Lecture notes to Stock and Watson chapter 4 Introductory linear regression Tore Schweder August 2008 TS () LN3 25/08 1 / 13

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lecture notes to Stock and Watson chapter 4Introductory linear regression

Tore Schweder

August 2008

TS () LN3 25/08 1 / 13

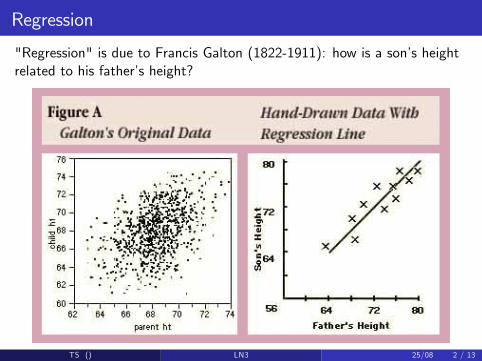

Regression

"Regression" is due to Francis Galton (1822-1911): how is a son�s heightrelated to his father�s height?

TS () LN3 25/08 2 / 13

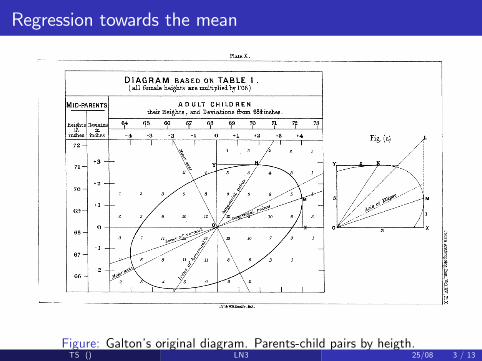

Regression towards the mean

Figure: Galton�s original diagram. Parents-child pairs by heigth.TS () LN3 25/08 3 / 13

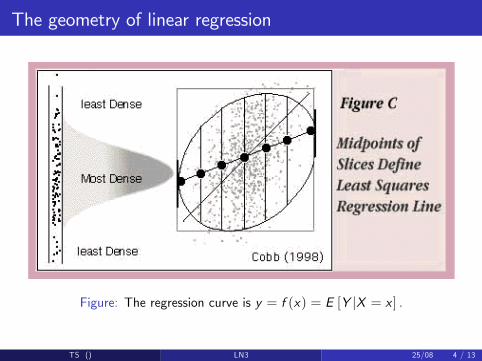

The geometry of linear regression

Figure: The regression curve is y = f (x) = E [Y jX = x ] .

TS () LN3 25/08 4 / 13

The linear regression model

Question: how is a response variable Y related to a stimulus variable X(explanatory/control/explanatory)? Assuming a linear relation,

1 what is the slope?2 is the slope positive?3 how good does the estimated line �t the observed data?

Example: Y = growth in BNP, X = in�ation previous year.

D : A sample of size n of pairs explanatory variables X and responsevariable Y .

M : (X1,Y1) , � � � , (Xn,Yn) is an iid random sample from an in�nitepopulation. Y = β0 + β1X + u;E [Y jX = x ] = β0 + β1x , Eu = 0, cov(u,X ) = 0. β0, β1 areparameters.

TS () LN3 25/08 5 / 13

OLS

Least squares and regression was known by Laplace and Gauss (80 yearsbefore Galton).

�bβ0, bβ1� = argminb0,b1

n

∑i=1(Yi � (b0 + b1Xi ))2

bβ1 =sXYs2X

= rsYsX, bβ0 = Y � bβ1X

Predicted response given the stimuli: bYi = bβ0 + bβ1Xi is the �ttedvalue.

(Empirical) residual: bui = Yi � bYi is the vertical distance from the�tted value to the observed value of Y . bu = 0, rbuX = 0

TS () LN3 25/08 6 / 13

Measures of �t

Homoscedasticity when var(Y jX = x) = σ2 is independent of x .

Then bσ2 = 1n�2 ∑n

i=1

�Yi � bYi�2 = 1

n�2RSS is unbiased.

TSS = ∑ni=1

�Yi � Y

�2= ∑n

i=1

�Yi � bYi�2 +∑n

i=1

�bYi � Y �2 =RSS + ESS

R2 = ESSTSS = 1�

RSSTSS = r

2XY

TS () LN3 25/08 7 / 13

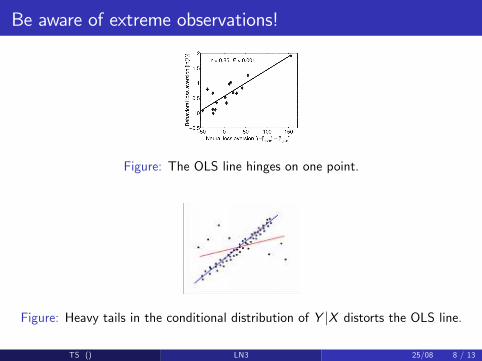

Be aware of extreme observations!

Figure: The OLS line hinges on one point.

Figure: Heavy tails in the conditional distribution of Y jX distorts the OLS line.

