KPMG Power and Utilities Tax Conference 12 June 2015

KPMG Power & Utilities Tax Conference – June 2015

Aug 05, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

KPMG Power and Utilities Tax Conference

12 June 2015

Welcome and introductions

Andrew Lister

KPMG Partner and Head of Energy and Natural Resources Tax

2© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

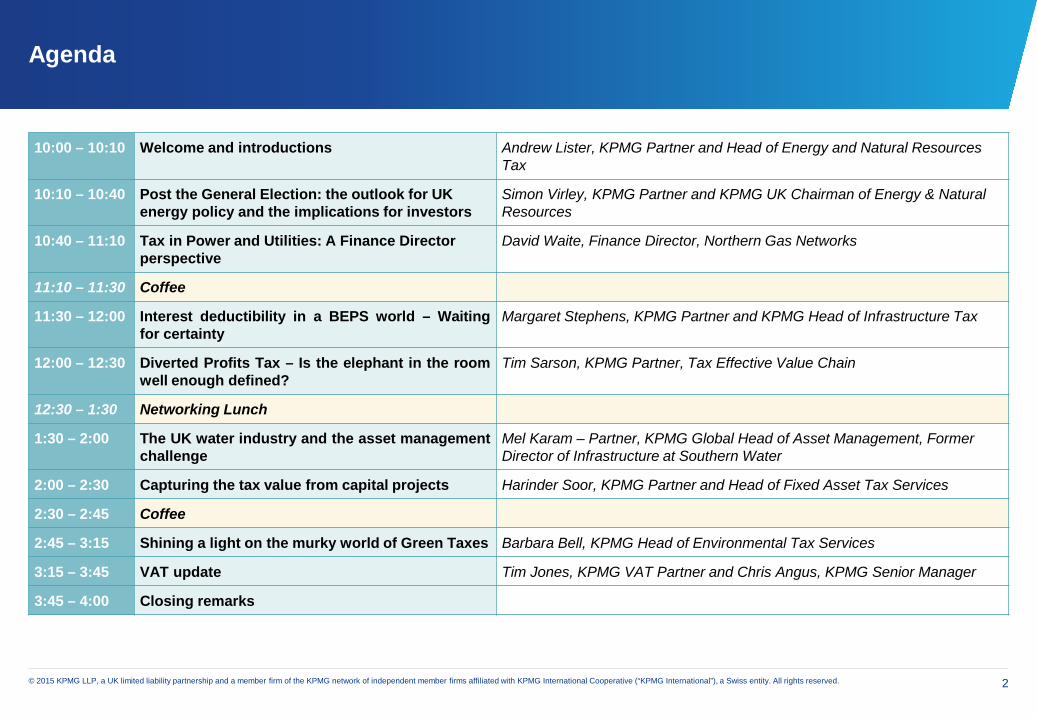

10:00 – 10:10 Welcome and introductions Andrew Lister, KPMG Partner and Head of Energy and Natural Resources Tax

10:10 – 10:40 Post the General Election: the outlook for UK energy policy and the implications for investors

Simon Virley, KPMG Partner and KPMG UK Chairman of Energy & Natural Resources

10:40 – 11:10 Tax in Power and Utilities: A Finance Director perspective

David Waite, Finance Director, Northern Gas Networks

11:10 – 11:30 Coffee

11:30 – 12:00 Interest deductibility in a BEPS world – Waitingfor certainty

Margaret Stephens, KPMG Partner and KPMG Head of Infrastructure Tax

12:00 – 12:30 Diverted Profits Tax – Is the elephant in the roomwell enough defined?

Tim Sarson, KPMG Partner, Tax Effective Value Chain

12:30 – 1:30 Networking Lunch

1:30 – 2:00 The UK water industry and the asset managementchallenge

Mel Karam – Partner, KPMG Global Head of Asset Management, Former Director of Infrastructure at Southern Water

2:00 – 2:30 Capturing the tax value from capital projects Harinder Soor, KPMG Partner and Head of Fixed Asset Tax Services

2:30 – 2:45 Coffee

2:45 – 3:15 Shining a light on the murky world of Green Taxes Barbara Bell, KPMG Head of Environmental Tax Services

3:15 – 3:45 VAT update Tim Jones, KPMG VAT Partner and Chris Angus, KPMG Senior Manager

3:45 – 4:00 Closing remarks

Post the General Election: the outlook for

UK energy policy and the implications for

investorsSimon Virley

KPMG partner and KPMG UK Chairman of Energy & Natural Resources

4© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

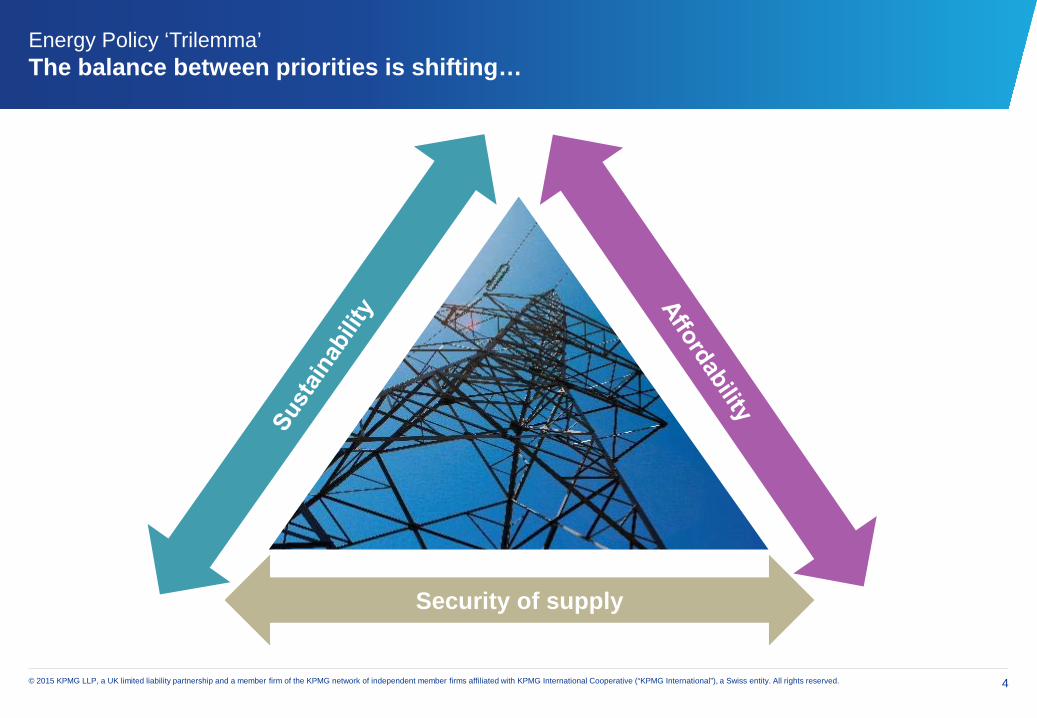

Energy Policy ‘Trilemma’The balance between priorities is shifting…

Security of supply

5© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

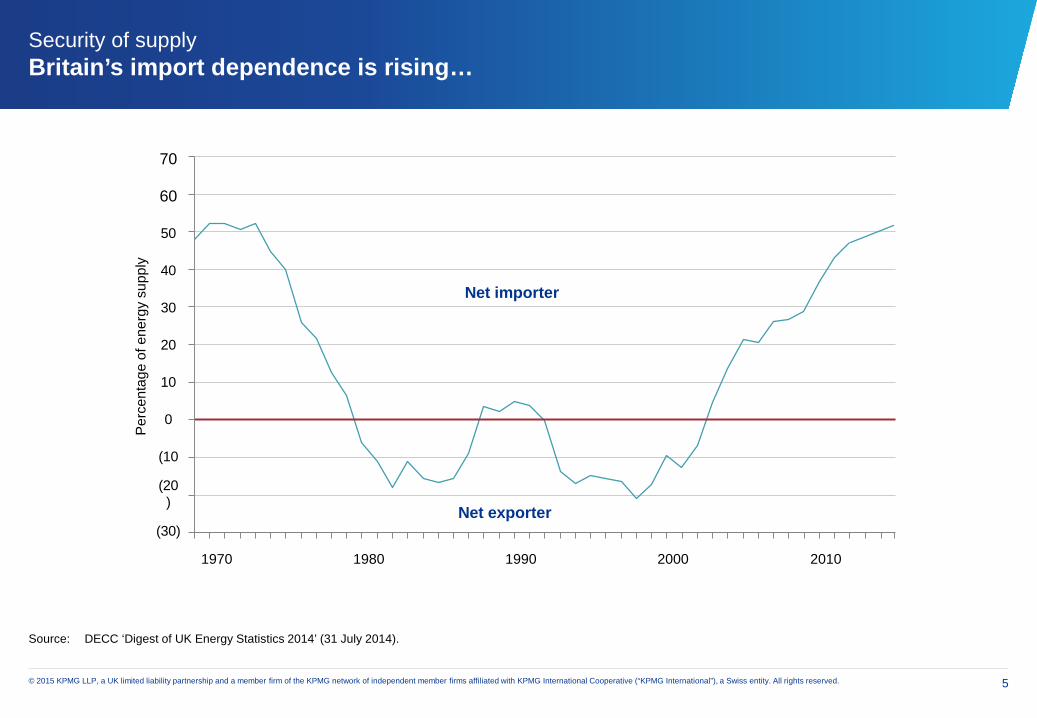

Security of supplyBritain’s import dependence is rising…

Source: DECC ‘Digest of UK Energy Statistics 2014’ (31 July 2014).

Net exporter

Per

cent

age

ofen

ergy

supp

ly

Net importer

20102000199019801970

70

(30)

60

50

40

30

20

10

0

(10

(20)

6© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

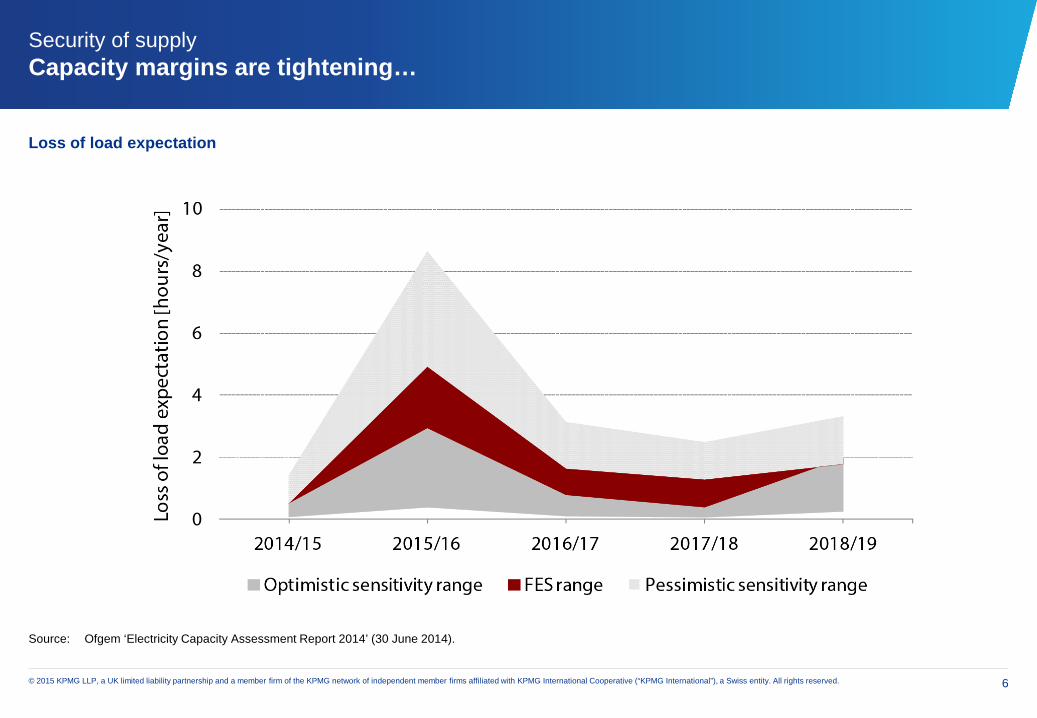

Security of supplyCapacity margins are tightening…

Loss of load expectation

Source: Ofgem ‘Electricity Capacity Assessment Report 2014’ (30 June 2014).

7© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

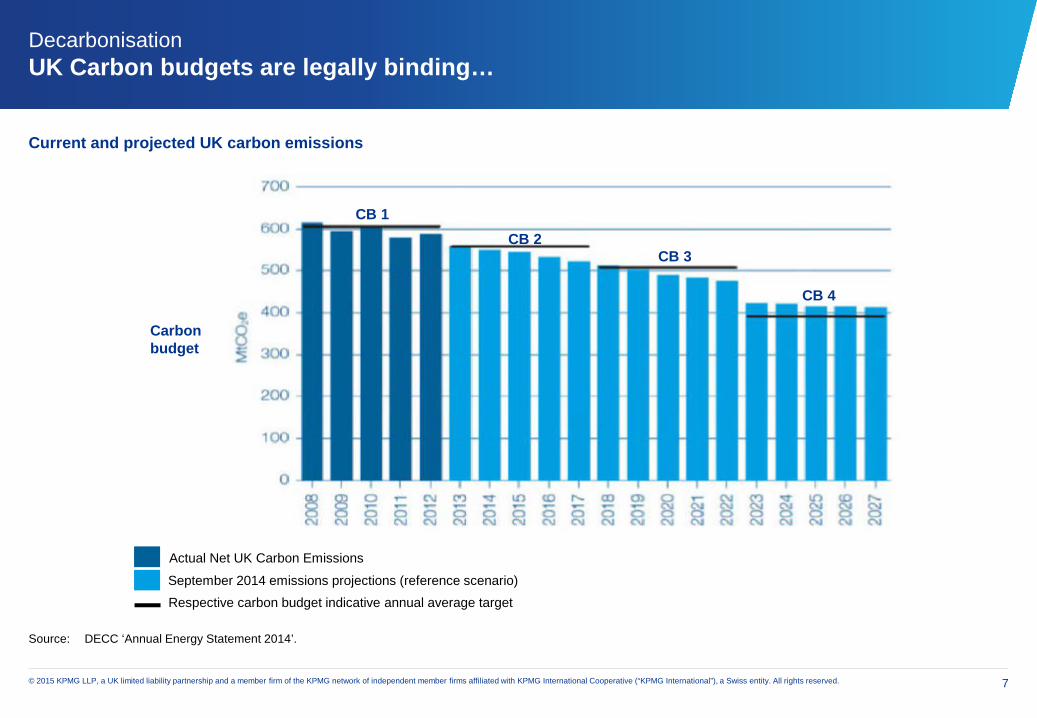

DecarbonisationUK Carbon budgets are legally binding…

Source: DECC ‘Annual Energy Statement 2014’.

CB 2 CB 3

CB 4

CB 1

Carbon budget

Actual Net UK Carbon Emissions

September 2014 emissions projections (reference scenario)Respective carbon budget indicative annual average target

Current and projected UK carbon emissions

8© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

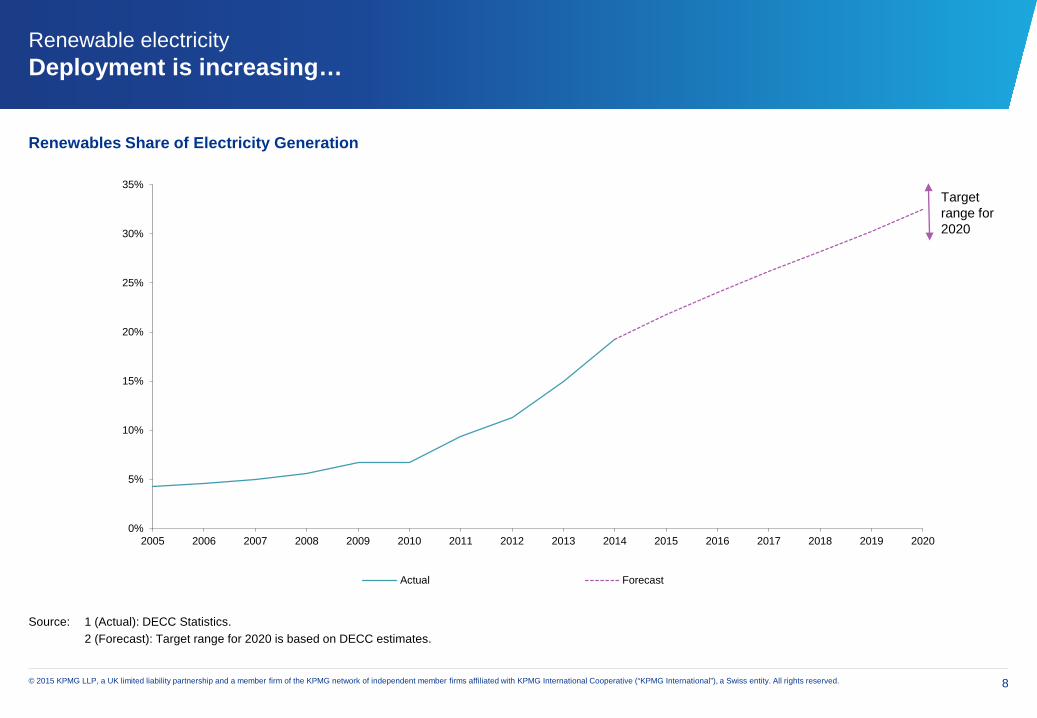

Renewable electricityDeployment is increasing…

Renewables Share of Electricity Generation

Source: 1 (Actual): DECC Statistics.2 (Forecast): Target range for 2020 is based on DECC estimates.

0%

5%

10%

15%

20%

25%

30%

35%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Actual Forecast

Target range for 2020

9© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

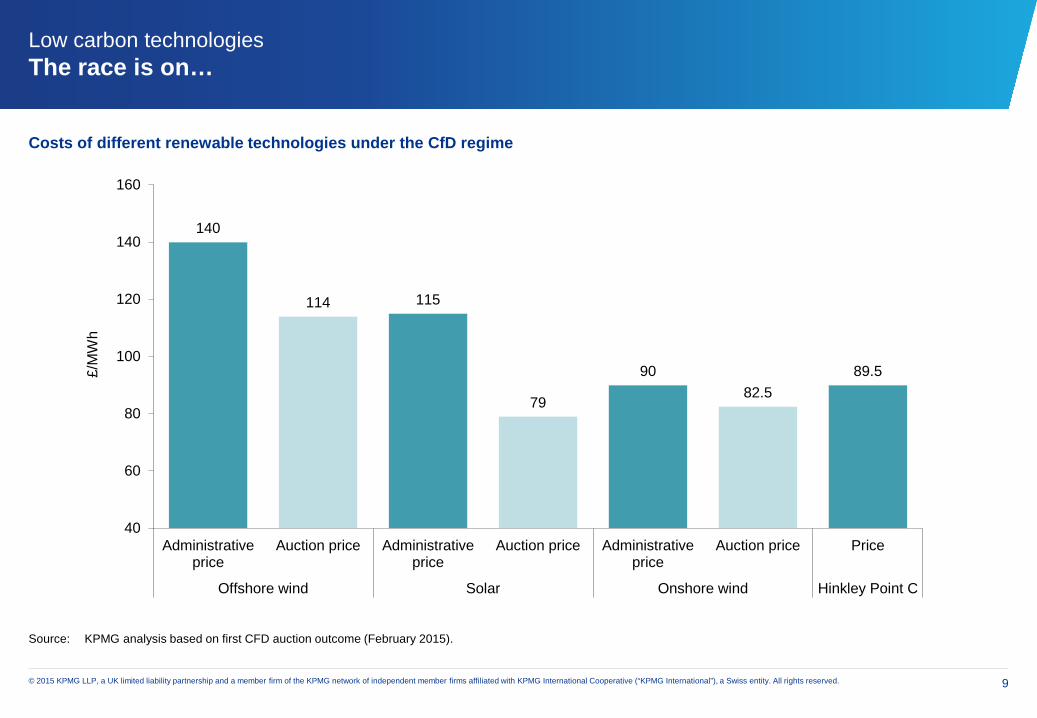

Low carbon technologiesThe race is on…

Costs of different renewable technologies under the CfD regime

140

114 115

79

9082.5

89.5

40

60

80

100

120

140

160

Administrativeprice

Auction price Administrativeprice

Auction price Administrativeprice

Auction price Price

Offshore wind Solar Onshore wind Hinkley Point C

£/M

Wh

Source: KPMG analysis based on first CFD auction outcome (February 2015).

10© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

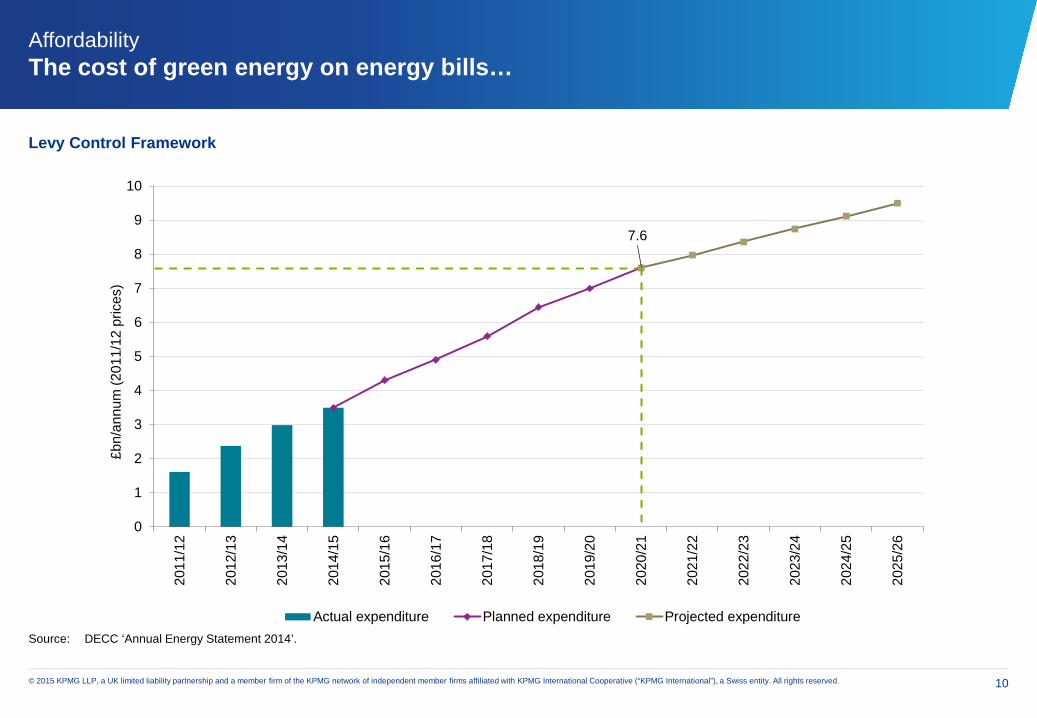

AffordabilityThe cost of green energy on energy bills…

Levy Control Framework

7.6

0

1

2

3

4

5

6

7

8

9

1020

11/1

2

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

2021

/22

2022

/23

2023

/24

2024

/25

2025

/26

£bn/

annu

m (2

011/

12 p

rices

)

Actual expenditure Planned expenditure Projected expenditureSource: DECC ‘Annual Energy Statement 2014’.

11© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

CMA Energy Market investigationPotential outcomes…

The market rules and regulation distort competition■ No major competition issues, but complexity may be a problem (see below)Generation and Vertical Integration ■ Initial views suggest the CMA does not see major competition issues in generation

markets■ Vertical integration – No major competition issues; additional ring-fencing requirements

may be recommended Energy suppliers face weak incentives to compete on price■ Retail tariff choice – CMA may recommend an increase from current mandated four

tariffs per supplierRegulatory complexity as barrier to entry ■ This suggests code/industry governance reform may be recommended

12© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The outlook for UK energy policySome provisional conclusions…

Focus will be on affordability and value for money

Commitment to stop funding for new onshore wind

Gas and nuclear to play key role

Legal targets for decarbonisation remain in place

CMA recommendations will be accepted and implemented

Potential for disruptive technology change

Security of supply challenges remain over the next few years

13

The role of the Tax function- a Finance Director’s viewKPMG Power and Utilities Tax Conference12 June 2015

14

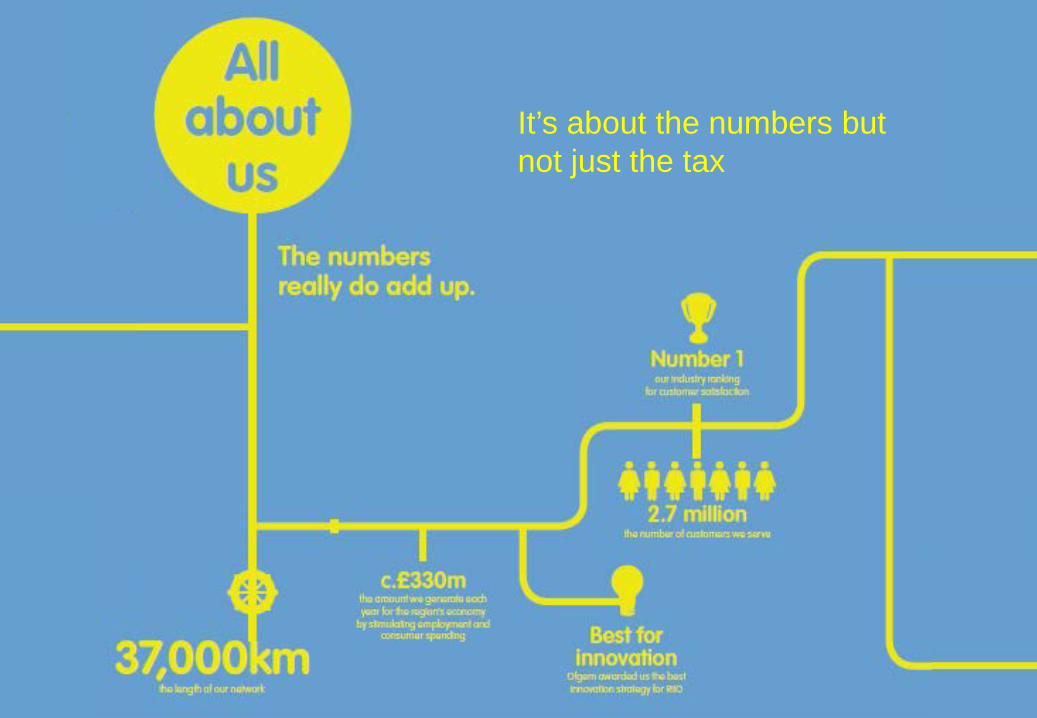

It’s about the numbers butnot just the tax

15

The Finance Director’s agenda• Long term ownership and long term stewardship of assets

• Strong emphasis on corporate governance and reputation with robust internal control framework

• No surprises! – earnings focus / delivering the Budget!

• Tax just like all costs has always been in the board room

• Reduction in tax rates welcome – equally need to signal bad news

• Factor risk into investment appraisals – country/political, inflation, interest rate / currency, change of law and tax!!`

• View of tax will depend on ownership structure UK, US, HK, China , Australia – all very different!!

• Regulatory angle

16

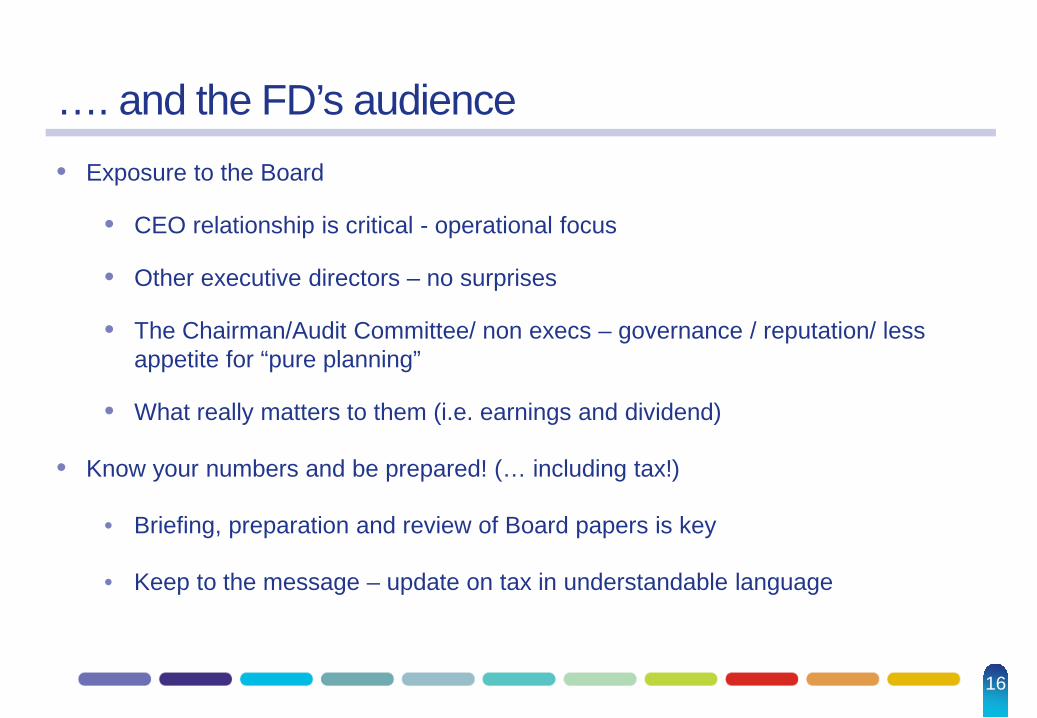

…. and the FD’s audience• Exposure to the Board

• CEO relationship is critical - operational focus

• Other executive directors – no surprises

• The Chairman/Audit Committee/ non execs – governance / reputation/ less appetite for “pure planning”

• What really matters to them (i.e. earnings and dividend)

• Know your numbers and be prepared! (… including tax!)

• Briefing, preparation and review of Board papers is key

• Keep to the message – update on tax in understandable language

17

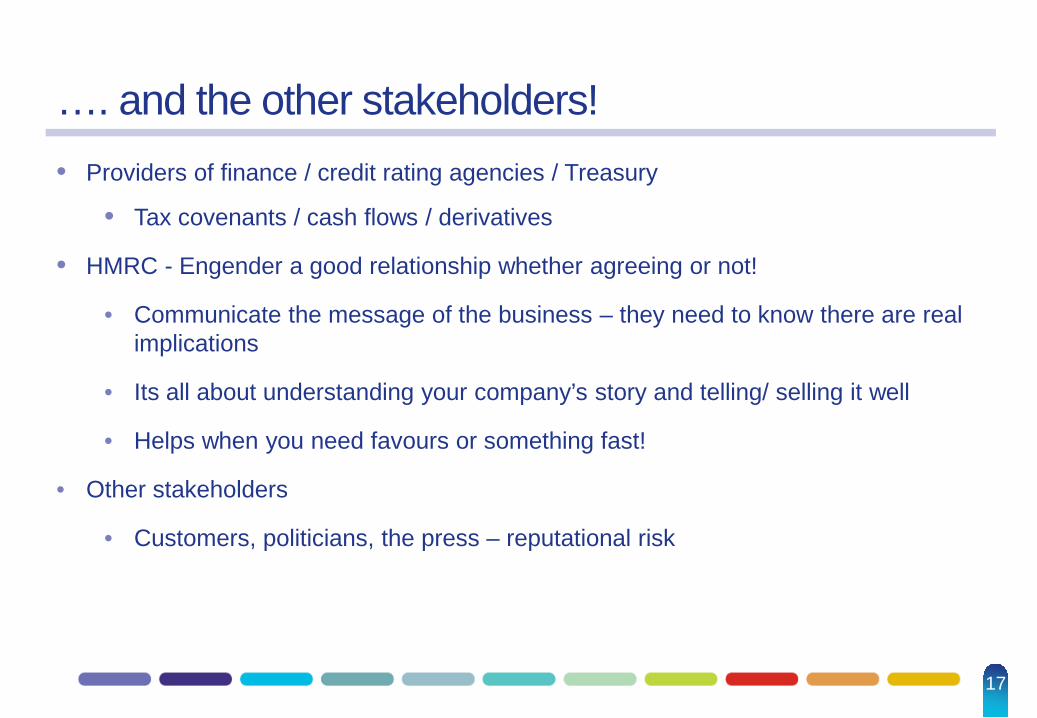

…. and the other stakeholders!• Providers of finance / credit rating agencies / Treasury

• Tax covenants / cash flows / derivatives

• HMRC - Engender a good relationship whether agreeing or not!

• Communicate the message of the business – they need to know there are real implications

• Its all about understanding your company’s story and telling/ selling it well

• Helps when you need favours or something fast!

• Other stakeholders

• Customers, politicians, the press – reputational risk

18

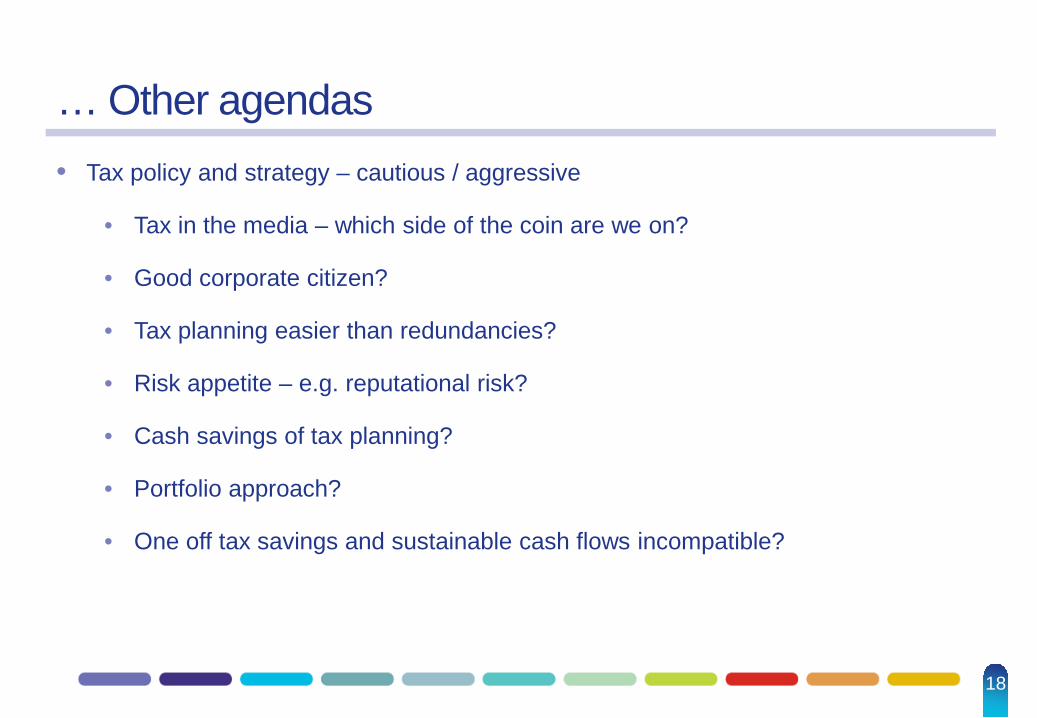

… Other agendas• Tax policy and strategy – cautious / aggressive

• Tax in the media – which side of the coin are we on?

• Good corporate citizen?

• Tax planning easier than redundancies?

• Risk appetite – e.g. reputational risk?

• Cash savings of tax planning?

• Portfolio approach?

• One off tax savings and sustainable cash flows incompatible?

19

Threats to sustainable cash tax / rate In a no surprises environment!

• Capital allowances – accounting depreciation

• Interest deductibility / Profits base – BEPS

• Diverted Profits Tax

• Windfall profits tax

The best of forecasts and project evaluation can have a hole blown through it!!!

Applies for projects, quoted companies and private equity alike !

– there are no exceptions

20

What do I want of my Tax team• The Tax team

• Selection is key, learn to remove blockers and then trust the team / recruitment

• Communicate with the business

• Managing throughout the game…not at final score!

• Good news and bad news in advance

• Maintain networks in and out of the company (and after you’ve left!)

• Utilities and other groups

• Political influence CBI / HMRC

21

My team…. what skills are important!• Overseas ownership

• Planning / M&A / International

• Close to the Business/ trusted reporting

• Professional teams / up to date / well informed – a given!

• Non-technical : Influencing and facilitation

• Doing the thinking… but in the business context

• Contingency – what could go wrong

• Regulated utility

• Lobbying for long term investment climate e.g. Capital allowances

• Mindful of regulatory tax allowance – it can be quite different and hypothetical

22

Focus of my Tax team • Getting it right!

• Enhance and optimise all legitimate claims

• Good relationships with auditors / advisers – well informed procurer / value for money

• Post IFRS / FRS102 less on effective tax rate – understand differences and cash tax

• Explain changes in tax rate / depreciation and effect on current /deferred tax

• Changes in GAAP can be key – accounts based tax deductions

• Understand tax profile / attributes – losses / other assets

23

What I want of my Tax team -credibility & the power to influence • Prove you can deliver on big projects

• Take the opportunities presented

• M&A projects/ transitional services

• MBWA

• Get out to the business

• Open door – don’t know the issue until your hear it!

24

Questions?• Tax as communicators / coaches?

• Amazon / Starbucks?

• Tax as decision makers?

• Monsanto?

• Non-tax skills required?

• The next Budget?

Interest deductibility in a BEPS world – Waiting

for certainty

Margaret Stephens

Partner, KPMG

Global Head of Infrastructure Tax

26© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty

‘To date, the UK has had a good policy around interest deductibility. Will this be changed going forward given OECD’s work on BEPS Action 4?’

Question to Fergus Harradence, HM Treasury, from Sovereign Wealth, Government and Public Pension Funds in June 2015

27© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

■ Arm’s length test on amount and pricing of debt■ Advance clearance■ Group relief rules enable Investor’s acquisition debt to shelter

future taxable profits■ No withholding tax on interest payments to UK corporate, EU

investors and on Quoted Eurobonds■ World Wide Debt Cap restriction allows UK deductions up to

‘whole’ consolidated debt (not just UK allocation) and 75% threshold

28© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

In addition■ Anti-avoidance rule on ‘Unallowable Purpose’ not generally

applied to debt funding of returns to shareholders■ HMRC guidance for tax inspectors on PFI funding in the

International Manual 2005■ Robust HM Treasury, public defence of the above as ‘a policy’ for

attracting investment to UK

29© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

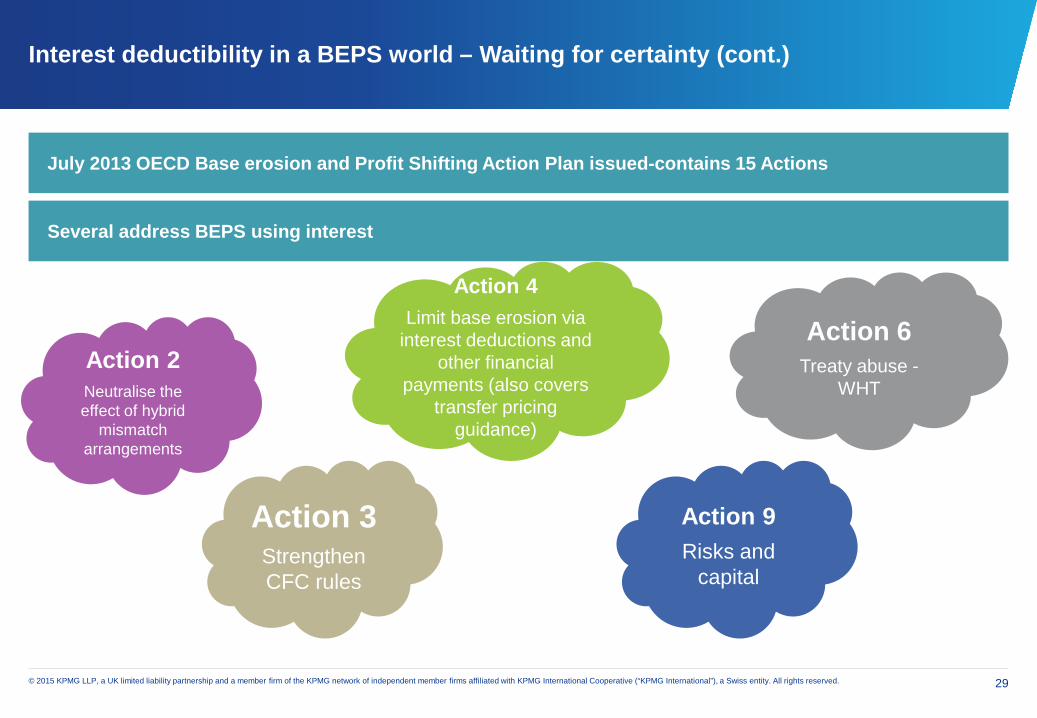

July 2013 OECD Base erosion and Profit Shifting Action Plan issued-contains 15 Actions

Action 2Neutralise the effect of hybrid

mismatch arrangements

Action 4Limit base erosion via

interest deductions and other financial

payments (also covers transfer pricing

guidance)

Action 3Strengthen CFC rules

Action 9Risks and

capital

Several address BEPS using interest

Action 6Treaty abuse -

WHT

30© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

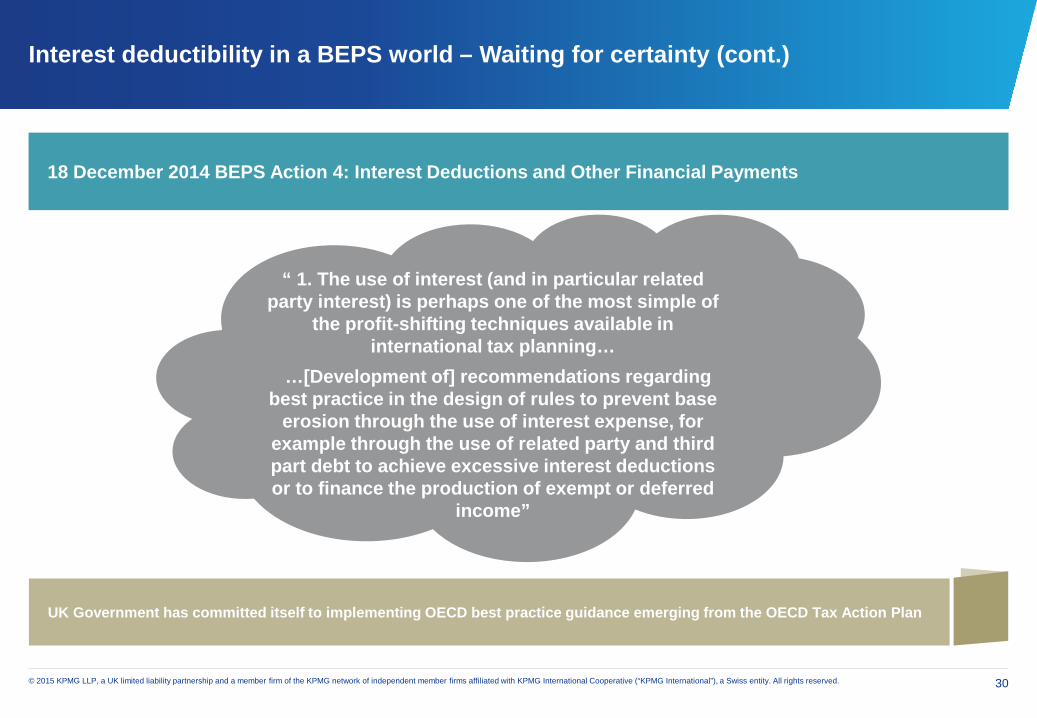

18 December 2014 BEPS Action 4: Interest Deductions and Other Financial Payments

“ 1. The use of interest (and in particular related party interest) is perhaps one of the most simple of

the profit-shifting techniques available in international tax planning…

…[Development of] recommendations regarding best practice in the design of rules to prevent base

erosion through the use of interest expense, for example through the use of related party and third part debt to achieve excessive interest deductions or to finance the production of exempt or deferred

income”

UK Government has committed itself to implementing OECD best practice guidance emerging from the OECD Tax Action Plan

31© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

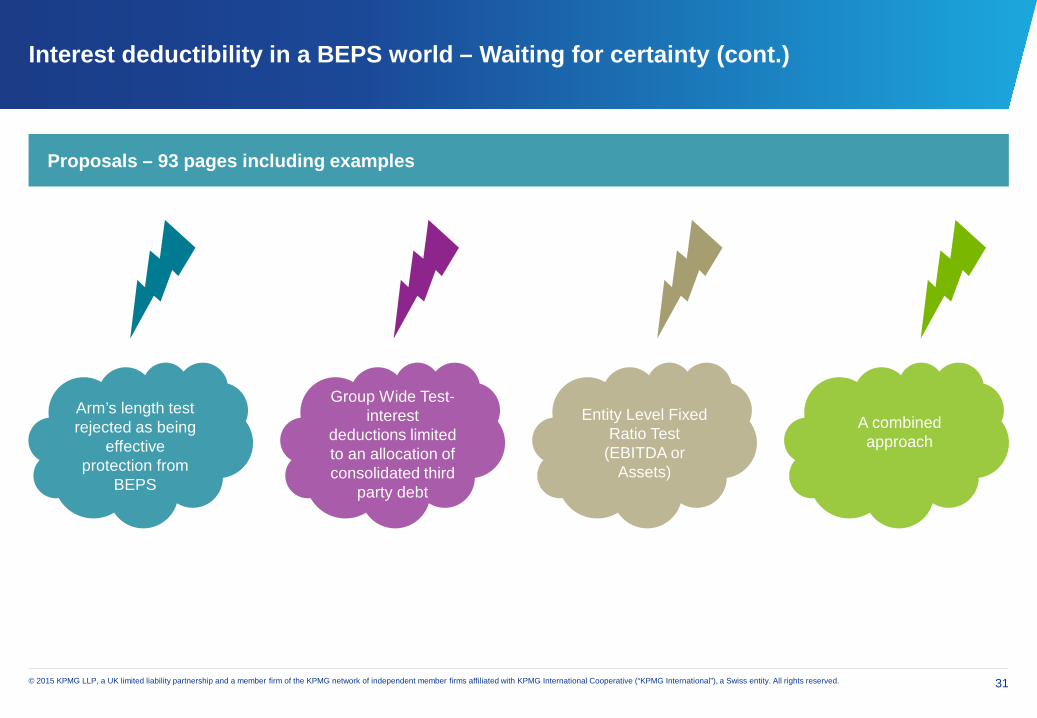

Proposals – 93 pages including examples

Arm’s length test rejected as being

effective protection from

BEPS

Group Wide Test-interest

deductions limited to an allocation of consolidated third

party debt

Entity Level Fixed Ratio Test

(EBITDA or Assets)

A combined approach

32© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

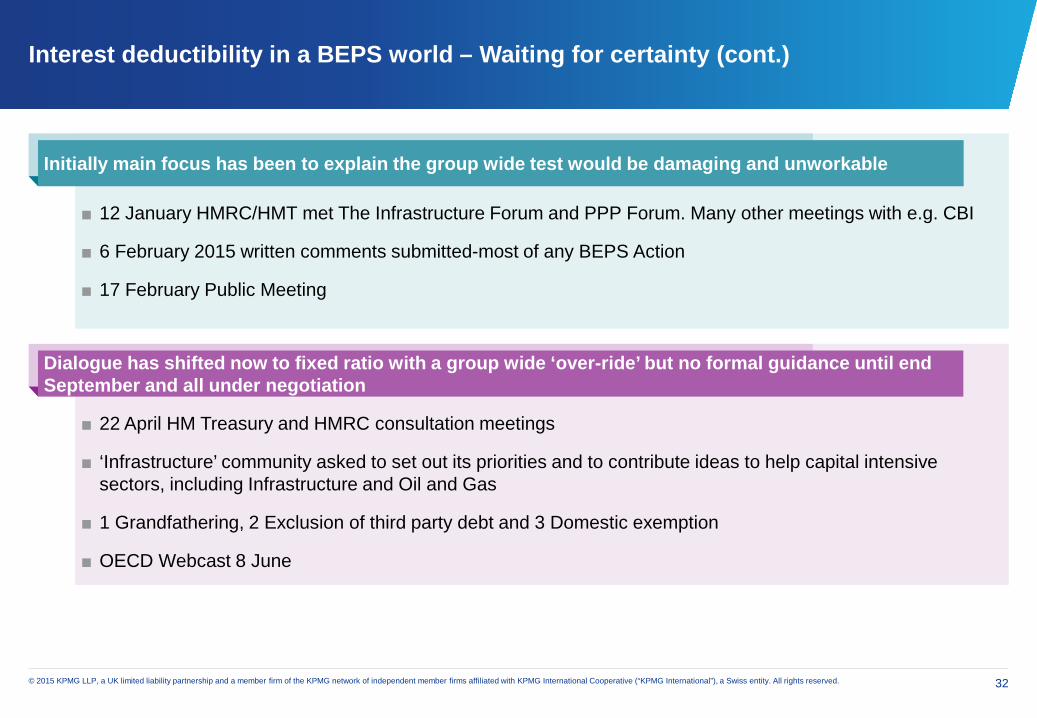

■ 12 January HMRC/HMT met The Infrastructure Forum and PPP Forum. Many other meetings with e.g. CBI

■ 6 February 2015 written comments submitted-most of any BEPS Action

■ 17 February Public Meeting

Initially main focus has been to explain the group wide test would be damaging and unworkable

■ 22 April HM Treasury and HMRC consultation meetings

■ ‘Infrastructure’ community asked to set out its priorities and to contribute ideas to help capital intensive sectors, including Infrastructure and Oil and Gas

■ 1 Grandfathering, 2 Exclusion of third party debt and 3 Domestic exemption

■ OECD Webcast 8 June

Dialogue has shifted now to fixed ratio with a group wide ‘over-ride’ but no formal guidance until end September and all under negotiation

33© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

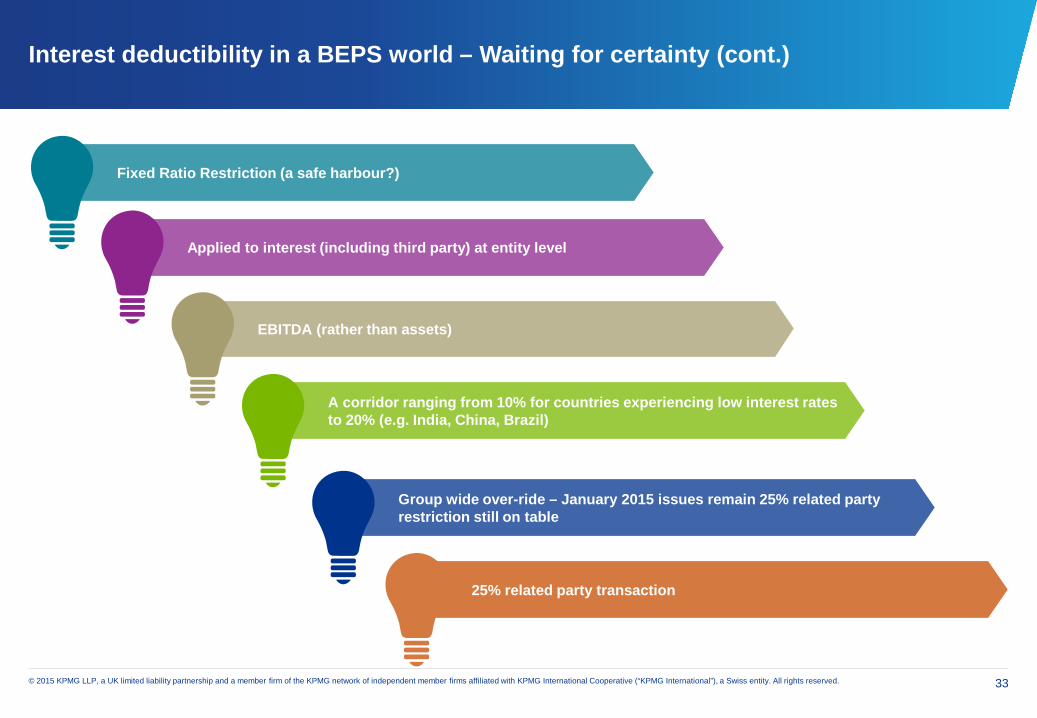

Fixed Ratio Restriction (a safe harbour?)

Applied to interest (including third party) at entity level

EBITDA (rather than assets)

A corridor ranging from 10% for countries experiencing low interest rates to 20% (e.g. India, China, Brazil)

Group wide over-ride – January 2015 issues remain 25% related party restriction still on table

25% related party transaction

34© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

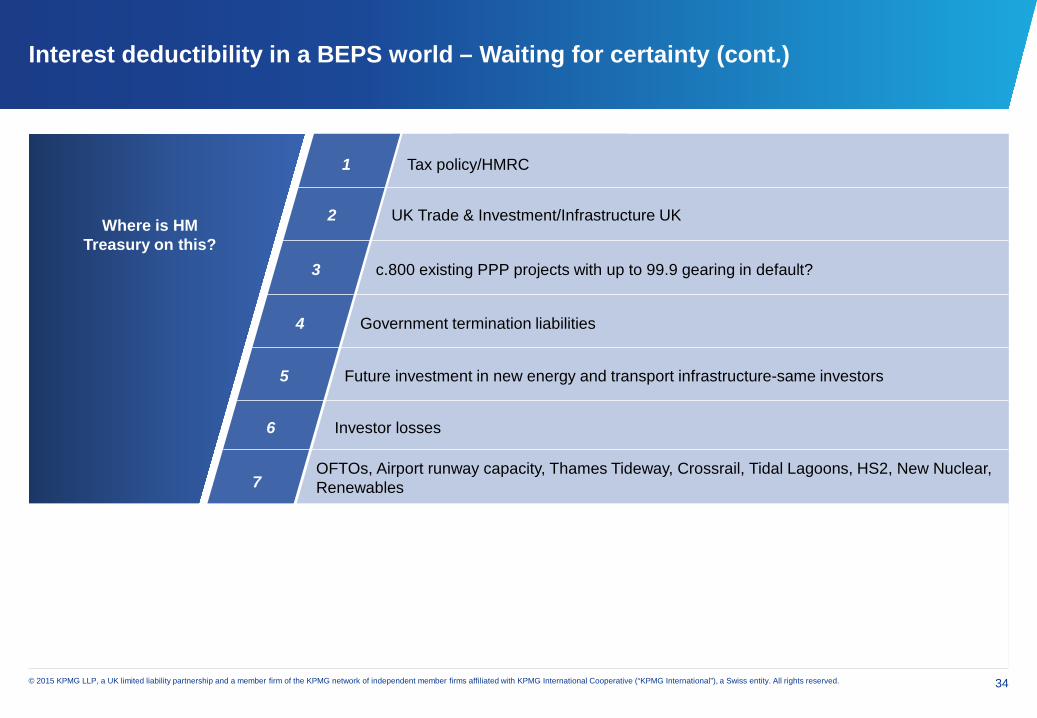

Where is HM Treasury on this?

Tax policy/HMRC

UK Trade & Investment/Infrastructure UK

c.800 existing PPP projects with up to 99.9 gearing in default?

Government termination liabilities

Future investment in new energy and transport infrastructure-same investors

1

10

2

3

4

5

6

7

8

9

Investor losses

OFTOs, Airport runway capacity, Thames Tideway, Crossrail, Tidal Lagoons, HS2, New Nuclear, Renewables

35© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

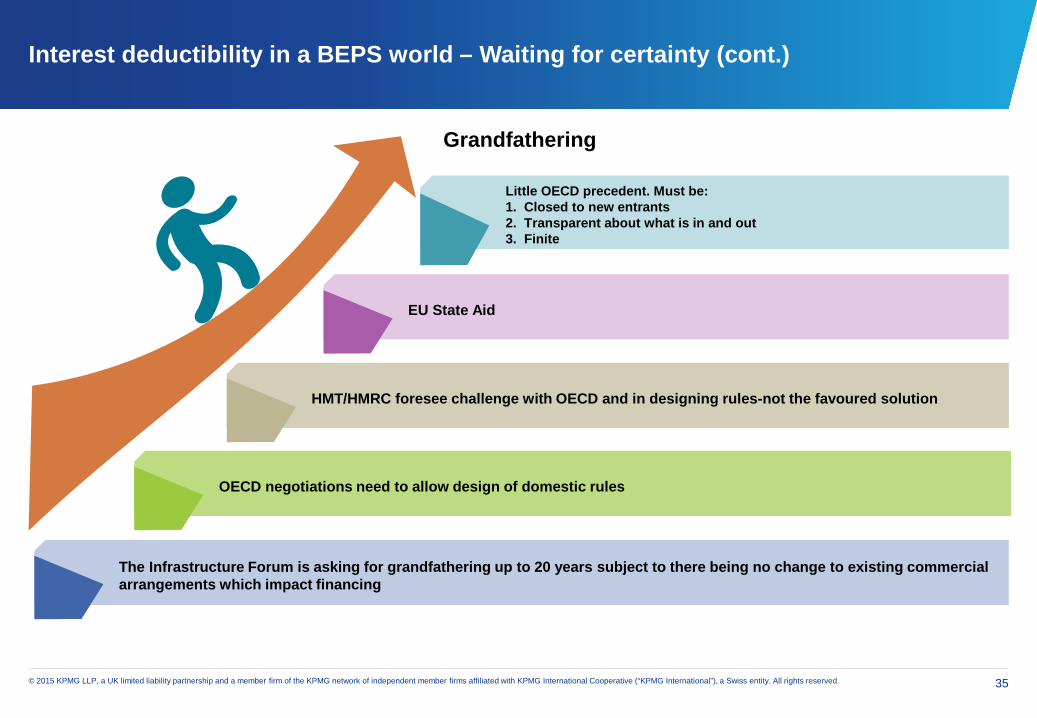

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

Little OECD precedent. Must be:1. Closed to new entrants2. Transparent about what is in and out3. Finite

EU State Aid

HMT/HMRC foresee challenge with OECD and in designing rules-not the favoured solution

OECD negotiations need to allow design of domestic rules

The Infrastructure Forum is asking for grandfathering up to 20 years subject to there being no change to existing commercial arrangements which impact financing

Grandfathering

36© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

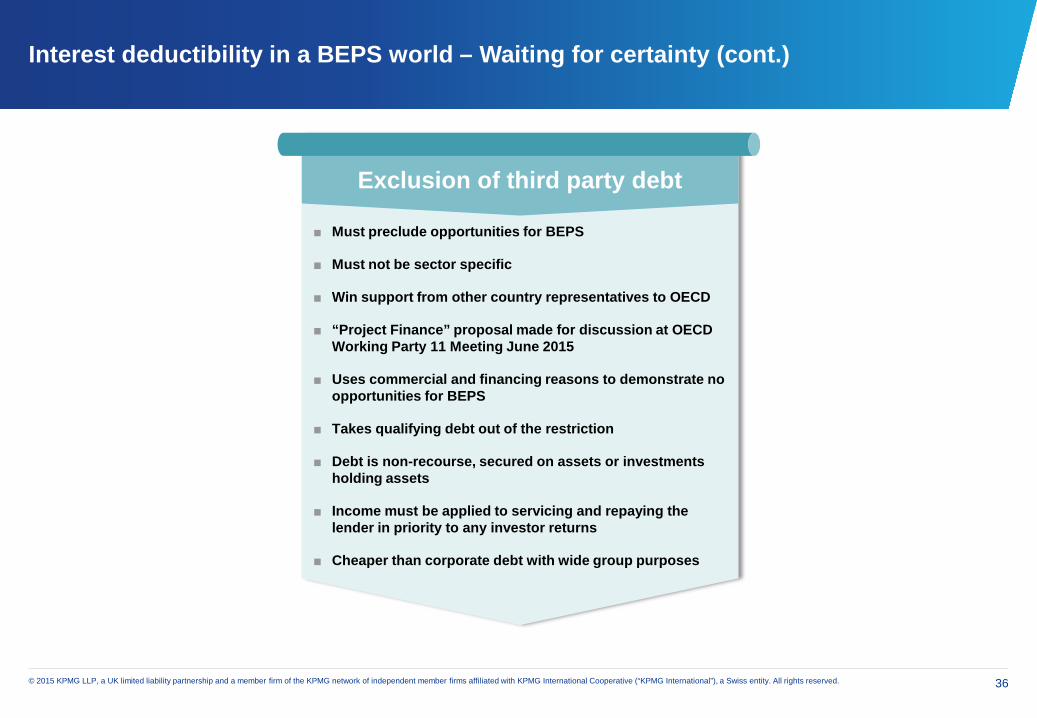

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

Exclusion of third party debt

■ Must preclude opportunities for BEPS

■ Must not be sector specific

■ Win support from other country representatives to OECD

■ “Project Finance” proposal made for discussion at OECD Working Party 11 Meeting June 2015

■ Uses commercial and financing reasons to demonstrate no opportunities for BEPS

■ Takes qualifying debt out of the restriction

■ Debt is non-recourse, secured on assets or investments holding assets

■ Income must be applied to servicing and repaying the lender in priority to any investor returns

■ Cheaper than corporate debt with wide group purposes

37© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

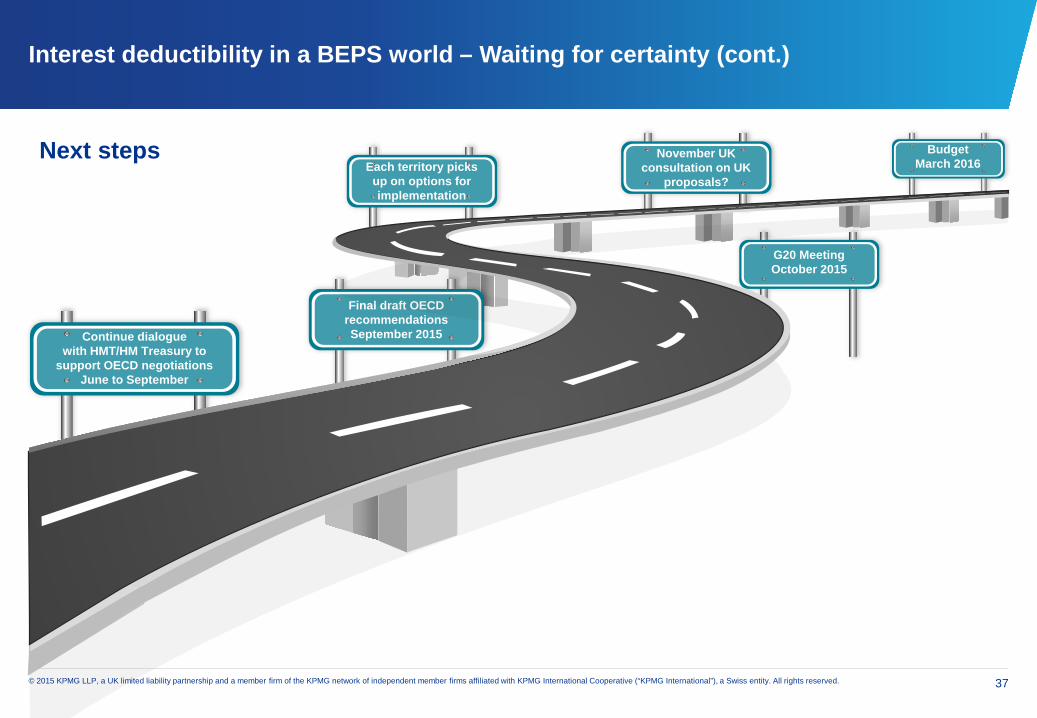

November UK consultation on UK

proposals?

G20 MeetingOctober 2015

Each territory picks up on options for implementation

Final draft OECD recommendations September 2015

Interest deductibility in a BEPS world – Waiting for certainty (cont.)

Budget March 2016

Continue dialoguewith HMT/HM Treasury to

support OECD negotiations June to September

Next steps

Diverted Profits Tax – is the elephant in the room

well enough defined?

Tim Sarson

KPMG Partner, Tax Effective Value Chain

Defining the Target

40© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Where is the Elephant: 1

UK IP exits where nobody moves

41© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Why was DPT introduced?

Context■ Publicity about U.S. multinationals who have many millions

of sales to U.K. customers but pay very little U.K. tax.■ BEPS and additional political angle due to General Elections

that were held on 7 May 2015.

Overview■ Aimed at multinationals either:

– Exploiting weakness in current PE legislation so profits are booked in low tax jurisdictions, and/or

– Reducing U.K. profits via excessive payments / aggressive transfer pricing

42© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

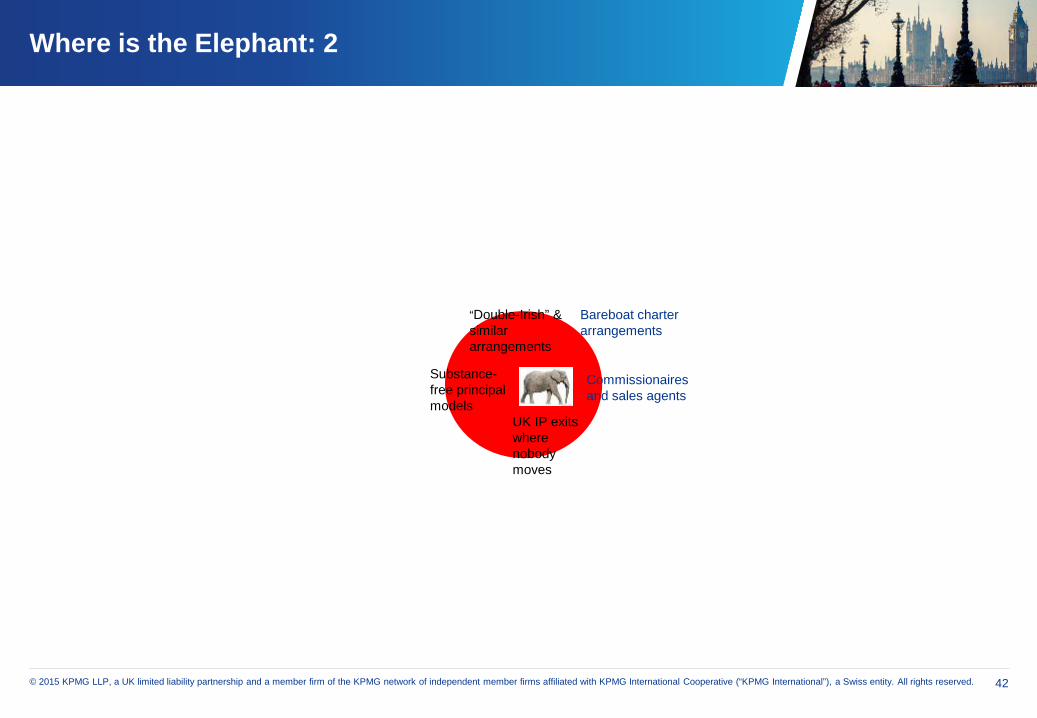

Where is the Elephant: 2

“Double-Irish” & similar arrangements

Substance-free principal models

Commissionaires and sales agents

UK IP exits where nobody moves

Bareboat charter arrangements

The Rules

44© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Companies avoiding a UK taxable presence (s.86)

Key features

■ Charge applies to non-UK companies where there is a “tax mismatch” (essentially 80% of UK ETR)

■ Potentially applicable to any “UK activity” in connection with sales of goods, services or other property worth more than £10m, regardless of where the customer is

■ Legislation tests whether there is a person, the “avoided PE”, carrying on activity in the UK in connection with supplies made by the foreign company.

