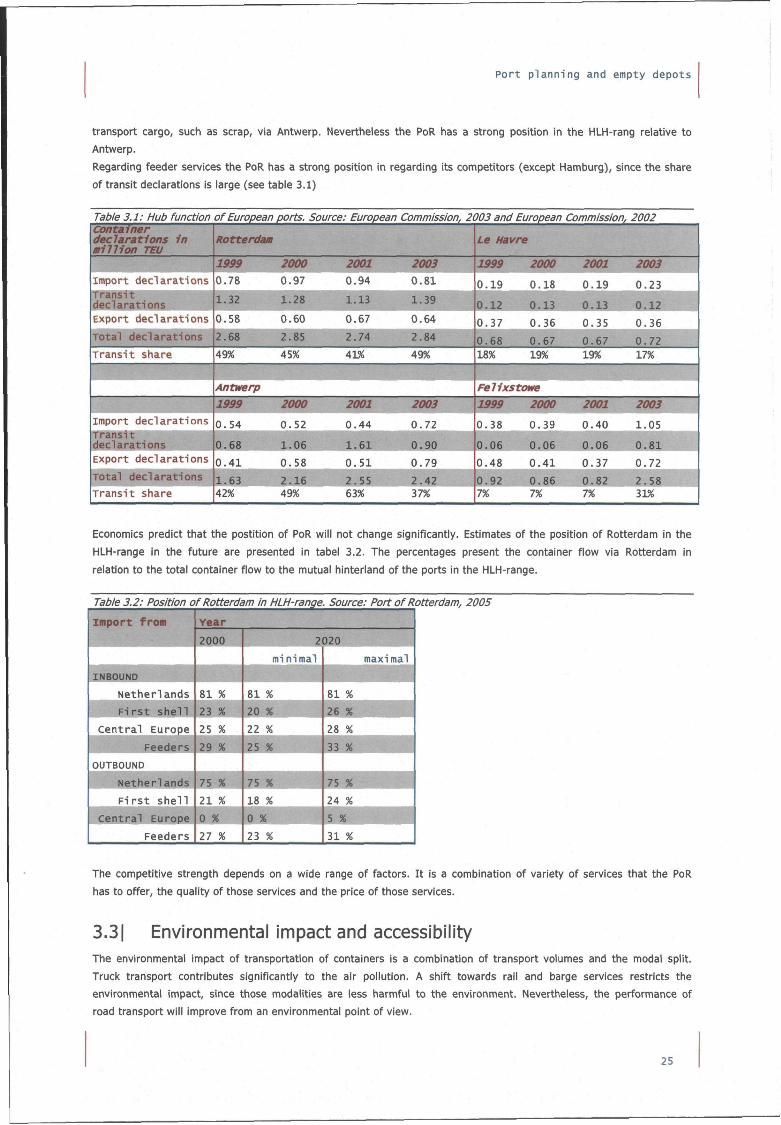

TABLE 3 . 1 : HUB FUNCTION OF EUROPEAN PORTS. SOURCE: EUROPEAN COMMISSION, 2003 AND EUROPEAN COMMISSION,

2002 25

TABLE 3.2: POSITION OF ROTTERDAM I N HLH-RANGE. SOURCE: PORT OF ROTTERDAM, 2005 25

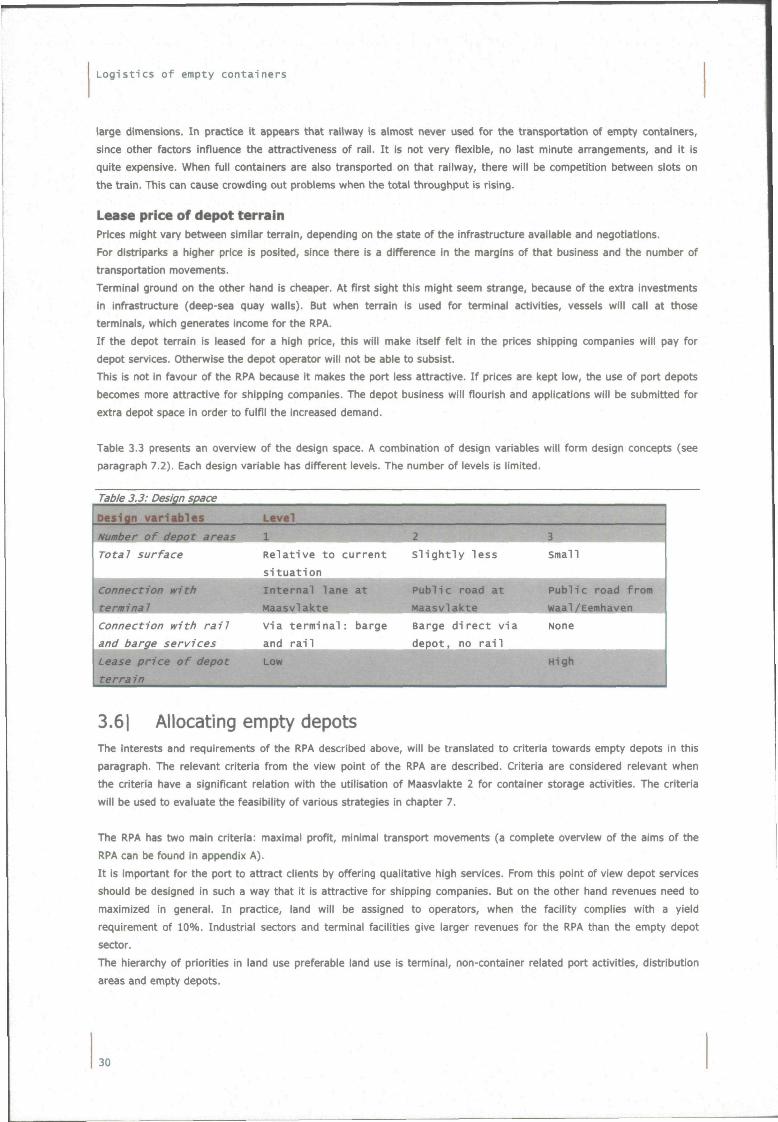

TABLE 3.3: DESIGN SPACE 30

TABLE 4 . 1 : SHARE OF MERCHANT HAULAGE 36

TABLE 4 .2 : DESTINATIONS OF TRUCKS WITH EMPTY CONTAINERS WITH AN EMPTY DEPOT AS ORIGIN (SOURCE:

