7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 1/20 Market Recap for All of 2015 The story for 2015 was largely written by the U.S. Federal Reserve as it wavered on increasing the Fed funds rate — and eventually did so in December. It seems to me that, as much as anything, the factors that influenced the Fed’s thinking and the expectations of investors as they interpreted Fed moves (or lack thereof), were the primary drivers for both equity and investment grade corpo- rate (IGC) bond performance in the U.S. Here are some of those factors: U.S. unemployment — The most watched unemployment rate fell from 5.7% in Januar y to 5% today, a level last seen in March 20 08. Surely, a positi ve moti- vation for the Fed to raise its policy rate, but not enough by itself as the growth in average hourly earnings barely kept pace with inflation. Non-farm payrolls — For the 12 monthly reports ending in November, non- farm payrolls increased an average of about 220,000/month, a small decrease from 2014, but a strong increase from 2012 and 2013. Another factor sup- porting a potential rate hike. Inflation — The Core PCE Index (excluding food and energy), is the Fed’s primary focus. An annualized increase of about 1.3% in 201 5 was well be- low the Fed’s target of 2% and, as such, provided little incentive to increase the policy rate. Global growth — Led by a decline in China, the UN estimates global growth in 2015 at 2.4%, a 0.4% reduction from an estimate of only 6 months ago. In the last 5 years, China’s GDP growth rate has fallen from nearly 12% to about 7%. I believe slow global growth was a primary factor that delayed the rate hike in 2015 and will continue to influence the Fed and markets in 2016. The net result for the S&P 500 was an increase of 1.23% while IGC bonds ac- tually slid 1.26%. Eurozone equities slid 1.64% while emerging markets, heavily in- fluenced by the fallen demand for oil and other commodities, fell 16.17%. Oil (using the ETF for oil, DBO) sank over 42% in 2015 after having fallen over 40% in 2014. Gold sank over 10%. One perspective would suggest that 2015 was a year of consolidation after having 3 very strong years. Another would suggest that we have entered a new normal re- flecting lower global growth for years to come. That’s my belief. My forecast for 2016 follows. 2015 Review and 2016 Fearless Forecast January 1, 2016 Lane Asset Management The charts on the following pages use mostly exchange-traded funds (ETFs) rather than market indexes since indexes cannot be invested in directly nor do they reflect the total return that comes from reinvested dividends. The ETFs are chosen to be as close as possible to the performance of the indexes while representing a realistic investment opportunity. Pro- spectuses for these ETFs can be found with an internet search on their symbol. Past performance is no guarantee of future results.

Lane Asset Management 2015 Review and 2016 Fearless Forecast

Mar 04, 2016

Stock market and economic commentary

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 1/20

Market Recap for All of 2015

The story for 2015 was largely written by the U.S. Federal Reserve as it wavered

on increasing the Fed funds rate — and eventually did so in December. It seems

to me that, as much as anything, the factors that influenced the Fed’s thinking

and the expectations of investors as they interpreted Fed moves (or lack

thereof), were the primary drivers for both equity and investment grade corpo-

rate (IGC) bond performance in the U.S. Here are some of those factors:

U.S. unemployment — The most watched unemployment rate fell from 5.7%

in January to 5% today, a level last seen in March 2008. Surely, a positive moti-

vation for the Fed to raise its policy rate, but not enough by itself as the

growth in average hourly earnings barely kept pace with inflation.

Non-farm payrolls — For the 12 monthly reports ending in November, non-

farm payrolls increased an average of about 220,000/month, a small decrease

from 2014, but a strong increase from 2012 and 2013. Another factor sup-

porting a potential rate hike.

Inflation — The Core PCE Index (excluding food and energy), is the Fed’s

primary focus. An annualized increase of about 1.3% in 2015 was well be-

low the Fed’s target of 2% and, as such, provided little incentive to increase

the policy rate.

Global growth — Led by a decline in China, the UN estimates global

growth in 2015 at 2.4%, a 0.4% reduction from an estimate of only 6

months ago. In the last 5 years, China’s GDP growth rate has fallen from

nearly 12% to about 7%. I believe slow global growth was a primary factor

that delayed the rate hike in 2015 and will continue to influence the Fed

and markets in 2016.

The net result for the S&P 500 was an increase of 1.23% while IGC bonds ac-

tually slid 1.26%. Eurozone equities slid

1.64% while emerging markets, heavily in-

fluenced by the fallen demand for oil and

other commodities, fell 16.17%. Oil (using

the ETF for oil, DBO) sank over 42% in

2015 after having fallen over 40% in 2014.

Gold sank over 10%.

One perspective would suggest that 2015

was a year of consolidation after having 3

very strong years. Another would suggest

that we have entered a new normal re-

flecting lower global growth for years to

come. That’s my belief.

My forecast for 2016 follows.

2015 Review and 2016 Fearless Forecast January 1, 2016

Lane Asset Management

The charts on the following pages use mostly exchange-traded funds (ETFs) rather than market indexes since indexes cannot be invested in directly nor do they reflect the total return

that comes from reinvested dividends. The ETFs are chosen to be as close as possible to the performance of the indexes while representing a realistic investment opportunity. Pro-

spectuses for these ETFs can be found with an internet search on their symbol. Past performance is no guarantee of future results.

