Annual Report 2010/2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Annual Report 2010/2011

www.lankem.lk

Lankem C

eylon P

LC | A

nnual Rep

ort 2010/2011

diverse strategic

solidfocuseddynamic

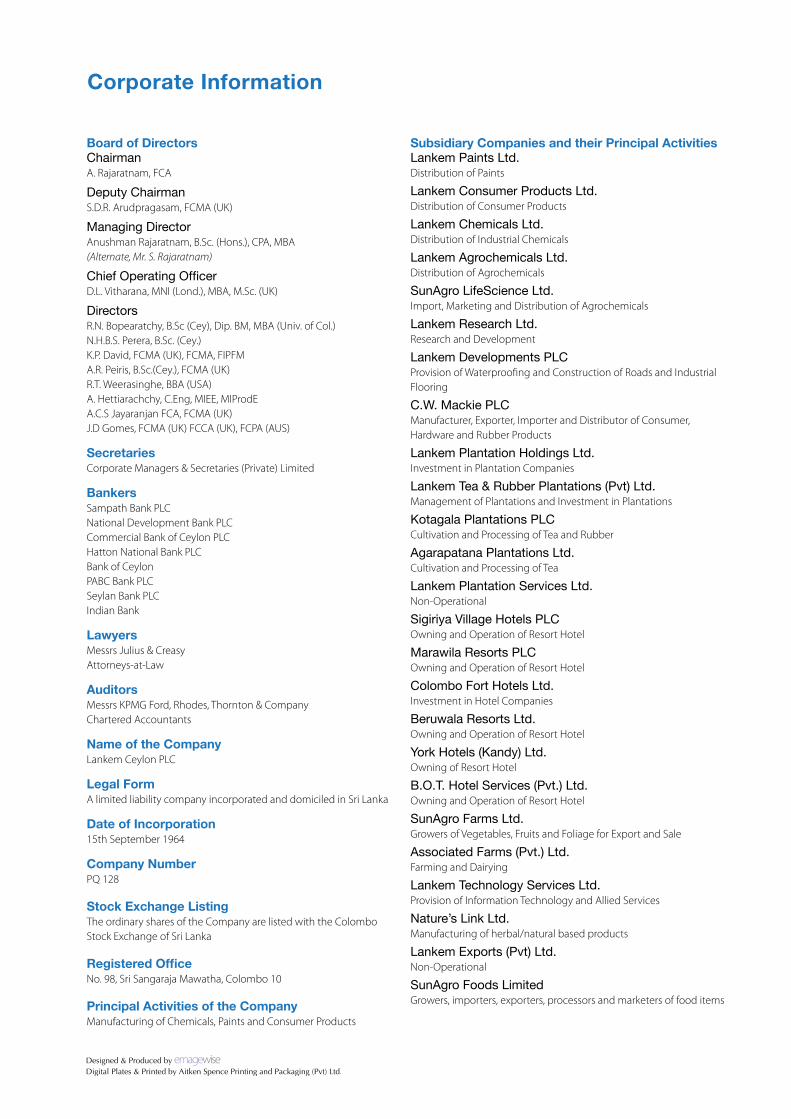

Corporate Information

Board of Directors ChairmanA. Rajaratnam, FCA

Deputy ChairmanS.D.R. Arudpragasam, FCMA (UK)

Managing DirectorAnushman Rajaratnam, B.Sc. (Hons.), CPA, MBA (Alternate, Mr. S. Rajaratnam)

Chief Operating OfficerD.L. Vitharana, MNI (Lond.), MBA, M.Sc. (UK)

DirectorsR.N. Bopearatchy, B.Sc (Cey), Dip. BM, MBA (Univ. of Col.) N.H.B.S. Perera, B.Sc. (Cey.)K.P. David, FCMA (UK), FCMA, FIPFMA.R. Peiris, B.Sc.(Cey.), FCMA (UK)R.T. Weerasinghe, BBA (USA)A. Hettiarachchy, C.Eng, MIEE, MIProdEA.C.S Jayaranjan FCA, FCMA (UK)J.D Gomes, FCMA (UK) FCCA (UK), FCPA (AUS)

SecretariesCorporate Managers & Secretaries (Private) Limited

BankersSampath Bank PLCNational Development Bank PLC Commercial Bank of Ceylon PLC Hatton National Bank PLCBank of CeylonPABC Bank PLCSeylan Bank PLCIndian Bank

LawyersMessrs Julius & Creasy Attorneys-at-Law

AuditorsMessrs KPMG Ford, Rhodes, Thornton & Company Chartered Accountants

Name of the Company Lankem Ceylon PLC

Legal FormA limited liability company incorporated and domiciled in Sri Lanka

Date of Incorporation 15th September 1964

Company NumberPQ 128

Stock Exchange ListingThe ordinary shares of the Company are listed with the Colombo Stock Exchange of Sri Lanka

Registered OfficeNo. 98, Sri Sangaraja Mawatha, Colombo 10

Principal Activities of the CompanyManufacturing of Chemicals, Paints and Consumer Products

Subsidiary Companies and their Principal Activities Lankem Paints Ltd.Distribution of Paints

Lankem Consumer Products Ltd. Distribution of Consumer Products

Lankem Chemicals Ltd. Distribution of Industrial Chemicals

Lankem Agrochemicals Ltd. Distribution of Agrochemicals

SunAgro LifeScience Ltd.Import, Marketing and Distribution of Agrochemicals

Lankem Research Ltd. Research and Development

Lankem Developments PLCProvision of Waterproofing and Construction of Roads and Industrial Flooring

C.W. Mackie PLCManufacturer, Exporter, Importer and Distributor of Consumer, Hardware and Rubber Products

Lankem Plantation Holdings Ltd. Investment in Plantation Companies

Lankem Tea & Rubber Plantations (Pvt) Ltd. Management of Plantations and Investment in Plantations

Kotagala Plantations PLCCultivation and Processing of Tea and Rubber

Agarapatana Plantations Ltd. Cultivation and Processing of Tea

Lankem Plantation Services Ltd. Non-Operational

Sigiriya Village Hotels PLCOwning and Operation of Resort Hotel

Marawila Resorts PLCOwning and Operation of Resort Hotel

Colombo Fort Hotels Ltd. Investment in Hotel Companies

Beruwala Resorts Ltd.Owning and Operation of Resort Hotel

York Hotels (Kandy) Ltd. Owning of Resort Hotel

B.O.T. Hotel Services (Pvt.) Ltd. Owning and Operation of Resort Hotel

SunAgro Farms Ltd.Growers of Vegetables, Fruits and Foliage for Export and Sale

Associated Farms (Pvt.) Ltd. Farming and Dairying

Lankem Technology Services Ltd.Provision of Information Technology and Allied Services

Nature’s Link Ltd.Manufacturing of herbal/natural based products

Lankem Exports (Pvt) Ltd. Non-Operational

SunAgro Foods LimitedGrowers, importers, exporters, processors and marketers of food items

Lankem Ceylon PLC | Annual Report 2010/2011 1

DIVERSED. STRATEGIC. SOLID. FOCUSED. DYNAMIC. THIS IS WHAT WE REPRESENT AND THIS IS WHO WEARE. THESE WORDS DEFINE OUR VALUES, OUR STRENGTHS AND THE SPIRIT THAT DRIVES US TOGREATER HEIGHTS EVERY DAY.

AS ONE OF THE NATION’S FASTEST GROWING DIVERSIFIED CONGLOMERATES, WE HAVE BEENBUILDING SUCCESS UPON SUCCESS IN EVERYSECTOR WE OPERATE, THUS GROWING VALUE FOR EVERY STAKEHOLDER WE PARTNER.

AGROCHEMICALS . PAINTS . BITUMEN . CHEMICALS . CONSUMER . LEISURE . PLANTATIONS . CONSTRUCTION . AGRICULTURE CROPS & LIVESTOCK PRODUCTION

2 Annual Report 2010/2011 | Lankem Ceylon PLC

ContentsFinancial Highlights ........................................... 4

Chairman’s Message ......................................... 5

Board of Directors ............................................. 8

Management Reports ...................................... 10

Financial Review .............................................. 30

Corporate Social Responsibility ....................... 35

Annual Report of the Board of Directors .......... 37

Corporate Governance ................................... 41

Risk Management Review ............................... 44

Audit Committee Report .................................. 46

Independent Auditors’ Report .......................... 50

Income Statement ........................................... 52

Balance Sheet ................................................. 53

Statement of Changes in Equity ....................... 54

Cash Flow Statement ...................................... 55

Notes to the Financial Statements ................... 57

Statement of Value Added ............................. 110

Share Information .......................................... 111

Ten Year Summary ......................................... 113

Notice of Meeting .......................................... 114

Form of Proxy ................................................ 115

Corporate Information - Inner Back Cover

Lankem Ceylon PLC | Annual Report 2010/2011 3

our business areasOUR BUSINESS AREAS ARE AGROCHEMICALS, PAINTS, BITUMINOUS PRODUCTS,

CHEMICALS, CONSUMER PRODUCTS. PLANTATIONS, LEISURE, CONSTRUCTION,

AGRICULTURE CROPS & LIVESTOCK PRODUCTION.

visionTo be the front runner in the chemical industry in Sri Lanka.

missionOur mission as a manufacturer and formulator of chemical products is to expand our business

through value addition and quality assurance with a commitment to society to continuously

improve management and performance in the areas of health, safety and the environment.

favourable rating outlookLong-and Short-term Corporate Credit Ratings of A- and P2 respectively assigned by RAM

Ratings (Lanka) Limited in August 2010.

