©Law Centres Network Page 1 Legal Aid Agency Audits Guide April 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

©Law Centres Network Page 1

Legal Aid Agency

Audits Guide

April 2013

©Law Centres Network Page 2

INTRODUCTION TO THIS GUIDE About this Guide This Guide is part of a set making up a toolkit for Law Centres. It is designed to give Law Centres a detailed understanding of the different types of audits (and verification visits) that the Legal Aid Agency (LAA) now undertake, together with detailed advice about how to pass the audits. The bulk of the Guide explains the different types of audit currently being undertaken, highlighting the issues the LAA is looking for and the possible consequences of failing the audit. Throughout, the Guide aims to give tips on how to survive audits. We have provided some checklists, in the appendices, which you can use to help yourself prepare for audits or, better still, for the purposes of ongoing periodic compliance self-checks. The LAA (and previously the Legal Services Commission) has been moving towards a system whereby every provider will receive some type of visit or audit at least once a year. The extent of the audit activity is wide-ranging. The LAA is currently carrying out the following audits:

• Contract Compliance Audits

• Onsite Audits (previously known as Control Audits)

• Contract Manager’s Visits (previously known as Financial Stewardship Audits)

• Costs Assessments; and

• Peer Review

However, the LAA is also carrying out other verification exercises to help it to deal with, amongst other things, issues raised in the National Audit Office’s qualification of their accounts. Data validation is an exercise that uses electronically generated reports to highlight areas of potential misclaiming, for instance the use of incorrect standard fees claimed against certain codes or incorrect VAT rates. These audits or verification visits have included:

• National Audit Office (NAO) Audits;

• Office & Consortia Verification Audits;

©Law Centres Network Page 3

• Exceptional Case Costs Assessments (Escape Fee Cases from 1 April 2013); and

• Payment Verification & Data Validation Audits.

A full list of all current LAA Audits, with a brief description of each, is available on the legal aid section of the Justice website at http://www.justice.gov.uk/legal-aid/quality-assurance/audits The Legal Services Commission (as it then was) previously said1

that Audits in 2012/13 would be scheduled for providers where:

1. there are anomalies in the management information that need to be explored; 2. Contract Managers request an audit; or 3. as a follow-up to a previous intervention(s) to ensure that matters have been

rectified. This is likely to continue for 2013/14. The LAA identify anomalies and provider errors though use of their:

• management information systems, • data validation; and • testing of the eligibility and accuracy of payments.

In this Guide, we will cover all of the above audits and/or assessment activity. The current audit/assessment names are used in this Guide although please remember that the LAA may re-categorise and re-name audit activity in the future. References in this Guide are to the LAA’s 2013 Standard Civil Contract and we make clear whether the provisions referred to are in the Standard Contract Terms or the Contract Specification. In January 2013, a new audit, conducted by the Ministry of Justice (MoJ), was brought to our attention. This is an I.T. audit of providers that use the MoJ’s secure email system. The secure email system provides a service to send encrypted emails from one party to another. Thousands of organisations use this service. Whist few if any Law Centres currently use this service, a section about the service and the audit is useful for future information.

1 http://www.justice.gov.uk/legal-aid/quality-assurance/audits

©Law Centres Network Page 4

CONTRACT COMPLIANCE AUDIT (CCA)

Who carries out the audit? The audit is carried out by the LAA. The audits were previously carried out by the LAA’s Regional Offices but are now carried out by the dedicated Provider Assurance Team, based in London and Nottingham.

Clause 7.6 of the Contract Terms requires that a provider must:

“…demonstrate to [the LAA’s] reasonable satisfaction that you are complying with, and have at all times while it has been in force complied with, this Contract. You must demonstrate this when [the LAA] are Auditing you and at such other times as [the LAA] may require in accordance with this Contract.”

Further Clause 9.1 of the Contract Standard Terms states: “We may from time to time require you to provide us with Records in connection with the performance of your obligations under this Contract, including during any Audit. You will provide us with the same promptly and in any event within such time period we reasonably specify. If any such Records are held by a third party you must promptly upon receipt of our request arrange for such Records to be sent to us.”

Why a Law Centre may receive a Contract Compliance Audit? In the past, providers were targeted dependent on their fund spend. For instance, the LSC (as it then was) confirmed that, in 2007/2008 for both Crime and Civil, the LAA audited the top 20% of fund spend. This audit is likely from now on to be triggered as a result of a referral from your Contract Manager or as a follow up to another audit. This audit may also be triggered if negotiations between the LAA and a Law Centre during a Contract Manager’s Visit (previously known as a Financial Stewardship Audit) break down.

©Law Centres Network Page 5

Audit Purpose The purpose of this audit is to confirm whether a number of contract requirements are being met on Controlled Work

case files. It is significantly different to the previous style of Cost Compliance Audits because the introduction of Fixed Fees negates the need for a ‘line-by-line’ assessment.

Scope of the Audit

(i) CW1 & CW2 Forms

The auditor is checking to ascertain, where applicable, whether the advisor has correctly assessed the client’s eligibility. Care should be taken to ensure that the form, and in particular, the eligibility section, is completed in full and that the client has correctly certified whether she/he has previously received CW1 advice and assistance.

(ii) Evidence of Means

The auditor is checking that, unless the very limited exceptions apply, there is clear evidence of means on file and that the evidence of means was obtained before the provider started work. The auditor will be checking that the evidence of means is acceptable (and in accordance with the LAA’s guidance) and covers the computation period (the month leading up to when the form is signed).

There have questions in relation to circumstances where the LAA will accept evidence of means obtained after the Legal Help form was completed. Point of Principle (PoP) 55 provides some useful guidance and is reproduced below.

CLA 55 EVIDENCE OF MEANS FOR CONTROLLED WORK CASES

POINT OF PRINCIPLE

The effect of paragraphs 6.1 and 6.2 of Section B6 of the Funding Code, and paragraphs 2.4 and 2.5 of Section 2 of the Unified Contract Specification are as follows:

1. Where it is not practicable to obtain evidence of eligibility before commencing work, there must be an assessment of means on the basis of whatever information is available from the client, and that assessment must

©Law Centres Network Page 6

be recorded on the form which is signed by the client as his or her affirmation of eligibility.

2. 2.5 of the Contract also states that, in these circumstances, it is necessary for the provider to require the client to provide evidence of means as soon as practicable. This is an on-going contractual duty until it has been fulfilled and a claim for payment should not be made to the LAA without such evidence having been obtained and retained on the file.

3. In any case which on audit is found to have no such evidence on file, the preliminary decision will be to nil assess. A provider appealing or seeking review of such decision will have to provide evidence of eligibility at the time the form was signed and a satisfactory explanation as to why a claim was submitted for payment without such evidence being on file. If these two requirements are fulfilled, the reviewer/ICA will be able to exercise discretion to allow payment in appropriate circumstances.

Financial Eligibility

The LAA’s Financial Eligibility guidance is available at

http://civil-eligibility-calculator.justice.gov.uk

(iii) Sufficient Benefit Test

The Civil Legal Aid (Merits Criteria) Regulations 2013 states (at Regulation 32) that:

"An individual may qualify for legal help only if the Director is satisfied that the following criteria are met— (a) it is reasonable for the individual to be provided with legal help,

having regard to any potential sources of funding for the individual other than under Part 1 of the Act; and

(b) there is likely to be sufficient benefit to the individual, having regard to all the circumstances of the case, including the circumstances of the individual, to justify the cost of provision of legal help. Help may only be provided where there is sufficient benefit to the client, having regard to the circumstances of the matter, including the personal circumstances of the client, to justify work or further work being carried out."

If this test is not met, then all costs may be disallowed.

It isn’t a mandatory requirement to make a note on the file that the test has been met but it is often good practice to do so, particularly in cases where it is not obvious that the test has been met.

©Law Centres Network Page 7

It needs to be clear that the matter has probable sufficient benefit at the outset and demonstrable sufficient benefit throughout the lifetime of the matter.

(iv) Scope of Funding

Cases can be nil-assessed on the basis that the work provided was not within the scope of public funding.

The matters in scope for civil legal aid are set out in Schedule 1, Part 1 of the Legal Aid, Sentencing and Punishment of Offenders Act 2012 (LASPO).

(v) Late Billing

Here, the auditor is checking to ascertain whether the case was reported within six months (for Civil Legal Help claims – see paragraph 4.32 of the Contract Specification) of the matter ending. Under the Standard Contract, matters reported late result in a breach of contract notice being issued. Be aware that if you receive three ‘late billing’ notices within 24 consecutive months, then the LAA may terminate your Law Centre’s Contract (see Clause 24.1 of the Contract Terms)!