■ Applies where “it is reasonable to assume that any of the activity of the avoided PE or the foreign company or both is designed so as to ensure that the foreign company does not, as a result of the avoided PE’s activity, carry on that trade in the UK for the purposes of corporation tax…”.

■ Diverted profits are then computed as the profits which would have been attributable to the avoided PE if it had been a UK PE through which the foreign company carried on its trade. This is complicated if the foreign company itself has been engaging in BEPS activity e.g. royalty strips.

Quote from s86(1)(e) FB 2015.

45© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

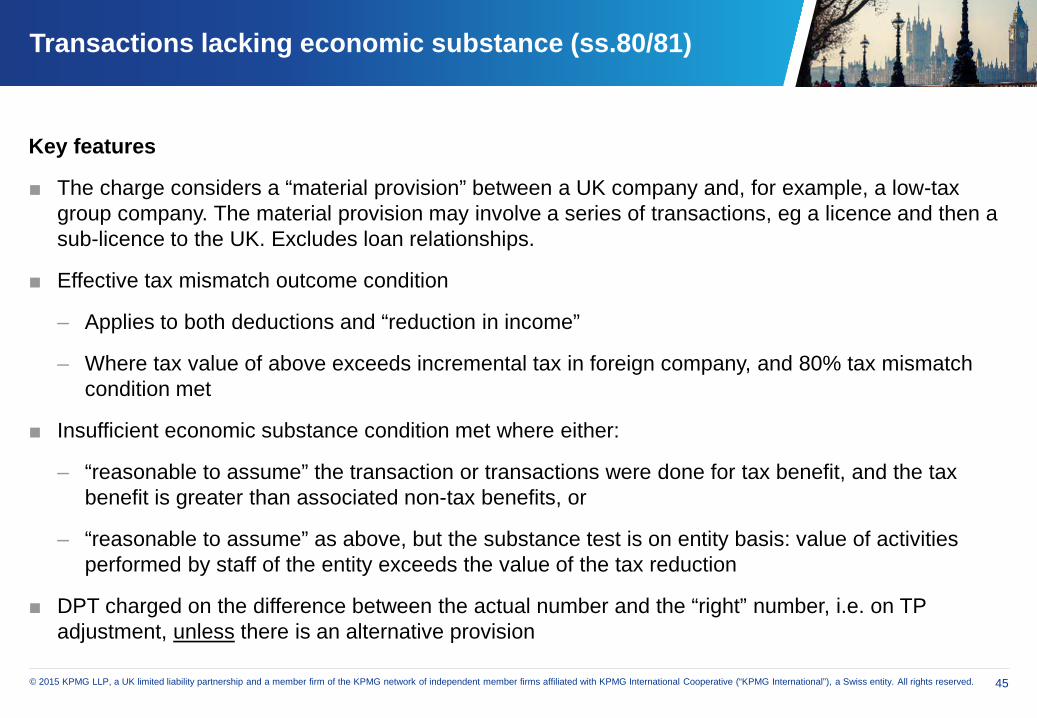

Transactions lacking economic substance (ss.80/81)

Key features

■ The charge considers a “material provision” between a UK company and, for example, a low-tax group company. The material provision may involve a series of transactions, eg a licence and then a sub-licence to the UK. Excludes loan relationships.

■ Effective tax mismatch outcome condition

– Applies to both deductions and “reduction in income”

– Where tax value of above exceeds incremental tax in foreign company, and 80% tax mismatch condition met

■ Insufficient economic substance condition met where either:

– “reasonable to assume” the transaction or transactions were done for tax benefit, and the tax benefit is greater than associated non-tax benefits, or

– “reasonable to assume” as above, but the substance test is on entity basis: value of activities performed by staff of the entity exceeds the value of the tax reduction

■ DPT charged on the difference between the actual number and the “right” number, i.e. on TP adjustment, unless there is an alternative provision

46© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

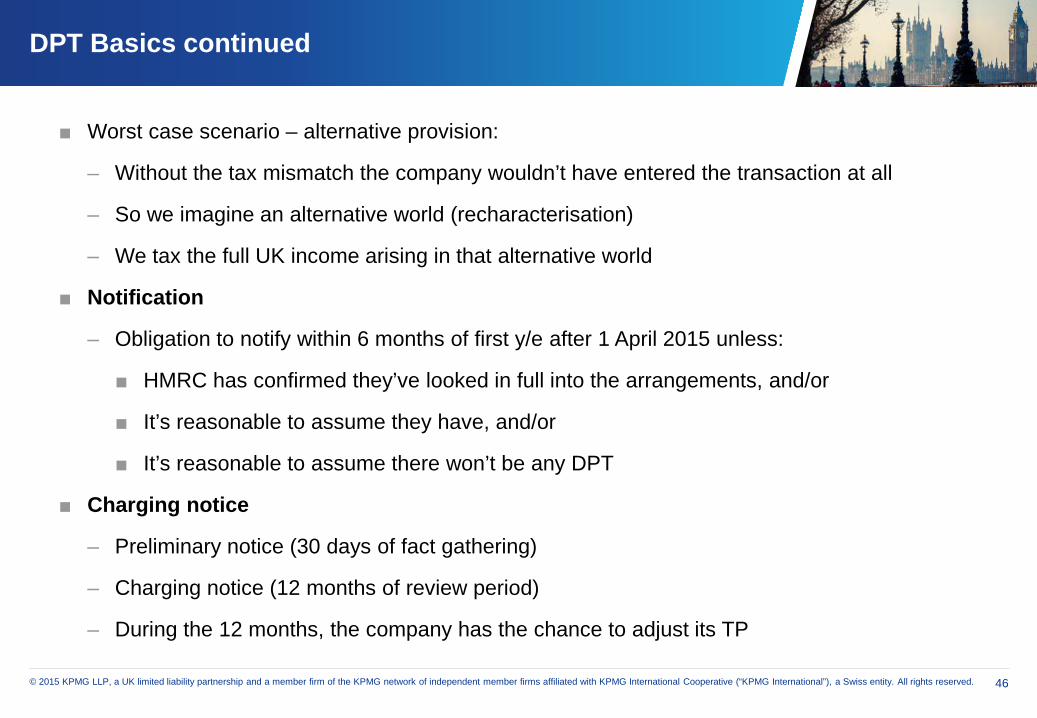

DPT Basics continued

■ Worst case scenario – alternative provision:

– Without the tax mismatch the company wouldn’t have entered the transaction at all

– So we imagine an alternative world (recharacterisation)

– We tax the full UK income arising in that alternative world

■ Notification

– Obligation to notify within 6 months of first y/e after 1 April 2015 unless:

■ HMRC has confirmed they’ve looked in full into the arrangements, and/or

■ It’s reasonable to assume they have, and/or

■ It’s reasonable to assume there won’t be any DPT

■ Charging notice

– Preliminary notice (30 days of fact gathering)

– Charging notice (12 months of review period)

– During the 12 months, the company has the chance to adjust its TP

Defining the target(Revisited)

48© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

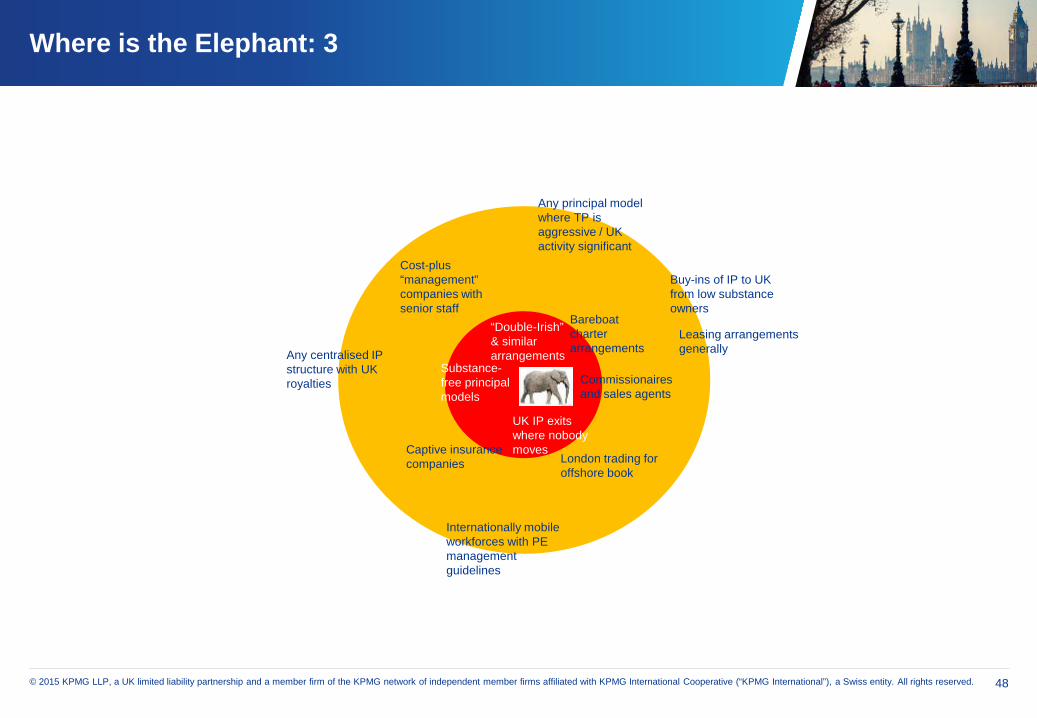

Where is the Elephant: 3

“Double-Irish” & similar arrangements

Substance-free principal models

Any principal model where TP is aggressive / UK activity significant

Commissionaires and sales agents

UK IP exits where nobody moves

Bareboat charter arrangements

Cost-plus “management” companies with senior staff

Captive insurance companies

Internationally mobile workforces with PE management guidelines

Any centralised IP structure with UK royalties

Buy-ins of IP to UK from low substance owners

Leasing arrangements generally

London trading for offshore book

49© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

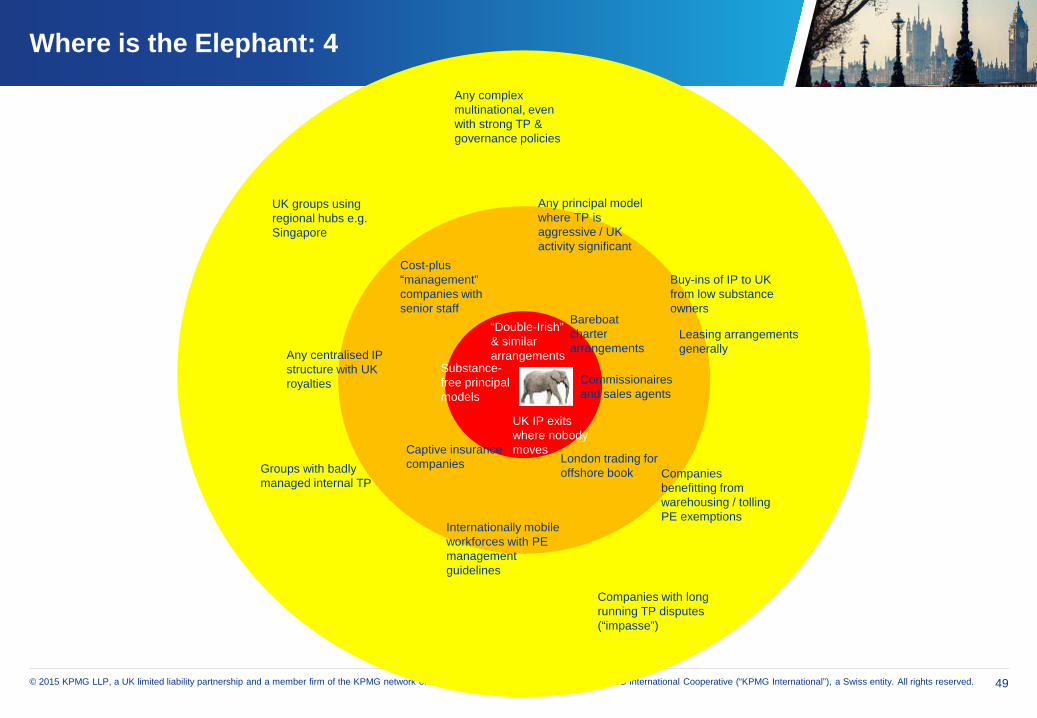

Where is the Elephant: 4

“Double-Irish” & similar arrangements

Substance-free principal models

Any principal model where TP is aggressive / UK activity significant

Commissionaires and sales agents

UK IP exits where nobody moves

Bareboat charter arrangements

Cost-plus “management” companies with senior staff

Captive insurance companies

Companies benefitting from warehousing / tolling PE exemptions

Internationally mobile workforces with PE management guidelines

Groups with badly managed internal TP

Any centralised IP structure with UK royalties

UK groups using regional hubs e.g. Singapore

Buy-ins of IP to UK from low substance owners

Companies with long running TP disputes (“impasse”)

Leasing arrangements generally

Any complex multinational, even with strong TP & governance policies

London trading for offshore book

50© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

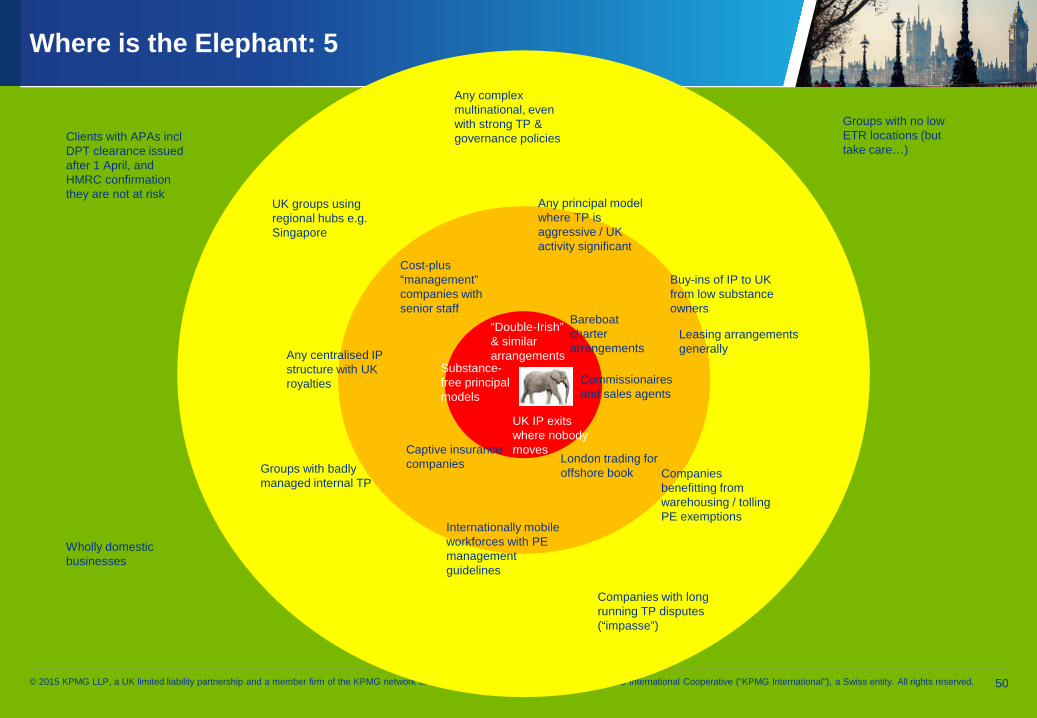

Where is the Elephant: 5

“Double-Irish” & similar arrangements

Substance-free principal models

Any principal model where TP is aggressive / UK activity significant

Commissionaires and sales agents

UK IP exits where nobody moves

Bareboat charter arrangements

Cost-plus “management” companies with senior staff

Captive insurance companies

Companies benefitting from warehousing / tolling PE exemptions

Internationally mobile workforces with PE management guidelines

Groups with badly managed internal TP

Any centralised IP structure with UK royalties

UK groups using regional hubs e.g. Singapore

Buy-ins of IP to UK from low substance owners

Companies with long running TP disputes (“impasse”)

Leasing arrangements generally

Any complex multinational, even with strong TP & governance policies

London trading for offshore book

Clients with APAs inclDPT clearance issued after 1 April, and HMRC confirmation they are not at risk

Wholly domestic businesses

Groups with no low ETR locations (but take care…)

51© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

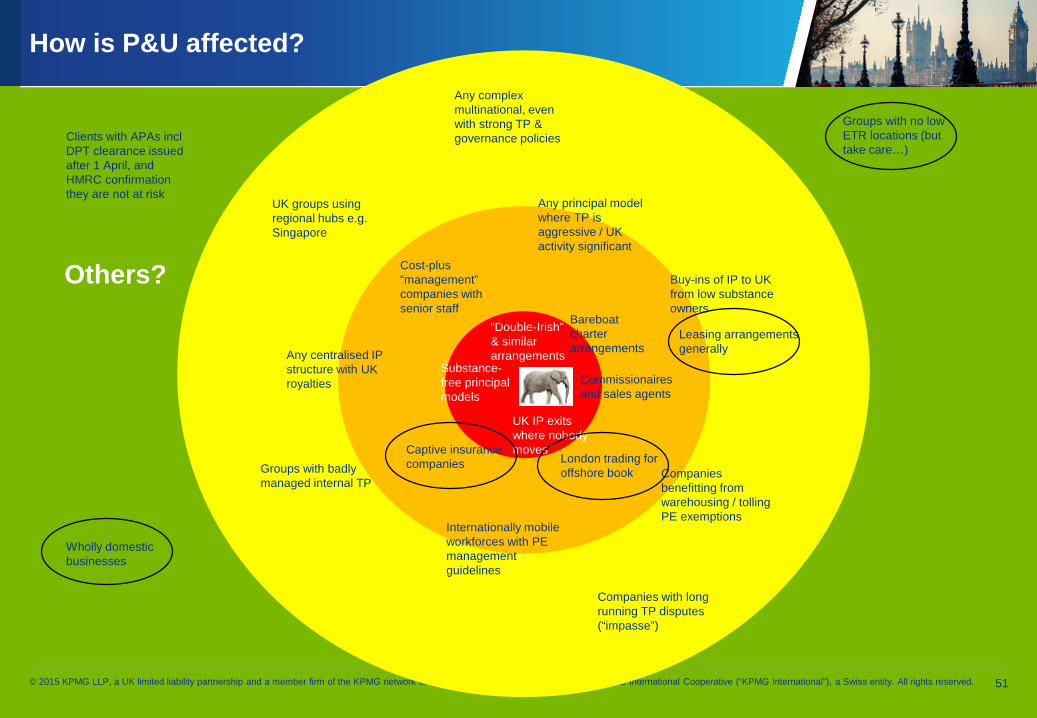

How is P&U affected?

“Double-Irish” & similar arrangements

Substance-free principal models

Any principal model where TP is aggressive / UK activity significant

Commissionaires and sales agents

UK IP exits where nobody moves

Bareboat charter arrangements

Cost-plus “management” companies with senior staff

Captive insurance companies

Companies benefitting from warehousing / tolling PE exemptions

Internationally mobile workforces with PE management guidelines

Groups with badly managed internal TP

Any centralised IP structure with UK royalties

UK groups using regional hubs e.g. Singapore

Buy-ins of IP to UK from low substance owners

Companies with long running TP disputes (“impasse”)

Clients with APAs inclDPT clearance issued after 1 April, and HMRC confirmation they are not at risk

Wholly domestic businesses

Groups with no low ETR locations (but take care…)

Leasing arrangements generally

Any complex multinational, even with strong TP & governance policies

London trading for offshore book

Others?

52© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

My TP is arm’s length. Surely there’s nothing to worry about?

In some circumstances this may not be enough:

■ Non-UK company with an “avoided PE” in the UK, where more profits could be attributed to a UK branch.

■ UK company making a payment or receiving income from a low-tax low-substance group company where there is a “relevant alternative provision”, ie HMRC can tax on the basis of a counterfactual position.

■ Possibly a situation where the TP method could be subject to challenge eg group uses a cost-plus method, HMRC are contending for a profit split basis.

■ Is your TP arm’s length as defined in BEPS actions 8-10?

We understand that HMRC have advised that they will be reviewing existing APAs to consider possible DPT angles.

