Radar Flash – October 8, 2015 Target Price $4.00 52-Week High / Low $1.68 / $3.87 Price Performance Source: Capital IQ and Haywood Securities Current Price $3.31 Shares O/S 131M (basic) Return (incl. dist’n) 21% 151M (F/D) YTD Performance 70% Market Capitalization $433M Dividend / Yield Nil Cash $68M Debt $17 Overall Risk Rating Very High Working Capital $61M Forecast Risk (High) 7 Enterprise Value $390M Financial Risk (Low) 3 YE 2015 (est.) Cash Balance $67M Valuation Risk (Moderate) 4 Daily Volume (3 month average) 363,310 Political Risk (Low) 3 Website www.klondexmines.com Risk Profile Definitions: See page 8 CEO Paul Huet Currency C$ unless noted Member of the Canadian Investor Protection Fund Please see rating structure, disclaimers, and notes on pages 6-9 Klondex Mines Ltd. (KDX-T, $3.31) Rating Buy Tara Hassan, PEng416-507-2603[email protected] Target Price $4.00 Danny Ochoa, PEng, CFA416-507-2427 [email protected] Return 21% Risk Profile High Analyst Certification, Important Information and Legal Disclaimers: See page 6 Midas Exploration Results Highlight Potential that Remains Valuation Our $4.00 target price is based on a blend of 1.0x our Corporate NAV of $1.98/sh (10%) and a 7.5x multiple to 2016 EV/CF (90%). Klondex is currently trading at 1.6x P/NAV and 4.2x EV/2016 CF, compared with North America peers trading at 0.6x P/NAV and 6.1x EV/2016 CF, and global peers trading at 0.6x P/NAV and 5.8x EV/2016 CF. Risks 1) Forecast Risk – Limited operating history as a company; 2) Political Risk – A number of permits are required in 1 to 3 years to continue both operations. Impact – Neutral This morning Klondex provided an update on recent underground and surface drilling at its Midas mine in Nevada. Results continue to highlight the prospectivity of the project, with encouraging results from two known zones and a new style of mineralization intersected. We are encouraged by the results, in particular from the Queen Vein as recent development activities at Midas will allow access to begin silling in this area in the near term. As such, this zone could begin contributing to the mine plan at Midas in a relatively quick fashion if drilling and silling continue to return positive results. At the Trinity Zone, although the results are largely below grade thicknesses normally seen at Midas, we are encouraged by the presence of a new mineralized style at the project. With further exploration the Trinity Zone could present an interesting opportunity for future resource and production growth at Midas, however, we expect it will be a longer term option as Klondex will need to complete significant exploration to better understand the zone, develop the correct geological model, and define resources in this area. Nevertheless, we are interested by the initial results as it drives home the geologic opportunity that remains at Midas. Beyond conversion of existing resources, we do not incorporate resource additions at Midas in our valuation so success in areas like those reported today could contribute positively to our valuation as more drilling is completed. This morning Klondex provided an update on recent underground and surface drilling at its Midas mine in Nevada. The 2015 drill program was designed to test historic vein drill intercepts and expand the existing resource to support the westward and southern districts. Drilling south of the Owyhee fault has revealed a very different style of mineralization than the bonanza veins that have been historically mined at Midas. The new area, called the Trinity Zone, is hosted in a permeable breccia body. Highlights of the results include: Trinity Zone 2.3 g/t AuEq over 35.1 metres in drill hole MUC-02882, 2.5 g/t AuEq over 3.0 metres in drill hole MUC-02773, 2.0 g/t AuEq over 7.9 metres in drill hole MUC-02776.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Radar Flash – October 8, 2015

Target Price $4.00 52-Week High / Low $1.68 / $3.87 Price Performance

Source: Capital IQ and Haywood Securities

Current Price $3.31 Shares O/S 131M (basic) Return (incl. dist’n) 21% 151M (F/D) YTD Performance 70% Market Capitalization $433M Dividend / Yield Nil Cash $68M Debt $17 Overall Risk Rating Very High Working Capital $61M Forecast Risk (High) 7 Enterprise Value $390M Financial Risk (Low) 3 YE 2015 (est.) Cash Balance $67M Valuation Risk (Moderate) 4 Daily Volume (3 month average) 363,310 Political Risk (Low) 3 Website www.klondexmines.com Risk Profile Definitions: See page 8 CEO Paul Huet Currency C$ unless noted

