1 Key words: international taxation, digital economy, digital services and products, global income, multinationals, tax policy. Abstract: In the Action Plan on Base Erosion and Profit Shifting (BEPS) the OECD set out to answer two fundamental questions related to the digital economy: “How enterprises in the digital economy add value and make their profits?” and “How the digital economy relates to the concepts of source and residence or the characterisation of income for tax purposes?” In the Final Report on the BEPS Project, the OECD did not directly answer either of these questions but raised a new one: “How taxing rights on income generated from cross-border activities in the digital age should be allocated among countries?” The question remained unanswered, mainly because the problem goes far beyond the issues related to BEPS as defined by the OECD. The paper seeks to the further discussion about the allocation of the rights to tax income earned from production and distribution of global digital services. Under the current model that guides states in relation to taxation of income from cross-border activities, it is impossible to allocate income from global digital services to only one state or to provide a basis for the taxation of this income in a market state. The allocation of income from global digital services, it is argued, requires global tax policy that would co-ordinate states in the digital era.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Key words: international taxation, digital economy, digital services and products, global income,

multinationals,taxpolicy.

Abstract:

In the Action Plan on Base Erosion and Profit Shifting(BEPS) the OECD set out to answer two

fundamentalquestionsrelatedtothedigitaleconomy:“Howenterprisesinthedigitaleconomyadd

valueandmaketheirprofits?”and“Howthedigitaleconomyrelatestotheconceptsofsourceand

residenceorthecharacterisationofincomefortaxpurposes?”

IntheFinalReportontheBEPSProject,theOECDdidnotdirectlyanswereitherofthesequestions

but raisedanewone: “Howtaxing rights on incomegenerated fromcross-borderactivities in the

digital age should be allocated among countries?” The question remained unanswered, mainly

becausetheproblemgoesfarbeyondtheissuesrelatedtoBEPSasdefinedbytheOECD.

Thepaperseeksto the furtherdiscussionabout theallocationof therightsto tax incomeearned

from production and distribution of global digital services. Under the current model that guides

states in relation to taxation of income from cross-border activities, it is impossible to allocate

income fromglobal digital services to only onestateor to providea basis for the taxationof this

incomeinamarketstate.Theallocationofincomefromglobaldigitalservices,itisargued,requires

globaltaxpolicythatwouldco-ordinatestatesinthedigitalera.

2

(Not)AddressingtheTaxChallengesoftheDigitalEconomy:AResponsetoAction1ofthe2015

FinalReportoftheOECD/G20BaseErosionandProfitShiftingProject1

VictoriaPlekhanova2

[The] ability to maintain some level of business connection within a

country without being subject to tax on business profits earned from

sources within that country is the result of particular policy choices

reflected indomesticlawsandrelevantdoubletaxtreaties,and isnot in

andofitselfaBEPSissue.3

1 Introduction

The “digital economy” is an umbrella term used to describe markets that focus on digital

technologies and typically involve the tradingof information goodsor services throughelectronic

commerce.4Thedigitaleconomyisthepartoftheglobaleconomythatisthemostintegrated.

TheActionPlanonBaseErosionandProfitShifting(BEPS)hassetout toanswertwo fundamental

questions related to the digital economy:“howenterprises in the digital economyadd value and

maketheirprofits”and“howthedigitaleconomyrelatestotheconceptsofsourceandresidenceor

thecharacterisationofincomefortaxpurposes.”5

However, the final outcome in terms of answering the above two questions in relation to direct

taxation in the digital economy was quite modest considering the time spent and resources

involved.The“outofthebox”thinkingpromiseddidnotoccur.6

In its Final Report, the Task Force on the Digital Economy (TFDE), a subsidiary body of the OECD

CommitteeonFiscalAffairs,inwhichnon-OECDG20countriesparticipateasAssociatesonanequal

footingwith OECD countries, agreed to proposemodifications to the definition of and the list of

exceptions to the definition of permanent establishment (PE), revised the guidance on transfer

1 ThepaperisapartofthePhDproject.TheauthorisverygratefultoProfessorCraigElliffeandAssociate

ProfessorChrisNoonan(FacultyofLaw,UniversityofAuckland)forvaluablecomments.2 PhDStudent,FacultyofLaw,UniversityofAuckland.3 OECD, “Addressing the Tax Challenges of the Digital Economy”,Action 1: 2015 Final Report, OECD/G20

BaseErosionandProfitShiftingProject(5October2015)79(hereinafterthe“TFDEFinalReport”).4 OECD,“TheDigitalEconomy”,ReportofHearingsontheDigitalEconomy(7February2013)5.5 OECD,“ActionPlanonBaseErosionandProfitShifting(BEPS)”,BEPSReport(19July2013)10.6 “TheOECDiscommittedtodeliveringaglobalandcomprehensiveactionplanbasedonin-depthanalysis

oftheidentifiedpressureareaswithaviewtoprovideconcretesolutionstorealigninternationalstandardswiththecurrentglobalbusinessenvironment.Thiswillrequiresome“outofthebox”thinkingaswellasambition and pragmatism to overcome implementation difficulties, such as the existence of current taxtreaties.”SeeOECD,“AddressingBaseErosionandProfitShifting”,BEPSReport(12February2013)9.

3

pricing,andmadesomerecommendationsonthedesignofcontrolledforeigncompany(CFC)rules.7

TherecommendationsoftheBEPSprojectcontainedintheTFDEFinalReportcreate(orconfirm)the

possibilityforstatestotax incomefromactivitiesthatincludetheproductionandsalesoftangible

products in their territories. However, the related issue of the taxation of income from digital

servicesandproductsthroughaccesstowebplatformsremainsunresolved.

Inotherwords, following theTFDE’sproposalsamarket statemayget theopportunity to tax the

income of Amazon and Apple from sales of tangible products to consumers located within its

territory under the modified definition of a PE. On the other hand, income from sales of digital

products, like digital books and apps, anddigital services to the same consumerswill escape the

allocationtoaPEinamarketstate.

The impact of the TFDE’s proposals on Google and Facebook – major suppliers of Internet

advertisingandcollectorsofpersonaldata–islikelytobeinsignificantfromtheperspectiveofmany

marketstates.SomestatesmaytrytousethemodifiedPEconcept.However,itisunlikelythatthese

statescangetsignificantadditional tax revenueswithoutapplyingsignificanteconomicorpolitical

pressure tomultinational suppliers of digital services and products and, therefore, force them to

createa localPEandallocateaportionofglobal incomeearnedona localmarketthisPE.8 States

can introduce a new direct tax,9 re-place10 or re-shape a corporate income tax11 to avoid the

7 TFDEFinalReportat12.8 For instance, under the Budget Law for 2014 Italian taxpayers can buy online advertising services and

sponsored links only from suppliers registered for VAT purposes in Italy. See Luigi Quaratino, “Newprovisionsregardingthetaxationofthedigitaleconomy”(2014)54(5)EuropeanTaxation211,211-217.

InChinae-commerceplatformsneedtoberegisteredand licensedtogetaccess to theChinese Internetspace and for the processing of payments. See Sophie Ashley, “The digital economy is creating a PEconundrum,taxreview”(2013)24(6)InternationalTaxReview34,34.

9 For instance, the UK has introduced the Diverted Profits Tax (DPT) on a company’s “taxable divertedprofits”whichwouldotherwisenotbesubjecttotaxintheUKatall,atleastinthecaseofbusinessprofitsthat could not be attributed to a permanent establishment. Australia also supported the idea of thedivertedprofitstax.SeeCraigElliffe,“Thelesseroftwoevils:doubletaxtreatyoverrideortreatyabuse?”[2016]1theBritishTaxReview(forthcoming).

SeealsoproposalsforataxononlineadvertisingandataxonelectroniccommerceinMinistryofFinanceofFrance,Rapportsurlafiscalitédusecteurnumérique(theColinandCollinReport)(18January2013)67,121-128 <http://www.redressement-productif.gouv.fr/files/rapport-fiscalite-du-numerique_2013.pdf>accessed15July2013.

10 Forinstance,acorporatetaxcanbereplacedbyanindirecttax.SeeReuvenAvi-Yonah,“Fromincometoconsumptiontax:someinternationalimplications”(1996)33SanDiegoLawReview1329,1332-1339;AlanAuerbach,“TheFutureofCapitalIncomeTaxation”FiscalStudies(2006)27InstituteforFiscalStudies399,414; Alan Auerbach, Michael Devereux and Helen Simpson, “Taxing Corporate Income” (2008) NBERWorking Paper14494, 47-50 and 54; Martin Sullivan, Corporate Tax Reform: Taxing Profits in the 21stCentury(S.l.Apress2011)135,139.

4

limitations on the right to tax imposed by double tax treaties. States also can “play” with some

limitationstostretchanationaltaxbase.12

TheTFDEFinalReportsupportsopportunisticbehaviourofstates.Byintroducinganyofthesenew

optionssomestatescouldbringwithin their tax jurisdictionsomeof the incomeofmultinationals

operatinginthedigitaleconomy.13Theseoptionscanbepursuedundernationallawwheretheyare

compatiblewith the existing international legal commitments of the states concerned.14With the

trend towards double tax treaty override already evident,15 the proposals of the TFDEwill surely

contributetothegrowthofthistrend.

It appears that for those stateswho are not “on trend”, the total impact of theBEPS project on

multinationals that supply digital services and products to customers in market states over the

Internet,iftherecommendationsareimplemented,wouldbeanobligationtoannuallyreporttheir

incomeearnedineachstateafter2016.Reportsshouldbefiledinlocaltaxadministrationsandalso

in the jurisdiction of tax residence of the ultimate parent entity of a multinational firm.16 The

reportingwill leavemost statesmerelywith knowledge that increases sorrow,17 butwithout real

opportunities to impose a corporate tax on income generated from the remote supply of digital

servicesandproductsand/ortocollecttaxrevenuesfromtheimposedtax.

