Financial Engineering Lecture 4

Lecture 4. Bullish StrategiesRiskReward Call purchaselimitedunlimited Synthetic long stockunlimitedunlimited Bull spreadlimitedlimited Protective Putlimitedunlimited.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Financial EngineeringLecture 4

Option Strategies

Bullish Strategies Risk RewardCall purchase limited

unlimitedSynthetic long stock unlimited

unlimitedBull spread limited limitedProtective Put limited

unlimitedBullish calendar spread limited

unlimitedCovered call unlimited limitedNaked put write unlimited limited

Option StrategiesBearish Strategies Risk RewardPut purchase limited

unlimitedSynthetic Put limited

unlimitedSynthetic short sale unlimited

unlimitedBear spread limited limitedCovered put write unlimited limitedBearish calendar spread limited

unlimitedNaked call write unlimited limited

Covered CallLong Stock, Short Call

Covered CallLong Stock, Short Call

Profit = S + call - P

BE = P - call

Protective PutLong Stock, Long Put

Protective PutLong Stock, Long Put

Profit = P - put - S

Synthetic Long Put Short Stock, Long Call

Synthetic Long Put Short Stock, Long Call

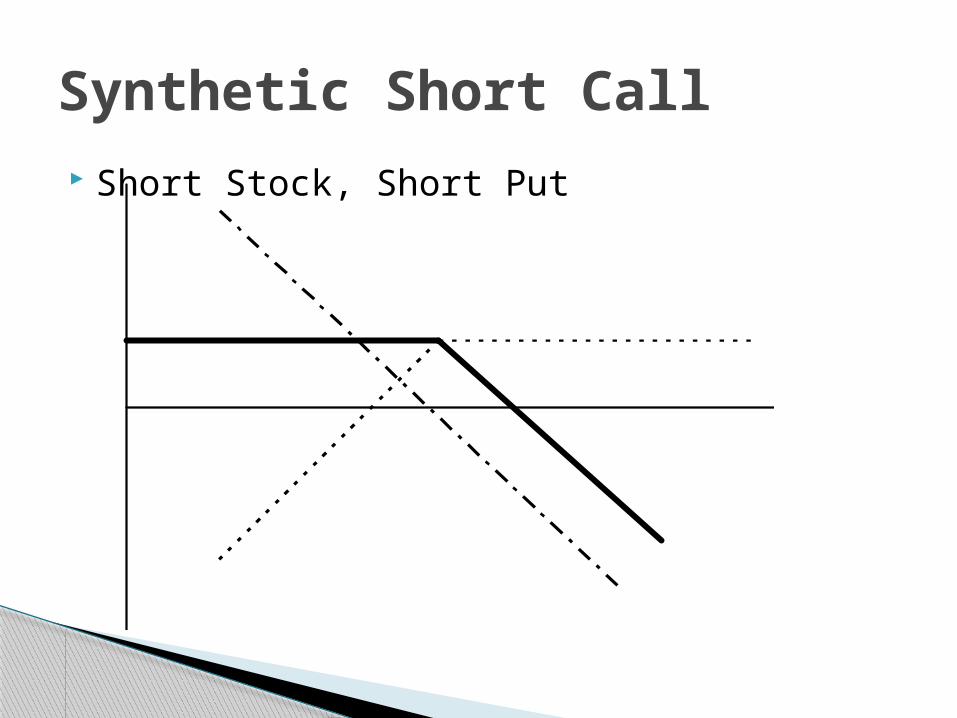

Synthetic Short Call Short Stock, Short Put

Synthetic Short Call Short Stock, Short Put

Synthetic Stock Short Put, Long Call

Synthetic Stock Short Put, Long Call

Synthetic Stock Short Put, Long Call

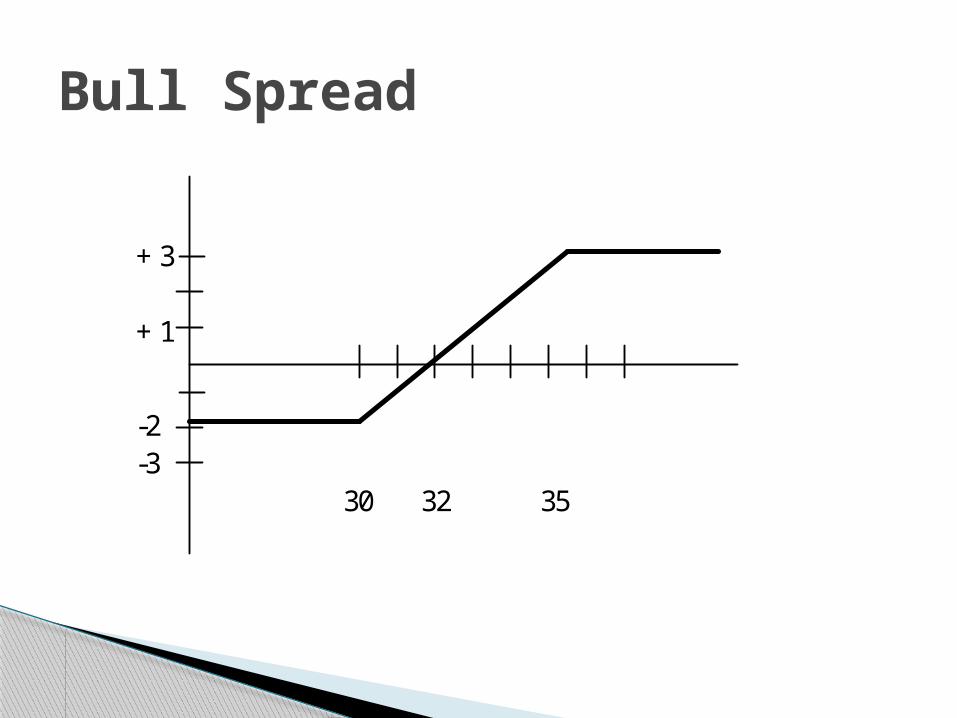

Bull Spread Long Call @ s1 s1 < s2 Short Call @ s2

Max Profit = s2 - s1 - c1 + c2 Break Even = s2 - MP = s1 - c2 + c1

Bull Spread

ExamplePrice = 32 Oct35C = 1 t=60days/365Oct30C = 3 v = .24

Buy Oct30C = -3Sell Oct35C = +1Max Profit = 35-30-3+1 = 3BE = 30-1+3 = 32Net Debit = -3 + 1 = -2