Member of the Canadian Investor Protection Fund

Please see rating structure, disclaimers, and notes on pages 6-9

Klondex Mines Ltd. (KDX-T, $3.31) Rating Buy Tara Hassan, [email protected]

Target Price $4.00 Danny Ochoa, PEng, CFA416-507-2427 [email protected] Return 21% Risk Profile High Analyst Certification, Important Information and Legal Disclaimers: See page 6

Midas Exploration Results Highlight Potential that Remains

Valuation Our $4.00 target price is based on a blend of 1.0x our Corporate NAV of $1.98/sh (10%) and a 7.5x multiple to 2016 EV/CF (90%). Klondex is currently trading at 1.6x P/NAV and 4.2x EV/2016 CF, compared with North America peers trading at 0.6x P/NAV and 6.1x EV/2016 CF, and global peers trading at 0.6x P/NAV and 5.8x EV/2016 CF.

Risks 1) Forecast Risk – Limited operating history as a company; 2) Political Risk – A number of permits are required in 1 to 3 years to continue both operations.

Impact – Neutral This morning Klondex provided an update on recent underground and surface drilling at its Midas mine in Nevada. Results continue to highlight the prospectivity of the project, with encouraging results from two known zones and a new style of mineralization intersected. We are encouraged by the results, in particular from the Queen Vein as recent development activities at Midas will allow access to begin silling in this area in the near term. As such, this zone could begin contributing to the mine plan at Midas in a relatively quick fashion if drilling and silling continue to return positive results. At the Trinity Zone, although the results are largely below grade thicknesses normally seen at Midas, we are encouraged by the presence of a new mineralized style at the project. With further exploration the Trinity Zone could present an interesting opportunity for future resource and production growth at Midas, however, we expect it will be a longer term option as Klondex will need to complete significant exploration to better understand the zone, develop the correct geological model, and define resources in this area. Nevertheless, we are interested by the initial results as it drives home the geologic opportunity that remains at Midas. Beyond conversion of existing resources, we do not incorporate resource additions at Midas in our valuation so success in areas like those reported today could contribute positively to our valuation as more drilling is completed.

This morning Klondex provided an update on recent underground and surface drilling at its Midas mine in Nevada. The 2015 drill program was designed to test historic vein drill intercepts and expand the existing resource to support the westward and southern districts.

Drilling south of the Owyhee fault has revealed a very different style of mineralization than the bonanza veins that have been historically mined at Midas. The new area, called the Trinity Zone, is hosted in a permeable breccia body.

Highlights of the results include:

Trinity Zone

2.3 g/t AuEq over 35.1 metres in drill hole MUC-02882,

2.5 g/t AuEq over 3.0 metres in drill hole MUC-02773,

2.0 g/t AuEq over 7.9 metres in drill hole MUC-02776.

