FN0449 Lecture 10 FN0449 Lecture 10 Good and Bad CSR – A Good and Bad CSR – A critical perspective… critical perspective… Dr Alex Hope

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FN0449 Lecture 10FN0449 Lecture 10Good and Bad CSR – A Good and Bad CSR – A critical perspective…critical perspective…

Dr Alex Hope

Objectives of the session

Explain basic features of CSR reporting

Understand the main reasons why companies become involved in CSR reporting

Explore the role of CSR reporting in the broader accounting process

Discuss key features of good CSR reporting and auditing

Understand the role of stakeholder dialogue in CSR reporting

Good and Bad aspects of reports…

Annual report (financial) targeted at shareholders CSR report (non-financial) targeted at broad range of stakeholders

Introduction

CSR reporting and auditing: Can help a business prove to its stakeholders that it is ‘doing the right thing’

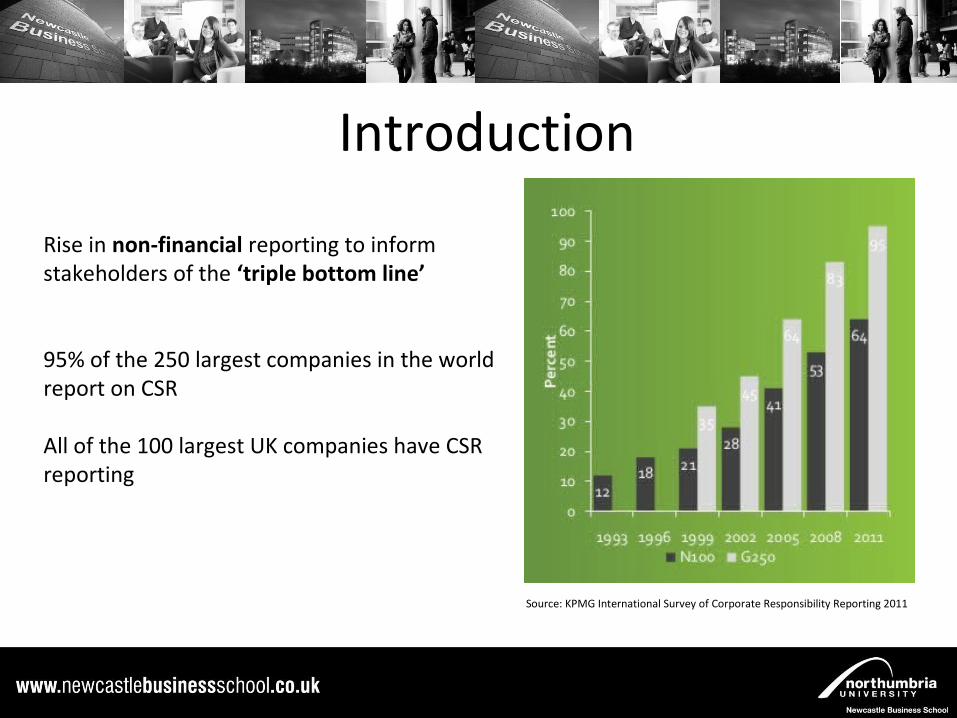

Rise in non-financial reporting to inform stakeholders of the ‘triple bottom line’

95% of the 250 largest companies in the world report on CSR

All of the 100 largest UK companies have CSR reporting

Introduction

Source: KPMG International Survey of Corporate Responsibility Reporting 2011

Part of social accounting / auditing process

CSR reporting is still voluntary = Heterogeneity of CSR reports

•Wide variety of language / content•Difficult for stakeholders to assess the quality of a company’s CSR•Prevents the reader from comparing different companies

Introduction

• Instrumental / economic: Social and environmental issues might pose a threat to the company’s financial performance (e.g. Nike boycotts).

• Political: Increase in corporate power = greater calls for more transparency and accountability to the public.

Reasons for Engaging in CSR Reporting & Auditing

Integrating stakeholder demands: CSR auditing and reporting helps companies to improve their interaction with stakeholders as part of a broader process of dialogue and engagement.

Ethical reasons (Responding to pressure): CSR reporting is a tool to communicate ethical values and performance.