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 2/20

Lane Asset Management Page 2

2015 Review and 2016 Fearless Forecast

as Europe’s bellwether country.

VEU lived up to expectations by trailing the S&P 500 by about 6%. On the other

hand, as with the S&P 500, I overestimated its performance for 2015 as the index

ETF ended the year down about 4.8%. I also greatly overestimated the results for

China and India (I’ll speak more about these later). On the other hand, commodity

producing regions lived up to expectations with a serious shortfall as energy and the

global slowdown took a major toll.

Bonds and Other Income Securities:

The 10-year Treasury yield surprised everyone in 2014, especially after its rapid

increase in 2013. The yield currently rests at about 2% and I believe it will end

the year near 2.5%. Total return for 7-15 year U.S. government bond funds in

2014 was a bit over 9% while investment grade corporate (IGC) bonds funds re-

turned a bit over 8%. For 2015, I expect total return for IGC bonds between 6%

and 8%, still better than current yield. I believe the best opportunities for in-

come investing will come from preferred stocks, REITs and established, long

term dividend paying common stocks.

Despite the long anticipation for a Fed rate hike and the eventual move, the 10-year

Treasury yield increased only marginally during 2015 from about 2.17% to 2.27% re-

flecting, I believe, the downward pressure from international government bond yields.

IGC bonds actually lost ground in 2015 with a decline in total return of nearly 1.3%.

A point that was driven home for me this year was the negative correlation between

the 10-year Treasury yield and the performance of IGC bonds (more on this later).

As expected, both REITs and preferred stocks both outperformed bonds, especially

preferreds of financial organizations. On the other hand, dividend paying common

stocks disappointed by underperforming the S&P 500.

** *** **

Every year is a learning experience and 2015 was no different. Three key mes-

sages from this past year were the importance of central bank policy here and

abroad, the lingering effects of the Great Recession, and the impact of China on

global growth.

2015 PREDICTIONS — HOW THEY FARED

Predictions in black; 2015 results in blue italics.

U.S. Equities

As I believe the primary drivers of stock market returns in 2015 will be corpo-

rate earnings and modest, if any, movement on the federal funds rate, my ex-

pectation for the S&P 500 for 2015 is for a total return of 8-10% (measured by

SPY) with risk to the downside on account of international considerations. On

a sector basis, I expect healthcare, technology, consumer discretionary and

small cap stocks to outperform. There may be a rebound in energy, but I’m not

prepared to go there now.

While I overestimated the total return for the S&P 500 in 2015 by quite a lot (the

actual return was about 1.2%), I was right that the risk was to the downside on ac-

count of international considerations (see below). As for the sector calls, healthcare,

technology and consumer discretionary all out performed the S&P 500 — by about

6.2%, 5.5%, and 9.9%, respectively. On the other hand, small caps stocks underper-

formed with a decline of 4.5%. The rebound in energy never occurred as the energy

ETF dropped over 20%.

As expected, it looks like corporate earnings were a key driver of equity perform-

ance in 2015 as earnings have become likely to turn out to be negative for the year

for the broad index. However, if energy is excluded, earnings growth is looking to

exceed 5%, a much healthier outcome. I was also directionally correct on the Fed

funds rate hike with the smallest possible hike at the latest possible moment.

International Equities

My estimate for total return from international equities, as measured by the

Vanguard All-world (ex U.S.) fund, VEU, is 2-3% less than SPY which, given the

above estimate, is 5-8% for VEU. I believe the international equity returns will

be very region specific with India and China leading the way and commodity-

producing regions lagging. Europe is a wild card as the broader economy

struggles while the ECB may come to the rescue. I’d keep an eye on Germany

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 3/20

Investment Forecast for 2016

I begin each year mindful of what Bob McTeer, the

former head of the Dallas Fed once said, “The first

rule of forecasting should be don’t do it. Nothing good

comes from it. … My rule is, if you have to do it, do it

often.” So what you read here is best taken with a

grain of salt and an understanding that the forecast

may change as events unfold.

Domestic Equities

Last year, by relying on 2014’s strong returns, I was overly optimistic about eq-

uity growth in the U.S. and abroad as I discounted the developing weakness in

global growth that had been telegraphed in a report by the IMF in October

2014. I also misread the Fed’s patience, appreciating the delay, but not giving

enough thought, in retrospect, to the underlying causes of that delay. Let’s see

if we can read the tea leaves a little better this year.

For 2016, I’ll be using the following criteria to form my year -end estimate for

the S&P 500:

Long term performance While the 20 – and 35-year total return for the

S&P 500 has hovered around 10%, the total return for the last 8 years has

been about 6.3%, including the weak return for 2015. With expectations for

U.S. and global GDP growth in 2016 to be about half the long term rate of

growth (2.4% vs. 4.6%) and a very high correlation between long term GDP

growth and the S&P total return, something on the order of 5% may be a

better starting point for an estimate of the S&P 500 total return for 2016.

Corporate earnings According to FactSet Research, taking the S&P 500 as

a whole (that is, including energy), the forecast is for the 4th quarter of 2015

to mark the first time since 2009 that there were 3 consecutive quarters of

negative earnings and 4 consecutive quarters of revenue declines. While

earnings for the full year could turn out negative, excluding the energy sec-

tor, they may be as high as 5% — not stellar, but consistent with my starting

point for 2016. A broader look at corporate profits is provided by the Bureau

of Economic Analysis (BEA). Close examination shows there’s been virtually

no growth in corporate profits since 2011. While the forecast for 2016 is

brighter than the outcome for 2015 — owing to less negative impact from

energy — the energy sector will continue to weigh down aggregate results.