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 2

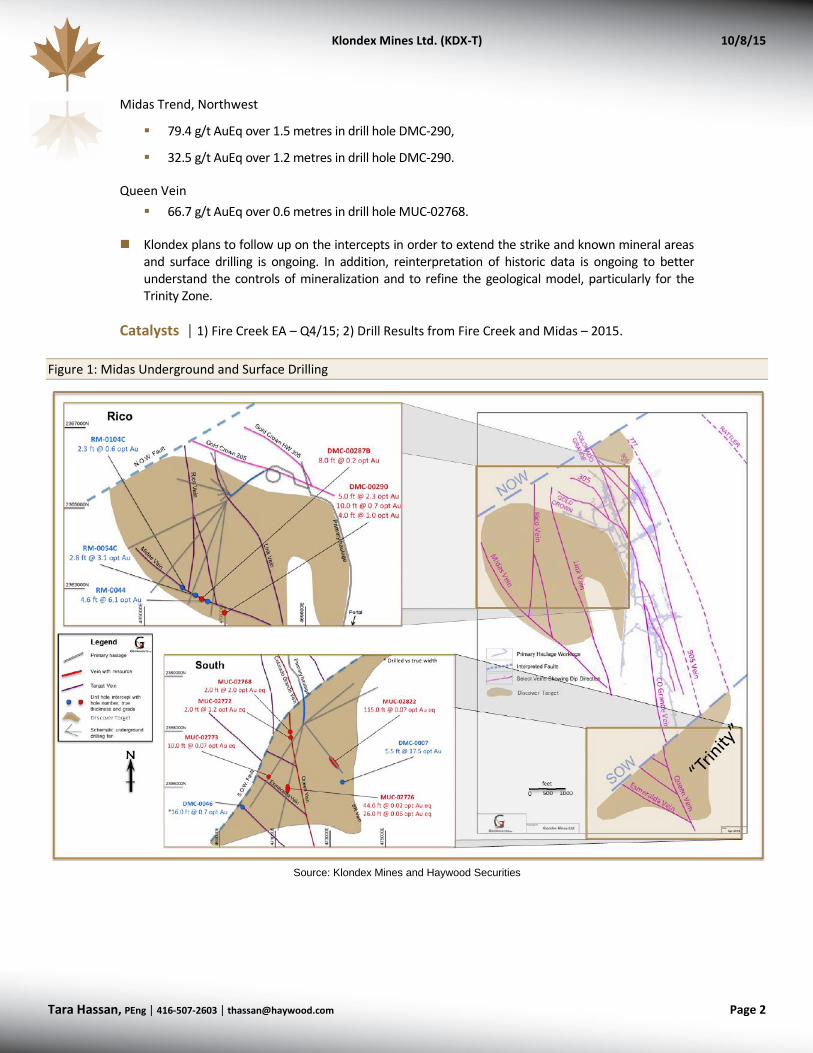

Midas Trend, Northwest

79.4 g/t AuEq over 1.5 metres in drill hole DMC-290,

32.5 g/t AuEq over 1.2 metres in drill hole DMC-290.

Queen Vein

66.7 g/t AuEq over 0.6 metres in drill hole MUC-02768.

Klondex plans to follow up on the intercepts in order to extend the strike and known mineral areas and surface drilling is ongoing. In addition, reinterpretation of historic data is ongoing to better understand the controls of mineralization and to refine the geological model, particularly for the Trinity Zone.

Catalysts 1) Fire Creek EA – Q4/15; 2) Drill Results from Fire Creek and Midas – 2015.

Figure 1: Midas Underground and Surface Drilling

Source: Klondex Mines and Haywood Securities

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 3

Investment Thesis

While the past 3 years have been challenging for gold miners and developers alike, Klondex has used this period to make a number of critical changes that have transformed the Company. What was a high-grade drill-hole story with a fledgling management team as recently as early 2012, has now become a low-cost, multi-asset producer that is positioned to deliver increased production, free cash flow, and resources and reserves over the next 2 to 3 years. This substantial transformation can be linked to an overhaul of the management team and Board of Directors beginning in H2/12 and the strategic acquisition of the Midas mine and mill in Q4/13. While Klondex has outperformed peers in 2015 as investors have rewarded the improvements to the management team and asset portfolio, we believe 2015 will be a pivotal year for Klondex that will help it attract a premium multiple.

Risks

Significant Investment Risks

The investment to which this report relates carries various risks which are reflected in our Overall Risk Rating. We consider the following to be the most significant of these investment risks:

Forecast Risk - Our forecasts are derived from consideration of management guidance, discussions with management, historical performance, and technical reports. Although Klondex’s projects have mine plans or resource estimates that have been published within the past 12 months, we view Forecast Risk to be high given the nature of the orebodies being mined and the stage of mining at the projects. We outline the components of the Forecast Risk as follows:

Operating Risk – At Midas, Klondex has been operating the mine for less than a year and is in the process of implementing new mining methods and improved mining practices to lower dilution. While these efforts appear to be successful in the initial stages, we caution that there is limited actual data to support cost estimates in some cases. Further, portions of the resources are in areas of historical mining, and recoveries or dilution may vary from projections, impacting costs. There is no current National Instrument 43-101 mine plan for Midas and only limited exploration outside active mining areas.

