A PROJECT REPORT ON “LOAN MANAGEMENT SYSTEM” At DHANSHRI MULTI-STATE CO-OPERATIVE SOCIETIES BANK LTD, SOLAPUR. SUBMITTED BY MR. SURYAWANSHI S.SANDIP Under The Guidance Of • Prof. ASHWINI BARPUTE • SUBMITTED TO University of Pune in partial fulfillment of the requirement for the award of degree of Master of Business Administration Through • Jaywant Shikshan Prasarak Mandal, Nahre Technical Campus. Batch – 2014-15

LOAN MANAGEMENT SYSTEM

Dec 06, 2015

LOAN MANAGEMENT SYSTEM

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A

PROJECT REPORT

ON

“LOAN MANAGEMENT SYSTEM”

At

DHANSHRI MULTI-STATE CO-OPERATIVE SOCIETIES BANK LTD, SOLAPUR.

SUBMITTED BY

MR. SURYAWANSHI S.SANDIP

Under The Guidance Of

• Prof. ASHWINI BARPUTE

• SUBMITTED TO

University of Pune in partial fulfillment of the requirement for the

award of degree of Master of Business Administration

Through

• Jaywant Shikshan Prasarak Mandal,

Nahre Technical Campus.

Batch – 2014-15

DECLARATION

I SURYAWANSHI S SANDIP. MBA II YEAR Studying at JSPM Narhe Technical

Campus Pune hereby declare that the project report titled. “LOAN MANAGEMENT

SYSTEM” was carried by me in the partial fulfillment of MBA program under university of

Pune

This project is undertaken as part of the academic curriculum according to university

rules and norms, and has no commercial motive or interest. It is original work. It is not submitted

to any other organization to any other purpose.

Date:

Place: Pune

SURYAWANSHI S.SANDIP

MBA (Finance)

ACKNOWLEDGEMENT

• I take this opportunity of submitting this report to express my regards towards those who

offered their individual guidance in the hour of need.

• I sincerely acknowledge with deep sense of gratitude and indebtedness to Director of JSPM

narhe technical campus Pune DR. N.S Nehe and my internal guide Prof. Ashwini Barpute

who has guided me with valuable inputs throughout the project. He gave knowledgeable

insights about the topic, which helped e throughout the problems.

• I also would like to thank prof. shobha kalunge for giving me this opportunity to work

on this topic; it surely has given me insights into areas I was not much familiar earlier. I have

tried to share those insights with you in this report.

• This project was really worthwhile to work on because it encompassed all the learning for a

management student. Thus it provided a ground to implement what is learned and also

depicted the real tasks that have to be undertaken in the witty-gritty involved in the system

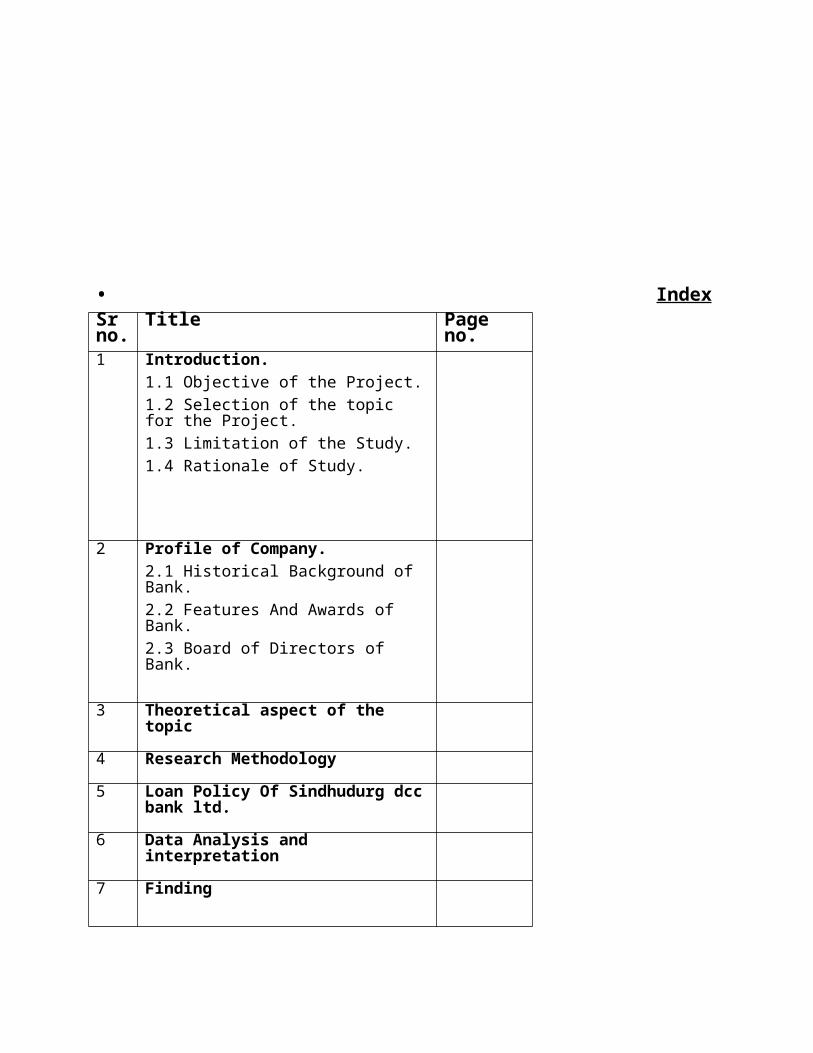

• IndexSr no.

Title Page no.

1 Introduction.

1.1 Objective of the Project.

1.2 Selection of the topic for the Project.

1.3 Limitation of the Study.

1.4 Rationale of Study.

2 Profile of Company.

2.1 Historical Background of Bank.

2.2 Features And Awards of Bank.

2.3 Board of Directors of Bank.

3 Theoretical aspect of the topic

4 Research Methodology

5 Loan Policy Of Sindhudurg dcc bank ltd.

6 Data Analysis and interpretation

7 Finding

8 Suggestion

9 Conclusion

10 Annexure

11 Bibliography

• EXECUTIVE SUMMARY

• EXECUTIVE SUMMARY

It’s a thing of massive gratification for me to present the Project Report on the topic “Study of

Loan Management System for Dhanshri Multi-state Co-operative Societies Bank Ltd. ”

I have deep interest in studying the loan procedure and system of credit risk management in

banking industry.

This project attempts to identify and know about loan sanctioning work and lending procedure in

Dhanshri Multi-state Co-operative Societies Bank Ltd. It also attempts to develop at least first

approach to these areas, to think through policies, principles, and practices to accomplish the

new tasks. By this practical training I am able to equip understanding, the thinking, the

knowledge, and the skills for today and also for tomorrow’s credit managerial work in financial

institutions.

Initially I was just having the bookish knowledge about all lending system, practices and

functions, but after doing this project, I got most of the practical knowledge. I have come to

know, what actually happens in the department of credit in banking industry.

Though it is not possible to have the information of all the spheres in market, in such a

very short period, but I tried to get more and more about all functions and practices applied in

practical working, I have particularly stresses on.

This study, complex as it is, has acquired new dimensions with the dynamic social

and technological changes of the past two decades. Changing trends, cultural diversity, more

educated work force and Awareness of rights and privileges have prompted a new look at the

entire organizational structures and systems.

After the study and analysis of various aspects about the system of Loan management

I have come to the various findings and observations regarding the actual data analysis which

have led me to the suggestions and recommendations which will help bank to improve its

position by reducing non-performing assets and lend money to increase profit position and status

of the bank.

I have studied Loan management system project in Dhanshri multi-state Co-Operative

Societies Ltd. through their financial statement of last 3 years. In 2012-13, 2013-14 & 2014-15

Deposits is high which a good sign is for the bank. It represents rapidly the increasing the

Deposites and comparively Loan. The amount sanctioned by bank as loan has shown gradual

increase year by year.

• Bank has to keep provision for its defaulter and N.P.A. it is up to 100% of loan amount

naturally it create financial burden on bank. The percentage of NPA is decreasing from year

2012 to 2013 which is good for the bank.

• CHAPTER 1

• INTRODUCTION

Introduction

I had complete project on”Loan Management System” at Dhanshri multi-state Co-operative

Societies bank ltd. Within two month. This project attempts to identify and know about loan

sanctioning work and lending procedure in Dhanshri multi-state Co-operative Bank Ltd. It also

attempts to develop at least first approach to these areas, to think through policies, principles, and

practices to accomplish the new tasks. By this practical training I am able to equip

understanding, the thinking, the knowledge, and the skills for today and also for tomorrow’s

credit managerial work in financial institutions.

