Key Issues in Oil & Gas Taxation December 5, 2014

Key Issues in Oil & Gas Taxation December 5, 2014.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Key Issues in Oil & Gas TaxationDecember 5, 2014

© 2011 Hein & Associates, LLP. All rights reserved.

Agenda

• General Discussion of Oil and Gas GAAP vs Tax Treatment

– Depletion Differences

– Asset Retirement Obligations (“ARO”)

– Intangible Drilling Costs (“IDC”)

– Domestic Production Activities Deduction (“DPAD”)

• Common Oil & Gas Tax Elections to Consider

• Oil & Gas Partnership K-1’s: Interpretations and Issues

© 2011 Hein & Associates, LLP. All rights reserved.

Methods of accounting

• Two acceptable methods under US GAAP– Successful efforts

• FASB ASC 932

• Activities are segregated into specific projects

• Costs associated with an unsuccessful project are expensed, while costs associated with a commercial discovery of reserves are capitalized

– Full cost• SEC Regulation S-X Rule 4-10

• Activities segregated by cost centers (i.e. – by country)

• Acquisition, exploration and development (successful or not) costs are capitalized

• IFRS Accounting method

© 2011 Hein & Associates, LLP. All rights reserved.

Common GAAP / Tax differences

• Depreciation, depletion, and amortization

• Gain/Loss on sale of assets

• Accretion

• Impairments

• Unrealized hedging gain/loss

• Delay rentals

• Geological & geophysical costs

• Intangible drilling costs

• Dry hole costs

• Plug and abandonment costs

Property Unit

Cost Depletion – Recoverable Reserves – 1/13/97

• Proved developed, proved undeveloped and "probable and prospective" reserves are regularly estimated using methods current in the industry.

• For purposes of computing cost depletion, the taxpayer is required to include all recoverable units of minerals in the total number of recoverable units at the end of the year.

• Recoverable units include both proved reserves (developed and undeveloped) and, under appropriate circumstances, additional reserves.

Property Unit

Cost Depletion – Unit of Property

• IRS seems to be focusing on this issue

• Industry norm is to calculate at well level or DD&A level

• This is not the method outlined in the Code

Successful Efforts

© 2011 Hein & Associates, LLP. All rights reserved.

Successful efforts

• Considered the more conservative method of accounting due to the capitalization policies

• As a general rule, the company should capitalize:– all property acquisition costs,

– all costs of development wells, and

– all costs of exploratory wells, as long as the well found proved reserved

© 2011 Hein & Associates, LLP. All rights reserved.

Successful effortsTypes of costs incurred

• Examples of costs and activities – Geological and geophysical

– Delay rentals

– Maintenance of land and lease records

– Exploratory wells (dry and successful)

– Test wells

– Costs to acquire properties

– Development costs

– Costs associated with surrendered or abandoned leases remain capitalized costs

Full Cost

© 2011 Hein & Associates, LLP. All rights reserved.

Full cost

• Topics– History

– Cost center

– Costs to capitalize

– Amortization

– Interest capitalization

– Ceiling

– Sale

© 2011 Hein & Associates, LLP. All rights reserved.

Full costCost centers

• Capitalized costs are aggregated and amortized by cost centers

– Country by country

© 2011 Hein & Associates, LLP. All rights reserved.

Full costCosts to capitalize

• All costs associated with acquisition, exploration and development activities– Acquisition – costs to acquire land / leases

• Lease costs, lease bonus, legal fees, brokerage fees

– Exploration – costs to explore and research land• Geophysical and seismic (G&G), intangible or tangible costs

– Intangible – ready the drilling site for equipment

– Tangible – actual costs incurred to set up drilling equipment and drilling

– Development – costs to develop a well and site• Further drilling and completion costs of a well for economic reserves, development infrastructure such as

roads, putting pumps in place, gathering costs (pipelines), storage costs (tanks)

– Production – costs to extract production from reserves• Expensed regardless of full cost or successful efforts

• Wages, electricity for pumps

• Internally capitalized costs– Required to be directly associated with acquisition, exploration and development activities

– Cannot capitalize costs associated with production, general corporate overhead or similar

© 2011 Hein & Associates, LLP. All rights reserved.