ADVIESBUREAU VAN RHOON, 2000) 50

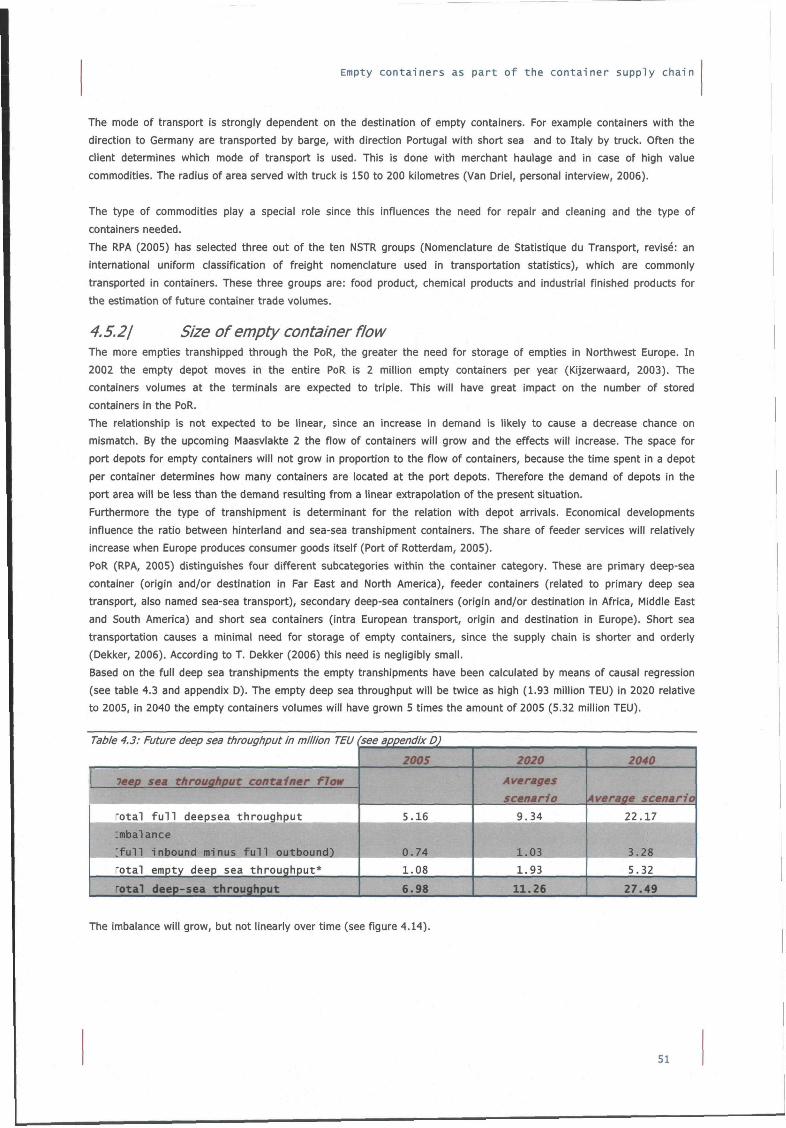

TABLE 4 .3 : FUTURE DEEP SEA THROUGHPUT I N MILLION TEU (SEE APPENDIX D ) 51

TABLE 5 . 1 : ACTIVITIES DURING A CONTAINER CYCLE (SOURCE: R O I , 2002) 60

TABLE 5.2: OPTIONS IN CASE OF SURPLUS OR DEFICIT (ADAPTED FROM LOPEZ, 2003) 61

TABLE 6 . 1 : LONG TERM DEMAND FOR SPACE FOR EMPTY STORAGE AT M V 2 (SOURCE; PORT OF ROTTERDAM, 2005) 70

TABLE 7 . 1 : ADVANTAGES AND DISADVANTAGES REFERENCE DESIGN 80

TABLE 7.2; ADVANTAGES AND DISADVANTAGES 'FAR I N FAR OUT' CONCEPT 81

TABLE 7.3: ADVANTAGES AND DISADVANTAGES TERMINAL BUFFER' CONCEPT 82

TABLE 7.4: ADVANTAGES AND DISADVANTAGES 'MAXIMAL SURFACE' CONCEPT 82

TABLE 7.5: ASSESSMENT FRAMEWORK 83

TABLE 7.6: CAPACITY DISTRIBUTION PER CONCEPT 84

TABLE 7.7 FUTURE DEPOT ARRIVALS I N MILLION TEU 84

TABLE 7.8: TRANSPORT PERFORMANCE PER CONCEPT I N MILLIONTEUKILOMETRES ( INCL. HINTERLAND AREA) 85

TABLE 7.9: TRANSPORT PERFORMANCE PER CONCEPT I N MILLIONTEUKILOMETRES (EXCL. HINTERLAND AREA) 85

TABLE 7.10: POSSIBIUTIES FOR COMBINING TRIPS PER CONCEPT 86

TABLE 7 . 1 1 : FUTURE MODAL SPLIT OF EMPTY CONTAINERS AT DEPOTS (SEE APPENDIX P) 86

TABLE 7.12: OPPORTUNITY COSTS PER CONCEPT 87

TABLE 7.13: SCORECARD 87

TABLE 7.14: ASSESSMENT BY RPA 87

TABLE 7.15: ASSESSMENT BY SHIPPING COMPANIES 88

TABLE 7.16; ASSESSMENT BY SHIPPING COMPANIES 88

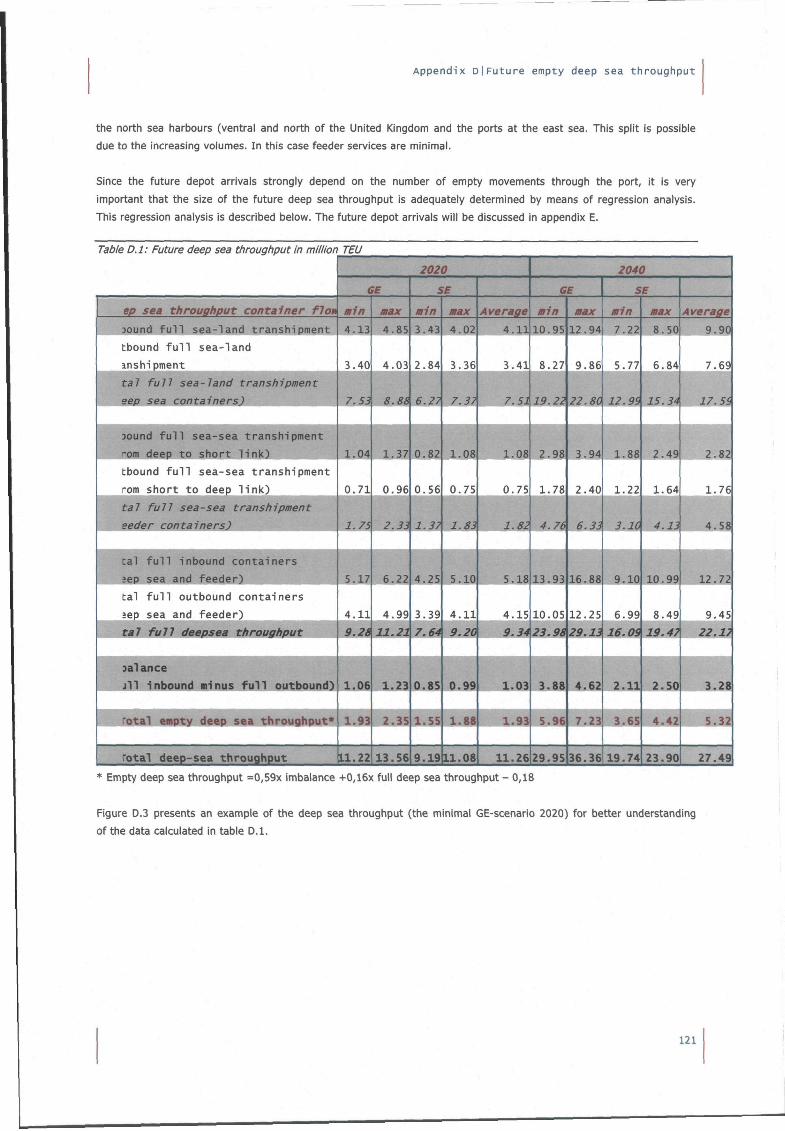

TABLE D . l : FUTURE DEEP SEA THROUGHPUT I N MILLION TEU 121

T A B L E D . 2 : HISTORICAL DATA I N TEU (SOURCE: DEKKER (2006)) 123

TABLE D . 3 : RESULTS REGRESSION ANALYSIS 123

TABLE D.4 :EMPTY SEA-LAND AND SEA-SEA TRANSHIPMENTS 123

TABLE E . l ; EMPTY CONTAINER TRAJECTORY DISTRIBUTION 126

TABLE E.2: DEPOT ARRIVALS PER TRAJECTORY I N MILLION TEU I N 2005 127

TABLE L . l : CALIBRATION OF E-VALUE 149

TABLE L.2; DEPOT TERRAIN REQUIRED I N GE-SCENARIO 2020 150

TABLE M . l : FUTURE DEPOT ARRIVALS PER TRAJECTORY I N MILLION TEU 151

TABLE M . 2 : FUTURE RANGE OF DEPOT ARRIVALS PER TRAJECTORY I N MILLIONTEU 152

TABLE O . l : FUTURE DEPOT ARRIVALS PER TRAJECTORY 157

TABLE 0 .2 : FUTURE DEPOT ARRIVALS PER DEPOT PER CONCEPT I N MILLION TEU 158

TABLE 0 .3 : DISTANCES BETWEEN ORIGIN AND DESTINATION VIA DEPOTS I N KILOMETRES 159

TABLE 0 . 4 : TRANSPORT PERFORMANCE PER CONCEPT I N MILLIONTEUKILOMETRES I N 2020 160

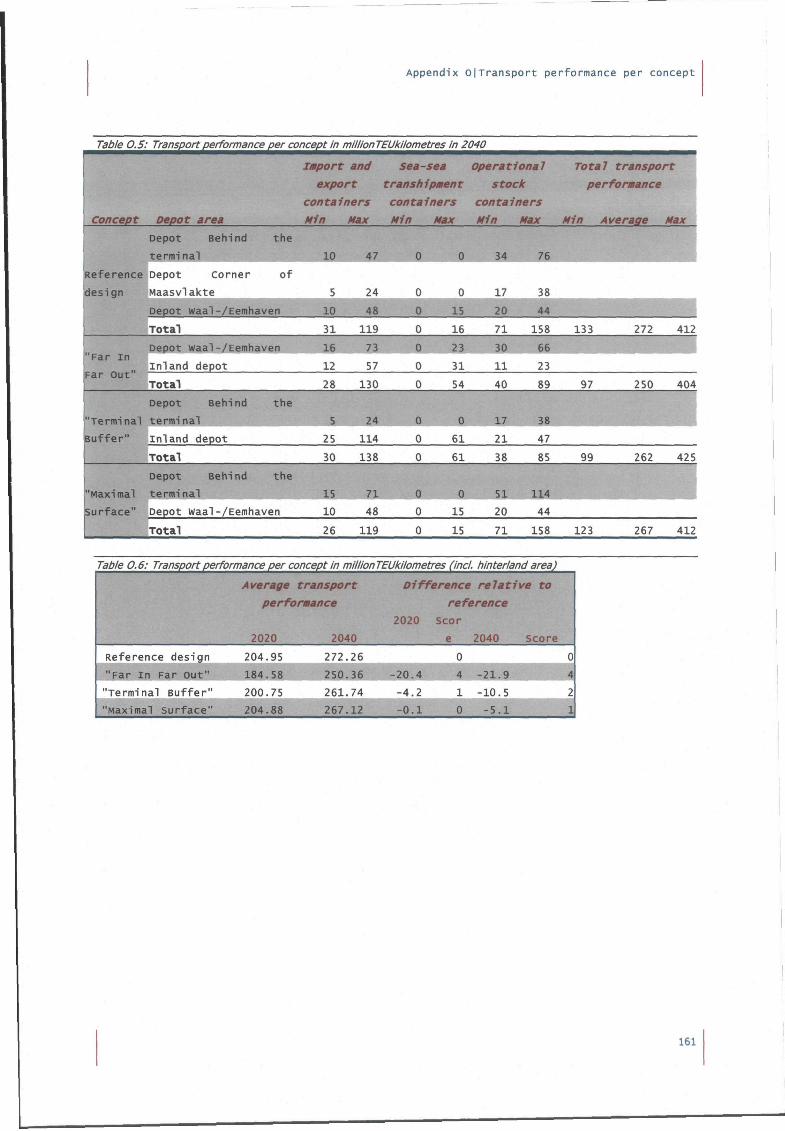

TABLE 0 .5 : TRANSPORT PERFORMANCE PER CONCEPT I N MILLIONTEUKILOMETRES I N 2040 161

TABLE 0 .6 : TRANSPORT PERFORMANCE PER CONCEPT I N MILLIONTEUKILOMETRES ( INCL. HINTERLAND AREA) 161

7

L o g i s t i c s o f empty c o n t a i n e r s

TABLE 0 . 7 : DISTANCES BETWEEN ORIGIN AND DESTINATION VIA DEPOTS I N KILOMETRES I N THE PORT AREA 163

TABLE 0 .8 : TRANSPORT PERFORMANCE PER CONCEPT I N MILUONTEUKILOMETRES I N PORT AREA (EXCL. HINTERLAND AREA)

