LCCA Design and Maintenance John Cunningham Iowa Concrete Paving Association ASCE Conference November 6, 2013 www.iowaconcretepaving.org

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LCCA Design and

Maintenance John Cunningham

Iowa Concrete Paving Association ASCE Conference November 6, 2013

www.iowaconcretepaving.org

Life Cycle Cost Analysis

Life cycle cost analysis (LCCA) is an economic

procedure to compare competing design alternates…

www.iowaconcretepaving.org

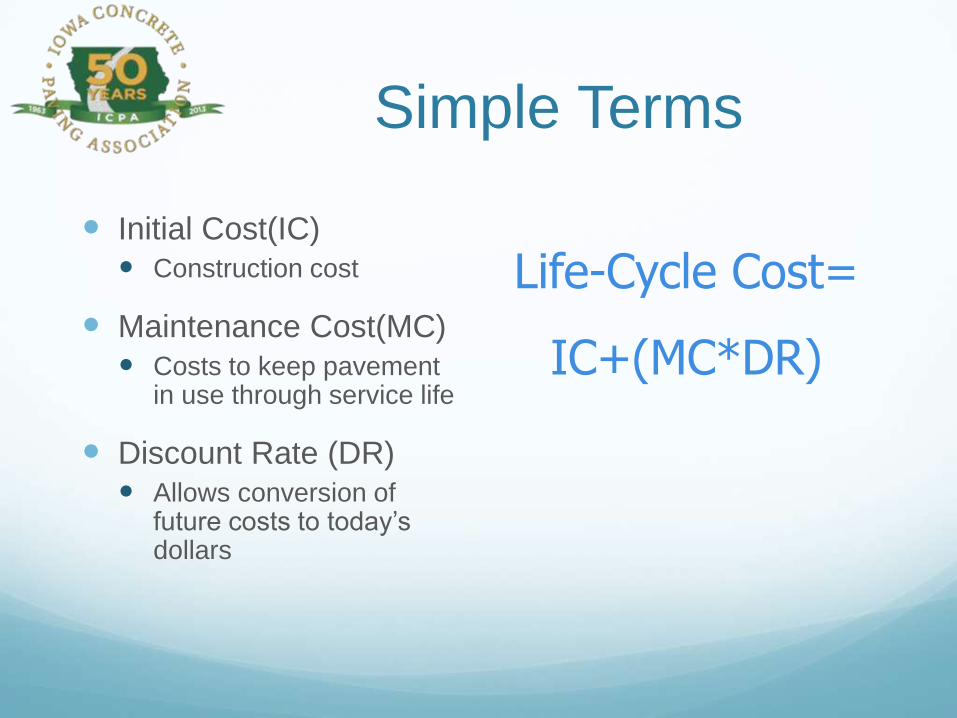

Simple Terms

Initial Cost(IC)

Construction cost

Maintenance Cost(MC)

Costs to keep pavement in use through service life

Discount Rate (DR)

Allows conversion of future costs to today’s dollars

Life-Cycle Cost=

IC+(MC*DR)