(vi) Matter Type and End Point Codes

This is another area where the LAA is keen to ensure that providers are reporting case codes accurately. If the incorrect end point code is used resulting in an incorrect level of payment being received, the LAA will seek to adjust the level of the fee received. Even if a financial penalty is not applicable, any errors could lead to a breach of contract notice being issued.

(vii) Disbursements

The auditor will be checking to see whether any disbursements incurred were reasonable and receipted.

©Law Centres Network Page 8

Audit Process Following discussions between the LAA and the representative bodies, the audit process changed in July 2011. Previously, this audit was often a two-stage process. The audit now involves assessing a single sample of casefiles. The number of files selected will be between 30 and 50 depending upon the number of controlled claims made over a 12 month period. Therefore, smaller Law Centres may be asked to provide less files than a larger Law Centre. The files are selected over the preceding year or since the last CCA, whichever is the shortest period. The files are selected using a computer programme which randomly selects files across the reported work, by category or type (the initial file sample is between 30 and 50, as mentioned above). Each file is checked (see above on the scope of the audit) to ascertain whether the file should be paid in full or reduced or entirely disallowed. After the files have been assessed, the final % value allowed is used to determine what action is taken. Previously, the results were also expressed as ratings but these are no longer used. The table below illustrates this. Final % value assessed down

Action and Sanctions Old Rating Name

0.00% - 10.00%

Recoup or credit value of incorrectly claimed files within audit sample.

Category 1

10.01% - 20.00%

Extrapolation of % reduction. Re-audit to be scheduled after at least 6 months. Contract notice(s).

Category 2

20.01% or more

Extrapolation of % reduction. Re-audit to be scheduled after at least 6 months. Contract notice(s). Further action, including possible termination, to be taken if matters have not improved by the second audit.

Category 3

Be aware that, if a file is not provided, it is automatically nil assessed. The LAA no longer choose a replacement file! The right to extrapolate from a finding in relation to Controlled Work is limited to other claims for Controlled Work (and only within the category or categories of law audited). There is no power to extrapolate and reduce claims for Licensed Work.

©Law Centres Network Page 9

To minimise the cost of dealing with appeals, the LAA will normally discount the extrapolation by 5% if a provider agrees not to appeal. The LAA will implement appropriate recoupment (where applicable) if no request for an appeal is received after 28 days. This will mean a reduction in the claims to be reconciled against the contract payments. Appeal Process There is a right to appeal against the assessment findings. Clauses 6.68 and 6.69 of the Contract Specification set out the appeal process. This is reproduced below: 6.68 If you or Counsel are dissatisfied with any decision of the Director as to the Assessment of the costs of Contract Work, you may appeal to an Independent Costs Assessor (“the Assessor”). For the avoidance of doubt, subsequent references in this rule and its related Guidance shall include “Assessors” in cases where an appeal is dealt with by a panel of three Assessors rather than a single Assessor alone. 6.69 The appeal must be made in writing (setting out full reasons) within 28 days of notification of the Assessment decision, and must be accompanied by the file. The Director will only extend the 28-day time limit where you have requested an extension for good reason within 21 days. Any extension of the time limit will be for a maximum of a further 14 days. Internal review While the above wording reflects the contractual position, in practice the LAA offer an informal review in order for the auditors to consider representations before putting the matter before Independent Costs Assessor. An Internal Reviewer will carry out a formal and detailed review of the original decision. They will write to the Law Centre with any changes to the original decision. If this decision is accepted the appeal process ends. Independent Costs Assessor If the decision is not accepted the matter can then proceed to an Independent Costs Assessor. They will review the assessment by confirming, increasing or decreasing the amount assessed. Any appeal to an Assessor is considered on paper.

©Law Centres Network Page 10

In exceptional circumstances either party can apply to the Assessor for an oral hearing. The Assessor will explain how the appeal will be carried out. The Assessor’s decision on the appeal will be forwarded to the Law Centre along with the revised assessment rate and any applicable recoupment figure. Clarifying Costs Rules and Guidance At any point after submitting an appeal to the Assessor, but not later than 21 days after receipt of the final decision, the LAA or the Law Centre can seek clarification on the costs rules, provisions and guidance. This is done by applying for a certificate of a ‘Point of Principle of General Importance’. Applications can be made to the LAA or direct to an Assessor if one has been appointed. The application will be forwarded within seven days of receipt to the LAA’s Legal Director and the Assessor (if one has been appointed).

The application must set out the exact wording of the Point of Principle of General Importance sought.

The LAA’s Legal Director will decide whether the matter should progress to the Costs Appeals Committee. The decision of the LAA’s Legal Director and/or the Costs Appeals Committee will be sent to the Law Centre, the LAA and if appropriate to the Assessor. Compliance Tips Set out below are some common recurring issues and points to note. The CW1 form is often the first document which is audited. Too many providers see this form as an example of unnecessary LAA bureaucracy. In fact, it is akin to a contract for payment. Unless the form is completed in full and with regard to the rules specified in the Standard Contract, the contract for payment is null and void. The form should be seen in the same light as a cheque. A bank would never honour a cheque that was not completed in full, signed and dated. As with a cheque, the use of tipp-ex must be avoided. If an alteration needs to be made, strike through the error and insert the correct information above the error. Ensure that you are using the most up to date version of the CW1 form. A more detailed version is applicable for matters opened on or after 1 April 2013. Where an advisor has accepted an application from a child or on behalf of a patient or a child, such a decision must be justified on Page 5 of the Legal Help form.

©Law Centres Network Page 11

Similarly, if the client has received Legal Help on the same matter within the previous six months, the advisor must justify in an appropriate level of detail, why the application was accepted. The LAA is particularly keen to ascertain whether the client has moved provider for a justifiable reason rather than say shopping for a second opinion which isn’t within scope of the Controlled Work scheme.

While it might seem a fairly straightforward task, inaccurate completion of the Legal Help form is one of the most frequent audit findings and in many cases will lead to a nil assessment which in turn will result in the loss of the fixed fee or, at worst, trigger extrapolation.

Assessing Eligibility and obtaining evidence

The LAA and the National Audit Office continue to insist on evidence of means being produced before completing the Legal Help form unless an exception applies. The evidence (or a copy) must be retained on the file. The Contract Specification states at paragraphs 3.24 and 3.25:

“You may assess the client’s means without the accompanying evidence where:

(a) it is not practicable to obtain it before commencing the Controlled Work; or (b) pre signature telephone advice is given; or (c) exceptionally, the personal circumstances of the Client (such as the Client’s

age, mental disability or homelessness) make it impracticable for the evidence to be supplied at any point in the case.

Unless sub-paragraph (c) above applies, you must require the Client to provide the evidence as soon as practicable. If satisfactory evidence of the Client’s financial eligibility is not subsequently supplied, or if the evidence shows that the Client is not financially eligible, you may claim the work carried out as a Matter Start provided that:-

(a) you have acted reasonably in undertaking work before receiving satisfactory

evidence of the Client’s means; (b) you have acted reasonably in initially assessing financial eligibility on the

information available; (c) you do not claim:

(i) any disbursement; or

©Law Centres Network Page 12

(ii) if the matter is remunerated at Hourly rates, profit costs beyond those incurred in the period before it is practicable to obtain satisfactory evidence of the Client’s means.”

The computation period is the calendar month ending on the day of the application (i.e. the date that the CW1 form is signed) and Law Centres should be looking to obtain evidence relating to that period. Written evidence that does not refer directly to the computation period itself may however be accepted by the LAA as confirmation of the client's statement of their income during that period where it seems reasonable to do so. The financial eligibility guidance in Volume 2E of the LAA Manual does make it easier to demonstrate compliance where the client is in receipt of a passported benefit. Paragraph 12.2.2 of the guidance states:

“Written evidence that does not refer directly to the computation period itself may be accepted as confirmation of the client's statement of their income during that period where it seems reasonable to do so. This might be for example where the client produces a letter from the Dept. Of Work and Pensions confirming their award of benefit - this may well be dated some time before the start of the computation period. In such cases, suppliers should try to ensure that the evidence the client provides is the most up to date in the client's possession - such as the last letter confirming an up rating of benefit…”

The guidance goes on to say that if the most recent letter is more than six months old then a recent bank statement showing continued receipt of the benefit is acceptable.

Signature

The assessment of means and client’s details sections must be fully completed and signed by the client in your presence before you start doing any legal work. However the Contract Specification does make clear that postal applications and telephone and email advice are allowed under the 2013 Standard Contract where the client requests it and

where it is necessary for the interest of the client or his or her case to attend in person (paragraph 3.14 and 3.18). This is subject to a limitation that the number of matter starts where a client does not attend must not exceed 10% of your total matters starts in any schedule period. This incorporates (but without making express reference to the term) the concept of good reason which was set out in the previous 2010 Contract Specification.

where, for good reason, the client cannot go to the providers office, he or she may authorise another person to attend (and thus sign) on their behalf. Good reason is defined at Paragraph 3.15 of the Contract Specification as:

©Law Centres Network Page 13

“’Good reason’ for the purposes of the Funding Code provision above will be where the Client requests that the application is made in this way and it is not necessary for the interests of the client or his or her case to attend in person.”