163

TABLE P . l : MODAL SPLIT PER AREA OF ALL CONTAINERS (FULL AND EMPTY) 164

TABLE P.2: FUTURE MODAL SPLIT OF EMPTY CONTAINERS AT DEPOTS 164

TABLE P.3: FUTURE MODAL SPLIT OF EMPTY CONTAINERS AT DEPOTS 165

TABLE P.4: FUTURE MODAL SPLIT OF EMPTY CONTAINERS AT DEPOTS 166

TABLE Q . l : CONTAINER FLOWS THROUGH THE PORT (SOURCE: REAUSE, 2004) 167

8

11 Introduction on empty container logistics

This research will focus on the strategy of the Rotterdam Port Authority for allocating empty depots in the Port of

Rotterdam a long time scale. The strategy will be on a conceptual level and will not contain design specifications on

terrain details (such as quay wall dimensions), but focusses on the size of the total depot terrain at various areas of

the Port of Rotterdam and its general characteristics, which can be determined by the Rotterdam Port Authority.

Therefore the issue of empty container and its economic and social context will be introduced first. Subsequently

several points of interest regarding the spatial planning of empty depots, will be brought up, with the purpose of

formulating the fundamental research objective, which underlies this thesis.

More than fifty years ago a trucker from rural North Carolina ran an experiment that forever altered international trade

and the global economy (ITS library, 2006). The trucker, named Malcom McLean, developed the first metal loading

unit, now better known as the marine container. Based on the current worldwide use of containers for cargo transport,

it can be concluded that the marine container has proved its efficiency.

A marine container (as from here container) is a re-usable packaging for cargo, that is being transported overseas.

Cargo flows vary in time and in space, due to fluctuations in trade. A structural inequity in cargo flows between two

points, where the flow in one direction is exceeding the flow in the opposite direction, is known as an imbalance of

tradelanes. Hence cargo has to be matched with empty containers in a dynamic market. Due to uncertainty, this

process often results in a certain mismatch between containers and cargo, which leaves containers empty at e.g. port

areas.

Carriers cannot afford a large build-up of idle containers, as the 'dead' handling costs and storage costs progressively

cut into their profitability. Moreover the empty containers occupy valuable port space. The question then rises: "What

to do with empty containers?"

The presence of many empty containers in the Rotterdam area Is part of the background for this research. Empty

containers are stored at so called empty depots. Motives for storing an empty container concern the time involved in

making a decision about the need to transport the empty container to a certain region with a cargo surplus and the

time needed for organising the operations involved.

A more specific issue of this research is the storage space, which empty marine containers will use at Maasvlakte 2 at

the Port of Rotterdam (from here the port of

Rotterdam itself, i.e. not the Authority, will be

referred to as PoR) in the future. Maasvlakte 2 is

the new port and industrial zone that is to be built

in the North Sea as part the PoR (see Box 1).

The difficulty within port planning is to allocate

empty depots at Maasvlakte 2. The spatial planning

of empty depots has a strong relation with the

number and type of transport movements with

empty containers. The environmental and

accessibility effects of these movements are of

societal relevance.

Due to the increase in scale, supported by the development of Maasvlakte 2, the flow of containers to and from the

PoR will increase. This, in combination with an imbalance in trade flows, which causes a significant surplus of empty

containers in North-West Europe, increases the number of empty containers handled at the PoR. Although it is likely

that there will be an increase in the demand for depot terrain, the effects of the growing number of empty containers

on the demand for storage and the accompanying transportation movements need thorough investigation,

9

"Rotterdam is creating

European location for port activities and

industries in the North Sea, linking

directly to the current port and

industrial zone. Maasvlakte 2 encompasses

some 1,000 hectares of industrial sites,

immediately adjacent to deep waters.

container transshipment, distribution and

the chemical industry will all find ample

Box 1: Maasvlakte 2. (Source: Maasvlakte 2 Project

Organization, 2006)

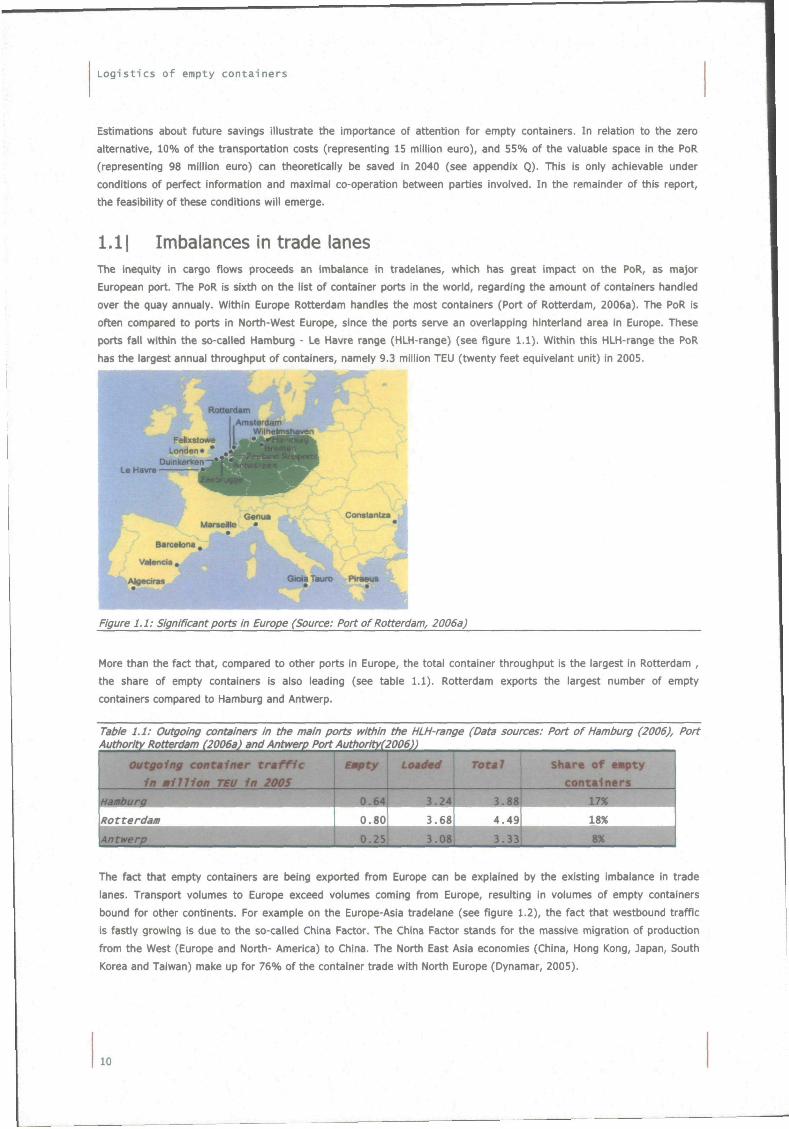

Logistics of empty containers

Estimations about future savings illustrate the importance of attention for empty containers. In relation to the zero

alternative, 10% of the transportation costs (representing 15 million euro), and 55% of the valuable space in the PoR

(representing 98 million euro) can theoretically be saved in 2040 (see appendix Q). This is only achievable under

conditions of perfect information and maximal co-operation between parties Involved. In the remainder of this report,

the feasibility of these conditions will emerge.

1.11 Imbalances in trade lanes The inequity in cargo flows proceeds an imbalance in tradelanes, which has great impact on the PoR, as major

European port. The PoR is sixth on the list of container ports in the world, regarding the amount of containers handled

over the quay annualy. Within Europe Rotterdam handles the most containers (Port of Rotterdam, 2006a). The PoR Is

often compared to ports in North-West Europe, since the ports serve an overlapping hinterland area in Europe. These

ports fall within the so-called Hamburg - Le Havre range (HLH-range) (see figure 1.1). Within this HLH-range the PoR

has the largest annual throughput of containers, namely 9.3 million TEU (twenty feet equlvelant unit) in 2005.

Figure 1.1: Significant ports in Europe (Source: Port of Rotterdam, 2006a)

More than the fact that, compared to other ports In Europe, the total container throughput is the largest in Rotterdam ,

the share of empty containers is also leading (see table 1.1). Rotterdam exports the largest number of empty

containers compared to Hamburg and Antwerp.