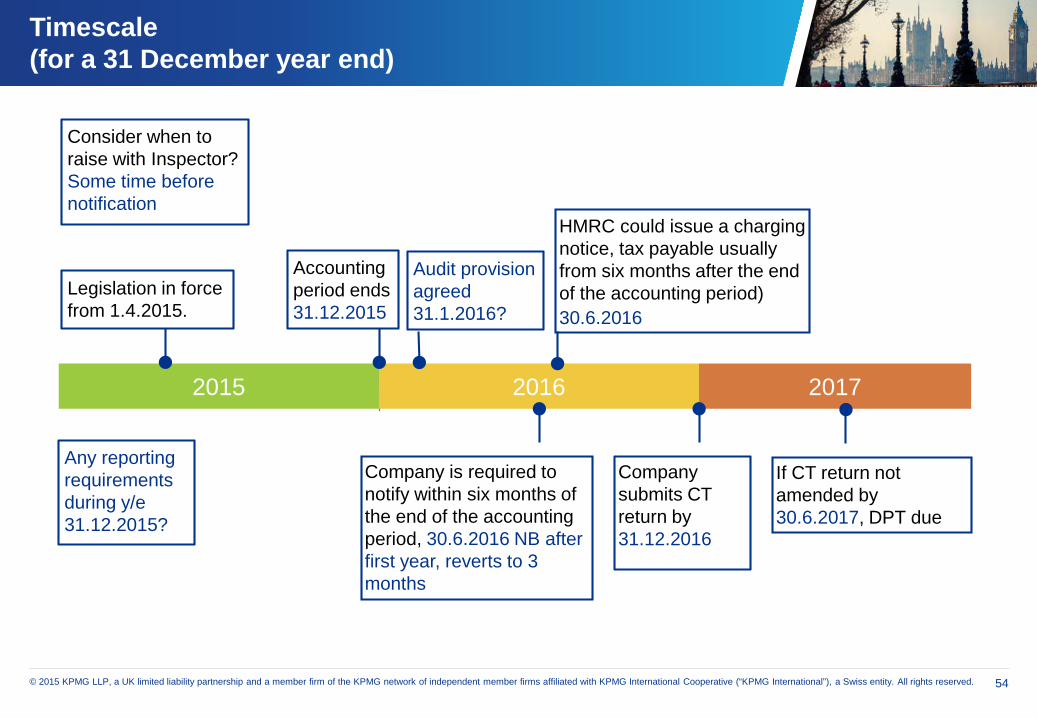

Compliance timetable

54© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Timescale(for a 31 December year end)

Company is required to notify within six months of the end of the accounting period, 30.6.2016 NB after first year, reverts to 3 months

HMRC could issue a charging notice, tax payable usually from six months after the end of the accounting period)30.6.2016

If CT return not amended by 30.6.2017, DPT due

Accounting period ends 31.12.2015

Company submits CT return by 31.12.2016

Legislation in force from 1.4.2015.

Any reporting requirements during y/e31.12.2015?

Audit provision agreed31.1.2016?

Consider when to raise with Inspector?Some time before notification

2015 2016 2017

55© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

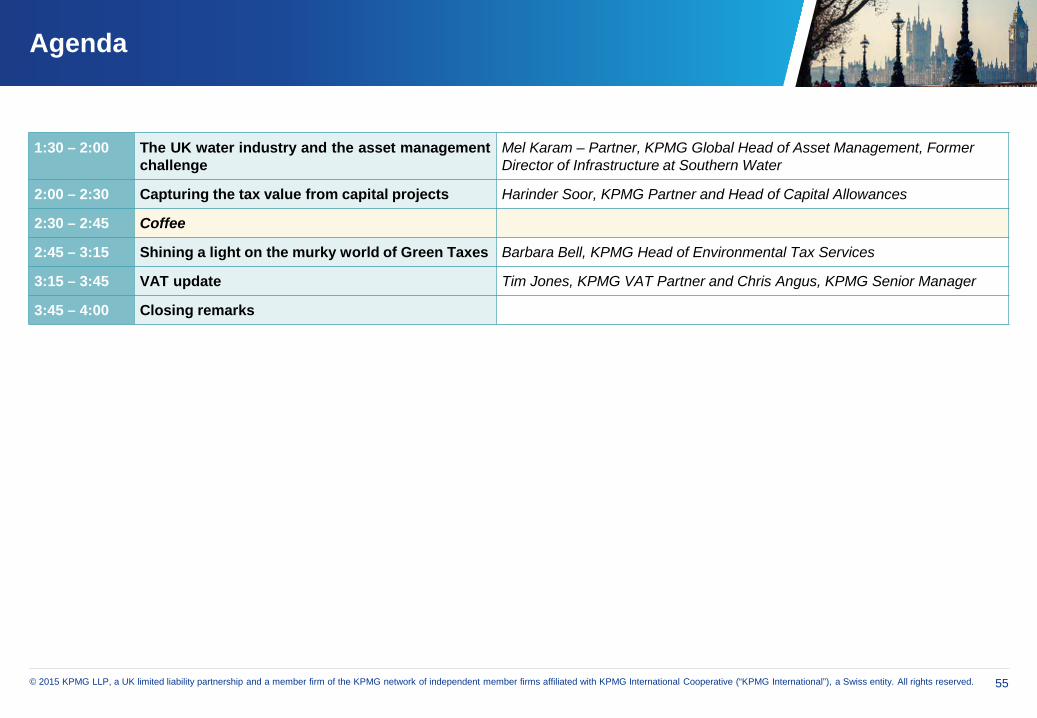

Agenda

1:30 – 2:00 The UK water industry and the asset managementchallenge

Mel Karam – Partner, KPMG Global Head of Asset Management, Former Director of Infrastructure at Southern Water

2:00 – 2:30 Capturing the tax value from capital projects Harinder Soor, KPMG Partner and Head of Capital Allowances

2:30 – 2:45 Coffee

2:45 – 3:15 Shining a light on the murky world of Green Taxes Barbara Bell, KPMG Head of Environmental Tax Services

3:15 – 3:45 VAT update Tim Jones, KPMG VAT Partner and Chris Angus, KPMG Senior Manager

3:45 – 4:00 Closing remarks

The UK water industry and the asset

management challenge

Mel Karam

Partner, KPMG Global Head of Asset Management

57© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

PR14 outcomes and challenges

Regulatory Reform

Wholesale Financial impact and challenges

Contents

58© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

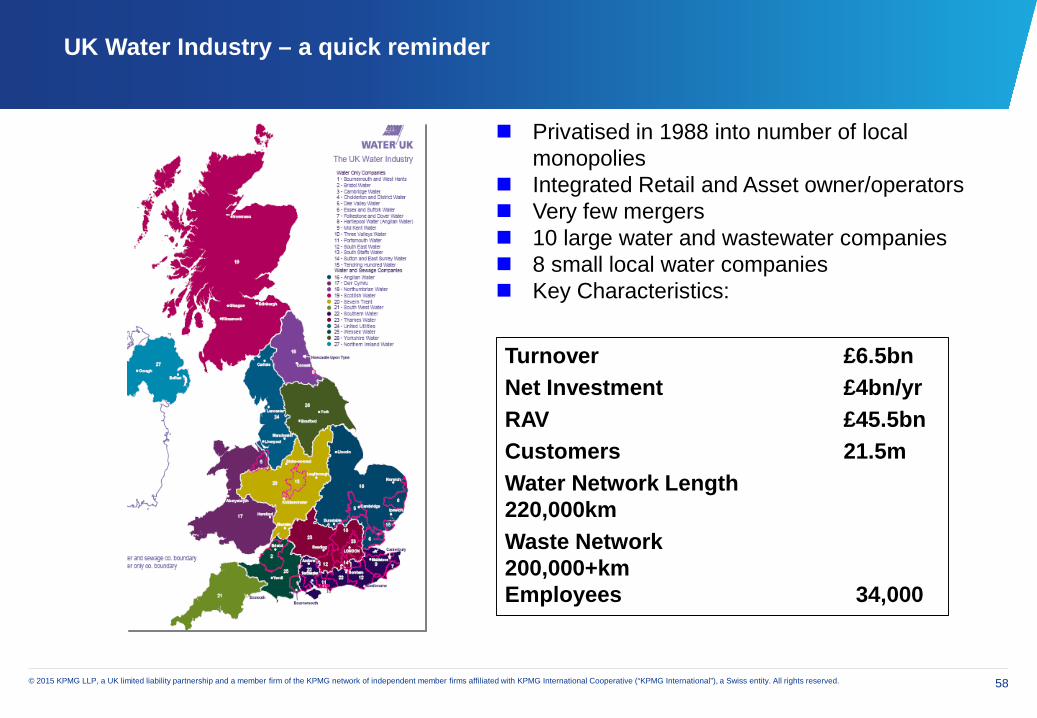

Privatised in 1988 into number of local monopolies

Integrated Retail and Asset owner/operators Very few mergers 10 large water and wastewater companies 8 small local water companies Key Characteristics:

Turnover £6.5bnNet Investment £4bn/yrRAV £45.5bnCustomers 21.5mWater Network Length220,000kmWaste Network200,000+kmEmployees 34,000

UK Water Industry – a quick reminder

PR14, Customer Engagement and future challenges

60© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

PR14 Summary

The Water sector 2015 – 2020 price control period has a different set of objectives: “Delivering Customer Outcomes” - which has necessitated a new perspective for the sector. Overall this price review is considered a success for the regulator, mostly down to the headlines of:

Prices downInvestment upService levels upCompetition starting

Introduction of Totex, as a new financial measure of total cost of operation and its efficiency, has created both an opportunity and a threat

Future structural changes for the industry are more a possibility than any time in the past. Including:

Retail (Non-household) separation (certain in 2017)Wholesale vertical unbundling, enabled by Water Act 2014 under “Upstream Reform”Horizontal mergers

61© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Two perspectives to the price review

Ofwat Perspective

Bills going down

Companies’ perspective

Revenues are at risk

Investment is going up Return on Equity is down

Service levels are improving There are no upsides to service improvements

Improve efficiency, Look for alternative revenue streams

Look for efficiencies

Deliver service levels, and no more

Potential response

Better balanced in favour of customers

Less favourable to shareholders

Find alternative SHV proposition, growth outside

regulation

Competition introduced RAV is at riskFind alternative SHV

proposition, growth outside regulation

62© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

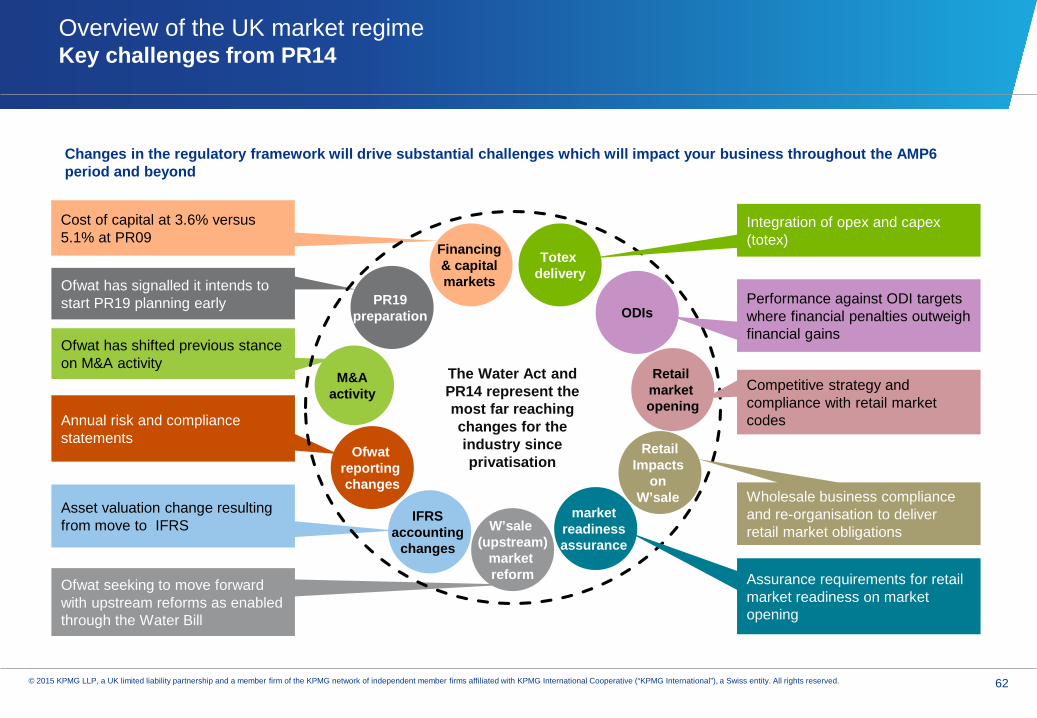

Overview of the UK market regimeKey challenges from PR14

Annual risk and compliance statements

Asset valuation change resulting from move to IFRS

Cost of capital at 3.6% versus 5.1% at PR09

Ofwat has signalled it intends to start PR19 planning early

Ofwat has shifted previous stance on M&A activity

Ofwat seeking to move forward with upstream reforms as enabled through the Water Bill

Retail market opening

RetailImpacts

on W’sale

market readiness assurance

IFRS accounting

changes

Ofwatreporting changes

Totexdelivery

Financing & capital markets

Competitive strategy and compliance with retail market codes

Assurance requirements for retail market readiness on market opening

Wholesale business compliance and re-organisation to deliver retail market obligations

Integration of opex and capex (totex)

PR19 preparation ODIs

M&A activity

W’sale(upstream)

market reform

Performance against ODI targets where financial penalties outweigh financial gains

The Water Act and PR14 represent the most far reaching changes for the industry since privatisation

Changes in the regulatory framework will drive substantial challenges which will impact your business throughout the AMP6 period and beyond

63© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

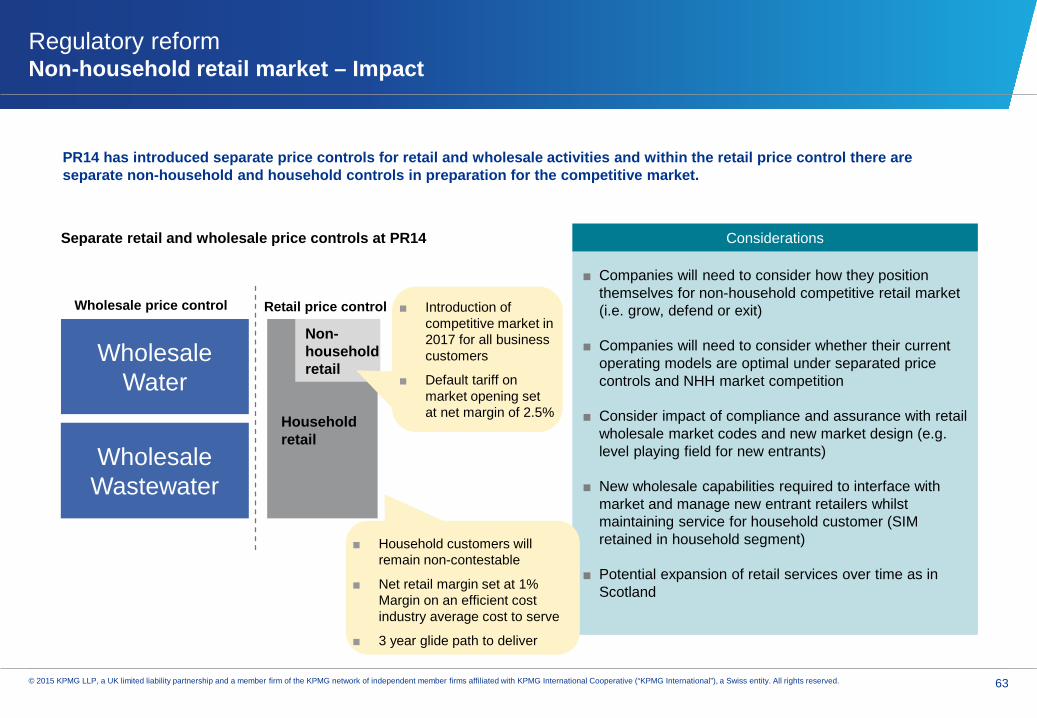

Regulatory reform Non-household retail market – Impact

■ Companies will need to consider how they position themselves for non-household competitive retail market (i.e. grow, defend or exit)

■ Companies will need to consider whether their current operating models are optimal under separated price controls and NHH market competition

■ Consider impact of compliance and assurance with retail wholesale market codes and new market design (e.g. level playing field for new entrants)

■ New wholesale capabilities required to interface with market and manage new entrant retailers whilst maintaining service for household customer (SIM retained in household segment)

■ Potential expansion of retail services over time as in Scotland

Considerations

PR14 has introduced separate price controls for retail and wholesale activities and within the retail price control there areseparate non-household and household controls in preparation for the competitive market.

Wholesale Water

Non-household retail

Household retail

■ Introduction of competitive market in 2017 for all business customers

■ Default tariff on market opening set at net margin of 2.5%

■ Household customers will remain non-contestable

■ Net retail margin set at 1% Margin on an efficient cost industry average cost to serve

■ 3 year glide path to deliver

Wholesale price control Retail price control

Separate retail and wholesale price controls at PR14

Wholesale Wastewater

64© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

2015-2020 Price Review: A new customer-centric process?

Genuine, extensive and rigorous customer and stakeholder engagement to understand customers’priorities. Final Business Plans were, on the whole, based on insight from customer engagements.

Final Determination was a substantial change from past regulatory cycles. Most notably in WACC, move from “output” regulation to “customer Outcomes” (reduced level of intrusion by the regulator) and introduction of Totex.

Delivery plans generally aim to outperform the regulatory settlement, despite the claims of “tough” outcomes for companies.

65© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 65

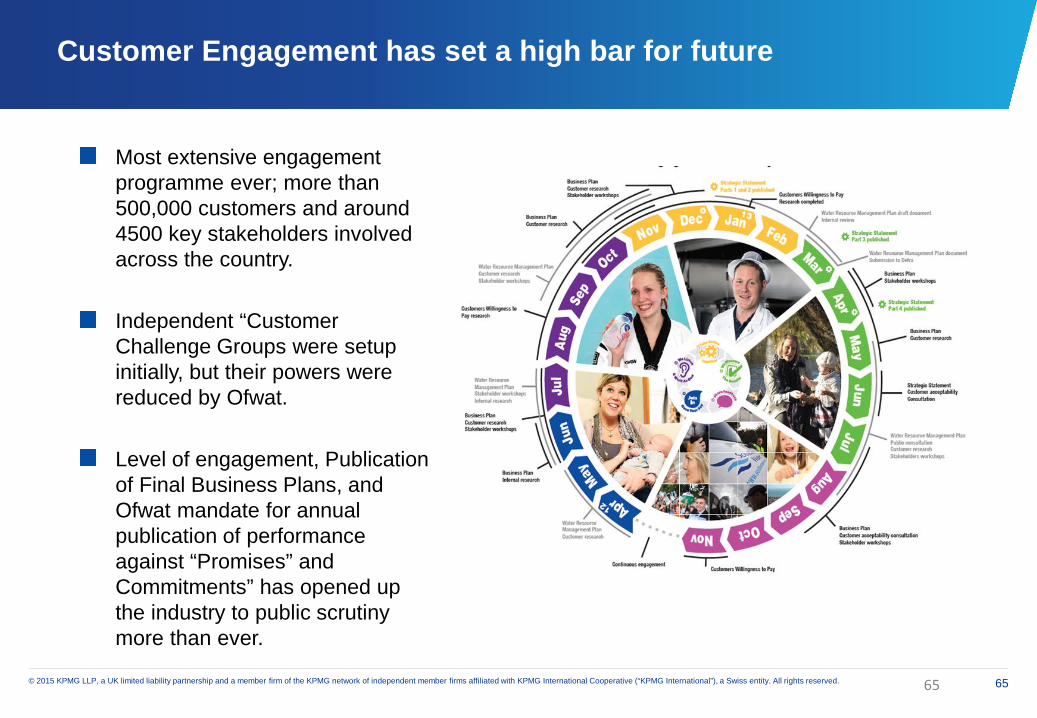

Customer Engagement has set a high bar for future

Most extensive engagement programme ever; more than 500,000 customers and around 4500 key stakeholders involved across the country.

Independent “Customer Challenge Groups were setup initially, but their powers were reduced by Ofwat.

Level of engagement, Publication of Final Business Plans, and Ofwat mandate for annual publication of performance against “Promises” and Commitments” has opened up the industry to public scrutiny more than ever.

66© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

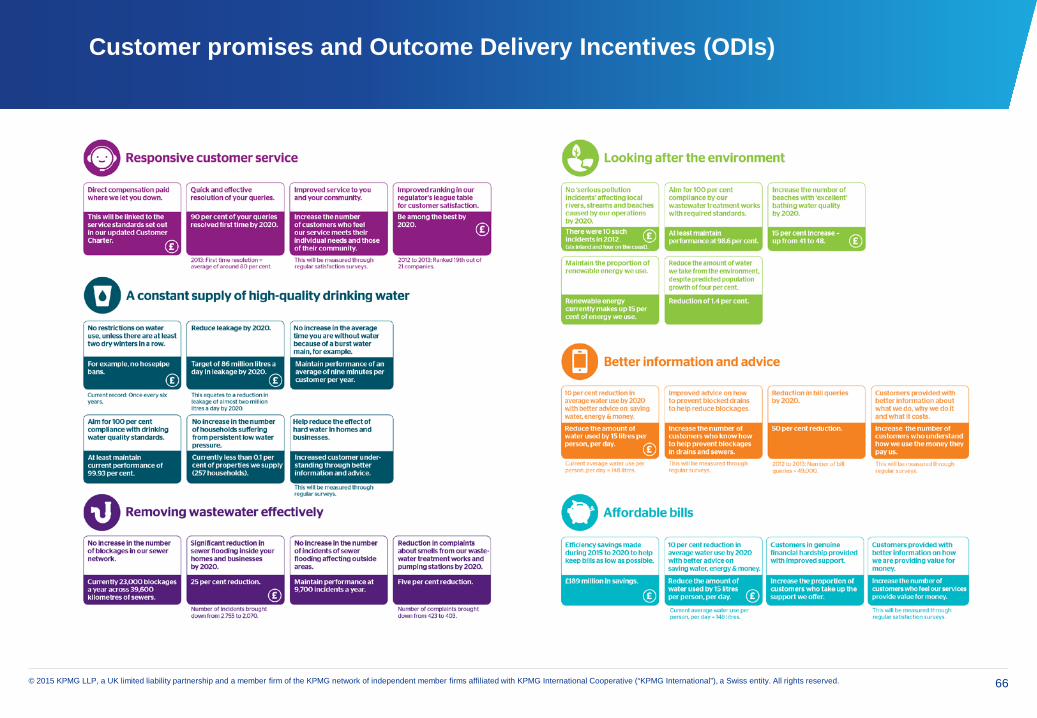

Customer promises and Outcome Delivery Incentives (ODIs)

Regulatory Reform

68© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

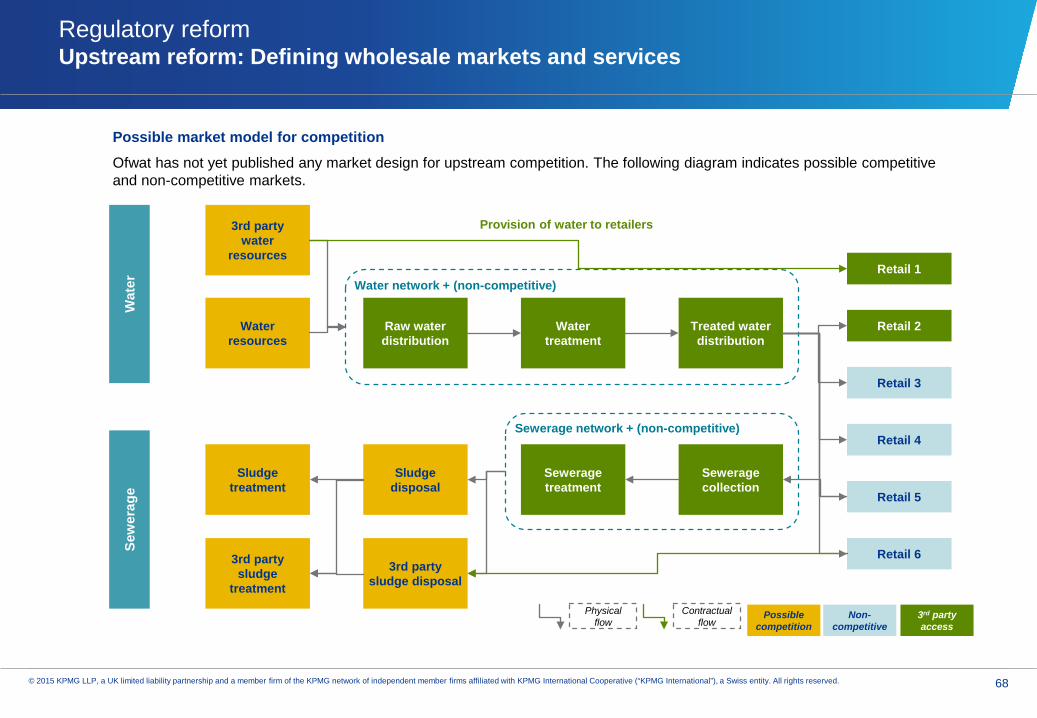

Possible market model for competition

Ofwat has not yet published any market design for upstream competition. The following diagram indicates possible competitive and non-competitive markets.

Waterresources

Raw water distribution

Watertreatment

Treated water distribution

Sewerage treatment

Sewerage collection

Sludge treatment

Sludgedisposal

Wat

erSe

wer

age

Water network + (non-competitive)

Sewerage network + (non-competitive)

3rd partywater

resourcesRetail 1

Retail 2

Retail 3

Retail 4

Retail 5

Retail 63rd partysludge

treatment

3rd partysludge disposal

Possible competition

Non-competitive

3rd party access

Provision of water to retailers

Physical flow

Contractual flow

Regulatory reformUpstream reform: Defining wholesale markets and services

Wholesale Challenges

70© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

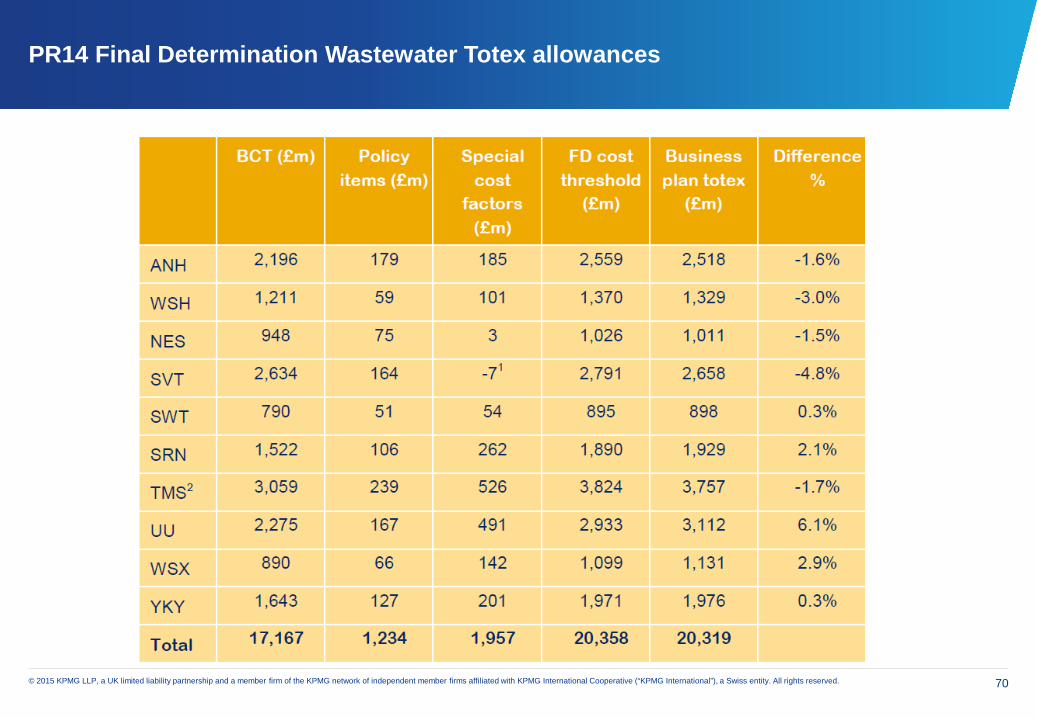

PR14 Final Determination Wastewater Totex allowances

71© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

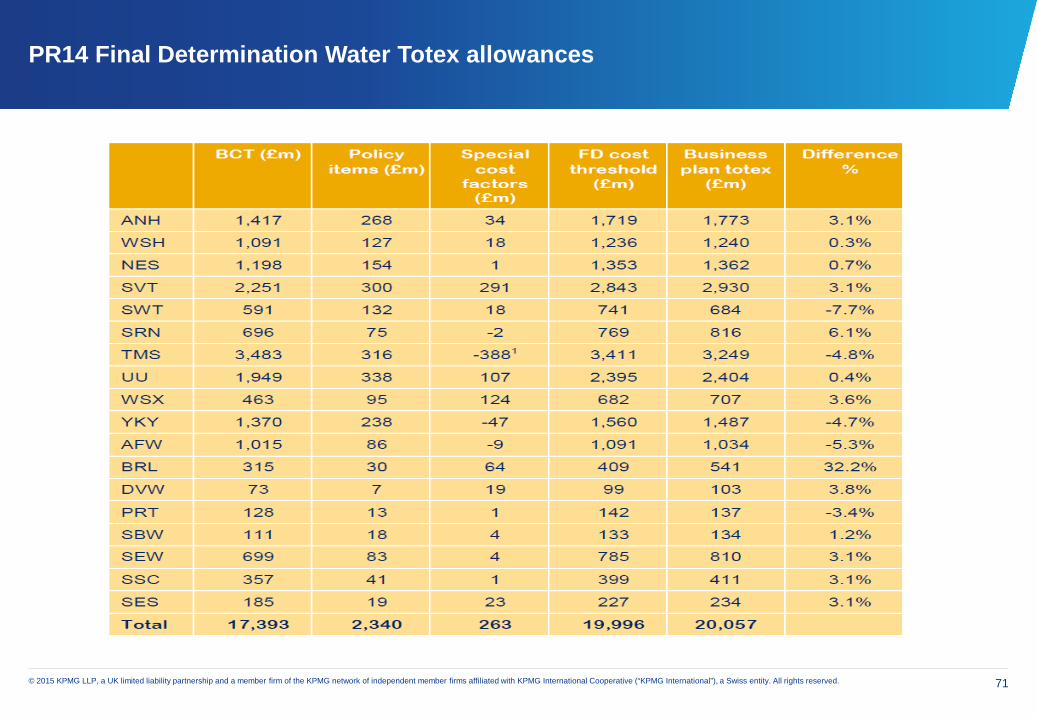

PR14 Final Determination Water Totex allowances

72© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

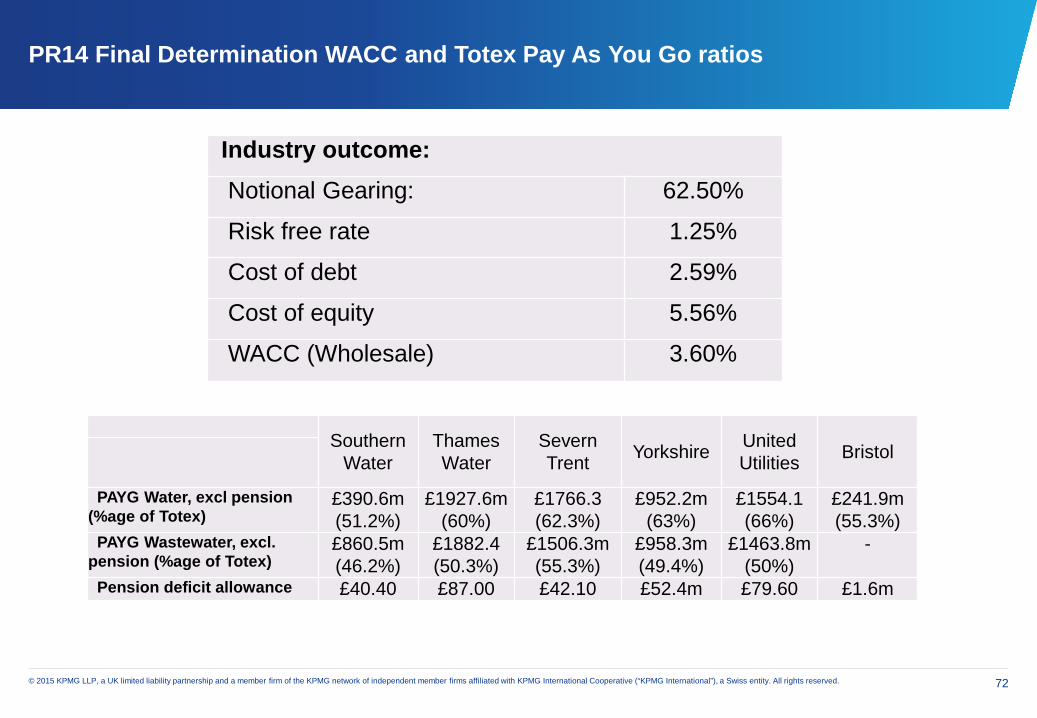

PR14 Final Determination WACC and Totex Pay As You Go ratios

Southern Water

Thames Water

Severn Trent Yorkshire United

Utilities Bristol

PAYG Water, excl pension (%age of Totex)

£390.6m (51.2%)

£1927.6m (60%)

£1766.3 (62.3%)

£952.2m (63%)

£1554.1 (66%)

£241.9m (55.3%)

PAYG Wastewater, excl. pension (%age of Totex)

£860.5m (46.2%)

£1882.4 (50.3%)

£1506.3m (55.3%)

£958.3m (49.4%)

£1463.8m (50%)

-

Pension deficit allowance £40.40 £87.00 £42.10 £52.4m £79.60 £1.6m

Industry outcome:Notional Gearing: 62.50%

Risk free rate 1.25%

Cost of debt 2.59%

Cost of equity 5.56%

WACC (Wholesale) 3.60%

73© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

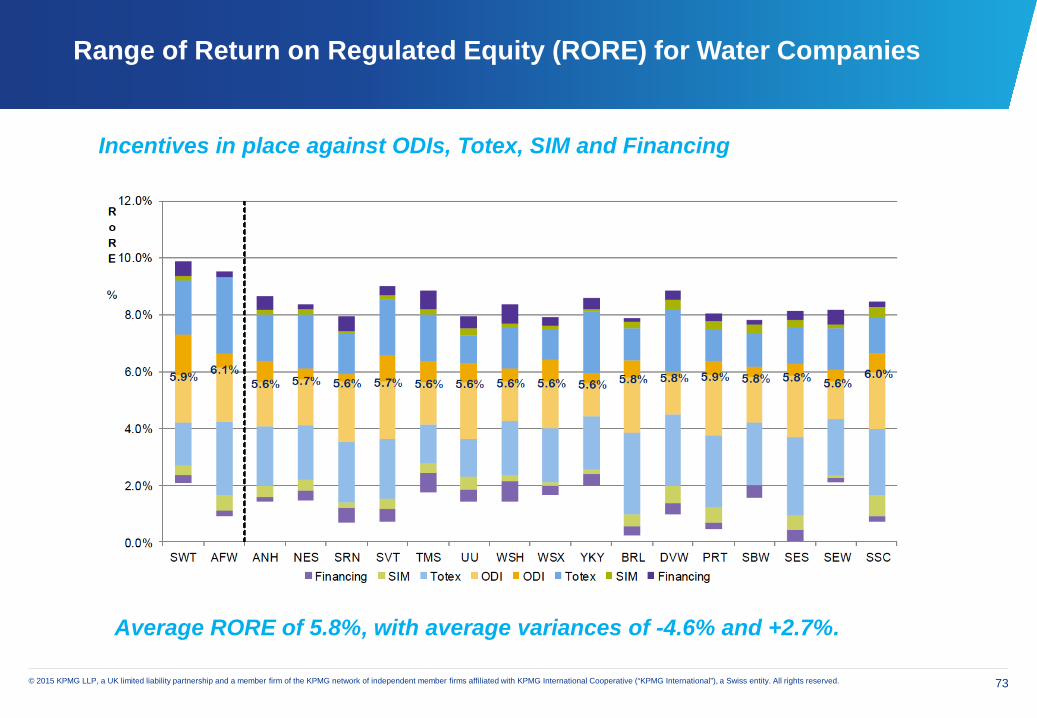

Range of Return on Regulated Equity (RORE) for Water Companies

Source: Ofwat PR14 Final determination – Policy Chapter A7 – Risk and Reward

Incentives in place against ODIs, Totex, SIM and Financing

Average RORE of 5.8%, with average variances of -4.6% and +2.7%.

74© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

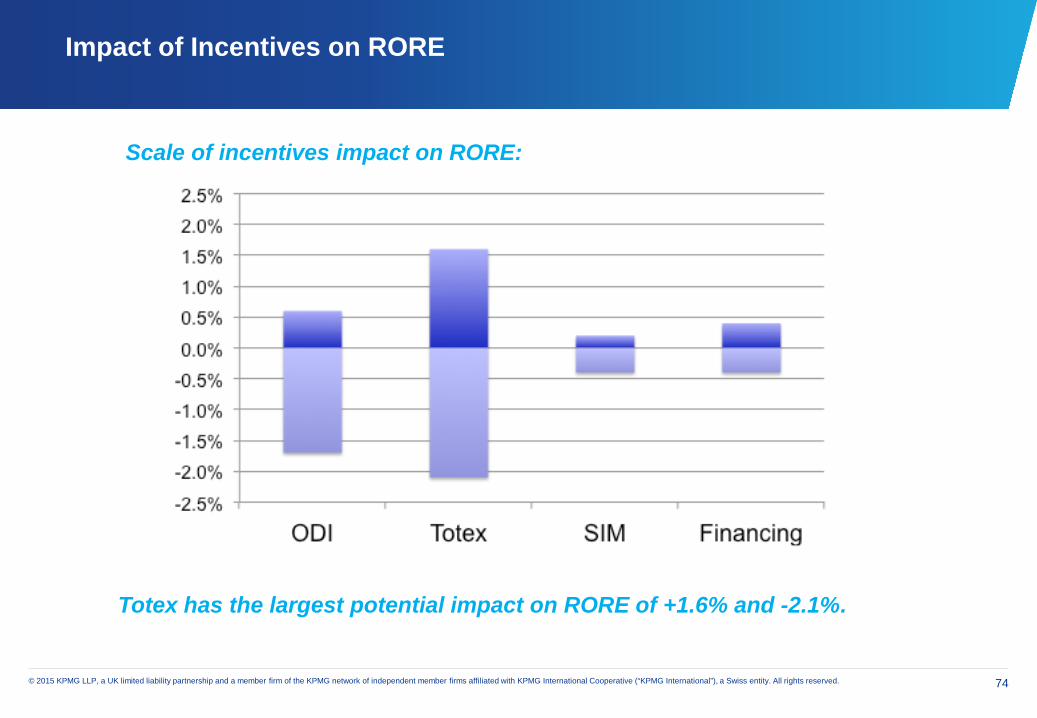

Impact of Incentives on RORE

Source: Ofwat PR14 Final determination – Policy Chapter A7 – Risk and Reward

Scale of incentives impact on RORE:

Totex has the largest potential impact on RORE of +1.6% and -2.1%.

75© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

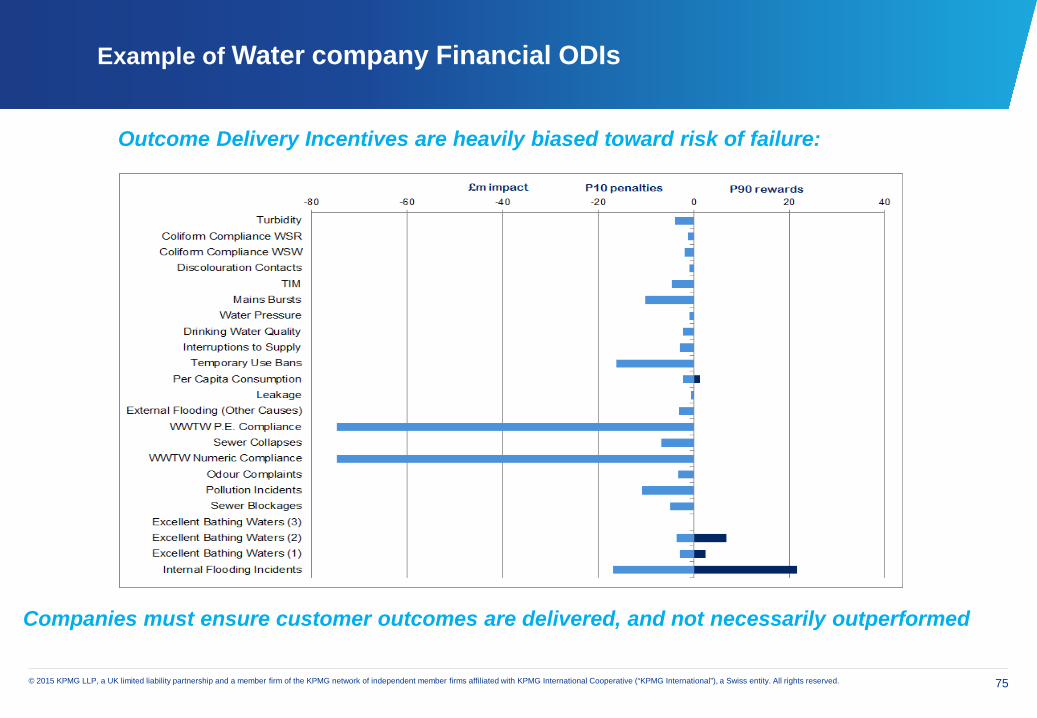

Example of Water company Financial ODIs

Outcome Delivery Incentives are heavily biased toward risk of failure:

Companies must ensure customer outcomes are delivered, and not necessarily outperformed

Capturing the tax value from capital projects

Harinder Soor

KPMG Partner and Head of Capital Allowances

77© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

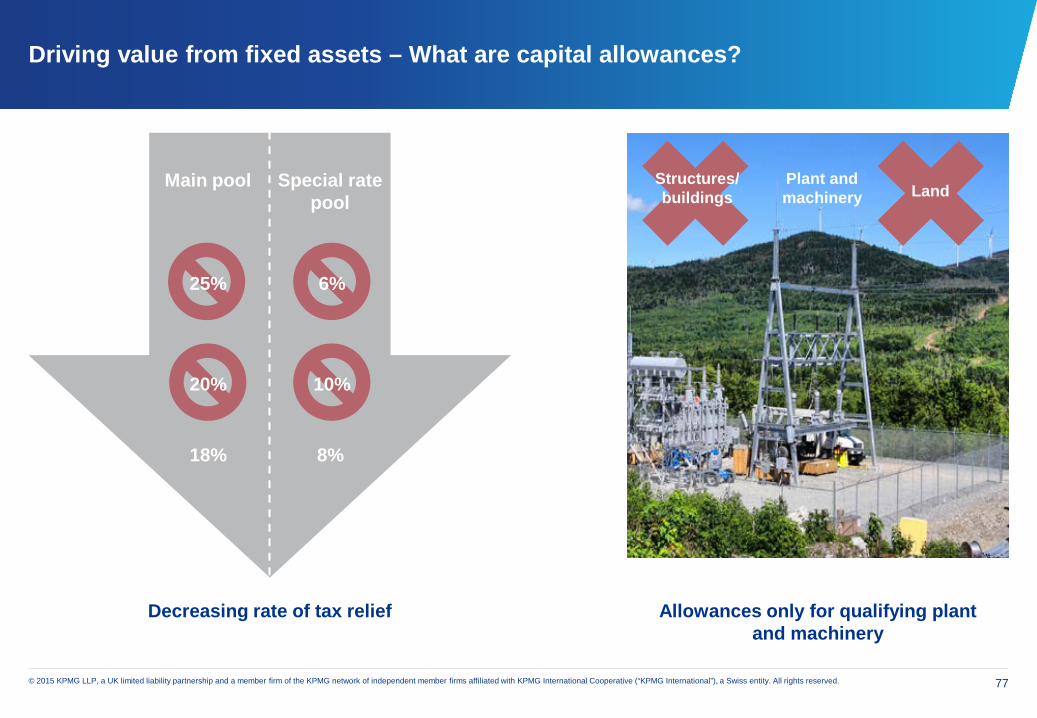

Driving value from fixed assets – What are capital allowances?