Bull Spread

+3

-2

+1

-330 32 35

Bull Spread

+3

-2

+1

-330 32 35

Bull Spread

+3

-2

+1

-330 32 35

Bull Spread

+3

-2

+1

-330 32 35

Bull Spread Profit / Loss Diagram Table

Bull Spread Compute probability of bull spread

Example

Vt = .24 (60/365).5 = .097

Prob (<32) = N[ln(32/32) /.097] = .5000Prob (>32) = 1 - .500 = .5000

Max Profit = $300Max Loss = -$200

• at 50% odds, makes good sense

Bull Spread

Aggressive Bull Spread s1 < P << s2 Good probability, good profit potential

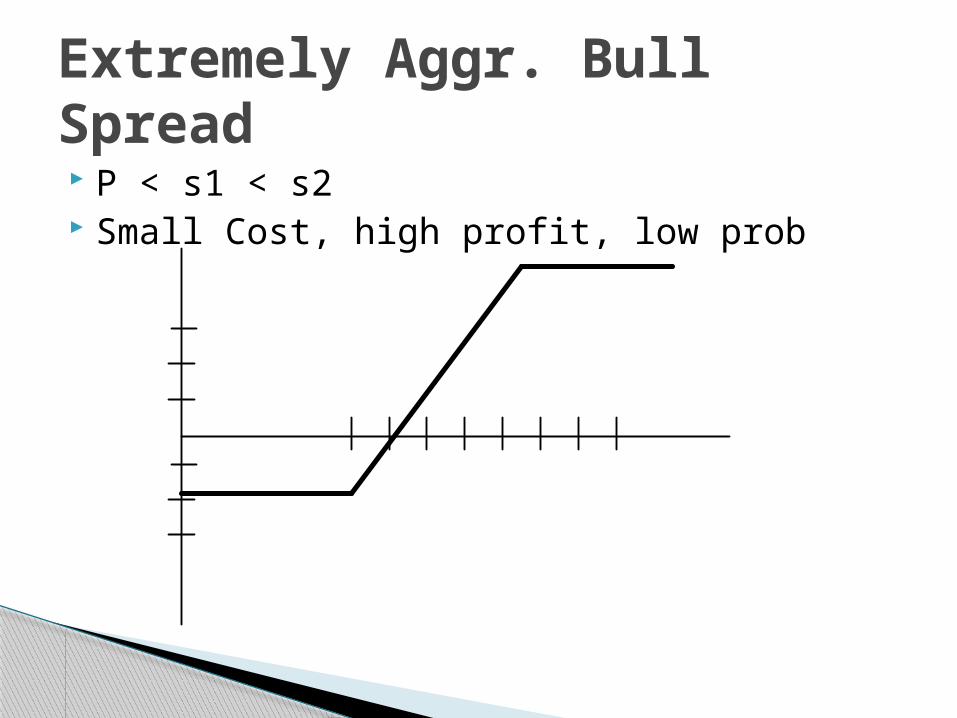

Extremely Aggr. Bull Spread P < s1 < s2 Small Cost, high profit, low prob

Least Aggr. Bull Spread S1 < s2 < P Low profit, high prob

Put Bull Spread

Long Put @ s1 s1 < s2Short put @ s2

example (Credit Spread)Price = 55Jan50P = 2Jan60P = 7

Net Credit = p2 - p1 = + 7 - 2 = + 5Break Even = S2 - credit = 60 - 5 = 55

Put Bull Spread+7

-2

+5

-550 55 60

Put Bull Spread+7

-2

+5

-550 55 60

Put Bull Spread+7

-2

+5

-550 55 60

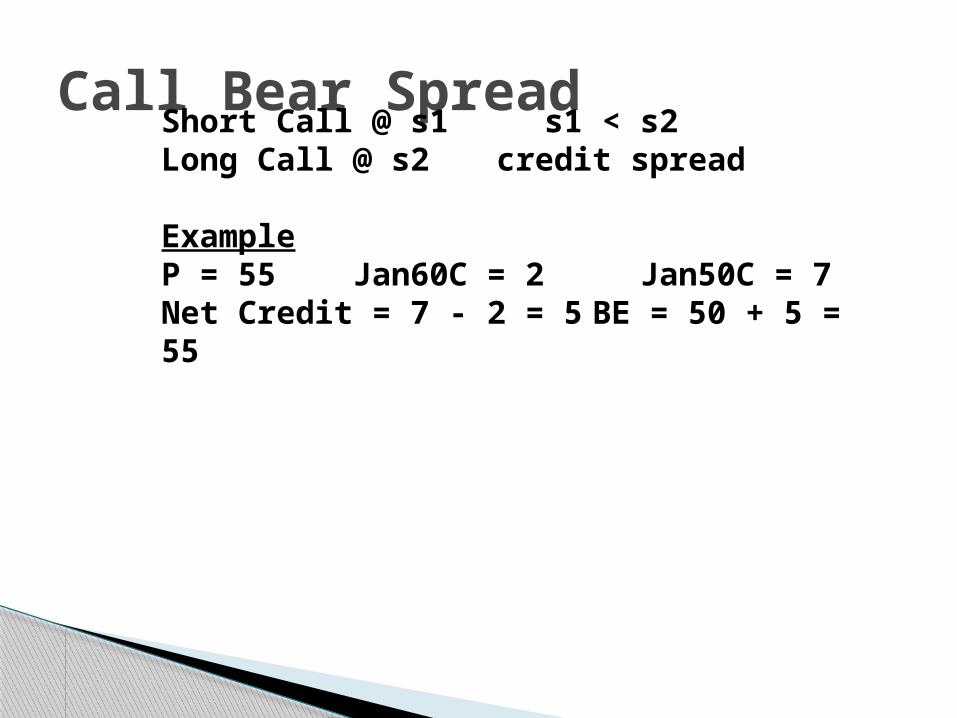

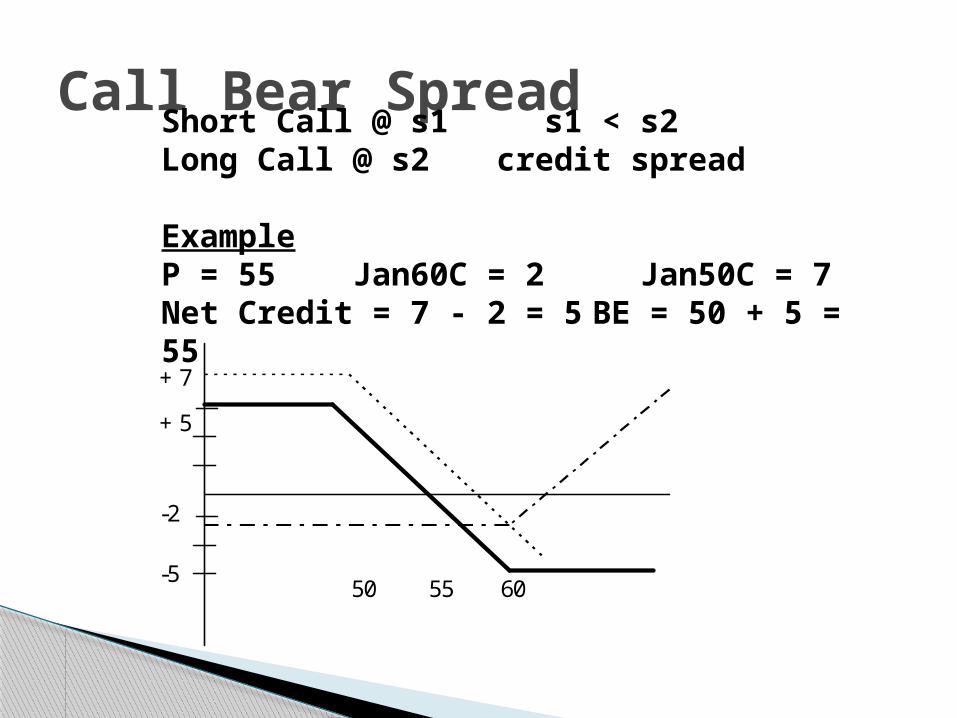

Call Bear SpreadShort Call @ s1 s1 < s2Long Call @ s2 credit spread

Call Bear SpreadShort Call @ s1 s1 < s2Long Call @ s2 credit spread

ExampleP = 55 Jan60C = 2 Jan50C = 7Net Credit = 7 - 2 = 5 BE = 50 + 5 = 55

Call Bear SpreadShort Call @ s1 s1 < s2Long Call @ s2 credit spread

ExampleP = 55 Jan60C = 2 Jan50C = 7Net Credit = 7 - 2 = 5 BE = 50 + 5 = 55

+7

-2

+5

-550 55 60

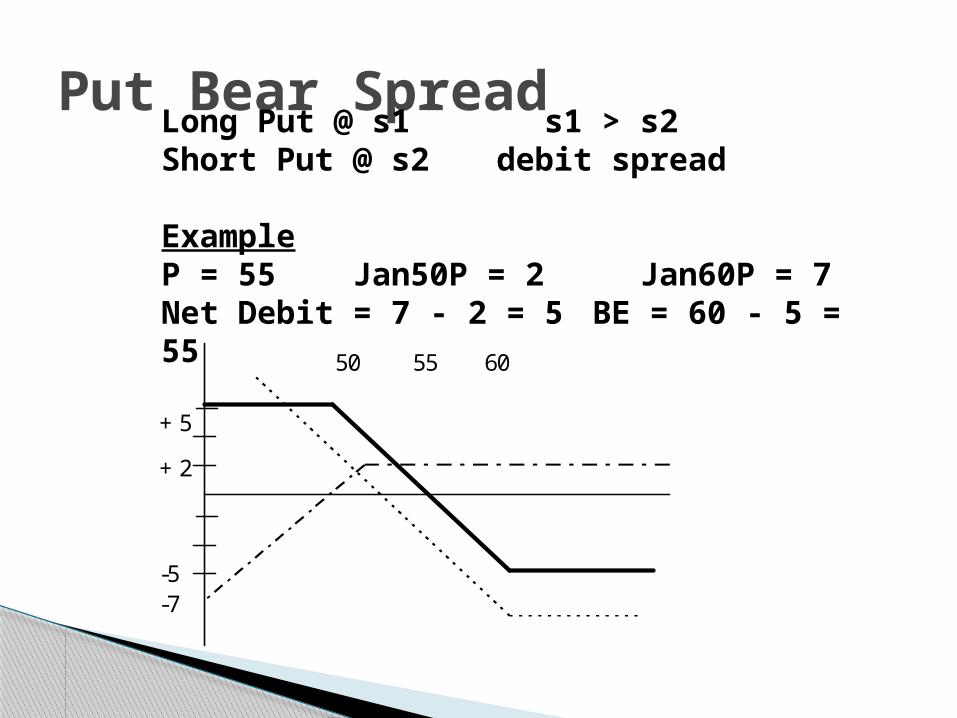

Put Bear SpreadLong Put @ s1 s1 > s2Short Put @ s2 debit spread

Put Bear SpreadLong Put @ s1 s1 > s2Short Put @ s2 debit spread

ExampleP = 55 Jan50P = 2 Jan60P = 7Net Debit = 7 - 2 = 5 BE = 60 - 5 = 55

Put Bear SpreadLong Put @ s1 s1 > s2Short Put @ s2 debit spread

ExampleP = 55 Jan50P = 2 Jan60P = 7Net Debit = 7 - 2 = 5 BE = 60 - 5 = 55

-7

+2

+5

-5

50 55 60

Call Bear vs. Put Bear +Credit spread- assignment risk? What causes assignment-Large Credit = P well above lower strike