Headwinds will come from a strong dollar that will depress income and prof-

its from overseas and dampen exports.

Monetary Policy The U.S. Federal Reserve finally took an initial step in rais-

ing the Fed funds rate in December with a promise to be slow and measured

when it comes to future increases. In effect, the policy rate is expected to re-

main highly accommodative throughout 2016. As for policy rate drivers:

The inflation rate remains well below the Fed target of 2% (about 1.3% in the

latest year-over-year reading) and there appears to be little evidence of pres-

sure from wages or commodities, I don’t see inflation as causing a Fed move

in the near future.

Although the unemployment rate is now at 5.0%, its lowest rate since 2007,

the Fed has backed off its focus on the absolute value as a trigger to its tim-

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 3

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 4/20

ing for the benchmark rate increase. One concerning issue is the labor

force participation rate, now at a level not seen since the late 70’s.

In the November reading recently released, the average hourly wage in-

creased by 0.2%, about the average since 2006 and an improvement that has

been largely eaten up by inflation. The absence of wage pressures will help

to maintain a slow path for Fed rate increases.

In terms of the expected Fed funds rate increase, my view is that an addi-

tional 50-75 basis points might be added in 2016, with risk to the downside

keeping in mind that 2016 is an election year. As expected last year, the Fed

prepared the market well for the eventual rate increase and suffered no

damage because of it. I expect a similar degree of communication this year.

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 4

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 5/20

Industrial Production Despite the approximate 30% share of U.S. GDP at-

tributable to manufacturing, there is a strong correlation between the U.S.

industrial production index (IPI) and the S&P 500, as shown on this next

chart. The observation to be made here is that both the IPI and the S&P

500 have been relatively flat since late 2014. Although I don’t know for sure,

I suspect that the IPI has been flattened by the reduction in energy-related

construction brought about by the sharp decline in the price of oil. If we ob-

serve any additional deterioration in the IPI, that would not bode well for

the broad S&P 500 index.

Oil And speaking of oil, it’s not at all clear to me where the price is headed

in the near-term. This next chart is for Brent, the global price benchmark

for Atlantic basin crude oil. Although the chart is hard to read, the point to

note is that it’s only in the last 10 years that oil’s per barrel price exceeded

$40. With low inflation, slowing global economic growth, Iranian oil likely

coming on-line, Saudi Arabia keeping supply levels high, and an end to U.S.

oil export prohibition, I am not expecting much in the way of price recovery

with a lower outcome by year-end more likely. If I’m right, this will be a tail-

wind for U.S. consumers but a headwind construction spending and emerg-

ing markets.

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 5

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 6/20

Analyst estimates According to a survey of 10 prominent analysts by Bar-

ron’s taken December 12th, the average expected increase for the S&P 500

index for 2016 amount to 6.8% taking dividends into account (I’ve ignored

the 2+% gain that the index increased in December after the predictions

were made since I’m assuming the predictions were made as if there was no

change in the remaining part of 2015 — otherwise, while I could be wrong,

their predictions would call for a 4.8% return for 2016 which I doubt was the

intention).

Market breadth One measure of market strength is a growing or persis-

tently high percentage of individual stocks that are above their 200-day

moving average (DMA). Over the last 10 years, there has been a positive

correlation between the performance of the S&P 500 and the number of

stocks within the index that are above their 200 DMA — that is, until re-

cently.

As the next chart shows, sudden reductions in the percent of stocks above

their 200 DMA have generally been followed by rapid recoveries as in the

period from 2004-2007 and 2009-2013. On the other hand, a more persis-

tent reduction — as in the period from 2007-2009 — seemed to portend the

significant market correction which came about as the percentage contin-

ued to deteriorate. The interpretation here is that the market continued to

advance on the strength of fewer and fewer large cap stocks until a certain

reality took hold bringing the entire market down.

Bearing in mind that this is only one example in the last 16 years and thatthere is absolutely no guarantee that past performance will be repeated,

this pattern seems to have begun again in 2014 (or a little earlier, depending

on your perspective) — so far without a corresponding correction. But this

divergence cannot last. Eventually, either the percentage of stocks under

their 200 DMA needs to improve or the broader market needs to adapt to a

new reality. While I don’t believe the market is primed for a major correc-

tion, it is something we need to watch carefully.

Recession Watch According to an early December article in Fortune, JPMor-

gan predicted a 76% chance of a recession in the next 3 years with a 25%

chance within the next 12 months. Citibank increased the ante by placing

the probability at 65% for 2016. And, if you do a Google search, you will find

JPMorgan and Citi are not alone in expressing concerns.

On the other hand, the New York Fed places the probability of a recession at

virtually zero using the highly respected yield curve as a predictor of reces-

sions (see next page). Note in the bottom chart that the nominal (not infla-

tion-adjusted) yield curve is no less steep than it was a year ago and the real

(inflation-adjusted) curve is actually a bit more steep, i.e., suggesting a reces-

sion is less likely.