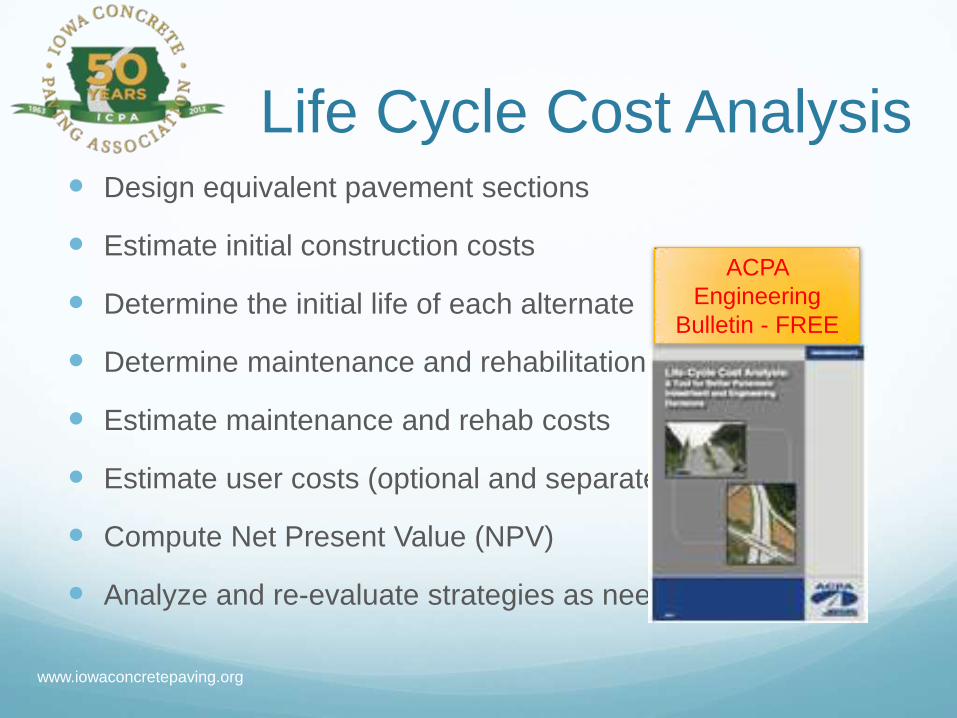

Life Cycle Cost Analysis Design equivalent pavement sections

Estimate initial construction costs

Determine the initial life of each alternate

Determine maintenance and rehabilitation

Estimate maintenance and rehab costs

Estimate user costs (optional and separate)

Compute Net Present Value (NPV)

Analyze and re-evaluate strategies as needed

ACPA

Engineering

Bulletin - FREE

www.iowaconcretepaving.org

Life Cycle Cost Analysis

Design

Maintenance

Analysis

Engineering factors

Economic factors

It’s important

to remember

the context of

the process as

a comparison

www.iowaconcretepaving.org

Bear Traps Appropriate analysis period

Equivalent designs

Realistic maintenance activities

Accurate cost estimates

Correct discount rate

www.iowaconcretepaving.org

Design Full-depth or overlay?

