L02-0279-LL For Agent or Broker Use Only. Not To Be Used With The General Public. L02-0279-LL Not a deposit, no FDIC-insured, not insured by any federal government agency, not guaranteed by any bank or savings association, and may go down in value.

L02-0279-LL For Agent or Broker Use Only. Not To Be Used With The General Public. L02-0279-LL Not a deposit, no FDIC-insured, not insured by any federal.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

L02-0279-LLFor Agent or Broker Use Only. Not To Be Used With The General Public.

L02-0279-LL

Not a deposit, no FDIC-insured, not insured by any federal government agency, not guaranteed by any bank or savings

association, and may go down in value.

L02-0279-LL

What is ?

• The MoneyGuard universal life insurance policies have a rider that accelerates the death benefit to pay for covered long-term care (convalescent care in MA & WA) expenses.

• Issued by The Lincoln National Life Insurance Company, Ft. Wayne, IN.

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

What is ?

the smart way

to self-insure for long-term care

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

&How does MoneyGuard fitinto their plan?

Who needs ?

financial

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• Target ages 60-75

• Currently self-insures the LTC risk

• Single women• Adequate invested assets (Excluding primary residence and qualified plan assets)

The client profile

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• Are there readily available funds for LTC?

• How much set aside?

• Where are funds?

• Which assets will be used first?

Identify source of funds

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Where are your clients’ ?assets

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Which would they use firstto pay for long-term care needs?

assets

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

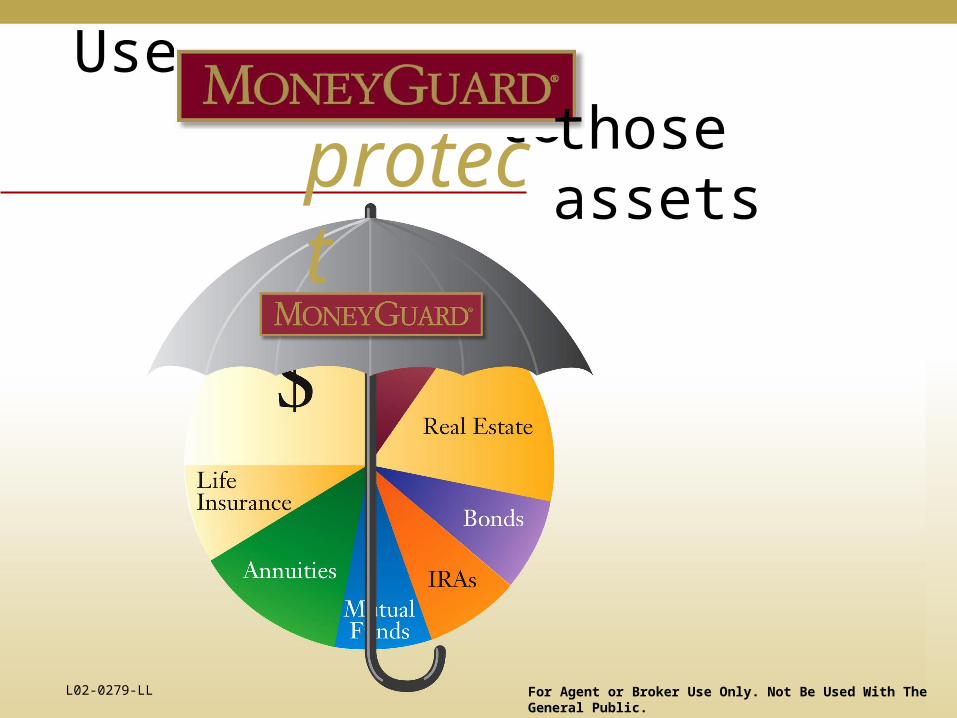

Use tothose assetsprotect

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

selling

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

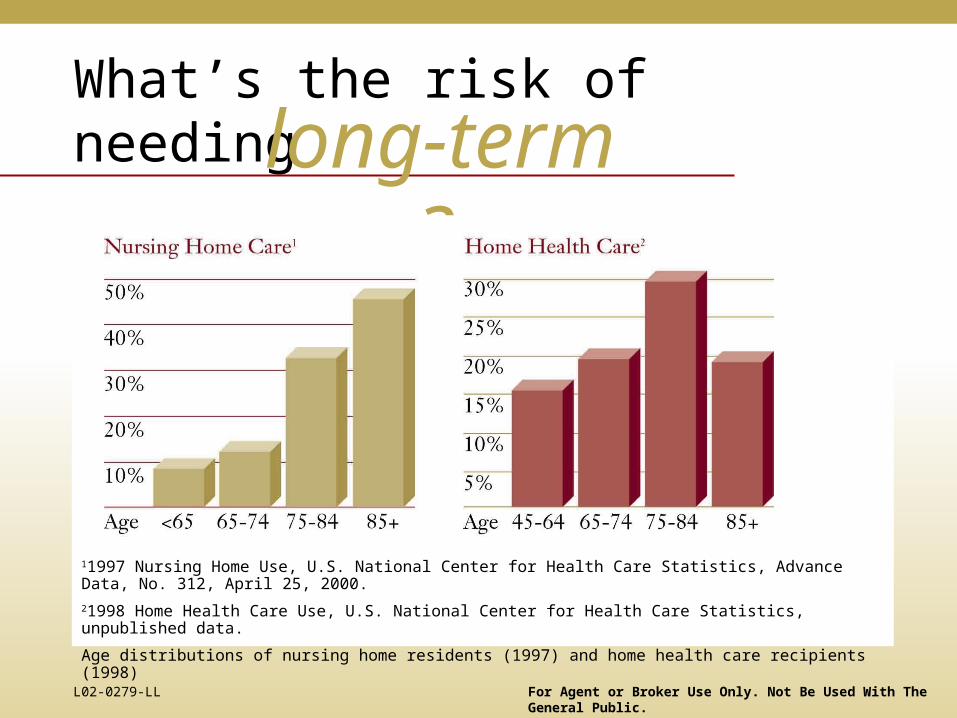

What’s the risk of needing long-term care?