At Fire Creek, the extremely high-grade nature of the mine could result in variance (both positive and negative) from grade projections, which could impact production. With limited mining history at Fire Creek, there is risk that costs could vary as the mine is developed further.

The mine life at Fire Creek is relatively short (4 years remaining), and only limited exploration has been completed outside active mining areas.

Currency and Commodity Risk – Klondex’s currency risk is minimal, as the majority of its operating costs and cash are denominated in U.S. dollars. With the Company reporting in Canadian dollars, results will be impacted by moves in the exchange rate at the time of reporting. As for any gold producer, Klondex is exposed to commodity price risk. Our valuation is based on a flat gold price of US$1,250 per ounce of gold which compares with consensus median estimates of US$1,250 per ounce for both 2015 and 2016.

Financial Risk – Klondex’s medium and long-term expenditure requirements are fully funded through forecasted cash flow from operations. As of June 30, 2015, the Company reported a cash balance of $68 million and outstanding debt of $23 million. Based on our estimates for operating performance and capital requirements, Klondex will not require external funding to continue to develop the Fire Creek and Midas operations. External funding could be required if Klondex pursued a cash acquisition or if it made a discovery that required a significant investment to develop or a shift in priorities.

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 4

Valuation Risk – Our valuation is based on consideration of NAV and cash-flow multiples that are in-line with current trading multiples and below the average of cash-flow based target multiples for Haywood-covered names.

Political Risk – Klondex’s projects are easily accessible and located in mining friendly jurisdictions. Both Midas and Fire Creek have the permits required to maintain operations in the short term, but will require permits beyond 2015 to maintain and grow production. Given Nevada’s history of mining, we expect that the required permits will be received, but note that there is risk of delays that could impact Klondex’s production beyond 2016.

Our Risk Profile Parameters ratings and Overall Risk Rating are set out on the cover page and are explained in our Rating Structure section under “Overall Risk Rating” and “Risk Profile Parameters”. These ratings are an integral part of our Report.

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 5

Source: Klondex Mines, Capital IQ, Bloomberg, and Haywood Estimates

Klondex Mines Ltd.(KDX-T,$3.31) Target Price (C$) 4.00 Mkt. Cap, C$M 433$

Rating: Buy Return (%) 21% CEO Paul Huet

Risk: High 52 Week High/Low (C$) $3.87/$1.68 Company Website

Daily Volume (3-month avg) 363,310

Capital Structure (as of August 2015) Shares PRODUCTION AND CASH COSTSMillions

Shares Outstanding 130.8

Warrants 9.2

Options 10.7

Fully Diluted Shares 150.7

Ownership (as of July 2015) Shares O/S (mln) % O/SSentry Investments 19.8 15.1%

Sun Valley Gold 14.3 10.9%

K2 12.0 9.2%

US Global 11.8 9.0%

Management 7.8 6.0%

HISTORICAL PERFORMANCE

TECHNICAL ASSUMPTIONS2013A 2014A 2015E 2016E 2017E 2018E

Gold (US$/oz) $1,409 $1,266 $1,210 $1,250 $1,250 $1,250

Exchange Rate (Cdn$/US$) 1.03 1.10 1.24 1.24 1.21 1.19

Production Estimates2014A 2015E 2016E 2017E 2017E

Gold Production, 000oz 86 108 119 141 149

GEO Production, 000oz 107 130 141 153 165

Cash Costs, US$/Au sold $478 $478 $504 $549 $600

Cash Costs, US$/AuEqoz sold $649 $654 $620 $604 $663

AISC, US$/Au sold $771 $731 $694 $832 $782

AISC, US$/AuEqoz sold $883 $865 $814 $878 $781

Capex Spending, US$mln $33 $29 $22 $39 $27

Resource Estimate* Tonnes Grade Mine Life EV/oz(as of January 29, 2015 (Mt) (g/t) (Yrs) (US$/oz)Fire Creek (100%) 5

