Life and Health Insurance State Law Supplement Florida

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Life and Health Insurance

State Law Supplement

Florida

Important: Check for Updates States sometimes revise their exam content outlines unexpectedly or on short notice. To see whether there is an update for this product because of an exam change, go to www.kaplanfinancial.com and check the Insurance Licensing Blog. If there is an update, it will be clearly noted in the blog entries for this state.

State Law Supplement

Effective January 1, 2016

Florida

Life and Health Insurance

Florida_L&H_LawSupplement_book.indb 1 11/11/2015 2:36:23 PM

At press time, this edition contains the most complete and accurate information currently available. Owing to the nature of license examinations, however, information may have been added recently to the actual test that does not appear in this edition. Please contact the publisher to verify that you have the most current edition.

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. If legal advice or other expert assistance is required, the services of a competent professional should be sought.

FLORIDA LIFE AND HEALTH INSURANCE LAW SUPPLEMENT, EFFECTIVE JANUARY 1, 2016©2016 Kaplan, Inc.

The text of this publication, or any part thereof, may not be reproduced in any manner whatsoever without written permission from the publisher.

If you find imperfections or incorrect information in this product, please visit www.kaplanfinancial.com and submit an errata report.

Published in December 2015 by Kaplan Financial Education.

Printed in the United States of America.

ISBN: 978-1-4754-3752-2

PPN: 3200-7148

Florida_L&H_LawSupplement_book.indb 2 11/11/2015 2:36:23 PM

iii

Contents

Introduction v

S E C T I O N 1 Cram Sheets 1

S E C T I O N 2 Class Notes 7

S E C T I O N 3 Detailed Text 83

S E C T I O N 4 Practice Exam 201

Florida_L&H_LawSupplement_book.indb 3 11/11/2015 2:36:23 PM

Florida_L&H_LawSupplement_book.indb 4 11/11/2015 2:36:23 PM

v

Introduction

What is a State Law Supplement?This book focuses on the state-specific statutes and regulations on the state exam content

outline. In order to be fully prepared for the exam, you must understand completely both the national License Exam Manual and this supplement.

How is the supplement organized?In order to make this book flexible and easy to use, we’ve divided it into four sections, and

are each broken into topic areas as seen below.

Section Topic Areas

Cram SheetsCram sheets focus on very specific details for your state. The information is presented in an easy to understand table format primarily highlighting days, dates, and dollars.

■ General Insurance Law ■ Life Insurance Law ■ Health Insurance Law

Class NotesThe class notes are meant to be a summary of the key topics in the law supplement, and are available to all students—classroom and self-study.

■ General Insurance Law ■ Life Insurance Law ■ Health Insurance Law

Detailed TextThe text section is the most detailed section of the law supplement. All topics in your state’s exam content outline law and regulations section are covered.

■ General Insurance Law ■ Life Insurance Law ■ Health Insurance Law

Practice ExamsThe practice exams test your retention of the law supple-ment material.

■ General Insurance Law ■ Life Insurance Law ■ Health Insurance Law

Do I have to learn everything in this book?Not necessarily! The table below shows the sections you should study depending on the

exam you are preparing for.

State Exam Sections to Study

Life and Health Insurance General (All Lines), Life, and Health Insurance

Life Insurance Only General (All Lines), and Life Insurance only

Health Insurance Only General (All Lines), and Health Insurance only

Florida_L&H_LawSupplement_book.indb 5 11/11/2015 2:36:23 PM

vi Florida Law Supplement

How should I study this information?Below is a best study practice for the law and regulations section of your exam.

1. Law Supplement Cram Sheet: Your exam will probably ask about specific fine amounts or days’ notice requirements (e.g., changing your address).

2. Law Supplement Class Notes: Reading the class notes exposes students to the majority of topics covered in the law supplement.

3. Law Supplement Detailed Text: Read this text for more in-depth descriptions of the state’s insurance laws and regulations.

4. Law Supplement Practice Exams: There are two law supplement practice exams. One is in the back of the law supplement. State specific law questions can also be found in the InsurancePro™ QBank at www.kaplanfinancial.com.

5. In your final preparation for the exam take the time to again review the cram sheet and class notes. Use them as a last-minute refresher of the most important law and regulation testable topics.

Florida_L&H_LawSupplement_book.indb 6 11/11/2015 2:36:23 PM

s e c t i o n

1

1s e c t i o n

1

Cram Sheets

HOW TO USE: In your final preparations for your insurance exam use

this cram sheet to memorize key days, dates, and dollars. A suggested tech-

nique is to cover the left hand column; read the right hand column; then

uncover the left hand column to reveal the correct answer.

Florida_L&H_LawSupplement_book.indb 1 11/11/2015 2:36:23 PM

2 Law Supplement

FLORIDA STATUTES, RULES AND REGULATIONS COMMON TO ALL LINES OF INSURANCEFinancial Services Regulation

15 divisions and offices

Chief Financial Officer (CFO) ■ Head of the Department of Financial Services ■ Oversees ___ divisions and offices

— Accounting and Auditing (Unclaimed Property) — Insurance Agents — Insurance Fraud — Consumer Services — Office of the Insurance Consumer Advocate

■ Regulation of insurance agents

Financial Services CommissionOffice of Financial Regulation (OFR)

■ Regulation of banks, credit unions, securities industry, finance companies, other financial institutions

■ Bureau of Financial Investigations — Investigates suspected wrongdoings

Office of Insurance Regulation (OIR) ■ Responsible for regulating insurers ■ Duties include

— rate-making supervision; — policy forms approval; — market conduct investigation; — issuing insurer certificates of authority; — assessing insurer solvency; — regulating viatical settlements; — regulating premium financing agreements; and — administrative supervision.

Office of Insurance Regulation

30 days Policy forms must be filed at least ___ days before use

5 yearsExamination of InsurersMarket conduct examinations at least once every ___ year

Licensing

24 months60 days30 days

AppointmentsAppointments renew every ___ monthsAn insurer that terminates an appointment must provide at least ___ days’ advance noticeTermination notice must be sent to Department within ___ days

40 hours40 hours60 hours

Prelicensing Education Requirement ■ Life agent license ■ Health agent license ■ Health and life agent license

5 times License exam may not be taken more than ___ times in a 12-month period

Florida_L&H_LawSupplement_book.indb 2 11/11/2015 2:36:24 PM

3Law Supplement

24 hours5 hours19 hours15 hours

5 hours

Continuing Education (CE) ■ Total hours required every two years

— Required hours of ethics and industry update — Elective hours specific to license

■ If licensed more than six years, elective hours requirement is ___ hours ■ If licensed 25 years or more, and has a CLU®, CPCU®, or BS in risk management,

the elective hours requirement is ___ hours

20 days Insurer must respond within ___ days once a complaint has been filed

30 days Report name, address, phone number, or email address within ___ days

30 days30 days

Criminal and Administrative ActionsReport administrative action against agent within ___ days Report within ___ days if guilty of a felony or sentenced to at least a year in prison

Agent Responsibilities 3 years Premium payment records must be maintained for ___ years

1st degree misdemeanor3rd degree felony2nd degree felony1st degree felony

Penalties for Misappropriation of Fiduciary Funds ■ Funds misappropriated $300 or less ■ Funds misappropriated $301 to $20,000 ■ Funds misappropriated $20,001 to $100,000 ■ Funds misappropriated $100,000 or more

Life and Health Insurance Guaranty Association

$100,000$250,000$300,000

The Association’s maximum liability is as follows: ■ Life insurance net cash surrender and withdrawal values ■ Annuity net cash surrender and withdrawal values ■ All life insurance benefits, including cash values, on any one life

Marketing Practices

Unfair Claims Practices

30 days Insurer must accept or deny claims within ___ days

$2,500$10,000$20,000$100,000

Unfair Competition Fines ■ Minimum fine per nonwillful violation ■ Maximum fine for all nonwillful violations ■ Minimum fine per willful violation ■ Maximum fine for all willful violations

$5,000$75,000

Penalties for Twisting or Churning ■ First-degree misdemeanor ■ Minimum fine per nonwillful violation ■ Maximum fine per willful violation

$5,000$50,000$75,000

$250,000

Penalties for Fraudulent Signatures ■ Third-degree felony ■ Minimum fine per nonwillful violation ■ Maximum fine for all nonwillful violations ■ Minimum fine per willful violation ■ Maximum fine for all willful violations

$50,000Violating a Cease and Desist OrderViolation not to exceed ___

4 years Advertisements must be maintained for ___ years

Florida_L&H_LawSupplement_book.indb 3 11/11/2015 2:36:24 PM

4 Law Supplement

FLORIDA STATUTES, RULES AND REGULATIONS PERTINENT TO LIFE AND ANNUITY INSURANCE, INCLUDING VARIABLE PRODUCTSFlorida Replacement Rule

5 days

3 years

Duties of Replacing CompanyIf requested by applicant, replacing insurer must send Comparative Information Form within ___ days of receipt of the applicationNotice to Applicant Regarding Replacement of Life Insurance must be maintained for at least ___ years

Policy Provisions

14 days21 days21 days

Free Look ■ Unconditional premium refunds for life insurance ■ Unconditional premium refunds for fixed annuity contract ■ Unconditional refund for variable annuity contracts

