Case analysis: Kota Fibers, Ltd. Group 1: Bhavananda Jha (14317) Chanda Kiran Adhikari (14301) Niraj Ghimire (14314) Pragya Joshi (14318)

Kota Fiber Case Study

Dec 14, 2015

This is a comprehensive case analysis of Kota Fiber case

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Group 1:

Bhavananda Jha (14317)

Chanda Kiran Adhikari (14301)

Niraj Ghimire (14314)

Pragya Joshi (14318)

Prajwal Sagar Shrestha (14331)

1/8/2015

Introduction

Kota fiber is nylon fiber producing company situated in Kota, India. The business has been

running smoothly with steady market share. But the company is facing serious liquidity crunch

and even in the heavy selling season, the business has to take more loans. The situation has

become worse as the company had overdrawn the bank account and could not pay the excise tax.

The company had taken loan from the bank with a contract to clean up on December 2001 but

the financial projection for 2001 shows inability of Kota Fiber to repay all its line of credit to

bank on the specified period. On the other hand, there are four different proposals from managers

of different departments, which may be beneficial for the company. The reassessment of the

financial forecast including the new proposals is needed to find out the actual debt position of the

company.

Issues

Some of the issues taken into consideration are:

1. The current situation of business.

2. The reasons for company to run out of cash and its consequences.

3. Analysis of clean up requirement of the bank

4. Analysis of Mehta’s financial forecast and cash cycle analysis.

5. Analysis of impact of proposals given by employees and managers of Kota Fibres on the

debt position of the company.

6. The actions that can be taken by Pundir.

Analysis of the Issues

Current Situation:

The firm does not have enough cash in their bank accounts to pay off the tax inspector that

demand the excise tax to be paid. This situation backlogs the trucks ready to depart the night

before, but is unable to until the tax inspectors paid.

The company has also overdrawn on its bank account three weeks in a row and that situation

needs to be addressed. The bank has already been disappointed by the company’s inability to

clean up its debt balance for 30 days during this past off-season and would be expected to

advance no more cash unless the situation changes.

The reasons for company to run out of cash and consequences:

Kota fiber has run out of cash for because of the following main reasons:

o Sales growth (20% anticipated in 2001): In the year 2000, the actual growth in sales is

18% but in 2001 the company is expected a growth rate of 20% for which the company

need more cash.

o Declining profitability: An analysis of case reveals that net profit as a percentage of sales

has fallen over the past year 2000, from 5.6% to 3.4% of gross sales and is projected to

fall to 1.5% in 2001

o Aggressive dividend payments: The Company is paying a dividend of INR 2 million per

year which is higher than the expected net profit of INR 1.33 million.

o Increase in Cost of goods sold: The ratio of cost of goods sold to gross sales has risen by

2% from 69% to 71% and is expected to mount to 73.7% in 2001.

o Decrease in ROE: Kota return on equity is 21.5% in 2000 and falls to 11.9% in 2001

which is below than interest rate of 14.5%.

The consequence for the company is going to be

o If Kota does not clear line of credit, the bank will stop providing credit facilities to the

company.

o Insufficient cash flow will hamper the day to day operations of the business.

Analysis of Clean- up requirement of Bank

Clean-up requirement is a traditional way through which banks can secure its loan from being

default. Normally clean up requirement are from 30 to 60 days. The cleanup period is usually

arranged right after the peak sales time in the year for a particular business. After peak sales

period when receivables have mostly been collected and cash need for purchasing new inventory

is comparatively low, the portion from gross profit is to be paid to bank to remain debt free for

the specified period. This is a banking practice that requires a borrower to pay off all balances of

any renewable lines of credit and keep them at zero for 30 to 60 days or so. Banks require

cleanup of loan in order to manage the unsecured loans provided to businesses. In case of Kota

Fibers, the bank may have added clean up requirement in the loan contract in order to prevent

Kota fibers to use line of credit as ongoing permanent financing.

The bank must not continue to waive compliance with clean-up of the loan for Kota Fibers. As

the business is facing scarcity of cash, for certain years, the waiver may be continued so that

Kota Fiber would not have extra burden of mandatory clean up. But in long run, the waiver must

be ceased. On the other hand, after few years, if Kota fibers can turn the business as highly

profitable and if the loan given by the bank can be declared as secured loan, then the waiver of

clean up may be given continuity for long run.

Analysis of Mehta’s Financial forecast and cash cycle analysis.