Table 1.1: Outgoing containers in the main ports within the HLH-range (Data sources: Port of Hamburg (2006), Port Authority Rotterdam (2006a) and Antwerp Port Authority(2006))

outgoing container traffic

in million TEU In 2005

^^^^m. ^ ^ H Rotterdam

Aattne^^^^^^^^^^^^^^^^M

emty

imi_ o.so • •

Loaded

nm^ 3.68

HHB

Total

m^gg 4.49

Shmre of eiipty

containers

^ f t 17% ^ H 18X 1

^^^^^^HM The fact that empty containers are being exported from Europe can be explained by the existing imbalance in trade

lanes. Transport volumes to Europe exceed volumes coming from Europe, resulting in volumes of empty containers

bound for other continents. For example on the Europe-Asia tradelane (see figure 1.2), the fact that westbound traffic

is fastly growing is due to the so-called China Factor. The China Factor stands for the massive migration of production

from the West (Europe and North- America) to China. The North East Asia economies (China, Hong Kong, Japan, South

Korea and Taiwan) make up for 76% of the container trade with North Europe (Dynamar, 2005).

10

In t roduct ion on empty container l o g i s t i c s

Europe - Far East trade

12.000.000

10.000.000

8.000.000

^ 6.000.000

4.000.000

2.000.000

0

I Westbound Far East-Med/Europe (TEU)

I Eastbound Med/Europe - Far East (TEU)

Year

Figure 1.2: Europe - Eastern Asia trade (Data source: Dynamar, 2005) (N.B. At the time of writing there are no exact

data available about 2005, only estimates)

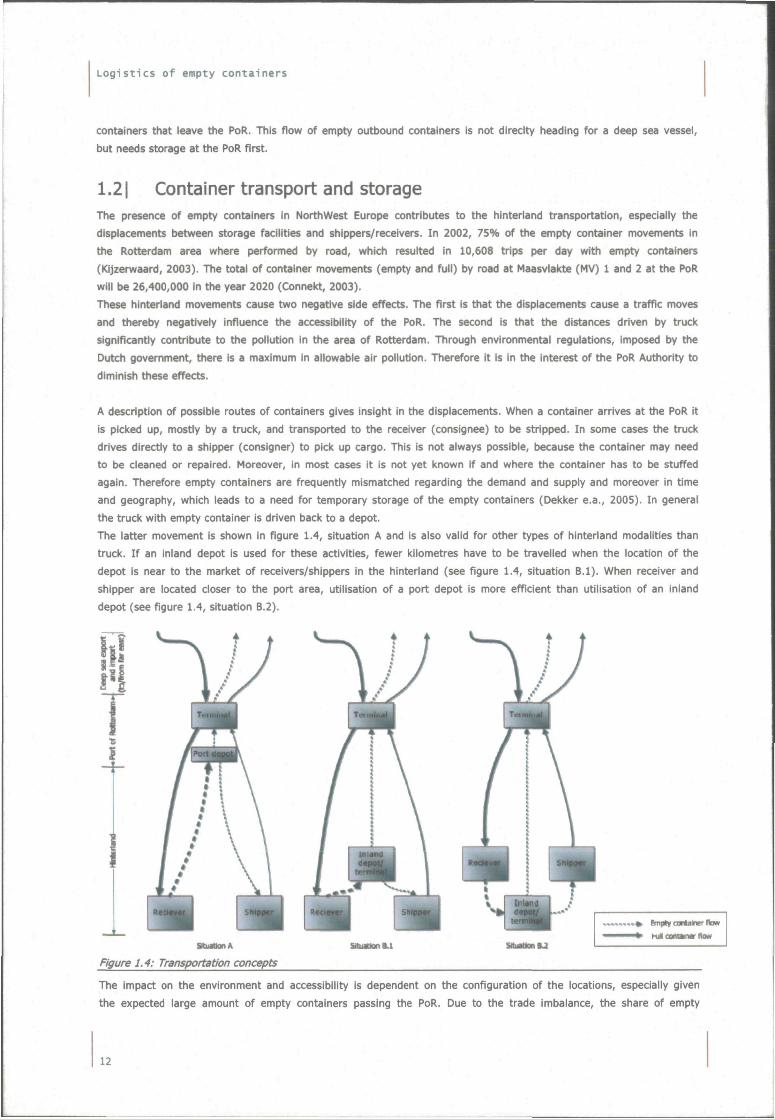

Within the global East-West trade three main routes of container traffic around the world can be distinguished, namely

transatlantic traffic (between America and Europe), transpacific traffic (between Far East and America) and the North

Europe/Mediterranean - Far East traffic. The imbalance in trade lanes is the biggest for the latter two (Dynamar,

2005). This is illustrated in figure 1.3.

\i. America - E. Asi

Figure 1.3: Container transport volumes in major east-west trade lanes (million TEU), 2005 (Data source:

Containerisation international, april 2006)

Based on economic forecasts it is likely that this pattern will last for at least the coming decades (Konings, 2005a). In

2005, the deep-sea throughput of the PoR was approximately 6 million TEU, of which 1 million TEU was empty. In

2020, the deep-sea throughput will be on average 11 million TEU of which 2 million empty and in 2040 27 million TEU

of which 5 million empty (see appendix D).

Since Rotterdam is the main container port of Northwest Europe, the effect of the imbalance in international trade

lanes in the PoR is severe and is likely to grow according to the mentioned economic forecasts. At this moment, in the

hinterland of PoR there is already a significant surplus of empty containers. There is a rather great amount of empty

11

Logistics of empty containers

containers that leave the PoR. This flow of empty outbound containers is not direclty heading for a deep sea vessel,

but needs storage at the PoR first.

1.21 Container transport and storage The presence of empty containers in Northwest Europe contributes to the hinterland transportation, especially the

displacements between storage facilities and shippers/receivers. In 2002, 75% of the empty container movements in

the Rotterdam area where performed by road, which resulted In 10,608 trips per day with empty containers

(Kijzerwaard, 2003). The total of container movements (empty and full) by road at Maasvlakte (MV) 1 and 2 at the PoR

will be 26,400,000 in the year 2020 (Connekt, 2003).

These hinterland movements cause two negative side effects. The first is that the displacements cause a traffic moves

and thereby negatively influence the accessibility of the PoR. The second is that the distances driven by truck

significantly contribute to the pollution in the area of Rotterdam. Through environmental regulations, imposed by the

Dutch government, there is a maximum in allowable air pollution. Therefore it is in the interest of the PoR Authority to

diminish these effects.

A description of possible routes of containers gives insight in the displacements. When a container arrives at the PoR It

is picked up, mostly by a truck, and transported to the receiver (consignee) to be stripped. In some cases the truck

drives directly to a shipper (consigner) to pick up cargo. This Is not always possible, because the container may need

to be cleaned or repaired. Moreover, in most cases it is not yet known if and where the container has to be stuffed

again. Therefore empty containers are frequently mismatched regarding the demand and supply and moreover in time

and geography, which leads to a need for temporary storage of the empty containers (Dekker e.a., 2005). In general

the truck with empty container is driven back to a depot.

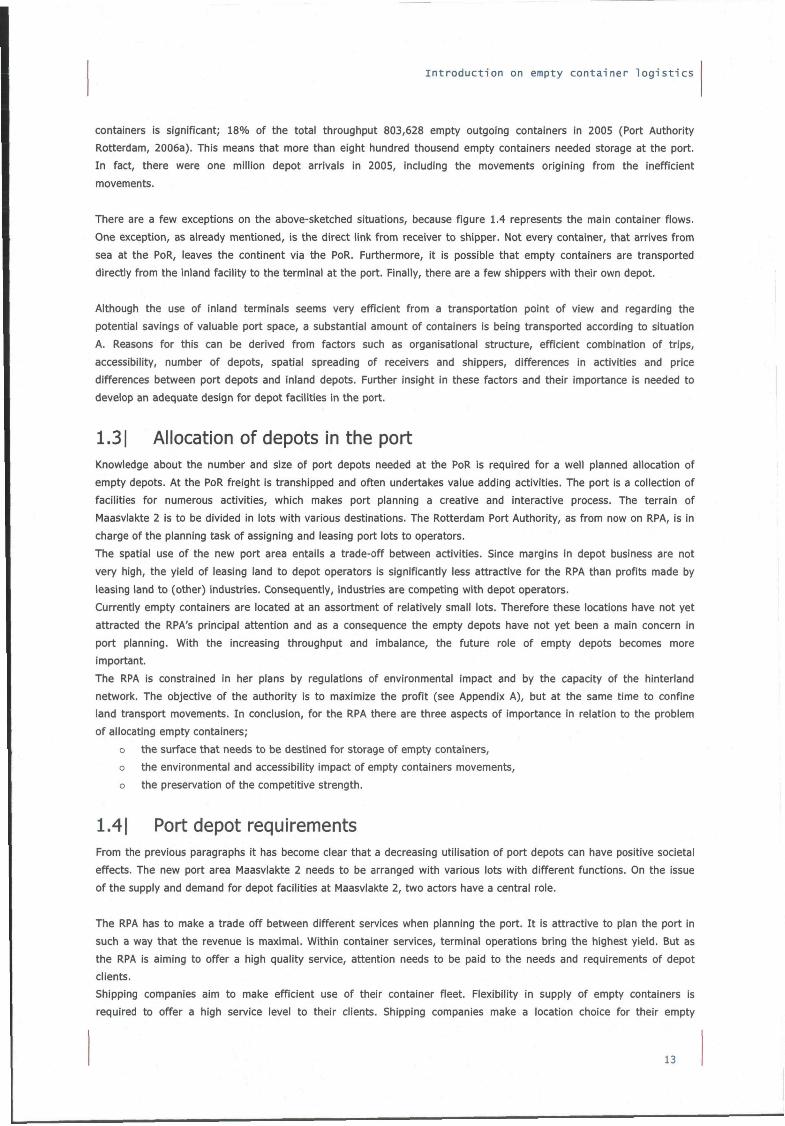

The latter movement is shown in figure 1.4, situation A and is also valid for other types of hinterland modalities than

truck. If an inland depot is used for these activities, fewer kilometres have to be travelled when the location of the

depot is near to the market of receivers/shippers in the hinterland (see figure 1.4, situation B.l). When receiver and

shipper are located closer to the port area, utilisation of a port depot is more efficient than utilisation of an inland

depot (see figure 1.4, situation B.2).