However the Contract Specification goes on to make clear that (a) whoever attends on the clients behalf must present all necessary means evidence and information demonstrating that the client is financially eligible and (b) that no “partner, member, associate, shareholder or employee of your organisation (or family member of such partner, member, associate, shareholder or employee) may act as an authorised person”. In addition, the actual client must be either present or resident in the European Union. It is vital that an attendance note records not just that the client was unable to go to your office to sign the form, but why. For example, if someone with children could not attend your office on the first occasion; but could subsequently, it is important to explain exactly what prevented them, otherwise the file is likely to fail an LAA audit on the basis that it did not demonstrate a ‘good reason’. In addition, the client’s case must still meet the sufficient benefit test and you must subsequently obtain evidence of means, as usual. It is advisable to consider reviewing procedures in relation to obtaining evidence of eligibility before the assessment. For instance, when booking an appointment for a client, it should be checked whether the client understands what evidence of income should be brought to the first appointment. A letter confirming the appointment together with acceptable types of evidence should follow swiftly afterwards. Further, a reminder letter or telephone call or text message should be sent to the client shortly before the appointment.

Client’s Certification

The client’s certification section of the CW1 form must be drawn to the client’s attention and filled in completely. If the client has previously received legal help assistance on the same matter, details should be set out on the CW1 form. A significant change in a client's financial circumstances may require a Law Centre to reassess their eligibility for Controlled Work and if on re-assessment it becomes clear that they have become ineligible then the Law Centre may not be able to provide further publicly funded work on their case. This has been effective since 1st April 2008. The current version of the CW1 form includes a paragraph as part of the client's declaration that they must tell you immediately if there are any changes in their (or their partner's) financial circumstances. Clients should be alerted specifically to this duty before they sign the declaration.

©Law Centres Network Page 14

Ensuring compliance While the scope of the audit is somewhat narrow and compliance would seem reasonably straightforward, every supervisor is aware how difficult it is to ensure that caseworkers consistently complete the Legal Help form correctly and obtain appropriate evidence of compliance. To prevent failing the audit, it is advisable that a system be put in place to ensure that each potential auditable issue is checked by the caseworker with conduct of the file. In addition your category supervisor should amend the file review checklist to include reference to the auditable issues such that they are checked as part of the normal file review process. Law Centres may wish to consider revising their file closing form to include the areas covered by the audit. Alternatively, a compliance checklist could be stapled to the flap of the file.

Compliance Checklist

A compliance checklist which can be attached to the sleeve of case-files and which may assist with Contract Compliance and Financial Stewardship Audits is at Appendix A of this Guide.

©Law Centres Network Page 15

ONSITE AUDIT

Who carries out this audit? This audit is carried out by the LAA’s Regional Offices. Under Clause 7.6 of the Contract Terms, the LAA requires that a provider must:

“…demonstrate to [the LAA’s] reasonable satisfaction that you are complying with, and have at all times while it has been in force complied with, this Contract. You must demonstrate this when [the LAA] are Auditing you and at such other times as [the LAA] may require in accordance with this Contract.”

The LAA can visit providers under Clauses 9.2 and 9.6 of the Contract Terms.

Audit Purpose This is an audit against a number of the requirements of the Standard Contract. Unlike a Contract Compliance Audit (CCA), this review also examines a number of Specialist Quality Mark (SQM) related requirements. Although the auditing of the SQM has been contracted out to the SQM Delivery Partnership, many of the SQM requirements have been incorporated into the Standard Contract which the LAA is therefore able to check. Scope of the Audit This audit checks compliance against the Contract. The audit is far broader in scope than a CCA or Contract Manager’s Visit (formerly known as a Financial Stewardship Audit). In addition to the areas covered in the CCA and Contract Manager’s Visits, a number of SQM requirements which have either been moved over or copied into the Standard Contract are also checked. The following table, which is used by the LAA, shows which former SQM requirements are now contained within the Standard Contract that the LAA may check on audit.

©Law Centres Network Page 16

SQM Provision Contract Reference A3.1 Non-discrimination in the provision of services D3.1 Non-discrimination in the selection, treatment and behaviour of staff F5.1 Non-discrimination when instructing suppliers

Contract Terms 5.1 – 5.7

B1.2 A procedure for conducting signposting and referral

Contract Specification 2.44-2.48

C2.2 Financial processes Requirement to maintain/produce profit and loss accounts, budgeting and expenditure

Contract Terms 4.1, 4.2, 4.3 and 4.6

C2.5 Professional indemnity insurance Requirement to maintain insurance up to £1 million

Contract Terms 7.4 and 7.5 (Requirement for £1 million for registered charities and standard SRA requirements (£2 million) for solicitors)

D3.1 Named category supervisor

Contract Specification 2.17 In order to receive or maintain a Schedule Authorisation in any Category you must employ a Full Time Equivalent Supervisor in that Category. If you cease to employ a Supervisor your right to undertake work in that Category will cease and a Sanction under Clause 24 of the Contract Terms may be applicable. Contract Specification 2.17 “All contact Work must be supervised by a Supervisor in the relevant Category of law”. Contract Specification 2.23-2.24 (temporary and external supervision)

D3.2 Supervisors’ legal competence D3.3 Supervisory skills D3.4 Supervisors legal training

Contract Specification 2.18 – 2.19

©Law Centres Network Page 17

SQM Provision Contract Reference D3.5 Conditions for supervision Contract Specification 2.30

D4.1 Case allocation Contract Terms 10.3

You must have in place processes to ensure that personnel that perform Contract Work are allocated work according to the role they are required to fulfil and on the basis of their skills, competence and capacity and any requirements set out in the Specification.

D5.2 Legal qualification of minimum hours (casework staff)

Contract Specification 2.29

E1.1 File lists (requirement to produce lists of open/closed files)

Contract Terms 7.16 (d) “You must have an IT System which enables you to perform your obligations under this Contract. Your IT System must include the following as a minimum:

(d) a system for accessing a list of all Matters and cases that are open and closed (where relevant)”

E1.3 Case files are logical and orderly

Contract Terms 8.1 “You must maintain a file for each Matter and/or case. Files, including electronic files, must be maintained in an orderly manner, showing all correspondence, attendance notes and disbursements on the relevant Matter or case, what Contract Work was performed, when it was performed and by whom, how it was performed and how long it took”

E2.1 File review processes and procedures E2.2 process management E2.3 File reviewers E2.5 Review records

Contract Terms 7.8 Contract Specification 2.31 “Each Supervisor must conduct file reviews for each Caseworker they supervise. The number of file reviews must reflect the skills, knowledge and experience of the individual. The Supervisor must record the outcome of files reviews, together with the details of corrective action taken (if any)”

F1.1 Recording and offering confirmation of basic information F1.2 recording and agreeing further information and confirmation in writing F2.3 Updating costs information F3.1 Confirming information at

Contract Terms 7.7 “You must have client services procedures that ensure that Clients are provided with appropriate information (including where relevant, information on costs incurred) in respect of their Matter or case”

©Law Centres Network Page 18

SQM Provision Contract Reference the end of the case G1.1 Complaints procedure G1.2 Central record and annual review of complaints

Contract Terms 7.9

G2.1 Client feedback procedure Contract Terms 7.8

In addition, the auditors may check for compliance against clauses 8.1, 8.2, 8.3 and 8.4 of the Contract Terms. These rules are reproduced below (emphasis added):

“Contract Work files 8.1 You must maintain a file for each Matter and/or case. Files, including electronic files, must be maintained in an orderly manner, showing all correspondence, attendance notes and disbursements on the relevant Matter or case, what Contract Work was performed, when it was performed and by whom, how it was performed and how long it took.

Recording information 8.2 You must record all information required by this Contract promptly and accurately and in accordance with this Contract. Material or repeated failure to do so shall be deemed to be a Fundamental Breach.