30 days Individual life insurance grace periods must be at least ___ days

31 days2 years31 days

Group LifeGrace period for group life insuranceIncontestable after policy has been in force for ___ yearsConversion to individual plan must be completed within ___ days after termination

2 employers2 years

Types of Groups/Eligible Groups ■ Trustee group must have ___ or more employers ■ Associations must have been in existence for at least ___ year(s) to offer group life

insurance

Annuities

5 years Records must be kept for at least ___ years

10%An annuity contract issued to a consumer age 65 or older may not contain a surrender charge exceeding ___ % of the amount with drawn

FLORIDA STATUTES, RULES AND REGULATIONS PERTINENT TO HEALTH INSURANCE

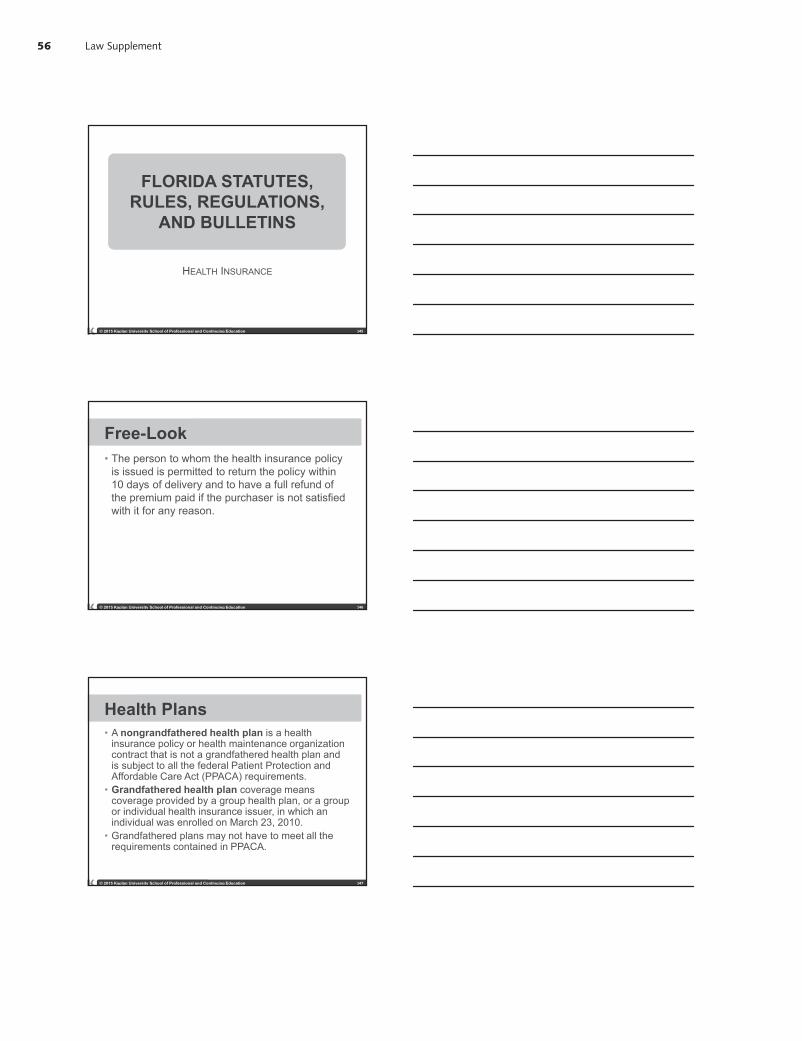

March 23, 2010 A PPACA grandfathered health plan is a plan in existence on or before ___, and has had no significant coverage changes

Age 2690 days

PPACA Provisions Applicable to Grandfathered Health PlansDependent coverage for unmarried adult children until age ___Waiting period may not exceed ___ days

18 months18th birthday

Newborn children of covered dependents are covered for up to ___ monthsAdopted and foster children are covered up to their ___ birthday

Required provisions

2 years

7 days10 days31 days

20 days15 days90 days60 days5 years

Time limit on certain defensesGrace period

■ Weekly premium payments ■ Monthly premium payments ■ All other premium payment modes

Notice of claim must be sent within ___ days of lossInsurer must sends claims forms to claimant within ___ daysProof of loss must be provided within ___ days after lossNo legal action allowed within ___ days after receipt of proof of lossNo legal action may be brought after ___ years

Florida_L&H_LawSupplement_book.indb 4 11/11/2015 2:36:24 PM

5Law Supplement

Group Health Insurance

5 people25 hours

25 members1 year

15 members

Trustee group must cover at least ___ peopleFull-time employees must work ___ hours or moreAssociationsAssociations must have at least ___ membersAssociations must have been in existence at least ___ year(s)At least ___ members must enroll in health plan

20 employees

63 days14 days30 days115%

18 months

11 months

Continuation of Coverage “Mini-COBRA”Florida’s “Mini-COBRA” is for small employers employing less than ___ employees

■ A qualified beneficiary must give written notice within ___ days ■ Election and premium notice form are sent within ___ days ■ Premium payment and election must be within made ___ days ■ Continuation of coverage premium may not exceed ___ of group premium ■ Coverage ends ___ months after qualifying event ■ If disabled (according to Social Security), extension of coverage for an additional

___ months

63 days

200%

Conversion (converted policy issued without evidence of insurability) ■ Application and first premium must be paid no later than ___ days after

termination of group policy ■ Premium may not exceed ___ % of the standard risk rate

Medicare Supplement Insurance

6 months30 days

6-month

6-month

Required ProvisionsMaximum pre-existing conditions exclusion periodFree-look periodOpen enrollment period—65 and older

■ The ___ -month period after an individual is age 65 and older and is first enrolled in Medicare Part B

Open enrollment period—under age 65 (due to disability or end-stage renal disease) ■ The ___ -month period in which an individual is eligible for Medicare by reason

of a disability or end-stage renal disease, and is first enrolled in Medicare Part B

5 days Replacing insurer must notify existing insurer within ___ working days

Long-Term Care Policies

5 days30 days

6 months30 days

5 months2 activities

Replacing insurer must notify existing insurer within ___ working daysFree-look period Maximum pre-existing conditions exclusion periodGrace period Reinstatement for unintentional lapseChronically Ill is defined as being unable to perform at least ___ activities of daily living for at least 90 days

Requirements for Small Employers

50 employees25 hours

Small employer employs at least one, but not more than ___ eligible employeesEligible employees must work ___ hours or more

30 days30 days30 days

Enrollment Periods (minimum number of days to enroll) ■ Initial enrollment period ■ Annual open enrollment ■ Special enrollment period

Florida_L&H_LawSupplement_book.indb 5 11/11/2015 2:36:24 PM

Florida_L&H_LawSupplement_book.indb 6 11/11/2015 2:36:24 PM

s e c t i o n

7

2s e c t i o n

7

Class Notes

HOW TO USE: The class notes are an excellent place to start when

studying the state specific laws and regulations. The class notes are a sum-

mary of the key law supplement topics. For some students the class notes

may be their primary section to study the law and regulation exam mate-

rial.