Loan Policy is aimed at accomplishing its mission of retaining the bank's position as a

Premier Financial Services Group, with World class standards and significant global business,

committed to excellence in customer, shareholder and employee satisfaction and to play a

leading role in the expanding and diversifying financial services sector, while continuing

emphasis on its Development Banking role.

All the function of a modern bank, lending is for the most important. Advances

comprise very large portion of a bank’s structure.The strength of a bank is thus primarily judged

by the soundness of its advances. A wise & prudent policy in regard to advances is considered an

important factor inspiring confidence in the depositors & prospective customers of a bank. All

types of business activity including trade, industry and agriculture depend on bank finance in one

form or the other. Bank assists in creating more avenues of employment and thus helps raising

the standard of living of people.

1.1 Objectives of the project:-

To understand the various types of loan accounts, documents, terms & condition for the

sanctioning of loans.

• To analyse the loan sanctioning procedures of the applicants in Dhanshri multi-state Co-

operative Societies Ltd

• To identify the credit worthiness of the borrowers.

• To study disbursement and Loan recovery in Dhanshri multi-state Co-operative Societies Ltd

• To analyse the profit generation out of money lending for the bank.

• To identify the proportion of advances against deposits.

• To provide suggestions and recommendation for improvisation.

• 1.2 Selection of the topic for the project:-

• I have deep interest in studying the loan procedure and system of credit risk management

in banking industry.This project attempts to identify and know about loan sanctioning work

and lending procedure in Dhanshri multi-state Co-operative Societies Ltd.

• On the discussion with the management, of Dhanshri multi-state Co-operative Societies Ltd.

it is understood that the subject of Loan Management System has not been studied earlier &

bank needs to study the same.

• Bank also wants to know the actual position of Deposits and Loan policy.

• 1.3 Limitations of the Study:-

• Some data due to the purpose of secrecy was not disclosed by the bank.

• The main limitation of the research is the data source. The data is collected from the audited

financial statements, which are prepared on the historical cost basis.

• These financial statements are prepared at the end of the financial year. So, it gives a view on

particular date.

• There was time constraint & restriction on the part of management while giving specific

financial information.

• Some information is provided by the staff of the Ltd.

• 1.4 RATIOANLE OF THE STUDY

• Study of Loan System requirement helps to know the banking position about Deposit and

loan comparision yearly.

• Any money accepted as deposits must be for the purpose of lending or investments, making

advances & making investments of funds are equally important function. They are two main

sources of the bank.

• There are few general principles of good lending which every banker follows when

appraising an advance proposal.

• In a demand loan account, the entire amount is paid to the debtor at one time, either in cash

or by transfer to his savings bank or current account. No subsequent debit is ordinarily

allowed except by way of interest, incidental charges, insurance premiums, expenses incurred

for the protection of the security etc. Repayment is provided for by installment without

allowing the demand character of the loan to be affected in any way

• Efficient management of Loan System could enable the bank to reap the benefits as and when

their proportion of Deposits and Loans are good and also enable the bank to consolidate its

position in the market.

Chapter 2• PROFILE OF THE BANK

• PROFILE OF THE BANK:

• BANK AT A GLANCE

Name of The Bank : Dhanshri Multi-state Co-operative Societies Ltd

Registered and Central Office : Damaji road,mangalwedha,Dist.solapur Maharashtra, India.

Registration Number : S.U.R /M.D.A /R.S.R 1436

Registered on : 1st Jan 2005

Email-id

WebsiteContact No.

: [email protected] & dhanshrimultistate@gmail.comwww.dhanshrimultistateb.com02188-220132

Number of Branches : 35

Regular Members : 2570

Nominal Members : 400

Paid Up share capital : 3.79 Crores

Reserves and Surplus : 1.5 Crores

Total Deposits : 180Crores

Total Staff : 250

Profit of the year : 1.70 Crore

Investments : 40.68Crores

Audit Class : A

• 2.1 Historical Background of Bank:

Dhanshri multi-state Co-operative Societies Ltd. is established on 1st Jan 2005.

This bank has constituded with the object of providing funds to Firms,Education,co-operative

societies & others in Solapur, Jat & Vijapur district. Prof. Shivajirav Kalunge is founder of

Dhanshri bank.Firstly Kalunge sir had started Dhanshri PATPEDHI but after 2002 Goverment

including so many Rules & restrication on all PATHPEDHI that's why they had started Dhanshri

co-operative society bank. Currently we are operating with the network of 35 branches in entire

Solapur, Jat & Vijapur district. Our bank playing very important role in financial sector of

Solapur, Jat, Vijapur District. Our bank is known as farmer's bank & We implemented different

schemes in the interest of farmer & people of Solapur, Jat & Vijapur are having full confidence

on our bank. Therefore nearly more than 40% people of total population of Those District are our

account holders. Currently our working capital is 40.68. crores & our total deposit is 180 cores.

• 2.2 FEATURES AND AWARDS OF BANK

Features

• Insurance security up to Rs 1,00,000/- deposit.

• Nomination facility available for deposit account

• Safe deposit Locker facility available in Solapur, Pandharpur, Jat, Borale, Sangola City,

Mohol, Gheradi, Marawade & Head Office .Counter branch.

• Dhanshri bank had started recuring deposite from 1Jan 2005.

• Easy Loan facility for 85 different categories Small scale industries.

• Rs 50,000 accidental insurance security for “ kishan”cardholder.

• Loan available for agriculture farming, dairy, poultry, forest farming & irrigation.

• Salary mortgage loan available.

• first multi-state bank in solapur which was started the ''KANYARATNA YOJNA''

• Half percent more interest available on all types FD for Senior citizen & co-operative

Society.

• Loan Available for agriculture graduates for agri clinic & agro industries.

• The bank has been awarded ‘A’ Audit classification for the year ended on 31st march 2015.

• AWARDS

• Awarded as SAHAKARRATNA Best Multi-State co-op Societies in the years 2011- 2012

• Awarded as SAHAKARRATNA Best Multi-State co-op Societies in the years 2013-2014

• State Co-op bank has Awarded our Bank as Best banker for fullfilment Financial criteria in

the year 2014-2015

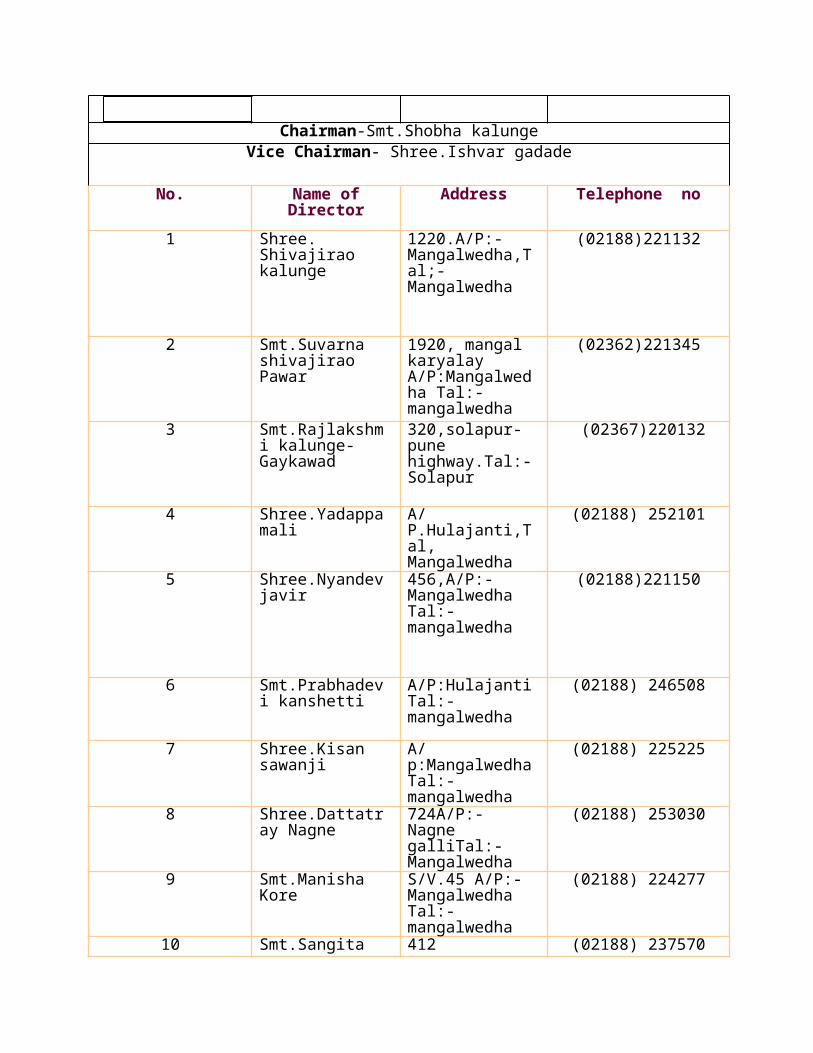

• 2.3Board of Directors:

