WINNING PORTFOLIOS POWERED BY KNOWLEDGE ISSUE 12 | April 2022 1 ‘Lallapalooza Effect’

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WINNING PORTFOLIOS

POWERED BY KNOWLEDGE

ISSUE 12 | April 20221

‘Lallapalooza Effect’

Our company name has changed to Motilal Oswal Wealth Ltd formerly known as Motilal Oswal Wealth Management Ltd.

APRIL 2022 | ISSUE 112 2

This document is not valid without disclosure; refer the last page for the disclosure

Readers Speaks ...………………………………………………………………........................................….….........03

Executive Summary………………………………………………………………........................................….…......04

Asset Class Performance ......…....................................................................................................05

Long Term Investing............….................................................................................................06-07

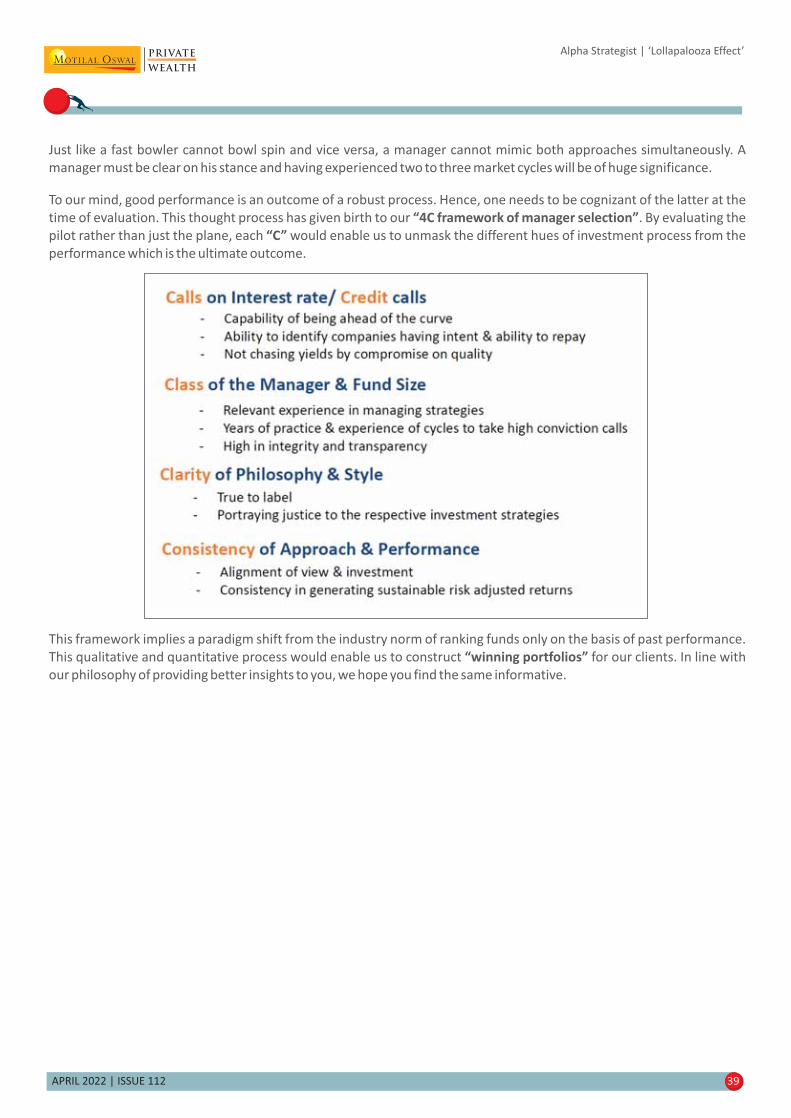

Section I……………………………………………………………….......................................................……….. -08 19

(Market through Graphs Portfolios Commentary, Temperature Gauge, Risk Return Matrix Investment, ,

Grid Our Recommendations,, DELPHI)

S 2 34ection II…………………………………………………….......................................................….……………... 0-

( , , , )Macro Economy Equities Fixed Income Gold

Section III…………………………………………………….........................................................….….……….35 44-

( , ,Advisory Approach 4C Framework For Equity Managers Fixed Income Manager Selection

Framework Hind-sight Investing Decoding Investment Style Investment Charter Sample Investment, , , ,

Charter, Estate Planning

Section VI…………………………………………………….........................................................…….….……. 5-694

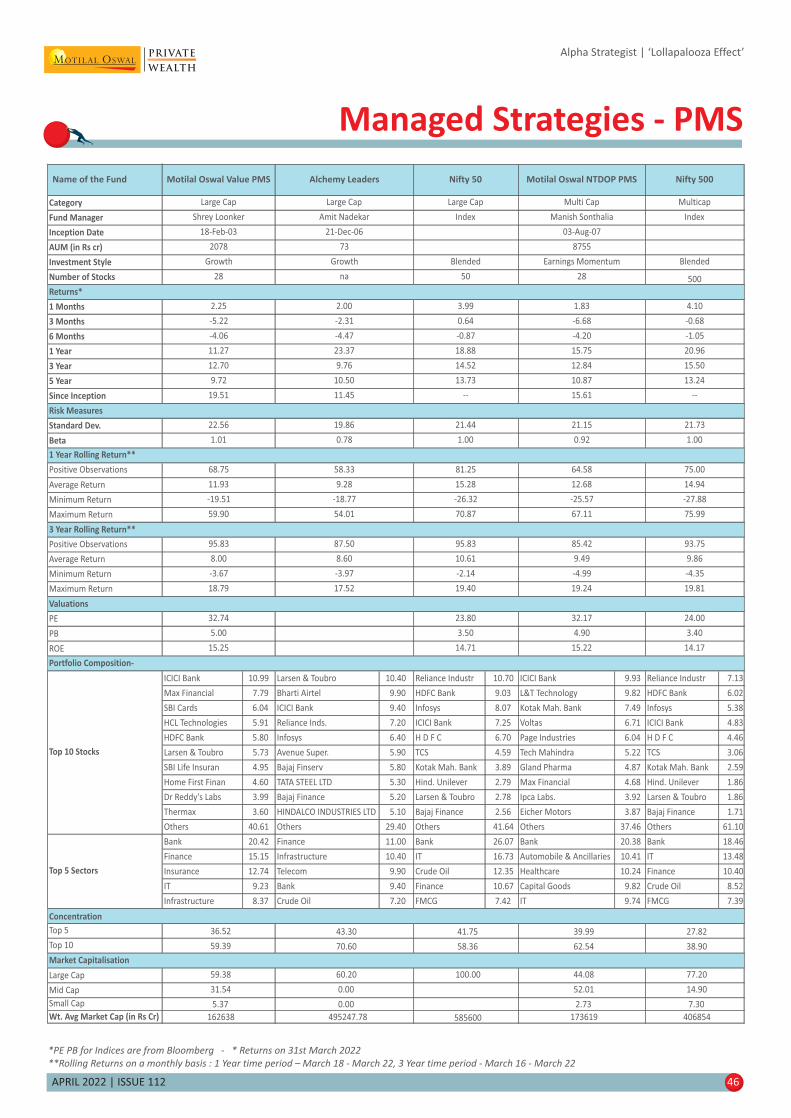

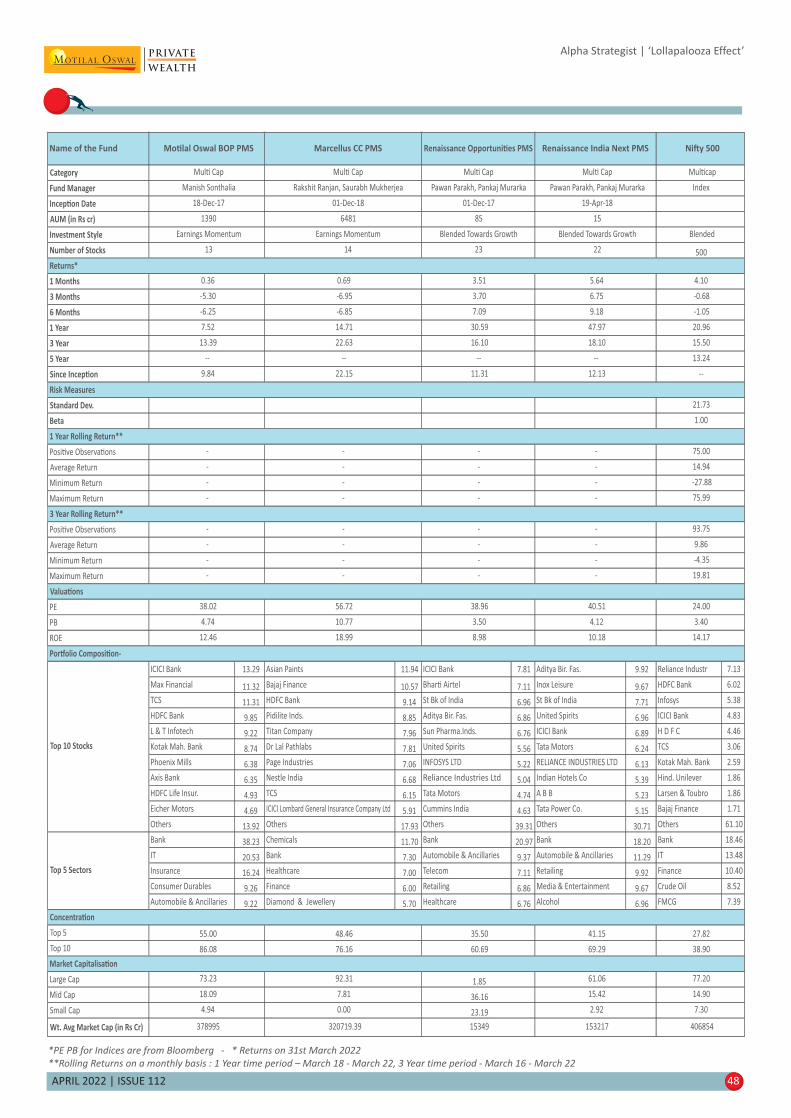

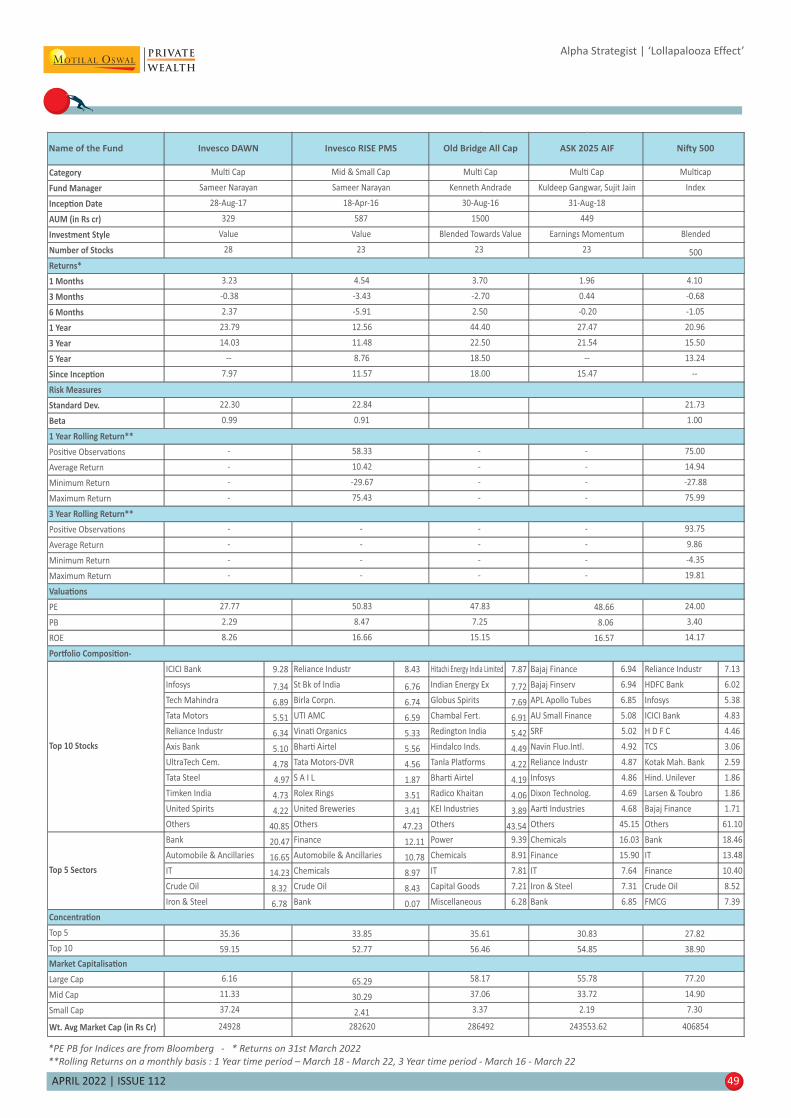

( , , )Managed Strategies - PMS Managed Strategies - MF Investment Charter Template

Alpha Strategist | ‘Lollapalooza Effect’

Contents

Alpha Strategist | ‘Lollapalooza Effect’

Readers Speak

APRIL 2022 | ISSUE 112 3

APRIL 2022 | ISSUE 112 4

Executive Summary

Alpha Strategist | ‘Lollapalooza Effect’

In the current environment, the “ ” is at play. From a short term lens, severalLollapalooza Effect

factors viz. war in Ukraine leading to elevated commodity prices on account of Russia being one of

the major suppliers of key commodities; hike in interest rates, etc. have meant heightened

volatility. Our stance on this being a year of consolidation still holds. From a longer term

viewpoint though, domestic Equity market fundamentals remain robust given healthy balance

sheets, low debt-equity & improving ROEs leading to steady earnings growth outlook. The

longer term vision for India's macro remains positive with gradual progression toward a $6 trillion

economy over the course of this decade.

Nifty50 ended FY22 with gains of 19% YoY, marking another year of strong returns. Given the multitude of challenges

(regional lockdowns due to the second COVID wave, gradual withdrawal of excess global liquidity, relentless rise in

commodity prices, disruption in supply chains, and weak rural demand), the fact that the Nifty is down barely 5% from

its recent high underscores its resilience. Markets never fail to astonish and what has been a pleasant development is

the rise of DIIs investing in equities to the tune of over $26 billion in FY22 countering the outflows by FIIs ($17.1 billion).

Before the breakout of War in Ukraine, the old economy of commodities (Crude Oil, Wheat, Natural Gas etc.) had not

made abnormal returns for the better part of a decade and the scarcity premiums have skyrocketed prices leading to

record profits for large energy companies across the globe; US Inflation scaled to a 40-year peak in February to 7.9%.

Minutes of the Fed meeting signalled it will reduce its substantial bond holdings at a maximum pace of $95 billion per

month compared to $50 billion in the previous cycle in 2017-19 further tightening credit across the economy.

BFSI & IT companies have been somewhat immune to the geopolitical crisis and could continue to do well; Metals &

Mining companies have benefitted on the back of unyielding rise in commodity prices while the same has had a negative

impact on consumption driven companies. Autos, consumer staples and cement could see a decline in margins due to

rising commodity costs in Q4FY22 results while upstream Oil & Gas as well as Metals could see a sharp uptick during the

same period. Almost half of NIFTY 50 companies would not have any direct impact of rising energy prices on its last

quarterly results while 29% will have a positive impact and 18% would gain from rupee depreciation. On a high base,

Nifty50 Q4FY22 PAT is expected to go up 23%.

Our proprietary Temperature Gauge Index indicates that Equity market is in the fair valuation zone. Hence for

incremental allocation to equities, we suggest 50% deployment immediately & 50% to be staggered over a period of 3-6

months. We continue to maintain bias towards Multi cap and select Mid & Small cap strategies across MF/PMS/AIF

platforms.

For the domestic fixed income market, concerns on higher inflation due to rising crude and commodity costs have led to

the yield curve getting steeper. Recently concluded MPC meeting revised growth projections to 7.2% for FY23 from 7.8%

earlier while keeping the rates unchanged and maintaining its accommodative stance. This was in line with RBI's earlier

stance to prioritize sustainable growth trajectory while remaining cognizant about the inflationary risks. Albeit, RBI's

move to replace FRRR with SDF indicates an explicit start of monetary tightening making it clear monetary policy

normalization has started.

For Fixed Income portfolios, we continue to suggest following a barbell portfolio approach i.e. having core allocation to

high quality accrual oriented funds with maturities of 4-6 years, complemented by 20-30% allocation towards long

maturity and high quality roll down strategies. Tactical allocation to select high yield strategies, MLDs, REITs, InvITs can

help enhance the yield on fixed income portfolios. Gold should be treated predominantly as a hedge against heightened

volatility.