Florida_L&H_LawSupplement_book.indb 7 11/11/2015 2:36:24 PM

8 Law Supplement

Florida_L&H_LawSupplement_book.indb 8 11/11/2015 2:36:24 PM

9Law Supplement

Florida_L&H_LawSupplement_book.indb 9 11/11/2015 2:36:25 PM

10 Law Supplement

Florida_L&H_LawSupplement_book.indb 10 11/11/2015 2:36:25 PM

11Law Supplement

Florida_L&H_LawSupplement_book.indb 11 11/11/2015 2:36:25 PM

12 Law Supplement

Florida_L&H_LawSupplement_book.indb 12 11/11/2015 2:36:26 PM

13Law Supplement

Florida_L&H_LawSupplement_book.indb 13 11/11/2015 2:36:26 PM

14 Law Supplement

Florida_L&H_LawSupplement_book.indb 14 11/11/2015 2:36:26 PM

15Law Supplement

Florida_L&H_LawSupplement_book.indb 15 11/11/2015 2:36:27 PM

16 Law Supplement

Florida_L&H_LawSupplement_book.indb 16 11/11/2015 2:36:28 PM

17Law Supplement

Florida_L&H_LawSupplement_book.indb 17 11/11/2015 2:36:28 PM

18 Law Supplement

Florida_L&H_LawSupplement_book.indb 18 11/11/2015 2:36:29 PM

19Law Supplement

Florida_L&H_LawSupplement_book.indb 19 11/11/2015 2:36:29 PM

20 Law Supplement

Florida_L&H_LawSupplement_book.indb 20 11/11/2015 2:36:29 PM

21Law Supplement

Florida_L&H_LawSupplement_book.indb 21 11/11/2015 2:36:30 PM

22 Law Supplement

Florida_L&H_LawSupplement_book.indb 22 11/11/2015 2:36:30 PM

23Law Supplement

Florida_L&H_LawSupplement_book.indb 23 11/11/2015 2:36:30 PM

24 Law Supplement

Florida_L&H_LawSupplement_book.indb 24 11/11/2015 2:36:31 PM

25Law Supplement

Florida_L&H_LawSupplement_book.indb 25 11/11/2015 2:36:31 PM

26 Law Supplement

Florida_L&H_LawSupplement_book.indb 26 11/11/2015 2:36:31 PM

27Law Supplement

Florida_L&H_LawSupplement_book.indb 27 11/11/2015 2:36:32 PM

28 Law Supplement

Florida_L&H_LawSupplement_book.indb 28 11/11/2015 2:36:32 PM

29Law Supplement

Florida_L&H_LawSupplement_book.indb 29 11/11/2015 2:36:32 PM

30 Law Supplement

Florida_L&H_LawSupplement_book.indb 30 11/11/2015 2:36:33 PM

31Law Supplement

Florida_L&H_LawSupplement_book.indb 31 11/11/2015 2:36:33 PM

32 Law Supplement

Florida_L&H_LawSupplement_book.indb 32 11/11/2015 2:36:34 PM

33Law Supplement

Florida_L&H_LawSupplement_book.indb 33 11/11/2015 2:36:34 PM

34 Law Supplement

Florida_L&H_LawSupplement_book.indb 34 11/11/2015 2:36:34 PM

35Law Supplement

Florida_L&H_LawSupplement_book.indb 35 11/11/2015 2:36:35 PM

36 Law Supplement

Florida_L&H_LawSupplement_book.indb 36 11/11/2015 2:36:35 PM

37Law Supplement

Florida_L&H_LawSupplement_book.indb 37 11/11/2015 2:36:35 PM

38 Law Supplement

Florida_L&H_LawSupplement_book.indb 38 11/11/2015 2:36:36 PM

39Law Supplement

Florida_L&H_LawSupplement_book.indb 39 11/11/2015 2:36:37 PM

40 Law Supplement

Florida_L&H_LawSupplement_book.indb 40 11/11/2015 2:36:37 PM

41Law Supplement

Florida_L&H_LawSupplement_book.indb 41 11/11/2015 2:36:38 PM

42 Law Supplement

Florida_L&H_LawSupplement_book.indb 42 11/11/2015 2:36:38 PM

43Law Supplement

Florida_L&H_LawSupplement_book.indb 43 11/11/2015 2:36:38 PM

44 Law Supplement

Florida_L&H_LawSupplement_book.indb 44 11/11/2015 2:36:39 PM

45Law Supplement

Florida_L&H_LawSupplement_book.indb 45 11/11/2015 2:36:39 PM

46 Law Supplement

Florida_L&H_LawSupplement_book.indb 46 11/11/2015 2:36:40 PM

47Law Supplement

Florida_L&H_LawSupplement_book.indb 47 11/11/2015 2:36:40 PM

48 Law Supplement

Florida_L&H_LawSupplement_book.indb 48 11/11/2015 2:36:40 PM

49Law Supplement

Florida_L&H_LawSupplement_book.indb 49 11/11/2015 2:36:41 PM

50 Law Supplement

Florida_L&H_LawSupplement_book.indb 50 11/11/2015 2:36:41 PM

51Law Supplement

Florida_L&H_LawSupplement_book.indb 51 11/11/2015 2:36:41 PM

52 Law Supplement

Florida_L&H_LawSupplement_book.indb 52 11/11/2015 2:36:42 PM

53Law Supplement

Florida_L&H_LawSupplement_book.indb 53 11/11/2015 2:36:43 PM

54 Law Supplement

Florida_L&H_LawSupplement_book.indb 54 11/11/2015 2:36:43 PM

55Law Supplement

Florida_L&H_LawSupplement_book.indb 55 11/11/2015 2:36:43 PM

56 Law Supplement

Florida_L&H_LawSupplement_book.indb 56 11/11/2015 2:36:44 PM

57Law Supplement

Florida_L&H_LawSupplement_book.indb 57 11/11/2015 2:36:44 PM

58 Law Supplement

Florida_L&H_LawSupplement_book.indb 58 11/11/2015 2:36:44 PM

59Law Supplement

Florida_L&H_LawSupplement_book.indb 59 11/11/2015 2:36:45 PM

60 Law Supplement

Florida_L&H_LawSupplement_book.indb 60 11/11/2015 2:36:45 PM

61Law Supplement

Florida_L&H_LawSupplement_book.indb 61 11/11/2015 2:36:46 PM

62 Law Supplement

Florida_L&H_LawSupplement_book.indb 62 11/11/2015 2:36:46 PM

63Law Supplement

Florida_L&H_LawSupplement_book.indb 63 11/11/2015 2:36:47 PM

64 Law Supplement

Florida_L&H_LawSupplement_book.indb 64 11/11/2015 2:36:47 PM

65Law Supplement

Florida_L&H_LawSupplement_book.indb 65 11/11/2015 2:36:47 PM

66 Law Supplement

Florida_L&H_LawSupplement_book.indb 66 11/11/2015 2:36:48 PM

67Law Supplement

Florida_L&H_LawSupplement_book.indb 67 11/11/2015 2:36:48 PM

68 Law Supplement

Florida_L&H_LawSupplement_book.indb 68 11/11/2015 2:36:49 PM

69Law Supplement

Florida_L&H_LawSupplement_book.indb 69 11/11/2015 2:36:49 PM

70 Law Supplement

Florida_L&H_LawSupplement_book.indb 70 11/11/2015 2:36:50 PM

71Law Supplement

Florida_L&H_LawSupplement_book.indb 71 11/11/2015 2:36:50 PM

72 Law Supplement

Florida_L&H_LawSupplement_book.indb 72 11/11/2015 2:36:51 PM

73Law Supplement

Florida_L&H_LawSupplement_book.indb 73 11/11/2015 2:36:51 PM

74 Law Supplement

Florida_L&H_LawSupplement_book.indb 74 11/11/2015 2:36:52 PM

75Law Supplement

Florida_L&H_LawSupplement_book.indb 75 11/11/2015 2:36:52 PM

76 Law Supplement

Florida_L&H_LawSupplement_book.indb 76 11/11/2015 2:36:53 PM

77Law Supplement

Florida_L&H_LawSupplement_book.indb 77 11/11/2015 2:36:53 PM

78 Law Supplement

Florida_L&H_LawSupplement_book.indb 78 11/11/2015 2:36:53 PM

79Law Supplement

Florida_L&H_LawSupplement_book.indb 79 11/11/2015 2:36:54 PM

80 Law Supplement

Florida_L&H_LawSupplement_book.indb 80 11/11/2015 2:36:55 PM

81Law Supplement

Florida_L&H_LawSupplement_book.indb 81 11/11/2015 2:36:55 PM

82 Law Supplement

Florida_L&H_LawSupplement_book.indb 82 11/11/2015 2:36:56 PM

s e c t i o n

83

3s e c t i o n

83

Detailed Text

HOW TO USE: All state specific topics in your state’s exam content

outline law and regulation section are covered in this detailed text. Stu-

dents are encouraged to read the text for in-depth descriptions of the state’s

insurance laws and regulations. In addition, some topics are not covered

in the Cram Sheets and Class Notes, and are only covered in the Detailed

Text.

Florida_L&H_LawSupplement_book.indb 83 11/11/2015 2:36:56 PM

84 Law Supplement

I. FLORIDA STATUTES, RULES, AND REGULATIONS COMMON TO ALL LINES

A. FINANCIAL SERVICES REGULATION

1. Chief Financial Officer (CFO) [Sec. 20.121]The Chief Financial Officer is an independently elected official and a member

of the Governor’s cabinet. The CFO serves as head of the Department of Financial Services and as a member of the Financial Services Commission.

The CFO directly oversees 15 divisions and offices, including a Division of Ac-counting and Auditing (Bureau of Unclaimed Property), a Division of Insurance Agents and Agency Services, a Division of Insurance Fraud, a Division of Consumer Services, and the Office of the Insurance Consumer Advocate, all five of which have a role in regulating insurance. Therefore, regulation of insurance agents is directly administered by the CFO, as is insurance fraud and insurance consumer protection. The CFO, the Financial Services Commission, and the Commissioner of the Office of Insurance Regulation administer the insurance laws of Florida.

2. Financial Services Commission [Sec. 20.121]The Financial Services Commission is composed of the Governor, the CFO, the

Attorney General, and the Commissioner of Agriculture. This Commission in turn supervises the Office of Insurance Regulation and the Office of Financial Regulation.

a. Office of Financial RegulationThe Office of Financial Regulation (OFR) is responsible for all activi-

ties of the Financial Services Commission relating to the regulation of banks, credit unions, other financial institutions, finance companies, and the securities industry. The head of the Office is the Director or Commissioner of Financial Regulation. The OFR includes a Bureau of Financial Investigations that may investigate suspected wrongdoing, both inside and outside of Florida, and may refer suspected violations of criminal law to state or federal law enforcement or prosecutorial agencies.

b. Office of Insurance Regulation The Office of Insurance Regulation (OIR) is responsible for all activi-

ties of the Financial Services Commission relating to the regulation of insur-ers and other risk-bearing entities. The head of the Office is the Director or Commissioner of Insurance Regulation. The specific duties of the Office include the following:

■ Insurer licensing ■ Rate-making supervision ■ Policy forms approval ■ Market conduct investigation ■ Issuing insurer certificates of authority ■ Assessing insurer solvency ■ Regulating viatical settlements ■ Regulating premium financing arrangements

■ Administrative supervision

Florida_L&H_LawSupplement_book.indb 84 11/11/2015 2:36:56 PM

85Law Supplement

B. DEPARTMENT OF FINANCIAL SERVICES The Department of Financial Services, headed by the Chief Financial Officer and the Commissioner of the Office of Insurance Regulation, oversees the insurance industry in accordance with the provisions of the Insurance Code. Members of the Department have broad administrative, quasi-legisla-tive (rule-making), and quasi-judicial powers in order to carry out their responsibilities.

