Lecture 10 MGMT 7730 - © 2011 Houman Younessi An important part of managing a business is to ensure that it is at all times under control. What does this mean? This means that as much as possible all risks to the business are identified and managed. But what is risk? Risk has to do with the unknown. Uncertainty breeds risk. When we are uncertain of the course and outcome of an event of importance, we are facing risk. Risk and Risk Analysis

Lecture 10 MGMT 7730 - © 2011 Houman Younessi An important part of managing a business is to ensure that it is at all times under control. What does this.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

An important part of managing a business is to ensure that it is at all times under control.

What does this mean?

This means that as much as possible all risks to the business are identified and managed.

But what is risk?

Risk has to do with the unknown. Uncertainty breeds risk.

When we are uncertain of the course and outcome of an event of importance, we are facing risk.

Risk and Risk Analysis

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Given that there are many unknowns in business, the entire management process may be perceived as one of handling risk, that is:

Management is reducing risk as we go forward in business

So when we find out about user needs and qualify them; when we design a product; when we test a market, when we set a price etc. we are managing risk

It is fair to state however that most if not all of business is focused on managing one type of risk: RISK TO UTILITY

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

We distinguish risks from other potential events by observing if:

What we don’t know about the event or process yet might have a negative impact. This is called RISK IDENTIFICATION.

We also need to consider:

The likelihood of this event occurring with the undesirable outcome. This is RISK ANALYSIS.

And

The degree to which we can influence the outcome. This is RISK CONTROL.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Risks can be of two general categories:

Common risk; e.g. the economy would take a down turn

Business specific risk; e.g. our chief scientist would resign

As much as we can, we need to attempt to safeguard against both types of risk.

In this discussion we will primarily deal with risks to business.

Business risks can be:

General risk;e.g. customer would disagree with X

Technical risk;e.g. this design would be unreliable

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

A complete process of risk identification does not end when we have completed the:

Identification of a particular project risk.

It continues through:

Definition of risk attributes or characteristics

Documentation and communication of the risk

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Decision Analysis:Every decision we take with respect to the business, is a potential source of risk. If there is certainty, there is no decision. If there is decision to be made, there is uncertainty. Where there is uncertainty, there is potential for risk.

Decision analysis is a technique in which we identify and question every decision we have to take regarding a project as a basis for identification of potential risk.

Examination of Assumptions:A related and similar technique to the one just described, this technique is based on the principal that if we have to make an assumption, we lack certainty. If we lack certainty, there is potential for risk.

The technique requires the identification and examination of every assumption made about the issue at hand or any individual aspect of it as a basis for identification of possible risk.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Definition of risk attributes or characteristics

Once we have identified our potential risks, we must evaluate them and define each clearly in terms of its attributes or characteristics. The three important risk attributes or characteristics are:

Probability: May be defined as a probability figure or on an ordinal scale.

Consequences: If a potential risk does not have a negative consequence, it is not a risk. We can again rank the severity of the consequence of the risk on an ordinal scale.

Timeframe: The amount of time we have to deal with this risk.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Risk Analysis:Once our risks are identified, documented and communicated, they must be analyzed. By doing so we can prioritize risks and concentrate on the more critical ones. The activities involved are:

Identify source of each risk

Identify risk drivers

Estimate risk exposure

Prioritize and rank

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Identify Source of each riskHere we attempt to identify why a risk would appear. We need to identify the “real” reason, the root-cause.

If we want to find out why? We must ask why?

Ask why, wait for the answer and ask why again, several times until a sufficient root-cause is identified.

Identify risk drivers

Risk drivers are those attributes or elements (variables) that significantly impact the probability, consequence or timeframe of a risk. They are both process and product attributes or elements and may impact product quality, project cost, project time and schedule, customer relationship and a whole host of other issues

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Estimate risk exposure

Risk exposure is closely related to the probability of unsatisfactory outcome of an event P(u), and the value of loss sustained should this event occur L(u).

)()( uLuPRE

In this sense the probability is a number between 0 and 1, where 0 indicates impossibility of outcome and 1 indicates certainty. L(u) is usually in terms of units of currency.

Calculating risk exposure allows comparisons and ranking.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Prioritize and rank

Using figures for risk exposure and also the timeframe available to deal with the risk, we can rank order our set of risks. This has the advantage that more critical risks would be ranked higher and probably higher priority attention.

As time passes and/or a risk is dealt with, the ranking may change. This further implies therefore that our Rank Ordered Risk List is a dynamic and evolving document.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Risk Control: Plan for risk resolution:

Now that we have analyzed our risks and can concentrate on the critical ones, we must move to control them. To do so however, we first have to create an action plan. We must:

Identify or develop risk resolution options

Compare and select best resolution approach

Develop a risk resolution strategy

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

There are usually more than one way to resolve a risk or a problem. Some are preferable to others. In a project context, we must identify the various ways that are open to us to deal with a particular risk. We could:

Accept the risk: Live with the risk and its potential consequences

Avoid the risk: Eliminate it altogether

Reduce the risk: Take steps to reduce the probability of it occurring

Mitigate the risk: Take steps to reduce the impact of it if it occurs

Each option would have a particular consequence

Identify or develop risk resolution options

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Given the options selected in the previous step, we can now estimate a remaining risk exposure after each potential approach has been (theoretically) employed. Obviously, the approach which leaves the least risk exposure is the most effective approach. But is it the most efficient approach? Can we afford to take that approach. This brings the issue of cost of risk resolution into the equation. Now it is ALWAYS possible to reduce the risk, but this is at a cost. Facing the law of diminishing returns, we must calculate the Risk Reduction Leverage (RRL), the efficiency of risk resolution of a particular risk resolution strategy or alternatively, the point beyond which risk reduction using a given technique is not economical.

Compare and select best resolution approach

rrafterbefore CRERERRL /)(

Where REbefore and REafter refer to risk exposure before and after risk reduction measure is taken. Crr is the cost of that risk resolution activity.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Develop a risk resolution strategy

Having selected the strategy to follow, we must now create a risk resolution action plan. This document shall list and describe:

the resources needed,

all critical times and deadlines,

all indictors (actions or events that help focus our attention)

all activities that must be performed,

person or persons responsible.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Having obtained a risk action plan document, we can use it to proceed to resolve the risk and track the progress we are making towards doing so. We can do this by:

Acknowledging the raising of an indicator

Taking action

Recording the action taken

Update the plan

Risk Control: Track the progress on risk resolution and mitigate the risk:

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Value of Information

One effective way of risk management is to obtain information relevant to the risk.