Example: p = 59, Jan60C=1, Jan50C=9

+9

-1

50 60

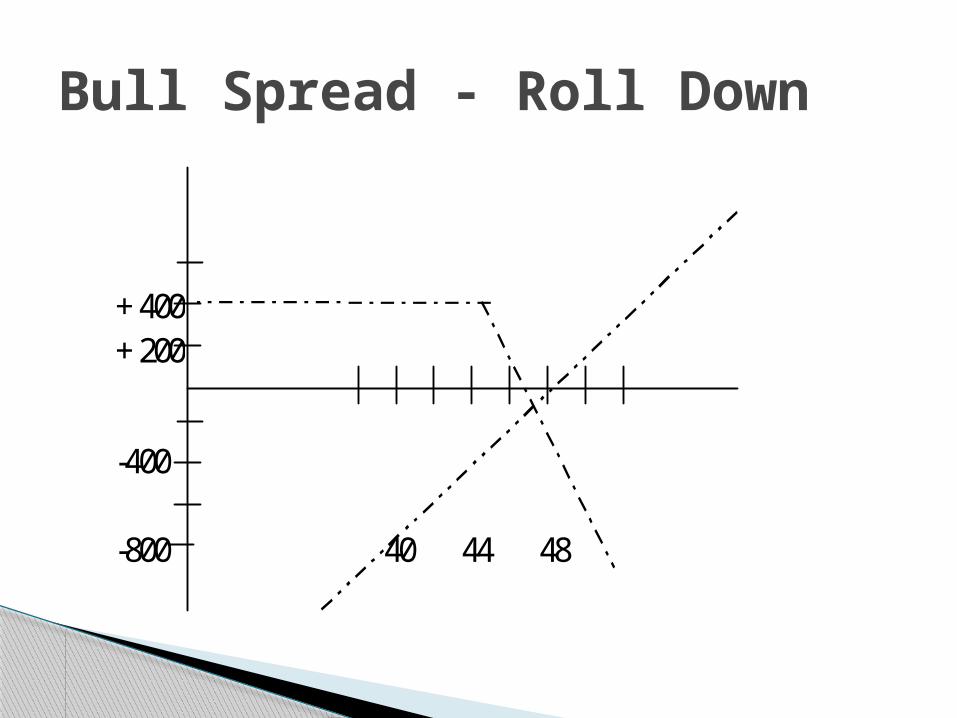

Bull Spread - Roll Down

Long Stock, Long Call, Short 2 Calls

ExampleOwn stock @ $48Price = 42Oct40Call = 4 (buy)Oct45Call = 2 (sell 2)Net Credit = 0BE = 44

Bull Spread - Roll Down

+400

-400

+200

-800 40 44 48

Bull Spread - Roll Down

+400

-400

+200

-800 40 44 48

+400

-400

+200

-800 40 44 48

Bull Spread - Roll Down

Bull Spread - Roll Down

+400

-400

+200

-800 40 44 48

Bull Spread - Roll Down

+400

-400

+200

-800 40 44 48

Bull Spread - Roll Down

Price P/LSt P/L Sh C P/L Lg C Net P/L35 -1300 +400 -400 -130038 -1000 +400 -400 -100040 -800 +400 -400 -80042 -600 +400 -200 -40044 -400 +400 0 045 -300 +400 +100 +20048 0 -200 +400 +20050 +200 -600 +600 +200

Synthetic Covered CallBull spread

If call is deep in the money and has no time to exp, a bull spread can be used to simulate a covered call.

ExamplePrice = 49Sell Apr50C = 3Buy Apr35C = 14

Synthetic Covered CallBull spread

+3

+11

35 46 50

+4

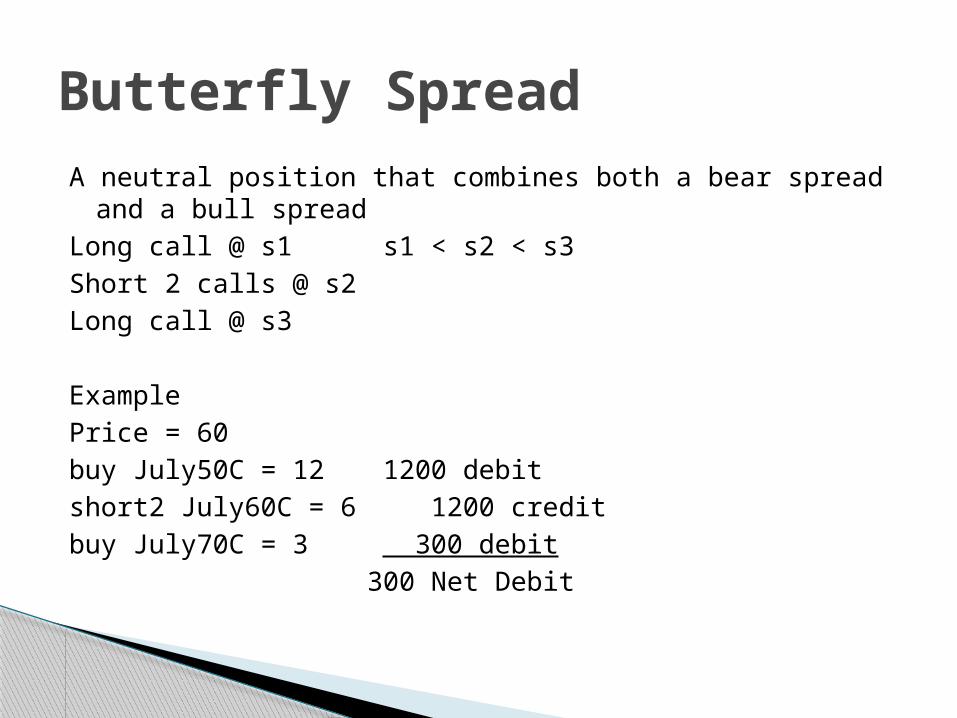

Butterfly SpreadA neutral position that combines both a bear spread and a

bull spreadLong call @ s1 s1 < s2 < s3Short 2 calls @ s2Long call @ s3

ExamplePrice = 60buy July50C = 12 1200 debitshort2 July60C = 6 1200 creditbuy July70C = 3 300 debit 300 Net Debit

Butterfly Spread

+12

+7

-1250 53 60 67 70

Butterfly Spread

+12

+7

-1250 53 60 67 70

Butterfly Spread

+12

+7

-1250 53 60 67 70

Butterfly Spread

+12

+7

-1250 53 60 67 70

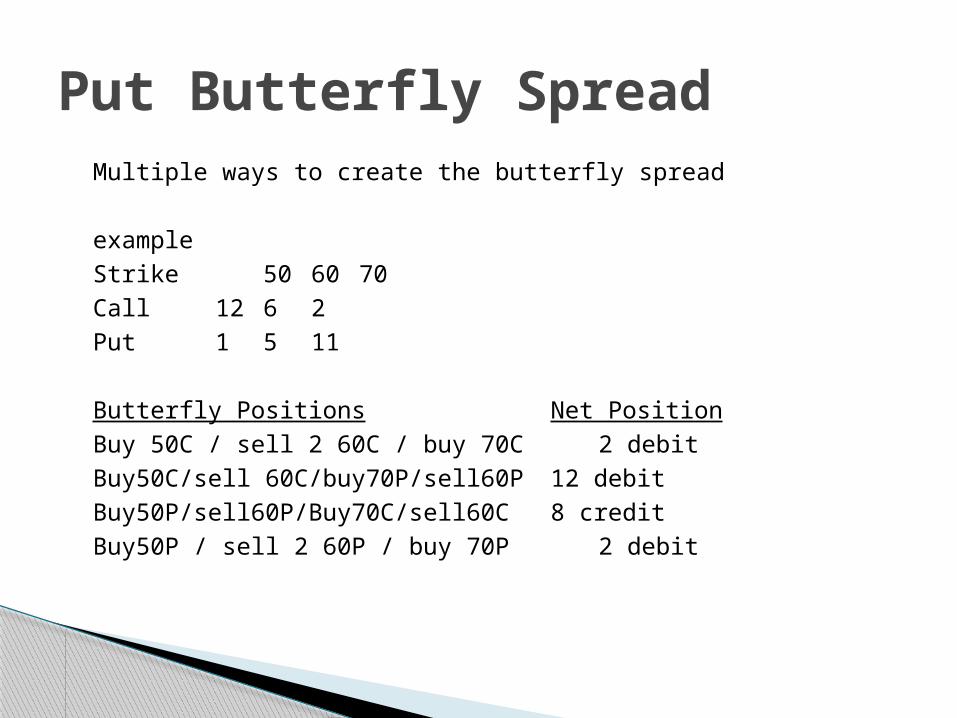

Put Butterfly SpreadMultiple ways to create the butterfly spread

exampleStrike 50 60 70Call 12 6 2Put 1 5 11

Butterfly Positions Net PositionBuy 50C / sell 2 60C / buy 70C 2 debitBuy50C/sell 60C/buy70P/sell60P 12 debitBuy50P/sell60P/Buy70C/sell60C 8 creditBuy50P / sell 2 60P / buy 70P 2 debit