1. General duties and powers [Sec. 624.307, 624.422] The Department and respective offices have the following powers and duties.

■ They enforce the Insurance Code and carry out those duties set forth by the code. ■ Their powers and authority may be expressed or implied in the Insurance Code. ■ They may conduct any investigation of insurance matters expressed in the code,

determine if a person has violated the code, or obtain information to administer the code.

■ They can collect, propose, publish, or disseminate information regarding the duties imposed upon it by the code.

■ They shall have additional powers and duties as provided by other laws of the state.

■ The Department and Office may each employ actuaries. Actuaries employed pursuant to this paragraph shall be members of the Society of Actuaries or the Casualty Actuarial Society.

■ Florida-licensed insurers must designate the CFO as their attorney to receive service of all legal process issued against them in any Florida civil action.

2. Policyholders’ rights [Sec. 626.9641] The principles expressed in the follow-ing statements serve as standards to be followed by the Department, Commission, and Office in exercising their powers and duties, in exercising administrative discretion, in dispensing administrative interpretations of the law, and in adopting rules.

■ Policyholders shall have the right to competitive pricing practices and marketing methods that enable them to determine the best value among comparable policies.

■ Policyholders shall have the right to obtain comprehensive coverage. ■ Policyholders shall have the right to insurance advertising and other selling

approaches that provide accurate and balanced information on the benefits and limitations of a policy.

■ Policyholders shall have a right to an insurance company that is financially stable. ■ Policyholders shall have the right to be serviced by a competent, honest insurance

agent or broker. ■ Policyholders shall have the right to a readable policy. ■ Policyholders shall have the right to an insurance company that provides an eco-

nomic delivery of coverage and that tries to prevent losses. ■ Policyholders shall have the right to a balanced and positive regulation by the

Department, Commission, and Office.

Florida_L&H_LawSupplement_book.indb 85 11/11/2015 2:36:56 PM

86 Law Supplement

C. OFFICE OF INSURANCE REGULATION [SEC. 624.302] In addition to duties and powers listed previously, the Office of Insurance Regulation is responsible for the following areas:

1. Policy approval authority rates and forms [Sec. 627.410, Rule 69O-149.002-023]

a. A basic insurance policy, annuity contract, application form, group certificates issued under a master contract delivered in this state, rider, endorsement, or renewal certificate may not be delivered in Florida unless the form has been filed with the Office and has been approved by the Office.

b. Every such filing must be made at least 30 days in advance of any such use or delivery. At the expiration of the 30 days, the form filed will be deemed approved unless prior thereto it has been affirmatively approved or disapproved by order of the Office.

c. The Office may, for cause, withdraw a previous approval.

d. An insurer may not deliver, issue for delivery, or renew in this state any health insurance policy form until it has filed with the Office a copy of every applicable rating manual, rating schedule, change in rating manual, and change in rating schedule.

2. Market conduct examinations [Sec. 624.316, Rule 69O-138.001] The Office of Insurance Regulation may examine each insurer as often as may be warranted for the protection of the policyholders and in the public interest, and must examine each domestic insurer not less frequently than once every five years.

a. In lieu of making its own examination, the Office may accept a full report of the last recent examination of a foreign insurer, certified by the insurance supervisory official of another state.

b. The examination by the Office of an alien insurer shall be limited to the alien insurer’s insurance transactions and affairs in the United States, except as other-wise required by the Office.

c. The examination may include examination of the affairs, transactions, accounts, and records relating directly or indirectly to the insurer and of the assets of the insurer’s managing general agents and controlling or controlled person.

d. To facilitate uniformity in examinations, the commission may use the methods in the Market Conduct Examiners Handbook and the Financial Condition Examiners Handbook of the National Association of Insurance Commissioners.

Florida_L&H_LawSupplement_book.indb 86 11/11/2015 2:36:56 PM

87Law Supplement

e. The Office will examine each insurer applying for an initial certificate of author-ity to transact insurance in this state before granting the initial certificate.

f. An examination under this section must be conducted at least once every year with respect to a domestic insurer that has continuously held a certificate of authority for less than three years. The examination must cover the preceding fiscal year or the period since the last examination of the insurer.

3. Agency actions The Office of Insurance Regulation major areas of responsibility are as follows:

■ Organizing and licensing of companies, including establishment of the initial financial requirements for insurance companies

■ Policing against unauthorized insurance activities ■ Continuing regulation of insurance company activities, including policy forms

and provisions and rates (although direct rate regulation is not applicable to life insurance)

■ Supervising the methods of obtaining business, including licensing of agents and control of unfair trade and advertising practices

■ Monitoring the financial condition of insurers, including specification of appropri-ate investment categories and appropriate methodology for developing liabilities

■ Rehabilitating or liquidating insurers where necessary

4. Investigation [Sec. 624.317, .321, 626.601] If the Department of Financial Services or Office of Insurance Regulation believe that any person has violated or is violating any provision the Insurance Code, it will conduct an investigation.

a. The Department of Financial Services may investigate the accounts, records, documents, and transactions pertaining to insurance affairs of any general agent, surplus lines agent, adjuster, managing general agent, insurance agent, insurance agency, customer representative, service representative, or other person subject to its jurisdiction.

b. The Office of Insurance Regulation will conduct such investigation as it deems necessary of the accounts, records, documents, and transactions pertaining to the insurance affairs of any:

■ administrator, service company, or other person subject to its jurisdiction; ■ person having a contract or power of attorney under which she or he enjoys

in fact the exclusive or dominant right to manage or control an insurer; or ■ person engaged in or proposing to be engaged in the promotion or formation of

— a domestic insurer, — an insurance holding corporation, or — a corporation to finance a domestic insurer or in the production of the

domestic insurer’s business.

Florida_L&H_LawSupplement_book.indb 87 11/11/2015 2:36:56 PM

88 Law Supplement

c. During an examination or investigation, the Department or Office may ■ administer oaths, examine and cross-examine witnesses, receive evidence;

and ■ subpoena witnesses, compel their attendance and testimony, and require by

subpoena the production of books, papers, records, files, correspondence, documents, or other evidence that is relevant to the inquiry.

d. Any individual who willfully obstructs an examination or investigation is guilty of a misdemeanor.

D. OFFICE OF FINANCIAL REGULATION

1. General duties and powers [Sec. 655.012] In addition to other powers con-ferred by Florida statutes, the Office of Financial Regulation has the following powers and duties:

a. General supervision over all state financial institutions, their subsidiaries, and service corporations

b. Access to all books and records of all persons over whom the Office exercises general supervision as is necessary for the performance of the duties and func-tions of the Office

c. Power to issue orders and declaratory statements

d. Provide for and promote safe and sound conduct of the business of financial institutions

e. Maintain public confidence in the financial institutions subject to the financial institutions’ codes

f. Protect the interests of the public in the safety and soundness, and the preser-vation, of the financial institution system in Florida and the protection of the interests of the depositors and creditors of financial institutions

2. Agency actions [Sec 655.031] In imposing any administrative remedy or pen-alty, the Office will take into account the appropriateness of the penalty with respect to the size of the financial resources and good faith of the person charged, the gravity of the violation, the history of previous violations, and such other matters as justice may require.

a. Cease and desist orders [Sec. 655.033] The Office may issue and serve upon any state financial institution a complaint stating charges whenever the Office has reason to believe that such state financial institution is engaging in or has engaged in conduct that is an:

■ unsafe or unsound practice; ■ violation of any law relating to the operation of a financial institution;

Florida_L&H_LawSupplement_book.indb 88 11/11/2015 2:36:56 PM

89Law Supplement

■ violation of any rule of the commission; ■ violation of any order of the Office; ■ breach of any written agreement with the Office; ■ prohibited act or practice pursuant to Sec. 655.0322; or ■ willful failure to provide information or documents to the Office or any

appropriate federal agency, or any of its representatives, upon written request.

1.) The complaint must contain the statement of facts and notice of opportu-nity for a hearing.

2.) If no hearing is requested within the time allowed, or if a hearing is held and the Office finds that any of the charges are true, the Office may enter an order directing the state financial institution to cease and desist from engaging in the conduct complained of and to take corrective action.

3.) If the state financial institution fails to respond to the complaint within the time allotted, such failure constitutes a default and justifies the entry of a cease and desist order.

4.) Whenever the Office finds that the conduct is likely to cause insolvency, substantial dissipation of assets or earnings of the state financial institu-tion or substantial prejudice to the depositors, members, or shareholders, it may issue an emergency cease and desist order requiring the state financial institution to immediately cease and desist from engaging in the conduct complained of and to take corrective action.

■ The emergency order is effective immediately upon service of a copy of the order upon the state financial institution and remains effective for 90 days.

b. Injunctions [Sec. 655.034] Whenever a violation of the financial institu-tions’ codes is threatened or impending and such violation will cause substantial injury to a state financial institution or to the depositors, members, creditors, or stockholders thereof, the circuit court has jurisdiction to hear any complaint filed by the Office and, upon proper proof, to issue an injunction restraining such violation or granting other such appropriate relief.