Records you must maintain 8.3 You must maintain true, accurate and complete records of all activities you undertake in connection with this Contract (“Records”), including:

(a) records of how you have (in accordance with Clause 7.8) effectively monitored your performance under and compliance with, this Contract, and the corrective action you have taken (if any);

(b) records of any Client complaints received and how they have been handled;

(c) the results of any Client satisfaction surveys;

(d) the results and reports of any internal (by you) and external (by us or a third party) audits, including any Audit (such as audits of your compliance with the Quality Standard by any third party);

(e) records of all identified non-compliances of the Contract and the corrective action taken;

(f) details of the operation of your Equality and Diversity Policy, procedures and communications and an assessment of its effectiveness;

©Law Centres Network Page 19

(g) information about your organisation for internal use including office manuals and information relating to your Clients;

(h) the annual accounts and information referred to in Clause 4.1, and 4.3;

(i) a comprehensive record of findings for each file review you undertake including records and details of corrective action taken to improve performance;

(j) the identity of, and work performed by, any Agents, Counsel, Approved Third Parties and sub-contractors you have instructed to carry out Contract Work pursuant to Clause 3;

(k) files for each Matter and/or case referred to in Clause 8.1; and

(l) up-to-date records (including accurate values) of current work in progress in respect of all Contract Work.

8.4 Records maintained pursuant to Clause 8.3 must be sufficient: (a) to verify and demonstrate performance of and compliance with your obligations under this Contract;

(b) to verify and demonstrate the accuracy of information supplied by you in respect of Contract Work;

(c) to enable Assessments to be performed;

(d) to verify and demonstrate the accuracy of all information supplied by you under or in connection with Clause 14;

(e) to facilitate an Official Investigation; and

(f) for such other purposes as we reasonably consider necessary in connection with our statutory duties or functions.”

On-Site Audit Plan An example LAA On-Site Audit Plan which is sent to the provider before the audit is at Appendix B of this Guide.

©Law Centres Network Page 20

Audit Process The auditors from the LAA will visit your offices and carry out the audit. The length of the audit will depend upon numbers of staff and offices (although two days is a likely length for such an audit). In addition to inspecting the central records as outlined above, a sample of files are selected from either the list of open files, from the filing cabinet or from the file review records. Files will be selected from each category that the Law Centre holds a Contract in plus a small number of ‘tolerance’ files. Typically, the auditor will look at approximately 7 files per category but the actual number may be higher or lower depending upon any issues identified in the files. If the auditor finds an issue, because this is not an official SQM audit, they do not raise a General or Critical Quality Concern. Instead, they may issue a Contract Notice or an Observation. If the auditors find an isolated example of non-compliance; for instance, evidence that a couple of scheduled file reviews had not taken place, then an Observation would be raised. If on the other hand, the majority of scheduled file reviews had not taken place, the auditors would raise a Contract Notice on the basis that the system was not found to have been in effective operation. There is no sanction applied to the Law Centre if an Observation is made but a Contract Notice should be taken seriously as any repeat of the same Contract Notice may lead to Contract Sanctions being taken. These sanctions are detailed in Clause 24 of the Contract Standard Terms. Compliance Tips Assuming that you have an internal audit system which includes internal Contract Compliance checks (see above) and an internal SQM audit checklist, then there is no need to implement an additional monitoring system.

Quality Assurance Checklist A simple one page checklist which is useful to check ongoing compliance is at Appendix C of this Guide.

©Law Centres Network Page 21

CONTRACT MANAGER’S VISIT (Formerly known as Financial Stewardship)

The latest guidance from the LAA seems to have re-named the Financial Stewardship Audit as a Contract Manager’s Visit. However, some LAA staff still occasionally refer to these types of audit as Financial Stewardship. Please note that the previously used Financial Stewardship manual is no longer available on their website and is rarely used by auditors now. Who carries out the audit? As the name suggests, a Contract Manager’s Visit is carried out by the LAA Contract (or Relationship) Manager at your offices. Audit Purpose This audit is similar to the Contract Compliance Audit in that it also covers form completion and evidence of means. However, it also covers other areas such as case splitting, management of payments on account and validation of tolerance claims. It is, however, fundamentally different in approach to a Costs Compliance Audit. Rather than the LAA staff auditing a large number of files, the LAA’s Contract Manager will ask the Law Centre to carry out the audit itself where concerns exist. Further information about how this happens in practice is outlined later in this section. Why a provider may receive a Contract Manager’s Visit The LAA aim to conduct such a visit at providers at regular intervals, usually annually. This is a relatively light touch audit which usually takes around 4 to 5 hours. Scope of the audit The Contract Manager’s visit will cover a selection of case files and will typically include one or more of the following areas:

(i) Completion of CW1 and CW2 Forms;

(ii) Evidence of Means;

(iii) Case Splitting & Duplicate Claiming;

(iv) Family Fees;

(v) Evaluating Work in Progress;

©Law Centres Network Page 22

(vi) Management of Certificated Payments on Account; and

(vii) Validation of tolerance Claims.

Checking the completion of forms and obtaining evidence of means is effectively a duplication of what is covered in the Contract Compliance Audit (for guidance therefore, please see the comments made earlier). Case Splitting All Law Centres should read and be familiar with the relevant provisions in the Contract. The general provisions are contained in the current Standard Contract Specification in sections 3.40 -3.50 (General Provisions), section 7 (Family), section 8 (Immigration) and Section 10 (Housing and Debt). Evaluating Work in Progress (WIP) Given that Law Centres may claim payments on account (POA) based upon their valuation of their WIP, the LAA wish to check that the level of WIP declared as at a certain date was accurate. On cases where a POA has been claimed, the Contract Manager asks the Law Centre how they can demonstrate that the value of unbilled work exceeds the value of the POA claimed. Management of Certificated Payments on Account This check follows on from evaluating WIP. Here, the Contract Manager selects 5 files to verify whether the WIP system is accurate in practice. Specifically, the Contract Manager is thinking about:

a. The Law Centre’s behaviour in response to their queries b. Whether the Law Centre understands the rules relating to claiming a POA c. Whether Law Centre is closing cases promptly

Most importantly, the Contract Manager is checking whether the amount of the POA exceeded 75% of the profit costs at the time of the POA claim. Law Centres should be claiming Payments on Account in order to help their cashflow. Validation of Tolerance Claims

©Law Centres Network Page 23

This may still be applicable for reviews of work undertaken pursuant to the 2010 Contract. Before the visit, the Contract Manager reviews all tolerance claims for the last 12 months and checks whether any claims have been made in tolerance barred categories (Family, Immigration, Clinical Negligence, Actions against the Police, Education, Public Law or Mental Health) and whether the number of tolerance matter starts in the contract schedule has been exceeded. Follow up action Contract Managers will disallow any claims made in tolerance barred categories or where matter starts have been opened in excess of the contract schedule limit. Be aware that any errors identified may result in a Contract Notice being issued.

Where errors have been found, it is common for the LAA to ask providers to carry out a follow up self-audit involving a much larger sample of case files. In some cases, this will be a few dozen casefiles but in other instances this can involve checking hundreds of files.

It is not mandatory to co-operate and carry out a self-review. However, if co-operation was

withheld, the LAA would probably arrange for a formal Contract Compliance Audit to be carried out.

©Law Centres Network Page 24

COSTS ASSESSMENT Who carries out the audit? The audit is carried out by the LAA. Costs are assessed by the LAA where cases are paid at hourly rates. These include a significant number of certificated claims, all (controlled) exceptional case cost claims and some immigration cases. Civil Costs Guidance The April 2013 version of the Costs Assessment Guidance applies to work governed by the 2013 Standard Civil Contract. The 2013 version of the guidance is available on the Justice website: http://www.justice.gov.uk/downloads/legal-aid/funding-code/costs-assessment-guidance-2013-standard-contract.pdf For detailed guidance on the Costs Assessment Guidance and Assessment process, please refer to the Costs Guide in this document.

Appeals

Assessment decisions may be appealed. The Contract Specification allows appeals within 28 days of notification of the assessment decision. You may request that the 28 day time limit be extended (up to a maximum of a further 14 days) for good reason. The appeal will be dealt with by the Assessor on the papers only; there is no general right for either party to attend or be represented at the appeal. At any point after the submission of an appeal, but no later than 21 days after receipt of the Assessor’s final decision, either you, the Director or the Assessor may seek clarification of a Point of Principle of General Importance. When submitting representations, many providers make the mistake of using a subjective as opposed to an objective style of writing. For instance, some focus on the unfairness of the assessment without providing clear reasons why the assessment is flawed.

©Law Centres Network Page 25

When challenging assessment decisions, it is a good idea to start by summarising the Assessor’s point before going on to explain why you disagree with the decision. The golden rule is to, wherever possible, quote a relevant paragraph from the Contract Terms, Contract Specification or Costs Guidance in support of your view. It is these documents that Assessors use when considering whether to uphold your representations.

