Mutual of Omaha 2015 Financial Review Laura Fender Senior Vice President, Enterprise Reporting and Analysis April 25, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mutual of Omaha2015 Financial Review

Laura FenderSenior Vice President,

Enterprise Reporting and AnalysisApril 25, 2016

Forward-Looking Statements

2

This document contains certain forward-looking statements about Mutual of Omaha Insurance Company and certain of its subsidiaries (collectively, the “Company”). Forward-looking statements include, but are not limited to, statements that represent the Company’s beliefs concerning future operations, strategies, financial results or other developments with respect to the Company, and contain words and phrases such as “may,” “expects,” “should” or similar expressions in this document. Forward-looking statements are not guarantees of future performance, involve risks and uncertainties, and actual results may differ materially from those in any forward-looking statement as a result of various factors. The following uncertainties, among others, may have such an effect: continued difficult conditions in the global capital markets and the economy; sustained periods of low interest rates or a sudden spike in interest rates; declining or volatile residential mortgage-backed securities values due to prepayment risks; adverse regulatory developments, including those resulting from the Dodd-Frank Wall Street Reform and Consumer Protection Act, limitations on premium levels, mandated benefits, increases in minimum capital and reserves, and other financial viability requirements; adverse credit market conditions; significant market valuation fluctuations of certain of the Company’s investments that are relatively illiquid; difficulties as to valuation of securities in the Company’s investment portfolio; exposure to below investment grade bonds; defaults on mortgage loans held by the Company; exposure to certain specific asset classes, including commercial and residential mortgage-backed securities, real estate and alternative investments; declines in the performance or valuation of real estate properties owned by the Company; heightened competition in the insurance or banking business, including, specifically, the intensification of price competition, the entry of new competitors and the development of new products by new and existing competitors; downgrades or potential downgrades in the Company’s ratings; the sensitivity of the amount of statutory capital the Company must hold to factors outside the Company’s control; subjectivity in determining the amount of allowances and impairments taken on certain of the Company’s investments; changes in the federal Medicare program and other adverse regulatory developments, including those resulting from the recently enacted Patient Protection and Affordable Care Act, that could adversely affect the demand for the Company’s Medicare supplement insurance policies or the Company’s competitive position in the Medicare supplement marketplace; impact on the Company’s reported statutory surplus or net income that could result from the adoption of certain accounting standards issued by the National Association of Insurance Commissioners or pursuant to applicable laws and regulations; impact on the Company’s reported GAAP equity or net income that could result from the adoption of the requirements of certain accounting pronouncements issued by authoritative bodies; tax law changes impacting the tax treatment of insurance and investment products; repeal of the federal estate tax; uncertainty as to the price and availability of reinsurance on business the Company currently writes or intends to write in the future; adequacy and recoverability of reinsurance that the Company has purchased; the failure of the Company’s distribution channels to obtain new customers or retain existing customers; deviations from assumptions regarding persistency, mortality, or morbidity; losses due to the financial impairment of, or defaults by, others, including bank borrowers, issuers of investment securities or reinsurance and derivative instrument counterparties; deviations from assumptions regarding future mortality, morbidity and interest rates used in calculating reserve amounts and pricing our products; requirements to post collateral or make payments related to declines in market value of specified assets, and possible declines in the value of securities available for posting as collateral; unanticipated losses resulting from the Company’s stable value wrap program; accelerated amortization of deferred acquisition costs; adverse results relating to the mixed-use real estate development adjacent to the Company’s home office property; regulatory restrictions, financial viability and other risks in connection with the Company’s ownership of Mutual of Omaha Bank; liquidity and other risks in connection with the Company’s securities lending program; impact of international tension between the United States and other nations, terrorist attacks, and ongoing military and other actions, or a large scale pandemic; changes in tax laws and the interpretation thereof; litigation and regulatory investigations; and a computer system failure or security breach.Consequently, such forward-looking statements should be regarded solely as the Company’s current plans, estimates and beliefs. The Company does not intend to undertake, and does not undertake, any obligation to update any forward-looking statements to reflect future events or circumstances after the date of such statements.All subsequent written and oral forward-looking information attributable to the Company or any person acting on its behalf is expressly qualified in its entirety by the cautionary statements contained or referred to in this section. The information contained in this document is accurate only as of the date of this document regardless of the time of delivery.

Organization and Ratings

Mutual of Omaha Insurance Company (Parent)

United of Omaha Life Insurance Company

Companion Life Insurance Company

United World Life Insurance Company

Omaha Financial Holdings, Inc.

