MARGIN MARGIN 2017 KPMG UK Fiduciary Management Survey Investment Advisory kpmg.com/uk

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

2017 KPMG UK Fiduciary Management SurveyInvestment Advisory

kpmg.com/uk

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

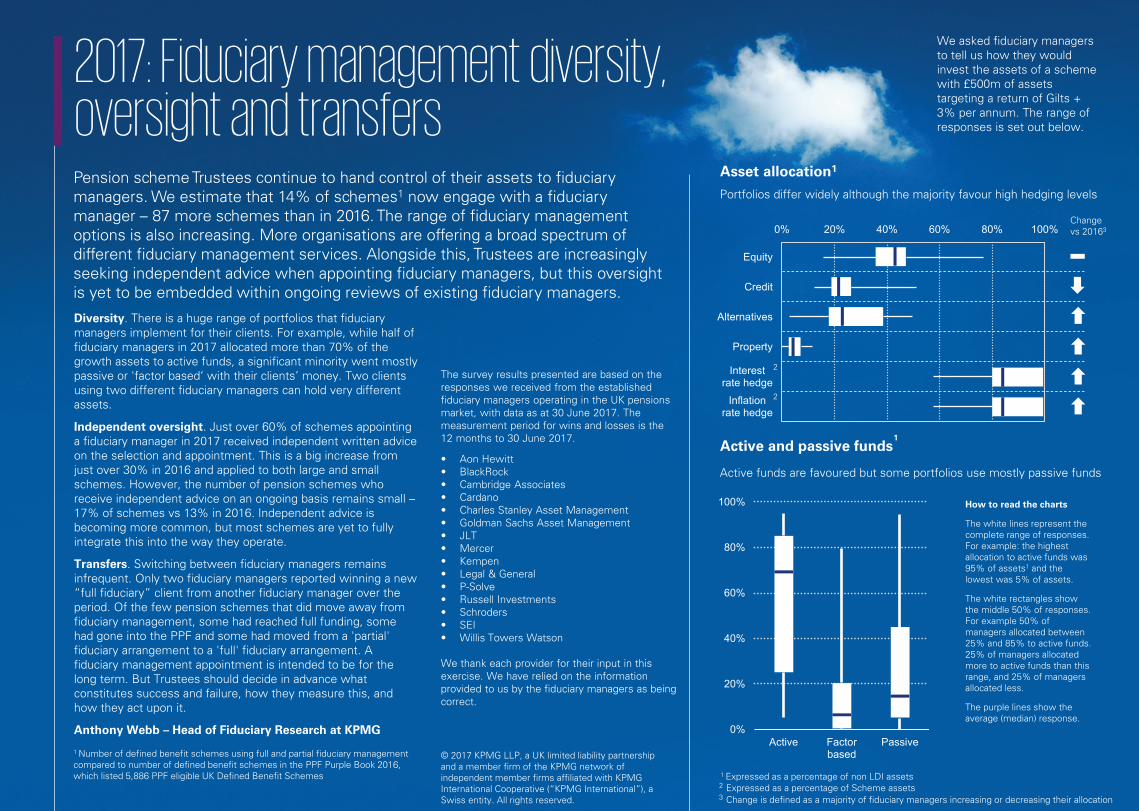

2017: Fiduciary management diversity, oversight and transfersPension scheme Trustees continue to hand control of their assets to fiduciary managers. We estimate that 14% of schemes1 now engage with a fiduciary manager – 87 more schemes than in 2016. The range of fiduciary management options is also increasing. More organisations are offering a broad spectrum of different fiduciary management services. Alongside this, Trustees are increasingly seeking independent advice when appointing fiduciary managers, but this oversight is yet to be embedded within ongoing reviews of existing fiduciary managers.

Diversity. There is a huge range of portfolios that fiduciary managers implement for their clients. For example, while half of fiduciary managers in 2017 allocated more than 70% of the growth assets to active funds, a significant minority went mostly passive or 'factor based‘ with their clients’ money. Two clients using two different fiduciary managers can hold very different assets.

Independent oversight. Just over 60% of schemes appointing a fiduciary manager in 2017 received independent written advice on the selection and appointment. This is a big increase from just over 30% in 2016 and applied to both large and small schemes. However, the number of pension schemes who receive independent advice on an ongoing basis remains small –17% of schemes vs 13% in 2016. Independent advice is becoming more common, but most schemes are yet to fully integrate this into the way they operate.