©Law Centres Network Page 26

ESCAPE FEE (PREVIOUSLY KNOWN AS EXCEPTIONAL CASE) COSTS AUDITS

Who carries out the audit? The audit is carried out by the LAA. Background Legal Help claims are usually paid by way of a fixed fee. However, if the costs reach the ‘escape feel threshold’, Law Centres may claim to be paid at hourly rates instead. Process for Claiming Escape Fee Costs The fixed fee element of the claim is triggered in the usual way by submitting a claim on the CMRF form. At the end of the case, the Law Centre also completes an Escape Fee form. Audit Purpose The audit is an assessment of the costs claimed in order to ensure that the costs claimed appear reasonable and are in accordance with the rules of the Standard Contract. As the assessment applies to each file individually, the LAA does not extrapolate reductions to other claims. Similarly, the LAA has not, as far as we are aware, issued Contract Notices to Law Centres as a result of having costs on individual files reduced on assessment. Impact of reductions on Law Centres Aside from the obvious reduction in income, the data generated by these audits is used by the LAA to measure one of the Key Performance Indicators (KPIs). This KPI is reproduced below:

“KPI 1: The aggregate amount by which the costs claimed by you in all relevant cases are reduced on assessment (after any appeals have been completed) must not exceed the following percentage: 10%”

©Law Centres Network Page 27

Appeals Appeals against any reductions may be made in the usual way described above.

©Law Centres Network Page 28

NATIONAL AUDIT OFFICE (NAO) AUDITS

Background and Initial Audit Until fairly recently, the National Audit Office had very little to do with the way in which the LAA conducted its auditing of providers. However, in October 2009 the NAO refused to sign off the LAA’s accounts on the basis of their view that appropriate financial and audit controls were not in place at the LAA. This was because the NAO established through audit that some providers had over-claimed for legal aid work to the figure of £18.3m in 2008-09. They also found that £6.4m was erroneously paid to solicitors who provided legal aid to claimants without evidence that they were eligible to receive it. This audit qualification led to the NAO insisting that the audit regime was stepped up and staff from the NAO were sent to the LAA to monitor the audit programme. This also resulted in the birth of the Financial Stewardship Audit (now Contract Manager’s Visit). Audit Purpose The purpose of the NAO audit is to establish whether the correct fee was paid to the provider and whether the client was eligible for advice. The NAO typically select a number of files (say 100 files from 100 providers (1 file each)) and extrapolates the results to work out the loss to the legal aid fund. Last year’s exercise suggested that £24.3 million was overpaid. Although an NAO audit is very similar in scope to a Contract Compliance audit, the end recipient of the audit is the LAA rather than the provider. Having said that, if the file selected results in costs being disallowed, the provider still has to refund the LAA! Follow up Audit Following increased scrutiny and the introduction of the FS audit, the NAO carried out a follow up exercise in order to determine whether audit performance had improved. That exercise demonstrated that, in their view, things are getting worse rather than better. The NAO has subsequently asked the LAA to further increase Financial Stewardship and other audit activity.

©Law Centres Network Page 29

DATA VALIDATION AUDITS

Background and Audit Purpose The NAO have also influenced the introduction of Data Validation Audits. These audits check whether the correct fee was paid to the provider and whether compliance with certain contract terms has been met e.g. whether issues leading to a Contract Notice being issued has been addressed. Who carries out the audit? This is carried out by the LAA’s Provider Assurance teams. Audit Process The LAA identify cases where the payment made is unusual or out of profile with other claims. These claims are listed in a spreadsheet. The spreadsheet outlines the nature of the LAA’s queries and invites comments in response. List of Activities Please refer to Appendix D for a complete list of the LAA Validation Audits provided by the LAA which explain how and why the audits are carried out together with potential outcomes.

©Law Centres Network Page 30

OFFICE VERIFICATION AUDITS

Law Centres may have experienced visits by their LAA Contract (or Relationship) Manager by way of a follow up or ‘verification’ of information submitted by the provider as part of previous bidding rounds for Standard Contracts. The LAA may wish to consider similar visits for the 2012/13 bidding round. Office Verification Where a new provider obtains a LAA Contract for the first time, the LAA will visit their offices. The purpose of this visit is to:

i. Verify that the office does indeed exist! (some providers have apparently made up offices in order to gain a contract for use at another office)

ii. Check that the provider understands how to report Controlled Work iii. Ascertain whether the provider has an I.T. system; and iv. Discuss the basics of the LAA Contract and compliance e.g. conducting file

reviews.

©Law Centres Network Page 31

PEER REVIEW

Peer Review is the measure that the LAA use to assess quality of advice. It has been developed over several years under the auspices of the Institute of Advanced Legal Studies (IALS). Peer reviewers have carried out thousands of assessments since 2000 and refined the process over the years. Who carries out the audit? This is developed and managed by IALS which is independent of the LAA. All peer reviewers are experienced practitioners, trained by IALS to carry out peer review using their framework. A sample of the peer reviewer’s own files has to be assessed at competence plus or above. Peer reviewers are consistency-checked against each other and receive regular training.

There are two reasons why a review might be carried out, e.g. routine bench-marking, or a Contract Manager’s concern about the potential quality of the work being carried out. The LAA’s current guidance on audits suggests that Peer Reviews are “usually triggered by an existing rating of 4 or 5 but that they may be requested by Contract Manager or as a result of other audit activity”. Paragraph 5.1 of Independent Peer Review Process specifically states that:

“Although the LAA retains the right to peer review a supplier at any time, and without specifying a reason, there are a number of different reasons why a supplier will commonly be selected for peer review. If peer review is used as a gateway assessment, or for access reasons, suppliers will either have put themselves forward for review or have been identified by their regional office. Suppliers may also be selected for peer review following the results of other LAA audit tools, to assess supplier performance. Suppliers are informed of the reason for the review. Peer reviewers are not

informed of the reasons for review.”

Possible results 1-5

There are five possible scores:

• Excellence (1)

• Competence plus (2)

• Threshold competence (3)

©Law Centres Network Page 32

• Below competence (4); or

• Failure in performance (5)

The LAA has defined the level of skill required under the Contract as at least threshold competence. At below competence level, the Law Centre will be given six months to improve. If they do not achieve at least threshold competence at their next assessment, their Contract will be terminated. A Law Centre assessed at failure in performance will have its Contract terminated quickly, because of the risk to clients. Issues of concern

Many Law Centres are concerned that the LAA’s standard fee schemes force them to spend less time on individual cases, with the risk that the quality of advice and client care may be reduced. The LAA have acknowledged that there is a tension between higher standards and fixed fees and reducing overall expenditure. However, they do not accept that ‘you get what you pay for’, they believe that there is no evidence to suggest that increasing quality will result in higher costs. They have said that there is evidence to suggest that threshold competence (3) work can be more expensive than competence plus or above2

. It is true that a poor advisor will often waste time on ineffective strategies, or conduct lengthy interviews due to a lack of interviewing skills. Nevertheless, peer reviewers characterise high quality advice as being holistic and tailored to the client’s circumstances, which does take time, and therefore tends to increase costs.

Good practice guidance

The LAA has tried to assist providers to reach competence plus by disseminating good practice Guides via its website: http://www.justice.gov.uk/legal-aid/quality-assurance/quality-guidance The LAA has also promoted workshops provided by the IALS and the Law Society in 2006 and 2008. Despite the tension between peer review and fixed fees, the workshops were received positively. The materials are also available from the LAA’s website. The peer review process

Twenty files are requested, of which at least fifteen are assessed. They are selected to cover all the different types of work carried out by the Law Centre within a category of law and are cases closed during the preceding twelve months. 2 ‘Quality Relationships Delivering Quality Outcomes’ - The Preferred Supplier Scheme: Response to

Consultation’ LSC December 2006

©Law Centres Network Page 33

Peer reviewers carry out the assessment at an LAA regional office. They do not meet the staff of the organisation being reviewed, which never finds out the identity of its particular reviewer, although they are sent a list of all the reviewers and asked to identify any possible conflict of interest. It usually takes 1-2 days to do an assessment and write a report.

The reviewers evaluate issues which relate to quality of advice and service. They do not look at how long was spent on the file and they do not carry out a Transaction Criteria3

audit. They apply the ‘pick up test’, which is the basic question – “if I, as another caseworker, picked up this file, could I understand what had been done and why, and what remained to do?”

They assess individual files and then consider the sample as a whole and form a conclusion about its overall quality. In many cases this involves a balancing act as some files may be good, others less so. Organisations scoring competence plus tend to have a higher level of consistency. For example, if there is a change of caseworker part way through the case the peer reviewer would look at the whole case, and in order to score competence plus or excellence, both caseworkers would need to achieve that level. Having assessed the fifteen files, the reviewer compiles a report identifying; positive findings, major areas of concern (if any), areas for development, suggested areas for improvement and any other comments. Reports are checked by IALS to ensure that the score reflects the comments the reviewer has made about the files. So, for example, they would pick up a contradiction if the sample scored competence plus but the reviewer had identified major areas of concern, and ask the reviewer to look at the report again. IALS does not double-check the assessment. The provider should receive the final report within 28 days. Scoring

Peer reviewers use checklists of criteria, which they score individually; but the overall score is not simply an average of the scores on individual files. Peer reviewers take account of any trends and patterns identified, including evidence of supervision.

