Legal and Accounting Legal and Accounting Presented by John D. Hawkins, JD, CPA

Legal and Accounting Presented by John D. Hawkins, JD, CPA

Dec 30, 2015

Legal and Accounting Presented by John D. Hawkins, JD, CPA. Agenda for today. Taxes Income tax Estate tax How property passes at death Sample language for bequests Endowments. Tax Benefits of Charitable Giving:. Income Tax Deduction Elimination of capital gains tax - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Legal and AccountingLegal and AccountingPresented by

John D. Hawkins, JD, CPA

Agenda for today

Taxes Income tax Estate tax

How property passes at deathSample language for bequestsEndowments

Tax Benefits of Charitable Giving:

Income Tax DeductionElimination of capital gains taxRemoval of property from taxable estate

3

Tax legislation

EGTRRA 2001- cut tax rates for both estate and income tax Changes “sunset” after 10 years Thus we would return to pre-2001 law on January 1, 2011

2010 Tax Relief Act (signed 12/17/10) Extended the EGTRRA sunset for two years Now return to pre-2001 law on January 1, 2013

2012 is an election year. Will congress pass tax legislation before the November election? If congress waits till after November election, how quickly can we know what the

law will be on 1/1/13?

4

Federal Income taxes – 2012

2012 Single Married Filing Joint

10% $0 - 8,700 $0 – 17,400

15% $8,701 - $35,350 $17,401 - $70,700

25% $35,351 - $85,650 $70,701 - $142,700

28% $85,651 - $178,650 $142,701 - $217,450

33% $178,651- $388,350 $217,451 - $388,350

35% $388,351 + $388,351 +

Federal Income taxes – 2013

2012 2013

10% N/A

15% Same but ends $10,000 less for MFJ

25% 28%

28% 31%

33% 36%

35% 39.6 +3.8 = 43.4

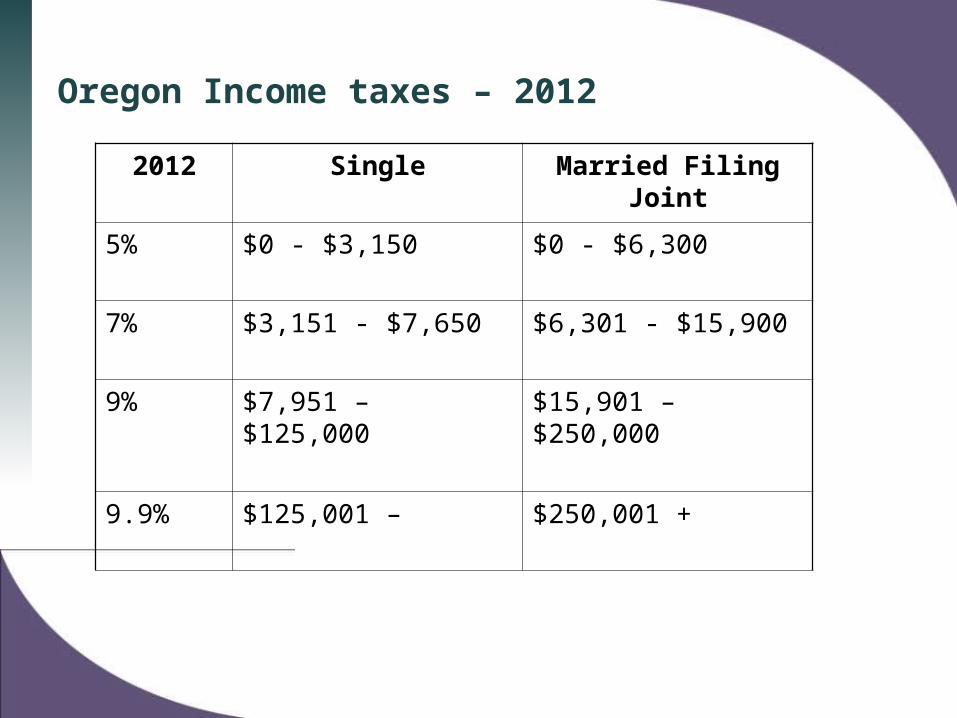

Oregon Income taxes – 2012

2012 Single Married Filing Joint

5% $0 - $3,150 $0 - $6,300

7% $3,151 - $7,650 $6,301 - $15,900

9% $7,951 – $125,000 $15,901 – $250,000

9.9% $125,001 – $250,001 +

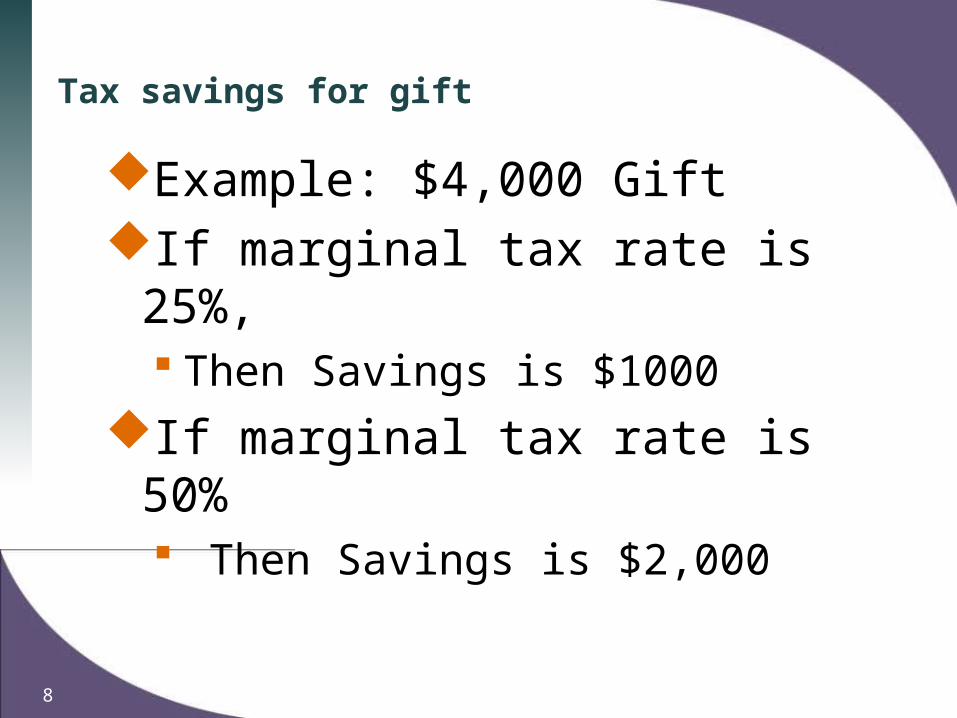

Tax savings for gift

Example: $4,000 GiftIf marginal tax rate is 25%,

Then Savings is $1000If marginal tax rate is 50%

Then Savings is $2,000

8

Estate and Gift Taxes

Years Estate exclusion

Lifetime gifts

Highest Tax rate

2009 $3,500,000 $1,000,000 45%

2010 $5,000,000 $5,000,000 35%

2011 $5,000,000 $5,000,000 35%

2012 $5,000,000 $5,000,000 35%

2013 $1,000,000 $1,000,000 55%

9

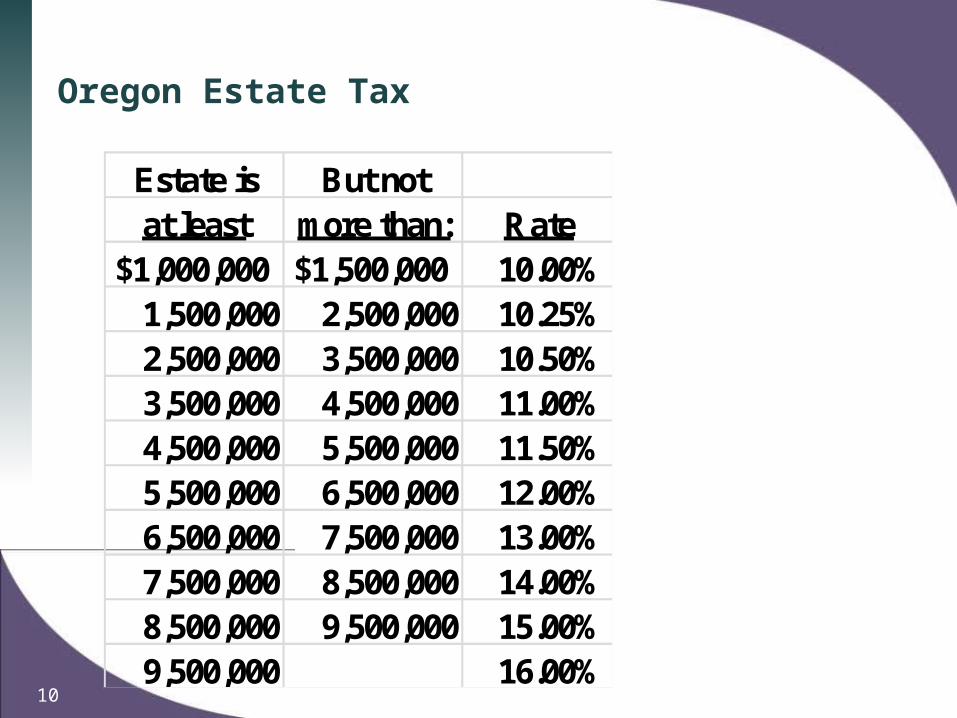

Oregon Estate Tax

10

Estate is But notat least more than: Rate