Transfers. Switching between fiduciary managers remains infrequent. Only two fiduciary managers reported winning a new “full fiduciary” client from another fiduciary manager over the period. Of the few pension schemes that did move away from fiduciary management, some had reached full funding, some had gone into the PPF and some had moved from a 'partial' fiduciary arrangement to a 'full' fiduciary arrangement. A fiduciary management appointment is intended to be for the long term. But Trustees should decide in advance what constitutes success and failure, how they measure this, and how they act upon it.

Anthony Webb – Head of Fiduciary Research at KPMG

1 Number of defined benefit schemes using full and partial fiduciary management compared to number of defined benefit schemes in the PPF Purple Book 2016, which listed 5,886 PPF eligible UK Defined Benefit Schemes

The survey results presented are based on the responses we received from the established fiduciary managers operating in the UK pensions market, with data as at 30 June 2017. The measurement period for wins and losses is the 12 months to 30 June 2017.

• Aon Hewitt• BlackRock• Cambridge Associates• Cardano• Charles Stanley Asset Management• Goldman Sachs Asset Management• JLT• Mercer• Kempen• Legal & General• P-Solve• Russell Investments• Schroders• SEI• Willis Towers Watson

We thank each provider for their input in this exercise. We have relied on the information provided to us by the fiduciary managers as being correct.

We asked fiduciary managers to tell us how they would invest the assets of a scheme with £500m of assets targeting a return of Gilts + 3% per annum. The range of responses is set out below.

Asset allocation1

Portfolios differ widely although the majority favour high hedging levels

0%

20%

40%

60%

80%

100%

Active Factorbased

Passive

Equity

Credit

ernatives

Property

Interestte hedgeInflationte hedge

2

2

0% 20% 40% 60% 80% 100%

Alt

ra

ra

1Active and passive funds

Active funds are favoured but some portfolios use mostly passive funds

How to read the charts

The white lines represent the complete range of responses. For example: the highest allocation to active funds was 95% of assets1 and the lowest was 5% of assets.

The white rectangles show the middle 50% of responses. For example 50% of managers allocated between 25% and 85% to active funds. 25% of managers allocated more to active funds than this range, and 25% of managers allocated less.

The purple lines show the average (median) response.

Change vs 20163

1 Expressed as a percentage of non LDI assets2 Expressed as a percentage of Scheme assets3 Change is defined as a majority of fiduciary managers increasing or decreasing their allocation