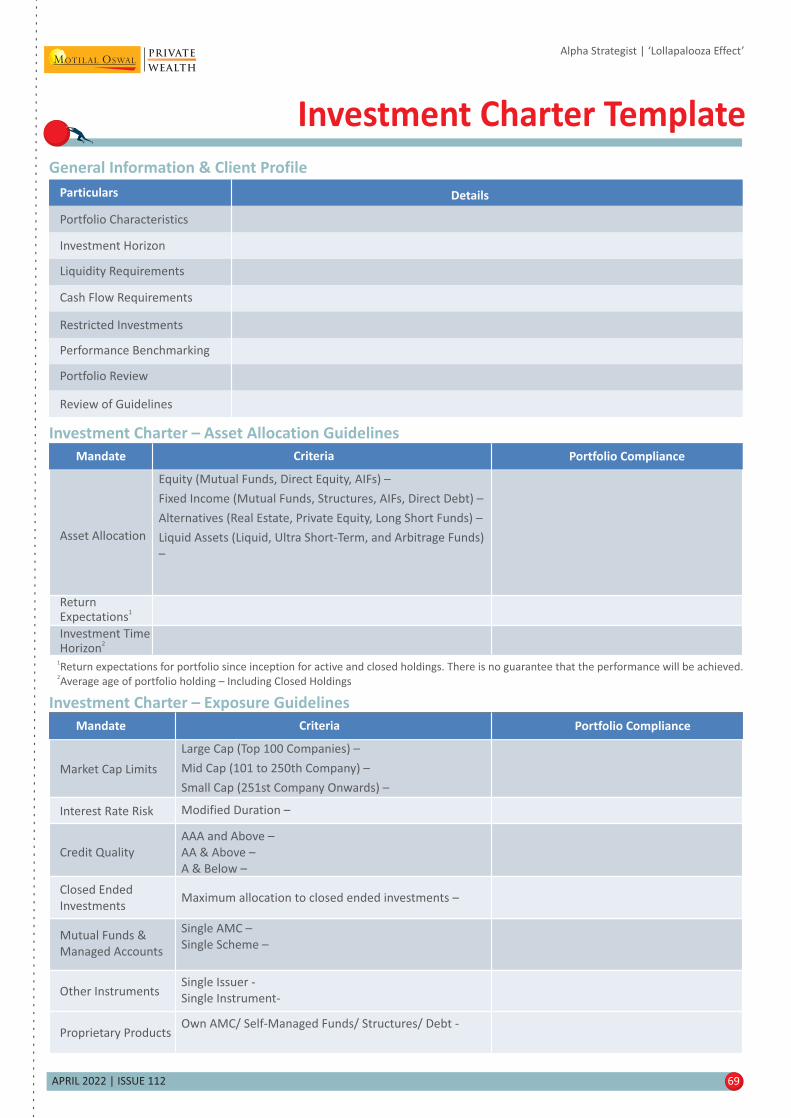

We reiterate emphasis on Investment Charter, Asset Allocation, and a disciplined staggered deployment strategy for

incremental equity investments.

Happy Investing!

Ashish Shanker

(MD & CEO – Private Wealth)

APRIL 2022 | ISSUE 112 5

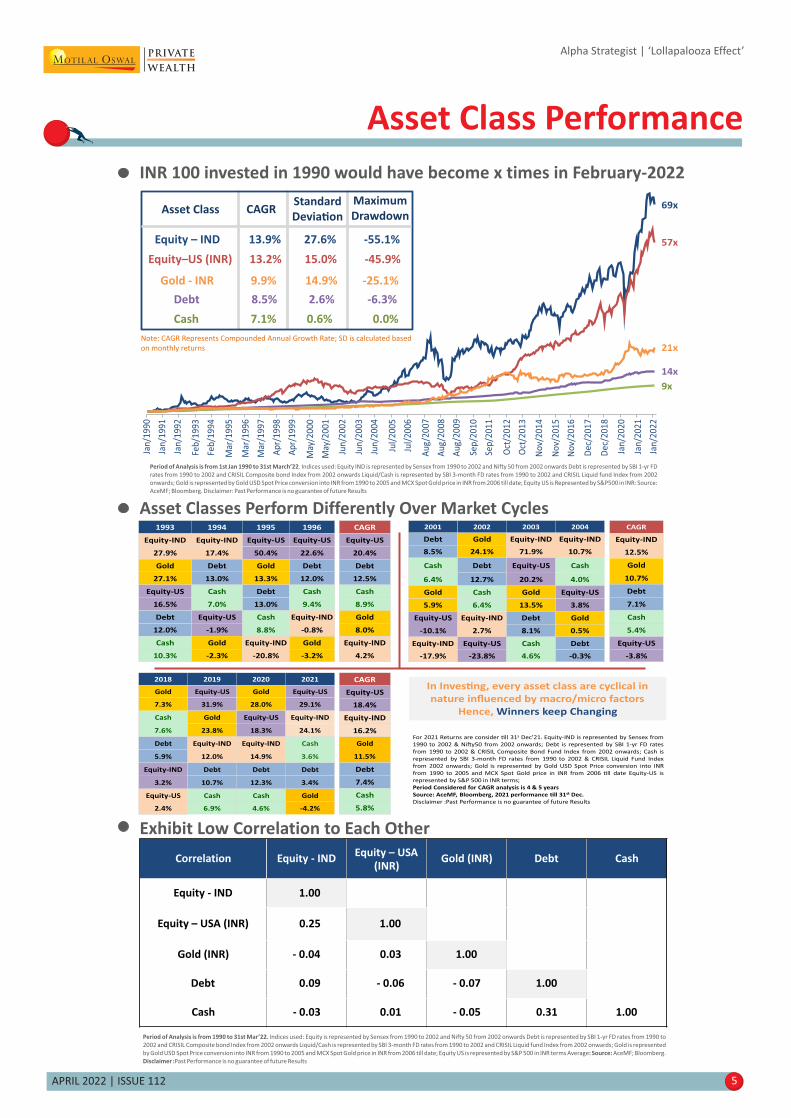

INR 100 invested in 1990 would have become x times in February-2022

Alpha Strategist | ‘Lollapalooza Effect’

A C Performancesset lass

Asset Classes Perform Differently Over Market Cycles

Exhibit Low Correlation to Each Other

Period of Analysis is from 1990 to 31st Mar’22. Indices used: Equity is represented by Sensex from 1990 to 2002 and Nifty 50 from 2002 onwards Debt is represented by SBI 1-yr FD rates from 1990 to

2002 and CRISIL Composite bond Index from 2002 onwards Liquid/Cash is represented by SBI 3-month FD rates from 1990 to 2002 and CRISIL Liquid fund Index from 2002 onwards; Gold is represented

by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR from 2006 till date; Equity US is represented by S&P 500 in INR terms Average AceMF; Bloomberg.: Source:

Disclaimer :Past Performance is no guarantee of future Results

Correlation Equity - INDEquity – USA

(INR)Gold (INR) Debt Cash

Equity - IND

Equity – USA (INR)

Gold (INR)

Debt

Cash

1.00

0.25

- 0.04

0.09

- 0.03

1.00

0.03

- 0.06

0.01

1.00

- 0.07

- 0.05

1.00

0.31 1.00

Period of Analysis is from 1st Jan 1990 to 31st March’22. Indices used: Equity IND is represented by Sensex from 1990 to 2002 and Nifty 50 from 2002 onwards Debt is represented by SBI 1-yr FD

rates from 1990 to 2002 and CRISIL Composite bond Index from 2002 onwards Liquid/Cash is represented by SBI 3-month FD rates from 1990 to 2002 and CRISIL Liquid fund Index from 2002

onwards; Gold is represented by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR from 2006 till date; Equity US is Represented by S&P500 in INR: Source:

AceMF; Bloomberg. Disclaimer: Past Performance is no guarantee of future Results

Cash 7.1% 0.6% 0.0%

Equity – IND 13.9% 27.6% -55.1%

Note: CAGR Represents Compounded Annual Growth Rate; SD is calculated based

on monthly returns

CAGRStandard

Devia�on

Maximum

DrawdownAsset Class

Equity–US (INR) 13.2% 15.0% -45.9%

Gold - INR 9.9% 14.9% -25.1%

Debt 8.5% 2.6% -6.3%

6 x9

5 x7

14x

9x

21x

Jan

/19

90

Jan

/19

91

Jan

/19

92

Feb

/19

93

Feb

/19

94

Mar

/19

95

Mar

/19

96

Mar

/19

97

Ap

r/1

99

8

Ap

r/1

99

9

May

/20

00

May

/20

01

Jun

/20

02

Jun

/20

03

Jun

/20

04

Jul/

20

05

Jul/

20

06

Au

g/2

00

7

Au

g/2

00

8

Au

g/2

00

9

Sep

/20

10

Sep

/20

11

Oct

/20

12

Oct

/20

13

No

v/2

01

4

No

v/2

01

5

No

v/2

01

6

De

c/2

01

7

De

c/2

01

8

Jan

/20

20

Jan

/20

21

Jan

/20

22

1993 1994 1995 1996

Equity-IND Equity-IND Equity-US Equity-US

27.9% 17.4% 50.4% 22.6%

Gold Debt Gold Debt

27.1% 13.0% 13.3% 12.0%

Equity-US Cash Debt Cash

16.5% 7.0% 13.0% 9.4%

Debt Equity-US Cash Equity-IND

12.0% -1.9% 8.8% -0.8%

Cash Gold Equity-IND Gold

10.3% -2.3% -20.8% -3.2%

2001 2002 2003 2004

Debt Gold Equity-IND Equity-IND

8.5% 24.1% 71.9% 10.7%

Cash Debt Equity-US Cash

6.4% 12.7% 20.2% 4.0%

Gold Cash Gold Equity-US

5.9% 6.4% 13.5% 3.8%

Equity-US Equity-IND Debt Gold

-10.1% 2.7% 8.1% 0.5%

Equity-IND Equity-US Cash Debt

-17.9% -23.8% 4.6% -0.3%

CAGR

Equity-US

20.4%

Debt

12.5%

Cash

8.9%

Gold

8.0%

Equity-IND

4.2%

CAGR

Equity-IND

12.5%

Gold

10.7%

Debt

7.1%

Cash

5.4%

Equity-US

-3.8%

In Inves�ng, every asset class are cyclical in

nature influenced by macro/micro factors

Hence, Winners keep Changing

For 2021 Returns are consider �ll 31s Dec’21. Equity-IND is represented by Sensex from

1990 to 2002 & Ni�y50 from 2002 onwards; Debt is represented by SBI 1-yr FD rates

from 1990 to 2002 & CRISIL Composite Bond Fund Index from 2002 onwards; Cash is

represented by SBI 3-month FD rates from 1990 to 2002 & CRISIL Liquid Fund Index

from 2002 onwards; Gold is represented by Gold USD Spot Price conversion into INR

from 1990 to 2005 and MCX Spot Gold price in INR from 2006 �ll date Equity-US is

represented by S&P 500 in INR terms;

Period Considered for CAGR analysis is 4 & 5 years

Source: AceMF, Bloomberg, 2021 performance �ll 31st Dec.

Disclaimer :Past Performance is no guarantee of future Results

CAGR

Equity-US

18.4%

Equity-IND

16.2%

Gold

11.5%

Debt

7.4%

Cash

5.8%

2018 2019 2020 2021

Gold Equity-US Gold Equity-US

7.3% 31.9% 28.0% 29.1%

Cash Gold Equity-US Equity-IND

7.6% 23.8% 18.3% 24.1%

Debt Equity-IND Equity-IND Cash

5.9% 12.0% 14.9% 3.6%

Equity-IND Debt Debt Debt

3.2% 10.7% 12.3% 3.4%

Equity-US Cash Cash Gold

2.4% 6.9% 4.6% -4.2%

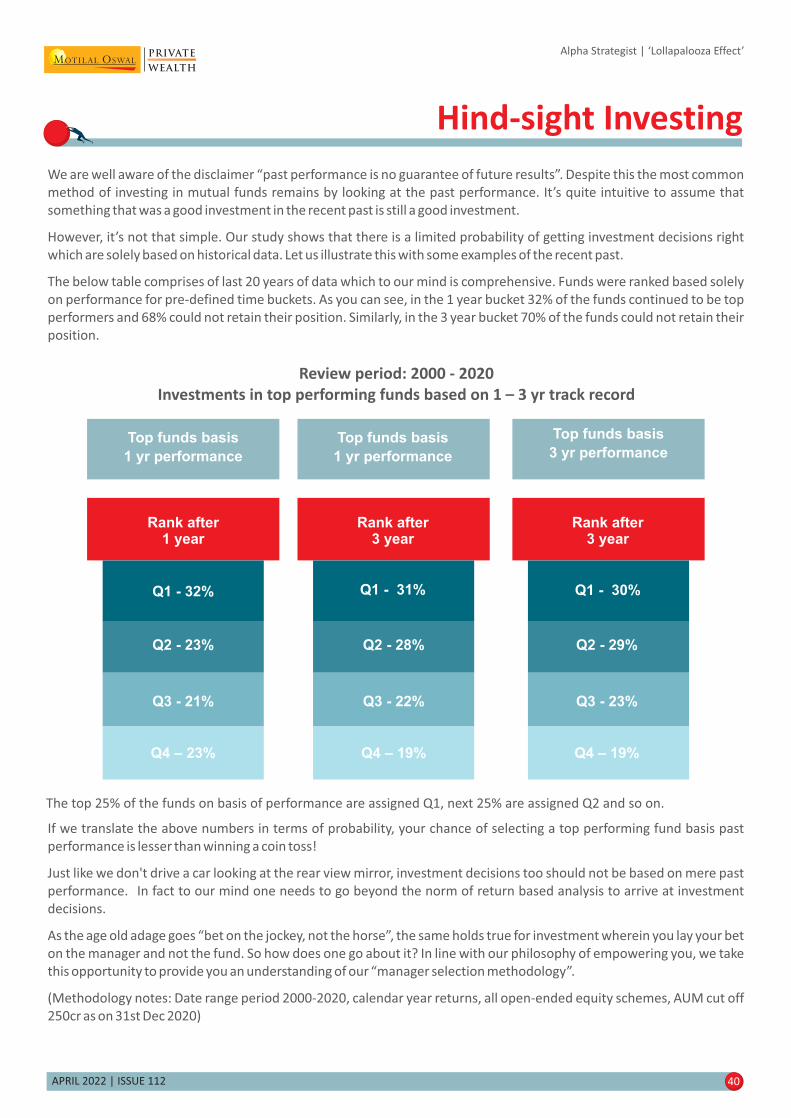

It is common knowledge that investments, when given time to grow, have a much higher chance of reaching their full

potential. One of the most successful and well known investors, Peter Lynch, once mentioned “You get recessions, you

have stock market declines, if you don't understand that's going to happen, then you're not ready, you won't do well in

the markets”. Even though these scenarios mentioned are known to investors, why are they not able to ride through the

cycle? The problem arises when personal capital is invested, as it is simple human nature to notice every small

turbulence that depletes one's capital. Initially an investor may be able to comprehend the situation, but when the bear

market last months or even years, portfolio profits and even capital begin to erode. This is when for most investors,

patience begins to wear thin and fear sets in. In such a mindset, investors end up making impulsive decisions that are

solely based on emotions without realizing that they are doing themselves more harm than good. Therefore we believe

that the key ingredient to healthy investment portfolios is to have a long term vision.

The most common question that then arises is: how long is long term? When it comes to computation of tax on capital

gains, long term is considered as a holding period of one year for equities and a period of three years for debt

instruments. However, from an investment perspective one year is considered as a very short period of time since

volatility can be very high and the investor could suffer losses. The fundamental reason for investing for a long period of

time is to deal with volatility, which can never be predicted. This is why many successful managers strongly believe in the

philosophy of 'Time in the market' as opposed to 'Timing the Market'. In hindsight, even if the entry point might have

been wrong, positive returns can still be made by patiently holding onto the investments and benefitting from the

subsequent rally. Some managers even try to improve their returns by increasing their investments in periods which are

negative or low return phases.

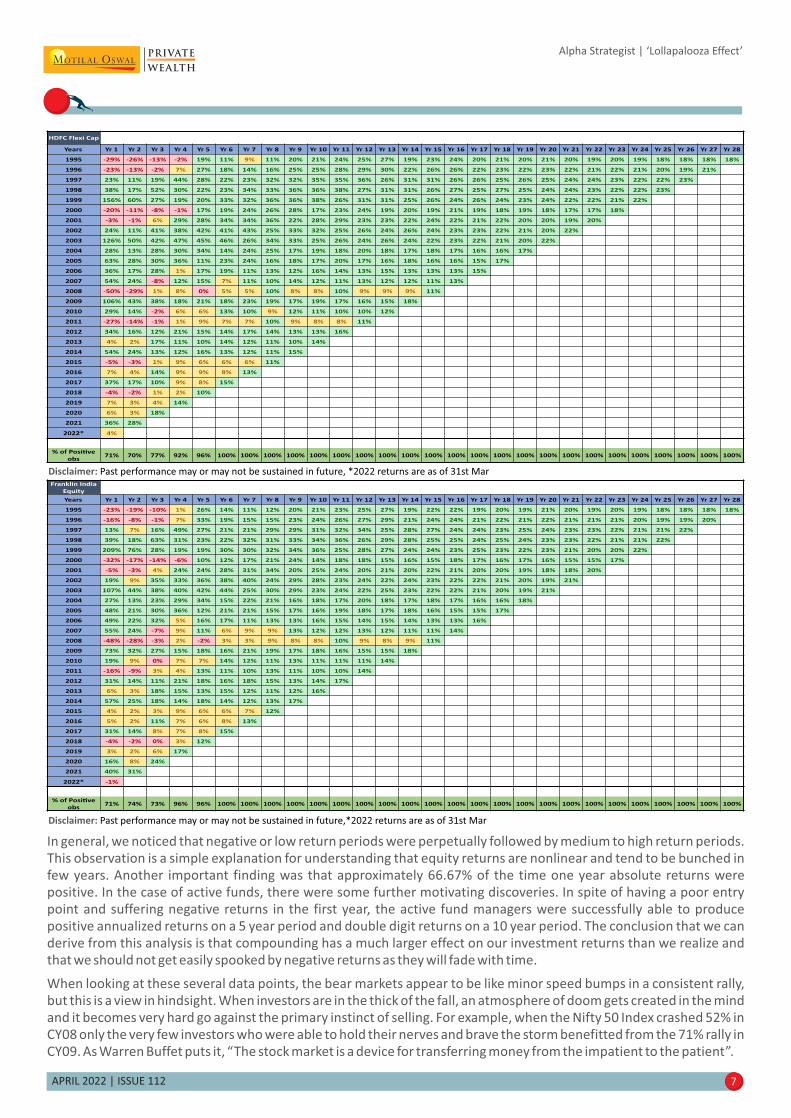

To understand the truth behind these statements, we conducted a small study that tracked the journey of the Nifty 50

Index and two actively managed funds in the last 27 years. We assumed 27 separate investments in each of the funds at

the start of every calendar year. The study yielded some very fascinating discoveries of the equity markets.