$1,000,000 $1,500,000 10.00%1,500,000 2,500,000 10.25%2,500,000 3,500,000 10.50%3,500,000 4,500,000 11.00%4,500,000 5,500,000 11.50%5,500,000 6,500,000 12.00%6,500,000 7,500,000 13.00%7,500,000 8,500,000 14.00%8,500,000 9,500,000 15.00%9,500,000 16.00%

How does the estate tax work?

Tax is based on the net value of estate; debts decrease the estateThe taxable estate is everything over which the person had control

Different from the probate estate Includes life insurance Includes gifts if they kept a “string”

A few deductions are allowed Charitable donations Unlimited Marital deduction

The exemption amount is deducted to determine the taxable estate

Gifts during life will reduce the exemption amount available at death

11

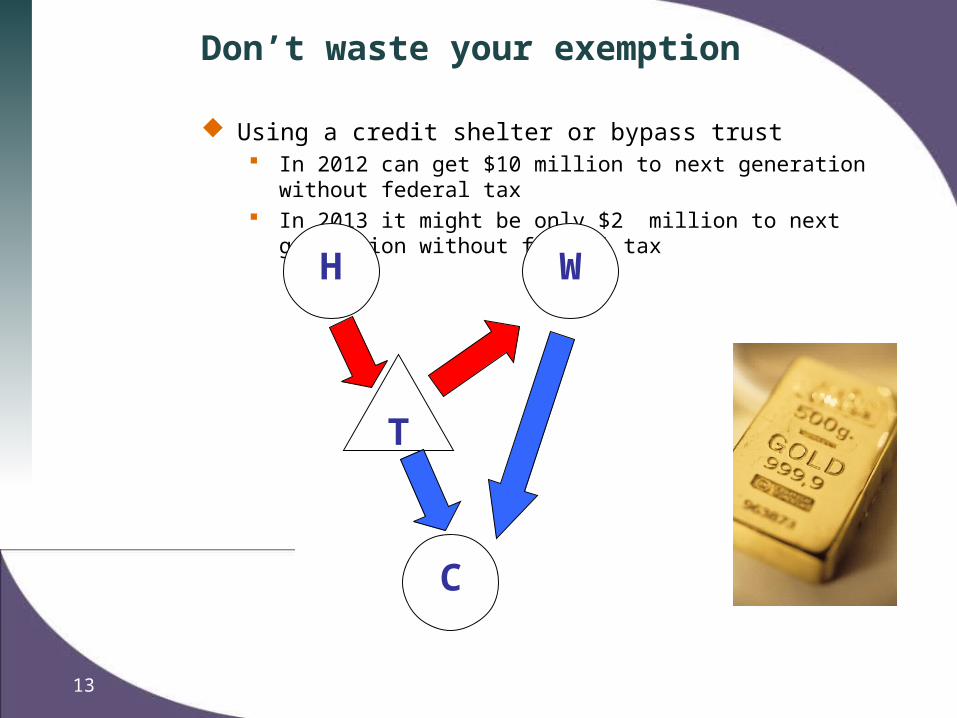

Don’t waste your exemption

The “l Love You” estate plan Pays no tax until the second death Husband did not use his exemption amount

H W

C

13

Don’t waste your exemption

Using a credit shelter or bypass trust In 2012 can get $10 million to next generation without federal tax In 2013 it might be only $2 million to next generation without federal tax

H W

C

T

Tax to family for inheritance

The estate may have to pay the federal or state estate tax depending on size of estate

Inheritance is not income so no income tax on receiptHeirs get a “step-up” in basis for assets

