Lecture 3: Business Values Discounted Cash flow, Section 1.3 © 2004, Lutz Kruschwitz and Andreas Löffler

Lecture 3: Business Values Discounted Cash flow, Section 1.3 © 2004, Lutz Kruschwitz and Andreas Löffler.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lecture 3: Business Values

Discounted Cash flow, Section 1.3

© 2004, Lutz Kruschwitz and Andreas Löffler

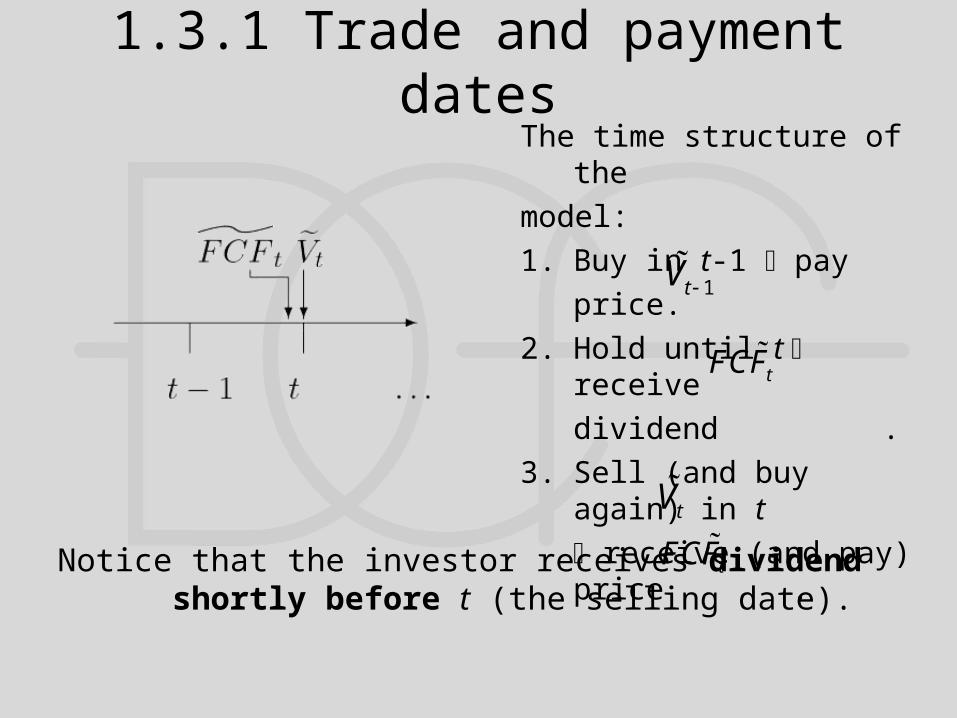

1.3.1 Trade and payment datesThe time structure of the

model:

1. Buy in t-1 pay

price.

2. Hold until t receive

dividend .

3. Sell (and buy again) in t

receive (and pay) price .

1tV

tV

Notice that the investor receives dividend shortly before t (the selling date).

tFCF

tFCF

1.3.1 A riskless worldWhat should happen if the future where certain?

In a certain world that is free of arbitrage wemust have

Otherwise, if for example

take loan, buy share in t, wait until t+1, get dividend and sell share

get infinitely rich without any cost.

1 1 .1t t

tf

FCF VV

r

1 1 (1 )t t f tFCF V r V

1.3.1 A risky world

In a risky world we have

What is absence of arbitrage now?

1

110 up,

90 down.tFCF

1 1

1t t

tf

E FCF VV

r

The account of the largest takeover in Wall Street history...

1.3.1 Three roads lead to Rome

Certainty equivalent

Risk-neutral probabilities

Risk premium

certainty equivalent

1 1 risk adjust n

1

me tt t t

tf

E FCF VV

r

F

1.3.1 Three roads lead to Rome

Certainty equivalent

Risk premium

Risk-neutral probabilities

1 1

cost of capital

risk pr1 emiumt t t

tf

E FCF VV

r

F

1.3.1 Three roads lead to Rome

Certainty equivalent

Risk premium

Risk-neutral probabilities

1 1

1t t t

tf

QE FCF VV

r

F

1.3.1 Roads to Rome: example

We are going to illustrate the three roads by using the following example:

And rf = 0.05. Because the cash flows have expectation

The value V0 will be less than

0.5 110 0.5 90 100,

10095.24.

1.05

1.3.1 Certainty Equivalent

If we assume a utility function

Then the «certainty equivalent» (CEQ)

and hence the price of the asset is given

by

( )u x x

0

0.5 110 0.5 90

99.75

99.7595.

1 1.05f

CEQ

CEQ

CEQV

r

Daniel Bernoulli, founder of

utility theory

1.3.1 Risk Premium

Valuation with a «risk premium» uses another idea: we modify

the denominator

Using the numbers of the example we get

0

0

1000.00263

1 0.05100

95.1 0.05 0.00263

V zz

V

1 1

0 .1 f

E FCF VV

r z

1.3.1 Risk-neutral ProbabilitesWith «risk-neutral probabilities» the probabilities pu=0.5 and

pd=0.5 are modified. The question is: find qu and qd such that

Holds.