APRIL 2022 | ISSUE 112 6

Alpha Strategist | ‘Lollapalooza Effect’

Long Term Investing

Disclaimer: Past performance may or may not be sustained in future, *2022 returns are as of 31st Mar

Ni�y 50

Years Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12 Yr 13 Yr 14 Yr 15 Yr 16 Yr 17 Yr 18 Yr 19 Yr 20 Yr 21 Yr 22 Yr 23 Yr 24 Yr 25 Yr 26 Yr 27 Yr 28

1995 -23% -13% -3% -7% 5% 1% -2% -1% 5% 6% 8% 11% 14% 7% 10% 11% 8% 9% 9% 10% 9% 9% 10% 10% 10% 10% 10% 10%

1996 -1% -1% 6% -1% 10% 6% 2% 2% 8% 9% 11% 13% 16% 9% 12% 13% 10% 11% 11% 12% 11% 11% 11% 11% 11% 11% 12%

1997 20% 10% -1% 13% 7% 3% 3% 10% 10% 12% 14% 17% 10% 13% 14% 11% 12% 11% 12% 12% 11% 12% 11% 11% 12% 12%

1998 -18% -9% 11% 4% 0% 0% 8% 9% 11% 14% 17% 9% 13% 13% 10% 11% 11% 12% 11% 11% 11% 11% 11% 11% 12%

1999 67% 29% 13% 5% 4% 13% 13% 16% 18% 21% 12% 16% 16% 13% 13% 13% 14% 13% 12% 13% 13% 13% 13% 14%

2000 -15% -8% -11% -7% 5% 6% 10% 13% 17% 7% 12% 13% 9% 10% 10% 11% 10% 10% 11% 10% 11% 11% 12%

2001 -16% -8% -5% 10% 10% 14% 18% 22% 10% 15% 15% 11% 13% 12% 13% 12% 12% 13% 12% 12% 12% 13%

2002 3% 2% 21% 18% 22% 25% 29% 14% 19% 19% 14% 15% 15% 16% 14% 14% 14% 14% 14% 14% 15%

2003 72% 31% 24% 27% 29% 33% 15% 22% 21% 16% 17% 16% 17% 15% 14% 15% 14% 14% 14% 15%

2004 11% 5% 15% 21% 27% 8% 16% 16% 11% 12% 12% 13% 12% 11% 12% 12% 12% 12% 13%

2005 36% 17% 24% 31% 7% 16% 17% 10% 12% 12% 13% 12% 11% 12% 12% 12% 12% 13%

2006 40% 18% 29% 1% 13% 14% 7% 10% 9% 11% 10% 9% 11% 10% 10% 10% 12%

2007 55% 24% -9% 7% 9% 3% 6% 6% 9% 7% 7% 8% 8% 8% 9% 10%

2008 -52% -31% -5% 0% -6% -1% 0% 4% 3% 3% 5% 5% 5% 6% 8%

2009 76% 33% 28% 12% 15% 13% 16% 13% 12% 14% 13% 13% 13% 14%

2010 18% 9% -4% 3% 4% 8% 6% 6% 8% 8% 8% 9% 10%

2011 -25% -13% -1% 1% 6% 4% 4% 7% 7% 7% 8% 10%

2012 28% 13% 11% 16% 11% 10% 12% 11% 11% 12% 14%

2013 7% 3% 12% 8% 7% 10% 9% 9% 10% 12%

2014 31% 15% 8% 7% 11% 9% 10% 10% 13%

2015 -4% -2% 0% 6% 6% 7% 8% 11%

2016 3% 1% 10% 8% 9% 10% 13%

2017 29% 13% 10% 10% 11% 15%

2018 3% 2% 5% 7% 12%

2019 12% 6% 9% 16%

2020 15% 7% 17%

2021 24% 19%

2022* 1%

% of Posi�ve

obs71% 70% 65% 84% 92% 96% 95% 95% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

APRIL 2022 | ISSUE 112 7

In general, we noticed that negative or low return periods were perpetually followed by medium to high return periods.

This observation is a simple explanation for understanding that equity returns are nonlinear and tend to be bunched in

few years. Another important finding was that approximately 66.67% of the time one year absolute returns were

positive. In the case of active funds, there were some further motivating discoveries. In spite of having a poor entry

point and suffering negative returns in the first year, the active fund managers were successfully able to produce

positive annualized returns on a 5 year period and double digit returns on a 10 year period. The conclusion that we can

derive from this analysis is that compounding has a much larger effect on our investment returns than we realize and

that we should not get easily spooked by negative returns as they will fade with time.

When looking at these several data points, the bear markets appear to be like minor speed bumps in a consistent rally,

but this is a view in hindsight. When investors are in the thick of the fall, an atmosphere of doom gets created in the mind

and it becomes very hard go against the primary instinct of selling. For example, when the Nifty 50 Index crashed 52% in

CY08 only the very few investors who were able to hold their nerves and brave the storm benefitted from the 71% rally in

CY09. As Warren Buffet puts it, “The stock market is a device for transferring money from the impatient to the patient”.

Alpha Strategist | ‘Lollapalooza Effect’

Disclaimer: Past performance may or may not be sustained in future, *2022 returns are as of 31st Mar

Disclaimer: Past performance may or may not be sustained in future,*2022 returns are as of 31st Mar

HDFC Flexi Cap

Years Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12 Yr 13 Yr 14 Yr 15 Yr 16 Yr 17 Yr 18 Yr 19 Yr 20 Yr 21 Yr 22 Yr 23 Yr 24 Yr 25 Yr 26 Yr 27 Yr 28

1995 -29% -26% -13% -2% 19% 11% 9% 11% 20% 21% 24% 25% 27% 19% 23% 24% 20% 21% 20% 21% 20% 19% 20% 19% 18% 18% 18% 18%

1996 -23% -13% -2% 7% 27% 18% 14% 16% 25% 25% 28% 29% 30% 22% 26% 26% 22% 23% 22% 23% 22% 21% 22% 21% 20% 19% 21%

1997 23% 11% 19% 44% 28% 22% 23% 32% 32% 35% 35% 36% 26% 31% 31% 26% 26% 25% 26% 25% 24% 24% 23% 22% 22% 23%

1998 38% 17% 52% 30% 22% 23% 34% 33% 36% 36% 38% 27% 31% 31% 26% 27% 25% 27% 25% 24% 24% 23% 22% 22% 23%

1999 156% 60% 27% 19% 20% 33% 32% 36% 36% 38% 26% 31% 31% 25% 26% 24% 26% 24% 23% 24% 22% 22% 21% 22%

2000 -20% -11% -8% -1% 17% 19% 24% 26% 28% 17% 23% 24% 19% 20% 19% 21% 19% 18% 19% 18% 17% 17% 18%

2001 -3% -1% 6% 29% 28% 34% 34% 36% 22% 28% 29% 23% 23% 22% 24% 22% 21% 22% 20% 20% 19% 20%

2002 24% 11% 41% 38% 42% 41% 43% 25% 33% 32% 25% 26% 24% 26% 24% 23% 23% 22% 21% 20% 22%

2003 126% 50% 42% 47% 45% 46% 26% 34% 33% 25% 26% 24% 26% 24% 22% 23% 22% 21% 20% 22%

2004 28% 13% 28% 30% 34% 14% 24% 25% 17% 19% 18% 20% 18% 17% 18% 17% 16% 16% 17%

2005 63% 28% 30% 36% 11% 23% 24% 16% 18% 17% 20% 17% 16% 18% 16% 16% 15% 17%

2006 36% 17% 28% 1% 17% 19% 11% 13% 12% 16% 14% 13% 15% 13% 13% 13% 15%

2007 54% 24% -8% 12% 15% 7% 11% 10% 14% 12% 11% 13% 12% 12% 11% 13%

2008 -50% -29% 1% 8% 0% 5% 5% 10% 8% 8% 10% 9% 9% 9% 11%

2009 106% 43% 38% 18% 21% 18% 23% 19% 17% 19% 17% 16% 15% 18%

2010 29% 14% -2% 6% 6% 13% 10% 9% 12% 11% 10% 10% 12%

2011 -27% -14% -1% 1% 9% 7% 7% 10% 9% 8% 8% 11%

2012 34% 16% 12% 21% 15% 14% 17% 14% 13% 13% 16%

2013 4% 2% 17% 11% 10% 14% 12% 11% 10% 14%

2014 54% 24% 13% 12% 16% 13% 12% 11% 15%

2015 -5% -3% 1% 9% 6% 6% 6% 11%

2016 7% 4% 14% 9% 9% 8% 13%

2017 37% 17% 10% 9% 8% 15%

2018 -4% -2% 1% 2% 10%

2019 7% 3% 4% 14%

2020 6% 3% 18%

2021 36% 28%

2022* 4%

% of Posi�ve

obs71% 70% 77% 92% 96% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Franklin India

Equity

Years Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12 Yr 13 Yr 14 Yr 15 Yr 16 Yr 17 Yr 18 Yr 19 Yr 20 Yr 21 Yr 22 Yr 23 Yr 24 Yr 25 Yr 26 Yr 27 Yr 28

1995 -23% -19% -10% 1% 26% 14% 11% 12% 20% 21% 23% 25% 27% 19% 22% 22% 19% 20% 19% 21% 20% 19% 20% 19% 18% 18% 18% 18%

1996 -16% -8% -1% 7% 33% 19% 15% 15% 23% 24% 26% 27% 29% 21% 24% 24% 21% 22% 21% 22% 21% 21% 21% 20% 19% 19% 20%

1997 13% 7% 16% 49% 27% 21% 21% 29% 29% 31% 32% 34% 25% 28% 27% 24% 24% 23% 25% 24% 23% 23% 22% 21% 21% 22%

1998 39% 18% 63% 31% 23% 22% 32% 31% 33% 34% 36% 26% 29% 28% 25% 25% 24% 25% 24% 23% 23% 22% 21% 21% 22%

1999 209% 76% 28% 19% 19% 30% 30% 32% 34% 36% 25% 28% 27% 24% 24% 23% 25% 23% 22% 23% 21% 20% 20% 22%

2000 -32% -17% -14% -6% 10% 12% 17% 21% 24% 14% 18% 18% 15% 16% 15% 18% 17% 16% 17% 16% 15% 15% 17%

2001 -5% -3% 4% 24% 24% 28% 31% 34% 20% 25% 24% 20% 21% 20% 22% 21% 20% 20% 19% 18% 18% 20%

2002 19% 9% 35% 33% 36% 38% 40% 24% 29% 28% 23% 24% 22% 24% 23% 22% 22% 21% 20% 19% 21%

2003 107% 44% 38% 40% 42% 44% 25% 30% 29% 23% 24% 22% 25% 23% 22% 22% 21% 20% 19% 21%

2004 27% 13% 23% 29% 34% 15% 22% 21% 16% 18% 17% 20% 18% 17% 18% 17% 16% 16% 18%

2005 48% 21% 30% 36% 12% 21% 21% 15% 17% 16% 19% 18% 17% 18% 16% 15% 15% 17%

2006 49% 22% 32% 5% 16% 17% 11% 13% 13% 16% 15% 14% 15% 14% 13% 13% 16%

2007 55% 24% -7% 9% 11% 6% 9% 9% 13% 12% 12% 13% 12% 11% 11% 14%

2008 -48% -28% -3% 2% -2% 3% 3% 9% 8% 8% 10% 9% 8% 9% 11%

2009 73% 32% 27% 15% 18% 16% 21% 19% 17% 18% 16% 15% 15% 18%

2010 19% 9% 0% 7% 7% 14% 12% 11% 13% 11% 11% 11% 14%

2011 -16% -9% 3% 4% 13% 11% 10% 13% 11% 10% 10% 14%

2012 31% 14% 11% 21% 18% 16% 18% 15% 13% 14% 17%

2013 6% 3% 18% 15% 13% 15% 12% 11% 12% 16%

2014 57% 25% 18% 14% 18% 14% 12% 13% 17%

2015 4% 2% 3% 9% 6% 6% 7% 12%

2016 5% 2% 11% 7% 6% 8% 13%

2017 31% 14% 8% 7% 8% 15%

2018 -4% -2% 0% 3% 12%

2019 3% 2% 6% 17%

2020 16% 8% 24%

2021 40% 31%

2022* -1%

% of Posi�ve

obs71% 74% 73% 96% 96% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

This document is not valid without disclosure; refer the last page for the disclosure

APRIL 2022 | ISSUE 112 8

Alpha Strategist | ‘Lollapalooza Effect’

Market through Graphs................................................................ .. .... .09........... .. .....

Portfolios Commentary.........................................................................................10

Temperature Gauge.............................................................................................12

Risk Return Matrix ...............................................................................................14

Investment Grid...................................................................................................15

Our Recommendations.........................................................................................16

DELPHI ............................................... .................................................................18

Section I

Alpha Strategist | ‘Lollapalooza Effect’

Market through Graphs

APRIL 2022 | ISSUE 112 9

Summary

Equity

Fixed Income High quality accrual funds (Short and Long term maturity)Barbell approach

Sovereign Gold Bonds, Gold ETF/FoFPositive Positive

Recommendations

Gold

Bias towards Multi cap strategies with select Mid

and Small cap strategies in MF/PMS/AIF platformsNeutral Positive

Economy

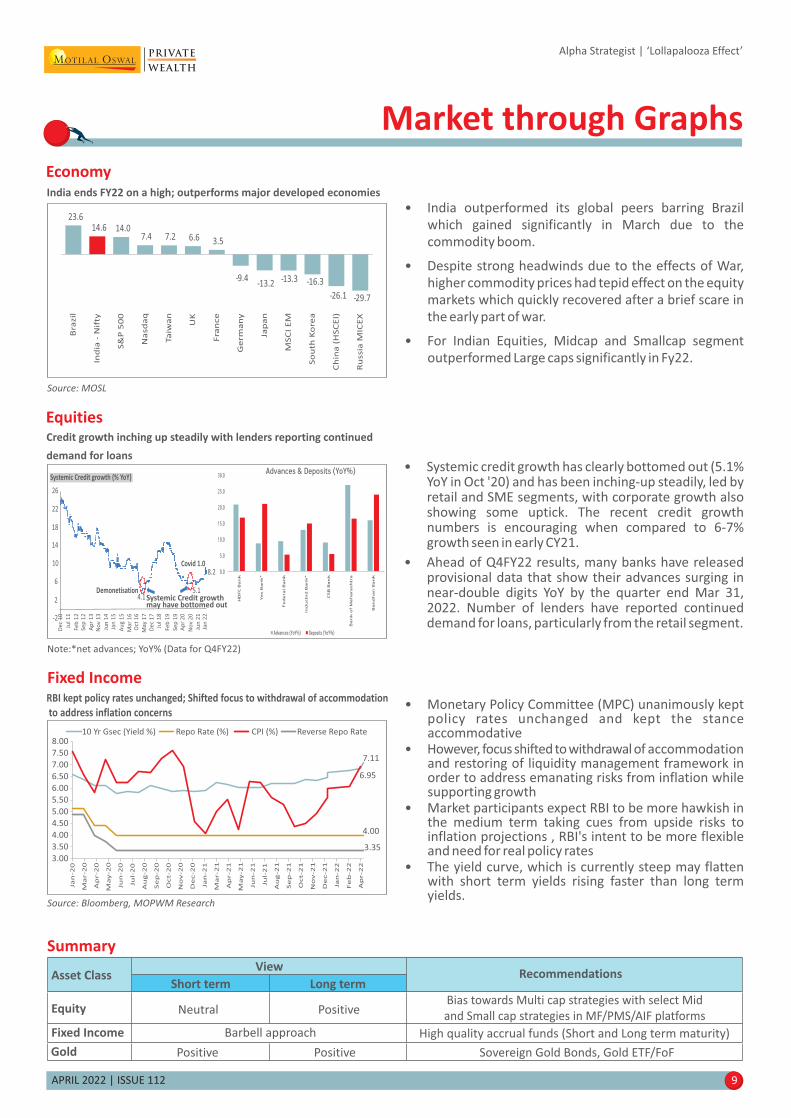

EquitiesCredit growth inching up steadily with lenders reporting continued

demand for loans• Systemic credit growth has clearly bottomed out (5.1%

YoY in Oct '20) and has been inching-up steadily, led byretail and SME segments, with corporate growth alsoshowing some uptick. The recent credit growthnumbers is encouraging when compared to 6-7%growth seen in early CY21.

• Ahead of Q4FY22 results, many banks have releasedprovisional data that show their advances surging innear-double digits YoY by the quarter end Mar 31,2022. Number of lenders have reported continueddemand for loans, particularly from the retail segment.

Note:*net advances; YoY% (Data for Q4FY22)

• India outperformed its global peers barring Brazil

which gained significantly in March due to the

commodity boom.

• Despite strong headwinds due to the effects of War,

higher commodity prices had tepid effect on the equity

markets which quickly recovered after a brief scare in

the early part of war.

• For Indian Equities, Midcap and Smallcap segment

outperformed Large caps significantly in Fy22.