Other Small Affiliates

3

Three Primary Strategic Business Units (SBUs)

Individual Financial

Services (IFS)

Group Benefit Services (GBS)

Bank

Financial Strength Ratings

A.M. Best A+ (Superior)Moody’s A1 (Good)Standard & Poor’s AA- (Very Strong)

Short-term Ratings

Moody’s P-1 (Prime-1, Superior)Standard & Poor’s A-1+ (Extremely Strong)

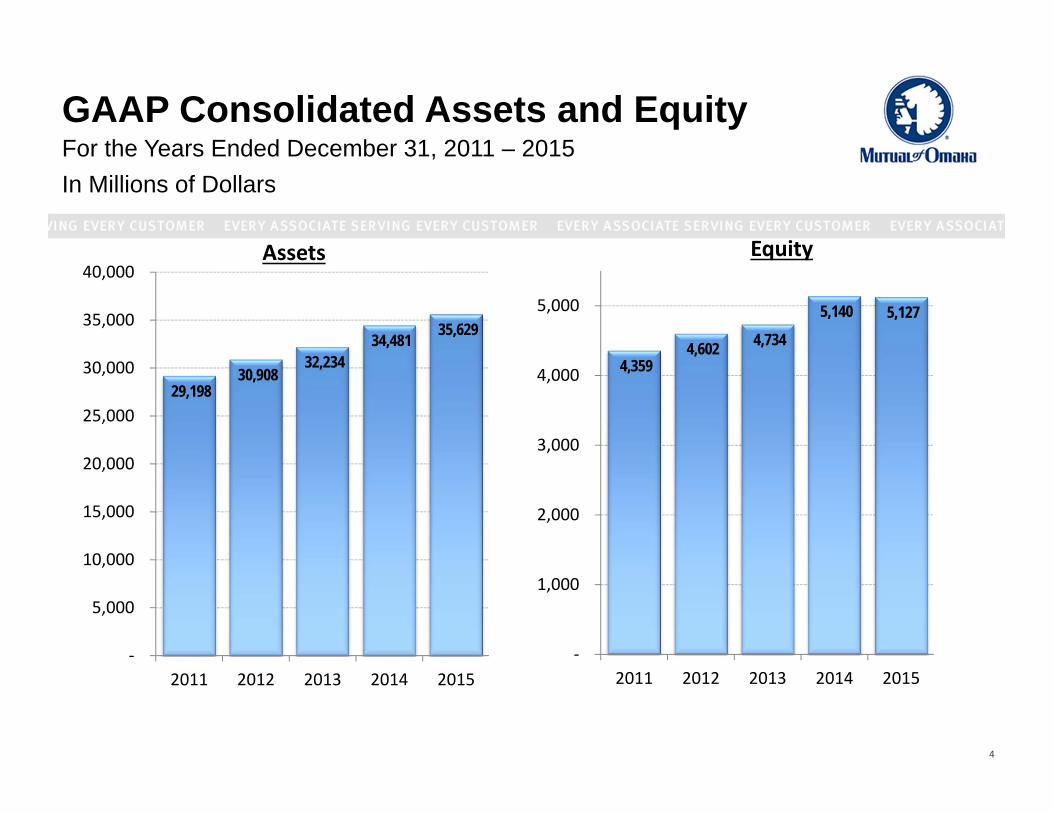

4,359 4,602 4,734

5,140 5,127

‐

1,000

2,000

3,000

4,000

5,000

2011 2012 2013 2014 2015

GAAP Consolidated Assets and EquityFor the Years Ended December 31, 2011 – 2015In Millions of Dollars