f (

SltuattanA

Figure 1.4: Transportation concepts

Silu«kinB.l SttuMicnU

The impact on the environment and accessibility is dependent on the configuration of the locations, especially given

the expected large amount of empty containers passing the PoR. Due to the trade imbalance, the share of empty

12

introduction on empty container logistics

containers is significant; 18% of the total throughput 803,628 empty outgoing containers in 2005 (Port Authority

Rotterdam, 2006a). This means that more than eight hundred thousend empty containers needed storage at the port.

In fact, there were one million depot arrivals in 2005, including the movements origining from the inefficient

movements.

There are a few exceptions on the above-sketched situations, because figure 1.4 represents the main container flows.

One exception, as already mentioned, is the direct link from receiver to shipper. Not every container, that arrives from

sea at the PoR, leaves the continent via the PoR. Furthermore, it is possible that empty containers are transported

directly from the inland facility to the terminal at the port. Finally, there are a few shippers with their own depot.

Although the use of inland terminals seems very efficient from a transportation point of view and regarding the

potential savings of valuable port space, a substantial amount of containers is being transported according to situation

A. Reasons for this can be derived from factors such as organisational structure, efficient combination of trips,

accessibility, number of depots, spatial spreading of receivers and shippers, differences in activities and price

differences between port depots and inland depots. Further insight in these factors and their importance is needed to

develop an adequate design for depot facilities in the port.

1.31 Allocation of depots in the port Knowledge about the number and size of port depots needed at the PoR is required for a well planned allocation of

empty depots. At the PoR freight is transhipped and often undertakes value adding activities. The port is a collection of

facilities for numerous activities, which makes port planning a creative and interactive process. The terrain of

Maasvlakte 2 is to be divided in lots with various destinations. The Rotterdam Port Authority, as from now on RPA, is in

charge of the planning task of assigning and leasing port lots to operators.

The spatial use of the new port area entails a trade-off between activities. Since margins in depot business are not

very high, the yield of leasing land to depot operators is significantly less attractive for the RPA than profits made by

leasing land to (other) industries. Consequently, industries are competing with depot operators.

Currently empty containers are located at an assortment of relatively small lots. Therefore these locations have not yet

attracted the RPA's principal attention and as a consequence the empty depots have not yet been a main concern in

port planning. With the increasing throughput and imbalance, the future role of empty depots becomes more

important.

The RPA is constrained in her plans by regulations of environmental impact and by the capacity of the hinteriand

network. The objective of the authority is to maximize the profit (see Appendix A), but at the same time to confine

land transport movements. In conclusion, for the RPA there are three aspects of importance in relation to the problem

of allocating empty containers;

o the surface that needs to be destined for storage of empty containers,

o the environmental and accessibility impact of empty containers movements,

o the preservation of the competitive strength.

1.41 Port depot requirements From the previous paragraphs it has become clear that a decreasing utilisation of port depots can have positive societal

effects. The new port area Maasvlakte 2 needs to be arranged with various lots with different functions. On the issue

of the supply and demand for depot facilities at Maasvlakte 2, two actors have a central role.

The RPA has to make a trade off between different services when planning the port. It is attractive to plan the port in

such a way that the revenue is maximal. Within container services, terminal operations bring the highest yield. But as

the RPA is aiming to offer a high quality service, attention needs to be paid to the needs and requirements of depot

clients.

Shipping companies aim to make efficient use of their container fleet. Flexibility in supply of empty containers is

required to offer a high service level to their clients. Shipping companies make a location choice for their empty

13

Logistics of empty containers

containers based on their requirements regarding depot services. The depot services themselves are being excecuted

by the depot operator, which is not a main but a facilitating task. Shipping companies use a forecasting system for the

demand for empty containers by their clients, the containers are repositioned at an interregional level. By creating a

safety stock, the inventory levels can be controlled. Through their empty positioning strategy, shipping companies have

the biggest Influence on the utilisation of empty depots at the port amongst other parties, which are involved In the

supply chain. Indirect clients of the port depots are the transport operators, who aim at efficient use of their vehicle

fleet.

The RPA prefers to use the available space in the port for other port related commercial activities than depots, because

this is more lucrative for the authority. Requirements for port depots are a small part of the total port planning

activities. The logistics of empty containers, requires storage at various places, amongst which port depots. In the

current situation shipping companies prefer to have containers in a buffer located at port depots. Empty containers

need to be within reasonable reach in order to be able to supply exporting companies. An inadequate facility of storage

possibilities could be a threat to the competitive position of the PoR.

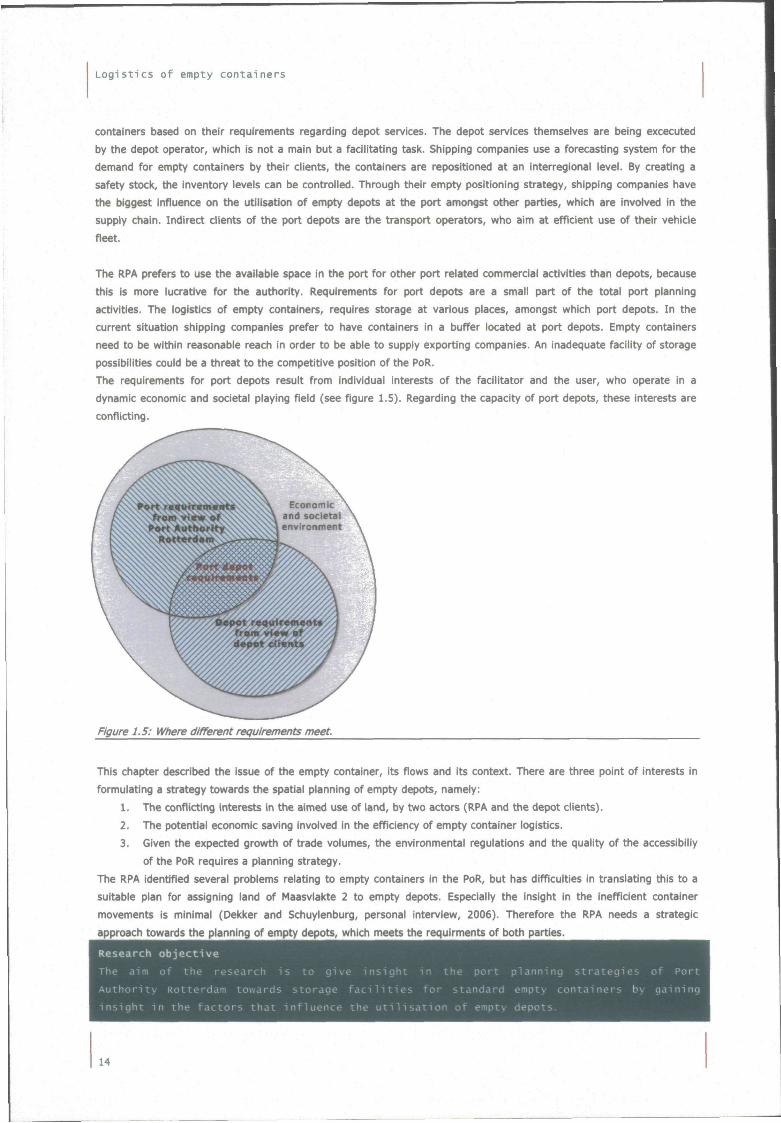

The requirements for port depots result from individual interests of the facilitator and the user, who operate in a

dynamic economic and societal playing field (see figure 1.5). Regarding the capacity of port depots, these interests are

conflicting.

Figure 1.5: Where different requirements meet.

This chapter described the issue of the empty container. Its flows and Its context. There are three point of Interests in

formulating a strategy towards the spatial planning of empty depots, namely:

1. The conflicting interests in the aimed use of land, by two actors (RPA and the depot clients).

2. The potential economic saving involved in the efficiency of empty container logistics.

3. Given the expected growth of trade volumes, the environmental regulations and the quality of the accessibiliy

of the PoR requires a planning strategy.

The RPA identified several problems relating to empty containers in the PoR, but has difficulties in translating this to a

suitable plan for assigning land of Maasvlakte 2 to empty depots. Especially the insight in the inefficient container

movements is minimal (Dekker and Schuylenburg, personal Interview, 2006). Therefore the RPA needs a strategic

approach towards the planning of empty depots, which meets the requirments of both parties.

