1-1 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Key Concepts and Skills • After studying this chapter, you should be able to: – Determine a firm’s cost of equity capital. – Determine a firm’s cost of debt. – Determine a firm’s overall cost of capital. – Identify some of the pitfalls associated with a firm’s overall cost of capital and what to do about them. 12-2 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1-1

Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Key Concepts and Skills

• After studying this chapter, you should be able to:

– Determine a firm’s cost of equity capital.

– Determine a firm’s cost of debt.

– Determine a firm’s overall cost of capital.

– Identify some of the pitfalls associated with a firm’s overall cost of capital and what to do about them.

12-2Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-2

Chapter Outline

12.1 The Cost of Capital: Some Preliminaries

12.2 The Cost of Equity

12.3 The Costs of Debt and Preferred Stock

12.4 The Weighted Average Cost of Capital

12.5 Divisional and Project Costs of Capital

12.6 Company Valuation with the WACC

12-3Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Cost of Capital Basics

• The cost to a firm for capital funding = the return to the providers of those funds– The return earned on assets depends on

the risk of those assets.

– A firm’s cost of capital indicates how the market views the risk of the firm’s assets.

– A firm must earn at least the required return to compensate investors for the financing

they have provided.

– The required return is the same as the appropriate discount rate.

12-4Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-3

Cost of Equity

• The cost of equity is the return required by equity investors given the risk of the

cash flows from the firm.

• Two major methods for determining the cost of equity

– Dividend growth model

– SML or CAPM

Return to

Quick Quiz

12-5Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

The Dividend Growth Model Approach

Start with the dividend growth model formula and rearrange to solve for RE.

gP

DR

gR

DP

0

1E

E

10

12-6Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-4

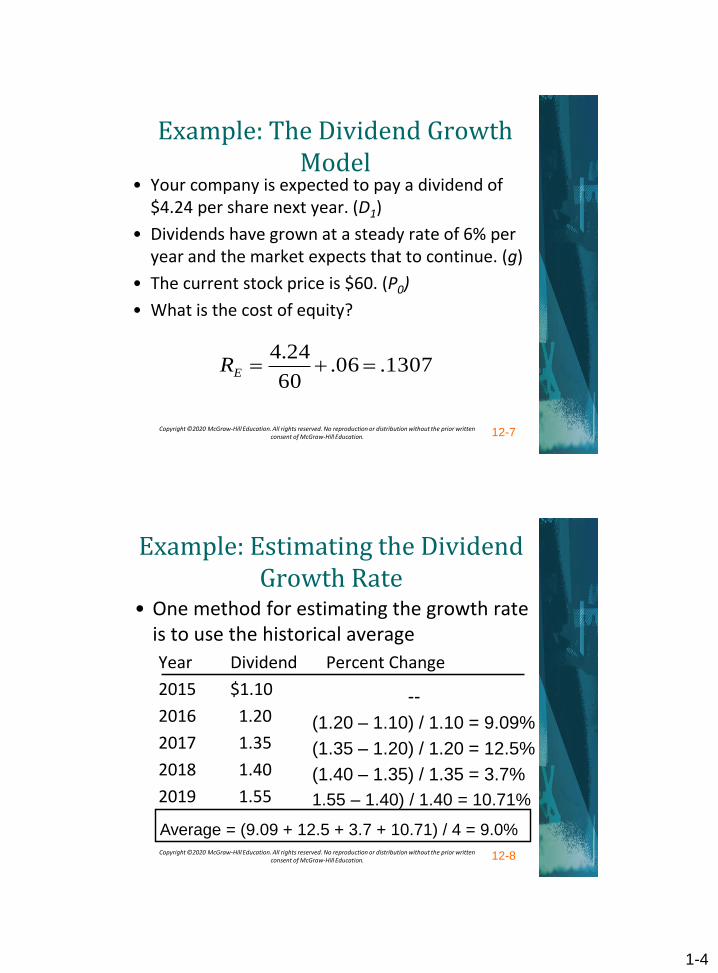

Example: The Dividend Growth Model

• Your company is expected to pay a dividend of $4.24 per share next year. (D1)

• Dividends have grown at a steady rate of 6% per year and the market expects that to continue. (g)

• The current stock price is $60. (P0)

• What is the cost of equity?