Dad bought land for $10,000, worth $100,000 at death If dad sold day before death, he would have a $90,000 capital gain Heirs get a new cost basis of value at death and could sell the next day

without a capital gain Income with Respect to a Decedent does not get a step up

IRA and retirement plans Annuities Installment sales (land sale contracts)

14

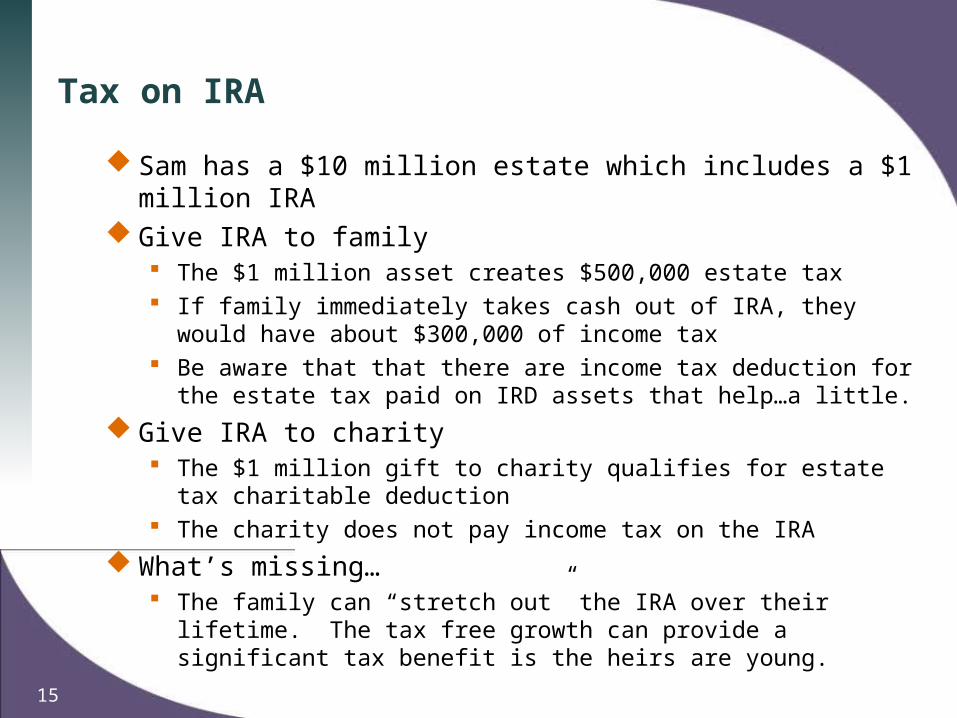

Tax on IRA

Sam has a $10 million estate which includes a $1 million IRA Give IRA to family

The $1 million asset creates $500,000 estate tax If family immediately takes cash out of IRA, they would have about $300,000 of

income tax Be aware that that there are income tax deduction for the estate tax paid on IRD

assets that help…a little. Give IRA to charity

The $1 million gift to charity qualifies for estate tax charitable deduction The charity does not pay income tax on the IRA

What’s missing… The family can “stretch out” the IRA over their lifetime. The tax free growth can

provide a significant tax benefit is the heirs are young.

15

Outright Cash Gift during life

Benefits: Help Charity – NOW Simple, easy Income Tax Deduction Reduce Your Taxable Estate Disadvantage-you need cash

Remember a loved one with a memorial gift

16

Property gift

Generally deduct value of property at time of giftMust file form 8283 if non-cash donations over

$500Must get appraisal if over $5000Special rules for car donations

17

Appreciated Property gift

Generally stock or real estate, but can be jewelry, art or collections

Deduct value of property and avoid capital gains

18

Avoid Capital Gains

Sale of Property:Property Value $ 300,000Cost Basis 100,000Capital Gain $200,000Tax x 24%Capital Gains Tax $48,000

Or…..