How much is this information worth?

To answer this question we define the expected value of information as the increase in expected profit if the decision maker has access to the full information concerning the outcome (knows the outcome). As such:

inf_inf_ beforeperfectVOI

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Attitude towards Risk and the Utility Function:

In all discussions so far we have assumed that the true objective is to maximize expected profit under all circumstances. But is this really true?

Let us play a game:

You have been given the choice of:

1. Being given $X in cash now, or

2. A 50-50 chance at $2.5X

Let us fill out a table for each of you:

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

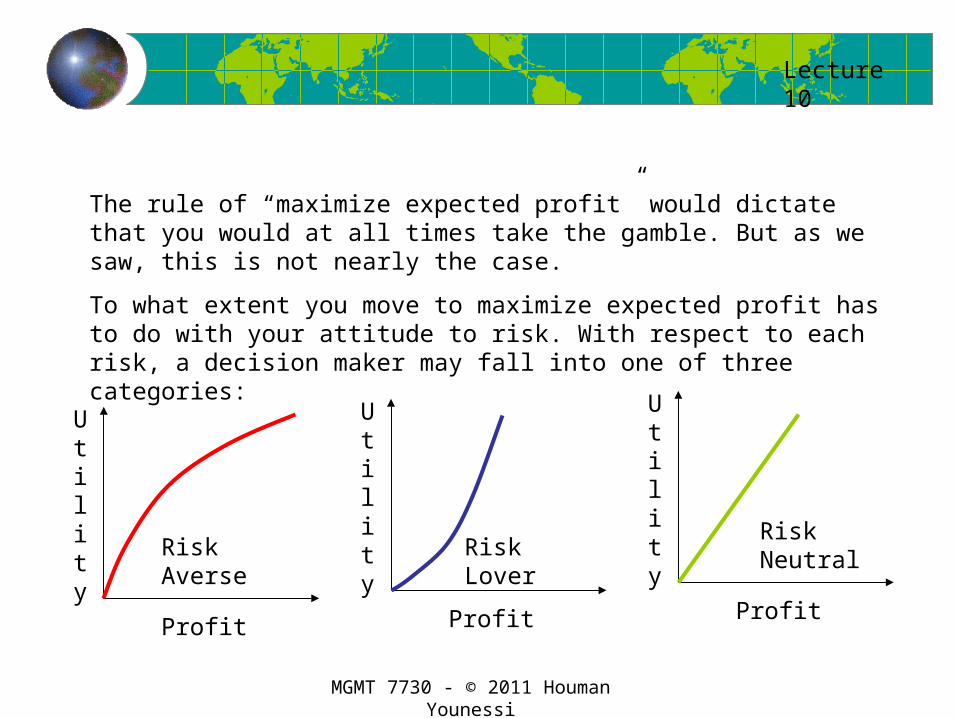

The rule of “maximize expected profit” would dictate that you would at all times take the gamble. But as we saw, this is not nearly the case.

To what extent you move to maximize expected profit has to do with your attitude to risk. With respect to each risk, a decision maker may fall into one of three categories:

Profit

Utility

Profit

Utility

Profit

Utility

Risk Averse Risk LoverRisk Neutral

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

If:

02

2

d

Ud

02

2

d

Ud

02

2

d

Ud

Then you are a risk lover

Then you are risk averse

Then you are risk neutral

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

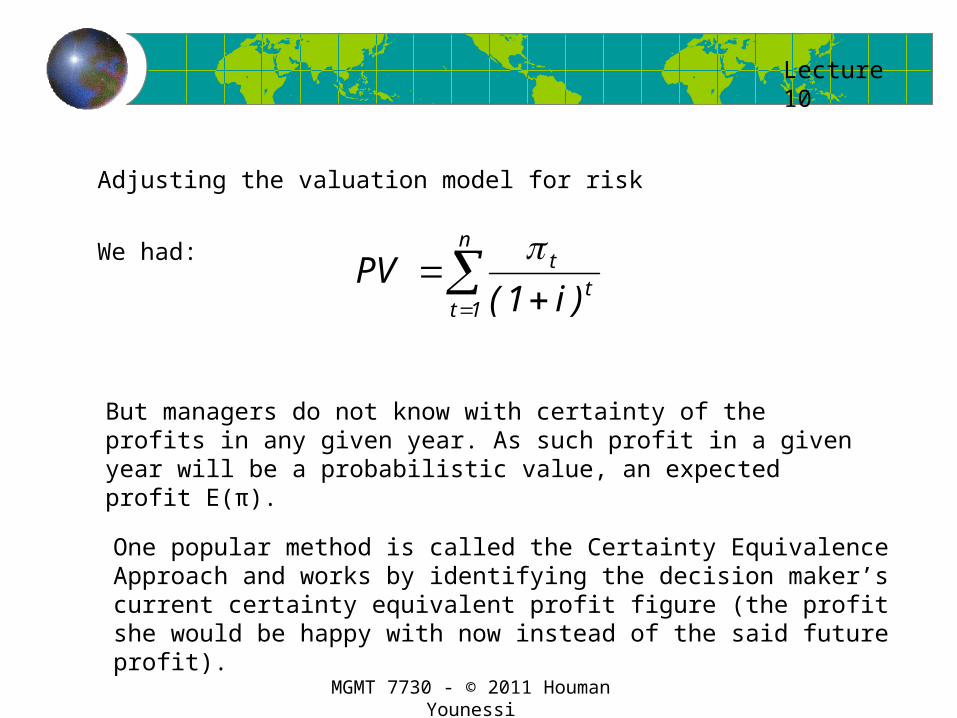

Adjusting the valuation model for risk

We had:

n

tt

t

iPV

1 )1(

But managers do not know with certainty of the profits in any given year. As such profit in a given year will be a probabilistic value, an expected profit E(π).

One popular method is called the Certainty Equivalence Approach and works by identifying the decision maker’s current certainty equivalent profit figure (the profit she would be happy with now instead of the said future profit).