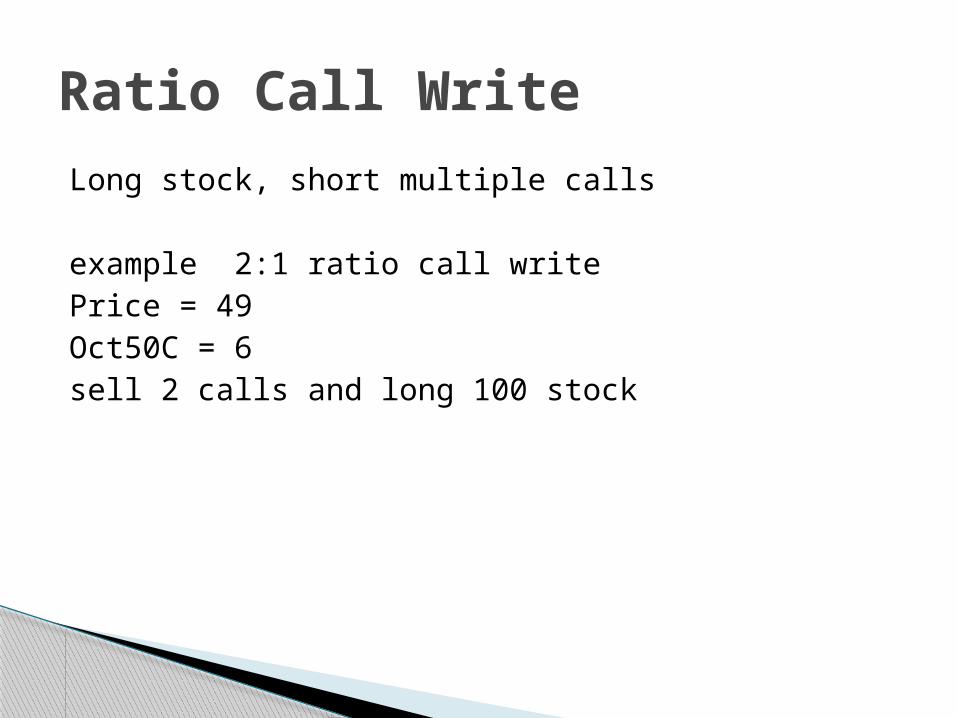

Ratio Call Write

Long stock, short multiple calls

example 2:1 ratio call writePrice = 49Oct50C = 6sell 2 calls and long 100 stock

Ratio Call Write

+13+12

-1237 49 50 63

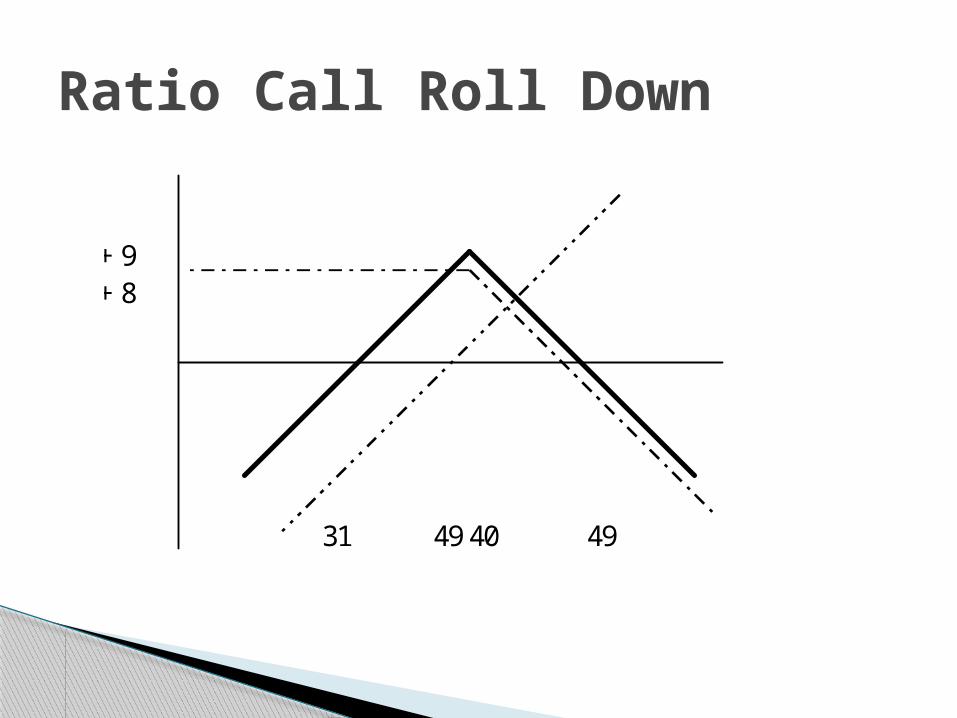

Ratio Call Roll Downexample 2:1 ratio call writePrice = 49Oct50C = 6sell 2 calls and long 100 stock

Price drops to 40Oct50C = 1Oct40C = 4Buy 2 Oct50C = profit = 12 - 2 = 10Sell 2 Oct40C

apply to stock price & pretend we own stock at $39

Ratio Call Roll Down

+9+8

31 49 40 49

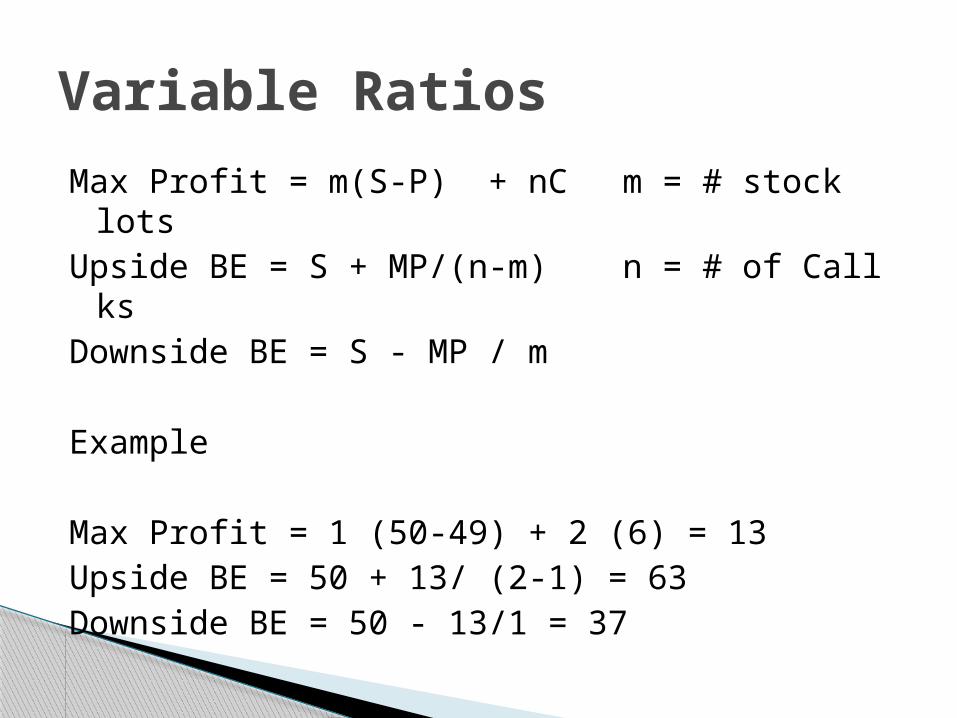

Variable Ratios

Max Profit = m(S-P) + nC m = # stock lots

Upside BE = S + MP/(n-m) n = # of Call ks

Downside BE = S - MP / m

Example

Max Profit = 1 (50-49) + 2 (6) = 13Upside BE = 50 + 13/ (2-1) = 63Downside BE = 50 - 13/1 = 37

Ratio Call Write

Example 3:1Buy 1 lot stock @ 49sell 3 oct50c@18Max Profit = 1 (50-49) + 3 (6) = 19Upside BE = 50 + 19/ (3-1) = 59.5Downside BE = 50 - 19/1 = 31

+13+12

-1237 49 50 63

Ratio Call Write

Example 3:1Buy 1 lot stock @ 49sell 3 oct50c@18Max Profit = 1 (50-49) + 3 (6) = 19Upside BE = 50 + 19/ (3-1) = 59.5Downside BE = 50 - 19/1 = 31

+19+18

-12 31 49 50 59.5

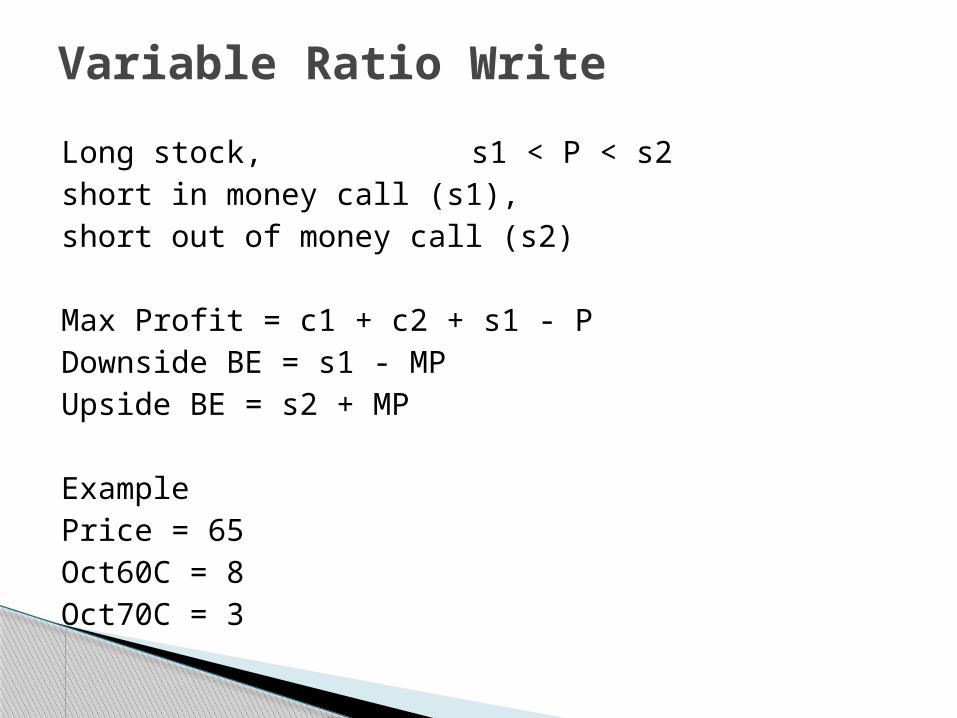

Variable Ratio Write

Long stock, s1 < P < s2short in money call (s1), short out of money call (s2)