19

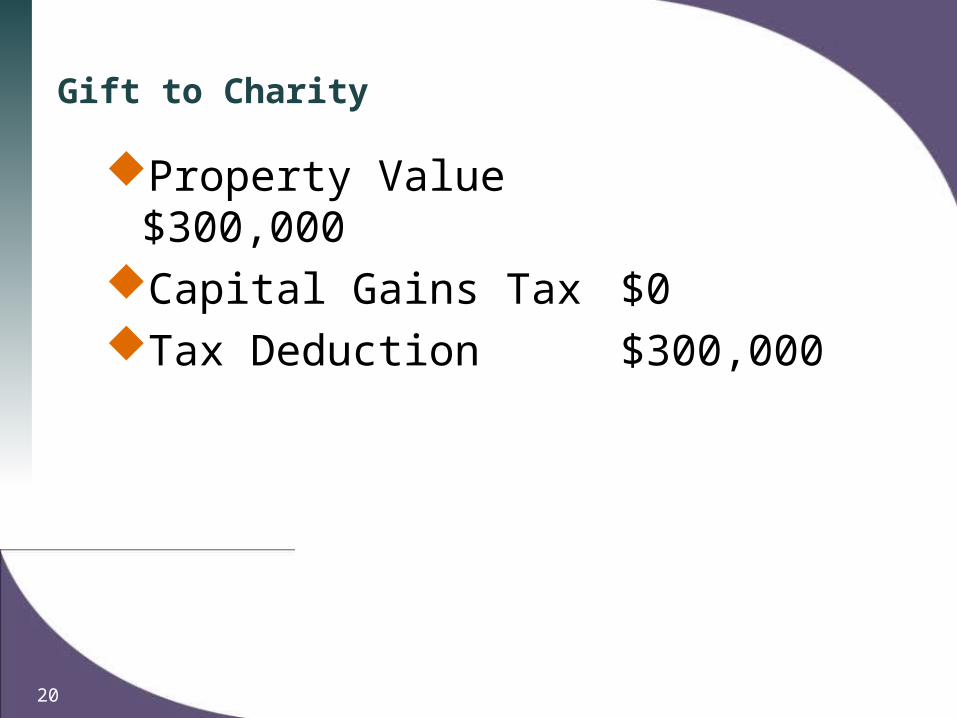

Gift to Charity

Property Value $300,000Capital Gains Tax $0Tax Deduction $300,000

20

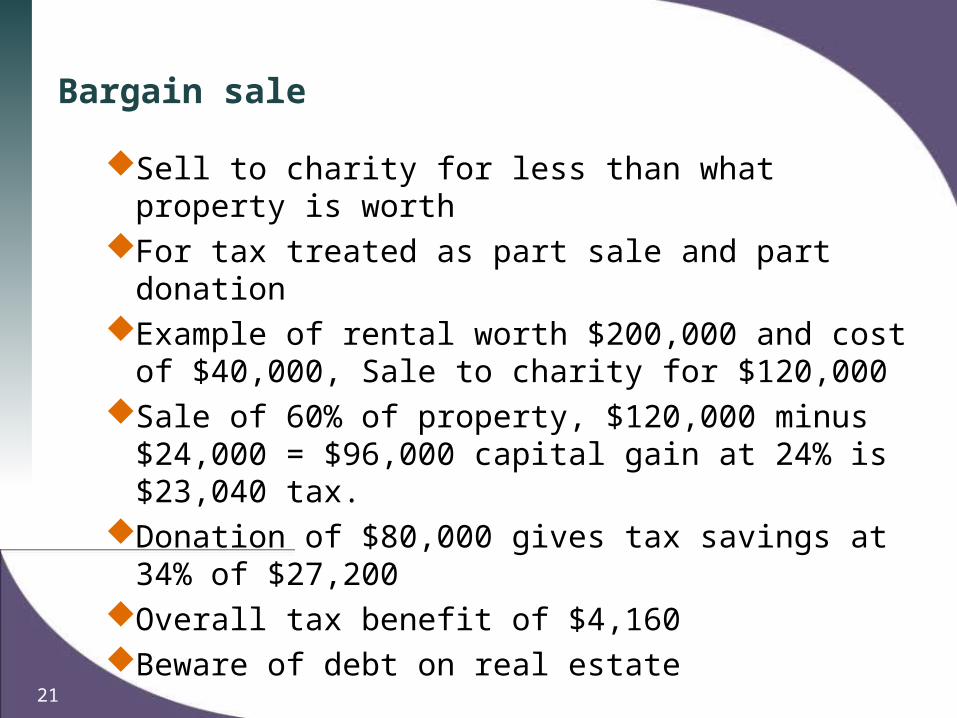

Bargain sale

Sell to charity for less than what property is worthFor tax treated as part sale and part donationExample of rental worth $200,000 and cost of $40,000,