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

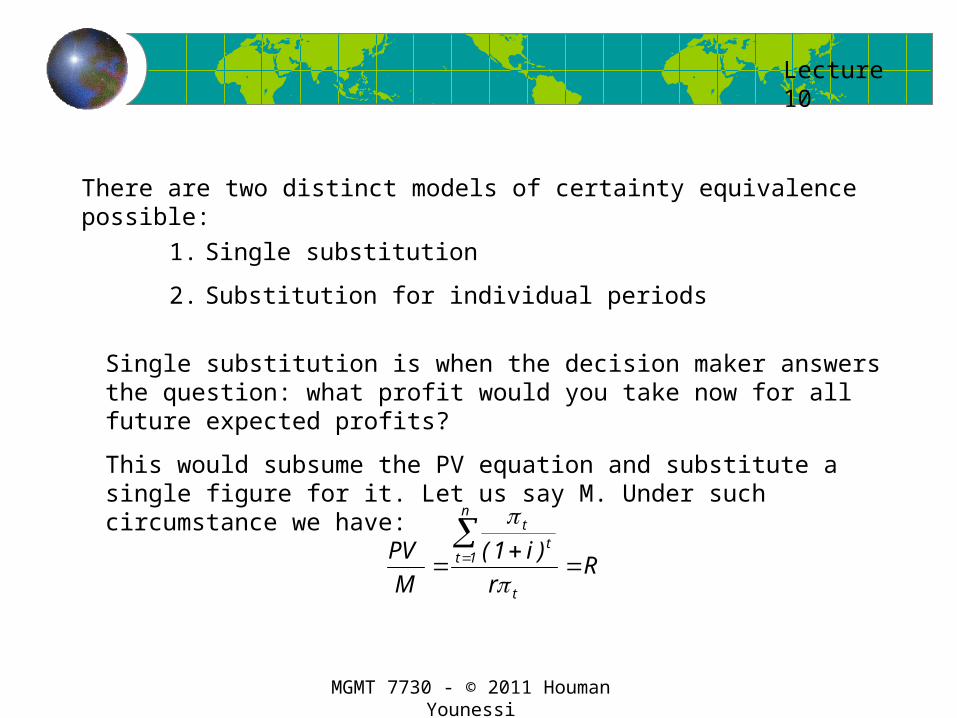

There are two distinct models of certainty equivalence possible:

1. Single substitution

2. Substitution for individual periods

Single substitution is when the decision maker answers the question: what profit would you take now for all future expected profits?

This would subsume the PV equation and substitute a single figure for it. Let us say M. Under such circumstance we have:

Rr

i

M

PV

t

n

tt

t

1 )1(

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

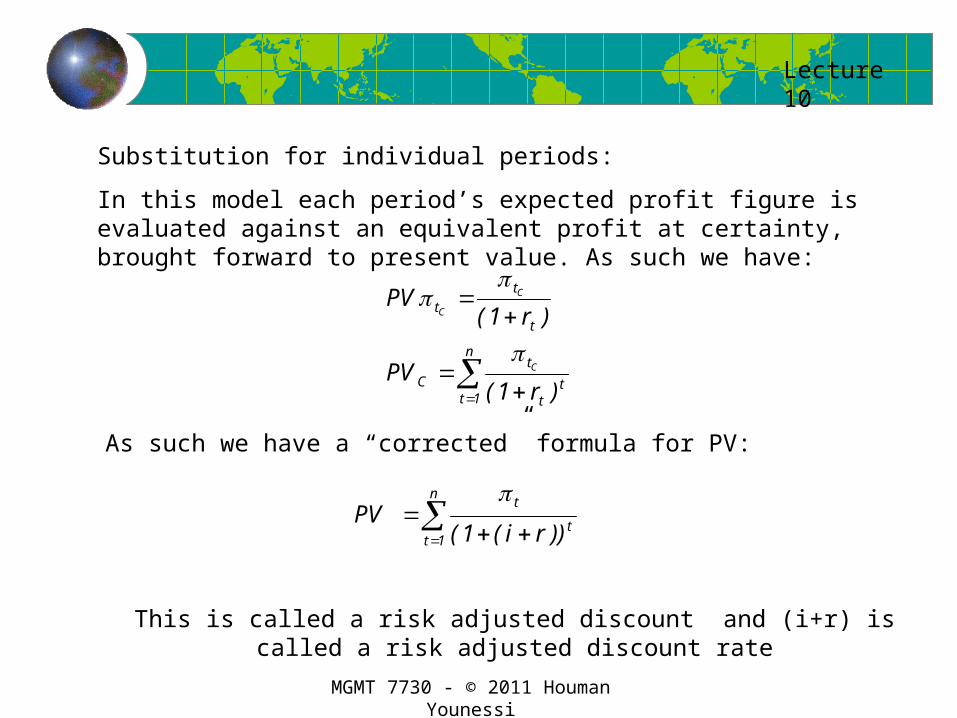

Substitution for individual periods:

In this model each period’s expected profit figure is evaluated against an equivalent profit at certainty, brought forward to present value. As such we have:

n

tt

t

tC

t

tt

rPV

rPV

C

C

C

1 )1(

)1(

As such we have a “corrected” formula for PV:

n

tt

t

riPV

1 ))(1(

This is called a risk adjusted discount and (i+r) is called a risk adjusted discount rate

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

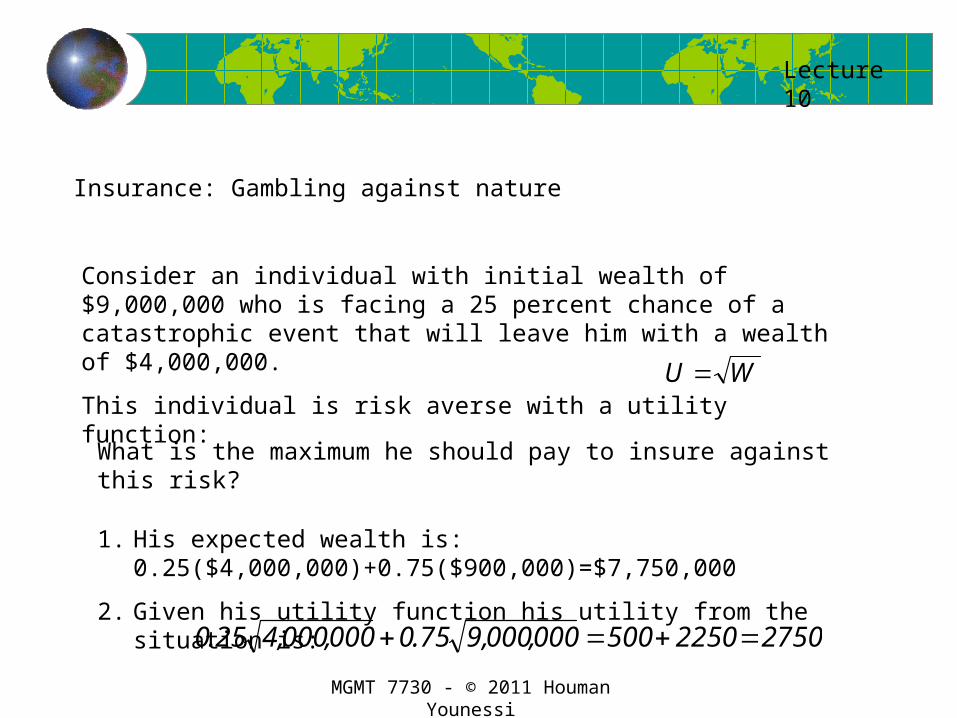

Insurance: Gambling against nature

Consider an individual with initial wealth of $9,000,000 who is facing a 25 percent chance of a catastrophic event that will leave him with a wealth of $4,000,000.