Files which show one or two poor quality indicators would not automatically mean that the whole sample would be assessed at below competence; but if 5 or 6 files in the sample did, it would be. On the other hand, if problems were picked up, for example by a supervisor and effective corrective action was taken, the file could

3 Transaction criteria enabled the LSC to assess the extent to which a lawyer had obtained appropriate

information and followed steps associated with best practice. They did not allow any assessment to be made of the quality of legal advice. They have been superseded by peer review.

©Law Centres Network Page 34

actually score better than one without a ‘near miss’ in terms of poor advice. Standard letters and documentation

Peer reviewers accept that standard letters have their place; but that it is important to take an individual approach to them. This means ensuring that standard letters should not be ‘catch-alls’ which try to cover all eventualities; but should be specific to a client’s circumstances. So, for example, a letter setting out the different possession proceedings in relation to both owner-occupiers and tenants would not impress a peer reviewer, who would expect the client to be given only the information that applied to his or her case. As in all kinds of file-based assessment, it is vital that the file is complete. Some organisations send leaflets to clients; but do not put a copy of standard information on the file, in order to save paper and printing costs. Peer reviewers advise that if that is the way you work, it is important to include copies of all standard information leaflets with the file sample. Peer Review: General Issues Examples of issues that commonly arise are:

• Providing a clear record for the client of the instructions received, the advice given and the agreed action

• Ensuring that linked issues are dealt with

• Providing advice that is tailored to the individual client’s needs

• Delay

• Taking and recording sufficient instructions; and

• Ensuring that the client is constantly advised regarding correspondence and documents received

©Law Centres Network Page 35

SECURE EMAIL AUDIT What is secure email? The secure email system is a service whereby members can easily send encrypted emails to other members of the system. Using secure email substantially reduces the risks of being spammed, hacked, or inadvertently downloading a virus. The system is financed by the government although the government has no right of access to emails sent using this system. It is free of charge to users and is popular with organisations that handle sensitive information. Initially, the system was designed for users of the Criminal Justice System but this has now been widened to include other groups such as civil solicitors and voluntary organisations. There are over 6000 organisations currently using the system. Information about the system can be accessed here: http://www.cjsm.cjit.gov.uk/ Users who sign up for the system must agree to the system’s terms and conditions. Who carries out the audit? The MoJ carry out audits at random to check that users are, in practice, following the terms and conditions of the service. The audit process An auditor from the MoJ asks to see evidence of compliance against a set of requirements contained the service’s terms and conditions. Typically, the audit could last for between 2 and 7 hours depending upon the size of the organisation. The full list of the areas audited is covered in the terms and conditions document in Appendix E. A shortened list is reproduced below:

i. A log of all persons accessing the service via SMTP (usually Outlook) covering the previous 6 months;

ii. Business Continuity/Disaster Recovery Plan; iii. Portable devices (e.g. USB drives) used for CJSM work are encrypted; iv. Wireless access must be via WPA/WPA2 standards (and not accessed in a

hotel, café etc);

©Law Centres Network Page 36

v. Any access to CJSM via a tablet, smartphone or wireless device has been specifically authorised by the MoJ;

vi. Firewall is in place; vii. Anti-virus and spyware software is in place; and

viii. Operating system updates and security patches are regularly applied to all servers and PCs.

On completion of the audit the auditor will provide the audit inspection report to the CJSM Accreditor who then forwards it to the organisation. The report lays out the breaches in order of Critical, Major and Minor. The organisation is given 6 weeks to fix Critical breaches, 6 months to fix a Major and 12 months to fix a Minor breach. This is tracked by the MOJ Operational Security Manager with responsibility for CJSM. What are the sanctions for non-compliance? If an organisation refuses to be audited or does not agree to complete the remedial actions, the MoJ will likely remove the organisation from the secure email system. If they believe personal sensitive data is at risk, they may report this to the ICO.

©Law Centres Network Page 37

APPENDIX A – COMPLIANCE CHECKLIST

COMPLIANCE

CHECK LIST

Y

N

NA

Matter within scope?

Sufficient Benefit test met?

Legal Help form properly completed?

Acceptable evidence of means?

Case closed & reported?

Correct matter type & end point code?

If the case was split, (Controlled cases) was this justified on the file?

Caseworker Signature:

Date:

COMPLIANCE

CHECK LIST

Y

N

NA

Matter within scope?

Sufficient Benefit test met?

Legal Help form properly completed?

Acceptable evidence of means?

Case closed & reported?

Correct matter type & end point code?

If the case was split, (Controlled cases) was this justified on the file?

Caseworker Signature:

Date:

©Law Centres Network Page 38

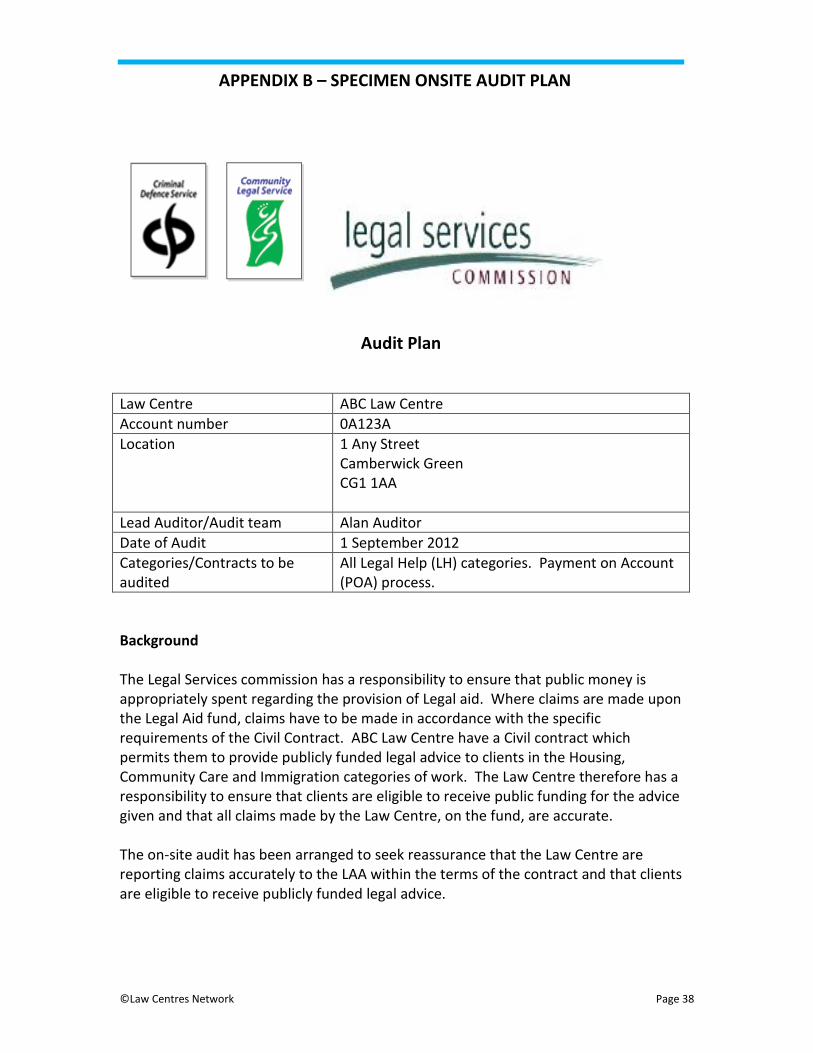

APPENDIX B – SPECIMEN ONSITE AUDIT PLAN

Audit Plan Law Centre ABC Law Centre Account number 0A123A Location 1 Any Street

Camberwick Green CG1 1AA

Lead Auditor/Audit team Alan Auditor Date of Audit 1 September 2012 Categories/Contracts to be audited

All Legal Help (LH) categories. Payment on Account (POA) process.

Background The Legal Services commission has a responsibility to ensure that public money is appropriately spent regarding the provision of Legal aid. Where claims are made upon the Legal Aid fund, claims have to be made in accordance with the specific requirements of the Civil Contract. ABC Law Centre have a Civil contract which permits them to provide publicly funded legal advice to clients in the Housing, Community Care and Immigration categories of work. The Law Centre therefore has a responsibility to ensure that clients are eligible to receive public funding for the advice given and that all claims made by the Law Centre, on the fund, are accurate. The on-site audit has been arranged to seek reassurance that the Law Centre are reporting claims accurately to the LAA within the terms of the contract and that clients are eligible to receive publicly funded legal advice.