Research objective

The aim of the research is to give insight in the port planning strategies of Por-:

Authority Rotterdam towards storage facilities for standard empty containers by gaininq Authority Rotterdam towards storage facilities for sta

insight in the factors that influence the utilisation of

14

21 Research frameworic

Justifications for methodological choices will be given in this chapter. First other studies within the field of empty

container logistics will be discussed. Next the scope of this research will be discussed. Followed by the research

questions, methods and a bookmark.

2.11 Literature Several studies have elaborated the logistics of containers. Most studies are concerned with loaded containers because

of their valuable contents.

Empty containers are often perceived as a side product of less importance. For example, De Hengst Bruggeling (1999)

elaborates in the coordination of information between organisations, but demarcates the problem to loaded containers.

But, as clarified in the previous chapter, since their expected increase the logistics of empty containers will involve

more and more costs, a bigger burden on port accessibility and in this case exceed limiting governmental regulations.

Therefore, there is a need to understand and thereby be able to steer logistics of empty containers.

Although literature about empty container logistics exists, their relation with port planning strategies has not yet been

thoroughly investigated. In this respect, the work of Vasiliauskas and Bazaras (2006) forms a good illustration. They do

mention the inefficiency of empty containers transport, but do not discuss its relation to port planning strategies. Their

work analyses the current state of the world container market, describes problems related to empty container trips and

gives an overview of the latest technological developments of the containers in the EU.

In literature there are few studies, which discuss empty container management, by (mathematical) logistic

optimization. Those studies are written from the point of view of shipping companies, since they are the parties who

manage the empty containers.

There are studies concentrating on the decision-making problem of optimal routing and minimal idle time of empty

containers from an algorithmic viewpoint (e.g. Lago (2003), Erera e.a. (2006), Coong e.a. (2002)).

Powell e.a. (2003) introduce the information aspects involved in the decision-making problem. Tioga (2002) continues

this line of thinking by designing an internet-based information system, which has a significant potential to ameliorate

the serious empty container problem Southern California is facing.

Debrito and Konings (2006) discuss other ways to diminish empty container transport and their need for storage by

applying the reverse logistics theory. This theory elaborates on drivers and possibilities for recovery of (empty)

containers.

The effects of the storage and movements of empty containers on the port accessibility have not been investigated

thoroughly before. Connekt (2003), Davies (2006) and van der Rakt (2003) investigated the truck handling for

Maasvlakte 2; these are unimodal approaches where movements to depots and distribution parks are handled as one

category. Notteboom (2004) uses a multimodal approach and focuses on functional roles of ports, but just briefly

brings up the specific empty container problem.

Furthermore there are studies elaborating on the empty container problem in specific regions, especially North

America, where the imbalance in trade lanes is also significant.

The research of Boilé (2006) analyzes the empty marine container accumulation problem, specific to the region of New

York and New Jersey and emphasizes on the complex relationships between players and stakeholders involved.

The situation in the USA differs from Europe, because of the difference in collaboration between parties and the

extensive use of rail (Van Driel, personal interview, 2006). The empty container problem in Europe cannot directly be

compared to the situation in the USA.

15

Logistics of empty containers

The RPA made an estimate of 625 hectare for the surface needed for transfer and storage of empty and full containers

on the Maasvlakte (Maasvlakte 2 Project Organization, 2006). The role of the PoR is to facilitate the logistics of

containers. The total surface needed for transfer and storage consists of different components, namely terminals,

distriparks and empty depots. According to T. Dekker (2006), research expert of the PoR, this is a rough estimate,

especially for part of the storage capacity at empty depots. While making this estimate, little attention was paid to the

functionality of empty depots relating to empty container logistics.

There has not been found a research with a multimodal approach, which elaborates on the effects of available storage

space at ports, and especially the PoR.

Many technical approaches involve merely the sub optimisation of container handling. For example within the field of

mechanical engineering, container logistics comprehends efficient container handling at terminals. A more integral and

a more broad approach are needed to optimise the complete supply chain of containers without displacements of

bottlenecks.

An integral approach is needed in order to balance the supply and demand for empty container storage in a feasible

manner. Therefore attention needs to be paid to the boundary conditions and the objectives of the two main actors at

the PoR. The emphasis will be on the storage of empty containers and their multimodal transport. The logistical system

and the economical and institutional environment will be taken into account, to map the factors affecting accumulation

of empty containers at the PoR. The following paragraph elaborates on this approach.

2.21 Scope Since there are different actors with minor consensus on the problem and because the context is dynamic, the issue

can be characterized as an ill-structured problem. A suitable way to approach this problem to give insight in the

background of the different interests and to use this in search for a feasible solution between the conflicting interests.

So a multiactor approach of the problem is needed. Furthermore a demarcation of the issue is necessary to focus on

the important aspects of the problem.

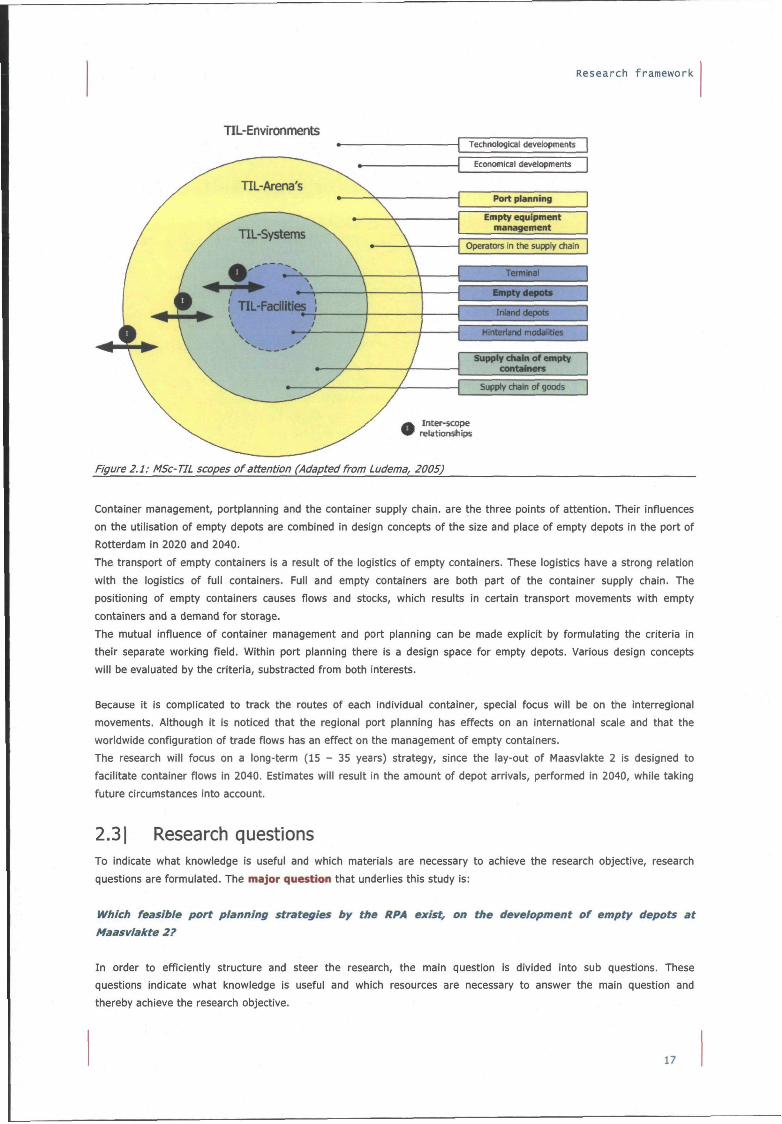

This research will approach the problem by taking notice of the interrelations between the different scopes. The scopes

of attention within the field of transport, infrastructure and logistics (TIL) are structured according to the TIL-model

(see figure 2.1).

The TIL-model consists of four elements; facilities, systems, arenas and environments. The middle-scope of attention

focuses on TIL-systems containing TIL-facilities and relates to the TIL-arena's. In relation to the above-sketched

problem the elements can be defined as follows:

• TIL-Facilities represent the physical infrastructure and the transportation modalities. The PoR can be considered as

a TIL-facillty, but the centre of attention within this research is the facility of empty depots. The empty container

itself is also considered to be a facility. The main type of containers are the standard dry containers.

• TIL-Systems represent physical and non-physical networks. The infrastructure is a physical network. The supply

chain of empty containers is a TIL-system. But since there is a strong relation between full and empty containers,

the total supply chain of containers cannot be neglected.

• TIL-Arenas represent the parties involved and their strategies and management. As mentioned in the previous

paragraph the shipping companies and the RPA are the main actors. From the point of view of shipping companies

the empty container management forms an important arena. On the other hand the port planning strategy is

important from the point of view of the RPA, where the confidential relationship with shipping companies should

be maintained.

• TIL-Environments are part of a larger economic and societal system. The performance of the PoR is of economic

relevance. The RPA used to be an public organisation, but was The external effects on the environment and

accessibility are of societal relevance. An important influence of the environment to the issue is the development

in trade, which determines the cargo flows.

16

Research framework

TIL-Environments Technological developinents

J Economical developments I

Port planning

Empty equipment management

Operators in the supply chain

Terminal

Empty depot*

Inland depots

Hinterland modalities

Supply chain ot empty containers

Supply chain of goods

Inter-smpe relationships

Figure 2.1: MSc-TIL scopes of attention (Adapted from Ludema, 2005)

Container management, portplanning and the container supply chain, are the three points of attention. Their influences

on the utilisation of empty depots are combined in design concepts of the size and place of empty depots in the port of

Rotterdam in 2020 and 2040.