This individual is risk averse with a utility function: WU

What is the maximum he should pay to insure against this risk?

1. His expected wealth is: 0.25($4,000,000)+0.75($900,000)=$7,750,000

2. Given his utility function his utility from the situation is:

27502250500000,000,975.0000,000,425.0

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

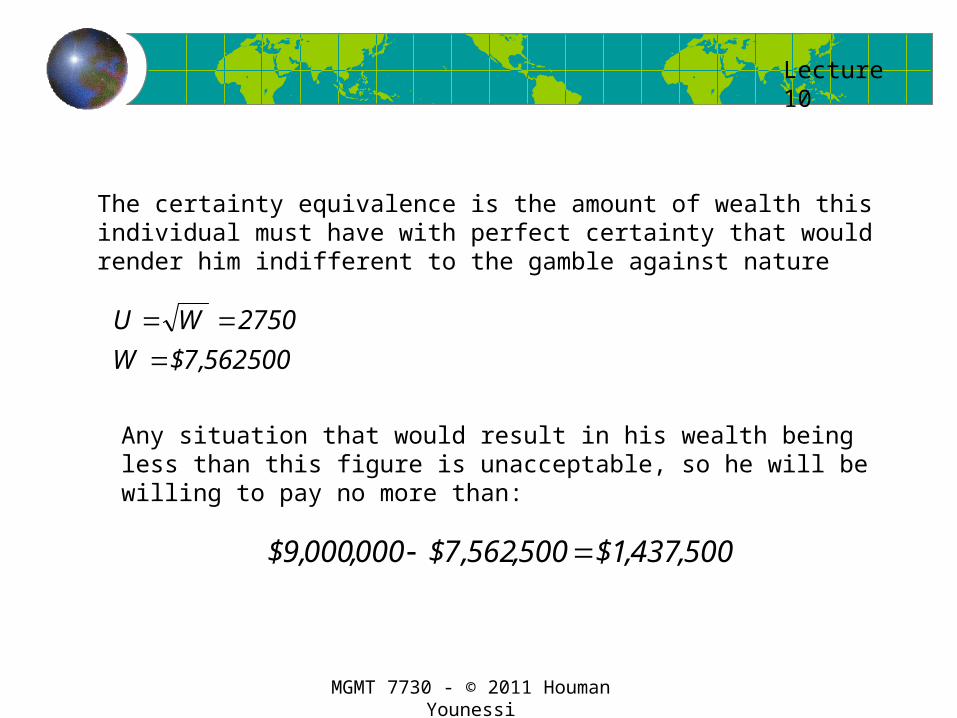

The certainty equivalence is the amount of wealth this individual must have with perfect certainty that would render him indifferent to the gamble against nature

562500,7$

2750

W

WU

Any situation that would result in his wealth being less than this figure is unacceptable, so he will be willing to pay no more than:

500,437,1$500,562,7$000,000,9$

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Up to what premium value is the insurance company willing to insure the risk?

The insurance company has 25% chance of paying $5,000,000 and a 75% chance of paying nothing. Therefore the expected payout is $1,250,000.

The insurance company will not insure the risk for less than this amount.

Therefore by knowing the customer’s attitude towards risk the insurance company can put itself in a better relative position.

What figure would the insurance company charge if they were a monopolist?

What figure would they charge if there was perfect competition for this business?

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Moral Hazard and the Principal-Agent Problem

The firm has to work as a single entity and to make decisions that maximize its wealth. However, firms cannot make decisions, people make decisions.

There are usually more than one category of stakeholder associated with a firm and they at times have conflicting interests.

The only way to ensure that the firm’s best interest is maintained, is to ensure that the firm’s best interest coincides with the best interest of the individuals responsible for maintaining the firms best interest in the first place.

Which would you prefer, all else the same :

-To ride in an aircraft that is controlled by a pilot from the ground,

-To ride in an aircraft that is controlled by a pilot in the cockpit on-board ?

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

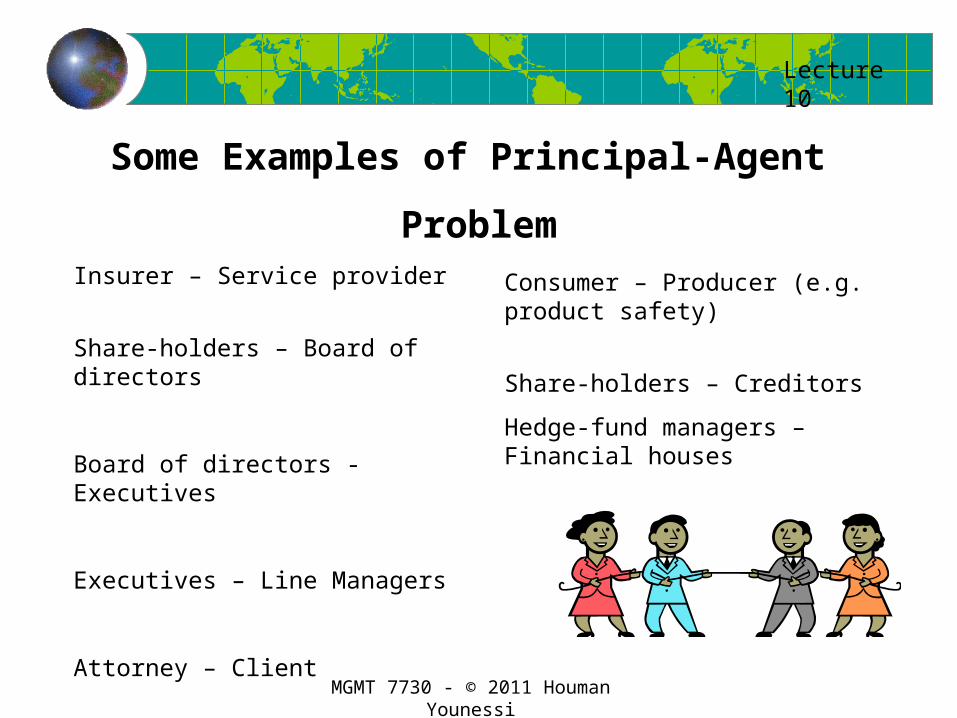

Some Examples of Principal-Agent

ProblemInsurer – Service provider

Share-holders – Board of directors

Board of directors - Executives

Executives – Line Managers

Attorney – Client

Consumer – Producer (e.g. product safety)

Share-holders – Creditors

Hedge-fund managers – Financial houses

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Owner- Executive Conflict

One of the most important principal-agent problems is that between owners of a firm (e.g. shareholders) and executives (e.g. CEO etc.)