Max Profit = c1 + c2 + s1 - PDownside BE = s1 - MPUpside BE = s2 + MP

ExamplePrice = 65Oct60C = 8Oct70C = 3

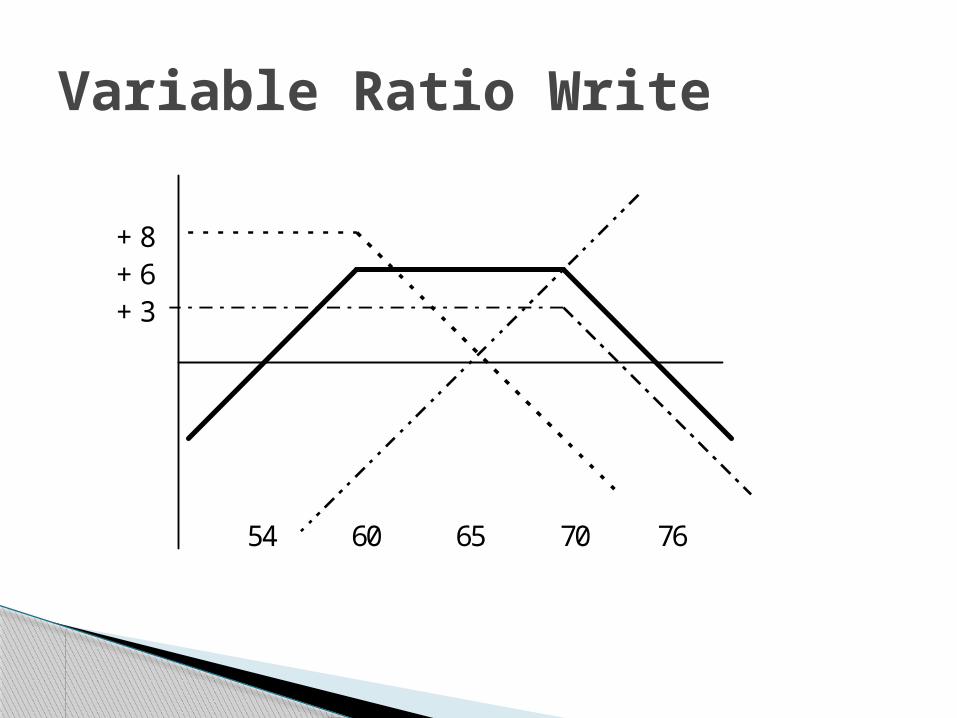

Variable Ratio Write

+8

+3

54 60 65 70 76

+6

Variable Ratio Write

+8

+3

54 60 65 70 76

+6

Variable Ratio Write

+8

+3

54 60 65 70 76

+6

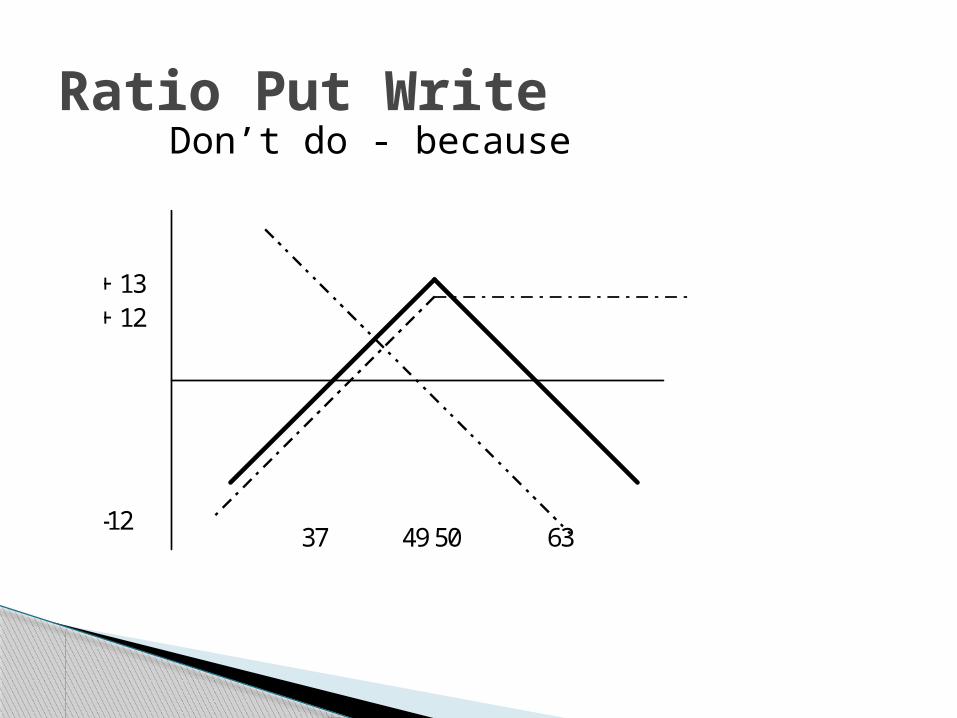

Ratio Put Write

+13+12

-1237 49 50 63

Don’t do - because

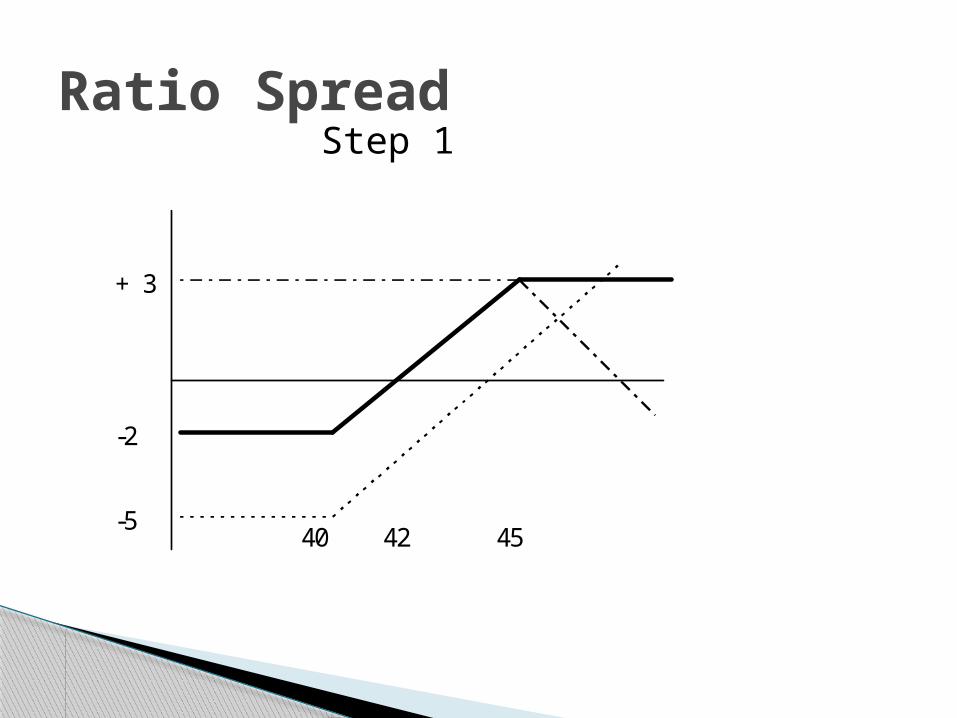

Ratio Spread

Long call @ s1 s1 < s2Short X calls @ s2

Example 2:1Price = 44Apr40C = 5 buy 1Apr45C = 3 sell 2

BE = 51MP = 6

Ratio Spread

+ 3

-2

-540 42 45

Step 1