TS () LN3 25/08 8 / 13

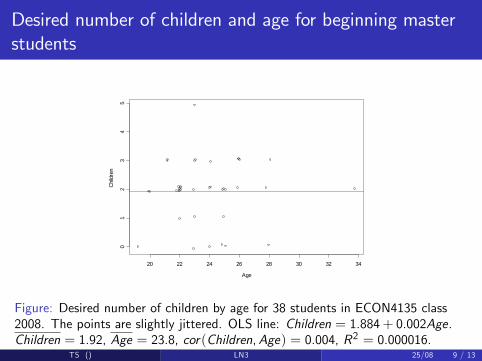

Desired number of children and age for beginning masterstudents

Age

Chi

ldre

n

20 22 24 26 28 30 32 34

01

23

45

Figure: Desired number of children by age for 38 students in ECON4135 class2008. The points are slightly jittered. OLS line: Children = 1.884+ 0.002Age.Children = 1.92, Age = 23.8, cor(Children,Age) = 0.004, R2 = 0.000016.

TS () LN3 25/08 9 / 13

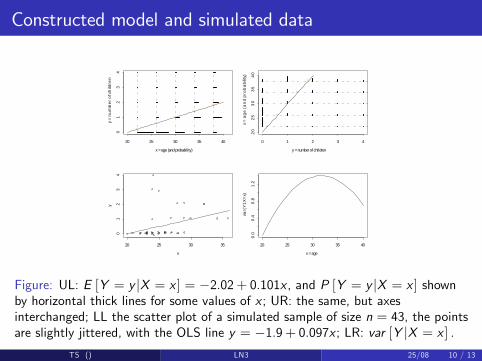

Constructed model and simulated data

x = age (and probability)

y =

nu

mb

er

of c

hild

ren

20 25 30 35 40

01

23

4

y = number of children

x =

ag

e (a

nd

pro

ba

bili

ty)

0 1 2 3 4

20

25

30

35

40

x

y

20 25 30 35

01

23

4

x = age

var(

Y1X

=x)

20 25 30 35 400

.00

.40

.81

.2

Figure: UL: E [Y = y jX = x ] = �2.02+ 0.101x , and P [Y = y jX = x ] shownby horizontal thick lines for some values of x ; UR: the same, but axesinterchanged; LL the scatter plot of a simulated sample of size n = 43, the pointsare slightly jittered, with the OLS line y = �1.9+ 0.097x ; LR: var [Y jX = x ] .

TS () LN3 25/08 10 / 13

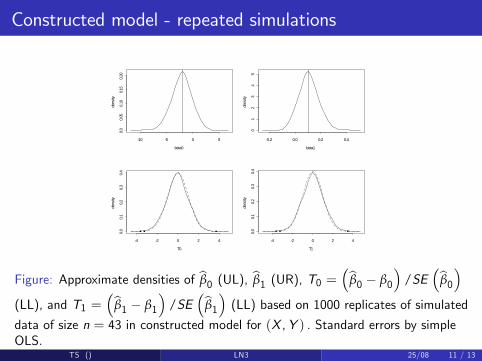

Constructed model - repeated simulations

beta0

dens

ity

10 5 0 5

0.0

0.05

0.10

0.15

0.20

beta1

dens

ity

0.2 0.0 0.2 0.4

01

23

45

T0

dens

ity

4 2 0 2 4

0.0

0.1

0.2

0.3

0.4

T1de

nsity

4 2 0 2 4

0.0

0.1

0.2

0.3

0.4

Figure: Approximate densities of bβ0 (UL), bβ1 (UR), T0 = �bβ0 � β0

�/SE

�bβ0�(LL), and T1 =

�bβ1 � β1

�/SE

�bβ1� (LL) based on 1000 replicates of simulateddata of size n = 43 in constructed model for (X ,Y ) . Standard errors by simpleOLS.

TS () LN3 25/08 11 / 13

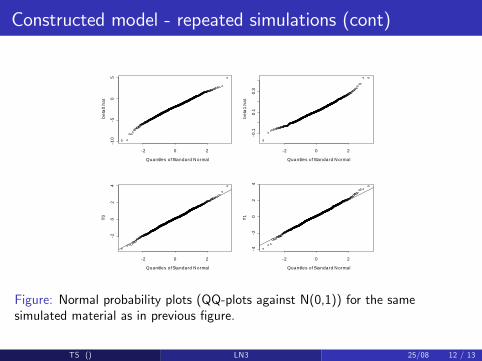

Constructed model - repeated simulations (cont)

Quantiles of Standard N ormal

beta

0.ha

t

2 0 2

10

50

5

Quantiles of Standard N ormal

beta

1.ha

t

2 0 2

0.1

0.1

0.3

Quantiles of Standard N ormal

T0

2 0 2

20

24

Quantiles of Standard N ormal

T1

2 0 24

20

24

Figure: Normal probability plots (QQ-plots against N(0,1)) for the samesimulated material as in previous �gure.

TS () LN3 25/08 12 / 13

Problems to be done in class

SW: 4.3

TS () LN3 25/08 13 / 13

Related Documents