Shareholders are concerned with the current and future value of their shares

Managers are concerned (amongst other things with):

- Minimizing effort - Enhancing their reputations

- Maximizing job security - Perks

- Avoiding failure - Compensation

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

A model of the Principal –Agent Problem

All Principal-Agent problems involve the separation of ownership and control: one party, the agent, has the control of the decision and the other party , the principal, bears the consequence of the decision.

In final analysis, the conflict is over incentives

We can summarize the idea of incentive conflict with the concept of effort.

To achieve the targets required a manager (say an executive) must incur some personal cost which we call effort. Managers would naturally want to minimize this cost, as it is a cost to them directly.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

So a bit more formally,

The profit to the firm, π, depends on the manager’s effort, e. Thus we can write π(e).

For the moment we assume that the profit is not risky. That is, once the manager chooses a level of effort, the profit corresponding to that level will ensue.

But we know that )()()( eCeRe and therefore revenue also depends on effort

and costs include the manager’s compensation but for simplicity are otherwise independent of the manager’s efforts.

)()()( CPeRe

Separating the manager’s package of compensation from other costs we have:

The owners of the firm would wish to maximize profit which would be obtained when revenue is maximized which in turn requires maximum effort. So the owners would wish to maximize effort. But they cannot choose the effort level which is chosen by the manager.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

The objective of the manager is to maximize net utility to himself or herself.

To gain this utility the manager must supply effort. The cost of supplying this effort we show as E(e), which we call the disutility of effort and is the measure of dissatisfaction of the manger in the effort-supply deal. So the total benefit to the manager becomes:

)()( eEPeB

Let us first assume that the compensation package P consists only of a constant salary figure S.

Because S is constant and E(e) increases with effort, B(e) must slope downwards.

So the manager who bears all the cost of effort but none of the rewards is actually best off with exerting zero effort!

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

In contrast the shareholders (firm owners) who get the benefit would want maximum effort from managers.

How do we resolve the problem?

Reward the manager in relation to the effort!

This would be easy and would solve the problem, we would have:

CeUKeRCePeRe

eUKeP

))(()()()()(

)()(

Where K is a flat salary, and U(e) is an additional amount that varies with effort. When U(e)=E(e) the manager feels fully compensated.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

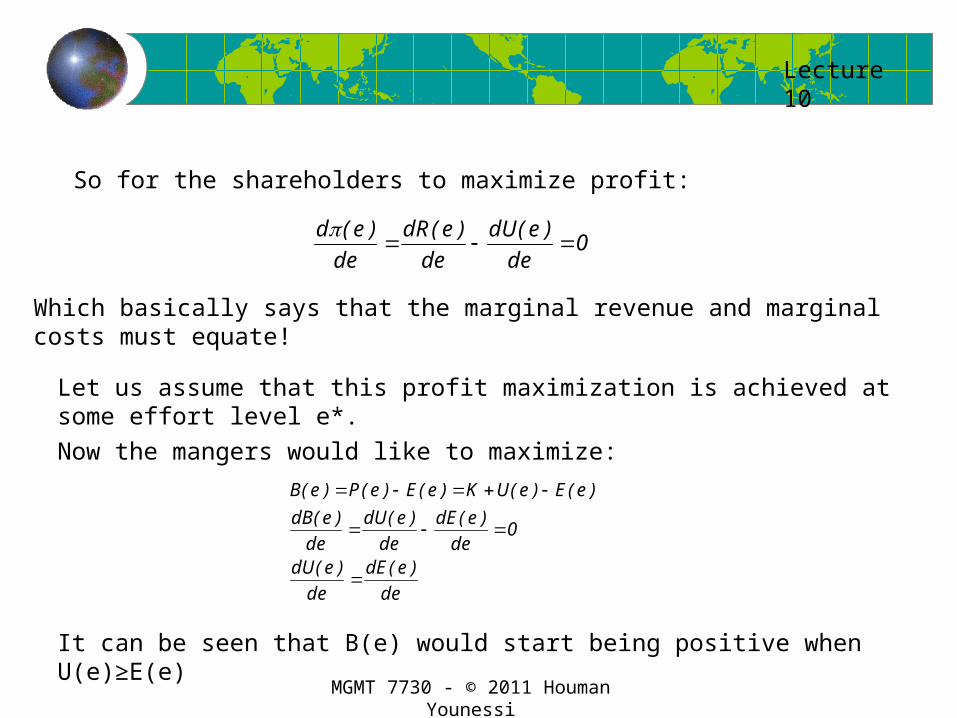

So for the shareholders to maximize profit:

0)()()(

de

edU

de

edR

de

ed

Which basically says that the marginal revenue and marginal costs must equate!

Let us assume that this profit maximization is achieved at some effort level e*.

Now the mangers would like to maximize:

de

edE

de

edUde

edE

de

edU

de

edB

eEeUKeEePeB

)()(

0)()()(

)()()()()(

It can be seen that B(e) would start being positive when U(e)≥E(e)

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Under such conditions B(e) ≥ K. The manager will fill adequately compensated.

But how do we get the managers to supply an effort exactly equal to e* so as to maximize firm’s profit?

One simple answer would be to tell the manager to produce e*. As given the compensation scheme, supply of any amount of effort is indifferent to the manager, there should be no impediment to choosing any e, including e*.