Chairman-Smt.Shobha kalungeVice Chairman- Shree.Ishvar gadade

No. Name of Director Address Telephone no

1 Shree. Shivajirao kalunge

1220.A/P:-Mangalwedha,Tal;-Mangalwedha

(02188)221132

2 Smt.Suvarna shivajirao Pawar

1920, mangal karyalay A/P:Mangalwedha Tal:-mangalwedha

(02362)221345

3 Smt.Rajlakshmi kalunge-Gaykawad

320,solapur-pune highway.Tal:-Solapur

(02367)220132

4 Shree.Yadappa mali A/P.Hulajanti,Tal, Mangalwedha

(02188) 252101

5 Shree.Nyandev javir 456,A/P:-Mangalwedha Tal:-mangalwedha

(02188)221150

6 Smt.Prabhadevi kanshetti

A/P:Hulajanti Tal:-mangalwedha

(02188) 246508

7 Shree.Kisan sawanji A/p:Mangalwedha Tal:-mangalwedha

(02188) 225225

8 Shree.Dattatray Nagne

724A/P:- Nagne galliTal:- Mangalwedha

(02188) 253030

9 Smt.Manisha Kore S/V.45 A/P:-Mangalwedha Tal:-mangalwedha

(02188) 224277

10 Smt.Sangita Tad 412 A/PMangalwedha Tal:-mangalwedha

(02188) 237570

11 Shree.Sharad Hembade

A/P:-Mangalwedha Tal:-mangalwedha (02188) 253031

.

• 2.4 Departments of the Dhanshri Multi-State Co-operative Societies Ltd

::Executives:: ::Name:: ::Contact No.::

Chief Executive Officer

Mr.R.K.Fadtare (02188) 220132

Manager (Adm.) Mr.S.B.Sawant

Mr.R.A.Unhale

(02188)220833

(02188)220832

(Accounts, & Audit) (02188)220134

Mr. P. S.

Sawant

EPABX

.Manager Mr.P.A.Kalunge (02188)244314

(Loan, Dev & Planning)

(02188)244315

Manager Mr. H.D.Bedare

(Field & Recovery) (02188) 245070

Manager Mr. R. B. Sawant EPABX(P&D) (02188)221215

Chapter 3

Theoretical aspect of the topic

3.1 CONCEPT OF BANK:

Banking means the accepting deposits for the purpose of lending or investments, from the public

repayable on demand or otherwise & withdrawal by cheque, draft, order or otherwise.

Any money accepted as deposits must be for the purpose of lending or investments, making

advances & making investments of funds are equally important function. They are two main

sources of the bank.

Importance of advances in banking business:-

All the function of a modern bank, lending is for the most important. Advances comprise very

large portion of a bank’s structure.

The strength of a bank is thus primarily judged by the soundness of its advances. A wise &

prudent policy in regard to advances is considered an important factor inspiring confidence in the

depositors & prospective customers of a bank.

All types of business activity including trade, industry and agriculture depend on bank finance in

one form or the other. Bank assists in creating more avenues of employment and thus helps

raising the standard of living of people.

3.2 MULTI-STATE CO-OPERATIVE SOCIETIES:

Co-Operative Societies

Definition-

A Society reggistered or deemed to be registered under (2002 *39* ) this Act and includes a

national co-operative society and a federal co-operative.it's main object to serve the interests of

members in more than one state.

A co-operative Society is an autonomous of persons united voluntarily to meet their common

economic, social and cultural needs and aspirations through a jointly owned and democratically

enterprise.

The co-operative Societies in plays an important role even today in rural financing.

Values-

Co-operative Society in India are registered under the Co-operative Societies(2002) Act. The

cooperative society is also regulated by the Central Govt. They are governed by the Banking

Regulations Act 1949 and Banking Laws (Co-operative Societies) Act, 1965.

Co-operative bank is based on the values of self-responsibility, democracy, equality and

solidarity. In the tradition of their founders, co-operative members believe in the ethical values of

honesty openness, social responsibility and caring for others.

• 3.3 Types of Co-operative Banks in India

The co-operative banks are small-sized units which operate both in urban and non-urban centers. They finance small borrowers in industrial and trade sectors besides professional and salary classes. Regulated by the Reserve Bank of India, they are governed by the Banking Regulations Act 1949 and banking laws (co-operative societies) act, 1965. The co-operative banking structure in India is divided into following 5 categories:

Primary Co-operative Credit Society

The primary co-operative credit society is an association of borrowers and non-borrowers residing in a particular locality. The funds of the society are derived from the share capital and deposits of members and loans from central co-operative banks. The borrowing

powers of the members as well as of the society are fixed. The loans are given to members for the purchase of cattle, fodder, fertilizers, pesticides, etc.

Central Co-operative Banks

These are the federations of primary credit societies in a district and are of two types-those having a membership of primary societies only and those having a membership of societies as well as individuals. The funds of the bank consist of share capital, deposits, loans and overdrafts from state co-operative banks and joint stocks. These banks provide finance to member societies within the limits of the borrowing capacity of societies. They also conduct all the business of a joint stock bank.

State Co-operative Banks

The state co-operative bank is a federation of central co-operative bank and acts as a watchdog of the co-operative banking structure in the state. Its funds are obtained from share capital, deposits, loans and overdrafts from the Reserve Bank of India. The state co-operative banks lend money to central co-operative banks and primary societies and not directly to the farmers.

Land Development Banks

The Land development banks are organized in 3 tiers namely; state, central, and primary level and they meet the long term credit requirements of the farmers for developmental purposes. The state land development banks oversee, the primary land development banks situated in the districts areas in the state. They are governed both by the state government and Reserve Bank of India. Recently, the supervision of land development banks has been assumed by National Bank for Agriculture and Rural development (NABARD). The sources of funds for these banks are the debentures subscribed by both central and state government. These banks do not accept deposits from the general public.

Urban Co-operative Banks

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to primary co-operative banks located in urban and semi-urban areas. These banks, till 1996, were allowed to lend money only for non-agricultural purposes. This distinction does not hold today. These banks were traditionally centered on communities, localities, work place groups. They essentially lend to small borrowers and businesses. Today, their scope of operations has widened considerably.

3.4 Difference between Commercial bank & Co-operative bank

Co-operative banks also perform the basic banking functions of banking but they differ from commercial banks in the following respects

1. Commercial banks are joint-stock companies under the companies’ act of 1956, or public sector bank under a separate act of a parliament whereas co-operative banks were established under the co-operative society’s acts of different states.

2. Commercial bank structure is branch banking structure whereas co-operative banks have a three tier setup, with state co-operative bank at apex level, central / district co-operative bank at district level, and primary co-operative societies at rural level.

3. Only some of the sections of banking regulation act of 1949 (fully applicable to commercial banks), are applicable to co-operative banks, resulting only in partial control by RBI of co-operative banks and

4. Co-operative banks function on the principle of cooperation and not entirely on commercial parameters.

3.3 FUNCTION OF BANK

Functioning of a Bank is among the more complicated of corporate operations. Since Banking

involves dealing directly with money, governments in most countries regulate this sector rather

stringently. The process of financial reforms, which started in 1991, has cleared the cobwebs

somewhat but a lot remains to be done. The multiplicity of policy and regulations that a Bank has

to work with makes its operations even more complicated. Banking Regulation Act of India,

1949 defines Banking as "accepting, for the purpose of lending or investment of deposits of

money from the public, repayable on demand or otherwise and withdrawal by cheques, draft,

order or otherwise."Deriving from this definition and viewed solely from the point of view of the

customers, banks essentially perform the following functions:

1) Accepting deposits from public/ others (Deposits)

2) Lending money to public (Loans)

3) Support to local business

4)Personal Finance

5) Support to farming

6) Small unit Industries

The banks are not limited only these six functions. There are so many functions involved in the

activities that a bank performs today. Banks are organized in a linear structure to perform these

activities at the base of which lies a Branch. The corporate office of a bank is normally called a

head office.

