Investment Banks Economics 71a Spring 2007 Mayo, Chapter 2 Lecture notes 2.2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Investment Banks

Economics 71a

Spring 2007

Mayo, Chapter 2

Lecture notes 2.2

Outline

What is an investment bank?Role in financial markets Investment banks and new securities

IPO mechanics

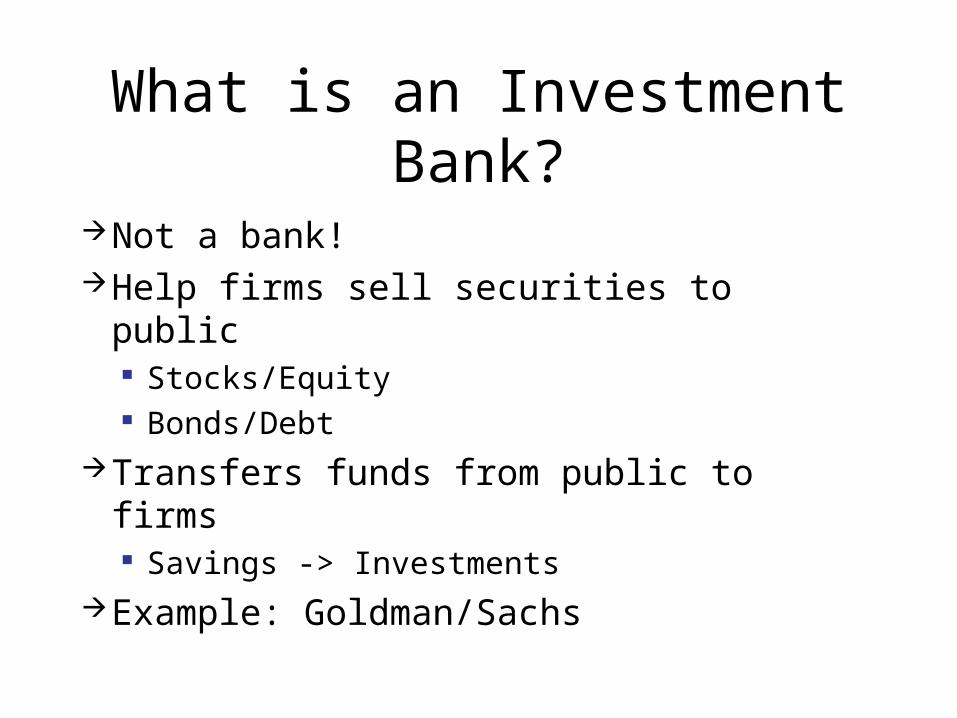

What is an Investment Bank?

Not a bank!Help firms sell securities to public

Stocks/Equity Bonds/Debt

Transfers funds from public to firms Savings -> Investments

Example: Goldman/Sachs

Initial Public Offering (IPO)

First sale of stock by firmOriginating investment bank

Key player in bringing the shares to market “Originating house” Handles most administrative details Reputation