Alas, this assumes that level of effort is observable, which is usually not the case.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

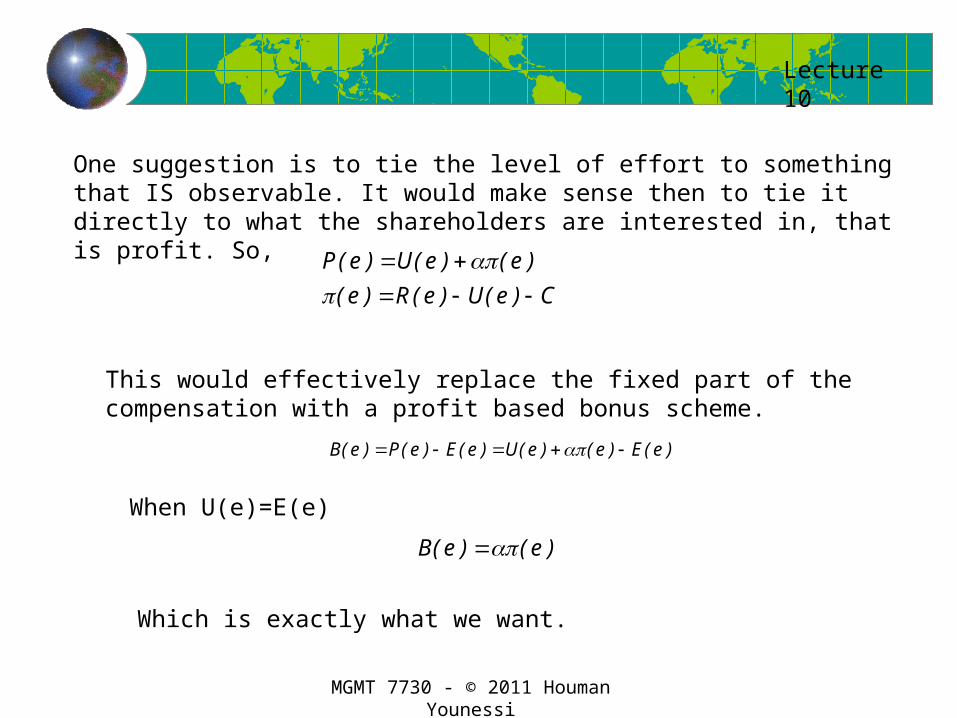

One suggestion is to tie the level of effort to something that IS observable. It would make sense then to tie it directly to what the shareholders are interested in, that is profit. So,

CeUeRe

eeUeP

)()()(

)()()(

This would effectively replace the fixed part of the compensation with a profit based bonus scheme.

)()()()()()( eEeeUeEePeB

When U(e)=E(e)

)()( eeB

Which is exactly what we want.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Unfortunately

The scheme below assumes that there is no risk. Remember that this is a scheme based on sharing the EXTENT of the profit not the risk of the profit. One side or another may have more or less incentive with regards to the risk of earning a profit. In general the shareholders are more diversified and less susceptible to risk.

To solve this problem we need to understand what is at risk and who controls that risk.

The entity at risk is revenue. Some parts of the risk to revenue is under the manager’s control and some other parts is not (e.g. drought in South America). We can therefore write:

21 )()( ReReR

Where only R1(e) is under the manager’s control.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

As the principal cannot observe the effort, nor can it now be inferred from profits, compensation cannot depend only on effort. We must re-introduced the fixed element back into the compensation package:

CKReRCKeRe

eKeP

21 )()()(

)()(

The net benefit is also exposed to risk as the bonus part is subject to risk. We must modify the utility function of the manager and replace it with his or her expected utility (utility that is acceptable under risk).

)()]([

)())(()(

eEeKEU

eEePEUeB

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

The principal must design a contract to offer the agent knowing that he will not be able to observe the agent’s actual effort. The principal anticipates that the agent will choose to make the effort after his/her expected utility is satisfied.

The agent, having seen the contract, selects a level of effort which may or may not be e*.

Therefore the challenge will be to design a compensation package that forces the agent to choose e*.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Share-holder – Creditor Principal Agent Problem

Given a fair and appropriately designed profit and risk sharing compensation scheme means that the shareholders will take over the control of the firm through their agents the executives. Creditors (e.g. bondholders) also have a direct interest in a firm. How would their interests be safe-guarded?

Consider the case of a drug company with an existing product line that exposes the firm to some risk. The present value of future earnings will be either: PV1=100 or PV2=200 each with a probability of 0.5.

The firm has borrowed money under a bond issue. The debt has a face value of 100.

Even under worst case, the firm is worth 100 and can pay back the debt. It is safe to assume there is no chance of default.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

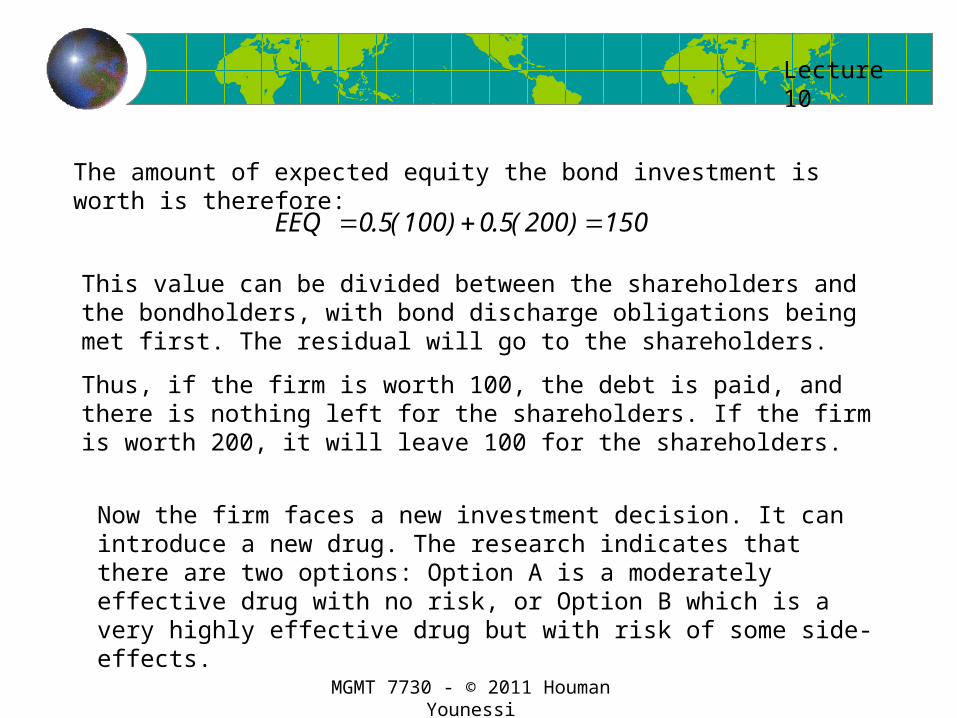

The amount of expected equity the bond investment is worth is therefore:

150)200(5.0)100(5.0 EEQ

This value can be divided between the shareholders and the bondholders, with bond discharge obligations being met first. The residual will go to the shareholders.