Answer:

We turn to this approach in more detail!

! 1 1

0 1

Q

f

E FCF VV

r

110 9095

1 0.05

110 1 9095

1 0.050.4875, 0.5125.

u d

u u

u d

q q

q q

q q

1.3.2 Cost of capital

Cost of capital is

definitely a key concept.

But: how is it precisely

defined?

1.3.2 Cost of capital – alternative definitions

There are several alternative definitions of cost of capital in a multi-period context:

• cost of capital =Def «Yields»• cost of capital =Def «Discount rates»• cost of capital =Def «Expected returns»• cost of capital =Def «Opportunity costs»

Are all definitions identical? We will show later: not necessarily!

1.3.2 Cost of capital is an expected return

Which definition is useful for our purpose? The following

definition turns out to be appropriate

Definition 1.1 (cost of capital): The cost of capital of a

firm is the conditional expected return

1 11.

t t t

tt

E FCF Vk

V

F

1.3.2 Shortcoming of definition

This appropriate definition has a

disadvantage: kt could be uncertain.

And you cannot discount with

uncertain cost of capital!

Another (big) assumption is necessary: from now on this cost of capital should be certain.

1.3.2 Alternative definitions?

Other attempts to simplify definition 1.1 fail to produce

reasonable results: aim is to have

as well as for t=1

with the same cost of capital in the denominator!

1

1 2

00 0

...1 (1 )(1 )

E FCF E FCFV

k k k

2 1 3 1

21 11 ...

1 (1 )(1 )

E FCF E FCFV

kk k

F F

1k

1.3.3 Market value

Theorem 1.1 (market value): When cost of capital is

deterministic, then

Notice that the lefthand side and the righthand side as well

can be uncertain for t>0.

1 1

.(1 )...(1 )

Ts t

ts t t s

E FCFV

k k

F

1.3.3 Proof of Theorem 1.1

Start with a reformulation of Definition 1.1,

Now use the similar relation for and plug in,

1 1.

1t t t

tt

E FCF VV

k

F

2 2 1

11 1

.1

t t t

t t

tt

t

E FCF

V

E FCF V

k

k

F

F

1tV

1.3.3 Proof (continued)

Costs of capital are deterministic, use rule 2 (linearity)

Rule 4 (iterated expectation) gives

2 1 2 11

1 1

.1 1 1 1 1

t t t t t tt t

tt t t t t

E E FCF E E VE FCFV

k k k k k

F F F FF

1 2 1 2 1

1 1

.1 1 1 1 1

t t t t t t

tt t t t t

E FCF E FCF E VV

k k k k k

F F F

1.3.3 Proof (continued)

Continue until T to get

Last term vanishes by transversality. QED

1 2

1

1 1

...1 1 1

.1 1 1 1

t t t t

tt t t

T t T t

t T t T

E FCF E FCFV

k k k

E FCF E V

k k k k

F F

F F

1.3.4 Fundamental Theorem

Let us turn back to risk-neutral probability Q: does Q always

exist?

This is not a trivial question: the numbers qu and qd must be

between 0 and 1! For example, would not be

considered as «probabilities».

Theorem 1.2 (Fundamental Theorem): If the markets are free of arbitrage, there is a probability Q such that for all claims

1 1.

1Q t t t

tf

E FCF VV

r

F

, 2,1u dq q

1.3.4 Fundamental theorem

What about a proof? Forget it.1

How to get Q for valuation of firms? No idea.

So why is this helpful? We will see (much) later.

Is there at least an interpretation of Q? Yes!

1If you cannot resist: see further literature

1.3.4 Risk-neutrality of Q

Why do we call Q a risk-neutral probability?

Look at the following:

1 1

1 1

1 1

1 1

1 fundamental theorem

1 rule 5

1 rule 3

1 rule 2.

Q t t t

ft

t tf Q t

t

t tf Q t Q t

t

t tf Q t

t

E FCF Vr

V

FCF Vr E

V

FCF Vr E E

V

FCF Vr E

V

F

F

F F

F

return on holding a share

1.3.4 Intuition of Q

The last equation

simply says: if we change our probabilites to Q, any security

has expected return rf.

Or: the world is risk-neutral under Q .

returnf Q tr E F

1.3.4 Uniqueness of Q

Is Q unique? Or can the value of the company depend on Q?

If the cash flows of the firm can be duplicated by traded assets

(market is complete) then any Q will lead to the same value.

Proof: Forget this as well...

1.3.4 Two assumptions

From now on two assumptions will always hold:

Assumption 1.1: The markets are free of arbitrage.

Assumption 1.2: The cash flows of the firm can be duplicated

by traded assets.

The risk-neutral probability Q exists and is (in some sense)

unique.

Summary

Costs of capital are conditional expected returns.

Costs of capital must be deterministic.

If markets are arbitrage free a «risk-neutral probability

measure» Q exists.

When using this probability Q the world is risk-neutral.

Related Documents