India ends FY22 on a high; outperforms major developed economies

Source: MOSL

23.614.6 14.0

7.4 7.2 6.6 3.5

-9.4-13.2 -13.3 -16.3

-26.1 -29.7

Bra

zil

Ind

ia -

Nif

ty

S&

P 5

00

Na

sd

aq

Ta

iwa

n

UK

Fra

nce

Ge

rma

ny

Jap

an

MS

CI

EM

So

uth

Ko

rea

Ch

ina

(H

SC

EI)

Ru

ssia

MIC

EX

Fixed IncomeRBI kept policy rates unchanged; Shifted focus to withdrawal of accommodation

to address inflation concerns

Source: Bloomberg, MOPWM Research

7.11

4.00

6.95

3.35

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Ja

n-2

0

Ma

r-2

0

Ap

r-2

0

Ma

y-2

0

Ju

n-2

0

Ju

l-2

0

Au

g-2

0

Se

p-2

0

Oct-2

0

No

v-2

0

De

c-2

0

Ja

n-2

1

Ma

r-2

1

Ap

r-2

1

Ma

y-2

1

Ju

n-2

1

Ju

l-2

1

Au

g-2

1

Se

p-2

1

Oct-2

1

No

v-2

1

De

c-2

1

Ja

n-2

2

Fe

b-2

2

Ap

r-2

2

10 Yr Gsec (Yield %) Repo Rate (%) CPI (%) Reverse Repo Rate

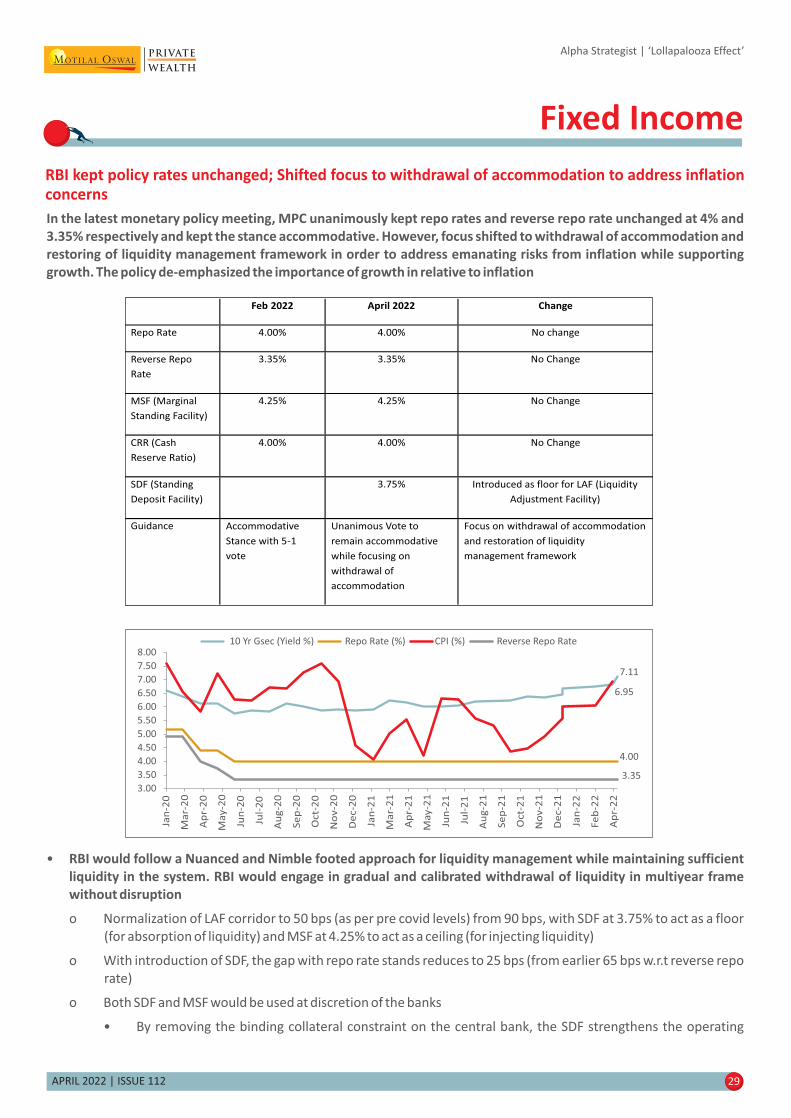

• Monetary Policy Committee (MPC) unanimously keptpolicy rates unchanged and kept the stanceaccommodative

• However, focus shifted to withdrawal of accommodationand restoring of liquidity management framework inorder to address emanating risks from inflation whilesupporting growth

• Market participants expect RBI to be more hawkish inthe medium term taking cues from upside risks toinflation projections , RBI's intent to be more flexibleand need for real policy rates

• The yield curve, which is currently steep may flattenwith short term yields rising faster than long termyields.

26

22

18

14

10

-2

De

c 1

0

Jul 1

1

Feb

12

Se

p 1

2

Ap

r 1

3N

ov

13

Jun

14

Jan

15

De

c 1

7

Au

g 1

5

Jul 1

8

Feb

19

Se

p 1

9A

pr

20

No

v 2

0

Jun

21

Jan

22

Ma

r 1

6O

ct 1

6

Ma

y 1

7

Systemic Credit growth (% YoY)

6

2Demonetisation

Systemic Credit growthmay have bottomed out

5.14.1

Covid 1.08.2

Tactical changes and strategies

� February 2013 –Reduced allocation to Gold by 25% and increased to Dynamic Bond Funds based on discussion in the Investment

Committee meeting

� April 2013 – Reduced further allocation to Gold by 25% and increased to Dynamic Bond Funds based on discussion in the

Investment Committee meeting

� May 2013 – Exited Gilt Fund's and moved to Short-term Funds (40%), Income Funds (40%) and Dynamic Bond Funds (20%) based

on the note released - “Yields came tumbling after…to plummet further”

� July 2013 – Exited Income Funds and other long duration investments and invested the redemption proceeds in Ultra Short-term

Funds based on the note released – “Ride the Tide”

� September 2013 – Cash allocation brought back to its strategic weight and invested the balance allocation into gilt funds based

on the note released – ; Switched 15% of equity allocation to Information Technology (IT) sector funds from large“The Gilt Edge”

cap and multi cap funds, based on the note released – ; Reduced 10% of“Information Technology – In a position on strength”

equity allocation and switched to ultra-short term funds based on the note released – “The Bear-nanke Hug– Underweight

Equities

� November 2013 – Switched 50% of Short-term Funds allocation to Gilt Funds, to increase duration of the portfolio, based on the

note released – ; Deployed Cash in Nifty ETFs, based on the note released –“Time to Rebuild Duration –A Déjà vu” “Equity

Markets – An Update”

� December 2013 – Switched all cash positions to gilt funds, to further increase duration of the portfolio

� May 5, 2014 – Reduced allocation to Gilts and moved to Ultra Short term Funds to create liquidity in the portfolio; Switched

allocation from IT Sector Funds and Nifty ETFs to Infrastructure Funds and Small cap Funds respectively, based on the note

released – “Good Times Ahead!”

� September 2014 – Switched allocation from Cash to Gilt funds, to increase the duration of the portfolio based on the note “Way

Ahead for Duration”; Switched allocation from Small & Midcap funds to Large Cap funds, on the back of relatively higher

valuations of midcaps as compared to large cap; on the fundamental front, demand side continues to be supportive for gold. We

have thereby revised out short term outlook on gold from underweight to neutral stance

� February 2016 – Reduced Gilt exposure and allocated the proceeds towards Gold, on the back of better risk reward scenario for

gold & bond yields coming below it long term average

� April 2016 – Switched allocation from Duration strategies to Accrual strategies, based on the note released – “Time to Shift

Gears”

� May 2018 – In Fixed Income, we reiterate our stance on accrual strategy, however, given the current valuations, tactical allocation

to dynamic bond funds can be considered by investors who can withstand interest rate volatility; Increase allocation towards

value oriented multi-cap strategies

� November 2018 - Recommended arbitrage fund with minimum 6 months investment horizon; put a hold on long duration accrual

strategies; Focus on multi cap and staggered investment to mid & small cap strategies; shift to high quality AAA rated high

accrual debt funds

� January 2019 – We favor a combination of multi cap strategies within Equity MFs and selected high conviction portfolios within

the PMS/AIF platform, we recommend high quality accrual funds for incremental investment in fixed income; we have changed

our stance to positive for gold in long term

� June 2019 -We favour a combination of Multi cap and Mid & Small cap strategies in MF/PMS/AIF platforms, we change our stance

on gold to neutral in long term and maintain neutral stance in short term

� July 2019 - Increased allocation to high quality “AAA” accrual strategies to benefit from the corporate bond spreads

� August 2019 - Increase allocation to Equity in a staggered manner for the next six months; we have changed our stance to positive

for gold in long term

� September 2019 – For incremental investment in equities we revise our stance to invest in lumpsum from staggered

� March 2020 – For incremental investment in equities we revise our stance to from lumpsum to staggered investment over the next

6 -12months

� April 2020 – Biased towards Large cap & Multicap strategies in MF/PMS/AIF platforms for incremental Equity Investment

� May 2020 - Recommended arbitrage fund with minimum 6 months investment horizon; put a hold on long duration accrual

strategies

� June 2020 - For incremental investment in equities we revise our stance to staggered investment over the next 3 - 6months biased

towards Multicap strategies in MF/PMS/AIF platforms

APRIL 2022 | ISSUE 112 10

Alpha Strategist | ‘Lollapalooza Effect’

Portfolio Commentary

APRIL 2022 | ISSUE 112 11

Alpha Strategist | ‘Lollapalooza Effect’

Investment CommitteeCommittee Members

Ashish Shanker – MD , Private Wealth& CEO

Gautam Duggad – Head of Research, Institutional Equities, MOSL

Kishore Narne – Head, Commodities & Currency

Nikhil Gupta – Economist, MOSL

Nitin Shanbhag – Head, Investment Products, Private Wealth

Product Team, Private Wealth

ExternalSpeakers: ExternalSpeakers:Mr.Shreyash Devalkar (SeniorFund Manager–Equity,Axis AMC)

and Mr.R.Sivakumar( Head - Fixed Income,Axis AMC)

� July 2020 – For incremental allocation in equity, we recommend to increase allocation by investing 50% immediately and the

balance in a staggered manner in Multicap strategies(MFs, PMS, AIF) over the next 3-6months

� October 2020 – For incremental allocation in equity, we recommend to increase allocation in a staggered manner in Multicap

strategies(MFs, PMS, AIF) over the next 3-6months; fixed income allocation can be complemented by tactical investments in select

credit oriented funds, high yield NCDs, bonds & MLDs

� November 2020 - To enhance the overall portfolio yield, investors with medium to high risk profile can consider 15 – 20% allocation

of the overall fixed income portfolio to select MLDs, NCDs and credit oriented strategies

� January 2021 -We change our stance in Gold to neutral in short term from positive

� February 2021 -We recommend to invest 50%in lumpsum and 50%in a staggered manner over the next 3-6months in Multi cap and

select Mid & Small Cap strategies(MFs, PMS, AIF); We recommend a barbell approach where 'Accrual' should precede 'Duration'

and the overall portfolio average maturity should be between 2-5 years with sufficient long term investment horizon according to

the investor's risk return profile

� June 2021 -We change our short term stance in Gold to Positive from Neutral

� July 2021 – In Fixed Income, we recommend a barbell approach where 'Accrual' should precede 'Duration' and the overall portfolio

average maturity should be between 4-6 years with long term investment horizon; To enhance the overall portfolio yield, investors

with medium to high risk profile can consider 20% – 25% allocation of the overall fixed income portfolio to select high yield

strategies, MLDs and NCDS. Fixed Income portfolios should also include REITs/InvITs which have highest credit rating & which aim

to offer regular (either quarterly or half yearly) &predictable cash flows - investment horizon should be at least 4-5 years to

mitigate interim mark to market volatility

� February 2022 - We recommend to invest 50%in lump sum and 50%in a staggered manner over the next 3 months in Multi cap and

select Mid & Small Cap strategies (MFs, PMS, AIF)

APRIL 2022 | ISSUE 112 12

Temperature Gauge

Alpha Strategist | ‘Lollapalooza Effect’

We are cognizant of the fact that investments are tuned to meet your objectives and thus calling for a suitable asset mix

basis your investment objective. However the challenge always remains to accurately estimate when the market is

cheap or expensive. In order to arrive at the decision of preferring equity over debt or vice versa, we believe earning

yield to bond yield is an excellent parameter to consider. This ratio indicates the perceived risk differential between

equity and bonds.

Historically whenever earnings yield and bond yield spreads are above 0.8, equities are considered to be undervalued.

The earning yield to bond yield parameter along with our in-house indicator of market valuations named as MOVI – The

Motilal Oswal Valuation Index enables us to arrive at a well-researched and thought through asset class outlook. MOVI

is basically an index which is calculated based on the Price to Earnings (PE), Price to Book Value (PB) and Dividend Yield

(DY) on the components of Nifty 50. By means of an algorithm the weighted average PE, PB and DY of the components of

Nifty 50, one arrives at index. A higher level on the MOVI means markets are expensive and hence one should reduce

equity exposure and vice versa.

With the above mentioned input variables, we have crafted a unique model coined as which helpTemperature Gauge

in making investment choices across asset classes.

This qualitative and quantitative process would enable us to construct “winning portfolios” for our clients. In line with

our philosophy of providing better insights to you, we hope you find the same informative.

Data as of 5th Apr’22, Source: Capital Line, Bloomberg Internal Research; Ni�y EPS considered for FY22E is INR 731 and FY23E is 874, es�mates are taken from MOFSL

Temperature Gauge Index using FY23E EPS is 100

117

60

70

80

90

100

110

120

130

140

150

Temperature Gauge Index

-7%

13%

33%

53%> 10% CAGR Between 0-10% CAGR < 0%Ni�y – 3 Year Forward Return

Cheap Zone Fair Zone Expensive Zone

100

APRIL 2022 | ISSUE 112 13

� Below grid is based on Temperature Gauge Index

Equity Allocation & Deployment Grid

No Ac�on Reduce Reduce

Invest Stay Invested Stay Invested

Invest Invest Stay Invested

Expensive

Fair

Cheap

Underweight Neutral Overweight

Strategic

Alloca�on

Valua�on

100% Staggered

50% Staggered

50% Lump sum

(Current Scenario)

100% Lump sum

Source: Capital Line, Internal Research, Data as of 5th Apr’22; *Total nos. of observa�on is 4,978

Temperature Gauge Index is

in the range of 115-120, the

3-yr forward return shows

h i g h e r p r o b a b i l i t y o f

positive returns

3 Yr Forward Returns Of Nifty At Different Levels Of TemperatureGauge Index

Alpha Strategist | ‘Lollapalooza Effect’

Nifty 50 3 Yr Return CAGR% Times in

CAGR range

Index in

Range

No. of

Observations

% of

ObservationsMin Max

Averag

e

%

Times

Positive

6% to

10%>=10%

65 70 26 0.5% 17% 58% 26% 100% 0% 100%

70 75 91 1.8% 14% 58% 31% 100% 0% 100%

75 80 54 1.1% 18% 56% 38% 100% 0% 100%

80 85 158 3.2% 15% 51% 39% 100% 0% 100%

85 90 190 3.8% 12% 45% 35% 100% 0% 100%

90 95 241 4.8% 10% 49% 28% 100% 0% 100%

95 100 583 11.7% 2% 48% 21% 100% 6% 93%

100 105 558 11.2% 1% 44% 15% 100% 20% 75%

105 110 611 12.3% -4% 33% 11% 98% 28% 57%

110 115 935 18.8% -6% 28% 8% 91% 38% 30%

115 120 887 17.8% -7% 14% 7% 95% 24% 38%

120 125 465 9.3% -4% 10% 5% 88% 28% 8%

125 130 55 1.1% -1% 6% 2% 78% 0% 0%

130 135 60 1.2% -2% 3% 0% 66% 0% 0%

135 140 64 1.2% -3% 0% -2% 0% 0% 0%

APRIL 2022 | ISSUE 112 14

Risk Return profile helps to determine one’s asset allocation frame work. The next logical step is to look at the different

investment strategies that would enable one to eventually achieve their financial goals.

Alpha Strategist | ‘Lollapalooza Effect’

Risk Return Matrix

From the above chart we can conclude that in debt, a high quality accrual strategy would have lower volatility as

compared to a dynamic strategy while generating similar average return over a 1 year holding period

While in equity, a large cap strategy has historically exhibited relatively lower volatility and generated lower return as

compared to the small cap strategy.

Thereby, one has to carefully examine if a particular investment strategy is aligned with their risk appetite before making

an investment decision.