The financial forecast was constructed based on the past financial report and to generate the

ability to clean up the loan by the end of 2001. The monthly forecast of the financial statements

was developed using the operating assumptions in exhibit 11 of the case. The forecast was

developed as the bank asked for a proper financial forecast of Kota fibers for the coming year.

The bank was refusing to extend further line of credit to Kota fibers unless the financial forecast

of the company demonstrated the ability of the firm to clear the loan by the end of 2001.

Mehta’s financial forecast shows that the expected Gross sales will be increased by 20% in 2001

which was increased by 18% in 2000. The expected gross net profit margin will be only 1.5% of

gross sales in 2001 which was 3.4% in 2000. The cost of goods sold which is increasing year by

year will expected to reach to 73.7% of sales in 2001 which was 71% in 2000.

According to the financial forecast, the current ratio as well as quick ratio are expected to decline

in 2001 indicating poor liquidity to be expected in the coming year. The gross profit margin is

also expected to decline to only 13.29 %. Return on assets is also expected to decline. And the

debt to assets ratio is expected to increase from 10.85% to 28.41 %, because of increase in short

term financing needs.

Financial Ratios Actual(2000) Forecast(2001)

Current ratio4684237/1,443,637 6,690,525/ 4,440,345

3.24 1.5

Quick ratio(4,684,237-1,249,185)/1,443,637 (6,690,525-2,225,373)/ 4,440,345

2 1

Gross profit margin64,487,358/10,621,447 77,265,092/10,271,712

16.47% 13.29%

Total asset turnover ratio64,487,358/13,295,604 77,265,092/15,628,161

4.85 4.94

Return on assets2,550,837/ 13,295,604 1,335,848 /15,628,161

19.18% 8.57%

Debt to asset ratio1,443,637/13,295,604 4,440,345/15,628,161

10.85% 28.41%

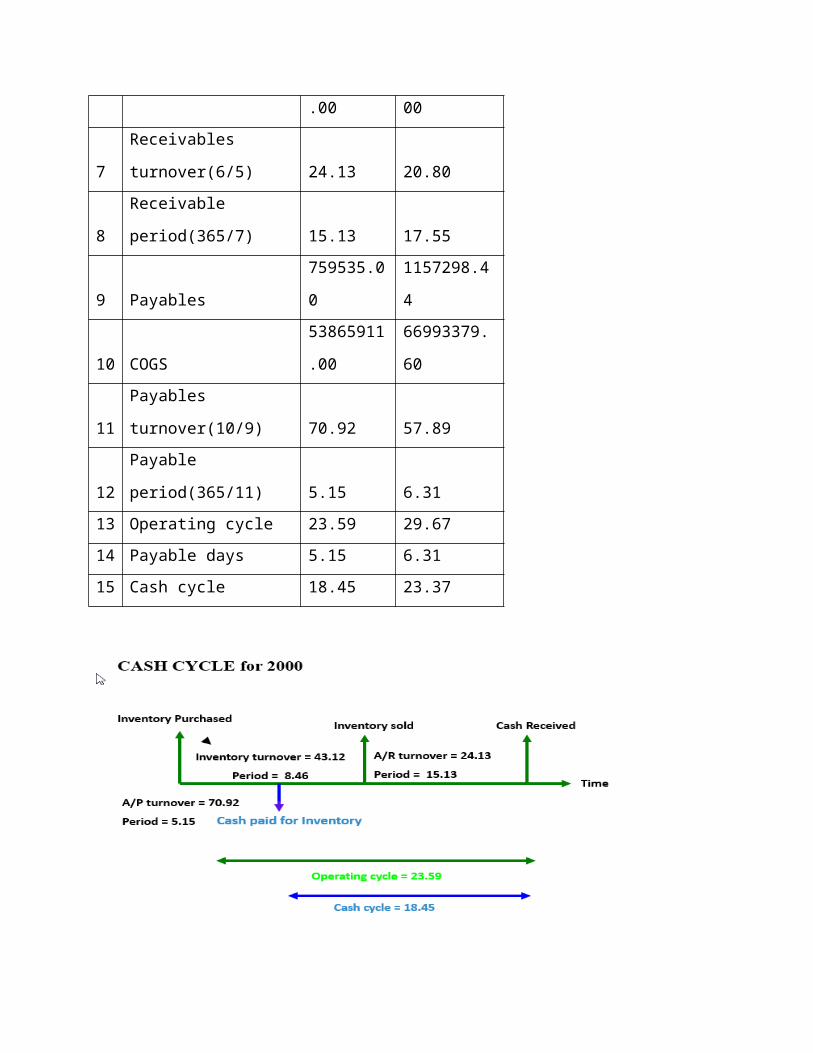

The calculation of Cash Cycle based on the financial forecast done by Mehta.