11997 Nursing Home Use, U.S. National Center for Health Care Statistics, Advance Data, No. 312, April 25, 2000.

21998 Home Health Care Use, U.S. National Center for Health Care Statistics, unpublished data.

Age distributions of nursing home residents (1997) and home health care recipients (1998)

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

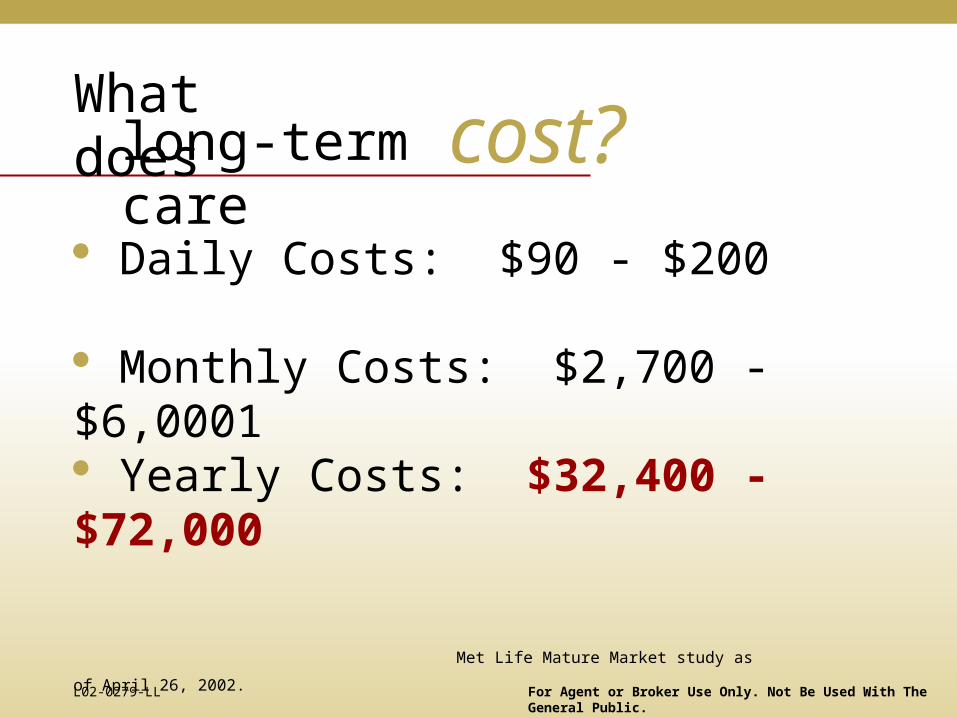

What does

Daily Costs: $90 - $200

Monthly Costs: $2,700 - $6,0001

Yearly Costs: $32,400 - $72,000

Met Life Mature Market study as of April 26, 2002.

long-term care cost?

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Who pays for

Medicare

Out Of Pocket

Medicaid

Other

<2% VA

Private Insurance

L02-0279-LL

long-term care?

11%

27%

39%

15%

7%

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Medicare Prior hospitalization required

Skilled Care only

100 days in a nursing home following a hospital confinement.

What does

cover?

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Medicaid? A Federal/State welfare program