Full costCosts to capitalize (cont’d)

• Examples of costs and activities – Geological and geophysical

– Delay rentals

– Maintenance of land and lease records

– Exploratory wells (dry and successful)

– Test wells

– Costs to acquire properties

– Development costs

– Costs associated with surrendered or abandoned leases remain capitalized costs

© 2011 Hein & Associates, LLP. All rights reserved.

Full costProperty sales

• Under full cost, generally a gain or loss is not recognized unless the sale significantly alters the relationship between capitalized costs and proved reserves in a cost center

– Removal of capitalized costs if insignificant sale

– 25% threshold• Removal of costs and accumulated depletion in proportion to assets

sold (assuming significant sale)

• Example – Capitalized costs $25MM, accum depletion $10MM, sold 200K BBLs of total 600K BBLs, sale price $12MM

© 2011 Hein & Associates, LLP. All rights reserved.

Full costImpairment

• Proved properties– Ceiling = limitation on capitalized costs

– Given all costs are capitalized, concern arose over costs exceeding the underlying value of the assets

– Calculation performed quarterly for SEC

– Cannot be reversed in subsequent periods

– Regulation S-X Rule 4-10(c)(4) and SAB 113 / SAB topic 12D (pre codification)

– Does take into account the tax impact

• Unproved (unevaluated)– Tested at least annually. If impaired, cost is added to the amortization

pool

Tax Depletion

© 2011 Hein & Associates, LLP. All rights reserved.

Tax Depletion - Cost

• What items do we need to calculate cost depletion?– Production (sold not produced)

– Reserves

– Undepleted Cost Basis (i.e. LHC)

• Is cost depletion ever limited? Do you ever not get the deduction?

– NO, You always get it.

© 2011 Hein & Associates, LLP. All rights reserved.

Tax Depletion - Percentage

• What items do we need to calculate percentage depletion?– Oil and Gas Income

– Oil and Gas Expenses

– Production

– Taxpayer Income/Loss

• Is percentage depletion ever limited? Do you ever not get the deduction?

– Yes.• Income Limitations – Will result in a carryover

• Production Limitations (1000 BBL a day) – Always get in on first 365,000 BBLs

• Type of Business (ie. Not an independent producer)

Oil & Gas Depletion Overview• Types of depletion

– Cost depletion - To compute cost depletion, divide cost of the mineral interest by the estimated recoverable reserves multiplied by the units sold during the tax year, or divide the total of the recoverable units at the end of the year into the units sold during the year. The resulting amount (which represents the portion of the property produced and sold) is then multiplied by the depletable basis in the property

– Statutory “Percentage” Depletion - Generally, percentage depletion is allowable at a rate of 15% of gross income from the property limited to the taxable income from the property. Numerous limitations are applicable to this general allowance based upon the status of the taxpayer, the status of the property, and the overall taxable income of the taxpayer.

Depletion Calculation• Depletion is limited to the greater allowed of Cost

Depletion or Statutory (“Percentage”) Depletion– Cost Depletion is generally computed as cost of the mineral

interest (“Leasehold Costs” or “LHC”)/estimated recoverable reserves x number of units sold during the year

• LHC $1,000,000/ total reserves 10,000,000 x the current year production 10,000 barrels or $1,000

– Statutory or Percentage Depletion is generally computed as 15% of the revenue received limited to income from the property, with other overall limitations

• Revenue $10,000, expenses on the Property $11,000, Depletion is $0

• Revenue $10,000, expenses $5,000, Depletion is $1,500

Depletion Calculation

• If Statutory exceeds Cost, the depletable basis in the property is reduced, but not below zero, by the excess.

• Requirements for Depletion:– Must have Economic Interest;

– Investment must be in the Mineral;

– The Natural Deposit must contain an exhaustible amount of mineral; and

– The mineral must be extracted and actually or constructively sold

Asset Retirement Obligation

© 2011 Hein & Associates, LLP. All rights reserved.

Asset retirement obligation

• An unavoidable cost associated with retiring a long-lived asset that arises as a result of either the acquisition or the normal operation of the asset.