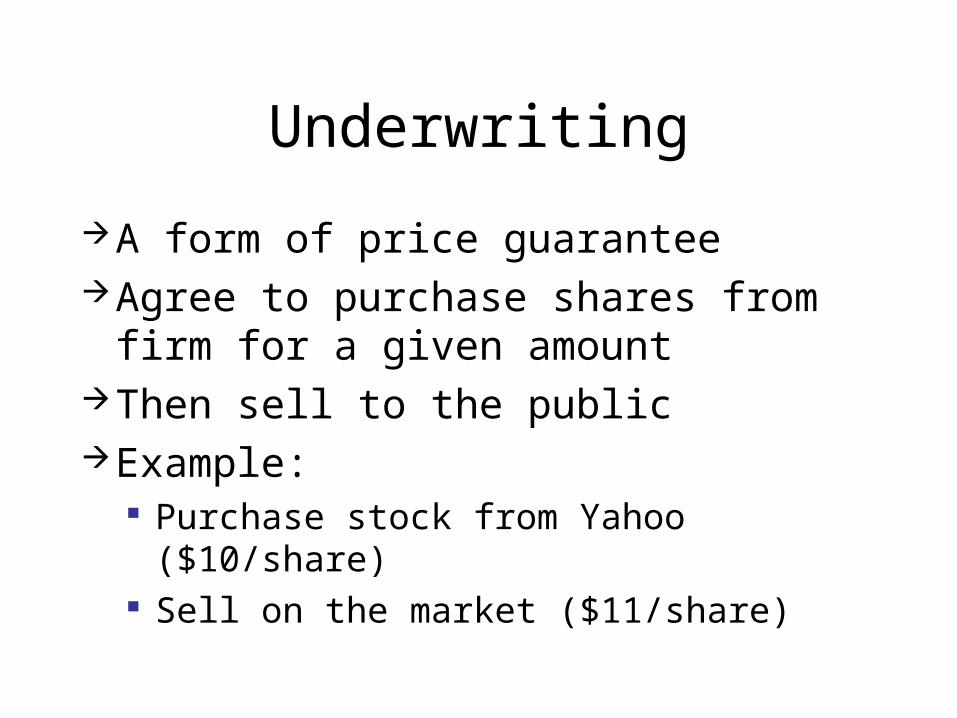

Underwriting

A form of price guarantee Agree to purchase shares from firm for

a given amountThen sell to the publicExample:

Purchase stock from Yahoo ($10/share) Sell on the market ($11/share)

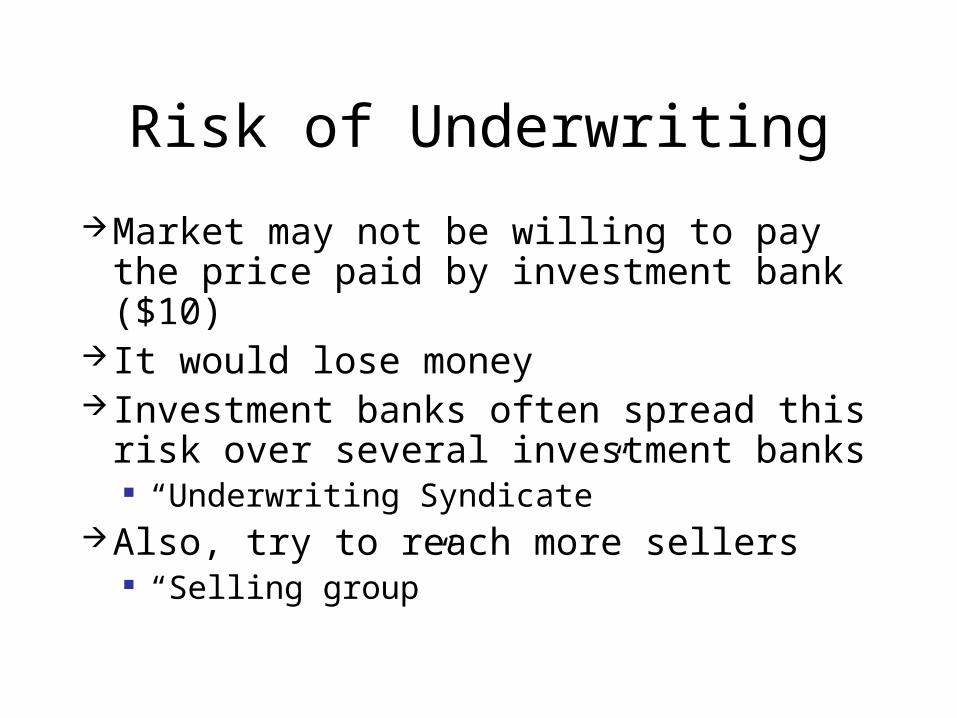

Risk of Underwriting

Market may not be willing to pay the price paid by investment bank ($10)