The transport of empty containers is a result of the logistics of empty containers. These logistics have a strong relation

with the logistics of full containers. Full and empty containers are both part of the container supply chain. The

positioning of empty containers causes flows and stocks, which results in certain transport movements with empty

containers and a demand for storage.

The mutual influence of container management and port planning can be made explicit by formulating the criteria In

their separate working field. Within port planning there is a design space for empty depots. Various design concepts

will be evaluated by the criteria, substracted from both interests.

Because it is complicated to track the routes of each individual container, special focus will be on the interregional

movements. Although it is noticed that the regional port planning has effects on an international scale and that the

woridwjde configuration of trade flows has an effect on the management of empty containers.

The research will focus on a long-term (15 - 35 years) strategy, since the lay-out of Maasvlakte 2 is designed to

facilitate container flows in 2040. Estimates will result In the amount of depot arrivals, performed in 2040, while taking

future circumstances into account.

2.31 Research questions To indicate what knowledge is useful and which materials are necessary to achieve the research objective, research

questions are formulated. The major question that underlies this study is:

Which feasible port planning strategies by the RPA exist, on the development of empty depots at

Maasvlakte 2?

In order to efficiently structure and steer the research, the main question is divided into sub questions. These

questions indicate what knowledge is useful and which resources are necessary to answer the main question and

thereby achieve the research objective.

17

Logistics of empty containers

1. Which locations in the region of Rotterdam are appropriate for the storage of empty depots, on a large

timescale?

(What is the position of the RPA regarding the facilities of empty container storage?) (Chapter 3: Port planning)

a. What are the interests and the constraints of the RPA?

b. What is the decision-making ability of the RPA?

(What is the role of empty containers in the container supply chain?) (Chapter 4: Empty container supply chain)

c. What is the function of an empty depot?

d. What is the configuration of the container supply chain?

(What is the position of depot clients towards the storage of empty containers?) (Chapter 5: Empty container

management)

e. Which parties are depot clients?

f. What are the requirements and interests of the depot clients towards empty depots at the PoR?

2. How much empty depot terrain is needed in 2020 and 2040, at the PoR and especially at Maasvlakte 2?

(Chapter 6: Balance between port planning and empty container logistics)

a. Which estimations of depot terrain exist and how valuable are the estimates?

b. What are the causal factors of the utilisation of port depots?

c. What are the developments of these factors in the future?

d. What overall picture does this generate, regarding the future demand for depot terrain in the

Rotterdam region?

3. What are the interaction effects of the different design elements within the decision space? (Chapter 7:

Evaluation of design concepts)

a. Which concepts are representative within the boundaries of the decision-making space?

b. To what extend do those concepts comply with the interests of the users and the facilitator?

c. On which aspects should the Rotterdam Port Authority focus?

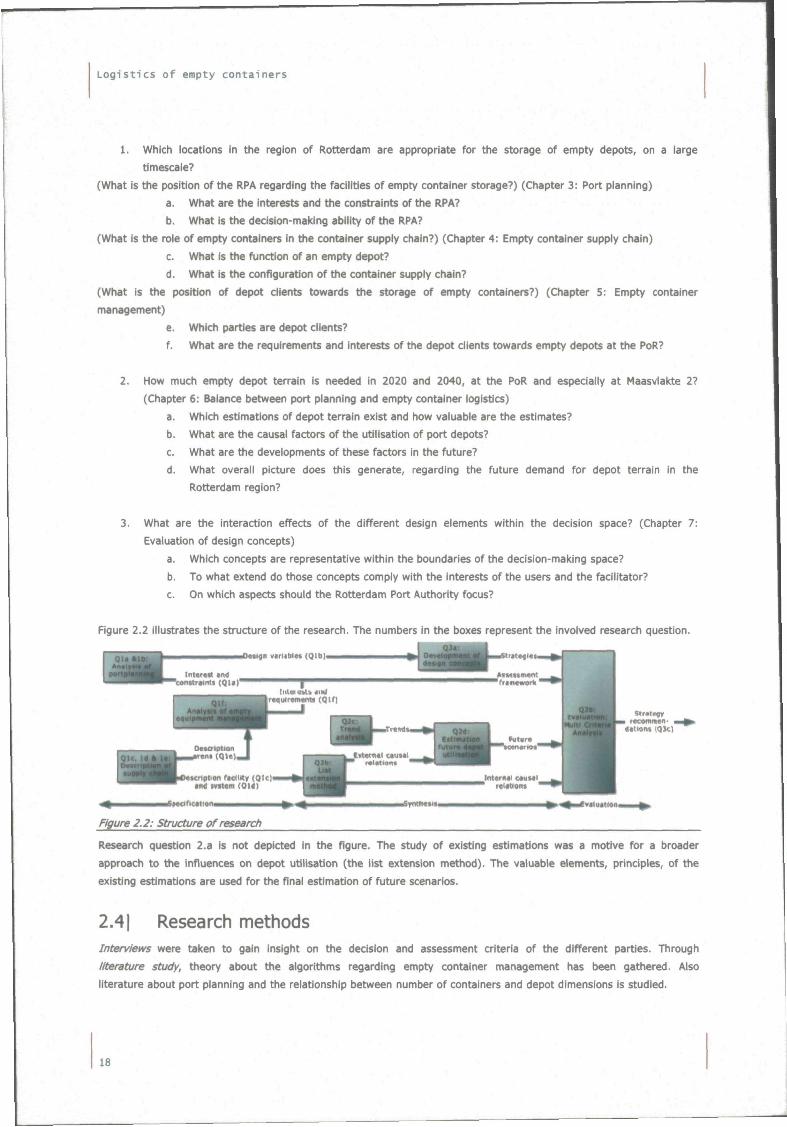

Figure 2.2 illustrates the structure of the research. The numbers in the boxes represent the involved research question.

Figure 2.2: Structure of research

Research question 2.a is not depicted in the figure. The study of existing estimations was a motive for a broader

approach to the influences on depot utilisation (the list extension method). The valuable elements, principles, of the

existing estimations are used for the final estimation of future scenarios.

2.41 Research methods Interviews were taken to gain insight on the decision and assessment criteria of the different parties. Through

literature study, theory about the algorithms regarding empty container management has been gathered. Also

literature about port planning and the relationship between number of containers and depot dimensions is studied.

18

Research framework

Based on the Information about port planning and the interviews different design concepts for the allocation of empty

depots in the PoR were set up, based on a morphological method. Furthermore a Ust extension method is applied to

identify the influencing factors on the utilisation of empty depots. The causal relations are used for identification of the

effects of design variables. Trend analysis is applied for revealing the development of external causal factors. Based on

the future conditions, the future depot arrivals is estimated. The combination of trend analysis and causality in

forecasting is also referred to as causal regression.

A suitable method to gain insight in different strategies is by evaluating different concepts with a multi criteria

analysis. This analysis fits a multi actor approach, since it has the possibility to asses solutions on various criteria from

several actors. A multi criteria decision-making (MCDM) method takes different criteria into account in a scientifically

justified way, while pointing out the final 'best' solution (Germis e.a., 2002). The steps in the process are the

following:

1. Which are reasonable solutions to the problem?

2. Which criteria are of importance on the position of the PoR?

3. Which weights can be assigned to the different criteria/what is the relative importance?

4. How do the different alternatives score on the various criteria?

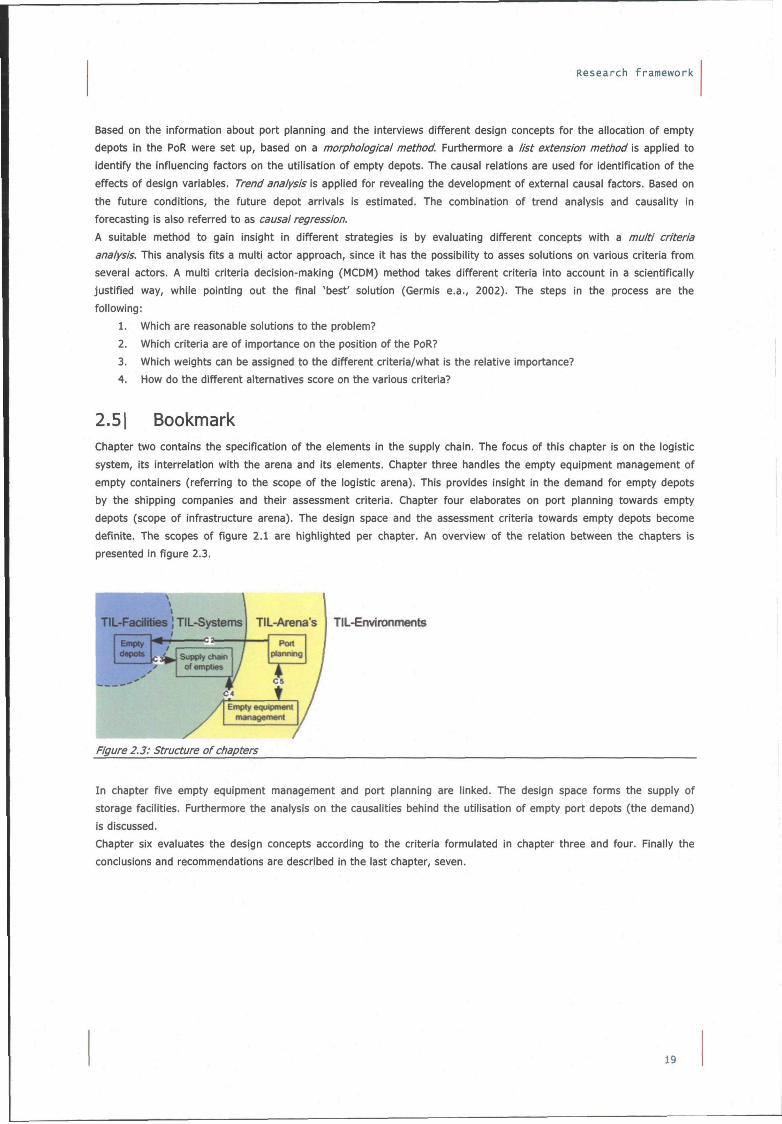

2.51 Bookmark Chapter two contains the specification of the elements in the supply chain. The focus of this chapter is on the logistic