• Asset retirement – Permanent removal from service

• Exploration & production typically includes:– Future dismantlement and removal of production

equipment and facilities

– Restoration and reclamation of the field’s surface to an ecological condition similar to that existing before drilling began

© 2011 Hein & Associates, LLP. All rights reserved.

Asset retirement obligation (cont’d)

• Company estimates the cost to plug and abandon (“P&A”)a well site using today’s dollars

• The estimate is inflated to the future value to an estimated P&A date

• The future value is then discounted back to the present value using a credit-adjusted risk free rate

• Entry is then made to both an asset and liability:

Dr. Asset retirement cost 100

Cr. Asset retirement obligation 100

© 2011 Hein & Associates, LLP. All rights reserved.

Asset retirement obligationSubsequent measurements

• Asset– Successful efforts – included as part of the lease & well

equipment and amortized over remaining proved developed reserves

– Full cost – included with the appropriate cost center and amortized over total proved reserves

• Liability– The liability (at the beginning of the period) is accreted to

the future value using the discount rate applied in the original estimate

© 2011 Hein & Associates, LLP. All rights reserved.

Asset retirement obligation – Example

Year 1: Drill well and put on production. Company estimates the cost to plug & abandon the well is $50,000 and it will occur in 3 years. Company inflates it at 1% to a future value of $51,515. They then discount it back to present value at a credit adjusted risk-free rate of 5% to $46,726.

Year 1 entry:

Dr. Asset retirement cost 46,726

Cr. ARO 46,726

Year 2 entry (Opening ARO x 5%):

Dr. Accretion expense 2,336

Cr. ARO 2,336

Year 3 entry (Opening ARO x 5%):

Dr. Accretion expense 2,453

Cr. ARO 2,453

Plug & abandon the asset:

Dr. ARO 51,515

Cr. Cash 51,515

© 2011 Hein & Associates, LLP. All rights reserved.

Asset retirement obligation – Tax Implications

– The ARO asset is not included in tax basis.

– Cash payment on ARO is a deduction for tax purposes and a timing difference from books

– Accretion is not allowed as and expense for tax purposes.

Intangible Drilling Costs

Intangible Drilling Costs (“IDCs”) – Overview

• What are Intangible Drilling Costs?– Intangible Drilling Costs are expenditures for wages, fuel,

repairs which are incidental to the drilling and preparation of wells for production and do not have any residual(“salvage”) value. (Reg. 1.612-4(a))

Intangible Drilling Costs (“IDCs”) – Overview

• How are they expensed?– The Treasury promulgated regulations granting taxpayer’s

the option of deducting as ordinary and necessary business expenses, the IDC for oil, gas or geothermal wells. This option is restricted to the owner of an operating interest or working interest but only if the owner bears such costs. Therefore, there must be an economic interest in the property for the taxpayer.

– The partnership makes this election• If the partnership fails to make this election, the costs must be

capitalized and depleted.

IDC – Deductibility

• Cash v Accrual– The IRS has ruled that a cash method taxpayer may

deduct prepaid IDC in the year in which it is paid as long as there exists a binding obligation to pay such costs without any form of a refund clause. IDC may be transferred between drilling projects, but not fully refunded. Prepaid IDC is deductible when paid even where the work would be performed in the following year, as long as the advance payments are a requirement of the contract.

IDC – Deductibility

• Cash v Accrual– An accrual method taxpayer may deduct expenditures in

the taxable year in which all of the events have occurred that establish the fact of the liability, the amount can be determined with reasonable accuracy, and economic performance has occurred with respect to the liability.

IDC – Deductibility

• The IRS will view a partnership that allocates more than 35% of its loss to limited partners to be a tax shelter for purposed of timing of deductions. However, the partners may still be able to deduct prepaid IDC’s under certain circumstances:

– The Contact must be payment, not a refundable deposit. It could be applied to another contract if drilling stops, but it must be “irretrievably out of pocket.”

IDC – Deductibility

– Economic performance must occur within 90 days after the close of the taxable year.

• In a prepaid drilling contract, this is having the well spudded

– This is called a “tax shelter,” but not the kind we generally think of or see in the news – No need to disclose.

