Lessons from NAFTA William Maloney, Luis Serven World Bank Canadian Standing Senate Committee on Foreign Affairs www.worldbank.org/laceconomist

Lessons from NAFTA William Maloney, Luis Serven World Bank Canadian Standing Senate Committee on Foreign Affairs .

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lessons from NAFTA

William Maloney, Luis ServenWorld Bank

Canadian Standing Senate Committee on Foreign Affairs

www.worldbank.org/laceconomist

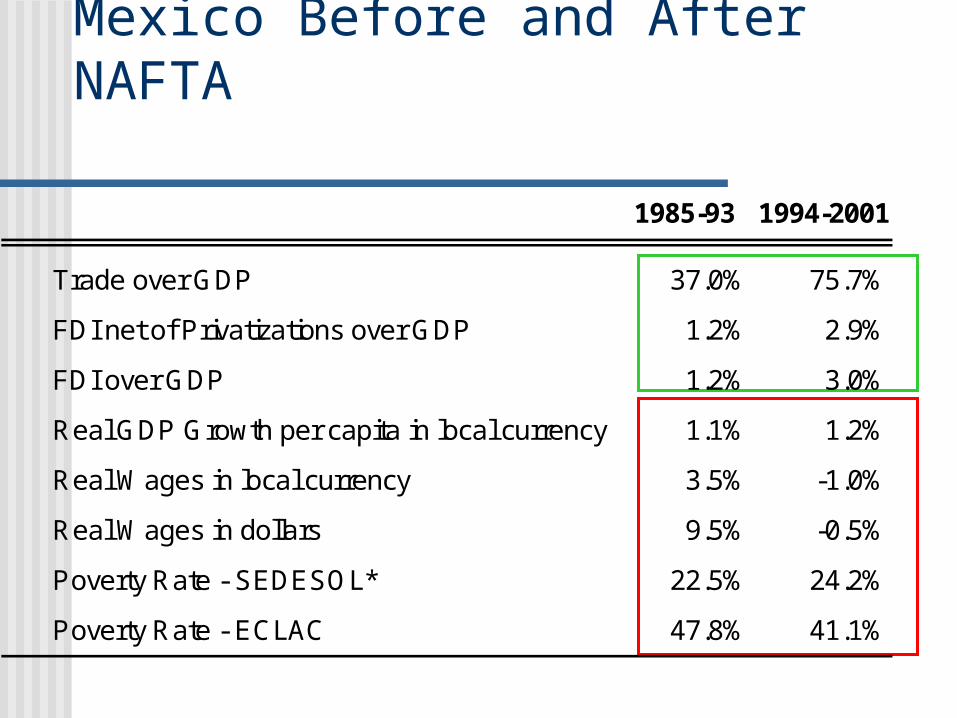

Mexico Before and After NAFTA

1985-93 1994-2001

Trade over GDP 37.0% 75.7%

FDI net of Privatizations over GDP 1.2% 2.9%

FDI over GDP 1.2% 3.0%

Real GDP Growth per capita in local currency 1.1% 1.2%

Real Wages in local currency 3.5% -1.0%

Real Wages in dollars 9.5% -0.5%

Poverty Rate - SEDESOL* 22.5% 24.2%

Poverty Rate - ECLAC 47.8% 41.1%

How to evaluate the impact of NAFTA?

Only ten years have elapsed. Other major events occurred simultaneously:

Tequila Crisis and 1995 recession Unilateral reforms 1986-1993 – anticipated NAFTA

effect and delayed reform effects FDI boom to “emerging” economies, not just Mexico Ongoing decline in commodity prices (agriculture) and

ongoing employment trends Our multifaceted approach:

History – before and after NAFTA – structural change? Differences across sectors and states International comparisons – Mexico versus other Latin

economies

Did Mexico benefit from NAFTA? Yes, but could have been better.