Sale to charity for $120,000Sale of 60% of property, $120,000 minus $24,000 =

$96,000 capital gain at 24% is $23,040 tax.Donation of $80,000 gives tax savings at 34% of $27,200Overall tax benefit of $4,160Beware of debt on real estate

21

How property passes at death

Bequests by Will or intestacyOperation of law (joint title)Beneficiary designation

22

How property passes at death

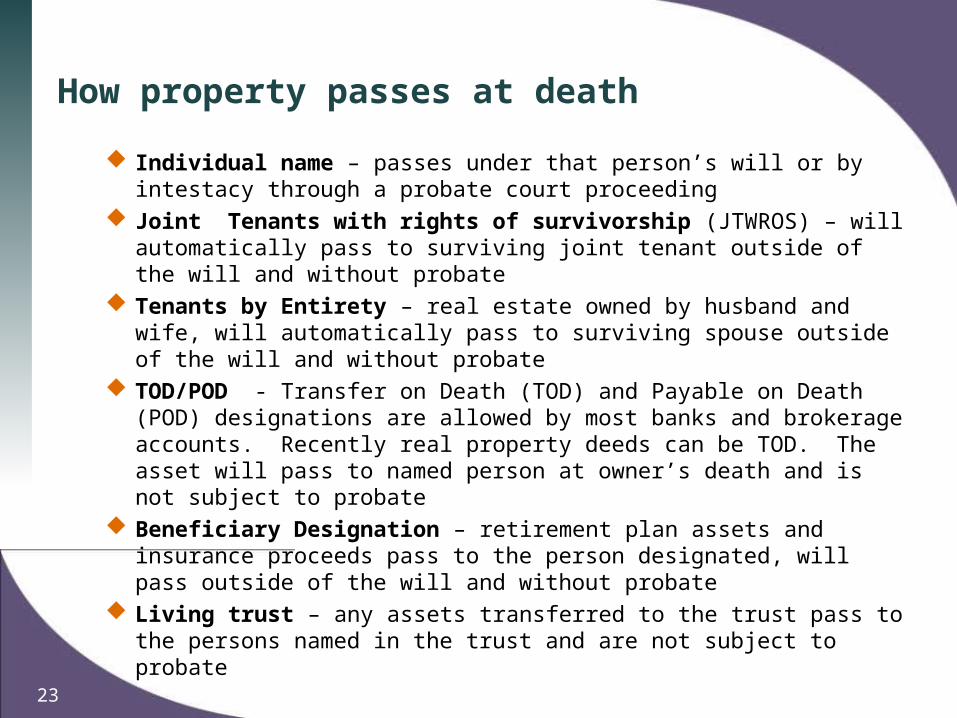

Individual name – passes under that person’s will or by intestacy through a probate court proceeding

Joint Tenants with rights of survivorship (JTWROS) – will automatically pass to surviving joint tenant outside of the will and without probate

Tenants by Entirety – real estate owned by husband and wife, will automatically pass to surviving spouse outside of the will and without probate

TOD/POD - Transfer on Death (TOD) and Payable on Death (POD) designations are allowed by most banks and brokerage accounts. Recently real property deeds can be TOD. The asset will pass to named person at owner’s death and is not subject to probate

Beneficiary Designation – retirement plan assets and insurance proceeds pass to the person designated, will pass outside of the will and without probate

Living trust – any assets transferred to the trust pass to the persons named in the trust and are not subject to probate

23

Will vs. Living Trust

The concept of the Living Trust is to avoid probate. The person is legally broke and there is nothing to probate

Advantages of Living Trust Private – no public court documents Saves probate costs – but have costs to set up trust Ability to manage assets if disabled

If I have a trust, do I still need a will??? YES! You need a will Assets leak out of trust over time Assets are never titled in name of the trust A “pour-over will” will catch these asset. Typically the will says anything in my

estate is given to my trust. If I have a trust, do I still need a power of attorney