State administered

Covers long-term care expenses once you qualify

State recovers costs from estate

What is

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

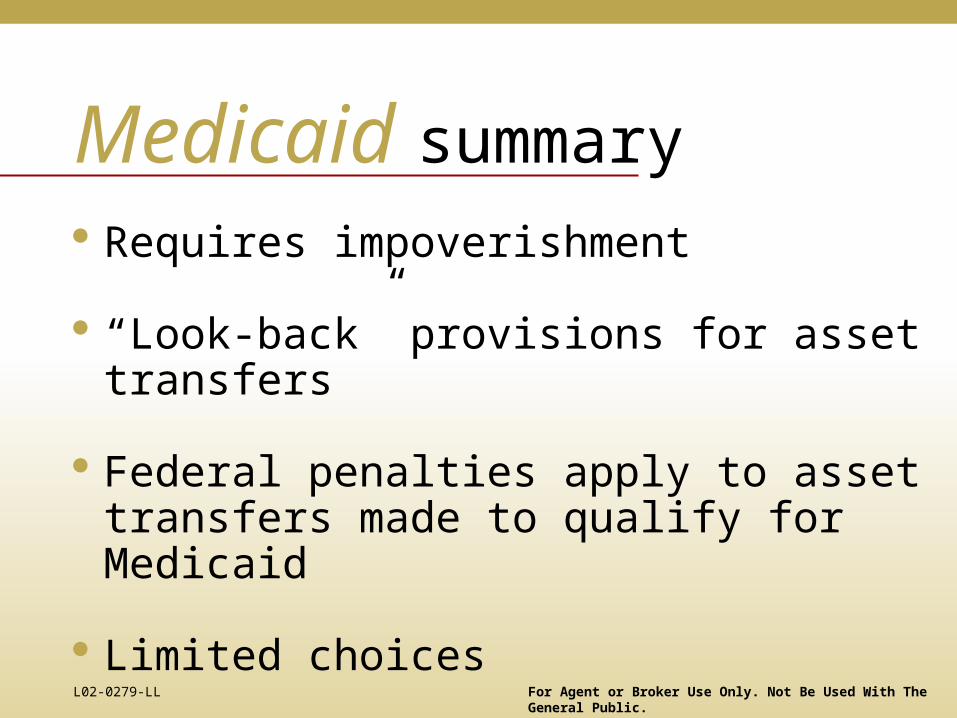

Medicaid summary Requires impoverishment

“Look-back” provisions for asset transfers

Federal penalties apply to asset transfers made to qualify for Medicaid

Limited choices

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

funding Long-Term Care

Long-Term Care Insurance

Self-Insure

options

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

is an optionself-insuring

Many of us plan to use our own assets to pay for long-term care.

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Which would you use firstto pay for long-term care needs?

assets

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Traditional long-term care insurance

ways totransfer the risk22

&

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

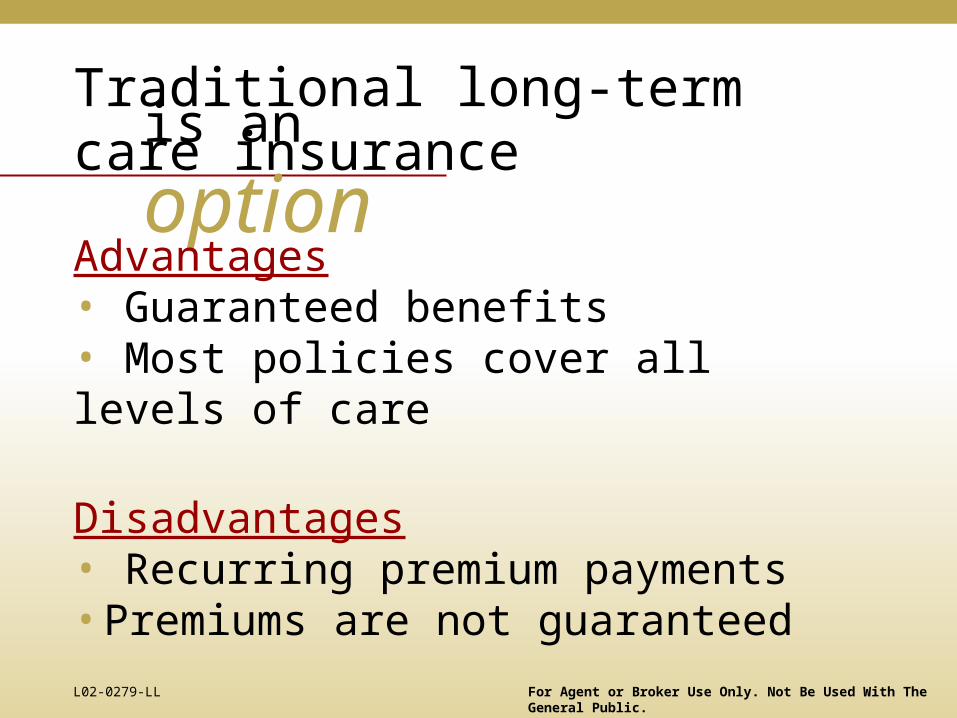

is an optionAdvantages• Guaranteed benefits• Most policies cover all levels of care

Disadvantages• Recurring premium payments• Premiums are not guaranteed

Traditional long-term care insurance

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

What if I don’t use it?