Chapter 4

RESEARCH METHODOLOGY

RESEARCH METHODOLOGY

Research:

According to Clifford Woody research comprises defining redefining problems, formulating

hypothesis or suggested solutions, collecting, organizing and evaluating data, making deductions

and reaching conclusions, last carefully testing the conclusions to determine whether they fit

formulating hypothesis.

The researcher has done the research by using two types of data. Mostly secondary data is used

for the study; in some cases the authorities of the Bank have provided their original record.

Sometimes informal discussions are also carried out for collecting the required information. In

order to collect the data the finance department extends its full co-operations.

PRIMARY DATA

The data collected originally by the investigator for his research project is called primary data

collection of primary data is not an easy task it requires good amount of time, money and effort

knowledge experience and common sense.

Following are the method of collecting primary data.

1) Observation Method.

2) Interview Method.

3) Information from Correspondents.

The primary data was collected by interview and discussion with manager & employees- staff.

SECONDARY DATA

Secondary data consist of information that already exists. Secondary data provide a starting point

for research and offer the advantage of the cost. Secondary data was collected through.

Internet.

Reference Book, Journal, Newspaper etc.

Bank Annual Report.

CHAPTER 5 LOAN POLICY

• 5.1 LOAN TYPES OF DHANSHRI MULTI-STATE CO-OPERATIVE SOCIETY.BANK LTD.

Name of loan:- Dhanshri Pagar Taran Karj Yojana (Salary mortgage loan)

Loan purpose:- Personal needs of the borrower

Eligibility:- Govt. servant, state transport cooperation, Insurance Company, M.S.E.C, Municipal corporation employee residing in Solapur District.

Limit of loan:-

• Maximum upto Rs 5,00,000/- 20 times salary of (bank salary, VDA and offer allowances).

• Salary deduction should not exceed 75% of total salary including EMI.

Rate of Interest:- 16% EMI

Repayment Period:- Maximum upto 7 years.

Security:- Two salaried guarantor, Tri-Party agreement between bank, borrower and salary issuing officer/employer.

Documents Required

• Photograph, Residence proof of borrower and guarantor.

• Recent salary slip of borrower and guarantor.

• Tri-party agreement.

• To facilitate borrower bank has deligated loan sanctioning powers of branch manages upto loan amount of loan amount of Rs. 75000/- at branches level.

Name of loan:- Home loan

Loan purpose:- Construction/purchase of house, purchase of flat, Repair/Renovation of Home/flat.Personal needs of the borrower

Eligibility:-

80% estimated cost or per square feet construction cost R.C.C – Rs 1800/- Sq. feetLoad Bering & slab – Rs 1500/- sq. feet Laterite/bricks construction of Rs 1000/- sq. feetMangalore roof/cement sheets cr mental sheets

As per estimated cost or cost as per above mentioned cost whichever is lowest for house/flat repair and renovation maximum loan limit is upto 2.00 lac.

Limit of loan:- Up to Rs 20.00 lac.

Rate of Interest:-

Upto Rs 5.00 lacs 15.0% EMI Above Rs 5.00 lacs 16.0% EMI

Repayment Period:-

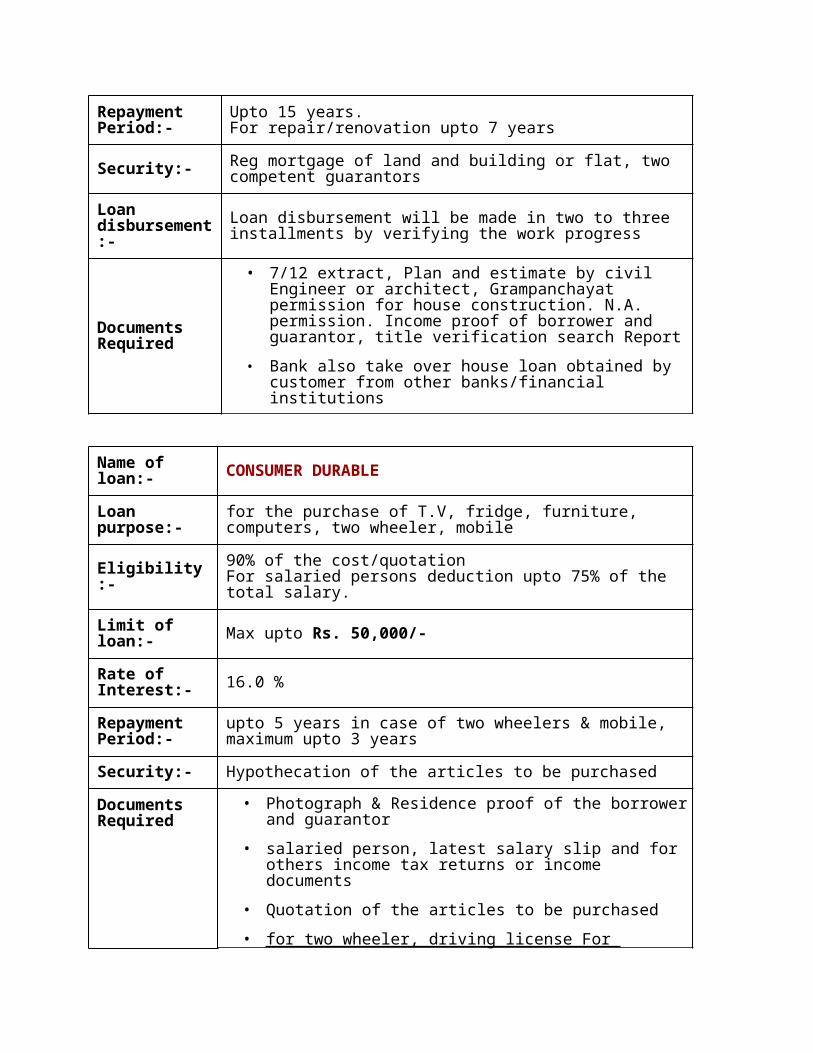

Upto 15 years.For repair/renovation upto 7 years

Security:- Reg mortgage of land and building or flat, two competent guarantors

Loan disbursement:-

Loan disbursement will be made in two to three installments by verifying the work progress

Documents Required

• 7/12 extract, Plan and estimate by civil Engineer or architect, Grampanchayat permission for house construction. N.A. permission. Income proof of borrower and guarantor, title verification search Report

• Bank also take over house loan obtained by customer from other banks/financial institutions

Name of loan:- CONSUMER DURABLE

Loan purpose:- for the purchase of T.V, fridge, furniture, computers, two wheeler, mobile

Eligibility:- 90% of the cost/quotation For salaried persons deduction upto 75% of the total salary.

Limit of loan:- Max upto Rs. 50,000/-

Rate of Interest:- 16.0 %

Repayment Period:- upto 5 years in case of two wheelers & mobile, maximum upto 3 years

Security:- Hypothecation of the articles to be purchased

Documents Required

• Photograph & Residence proof of the borrower and guarantor

• salaried person, latest salary slip and for others income tax returns or income documents