Do I think a recession is likely? I’d have to say no on the basis of the steady, if

slow, recovery underway since 2008. But, with a consensus for global growth

in 2016 around 2.4%, it wouldn’t take much of a slippage to raise the poten-

tial for a recession. It is for this reason that it is important for investors to

remain alert and flexible, with a game plan in mind should events turn ugly.

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 6

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 7/20

While we’re on the subject of a market correction, here’s another perspec-

tive: As this next chart shows, since around 1995, there has been a fairly con-

sistent and significantly high negative correlation between the U.S. unem-

ployment rate and the performance of the S&P 500. While the economic

conditions resulting in a major correction are never exactly the same, if this

pattern was to continue, it would appear that at some point, perhaps in the

not too distant future, there would be another significant correction in the

S&P 500. While nothing guarantees that past performance will be repeated,

it presents another data point worth watching.

** *** **

International Equities

The international economic situation is complex and very region and country

specific.

For the Eurozone, GDP growth of about 1.5% translated into a small decline

for EMU equities in 2015. For 2016, the outlook is for only a small improve-

ment. Dollar strength along with accommodative policy from the ECB and

growing capacity utilization will help to keep Europe out of recession despite

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 7

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 8/20

being dogged with high unemployment (twice the level of the U.S.).

Japan emerged from recession in the second quarter of 2015 but continues

to have structural (especially demographic) problems in addition to suffer-

ing from reduced demand for exports to China. One positive factor that

sets Japan apart is the willingness to take fiscal measures to support the

economy (not relying entirely on monetary policy) although it’s not clear

whether policy will be strong enough. Meanwhile, for all its troubles, Japan

had one of the best equity performance outcomes in 2015, pulled forward

by its financial sector. For 2016, the outlook is for GDP growth in the 1%

range, similar to 2015.

China equities struggled in 2015, turning in a negative performance as the

country adapts to a lower rate of growth (still a healthy 7%) and conversion

to a more consumer-led economy — the impact of which is being felt

around the world in the form of less exports of commodities to China. The

outlook for 2016 is more of the same although surprise moves by the gov-

ernment have a way of shaking things up.

With GDP growth in excess of 7% and expanding foreign direct investment,

I expected a stronger return from India equities in 2015 than what we actu-

ally experienced (the Bombay stock exchange declined over 5% for the

year). The culprit seems to be exports that fell to their lowest level in 5

years. The challenge in India is a complex environment with structural, so-

cial and economic headwinds. With 2016 GDP growth expected to continue

to exceed 7%, India equities bearing watching for a turnaround.

Since the beginning of 2011, Latin American region equities and the rate of

change in GDP have been in a downward trajectory, largely driven by Brazil

and Chile and, since 2013, including Mexico and Peru. The reasons are com-

plex and include both economic factors (declining commodities) and politics.

In light of the current global economic slowdown which has been taking a toll

on oil, copper, precious metals and other commodities, not to mention politi-

cal challenges in Brazil, there’s little reason to expect a significant turn-

around in the foreseeable future for countries in the region.

Canada, like other commodity exporting countries, had a difficult year in

2015 with GDP growth slipping from about 2.5% in 2014 to about 1.2% in

2015 and the Toronto Stock Exchange slipping about 9%. A recovery in Can-

ada, like a recovery for other commodity producers, will depend upon im-

proved global demand and a recovery of some type in the price of oil. I am

not convinced that such a recovery will take place in 2016.

** *** **

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 8

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 9/20

Interest rates

While there’s been a lot of focus on the Federal funds rate lately, and under-

standably so, the 10-year government bond rate in the U.S. and in other major

developed markets deserves similar attention as this rate has considerable in-

fluence on the economy and investments. A very high rate snuffs out borrow-

ing and can draw investor funds from equities to bonds while a very low rate

motivates investors to seek higher returns, drawing investor funds out of

bonds and into equities, taking on increased risk in the process. With the cur-

rent U.S. 10-year Treasury bond yielding 2.27% — just 10 basis points above

where 2015 began — it’s in the very low rate environment that we find our-

selves today.

While the U.S. 10-year yield is not far from its historic low point of 1.5%, it is

important to note that it is considerably higher than comparable bond yields

in the Eurozone, U.K., Japan, and Canada, and roughly the same as in China,

South Korea and Australia. Interestingly, the comparable bond yield in India is

an outlier at about 7.75%.

As the U.S. rate barely budged following the Fed’s December rate hike nor for

the year as a whole, the relationship with comparable rates in other developed

economies illustrates the demand for the strength and safety of the U.S. dollar

(up about 8% in 2015). I expect the same pressures will continue in 2016 with

only a modest change for the year.

** *** **

Summary

While, on balance, I’m expecting equity and bond performance in 2016 to be

very similar to 2015, as discussed in preceding paragraphs, there are some

hints that equities could be in store for a significant correction. Beyond those

technical considerations, geopolitics and terrorist activities have the world on

edge. The U.S. presidential election adds uncertainty. Investors should review

their risk tolerance and be prepared for volatility and market disruption.

2016 PREDICTIONS

So, if you are still with me, here are my predictions for 2016. They apply to mar-

ket conditions that are evident today. Paraphrasing Keynes famous comment, if

market conditions change, I’ll change my opinion. Wouldn’t you?

U.S. Equities

With the slowdown in global growth and weakness in U.S. profits, I’m expecting

another year like the one we had in 2015 with the S&P 500 advancing 3-5% with

risk to the downside.