29,198 30,908

32,234 34,481 35,629

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2011 2012 2013 2014 2015

EquityAssets

4

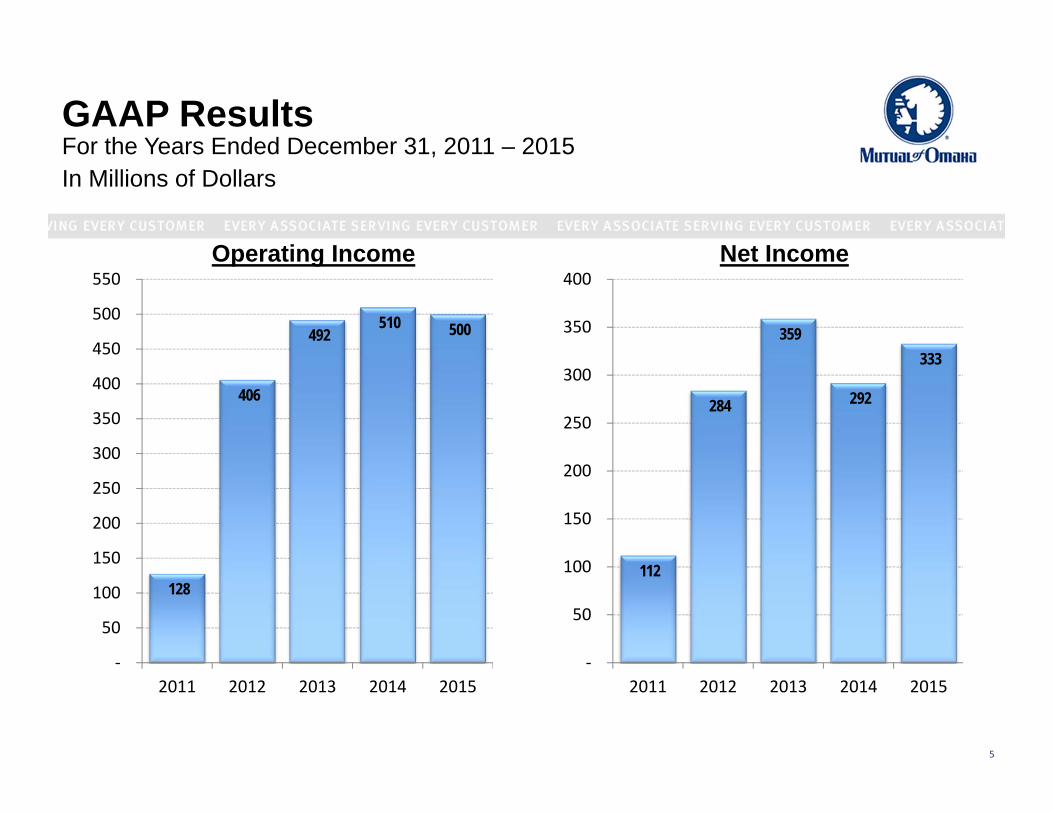

GAAP ResultsFor the Years Ended December 31, 2011 – 2015 In Millions of Dollars

128

406

492 510 500

‐

50

100

150

200

250

300

350

400

450

500

550

2011 2012 2013 2014 2015

Net IncomeOperating Income

5

112

284

359

292

333

‐

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015

Consolidated GAAP RevenueFor the Year Ended December 31, 2015

2015 Revenues $7.2 Billion

IFS Med supp40%

IFS LTC5%

IFS Life22%

IFS Annuity3%

IFS Other 3%

GBS Benefit Solutions

15%

GBS Retirement

Plans8%

Bank 3%

Corporate1%

6

Statutory Operating ResultsFor the Years Ended December 31, 2011 – 2015In Millions of Dollars

(138)

200 272

343 288

(150)

(100)

(50)

‐

50

100

150

200

250

300

350

2011 2012 2013 2014 2015

7

2,315 2,406

2,675 2,796 2,863

448% 450%

489% 484%476%

420%

440%

460%

480%

500%

520%

540%

560%

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

3,100

2011 2012 2013 2014 2015

(Per

cent

)

(In M

illio

ns o

f Dol

lars

)

Surplus Consolidated RBC

Statutory Surplus andConsolidated Risk-Based CapitalAs of December 31, 2011 – 2015

8

United of OmahaStatutory Results

9

United of OmahaStatutory Operating ResultsFor the Years Ended December 31, 2015 – 2012(In Millions of Dollars)

10

2013 201220142015

Premiums and Annuity Considerations $3,572 $2,713 $3,428 $3,466

Net Investment Income and IMR Amortization 829 722 701 692

Other Income 124 139 107 84

Total Income 4,525 3,574 4,236 4,242

Commissions, Operating Expenses

and Insurance Taxes 4,310 3,389 4,149 4,266

Net Gain (Loss) Before Federal Income Taxes 215 185 87 (24)

Federal Income Tax (Benefit) 38 2 1 (3)

Net Gain (Loss) From Operations 177 183 86 (21)

Net Realized Capital Losses (23) (19) (16) (10)

Net Gain (Loss) $ 154 $ 164 $ 70 $ (31)

Health $ 114 $ 115 $ 61 $ (57)

Life (109) (16) (44) (12)

Annuity 50 62 75 67

Other 161 24 (5) (22)

Net income (loss) before federal income taxes $ 216 $ 185 $ 87 $ (24)

11

20122015 2014 2013

United of OmahaStatutory Operating ResultsFor the Years Ended December 31, 2015 – 2012(In Millions of Dollars)