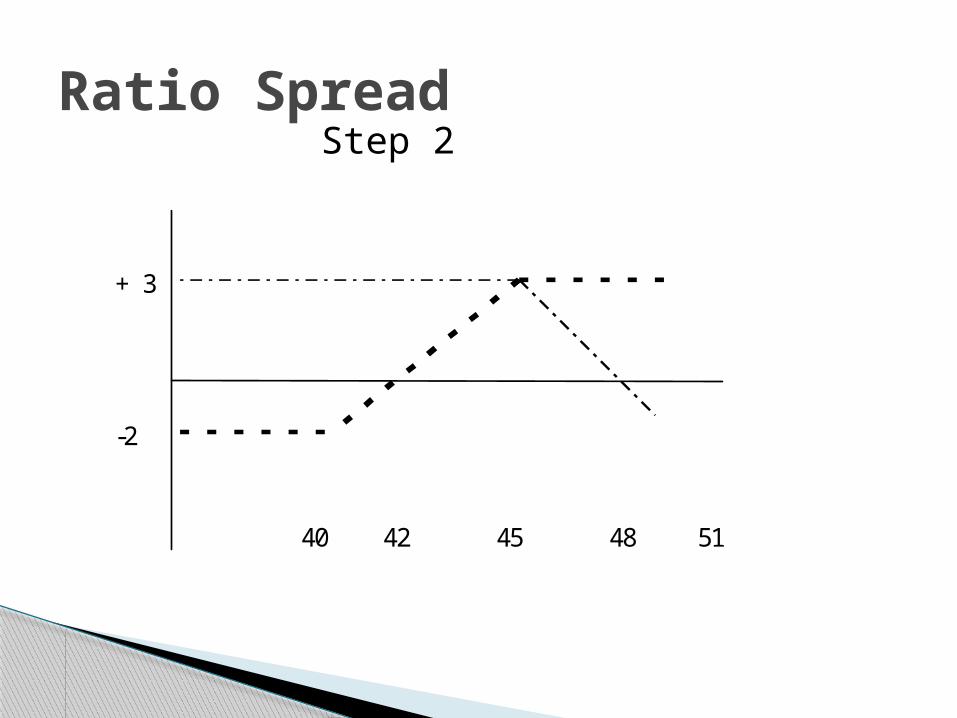

Ratio Spread

+ 3

-2

-540 42 45 48 51

Step 2

Ratio Spread

+ 3

-2

40 42 45 48 51

Step 2

Ratio Spread

+ 3

-2

+6

40 42 45 48 51

+1

Step 2

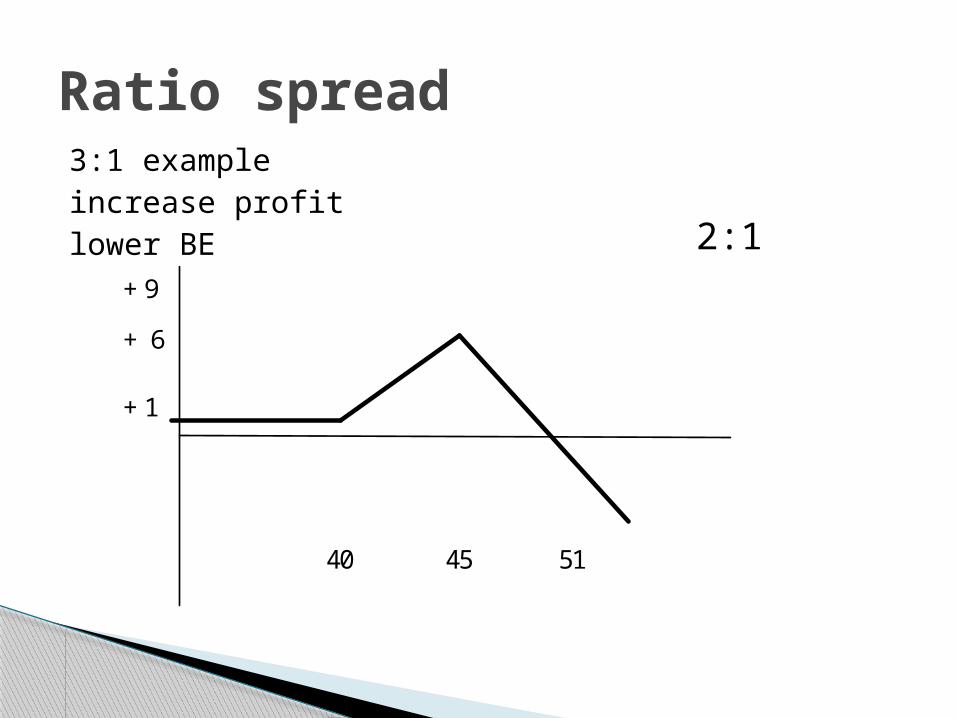

Ratio spread3:1 exampleincrease profitlower BE 2:1

+ 6

+9

40 45 51

+1

Ratio spread3:1 exampleincrease profitlower BE

+ 6

+9

40 45 49.5

+4

3:1

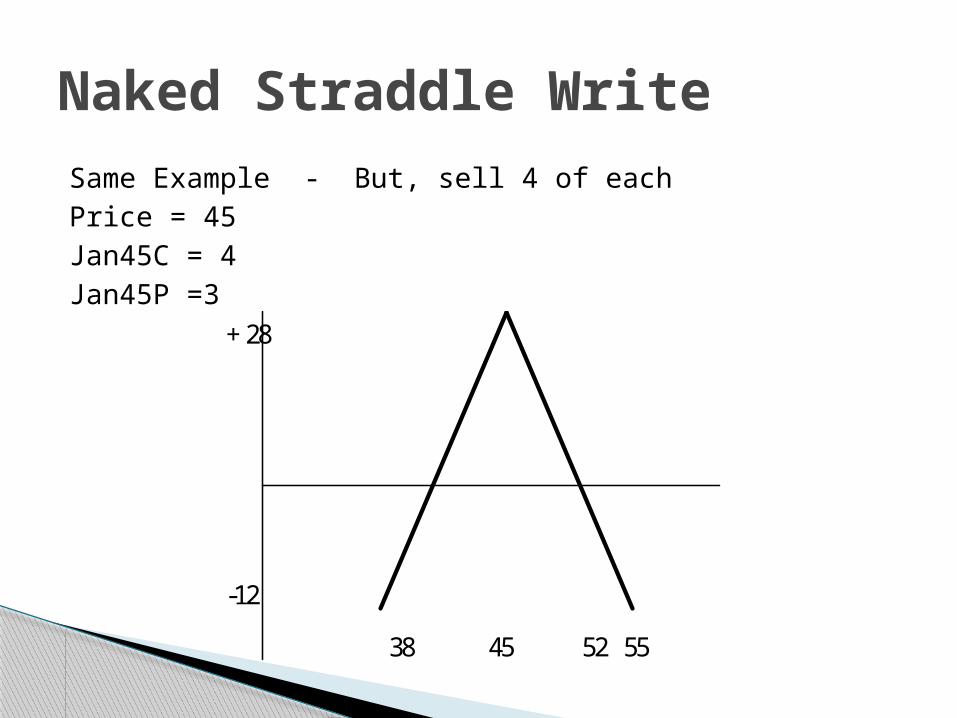

Naked Straddle WriteShort PutShort Call

ExamplePrice = 45Jan45C = 4Jan45P =3

+7

+4+3

38 45 52 55

-3

Naked Straddle WriteSame Example - But, sell 4 of eachPrice = 45Jan45C = 4Jan45P =3