S

N Particulars Actual 2000

Forecasted

2001

1 Average inventory 1249185.00 2225372.57

2 COGS

53865911.0

0 66993379.60

3

Inventory turnover

ratio(2/1) 43.12 30.10

4 Inventory period(365/3) 8.46 12.12

5 Receivable 2672729.00 3715152.20

6 Sales

64487358.0

0 77265092.00

7

Receivables

turnover(6/5) 24.13 20.80

8 Receivable period(365/7) 15.13 17.55

9 Payables 759535.00 1157298.44

10 COGS

53865911.0

0 66993379.60

11 Payables turnover(10/9) 70.92 57.89

12 Payable period(365/11) 5.15 6.31

13 Operating cycle 23.59 29.67

14 Payable days 5.15 6.31

15 Cash cycle 18.45 23.37

The Cash Cycle prepared with the financial forecast shows that both operating cycle and cash

cycle will increase in 2001 from 23.59 days to 29.67 days and 5.15 days to 6.31 days

respectively because of which the company have to face crisis of cash flow in upcoming year

with this financial forecast.

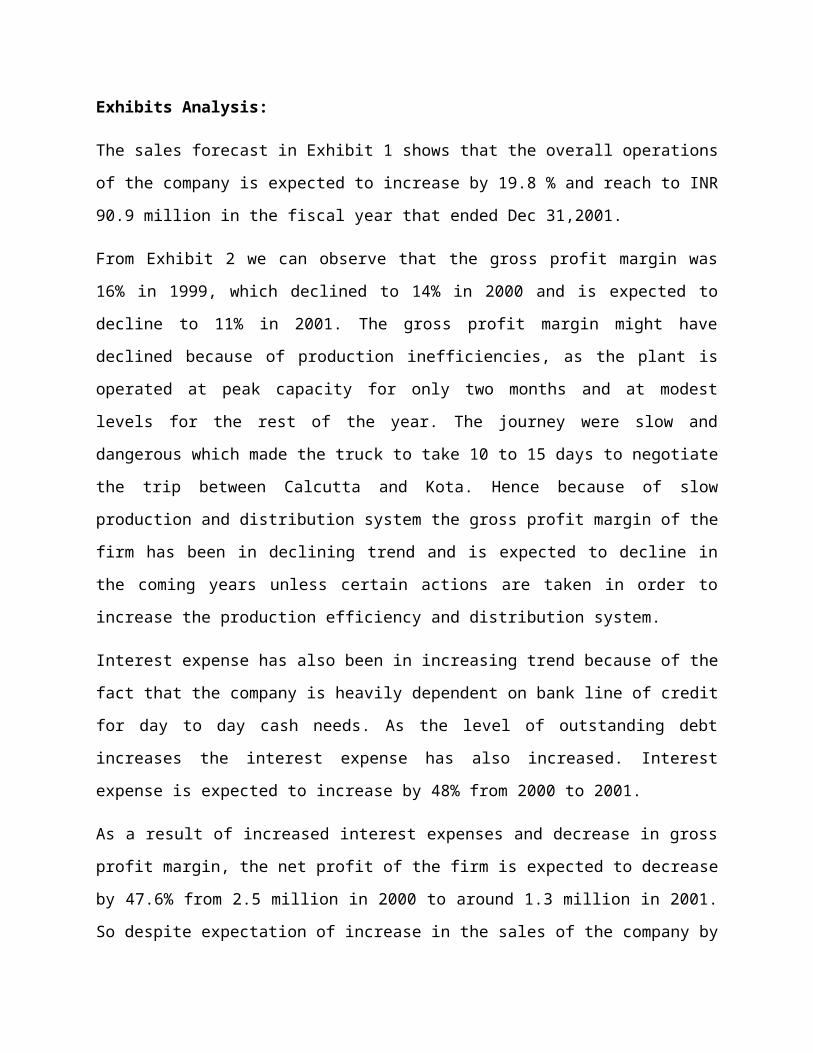

Exhibits Analysis:

The sales forecast in Exhibit 1 shows that the overall operations of the company is expected to

increase by 19.8 % and reach to INR 90.9 million in the fiscal year that ended Dec 31,2001.