On a sector basis, I expect healthcare (especially biotech), technology, con-

sumer discretionary and regional banks to outperform the S&P 500. But here’s

a concern. Recall comments on page 6 about the lack of market breadth. In

the case of the popular consumer discretionary ETF (XLY), 30% of the portfolio

is represented by 4 stocks and in the case of the popular technology ETFs(QQQ and XLK), 40% of the portfolios are represented by 5 and 4 companies,

respectively. So there’s some danger there that a reversal in just a few stocks

could upend the performance of the entire sector. Here’s how those sectors

performed compared to the S&P 500 in 2015 using representative ETFs for

each sector. Of course, while I believe these will be the outperforming sectors

again in 2016, there’s no guarantee that past performance will be repeated.

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 9

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 10/20

International Equities

My estimate for total return from international equities, as measured by the

Vanguard All-world (ex U.S.) fund, VEU, is 0% to 2%. I believe the international

equity returns will be very region specific with developed markets leading the

way and commodity-producing regions lagging. Improving dollar strength will

benefit investments in developed economies that are hedged against the dollar.

The hedged regions that I believe will outperform the broad (unhedged) index

in 2016 are Japan, Germany, and the Eurozone. Here’s how ETFs representing

these three areas (unhedged and hedged) performed in 2015 compared to the

broad international index, VEU. Again , past performance does not guarantee

future results.

Bonds and Other Income Securities:

The 10-year Treasury yield surprised everyone again in 2015 with very little up-

ward movement. I expect the same in 2016 despite a few Fed funds rate hikes

and believe it will end the year near 2.5%. Total return for 7-15 year U.S. gov-

ernment bond funds in 2015 was about 1.4% while investment grade corporate

(IGC) bonds funds declined about 1.3%. For 2016, I expect total return for IGC

bonds to be very close to zero consistent with a small increase in the 10-year

Treasury bond yield. As with 2015, I believe the best opportunities for income

investing will come from preferred stocks, especially in the financial sector, and

REITs. Here’s how representative ETFs performed in 2015 and keeping in mind

that past performance does not guarantee future results.

If the S&P 500 meets my goal for 3-5%, I believe it will continue to reflect the

strength of a limited-breadth market which did not favor dividend-paying stocks

in 2015. Therefore, I’ve dropped them from my outperform list for 2016.

** *** **

This completes my 2016 Fearless Forecast. It reflects my view that investment

returns have moved into a new, lower trajectory on account of the slowdown in

global growth caused in part by China’s slowdown, but also by the unwillingness

of developed nations, including the U.S., to make the necessary fiscal interven-

tions (read: investments in infrastructure, innovation and education) required to

support a higher level of sustainable growth. In the following pages, I provide

additional technical perspective on today’s markets. Thank you for reading.

2015 Review and 2016 Fearless Forecast

Lane Asset Management Page 10

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 11/20

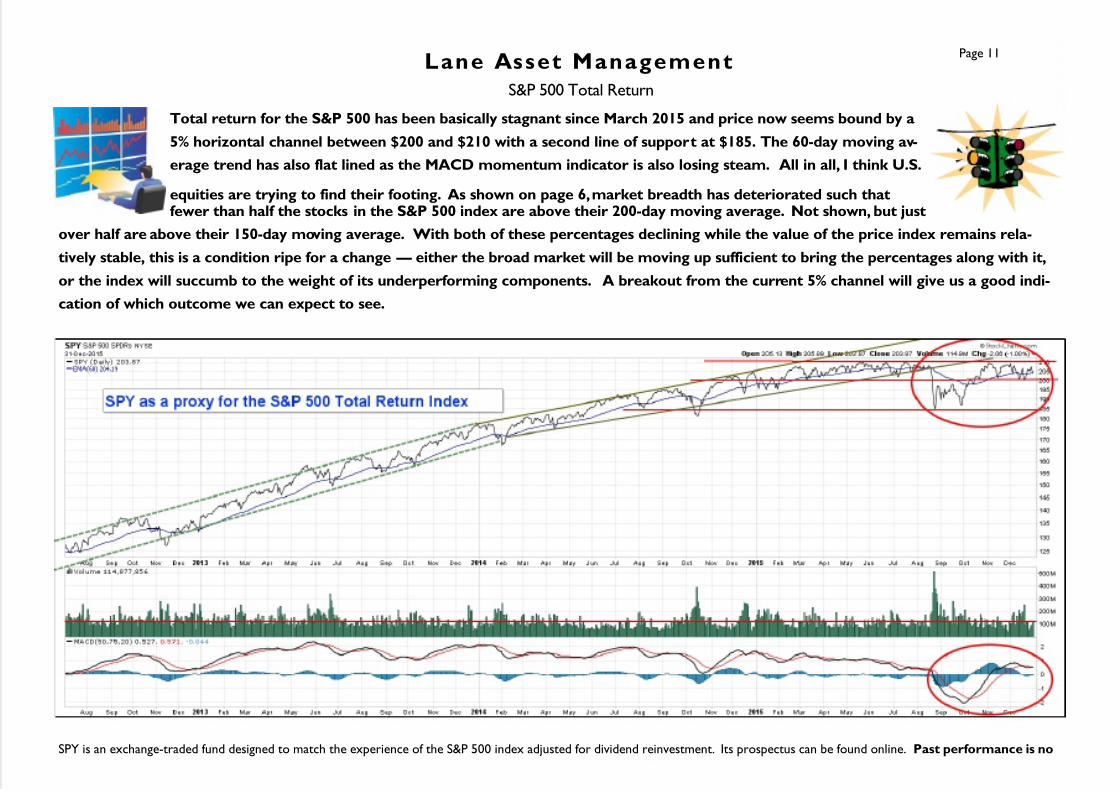

SPY is an exchange-traded fund designed to match the experience of the S&P 500 index adjusted for dividend reinvestment. Its prospectus can be found online. Past performance is no