Strategies considered for the analysis:

Large cap fund category:ABSL frontline, ABSL focused equity, SBI bluechip, Motilal Value PMS & Motilal Oswal focused 25

Multi cap fund category: ABSL equity, ASK IEP PMS, ASK Select PMS, Motilal NTDOP PMS, DHFL Deep Value PMS, Franklin

India equity, Franklin focused equity, I-Pru multi cap, Invesco contra, L&T value & Kotak standard multicap

Mid cap category: Franklin prima, HDFC midcap opps, Motilal IOP PMS, Kotak emerging equities, Sundaram midcap &

Motilal focused 30

Small cap category: Franklin smaller cos, DSP small Cap & HDFC small cap

High quality accrual: ABSL Corp Bond, Axis Banking PSU, BNP Corp bond, ICICI Short term bond fund, IDFC Banking & PSU

& IDFC bond fund –ST, ICICI Banking and PSU, Kotak Banking and PSU

Credit risk: BOI AXA credit risk, Franklin India ST income, ICICI credit risk, L&T resurgent, Reliance credit risk & Reliance

strategic debt fund

Dynamic: IDFC Dynamic, SBI Dynamic, UTI Dynamic & ABSL Dynamic

Long/Short: Performance of Ambit Alpha fund from 31 May 2013 – 30 Sep 2016, Liquid return assumed from 1st Oct 16-

29th Feb 17 and performance of Avendus Absolute Return Fund from 31st Mar 2017 onwards

Data used from December 2009, Source: Ace MF

*Every category consists of fund equally weighted

Multi Cap

Average

Max

Min

8.0%

18.7%

-3.3%

6. %7

1 . %3 0

-13.1%

7 9. %

. %17 3

0.1%

10.6%

16.5%

1.8%

16.8%

86.9%

-23.1%

20.9%

112.3%

-25.6%

22.3%

123.6%

-2 . %2 8

25.5%

145.9%

-36.3%

Credit Risk Dynamic Mid Cap Small CapHigh Quality

AccrualLarge CapLong Short

1 -Year

Rolling Return

Risk Return matrix of various investment strategies

Large Cap

Multi CapMidcap

Small cap

ST &

AccrualCredit

Dynamic

Long short

0

0.05

0.1

0.15

0.2

0.25

0.3

0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4

Av

era

ge

1 -

ye

ar

roll

ing

pe

rio

d

Standard Deviation (monthly data)

Large Cap Multi Cap Midcap Small cap ST & Accrual Credit Dynamic Long short

APRIL 2022 | ISSUE 112 15

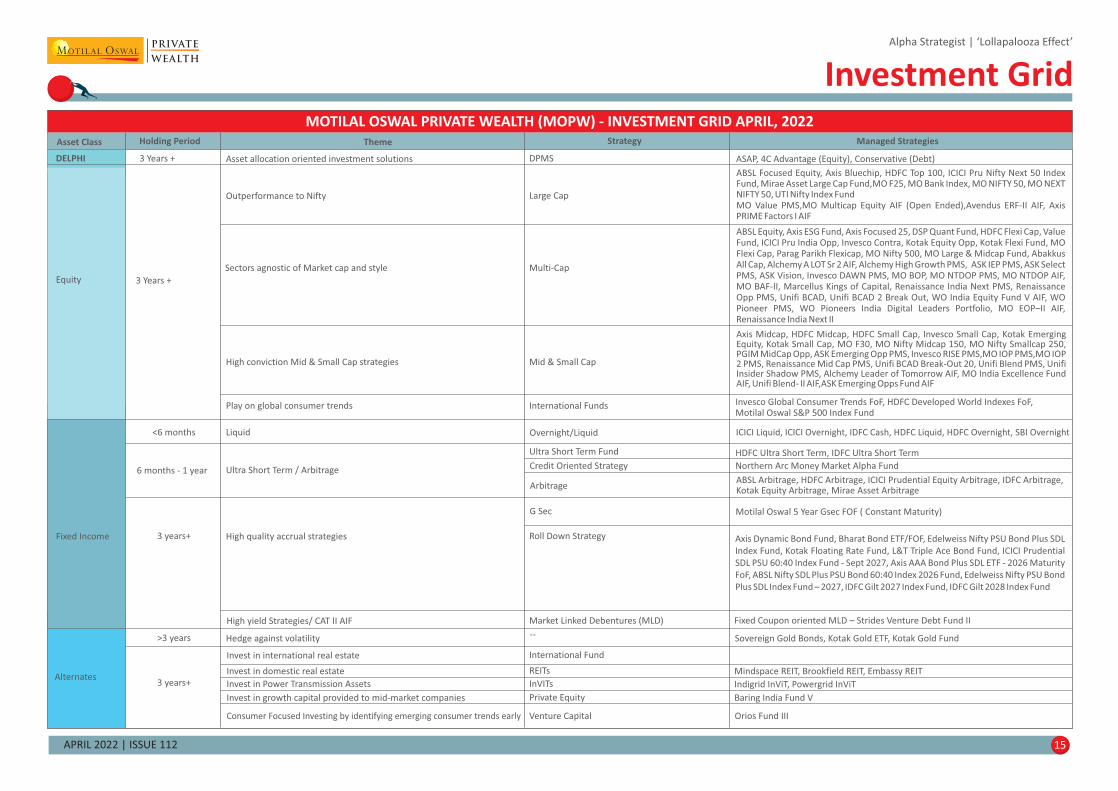

Alpha Strategist | ‘Lollapalooza Effect’

Investment Grid

6 months - 1 year

Fixed Income

Alternates

Ultra Short Term / Arbitrage

3 years+ High quality accrual strategies

Ultra Short Term Fund

Credit Oriented Strategy

Arbitrage

High conviction Mid & Small Cap strategies Mid & Small Cap

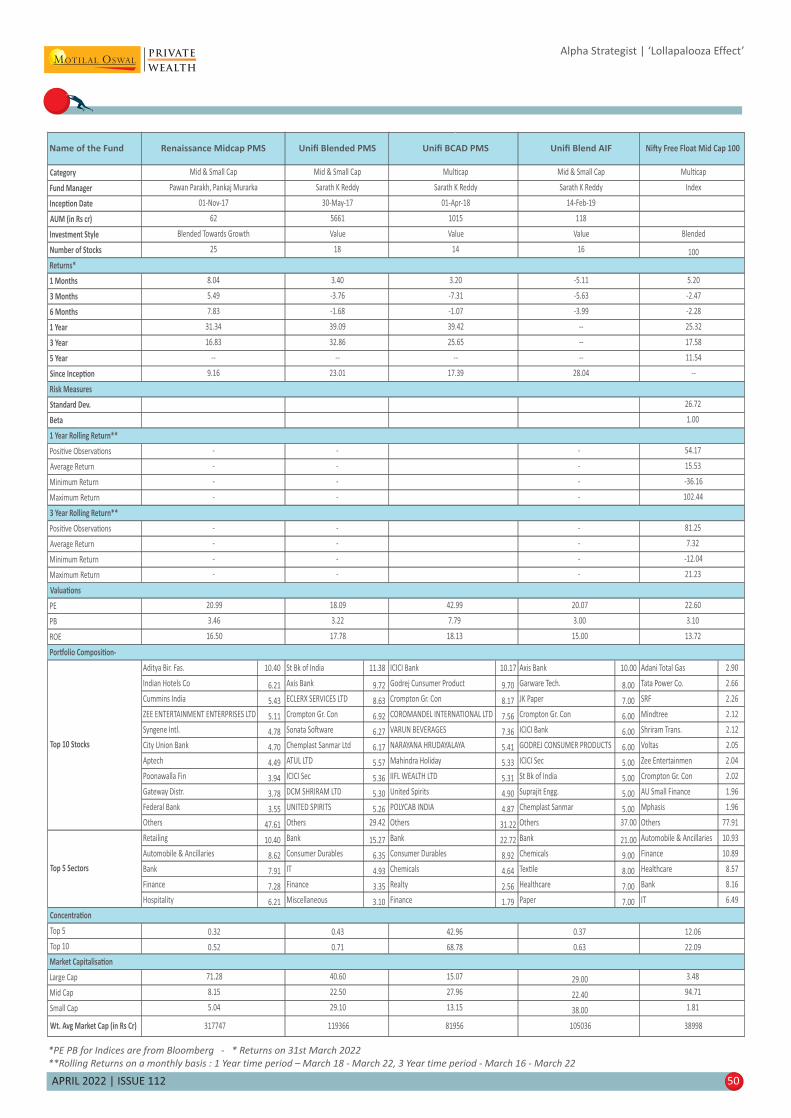

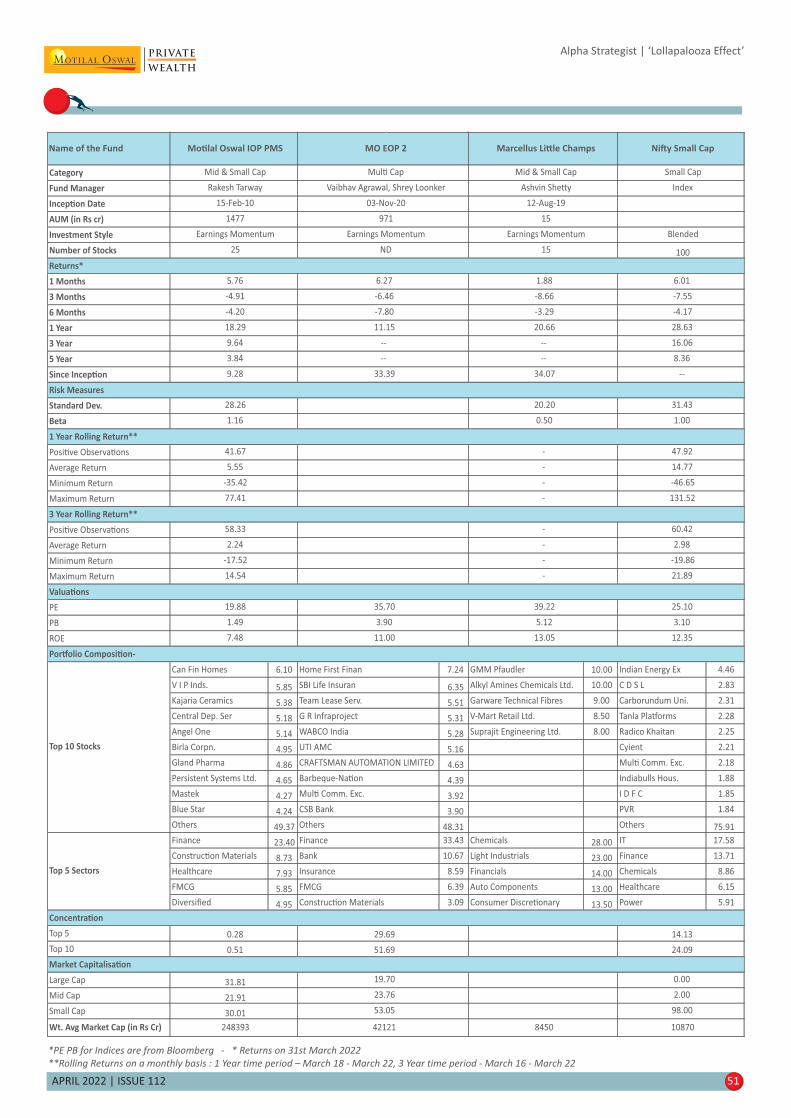

Axis Midcap, HDFC Midcap, HDFC Small Cap, Invesco Small Cap, Kotak EmergingEquity, Kotak Small Cap, MO F30, MO Nifty Midcap 150, MO Nifty Smallcap 250,PGIM MidCap Opp, ASK Emerging Opp PMS, Invesco RISE PMS,MO IOP PMS,MO IOP2 PMS, Renaissance Mid Cap PMS, Unifi BCAD Break-Out 20, Unifi Blend PMS, UnifiInsider Shadow PMS, Alchemy Leader of Tomorrow AIF, MO India Excellence FundAIF, Unifi Blend- II AIF,ASK Emerging Opps Fund AIF

MOTILAL OSWAL PRIVATE WEALTH (MO W) - INVESTMENT GRID APRIL 2022P ,

Asset Class Holding Period Theme Strategy

Equity

Outperformance to Nifty

Sectors agnostic of Market cap and style

Large Cap

Multi-Cap

3 Years +

Managed Strategies

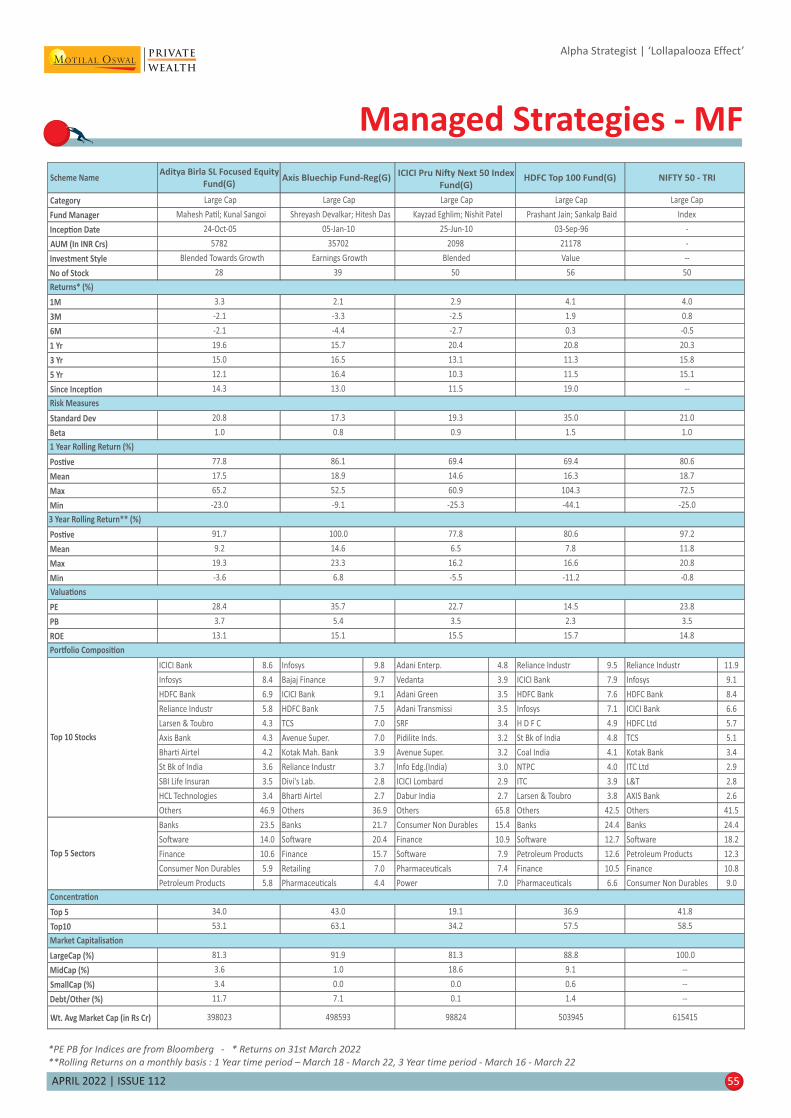

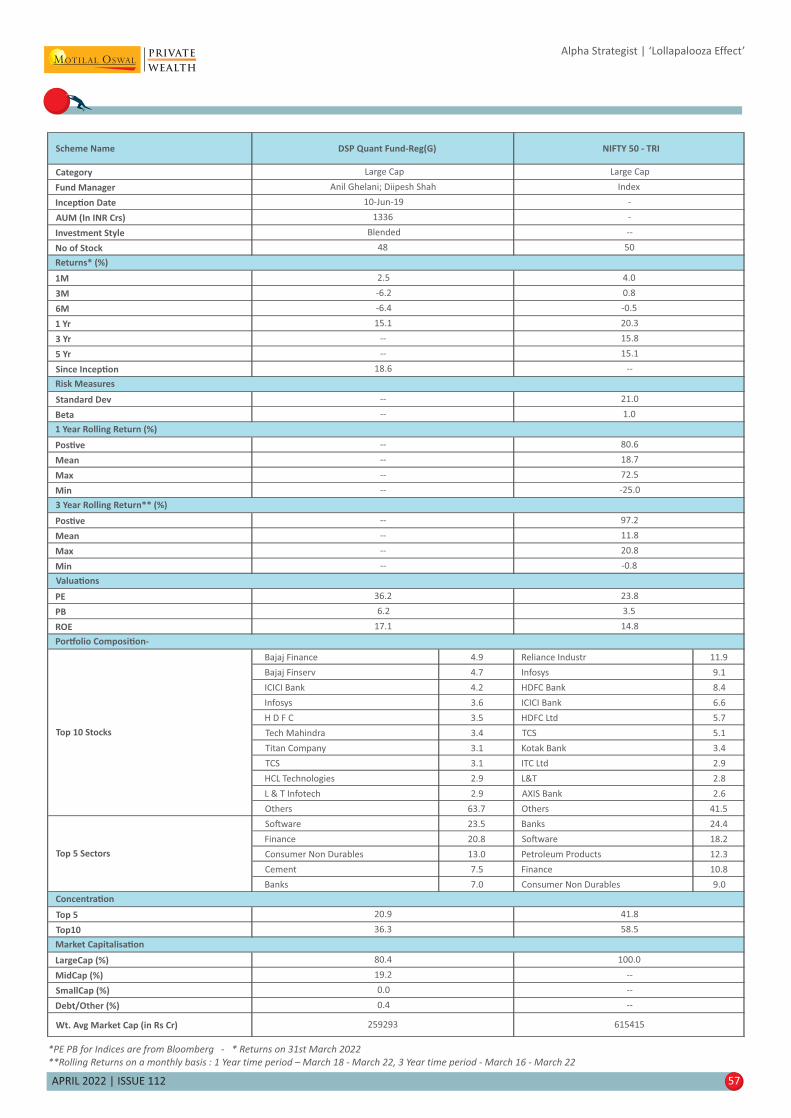

ABSL Focused Equity, Axis Bluechip, HDFC Top 100, ICICI Pru Nifty Next 50 IndexFund, Mirae Asset Large Cap Fund,MO F25, MO Bank Index, MO NIFTY 50, MO NEXTNIFTY 50, UTI Nifty Index FundMO Value PMS,MO Multicap Equity AIF (Open Ended),Avendus ERF-II AIF, AxisPRIME Factors I AIF

ABSL Equity, Axis ESG Fund, Axis Focused 25, DSP Quant Fund, HDFC Flexi Cap, ValueFund, ICICI Pru India Opp, Invesco Contra, Kotak Equity Opp, Kotak Flexi Fund, MOFlexi Cap, Parag Parikh Flexicap, MO Nifty 500, MO Large & Midcap Fund, AbakkusAll Cap, Alchemy A LOT Sr 2 AIF, Alchemy High Growth PMS, ASK IEP PMS, ASK SelectPMS, ASK Vision, Invesco DAWN PMS, MO BOP, MO NTDOP PMS, MO NTDOP AIF,MO BAF-II, Marcellus Kings of Capital, Renaissance India Next PMS, RenaissanceOpp PMS, Unifi BCAD, Unifi BCAD 2 Break Out, WO India Equity Fund V AIF, WOPioneer PMS, WO Pioneers India Digital Leaders Portfolio, MO EOP–II AIF,Renaissance India Next II