• Quotation of the articles to be purchased

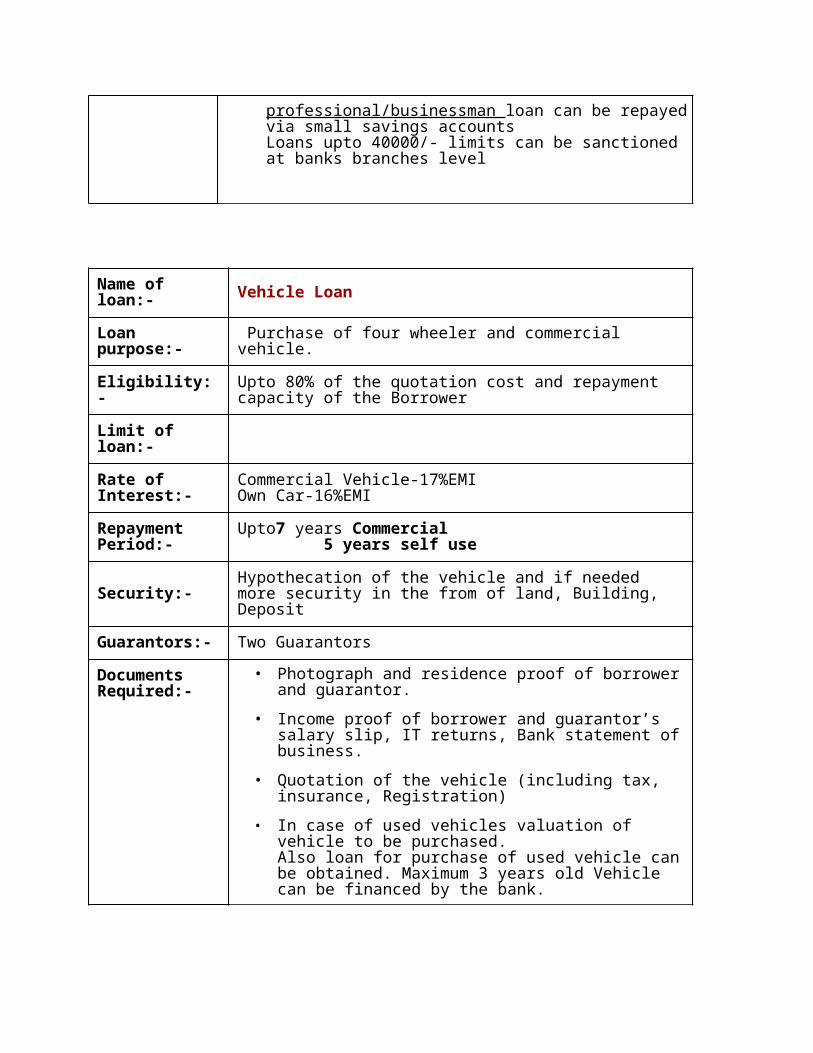

• for two wheeler, driving license For professional/businessman loan can be repayed via small savings accounts Loans upto 40000/- limits can be sanctioned at banks branches level

Name of loan:- Vehicle Loan

Loan purpose:- Purchase of four wheeler and commercial vehicle.

Eligibility:- Upto 80% of the quotation cost and repayment capacity of the

Borrower

Limit of loan:-

Rate of Interest:- Commercial Vehicle-17%EMIOwn Car-16%EMI

Repayment Period:-

Upto7 years Commercial 5 years self use

Security:- Hypothecation of the vehicle and if needed more security in the from of land, Building, Deposit

Guarantors:- Two Guarantors

Documents Required:-

• Photograph and residence proof of borrower and guarantor.

• Income proof of borrower and guarantor’s salary slip, IT returns, Bank statement of business.

• Quotation of the vehicle (including tax, insurance, Registration)

• In case of used vehicles valuation of vehicle to be purchased. Also loan for purchase of used vehicle can be obtained. Maximum 3 years old Vehicle can be financed by the bank.

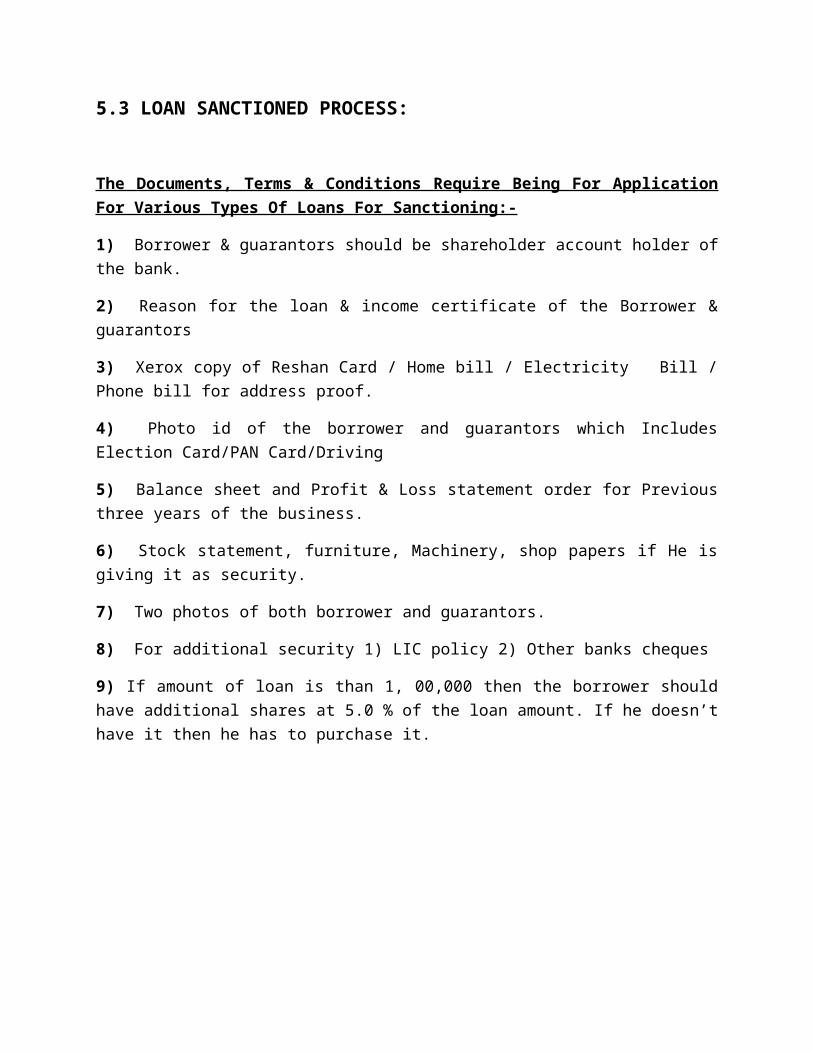

5.3 LOAN SANCTIONED PROCESS:

The Documents, Terms & Conditions Require Being For Application For Various Types Of

Loans For Sanctioning:-

1) Borrower & guarantors should be shareholder account holder of the bank.

2) Reason for the loan & income certificate of the Borrower & guarantors

3) Xerox copy of Reshan Card / Home bill / Electricity Bill / Phone bill for address proof.

4) Photo id of the borrower and guarantors which Includes Election Card/PAN Card/Driving

5) Balance sheet and Profit & Loss statement order for Previous three years of the business.

6) Stock statement, furniture, Machinery, shop papers if He is giving it as security.

7) Two photos of both borrower and guarantors.

8) For additional security 1) LIC policy 2) Other banks cheques

9) If amount of loan is than 1, 00,000 then the borrower should have additional shares at 5.0 % of

the loan amount. If he doesn’t have it then he has to purchase it.

In case of house /Flat /Shops /Plot there are some extra documents required as:

• Plot purchase copy

• Ownership city survey 7/12 document original.

• Original agreement copy between & builder.

• To be complete.

• Stamp paper according to demand condition.

Loan procedure of The Dhanshri Multi-State Co-operative Society Bank Ltd

Why people take loan from bank? The answer for this question is very loan & the best answer for

this question can be given by the banker only. People take loan for their personal need, because

they don’t have money spend to satisfy their needs and wants etc. The reason of the loan can be

anything. By categorizing these reasons the bank introduces the various types of loan into the

market.

All the files for the loan proposal comes to the head office of the Bank.At the Head Office in

every month the bank conduct two meeting of board directors where the files are decided to

sanction or

Every file comes to the head office with the report of the manager. Because bank manager knows

very well that how is the transaction of that applicant on his account. Then the file goes to the

Loan Manager at Head Office for his report on that report. Every one gives their own view on the

basis of the applicant’s transaction & on the basis of document which is submitted by the

applicant.

After the report the file is placed in to the Director’s Meeting on 5 th or 21st of every month in

which board of directors decides that which file should be sanctioned and which is not to be

sanctioned. After the meeting all the unsanctioned files is sent to the respective with all

document which was previously submitted by the applicant & the sanctioned files remains in the

Head Office in the Loan Department for the further provisions

Then bank takes the signature of the person to whom the loan is sanctioned along with his two

guarantors. The bank takes the signature of their own sanctioned form on which it is written that

the borrower and the guarantors are liable to pay the amount of loan. The bank also takes the

signature of the borrower on three debit voucher. Debit voucher and Credit voucher is used for

internal transaction of the bank. Bank also takes the signature on another four documents that are

• 1) Promissory Note

• 2) Loan Agreement

• 3) Lien & Set Off

• 4) Letter of Guarantee

After that bank ask for the original papers of the property which is to be given as security. If the

borrower had given the LIC policy then bank assigns it in bank’s favours. So that if the borrower

will fail to pay that loan amount of the bank then the bank can recover it from LIC policy by

giving it to the LIC Company. The bank always gives loan to the borrower up to 75% to 80% of

the total security which is given by the borrower.