Page 11Lane Asset Management

Total return for the S&P 500 has been basically stagnant since March 2015 and price now seems bound by a

5% horizontal channel between $200 and $210 with a second line of support at $185. The 60-day moving av-

erage trend has also flat lined as the MACD momentum indicator is also losing steam. All in all, I think U.S.

equities are trying to find their footing. As shown on page 6, market breadth has deteriorated such thatfewer than half the stocks in the S&P 500 index are above their 200-day moving average. Not shown, but just

over half are above their 150-day moving average. With both of these percentages declining while the value of the price index remains rela-

tively stable, this is a condition ripe for a change — either the broad market will be moving up sufficient to bring the percentages along with it,

or the index will succumb to the weight of its underperforming components. A breakout from the current 5% channel will give us a good indi-

cation of which outcome we can expect to see.

S&P 500 Total Return

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 12/20

SPY is an exchange-traded fund designed to match the experience of the S&P 500 index adjusted for dividend reinvestment. Its prospectus can be found online. Past performance is no

guarantee of future results.

Page 12Lane Asset Management

Below is a 20-year weekly chart of the total return for the S&P 500 with a 60-week moving average trend

line and the momentum indicator MACD. A year ago, we were near the top of the uptrend channel with

flattening momentum. Since then, we find the trend line flattening while the momentum is weakening.

With this perspective, we should anticipate a higher likelihood of a correction similar to the one we had inthe Fall. Given other issues, like weakness in global growth and lack of market breadth, a more severe correction cannot be

ruled out. Investors should be prepared for this possibility with either a strategy to lower exposure early (with a plan to re-

enter) or a willingness to ride out a condition that could last for months or longer.

S&P 500 — The Longer Term View

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 13/20

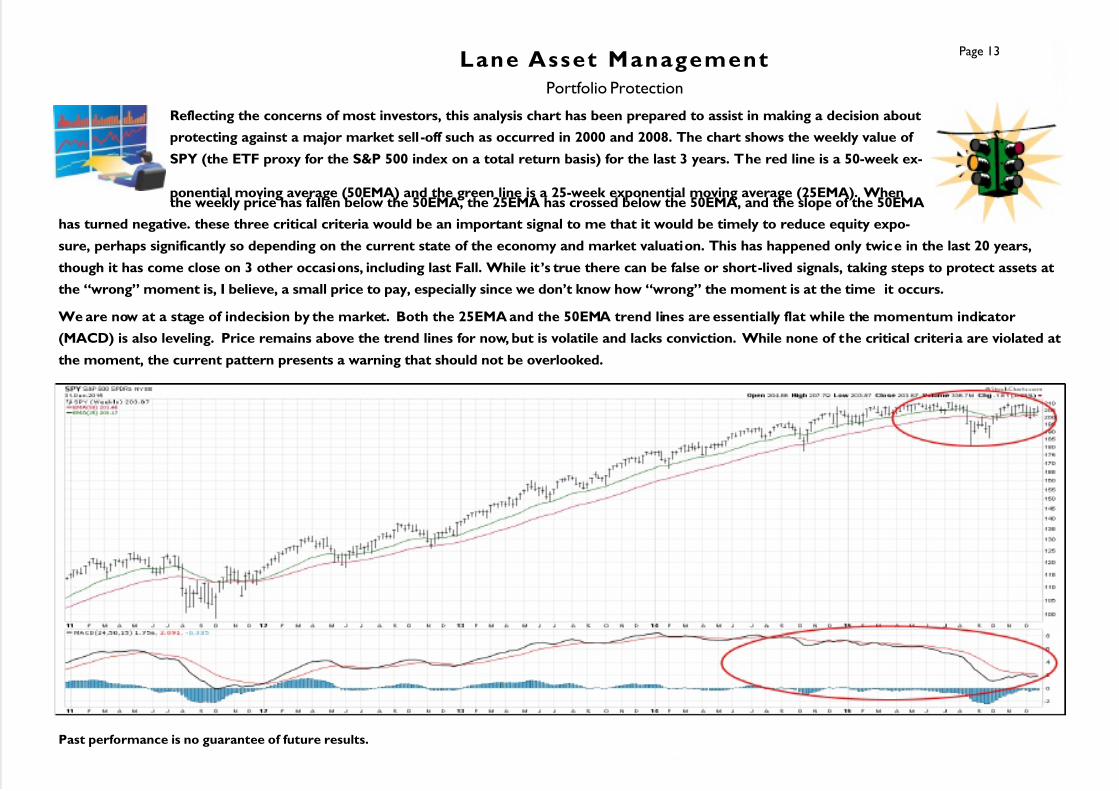

Past performance is no guarantee of future results.