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

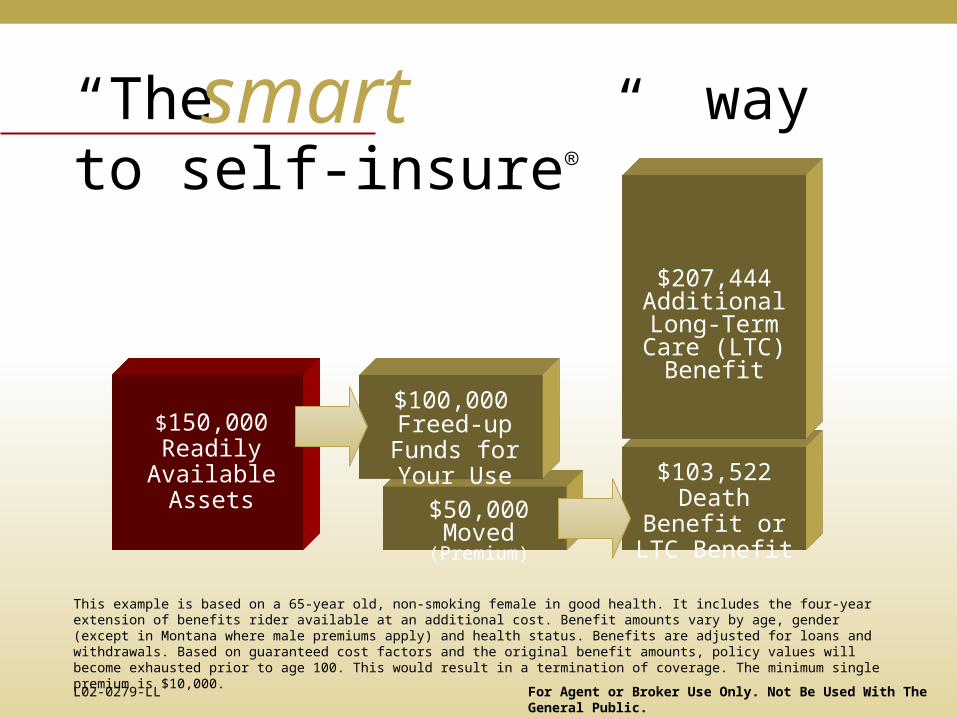

“The way to self-insure”smart

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

$150,000 Readily

Available Assets

“The way to self-insure”smart

This example is based on a 65-year old, non-smoking female in good health. It includes the four-year extension of benefits rider available at an additional cost. Benefit amounts vary by age, gender (except in Montana where male premiums apply) and health status. Benefits are adjusted for loans and withdrawals. Based on guaranteed cost factors and the original benefit amounts, policy values will become exhausted prior to age 100. This would result in a termination of coverage. The minimum single premium is $10,000.

Freed-up Funds for Your Use

$50,000 Moved (Premium)

$100,000

$207,444 Additional

Long-Term Care (LTC) Benefit

$103,522 Death Benefit or LTC

Benefit

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

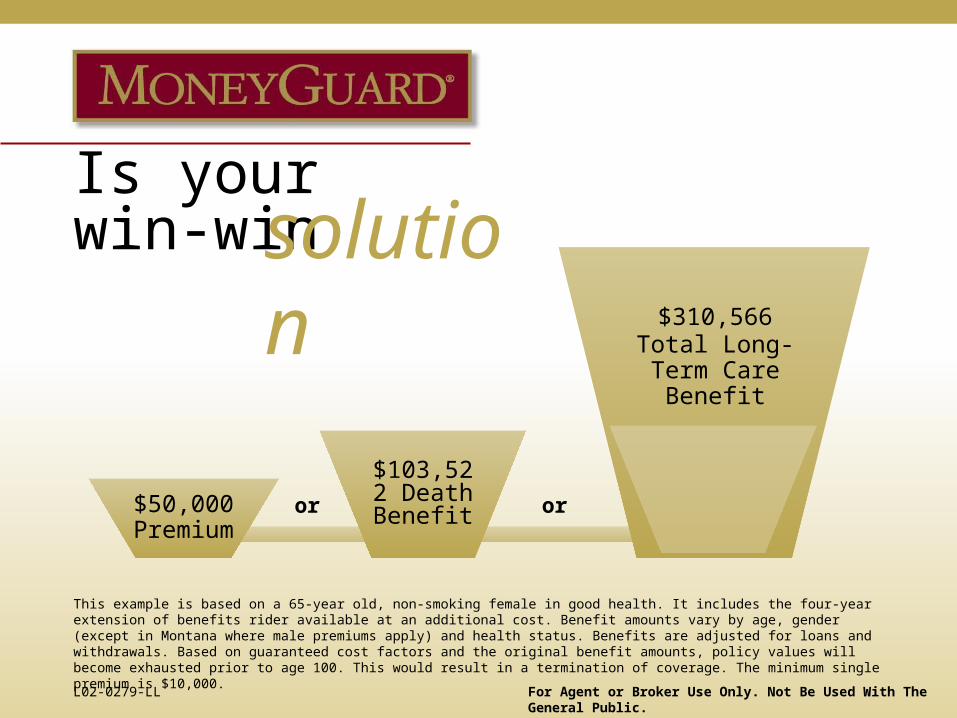

Is your win-winsolution

This example is based on a 65-year old, non-smoking female in good health. It includes the four-year extension of benefits rider available at an additional cost. Benefit amounts vary by age, gender (except in Montana where male premiums apply) and health status. Benefits are adjusted for loans and withdrawals. Based on guaranteed cost factors and the original benefit amounts, policy values will become exhausted prior to age 100. This would result in a termination of coverage. The minimum single premium is $10,000.

$310,566

or

Total Long-Term Care Benefit

$103,522 Death

Benefitor

For Agent or Broker Use Only. Not Be Used With The General Public.

$50,000 Premium

L02-0279-LL

How doescompare?

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Which option fits your plan?