From Exhibit 2 we can observe that the gross profit margin was 16% in 1999, which declined to

14% in 2000 and is expected to decline to 11% in 2001. The gross profit margin might have

declined because of production inefficiencies, as the plant is operated at peak capacity for only

two months and at modest levels for the rest of the year. The journey were slow and dangerous

which made the truck to take 10 to 15 days to negotiate the trip between Calcutta and Kota.

Hence because of slow production and distribution system the gross profit margin of the firm has

been in declining trend and is expected to decline in the coming years unless certain actions are

taken in order to increase the production efficiency and distribution system.

Interest expense has also been in increasing trend because of the fact that the company is heavily

dependent on bank line of credit for day to day cash needs. As the level of outstanding debt

increases the interest expense has also increased. Interest expense is expected to increase by 48%

from 2000 to 2001.

As a result of increased interest expenses and decrease in gross profit margin, the net profit of the

firm is expected to decrease by 47.6% from 2.5 million in 2000 to around 1.3 million in 2001. So

despite expectation of increase in the sales of the company by 19.8%, the net profit is expected to

decrease by 47.8%. The main reason behind this is in efficiency in production, poor management

of working capital and higher outstanding debt for financing short term financing needs.

By analyzing the actual and forecasted balance sheet of the Kota fiber, we can say that the

ending cash balance has not changed that much and firm is expected to maintain a minimum cash

balance of 750,000 in all the months of the coming year. But for maintaining the cash balance

the firm is expected to take more line of credit from the bank. So the notes payable to bank is

expected to increase by 406% from 648102 in 2000 to 3463701 in 2001. The main reason behind

his huge increase in notes payable might be attributed to poor cash management of the firm. The

firm is not expected to generate enough cash collections to cover the cash disbursement in each

month of the coming fiscal year, as a result of which the outstanding debt is expected to increase

in order to maintain the minimum cash balance at the end of each month.

Analysis of proposals and their impact on the debt position of the company.