(Framework from Garriga and Mele - see Chapter 3)

Reasons for Engaging in CSR Reporting & Auditing

Current Trends in CSR Reporting

•Standardization of CSR reporting to enhance credibility:

Standardizing CSR reports: e.g. The ‘Global Reporting Initiative’ (GRI) framework for sustainability reports (published for the first time in 2000).

Assurance: e.g. The ‘AA1000S Assurance Standard,’ launched by AccountAbility in 2002, provides a framework for assessing processes underlying a CSR report.

Current Trends in CSR Reporting

Regulation: The voluntary nature of CSR reporting is starting to be challenged in Denmark, France, Japan, Malaysia, and the UK.

Integrated reporting: e.g. The International Integrated Reporting Committee (IIRC) proposes one integrated report combining the annual and CSR report.

Current Trends in CSR Reporting

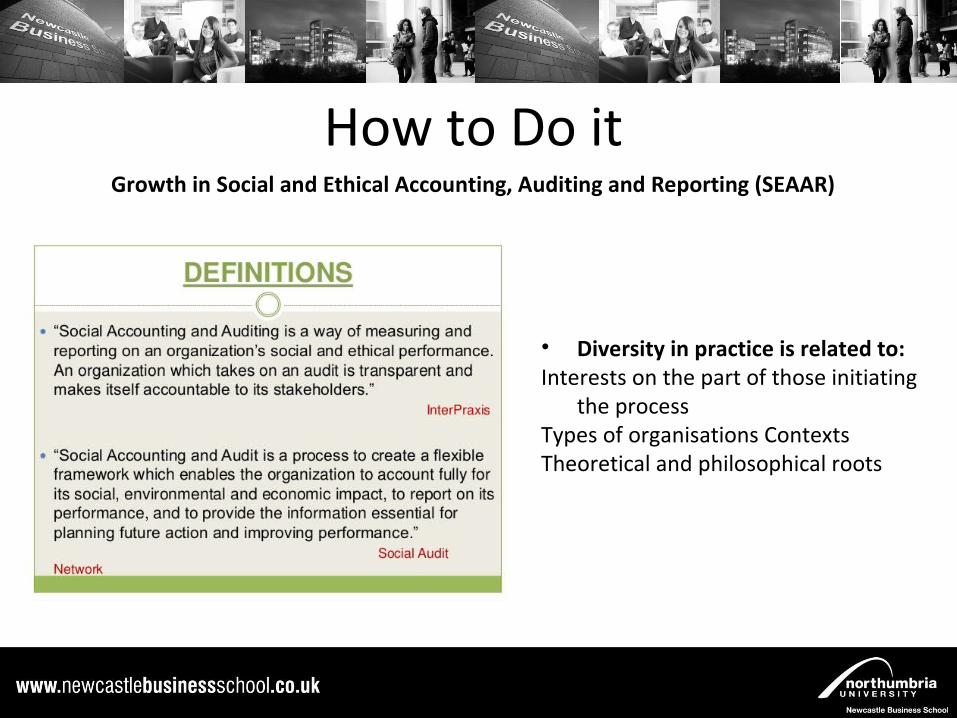

How to Do it

• Diversity in practice is related to:Interests on the part of those initiating

the processTypes of organisations ContextsTheoretical and philosophical roots

Growth in Social and Ethical Accounting, Auditing and Reporting (SEAAR)

How to Do it

• Poor practices can be related to:

Insufficient knowledge, skills, experience and/or resources

A deliberate attempt to underspecify the accounts and/or verification process to report in a less than accurate, incomplete manner

Outlay audit: Considers financial cost, not outcome valueConstituency accounting: Examine report in relation to demands of key constituenciesCorporate rating against social / ethical criteria: External ratingsSocial indicators movement: Internal and external involvement

How to Do itMethodological approaches:

http://www.slideshare.net/Bull_UK/corporate-social-responsibility-a-new-business-asset