12

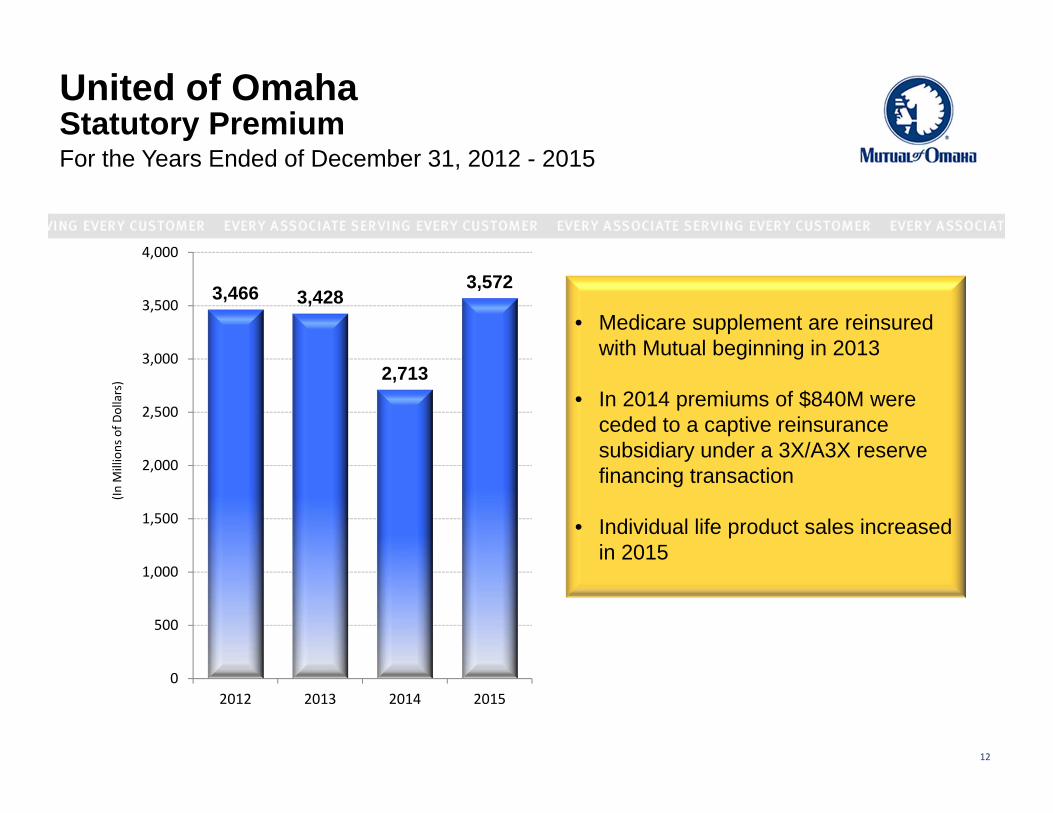

United of OmahaStatutory PremiumFor the Years Ended of December 31, 2012 - 2015

3,466 3,428

2,713

3,572

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2012 2013 2014 2015

(In M

illions of D

ollars)

• Medicare supplement are reinsured with Mutual beginning in 2013

• In 2014 premiums of $840M were ceded to a captive reinsurance subsidiary under a 3X/A3X reserve financing transaction

• Individual life product sales increased in 2015

1,036 1,027

1,227

1,423 1,442

‐

250

500

750

1,000

1,250

1,500

2011 2012 2013 2014 2015

15,738 16,698

18,122 18,787

19,623

‐

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

2011 2012 2013 2014 2015

SurplusAssets

13

United of OmahaStatutory Operating ResultsFor the Years Ended December 31, 2011 – 2015(In Millions of Dollars)

1,036 1,027 1,227

1,423 1,442

347% 333%382% 405% 397%

0%

100%

200%

300%

400%

500%

600%

700%

-

200

400

600

800

1,000

1,200

1,400

1,600

2011 2012 2013 2014 2015

(In M

illio

ns o

f Dol

lars

)

Surplus RBC

United of OmahaStatutory Surplus and Risk-Based CapitalFor the Years Ended December 31, 2011– 2015

14

Companion

15

CompanionStatutory Operating Results, Surplus & RBC For the Years Ending December 31, 2011 – 2015 (In Millions of Dollars)

1

10

2

(3)

(6)

($10)

($5)

$0

$5

$10

2011 2012 2013 2014 2015

Operating Results

16

66 59 47

57 51

485%

367%

244%

301%252%

0%

100%

200%

300%

400%

500%

600%

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2011 2012 2013 2014 2015

Surplus and Risk‐Based Capital

Surplus RBC

Related Documents