Equivalent design life

Sets the LCCA term or analysis period

AASHTO design guides

Darwin ME

MEPDG

AASHTO 93

ACPA

StreetPave

WinPAS

Both have LCCA components

Both available free from ICPA

www.iowaconcretepaving.org

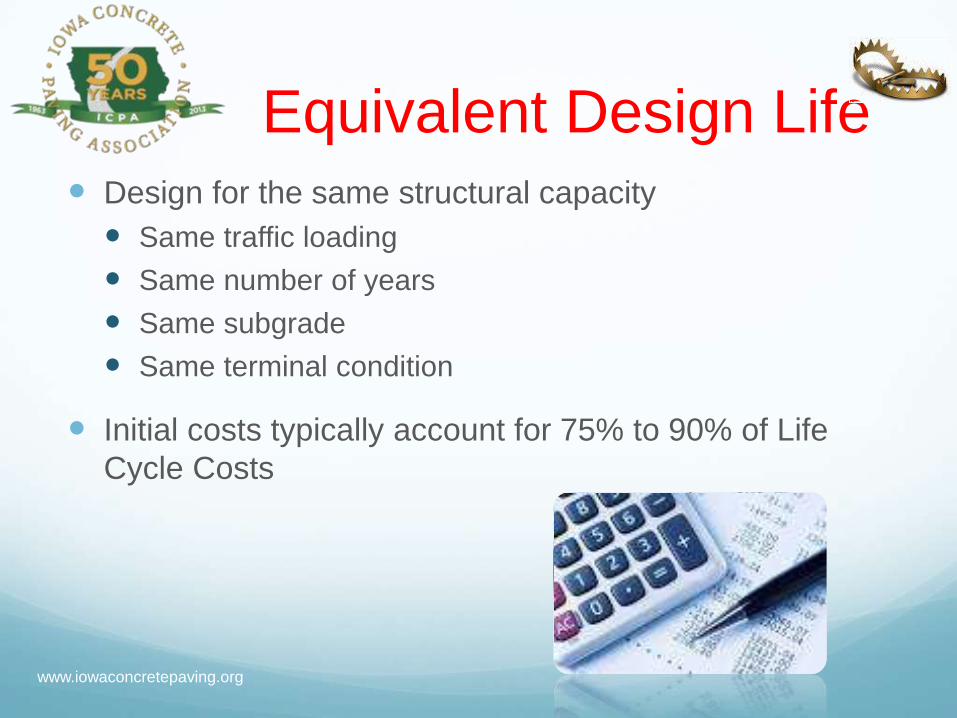

Equivalent Design Life Design for the same structural capacity

Same traffic loading

Same number of years

Same subgrade

Same terminal condition

Initial costs typically account for 75% to 90% of Life

Cycle Costs

www.iowaconcretepaving.org

Equivalent Design Life Same traffic loading

Same number of years

Same and reasonable subgrade support value

Vast variability in Iowa soils

Research is suggesting lower than estimated values

Caution if…

K > 200

CBR > 3

MR > 3,100

www.iowaconcretepaving.org

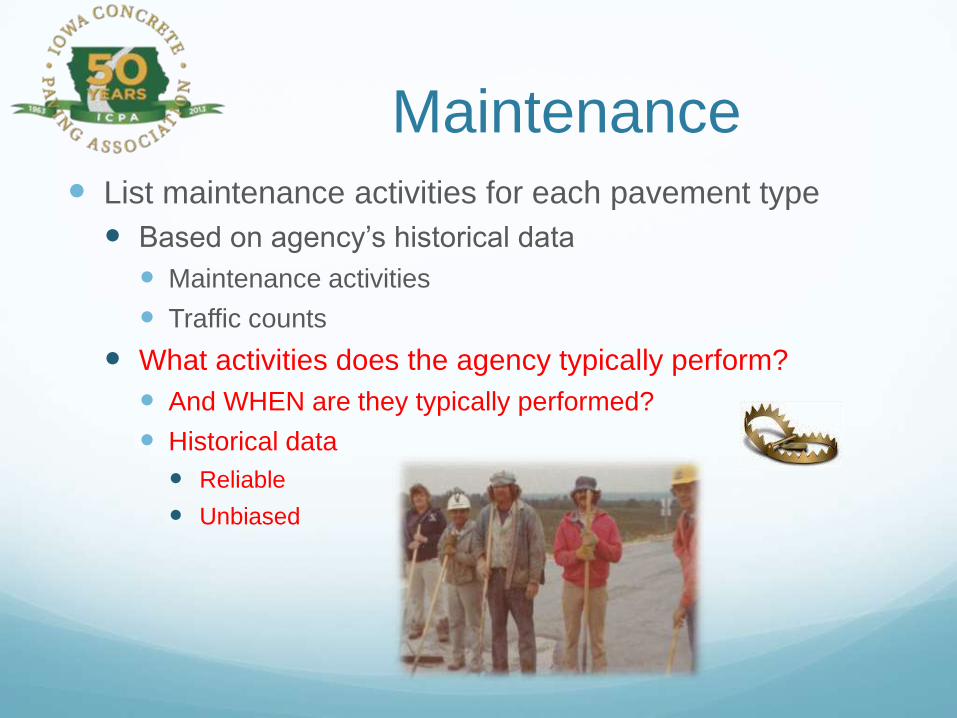

Maintenance List maintenance activities for each pavement type

Based on agency’s historical data

Maintenance activities

Traffic counts

What activities does the agency typically perform?

And WHEN are they typically performed?

Historical data

Reliable

Unbiased

30 Year

Analysis

Concrete Asphalt

Year 0 (construction) (construction)

Year 10 •Joint rehab --

Year 15 -- •Patching

•Overlay

•Base clean &

prep

•Binder

•Surface

•Asphalt

cement

•Shoulders

•Traffic control

•Mobilization

•Samples

•Lab

Year 20 •Joint rehab --

Year 30 •Joint rehab

•Patching

•Structural

overlay

•Shouldering

•Milling

•Patching

•Structural

overlay

•Shouldering

Example of LCCA

(Iowa DOT)

30 Year

Analysis

Concrete Asphalt

Year 0 (construction) (construction)

Year 10 •Joint rehab --

Year 15 -- •Patching

•Overlay

•Base clean &

prep

•Binder

•Surface

•Asphalt

cement

•Shoulders

•Traffic control

•Mobilization

•Samples

•Lab

Year 20 •Joint rehab --

Year 30 •Joint rehab

•Patching

•Structural

overlay

•Shouldering

•Milling

•Patching

•Structural

overlay

•Shouldering

Analysis Estimate initial costs

Estimate maintenance costs

Convert costs to present value

Estimating how economic factors of inflation and interest

might impact our comparison

After all, it is an economic comparison

Cost Estimates Calculate in today’s dollars

Based on actual cost data

Bid tabulations

From similar projects

ICPA retains files of bid tabs

Iowa DOT’s Price Trend Index Report

Concrete is reported by the square yard for 9” dowelled

Asphalt is reported by the ton

Indicator of trends

Cost Estimates Account for differential inflation rates

Each material has experienced different rates

LCCA is a comparison

The different rates must be accounted for

In order to get an accurate comparison of future costs

Mechanism for this is escalation

Escalation To account for differences in material specific inflation

rates, good economic practices say that we should use

a process known as “escalation”.