4 Annual Report 2010/2011 | Lankem Ceylon PLC

Financial Highlights

Revenue

Rs. 23,030 Mn.

Shareholders’ Funds

Rs. 3,260 Mn.

Profit Before Tax

Rs. 2,109 Mn.

Net Assets per Share

Rs. 135.84

0

2,000

4,000

6,000

8,000

10,000

Property, Plant & Equipment (Rs. Mn)

2005/06

Company

2006/07 2007/08 2008/09 2009/10 2010/11

Group

240

295

315

329

481

551

4,24

5 4,93

4

5,26

3 5,81

2 6,88

5

8,27

4

0

500

1,000

1,500

2,000

2,500

Profit Before Tax (Rs. Mn)

2005/06

Company

2006/07 2007/08 2008/09 2009/10 2010/11

Group

199

136

180 28

6

317

530

376 50

3

918

257

804

2,10

9

0

3,000

6,000

9,000

12,000

15,000

Current Assets & Liabilities (Rs. Mn.)

2005/06

Group Current Liabilities

2006/07 2007/08 2008/09 2009/10 2010/11

Group Current AssetsCompany Current Liabilities Company Current Assets

1,95

82,

5241,56

51,

634

1,75

91,

776

3,29

1

3,10

62,

067

2,55

9

1,08

7

1,41

41,

268 5,

631

7,71

5

2,20

91,

878

3,64

63,

187

4,98

95,

036

3,59

53,

332

958

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Shareholder Funds (Rs. Mn)

2005/06

Company

2006/07 2007/08 2008/09 2009/10 2010/11

Group

854

916

1,05

9

1,15

4 1,36

3

2,12

2

251 71

6 1,07

2

1,17

7

1,81

3

3,26

0

0

30

60

90

120

150

Net Assets per Share (Rs.)

2005/06

Company

2006/07 2007/08 2008/09 2009/10 2010/11

Group

47.4

3

50.8

8

50.4

4

54.9

5

64.9

3

88.4

3

13.9

3

39.7

5 51.0

5

56.0

4

86.3

3

135.

84

0

5,000

10,000

15,000

20,000

25,000

Revenue (Rs. Mn)

2005/06

Company

2006/07 2007/08 2008/09 2009/10 2010/11

Group

2,60

2

3,02

7

3,25

2

3,93

8

3,58

9

4,90

46,78

5

7,93

7 9,45

2

9,75

2

11,0

46

23,0

30

Lankem Ceylon PLC | Annual Report 2010/2011 5

It gives me great pleasure to present on behalf of the Board of

Directors the Annual Report and the audited financial statements

of Lankem Ceylon PLC and its subsidiaries for the year ended

31st March 2011.

Free from the burden of an ethnic conflict that has dogged the

country for the last thirty years the Sri Lankan economy has

improved markedly over that of the past financial year. Low levels

of inflation and interest rates have helped the economy post an

economic growth rate of 8%. The Government has also placed

a heavy emphasis on improving the infrastructure available for

businesses in the country. This investment in infrastructure has

had the effect of spurring economic growth. The fiscal policies

adopted by Parliament during the financial year will bring down

the levels of taxation that had been a burden to corporate

entities.

In this buoyant economic environment, the performance of the

Company and its subsidiaries has been exceptional. Turnover

at Group level rose to Rs. 23 Billion and the profitability of the

Group rose to Rs. 2.1 Billion before tax. At Company level,

turnover was Rs.4.9 Billion and profitability was Rs. 575.2 Million

after taxation. These financial performances were all time highs

and reflects the progress and the hard work of all the employees

across the Group.

ReviewAll the operating divisions of the Company have shown strong

growth for the year under review. The Financial year 2010/2011

was a landmark year for the crop protection unit as it moved to

it’s new operating hub at Pannala in the Kurunegala district. This

new operating location will not only serve as its factory for the

formulation and packing of crop protection chemicals but will

also serve as a processing site for the seeds division. Extremely

favorable Agro climatic conditions helped the crop protection

division record its highest levels of sales ever. The Division remains

the market leader in this segment of business. The Company,

continues its commitment to being the provider of choice for

crop protection chemicals by investing heavily in research and

Chairman’s Message

product development activities with the collaboration of our

foreign partners. It is heartening to note that there are many

new chemicals in the pipeline that the Company plans to obtain

regulatory approval during the course of the next financial year.

The seeds division continues to grow at a very robust pace. We

now play an active role not only in the seed paddy market but

also in the sale of hybrid vegetable seeds. In order to further

expand our presence in the seed paddy market, the division

plans to open two new seed paddy collecting and distributing

points in the North Central and Uva provinces. Our collaboration

with Monsanto Corporation of the United States have helped

us to penetrate in to the market for maize seeds. Following the

successful launch of the Company’s range of foliar fertilizers and

micro-nutrients in the previous financial year, the Company has

begun to market a range of NPK fertilizer mixes to the paddy

cultivation sector. The Company will move very cautiously in the

fertilizer market on account of the risks involved in collecting

subsidies on time from the State institutions. Our presence in

this sector is essential to offer the full range of agrochemical

inputs needed by the farmer.

A major upturn in the construction industry has helped the Paints

sector perform admirably during the year. Aided by a growth in

institutional sales, especially to the hospitality segment of the

market, volume sales have grown by nearly 20% year on year.

During the year, the Company has partnered with ALCEA of

Italy to offer a range of water based wood care products to

the Sri Lankan market. The Company strives to offer the most

environmentally friendly coating solutions to the local market.

The Company is now actively seeking opportunities to expand

its operations regionally.

With a heavy emphasis being placed by the Government on

infrastructure development, the prospects for the bitumen

division are bright. Lankem remains the only public company

actively involved in this sector. The Company remains the

preferred supplier for many of the new road construction projects

taking place across the country. Over the next few years, the

6 Annual Report 2010/2011 | Lankem Ceylon PLC

Company plans to introduce polymer modified bitumen to the

local market. The new product will improve the durability and

ease of laying new road surfaces.

The increased levels of economic activity have helped ensure

that the industrial chemicals division maintains a steady growth

in the year under review. With the Government encouraging

industrialization and with the new chemicals from their foreign

principals in line to be introduced locally, I am confident that the

prospects for the division are excellent.

I am pleased to report that the hitherto loss sustained by the

consumer division has been reduced compared to the last

financial year. The Division has taken steps to rationalize the

range of products that it manufactures and distributes. By

narrowing the focus to a few products, the Company is able to

target its marketing efforts more effectively in order to ensure a

renewed demand for its products.

The strength of the Group’s performance was not limited only to

the core operations of the Company but also to the many other

entities within the Group. The financial results of C.W. Mackie

PLC was consolidated for the first time and is for a period of 15

months on account of the need to bring its financial year in line

with that of Lankem Ceylon PLC. The profitability of C. W. Mackie

PLC for the period under review grew to Rs. 223.4 Million after

taxation. C.W. Mackie PLC, with its mix of operations in FMCG,

Industrial products, Sugar Trading and Rubber exports provides

the Group with many opportunities for growth.

During the course of the financial year, the Group acquired a

controlling interest of the company B.O.T Hotels Services

(Private) Limited, which owns the Weligama Bay Beach Hotel,

a sixty roomed property located on the Southern coast of Sri

Lanka. The Group intends to renovate and refurbish this property

comprehensively. The Group’s three properties in the leisure

industry have all returned to profitability. Sigiriya Village Hotels

PLC and Marawilla Resorts PLC have both raised additional

equity funding in order to upgrade the facilities of the respective

hotels. These refurbishments will be completed on time for the

coming winter season. The prospects for the tourism industry

are bright and the Group will actively look to increase the number

of rooms to its inventory.

Our Plantation sector had an excellent year made possible by

the record Tea crops and significantly increased prices for both

Tea and Rubber. Rubber production was less than what was

produced in the previous year due to the unusual wet weather

which reduced the number of tapping days. However, record

prices offered for both crepe and RSS rubber improved the

profits earned over that achieved in the previous year. The

island’s tea crop for 2010 was an all time record high in spite of

the adverse weather conditions.