Fire Creek Reserves 0.2 44.1

Fire Creek M&I Resources 0.3 37.7

Fire Creek Inferred Resources 0.8 14.7

Midas (100%) 6Midas Reserves 0.2 13.0

Midas M&I Resources 1.0 12.9

Financial Summary ($mln) Midas Inferred Resources 0.8 9.6

Year-end Dec 31 2013A 2014A 2015E 2016E 2017E Total Reserves & Resources 2.9 15.4 $224

Shares Outstanding, mln 66.2 127.3 130.8 136.3 141.0 Total Haywood Mineable Resource 1.9 16.1

FD Shares, mln 90.4 149.2 149.2 149.2 149.2 *M&I Resources inclusive of Reserves

EPS (0.16) 0.16 0.16 0.14 0.29 NET ASSET VALUECFFOPS (0.05) 0.35 0.43 0.58 0.63 (US$M) (C$M) (C$/Sh) Multiple Adj. (C$/Sh)

P/CF - 7.2x 6.0x 4.4x 4.0x Fire Creek $180 $224 $1.50 1.0x $1.50

Income Statement ($mln) Midas $24 $30 $0.20 1.0x $0.20

Revenue 0.0 121.7 194.7 211.8 226.7 Project NAV $205 $254 $1.70 $1.70

Operating Expenses 0.0 60.0 105.0 104.0 89.8 Net Cash, Corp. Adj. (G&A, Options) $33 $41 $0.27 $0.27

Depreciation 0.1 25.7 37.3 48.4 48.4 Total NAV $238 $295 $1.98 $1.98

General & Admin 1.8 10.0 15.0 15.0 15.0 COMPARABLESGeneral Exploration 0.0 0.0 0.0 0.0 0.0 Company Price EV P/NAV P/CFPS EV/CFPS

Net Income (14.1) 18.3 22.0 20.5 43.7 C$ US$M 2015 2016 2015 2016

Balance Sheet ($mln) Alamos Gold Inc. 5.73 $1,309 0.57x 8.0x 6.3x 9.3x 7.3x

Cash & Equivalents 13.5 52.8 66.7 102.5 138.1 Dundee Precious Metals Inc. 2.23 $360 0.34x 3.2x 3.0x 4.7x 4.5x

Debt 7.0 22.3 18.6 14.6 0.0 Kirkland Lake Gold Inc. 5.95 $401 0.87x 9.2x 5.3x 10.1x 5.8x

Cash Flow ($mln) Primero Mining Corp. 3.74 $552 0.78x 5.3x 3.7x 6.2x 4.4x

Op. CF (before W/C) (4.1) 40.9 55.5 76.4 88.9 Richmont Mines Inc. 4.13 $97 0.74x 7.4x 7.6x 4.7x 4.8x

Financing CF 13.7 121.8 (2.3) 3.5 (6.1) Wesdome Gold Mines Ltd. 1.00 $91 0.67x 9.4x 5.9x 10.0x 6.3x

Investing CF (15.3) (117.5) (44.4) (44.2) (47.2) Selected Company Average 0.66x 7.1x 5.3x 7.5x 5.5x

Change in Cash (4.5) 39.3 13.9 35.8 35.7 Klondex Mines Ltd. 3.31 $321 1.59x 6.0x 4.4x 6.9x 4.2x

SENSITIVITY OF NAV VALUATION SENSITIVITY OF NAV VALUATION TO DISCOUNT RATE

241

1,436

1,008

www.klondexmines.com

Contained Gold(000 oz)

421

416

358

239

92

100

150

200

250

300

350

400

450

-25% -20% -15% -10% -5% 0% 5% 10% 15% 20% 25%

NA

V (

$M

ln)

Percent Change from Base (%)

OPEX CAPEX GOLD PRICE OIL FX:CAD/USD

265

270

275

280

285

290

295

300

305

0% 5% 10% 15%

NA

V (

$M

ln)

Discount Rate (%)