ThetaxationofincomeearnedbyGoogleinNewZealandillustratesboththeproblemthattheTFDE

failed todealwith and thenegative impactof this problemfor individuals.Google doesnot have

data centres inNewZealand anddoes not report on its income from Internetadvertising inNew

Zealand.ThetotalInternetadvertisingspendinNewZealandin2014wasestimatedatNZD589.32

11 Inparticular,astatecantransformastandardcorporateincometaxfromtraditionalsource-basedtaxinto

thedestination-based tax. SeeAlanAuerbach,MichaelDevereux andHelen Simpson, “TaxingCorporateIncome”(2008)NBERWorkingPaper14494,52-53.Inthiscasethesupplyapproachofthecurrentmodelof theallocationof rights to taxwillbe implicitly replacedby thedemandapproach thatseesaplaceofsalesasakeyvaluecreatingfactor.

12 For instance, Brazil usually classifies services of non-residents either as technical or administrativeassistance that are subject to a withholding tax in Brazil. See Sergio Andre Rocha, “Brazil report” inEnterpriseServices,97AIFACahiers(InternationalBureauofFiscalDocumentation2012)158.

13 TFDEFinalReportat13andChapter9oftheTFDEFinalReport.14 TFDEFinalReportat13.15 Formoredetail seeCraigElliffe,“TheLesserofTwoEvils:DoubleTaxTreatyOverrideorTreatyAbuse?”

[2016]1theBritishTaxReview(forthcoming).16 OECD,“TransferPricingDocumentationandCountry-by-CountryReporting”,Action13:2015FinalReport,

OECD/G20BaseErosionandProfitShiftingProject(5October2015)9-10.17 “For inmuchwisdomismuchvexation,andhewho increasesknowledge increasessorrow”:Ecclesiastes

1:18.

5

million,18 at least a half of which was probably spent on Google advertising services. With the

assumption that net income of Google in 2014 was about 22.5 % of its gross income,19 Google

earnedatleastNZD60millionfromInternetadvertising inNewZealandin2014.However,Google

doesnotpayanytaxonthisincomeinNewZealand.In2014GoogledeclaredNZD522,641asitsnet

incomeinNewZealand,20andpaidatotalofNZD361,665inincometax.21

GoogleisincorporatedintheUS.22On5October2015NewZealandfinalisedthenegotiationofthe

Trans-Pacific Partnership (TPP) with the US and other eleven states. When this mega-regional

agreementcomesintoforce,the rightofNewZealand,aswellasotherparticipantsof theTPP,to

require Google to use or locate computing facilities in its territory as a condition for conducting

business in New Zealand will be limited.23 Moreover, the TPP imposes on its participants an

obligation to develop and maintain national legislation governing electronic transactions and to

promoteelectroniccommerce.24

Between2013-2014thetaxratioincreaseinNewZealandwas1.0percentagepoint.“About80%of

theincreaseinrevenue[ofOECDcountries]between2013and2014istheresultofrisingrevenues

fromacombinationofconsumptiontaxesandtaxesonpersonalincomeandprofits”.25Bycontrast,

corporate tax revenues have been falling across OECD countries since the global economic crisis,

shifting the taxburdenonto individual taxpayers. “Average revenues fromcorporate incomesand

gains fell from 3.6% to 2.8% of gross domestic product (GDP)over the 2007-14 period. Revenues

fromindividualincometaxgrewfrom8.8%to8.9%andVATrevenuesgrewfrom6.5%to6.8%over

18 IABNZandPwCOnlineAdSpendReports<http://www.iab.org.nz/resources/online_ad_spend/>accessed

19August2015.19Basedonthe information inGoogle,TheAnnualReportPursuanttoSection13or15(d)oftheSecurities

Exchange Act of 1934 (form 10-K) for the fiscal year ended 31 December2014, 33<http://investor.google.com/earnings.html>accessed19August2015.

20 GoogleearnedNZD521,735 from sales,marketingandR&D services, andNZD1,151 from services as apaymentcollectionagent.

21 Google New Zealand Ltd., Financial Statements for the year ended 31 December 2014<https://www.business.govt.nz/companies/app/service/services/documents/23411216F0B792CE4D05DD4225577957> accessed 16 August 2015; Google Payment New Zealand Ltd., Financial Statements for theyear ended 31 December 2014 <https://www.business.govt.nz/companies/app/service/services/documents/B18889364E802EA16AE2547C0BD08296>accessed16August2015.

22 FourthAmendedandRestatedCertificateof IncorporationofGoogle Inc.Retrieved25March2013 from<http://investor.google.com/corporate/certificate-of-incorporation.html> 25 March 2013; see also<www.google.com/about/company/history/> and <www.google.com/about/company/facts/locations/>accessed11April2013.

23 Article14.13(2)oftheTrans-PacificPartnership(Atlanta,5October2015)(hereinafter“theTPP”).24SeeArticles14.5and14.15oftheTPP.25 OECD,RevenueStatistics2015(3December2015)14.

6

thesameperiod”.26Thedifficultyofmarketstatesbeingabletotaxmultinationalsoperatinginthe

digitaleconomyhassubstantiallycontributedtothisshiftinthetaxburden.

However,theanalysisofthetaxproblemsassociatedwiththedigitaleconomymadebytheTFDEin

a frameworkof theBEPSprojectwas artificially limited by the definitionof thebase erosion and

profitshiftingproblem.Therefore,whenitcomestothetaxationofmultinationalsoperatinginthe

digital economy, the outcome of the BEPS project is rather tricky, especially for states providing

accesstotheirmarketsforremotelysupplieddigitalservicesandproducts.

First,ifastatehasacorporateincometaxandprovidesaccesstoitsmarketsfordigitalservicesand

products of foreign suppliers, but cannot impose income tax on this income because of the

limitations on its tax jurisdiction imposed by international law and treaties, the base erosion

probleminthisstatedoesnotexist.Inthiscasethestateprovidingaccesstoitsmarkethasno‘right’

to consider the activity of the foreign supplier as creating corporate income tax base within the

state’sborders.

FromtheviewpointoftheTFDEFinalReportthebaseerosionproblemalsodoesnotoccurinacase

whereastatecannoteffectivelyexercise its sovereignrighttotax incomeofforeignsuppliersand

collect taxes imposed on income of these suppliers. This situation is common where income is

earned from the supply of digital services and products to a market state over the Internet.

However, this situationdiffers from theprevious onewhen the rightofa state to imposea tax is

limited.Ataxbaseinrelationtoaparticulartaxoriginateswithanintroductionofthetaxbynational

tax law. If the tax imposed is not paid and tax revenues cannot be collected by a state through

enforcementoftaxclaims,ataxbaserelatedtothetaxiseroded.

Second, the TFDEFinalReport suggestsmeasures toputanend to thephenomenonof“stateless

income”but does not clarify the concept of stateless income.27 In general, incomeearned in the

digitaleconomycanbedescribedas“stateless”becausetherighttotaxthisincomeis limited,has

not been exercised or does not exist. The right to tax can be limited under national law or the

international lawobligationsofa particular state.ThePEconcept is anexampleof this limitation.

TheTFDEFinalReportdealsonlywithstateless incomethat is theresultoftheartificialuseofthe

limitationsimposedbydoubletaxtreaties.

26 OECD, “Corporate Tax Revenues Falling, Putting Higher Burdens on Individuals”

www.oecd.org/tax/corporate-tax-revenues-falling-putting-higher-burdens-on-individuals.htm accessed 7December2015.

27TFDEFinalReportat12,82,84,146.

7

However,theothertwocasesofstatelessincome(whentherighttotaxisnotexercisedordoesnot

exist) fallwithin the scopeof theBEPSproject. In particular, the fact that some statesdonot tax

incomeand,therefore,provideshelterfortheforeigncapitalofmultinationalfirmsthatarethereby

abletoavoidtaxationifthestateoftheirultimateparentcompany(inotherwords,thehomestate

ofamultinationalfirm)doesnottaxcorporateincomeonaworldwidebasis.Thethirdcaseisrather

futuristic,butnotbeyondtherealmsofpossibility:

TheU.S. Patent and TrademarkOffice grantedGoogle’s patent on awater-based data center on

April28,2009.Thedatacenterwouldbemadeupofserversinsidecontainers likethosenormally

usedforthecarriageofgoodsbyseaorrail.Craneswouldplacethesecontainersonshipsorbarges.

Thecontainerswould be linked together to form largedata centers thatwouldbe locatedat sea

wherever necessary. Ocean waves, tides, or currents would supply power to these floating data

centers,andpumpingthesurroundingwaterthroughanonboardsystemwouldcoolthem.28

This type of technological development may have a direct impact on the taxation of corporate

incomeifthecurrentmodeloftheallocationoftaxingrightsisappliedtosuppliersofdigitalservices

andproducts.Therightchoiceofthehomestatefortheparentcompanyofamultinationalgroup,

withthesourceofincomelocatedinaplacethatisnotsubjecttosovereignrightsofanyparticular

state,mightbetheultimatetaxminimisationstrategy.29TheCFCrulesasatoolforanextensionofa

taxjurisdictionmightnotbehelpfulorfairwhentheextensioncoversa“sovereignfreezone”.

Third,theTFDEFinalReportandotherdocumentsdevelopedintheframeworkoftheBEPSproject

refertotheBEPSproblem.However, there isnotasingleBEPSproblemfacedbyallstates.States

notonly face differentBEPSproblems, but also evaluate them from their individual state-centred

perspectives.Forexample,taxplanningmadebythesamefirmcanerodethecorporateincometax

baseofonestate,butcontributeto increasingofthe taxbasesofanother state.Taxbasesof the

second state might be related to other types of taxes. In the case of Google30 and other

multinationalsthathavechosenBermudaasashelterfortheircapital,Bermudadoesnotimposetax

onincomeandprimarilyreliesonpayrolltaxesandtaxesonconsumption.31ThefactthatBermuda

28 Steven R. Swanson, “Google Sets Sail: Ocean-Based Server Farms and International Law” (2011) 43

ConnecticutLawReview709at716-717.29 For instance,rescommunisarenotsubjectof jurisdictionofaparticularstate.Therescommunis include

highseas, togetherwithexclusiveeconomiczones,andouterspace.SeeMalcolmN.Shaw, InternationalLaw (6thedn,CambridgeUniversityPress2008)492; IanBrownlie,PrinciplesofPublic International Law(5thedn,ClarendonPress1998)105,173-175.