• Government programs

• Self-insuring

• Traditional long-term care insurance

•

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• MoneyGuard

• MoneyGuard LS

• MoneyGuard Flex I

• MoneyGuard Flex II

• MoneyGuard VUL

optionsfunding

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

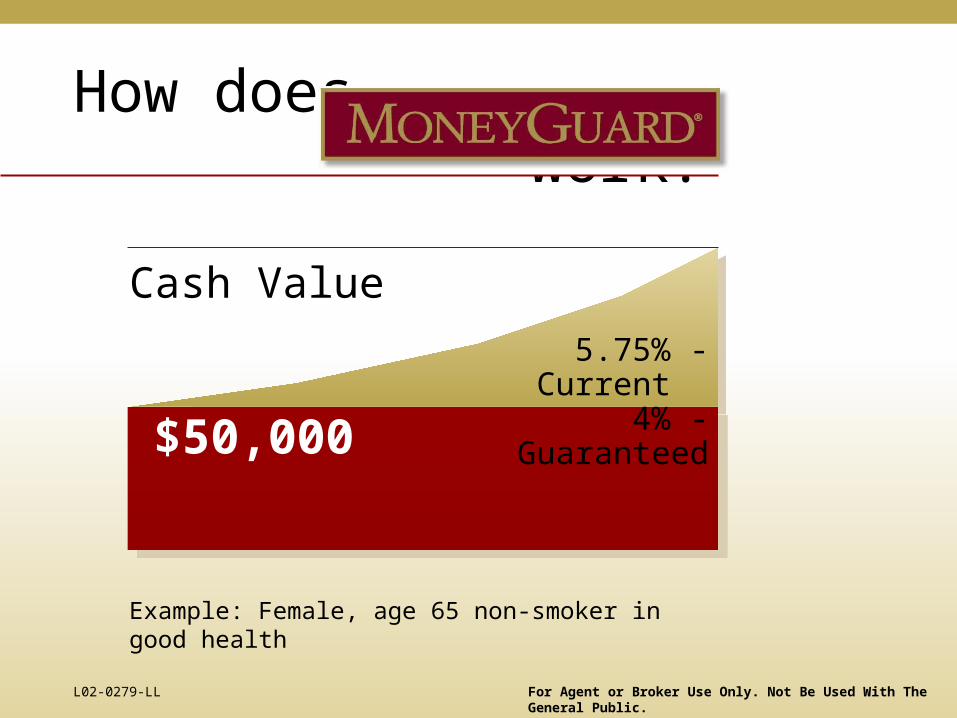

How does work?

$50,000• Guaranteed Return of Principal

• 3.5% First Year Premium Load

Example: Female, age 65 non-smoker in good health

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

How does work?

$50,000

5.75% - Current 4% - Guaranteed

Cash Value

Example: Female, age 65 non-smoker in good health

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

What if I

$50,000

$103,522 Death Benefit

Example: Female, age 65 non-smoker in good health

For Agent or Broker Use Only. Not Be Used With The General Public.

never need long-term care?

L02-0279-LL

$50,000

• 2 yr. benefit (24 months)

• $4,313/monthly

$103,522 Death Benefit

Example: Female, age 65 non-smoker in good health

What if Ineed long-term care?

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

long-term care

• All levels of care: Assisted Living*, Home Health, Nursing Home and Adult Day Care

• Homemaker and personal care

• Hospice and respite care

*Residential care in CA

features

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• 90-day elimination period

• 2 of 6 activities of daily living (bathing, continence, dressing, eating, toileting and transferring)

• Cognitive impairment

• Need for care can be certified by personal physician

long-term care triggers

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

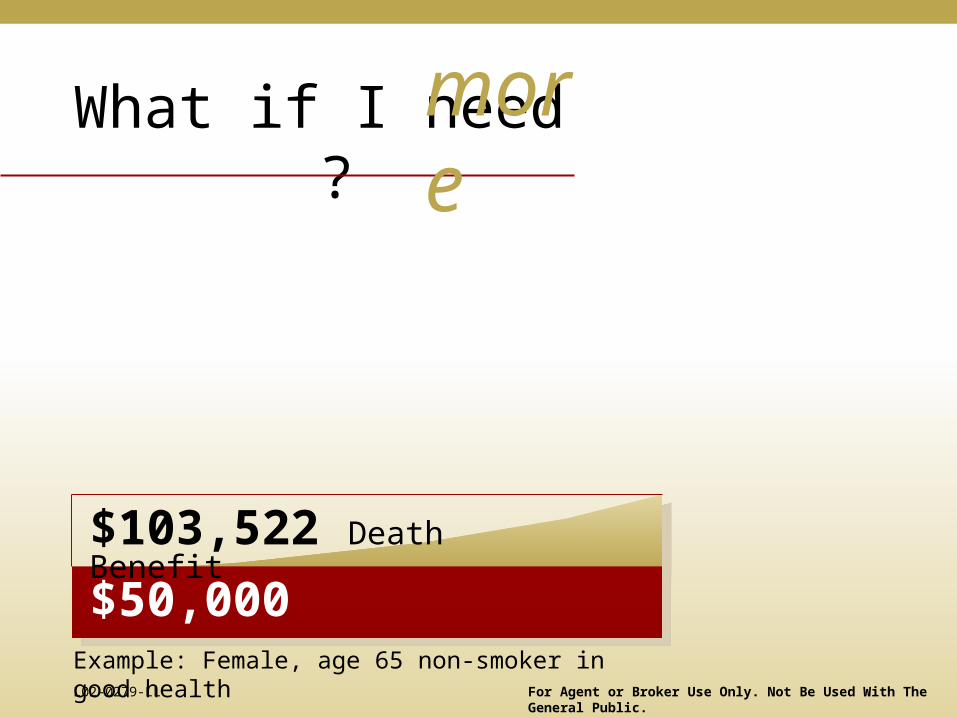

What if I need ?

Example: Female, age 65 non-smoker in good health

more

$50,000

$103,522 Death Benefit

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

$50,000

$207,044 EOB

Example: Female, age 65 non-smoker in good health

$103,522 Death Benefit

• Total 6-year benefit

• $4,313/monthly

$310,566Total LTC benefits

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Example: Female, age 65 non-smoker in good health

Will there beheirsanything left for my ?

$50,000

$207,044 EOB

$103,522 Death Benefit

$310,566Total LTC benefits

$10,352ResidualDeath Benefit

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

Will this be ?enough

Example: Female, age 65 non-smoker in good health

$50,000

$207,044 EOB

$103,522 Death Benefit

$310,566Total LTC benefits

$10,352ResidualDeath Benefit

For Agent or Broker Use Only. Not Be Used With The General Public.