<6 months Liquid Overnight/Liquid ICICI Liquid, ICICI Overnight, IDFC Cash, HDFC Liquid, HDFC Overnight, SBI Overnight

HDFC Ultra Short Term, IDFC Ultra Short Term

Northern Arc Money Market Alpha Fund

ABSL Arbitrage, HDFC Arbitrage, ICICI Prudential Equity Arbitrage, IDFC Arbitrage,Kotak Equity Arbitrage, Mirae Asset Arbitrage

High yield Strategies/ CAT II AIF Market Linked Debentures (MLD) Fixed Coupon oriented MLD – Strides Venture Debt Fund II

Play on global consumer trends International Funds Invesco Global Consumer Trends FoF, HDFC Developed World Indexes FoF,Motilal Oswal S&P 500 Index Fund

REITsInvest in domestic real estate Mindspace REIT, Brookfield REIT, Embassy REIT

DELPHI 3 Years + Asset allocation oriented investment solutions DPMS ASAP, 4C Advantage (Equity), Conservative (Debt)

InVITsInvest in Power Transmission Assets Indigrid InViT, Powergrid InViT

Invest in growth capital provided to mid-market companies Private Equity Baring India Fund V

Roll Down Strategy Axis Dynamic Bond Fund, Bharat Bond ETF/FOF, Edelweiss Nifty PSU Bond Plus SDL

Index Fund, Kotak Floating Rate Fund, L&T Triple Ace Bond Fund, ICICI Prudential

SDL PSU 60:40 Index Fund - Sept 2027, Axis AAA Bond Plus SDL ETF - 2026 Maturity

FoF, ABSL Nifty SDL Plus PSU Bond 60:40 Index 2026 Fund, Edelweiss Nifty PSU Bond

Plus SDL Index Fund – 2027, IDFC Gilt 2027 Index Fund, IDFC Gilt 2028 Index Fund

G Sec Motilal Oswal 5 Year Gsec FOF ( Constant Maturity)

--Hedge against volatility Sovereign Gold Bonds, Kotak Gold ETF, Kotak Gold Fund>3 years

3 years+

Consumer Focused Investing by identifying emerging consumer trends early Orios Fund IIIVenture Capital

Invest in international real estate International Fund

Alpha Strategist | ‘Lollapalooza Effect’

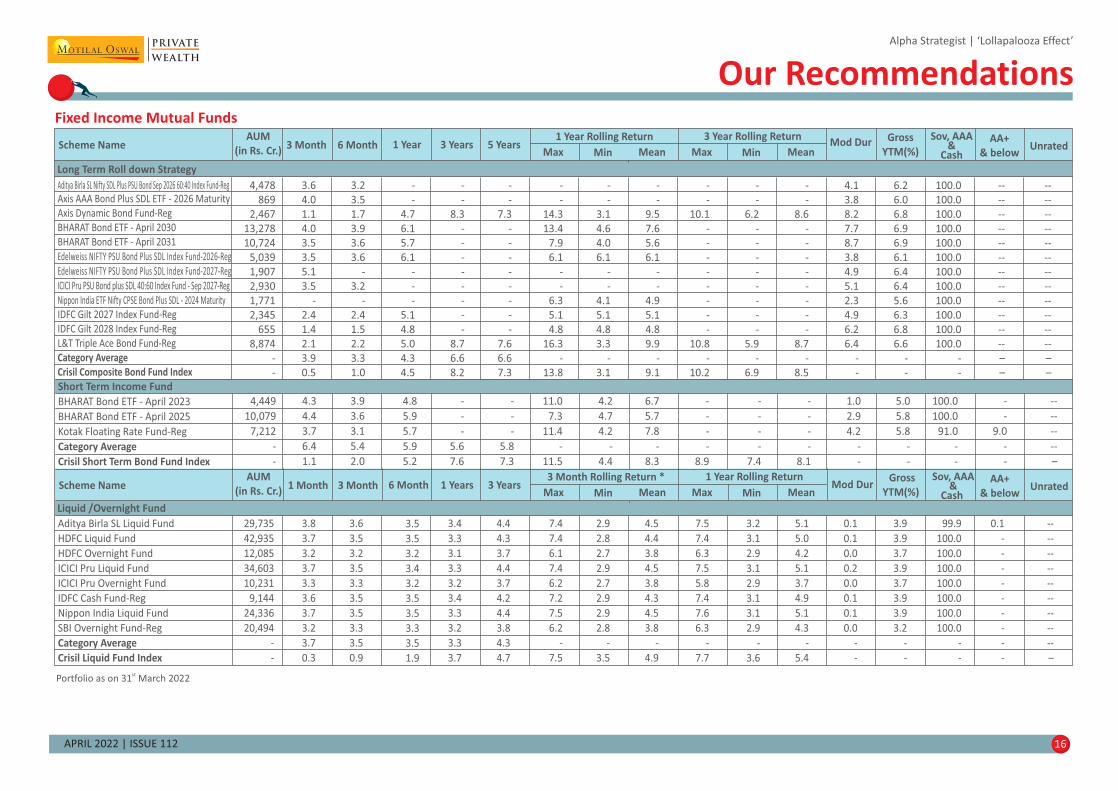

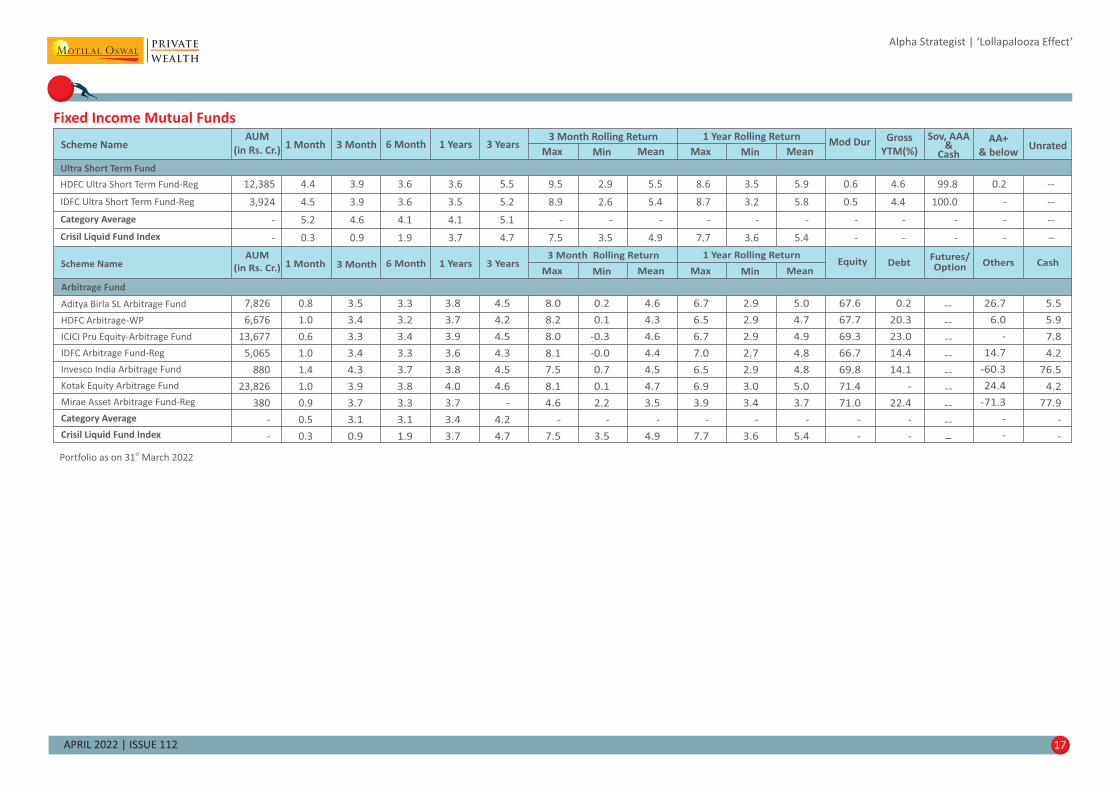

Our RecommendationsFixed Income Mutual Funds

APRIL 2022 | ISSUE 112 16

Aditya Birla SL Liquid Fund

HDFC Liquid Fund

HDFC Overnight Fund

ICICI Pru Liquid Fund

ICICI Pru Overnight Fund

IDFC Cash Fund-Reg

Nippon India Liquid Fund

SBI Overnight Fund-Reg

Category Average

Crisil Liquid Fund Index

Liquid /Overnight Fund

Scheme NameAUM

(in Rs. Cr.)1 Month 3 Month 6 Month 3 Years Mod Dur

Gross

YTM(%)

Sov, AAA&

CashUnrated

3 Month Rolling Return *

Min MinMax Max

1 Year Rolling Return AA+

& below1 Years

Mean Mean

29,735

42,935

12,085

34,603

10,231

9,144

24,336

20,494

-

-

3.8

3.7

3.2

3.7

3.3

3.6

3.7

3.2

3.7

0.3

3.6

3.5

3.2

3.5

3.3

3.5

3.5

3.3

3.5

0.9

3.5

3.5

3.2

3.4

3.2

3.5

3.5

3.3

3.5

1.9

3.4

3.3

3.1

3.3

3.2

3.4

3.3

3.2

3.3

3.7

4.4

4.3

3.7

4.4

3.7

4.2

4.4

3.8

4.3

4.7

7.4

7.4

6.1

7.4

6.2

7.2

7.5

6.2

-

7.5

2.9

2.8

2.7

2.9

2.7

2.9

2.9

2.8

-

3.5

4.5

4.4

3.8

4.5

3.8

4.3

4.5

3.8

-

4.9

7.5

7.4

6.3

7.5

5.8

7.4

7.6

6.3

-

7.7

3.2

3.1

2.9

3.1

2.9

3.1

3.1

2.9

-

3.6

5.1

5.0

4.2

5.1

3.7

4.9

5.1

4.3

-

5.4

0.1

0.1

0.0

0.2

0.0

0.1

0.1

0.0

-

-

3.9

3.9

3.7

3.9

3.7

3.9

3.9

3.2

-

-

99.9

100.0

100.0

100.0

100.0

100.0

100.0

100.0

-

-

0.1

-

-

-

-

-

-

-

-

-

--

--

--

--

--

--

--

--

--

–

Long Term Roll down Strategy

Scheme NameAUM

(in Rs. Cr.)3 Month 6 Month 1 Year 5 Years Mod Dur Gross

YTM(%)

Sov, AAA&

CashUnrated

1 Year Rolling Return

Min MinMax Max

3 Year Rolling Return AA+

& below3 Years

Mean Mean

BHARAT Bond ETF - April 2023

BHARAT Bond ETF - April 2025

Kotak Floating Rate Fund-Reg

Category Average

Crisil Short Term Bond Fund Index

Short Term Income Fund

4,449

10,079

7,212

-

-

4.3

4.4

3.7

6.4

1.1

3.9

3.6

3.1

5.4

2.0

4.8

5.9

5.7

5.9

5.2

-

-

-

5.6

7.6

-

-

-

5.8

7.3

11.0

7.3

11.4

-

11.5

4.2

4.7

4.2

-

4.4

6.7

5.7

7.8

-

8.3

-

-

-

-

8.9

-

-

-

-

7.4

-

-

-

-

8.1

1.0

2.9

4.2

-

-

5.0

5.8

5.8

-

-

100.0

100.0

91.0

-

-

-

-

9.0

-

-

--

--

--

--

–

4,478

869

2,467

13,278

10,724

5,039

1,907

2,930

1,771

2,345

655

8,874

-

-

3.6

4.0

1.1

4.0

3.5

3.5

5.1

3.5

-

2.4

1.4

2.1

3.9

0.5

3.2

3.5

1.7

3.9

3.6

3.6

-

3.2

-

2.4

1.5

2.2

3.3

1.0

-

-

4.7

6.1

5.7

6.1

-

-

-

5.1

4.8

5.0

4.3

4.5

-

-

8.3

-

-

-

-

-

-

-

-

8.7

6.6

8.2

-

-

7.3

-

-

-

-

-

-

-

-

7.6

6.6

7.3

-

-

14.3

13.4

7.9

6.1

-

-

6.3

5.1

4.8

16.3

-

13.8

-

-

3.1

4.6

4.0

6.1

-

-

4.1

5.1

4.8

3.3

-

3.1

-

-

9.5

7.6

5.6

6.1

-

-

4.9

5.1

4.8

9.9

-

9.1

-

-

10.1

-

-

-

-

-

-

-

-

10.8

-

10.2

-

-

6.2

-

-

-

-

-

-

-

-

5.9

-

6.9

-

-

8.6

-

-

-

-

-

-

-

-

8.7

-

8.5

4.1

3.8

8.2

7.7

8.7

3.8

4.9

5.1

2.3

4.9

6.2

6.4

-

-

6.2

6.0

6.8

6.9

6.9

6.1

6.4

6.4

5.6

6.3

6.8

6.6

-

-

100.0

100.0

100.0

100.0

100.0

100.0

100.0

100.0

100.0

100.0

100.0

100.0

-

-

--

--

--

--

--

--

--

--

--

--

--

--

–

–

--

--

--

--

--

--

--

--

--

--

--

--

–

–

Axis AAA Bond Plus SDL ETF - 2026 Maturity

Axis Dynamic Bond Fund-Reg

BHARAT Bond ETF - April 2030

BHARAT Bond ETF - April 2031

IDFC Gilt 2027 Index Fund-Reg

IDFC Gilt 2028 Index Fund-Reg

L&T Triple Ace Bond Fund-Reg

Category Average

Crisil Composite Bond Fund Index

Aditya Birla SL Nifty SDL Plus PSU Bond Sep 2026 60:40 Index Fund-Reg

Edelweiss NIFTY PSU Bond Plus SDL Index Fund-2026-Reg

Edelweiss NIFTY PSU Bond Plus SDL Index Fund-2027-Reg

ICICI Pru PSU Bond plus SDL 40:60 Index Fund - Sep 2027-Reg

Nippon India ETF Nifty CPSE Bond Plus SDL - 2024 Maturity

Portfolio as on 20231 March 2st

APRIL 2022 | ISSUE 112 17

Alpha Strategist | ‘Lollapalooza Effect’

Portfolio as on 20231 March 2st

Fixed Income Mutual Funds

Arbitrage Fund

Aditya Birla SL Arbitrage Fund

HDFC Arbitrage-WP

ICICI Pru Equity-Arbitrage Fund

IDFC Arbitrage Fund-Reg

Invesco India Arbitrage Fund

Kotak Equity Arbitrage Fund

Mirae Asset Arbitrage Fund-Reg

Category Average

Crisil Liquid Fund Index

26.7

6.0

-

14.7

-60.3

24.4

-71.3

-

-

5.5

5.9

7.8

4.2

76.5

4.2

77.9

-

-

Scheme NameAUM

(in Rs. Cr.) 1 Month 3 Month 6 Month 3 Years Equity DebtFutures/Option Cash

3 Month Rolling Return

Min MinMax Max

1 Year Rolling ReturnOthers1 Years

Mean Mean

7,826

6,676

13,677

5,065

880

23,826

380

-

-

0.8

1.0

0.6

1.0

1.4

1.0

0.9

0.5

0.3

3.5

3.4

3.3

3.4

4.3

3.9

3.7

3.1

0.9

3.3

3.2

3.4

3.3

3.7

3.8

3.3

3.1

1.9

3.8

3.7

3.9

3.6

3.8

4.0

3.7

3.4

3.7

4.5

4.2

4.5

4.3

4.5

4.6

-

4.2

4.7

8.0

8.2

8.0

8.1

7.5

8.1

4.6

-

7.5

0.2

0.1

-0.3

-0.0

0.7

0.1

2.2

-

3.5

4.6

4.3

4.6

4.4

4.5

4.7

3.5

-

4.9

6.7

6.5

6.7

7.0

6.5

6.9

3.9

-

7.7

2.9

2.9

2.9

2.7

2.9

3.0

3.4

-

3.6

5.0

4.7

4.9

4.8

4.8

5.0

3.7

-

5.4

67.6

67.7

69.3

66.7

69.8

71.4

71.0

-

-

0.2

20.3

23.0

14.4

14.1

-

22.4

-

-

--

--

--

--

--

--

--

--

–

HDFC Ultra Short Term Fund-Reg

IDFC Ultra Short Term Fund-Reg

Category Average

Crisil Liquid Fund Index

Scheme NameAUM

(in Rs. Cr.)1 Month 3 Month 6 Month 3 Years Mod Dur Gross

YTM(%)

Sov, AAA&

CashUnrated

3 Month Rolling Return

Min MinMax Max

1 Year Rolling Return AA+

& below1 Years

Mean Mean

Ultra Short Term Fund

12,385

3,924

-

-

4.4

4.5

5.2

0.3

3.9

3.9

4.6

0.9

3.6

3.6

4.1

1.9

3.6

3.5

4.1

3.7

5.5

5.2

5.1

4.7

9.5

8.9

-

7.5

2.9

2.6

-

3.5

5.5

5.4

-

4.9

8.6

8.7

-

7.7

3.5

3.2

-

3.6

5.9

5.8

-

5.4

0.6

0.5

-

-

4.6

4.4

-

-

99.8

100.0

-

-

0.2

-

-

-

--

--

--

–

APRIL 2022 | ISSUE 112 18

ASAP – The Big Picture!