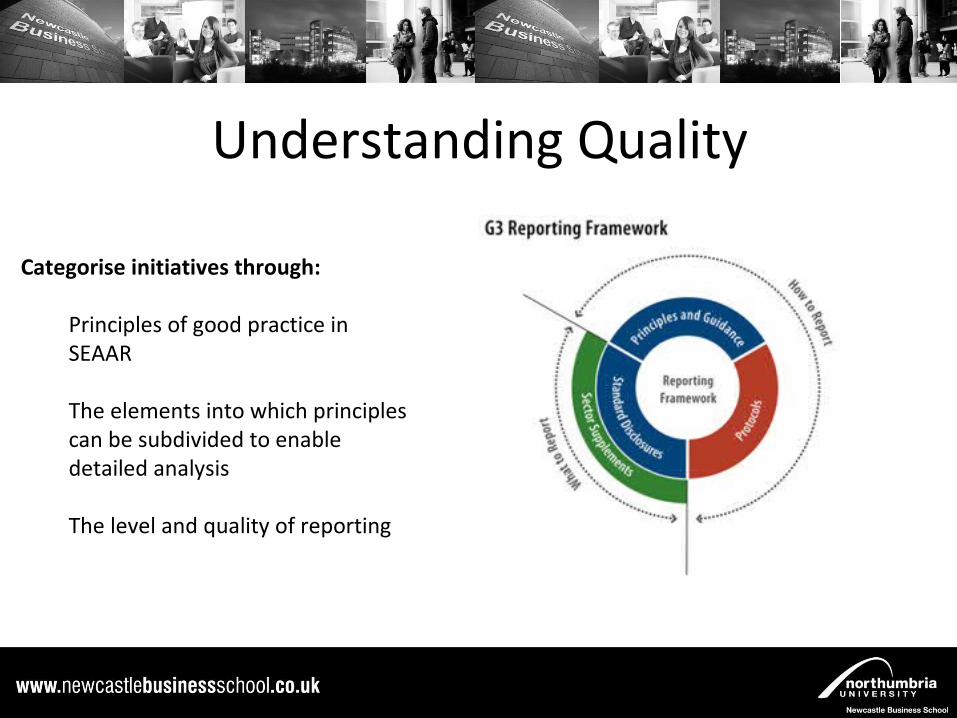

Understanding Quality

Categorise initiatives through:

Principles of good practice in SEAAR

The elements into which principles can be subdivided to enable detailed analysis

The level and quality of reporting

1.Inclusivity: Reflect views of all principal stakeholders

2.Comparability: Compare performance as a basis for assessment

3.Completeness: All areas of company activity are included

4.Evolution: Repetition to demonstrate continual learning

Understanding QualityThe 8 Principles of Quality:

Understanding QualityThe 8 Principles of Quality:

4.Management policies and systems: Clear internal processes

4.Disclosure: Formality or active means of communication?

5.Externally verified: Validate material professionally & independently

6.Continuous improvement: Assess progress over time

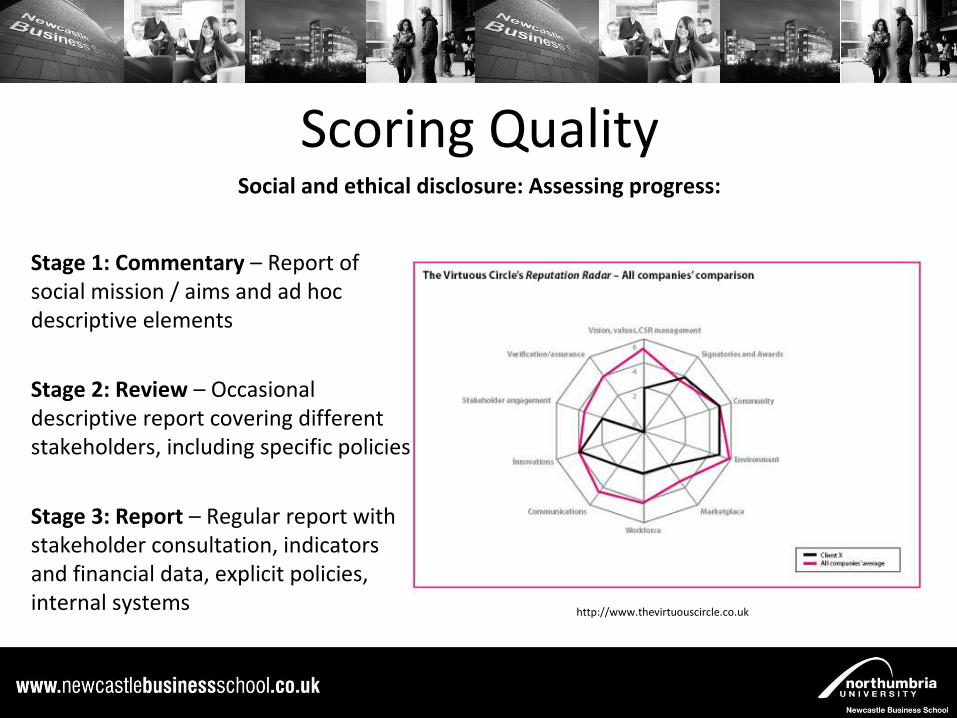

Scoring Quality

Stage 1: Commentary – Report of social mission / aims and ad hoc descriptive elements