IDC – Deductibility

• Initial Timing– In view of the uncertainties concerning the taxable year in

which IDC may be deducted, a taxpayer who has not previously exercised the option to deduct such costs would be well advised to make an election in its return for the earliest year in which it could incur an obligation for such costs.

– No official election is required by statute, but in the absence of any IDC to actually deduct it is suggested. Tax returns well in advance of any oil and investment are routinely filed with this as a protective election, amongst others.

IDC – Recapture

• Previously deducted IDC must be recaptured as ordinary income on the disposition of Section 1254 property. It is limited to the lesser of the gain on the property or the amount of Section 1254 costs. This is determined at the partner level.

• Gain from the disposition of an oil and gas property will be reported on K-1 Line 11 code F. Additional information regarding recapture such as IDC passed through to the taxpayer should be included on a separate note.

• It is up to the taxpayer to determine the correct recapture amount based upon the amount of IDC they have expensed, as capitalized IDC is not recaptured until it is amortized or depleted.

What are the AMT Impacts

• When computing the Alternative Minimum Tax impacts of Oil and Gas items, there are several items to consider:

– Excess Intangible Drilling and Development Costs

– Percentage Depletion in Excess of Basis pre-1993

• What are “Excess Intangible Drilling Costs”– The amount deducted that exceeds the deduction that would

have been allowed if the taxpayer capitalized and amortized over 120 months

– Taxpayer incurred $73,421 of IDC on July 1, X2. If the IDC is deducted on the X2 return, the excess IDC is $69,750

• ($73,421- ($73,421/120*6) or $3,671 = $69,750

Excess Intangible Drilling Cost

• The AMT preference is the amount by which the “excess IDCs” paid or incurred exceed 65% for the taxpayer’s net income from the properties for the taxable year, including amortization of IDC, but only the extend that is exceeds 40% of what the preference would have been in prior to 1993 (when the IDC preference was repealed)

• Let’s look at an example:– IDCs incurred $73,421

– Income from properties $31,785

– AMTI before IDC preference $167,763

IDC Preference Item Example2013

IDCs $ 73,421

Amortization of IDCs $ 3,671

Excess IDC $69,750

Income from O&G $31,785

65% of Taxable Income $20,660

Potential IDC Preference $49,090

AMTI before IDC preference $167,763

Tentative IDC preference $49,090

AMTI with Tent. IDC preference $216,852

IDC Preference Reduction @ 40% $ 86,741

Actual IDC Preference -

Allowable IDCs $73,421

*Example for Independent Producers Only

Domestic Production Activities Deduction (“DPAD”)

Section 199 Deduction

• Section 199, Domestic Production Activities Deduction (DPAD) – Line 13T

– Allows for a deduction equal to the percentage of the qualified production activity income (QPAI) for the year. It is limited to 50% of the W-2 wages paid that are allocable to domestic production gross receipts (DPGR). The deduction is normally 9% of the lesser of QPAI or a taxpayers AGI for the year.

– QPAI is gross receipts reduced by cost of goods sold, other expenses, etc. allocated to those receipts. It applies to production from property produced or extracted in the U.S.

– Information required to compute the DPAD should be presented as a footnote under line 13 codes T/U

Section 199 Deduction

• Oil and Gas Nuances– Depletion is allocated. With regard to IDC, there is no

guidance. It may be argued that they are a direct allocation, however it may be argued that they should be indirectly allocated because they are incurred before extraction and are not currently allocable to any receipts.

– Oil and gas activities use a 6% rate for the calculation or 1/3 less than the enacted rate if in a prior year

– The DPAD does not reduce taxable income for the 65% depletion limitation

Common Oil & Gas Tax Elections to Consider

What Elections Should be Considered

• Generally there are a couple of elections that taxpayers must consider when they have investments in oil and gas properties

• These are taxpayer/partner elections that must be made by the partner and the partnership

• First Year Elections – A MUST!!!!!– IDC – in the first year a taxpayer incurred IDC he/she should

make an election to expense them. Absent that, they must capitalize the costs each and every year. No formal election is required, but I suggest you make one.