On the whole, yes But not so much as proponents promised. Not as

bad as critics claimed either. Gave a modest impulse to economic convergence in

N.A. Notable impact on trade and FDI

Benefits were not equally shared by all sectors and regions

The benefits are not automatic They depend on complementary domestic reforms Institutions, education, technology, infrastructure

Plan of the presentation Trade FDI Income convergence with N.A. Divergence across regions Productivity and innovation Labor Markets Agriculture

Trade

Nafta spurs trade

But the FTA was not the only factor: rapid US growth in late 1990s Real depreciation of the peso Lagged effect of unilateral reforms of the 1980s

No evidence of trade diversion in the aggregate NAFTA estimated to be responsible for a 25-30% increase in

exports

Big increase in trade

Figure 4. Latin America: Imports plus Exports over GDP

0

20

40

60

80

100

120

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

ARG BRA CHL COL CRI MEX ALC

Trade/GDP

Foreign Direct Investment

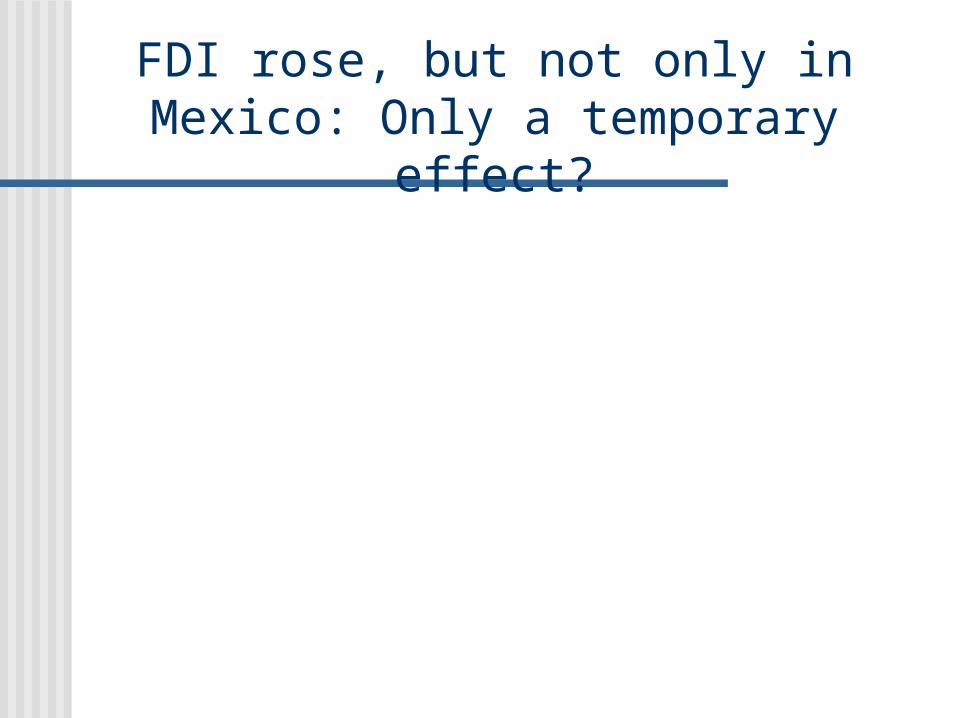

FDI rose, but not only in Mexico: Only a temporary effect?

Entradas Netas de Inversión Extranjera Directa(porcentaje del PIB)

0%

1%

2%

3%

4%

5%

6%

7%

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

México América Central y el Caribe América del Sur

Sources: WIR and IMF.

Net FDI inflows as a % of GDP

Convergence of GDP/Capita

The development gap between the U.S. and Mexico

Debt Crisis

Tequila

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 20001.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Ratio of GDP per capita US/Mexico