Stage 2: Review – Occasional descriptive report covering different stakeholders, including specific policies

Stage 3: Report – Regular report with stakeholder consultation, indicators and financial data, explicit policies, internal systems

Social and ethical disclosure: Assessing progress:

http://www.thevirtuouscircle.co.uk

Stage 4: Statement – Regular externally verified report with two-way stakeholder dialogue, indicators, targets and benchmarks and commitment to comprehensive coverage over time

Stage 5: Sustainability statement – Regular externally verified sustainability statement with linkages to environmental, animal, economic and financial data

Scoring Quality

Stakeholder Engagement and Dialogue

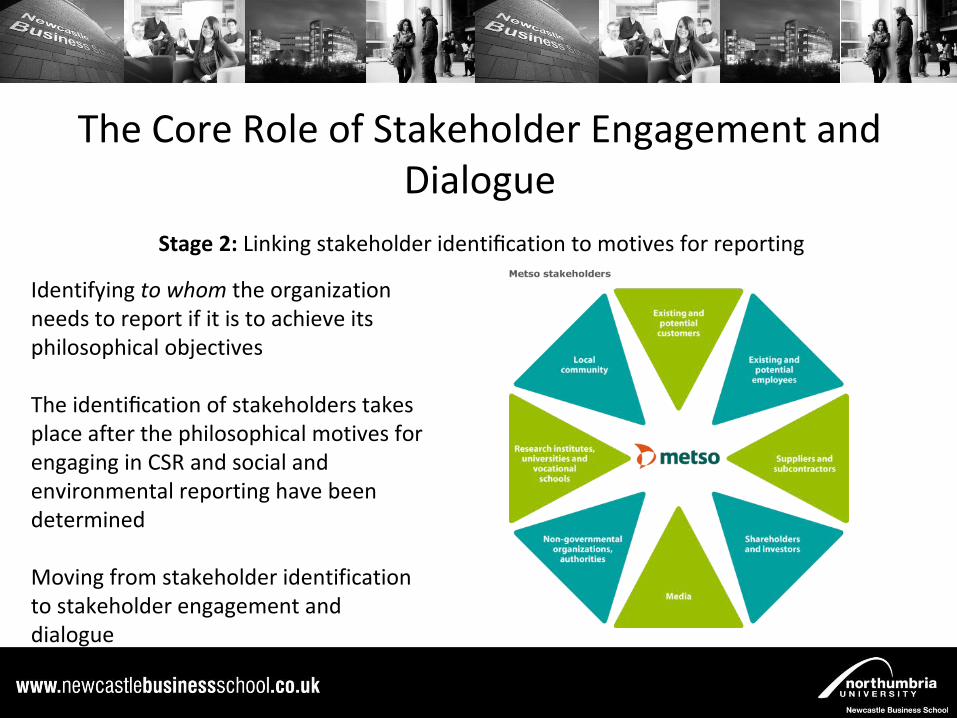

The Core Role of Stakeholder Engagement and Dialogue

Stage 1: Understanding organizational motives for stakeholder engagement and dialogue

Holistic perspective: Social and environmental reporting and CSR as processes which transform business practices to become socially and environmentally sustainable. Strategic perspective: Social and environmental reporting as a tool to win or retain the support of stakeholders who have the power to influence the achievement of an organization’s goals.