The new Collective Agreement covering workers remuneration

which was negotiated in June this year will dampen profits and

have an unfavourable impact on the future of the tea industry,

unless there is a corresponding effort by Trade Unions to co-

operate and improve worker productivity in the plantation

industry.

We continue to invest heavily on capital expenditure and provide

all the agricultural inputs necessary for improving yields. It is

noteworthy that Kotagala Plantations PLC had the distinction

of once again surpassing the highest yield to establish a new

benchmark of 2,182 Kilograms per hectare. In a move to further

diversify its crops, Kotagala Plantations PLC has undertaken to

plant 1000 hectares of oil palm on previously low yielding rubber

lands. It is hoped that with this diversification the Company will

enhance its profitability in the years ahead.

This year has seen an excellent financial performance from

Lankem Ceylon PLC and its subsidiaries. The Company

endeavours to meet the aspirations of all our consumers. We

will continue to strengthen the Company in the markets that

we are present now and place heavy emphasis on achieving a

Chairman’s Message

Lankem Ceylon PLC | Annual Report 2010/2011 7

regional presence in order to continue improving the corporate

profitability.

During the year, the Company paid an interim dividend of Rs.

1.00 per share and the Directors have recommended a final

dividend of Rs. 1.50 per share to all its shareholders.

ConclusionI would like to take this opportunity to thank our many

stakeholders for their continued support and also for their faith

in our Group. It is this unwavering support that allows LANKEM

to remain a premium brand in Sri Lanka. I thank my colleagues

on the board for their valuable support and counsel at all times.

A.Rajaratnam

Chairman

23rd August 2011

8 Annual Report 2010/2011 | Lankem Ceylon PLC

A. Rajaratnam [FCA]

ChairmanMr.A. Rajaratnam joined the Board in 1990 and was appointed

Chairman in the year 2003. He also serves as Chairman on the

Boards of several subsidiaries of the Lankem Group and holds

other Directorships within The Colombo Fort Land & Building

Group.

S.D.R. Arudpragasam [FCMA - UK]

Deputy ChairmanMr.S.D.R. Arudpragasam is a Chartered Management

Accountant. He was appointed to the Board in 1989 and was

appointed as Deputy Chairman in 1990. He also holds the

position of Managing Director of E.B. Creasy & Company PLC

in addition to serving on the Boards of other Companies in The

Colombo Fort Land and Building Group.

Anushman Rajaratnam [B.Sc (Hons.), CPA, MBA] Managing DirectorMr.Anushman Rajaratnam was appointed to the Board as

Deputy Managing Director in the year 2005 and was appointed

Managing Director in April 2009. He has spent several years

working overseas as a Consultant for a leading Accountancy

Firm. He also serves on the Boards of several subsidiaries of the

Lankem Group.

D.L Vitharana [MNI (Lond), MBA, M.Sc. (UK)]

Chief Operating OfficerMr.D.L. Vitharana was appointed to the Board in 2005. He joined

Lankem Ceylon PLC in 1997 and has headed the Lankem Agro

Cluster since 1999. He is currently the Chief Operating Officer of

Lankem Ceylon PLC and also serves on the Boards of several

subsidiaries of the Lankem Group.

R.N. Bopearatchy [B.Sc. (Cey), Dip. BM., MBA (Univ. of Col)]

DirectorMr.R.N. Bopearatchy was appointed to the Board in 1996. He has

considerable expertise in product development, manufacturing

and marketing of pesticides, pharmaceuticals and consumer

products. Soon after graduation he was employed in Research

in the Plant Pathology Division of the Tea Research Institute and

subsequently joined Chemical Industries Colombo Ltd, and

Board of Directors

was appointed to its Board. He also served on the Boards of

Crop Management Services (Pvt) Ltd., the managing agents

for Mathurata Plantations Ltd., CIC Fertilizers Ltd and Cisco

Speciality Packaging (Pvt) Ltd. He has been a former Chairman

of the Pesticide Association of Sri Lanka and the Toxicological

Society of Sri Lanka and is now the Chairman of the International

Mosquito Spiral Manufacturers Association (IMSMA). Mr.R.N.

Bopearatchy currently holds several other Directorships within

The Colombo Fort Land & Building Group.

N.H.B.S. Perera [B.Sc. (Cey)]

DirectorMr.N.H.B.S. Perera joined the Board in 1999. He is a former

Chairman of Harrisons (Colombo) Ltd, and the Pesticides

Association of Sri Lanka. He has held office as Deputy Chairman

of the Planters Association of Sri Lanka and has functioned as

Group Director of The Maharaja Organization Ltd. Mr.Perera

has also served as Director on the Board of Harrison Lister

(Colombo) Ltd, and several plantation company Boards such

as Aislaby Estates Ltd, Attampettia Estates Ltd., Newburgh

Estates Ltd, Kinross Estates Ltd, and Lunuwa Plantations Ltd,

prior to nationalisation. He presently serves on the Boards of

The Colombo Fort Land & Building Company PLC and Lankem

Tea & Rubber Plantations (Pvt) Ltd. Mr.Perera has considerable

expertise in the field of developing and marketing Agri Chemicals,

managing of plantation companies, manufacture and distribution,

shipping and warehousing.

K.P. David [FCMA-UK, FCMA, FIPFM]

DirectorMr.K.P. David was appointed to the Board in 2007. Having

commenced his career in the Banking sector, he joined the Parent

Company E.B.Creasy & Company PLC as Group Accountant in

1993. He also serves on the Boards of several subsidiaries of

the Lankem Group.

A.R. Peiris [B.Sc. (Cey), FCMA-UK]

DirectorMr.A.R. Peiris was appointed to the Board in the year 2007.

He has served the Petroleum Corporation for 10 years in

Technical, Planning & Finance Divisions and at the time he

left the Corporation in 1979, he was the Head of the Refinery

Finance Division. Thereafter, he joined National Development

Lankem Ceylon PLC | Annual Report 2010/2011 9

Bank PLC where he held several senior positions for 24 years.

He has held Directorships in several reputed public listed and

unlisted companies. Mr.Peiris also holds Directorships in several

companies within the Lankem Group.

R.T. Weerasinghe [BBA - USA]

DirectorMr.R.T. Weerasinghe was appointed to the Board in April 2009.

He joined Darley Butler & Company Ltd, in the year 1994 as a

Trainee Product Manager and was seconded to Lankem Ceylon

PLC as the Marketing Manager of the Consumer Division in

1998. He was promoted as General Manager of the Consumer

Division in 2005 and was also appointed as General Manager of

the Paints Division. In addition he was appointed as the Head

of the Industrial Chemicals Division in 2009. Mr.Weerasinghe

possess expertise in the fields of Marketing and Management.

Mr.Weerasinghe also serves on the Boards of certain subsidiaries

of Lankem Ceylon PLC.

A. Hettiarachchy [C.Eng, MIEE, MIProdE]

DirectorMr.A. Hettiarachchy was appointed to the Board as an

Independent Non-Executive Director in April 2010. He is a

Chartered Engineer and a Member of the Institution of Engineering

and Technology. He serves on the Boards of National Science

Foundation and as Chairman on the Boards of ISB Services

Limited, ISB Environmental Services Limited, and ISB Technical

Services Limited. He has served on the Board of Hayleys PLC

and functioned as Managing Director on the Boards of Haycarb

PLC, Recogen Limited and Puritas Limited and also served on

several other subsidiaries of Haycarb PLC and Hayleys PLC both

in Sri Lanka and Overseas. He was also a Board Member of The

Sri Lanka Institute of Nanotechnology. Member of the National

Nano Committee and a member of several advisory Boards of the

NSF. Mr.Hettiarachchy possess expertise in the fields of Process

Design, Construction and Commissioning; Instrumentation and

Control-Design, Installation and Commissioning; Mechanical

Engineering, Thermal and Electrical Energy- Generation and

Storage and Nano Technology.

A.C.S. Jayaranjan [FCA, FCMA-UK]

DirectorMr.A.C.S. Jayaranjan was appointed to the Board as an

Independent Non-Executive Director in June 2010. He started

his career as a professional at KPMG Ford Rhodes Thornton &

Company. Thereafter he has been working for thirty five years in

the commercial and industrial sectors at senior managerial level.

He was the Chief Accountant at James Finlay & Company PLC

and Deputy Chief Executive Officer/Executive Director Shaw

Wallace & Hedges PLC. Mr. Jayaranjan then joined as the Group

Finance Director of Pership Group and later joined John KeeIls

Holdings PLC, as Senior Vice President, Head of Learning &

Development. His experience covers diverse areas in commerce

and industry.