30 ForanoverviewofthetaxplanningschemeofGoogleseeTFDEFinalReportat171-175.31 GovernmentofBermuda,Ministryof Finance,Budget Statement in Supportof theEstimatesofRevenue

and Expenditure 2015-2016, 11-12, 32 <https://oba.bm/256381811_Bermuda_2015_2016_Budget.pdf>accessed24August2015.

8

has no taxon incomeattracts foreign capitalandmaintains its key nationalexport industry– the

provision of services for international business. Therefore, the income tax-free environment

becomesanationalresourcethatstimulatesnationaleconomicgrowthofBermudaandincreasesits

tax base related to payroll and consumption taxes. TheBEPSproblemsof other states that occur

becauseofforeigncapitalisshelteredinBermudaareina“blindspot”forBermuda,becauseitdoes

nothaveacorporateincometaxbasethatcanbeerodedbecauseoftheactivitiesofGoogle.

TheBEPSfocusedanalysisoftheTFDEFinalReport,withitsverynarrowdefinitionofabaseerosion

andprofitshiftingproblemandastate-centeredviewoftheproblem,haslefttaxpolicymakerswith

the intuitive feeling that something is not right in thedigital economy,where the “something” is

describedbythevaguephrase“broadertaxchallenges”.32

The TFDE Final Report, as noted above, distinguishes two general groupsof tax challenges in the

digitaleconomy:thebaseerosionandprofitshiftingproblemandthequestionoftheallocationof

taxingrightsinthedigitaleconomy.

WhiletheReportmakessomeproposalsrelatedtotheBEPSproblemsingeneral,33withrespectto

theallocationoftaxingrightsinthedigitaleconomytheReportoffersnorealassistance:

Thedigital economy triggers systemicquestionsabout theability of the currentdomesticand

international tax systems to dealwith the changes brought about byadvances in information

and communication technology (ICT). These tax policy issues have implications for the overall

designoftaxsystems.ThesechallengesmaythereforehavebroaderimplicationsthanBEPSand

thecountermeasuresdevelopedinthecourseoftheProject.Theseincludeissuesrelatedtothe

allocationoftaxingrightsamongcountriesaswellastothetaxpolicyconsiderationsthatshould

betakenintoaccountwhenweighingtherelativecostsandbenefitsofthevarioustaxsolutions.

Withrespecttodirecttaxes,thebroadertaxchallengesraisedbythedigitaleconomygobeyond

thequestionofhowtoputanendtodoublenon-taxation,andchieflyrelatetothequestionof

howtaxingrightsonincomegeneratedfromcross-borderactivitiesinthedigitalageshouldbe

allocatedamongcountries.34

The TFDE, therefore, admits that the current problem with tax policy for the digital economy is

structural.However,what ismissed is that theproblem cannotbeunderstood froman individual

state-centred perspective and, therefore, cannot be resolved by unilateral changes in national or

internationaltaxpolicy.Abilateralco-operationofstatesunderdoubletaxtreaties isalsonotvery

32 TFDEFinalReportat13.33 Seefootnote13.34 TFDEFinalReportat132,para340.

9

helpful because it does not consider interests of all states that can be potentially affected by a

decisionbetweentwostates.

Whenviewed fromaglobalperspective theproblem is self-evidently the lackoffair,efficientand

effective global tax environment that is coherent with the global economic and technical

environment known as the digital economy. The problem affects not only states but also

multinationalfirmsthatuse theInternetasameanofproductionanddistributionofglobaldigital

servicesandproducts.

In an unfair, inefficient and ineffective global tax environment, opportunism by both states and

multinationalsseemsarelativelypredictable,ifnotreasonable,responsetothecircumstances.

The Paper aims to start a discussion related to creation of fair, efficient and effective global tax

environmentthatwouldbenefitallstatesandmultinationals.

Part2ofthepaperprovidesanexampleofabusinessmodelthatincludesadvertisingwebplatforms

as a part of the process of production of global digital services.Digital services andproducts are

globalwhentheyareproducedonandsuppliedovertheglobalelectronicnetworktomanymarket

states.

Thevaluecreatedbytheseplatformsisanalysedunderthetraditionalvaluechainanalysisappliedto

the digital economy. It is suggested that the value chain in the process of production of digital

services has an additional layer not present in other goods and services, namely: the global

economicandtechnicalinfrastructure:anintegratedglobaleconomicsystemmadeofopennational

economiesandtechnicalinfrastructureinterconnectedintoaglobalelectronicnetwork.Theanalysis

alsoexplainsthemultisidedmarketstructureofthosebusinessmodelsinthedigitaleconomythat

includeadvertisingwebplatforms.

Part3explainshowthecontemporarymodelfor theallocationofrightstotax incomefromcross-

borderactivitiesfoundinTaxTreatyModelConventions35isnotcompatiblewiththeglobalprocess

ofproductionofwebplatformoperators.Theanalysisofthreegeneralassumptionsthatunderpin

this allocation model demonstrates its non-applicability to economic activities that involve

35 OECDModelTaxConventiononIncomeandonCapital:CondensedVersion(9thedn,Paris,15July2014);

theUNModelDoubleTaxationConventionbetweenDevelopedandDevelopingCountries (2011update,NewYork,9-10June2011);theUSModel IncomeTaxConvention(Washington,15November2006);theModel Tax Treaty with Russian Federation for prevention of Double Taxation and Tax Avoidance withRespect to Taxes on Income and Property (Moscow, 24 February 2010); the Intra-ASEANModel DoubleTaxation Convention (Manila, 15December 1987). The paper primarily focuses on theOECDModel TaxConventiononIncomeandonCapital.

10

interactionwith awebplatformasan elementof aprocessof production.Abusinessmodel that

includesanadvertisingwebplatformisusedastheexample.

Part4describestheglobaldistributionalconflictarsingfromtheuseoftheaforementionedbusiness

model. This part discusses the interdependence of states and also of states and multinationals,

whichisakeycircumstancesurroundingtheconflictalongwiththecurrentlevelofglobalisationand

technologicaldevelopment.

Therighttotaxapersonorentityistraditionallylinkedwithpublicservicesprovidedtothatperson

orentity.This isalmost seenasaxiomaticandisappliedatbothnationaland international levels.

With theaimof identifying theprovidersofpublic services in thedigitaleconomy,Part5 deploys

systemstheory.Analysingtheoriginofthedigitaleconomyandthestructureofinteractionsinthis

economybetweenstatesandalsobetweentheworldcommunityofstatesandmultinationals,Part

5concludesthatstatesactingastheworldcommunitycreateglobalpublicservices:globaleconomic

and technical infrastructure. While this infrastructure is a part of the value creation chain of

multinationals that produce global digital services and products on and supply them over the

Internet worldwide, the input of each of the members of the world community of states into

productionoftheseservicesandproductsisnotpresentlyadequatelypaidforbystatetaxes.

Part6discussesthebasisofpotentialmultilateralco-operationthatwouldresolvethedistributional

conflictdescribedinPart4inamannerthatwouldsatisfybothstatesandmultinationals.

Part 7 suggests principles for multilateral co-operation that would guarantee that all income is

taxed,buttaxedonlyonce;thetotaltaxburdenformultinationalsisreasonable;andglobalincome

apportionedinamannerthatcorrespondstopublicservices(nationalandglobal)providedbyeach

state.

Part8discussesinstitutionalarrangementsnecessaryfortheimplementationofprinciplessuggested

inPart7.

2 GlobalProcessofProductionintheDigitalEconomy

a.ValueChain

Fromthe traditionalperspective, at least in the taxworld,basedon the traditional valuecreation

analysis,aproductionprocessmightbeviewedasglobalwhenafirmcreatesoracquiresinputsfor

productionofafinalproductinterritoriesofmanystates.

Thevaluecreationcanbepresentedasthelinearprocessoftransforminginputsintooutputswhere

thedifferencebetweenincomefromsellingofthefinaloutputandcostsforacquiringandcreation

11

ofinputsconstitutesprofitofthefirm.36

Thegenericvaluechainconsistsofvaluecreatingactivities(“buildingblocks”thatareusedforthe

creationaproduct)andmargins (thedifferencebetween the totalvalueand thecollectivecostof

performingvaluecreatingactivities).37Valuecreatingactivitiesaredividedintotwogroups:primary

activitiesandsupportactivities.Primaryactivitiesarethosethatdirectly result inacreationofthe

productanditssale,whereassupportactivitiesimprovetheperformanceofprimaryactivities.38

Diagram1.GenericValueChain39

Traditional value creation analysis considers all inputs that the firm uses as a part of its value

creatingactivities.

ThegenericvaluechainmodelwasdevelopedbyMichaelE.Porterbeforethecommercialisationof

the Internet and significant integration of the global economy. This model does not include the

globaleconomicandtechnicalinfrastructureasavaluecreationactivity.However,thisactivityisan

input that the world community of states makes in the process of production of global digital

servicesandproducts.Digitalservicesandproductsareglobalwhentheproducedonandsupplied

overtheInternettomanymarketstates.

“The microeconomic theory of the firm uses a “production function” to formally describe the

relationshipbetweeninputsandoutput.Initssimplestform,aproductionfunctiontreatsinputsasif

36 Geoffrey Alexander Jehle and Philip J. Reny, Advanced Microeconomic Theory (3rd edn, Financial

Times/PrenticeHall2011)125-126,135,146.37 Michael E. Porter, Competitive Advantage: Creating and Sustaining Superior Performance (Free Press;

CollierMacmillan1985)38.38 Ibid39-40.39 Ibid37.