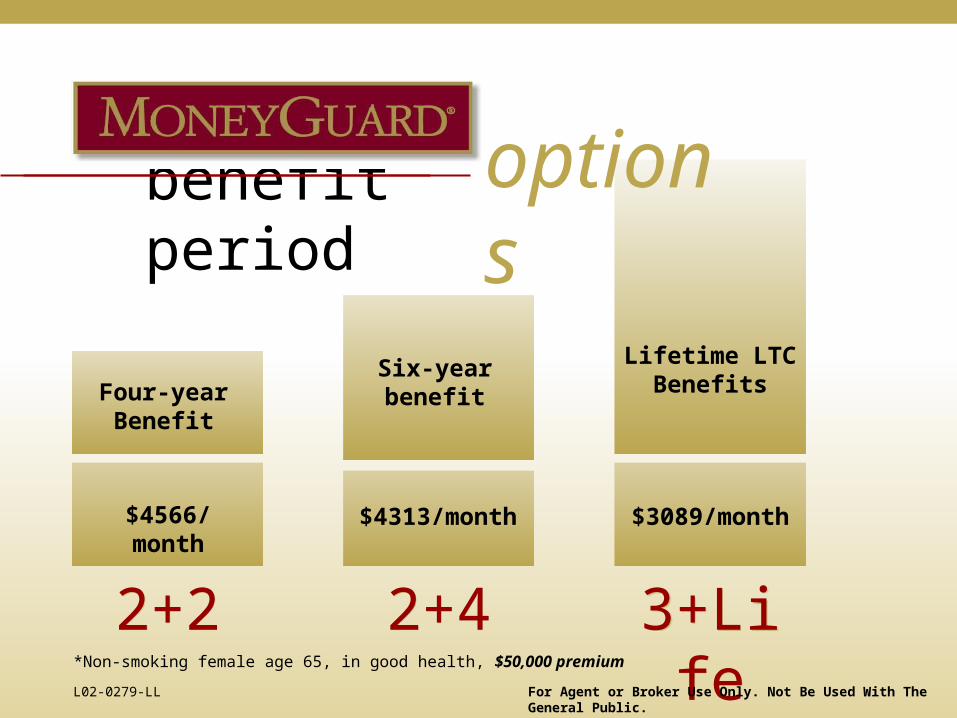

L02-0279-LL

benefit period

*Non-smoking female age 65, in good health, $50,000 premium

2+22+2

$109,572Death Benefit

$109,572Additional LTC

benefit

$103,522 Death Benefit

$207,046 Additional LTC

Benefit

2+42+4 3+Life3+Life

$111,200 Death Benefit

Lifetime LTC Benefits

options

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

benefit period

*Non-smoking female age 65, in good health, $50,000 premium

2+22+2

$4566/month

Four-yearBenefit

$4313/month

Six-year benefit

2+42+4 3+Life3+Life

$3089/month

Lifetime LTC Benefits

options

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

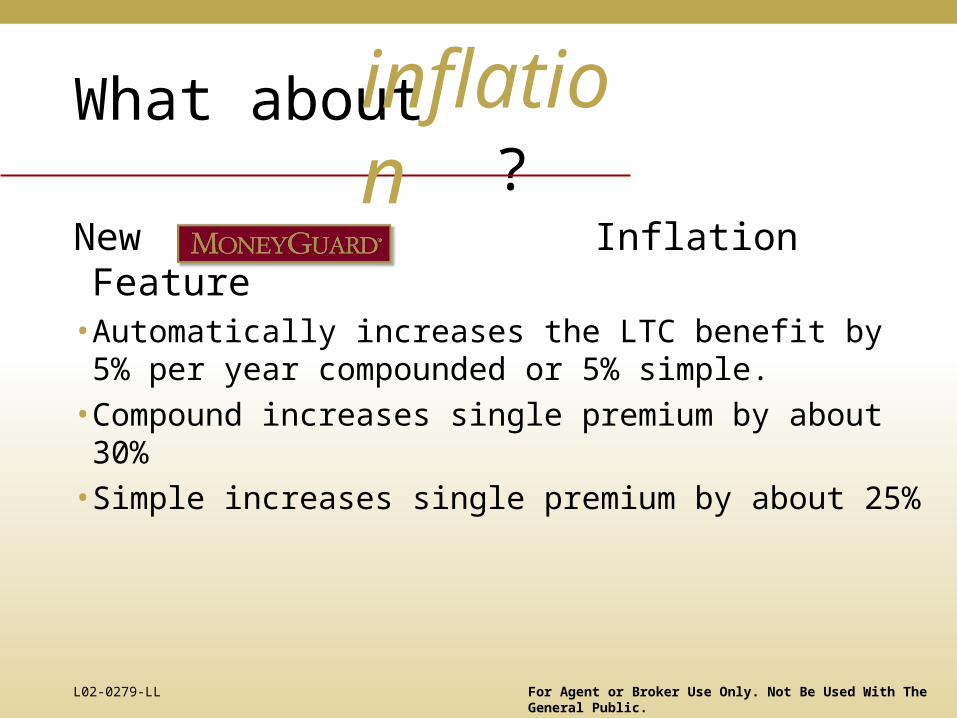

New Inflation Feature

• Automatically increases the LTC benefit by 5% per year compounded or 5% simple.