Yes, the attorney-in-fact can transfer forgotten assets to trust

24

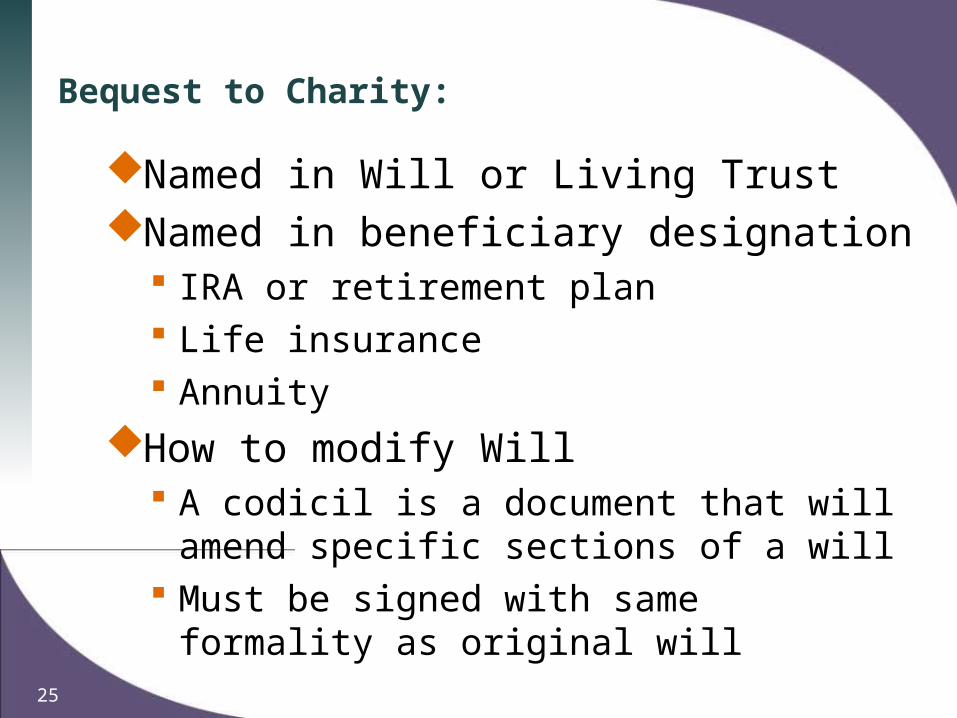

Bequest to Charity:

Named in Will or Living TrustNamed in beneficiary designation

IRA or retirement plan Life insurance Annuity

How to modify Will A codicil is a document that will amend specific

sections of a will Must be signed with same formality as original will

25

Bequest to Charity:

Benefits: Help charity -- after death Retain the asset during your lifetime Removes asset from your Taxable Estate You can designate how your gift is to be used (i.e. -

programs, operations, endowment)

26

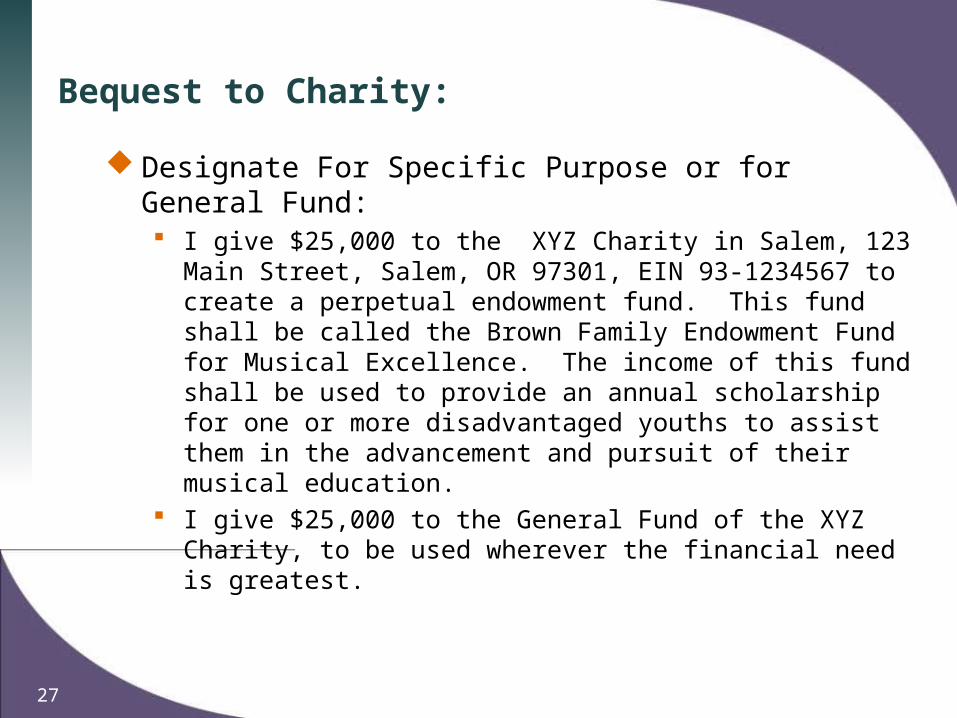

Bequest to Charity:

Designate For Specific Purpose or for General Fund: I give $25,000 to the XYZ Charity in Salem, 123 Main Street, Salem, OR

97301, EIN 93-1234567 to create a perpetual endowment fund. This fund shall be called the Brown Family Endowment Fund for Musical Excellence. The income of this fund shall be used to provide an annual scholarship for one or more disadvantaged youths to assist them in the advancement and pursuit of their musical education.