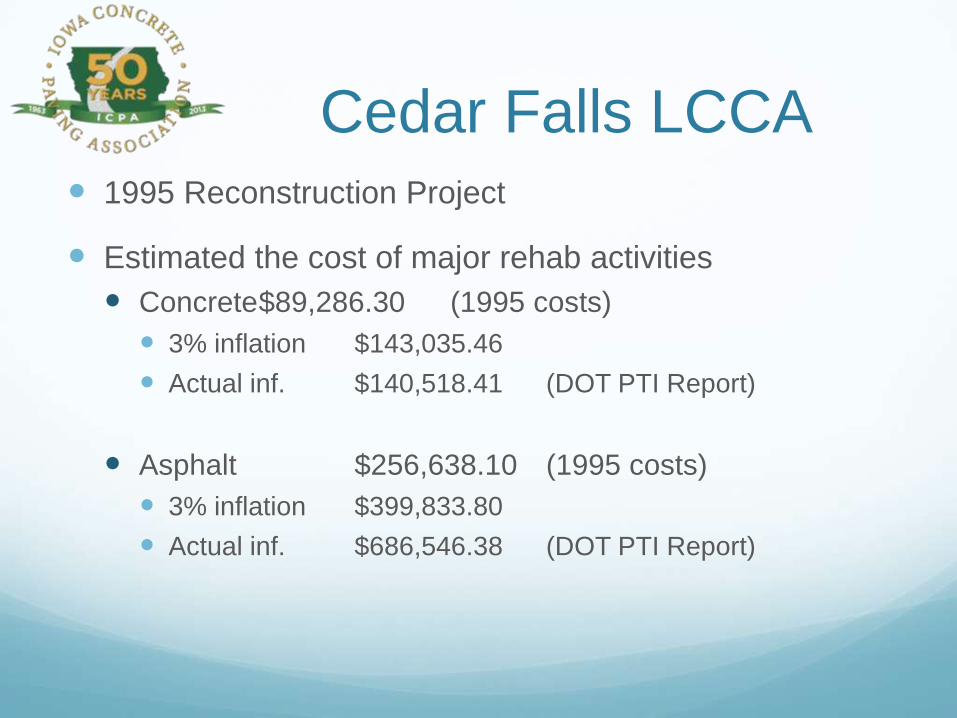

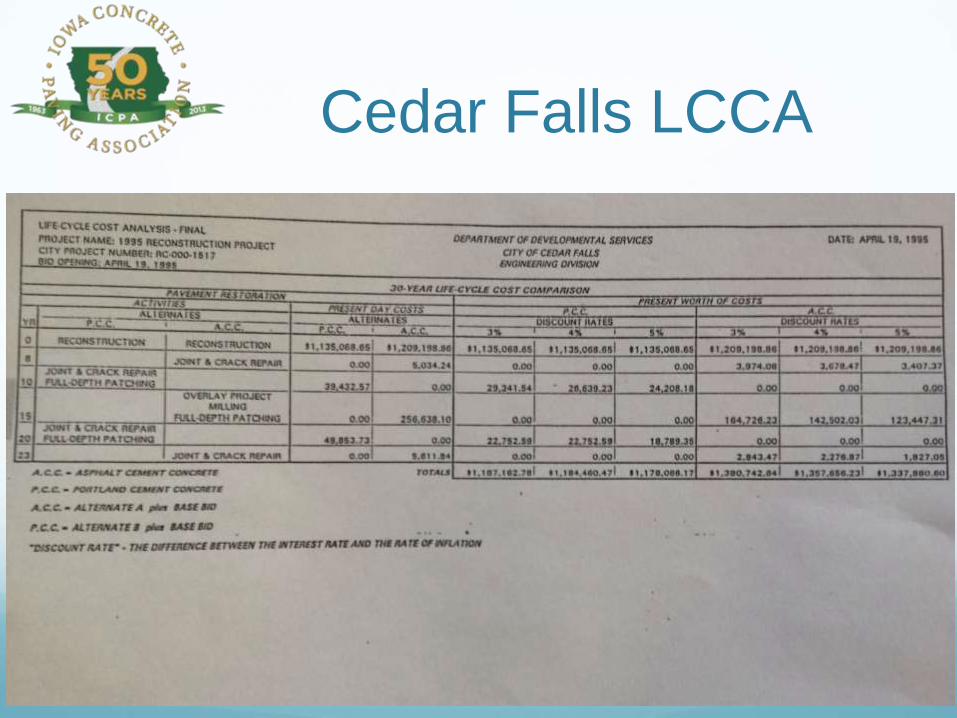

Cedar Falls LCCA 1995 Reconstruction Project

Estimated the cost of major rehab activities

Concrete $89,286.30 (1995 costs)