12

theyareconsumedintheproductionofoutputs.Capital is,ofcourse,onetypeof input.However,

capital goods do not neatly conform with the simple production model.

Among other things, they are not consumed in production. Nonetheless, capital goods must

specificallybedeployedinproductionforaperiodoftimeinordertorenderservices.Ameasureof

capitalinputwhichwouldbeconsistentwiththeoryisthereforethequantityoftheflowofservices

providedbycapitalgoods.”40

In general, a process of production is a transformation of inputs into the final output. From the

perspective of international trade, the place of goods origin is a territory of a state where a

substantial transformation of inputs made in a production of these goods occurs. The same

approachappliedtoaproductionofdigitalservicesandproductsmeansthattheplaceoforiginof

theseservicesandproductsisalwaysamarketstate.Fordigitalservicesandproducts,thefinaland

themost substantial transformationof inputs takes placewhen information that constitutes “the

body”oftheserviceorproductisdownloadedbyanelectronicdeviceofanInternetuser.

Ininternationaltradetheoriginofservicesisusuallydeterminedbyalocationofaservicesupplier.

The digital economy, by its nature, significantly relies on automatic processes performed byweb

servers and electronic devices. Therefore, a supplier of digital services, its personnel and web

servers, as well as electronic devices involved in the process of production of services, can be

locatedindifferentstates.Whenwebserversandelectronicdeviceslocatedindifferentstates,the

electronic network of more than a single state is involved. Therefore, following the traditional

international trade approach to the origin of services, in some circumstances the single digital

servicemaybeseenasoriginatingfromterritoriesofmanystates.

The issue of origin or multi-territorial origin of digital services is usually not addressed in

internationaltaxpolicy.Forthepurposeoftaxpolicy,thepapersuggestsconsideringdigitalservices

and products as local onlywhen information inputs arrive from localweb servers interconnected

throughthelocalelectronicnetworkontheelectronicdevicelocatedwithinaterritoryofthestate.

When the process of production of digital services or products involves the infrastructure of the

Internetthatwhollyorpartlybelongstomorethanasinglestate,theserviceorproductcannotbe

consideredaslocal.

40 MichaelJ.Harper,“EstimatingCapitalInputsforProductivityMeasurement:AnOverviewofConceptsand

Methods”, Conference on Measuring Capital Stock (Canberra, 10-14 March 1997) 2 <http://www.oecd.org/std/na/2666894.pdf>accessed30December2016.

13

Whenweb servers used for a productionof digital services and products are located in different

states, and the entire business model structured around a global web platform or centrally

coordinatedwebplatformslocatedindifferentstates,thedigitalservicesandproductsareglobal.

Whendigitalservicesandproductsareglobal,inadditiontoinputsmadeoracquiredworldwideby

the firm itself, the production process necessarily includes the global input made of the world

community of states in a formof global public services. Theproductionprocess alsomay include

contributions of Internet users from all over the world made in a form of group and personal

inputs.41

In thedigitaleconomy, inaddition to inputs acquired fromthird suppliers, firmsproducing global

digitalservicesandproductsalwaysuseaglobalinputproducedbytheworldcommunityofstates.

Theinputofstatesworldwideintotheproductionofsomedigitalservicesandproductsismadeup

of coordinated contributions of individual states to the creation and maintenance of the global

economicandtechnicalinfrastructurebyenteringinmultilateralandinternationalagreementsand

development of national laws in support of these agreements. At the international level these

contributions are made by participation of states in multilateral treaties related to electronic

commerce42 and the creation of international institutions.43 By its very nature, this input can be

viewed as a global public service provided by the world community of state to multinationals

operatinginthedigitallayeroftheglobaleconomy.

Theinputoftheworldcommunityofstateshasaformoftheglobalpublicservice:globaleconomic

andtechnicalinfrastructurethatallowsfreemovementsofdigitalflowsofcapital,services,products

and information. This global public service is essential to the creation of a unique effect: spatial

freedom.Asa result,multinationalsoperating in thedigitaleconomypotentiallyhavemuchmore

freedomintheallocationoftheirresources,factorsofproductionandchoiceofamarketfortheir

products.

The idea of global public services is consistent with the acknowledged view that in some

41 Article 14.2 (4) of the Trans-Pacific Partnership (Atlanta, 5 October 2015) also distinguishes a service

deliveredelectronicallyfromaserviceperformedelectronically.42Forinstance,theUNCITRALModelLawonElectronicCommerce(12June1996)withadditionalarticle5bis

as adopted in 1998 (New York, 1999); the United Nations Convention on the Use of ElectronicCommunications in International Contracts (New York, 2005); the Trans-Pacific Partnership (Atlanta, 5October2015).

43 Inparticular, theWorldTradeOrganization (WTO);the InternetAssignedNumbersAuthority (IANA); theInternetCorporationforAssignedNamesandNumbers(ICANN);theWorldWideWebConsortium(W3C);TheInstituteofElectricalandElectronicsEngineers(IEEE)andtheInternationalTelecommunicationUnion(ITU);theInternetEngineeringTaskForce(IETF).

14

circumstances,statesprovidepublicservices(alsoknowaspublicgoods)asagroup.44Whenpublic

goodsareavailableforalltoconsumetheyareglobal.45Therefore,fromtheperspectiveofthevalue

creation analysis, the use of the global economic and technical infrastructure for production of

services and products on these infrastructure (on the Internet), is an input in the form of a

supportingactivityforvaluecreationbyamultinationalsupplierofdigitalservicesandproducts.This

isrepresentedonDiagram2.46

Diagram2.Valuechaininthedigitaleconomy

Therefore,whenamultinationalfirmisoperatinginthedigitaleconomyandusestheInternetasa

meansofproductionandtransmissionofthefinalproducttofinalcustomersaroundtheworld,the

firm creates a global product. In this case the value chain of the firm is truly global because it

involvestheglobalpublicservice.47

b.Interactivity

Originally,theWeb,orwhatisknownnowastheWeb1.0,wasananalogueofthetraditionalmedia.

The only key difference was the form in which the information was present and the method of

access to it. TheWeb, orWorld WideWeb (WWW), is a part of the Internet arising out of the

44 JhaRaghbendra,ModernPublicEconomics(2ndedn,Routledge2010)480-489.45 IngeKaul,ProvidingGlobalPublicGoods:ManagingGlobalization(OxfordUniversityPress2003)5.46 Primaryactivitiesofthosefirmsthatusewebplatformsintheirbusinessmodelsforproductionandsupply

of digital services and products identified as suggested byCharles B. Stabell andØysteinD. Fjeldstad in“Configuring Value for Competitive Advantage: on Chains, Shops, andNetworks” (1998) 19 (5) StrategicManagementJournal413,429.

47 The OECD defines the global value chain as “the full range of activities that firms engage in to bring aproduct to themarket, fromconception to finaluse.” SeeOECD, “InterconnectedEconomies:BenefitingfromGlobalValueChains”,SynthesisReport(OECD2013)8.

15

collection of technologies48 that allows digital information to be transferred from one Internet

Protocol (IP) address to another. Every device for the Internet communications has its own IP

address.Digitalinformationcan“travel”betweendevicesconnectedtoanetworkofinterconnected

web servers49 around the world. From the economic perspective, the Web is a distributed

hypermediaenvironmentwithintheInternetthatallowsmultimediainformationtobelocatedona

networkofinterconnectedserversandbetransferredtoaparticulardevicebyclickingonhyperlinks

(texts,iconsorimages)onawebpage.50

Theideaofinteraction,thecornerstoneoftheWeb2.0philosophy,transformedthecommercialuse

of the Internet and boosted the development of the digital economy. According to one of the

authorsofthenewphilosophy,TimO’Reilly:

Web2.0isthenetworkasplatform,spanningallconnecteddevices;Web2.0applicationsarethose

thatmakethemostoftheintrinsicadvantagesofthatplatform:deliveringsoftwareasacontinually-

updatedservicethatgetsbetterthemorepeopleuseit,consumingandremixingdatafrommultiple

sources,includingindividualusers,whileprovidingtheirowndataandservicesinaformthatallows

remixingbyothers,creatingnetworkeffectsthroughan“architectureofparticipation”, andgoing

beyondthepagemetaphorofWeb1.0todeliverrichuserexperiences.51

TheWeb2.0philosophyadvocatesforthecreationofopenwebplatformsanddevelopmentoftools

for interactionwith Internet users. The idea of interaction suggested by theWeb 2.0 philosophy

evolvedinto“theInternetofthings”–theideathatdifferentelectronicdevicescouldinteractwith

eachotherovertheInternet.52TheWebnowisanetworkthatlinksalldevicesthatcanaccessthe

Internet(computers,laptops,smartphones,andsoforth).

48 RequirementsforStringIdentityMatchingandStringIndexing,WorldWideWebConsortiumWorkingDraft

(W3,10July1998)<http://www.w3.org/TR/WD-charreq#Glossary>accessed10March2013.49 Web serversare computers thatdeliver (servesup)webpages. Everyweb serverhasan IPaddressand

possiblyadomainname.Forexample,ifyouentertheURLhttp://www.webopedia.com/index.htmlinyourbrowser,thissendsarequesttotheWebserverwhosedomainnameiswebopedia.com.Theserverthenfetchesthepagenamedindex.htmlandsendsittoyourbrowser.

AnycomputercanbeturnedintoawebserverbyinstallingserversoftwareandconnectingthemachinetotheInternet<http://www.webopedia.com/TERM/W/Web_server.html>accessed10December2015.

50 Donna L. Hoffman, Tomas P. Novak and Patrali Chatterjee, “Commercial Scenarios for the Web:Opportunities and Challenges” (1995) 1(3) Journal of Computer-Mediated Communication<http://onlinelibrary.wiley.com/doi/10.1111/j.1083-6101.1995.tb00165.x/full>accessed13June2013.