+28

-12

38 45 52 55

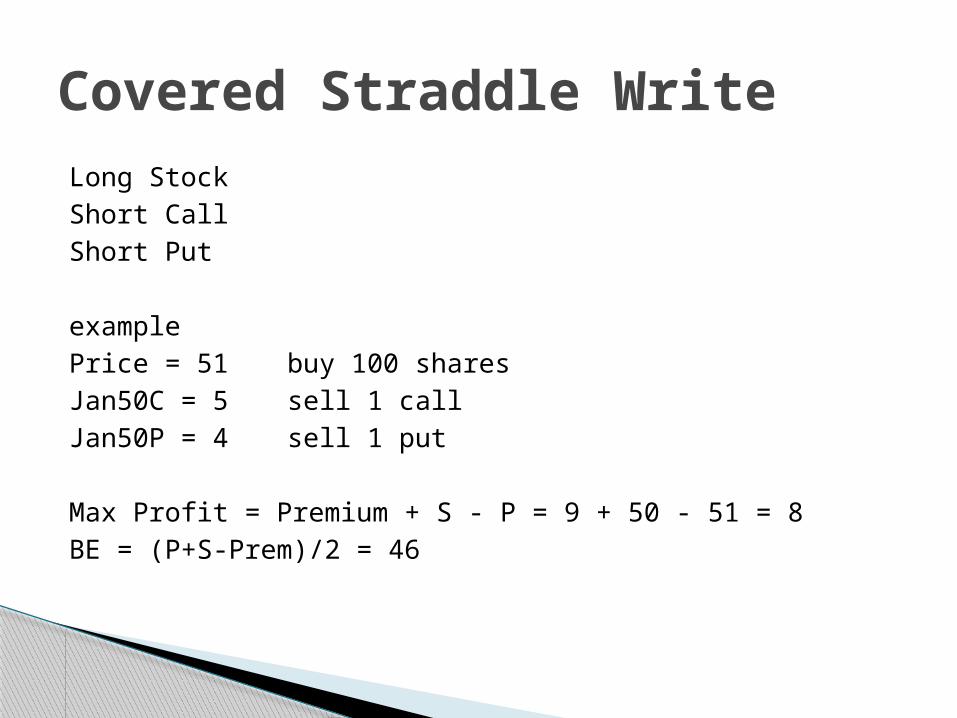

Covered Straddle WriteLong StockShort CallShort Put

examplePrice = 51 buy 100 sharesJan50C = 5 sell 1 callJan50P = 4 sell 1 put

Max Profit = Premium + S - P = 9 + 50 - 51 = 8BE = (P+S-Prem)/2 = 46

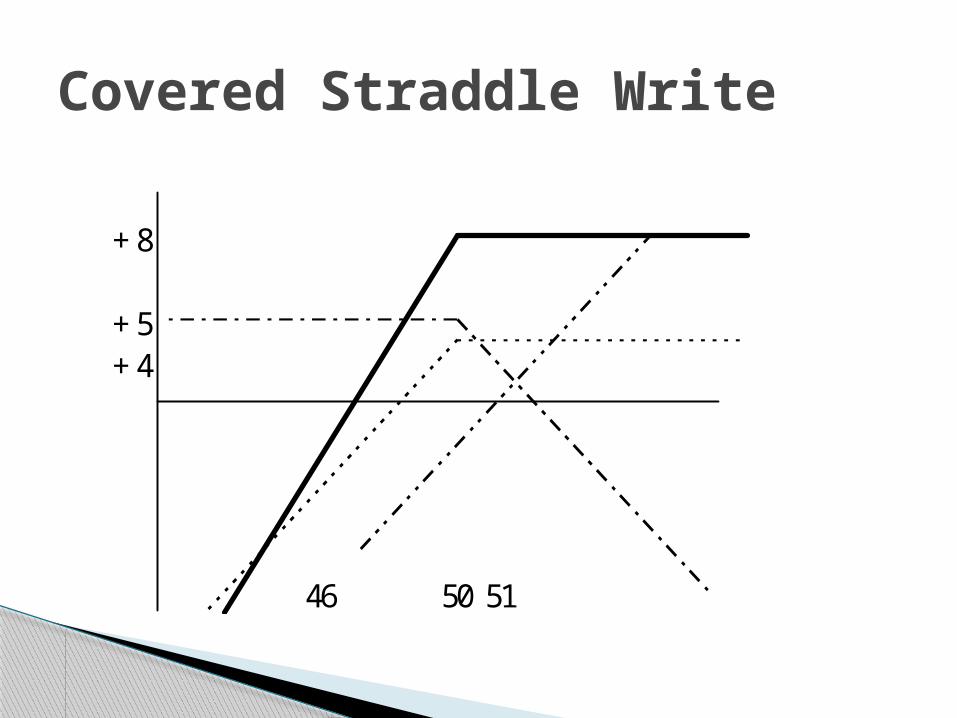

Covered Straddle Write

+8

+5+4

46 50 51

Covered Straddle vs Covered call

+8

+4

46 50 51

Combination Writeor Strangle Write

Short put (out of money)Short call (out of money)

exampleprice = 65Jan70C = 4Jan60P = 3Downside BE = Sp - put - call = 60-3-4 = 53Upside BE = Sc + put + call = 70+3+4 = 77Max Profit = put + call = 3+4 = 7

Combination Writeor Strangle Write

+7

+3

53 60 65 70 77

+4

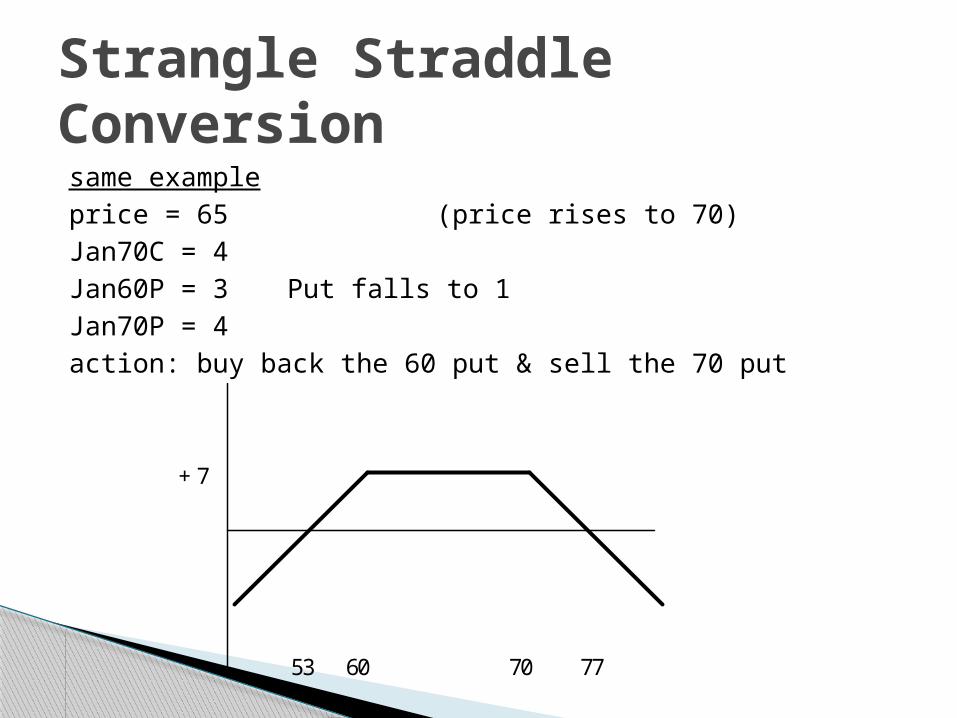

Strangle Straddle Conversionsame exampleprice = 65 (price rises to 70)Jan70C = 4Jan60P = 3 Put falls to 1Jan70P = 4action: buy back the 60 put & sell the 70 put

+7

53 60 70 77

Strangle Straddle Conversion

+7

53 60 70 77

-1

Strangle Straddle Conversion

+7

53 60 70 77

-1

+4

Strangle Straddle Conversion

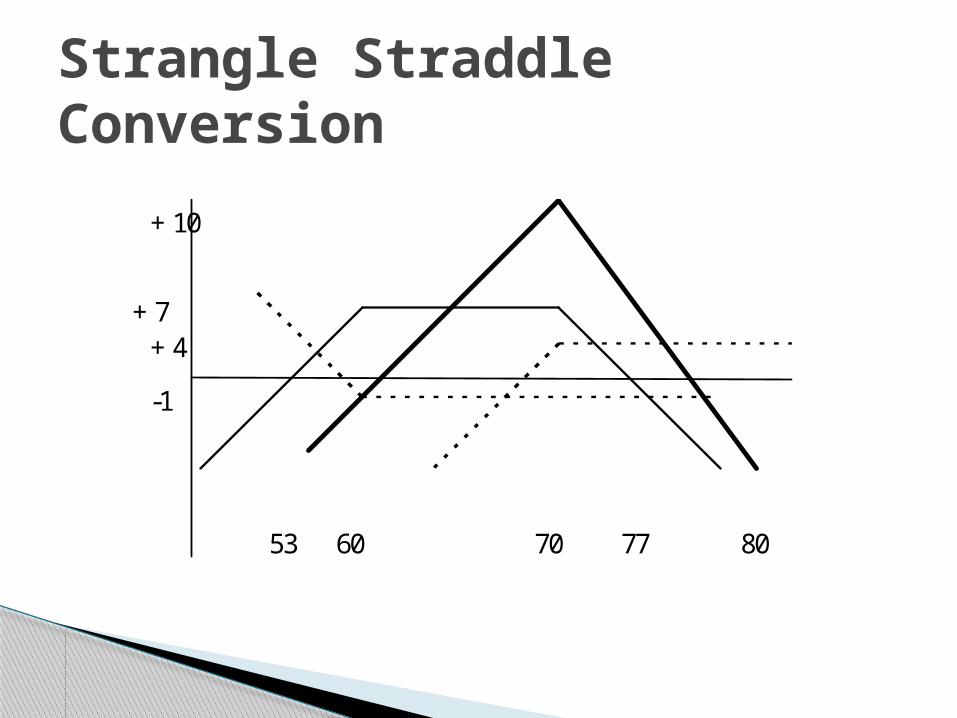

+7

53 60 70 77 80

-1

+4

+10

Splitting The Strikes& Synthetic StocksShort out of money putLong out of money call