©Law Centres Network Page 39

Scope of audit

• A review of WIP/running record of costs, account ledger reports and financial information

• Discussions with members of ABC Law Centre where applicable (caseworkers, supervisors and particularly administration/accounts staff involved with publicly funded files including the staff responsible for billing the work)

• A review of closed and open LH files. The audit will encompass (but will not necessarily be limited to) the following specific areas: Work in Progress (WIP) and Payments on account (POA) • Format for audit

o Discussion with Liaison Manager and potential discussion with billing/accounts staff and possible review of certificated files

• Documentation required for the audit o The Law Centre should provide a full summary/statement setting out

their overall WIP figure for all publicly funded work. This will then be discussed during the opening meeting

o Individual print outs of the accounts ledgers and the WIP and running record of costs for each of the certificated cases listed at the end of the audit plan.

Accuracy of claims made and codes used • Format for audit.

o Review of closed files and discussion with fee earners, supervisors & staff responsible for allocating final claim codes

• Documentation needed for the opening meeting o Civil Legal Help files as per the closed file list at end of audit plan.

Eligibility of Clients • Format for audit.

o Review of closed files and discussion with fee earners, supervisors & staff

• Documentation needed for the opening meeting o Civil Legal Help files as per the closed file list at end of audit plan

Supervisory requirements • Format for audit

©Law Centres Network Page 40

o Review of completed supervisor self declaration forms. Discussion with supervisors and fee earners if applicable.

• Documentation needed at the opening meeting o Completed supervisor self declaration forms for all supervisors

undertaking publicly funded work (forms must have been completed in the month prior to the audit to be considered up to date)

General requirements The following will be required and should be made available in time for the commencement of the opening meeting;

• Staff structure chart – identifying staff dealing with publicly funded cases, supervisors and support staff

• Open file list – detailing file opening date and identifying whether a case is LH or Certificated

• Complaints records • File review records for last 12 months • Training records • Business Plan • Office Manual • Profit and loss accounts

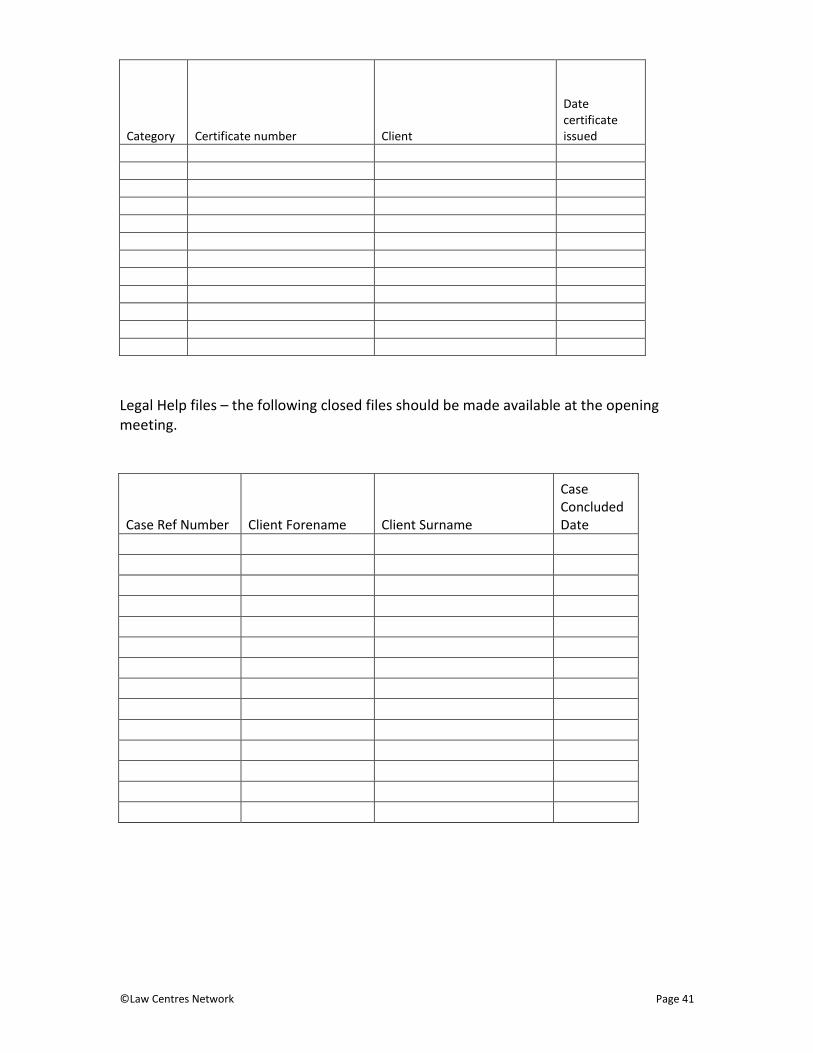

Other documents and / or files may be required during the audit and will be identified as soon as possible after the opening meeting. Timetable The timetable is flexible and every attempt will be made to work around client appointments etc wherever possible. The auditor anticipates arriving on the day of the audit at approximately 9.30am, with a view to commencing the opening meeting shortly after arrival. Certificated cases For the following cases full ledger/account print outs, WIP and running record of costs/time recording should be available at the opening meeting.

©Law Centres Network Page 41

Category Certificate number Client

Date certificate issued

Legal Help files – the following closed files should be made available at the opening meeting.

Case Ref Number Client Forename Client Surname

Case Concluded Date

©Law Centres Network Page 42

APPENDIX C – QUALITY ASSURANCE SELF ASSESSMENT CHECKLIST

Y/N

N/A Y/N

N/A Personnel Records Have any new members of staff joined in the last month? If yes, have the following been set up for each new member of staff:

• training plan • training record • induction plan/record • job description

Are all training records up to date? Do all members of staff have training plans? Have all members of staff employed for more than 12 months had an appraisal in the last year? Have recruitment records been kept for 12 months & then destroyed?

Client Satisfaction Have client satisfaction questionnaires been sent out to clients? Have any complaints been reported to the complaints handling person?

If yes, has a reply to the client/Legal Ombudsman been sent? If yes, is a copy filed in the central register? How many complaints have yet to be settled? Is any action outstanding on the part of the Law Centre?

Experts Has the Quality Rep been notified of any new experts that have been instructed? If yes, has the new expert been evaluated? Is the new expert approved for future use? If so, has the expert been added to the list of approved suppliers?

Financial Records Is there a current business plan? Is there a current annual budget? Is variance analysis up to date? Is time recording up to date (up to one month behind)?

File Reviews Are file reviews up to date? If no, which reviews are missing?

Referrals Has the Quality Rep been notified of any client that has been referred? If yes, has a copy of the completed form been posted to the Central Register?

©Law Centres Network Page 43

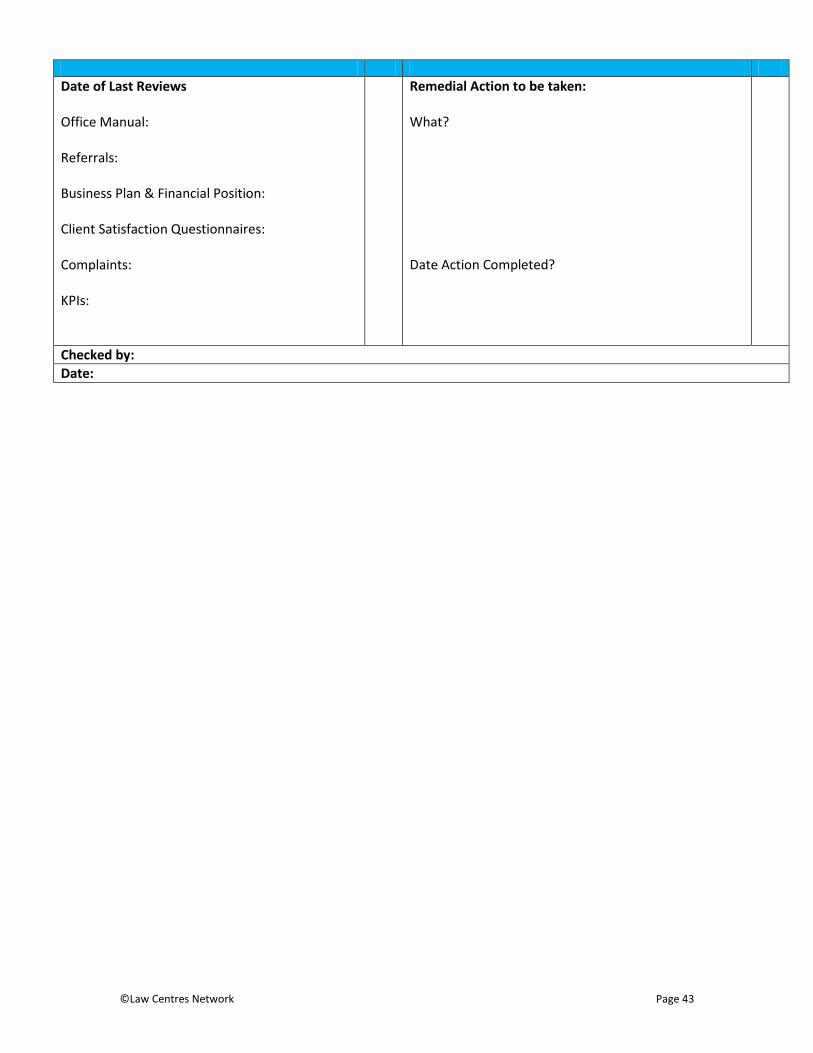

Date of Last Reviews Office Manual: Referrals: Business Plan & Financial Position: Client Satisfaction Questionnaires: Complaints: KPIs:

Remedial Action to be taken: What? Date Action Completed?