Mr. Jayaranjan is a Fellow Member of the Institute of Chartered

Accountants of Sri Lanka, and a Fellow Member of the Chartered

Institute of Management Accountants UK. He is an external

examiner/lecturer at the Faculty of Graduate Studies, University

of Colombo.

J.D. Gomes [FCMA (UK), FCCA (UK,) FCPA (AUS)]

DirectorMr. Dian Gomes was appointed to the Board as an Independent

Non-Executive Director in June 2010. Mr. Gomes is a Group

Director of MAS Holdings and the Managing Director of MAS

Intimates (Private) Limited. In addition to his role as Managing

Director for the Intimates Cluster, Mr. Gomes is also the head of

Human Resources, Corporate Communications, Branding and

CSR for the MAS Holdings Group.

He is a Fellow member of the Chartered Institute of Management

Accountants (UK), the Association of Chartered Certified

Accountants (UK) and Certified Practicing Accountants

(Australia). A Past President of the CIMA — Sri Lanka Division

(2001/2002) and the Sri Lanka Amateur Boxing Association

(2004 to 2009), Mr. Gomes is presently the Vice President of the

National Olympic Committee of Sri Lanka.

10 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 11

management report

growth

As one of the nation’s strongest

and most diversified conglomerates we

see our ability to innovate as the most

powerful tool in overcoming industry

challenges.

12 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 13

agri inputsThe division formulates

and distributes crop protection solutions across the country.

We continue to partner with many leading global agrochemical

companies to develop new crop protection solutions.

The seed business has shown a rapid growth in market share

in both seed paddy and vegetable seeds. The seed division has

introduced 42 seed varieties and Lankem has tied up with giants

such as Monsanto (USA), Kaneko seeds (Japan), Singenta,

Chiathai (Thailand), Hollar seeds (USA) and Vickima seeds

(Denmark), to market their hybrid ranges of seeds.

Last year the Company ventured into the fertilizer sector and

operates in the market segments of foliar fertilizer, fertilizer

mixtures, straight fertilizer and micro-nutrients.

Agrochemicals has predominantly been the core business of Lankem, and this sector has been in operation for more than four decades. Today the Company is the undisputed market leader.

We have lived up to the slogan of “Farmer’s Friend” and it remains the retailer of choice for a majority of the cuntry’s farmers.

Lankem has been accredited with the ISO 9001:2008 for Quality

Management Systems, ISO 14001:2004 for Environmental

Management Systems and OSHAS 18001:2007 Certification for

Occupational Health and Safety at the Company’s production

facility.

The quality control process at Lankem’s Agro Chemical Factory in Pannala.

growth

14 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 15

paints

Lankem Paints has also partnered with Akzo Nobel, Netherlands

- the largest auto refinish company in the world, to distribute its

products in Sri Lanka.

The Paint division operates in a very competitive market. The

division has shown remarkable resilience and we have maintained

our market share even in this challenging environment.

Lankem Paints division continuously improves and monitors its

pricing strategies, distribution channels and promotional mix, in

order to improve and expand its market share. We also continue

to improve product quality in order to ensure that our products

meet global standards.

The Paint sector also includes the C. W. Mackie PLC operations

of import and sale of ‘Hempel’ Marine Paints & Protective

Coatings.

Lankem Paints Limited is one of the pioneer coating manufacturers in Sri Lanka. The division commenced operations in 1984. The Company offers a range of quality products under the international brand name ‘Robbialac’ and we are the first and only paint company in Sri Lanka to be accredited with ISO 9001: 2008 Quality Management Systems, ISO 14001: 2004 Environmental Management Systems and SLS Product Quality.

Our operations include Decorative Coating, Auto Refinish,

Wood Coating, Epoxy Coating, NC-based Coating and Epoxy

Adhesives. We also operate six Colour Studios and over 150

“Pata” Shops across the island.

The Company’s second brand ‘Rolac’ was introduced in 2010,

to cater to a more price concious market segment. We have

also partnered with ALCEA Italy, to offer water-based Wood Care

Solutions to the Sri Lankan market.

Lankem Paints Limited is one of the pioneer

coating manufacturers in Sri Lanka.

Lankem Paints Ltd. manufactures “Robbialac” Paints at our factory in Kanuwana, Ja-ela.

growth

16 Annual Report 2010/2011 | Lankem Ceylon PLC

chemicals

Lankem Ceylon PLC | Annual Report 2010/2011 17

chemicals Lankem Chemicals Division comprises of three sections -

Industrial Chemicals, Thinners, Food and

Feed Ingredients.

Lankem’s Chemicals Division comprises of three sectors: Industrial Chemicals, Thinners, Food and Feed Ingredients. The Industrial section imports and trades solvents, rubber chemicals, detergent raw materials and pigments while the Thinner section manufactures thinners and related products. The Food and Feed Ingredient section launched during the year, imports and trades food and feed ingredients.

The division imports materials from Singapore, Europe, India, China, Korea, USA, Middle East, Vietnam and Taiwan.

Our key emphasis is to provide consistently high quality products

to our clientele. The Company has recently invested in a semi

automated manufacturing plant conforming to the international

standards, which will come into operation by the end of 2011.

The division has recently embarked on a strategy of product

diversification, intended to supply a greater variety of products

to our target customer segment.

Lankem Chemicals deals in a wide variety of chemicals and in food and feed ingredients.

growth

18 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 19

bitumenThe Bitumen Division

remains the largest supplier of Emulsion and Road Surfacing

Bitumen in the country.

The Bitumen Division remains the largest supplier of emulsion and road surfacing bitumen in the country. Sri Lanka has over 110,000 km of paved road, which are maintained by the Government. In view of the Government’s current emphasis on the rehabilitation and reconstruction of the existing road network, it can be expected that this industry will record robust growth in the future.

The Bitumen Division strives to introduce innovative products

into its portfolio and continues to maintain very high quality of

manufactured products.

Lankem is the only public Company actively involve in this

sector. Lankem remains the preferred supplier for many of the

road construction projects across the country.

Bituminous products supplied by Lankem Bitumen Division are used in road and highway construction across the island.

growth

20 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 21

consumerLankem Consumer

Division produces and distributes detergent

powder, detergent liquid, laundry

soap, household cleansing products,

dry cell batteries, pharmaceutical

products and personal care products.

Lankem’s Consumer Division produces and distributes detergent powder, detergent liquid, laundry soap, household cleaning products, dry cell batteries, pharmaceutical products and personal care products. Our key target consumer segments are households from both urban and rural areas.

The Consumer sector also includes the consumer and domestic

trading operations of C.W.Mackie PLC , which has local and

global flagship brands such as Sunquick, Ovaltine, Star Brand

Essence and Coloring, Ocean Fresh Tuna and the Scan products

range.

The Sunquick bottling plant of C.W. Mackie PLC, at Munagama, Horana

growth

22 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 23

Comprises of three business units. Core operations in Road Construction,

Water Proofing, Industrial Flooring, Sports Courts Flooring, Epoxy Flooring, Termite

& General Pest Control.

Pest ManagementThe Pest Management division is engaged in termite and general pest control. Lankem Ceylon is a pioneer in the termite control industry in Sri Lanka, holding a market leader’s position in the industry for over two decades.

This division’s main product “Biflex” is an established termiticide

control solution.

Despite the challenges in the local construction industry, the Pest

Management division continued to successfully market its highly

effective pest control solutions to Corporate and Institutional

customers.

construction & pest

management

ConstructionThe Construction division engages in Road Construction, Waterproofing, Industrial Flooring, Sports Courts Flooring, Epoxy Flooring and undertakes Painting.

Lankem’s Construction division is poised to perform better with variety of products and services.

growth

24 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 25

plantationsLankem Ceylon PLC owns and manages

two regional plantation companies - Kotagala

Plantations PLC and Agarapatana

Plantations Ltd.

Kotagala Plantations PLC cultivates a mixture of high grown tea,

low grown tea and rubber.

Agarapatana Plantations Ltd cultivates high grown tea in

Agarapatana and Uva tea growing districts.

Our plantation sector had an excellent year, made possible by

the record Tea crops and significantly increased prices for Tea

and Rubber.

Lankem Ceylon PLC manages two plantation companies engaged in tea and rubber.

growth

26 Annual Report 2010/2011 | Lankem Ceylon PLC

Lankem Ceylon PLC | Annual Report 2010/2011 27

The Palms Hotel - Moragalla, Beruwala

leisureThe Company has

made investments in four resort hotels on

the west coast and cultural triangle - Club Palm Bay, The Palms, Bay Beach & Sigiriya

Village.

The Leisure sector portfolio includes The Club Palm Bay operated by Marawila Resorts PLC, Sigiriya Village operated by Sigiriya Village Hotels PLC and The Palms Hotel operated by Beruwala Resorts Ltd.