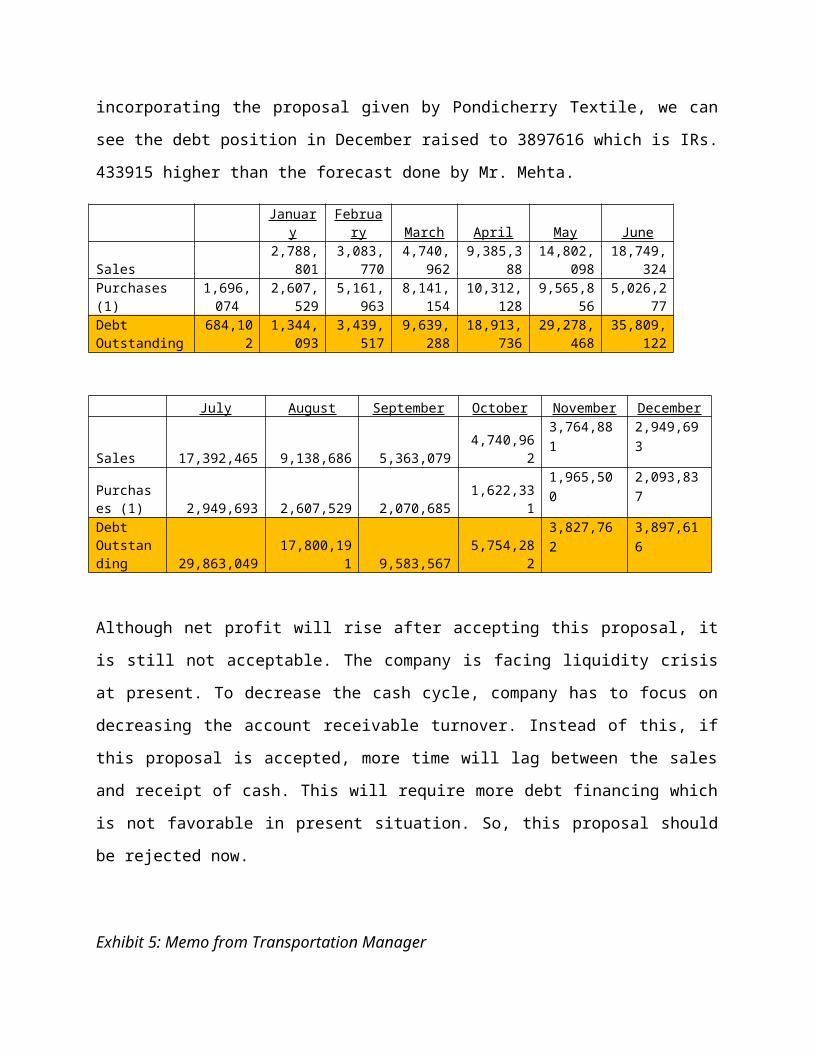

Exhibit 4: Memo from field Sales Manager

One of firm’s goals is to keep the credit terms to 45 days. Pondicherry textiles propose that Kota

fibers, ltd extend the credit terms to 80 days and they will make the Kota as its prime yarn

suppliers. From the calculation of debt outstanding after incorporating the proposal given by

Pondicherry Textile, we can see the debt position in December raised to 3897616 which is IRs.

433915 higher than the forecast done by Mr. Mehta.

January February March April May June

Sales2,788,80

13,083,77

04,740,96

2 9,385,38814,802,09

818,749,32

4

Purchases (1)1,696,07

42,607,52

95,161,96

38,141,15

410,312,12

8 9,565,856 5,026,277Debt Outstanding 684,102

1,344,093

3,439,517

9,639,288

18,913,736

29,278,468

35,809,122

July August September October November December

Sales 17,392,465 9,138,686 5,363,079 4,740,9623,764,881 2,949,693

Purchases (1) 2,949,693 2,607,529 2,070,685 1,622,331

1,965,500 2,093,837

Debt Outstanding 29,863,049 17,800,191 9,583,567 5,754,282

3,827,762 3,897,616

Although net profit will rise after accepting this proposal, it is still not acceptable. The company

is facing liquidity crisis at present. To decrease the cash cycle, company has to focus on

decreasing the account receivable turnover. Instead of this, if this proposal is accepted, more

time will lag between the sales and receipt of cash. This will require more debt financing which

is not favorable in present situation. So, this proposal should be rejected now.