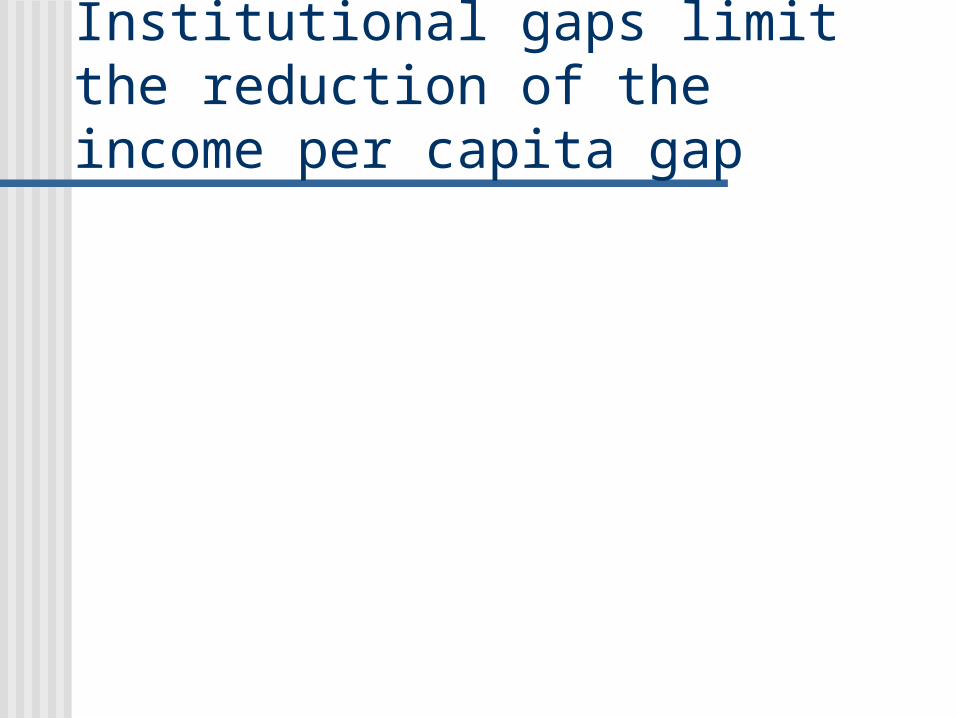

Institutional gaps limit the reduction of the income per capita gap

1.331.24

2.05

1.45

0.58

1.71

1.07

1.70

1.241.18

1.58

1.19

1.58

0.28

0.120.06

-0.41-0.28

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

Va

ria

ble

ra

ng

es

fro

m -

2 t

o +

2 f

or

all

cou

ntr

ies

CAN USA MEX

Voice and Accountability

Political Stability

Government Effectiveness

Regulatory Quality

Rule of Law Control of Corruption

Divergence across Regions

The development gap within Mexico: state GDP/capita

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1940 1950 1960 1970 1980 1988 1990 1993 1995 2000

GD

P p

er

Ca

pit

a (

19

93

pe

so

s)

Chiapas Chihuahua Guerrero Nuevo LeónOaxaca Sonora Distrito Federal

Why Different Performance of Mexican States during the 1990s?

Initial education (literacy,education level)

Infrastructure Political instability and institutions If poor States had had the same

education, and infrastructure in 1990, they would have grown more than the rich ones (“conditional convergence”)