Page 13Lane Asset Management

Reflecting the concerns of most investors, this analysis chart has been prepared to assist in making a decision about

protecting against a major market sell-off such as occurred in 2000 and 2008. The chart shows the weekly value of

SPY (the ETF proxy for the S&P 500 index on a total return basis) for the last 3 years. The red line is a 50-week ex-

ponential moving average (50EMA) and the green line is a 25-week exponential moving average (25EMA). Whenthe weekly price has fallen below the 50EMA, the 25EMA has crossed below the 50EMA, and the slope of the 50EMA

has turned negative. these three critical criteria would be an important signal to me that it would be timely to reduce equity expo-

sure, perhaps significantly so depending on the current state of the economy and market valuation. This has happened only twice in the last 20 years,

though it has come close on 3 other occasions, including last Fall. While it’s true there can be false or short-lived signals, taking steps to protect assets at

the “wrong” moment is, I believe, a small price to pay, especially since we don’t know how “wrong” the moment is at the time it occurs.

We are now at a stage of indecision by the market. Both the 25EMA and the 50EMA trend lines are essentially flat while the momentum indicator

(MACD) is also leveling. Price remains above the trend lines for now, but is volatile and lacks conviction. While none of the critical criteria are violated at

the moment, the current pattern presents a warning that should not be overlooked.

Portfolio Protection

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 14/20

VEU is an exchange-traded fund designed to match the experience of the FTSE All-world (ex U.S.) Index. Its prospectus can be found online. As of 11/30/14, VEU was allocated as follows:

approximately 19% Emerging Markets, 46% Europe, 28% Pacific and about 7% Canada. Past performance is no guarantee of future results.

Page 14Lane Asset Management

International equities, represented here by Vanguard’s all-world (ex US) ETF, VEU, was unable to break

through a previous high just below $51and has now fallen back to a range roughly between $43 and $45.

From a technical perspective, the outlook is turning negative as both the trend and momentum are

weakening. With a 17% weighting in emerging markets, VEU has been buffeted by the weakness in oil and

other commodities — a condition I expect to continue for 2016. But the problems for the broad index go beyond emerging

markets where, except for China and India, the GDP growth outlook for 2016 is below the projected global growth rate.

On the other hand, there are a few countries within the broad index worth a place in a diversified portfolio. Best among the lot as I see it today

would be India despite the weakness in the Bombay stock exchange during 2015. India is projected to have GDP growth in 2016 in excess of 7%,

well above the expected global growth rate. India is not without its structural problems that will take many years to resolve. That said, as a ma-

jor destination for foreign direct investment, the long term outlook is good. Other countries worth examining include Japan and Europe on a

dollar-hedged basis.

All-world (ex U.S.)

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 15/20

SPY and VEU are exchange-traded funds designed to match the experience of the S&P 500, (with dividends) and the FTSE All-world (ex US) index, respectively. Their prospectuses can be

found online. Past performance is no guarantee of future results.

Page 15Lane Asset Management

Asset allocation is the mechanism investors use to enhance gains and reduce volatility over the long term. One useful tool I’ve

found for establishing and revising asset allocation comes from observing the relative performance of major asset sectors (and

within sectors, as well). The chart below shows the relative performance of the S&P 500 (SPY) to the Vanguard All-world (ex U.S.)

index fund (VEU).

In this chart, the relative strength of equities remains in an established up-channel although there has been considerable volatility. I expect the

trend going forward will continue to favor domestic equities.

Asset Allocation and Relative Performance

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 16/20

LQD is an ETF designed to match the experience of the iBoxx Investment Grade Corporate Bond Index. Prospectuses can be found online. Past performance is no guarantee of

future results.

Page 16Lane Asset Management

Investment grade corporate bonds, represented below by LQD, began the year strongly as the yield on

the 10-year Treasury slipped, but eventually were overtaken by the recovery of the 10-year yield as it be-

gan to respond to the increased likelihood of the Fed funds rate increase. At this stage, we have a virtu-

ally flat channel of performance with weakened trend in the last two months along with a loss of mo-

mentum.

One lesson I learned in 2015 after projecting a strong return for LQD at the same time as an increasing 10-year Treasury yield was that the cor-

relation between the two is strongly negative. LQD had a total return in 2015 of negative1.3%, nearly 5% less than its current yield of about

3.5%. With an expectation of a slowly rising 10-year Treasury yield, it would be completely consistent to expect a very small total return for

LQD, if not a negative return in 2016.

Income Investing

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 17/20

SPY and LQD are exchange-traded funds designed to match the experience of the S&P 500, (with dividends) and the iBoxx Investment Grade Corporate Bond Index, respectively. Their

prospectuses can be found online. Past performance is no guarantee of future results.

Page 17Lane Asset Management

In this chart, we see the continuation of a pattern of outperformance of U.S. equities relative to an index of investment grade cor-

porate bonds following a period of reversal last Fall. This pattern reflects the weakness in bonds as interest rates begin to move up.

From a technical, perspective, the trend appears to be continuing and momentum seems to be increasing in favor of equities. That

said, given concerns about equity performance going forward, I would not be overweighting equities at this stage until we have a

more convincing outlook.

Asset Allocation and Relative Performance

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 18/20

PFF seeks to track the investment results of the S&P U.S. Preferred Stock Index (TM) which measures the performance of a select group of preferred stocks . LQD is an ETF designed to

match the experience of the iBoxx Investment Grade Corporate Bond Index. Prospectuses can be found online. Past performance is no guarantee of future results.