Latest addition to our portfolio was Bay Beach Hotel in Weligama,

which is owned by B.O.T. Hotel Services (Pvt) Ltd. This is a sixty

roomed property located on the Sourthern coast of Sri Lanka.

All hotels recorded improved performance during the year under

review.

growth

28 Annual Report 2010/2011 | Lankem Ceylon PLC

agriculture, crop and livestock

production

Lankem Ceylon PLC | Annual Report 2010/2011 29

agriculture, crop and livestock

production

growth

The Company has diversified into

agriculture, crop and livestock production.

The company has diversified into agricultural crops and livestock production through its subsidiary companies: SunAgro Farms Ltd and Associated Farms (Pvt) Ltd.

SunAgro Farms Ltd. pioneered asparagus cultivation in Sri Lanka

and plans are underway to commence commercial cultivation.

The asparagus farm is located in Madurankuliya, Puttalam.

Associated Farms (Pvt) Ltd. is primarily involved in livestock

production.

This sector is in it’s early stages of operation.

The Asparagus Nursery section at our Madurankuliya Farm.

30 Annual Report 2010/2011 | Lankem Ceylon PLC

0

5

10

15

20

25

Group & Company Revenue (Rs. Bn)

2005/06

Group

2006/07 2007/08 2008/09 2009/10 2010/11

Company

OverviewThe year 2010/11 was a milestone for Lankem Ceylon PLC

Group which recorded the highest ever Revenue and Profits in

the long history of Lankem Ceylon PLC Group. In the backdrop

of improved macro-economic environment of the country, all the

business sectors of Lankem Ceylon PLC Group have shown

commendable results during the financial year 2010/11.

However it should be noted that the above financial performance

includes 15 months results of C.W. Mackie PLC which is

consolidated for the first time.

Revenue AnalysisLankem Ceylon PLC Group reported a Consolidated Revenue of

Rs. 23.03 Bn. for the year under review compared to a Revenue

of Rs.11.05 Bn. during the previous year. This resulted in the

growth of Group Revenue by 108.50% year-on-year and an

average growth rate of 27.69% over the last five years.

Financial Review

0

2

4

6

8

10

Group Revenue (Quarterly) (Rs. Bn)

Q1 Q2 Q3 Q4

2010/112007/08 2008/09 2009/10

Segmental Contribution to Group Revenue 2010/11

Consumer

Hardware

Hotel

Plantations

Chemicals

17%

24%

39%

2%

17%

The main contributors to the Group Revenue are, the Plantation

sector followed by Hardware, Chemical and Consumer sectors.

The Revenue attributable to the Company was Rs. 4.90 Bn.

compared to Rs. 3.59 Bn. achieved during the previous year. This

represents Company Revenue growth of year-on-year basis by

36.63% and average growth of 13.5 % over the last five years.

The Tea and Rubber commodities experienced high prices

during the year which resulted in the plantation companies

recording a strong Group Revenue. However the plantation

crops were hampered by adverse weather conditions which

prevailed throughout the country during the year. Consequently

the plantation sector Revenue grew by 53.61% from Rs. 6.43 Bn

to Rs. 9.88 Bn, which accounts for 39% of the Group Revenue.

Lankem Ceylon PLC | Annual Report 2010/2011 31

0

2

4

6

8

10

Segmental Revenue Performance (Rs. Bn)

Plantations

2010

Hardware Chemicals Consumer Hotel

2011

9,75

2

The Hardware sector accounts for 24% of the Group Revenue

as opposed to 18% contribution made in the previous financial

year. The improvement in the contribution from this sector was

mainly due to strong demand for construction and hardware

related products with the boom in construction activities in

the Island. The Hardware sector also showed a remarkable

performance with its strong market presence in the Northern

and Eastern regions.

The Chemical sector also witnessed a growth of 37.68%,

recording a Revenue of Rs. 4.34 Bn. compared to the previous

year Revenue of Rs. 3.15 Bn. The improved contribution from

this sector was mainly due to strong demand for crop protection

and solution products and chemical products. The Agri-inputs

cluster experienced favourable climatic conditions and aslo was

able to penetrate and gain market position in the Northern and

Eastern regions by extending the distribution network.

ProfitabilityThe Group has made an outstanding performance in terms of

Profit before tax and Profit after tax. The Profit before tax of

Rs. 2,108.56 Mn. during the year under review compared to the

previous year’s Profit before tax of Rs. 803.58 Mn. represents an

increase of 162.40% year-on-year. The average growth rate of

Profit before tax was 41.19% over the last five years.

The Profit after tax for the financial year grew by 241.20%

on a year-on-year basis to Rs. 1,871.75 Mn. as opposed to

Rs. 548.58 Mn. during the previous year. The Profit after tax for

the Group grew by 42.80% on average over the last five years.

The Profit before tax of the Company for the year under review

rose to Rs. 530.25 Mn. from Rs. 317.36 Mn. in the previous year

representing a growth of 67.08% year-on-year and an average

growth rate of 21.65% over the last five years.

The Profit after tax of the Company grew by 174.87% to

Rs. 575.20 Mn. compared to Rs. 209.26 Mn. during the previous

year.

The biggest contributors to the Group’s profitability are the

Plantations and Chemicals segments with contributions of 52%

and 32% respectively.

0

500

1000

1500

2000

2500

Group & Company Profit Before Tax (Rs. Mn)

2005/06

Group

2006/07 2007/08 2008/09 2009/10 2010/11

Company

The Consumer segment recorded strong growth during the

financial year with excellent performance of domestic trading

activities. The Sri Lankan Economy grew by 8% which boosted

consumer confidence and disposable income which contributed

to the consumer segment performance during the financial year.

The Consumer segment having renowned international and local

brands under C.W.Mackie PLC posted a Group Revenue of

Rs. 4.16 Bn. during the financial year.

32 Annual Report 2010/2011 | Lankem Ceylon PLC

Financial Review

Finance CostsDuring the financial year under review the Group saw remarkable

improvement in its interest cover as the ratio improved from 3.73

times to 5.66 times. This was mainly due to improved Operating

profits of the Group with the associated fall in market interest

rates as a result of an improved macro environment.

0

100

200

300

400

500

Finance Cost and Interest Cover Ratio

2006/07

Finance Cost

2007/08 2008/09 2009/10 2010/11

Interest Cover

1.00

2.00

3.00

4.00

5.00

6.00

7.00Rs. Mn. Times

Financial and Liquidity PositionNon-Current Assets PositionThe total non-current assets grew by 15.90% from Rs. 8.35

Bn. to Rs. 9.68 Bn. during the year under review due to the

capital expenditure incurred by the Group. The Property, Plant &

Working CapitalThe working capital investment of the Group significantly

improved during the year under review due to aggressive

working capital management, which resulted in an improvement

in the cash and the trade receivable balances of the Group. The

Group working capital investment increased to Rs. 2,084.73

Mn. from previous year’s Rs. 47.41 Mn. Hence the current ratio

improved from 1.01 to 1.37, whilst quick asset ratio improved

from 0.67 to 0.94.

0

2,000

4,000

6,000

8,000

10,000

Non-Current Assets (Rs. Mn)

2005/06

PPE

2006/07 2007/08 2008/09 2009/10 2010/11

Others

0

500

1000

1500

2000

Group & Company Profit After Tax (Rs. Mn)

2005/06

Group

2006/07 2007/08 2008/09 2009/10 2010/11

Company

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Working Capital and Liquidity Position

2006/072005/06

Current Assets

2007/08 2008/09 2009/10 2010/11

Current Ratio

Current Liabilities Quick Asset Ratio

Rs. Mn. Times

Equipment for the Group which is the major component of non-

current assets amounted to Rs.8.27 Bn. as at 31st March 2011.

Lankem Ceylon PLC | Annual Report 2010/2011 33

Capital Structure 2010/11

Debt

Equity

54% 46%

Capital StructureThe Group’s Debt as a percentage of Total Capital is 46% whilst

the Equity component amounted to 54% during the year under

review which was a significant improvement compared to the

previous years restated debt and equity percentages of 55%

and 45% respectively.

During the financial year the Company raised additional funds by

way of a rights issue of 3 million ordinary shares at a price of Rs.85

per share for a total consideration of Rs. 255 Mn. The purpose of

this issue was to meet the working capital requirements.

During the financial year the Group obtained additional interest

bearing long term and short term borrowings by way of term

loans, finance leases and debentures amounting to Rs.1.90 Bn.,

whilst it settled Rs.1.34 Bn. in the form of interest bearing term

loans, finance leases and redemption of debentures.

Cash FlowThe Group’s net cash flows from operating activities decreased

to Rs. 593.06 Mn from the previous year’s amount of

Rs. 601.35 Mn, representing a slight drop of 1% year-on-year.