$0$200$400$600$800$1,000$1,200$1,400$1,600

0

50

100

150

200

2014 2015 2016 2017 2018 2019 2020

Pro

du

ctio

n (

Ko

z)

Fire Creek Midas Cash Cost AISC

0

1

2

3

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Oct

-15

Vo

lum

e (0

00

's)

Klondex Mines Ltd. (TSX:KDX)

Price Daily Volume 50-day MA 100-day MA

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 6

Important Information and Legal Disclaimers This report is neither a solicitation for the purchase of securities nor an offer of securities. Our ratings are intended only for clients of Haywood Securities Inc., and those of its wholly owned subsidiary, Haywood Securities (USA) Inc. and such clients are cautioned to consult the respective firm prior to purchasing or selling any security recommended or views contained in this report.

Estimates and projections contained herein, whether or not our own, are based on assumptions that we believe to be reasonable. The information presented, while obtained from sources we believe reliable, is checked but not guaranteed against errors or omissions. Changes in the rates of exchange between currencies may cause the value of your investment to fluctuate. Past performance should not be seen as an indication of future performance. The investments to which this report relates can fluctuate in value and accordingly you are not certain to make a profit on any investment: you could make a loss.

Haywood Securities, or certain of its affiliated companies, may from time to time receive a portion of commissions or other fees derived from the trading or financings conducted by other affiliated companies in the covered security. Haywood analysts are salaried employees who may receive a performance bonus that may be derived, in part, from corporate finance income.

Haywood Securities, Inc., and Haywood Securities (USA) Inc. do have officers in common however, none of those common officers affect or control the ratings given a specific issuer or which issuer will be the subject of Research coverage. In addition, the firm does maintain and enforce written policies and procedures reasonably designed to prevent influence on the activities of affiliated analysts.

Dissemination of Research Research reports are disseminated either through electronic medium or in printed copy. Clients may access reports on our website, or receive publications directly via email. Haywood strives to ensure all clients receive research in a timely manner and at the same time. It is against our policy for analysts to discuss or circulate their recommendations internally prior to public distribution. This policy applies equally to recommendation changes, target changes and/or forecast revisions.

For Canadian residents: Haywood Securities Inc. is a Canadian registered broker-dealer and a member of the Investment Industry Regulatory Organization of Canada, the Toronto Stock Exchange, the Toronto Venture Exchange and the Canadian Investor Protection Fund and accepts responsibility for the dissemination of this report. Any Canadian client that wishes further information on any securities discussed in this report should contact a qualified salesperson of Haywood Securities Inc.

For U.S. residents: This investment research is distributed in the United States, as third party research by Haywood Securities (USA) Inc. Haywood Securities (USA) Inc. is a wholly owned subsidiary of Haywood Securities Inc., registered with the U.S. Securities and Exchange Commission, and is a member of FINRA and the Securities Investor Protection Corporation (SIPC). Haywood Securities (USA) Inc. as a U.S. registered broker-dealer accepts responsibility for this Research Report and its dissemination in the United States. Any U.S. client that wishes further information on any securities discussed in this report or wish to effect a transaction in these securities should contact a qualified salesperson of Haywood Securities (USA) Inc. Haywood Securities Inc. Research Analysts are considered Foreign Research Analysts to the USA and are not registered/qualified as Research Analysts with FINRA. As these analysts are considered Foreign Research Analysts they may not be specifically subject to FINRA (formerly NASD) Rule 2711 and FINRA (formerly NYSE) Rule 472 restrictions on communications with a Subject Company, Public Appearances and trading securities held by a Research Analyst Account.

This report is intended for institutional investors and may only be distributed to non-institutional US clients in the following states: Alaska, Arkansas, Arizona, Colorado, Connecticut, District of Columbia, Delaware, Florida, Georgia, Hawaii, Iowa, Idaho, Illinois # 2, Indiana, Kansas, Louisiana, Massachusetts, Maryland, Maine, Michigan, Minnesota, Missouri, Mississippi, North Carolina, Nebraska, New Jersey, New Mexico, Nevada, New York, Ohio, Oklahoma, Oregon, Pennsylvania, Puerto Rico, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Vermont, Washington, Wisconsin, West Virginia, and Wyoming.