3. Investigations [Sec. 655.032] The Office may make investigations, within or outside this state, which it deems necessary to determine whether a person has vio-lated or is about to violate any provision of the Florida financial institutions codes or of the rules adopted by the commission. In an investigation, the Office has the follow-ing powers:

a. Administer oaths and affirmations

b. Take testimony and depositions

Florida_L&H_LawSupplement_book.indb 89 11/11/2015 2:36:56 PM

90 Law Supplement

c. Issue subpoenas to require persons to be or appear before the Office at a specific time and place, and to bring books, records, and documents for inspection

■ In the event of noncompliance with a subpoena, the Office may petition the circuit court for an order requiring the subpoenaed person to appear and testify and to produce such books, records, and documents.

■ Failure to comply with an order granting a petition for enforcement of a subpoena is a contempt of court.

d. Assess reasonable and necessary investigation expenses incurred by the Office against the person or entity being investigated

Financial Svcs CommissionMembers—Governor, Chief

Financial Officer (CFO)Attorney General, Agriculture

Commissioner

Ofc Insurance RegulationCommissioner of Ins Reg

Licensing, Rates, Forms,Market Conduct, Claims,

Certs of Authority, Solvency,Viaticals, Premium Financing

Ofc Financial RegulationCommissioner of Fin Reg

Banks, Credit Unions,Finance Companies,Securities Industry

Dept Financial SvcsChief Financial Officer (CFO)

4 related to insurance—Accounting & Auditing,

Insurance Fraud, ConsumerServices, Office of Insurance Advocate

E. DEFINITIONS

1. Insurance transaction [Sec. 624.10] Includes any of the following provisions of the Insurance Code:

■ Solicitation or inducement to purchase insurance ■ Preliminary negotiations toward the sale of insurance ■ Effectuation of a contract of insurance ■ Transaction of matters subsequent to effectuation of a contract of insurance and

arising out of it

2. Certificate of authority [Sec. 624.401] No person may act as an insurer, directly or indirectly transacting insurance, in Florida except as authorized by a certifi-cate of authority issued to the insurer by the Office. Any person who acts as an insurer, transacts insurance, or otherwise engages in insurance activities without a certificate of authority in violation of this section commits a felony of the third degree.

3. Authorized and unauthorized companies/admitted and non-admitted companies [Sec. 624.09] An authorized insurer is one duly authorized by a cer-tificate of authority issued by the Office to transact insurance in this state. An unau-thorized insurer is an insurer that does not have a certificate of authority.

4. Unlicensed entities [Sec. 626.901] No person may directly or indirectly act as agent for, or otherwise represent or aid on behalf of another, any insurer not then authorized to transact such insurance in Florida. If an unauthorized insurer fails to pay in full or in part any claim or loss within the provisions of any insurance contract that is entered into in violation of this section, any person who knew or reasonably should

Florida_L&H_LawSupplement_book.indb 90 11/11/2015 2:36:57 PM

91Law Supplement

have known that such contract was entered into in violation of this section and who solicited, negotiated, took application for, or effectuated such insurance contract is liable to the insured for the full amount of the claim or loss not paid.

a. Penalties for violation [Sec. 626.902] In addition to any other penal-ties provided in the Insurance Code, any insurance agent licensed in Florida who knowingly represents or aids an unauthorized insurer in violation of Section 626.901 commits a felony of the third degree.

5. A mail order insurance company is one that operates principally by mail without personal agent solicitation of prospects. Florida law prohibits unauthorized mail order insurers from soliciting in Florida. The transaction of insurance, including the applica-tion for insurance, must be taken by and the policy delivered through a licensed and appointed Florida agent.

F. LICENSING [SEC. 626.011–939]

1. Purpose The purpose of the Florida licensing statutes is to help protect the general public by requiring a minimum level of insurance knowledge and competence of the licensee. In addition, licensees are expected to have an understanding of Florida insur-ance statutes and regulations.

2. License types [Sec. 626.015]

a. Agent means a general lines agent, life agent, health agent, or title agent. The term agent does not include a customer representative, limited customer repre-sentative, or service representative.

b. Adjuster [Sec. 626.851, .854, .8548]

1.) A public adjuster is any person, except a licensed attorney exempt under Florida law who, for compensation, prepares, completes, or files an insur-ance claim form for an insured or third-party claimant. The term also includes any person who, for compensation, acts on behalf of or aids an insured or third-party claimant in negotiating or effecting the settlement of claims for loss or damage covered by an insurance contract.

2.) An all-lines adjuster is a person who is self-employed, employed by an insurer, or an independent adjusting firm, and who undertakes on behalf of an insurer to ascertain and determine the amount of any claim, loss, or damage payable under an insurance contract or undertakes to effect settle-ment of such claim, loss, or damage.

c. Agency [Sec. 626.015, .112, 626.015(18), .311]

1.) Insurance agency means a business location at which an individual, firm, partnership, corporation, association, or other entity engages in any activ-ity that by law may be performed only by a licensed insurance agent. The term agency does not include an insurer or an adjuster.

Florida_L&H_LawSupplement_book.indb 91 11/11/2015 2:36:57 PM

92 Law Supplement

2.) No individual, firm, partnership, corporation, association, or any other entity shall act in its own name or under a trade name, directly or indi-rectly, as an insurance agency, unless it possesses an insurance agency license for each place of business.

d. Unaffiliated agent [Sec. 626.015(18), .311] An unaffiliated agent is a licensed agent (excluding a limited lines agent) who is not appointed by or affili-ated with any insurer, but is self-appointed. This agent acts as an independent consultant in the business of analyzing insurance policies, providing insurance advice or counseling, or making specific recommendations or comparisons of insurance products for a fee. The fee must be established in advance by a writ-ten contract signed by the parties. Unaffiliated agents are prohibited from being affiliated with an insurer, insurer-appointed insurance agent, or insurance agency contracted with or employing insurer-appointed insurance agents. However, unaffiliated agents may continue to receive commissions on sales made before the date of appointment as an unaffiliated insurance agent, as long as the agent discloses the receipt of commissions to the client when making recommenda-tions or evaluating products of the entity from which commissions are received. Unaffiliated insurance agents will pay the same appointment fees required of agents appointed by insurers.

3. Appointments [Sec. 626.112, .311, .381, .431, .471, .511, Rule 69B-211.004]

a. No person may act as an insurance agent unless she is currently licensed by the Department and appointed by an insurer or other appropriate appointing entity.

b. Unaffiliated agents, however, must appoint themselves and may not be appointed by an insurer.

c. An individual who fails to maintain an appointment with an insurer or appoint-ing entity during any 48-month period will not be granted an appointment by the Department until he or she qualifies as a first-time applicant.

d. Term of appointment [Rule 69B-211.004]

1.) In the case of natural persons, new appointments or appointments being continued, which are effectuated in a licensee’s birth month, shall expire 24 months later on the last day of the licensee’s birth month and shall be subject to renewal at that time by the entity for which they are appointed.

2.) In the case of entities other than natural persons, new appointments or appointments being continued, which are effectuated in the same month a licensee was first licensed as an insurance representative, shall expire 24 months later on the last day of the licensee’s license issue month and shall be subject to renewal at that time by the entity for which they are appointed.

Florida_L&H_LawSupplement_book.indb 92 11/11/2015 2:36:57 PM

93Law Supplement

3.) Appointments effectuated during any month other than the licensee’s birth month in the case of natural persons, or during the license issue month in the case of entities other than natural persons, shall be valid for not less than 24 months and no longer than 36 months. This minimum and maximum number of months are necessary to convert the original issue month to the licensee’s birth month or license issue month, which-ever the case may be.

4.) Appointments renew every 24 months thereafter unless suspended, revoked, or otherwise terminated at an earlier date.

e. Appointment termination [Sec. 626.471, .511]

1.) Except when appointment termination is based on the suspension or revo-cation of an appointee’s license, an appointing entity may terminate its appointment of any appointee at any time, with at least 60 days’ advance written notice.

2.) Within 30 days after terminating the appointment of an appointee, the appointing entity must file written notice with the Department including the reasons and facts involved in the termination.