After the completion of all the document and signature the file goes to the branch manager for

the signature on the Sanctioned Letter. Once the signature is done then the bank staffs open the

loan account of the borrower and transfer the amount of the loan to the Saving, Current, Cash

Credit or any other account of the borrower.

5.4 Loan Recovery Procedure:

This is the more significant section of the whole bank as people here are having more work. This

is so because, the Bank has 3.44% NPA (Non Performing Asset) and it is harmful to the banks

business, as the name implies this section deals with the recovery of loan.

Researcher study the loan recovery procedure, each bank has its own procedure of recovery it

includes policy adopted by bank for its recovery. Each and every bank tries to recover its money

as early as possible so banks take observation and also strict supervision from borrowers. If bank

fails to recover the money in time then it is adversely impacted on banks reputation, so to reduce

upcoming problems recovery is necessary. ‘Recovery procedure’ includes

• Importance of recovery of loan

• Provision of bank as per category of borrower

• Recovery of loan to its doubtful borrower.

• Recovery of loan before its maturity period.

I. Importance of recovery of loan-:

Every banks loan department focuses more attention on its recovery of loan. In brief quick

recovery of loan shows financial soundness of bank to protect from restrictions of R.B.I. and

N.P.A. provision, each bank has very serious about recovery of loan. The loan recovery policy

and its terms are as follows.

1. Banks first recover its interest amount and then recover the principle amount.

2. Bank has to bridge the gap between loan amount and its financial burden and provision.

3. Recovery is important because it converted borrower into defaulter then bank has to bear

various expenditure, such as

a) Maintaining proper books of loan.

b) Proper inspection of mortgaged items

c) Expansion incurred due to recovery such as legal expenses.

4. Defaulter converted into N.P.A., and then it is permanent loss of bank which cannot fill up.

5. Each and every time bank has to make the provision for doubtful loan.

6. Share of profit will decreases due to provision.

7. Due to rising N.P.A., R.B.I. takes strict action against those banks it will harmful for bank it

may lose its reputation.

Above mentioned are points shows that why recovery of loan is important and how it will impact

on banks financial condition.

II. Provision of bank as per category of borrower

The bank divides the borrower into 2 type’s viz. standard borrower doubtful borrower. The

borrower who pay the instalment at regular interval/period, called ‘standard borrower and those

borrower who do not pay the instalment regularly called doubtful borrower.

Bank should make a provision on its standard and doubtful borrower, it standard borrower pay

instalment regularly still bank has to make provision on that loan amount.

III. Recovery of loan to its doubtful borrower

Recovery of loan from doubtful borrower is very difficult task, so bank must be proper alert

about its recovery from doubtful borrower. Bank has to take following steps to doubtful

borrower.

1. Bank sends remerging notice to borrower which inform borrower that his loan account was

overdue

2. Bank charge penalty interest on loan account.

3. Bank sends notice to guarantor, to pay the balancing instalment.

4. If still borrowers don’t give any responses then bank send him 2nd notice to repay the loan

amount within given period.

5. If borrower don’t repay the loan, then bank take legal action against him. Bank has full right to

recover of loan and for recollecting loan, bank sale the mortgaged asset into market and recover

amount. If still the selling value should lesser than actual loan amount, then bank strictly recover

the balancing amount from borrower.

IV. Recovery of loan before its maturity period

Recovery is important we know that to recover loan amount, from defaulter is very difficult task

for bank. So bank has to careful watch on recovery. In some cases bank already found that to

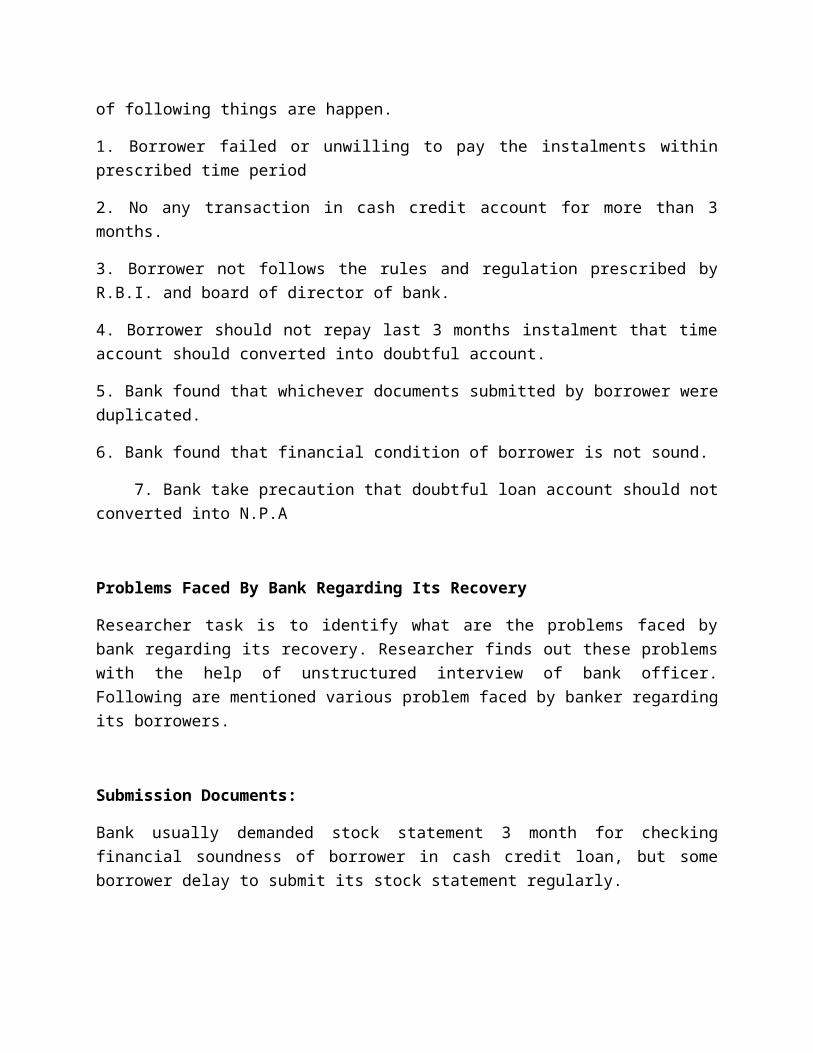

recollect loan so its demands loan before its maturity. In case of following things are happen.

1. Borrower failed or unwilling to pay the instalments within prescribed time period

2. No any transaction in cash credit account for more than 3 months.

3. Borrower not follows the rules and regulation prescribed by R.B.I. and board of director of

bank.

4. Borrower should not repay last 3 months instalment that time account should converted into

doubtful account.

5. Bank found that whichever documents submitted by borrower were duplicated.

6. Bank found that financial condition of borrower is not sound.

7. Bank take precaution that doubtful loan account should not converted into N.P.A

Problems Faced By Bank Regarding Its Recovery

Researcher task is to identify what are the problems faced by bank regarding its recovery.

Researcher finds out these problems with the help of unstructured interview of bank officer.

Following are mentioned various problem faced by banker regarding its borrowers.

Submission Documents:

Bank usually demanded stock statement 3 month for checking financial soundness of borrower

in cash credit loan, but some borrower delay to submit its stock statement regularly.

Dividend:

Borrower must be member of bank if he is not the member of bank, then bank give him

temporary membership and give some shares.

Bank must pay dividend on share holders suppose the borrower become defaulter and he does

not pay instalment regularly still bank has to pay dividend on shares. It creates financial burden

for bank.

Misuse of loan:

Many times it was found that borrower take loan for some purpose but it used for different

purpose. It is misuse of loan and such condition there may be possibility of defaulter of loan.

Overdue, N.P.A. provision:

Bank has to keep provision for its defaulter and N.P.A. it is up to 100% of loan amount naturally

it create financial burden on bank.

Expenditure:

For recovery defaulter of loan bank has to pay various expenditure such as legal, suspensions of

property etc. there will not any possibility of getting money back so it is unavoidable expenditure

for bank.

Above mentioned are the various problems faced by bank regarding its sanctioning procedure as

well as recovery. I.e. Duplicate documents, misuse of loan are the most important problems. If

bank has overcome these problems then it help to improve the banking business.

CHAPTER 6

DATA ANALYSIS & INTERPRETATION

DATA ANALYSIS & INTERPRETATION

6.1) Performance Analysis of Deposit & Loans Of The Dhanshri Multi-State Co-operative

Society Bank Ltd

Table 1

Year Deposit Loan

2012-2013 150.35 Cr. 110.7 Cr.