Analyst Certification I, Tara Hassan, hereby certify that the views expressed in this report (which includes the rating assigned to the issuer’s shares as well as the analytical substance and tone of the report) accurately reflect my/our personal views about the subject securities and the issuer. No part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendations.

Important Disclosures Of the companies included in the report the following Important Disclosures apply:

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 7

Haywood Securities, Inc. has reviewed lead projects of Alamos Gold Inc. (AGI-T) and Klondex Mines (KDX-T) and a portion of the expenses for this travel have been reimbursed by the issuer.

Haywood Securities Inc. or one of its subsidiaries has managed or co-managed or participated as selling group in a public offering of securities for Klondex Mines (KDX-T) in the last 12 months.

Other material conflict of interest of the research analyst of which the research analyst or Haywood Securities Inc. knows or has reason to know at the time of publication or at the time of public appearance:

n/a

Rating Structure Each company within an analyst’s universe, or group of companies covered, is assigned: (i) a recommendation or rating, usually BUY, HOLD, or SELL; (ii) a 12 month target price, which represents an analyst’s current assessment of a company’s potential stock price over the next year; (iii) an overall risk rating which represents an analyst’s assessment of the company’s overall investment risk; and (iv) specific risk ratings or risk profile parameters which in their aggregate support an analyst’s overall risk rating. These ratings are more fully explained below. Before acting on our recommendation we caution you to confer with your Haywood investment advisor to determine the suitability of our recommendation for your specific investment objectives, risk tolerance and investment time horizon.

Recommendation Rating BUY –The analyst believes that the security will outperform other companies in their sector on a risk adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) BUY rating.

HOLD – The analyst believes that the security is expected to perform in line with other companies in their sector on a risk adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) HOLD rating.

SELL – Investors are advised to sell the security or hold alternative securities within the sector. Stocks in is expected to under-perform other companies on a risk adjusted basis or for the reasons stated in the research report the analyst believes that the security is deserving of a (continued) SELL rating.

TENDER – The analyst is recommending that investors tender to a specific offering for the company’s stock.

RESEARCH COMMENT – An analyst comment about an issuer event that does not include a rating or recommendation.

UNDER REVIEW – Placing a stock Under Review does not revise the current rating or recommendation of the analyst. A stock will be placed Under Review when the relevant company has a significant material event with further information pending or to be announced. An analyst will place a stock Under Review while he/she awaits sufficient information to re-evaluate the company’s financial situation.

COVERAGE DROPPED – Haywood Securities will no longer cover the issuer. Haywood will provide notice to clients whenever coverage of an issuer is discontinued.

Haywood's focus is to search for undervalued companies which analysts believe may achieve attractive risk-adjusted returns. This research coverage on potentially undervalued companies may result in an outweighed percentage of companies rated as BUY. Management regularly reviews rating and targets in all sectors to ensure fairness and accuracy.

For further information on Haywood Securities’ research dissemination policies, please visit: http://www.haywood.com/research_dissemination.asp

Overall Risk Rating Very High Risk: Venture type companies or more established micro, small, mid or large cap companies whose risk profile parameters and/or lack of liquidity warrant such a designation. These companies are only appropriate for investors who have a very high tolerance for risk and volatility and who are capable of incurring temporary or permanent loss of a very significant portion of their investment capital.

High Risk: Typically micro or small cap companies which have an above average investment risk relative to more established or mid to large cap companies. These companies will generally not form part of the broad senior stock market indices and often will have less liquidity than more established mid and large cap companies. These companies are only appropriate for investors who have a high tolerance for risk and volatility and who are capable of incurring a temporary or permanent loss of a significant loss of their investment capital.

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 8

Medium-High Risk: Typically mid to large cap companies that have a medium to high investment risk. These companies will often form part of the broader senior stock market indices or sector specific indices. These companies are only appropriate for investors who have a medium to high tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital

Moderate Risk: Large to very large cap companies with established earnings who have a track record of lower volatility when compared against the broad senior stock market indices. These companies are only appropriate for investors who have a medium tolerance for risk and volatility and who are prepared to accept general stock market risk including the risk of a temporary or permanent loss of some of their investment capital.