4. License requirements [Sec. 626.171 .191, .281, .7851, .8311] Applicants for an insurance license must file a written application, com pleted under oath and signed by the applicant, meet the required qualifica tions, and pay all appli-cable fees in advance to the Department. The applica tion will require applicants to provide their full name, age, Social Security number, residence address, business address, mailing address, contact phone numbers, and email address. Applicants must also provide proof that they have completed, or are in the process of completing, any required prelicens ing education.

a. Prelicensing education [Sec. 626.7851, .8311]

1.) Applicants for a life agent license, except those who have a Chartered Life Underwriter® (CLU®) designation, must meet the following knowl-edge, experience, or instruction requirements within four years immedi-ately preceding the license application:

■ Completed 40 hours of approved coursework in life insurance, annuities, and variable contracts, including three hours of ethics and instruction on unauthorized entities engaging in the business of insurance

■ Completed a minimum of 60 hours of approved coursework in mul-tiple areas of insurance, which included life insurance, annuities, and variable contracts, including three hours of ethics and instruction on unauthorized entities engaging in the business of insurance

— For example, applicants for a Florida Health & Life (including Annuities & Variable Contracts) license only need to complete 60 prelicensing hours instead of having to meet the 40-hour requirement for both life agent and health agent

Florida_L&H_LawSupplement_book.indb 93 11/11/2015 2:36:57 PM

94 Law Supplement

■ Earned or maintained an active Chartered Financial Consultant® (ChFC®) or Fellow, Life Management Institute (FLMI) designations

■ Held an active license in life insurance in another state that grants reciprocal treatment to licensees formerly licensed in Florida

■ Been employed by the Department or Office for at least one year, full time in life insurance regulatory matters, and who was not terminated for cause

2.) Applicants for a health agent license, except those who have a Chartered Life Underwriter® (CLU®) designation, must meet the following knowl-edge, experience, or instruction requirements within four years immedi-ately preceding the license application:

■ Completed 40 hours of approved coursework in health insurance, including three hours of ethics and instruction on unauthorized entities engaging in business of insurance, to include the Florida Nonprofit Multiple-Employer Welfare Arrangement Act and the Employee Retirement Income Security Act, as it relates to the provi-sion of health insurance by employers to their employees and the regulation thereof

■ Completed a minimum of 60 hours of approved coursework in multi-ple areas of insurance, three hours of ethics and instruction on subject matter of unauthorized entities engaging in business of insurance

— For example, applicants for a Florida Health & Life (including Annuities & Variable Contracts) license only need to complete 60 prelicensing hours instead of having to meet the 40-hour requirement for both life agent and health agent

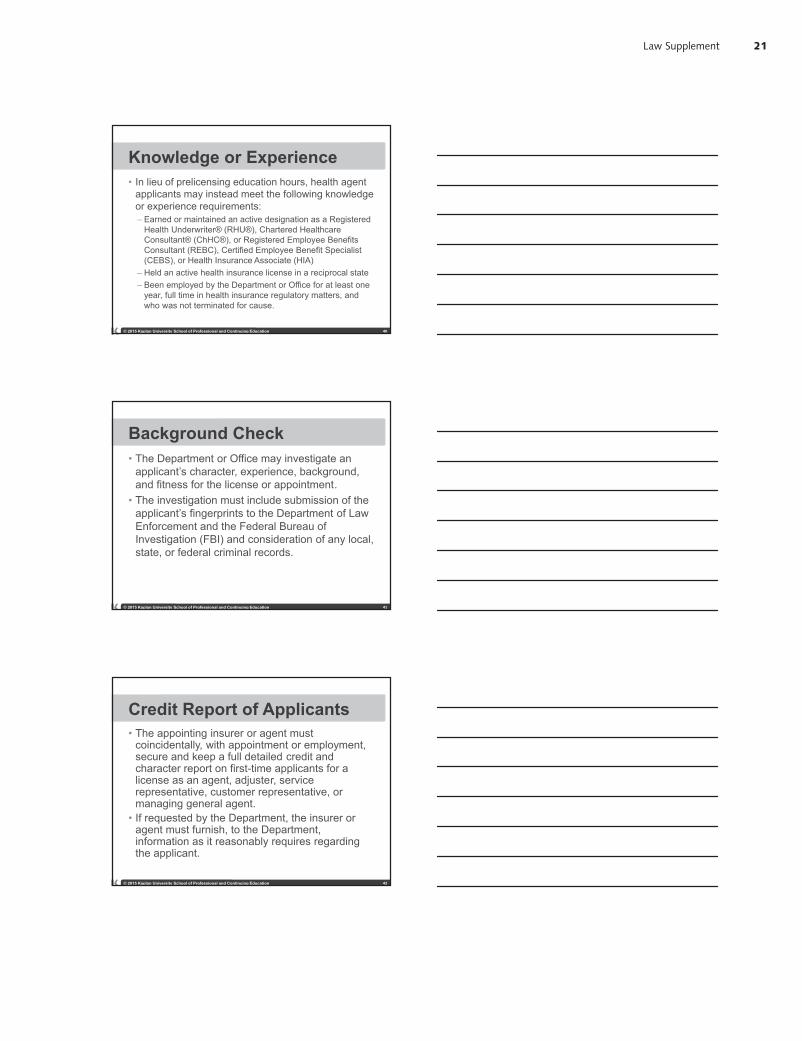

■ Earned or maintained an active designation as a Registered Health Underwriter® (RHU®), Chartered Healthcare Consultant® (ChHC®), or Registered Employee Benefits Consultant® (REBC®), Certified Employee Benefit Specialist (CEBS), or Health Insurance Associate (HIA)

■ Held an active license in health insurance in another state that grants reciprocal treatment to licensees formerly licensed in Florida

■ Been employed by the Department or Office for at least one year, full time in health insurance regulatory matters, and who was not termi-nated for cause

b. Background check [Sec. 626.201, .521, .621, .651; 624.34]

1.) The Department or Office may ask questions, in addition to those con-tained in the application, to any applicant for license or appointment, any license renewal, or license reinstatement, relating to the applicant’s qualifications, residence, prospective place of business, and any other mat-ter that, in the opinion of the Department or Office, is deemed necessary or advisable for the protection of the public and to ascertain the applicant’s qualifications.

Florida_L&H_LawSupplement_book.indb 94 11/11/2015 2:36:57 PM

95Law Supplement

2.) The Department or Office may, upon completion of the application, make such further investigation as it may deem advisable of the applicant’s char-acter, experience, background, and fitness for the license or appointment.

3.) An inquiry or investigation of the applicant’s qualifications, character, experience, background, and fitness must include submission of the appli-cant’s fingerprints to the Department of Law Enforcement and the Federal Bureau of Investigation and consideration of any state criminal records, federal criminal records, or local criminal records obtained from these agencies or from local law enforcement agencies.

4.) Credit or character report of license applicants [Sec. 626.521]

a.) For each applicant who for the first time in this state is applying and qualifying for a license as agent, adjuster, service representative, customer representative, or managing general agent, the appoint-ing insurer or agent will coincidentally with such appointment or employment secure and thereafter keep on file a full detailed credit and character report made by an established and reputable indepen-dent reporting service.

b.) If requested by the Department, the insurer or agent will furnish to the Department information as it reasonably requires regarding the applicant and investigation.

c. License examination [Sec. 626.221–291]

1.) Scope of examinations [Sec. 626.241] Applicants for an agent, customer representative, or adjuster license must pass an examination that will test the applicant’s ability, competence, and knowledge of the kinds of insurance to be handled under the license applied for (life, health, general lines, etc.). The exam will also cover the duties and responsibilities of a licensee and the pertinent provisions of Florida law.

2.) Within 30 days after the applicant has passed the license exam, the Department will notify the applicant and issue the insurance license. For those applicants who have passed the examination prior to submitting the license application, the Department will promptly issue the license as soon as the Department approves the application. A passing grade on an examination is valid for a period of one year. The Department will not issue a license to an applicant based on an examination taken more than one year prior to the date that an application for license is filed.

3.) An examination is not necessary for any of the following: ■ An applicant for renewal of appointment as an agent, customer

representative, or adjuster, unless the Department determines that an examination is necessary to establish the competence or trustworthi-ness of the applicant

Florida_L&H_LawSupplement_book.indb 95 11/11/2015 2:36:57 PM

96 Law Supplement

■ An applicant for a limited license as agent for travel insurance, motor vehicle rental insurance, credit insurance, in-transit and storage per-sonal property insurance, or portable electronics insurance

■ In the discretion of the Department, an applicant for reinstatement of license or appointment as an agent, customer representative, or all-lines adjuster whose license has been suspended within the four years before the date of application or written request for reinstatement

■ An applicant for a temporary license ■ An applicant for a license as a life or health agent who has received

the designation of Chartered Life Underwriter® (CLU®) (an applicant may be required to take an exam regarding Florida insurance laws and regulations)

■ An applicant for license as a general lines agent, personal lines agent, or all-lines adjuster who has received the designation of Chartered Property Casualty Underwriter® (CPCU®) (except an applicant may be required to take an exam regarding Florida insurance laws and regulations)

■ An applicant for license as a general lines agent or an all-lines adjuster who has received a degree in insurance from an accredited institution of higher learning approved by the Department (except an applicant may be required to take an exam regarding Florida insurance laws and regulations); qualifying degrees must indicate a minimum of 18 credit hours of insurance instruction, including specific instruction in the areas of property, casualty, health, and commercial insurance

■ An applicant for license as a life agent who has received a degree from an accredited institution of higher learning approved by the Department (except that the applicant may be examined on Florida insurance laws and regulations); qualifying degrees must indicate a minimum of nine credit hours of insurance instruction, including spe-cific instruction in the areas of life insurance, annuities, and variable insurance products

■ An applicant for license as a health agent who has received a degree from an accredited institution of higher learning approved by the Department (except that the applicant may be examined on Florida insurance laws and regulations); qualifying degrees must indicate a minimum of nine credit hours of insurance instruction, including specific instruction in the area of health insurance products

■ An applicant applying for a nonresident license, or a license transfer from another state, if the applicant holds a comparable license in another state with similar examination requirements as in Florida

4.) Retaking the examination [Sec. 626.281] An applicant for license or examination who has taken an examination and failed to make a passing grade may take additional examinations, after filing for reexami-nation together with applicable fees. Applicants may not take an exami-nation for a license type more than five times in a 12-month period.