Productivity and Innovation

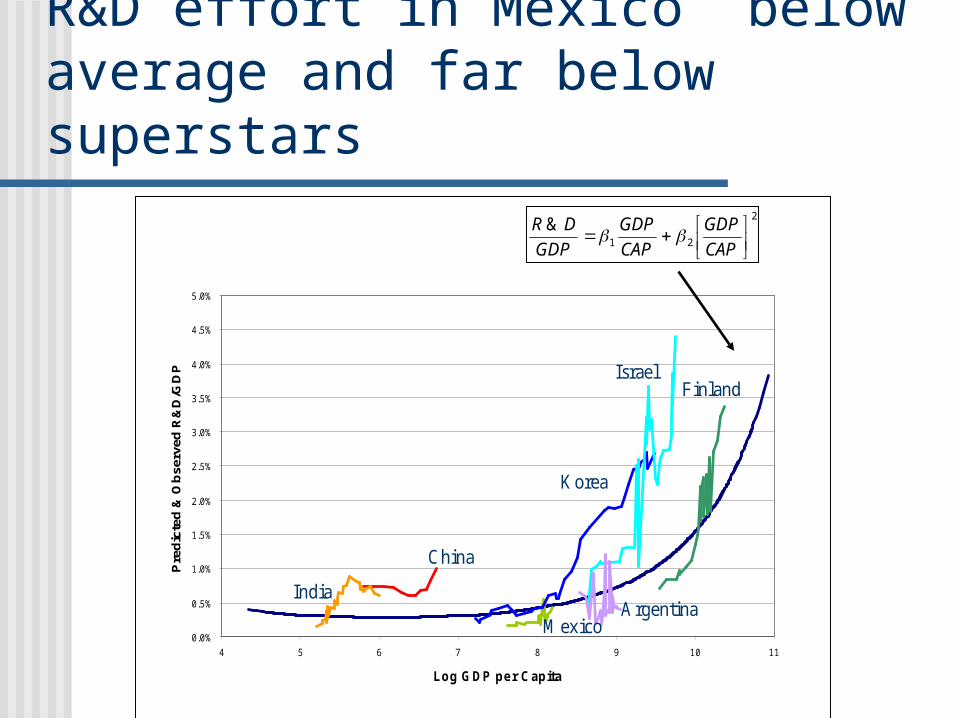

R&D effort in Mexico below average and far below superstars

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

4 5 6 7 8 9 10 11

Log G DP pe r Capita

Pre

dic

ted

& O

bse

rved

R&

D/G

DP

IndiaArgentina

China

IsraelFinland

Korea

M exico

2

21

&

CAP

GDP

CAP

GDP

GDP

DR

R&D gap in Mexico, modest post-NAFTA recovery …

-160%

-140%

-120%

-100%

-80%

-60%

-40%

-20%

0%

Per

cen

t D

evia

tio

n f

rom

th

e M

edia

n

Mexico's R&D

NAFTA

Labor Markets

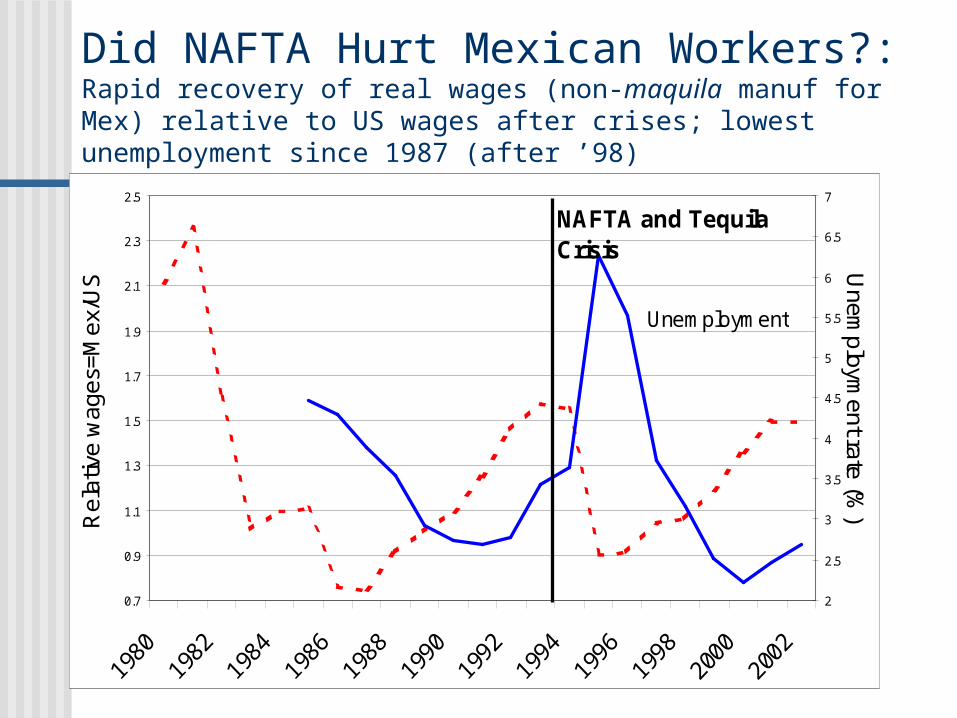

Did NAFTA Hurt Mexican Workers?:Rapid recovery of real wages (non-maquila manuf for Mex) relative to US wages after crises; lowest unemployment since 1987 (after ’98)