Risk Profile Parameters – Mining and Minerals Sector Forecast Risk: High (7-10) – The Company's primary project(s) is at an earlier stage of exploration and/or resource delineation whereby grades, tonnages, capital and operating costs, and other economic/operational parameters are not yet reliably established. Moderate (4-6) – The Company has taken steps to de-risk its primary producing, or soon to be producing project(s) and has established reasonably reliable operational and economic parameters. Low (1-3) – The Company has de-risked the majority of its primary project(s) through operational history and established production profile(s).

Financial Risk: High (7-10) – The Company’s near- and medium-term (capital) expenditure considerations, including the current year or next forecast year, are not fully funded through a combination of established debt facilities, cash on hand, and/or anticipated cash flow from existing operations—successful project execution depends, in part, on future (equity) financing(s). Existing and/or forecast levels of leverage are above average relative to the Company's peer group. The risk of a significant capital cost overrun(s) is high given the early stage of project development. Moderate (4-6) – The Company's near-term (capital) expenditure program, in the current year or next forecast year, is fully funded through a combination of established debt facilities, cash on hand, and/or anticipated cash flow from existing operations. Medium-term funding requirements will likely require additional financing consideration, but should be achievable assuming no significant uncontrollable events impede access to capital. Existing and/or forecast levels of leverage are in-line with the Company's peer group. The risk of a significant capital cost overrun(s) is moderate given the advanced stage of project development. Low (1-3) – the Company's near- and medium-term (capital) expenditure program is fully funded through a combination of established debt facilities, cash on hand, and/or anticipated cash flow from existing operations. Existing and/or forecast levels of leverage are below average relative to the Company's peer group.

Valuation Risk: High (7-10) – The current valuation is at a premium to peers. The valuation reflects considerable future exploration success and/or commodity appreciation. Where applicable, the current capitalization exceeds the “DCF” evaluation by more than 50%. Moderate (4-6) – The current valuation is within historic ranges and generally consistent with peers. The valuation reflects reasonable exploration success and/or commodity appreciation. Where applicable, the current capitalization exceeds the DCF valuation by 15% to 50%. Low (1-3) – The current valuation is at the low end of historic ranges and at a discount to peer valuations. The valuation reflects limited new exploration success and no commodity appreciation. Where applicable, the current capitalization exceeds the DCF valuation by less than 15% or falls below the current market value.

Political Risk: High (7-10) –Obtaining permits is challenging. Properties are located in an area(s) with high geo-political uncertainty, limited access, and/or have significant new infrastructure requirements. Moderate (4-6) – Properties are located in an area(s) with moderate geo-political risk, reasonable or manageable access, and some established infrastructure. Low (1-3) – Properties are located in areas with a manageable geo-political risk profile and established access/infrastructure.

Klondex Mines Ltd. (KDX-T) 10/8/15

Tara Hassan, PEng416-507-2603 [email protected] Page 9

Distribution of Ratings (as of October 8, 2015)

Distribution of Ratings IB

Clients

% # (TTM)

Buy 65.4% 70 93.8%

Hold 11.2% 12 0.0%

Sell 1.9% 2 0.0%

Tender 0.0% 0 0.0%

UR (Buy) 3.7% 4 6.3%

UR (Hold) 0.0% 0 0.0%

UR (Sell) 0.0% 0 0.0%

dropped (TTM) 17.8% 19 0.0%

Price Chart, Rating and Target Price History (as of October 8, 2015)

B: Buy; H: Hold; S: Sell; T: Tender; UR: Under Review Source: Capital IQ and Haywood Securities

Klondex Mines Ltd. (KDX-T) Date Target(C$) Rating7/15/15 $4.00 Buy1/22/15 $3.50 Buy

Initiated Coverage 01/22/15

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Oct12

Jan13

Apr13

Jul13

Oct13

Jan14

Apr14

Jul14

Oct14

Jan15

Apr15

Jul15

Price History (C$) Target/Rating/Coverage Change

Related Documents