system, its interrelation with the arena and its elements. Chapter three handles the empty equipment management of

empty containers (referring to the scope of the logistic arena). This provides insight in the demand for empty depots

by the shipping companies and their assessment criteria. Chapter four elaborates on port planning towards empty

depots (scope of infrastructure arena). The design space and the assessment criteria towards empty depots become

definite. The scopes of figure 2.1 are highlighted per chapter. An overview of the relation between the chapters is

presented in figure 2.3.

L-Facilities ] TIL-Systenis TIL-Arena's TIL-Environments

Empty depots C 3 ^ Supptychain

ofempiias

Port planning

T cs

t Empty aQulpaMnl

Figure 2.3: Structure of chapters

In chapter five empty equipment management and port planning are linked. The design space forms the supply of

storage facilities. Furthermore the analysis on the causalities behind the utilisation of empty port depots (the demand)

is discussed.

Chapter six evaluates the design concepts according to the criteria formulated in chapter three and four. Finally the conclusions and recommendations are described in the last chapter, seven.

19

Logistics of empty containers

20

31 Port planning and empty depots

The facilities and services provided by a port are services and facilities for ships, administrative formalities, cargo

transfer, services and facilities for cargo (e.g. cargo handling on ship and on quay transport to and from storage,

storage and warehousing) and additional value added services (Alderton, 2005). Storage, value adding services and

transport of empty containers is one part of the wide range of facilities and services provided by a port.

A port is a connection between seaside and landside operations. Besides the primary function of traffic node, other

activities are facilitates by ports, like industrial activities, often in relation to cargo flows or ship repair (Ligteringen).

According to Ligteringen this traffic function requires three conditions to be fulfilled; a good front door (accessibility

from sea), a good backdoor (hinteriand accessibility) and sufficient capacity in the port itself. Planning a port is a

creative and interactive process, since a lot of different facilities should be taken into account.

The RPA has an active role in the supply of depot terrain. The RPA has the objective to maximize the profit, but at the

same time to confine land transport movements. Minimum transport movements through the port are beneficial for

environment and accessibility.

Translating that objective to the allocation of the new port area results in a trade off between supporting activities

(like storage of empty containers, distriparks and partly terminal operations).

The incomes of the RPA consist of harbour dues and lease revenues. Lots with a quayside are very valuable for the RPA

since it also generates to harbour dues. Harbour dues are charged for the use by sea going vessels of the Rotterdam

harbours. For other land areas there is a trade off between activities other than terminal operations. In this way

industry is competing with depot operators. The relatively low margins in the depot business form a motive for the RPA

to reduce the surface of land dedicated to depot services.

The yield of leasing land to depot operators is significantly less attractive for the RPA than of leasing land to (other)

industries. Since empty containers are located at an assortment of relatively small lots, the empty depots do not have

right of way in the current port planning.

The modal split is important for the environmental effects of transport movements. The current modal split of empty

containers is approximately 55% via road, 10% via rail and 35% via barge. A substantial shift towards rail transport is

not to be expected, since rail is not enough flexible and because it is not feasible to realize sufficient rail connection

for the empty depots. A modal shift of empty container transport towards barge is inclined. The role of the RPA Is to

encourage the modal shift by supplying infrastructural necessities.

Not just the kilometres travelled with empty containers contribute to traffic flows, the kilometres travelled without any

container are also important. An efficient system ensures a high degree of utilisation. The better the possibility to

make combinations between trips, the better the utilisation of transport means and the less the chance of trips without

containers. Besides the yield of leasing land lots, transport performance and the modal split within the port area, the

combination of trips also forms a criterion. A depot, which is only accessible by truck, creates more than a million truck

movements per year (Dekker and Schuylenburg., personal interview 2006).

This chapter will specify the difficulties within port planning, regarding the empty container logistics (see figure 3.1).

TIL-Environnnents TIL-Fadlities | TIL-Systems

/ i i jpp iy t.tiLiin ^^^J / of empties ^ ^ T "

• ,.' ' /

TIL-Arena's

Port planning

/

Figure 3.1: Port planning scope

The first paragraph elaborates on the development of ports. In paragraph 3.1 the interest regarding the competitive

strength is discussed, followed by a paragraph on the environmental effects of empty container logistics (paragraph

3.3). The current planning policy, regarding empty depots is considered in paragraph 3.4. The criteria of the RPA are

21

Logistics of empty containers

formulated in paragraph 3.5. Next the possible design variables of the allocation of empty depots are presented in

paragraph 3.6. The chapter is concluded with a summarizing paragraph.

3.11 Port development Notteboom (2004) explains that there is a stage in port development, which he names port regionalisation. Port

regionalisation represents a stage in port development where efficiency is derived with higher levels of integration with

inland freight distribution systems. Containerisation, intermodallty and ICT enhance the spatial and functional

reconfiguration among iogistics nodes. The PoR is developing from port city to port network.

The new function of port terminals requires the elaboration of inland terminals to accommodate new port-Inland

linkages. The immense pressure on the collection and distribution networks, demands and promotes the development

of inland terminals. The implementation of the concept has affected trade flows, the routings between ports and

hinteriands and some traditional port functions.

In the regionalization phase iogistics chains have become the relevant scope of port competition. The success of a port

will depend on its capability to fit into the networks. The port community has to fully benefit from synergies with other

transport nodes and other players within the networks of which they are part.

In the tradition of the landlord port, it is presumed that port authorities should act as 'facilitators' in transport chains.

In general four types of port management can be distinguished; the privately owned and operated port, the landlord

fiort (publicly owned land, privately operated port services), the tool port (publicly owned land and port tools, privately

operated labour) and the service port (all services provided by public bodies) (Ecorys, 2005). The PoR is a landlord

port. This means that the RPA is responsible for the land subject, administration, development and maintenance of the

infrastructure. The RPA used to be a public institution, but transferred into private ownership in 2004. The land subject

concerns the assessment and contracting of terminals and in a later stage other operators, like depot operators (see

box 2).

six proposals for Maasvlakte 2

30 June 2006

te rminal

This week, the Port of Rotterdam Authority received six proposals from

companies and consortiums for a container terminal on Maasvlakte 2~. This 138

ha terminal, which will be the first to become operational on Maasvlakte 2. is

to be allocated via a so-called Open Assessment procedure. Separately from

this, the Port Authority last week concluded a contract with A P M Terminals for

the right to operate another terminal on Maasvlakte 2. These two ter

be opposite each other.

The large number of proposals confirms the great interest in Maasvlakte 2 as a

business location. The Port of Rotterdam Authority is now analysing the

proposals and, in this connection, will consult with the parties. They must

submit a final proposal at the end of September, after which negotiations will

be held with a selection of companies or consortiums. The Port Aut!

expects to sign a contract with the winner by mid 2007.

Next week, the Port Authority is expecting the tenders from the two contractor

consortiums for Maasvlakte 2. Any special requirements or wishes cont rvactor_s

and terminal operators might have can then be taken into account in the EIR and

pe rmi t procedu res.

•For the sake of completeness: Fourteen companies applied last year for this

Open Assessment Procedure. A number of them have formed consortiums in the

meantime. One of the six proposals made this week was from A P M Terminals. It

has been agreed that A P M Terminals will withdraw from this open Assessment

Procedure, but not until the terms and conditions referred to in the contract

(such as 'board approval') have been met.

BOX 2 Terminal proposals

22

Port planning and empty depots

The assessment procedure is open for every party. The plot and the dimensions of the terminal terrain are known.

Nevertheless the RPA formulated requirements regarding throughput volumes and environmental aspects (a.o. modal

split). An individual terminal operator has difficulties with the guarantee of throughput volumes, since they have

limited influence on container trade flows (van Dijk, personal interview, 2006). The used assessment procedures

stimulates the vertical integration of the supply chain.

The depot operators have little impact on the location of empty depots at MV2 (Schepen, personal interview, 2006).The

RPA and the shipping companies have the largest influences.

The growth of container volumes proceeding in stages and the relation between container terminals and depots makes

the planning process complicated. At the start, when a new terminal is operational, there is an overcapacity. The

available terminal space is then used for storage of empty containers (Borsodi, personal interview, 2006). Terminal

operators offer other depot services, e.g. they allow empty containers with a large dwell time. Therefore the empty