Manufacturing Real Wages and Unemployment Evolution

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

Rel

ativ

e w

ages

=Mex

/US

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

7

Unem

ployment rate (%

)

Unemployment

NAFTA and Tequila Crisis

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

% a

bo

ve n

on

-tra

da

ble

s

Note: Non agricultural workers. Conditional on human capital

NonTrad.

More Exports/Worker More Imports/Worker

Human Capital Adjusted Wages

Did NAFTA hurt Mexican workers?Higher wages paid by firms with international competition; wages recovered faster after 1995 in export sectors; & limited effect on rural employment

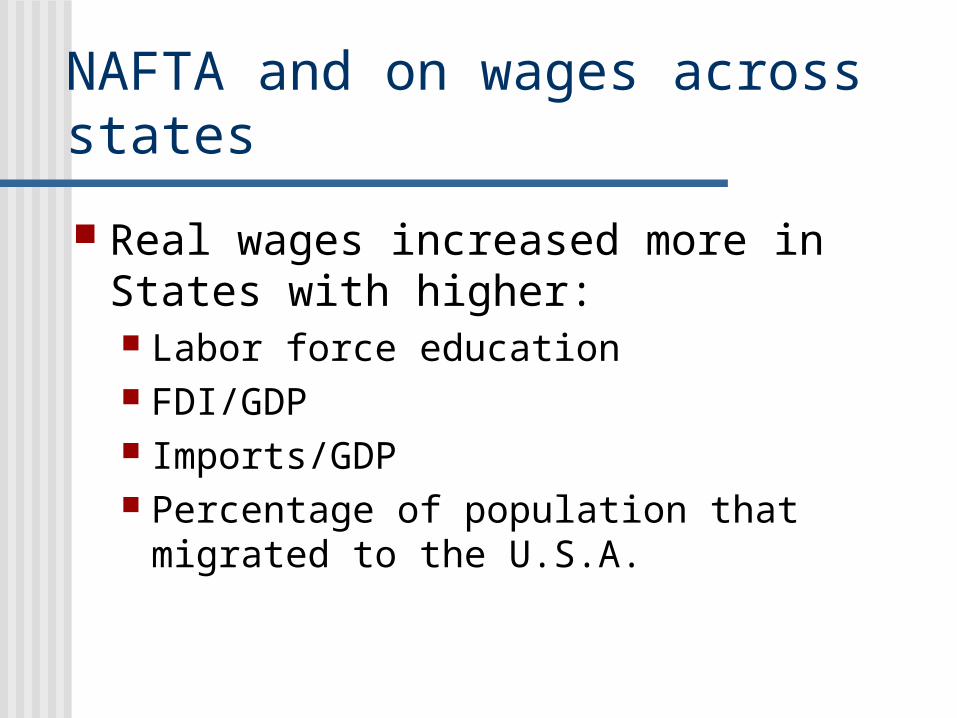

NAFTA and on wages across states

Real wages increased more in States with higher: Labor force education FDI/GDP Imports/GDP Percentage of population that migrated

to the U.S.A.