Identifying to whom the organization needs to report if it is to achieve its philosophical objectives

The identification of stakeholders takes place after the philosophical motives for engaging in CSR and social and environmental reporting have been determined

Moving from stakeholder identification to stakeholder engagement and dialogue

The Core Role of Stakeholder Engagement and Dialogue

Stage 2: Linking stakeholder identification to motives for reporting

Key Issues & Difficulties in Stakeholder Engagement & Dialogue

Identifying the range of stakeholders to be considered

Impossibility of direct dialogue and engagement with some stakeholders

Addressing heterogeneous stakeholder views and expectations

Key Issues & Difficulties in Stakeholder Engagement & Dialogue

Prioritizing stakeholder needs on the basis of maximum negative consequences

Negotiating a consensus among mutually exclusive stakeholder views through discourse ethics

What makes a good or bad report?Context: The Company's Role in Society

“Our role in society is an extension of our core purpose: we make what matters better, together.”

http://www.tescoplc.com/files/pdf/responsibility/2014/tesco_and_society_review_2014.pdf

“Banks play an important role in society. By assisting customers with financing, investments, secure payments and asset management, we support economic development and international trade and contribute to financial security”

http://sebgroup.com/about-seb/who-we-are/our-role-in-society

Material Issues

What makes a good or bad report?

http://report.basf.com/2012/en/pics/img/028a_nochart_en.png

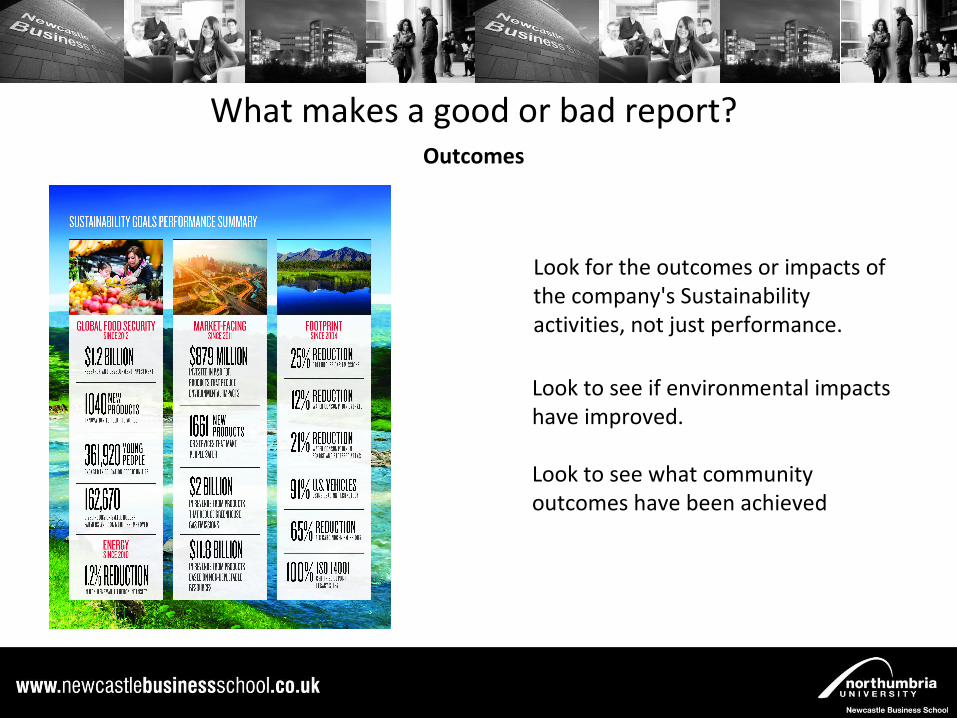

Outcomes

What makes a good or bad report?

Look for the outcomes or impacts of the company's Sustainability activities, not just performance.

Look to see if environmental impacts have improved.