It would lose money Investment banks often spread this risk

over several investment banks “Underwriting Syndicate”

Also, try to reach more sellers “Selling group”

IPO Scandals

Most involve investment banks giving special deals to some favored customers (low prices)

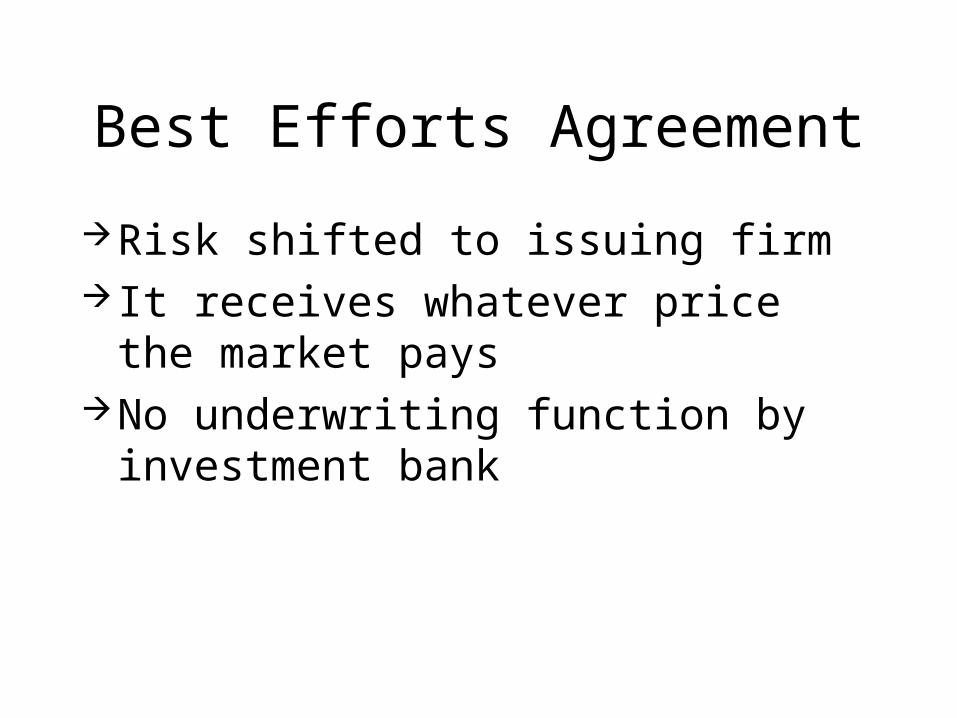

Best Efforts Agreement

Risk shifted to issuing firm It receives whatever price the market

paysNo underwriting function by investment

bank

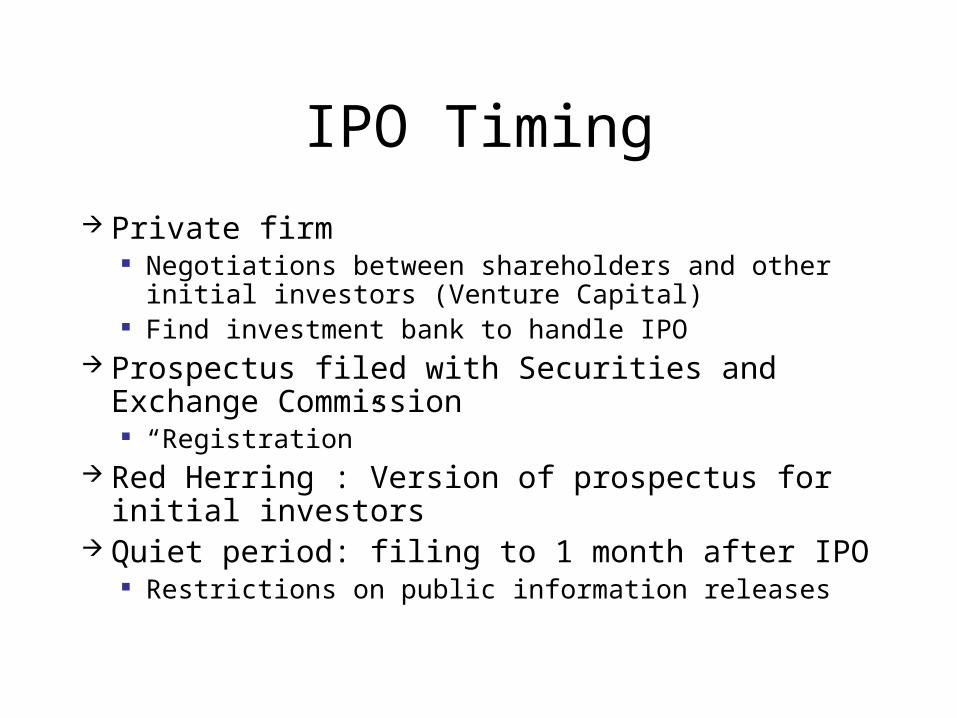