example (Bullish Strike Split)price = 53Jan50P = 2Jan60C = 1

BE = 48

Bullish Strike Split

+2

50 60

-1+1

Bearish Strike Split

+2

50 60

-1+1

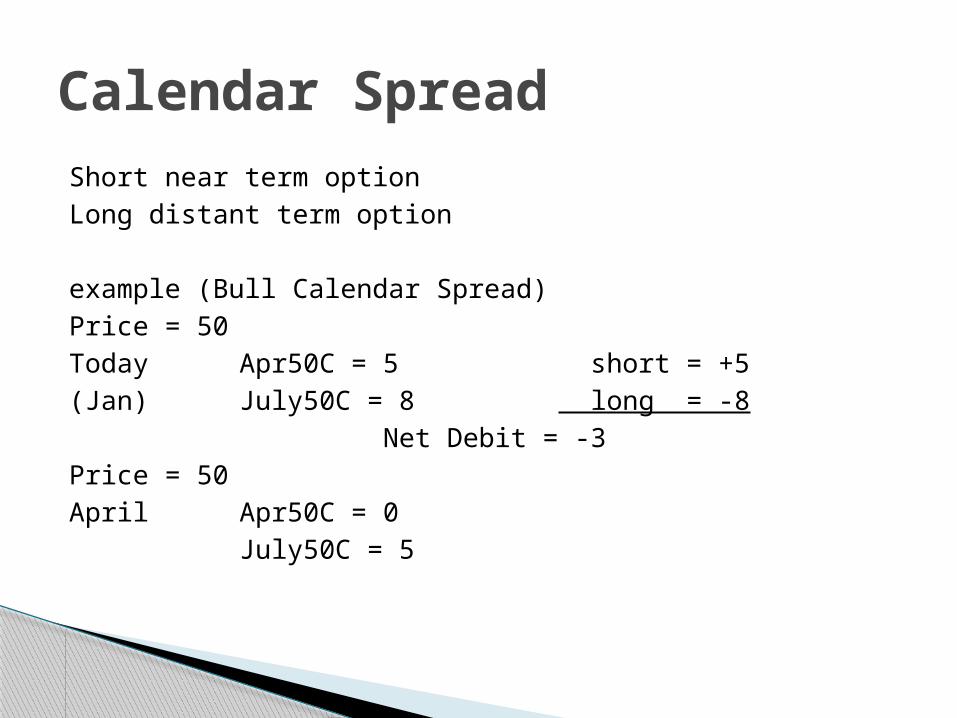

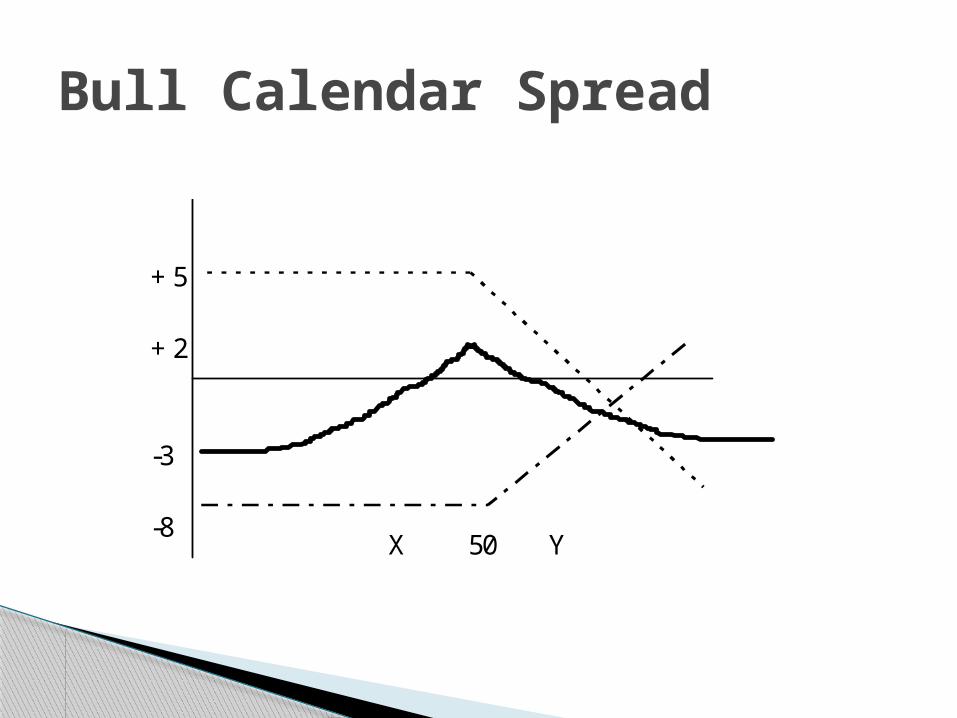

Calendar SpreadShort near term optionLong distant term option

example (Bull Calendar Spread)Price = 50Today Apr50C = 5 short = +5(Jan) July50C = 8 long = -8 Net Debit = -3Price = 50April Apr50C = 0 July50C = 5

Bull Calendar Spread

+2

X 50 Y

-3

+5

-8

Bull Calendar Spread

+2

X 50 Y

-3

+5

-8

Price Apr50C/PL July50C/PL Net Profit40 0/+500 .5/-750-25045 0/+500 2.5/-550 -5048 0/+500 4/-400 +10050 0/+500 5/-300 +20052 2/+300 6/-200 +10055 5/0 8/0 060 10/-500 10.5/+250 +250

Bull Calendar SpreadApril Profit/Loss Table

Put Calendar Spread(Bearish)Same as callshort near term & long distant termex - price = 50, Jan50P = 2, Apr50P = 3

+1

X 50 Y

-1

+2

-3

Reverse SpreadOpposite of all other common positions

Example (Reverse ratio - backspread) 2:1Short call @ s1 s1<s2Long x calls @ s2

Price = 43July40C = 4July45C = 1

Step 1

+ 3

-2

+4

40 43 45 48

-1

Reverse Ratio Backspread

Reverse Ratio Backspread

+ 3

-2

+2

40 43 45 48

-1

-3

Reverse Butterfly

+12

+7

-1250 53 60 67 70

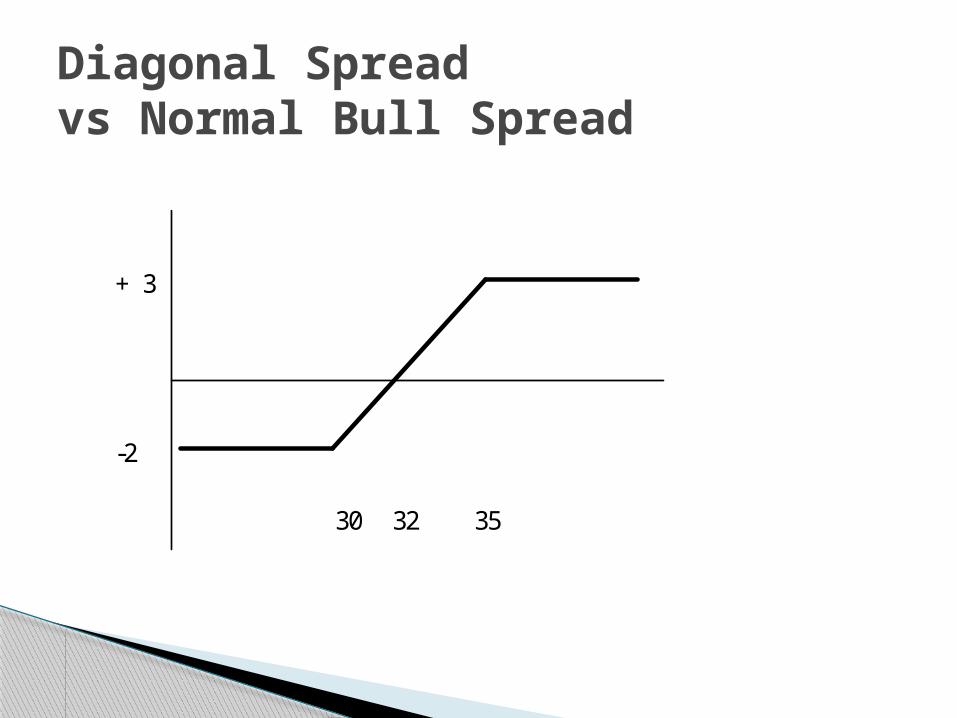

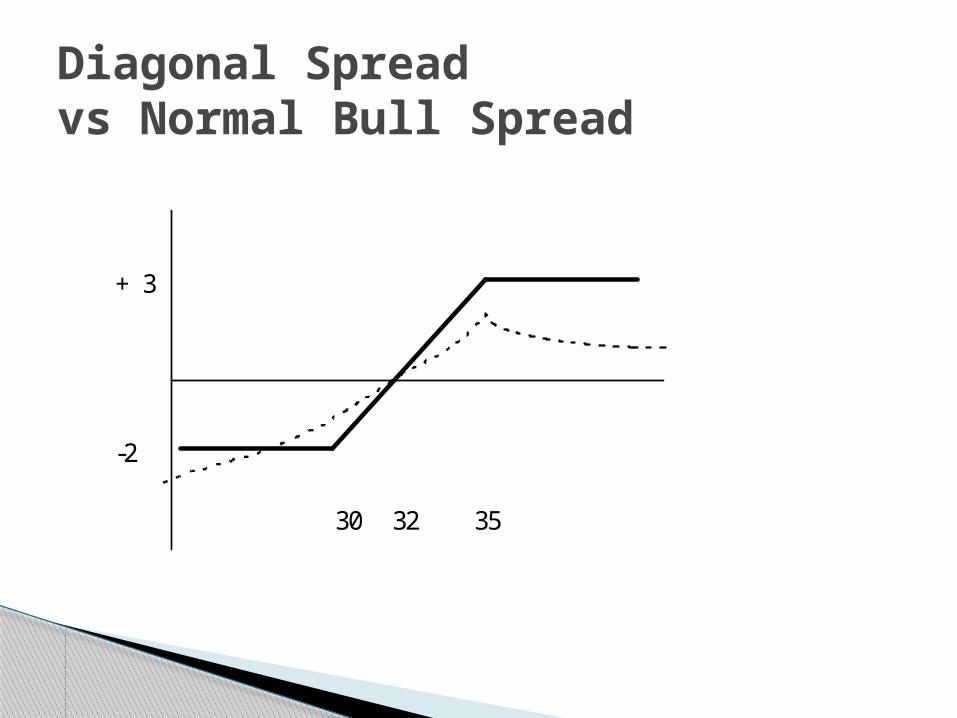

Diagonal Spreaddiff strikes & diff exp

example (Diagonal Bull Spread)Price = 32Apr30C = 3Apr35C = 1July30C = 4 Long July30CJuly35C = 1.5 Short Apr35C

Normal Bull Spread - Long Apr30C Short Apr35C

Diagonal Spreadvs Normal Bull Spread

+ 3

-2

30 32 35

Diagonal Spreadvs Normal Bull Spread

+ 3

-2

30 32 35

Related Documents