I give $25,000 to the General Fund of the XYZ Charity, to be used wherever the financial need is greatest.

27

Bequest to Charity:

1. Designate Percentage of your Estate I give to the XYZ Charity in Salem, 123 Main Street, Salem,

OR 97301, EIN 93-1234567, twenty-five percent (25%) of the residue of my estate.

2. Designate Dollar Amount I give $100,000 to the XYZ Charity in Salem, 123 Main Street,

Salem, OR 97301, EIN 93-1234567 3. Designate a Specific Asset of your Estate

I give to the XYZ Charity in Salem, 123 Main Street, Salem, OR 97301, EIN 93-1234567 my entire interest in the real property located at 111 Liberty Street, Salem, Oregon. The legal description of the property is …

28

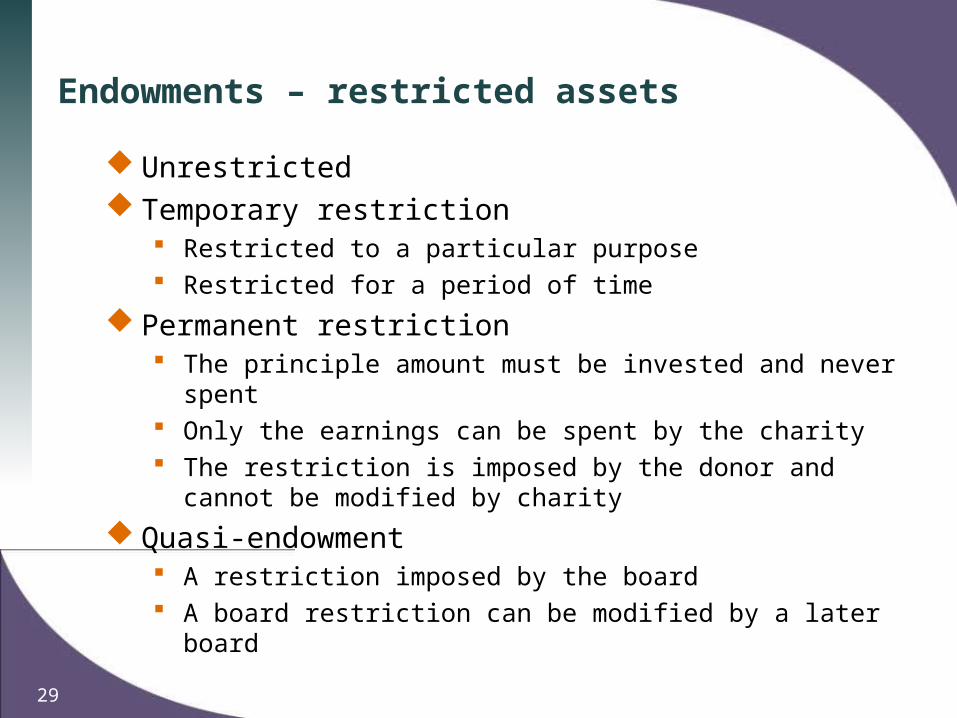

Endowments – restricted assets

Unrestricted Temporary restriction

Restricted to a particular purpose Restricted for a period of time

Permanent restriction The principle amount must be invested and never spent Only the earnings can be spent by the charity The restriction is imposed by the donor and cannot be modified by charity

Quasi-endowment A restriction imposed by the board A board restriction can be modified by a later board

29

Endowments

Uniform Prudent Management of Institutional Funds Act ORS 128.305

Gift Instrument includes the organization’s solicitation documents under which the property was granted

The appropriation for expenditure in any year of more than 7% creates a rebuttable resumption of imprudence Fair market value is average of quarterly account values over

last 3 yearsDonor can consent to release or modification of

restriction Court can modify restrictions if impractical or wasteful, etc

30

Questions????

Related Documents