Is there an inequality story?: yes in wages, but not in household income

Year World Bank Gini

SEDESOL Gini

1992 55.9 47.5

1996 54.4 45.6

2000 54.6 48.1

2002 n.a. 45.4

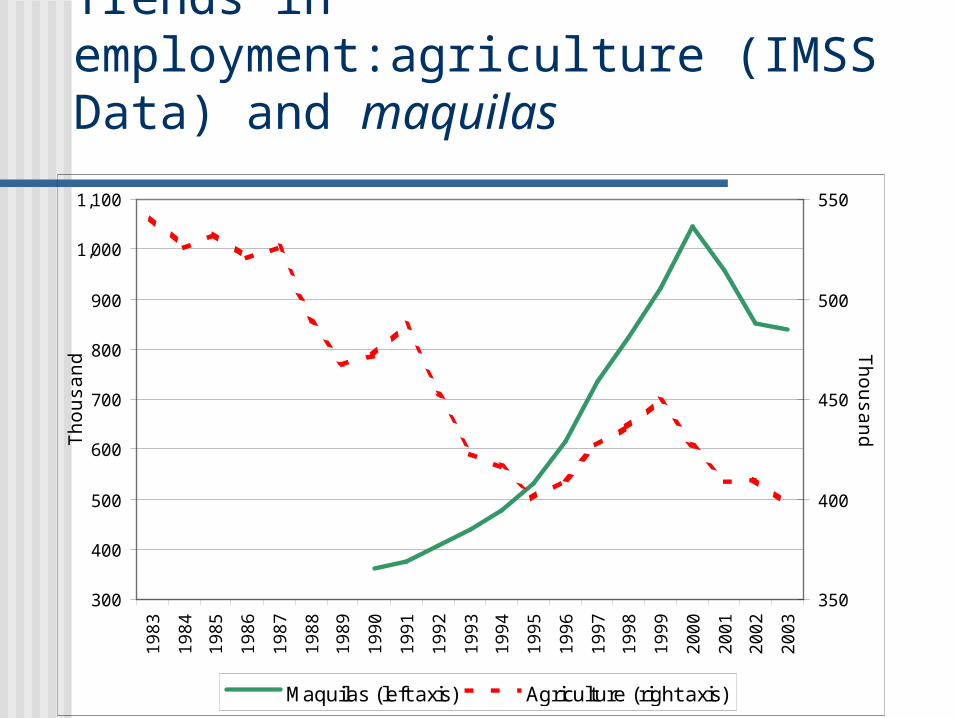

Trends in employment:agriculture (IMSS Data) and maquilas

300

400

500

600

700

800

900

1,000

1,100

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

Tho

usan

ds

350

400

450

500

550

Thousands

Maquilas (left axis) Agriculture (right axis)