Look to see what community outcomes have been achieved

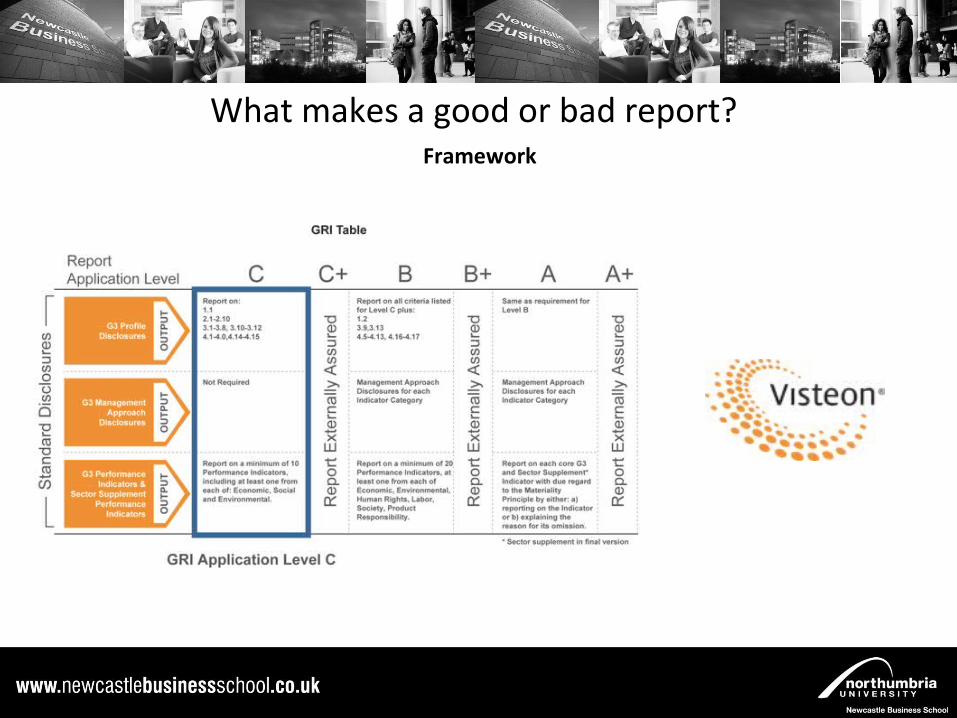

Framework

What makes a good or bad report?

Authentic Style and Tone

What makes a good or bad report?

Clear Data

What makes a good or bad report?

Targets, Progress and Future PlansWhat makes a good or bad report?

Stakeholder Voices

What makes a good or bad report?

How Sustainability is Managed

What makes a good or bad report?

Accessibility

What makes a good or bad report?

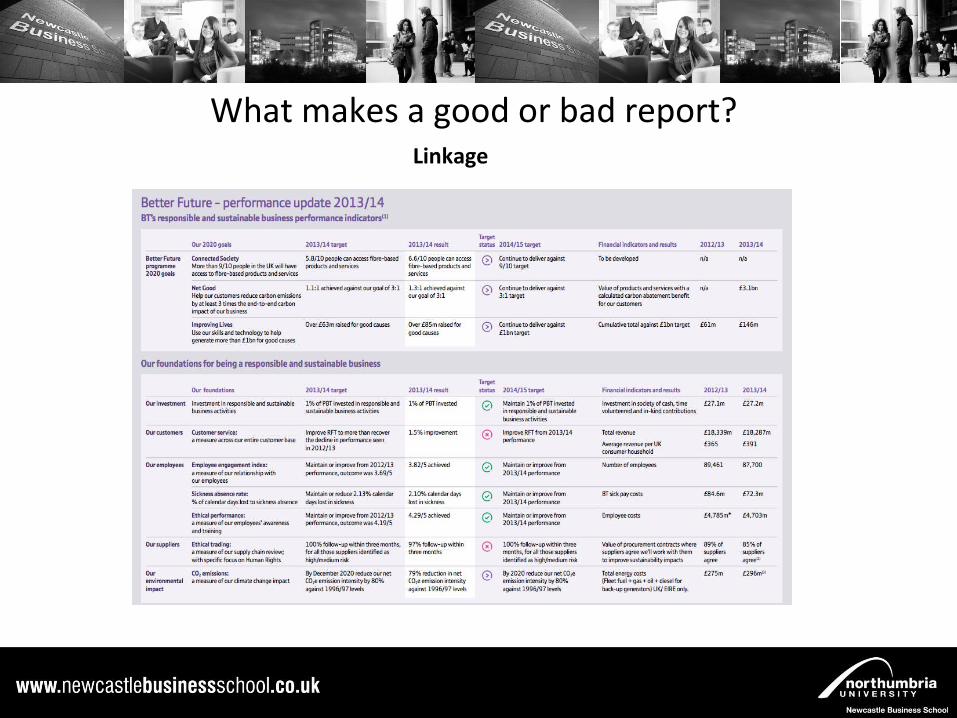

Linkage

What makes a good or bad report?

Linkage

What makes a good or bad report?

Summary

Explain basic features of CSR reporting

Understand the main reasons why companies become involved in CSR reporting

Explore the role of CSR reporting in the broader accounting process

Discuss key features of good CSR reporting and auditing

Understand the role of stakeholder dialogue in CSR reporting

Good and Bad aspects of reports…

Related Documents