• Compound increases single premium by about 30%

• Simple increases single premium by about 25%

What about ?inflation

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

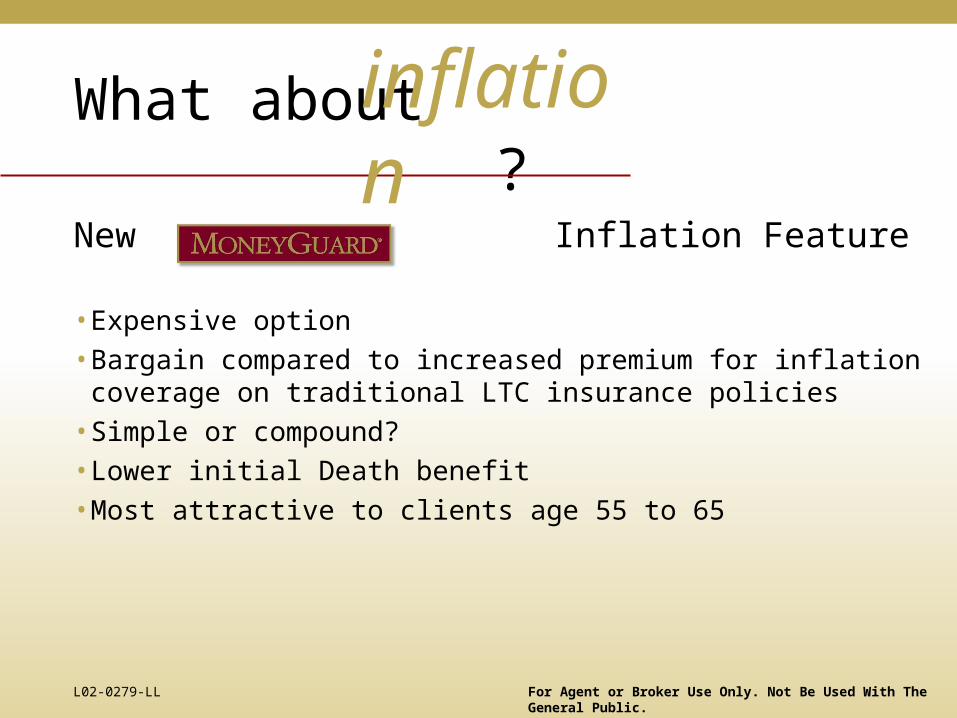

New Inflation Feature• Expensive option• Bargain compared to increased premium for inflation

coverage on traditional LTC insurance policies• Simple or compound?• Lower initial Death benefit• Most attractive to clients age 55 to 65

What about ?inflation

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• Joint-Last Survivor Design• Better chance to place the impaired risk

• Lifetime Money-back Guarantee

• Lifetime Minimum Death and LTC Benefits

• No Residual Benefit

• No Maturity Age

featureslife insurance

For Agent or Broker Use Only. Not Be Used With The General Public.

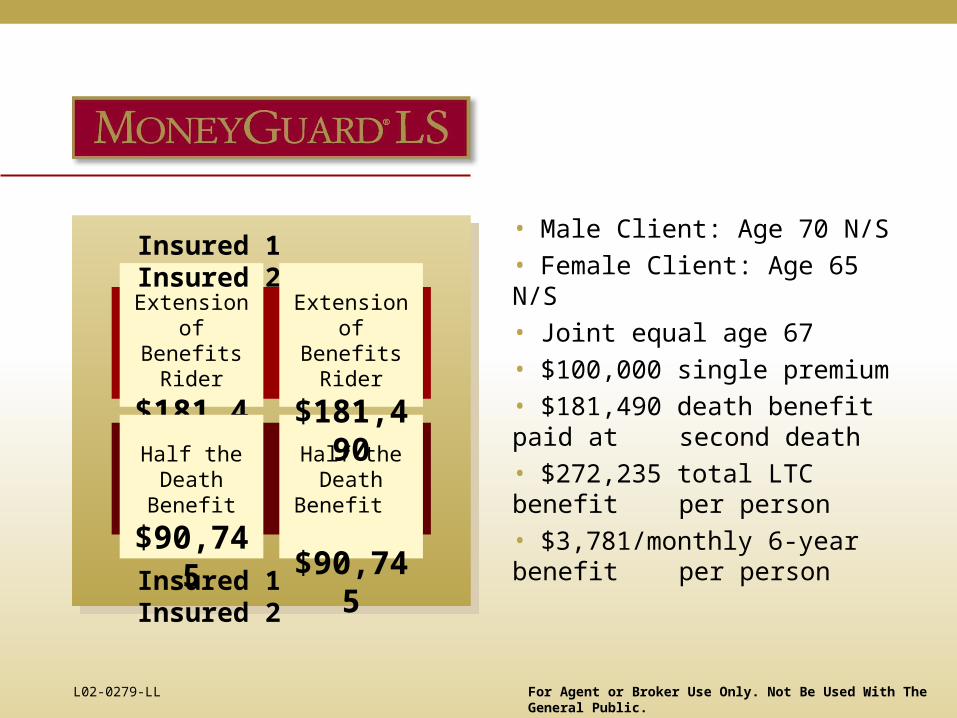

L02-0279-LL

• Male Client: Age 70 N/S

• Female Client: Age 65 N/S

• Joint equal age 67

• $100,000 single premium

• $181,490 death benefit paid at second death

• $272,235 total LTC benefit per person

• $3,781/monthly 6-year benefit per person

Extension of Benefits Rider

$181,490

Insured 1 Insured 2

Insured 1 Insured 2

Extension of Benefits Rider

$181,490

Half the Death Benefit

$90,745

Half the Death Benefit

$90,745

For Agent or Broker Use Only. Not Be Used With The General Public.