3% inflation $143,035.46

Actual inf. $140,518.41 (DOT PTI Report)

Asphalt $256,638.10 (1995 costs)

3% inflation $399,833.80

Actual inf. $686,546.38 (DOT PTI Report)

Cedar Falls LCCA

Escalation Gather actual rates of inflation for each material

Bureau of Labor Statistics

Producer Price Index

Iowa DOT

Price Trend Index Report

1986-2013

4.08% asphalt

3.04% concrete

Subtract general rate of inflation

Consumer price index

2.9%

Escalation Apply the difference to estimated costs

Concrete Costs X 1.0014 ^time to rehab

Asphalt Costs X 1.0118 ^time to rehab

Cedar Falls example

Concrete $39,432.57 X 1.0014 ^10 = $39,988.12

$49,853.73 X 1.0014 ^20 = $51,268.36

Asphalt $256,638.10 X 1.0118 ^15 = $306,013.97

Present Value Converting future costs to their present value allows us

to take general inflation and interest into account

Time value of money

Select a discount rate

FHWA and ACPA recommend OMB

Office of Management and Budget

Release recommended rates every year for use in economic

analysis for government projects

OMB Circular A-94

Appendix C of annual memorandum

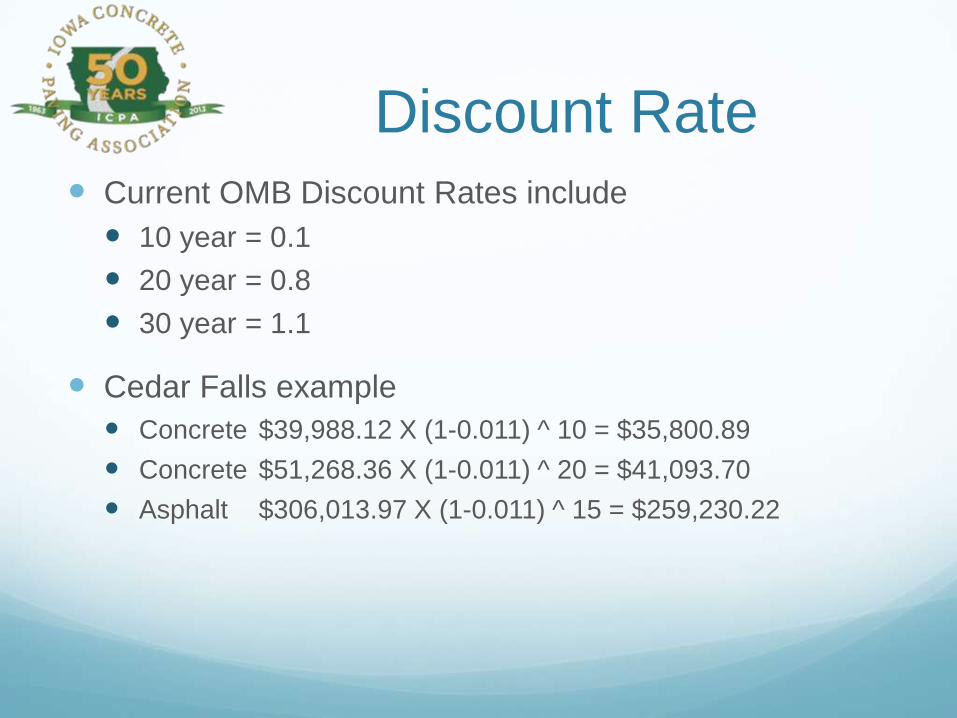

Discount Rate Current OMB Discount Rates include

10 year = 0.1

20 year = 0.8

30 year = 1.1

Cedar Falls example

Concrete $39,988.12 X (1-0.011) ^ 10 = $35,800.89

Concrete $51,268.36 X (1-0.011) ^ 20 = $41,093.70

Asphalt $306,013.97 X (1-0.011) ^ 15 = $259,230.22

Cedar Falls LCCA

Questions?

Related Documents