Thus, if the firm is worth 100, the debt is paid, and there is nothing left for the shareholders. If the firm is worth 200, it will leave 100 for the shareholders.

Now the firm faces a new investment decision. It can introduce a new drug. The research indicates that there are two options: Option A is a moderately effective drug with no risk, or Option B which is a very highly effective drug but with risk of some side-effects.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

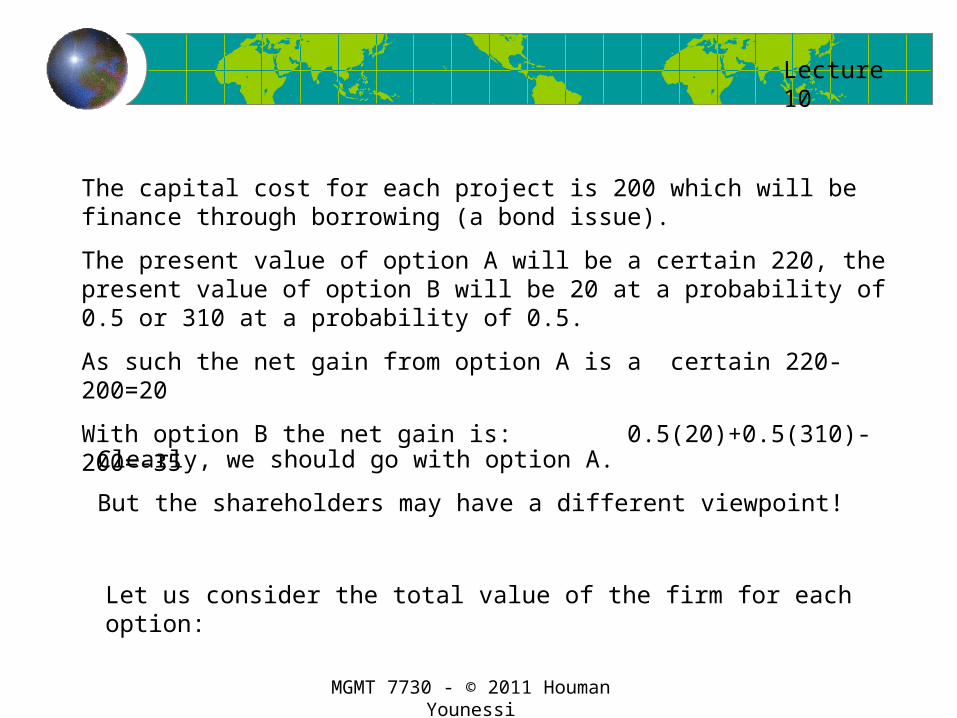

The capital cost for each project is 200 which will be finance through borrowing (a bond issue).

The present value of option A will be a certain 220, the present value of option B will be 20 at a probability of 0.5 or 310 at a probability of 0.5.

As such the net gain from option A is a certain 220-200=20

With option B the net gain is: 0.5(20)+0.5(310)-200=-35

Clearly, we should go with option A.

But the shareholders may have a different viewpoint!

Let us consider the total value of the firm for each option:

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

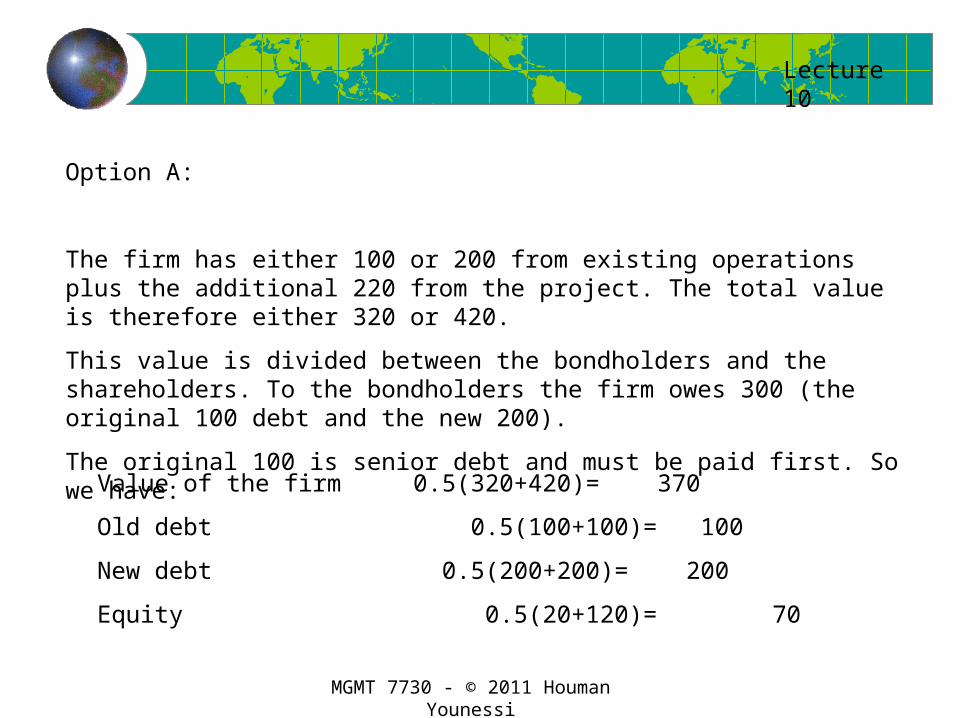

Option A:

The firm has either 100 or 200 from existing operations plus the additional 220 from the project. The total value is therefore either 320 or 420.

This value is divided between the bondholders and the shareholders. To the bondholders the firm owes 300 (the original 100 debt and the new 200).

The original 100 is senior debt and must be paid first. So we have:

Value of the firm 0.5(320+420)= 370

Old debt 0.5(100+100)= 100

New debt 0.5(200+200)= 200

Equity 0.5(20+120)= 70

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Option B:

The total value can be either 100 or 200 from existing operations plus either 20 or 310 from the project. This leaves the total values of:

100+20=120

100+310=410

200+20=220

200+310=510

Correspondingly we have:

Value of the firm 0.25(120+220+410+510)= 315

Old debt 0.25(100+100+100+100)= 100

New debt 0.25(20+120+200+200)= 135

Equity 0.25(0+0+110+210)= 80

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

Here is the problem:

The firm borrows 200 in new debts. The shareholders (through their agents) must choose which project to go for. Share holders are better off with option B where equity is 80 than with option A where it is only 70.