Page 18Lane Asset Management

In this chart, we have the relative performance of the S&P U.S. Preferred Stock Index ETF (PFF) to invest-

ment grade corporate bonds showing relative strength of preferred stocks.

While investment grade corporate bonds have been inversely related to the 10-year Treasury yield, the same

has not been true to preferred stocks, especially those of financial institutions, or REITs. In fact, as shown be-

low, there is a generally positive correlation between the yield on the 10-year Treasury bond and the relative

performance of preferred stocks to investment grade corporate bonds, probably driven more by the search for yield more than

the change in the Treasury yield. With the expectation of a slowly rising 10-year Treasury yield, and the improving trend and momentum of the

relative performance with bonds, I believe preferred stocks offer an excellent alternative income-oriented investment.

Income Investing

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 19/20

Page 19Lane Asset Management

This chart shows the relationship of the U.S. dollar (USD) to a basket of developed-economy currencies (the Euro (nearly

60% of the weighting), Yen, British Pound, Canadian Dollar, Swiss Franc and Swedish Krona). Against those currencies, the

USD gained strength in 2014 and 2015, and is now more than half way from the 35-year low established in 2008 to the last

high point reached in 2001-2002.

The strength of the dollar has major implications for U.S. and foreign exports, a headwind for the former and a tailwind for

the latter. While there are multiple factors that affect dollar strength, high on the list is the divergence of U.S. Fed policy (tightening, if slowly)

while policy from the other major central banks are all either standing pat or increasingly accommodative. My expectation is that the dollar

will continue to gain strength, but that the pace will moderate as it has done this year.

U.S. Dollar

7/21/2019 Lane Asset Management 2015 Review and 2016 Fearless Forecast

http://slidepdf.com/reader/full/lane-asset-management-2015-review-and-2016-fearless-forecast 20/20

Edward Lane is a CERTIFIED FINANCIAL PLANNER™. Lane Asset Manage-

ment is a Registered Investment Advisor with the States of NY, CT and

NJ. Advisory services are only offered to clients or prospective clients

where Lane Asset Management and its representatives are properly li-

censed or exempted. No advice may be rendered by Lane Asset Man-

agement unless a client servi ce agreement is in place.

Investing involves risk including loss of principal. Investing in interna-

tional and emerging markets may entail additional risks such as currency

fluctuation and political instability. Investing in small-cap stocks includes

specific risks such as greater volatility and potentially less liquidity.

Small-cap stocks may be subject to higher degree of risk than more es-

tablished companies’ securities. The illiquidity of the small-cap market

may adversely affect the value of these investments.

Investors should consider the investment objectives, risks, and charges

and expenses of mutual funds and exchange-traded funds carefully for a

full background on the possibility that a more suitable securities trans-

action may exist. The prospectus contains this and other information. A

prospectus for all funds is available from Lane Asset Management or

your financial advisor and should be read carefully before investing.

Note that indexes cannot be invested in directly and their performance

may or may not correspond to securities intended to represent these

sectors.

Investors should carefully review their financial situation, making sure

their cash flow needs for the next 3-5 years are secure with a margin

for error. Beyond that, the degree of risk taken in a portfolio should be

commensurate with one’s overall risk tolerance and financial objectives.

The charts and comments are only the author’s view of market activity

and aren’t recommendations to buy or sell any security. Market sectors

Page 20 Lane Asset Management

Disclosures

Periodically, I will prepare a Commentary focusing on a specific investment issue.

Please let me know if there is one of interest to you. As always, I appreciate your feed-

back and look forward to addressing any questions you may have. You can find me at:www.LaneAssetManagement.com

Edward Lane, CFP ®

Lane Asset Management

Kingston, NY

Reprints and quotations are encouraged with attribution.

and related exchanged-traded and closed-end funds are selected based on his opinion

as to their usefulness in providing the viewer a comprehensive summary of market

conditions for the featured period. Chart annotations aren’t predictive of any future

market action rather they only demonstrate the author’s opinion as to a range of pos-

sibilities going forward. All material presented herein is believed to be reliable but its

accuracy cannot be guaranteed. The information contained herein (including historical

prices or values) has been obtained from sources that Lane Asset Management (LAM)considers to be reliable; however, LAM makes no representation as to, or accepts any

responsibility or liability for, the accuracy or completeness of the information con-

tained herein or any decision made or action taken by you or any third party in reli-

ance upon the data. Some results are derived using historical estimations from available

data. Investment recommendations may change without notice and readers are urged

to check with tax advisors before making any investment decisions. Opinions ex-

pressed in these reports may change without prior notice. This memorandum is based

on information available to the public. No representation is made that it is accurate or

complete. This memorandum is not an offer to buy or sell or a solicitation of an offer

to buy or sell the securities mentioned. The investments discussed or recommended in

this report may be unsuitable for investors depending on their specific investment ob-

jectives and financial position. The price or value of the investments to which this re-

port relates, either directly or indirectly, may fall or rise against the interest of inves-

tors. All prices and yields contained in this report are subject to change without notice.

This information is intended for illustrative purposes only. PAST PERFORMANCE

DOES NOT GUARANTEE FUTURE RESULTS.

Related Documents