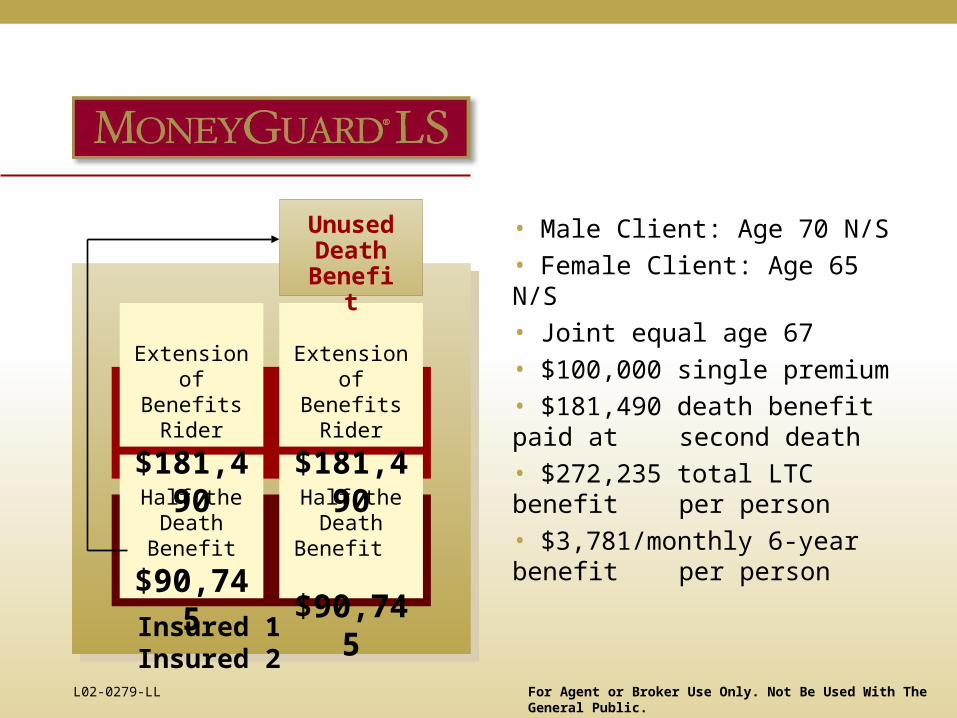

L02-0279-LL

• Male Client: Age 70 N/S

• Female Client: Age 65 N/S

• Joint equal age 67

• $100,000 single premium

• $181,490 death benefit paid at second death

• $272,235 total LTC benefit per person

• $3,781/monthly 6-year benefit per person

Insured 1 Insured 2

Half the Death Benefit

$90,745

Half the Death Benefit

$90,745

Extension of Benefits Rider

$181,490

Extension of Benefits Rider

$181,490

Unused Death

Benefit

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• Male Client: Age 70 Table 16

• Female Client: Age 65 N/S

• Joint equal age 70

• $100,000 single premium

• $160,910 death benefit paid at second death

• $241,367 total LTC benefit per person

• $3,352/monthly 6-year benefit per person

Extension of Benefits Rider

$160,910

Insured 1 Insured 2

Insured 1 Insured 2

Extension of Benefits Rider

$160,910

Half the Death Benefit

$80,455

Half the Death Benefit

$80,455

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• Minimum death benefit guarantees available on Flex II.

• 5-pay, 7-pay, 10-pay and life-pay funding only• Annual mode only

• No return of premium guarantee on Flex I or Flex II

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

• MoneyGuard is fully underwritten.

• No exams on single premium cases for clients age 60 and over.

• Contact a MoneyGuard underwriter directly!

underwriting

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LL

informationThe MoneyGuard® universal life insurance products have a rider that accelerates the death benefit to pay for covered long-term care (convalescent care in MA & WA) expenses. An Extension of Benefits rider is available at an additional cost to continue long-term care (or convalescent) care benefit payments after the entire death benefit has been paid. Issued by The Lincoln National Life Insurance Company. Products and features subject to state availability. Guarantees are subject to policy terms and conditions. MoneyGuard is a registered service mark of Lincoln National Corporation and its affiliates.

MoneyGuard VUL is offered through broker/dealers with effective selling agreements. Solicitation must be preceded or accompanied by current product and funds prospectuses. Policy value will fluctuate with the performance of the investment options selected. This product and features are subject to state availability. Policy Form VLL-2020 Series and Rider Form VLL-2802 Series.

MoneyGuard and MoneyGuard Flex Policy Form LL-2020 Series and Rider Form LL-2800 Series. MoneyGuard LS Policy Form LL-2021 Series and Rider Form LL-2801 Series.

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.

© 2002 The Lincoln National Life Insurance Company, Ft. Wayne, IN 46801 www.LFG.com/Lifewww.moneyguard.com

important

For Agent or Broker Use Only. Not Be Used With The General Public.

L02-0279-LLFor Agent or Broker Use Only. Not To Be Used With The General Public.

L02-0279-LL

Related Documents