© 2017 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

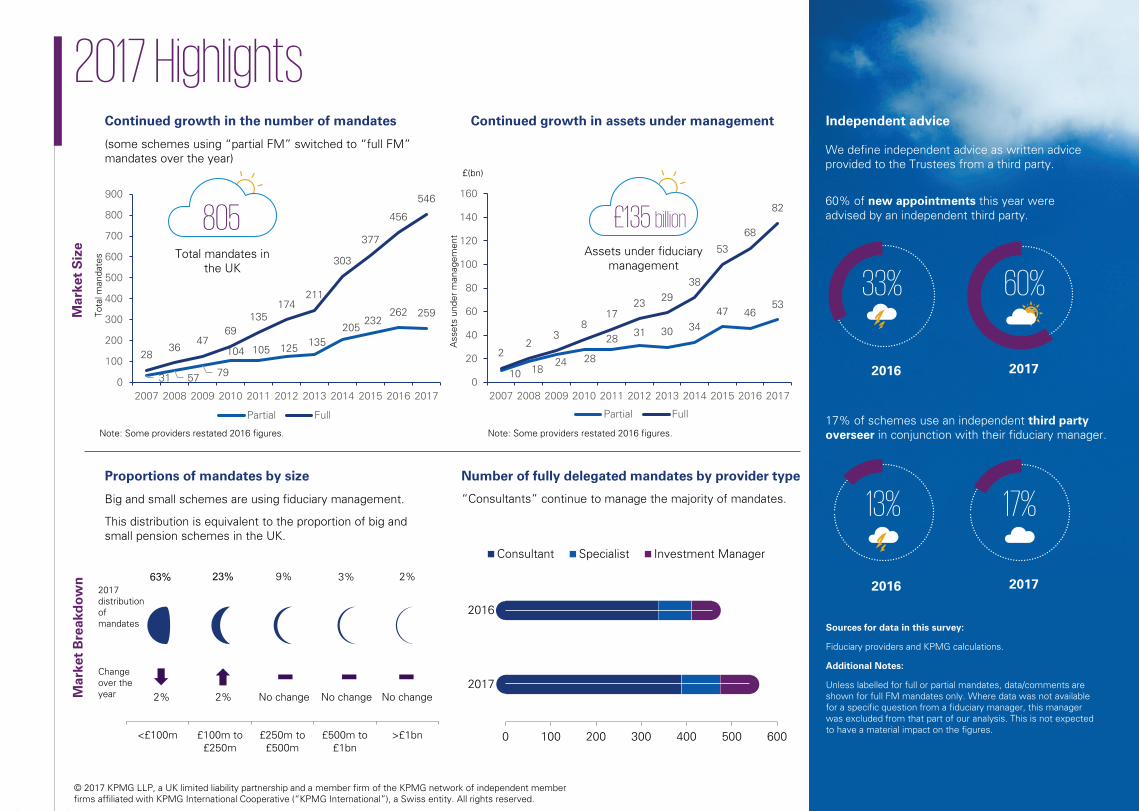

2017 HighlightsContinued growth in the number of mandates

(some schemes using “partial FM” switched to “full FM” mandates over the year)

Note: Some providers restated 2016 figures.

Continued growth in assets under management

Note: Some providers restated 2016 figures.

Proportions of mandates by size

Big and small schemes are using fiduciary management.

This distribution is equivalent to the proportion of big and small pension schemes in the UK.

nd

ow

kare

Bt

kear

M

Number of fully delegated mandates by provider type

“Consultants” continue to manage the majority of mandates.

Independent advice

We define independent advice as written advice provided to the Trustees from a third party.

60% of new appointments this year were advised by an independent third party.

2016 2017

17% of schemes use an independent third party overseer in conjunction with their fiduciary manager.

2016

13%

2017

17%

60%

31 57 79

104 105 125 135205

232262 259

2836

4769

135174

211

303

377

456

546

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Partial Full

Total mandates in the UK

805

Mar

ket

Siz

e

Tota

l man

date

s

10 1824 28

28 31 30 3447 46

53

22

38

1723 29

38

53

68

82

0

20

40

60

80

100

120

140

160

£(bn)

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Partial Full

Sources for data in this survey:

Fiduciary providers and KPMG calculations.

Additional Notes:

Unless labelled for full or partial mandates, data/comments are shown for full FM mandates only. Where data was not available for a specific question from a fiduciary manager, this manager was excluded from that part of our analysis. This is not expected to have a material impact on the figures.

Assets under fiduciary management

0 100 200 300 400 500 600

2017

2016

Consultant Specialist Investment Manager

63% 23% 9% 3% 2%

<£100m £100m to£250m

£250m to£500m

£500m to£1bn

>£1bn

£135 billion

33%

2% 2% No change No change No change

Change over the year

2017 distribution of mandates

Ass

ets

unde

r m

anag

emen

t

© 2017 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

EDGE OF PAGEMARGIN

CR

OP

MA

RK

SM

AR

GIN

KPMG and fiduciary management advice

Where does KPMG fit in?

KPMG is experienced in providing independent advice on a wide range of aspects of fiduciary management.

This includes the following:

• Governance assessment

Deciding if fiduciary management is appropriate, and if so, which governance structure is right.

• Fiduciary management selection

From setting criteria to assisting with selection exercises.

• Mandate & guidelines set-up

Setting up and designing the framework against which to measure the provider.

• Ongoing monitoring & reporting

Independently checking progress against objectives and providing challenge where necessary.

• One-off independent reviews

Assessing the manager’s progress since inception, and providing insight into its capabilities.

Anthony Webb FIA

Head of Fiduciary Research, Investment Advisory

KPMG15 Canada SquareLondon E14 5GL

+44 (0)20 7311 8508+44 (0)75 5758 [email protected]

Faye Mullen CFA

Executive Consultant,Investment Advisory

KPMG1 Sovereign SquareLeeds LS1 4DA

+44 (0)113 231 3076+44 (0)74 6835 [email protected]

Editors: Anthony Webb, Faye Mullen

Authors: Daniel Walsh, Alexander Owen, Shawn Mwatu

Definitions used in this survey

Full delegation – the fiduciary manager is typically engaged under an investment management agreement to manage 100% of scheme assets. The services provided include all or the majority of the following: journey plan design, strategic and tactical asset allocation, growth and matching portfolio structuring, manager selection, implementation and administration.

Partial delegation – Trustees delegate only a subset of the investment management to provider. The subset may comprise a portion of the scheme assets or a portion of the “full fiduciary” responsibilities.

For further information on fiduciary management…

…please see our three page guide, which addresses the questions:

• Is fiduciary management right for me?• How to choose a fiduciary manager?• Keeping your fiduciary manager on track.

This is available at the link:https://home.kpmg.com/uk/en/home/services/tax/pensions/fiduciary-management-advisory.html

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2017 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

© 2017 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Related Documents