How can a worse project make the shareholders better off?

The issue is limited liability. If the firm undertakes A, it creates no risk of defaulting. Shareholders gain will be 20 (was 50 before the project 70 after the project).

If B is chosen, there is 50 percent chance that the project will fail and the company will go bankrupt. Under those circumstances the firm is unable to pay its debts. On the other hand, if the project succeeds, (worth 310), shareholders reap major benefit. So if things go well, the shareholders will reap the upside, if things go bad, the shareholders walk away, and the bondholders suffer! (their debt will not be paid).

This is why shareholders tend to favor risky ventures to be undertaken by the firm.

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

But the bondholders are not totally helpless.

Bond holders must decide whether to lend to the firm and how much they wish to pay for the bonds.

In this case, the firm is trying to issue bonds at face value of 200.

From a game theory perspective the argument might flow as follows:

“If I were to pay 200 for these bonds, the shareholders will have access to 200 and their rational decision will be to choose option B. At that, my risk corrected bond value would then be 135. Consequently, I will not pay more than 135 for the bonds as that is what they are worth.”

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

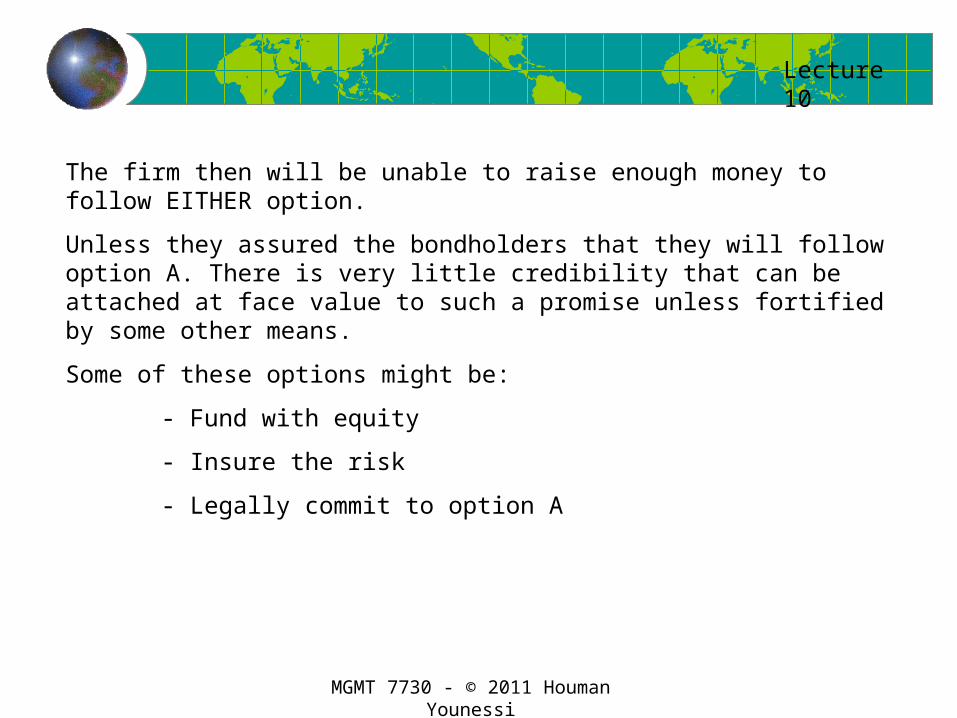

The firm then will be unable to raise enough money to follow EITHER option.

Unless they assured the bondholders that they will follow option A. There is very little credibility that can be attached at face value to such a promise unless fortified by some other means.

Some of these options might be:

- Fund with equity

- Insure the risk

- Legally commit to option A

Lecture 10

MGMT 7730 - © 2011 Houman Younessi

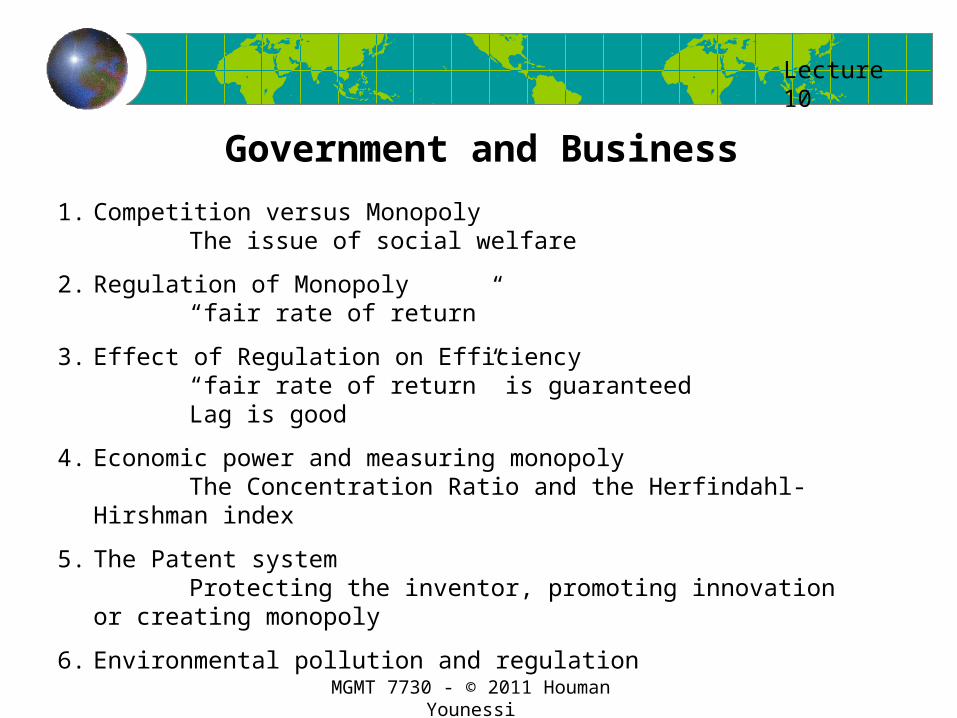

Government and Business

1. Competition versus MonopolyThe issue of social welfare

2. Regulation of Monopoly“fair rate of return”

3. Effect of Regulation on Efficiency“fair rate of return” is guaranteedLag is good

4. Economic power and measuring monopolyThe Concentration Ratio and the Herfindahl-Hirshman index

5. The Patent systemProtecting the inventor, promoting innovation or creating

monopoly

6. Environmental pollution and regulation

Related Documents