2013-2014 165.50 Cr. 122.12 Cr.

2014-2015 180.75 Cr. 136.48 Cr.

• Graph Showing The Increase And Decrease In The Deposit & Loan Of Dhanshri

Multi-State Co-operative Society bank ltd.

• Figure 1

• Interpretation:-

As we have seen Deposits are continuously increasing from 2013, 2014 & 2015.

Because Fixed Deposits are increasing continuously last three years.

As we have seen deposits are increasing so that loan is also increasing in same proportion.

• 6.2) Performance Analysis Of Loans Of The Dhanshri Multi-State Co operative Society

Bank Ltd For Last 3 Years.

• Table 2

Items Loan2010 Loan 2011 Loan 2012

Book Debt 412125.39 838892.78 8312390.75

Hypothecation3411808.6 2557707.3 1481648.6

Agst Fixed Deposit 503167 537708.13 850559.5

Gold Loan

Cash Credit 1554336 2997983 3524165.6

House hold 1898127.22 1461691.46 1213650.11

Plant & Mach. 68647 48602.62 48364.62

Vehicle Loan 76574 76402 57480

Term Loan against Saving

A/c 1726174.55 2189680.1 2623162.45

Housing Loan A/c 194555 289192 229562

Term Loan For Staff 3703655.96 4837503.5 5631362.55

• % Change In Amounts Given For Various Loans.

• Figure 2

Interpretation:-

• The Housing, Vehicle, Gold Loan of Bank increased continuously.

• The Hypothecation, Cash Credit Loan of Bank decreased on 2012-2013.

6.3)Table Showing The Amount Of Hypothecation Loan Of Bank For The Last 3 Years.

• Table 3

FINANCIAL YEAR AMOUNT (IN RS)

2012-13 127887940

2013-14 87582872

2014-15 68075425

• Graph Showing The Increase And Decrease In Hypothecation Loan Of Bank For The

Last 3years.

• Figure 3

Interpretation:-

The hypothecation loan was disbursed the most in the year 2013 & 2014 and then there was a

gradual decrease in the loan as other kinds of loans like, Gold loan etc. loans come up

6.4) Table Showing the Amount of Gold Loan for Last 3 Years

Table 4

FINANCIAL YEAR AMOUNT (IN Cr.)

2012-13 22.48

2013-14 19.26

2014-15 16.62

• Graph Showing The Increase And Decrease In The Gold Loan of Bank.

• Figure 4

Interpretation:

Gold Loan was provided by Bank and hence it took time for the bank to

increase its loan sales. Because Interest taken on gold loan is “10%”And method is use for

interest is daily rating method. And the chances of loss are very low.

6.5) Table Showing The Amount Of Cash Credit Of Bank For Last 3 Years

• Table 5

FINANCIAL YEAR AMOUNT (IN RS)

2012-13 189278714

2013-14 147065875

2014-15 115547820

• Graph Showing The Cash Credit Bank .

• Figure 5

• Interpretation:-

The year 2012-13 the Cash Credits decreases slightly. Because of that bank management decided

to overcome of that type of loans. Because Recovery of this loan low as compared to other types

of loan.

6.6) Table Showing Profit Amount Of The For The Last 3 Years

• Table 6

FINANCIAL YEAR AMOUNT (IN RS)

2012-13 1.22 Cr.

2013-14 1.40 Cr.

2014-15 1.70 Cr.

• Graph Showing The Amount Of Profit The Dhanshri Multi-State Co-operative Society

Bank For The Last 3 Years

• Figure 6

• Interpretation:-

Profit of bank is increase due to housing loan finance and Gold loan is increased that’s why it

affects follows on profit. In bank its NPA percentage is low so that provision for it is decreased

by bank. Recovery of loan is also increased. But so far for last 3 years it has been observed that

the degree of increase of the profit is steady and big rise in profit has not seen for Bank.

6.7) NON PERFORMANCE ASSET

Meaning:

According to RBI ,Terms loans on which interest or installment of principal remain overdue

for a period of more than 90 days from the end of a particular quarter is called a Non

Performing Asset.

• An asset, including a leased asset, becomes nonperforming when it ceases to generate

income for the bank.

• A NPA is a loan or an advance where Interest and/ or instalment of principal remain

overdue for a period of more than 90 days in respect of a term loan.

• EXAMPLE :-

We suppose that a party was disbursed a loan on 1st Jan 2012, it's due date is 1st June 2012.

But a party does not make a payment.So

*It will be an Standard asset from 1st Jan 2012 till 1st June 2012 (Due Date)

*It will be Special Mention Account from 2nd June 2012 till 29th August 2012 (90 Days )

*It will be Sub-standard from 30th August 2012 till 29th August 2013

*It will be doubtful from 30th august 2013 till 29th august 2014

• Comparative Statement of NPA’s;

• Table 7

Sr. No. Particulars 2010-11 2011-12 2012-13

1 Total adv. 1963 2149.64 2500.03

Less provision 160 166 169

2 Net adv. 1803 1983.64 2331.03

3 Gross NPA 298.18 283.55 249.28

4 Net NPA 138.18 117.55 80.28

7.66% 5.93% 3.44%

• Graph Of Comparative Statement Of NPA :

• Figure 7

Interpretation:-

NPA of the year 2012-13 is less than the previous two years i.e. year 2010-11& 2011-12. It is the

good for bank but it is expected less the NPA, more it will be beneficial to bank so that the whole

managing body of the bank is focused on how to minimize the NPA or how to avoid the

blockages so that bank run very well in competitive situation.

CHAPTER 7

• FINDINGS

FINDINGS:-

1)Bank takes into consideration the Character, Capacity, Collateral and Condition while

sanctioning the loan.

2) Loans and deposits increase in same manner. Due to deposits are increased in

2014, we have seen in increment in loans sanctioned accordingly.

3) The Housing loan finance is having highest portion of loan in total loan.

4) The amount sanctioned by bank as loan has shown gradual increase year by year.

5) Cash credits have inctreased in 2014 due to the recovery from NPAs is observed.

6) The amount of profit from year 2013 to 2015 has shown increase.

The percentage of NPA is decreasing from year 2013to 2015 which is good for the bank.

FINDING ABOUT WORKING OF BANK:

Loans for self employment

Due to recession, lock outs and frequent strikes in the industry, people find it safe to be self

employed. So there is a need to attract new and young entrepreneurs.

Bank lending for a self employment purpose is increasing therefore more attention should be

given towards this area.

Advertising

The area of operations of the bank is mainly the industrial as well as residential sector in the area

of Solapur, Vijapur, and other district’s places. The bank should take advantage of this and

arrange any advertising campaigns and loan festivals to attract new customers.

Housing Loans

As there is more demand for housing loans, it forms the major part of advances portfolio of the

bank. Almost 25% of the total advances are given for the housing loan purpose. Population is

increasing rapidly in the places where the branches are located especially in the area of Solapur,

Pandharpur and mohol and also people shift their homes from old chawls and buildings to newly

constructed, fully furnished flat systemised buildings, which costs a lot than the resale value of

their previous houses. Now in this case people require housing loans to meet the margin. So such

customers can be targeted and served considering their convenience.

First of all is to keep the margin for housing loans to lower side. Because the cost of

accommodation is increasing and its very much difficult for a common man to buy a house with

his own savings.

The bank may bring flexibility in their rules and follow easy instalment schemes.

If possible, the bank should be more liberal while lending for housing purposes. At present the

bank advances 30 times of the net income of the borrower. Instead the bank should advance more

times of customer’s salary/ income.

Broaden the work area

The bank should broaden the area of work and its service. At present the bank already has 35

branches in Maharashtra & Karnataka. But still some important districts are unexplored by the

bank. Districts like Baramati and Usmanabad, where the industrial area is much widen now a

days, these districts are still untouched by Bank.

Special scheme offering

Bank can introduce new and attractive loan scheme at the time of festival or such occasions so

that more number of customers can be delighted with the special offers or discounts. The bank

has to give attention towards the interest rates it charges from the competitor analysis it has been

found that almost all the banks charge at reducing balance method. Today the bank has to change

with changing time and improve their lending rates.

Concentration on personal loan

It has been observed that the personal loan has higher interest rates. Personal loan in the bank is

given up to 6.65 Cr. only. Thus it indicates that the proportion of the money lend is relatively

smaller than the money they will have to lend in case of housing loan or vehicle loan. It is also

observed that the customers are willing to get personal loan for the purpose of repayment of

previous debts. It means the customer has hurry to get the personal loan from the bank as soon as

possible. Thus on higher rate of interest and with lenient security against loan or without any

mortgage the bank can provide the loan and create the bank value in the eyes of the customer.