– The Election - “Taxpayer hereby elects to expense all intangible drilling and development costs of oil and gas wells under the authority of Sec. 263(c) and Reg. Sec. 1.612-(4)(a)”

What Elections Should be Considered

• The Second election to consider is IRC Section 59(e) when the taxpayer wants to capitalize IDCs – Generally for AMT purposes, but not always

• You must have made the initial election 263(C)

• You must have a working interest to deduct IDCs– Attach a statement to the return stating how much the taxpayer is

capitalizing

– Amortize the amount over 5 years

– The amount of IDC that is capitalized in not subject to the AMT preference

– This election is only made at the partner level and if the partner made the expensing election.

• You cannot amend to change your elections

What Elections Should be Made?

• Dry Hole – if you capitalized the IDC and you drill a dry hole

– You can attach an election on your return to expense dry hole costs in the first year you drill a dry hole.

– This is the year the well is completed

• The IRS is bound by these elections, they cannot force a taxpayer to capitalize costs if they elect to expense them.

• Partnership Elections:– 105% Reserve Elections

– Property Elections

Summary of Common Differences

© 2011 Hein & Associates, LLP. All rights reserved.

Summary of common differences

Cost Book Regular Tax AMT

Leasehold Costs Depleted Depleted No Difference

Delay RentalsExpense (Successful Efforts)Depleted (Full Cost method) Depleted with LHC No Difference

IDC/ICC Depleted Expense or Cap over 60 mos.Exp -95% Addback, or Cap - no diff

TDC/TCC Depleted 7 yr MACRS7 yr 150%DDB (when bonus does not apply)

G & G Depleted 2 yr amort No Difference

ARO Accreted Expense when paid No Difference

Oil & Gas Partnership K-1’s:Interpretation and Issues

Agenda

• How to read the Form K-1

• How to analyze the Form K-1 for amounts to determine partnership basis

• How do the passive activity rules apply

• What elections should be considered

• What are the AMT Impacts

Knowing Where to Find Income and Deductions on a Properly Prepared K-1

• 2 Types of K-1 Items– Non Separately Stated Income/Loss

• Activity ordinary in nature

• Not subject to limitations outside of the partnership

• Can be found on Line 1 of the K-1s

– Separately stated items (Intangible Drilling Cost “IDC’s”, DPAD Info)

• Must be reported on the appropriate lines with the corresponding codes

• Listed separately as they may be subject to separate limitations (e.g. Charitable Contributions, Gains/Losses), additional disclosures or require elections to be made outside of the partnership

Knowing Where to Find Income and Deductions on a Property Prepared K-1

Knowing Where to Find Income and Deductions on a Properly Prepared K-1

Non separately stated Items – Line 1

Line 1 Ordinary Income

• Generally Line 1 income/(loss) is all non-rental passive income from a trade or business.

• For an Exploration and Production Company (“E&P”) this is generally going to be all income from the sale of oil and gas, non-royalty, and all ordinary and necessary business expense. It does not include anything that is separately stated or computed at the partner level, i.e.:

– IDCs

– Royalty Income/Expenses (sometimes people include it)

– Depletion

Royalty Activity

* Next to line codes usually denote extra information on attached statements

Royalty Income/Deductions Line 7/13(I)

• Income/Deductions from oil and gas interests that are not working interests are reported here

– Generally a leasing arrangement in which a landowner assigns an interest to an operator is known as the operating mineral interest, working interest (“WI”) or lease. The owner of the WI assumes the burden of developing and operating the premises.

Royalty Income/Deductions Line 7/13(I)

– A "royalty interest" commonly consists of an interest in the underlying oil and gas reserves which is retained when an owner of land grants to another the right to develop the property and produce minerals. A royalty bears no portion of the costs of exploration, development and production. Accordingly, it is referred to as a non-operating mineral interest.

• Examples: Landowner Royalty, Overriding Royalty, Minimum Royalty, Net Profits Interests (Single and Multi-Burden Agreements)

Royalty Income/Deductions Line 7/13(I)

• Royalty Income Line 7– Payments from aforementioned interests

• Deductions connected with the royalty income – Line 13 Code I

– Generally only production taxes

– Most expenses related to these activities will already have been deducted pre-royalty payment

– IDC’s, LOE, Overhead, etc. are not expenses that should be reported by royalty interest owners as they are expenses associated with WI’s.