Share PerformanceThe All Share Price index (ASPI) of the Colombo Stock Exchange

(CSE) for the financial year ended 31st March 2011 had

increased by 93% to 7,226 points. The closing share price of

Lankem Ceylon PLC (LCEY) was Rs. 401.50 at the end of the

financial year representing a growth of 518% over the previous

year. The total market capitalisation of Lankem Ceylon PLC as at

31st March 2011 stood at Rs. 9.64 Bn.

0

400

800

1,200

1,600

2,000

Cash Flow & Profit After Tax (Rs. Mn.)

2006/072005/06

Net Cash Flow- Operating Activities

2007/08 2008/09 2009/10 2010/11

Profit after Tax

Lankem Share Price & Volume Movement

Share price Volume

In ’000

50

-

100

150

200

250

300

350

400

65

115

165

215

265

315

365

415

465

515

1-A

pr-

10

22-A

pr-

10

7-M

ay-1

0 21

-May

-10

8-Ju

n-10

23

-Jun

-10

8-Ju

l-10

22-J

ul-1

0 5-

Aug

-10

19-A

ug-1

0 3-

Sep

-10

20-S

ep-1

0 5-

Oct

-10

19-O

ct-1

0 3-

Nov

-10

22-N

ov-1

0 6-

Dec

-10

21-D

ec-1

0

4-Ja

n-11

2-Fe

b-1

1 18

-Jan

-11

21-F

eb-1

1 8-

Mar

-11

22-M

ar-1

1

Rs.

LCEY shares have continuously outperformed the market indices

ASPI and MPI. During this period LCEY prices appreciated by

593% as opposed to a 193% appreciation observed in the ASPI

performance.

34 Annual Report 2010/2011 | Lankem Ceylon PLC

LCEY- Based on 1/4/2010 Prices ASPI - Based on 1/4/2010 Index Value

All equated to 100 as at 1/4/2010

Relative Performance of ASPI and LCEY

100%

200%

300%

400%

500%

600%

700%

1-A

pr-

10

15-A

pr-

10

29-A

pr-

10

13-M

ay-1

0 27

-May

-10

10-J

un-1

0 24

-Jun

-10

8-Ju

l-10

22-J

ul-1

0 5-

Aug

-10

19-A

ug-1

0 2-

Sep

-10

16-S

ep-1

0 30

-Sep

-10

14-O

ct-1

0 28

-Oct

-10

11-N

ov-1

0 25

-Nov

-10

9-D

ec-1

0 23

-Dec

-10

6-Ja

n-11

20

-Jan

-11

3-Fe

b-1

1 17

-Feb

-11

3-M

ar-1

1 17

-Mar

-11

31-M

ar-1

1

0.0

0.50

1.00

1.50

2.00

2.50

3.00

Dividend Per Share & Dividend Yield

2006/072005/06

Dividend per Share

2007/08 2008/09 2009/10 2010/11

Dividend Yield

0

1%

2%

3%

4%

5%

6%

7%

8%Rs.

The Earnings Per Share (EPS) of Lankem Ceylon PLC Group

increased from Rs.15.72 to Rs.47.16 due to the significant

increase in Group profitability. The Net Asset Value Per Share

(NAV) of the Group has also increased to Rs.135.84 from

Rs.86.33.

DividendsDuring the year the Company declared an interim dividend of

Rs.1.00 per share and the Directors have recommended a final

dividend of Rs. 1.50 per share for the year ended 31st March

2011. This represents a dividend payout of 10%. Due to an

increase in the share price during the year, the dividend yield has

reduced to 1% from previous year’s dividend yield of 3%.

Financial Review

0

30

60

90

120

150

Earnings Per Share & Net Assets Per Share (Rs.)

2005/06

EPS

2006/07 2007/08 2008/09 2009/10 2010/11

NAV

Lankem Ceylon PLC | Annual Report 2010/2011 35

Corporate Social Responsibility

As a diversified business entity, Lankem continued to support

the community and the environment through its comprehensive

CSR vision. Being a mature corporate citizen, we strongly believe

in improving the quality of life of our community, enhancing the

potential and standards of living of our human resource, and

ensuring environmental safety while incorporating the best social

values and ethics in every aspect of our business at every level

within the group.

CommunityOn our journey as a caring community partner, we have

partenered with a multitude of stakeholders, covering a wide

spectrum in terms of social cluster, ethnicity and demography.

We have extended our support to uplift their quality of life and

social well-being.

During the year, we joined hands with “Ability Foundation”, a not

for profit organization, engaged in empowering and enabling

people with intellectual disabilities. Under the theme of “Creating

a Future for All” to create awareness, a programme was launched

on the opportunities and support available for children and

young adults with intellectual disabilities across Sri Lanka, with

a view to bridging the social gaps that affect such individuals.

Special resource personnel were brought in to carry out various

training and awareness building sessions in the Ampara District.

In addition, the web site of Ability Foundation was upgraded and

formally handed over as a gesture of good faith.

Leptospirosis, a disease commonly known in Sri Lanka as

“Mee-Una” reached epidemic proportions during the year and

it was found that farmers were among the most affected. As

the “Farmer Friendly” Agro Chemicals pioneer, we launched an

awareness building campaign carrying television snippets on

channel ITN. The snippets carried information to help control

the spread of the disease and also to create awareness on

preventive techniques.

In our efforts to extend support to preserve traditional values

in the community, we were privileged to continue with our

commitments to colour wash Dalada Maligawa - Kandy,

Poorwaramaya – Dehiattakandiya, Sri Sudarmaramaya -

Meepawala, Bellanwila Rajamaha Vihara, St. Mary’s Church-

Mukkuthuduwawa, and many childrens’ homes, elderly homes

and schools. Free Pest control services were provided to Giriulla

Medapola Maha Vidyalaya – Kirimetiyawa and school stationary

was provided to support children of Isuru Sevana Children

Orphanage, Kuruwita.

We donated water bottles to the National Blood Bank for the

consumption of blood donors, thereby extending a helping hand

to make island wide blood donation campaigns a success.

In view of upgrading the health conditions of the local community,

large garbage bins were provided to encourage the safe and

effective disposal of waste in urban and suburban areas.

EnvironmentAs a company working with hazardous chemicals, we continued

to conduct regular awareness programmes for school children

and farmers on the safe use of pesticides, with particular attention

on the usage of correct dosage to minimise environmental

damage.

Demarcating our footprint as a corporate citizen with a sound

Environmental Philosophy, we were successful in obtaining ISO

9001:2008 for Quality Management Systems, ISO 14001:2004

for Environmental Management Systems, OSHAS 18001;2007

Certification for Occupational Health and Safety for our

production facility and SLSI Product Quality Certification for our

products.

It has been identified that the Rubber Processing Industry is the

main cause of pollution of the natural waterways in Sri Lanka. As

a company that has a significant involvement in rubber cultivation

and manufacturing, Kotagala Plantation PLC has ensured that

all plants are provided with modern effluent treatment plants

that conform to the COD (Chemical Oxygen Demand) and BOD

(Biochemical Oxygen Demand) levels stipulated by the Central

Environmental Authority, thereby minimising the environmental

damage. Furthermore, our factories are equipped with energy

efficient fans and lighting.We have also taken steps to use

Biomass to operate tea driers thereby minimizing the usage

of fuel and oil. This has resulted in a cost saving as well as a

reduction in air pollution due to reduced level of carbon and

sulphur emissions.

36 Annual Report 2010/2011 | Lankem Ceylon PLC

EmployeesThroughout the Group, employees are considered the life blood

of the organisation.

We are an equal opportunity employer and ensure that our

employees are not discriminated against and that they are

compensated above industry average levels.

The company follows an extensive and effective Health and

Safety Policy to avoid operational hazards. Compliance is

strongly monitored and reported on a routine basis.

Due to the high level of involvement in hazardous chemicals,

extensive training is provided to all employees at the factory level,

on health and safety measures together with knowledge on the

composition of the chemicals. Fully equipped medical centers

are maintained at factories with full time professional nurses.

Cholinesterase tests are carried out as a routine to identify

possible chemical contaminations by the production floor staff.

We believe that long term investment in training will not only

benefit the company through the creation of a more competitive

and skilled workforce, but will also enable our employees to

pursue better careers and lifestyles in the future.

During the year, initiatives taken by the company to conduct

welfare and social events, sports and recreation programmes

which made employees happier and more productive. Lankem

Sports Club created opportunities for the employees to benefit

from the use of gymnasium facilities and other indoor and

outdoor sports for entertainment, physical and mental wellbeing.

In addition, company has hosted a variety of social events to add

colour to their work life.