51 Tim O’Reilly, “Web 2.0: Compact Definition?” <http://radar.oreilly.com/2005/10/web-20-compact-definition.html> accessed 17 June 2013; see also Tim O’Reilly, “What Is Web 2.0. Design Patterns andBusiness Models for the Next Generation of Software” (30 September 2005)<http://oreilly.com/web2/archive/what-is-web-20.html>accessed17June2013.

52TFDEFinalReportat42-43.

16

NowadaystheWebisnotonlyamarketplaceitselfwheredigitalservicesandproductsareoffered

forsale.TheWeb,aswellastheInternetinwhole,isthemeansbywhichInternetusersareinvolved

in the process of production through the interaction either with web platforms, or and among

themselves through web platforms. Some firms operating in the digital economy have business

modelsthatrelyontheinputsofindividuals(Internetusers)intheprimaryvaluecreatingactivities:

supplyofdigitalservicesandproductsormarketingandsales.Theinvolvementof individuals into

theprocessof productionofdigital services andproducts isa featureof theWeb2.0philosophy,

whichwasthesecondInternetrevolutionafterthecommercialisationoftheInternet.

The interactionwithawebplatformorthrough it,aswellasotherWeb-basedactivitiescreatesa

“digital trace” on theWeb – in otherwords, data.Millions of gigabytes of digital information are

producedeverysecondbyInternetusers,serversandelectronicdevicesandtransferredthroughthe

Web commonly referred to as “big data”.53 In the digital economy, data is a core asset and

commodityformanydigitalservicesandproducts.

c.MultisidedBusinessModels

Whenthesupplyofdigitalproductsandservices,asaprimaryvaluecreatingactivitypresentedon

Diagram 2, includes advertising web platforms, the business model often has a structure of a

multisidedmarket because it includeswebplatforms that provide free services for Internet users

andadvertisingwebplatforms(alsoknownas“adnetworks”54).Themoresophisticatedmodelsalso

includeanadexchangeplatform55-avirtualmarketwhereunreservedadplaces(adslots)56canbe

offeredby anagencyoran adnetwork that represents awebsiteowner to other adnetworks or

advertisingagencies.

As presented on Diagram 3, the business model that includes web platforms that produce

advertisingandfreeserviceshastriangularstructurewhereeachsideisasetofbilateralexchanges:

betweenaplatformoperatorandInternetusers;Internetusersandadvertisers;advertisersandthe

platform operator. The platform operator in this model is an entity that supplies both Internet

advertisingandfreeservices.

53 OECD,“ExploringData-DrivenInnovationasaNewSourceofGrowth:MappingthePolicyIssuesRaisedby

‘BigData’”(2013)OECDDigitalEconomyPapers222,4.54 <http://www.iab.net/wiki/index.php/Ad_network>accessed1May2014.55<http://www.iab.net/wiki/index.php/Ad_exchange>accessed13November2013.56<http://www.iab.net/wiki/index.php/Ad_space> accessed 1 May 2014; see also Lim Hongkiat, “How To

SetupGoogleAdManagerOnYourBlog/Website”<http://www.hongkiat.com/blog/how-to-setup-google-ad-manager-on-your-blogwebsite/>accessed1May2014.

17

Diagram3.Advertisingwebplatformasathree-sidedmarket

3 IncompatibilityoftheCurrentModeloftheInternationalAllocationofTaxingRightswiththe

GlobalProcessofProductionintheDigitalEconomy

Themultisidedstructure of thebusinessmodels commonly found in thedigital economywasnot

anticipatedbythecurrenttaxtreatysystem.

ThecurrentmodelfortheallocationoftaxingrightsinrelationtomultinationalsisshapedbytheTax

Treaty Model Conventions that are based on three general assumptions. First, individuals and

entities within states are involved in the cross-border commercial activities and, therefore,

participate in the economic exchange. States stimulate this exchange by their national and

internationaltrade,investmentandtaxpolicies.Therefore,thegoaloftaxpolicyistostimulatethe

internationalexchangeofgoods,servicesandcapital.

The second assumption is that income from cross-border economic activity creates economic

allegiancewithmore thanone state. Therefore, to reduce a risk of double taxation states should

decide“whereapersonought tobe taxedorhowthedivisionought tobemadeasbetween the

varioussovereigntiesthatimposethetax.”57

Thecoordinateddecisionthatisre-introducedbystatesthroughtheirdoubletaxtreatiesisbasedon

twoacceptedcriteriaofeconomicallegiance:theoriginofincomeandthedomicileofataxpayer.58

Accordingly,therightstotaxitemsofincomeareallocatedbetweenasourceandresidencestates.

Thethirdassumptionsuggeststhatentitiesofeverymultinationalfirmareseparatetaxpayers.

57 LeagueofNations,ReportonDoubleTaxation:SubmittedtotheFinancialCommitteebyProfessorsBruins,

Einaudi,SeligmanandSirJosiahStamp(Geneva,15April1923)20.58 Ibidat23-25.

18

Thesethreeassumptionsdonotfittherealityoftheproductionofglobaldigitalservicesandgoods

andarediscussedfurtherthroughcounterarguments.

a.Co-productionvsExchange

Manyofthebusinessmodelsoffirmsoperatinginthedigitaleconomyrelyonnetworkeffectsand

aggregationofpersonaldata.

Theconceptofanetworkeffecthasbeenknownsincethecreationofthefirsttelephonenetworks.

Theeffectariseswherethevalueofaproducttoitsusersincreaseswiththenumberofotherusers

oftheproduct.59TheWeb2.0philosophymadethenetworkeffectsoftheWebmorepowerfulby

combiningitwithopenplatforms.ThenetworkeffectintheWeb2.0erameans“farmorethanjust

offering old applications via the network (“software as a service”); itmeans building applications

that literallygetbetter themorepeopleuse them,harnessingnetworkeffectsnotonlytoacquire

users,butalsotolearnfromthemandbuildontheircontributions.”60TimO’ReillyandJohnBattelle

argue: “[m]any people now understand this idea in the sense of “crowdsourcing”, namely that a

largegroupofpeoplecancreateacollectiveworkwhosevaluefarexceedsthatprovidedbyanyof

theindividualparticipants.”61Fromtheperspectiveofvaluecreationanalysisthenetworkeffectisa

groupinputmadebyindividuals,fromthegroup,inaprimaryvaluecreatingactivityofasupplierof

global digital services and products. By making this “group input” individuals participate in the

process of production. The network effects can add value to both the supply of services and

marketingandsalesactivities.Spaceconstraints,however,meanthispapercannotaddresstheissue

infurtherdetail.

Aggregationofdata, includingpersonaldata, isanother featureofmanybusinessmodels thatare

usedinthedigitaleconomy.Likethenetworkeffects,collectingofinformationaboutcustomers is

not a newmarketing tool. However, never in the history of the world has a single firm had the

possibilitytocollect,store,analyseandoperatewithsuchanenormousvolumeofdatacomingfrom

allovertheworld.

Data collection is not limited to social networking sites. “Nearly everything manufactured today

existssimultaneously inthephysicalworldandintheworldofdata.Adigitalrepresentationisthe

object'sinformationshadow.Informationshadowcanbeexaminedandmanipulatedwithouthaving

59 OECD,“TheDigitalEconomy”,ReportofHearingsontheDigitalEconomy(7February2013)8.60 TimO’ReillyandJohnBattelle,“WebSquared:Web2.0FiveYearsOn”(Web2summit,October2009)7-8

<http://www.web2summit.com/web2009/public/schedule/detail/10194>accessed17June2013.61 TimO’ReillyandJohnBattelle,“WebSquared:Web2.0FiveYearsOn”(Web2summit,October2009)7-8

<http://www.web2summit.com/web2009/public/schedule/detail/10194>accessed17June2013.

19

totouchthephysicalobject.”62Moreandmoreinformationshadowsarelinkedwiththeirrealworld

analogues by unique identifiers.63 Whether you are playing web games, searching for holiday

accommodationorpostingphotosona socialnetwork,all this information is collected for further

monetisation.64This“shadowworld”generatesrealrevenues.

Networkeffects,datacollectionandother activitieson the Internet like registrationonawebsite,

searching for informationorweb surfing65makes Internet usersunwitting “workers” in theglobal

processofproductionofdigitalservicesandproducts.

Whenawebsiteisdesignedasanopensourceplatform,userscancreate“content”andplaceiton

theplatform.Themoreinterestingthecontentthatisplacedonthewebplatform,themorepopular

theweb platform becomes.Web platforms that are popular attractmore advertisers. Therefore,

thesepersonalinputsaddthevaluetotheeconomicproductproducedbythefirmandalsoaffects

themarketvalueof the firm.Feedback ina formof“Likes”onopenwebplatformshas thesame

effect.Thistypeof interactioncreatesthe“self–reinforcingvirtuousfeedbackloop”thatkeepsold

usersengagedwhilealsoattractingnewusers.66

Somewebplatformsarenotopenbutdesignedforcertaintypesof interactionwithInternetusers

thatalsocanaddvaluetothedigitalproductortothebusinessofaplatformowner.Forinstance,

everytimewhenInternetusersmakesearchqueriesontheGooglesearchplatformtheyaddvalue

to the search service – and toGoogle. A greater quantity of search queries enhances the search

platformandmakes thesearch resultsmoreprecise. In its turn, the increase in thequalityof the

searchresultsattractsmoreInternetuserstothesearchplatform.