Royalty Income/Deductions Line 7/13(I)

• Sometimes taxpayers only take percentage depletion, but information can be acquired to determine cost depletion in certain cases

IDC – Line 13 Code J

IDC – Item 13J

• Productive expensed IDC’s under Section 263(c)– Nonproductive IDC’s generally expensed as ordinary

expenses as Dry Hole Costs, if properly elected

• IDC’s reported here are eligible for the 59(e) treatment

– A taxpayer may elect to deduct IDC over a 60 month period beginning in the month in which the IDC was incurred.

– Useful in managing possible AMT liability

DPAD – Line 13 Code T

Usually listed on footnotes in statements due to volume of information provided

Where Else do I look - Footnotes• Generally many valuable pieces of information are

included in the footnotes and not included in the body of the K-1. These include, but are not limited to depletion

• Well prepared K-1’s will include a detailed depletion schedule by taxable unit of property which will show each of the following:

– Revenue by Property

– Expense by Property

– IDC by Property

– Tentative and allowable depletion, before adjustments, by Property

Partnership Oil & Gas Depletion

• Oil & Gas depletion for an independent producer/royalty owner, whether cost or percentage, is computed by each partner and not by the partnership

– Independent producer – taxpayers who are neither retailers nor refiners (Code Sec. 613A(d)). Further defined as producers who do not have more than $5,000,000 in retail sales of oil or gas in a year and who do not refine more that 75,000 barrels of crude oil on any given day during the year.

• Still subject to certain limitations:– 65% of taxable income

– 1,000 E.U. Bbls/day

Partnership Oil & Gas Depletion

• Simulated depletion usually required by partnership agreement for capital account purposes

– The partnership usually will compute tentative depletion for each of its partners, and as such needs to provide the following to it’s partners to substantiate:

• Gross income

• Operating expenses, production taxes, depreciation, and allocated overhead

• Intangible drilling costs (IDC)

• Original share of and subsequent adjustments to the basis in the properties (leasehold costs & accumulated depletion)

– A/D may not be correct due to differences in depletion

Partnership Oil & Gas Depletion

• Estimated reserves; and

• Production in barrels or cubic feet for the tax year from each depletable property

• All of the above items should be reported by taxable unit of property (TUP)

– See partner depletion schedule example

Partner Depletion Schedule Example

Complete Information Disclosure

Partner Depletion Schedule Part 2

Complete Information Disclosure

Partner Depletion Schedule Part 3

Complete Information Disclosure

Insufficient Depletion Information Example

Incomplete Information Disclosure

Partnership Basis

• The taxpayers basis in the partnership will follow the general rules under IRC Section 705

– Basis on Contributed Property, including cash, increased by

• Income allocated – taxable and tax exempt

• Excess of deduction for depletion over the basis of the property subject to depletion (Excess % Depletion)

– Decreased (but not below zero) by distributions; and• Losses allocated

• Non-deductible expenses

• Partners Depletion deduction, but not below zero to the extent it does not exceed the properties basis

Partnership Basis

• Other items to consider in determining Partnership Basis:

– IDCs – since these are deducted at the partner level and not the partnership level, the K-1 will not necessarily represent what has been deducted by the taxpayer.

– Depletion – as stated above, the amounts included on the K-1 are simulated depletion, but that may or may not be what was deducted on the tax return. This may be limited by many factors including capitalized IDCs, taxable income limitation, production limitations or other factors. These need to be considered when computing the taxpayer’s basis in the partnership.

When tax basis is not tax basis

• As a tax preparer, generally you can rely on a K-1 that says the capital account is on tax basis, that it is on a tax basis

• For an Oil and Gas K-1, it might be, but never make that assumption

• Due to the partner level limitations, the K-1 preparer does not know if you expensed or capitalized IDCs or how much depletion the taxpayer has taken.

How do the Passive Loss Rules Apply?