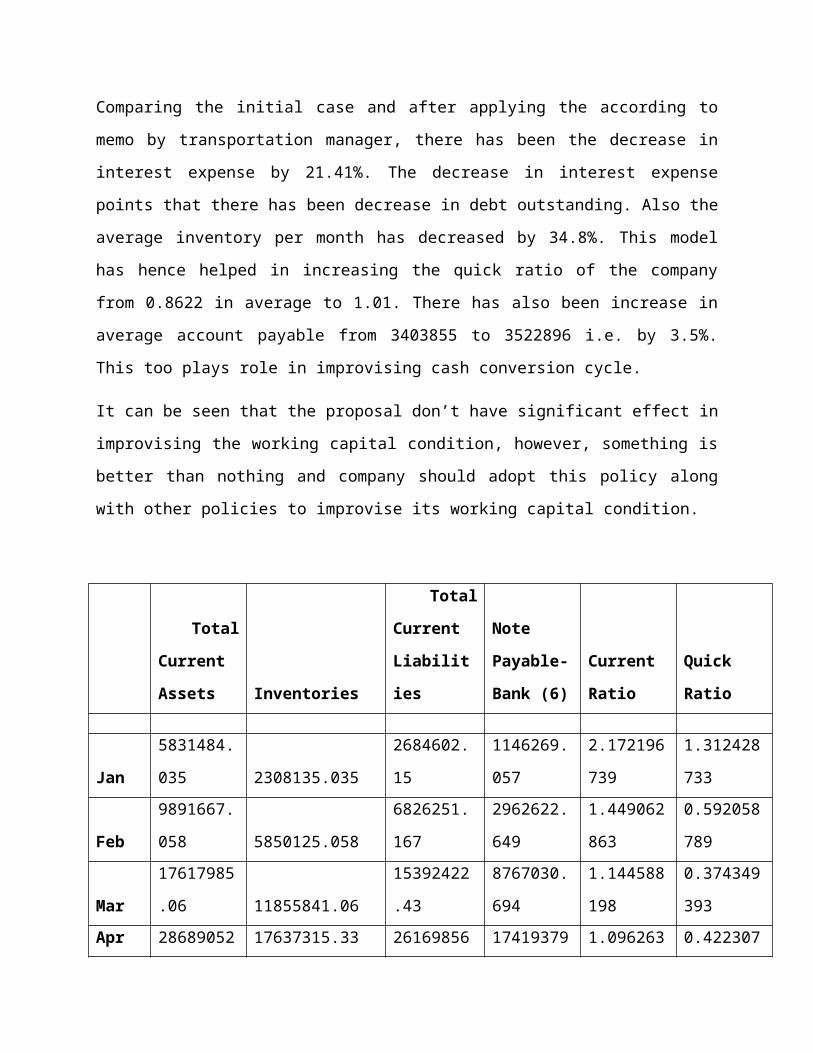

Exhibit 5: Memo from Transportation Manager

Comparing the initial case and after applying the according to memo by transportation manager,

there has been the decrease in interest expense by 21.41%. The decrease in interest expense

points that there has been decrease in debt outstanding. Also the average inventory per month has

decreased by 34.8%. This model has hence helped in increasing the quick ratio of the company

from 0.8622 in average to 1.01. There has also been increase in average account payable from

3403855 to 3522896 i.e. by 3.5%. This too plays role in improvising cash conversion cycle.

It can be seen that the proposal don’t have significant effect in improvising the working capital

condition, however, something is better than nothing and company should adopt this policy

along with other policies to improvise its working capital condition.

Total

Current

Assets Inventories

Total

Current

Liabilities

Note

Payable-

Bank (6)

Current

Ratio

Quick

Ratio

Jan

5831484.03

5 2308135.035 2684602.15

1146269.05

7

2.17219673

9

1.31242873

3

Feb

9891667.05

8 5850125.058 6826251.167

2962622.64

9

1.44906286

3

0.59205878

9

Mar

17617985.0

6 11855841.06 15392422.43

8767030.69

4

1.14458819

8

0.37434939

3

Apr

28689052.7

3 17637315.33 26169856.88

17419379.4

2

1.09626326

4

0.42230790

4

May

38413382.0

7 19666227.07 35275721.32

26997556.9

9 1.08894675

0.53144639

7

Jun

39968408.8

3 14469651.83 36834199.82

32950665.3

7

1.08508964

6

0.69225766

1

July 33262875.7 6815272.098 29383517.74

27167192.8

1

1.13202496

7

0.90008295

9

Aug

21825158.8

1 3883970.01 17740549.36

15795793.1

9 1.23024143

1.01130965

2

Sept

12703996.0

6 2950256.658 9463849.618

8352899.26

8

1.34237087

1

1.03063127

5

Oct 8899885.90 1854836.904 5654716.21 5002010.51 1.57388727 1.24587136

4 5 8 5

Nov 7419141.86 1639892.46 4219913.831

3278055.00

1

1.75812638

7

1.36951834

3

Dec 6690524.77 2225372.569 4440346.362 3463701.86

1.50675740

7

1.00558646

5

Total

231213562.

9 91156896.09 194085946.9

153303176.

8

1.19129471

5

0.72162188

5

Particulars Actual (2000)

Forecasted

model

Exhibit

5 option

Inventory 1249185

2225372.56

9 1827609

Accounts

Payable 759535

1157298.43

8 1191195

Accounts

receivable 2672729 3715152.2 3715152

Debt outstanding 684102 3463701.86 2957147

Sales 75867480 90900108

9090010

8

COGS 53865911 66993379.6

6699338

0

Inventory days 8.46 12.12 9.96

Receivable days 12.86 14.92 14.92

Payable days 5.15 6.31 6.49

Cash cycle 16.18 20.74 18.39

From the above table we can see that the inventory is expected to decline if the proposal from the

transportation manager is accepted. The inventory is expected to decrease because the purchase

will be required to be made for only one month now, compared to two months previously. As a

result of this the accounts payable is also expected to decrease. All of these will decrease the

level of outstanding debt at the end of 2001.

The proposal will have a good impact on Kota’s short-term debt position as reduced amount of

inventory will reduce the net working capital requirement for the company and eventually the

debt outstanding in all the months from January to December is expected to decrease. Also the

cash cycle is expected to be shortened to 18 days after this proposal is accepted. So this proposal

will have a good impact on short term debt position of Kota fibers.

The decrease in borrowing requirement and debt outstanding makes sense as the proposal

reduces inventory requirements to half, which means that the amount of financing required for

current assets is lesser.