During the latter part of the financial year the “Lankem Ladies

Corner” was launched with the objectives of empowering the

female employees with knowledge, awareness, leadership skills

and attitudinal changes to help them balance work and personal

life and provide them with a forum to discuss issues in their work

lives. The programmes will commence in the coming year.

At Kotagala Plantations, workshops were conducted to teach

crafting work, sewing etc. to female workers, who make up about

about 60% of the total workforce, thus creating opportunities for

entrepreneurship.

Labour welfare was also given highest priority, through initiatives

such as building new worker housing, re-roofing, new factory

and field rest rooms and modernised creche units for estate

workers’ children.

We also carried out immunization programmes to keep in line

in building a healthy national. Therefore periodical medical

camps were held for workers together with regular nutrition and

health checks, dengue awareness programme, and sanitation

pragammes.

In addition a “New Life Housing Scheme” was initiated to build

25 houses for the workers on Gikiyanakanda estate.

Corporate Social Responsibility

Lankem Ceylon PLC | Annual Report 2010/2011 37

Annual Report of the Board of Directors

The Board of Directors of Lankem Ceylon PLC present their

Report on the affairs of the Company together with the Audited

Financial Statements for the year ended 31st March 2011.

The details set out herein provide the pertinent information

required by the Companies Act No. 07 of 2007, and the Colombo

Stock Exchange Listing Rules and are guided by recommended

best practices.

GeneralThe Company was re-registered on 18th March 2008 as required

under the Companies Act No. 07 of 2007.

Principal Activities, Business and Future ProspectsThe principal activities of the Company together with those of

its subsidiary companies have been described along with the

Corporate Information in this Annual Report. A review of the

Company’s business and its performance during the year with

comments on financial results and future prospects is contained in

the Chairman’s Message, Business Review and Financial Review

sections of this Annual Report. These reports together with the

Financial Statements reflect the state of affairs of the Company.

The Directors to the best of their knowledge and belief confirm

that the Company has not engaged in any activities that

contravene laws and regulations.

Financial StatementsThe Financial Statements of the Group are given on pages 52

to 109.

Auditors’ ReportThe Auditors’ Report on the Financial Statements is given on

pages 50 and 51.

Accounting PoliciesThe Accounting Policies adopted in the preparation of the

Financial Statements are given on pages 57 to 63. There were

no changes in the Accounting Policies adopted.

Interest RegisterDirectors’ Interest in TransactionsThe Directors have made general disclosures as provided for in

Section 192 (2) of the Companies Act No. 07 of 2007. Arising

from this, details of contracts in which they have an interest are

disclosed in Note 29 to the Financial Statements on pages 97

to 102.

Directors’ RemunerationThe Directors’ remuneration in respect of the Group for the

financial year 2010/11 is Rs. 75.86 Mn. (2009/10 - Rs. 64.60

Mn) and in respect of the Company for the financial year 2010/11

is Rs. 71.12 Mn. (2009/10 - Rs. 60.40 Mn.).

Directors’ Interest in SharesThe Directors of the Company who have an interest in the shares

of the Company have disclosed their shareholdings and any

acquisitions/disposals to the Board in compliance with Section

200 of the Companies Act No. 07 of 2007.

Details pertaining to Directors’ direct and indirect Shareholdings

are given below:

No. of Shares

As at As at

31.03.2011 31.03.2010

Mr.A. Rajaratnam 12,198 7,000

Mr.S.D.R. Arudpragasam 5,132 4,459

Mr.Anushman Rajaratnam 5,403 4,728

Mr.D.L. Vitharana - -

Mr.R.N. Bopearatchy - -

Mr.N.H.B.S. Perera - -

Mr.K.P. David 8,150 7,083

Mr.A.R. Peiris 5,435 4,723

Mr.R.T. Weerasinghe 3,500 -

Mr.A. Hettiarachchy - -

(Appointed w.e.f. 01.04.2010)

Mr.A.C.S. Jayaranjan - -

(Appointed w.e.f. 01.06.2010)

Mr.J.D. Gomes - -

(Appointed w.e.f. 01.06.2010)

Corporate DonationsDonations made by the Group amounted to Rs. 99,000/- during

the year under review. (2009/10- Rs. 30,000/-)

38 Annual Report 2010/2011 | Lankem Ceylon PLC

Annual Report of the Board of Directors

DirectorateThe names of the Directors who held office during the financial

year and are given below. Brief profiles of these Directors appear

on pages 8 and 9.

Mr.A. Rajaratnam Chairman

Mr.S.D.R. Arudpragasam Deputy Chairman

Mr.Anushman Rajaratnam Managing Director

Mr.D.L. Vitharana Director/Chief Operating Officer

Mr.R.N. Bopearatchy Director

Mr.N.H.B.S. Perera Director

Mr.K.P. David Director

Mr. A.R. Peiris Director

Mr. R.T. Weerasinghe Director

Mr. A. Hettiarachchy Director

(Appointed w.e.f. 01. 04.2010)

Mr. A.C.S. Jayaranjan Director

(Appointed w.e.f. 01. 06.2010)

Mr.J.D. Gomes Director

(Appointed w.e.f. 01. 06.2010)

Mr. A. Hettiarachchy was appointed as an Independent Non-

Executive Director with effect from 1st April 2010. Mr.A.C.S.

Jayaranjan and Mr.J.D. Gomes were appointed as Independent

Non- Executive Directors with effect from 1st June 2010.

In terms of Articles 85 and 86 of the Articles of Association, Mr.

J.D. Gomes retires by rotation and being eligible offers himself

for re-election.

Mr.N.H.B.S. Perera, Director, being over seventy years of age

retires and offers himself for reappointment under and by virtue of

the Special Notice received from a shareholder of the Company

which is referred to in the Notice of Meeting.

Mr. R.N. Bopearatchy who has attained the age of seventy years

offers himself for reappointment under and by virtue of a Special

Notice received from a shareholder of the Company which is

referred to in the Notice of Meeting.

Mr. A. Rajaratnam who has attained the age of seventy years

offers himself for reappointment under and by virtue of a Special

Notice received from a shareholder of the Company which is

referred to in the Notice of Meeting.

AuditorsThe Financial Statements of the Company for the year have

been audited by Messrs KPMG Ford, Rhodes, Thornton & Co.

the retiring auditors who have expressed their willingness to

continue as Auditors of the Company and are recommended for

reappointment. A resolution to reappoint them and to authorize

the Directors to determine their remuneration will be proposed at

the Annual Genaral Meeting

The Auditors, Messrs KPMG Ford, Rhodes, Thornton & Co.

were paid Rs. 7.18 Mn. during the year under review (2009/10-

Rs. 6.75 Mn.) as audit fees and fees for audit related services by

the Group. In addition, they were paid Rs. 0.47 Mn. (2009/10-

Rs. 0.56 Mn.) by the Group for non-audit related work, which

consisted mainly of tax related work. In addition to the above,

Group companies are engaged with other audit firms. Audit fees

in respect of these firms amounted to Rs. 4.69 Mn. during the

year under review (2009/10- Rs. 3.75 Mn.). Further, the fees for

non-audit related services by these audit firms during the year

2010/11 was Rs. 0.04 Mn.

As far as the Directors are aware, the Auditors do not have any

relationship (other than that of an Auditor) with the Company.

The Auditors do not have any interest in the Company.

RevenueThe revenue of the Group for the year was Rs. 23,031 Mn.

(2009/10-Rs. 11,046 Mn.).

ResultsThe Group made a profit before tax of Rs. 2,109 Mn. against a

profit of Rs. 804 Mn. in the previous year. The detailed results are

given in the Income Statements on page 52.

DividendsThe Board of Directors approved the payment of an Interim

Dividend of Rs.1/- per share which was paid on 9th February

2011 and have recommended the payment of a Final Dividend of

Rs. 1.50 per share on the ordinary shares of the Company for the

year ended 31st March 2011 for approval by the shareholders at

the Annual General Meeting to be held on 30th September 2011.

The Directors have confirmed that the Company satisfies the

solvency test requirement under Section 56 of the Companies

Act No. 07 of 2007 for the dividend proposed. A solvency

certificate has been sought from the Auditors in respect of the

aforementioned dividend.

Lankem Ceylon PLC | Annual Report 2010/2011 39

InvestmentsInvestments made by the Group are given in Notes 17 and 18 to

the Financial Statements on pages 78 to 82.

Property, Plant & EquipmentDuring 2010/11 the Group invested Rs. 1,305.70 Mn. in Property,

Plant & Equipment (2009/10 - Rs. 1,320.36 Mn.). Further, your

Directors are of the opinion that the net amounts at which Land

and other Property, Plant & Equipment appear in the Balance

Sheets are not greater than their market value as at 31st March

2011.

Stated CapitalThe stated capital of the Company as at 31st March 2011 was

Rs. 536,218,000/- and is represented by 24,000,000 issued and

fully paid Ordinary Shares.