ASAP - Simple Equal-Weight Portfolio…

Alpha Strategist | ‘Lollapalooza Effect’

DELPHI

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Equity-IND Equity-IND Equity-IND Equity-IND Equity-IND Equity-US Equity-US Equity-US Equity-US Equity-IND Debt Debt Gold Equity-IND Equity-IND Equity-IND

34.4% 82.1% 37.0% 27.9% 17.4% 50.4% 22.6% 43.3% 37.3% 63.8% 9.0% 8.5% 24.1% 71.9% 10.7% 36.3%

ASAP Equity-US Equity-US Gold Debt Gold Debt Equity-IND Debt Equity-US Cash Cash Debt ASAP ASAP ASAP

10.4% 79.8% 17.3% 27.1% 13.0% 13.3% 12.0% 18.6% 10.5% 22.5% 5.6% 6.4% 12.7% 27.1% 6.7% 14.5%

Debt ASAP ASAP ASAP Cash Debt Cash ASAP ASAP ASAP Gold Gold Cash Equity-US Cash Gold

9.0% 42.2% 16.7% 18.8% 7.0% 13.0% 9.4% 13.2% 9.2% 20.7% 1.3% 5.9% 6.4% 20.2% 4.0% 13.6%

Cash Gold Cash Equity-US ASAP ASAP ASAP Debt Gold Debt ASAP ASAP ASAP Gold Equity-US Equity-US

8.0% 31.3% 12.1% 16.5% 6.6% 12.9% 8.0% 11.0% 8.1% 9.0% -1.7% -1.4% 4.4% 13.5% 3.8% 6.8%

Gold Debt Debt Debt Equity-US Cash Equity-IND Cash Cash Cash Equity-US Equity-US Equity-IND Debt Gold Debt

2.3% 9.0% 11.0% 12.0% -1.9% 8.8% -0.8% 7.0% 6.5% 5.7% -3.7% -10.1% 2.7% 8.1% 0.5% 4.8%

Equity-US Cash Gold Cash Gold Equity-IND Gold Gold Equity-IND Gold Equity-IND Equity-IND Equity-US Cash Debt Cash

-1.5% 9.0% 6.3% 10.3% -2.3% -20.8% -3.2% -14.0% -16.5% 2.4% -20.6% -17.9% -23.8% 4.6% -0.3% 4.6%

2006 2007 2008 2009 2010 2011 2012 2013^ 2014 2015 2016 2017 2018 2019 2020 2021 2022*

Equity-INDEquity-IND Gold Equity-IND Gold Gold Equity-IND Equity-US Equity-IND Debt Debt Equity-IND Gold Equity-US Gold Equity-US Gold

39.8% 54.8% 26.1% 75.8% 23.2% 31.7% 27.7% 45.6% 31.4% 8.6% 12.9% 28.6% 7.9% 31.9% 28.0% 29.1% 7.1%

Gold Gold Debt ASAP Equity-IND Equity-US Equity-US ASAP Debt Cash Equity-US ASAP Cash Gold Equity-US Equity-IND Cash

20.3% 16.0% 9.1% 29.4% 17.9% 18.7% 17.5% 12.2% 14.3% 8.2% 12.5% 12.4% 7.6% 23.8% 18.3% 24.1% 0.9%

ASAP ASAP Cash Gold ASAP ASAP ASAP Cash ASAP Equity-US Gold Equity-US Debt ASAP ASAP ASAP Equity-IND

15.4% 14.0% 8.4% 24.2% 11.6% 8.3% 15.3% 9.0% 14.2% 4.2% 11.3% 12.3% 5.9% 16.6% 16.7% 13.7% 0.6%

Equity-US Cash ASAP Equity-US Equity-US Cash Gold Equity-IND Equity-US ASAP ASAP Cash ASAP Equity-INDEquity-IND Cash ASAP

11.7% 7.5% -7.6% 17.7% 8.4% 8.2% 12.3% 6.8% 13.6% 3.1% 9.9% 6.7% 3.8% 12.0% 14.9% 3.6% 0.6%

Cash Debt Equity-US Cash Cash Debt Debt Debt Cash Equity-IND Cash Gold Equity-IND Debt Debt Debt Debt

6.0% 6.9% -23.8% 4.9% 5.1% 6.9% 9.4% 3.8% 9.2% -4.1% 7.5% 5.1% 3.2% 10.7% 12.3% 3.4% 0.5%

Debt Equity-US Equity-IND Debt Debt Equity-IND Cash Gold Gold Gold Equity-IND Debt Equity-US Cash Cash Gold Equity-US

4.0% -7.8% -51.8% 3.5% 5.0% -24.6% 8.5% -4.5% -7.9% -6.6% 3.0% 4.7% 2.4% 6.9% 4.6% -4.2% -3.0%

*CAGR is for period 1990 to 31st March 2022; Data updated as of 31st Mar'22. Equity-IND is represented by Sensex from 1990 to 2002 and Nifty 50 from 2002 onwards; Debt is represented by SBI 1-yr FD rates from 1990 to 2002 and CRISIL Composite bond

Index from 2002 onwards; Cash is represented by SBI 3-month FD rates from 1990 to 2002 and CRISIL Liquid fund Index from 2002 onwards; Gold is represented by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR

from 2006 till date; Equity-US is represented by S&P 500 in INR terms; Source: AceMF; Bloomberg

Note: ASAP Portfolio (Equity Sensex 1990-2002,Nifty200-2012 and MF Model Portfolio 2013 onwards; Debt: SBI 1 yr 1990-2002; CRISIL Composite 2002-2012, Debt only Model Portfolio 2013 onwards; Cash- SBI 3 month deposit 1900-2002; HDFC liquid (g)-

REG 2002-2012;HEFC Liquid (G)- Direct 2013 onwards; Gold is represented by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR from 2006 till date; S&P 500 in INR 1990 onwards Disclaimer :Past Performance is no

guarantee of future Results

^ For ASAP: Model Portfolios are used from 2012 onwards; ASAP - Alpha Strategist Advantage Portfolio

Data up to 31st March 2022. Returns are represented on CY basis. Equity-IND is represented by Sensex from 1990 to 2002 and Nifty 50 from 2002 onwards; Debt is represented by SBI 1-yr FD rates from 1990 to 2002 and CRISIL Composite bond Index from 2002 onwards; Cash is

represented by SBI 3-month FD rates from 1990 to 2002 and CRISIL Liquid fund Index from 2002 onwards; Gold is represented by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR from 2006 till date; Equity-US is represented by S&P 500 in INR

terms; Source: AceMF; Bloomberg

Note: ASAP Portfolio (Equity Sensex 1990-2002,Nifty200-2012 and MF Model Portfolio 2013 onwards; Debt: SBI 1 yr 1990-2002; CRISIL Composite 2002-2012, Debt only Model Portfolio 2013 onwards; Cash- SBI 3 month deposit 1900-2002; HDFC liquid (g)- REG 2002-

2012;HEFC Liquid (G)- Direct 2013 onwards; Gold is represented by Gold USD Spot Price conversion into INR from 1990 to 2005 and MCX Spot Gold price in INR from 2006 till date; S&P 500 in INR 1990 onwards

ASAP - Alpha StrategistAdvantage Portfolio

Asset Class Equity-IND Equity-US Debt Cash Gold ASAP

CAGR from 1990 to 2022* 14.0% 13.3% 8.4% 7.1% 10.0% 11.9%

Standard Deviation 27.6% 15.0% 2.6% 0.6% 14.9% 8.0%

Maximum Drawdown -55.1% -45.9% -6.3% 0.0% -25.1% -11.4%

Maximum Returns - 3Y 59.6% 41.1% 12.7% 10.6% 32.2% 27.1%

Minimum Returns - 3Y -15.7% -14.9% 2.4% 4.4% -7.3% 0.1%

Average Returns - 3Y 12.6% 13.3% 8.6% 7.1% 10.2% 11.4%

Positive Observations (%) - 3Y 84.7% 81.8% 100.0% 100.0% 83.8% 100.0%

Returns Distribution

(3Y Rolling Returns)

% Observations

Equity-IND Equity-US Debt Cash Gold ASAP

-20% to -10% 3.1% 4.5%

-10% to 0% 12.2% 13.6% 16.2%

0% to 6% 21.0% 9.7% 15.3% 24.1% 19.9% 10.3%

6% to 10% 15.3% 8.5% 55.7% 70.5% 12.8% 24.7%

10% to 15% 17.6% 20.2% 29.0% 5.4% 19.6% 52.3%

15% to 20% 7.7% 13.9% 13.6% 7.4%

20% to 30% 8.2% 16.5% 17.3% 5.4%

Above 30% 15.6% 13.8% 0.6%

APRIL 2022 | ISSUE 112 19

Alpha Strategist | ‘Lollapalooza Effect’

DELPHI

4C – Average Rolling Returns

4C – Average Rolling Returns

ASAP – Time Window Performance

Data up to 31st Mar 2022. Source: AceMF; Bloomberg, MOPWM Disclaimer :Past Performance is no guarantee of future Results

For ASAP: Model Portfolios are used from 2012 onwards; ASAP - Alpha Strategist Advantage Portfolio

*Note: ASAP Portfolio (Equity - Nifty2000-2012 and MF Model Portfolio 2013 onwards; Debt - CRISIL Composite 2002-2012, Debt only Model Portfolio 2013 onwards; Cash- HDFC liquid (g)- REG 2002-2012; HEFC Liquid (G)-

Direct 2013 onwards; Gold – MCX Gold sport Price; S&P 500 in INR terms

Data up to 31st Mar’2022; Rolling Returns Analysis is from Oct’12 to Mar’22

Source: AceMF; Bloomberg, ACEMF, MOPWM Disclaimer :Past Performance is no guarantee of future Results Conservative consist of MOPWM Debt Model Portfolio

Data up to 28th Feb’2022; Rolling Returns Period of Analysis is Oct’12 to Feb’22

Source: AceMF; Bloomberg, MOPWM Disclaimer :Past Performance is no guarantee of future Results 4C Advantage Portfolio consist of MOPWM MF Model Portfolio

Performance as on 31/03/2022 Absolute CAGR(%)

Strategy 1M 3M 6M 1Y 2Y 3Y 5Y 7Y 10Y

ASAP* 2.1% 0.6% 3.6% 13.6% 19.0% 14.0% 11.6% 10.5% 11.0%

Nifty 50 4.0% 0.6% -0.9% 18.9% 42.5% 14.5% 13.7% 10.8% 12.7%

S&P 500 – INR 4.2% -3.0% 7.4% 18.3% 32.6% 20.5% 17.5% 15.0% 17.0%

Gold – INR 1.7% 7.1% 12.5% 16.6% 7.1% 17.5% 12.5% 10.1% 6.2%

Crisil Composite 0.2% 0.5% 1.0% 4.5% 6.1% 8.2% 7.3% 8.0% 8.4%

Crisil Liquid 0.3% 0.9% 1.9% 3.7% 3.9% 4.7% 5.7% 6.2% 7.0%

17.1%

14.2%

12.4% 12.5%

17.3%

14.1%

12.5%13.0%

1Y 2Y 3Y 5Y

Average Rolling Returns

4c Nifty 500 TRI

Performance as on 31/03/2022 Annualized CAGR(%)

Strategy 1M 3M 6M 1Y 2Y 3Y 5Y 7Y

Conservative 4.3% 3.5% 3.2% 5.5% 6.7% 8.2% 7.5% 7.7%

Crisil Composite 2.5% 1.9% 2.1% 4.5% 6.1% 8.2% 7.3% 8.0%

8.76%

9.03%

8.80%

8.59%8.64%

9.07%

8.96%

8.62%

1Y 2Y 3Y 5Y

Average Rolling Returns

Conservative CRISIL Composite Bond

This document is not valid without disclosure; refer the last page for the disclosure

APRIL 2022 | ISSUE 112 20

Alpha Strategist | ‘Lollapalooza Effect’

Section II

Macro Economy...................................................................................................21

Equities...............................................................................................................25

Fixed Income.......................................................................................................29

Gold....................................................................................................................33

Sources: BNP Paribas MF, tradingeconomics.com, SIAM (www.siam.in), Petroleum Planning & Analysis Cell

(https://www.ppac.gov.in/content/147_1_ConsumptionPetroleum.aspx), RBI (https://rbi.org.in/Scripts/Data_MSupply.aspx)

(https://www.rbi.org.in/Scripts/BS_NSDPDisplay.aspx?param=4)

*Only central government expenditure has been considered

Alpha Strategist | ‘Lollapalooza Effect’

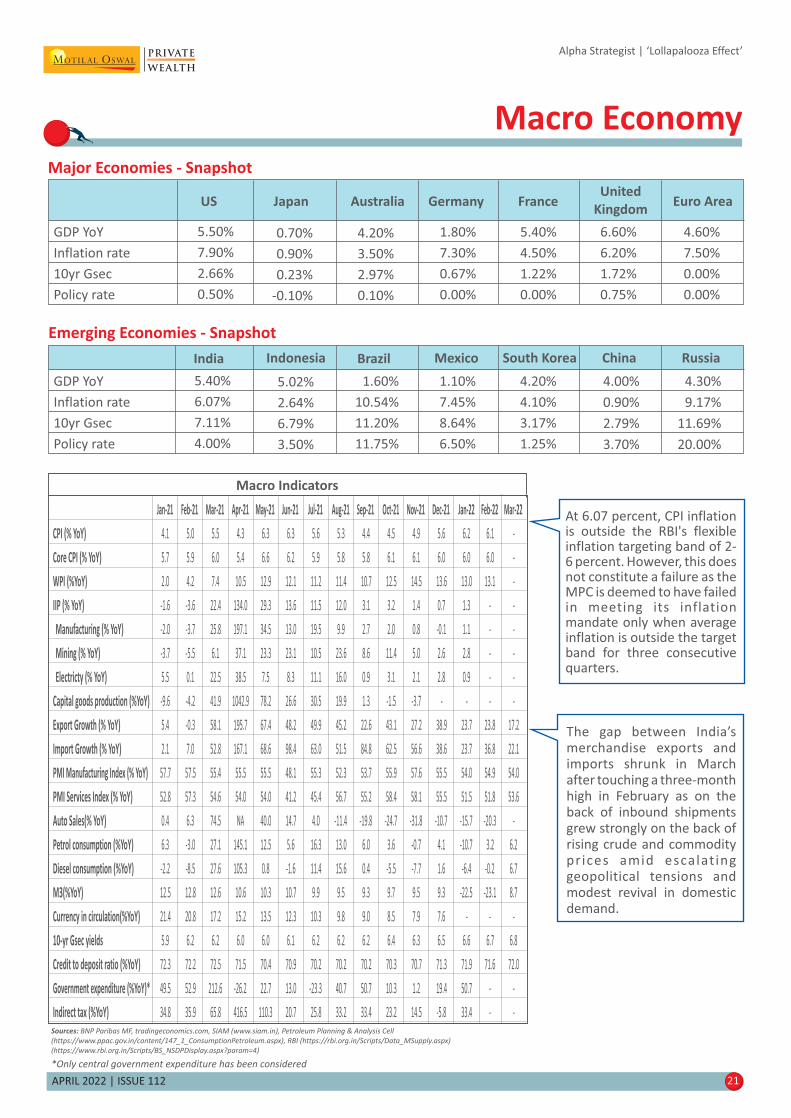

Macro Economy

Emerging Economies - Snapshot

Major Economies - Snapshot

GDP YoY

Inflation rate

10yr Gsec

Policy rate

5.50%

7.90%

2.66%

0.50%

0.70%

0.90%

0.23%

-0.10%

4.20%

3.50%

2.97%

0.10%

1.80%

7.30%

0.67%

0.00%

5.40%

4.50%

1.22%

0.00%

6.60%

6.20%

1.72%

0.75%

4.60%

7.50%

0.00%

0.00%

US Japan Australia Germany FranceUnited

KingdomEuro Area

GDP YoY

Inflation rate

10yr Gsec

Policy rate

5.40%

6.07%

7.11%

4.00%

1.60%

10.54%

11.20%

11.75%

1.10%

7.45%

8.64%

6.50%

4.20%

4.10%

3.17%

1.25%

4.00%

0.90%

2.79%

3.70%

4.30%

9.17%

11.69%

20.00%

India

5.02%

2.64%

6.79%

3.50%

Indonesia Brazil Mexico South Korea RussiaChina

APRIL 2022 | ISSUE 112 21

At 6.07 percent, CPI inflationis outside the RBI's flexibleinflation targeting band of 2-6 percent. However, this doesnot constitute a failure as theMPC is deemed to have failedin meeting its inflationmandate only when averageinflation is outside the targetband for three consecutivequarters.

The gap between India’smerchandise exports andimports shrunk in Marchafter touching a three-monthhigh in February as on theback of inbound shipmentsgrew strongly on the back ofrising crude and commodityprices amid escalat inggeopolitical tensions andmodest revival in domesticdemand.