1. Managing your tax position with HMRC

2. Maintaining a robust fixed

asset process

Main pool Special ratepool

18% 8%

25%

20% 10%

6%

Decreasing rate of tax relief Allowances only for qualifying plant and machinery

Plant and machinery

Structures/ buildings Land

78© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

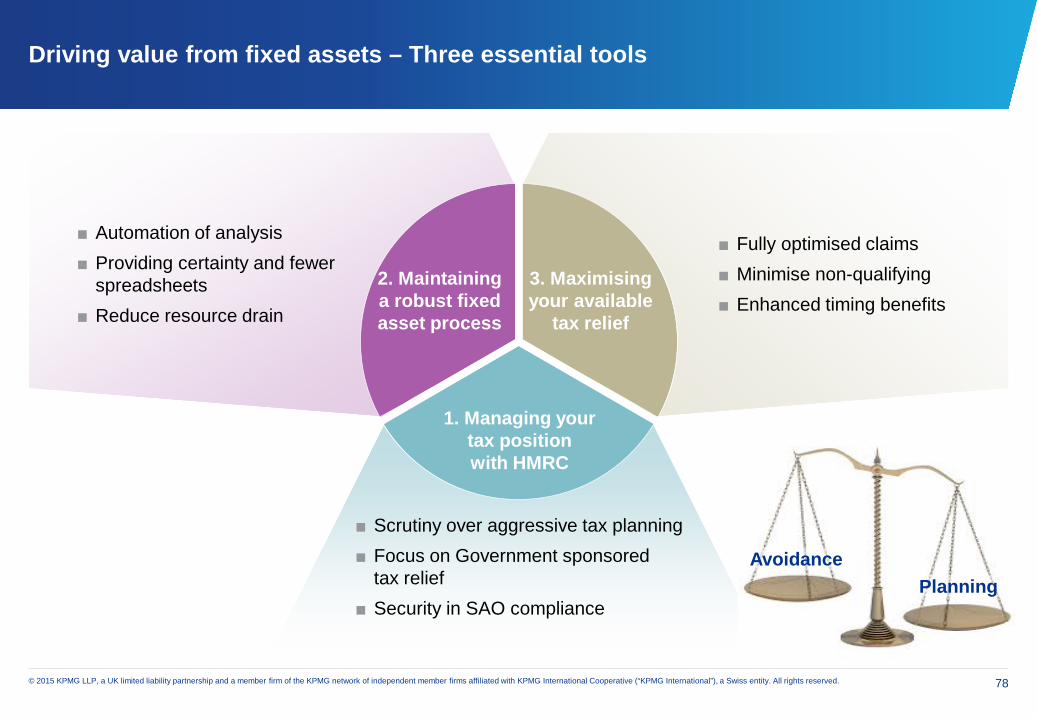

Driving value from fixed assets – Three essential tools

■ Fully optimised claims■ Minimise non-qualifying■ Enhanced timing benefits

■ Automation of analysis■ Providing certainty and fewer

spreadsheets■ Reduce resource drain

■ Scrutiny over aggressive tax planning■ Focus on Government sponsored

tax relief■ Security in SAO compliance

1. Managing yourtax positionwith HMRC

2. Maintaining a robust fixed asset process

3. Maximising your available

tax relief

AvoidancePlanning

79© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

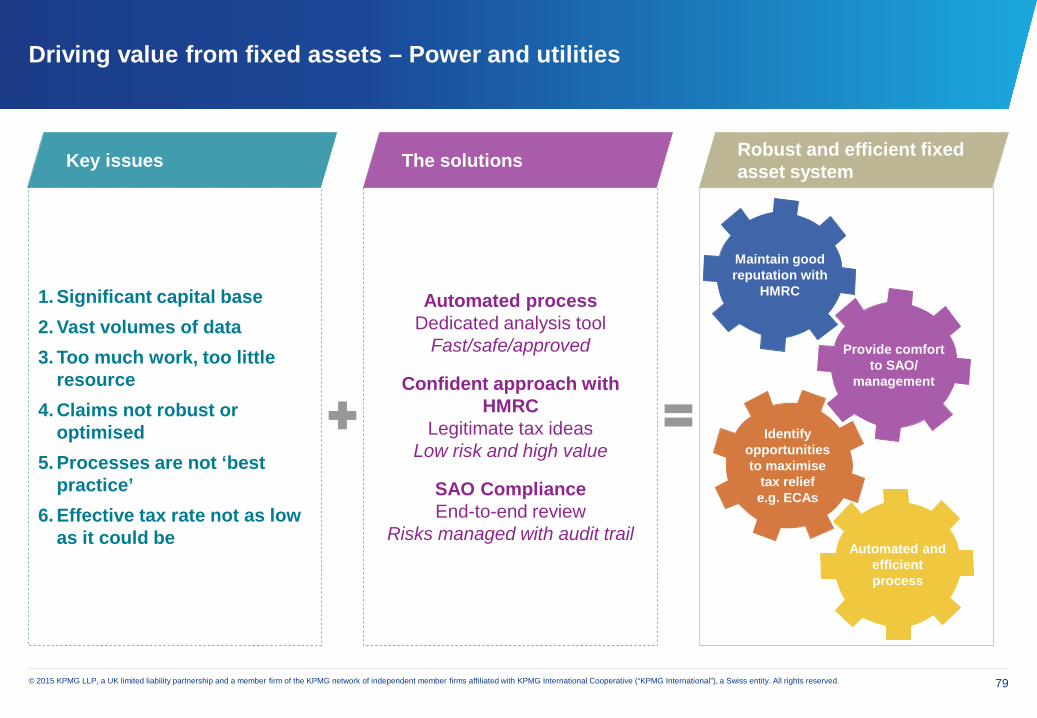

Driving value from fixed assets – Power and utilities

Automated processDedicated analysis tool

Fast/safe/approved

Confident approach with HMRC

Legitimate tax ideasLow risk and high value

SAO ComplianceEnd-to-end review

Risks managed with audit trailAutomated and

efficient process

Identify opportunities to maximise

tax relief e.g. ECAs

Maintain good reputation with

HMRC

Provide comfort to SAO/

management

1. Significant capital base2. Vast volumes of data3. Too much work, too little

resource4. Claims not robust or

optimised5. Processes are not ‘best

practice’6. Effective tax rate not as low

as it could be

Key issues The solutions Robust and efficient fixed asset system

80© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

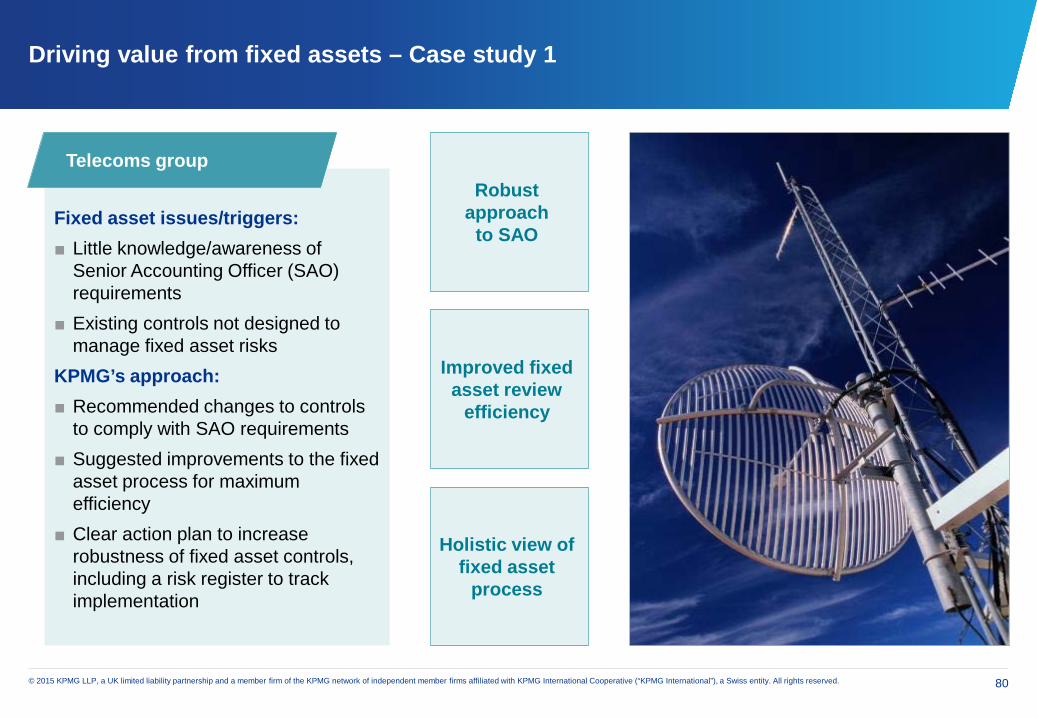

Driving value from fixed assets – Case study 1

Fixed asset issues/triggers:■ Little knowledge/awareness of

Senior Accounting Officer (SAO) requirements

■ Existing controls not designed to manage fixed asset risks

KPMG’s approach:■ Recommended changes to controls

to comply with SAO requirements■ Suggested improvements to the fixed

asset process for maximum efficiency

■ Clear action plan to increase robustness of fixed asset controls, including a risk register to track implementation

Telecoms group

Improved fixed asset review

efficiency

Robust approach

to SAO

Holistic view of fixed asset

process

81© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

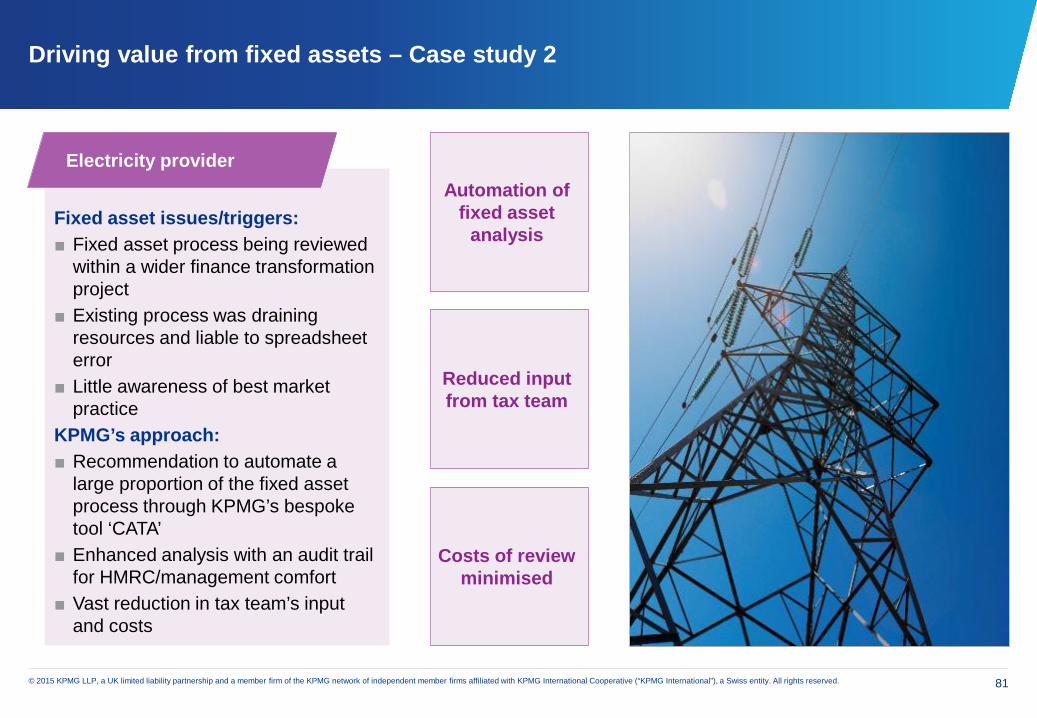

Driving value from fixed assets – Case study 2

Fixed asset issues/triggers:■ Fixed asset process being reviewed

within a wider finance transformation project

■ Existing process was draining resources and liable to spreadsheet error

■ Little awareness of best market practice

KPMG’s approach:■ Recommendation to automate a

large proportion of the fixed asset process through KPMG’s bespoke tool ‘CATA’

■ Enhanced analysis with an audit trail for HMRC/management comfort

■ Vast reduction in tax team’s input and costs

Electricity provider

Reduced input from tax team

Automation of fixed asset

analysis

Costs of review minimised

82© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

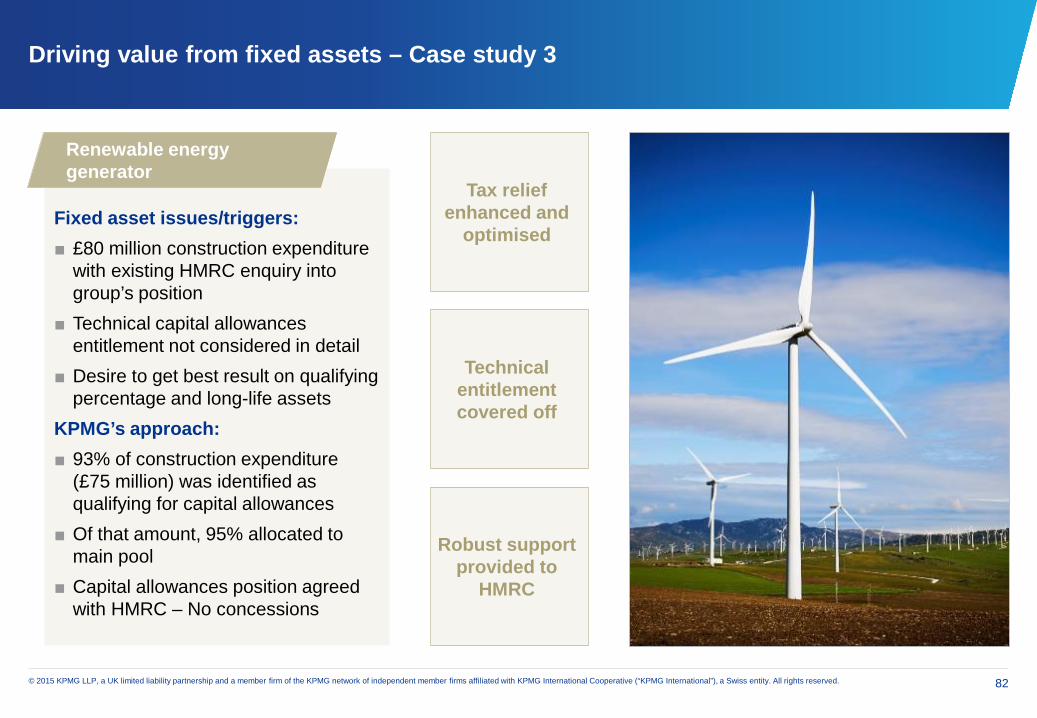

Driving value from fixed assets – Case study 3

Fixed asset issues/triggers:■ £80 million construction expenditure

with existing HMRC enquiry into group’s position

■ Technical capital allowances entitlement not considered in detail

■ Desire to get best result on qualifying percentage and long-life assets

KPMG’s approach:■ 93% of construction expenditure

(£75 million) was identified as qualifying for capital allowances

■ Of that amount, 95% allocated to main pool

■ Capital allowances position agreed with HMRC – No concessions

Renewable energy generator

Technical entitlement covered off

Tax relief enhanced and

optimised

Robust support provided to

HMRC

83© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

■ Proliferation of renewable generation

■ Onshore Transmission Owners ‘ONTOs’

■ Interconnectors

■ Infrastructure allowances?

■ Relief for power investment?

■ Office for Tax Simplification comments

■ Supportable and robust process

■ Automated process

■ Accurate and optimised analysis

■ HMRC leadership changes

■ Balance of power not all in HMRC’s favour

Driving value from fixed assets – On the horizon…

HMRC relationship with taxpayers New asset classes Legislation

changes Challenge to you

Shining a light on the murky world of

Green Taxes

Barbara BellKPMG, Head of Environment Tax Services

85© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

Environmental tax theory

Achieving environmental policy objectives through green taxation

The evolving picture

Why is this important for business?

Hot topics

86© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Six ways governments influence environmental behaviour

Regulation Cap and trade schemes Subsidies

Voluntary agreements Persuasion Taxation

87© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

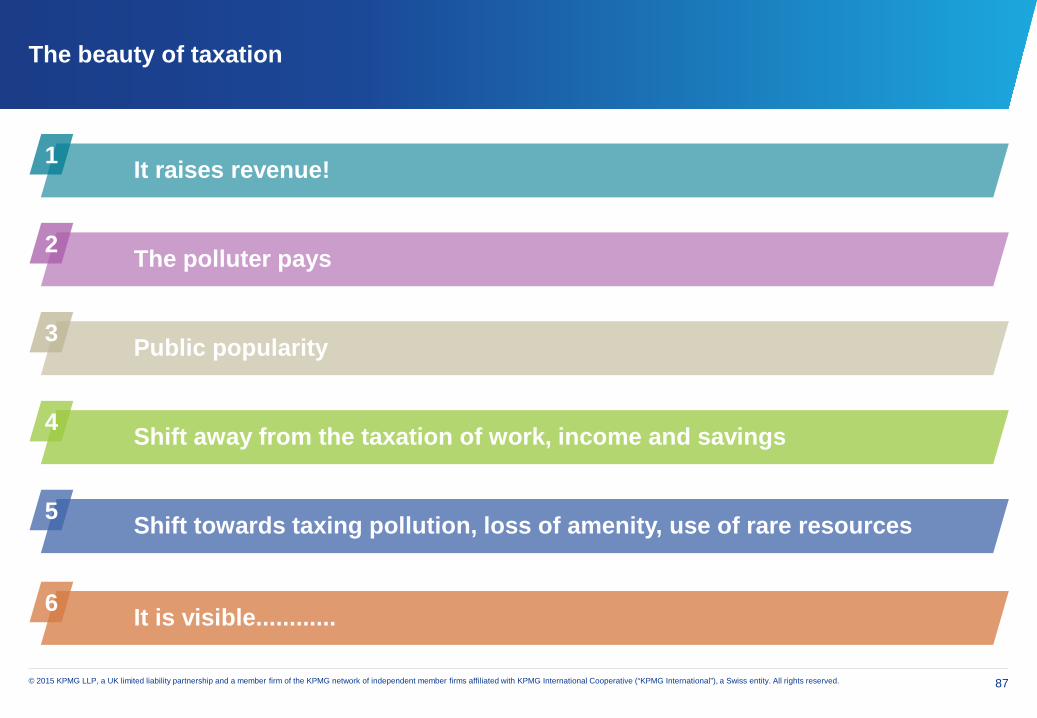

The beauty of taxation

It raises revenue!1

The polluter pays2

Public popularity3

Shift away from the taxation of work, income and savings4

Shift towards taxing pollution, loss of amenity, use of rare resources5

It is visible............6

88© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Environmental tax policy – The theory

Climate change Energy and fuel Material resource scarcity Water scarcity Population growth

Wealth Urbanization Food security Ecosystem decline Deforestation

89© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Environmental taxes

How is the UK using environmental taxation?Uncomfortable mixture of taxes and incentives

■ Excise duties

■ Landfill tax and air passenger duty

■ Climate change levy

■ Aggregates levy

■ Employment taxes

90© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Environmental taxation – Waste

91© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Hot topics – Landfill tax

Loss on Ignition (LoI) testing

Determining lower rated materials

Mixed loads

92© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Environmental taxation – Energy

93© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Hot topics – Climate change levy

Renewable Source Energy (RSE)Evidence to support exemptionLevy Exemption Certificates (LECs)HM Revenue and Customs activity

94© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Environmental taxation – Construction and infrastructure

95© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Northumbrian Water decisionHow does this affect construction projectsExemptions:■ Impact of EU Commission investigation findingsHM Revenue and Customs activity

Hot topics – Aggregates levy

96© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Why is this important to business?

Investment decisions1

Location2

Compliance3

Cashflow and pricing4

Future viability – markets, products, strategy5

Corporate responsibility6

97© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What next…..

New Environmental Taxes?

Indirect tax update

Tim Jones, KPMG Partner and Chris Angus, Senior Manager

99© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

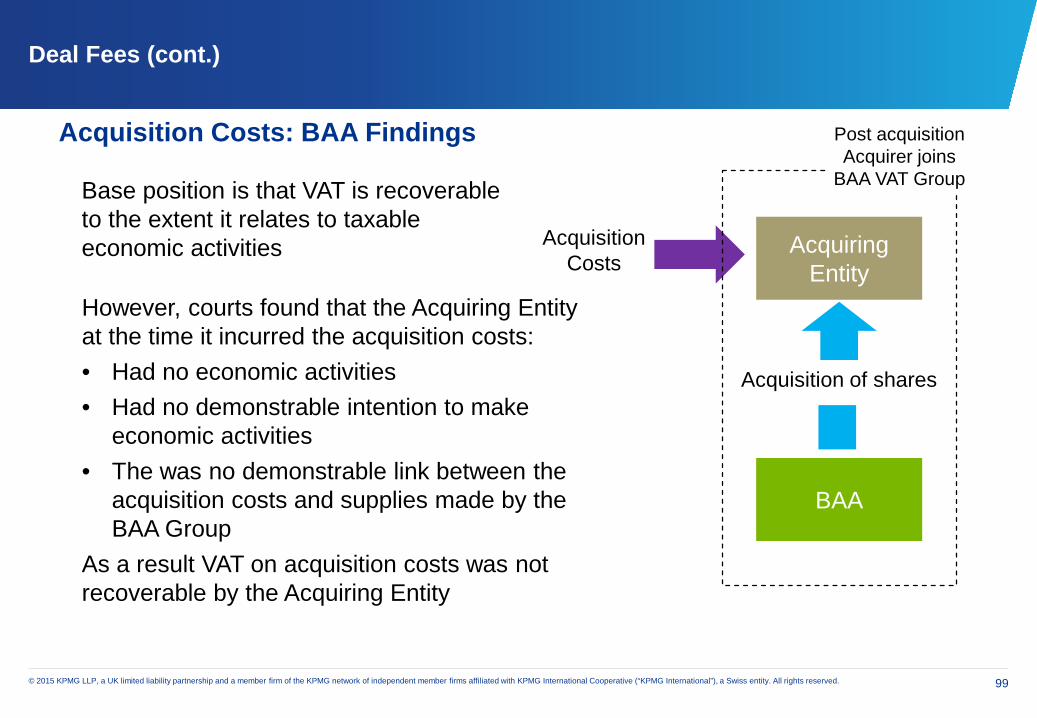

Deal Fees (cont.)