Checked by: Date:

©Law Centres Network Page 44

APPENDIX D – DATA VALIDATION ACTIVITIES

Data Validation Activities Activity Why How Potential Outcomes Validation Crime Lower Claim

Providers claims analysed to identify potential mis-claims

Claims data entered into a tool which draws out possible discrepancies. The provider receives a letter asking for validation of the claims. If the analysts are happy with the response, no further action is required. If the issue is not resolved, files may be requested and reviewed by the analysts.

• No issues identified – no provider contact

• Some issues identified – provider self review required

• Significant issues or self review provides evidence of significant misclaims – LAA audit to be conducted

• Recoupments made where overclaims identified

• Contract Notices may be issued

Validation Family Level 2 Review sample of provider

claims based on volume of Level 2 claims submitted in financial year 09/10. May also be referral from Contract Managers/Auditors

Individual files selected using claim submission data (there is no limit to the number of files selected in a sample) taking into account combinations of claim/matter type/outcome codes and actual profit cost data, which could indicate inappropriate fees claimed. Reviews undertaken through a mixture of file assessment and provider self-review.

• No issues identified – no provider contact

• Some issues identified – provider self review

• Significant issues or self review provides evidence of significant misclaims – LAA audit to be conducted

• Individual claims will be appropriately re-priced/ nilled on assessment

• Contract Notices may be issued

©Law Centres Network Page 45

Data Validation Activities Activity Why How Potential Outcomes Validation Recurring Client (Civil)

Referral from Contract Manager/Auditor following Financial Stewardship and/or Audit activity, where Recurring Client has been identified as a particular issue.

Individual files selected using claim submission data (there is no limit to the number of files selected in a sample) taking into account combinations of claim data. Reviews undertaken through a mixture of file assessment and provider self-review.

• No issues identified – no provider contact

• Some issues identified – provider self review

• Significant issues or self review provides evidence of significant misclaims – LAA audit to be conducted

• Individual claims will be appropriately re-priced/ nilled on assessment

• Contract Notices may be issued.

Validation Magistrates Court Fees

Individual claims identified as requiring validation as incompatible claim codes and data submitted.

Providers contacted and asked to correct the specific element of the claims.

• No validation issues – no provider contact

• Some validation issues - Individual claims amended as per provider response to validation request

Validation Exact/Near Exact Duplicates

Individual claims identified as requiring validation where a number of key fields on the claim submission data duplicates that of another claim.

Providers contacted and asked to confirm correct claim information.

• No validation issues – no provider contact

• Some validation issues - Individual claims amended as per provider response to validation request

©Law Centres Network Page 46

Data Validation Activities Activity Why How Potential Outcomes Validation Litigator Fees Data Validation activity

whereby a provider’s Litigator Fee claims are analysed to identify possible incorrect or duplicate claiming

Claims data is run through a validation database to identify matters which appear similar. The firm receive a letter asking for validation of the claims. If the analysts are happy with the response, no further action is required. If the issue is not resolved, files may be requested and reviewed by the analysts. There is a right to appeal as per the funding order

• No issues – no provider contact

• Possible duplication – Provider receives a letter detailing possible issue. Full right of response and opportunity to provide further evidence

• Recoupments will be made where duplicate or misclaims

identified

• Contract Notice may be issued if incorrect claiming identified

Validation Mediation Claim

Referral from Contract Manager/Auditor following Financial Stewardship and/or Audit activity.

Individual files selected for review (limited number in a sample). These will be chosen on a random basis or to resolve specific issues i.e. financial eligibility.

• Individual claims will be appropriately re-priced/nilled on assessment

• Contract Notice issued if incorrect claiming identified on two or more files

Fund Risk File Review NAO mandatory testing across all categories

Quarterly review . Usual impact on providers is to request additional information or supporting evidence.

• No errors or missing evidence – no action or contact with providers

• Errors or missing evidence – Providers contacted to provide extra information necessary

Contract Notice Verification Process

Verified six months after issue to measure improvement in behaviour

Limited review of files to ascertain whether the issue resulting on the Contract Notice has been addressed.

• Issued addressed – no further action required

• Issue still in evidence – repeat Contract Notice issued which may result in Termination

©Law Centres Network Page 47

Data Validation Activities Activity Why How Potential Outcomes Validation Immigration Claim Duplicate Claims Checking CWA submissions – Nov07- present for duplicate submissions

Review claim data to ensure correct claiming in this category

Data analysed for evidence of duplicate client, additional payments, hourly rate –v- standard fee claims.

• No issues – no provider contact

• Issues identified – data sent to providers asking for clarification of submissions

• Recoupment if duplicate and voiding of submission

• Significant issues identified – Contract Notice may be

issued

Validation Immigration Claim Phase 2 Validation of VAT paid on Asylum cases.

Review claim data to ensure correct claiming in this category

Data analysed to ensure correct VAT rate claimed with asylum cases, recurring client and low advice times.

• No issues – no provider contact

• Some issues – data sent to providers for clarification of submissions

• Recoupment and/or voiding of submission

• Likely Contract Notice if large numbers of incorrect submissions made

Debt Advice in Prison (DAiP)

Conclusion of pilot scheme (April 2011) necessitating final verification of claim data

Limited review of files per prison to ascertain compliance with DAiP Contract terms.

• No issues – no provider contact

• Some issues – further sample of files reviewed. Individual claims will be appropriately re-priced/ nilled on assessment and factored in to final reconciliation of Contract

©Law Centres Network Page 48

APPENDIX E – SECURE eMail Terms and Conditions

Terms & Conditions for Connection to the Criminal Justice Secure eMail Service (CJSM) This version (8.5M L) for completion by organisations, including sole practitioners with staff.

1. We will ensure that all users in our organisation comply with UK Data Protection and Privacy Laws and all professional codes of conduct under which we are bound and all information transmitted through CJSM is treated as ‘Restricted’*. We acknowledge that any breach of these provisions may result in access to CJSM being suspended or terminated.

2. We agree to ensure that all members and employees of our organisation who are given accounts on, or authorised access to, the CJSM understand the conditions on which connection has been granted as set out in this document and that the conditions are ongoing and cover any continuous use of CJSM. To this end: all those users given accounts will sign a commitment to adhere to the Terms and Conditions.

3. To enable the source of any causes of security breaches to be traced for SMTP users, we confirm that we will maintain accurate and up to date records/logs of use showing who has accessed CJSM via SMTP for a rolling period of 6 months.

4. In the event of a security breach, or suspected breach of security, within our environment and involving Justice Data or our access to the CJSM, we will inform the CJSM Administrators immediately (via the CJSM Helpdesk). We understand that the MOJ reserves the right to investigate security incidents and we confirm that, should such an investigation be necessary, we will provide any necessary support, which may include the supply of relevant logs, to the best of our ability.

5. We will communicate to the MOJ (via the CJSM Helpdesk) all significant changes to the organisation’s technical infrastructure that impact access to, or could impact the integrity of, the CJSM service so that an assessment can be undertaken.

6. We confirm that all users of our organisation’s IT systems (including, where relevant, contractors and third party users):

• are authorised users and can be individually identified by having unique user names, email addresses and passwords (passwords must be a minimum of 8 alphanumeric characters and changed at least every 90 days); i.e. passwords must be a mix of upper and lower case alphabetic characters plus numeric and/or special characters.

• will not share their user credentials, and that if any user credential is compromised it will be changed as soon as possible and that users will be prevented from having multiple concurrent email sessions;

• receive appropriate security awareness training and awareness updates in organisational policies and procedures as relevant for their role.

©Law Centres Network Page 49

7. We will not transmit information through the CJSM that we know, suspect or have been advised is of a higher level of sensitivity than the CJSM is designed to carry (that is ‘Restricted’ material) nor will material be forwarded to anybody other than on a strict need to know basis.

8. We will not use CJSM for system to system automated emails without the permission of the MOJ.