Florida_L&H_LawSupplement_book.indb 96 11/11/2015 2:36:57 PM

97Law Supplement

5. Maintaining a license

a. Continuing education [Sec. 626.2815, Rule 69O-228] As described in the following, a licensee must complete a total of 24 hours of continuing edu-cation every two years.

1.) Each licensee except a title insurance agent must complete a five-hour update course every two years that is specific to the license held by the licensee. A licensee who holds multiple insurance licenses must complete an update course that is specific to at least one of the licenses held. The course must be developed and offered by providers and approved by the Department. The content of the course must address all lines of insurance for which examination and licensure are required and include the follow-ing subject areas:

■ Insurance law updates ■ Ethics for insurance professionals ■ Disciplinary trends and case studies ■ Industry trends ■ Premium discounts ■ Determining suitability of products and services ■ Other similar insurance-related topics the Department determines are

relevant to legally and ethically carrying out the responsibilities of the license granted

2.) Each licensee must also complete 19 hours of elective continuing educa-tion courses every two years, except in the following circumstances.

a.) A licensee who has been licensed for six or more years must complete a minimum of 15 hours of elective continuing education every two years.

b.) A licensee who has been licensed for 25 years or more and is a CLU® or a CPCU® or has a Bachelor of Science degree in risk management must complete a minimum of five hours of elective continuing educa-tion courses every two years.

c.) An individual who holds a license as a customer representative, lim-ited customer representative, title agent, motor vehicle physical dam-age and mechanical breakdown insurance agent, or an industrial fire insurance or burglary insurance agent and who is not a licensed life or health agent, must complete a minimum of five hours of continuing education courses every two years.

d.) Bail bond agents must complete the five-hour update course and a minimum of nine hours of elective continuing education courses every two years.

Florida_L&H_LawSupplement_book.indb 97 11/11/2015 2:36:57 PM

98 Law Supplement

3.) Licensees who are unable to comply with the continuing education requirements due to active duty in the military may submit a written request for a waiver to the Department.

4.) Excess hours accumulated during any two-year compliance period may be carried forward to the next compliance period.

5.) A nonresident licensee who must complete continuing education requirements in her home state may use the home state requirements to also meet Florida’s continuing education requirements if the licensee’s home state recognizes reciprocity with Florida’s continuing education requirements.

6.) The following courses may be completed in order to meet the elective continuing education course requirements:

■ Any part of the Life Underwriter Training Council Life Course Curriculum: 24 hours; Health Course: 12 hours

■ Any part of the American College CLU® curriculum: 24 hours ■ Any part of the Insurance Institute of America’s program in general

insurance: 12 hours ■ Any part of the American Institute for Property and Liability

Underwriters’ Chartered Property Casualty Underwriter® (CPCU®) professional designation program: 24 hours

■ Any part of the Certified Insurance Counselor program: 21 hours ■ Any part of the Accredited Advisor in Insurance: 21 hours

7.) The Department may immediately terminate or refuse to renew the appointment of an agent or adjuster who has been notified by the Department that his continuing education requirements have not been certified, unless the agent or adjuster has been granted an extension or waiver by the Department. The Department may not issue a new appoint-ment of the same or similar type to a licensee who was denied a renewal appointment for failing to complete continuing education as required until the licensee completes his continuing education requirement.

c. Communicating with the Department [Sec. 20.121]

1.) Insurance companies, by statute, have 20 days to respond to the Department once a complaint has been filed.

d. Recordkeeping [Sec. 626.551]

1.) A licensee must notify the Department, in writing, within 30 days after a change of name, residence address, principal business street address, mail-ing address, contact telephone numbers, including a business telephone number, or email address. A licensee who has moved her principal place of residence and principal place of business from this state shall have her license and all appointments immediately terminated by the Department.

Florida_L&H_LawSupplement_book.indb 98 11/11/2015 2:36:57 PM

99Law Supplement

Failure to notify the Department within the required time shall result in a fine not to exceed $250 for the first offense and a fine of at least $500 or suspension or revocation of the license for a subsequent offense.

e. Criminal and administrative actions [Sec. 626.451, .536]

1.) Administrative action [Sec. 626.536] Within 30 days after the final disposition of an administrative action taken against a licensee or insurance agency by a governmental agency or other regulatory agency in this or any other state or jurisdiction relating to the business of insurance, the sale of securities, or activity involving fraud, dishonesty, trustworthi-ness, or breach of a fiduciary duty, the licensee or insurance agency must submit a copy of the order, consent to order, or other relevant legal docu-ments to the Department.

2.) Criminal action [Sec. 626.621] An agent must report in writing to the Department within 30 days if he has plead guilty or nolo contendere to, or has been convicted or found guilty of, a felony or a crime punishable by imprisonment of one year or more under any state law, federal law, or law of any other country. This written report is required whether or not the agent was convicted by the court having jurisdiction of the case.

f. Appointments [Sec. 626.341, 793, .837]

1.) Agents’ additional appointments [Sec. 626.341] At any time while a licensee’s license is in force, an insurer may apply to the Department for an additional appointment as a general lines agent or life or health agent. Upon receipt of the appointment and payment of the applicable appointment taxes and fees, the Department may issue the additional appointment without further investigation concerning the applicant.

■ A life or health agent with an appointment in force may solicit applications for policies on behalf of an insurer for which she is not an appointed life or health agent if the agent simultaneously with the submission to such insurer of the application for insurance requests the insurer to appoint him or her as agent. However, no commissions may be paid by such insurer to the agent until the additional appoint-ment has been received by the Department.

2.) Excess or rejected business [Secs. 626.793, .837] An agent is permitted to place business with another company if the agent’s own company rejects the applicant or if the amount is in excess of that which the agent’s own company will write. This is called excess or rejected busi-ness. No additional license is required, and commis sions can be paid under what is known as a single case agreement. This is governed by Florida’s exchange of business law.

Florida_L&H_LawSupplement_book.indb 99 11/11/2015 2:36:57 PM

100 Law Supplement

6. Insurance agency licensing [Sec. 626.112, .172] An insurance agency owned and operated by a single licensed agent who does business in his own name, and does not employ or use other licensees, is not required to obtain an insurance agency license.

a. An agency license will continue in force until canceled, suspended, revoked, or until it is otherwise terminated or it expires by operation of law. A branch place of business of a licensed insurance agency is not required to be licensed if it transacts business under the name and federal tax identification number as the licensed agency and has designated with the Department a licensed insurance agent in charge of the branch.

b. Insurance agency applications must include the names of each owner, partner, officer, director, treasurer, and limited liability company member who directs or participates in the management or control of the agency whether by ownership of voting securities, by contract, by ownership of any agency bank account, or otherwise. The application must also include street and email addresses of the agency, any branch location(s), and the name of the agent in full-time charge of the agency and branch location(s).

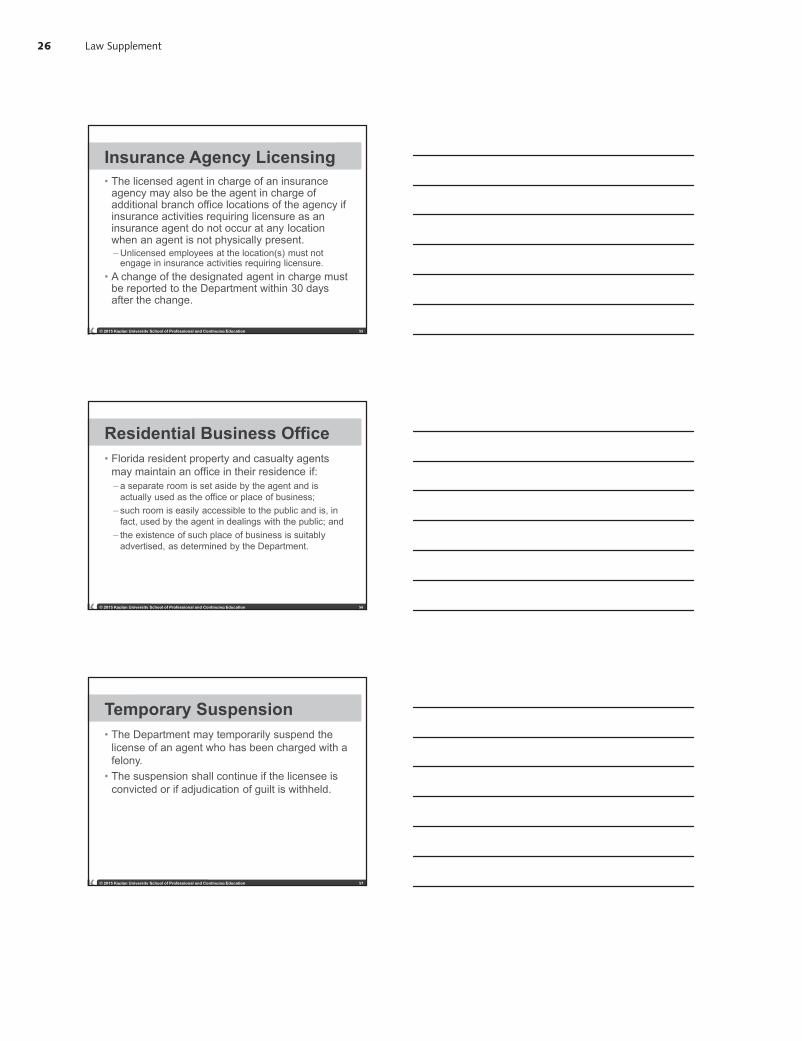

c. The licensed agent in charge of an insurance agency may also be the agent in charge of additional branch office locations if insurance activities requiring licensure as an insurance agent do not occur at any location when an agent is not physically present. Unlicensed employees at the location(s) must not engage in insurance activities requiring licensure as an insurance agent or customer repre-sentative. An insurance agency and each branch place of business of an insur-ance agency must file the name and license number of the agent in charge and the physical address of the insurance agency location with the Department at the Department’s designated website.

d. A change of the designated agent in charge is effective upon notification to the Department, which must be provided within 30 days after such change.