Thecurrentmodelof theinternationalallocationof taxingdoesnotcapture theglobal,groupand

personal inputs, made by states and individuals in the process of production digital services and

products. Inthecaseof individuals,theexchangeofpersonal inputforfreeservicescouldbeseen

paymentforthe“freework”andagreementtoreceiveInternetadvertisements.However,theissue

62Mike Kuniavsky, “Smart Things: an outline” (Orangecone, 8 February 2009)

<http://www.orangecone.com/archives/2009/02/smart_things_an.html>accessed10November2013.63 TimO’ReillyandJohnBattelle,“WebSquared:Web2.0FiveYearsOn”(Web2summit,October2009)7-8

<http://www.web2summit.com/web2009/public/schedule/detail/10194>accessed17June2013.64 Kenneth C. Laudon and Carol Guercio Traver, E-commerce: Business, Technology, Society (Prentice Hall

2011)451-453.65 Thetermsurfingisgenerallyusedtodescribearatherundirectedtypeofwebbrowsinginwhichtheuser

jumpsfrompagetopageratherwhimsically,asopposedtospecificallysearchingforspecific information<http://www.webopedia.com/TERM/S/surf.html>accessed10December2015.

66 AlagSatnam,“UnderstandingCollectiveIntelligence”inJörnAltmann,UlrikeBaumöl,andBerndJ.Krämer(eds)AdvancesinCollectiveIntelligence(Springer2012)7.

20

ofcompensationofthe inputsmadebystates fromaroundtheworld into theproductionprocess

wouldremain.Afewstates(andtheirsecuritiesservices)maygetcompensationinaformofaccess

todataasaresultofinteractionofInternetuserswithawebplatform.However,thisfactmakesthe

entire situation more complex. The access of one state to the information related to foreign

nationals locatedoutsidetheterritoryofthatstatecreatessecurityrisksforother statesandtheir

nationals. From the pragmatic viewpoint, if the risk cannot be eliminated it at least should be

compensatedfor.Thebestformofthiscompensation,itissuggested,wouldbeataxpayment.

Consequently, in thedigitaleconomy individualsand entities,aswell as states themselvescanbe

involvedinco-productionofdigitalservicesandproducts.

b.GlobalvsCross-Border

In general, multinationals can be involved in business and investment activities. This part of the

paperdiscussesonlybusinessactivitiessuchasproductionofdigitalservicesandproducts.Theissue

of investment activities of multinationals addressed briefly in Part 6 (Section b. “Principle of

integratedincome”).

DigitalservicesandproductsareperformedontheInternet,ormorepreciselyontheWorldWide

Web. These activities and their outcome have a digital form. In the case of digital services and

products the activity and its outcome are inseparable; they are two sides of the same coin. The

activity always results in a particular outcome that has a digital formand thereby is available for

human’sperception.Consequently,thecreationofadigitalserviceandproductanditssupplytoa

consumercannotbesplitintoseparatestages.Technicallythecreationandsupplyareelementsofa

singleprocessofproductionofdigitalservicesandproducts.

Whendigitalservicesandproductsareglobal,theconceptof“cross-borderactivity”isnon-sensible

forthreegeneralreasons.First,theprocessofproductionoftheseservicesandproductsdoesnot

takeplace on a territory of any particular state. Second, productionof global digital services and

productsinvolvesnotonlynationalsofmanystates(includingInternetusersthatmakepersonaland

groupinputs,themultinationalfirmitselfandthirdpartysuppliers),butalsotheworldcommunity

ofstatesthatprovidestheglobalpublicservicethat isanessential input.Third,anoutcomeofthe

digital services andproducts does not cross the geographical border ofamarket state asa single

object arriving from a territory of a particular foreign state. This outcome also does not “pass

throughcustoms”67asdotraditionalgoods.

67 JinyanLi,“ConsumptionTaxationofElectronicCommerce:Problems,PolicyImplicationsandProposalsfor

Reform”(2003)38CanadianBusinessLawJournal425,442.

21

Every process of production of digital services and products finishes at the moment when

informationinadigitalformisdownloadedbyanelectronicdeviceofanInternetuser.However,the

informationdoesnot“travel”ontheInternetasasinglemessageuni-directionallybetweensender

andreceiver.

Anyactivityonanelectronicnetwork, liketheInternet, isa setoftechnical transactionsbasedon

the request-response communication between the sender and receiver. Digital information

transferred into signals can be successfully delivered only when all requests were responded

correctly.68

Forthepurposeoftransmission,dataissplitintochunks(“packets”)thatareassembledintoasingle

pieceand reconvertedfromelectronic signals intooriginaldata (a“message”)atthefinalstageof

thedatatransmissionprocess.69Packetsofdatacanbestoredorgeneratedonserversthatarenot

necessarilylocatedinasingleplace.70

As a result, an outcome of the digital service or product downloaded on the electronic device is

oftena“patchwork”craftedwiththeparticipationofservers,electronicdevicesandtheelectronic

network.Whenserversandelectronicdevicesarelocatedindifferentstatesandtheentiretechnical

infrastructure of the Internet is used, the digital service or product cannot be seen as produced

withinaterritoryofaparticularstate.

Therefore, the “origin of income”, as a basis of the allocation of taxing rights becomes a very

complexcriteriaofeconomicallegiance.Inprinciple,thiscriterionremainsrelevantbecauseincome

generated in the digital economy can be linked with physical points located within a particular

geographic territory.However, thereareat least two general problems that the currentmodelof

theallocationcannotresolve.First, incomefromglobaldigitalservicesandproductshas“pointsof

connection” located in many states. However, the current model does not allocate taxing rights

betweensourcestates. Second, the geographic territorywhere thepointof connection is located

maynotbelongtoanystate.

68 More sophisticated process of data transmission can include additional stages like digitizing and

compression for audio and video signals. See A. Forouzan Behrouz and Fegan Sophia Chung, DataCommunicationsandNetworking(4thedn,McGraw-Hill2007)chapter29.

69 Rus Shuler, “How Does the Internet Work?” (2002, 2005) <http://www.theshulers.com/whitepapers/internet_whitepaper/index.html> accessed 2 June 2015; see also PhilipA. Bernstein and EricNewcomerBernstein,PrinciplesofTransactionProcessing(MorganKaufmannPublishers2009)4.

70FormoredetailseePhilipA.BernsteinandEricNewcomerBernstein,PrinciplesofTransactionProcessing(MorganKaufmannPublishers2009)4-6.

22

c.SingleEconomicandTaxEntityvsSetofSeparateTaxpayers

National lawsof somestatesconsidersa local corporategroupasasinglesubjectoftax liability.71

However,undertheseparateentityapproachintroducedthroughdoubletaxtreatiesornationaltax

laws,entitiesofamultinationalfirmlocatedindifferentstatesareseenasseparatetaxpayers.

The separateentity approachas abasis for the internationalallocationof incomeand lossesofa

multinationalfirmforthepurposesoftaxationwasfirstsuggestedbytheLeagueofNationsin1933

inthe“CarrollReport”.72Thereportwasissuedafterinvestigationoftaxsystemsof35countries.

Inaddition to theseparateentityapproach, theCarrollReportdescribedanalternativeapproach:

consolidation of the corporate income tax base and formula apportionment. The alternativewas

declinedmainlybecauseoftaxsovereigntyconcerns,73ratherthananyparticulareconomicreason.

However, originally the LeagueofNations discussed the apportionment asamethod to dealwith

incomeearnedbymultinationals.In1927theLeagueofNationssuggestedto“drawupmodelrules

for the apportionment of taxation applicable to the profits or capital of undertakingsworking in

several countries” asoneof themeasures “in order to eliminatedouble taxation and tosecure a

moreequitabledistributionoffiscalburdens.”74

The choice made in a favour of the separate entity approach is incoherent with the view on a

multinational firm as a single economic unit. Corporate law of many states applies the single

economicentity(orunit)conceptthatsuggeststhatentitiesassociatedwitheachotherinavirtueof

commoncontroloperateasasingleeconomicunit.Fromaneconomicperspective,amultinational

firm acts as a single economic unit when its entities jointly contribute to a single economic

enterprise.75

71 PeterHarrisandJ.DavidB.Oliver,InternationalCommercialTax(CambridgeUniversityPress2010)57.72 Mitchel B. Carrol, “MethodsofAllocating Taxable Income”Vol. IV in the LeagueofNations,Taxation of

Foreign and National Enterprises (Geneva, 30 September 1933); see also Raffaele Russo, Report on theHistorical Development of Article 7 of the OECD Model” in The Attribution of Profits to PermanentEstablishments, IFA Cahiers 91B (International Bureau of Fiscal Documentation 2006) 90; Thomas Rixen,ThePoliticalEconomyofInternationalTaxGovernance(PalgraveMacmillan2008)93.

73 ThomasRixen,ThePoliticalEconomyof InternationalTaxGovernance (PalgraveMacmillan2008)95;seealso Raffaele Russo, “Report on the Historical Development of Article 7 of the OECD Model” in TheAttribution of Profits to Permanent Establishments IFA Cahiers Vol. 91B (International Bureau of FiscalDocumentation2006)89.

74League of Nations, Double Taxation and Tax Evasion, Report of the Committee of Technical Experts(Geneva,April1927).

75 PieterVanCleynenbreugel,“SingleEntityTests inUSAntitrustandEUCompetitionLaw”(June21,2011)<http://ssrn.com/abstract=1889232>accessed10December2015.

23

The model concept of a “group of associated enterprises”76 suggested for the purpose of

international tax policy and applied tomultinationals, combines both elements: common control

andjointcontributions.However,theacknowledgementthatentitiesofagroupareundercommon

controland“shareeconomiclifewithinasingleeconomicunit”doesnotaffecttheentiremodelof

theallocation-thatistheallocationoftaxingrightsbutnottheallocationofportionsofglobaltax

base.

In addition to the general problems that the separate entity approach creates in practice,77 the

allocationof taxing rights insteadof anapportionment of theglobal taxbase, isunfairbecause it

cannotconsidertheglobalinputmadebytheworldcommunityofstates.

Any income or loss that originates through theproductionof global digital services and products

shouldcreateasingleincometaxbase,becausetheincomeorlosscannotrealisticallybeallocated

inanyoneterritory.Theglobalincometaxbase,itwillbearguedbelow,shouldbeassessedatthe

globallevel.Forthispurpose,amultinationalfirmshouldbeseenasasingletaxpayer.