IPO Timing

Private firm Negotiations between shareholders and other initial

investors (Venture Capital) Find investment bank to handle IPO

Prospectus filed with Securities and Exchange Commission

“Registration” Red Herring : Version of prospectus for initial

investors Quiet period: filing to 1 month after IPO

Restrictions on public information releases

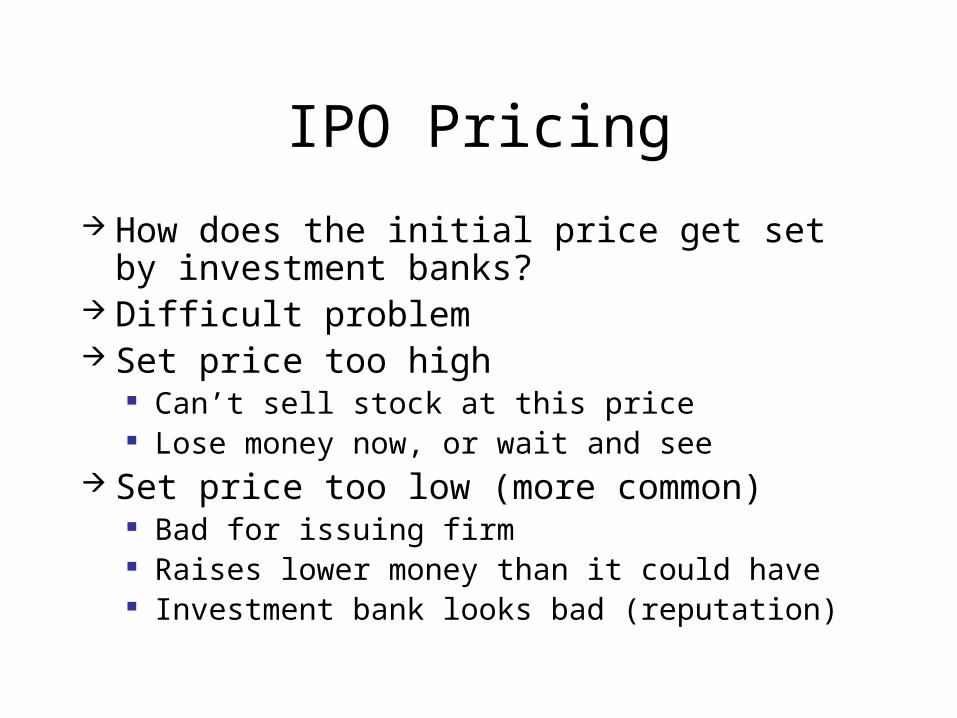

IPO Pricing

How does the initial price get set by investment banks?