Agriculture

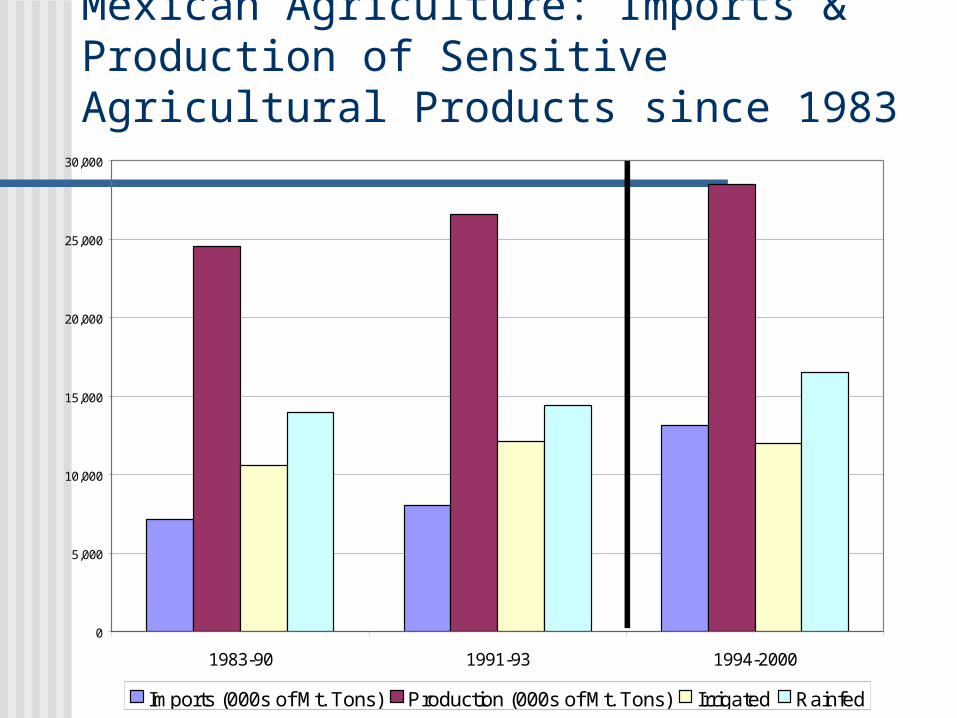

Mexican Agriculture: Imports & Production of Sensitive Agricultural Products since 1983

0

5,000

10,000

15,000

20,000

25,000

30,000

1983-90 1991-93 1994-2000

Imports (000s of Mt. Tons) Production (000s of Mt. Tons) Irrigated Rainfed

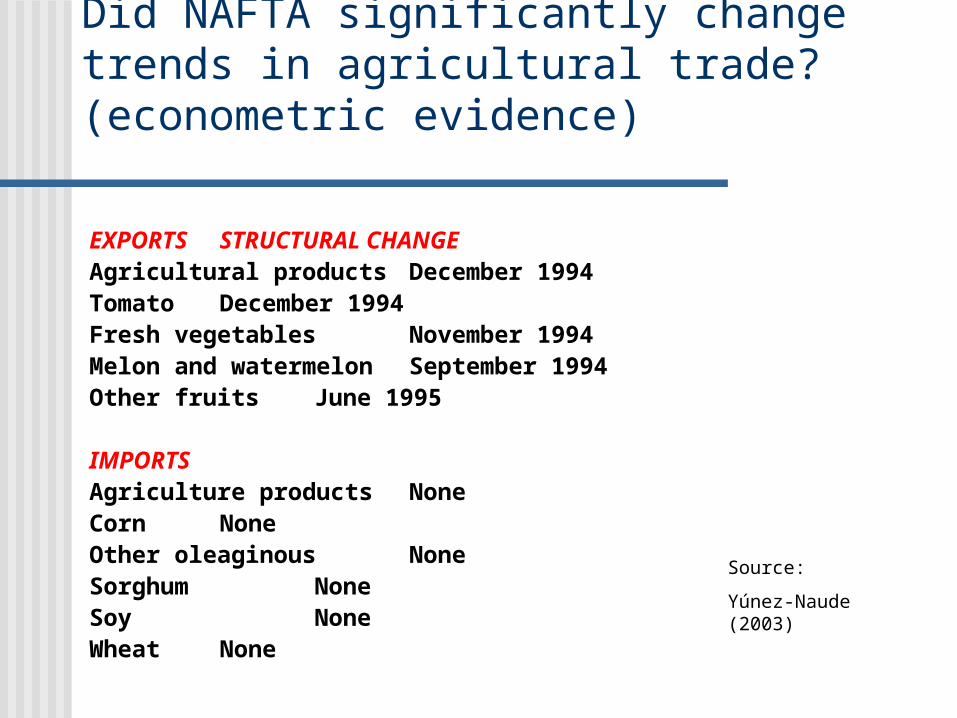

Did NAFTA significantly change trends in agricultural trade? (econometric evidence)

EXPORTS STRUCTURAL CHANGEAgricultural products December 1994 Tomato December 1994 Fresh vegetables November 1994 Melon and watermelon September 1994 Other fruits June 1995

IMPORTS Agriculture products NoneCorn NoneOther oleaginous NoneSorghum NoneSoy NoneWheat None

Source:

Yúnez-Naude (2003)

Why didn’t Mexican agriculture suffer as much as some feared?

Demand growth in Mexico & U.S. during 1995-2000 combined with …

… productivity growth in Mexican agriculture with irrigation

Innovative agricultural support programs (PROCAMPO)

But challenge is to help reduce rural poverty without protectionism, which condemns generations of rural poor to dependence on low quality jobs and government favors … towards the transformation of the Mexican

rural economy

End

Related Documents