Acquisition Costs: BAA Findings

Acquiring Entity

BAA

Acquisition of shares

Acquisition Costs

However, courts found that the Acquiring Entity at the time it incurred the acquisition costs:• Had no economic activities • Had no demonstrable intention to make

economic activities• The was no demonstrable link between the

acquisition costs and supplies made by the BAA Group

As a result VAT on acquisition costs was not recoverable by the Acquiring Entity

Base position is that VAT is recoverable to the extent it relates to taxable economic activities

Post acquisition Acquirer joins

BAA VAT Group

100© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

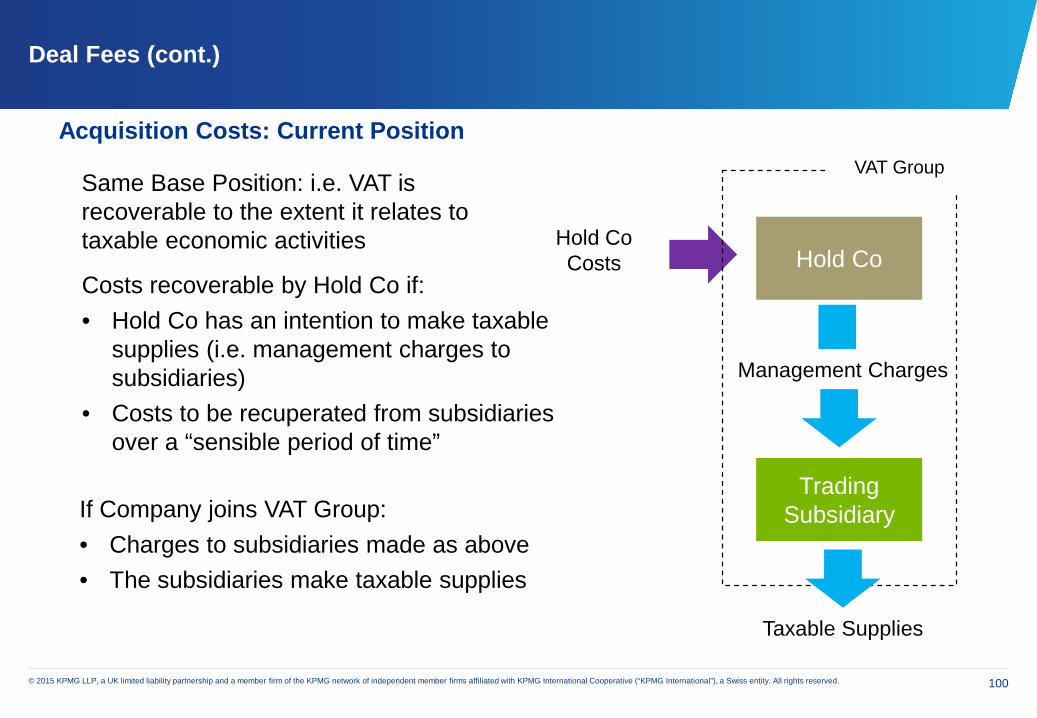

Deal Fees (cont.)

Acquisition Costs: Current Position

Hold Co

TradingSubsidiary

Costs recoverable by Hold Co if:• Hold Co has an intention to make taxable

supplies (i.e. management charges to subsidiaries)

• Costs to be recuperated from subsidiaries over a “sensible period of time”

Same Base Position: i.e. VAT is recoverable to the extent it relates to taxable economic activities

VAT Group

Management Charges

Taxable Supplies

Hold Co Costs

If Company joins VAT Group:• Charges to subsidiaries made as above• The subsidiaries make taxable supplies

101© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

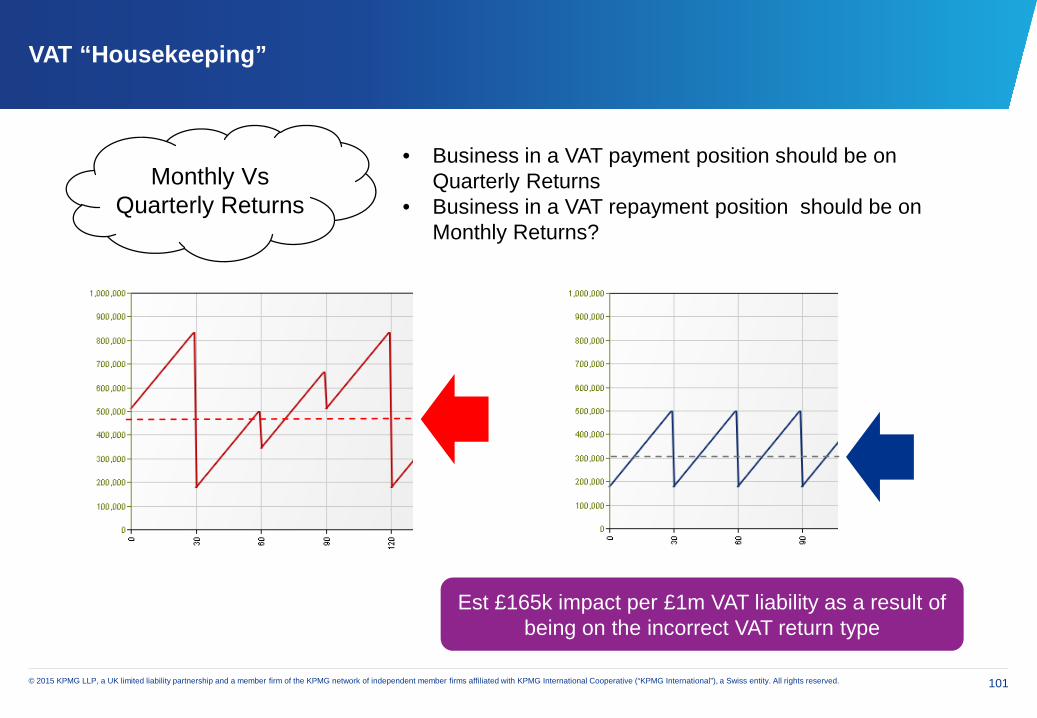

VAT “Housekeeping”

Monthly Vs Quarterly Returns

• Business in a VAT payment position should be on Quarterly Returns

• Business in a VAT repayment position should be on Monthly Returns?

Est £165k impact per £1m VAT liability as a result of being on the incorrect VAT return type

102© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

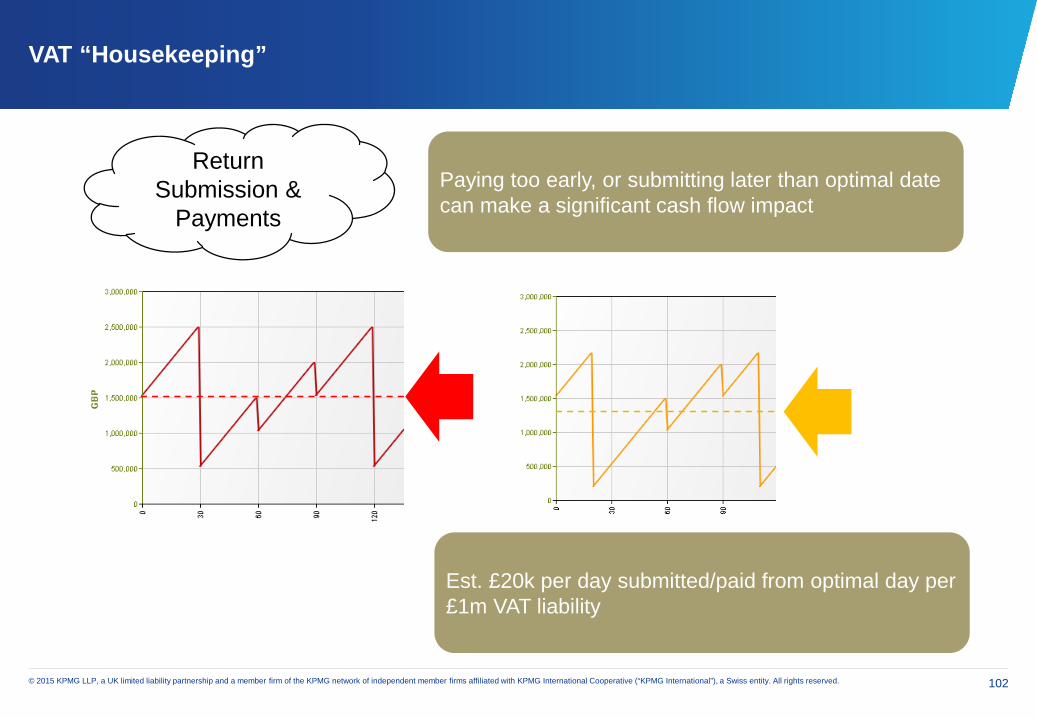

VAT “Housekeeping”

Return Submission &

PaymentsPaying too early, or submitting later than optimal date can make a significant cash flow impact

Est. £20k per day submitted/paid from optimal day per £1m VAT liability

103© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

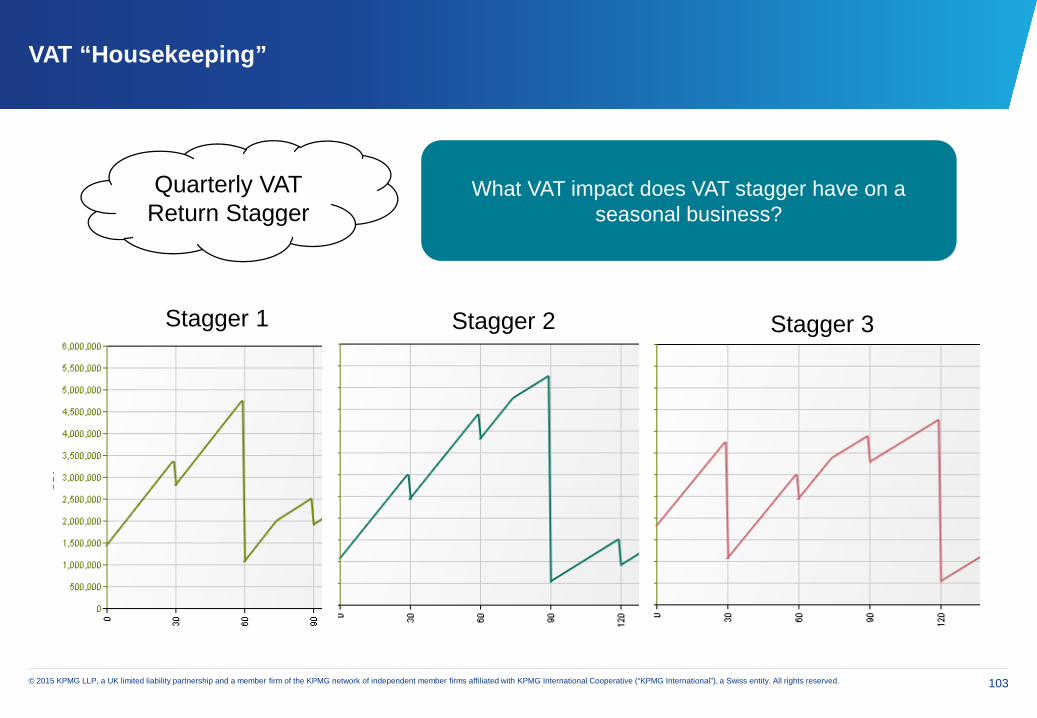

VAT “Housekeeping”

Quarterly VAT Return Stagger

What VAT impact does VAT stagger have on a seasonal business?

Stagger 1 Stagger 2 Stagger 3

104© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

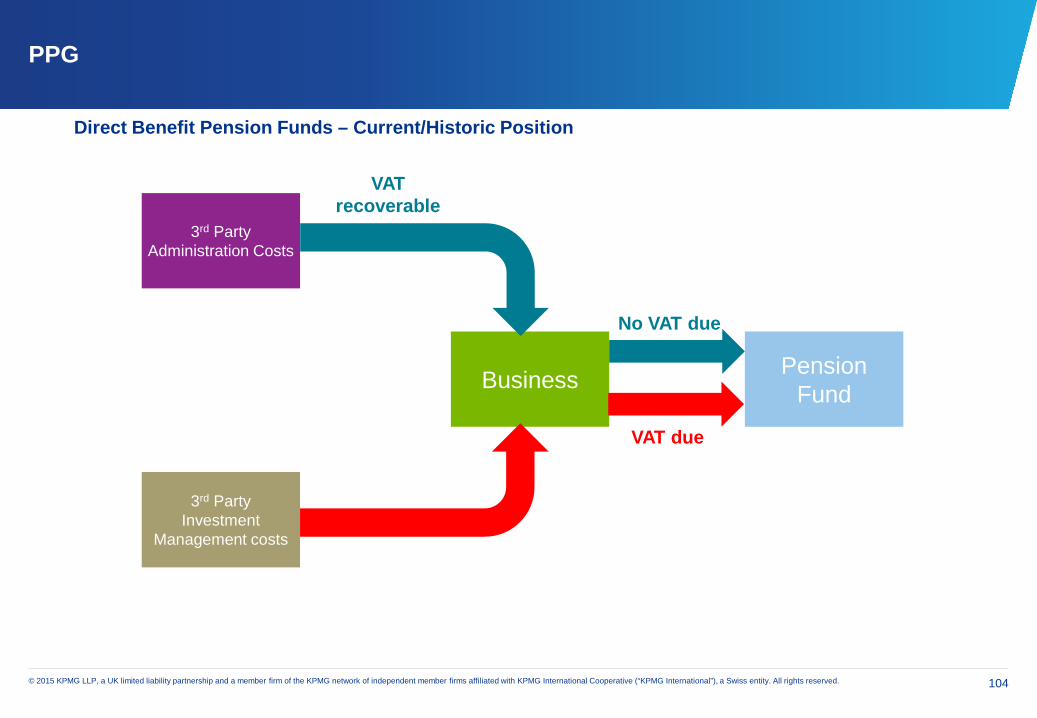

PPG

Direct Benefit Pension Funds – Current/Historic Position

Business Pension Fund

3rd PartyInvestment

Management costs

3rd PartyAdministration Costs

VAT recoverable

No VAT due

VAT due

105© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

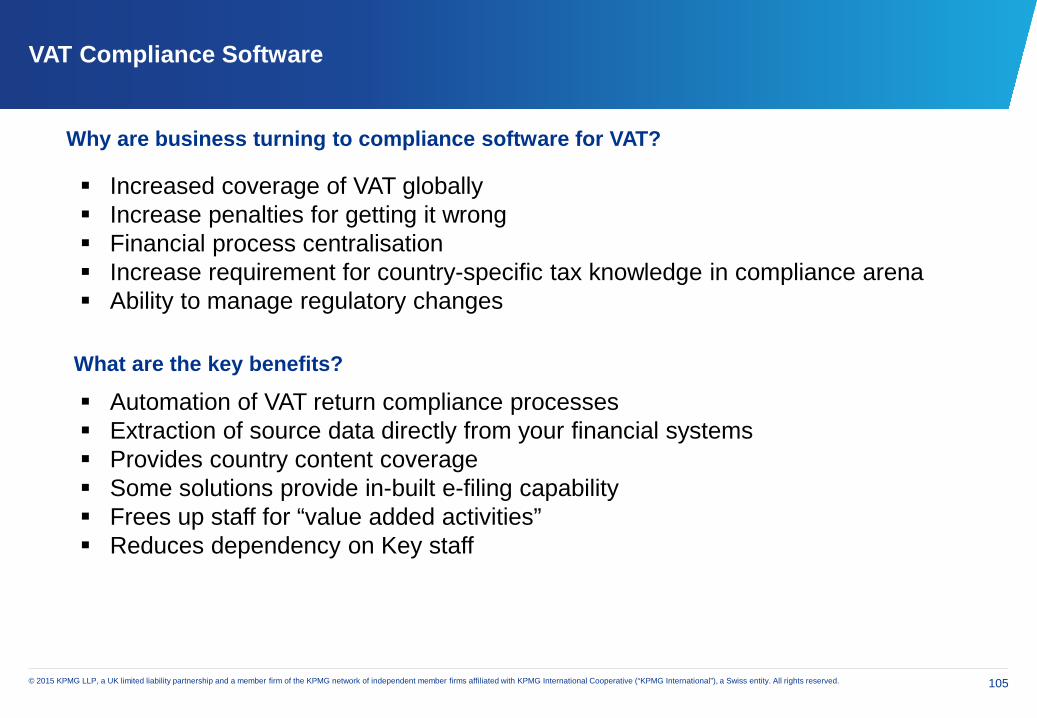

VAT Compliance Software

Why are business turning to compliance software for VAT?

Increased coverage of VAT globally Increase penalties for getting it wrong Financial process centralisation Increase requirement for country-specific tax knowledge in compliance arena Ability to manage regulatory changes

What are the key benefits?

Automation of VAT return compliance processes Extraction of source data directly from your financial systems Provides country content coverage Some solutions provide in-built e-filing capability Frees up staff for “value added activities” Reduces dependency on Key staff

106© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

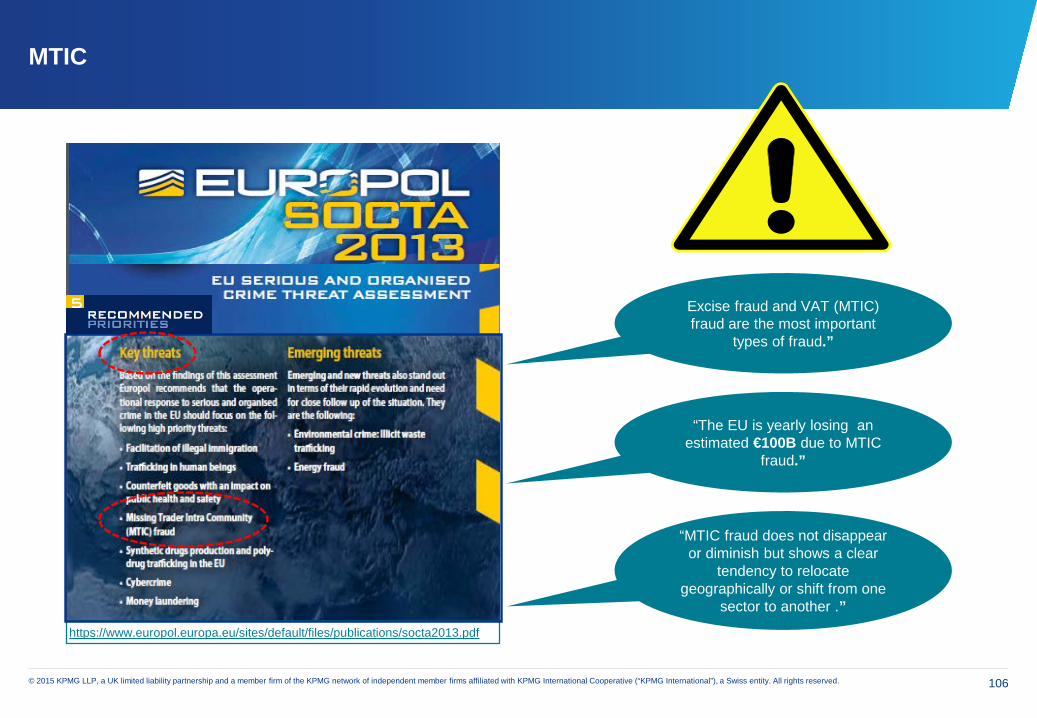

https://www.europol.europa.eu/sites/default/files/publications/socta2013.pdf

“The EU is yearly losing an estimated €100B due to MTIC

fraud.”

“MTIC fraud does not disappear or diminish but shows a clear

tendency to relocate geographically or shift from one

sector to another .”

Excise fraud and VAT (MTIC) fraud are the most important

types of fraud.”

MTIC

107© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

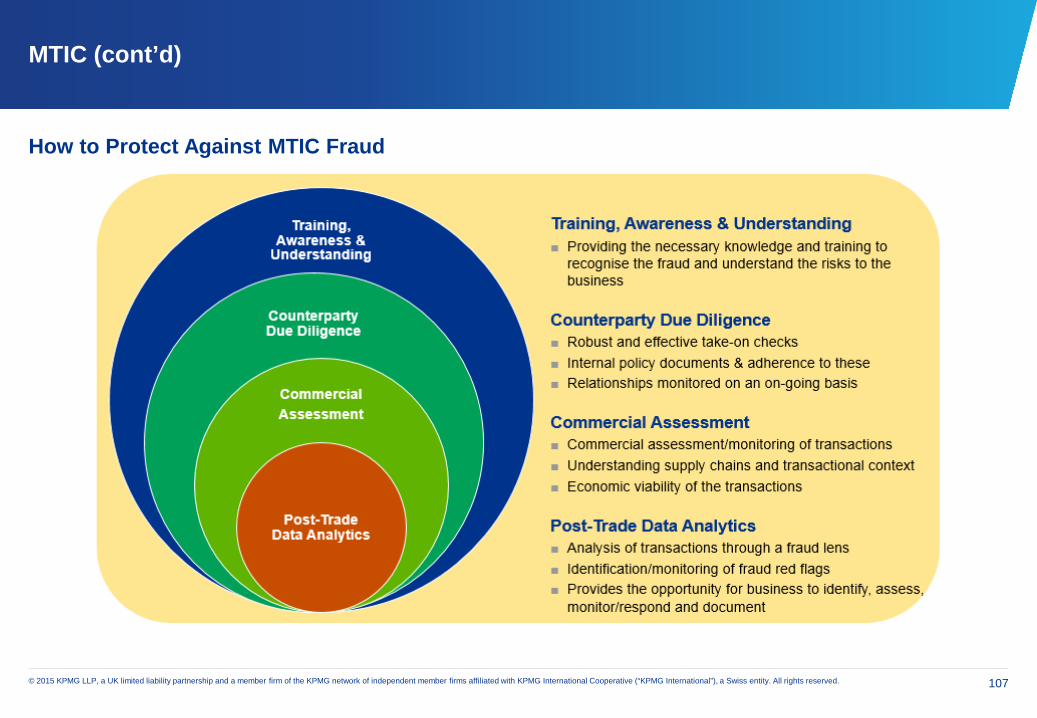

MTIC (cont’d)

How to Protect Against MTIC Fraud

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Produced by Create Graphics | Document number: CRT042444

Related Documents