Macro ndicatorsI

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22

CPI (% YoY) 4.1 5.0 5.5 4.3 6.3 6.3 5.6 5.3 4.4 4.5 4.9 5.6 6.2 6.1 -

Core CPI (% YoY) 5.7 5.9 6.0 5.4 6.6 6.2 5.9 5.8 5.8 6.1 6.1 6.0 6.0 6.0 -

WPI (%YoY) 2.0 4.2 7.4 10.5 12.9 12.1 11.2 11.4 10.7 12.5 14.5 13.6 13.0 13.1 -

IIP (% YoY) -1.6 -3.6 22.4 134.0 29.3 13.6 11.5 12.0 3.1 3.2 1.4 0.7 1.3 - -

Manufacturing (% YoY) -2.0 -3.7 25.8 197.1 34.5 13.0 19.5 9.9 2.7 2.0 0.8 -0.1 1.1 - -

Mining (% YoY) -3.7 -5.5 6.1 37.1 23.3 23.1 10.5 23.6 8.6 11.4 5.0 2.6 2.8 - -

Electricty (% YoY) 5.5 0.1 22.5 38.5 7.5 8.3 11.1 16.0 0.9 3.1 2.1 2.8 0.9 - -

Capital goods production (%YoY) -9.6 -4.2 41.9 1042.9 78.2 26.6 30.5 19.9 1.3 -1.5 -3.7 - - - -

Export Growth (% YoY) 5.4 -0.3 58.1 195.7 67.4 48.2 49.9 45.2 22.6 43.1 27.2 38.9 23.7 23.8 17.2

Import Growth (% YoY) 2.1 7.0 52.8 167.1 68.6 98.4 63.0 51.5 84.8 62.5 56.6 38.6 23.7 36.8 22.1

PMI Manufacturing Index (% YoY) 57.7 57.5 55.4 55.5 55.5 48.1 55.3 52.3 53.7 55.9 57.6 55.5 54.0 54.9 54.0

PMI Services Index (% YoY) 52.8 57.3 54.6 54.0 54.0 41.2 45.4 56.7 55.2 58.4 58.1 55.5 51.5 51.8 53.6

Auto Sales(% YoY) 0.4 6.3 74.5 NA 40.0 14.7 4.0 -11.4 -19.8 -24.7 -31.8 -10.7 -15.7 -20.3 -

Petrol consumption (%YoY) 6.3 -3.0 27.1 145.1 12.5 5.6 16.3 13.0 6.0 3.6 -0.7 4.1 -10.7 3.2 6.2

Diesel consumption (%YoY) -2.2 -8.5 27.6 105.3 0.8 -1.6 11.4 15.6 0.4 -5.5 -7.7 1.6 -6.4 -0.2 6.7

M3(%YoY) 12.5 12.8 12.6 10.6 10.3 10.7 9.9 9.5 9.3 9.7 9.5 9.3 -22.5 -23.1 8.7

Currency in circulation(%YoY) 21.4 20.8 17.2 15.2 13.5 12.3 10.3 9.8 9.0 8.5 7.9 7.6 - - -

10-yr Gsec yields 5.9 6.2 6.2 6.0 6.0 6.1 6.2 6.2 6.2 6.4 6.3 6.5 6.6 6.7 6.8

Credit to deposit ratio (%YoY) 72.3 72.2 72.5 71.5 70.4 70.9 70.2 70.2 70.2 70.3 70.7 71.3 71.9 71.6 72.0

Government expenditure (%YoY)* 49.5 52.9 212.6 -26.2 22.7 13.0 -23.3 40.7 50.7 10.3 1.2 19.4 50.7 - -

Indirect tax (%YoY) 34.8 35.9 65.8 416.5 110.3 20.7 25.8 33.2 33.4 23.2 14.5 -5.8 33.4 - -

APRIL 2022 | ISSUE 112 22

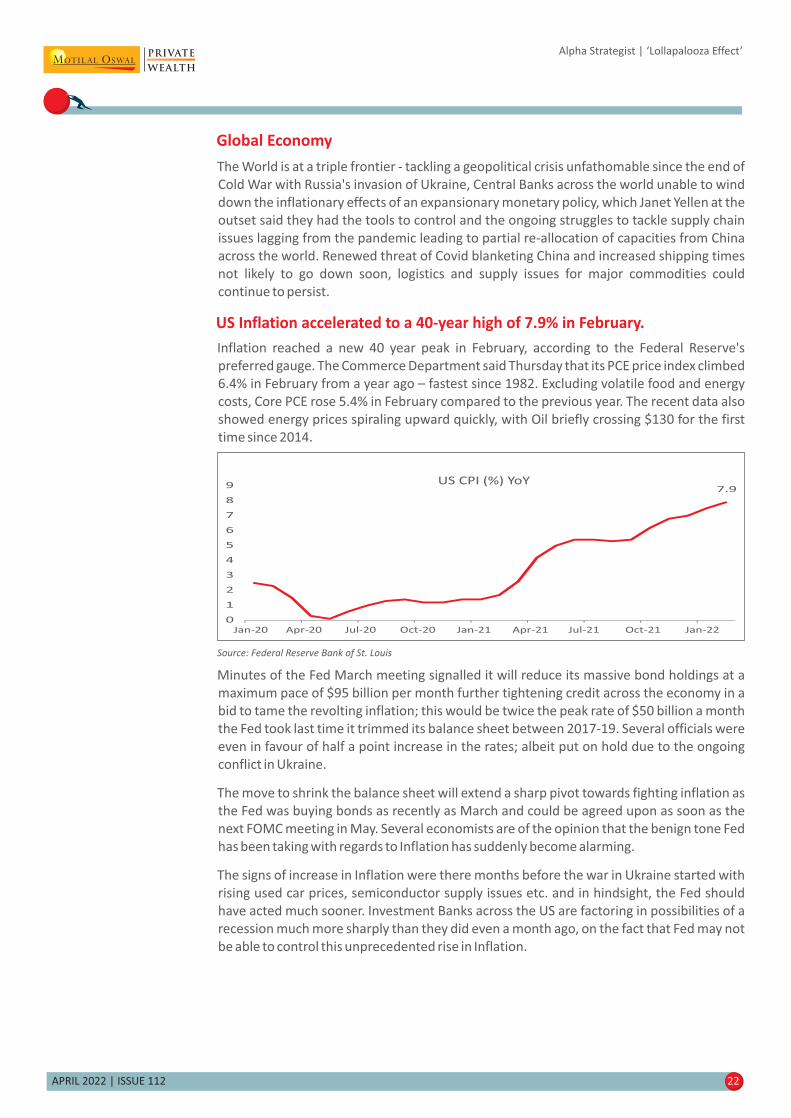

Global Economy

US Inflation accelerated to a 40-year high of 7.9% in February.

Inflation reached a new 40 year peak in February, according to the Federal Reserve's

preferred gauge. The Commerce Department said Thursday that its PCE price index climbed

6.4% in February from a year ago – fastest since 1982. Excluding volatile food and energy

costs, Core PCE rose 5.4% in February compared to the previous year. The recent data also

showed energy prices spiraling upward quickly, with Oil briefly crossing $130 for the first

time since 2014.

Alpha Strategist | ‘Lollapalooza Effect’

The World is at a triple frontier - tackling a geopolitical crisis unfathomable since the end of

Cold War with Russia's invasion of Ukraine, Central Banks across the world unable to wind

down the inflationary effects of an expansionary monetary policy, which Janet Yellen at the

outset said they had the tools to control and the ongoing struggles to tackle supply chain

issues lagging from the pandemic leading to partial re-allocation of capacities from China

across the world. Renewed threat of Covid blanketing China and increased shipping times

not likely to go down soon, logistics and supply issues for major commodities could

continue to persist.

Source: Federal Reserve Bank of St. Louis

Minutes of the Fed March meeting signalled it will reduce its massive bond holdings at a

maximum pace of $95 billion per month further tightening credit across the economy in a

bid to tame the revolting inflation; this would be twice the peak rate of $50 billion a month

the Fed took last time it trimmed its balance sheet between 2017-19. Several officials were

even in favour of half a point increase in the rates; albeit put on hold due to the ongoing

conflict in Ukraine.

The move to shrink the balance sheet will extend a sharp pivot towards fighting inflation as

the Fed was buying bonds as recently as March and could be agreed upon as soon as the

next FOMC meeting in May. Several economists are of the opinion that the benign tone Fed

has been taking with regards to Inflation has suddenly become alarming.

The signs of increase in Inflation were there months before the war in Ukraine started with

rising used car prices, semiconductor supply issues etc. and in hindsight, the Fed should

have acted much sooner. Investment Banks across the US are factoring in possibilities of a

recession much more sharply than they did even a month ago, on the fact that Fed may not

be able to control this unprecedented rise in Inflation.

7.9

0

1

2

3

4

5

6

7

8

9

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21 Jan-22

US CPI (%) YoY

APRIL 2022 | ISSUE 112 23

Alpha Strategist | ‘Lollapalooza Effect’

Indian Economy

Current Account deficit widens to 2.7% in Q3FY22

India's current account balance stood at USD23b (or 2.7% of GDP) in 3QFY22, higher than

USD10b (or 1.3% of GDP) in 2QFY22. It implies a CAD of USD26.5b (or 1.2% of GDP) in

9MFY22 as compared to a surplus of USD32.1b (or 1.7% of GDP) in 9MFY21.

Wider CAD was on account of larger merchandise trade deficit, which stood at 7.2% of GDP

(or USD60.4b), after a deficit of 5.9% of GDP (or USD44.5b) in 2QFY22. Higher imports (up

52% YoY in 3QFY22) vis-à-vis exports (up 41% YoY) led to a wider merchandise deficit.

The quantum of hit from crude related products is clearly visible here; excluding petroleum

products, India had a current account surplus of 0.8% of GDP, lower than 2.2% of GDP in

2QFY22. Excluding gold, India had a current account deficit of 1.1% of GDP in 2QFY22.

FII Outflows for the last quarter of FY22 stood at $13.5 bn, compared to $4.8 bn in the

previous quarter. What was more surprising is that DII Inflow almost stemmed the outflow

with $11.5 bn inflow in the last quarter. Going forward, a further widening of the

merchandise trade deficit in 4QFY22 could take the current account deficit to 1.5% of GDP

in FY22 as against a surplus of 0.9% in FY21.

Not unlike the global economy, India is plagued by its own set of challenges; Prominently

being an oil importing country, higher oil prices were bound to hurt economic growth; With

crude oil prices remaining above USD100/bbl, OMCs have started to pass on the increase to

consumers. The ~INR10/litre hike in petrol and diesel prices is likely to raise freight costs for

companies as well as impact consumer sentiment.

This was also highlighted in RBI's April commentary where Inflation projections were

revised upwards for FY23 to 5.7% from 4.5% just this Feb largely on account of higher

energy prices emanating from the Russia-Ukraine War; It also adjusted growth

expectations to a modest 7.2% from 7.8% previously with the latter half growth expected at

a tepid 4%. Despite headwinds, the MPC kept all policy rates unchanged in a unanimous

decision and maintained its accommodative stance to not hinder economic growth in a bid

to control inflation as RBI had stated earlier. Overall, it is clear that monetary policy

normalization in India has begun.

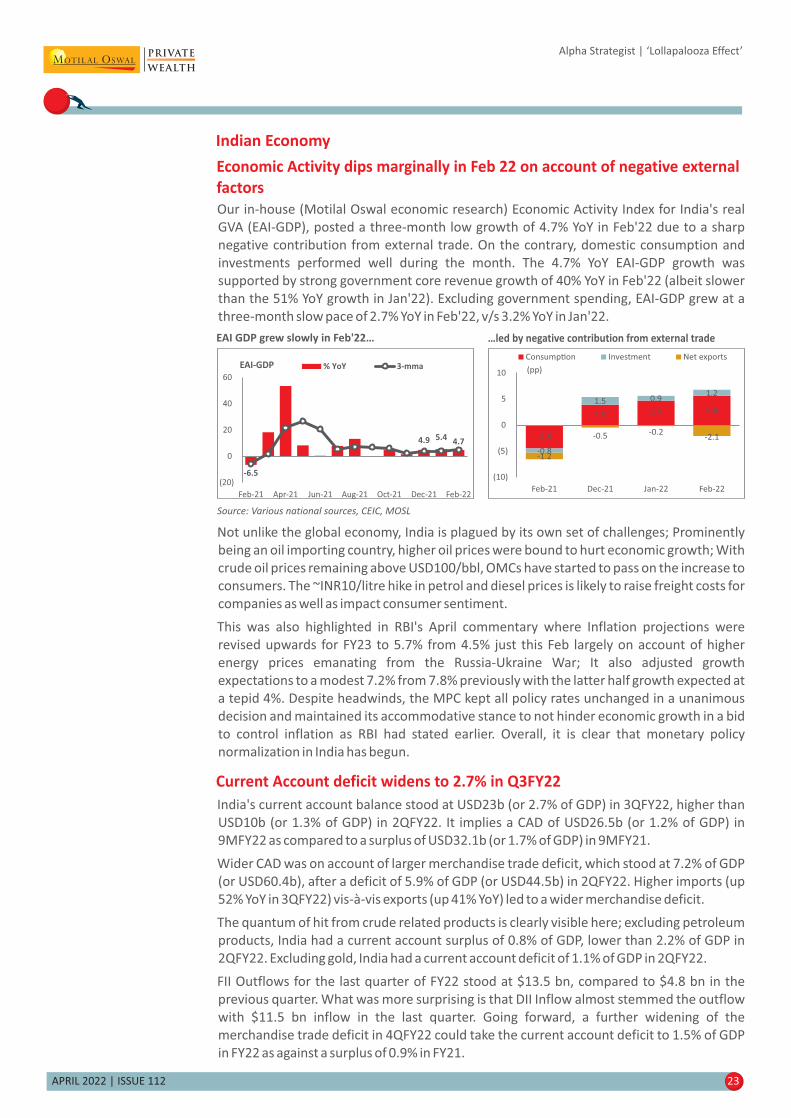

Economic Activity dips marginally in Feb 22 on account of negative external

factors

Our in-house (Motilal Oswal economic research) Economic Activity Index for India's real

GVA (EAI-GDP), posted a three-month low growth of 4.7% YoY in Feb'22 due to a sharp

negative contribution from external trade. On the contrary, domestic consumption and

investments performed well during the month. The 4.7% YoY EAI-GDP growth was

supported by strong government core revenue growth of 40% YoY in Feb'22 (albeit slower

than the 51% YoY growth in Jan'22). Excluding government spending, EAI-GDP grew at a

three-month slow pace of 2.7% YoY in Feb'22, v/s 3.2% YoY in Jan'22.

Source: Various national sources, CEIC, MOSL

EAI GDP grew slowly in Feb'22… …led by negative contribution from external trade

-6.5

4.9 5.44.7

(20)

0

20

40

60

Feb-21 Apr-21 Jun-21 Aug-21 Oct-21 Dec-21 Feb-22

EAI-GDP % YoY 3-mma

-4.5

3.9 4.7 5.6

-0.8

1.5 0.91.2

-1.2

-0.5 -0.2-2.1

(10)

(5)

0

5

10

Feb-21 Dec-21 Jan-22 Feb-22

Consump�on Investment Net exports

(pp)

APRIL 2022 | ISSUE 112 24

Alpha Strategist | ‘Lollapalooza Effect’

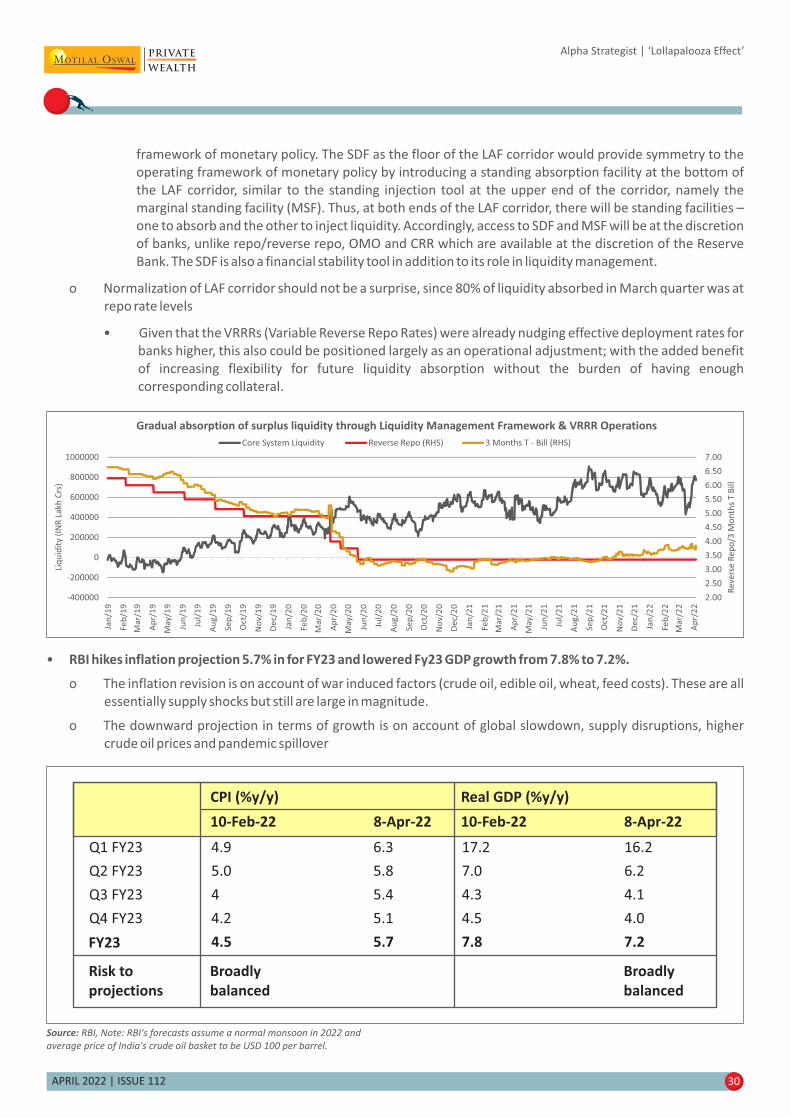

Source: Motilal Oswal Economic Research

GST Collection hits an all-time high in March of INR 1.42 trillion

A domestic economic recovery provides relief, with multiple indicators not least GST