Exhibit 6: Memo from Purchasing Agent

The use of JIT method as proposed by Hibachi Chemicals includes purchase of 35% of one of

the raw materials. The proposal included the reduction of pellets inventory from 60 days

outstanding to 2 to 3 days.

The proposal was calculated in excel sheet and was found to have following positive impact on

the debt outstanding and borrowing of the company.

January February March April May June

Debt Outstanding 1,353,298 2,017,987 5,754,53712,043,361

19,390,528

24,728,089

Debt Outstanding initially

1,146,269 2,962,623 8,767,03117,419,379

26,997,557

32,950,665

July August September October November DecemberDebt Outstanding

21,067,369 12,403,927 5,990,806 2,980,827 1,646,578 1,844,640

Debt Outstanding initially

27,167,193 15,795,793 8,352,899 5,002,011 3,278,055 3,463,702

Total Current

Assets

Inventories

(3)

Total

Current

Liabilities

Note Payable-

Bank (6)

Current

Ratio

Quick

Ratio

Jan 4975358.765 1452009.765 2035130.44 1353297.856

2.44473

7 1.731264

Feb 7219122.884 3177580.884 4357241.09 2017987.213

1.65681

1 0.927546

Mar 12700823.76 6938679.761 10662059.87 5754536.944

1.19121

7 0.540434

Apr 21578653.44 10526916.04 19210779.92 12043361.35 1.12325 0.575288

8

May 30312426.48 11565271.48 27271180.58 19390527.64

1.11151

9 0.687435

Jun 33365082.66 7866325.664 30260342.47 24728088.95

1.10260

1 0.842646

Jul 29283772.99 2836169.388 25373312.02 21067368.77

1.15411

7 1.042339

Aug 19302136.33 1360947.533 15146281.94 12403926.55

1.27438

1 1.184528

Sep 10711655.03 957915.6323 7375929.187 5990805.687

1.45224

5 1.322374

Oct 7308058.487 263009.4868 3948771.776 2980826.654

1.85071

7 1.784111

Nov 5955715.801 176466.4009 2626923.044 1646577.928

2.26718

3 2.200007

Dec 5079974.454 614822.2544 2686484.25 1844640.455

1.89093

8 1.66208

This gives that the average current ratio of the company is upgraded to 1.54 per month. On

January, November and December, the working capital is relatively higher than other months as

well as the overall current ratio is better than the base model. Similar goes with the quick ratio.

The quick ratio is 1.2 and is better than the scenario of improvised transportation model. Also the

interest expense on debt is dropped down drastically by 99.4%. The decrease in debt outstanding

on average is reduced by 28.44% monthly ranging from 21% to 49.8%.

Particulars Actual (2000) Base model HibachiInventory 1249185 2225372.569 614822.3Accounts Payable 759535 1157298.438 1002041Accounts receivable 2672729 3715152.2 3715152Debt outstanding 684102 3463701.86 1844640Sales 75867480 90900108 90900108COGS 53865911 66993379.6 66993380

Inventory days 8.46 12.12 3.35Receivable days 12.86 14.92 14.92Payable days 5.15 6.31 5.46Cash cycle 16.18 20.74 12.81

By accepting Hibachi proposal the inventory level is expected to decline drastically to only IRS

614822.3 from original expectation of IRS 2225372.569. The debt outstanding is also expected

to decline drastically to only IRS 1.8 million from original forecast of IRS 3.46 million. The

decrease in debt outstanding is as a result of decrease in net working capital requirement of the

firm after the implementation of JIT proposal. The decrease in net working capital requirement is

also indicated by decrease in current and quick ratio after implementing JIT proposal. If this

proposal is accepted, cash cycle is expected to decrease to 12.81 days from 20.74 days.

Therefore, it is better to include Hibachi proposal. It is better to go both with the proposal by the

transportation manager and Hibachi proposal simultaneously.