Small scale industry finance.

Small scale industry finance seems the ignorant sector from the big commercial bank like ICICI ,

IDBI and HDFC banks. Small scale sector is growing rapidly. So that, the bank needs to attend

the small scale industry customers and serve their purpose. Today small scale industry can be

said as the back bone of industry. So the bank can’t ignore this anymore. More encouragement is

required to be given to the small scale businessmen by the bank.

Documentation of guarantors

To decrease the growing numbers of NPAs, bank needs to take more care while selecting the

guarantor. The guarantor’s financial viability should be up to the mark and he should complete

his all the documentation work for the forward procedure of the money lending. At least 2 valid

guarantors should be there in any loan application.

Easy instalment facility

The applicant should be made available with the easy instalment facility. The borrower

sometimes may be busy with the work or due to any other reasons he may not be able to come to

the bank personally to make the payment of instalment of the loan taken. In this case the bank

should facilitate the borrower with the direct debit from the saving bank account service. This

will save the time of borrower and make him relax and tensionless. From the bank’s point of

view, time to time payment will be made from the borrower which will result into a good

reputation of the bank.

Check of fraud

It is observed that in general more number of bank related frauds is made by borrower of loan.

Fake and forger documents are represented and thus loans are taken. So to avoid that special

auditing department to check the viability and competency level of the loan applicant should be

created. Document inspection, special interview and personal inspection in case of property

mortgage should be done by the department. This department should check the creditworthiness

of the loan applicant and then they will submit their report to upper level which is Credit

department which is in charged by Mr.Fadatare.R.V

Proper Remainder System:

It is very much observed that Bank lacks in proper remainder system for the loan account holders

to pay their due instalments in time. It will also help their creditworthiness with the bank.

Therefore, I would advice to the bank to keep good remainder system to remind its loan account

holders. It will certainly reduce the amount of NPAs. If the NPAs amount goes down then, it will

surely reflect in the profit of the bank.

CHAPTER 8 SUGGESTIONS

•

• Suggestions:

• The basic function of the bank is to accept deposits in various ways through customers which

are account holders of the bank and invest them into productive activities in the form of

loans. The difference between the rate of deposits and the rate of interest on lending money

in term of loan is the profit for the bank.

• Suggestions to improve bank’s lending procedure

• Finance to business community

• Focus on housing and commodity loan

• Bifurcate housing loans according to the loan amount

• Finance to small scale industries

• Service area should be broadened

CHAPTER 9

• CONCLUSION

• CONCLUSION:

While doing my project I had a chance to look into the vast field of Loan Procedure and

disbursement. I could only touch a small part of the topic. But after going through the whole

process I firmly believe that before going for any loan decision there is a need to classify the

borrower type and his need according to the creditworthiness of the borrower. It is also true that

there is confusion towards a new loan offer by the Banks. Not it’s always better to take loan from

the bank having good past record.

I have learnt the provisions of granting the loan to the borrower according to their income level

and degree of need. The Dhanshri Multi-State Co-operative Bank Ltd is marketing its bank

properly by adopting new banking schemes like SMS Banking, Internet Banking and Telephone

Banking. Bank is the first Dhanshri Multi-State cooperative bank in Solapur,jat to introduce SMS

Banking. Keeping proper marketing agenda in mind

The bank is also visiting to the villages which are near to the Solapur, Jat, Vijapur district.

Bank has to start the Transferring money from one place to another (remittances).It is first Multi-

State Co-operative bank in Solapur ,Jat ,Vijapur to start Call Deposite for 15 Days to the

customer.

The Loan management of this Bank consists of many stages. It is responsibility of Loan officer

to check the credit worthiness of the applicant.

Chapter 10• Annexure

Financial Highlights

Years Gross

profit

Total

Provision

Net

profit

No.of

staff

Working

Capital

No.of

Branches

Credit

Deposit

Ratio

N.P.A Provision Rate Of

Dividend

Audit

ClassImpaired

Credit

Gross NPA

%

As on

1-1-

2005

- - - 205 1228.45 26 58.30% - -

2005-

06

144.00 96.30 47.70 437 10853.91 51 31.70% - - 10% A

2006-

2007

226.12 173.41 52.71 430 13304.51 51+2 53.15% 844.49 13.91% 10% A

2007-

2008

244.52 185.25 59.27 421 15044.54 51+7 29.31% 761.02 19.80% 10% A

2008-

2009

253.37 171.88 81.49 417 18546.16 52+14 40.99% 779.09 11.92% 12% A

2009-

2010

290.26 196.42 93.84 410 22147.91 52+15 68.05% 749.23 5.79% 13% A

2010-

2011

450.02 340.77 109.25 419 25571.14 55+13 70.33% 811.74 5.24% 13.5% A

2011-

2012

593.14 469.14 124.00 419 32545.14 62+12 65.75% 1064.48 5.68% 14% A

2012-

2013

550.27 398.22 152.05 425 36461.01 64+13 37.69% 1183.45 10.00% 14% A

2013-

2014

298.07 136.47 161.60434+15 41546.07 66+11 54.43% 1380.57 7.13% 13% B

2014-

2015

340.38 165.38 175.00 433 4651.47 68+10 57.79% 1239.90 5.34% 10% B

2005-

2006

200.15 163.17 163.17 453 50876.46 70+9 61.77% 1384.09 5.04% 10% A

2006-

2007

379.22 263.22 116.00 442 57594.52 70+9 70.25% 1785.21 5.31% 10% A

2007-

2008

847.41 722.41 125.00 569 63202.57 70+10 69.93% 2265.37 6.07% 7.50% B

2008-

2009

371.75 91.82 279.93 607 69128.60 71+09 65.94% 3086.74 7.94%

2008-

2009

464.43 184.43 280.00 607 69128.60 71+9 65.95% 3086.55 7.94% 5% B

2009-

2010

777.71 440.11 337.60 591 83184.52 82+12 68.32% 3206.88 6.57%

•Years No of

Members

Share

Capital

Reserves

and others

funds

Total

Deposits

Total Advances Investments

& Bank

Balance

Total

Income

Total

Expenditure

Sty. Indl. Agri Non-Agri

As on 1/7/83 368 65 37.58 75.60 632.30 128.58 240.09

1995-1996 579 56 236.49 764.54 9467.16 942.11 2059.83 5585.37 1215.01 1167.31

1996-1997 594 71 265.45 942.12 11418.41 986.26 2082.80 5301.90 1519.54 1466.83

1997-1998 631 81 291.14 1118.93 13114.05 1295.66 2548.84 9214.50 1732.95 1673.68

1998-1999 653 82 338.82 1263.02 15940.31 1139.08 5395.08 9314.15 1967.70 1886.21

1999-2000 662 83 387.59 1451.61 19025.83 1212.23 11735.30 6982.80 2394.07 2300.23

2000-2001 681 91 450.82 1689.19 22025.45 1492.06 13998.00 7928.00 2908.17 2798.92

2001-2002 736 94 497.29 2150.11 28477.24 1725.71 16999.67 10114.56 3597.16 3473.16

2002-2003 771 93 540.48 2610.20 31393.35 1956.05 9876.58 21471.76 3776.95 3624.90

2003-2004 829 94 635.08 2766.69 35551.76 2530.27 16823.59 19325.62 3646.27 3484.67

2004-2005 851 98 711.06 3013.62 40143.75 2952.57 20247.87 20532.50 3782.43 3607.43

2005-2006 868 101 789.26 3192.72 44487.80 3613.92 23868.12 21285.08 3669.43 3506.26

2006-2007 847 103 866.47 3486.15 47895.58 4144.55 29505.73 22187.01 4123.36 3850.25

2007-2008 848 58 1068.65 4214.72 53376.54 5131.36 32196.59 23905.56 5191.07 5066.07

2008-2009 866 63 1280.33 4380.66 58921.53 4496.33 34361.42 27878.08 5486.48 5206.55

• CHAPTER 10

• BIBLIOGRAPHY

• Bibliography

• Reserve Bank Manual.

• Diary for co-operative banks

• Balance sheet and manual reports of last three years of the Dhanshri Multi-State Co-

operative Society Bank Ltd

• Practical banking advance

• Websites

• www.loanmanagements.com

• www.rbi.org.in

• www.databasemanagers.com

• www.dhanshrimsbank.com

Related Documents