• When determining how much of a loss a taxpayer can take from their oil and gas K-1, they still must consider the two main factors:

– At Risk Rules under IRC Section 465; and

– The Passive Loss Limitation rules under IRC Section 469

• For purposes of this presentation, we will assume that the taxpayer does not have any basis limitation under IRC Section 465

What is Passive

• To determine if the taxpayer is passive, we start with the same base criteria that would apply to other activities. The taxpayer materially participates if he/she meets one of these tests for the year:

– Participates in the activity for more than 500 hours;

– The taxpayer’s activity is substantially all of the participation in the activity by all individuals (including non-owners) for the year;

What is Passive

– The taxpayer participates for more than 100 hours and that isn’t less than the participation of any other person (non-owners)

– The activity is a “significant participation activity” for the tax year and the aggregation of all “significant participation activities” is more than 500 hours

What is Passive

• Material Participation Continued – Non Hours Based– The taxpayer materially participated in the activity for any

5 tax years (does not have to be consecutive) of the last 10 immediately preceding tax years;

– The activity is a personal service activity and the taxpayer materially participated in the activity for any 3 tax years (consecutive or not) before the current tax year

• This one should not matter in our situation

– Facts and circumstances• Not the best one to rely on

Working Interest Exception

• Generally a working interest in not considered a passive activity

• Under IRC Section 469(c)(3)(A) – The term “passive activity” shall not include any working interest in any oil and gas property which the taxpayer holds directly or though an entity which does not limit the liability of the taxpayer with respect to such interest.

– Temp Reg. 1.469(e)(4)(v) clarifies the entities that limit the liability: Limited partnership interest, Corporation, an entity that limits the liability under state law

Working Interest Exception

• Factors that do no limit the liability:– Indemnification agreement;

– Stop loss arrangement;

– Insurance;

– Any similar arrangements (such as a Turnkey Drilling Contract) or

– Any combination of the above

• Conversion of interest– Some partnership agreements will allow the conversion of

a general partnership interest into a limited partnership interest after drilling is completed

– Once the interest is converted, the working interest exception no longer applies to that activity

Conversion of Interest – Can’t Have Your Cake and Eat it Too

• Under the Regulation, once an interest is converted the following limitations apply:

– All future income from the activity is considered active, so it cannot be used to offset other passive losses;

– All future losses will be treated as passive

• Under IRC Section 469(c)(3)(B), it states that “any taxpayer has losses” implying that any future taxpayer that acquired the property would carry over the taint:

– However, the Committee Reports and the Regulations limit the “taint” to the taxpayer who deducted the losses

Master Limited Partnerships

• Generally Master Limited Partnership (“MLPs”) are generally, even if not passive, can only offset the income of THAT MLP. They cannot offset the income of any other entity, even another MLP.

Passive Activities – Royalties and Production Payments

• Generally Royalties are not considered passive unless the related income is derived in the ordinary course of a trade or business

– The Internal Revenue Service (“IRS”) is continuing to develop the criteria of when the royalties are developed in the ordinary course of a trade or business and the temporary regulations do not provide any guidance

– Pending any additional guidance from the IRS, taxpayers cannot treat royalty income as passive without a Private Letter Ruling (“PLR”) from the IRS

• Production Payments– If they are treated as a loan under IRC Section 636 it will

be treated as debt

– If treated as an economic interest, it will be considered a royalty

Where do I find this information?• Line 13j – Section 59(e)(2) Expenditure

– This is the IDC incurred during the tax year

• Line 17d - Include gross receipts from oil and gas activities already included in line 1 only

– It’s not uncommon for gross royalty income to be included here, so be aware of that possibility

• Line 17e – Include deductions connected with oil and gas activities included in line 1 only

– As with 17d, be aware of separately stated deductions being included here

Where do I find this information?Line 17 F – May contain information regarding partnership level Excess IDC

• Footnotes - Should show information to compute IDC preference and depletion information

AMT Items

Other AMT Concerns

• Excess Depletion – Only applies to tax years 1992 and before

• AMT Credit Carryforward– In the past minimization of the AMT liability has been the

main goal when dealing with AMT. If tax rates are expected to increase, accelerating/increasing an AMT liability could be the best tax planning idea.