Exhibit 7: Memo from Operation Manager

From the application of this proposal, it is expected that gross profit margin will increase by 2%

to 3% which may be because of reduction in seasonal training and set up cost and increase in

production efficiency. The work force will be more motivated to work and machine break down

will be less frequent. But, if we see the following calculation, the proposal seems vague and

inapplicable. If we convert the monthly sales as percentage of total sales in a year we will get the

following percentage of sales as shown in figure below. To make level production means to have

same percentage of total production every month which will eventually add up to 100%

annually. Now of when we add total sales requirement the product up to July i.e. till the end of

peak sales season, we find 73.21% of sales is made up to July. But when we add up the total

production only 58.33% is produced till the end of July. The strategy of the company is to

produce goods only according to demand and it is mentioned in the case description that

company does not follow overproduce the product as the profit margin is small and carrying cost

will be high. This also means the sales and production amount must be approximately equal. But

if level production strategy is followed, the company will not be able to fulfill the market

demand in time of peak sales due to under production. While on the other hand, company will be

over producing in the time of slack sale from the month of August till December. This will create

imbalance in the demand supply mechanism of the business.

LEVEL PRODUCTION PLAN

J anuary February March April May J une

Sales as percentage of year 2.88% 3.18% 4.89% 9.69% 15.28% 19.35%Production as percentage of year 8.33% 8.33% 8.33% 8.33% 8.33% 8.33%

J uly August September October November December

17.95% 9.43% 5.53% 4.89% 3.89% 3.04%8.33% 8.33% 8.33% 8.33% 8.33% 8.33%

Total sales through J uly 73.21%Total production through J uly 58.33%

Hence, this proposal of level production must be rejected.

Summary of all the Proposals.

Initial Forecast Pondicherry Inventory Hibachi JIT

Debt Balance Summary Debt Balance SummaryDebt Balance

Summary Debt Balance Summary

Jan 01 1,146,269 Jan 01 1,344,093 Jan 01 1,200,185 Jan 01 1,353,298

June 01 32,950,665 June 01 35,809,122 June 01 25,435,575 June 01 24,728,089

Dec 01 3,463,702 Dec 01 3,897,616 Dec 01 2,957,147 Dec 01 1,844,640

The action that can be taken by Pundir

Pundir can take the following steps:

o Reject the proposal from Field sales manager.

o Accept the proposal of Transportation manager

o Reducing raw material inventory by 30 days will reduce peak debt to INR 25

million and ending debt to INR 3 million, respectively, and will also increase the

profitability of the firm by INR 275,202. But the company should be aware of the

dangers of reducing inventory, a reduction from 60 to 30 days, although

significant, still leaves a good margin of safety.

o Accept the proposal of JIT from Hibachi Chemicals.

o Reject the proposal from Operations manager.

o Instead of providing quarterly dividend of INR 500000, the money can be used in the

business to manage the liquidity need. The Pundir family’s belief is not appreciable

regarding the funds of firm. The excess money would play significant role in enhancing

debt position of the company if used wisely rather than just giving out dividends.

Dividends can be taken when the debt position gets stronger after time being.

Only after implementing the strategies mentioned above, the level of debt outstanding can be

reduced to zero by the end of 2001. Which would mean that the company would be able to clear

the line of credit by December 2001.

Recommendations

o The firm should move towards cutting down the cash cycle and increase its liquidity. One of

the way the firm can do this is moving towards receiving their supplies on a JIT basis. This

will tie up less cash in inventory that is sitting in the warehouse. They could also lower credit

terms to receive funds quicker from their buyers. This strategy will lower their cash cycle and

free up cash and have more liquidity on hand. From these plans, company does not have to

purchase more inventory in the first two months since it will use raw material on hand and

order accordingly.

o The company should also request that the note payable be repaid in December of the fiscal

year, not October. This allows Kota fibers time to collect its outstanding receivables from its

peak selling season.

o The company should not provide dividend to its shareholder till all outstanding debt are

settled.

o The company can ask shareholder to invest in the company.

Learnings from the case

o The firm with poor cash management generally has trouble in carrying out day to day

operating activities such as making payments to the tax inspector for the excise tax due

to lack of liquidity in their cash balance. As a result of which, the level of debt increases

to meet the liquidity needs.

o If the firm is unable to manage its working capital, especially cash, then the short term

debt of the firm is going to increase which will have negative impact on the profitability

of the company through increased interest expenses.

o In order to manage the cash effectively and efficiently, the firm should try either to

decrease its inventory days or accounts receivable days or increase its accounts payable

days so that the cash cycle of the firm can be shortened.

o One of the ways a firm can reduce its inventory level is to implement Just in time system.

JIT production strategy strives to improve business return on investment by reducing in

process inventory and associated carrying cost. JIT focuses on continuous improvement

and can improve a manufacturing organization’s return on investment, quality and

efficiency.

Related Documents