Difficult problem Set price too high

Can’t sell stock at this price Lose money now, or wait and see

Set price too low (more common) Bad for issuing firm Raises lower money than it could have Investment bank looks bad (reputation)

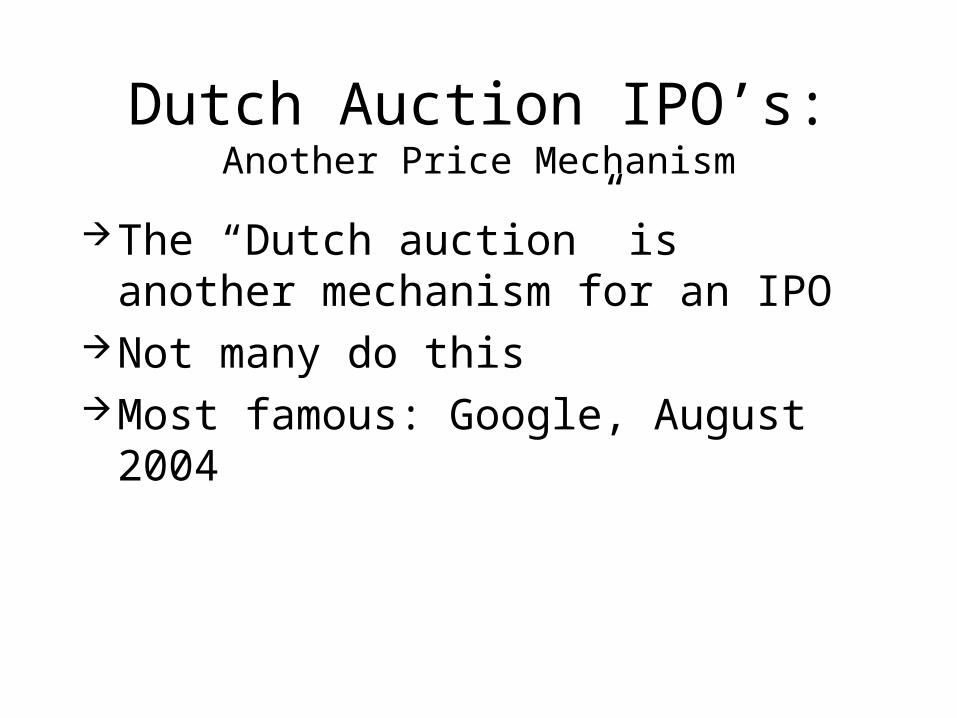

Dutch Auction IPO’s:Another Price Mechanism

The “Dutch auction” is another mechanism for an IPO

Not many do thisMost famous: Google, August 2004

Dutch Auction

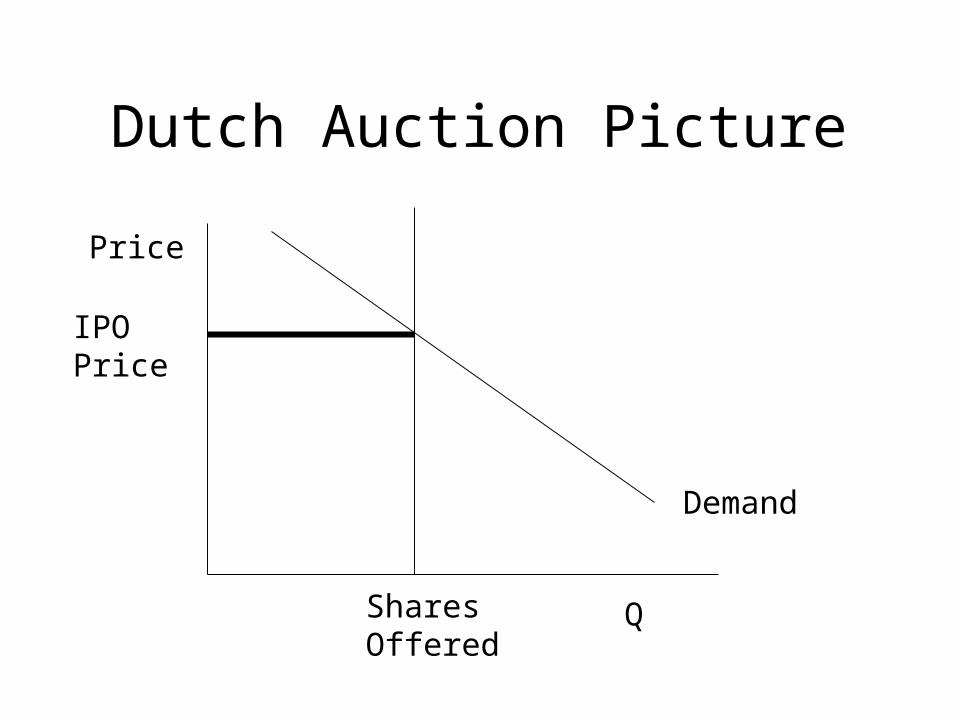

Seller announces total shares to be auctioned (Qshares)

Potential buyers submit bids for (Shares, Price)