7. Residential business office [Sec. 626.749] Florida resident property and casualty agents may maintain an office in their residence if:

■ a separate room is set aside by the agent and is actually used as the office or place of business;

■ such room is easily accessible to the public and is used by the agent in her dealings with the public; and

■ the existence of such place of business is suitably advertised, as determined by the Department.

G. PROHIBITED PRACTICES

1. Temporary suspension for felony charge [Sec. 626.611] The Department may temporarily suspend the license of an agent who has been charged with a felony. The suspension shall continue if the licensee is convicted or if adjudication of guilt is withheld.

Florida_L&H_LawSupplement_book.indb 100 11/11/2015 2:36:57 PM

101Law Supplement

2. Denial, suspension, revocation, or refusal to renew [Sec. 626.621] The Department may deny an application, suspend, revoke, or refuse to renew the license or appointment of any applicant, agent, adjuster, customer representative, ser-vice representative, or managing general agent if it finds that the applicant, licensee, or appointee has engaged in any one or more of the following:

■ Violation of any provision of this code or of any other law applicable to the busi-ness of insurance

■ Violation of any lawful order or rule of the Department, commission, or Office ■ Failure to pay to any insurer any money belonging to the insurer ■ Violation of the provision against twisting ■ Engaging in unfair methods of competition or in unfair or deceptive acts or

practices ■ Willful overinsurance of any property or health insurance risk ■ Having been found guilty of or having pleaded guilty or nolo contendere to a

felony or a crime punishable by imprisonment of one year or more under the law of the United States of America or any state thereof or under the law of any other country, without regard to whether a judgment of conviction has been entered by the court having jurisdiction of such cases

■ If a life agent, violation of the code of ethics ■ Cheating on an examination required for licensure ■ Failure to inform the Department in writing within 30 days after pleading guilty

or nolo contendere to, or being convicted or found guilty of, any felony or a crime punishable by imprisonment of one year or more under the law of the United States or any state thereof, or under the law of any other country without regard to whether a judgment of conviction has been entered by the court having jurisdic-tion of the case

■ Knowingly aiding, assisting, procuring, advising, or abetting any person in the violation of, or to violate a provision of the insurance code or any order or rule of the Department, Commission, or Office.

■ Has been the subject of or has had a license, permit, appointment, registration, or other authority to conduct business subject to any decision, finding, injunc-tion, suspension, prohibition, revocation, denial, judgment, final agency action, or administrative order by any court of competent jurisdiction, administrative law proceeding, state agency, federal agency, national securities, commodities, or option exchange, or national securities, commodities, or option association involving a violation of any federal or state securities or commodities law or any rule or regulation adopted thereunder, or a violation of any rule or regulation of any national securities, commodities, or options exchange or national securities, commodities, or options association

■ Failure to comply with any civil, criminal, or administrative action taken by the child support enforcement program to determine paternity or to establish, modify, enforce, or collect child support

H. AGENT RESPONSIBILITIES

1. Fiduciary capacity [Sec. 626.561]

a. Definition A fiduciary is a person in a position of special trust and confidence.

Florida_L&H_LawSupplement_book.indb 101 11/11/2015 2:36:57 PM

102 Law Supplement

b. Premium accountability All premiums, return premiums, or other funds belonging to insurers or others received by an agent or insurance agency are trust funds received by the licensee in a fiduciary capacity.

c. Separate account requirements An agent or insurance agency shall keep the funds belonging to each insurer for which an agent is not appointed, other than a surplus lines insurer, in a separate account so as to allow the Department or Office to properly audit such funds. The licensee in the applicable regular course of business shall account for and pay the premiums to the insurer, insured, or other person entitled to the premium.

1.) The licensee must keep and make available to the Department or Office books, accounts, and records, as they will enable the Department or Office to determine whether such licensee is complying with the provisions of this code. Every licensee shall preserve books, accounts, and records per-taining to a premium payment for at least three years after payment.

2.) The three-year requirement does not apply to insurance binders when no policy is ultimately issued and no premium is collected.

d. Any agent or insurance agency that diverts or misappropriates fiduciary funds commits the offense specified in the following:

■ If the funds diverted or misappropriated are $300 or less, a misdemeanor of the first degree

■ If the funds diverted or misappropriated are more than $300, but less than $20,000, a felony of the third degree

■ If the funds diverted or misappropriated are $20,000 or more, but less than $100,000, a felony of the second degree

■ If the funds diverted or misappropriated are $100,000 or more, a felony of the first degree

2. Commissions and compensation/charges for extra services [Sec. 624.428, 626.572, .581, .593, .794] Agents are generally compensated by the payment of commissions that are a certain percentage of the initial (first year) and subsequent (renewal) premiums. Florida law specifies that no policy of life or health insurance may be issued for delivery in this state unless the application is taken by, and the policy delivered through, a licensed agent who will receive the usual commission.

a. No person other than a licensed and appointed agent may accept any commis-sion or other valuable compensation for soliciting or negotiating insurance.

b. Commission for examining any group health insurance [Sec. 626.593] Florida law was amended in 2004 to permit a licensed health agent to be compensated at rates other than that which an insurer files with the Office of Insurance Regulation. This alternative form of compensation is limited to providing advice, counsel, or recommendations regarding any group health insurance or group health benefit plans. Such compensation must be based upon a written contract between the agent and the party being charged the separately

Florida_L&H_LawSupplement_book.indb 102 11/11/2015 2:36:57 PM

103Law Supplement

negotiated fee. Such written contract must clearly define the amount of compen-sation to be paid to the agent and must inform the person being charged that any commission received by the agent from the insurer will be rebated to that party within 30 days of receipt by the agent from the insurer. A copy of such contract must be retained by the licensed agent for three years after services have been fully performed.

c. Commission rebates [Sec. 626.572] An insurance agency or agent may not rebate any portion of a commission except as follows.

■ The rebate shall be available to all insureds in the same actuarial class. ■ The rebate shall be in accordance with a rebating schedule filed by the agent

with the insurer issuing the policy to which the rebate applies. ■ The rebating schedule shall be uniformly applied in that all insureds who

purchase the same policy through the agent for the same amount of insur-ance receive the same percentage rebate.

■ Rebates shall not be given to an insured with respect to a policy purchased from an insurer that prohibits its agents from rebating commissions.

■ The rebate schedule is prominently displayed in public view in the agent’s place of doing business, and a copy is available to insureds on request at no charge.

■ The age, sex, place of residence, race, nationality, ethnic origin, marital status, or occupation of the insured or location of the risk is not utilized in determining the percentage of the rebate or whether a rebate is available.

1.) The insurance agency or agent must maintain a copy of all rebate sched-ules for the most recent five years and their effective dates.

2.) No rebate may be withheld or limited in amount based on factors that are unfairly discriminatory.

3.) No rebate may be given that is not reflected on the rebate schedule.

4.) No rebate may be refused or granted based upon the purchase or failure of the insured or applicant to purchase collateral business.

d. Commissions contingent on loss settlements prohibited [Sec. 626.581] When agents of the insurer are acting as an adjuster of claims, it is unlawful for the insurer to enter into any agreement or understanding with its agents in Florida, which base the agents’ commissions on Florida policies contingent upon savings in the settlement of claims. Nothing in this section will be construed to apply to any contingent commissions agreement under which agents do not pay claims arising under policies of the insurer.

3. Ethics [Sec. 626.797; Rule 69O-230, 69B-215.210 to .235]

a. Scope [Rule 69B-215.210, F.A.C.] The business of life insurance is hereby declared to be a public trust in which all agents of all companies have a common obligation to work together in serving the best interests of the insur-

Florida_L&H_LawSupplement_book.indb 103 11/11/2015 2:36:57 PM

104 Law Supplement

ing public, by understanding and observing the laws governing life insurance in letter and in spirit by presenting accurately and completely every fact essential to a client’s decision, by being fair in all relations with colleagues and competitors, and by always placing the policyholder’s interests first.

b. Use of designations [Rule 69B-215.235, F.A.C.]

1.) The purpose of this rule is to set forth standards to protect consumers from dishonest, deceptive, misleading, and fraudulent trade practices with respect to the use of certifications and professional designations in the marketing, solicitation, negotiation, sale, or advice made in connection with an insurance transaction by any licensee.

2.) The Department does NOT endorse any professional designation.

3.) For purposes of this rule: ■ a designation is any combination of words, any acronym standing for

a combination of words, or any job title that indicates or implies that a licensee has special knowledge or training in advising or servicing consumers beyond the knowledge or training required for the license held; and