4 Conflict

Thecontemporarysystemfortheinternationalallocationoftaxingrightsisdescribedasa“delicate

consensusamongnations”.78Inpractice,thisconsensuscouldbedescribedasthe“warofallagainst

all”79whenitcomestotaxationofincomeearnedbymultinationals.

Statesare“fighting”eachother for theopportunity tobe the first,and,witha sufficient luck, the

onlystatethatcantax incomeofaparticularmultinationalfirm.The fight isplayedaccording toa

set of rules and may take the form of direct or indirect tax treaty overrides, as discussed in the

Introduction, or a form of avoidance of entering into double tax treaties and/or treaties for tax

assistance.80

76 Paragraph1(a)ofArticle9ofOECDModelTaxConventiononIncomeandonCapital:CondensedVersion

(9thedn,Paris,15July2014).77 ForsomeexamplesseePremSikkaandHughWillmott,“TheDarkSideofTransferPricing: ItsRoleinTax

AvoidanceandWealthRetentiveness”(2010)21(4)CriticalPerspectivesonAccounting342,344-352.78 Reuven Avi-Yonah, “From Income to Consumption Tax: Some International Implications” (1996) 33 San

DiegoLawReview1329,1329.79 ThisisaparaphraseofThomasHobbes’snotionthat“duringthetimemenlivewithoutacommonpower

tokeepthemallinawe,theyareinthatconditionwhichiscalledwar;andsuchawar,asisofeverymanagainst everyman.” Thomas Hobbes, Leviathan or TheMatter, Forme and Power of a Commonwealth,EcclesiasticalandCivil(GeorgeRoutledgeandSons1651/1886)64.

80 For instance, theMultilateralConventiononMutualAdministrativeAssistance inTaxMattersdevelopedjointlybytheOECDandCouncilofEuropein1988andamendedbyProtocolin2010(1June2011).

24

The fight for rights among states is supplemented by the fight by states for tax revenue from

multinationals. The multinationals are fighting back through tax planning that legitimately avoids

taxablepresenceinamarketstate81orsignificantlyreducesthesizeofataxliability.82

States commonly refer to their “sovereignty” to justify their actions against other states or

multinationals.However,thisjustificationismerelyemptyrhetoricthatdoesnotresolvetheglobal

distributionalconflict,especiallywhentheplaceoftheconflictisthedigitaleconomy.

Whileeachstatehastwogroupsof“enemies”–multinationalsandotherstates–thedistributional

conflictistwofold.

Thefirstpartispurelyeconomic:stateswanttogetrevenuesfromthetaxationofincomeearnedby

multinationalswhilemultinationalsdonotwanttopayataxmorethanonceortohaveanexcessive

taxburden.Therefore,statesaretryingtostretchtheirnationaltaxbasesthroughnationaltaxlaws,

whilemultinationalstrytominimisetheirtaxburden.Thispartoftheconflictcouldbelessened,or

maybeevenresolved,oratleastreduced,ifthestatesthatlevyataxonincomewouldbesurethat

thetaxleviedwouldbepaid,whilemultinationalswouldbecertainthatthetaxisbepaidonlyonce.

Thesecondpartoftheconflictispolitical:eachstate,asasovereignpoliticalbody,believeseitherin

theexclusivityorinthepriorityofitsownrighttotaxitemsofincomeearnedbymultinationals.

Statesneedtaxrevenues.Thisneedcanbesatisfiediftherightofastatetolevyataxonanitemof

incomeisnotlimitedandcanbeeffectivelyexercised.Thelatermeansthatthestatewillnotonlybe

abletolevyatax,butalsowillcollecttaxrevenuesinfullandontime.

For a state, inprinciple, it shouldnotmatterwhether it is allocated a right to taxor a shareof a

globaltaxbasewithrespecttowhichtherighttotaxcanbeexercised.Whatmattersisthefactthat

astatecangettaxrevenuesfromthetaxationofincomeofmultinationals.Thiscouldbepossibleif

incomeandlossesrelatingtoproductionofglobaldigitalservicesandproducts,areassessedatthe

globallevelundertheglobalconsensusthatdefinesrulesforapportionment.

Thepoliticalpartoftheconflicttriggersitseconomicpartandviceversa.Ifstatesdisagreewiththe

modeloftheallocationoftheglobaltaxbase,theywillnotguaranteethesingletaxationofglobal

income.Ifmultinationalswouldfindthatthemodeloftheallocationisunableguaranteeonlysingle

taxationandpreventexcessivetaxburdens,theywillseekopportunitiestoavoidtaxation,whichwill

impact on the tax revenuesof states. Therefore, the global tax base should be allocatedunder a

81 OECD, “Addressing the Tax Challenges of the Digital Economy”, Action 1: 2014 Deliverable, Report,

OECD/G20BaseErosionandProfitShiftingProject(16September2014)102.82 FortypicaltaxplanningstructuresusedinthedigitaleconomyseetheTFDEFinalReport,168-180.

25

globalconsensusthatconsidersinterestsnotonlystates,butalsomultinationalsandhasaformof

globaltaxpolicy.

To be fair, efficient and effective, global tax policy must correspond with the political-economic

reality. That reality is determined by the current level of globalisation, including the

interdependencybetweenstates,andalsobetweenstatesandmultinationals.

The interdependenceof states in theglobal economy is awell-knownphenomenon. Cross-border

investments and borrowingmoney from foreign governments and international institutions, have

ledtothesituationwhere“everycountryistoatlargeextentownedbyothercountries,whichnot

only distorts perceptions of the global distribution of wealth but also represents an important

vulnerabilityforsmallercountriesaswellasa sourceof instability in theglobaldistributionofnet

positions.”83 In addition to financial interdependence, states are dependent on each other as co-

creatorsoftheglobaleconomicandtechnicalenvironment.Withoutinputsofalmostallmembersof

theworldcommunityofstates,theglobalfreedomofdigitalflowsofcapital,services/productsand

information,aswellastheveryexistenceofmultinationalgiantslikeGoogle,wouldnotbepossible.

Another side of the phenomenon is the interdependency between states and somemajor firms

operating in thedigitaleconomy. Inparticular, thevastmajority of states arenot inaposition to

closetheirmarketstothedigitalservicesandproductsofGooglesupplieddirectlyovertheInternet.

Theoutcomethat the“localisation”of themarket for theseservicesandproductswouldhave for

manystatesmaybeworsethantheimpactofGoogle’staxavoidance/planningonthosestates.84For

instance,ifthestatewouldcloseitsmarketforInternetadvertisingservicesofGoogle,itwouldbe

difficultforlocalfirmstoadvertisetheirproductsinforeignmarketsovertheInternet.Besides,the

local firms and individuals that were involved in production or marketing of Internet advertising

services of Google would lose their income. As a result, the national tax base of the state that

localiseditsmarketofInternetadvertisingserviceswouldshrink.

Furthermore, if somemarketswere closed, itmight affect the profitability of the global Internet

advertising industry, and also firms that are dependent on that industry. It would also reshape

businessmodelsusedintheindustry.Inparticular,ifGooglewouldnotgetsufficientrevenuesfrom

Internetadvertising, itwouldnotprovidefreeservicesfor Internetusers. Inthebusinessmodelof

Google production and consumption of free services and Internet advertising are interrelated.

Consequently,ifInternetuserswouldbeforcedtopayfordigitalservicesthatGoogleprovidesfree83 ThomasPiketty,Capital intheTwenty-FirstCentury (TheBelknapPressofHarvardUniversityPress2014)

193.84Article 14.15 of the Trans-Pacific Partnership (Atlanta, 5October 2015) emphasises the global nature of

electroniccommerceandsuggestsmultipleformsofcooperationtopromoteitsdevelopment.

26

of charge, it would reduce the consumption of both free services and Internet advertising. The

replacementof thebusinessmodel that is “drivenbyadvertising revenues”by theclassicalmodel

“productvs.money”,couldevenaffecttheentireprofitabilityifnottheviabilityofGoogle.

5 FreeConsumptionofGlobalPublicServicesintheDigitalEconomy

Thesystemsapproach85appliedinthisParthelpsustounderstandtheoriginofthedigitaleconomy

and the general structural problem of tax policy related to this economy – the impossibility to

monetise global public services at the national or international level. The systems approach, in

general,investigatesaformalrelationshipbetweenobservedfeaturesorattributesthatconstitutea

system.Systemsareseenasexistingwithinanenvironment (amegasystem)and interactingwith

eachotherandalsowiththeenvironment.Theresultofeachinteraction(anoutput)mayaffectthe

environmentand/orsystemsexistingwithinit.

Diagram4demonstrateshowasingle idea(the freedomofdigital flowsofcapital,goods,services

andinformation)hasdeterminedthebirthofanewmega-system-the“digitaleconomy”,drives it

andkeepsitselements(states,internationalinstitutions,multinationals)together.

(a) Commitment of states to the idea of

freedomofdigitalflowsofcapital,goods,

servicesandinformation

85 Systemsapproachisaheuristicmethodthatisappliedinmanydisciplineforanalysisofcomplexproblems,

see M.D. Mesarovic and Yasuhiko Takahara (eds), General Systems Theory: Mathematical Foundations(AcademicPress1975)1.

27

(b) Creationoftheglobal“digitaleconomy”–

the economic and technical environment

where capital, services, products and

information in digital form can move

between states without significant

limitations

(c) Originofmultinationalsuppliersofdigital

services and products as a result of the

general output produced by the global

digitaleconomy

Diagram4.Originoftheglobaldigitaleconomyandmultinationalfirmsoperatinginit

Thediagramdemonstratesthatstates throughtheircommitment totheideaof freedomofdigital

flowsof capital, services/products and information co-participate in a single process that leads to

thecreationoftheglobaldigitaleconomy,whichisthehabitatfornewtypesofmultinationalfirms-

inherentlyglobal.