Auction moves price down until Shares demanded above this price =

Qshares

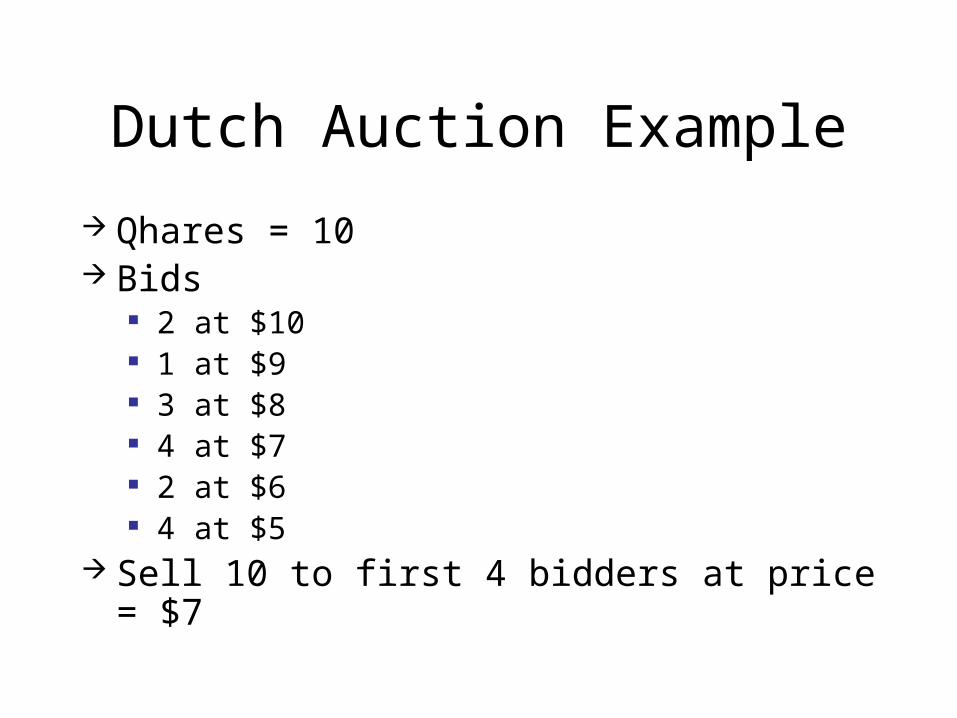

Dutch Auction Example

Qhares = 10 Bids

2 at $10 1 at $9 3 at $8 4 at $7 2 at $6 4 at $5

Sell 10 to first 4 bidders at price = $7

Dutch Auction Picture

Q

Price

Demand

IPOPrice

Shares Offered

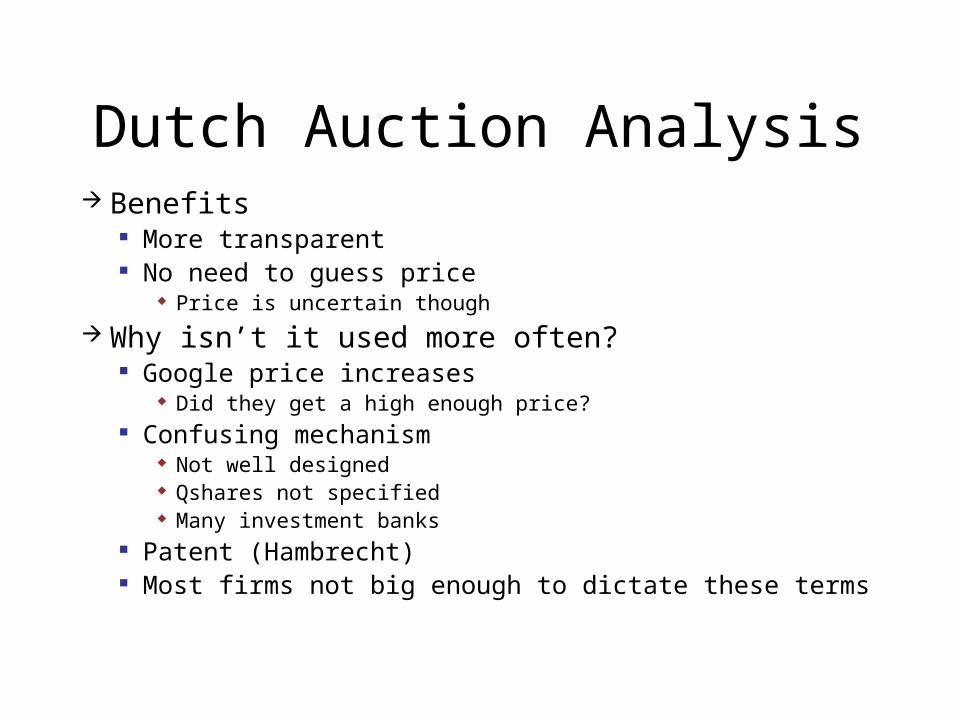

Dutch Auction Analysis Benefits

More transparent No need to guess price

Price is uncertain though

Why isn’t it used more often? Google price increases

Did they get a high enough price? Confusing mechanism

Not well designed Qshares not specified Many investment banks

Patent (Hambrecht) Most firms not big enough to dictate these terms

Later Stock Offerings

“Seasoned equity” Stock issued after IPO Registered with SEC Sold at current market prices Firm often stores these shares

“Shelf registration” Google again: How to estimate shelf shares

from web (public float and shares outstanding)

Private Placements

Shares sold to private investment groups Venture capital firms Private equity hedge funds

Usually, smaller, younger, riskier firms

Regulation

Securities and Exchange Commission Set up in the early 1930’s to oversee

securities markets Oversees publicly traded firms Public investment companies (mutual

funds)

SEC: Information and Regulation

Require timely release of information to public

10-K report: Annual information on firmFirms required to report major

information events to public

Insider Trading

Trading on private information Illegal (why?) Who’s an insider?

Employees Associated

Lawyers Investment bankers

Enforcement Trade reporting

Securities Investor Protection Corporation (SIPC)

Insures investors against failure in brokerage firms

Not insurance against price dropsLimited amounts

$500,000 total $100,000 cash balances

Sarbanes-Oxley (2002)

Scandals of the 1990’s Accounting information shaky and

deceptive (Enron, Worldcom,..)Government responseProtect investors from fraud

Sarbanes-Oxley

Basic provisions Creates Public Company Accounting

Oversight Board Strengthen the independence of auditors

(accountants) Firm directors take responsibility for

numbers

Conflict of Interest Problems

Many investment banks have brokerage sides

They will recommend stocks to investors: Analyst recommendations

What if same firm is doing IPO and writing recommendations?

There is supposed to be a “firewall”

Reponses to Sarbanes/Oxley

Board insurancePrivatizationMoving off shoreStill very much untested and

controversial

Related Documents