During the year the Company made a Rights Issue of shares to

its ordinary shareholders the details of which are disclosed under

Note 22 to the Financial Statements on page 83.

ReservesThe total Group Reserves as at 31st March 2011 comprised

Revaluation Reserves of Rs. 462.09 Mn., Capital Redemption

Reserve Rs. 8.33 Mn., Other Capital Reserves Rs. 22.50 Mn.,

General Reserves of Rs. 305.95 Mn. and Retained Earnings

Rs. 1,924.96 Mn. whereas the total Group Reserves as at 31st

March 2010 comprised Revaluation Reserves of Rs. 412.25

Mn., Capital Redemption Reserve Fund of Rs. 8.33 Mn.,

Other Capital Reserves of Rs. 22.50 Mn., General Reserves of

Rs. 305.95 Mn. and Retained Earnings of Rs. 782.67 Mn.

The movements are shown in the Statement of Changes in

Equity in the Financial Statements.

TaxationThe Group’s liability to taxation has been computed in

accordance with the provisions of the Inland Revenue Act No.

10 of 2006, and subsequent amendments thereto.

Income tax and other taxes paid and liable by the Group are

disclosed in Notes 6 and 10 to the financial statements on pages

64, and 66 to 68.

Share InformationInformation relating to earnings, dividend, net assets, market

value per share and share trading is given on pages 68, 111

and 112.

Events Occurring after the Balance Sheet DateEvents occurring after the Balance Sheet date that would require

adjustments to or disclosures are disclosed in Note 34 on

page 105 to 106.

Capital Commitments and Contingent LiabilitiesCapital commitments and contingent liabilities as at the

Balance Sheet date are disclosed in Notes 30 and 31 on pages

102 to 104.

Employment PolicyThe Company’s recruitment and employment policy is

non¬discriminatory. The occupational health and safety

standards receive substantial attention. Appraisals of individual

employees are carried out in order to evaluate their performance

and realize their potential. This process benefits the Company

and the employees.

ShareholdersIt is the Company’s policy to endeavour to ensure equitable

treatment to its shareholders.

Statutory PaymentsThe Directors, to the best of their knowledge and belief, are

satisfied that all statutory payments of the Company due in

relation to employees and the Government have been made

promptly and are up to date.

Environmental ProtectionThe Company’s business activities can have direct and indirect

effects on the environment. It is the Company’s policy to minimize

any adverse effect its activities have on the environment and

to promote co-operation and compliance with the relevant

authorities and regulations. The Directors confirm that the

Company has not undertaken any activities which have caused

or are likely to cause detriment to the environment.

Internal ControlThe Directors acknowledged their responsibility for the

Company’s system of internal control. The system is designed

to give assurance regarding the safeguarding of assets, the

40 Annual Report 2010/2011 | Lankem Ceylon PLC

maintenance of proper accounting records and the reliability

of financial information generated. However, any system can

ensure only reasonable and not absolute assurance that errors

and irregularities are either prevented or detected within a

reasonable period of time.

The Board is satisfied with the effectiveness of the system of

internal control for the period up to the date of signing these

Financial Statements.

Going ConcernThe Directors, after making necessary inquiries and reviews

including reviews of the Company’s budget for the subsequent

year, capital expenditure requirements, future prospects and

risks, cash flows and borrowing facilities, have a reasonable

expectation that the Company has adequate resources to

continue in operational existence for the foreseeable future.

Therefore, the going concern basis has been adopted in the

preparation of the Financial Statements.

For and on behalf of the Board

Anushman Rajaratnam K. P. David

Director Director

By Order of the Board

Corporate Managers & Secretaries (Private) Limited

Secretaries

Colombo

23rd August 2011

Annual Report of the Board of Directors

Lankem Ceylon PLC | Annual Report 2010/2011 41

Corporate Governance is a way of structuring the organisation in

order to safeguard the interests of a wide variety of stakeholders.

It needs to balance the Corporate Governance with everyday

business management in today’s dynamic corporate world.

We at Lankem firmly promise our stakeholders better business

performance which is nurtured and backed through properly

formulated governance practices and procedures.

Lankem Ceylon PLC is in compliance with the majority of the

good corporate governance practices listed in the code of Best

Practice on Corporate Governance issued by The Institute of

Chartered Accountants in Sri Lanka and the rules on Corporate

Governance set out in the Colombo Stock Exchange Listing

Rules.

We present below the Corporate Governance practices adopted

and practiced by Lankem Ceylon PLC.

The Board of Directors1.1 The Board, Composition and MeetingsThe Board of Directors of Lankem Ceylon PLC is responsible

for the governance practices adopted in all the companies

within the Group. The Board comprises the Chairman, Deputy

Chairman, Managing Director, Chief Operating Officer and eight

other Directors. All the Directors are professionals who have

acquired a wealth of experience and knowledge in the fields of

Management, Marketing and Finance.

Name of Director

Mr. A. Rajaratnam

(Chairman) Non-Executive

Mr. S. D. R. Arudpragasam

(Deputy Chairman) Non-Executive

Mr. Anushman Rajaratnam

(Managing Director) Executive

Mr. D. L. Vitharana

(Chief Operating Officer) Executive

Mr. R. N. Bopearatchy Executive

Mr. N. H. B. S. Perera Independent Non-Executive

Mr. K. P. David Executive

Mr. A. R. Peiris Executive

Mr. R. T. Weerasinghe Executive

Mr. A. Hettiarachchy Independent Non-Executive

(Appointed w.e.f. 01.04.2010)

Mr. A. C. S. Jayaranjan Independent Non-Executive

(Appointed w.e.f. 01.06.2010)

Mr. J. D. Gomes Independent Non-Executive

(Appointed w.e.f. 01.06.2010)

Corporate Governance

The Board meets regularly and has met seven times during the

year under review. In addition to Board Meetings, matters are

referred to the Board and decided by resolutions in writing.

The number of meetings of the Board and the individual

attendance by members is shown below :

Total number of Meetings held 7

Name of Director Directorship Board Meetings

Status Attended

Mr. A. Rajaratnam Chairman 5/7

Non-Executive

Mr. S.D.R. Arudpragasam Deputy Chairman 6/7

Non-Executive

Mr. Anushman Rajaratam Managing Director 7/7

Executive

Mr. D.L. Vitharana Chief Operating 6/7

Officer/Executive

Mr. R.N. Bopearatchy Executive 5/7

Mr. N.H.B.S. Perera Independent 7/7

Non-Executive

Mr. K.P. David Executive 7/7

Mr. A.R. Peiris Executive 7/7

Mr. R.T. Weerasinghe Executive 6/7

Mr. A. Hettiarachchy Independent 5/7

(Appointed w.e.f. 1.4.2010) Non-Executive

*Mr. A.C.S. Jayaranjan Independent 6/6

(Appointed w.e.f. 1.6.2010) Non-Executive

*Mr. J.D. Gomes Independent 1/6

(Appointed w.e.f. 1.6.2010) Non-Executive

* Six Board Meetings were held after the appointment of

Mr. A.C.S. Jayaranjan and Mr. J.D. Gomes on 1st June 2010.

Availability of Formal Schedule of Matters

The code of Best Practice on Corporate Governance of The

Institute of Chartered Accountants of Sri Lanka suggests that

the Board should have a formal schedule

42 Annual Report 2010/2011 | Lankem Ceylon PLC

Corporate Governance

of matters specially reserved for its decision making. Sufficient time was dedicated at meetings in order to ensure the following.

• Offer guidance on overall direction and related strategies, financial and non-financial objectives of Lankem Ceylon PLC.

• Formulation, implementation and monitoring of business strategy of the Company.

• Overseeing the effectiveness of the internal control systems and proactive risk management system.

• Ensuring compliance with legal requirements and ethical standards.

• Approval of budgets, corporate plans, major investments and divestments.

• Approval of interim and annual Financial Statements for publication.

• Approval and review of the succession planning of the Boards and top management.

• Approval of any issue of equity and debt securities of the Company.

• Any other matter which is important to ensure that the Company conducts its business in the best interest of all stakeholders.

Company Secretary and Independent Professional AdviceLankem Ceylon PLC and all the Directors seek advice from Corporate Managers and Secretaries (Private) Ltd, who are qualified to act as Secretaries as per the provisions of the Companies Act No. 07 of 2007. In addition, the Board seeks professional advice as and when, and where necessary from independent external professionals.

Independent JudgementThe Board of Directors as a whole and individually are committed to exhibit high standards of integrity and independence of judgement on various issues from strategy to performance.

Training for DirectorsThe Directors are provided with adequate and relevant training opportunities for their continuous development.

1.2 Segregation of the Role of Chairman and Chief Executive Officer