IDC Adjustment Example

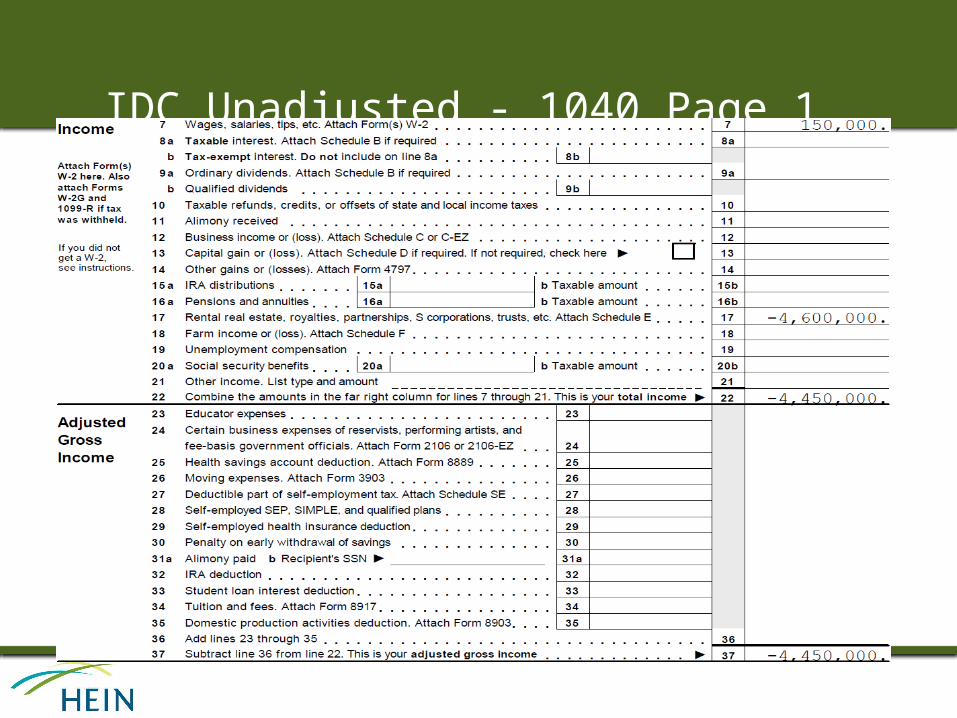

• Assume Individual A incurred, through investment in a partnership, $6,000,000 of intangible drilling and development costs during the year on a well that started producing July 1. Gross income from the well was $1,500,000 and it represented all of A's income from oil and gas for the year. The only expense other than IDC for the property were lease operating expenses of $100,000. Individual A also earned $150,000 of W-2 wages from outside of the partnership.

Source K-1 - Part III

Source K-1 – Depletion Schedule

Source K-1 – Footnotes

IDC Unadjusted - 1040 Page 1

1040 Page 2 – Tax & Credits

Schedule E Part II

Depletion Schedule

6251 - AMT

6251 - AMT

AMT IDC CalculationTotal Expensed IDC

6,000,000

IDC Amortization if Capitalized

300,000

Excess IDC

5,700,000

Gross Receipts from property

1,500,000 Deductions allocable to property (LOE + Amortization of IDC)

400,000

Recalculated Net Income from the property

1,100,000

65% of Recalculated NI from O&G properties

715,000

IDC Tax Preference

4,985,000

*Example for Independent Producers Only

AMTI before tax preference IDC

(4,450,000)

AMTI after tax preference IDC

535,000

40% reduction of IDC preference

214,000

Final AMT IDC preference adjustment

4,771,000

Adjusted AMTI

321,000

IDC Adjusted - 1040 Page 1

1040 Page 2 – Tax & Credits

Schedule E Part II

Depletion Schedule

6251 - AMT

6251 - AMT

AMT IDC ExampleTotal Expensed IDC

760,023

IDC Amortization if Capitalized

38,001

Excess IDC

722,021

Gross Receipts from property

1,500,000 Deductions allocable to property (LOE + Amortization of IDC)

661,999

Recalculated Net Income from the property

838,001

65% of Recalculated NI from O&G properties

544,701

IDC Tax Preference

177,321

*Example for Independent Producers Only

AMTI before tax preference IDC

265,980

AMTI after tax preference IDC

443,300

40% reduction of IDC preference

177,320

Final AMT IDC preference adjustment

1

Adjusted AMTI

265,980

Questions / Comments?

Related Documents