The creationof the Internet goes back to 1962when J.C.R. Licklider andWeldenClark presented

their“GalacticNetwork”conceptthatwouldallowgloballyinterconnectedcomputersquicklyaccess

digitalinformationfromanysite.86Originallydevelopedforanon-commercialpurpose,theInternet

grew intoa global information infrastructure that links electronic devicesall over theworld87 and

providesthetechnicalsideofthedigitaleconomy.TheInternetwascommercialisedwithimmense

86 J.C.R.LickliderandWeldenE.Clark,"On-LineMan-ComputerCommunication"TheAmericanFederation

of Information Processing Societies (AFIPS), International Workshop on Managing RequirementsKnowledge(Philadelphia,December1962)113-128.

87 Formore details about the history of the Internet see BarryM. Leiner; Vinton G. Cerf; David D. Clark;RobertE.Kahn;LeonardKleinrock;DanielC.Lynch;JonPostel;LarryG.RobertsandStephenWolff,“BriefHistory of the Internet” <http://www.internetsociety.org/internet/what-internet/history-internet/brief-history-internet#JCRL62>accessed1July2015.

28

supportfromtheUSGovernmentandtheeffortsoftheEU, international institutions, inparticular

theWTO, aswellasprivate investors.88 In thepast15years the Internet hasgeneratedasmuch

economicgrowthastheIndustrialRevolutiondidin50years.89

SincethecommercialisationoftheInternet,states,ingeneral,hasbeenpromotingglobalfreedom

of movement for digital flows of capital, services/products and information. Through multiple

interactions, states have created the global economic and technical environment where a new

industry–thedigitaleconomy–wasestablished. Inthenewenvironment,theproductionprocess

fordigitalservicesandproductscanoftenbeglobal.Thebusinessopportunitiesfortheprovidersof

such services and products would not exist without the current level of integration of national

economies intotheglobaleconomy,aswellastheintegrationoflocalelectronicnetworks intothe

globalelectronicnetwork.

From the perspective of the systems theory, within the global economic environment (a mega

system),statesandmultinationals(systemsoflowerlevel)interactnotonlywitheachotherbutalso

with the global economic environment. These interactions have a triangular structure.90 For

instance, contributions of states to the maintenance of the global economic and technical

environment and the general outcomeof these contributions is an interactionwith environment.

Whileacooperationthatcreatesabasisofthesecontributionsisaninteractionbetweenstates.

88 FormoredetailseeDanSchiller,DigitalCapitalism:NetworkingtheGlobalMarketSystem(MITPress1999)

13-88.89 McKinseyGlobalInstitute,“InternetMatters:TheNet‘sSweepingImpactonGrowth,Jobs,andProsperity”,

Executive Summary (McKinsey, May 2011) 3<http://www.mckinsey.com/insights/high_tech_telecoms_internet/internet_matters> accessed 12 June2015.

90 It is an adaptation of the idea of Lorenz von Stein about the triangular relationship between a state,economy and society. The idea discussed in Klaus Vogel, “The Justification for Taxation: a ForgottenQuestion”(1988)33(1)AmericanJournalofJurisprudence19,49.

29

Diagram5.Interactionofstatesinandwiththeglobaleconomicenvironment

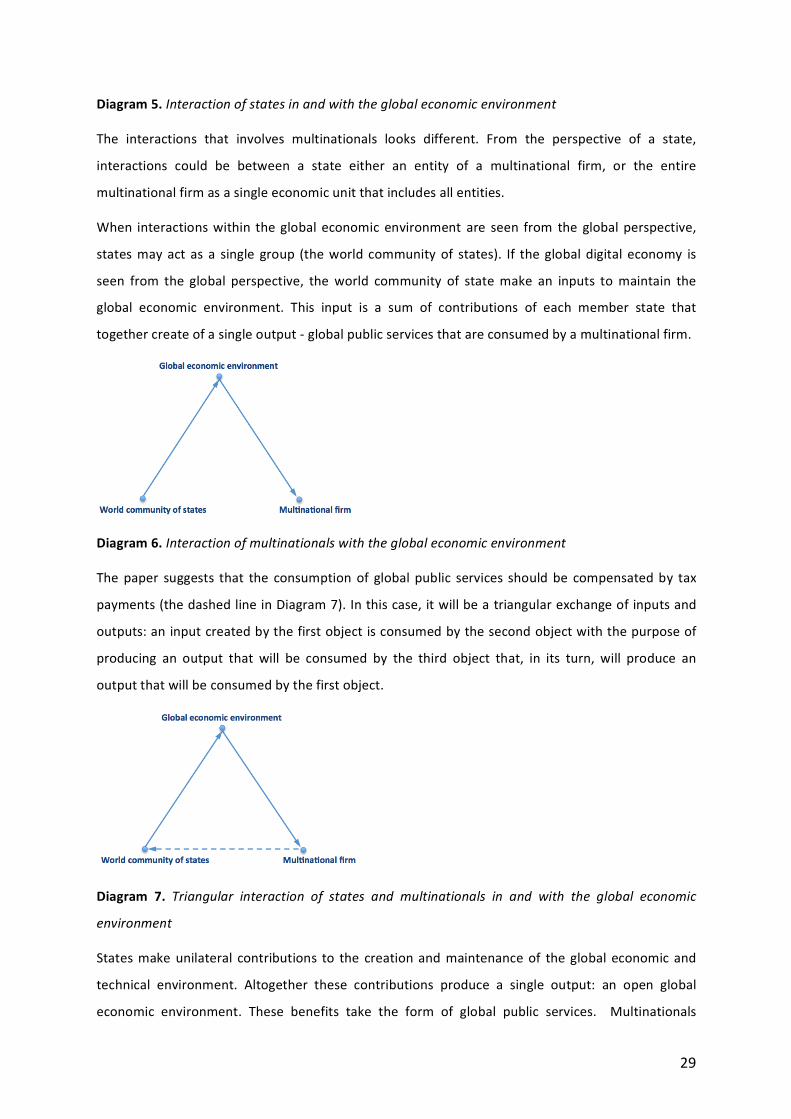

The interactions that involves multinationals looks different. From the perspective of a state,

interactions could be between a state either an entity of a multinational firm, or the entire

multinationalfirmasasingleeconomicunitthatincludesallentities.

When interactionswithin theglobal economic environment are seen from the globalperspective,

statesmay actas a single group (theworldcommunity of states). If theglobal digital economy is

seen from the global perspective, theworld community of statemake an inputs tomaintain the

global economic environment. This input is a sum of contributions of each member state that

togethercreateofasingleoutput-globalpublicservicesthatareconsumedbyamultinationalfirm.

Diagram6.Interactionofmultinationalswiththeglobaleconomicenvironment

Thepaper suggests that the consumptionof globalpublic services should be compensatedby tax

payments(thedashedlineinDiagram7).Inthiscase, itwillbeatriangularexchangeofinputsand

outputs:an inputcreatedbythefirstobjectisconsumedbythesecondobjectwiththepurposeof

producing an output that will be consumed by the third object that, in its turn, will produce an

outputthatwillbeconsumedbythefirstobject.

Diagram 7. Triangular interaction of states and multinationals in and with the global economic

environment

Statesmakeunilateral contributions to the creationandmaintenanceof theglobal economicand

technical environment. Altogether these contributions produce a single output: an open global

economic environment. These benefits take the form of global public services. Multinationals

30

operatinginthedigitaleconomyarethemajorconsumersofthesepublicservices.Theconsumption

of these global public services takes placeduring the interaction of amultinational firmwith the

globalenvironment.

The consumption of global public services is not the result of the direct interaction between a

particular state and a multinational firm. This consumption activity cannot be “captured” and

“monetised”bynationalorinternationaltaxpolicyofastate.Therefore,multinationalsoperatingin

thedigitaleconomyenjoyglobalpublicserviceswithoutmakinganysacrifices.

Ataxisaninstrumentthatcanbeseenasmonetisingpublicservices.Thisinstrumentistraditionally

applied at a national level where a state and a taxpayer are seen as participating in a bilateral

exchangeof public services into taxes. However, in the case of global services andproducts, the

monetisation of global public services cannot take place at the national level because states co-

produceglobalpublicservices.Consequently,themonetisationofglobalpublic services ispossible

onlyundersomeformofglobaltaxpolicy.

6 BasisforMultinationalCo-operationintheDigitalEconomy

This global tax policy requires global political co-operation. States cooperate when it is in their

intereststodoso.Thoseinterests,aswellastheopportunitytoprotectthem,differfromstateto

state.Multinationals,atleastgiantslikeGoogle,canaffecttheprocessofmultinationalco-operation

bylobbyingfortheirowninterestsindifferentstates.Therefore,anassessmentofthelikelihoodof

political co-operation on matters that affect multinationals should consider interests of

multinationalsaswell.Ascommercialenterprises,multinationalswouldliketopaynotaxoratleast

pay no more tax than their competitors. The paper proposes a newmodel of cooperation that

potentially can reconcile interests of both states andmultinationals,mitigate theopportunism of

bothgroupsandcreateafair,efficientandeffectiveglobaltaxenvironmentforthedigitaleconomy.

Political co-operation assumes an adjustment of behaviour by one actor to actual or expected

preferencesofothersthroughaprocessofnationalpolicycoordination.91Theco-operationcantake

manyforms,includingacommitmenttoacommongoalorasetofprinciplesorrules.

Thispapersuggeststhatinthedigitaleconomystateshavealreadyagreedacommongoal,namely:

the freedom of digital flows of capital, services/products and information. This goal, and the

internationalcommitmentsdesignedtoadvancethisgoal,promotestheinterestsofmultinationals

operating in the digital economy. However, for the better coordination of national tax policies,

91 FormoredetailseeChristopherNoonan,TheEmergingPrinciplesofInternationalCompetitionLaw(Oxford

UniversityPress2008)13-14.

31

statesshouldbeginbyagreeingongeneralprinciplesoftaxationofglobal incomegeneratedinthe

digital economy. The lack of agreement on principles guiding international tax policies has been

discussedbyacademics.92