1307.06.60

24.4ER

12-7Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Example: Estimating the Dividend Growth Rate

• One method for estimating the growth rate is to use the historical average

Year Dividend Percent Change

2015 $1.10

2016 1.20

2017 1.35

2018 1.40

2019 1.55

--

(1.20 – 1.10) / 1.10 = 9.09%

(1.35 – 1.20) / 1.20 = 12.5%

(1.40 – 1.35) / 1.35 = 3.7%

1.55 – 1.40) / 1.40 = 10.71%

Average = (9.09 + 12.5 + 3.7 + 10.71) / 4 = 9.0%

12-8Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-5

Advantages and Disadvantages of the Dividend Growth Model

• Advantage – easy to understand and use

• Disadvantages

– Only applicable to companies currently paying dividends

– Not applicable if dividends aren’t growing at a reasonably constant rate

– Extremely sensitive to the estimated growth rate

– Does not explicitly consider risk

12-9Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

The SML Approach

• Use the following information to compute the cost of equity

– Risk-free rate, Rf

– Market risk premium, E(RM) – Rf

– Systematic risk of asset, β

Click on this link for further information.

)R)R(E(RR fMEfE

12-10Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-6

Example: SML

• Company’s equity beta = 1.15

• Current risk-free rate = 7%

• Expected market risk premium = 6%

• What is the cost of equity capital?

%95.9)7(15.190.1 ER

12-11Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Advantages and Disadvantages of SML

• Advantages

– Explicitly adjusts for systematic risk

– Applicable to all companies, as long as beta is available

• Disadvantages

– Must estimate the expected market risk premium,

which does vary over time

– Must estimate beta, which also varies over time

– Relies on the past to predict the future, which is not

always reliable

12-12Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-7

Example: Cost of Equity

• Data:– Beta = 1.2 – Market risk premium = 8% – Current risk-free rate = 6%– Analysts’ estimates of growth = 8% per year – Last dividend = $2– Current stock price =$30

– Using SML: RE = 6% + 1.2(8%) = 15.6%

– Using DGM: RE = [2(1.08) / 30] + .08 = 15.2%

12-13Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Cost of Debt

• The cost of debt = the required return on a company’s debt

• Method 1 = Compute the yield to maturity on existing debt

• Method 2 = Use estimates of current rates based on the bond rating expected on new debt

• The cost of debt is NOT the coupon rate.

12-14Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-8

Example: Cost of Debt

Current bond issue:

– 22 years to maturity

– Coupon rate = 7%

– Coupons paid semiannually

– Currently bond price = $960

22*2 N

-960 PV

1000 FV

35 PMT

CPT I/Y 3.685%

YTM = 3.685%*2 = 7.37%

12-15Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Component Cost of Debt

• Use the YTM on the firm’s debt

• Interest is tax deductible, so the after-tax (AT) cost of debt is:

• If the corporate tax rate = 21%:

RD,AT

= RD,BT

(1-TC)

%82.5)21.1%(37.7, ATDRReturn to

Quick Quiz12-16Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

1-9

Cost of Preferred Stock

• Preferred pays a constant dividend every period

• Dividends expected to be paid forever

• Preferred stock is a perpetuity

• Example:

– Preferred annual dividend = $1.25

– Current stock price = $25.85

RP = 1.25 / 25.85 = 4.84%

0

PP

DR

12-17Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Weighted Average Cost of Capital

• Use the individual costs of capital to compute a weighted “average” cost of capital for the firm.

• This “average” = the required return on the firm’s assets, based on the market’s perception of the risk of those assets

• The weights are determined by how much of each type of financing is used. Return to

Quick Quiz

12-18Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-10

Determining the Weights for the WACC

• Weights = percentages of the firm that will be financed by each component

• Always use the target weights, if possible.

– If not available, use market values

12-19Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Capital Structure Weights

• Notation

E = market value of equity

= # outstanding shares times price per share

D = market value of debt

= # outstanding bonds times bond price

V = market value of the firm = D + E

• Weights

E/V = percent financed with equity

D/V = percent financed with debt

Return to

Quick Quiz

12-20Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-11

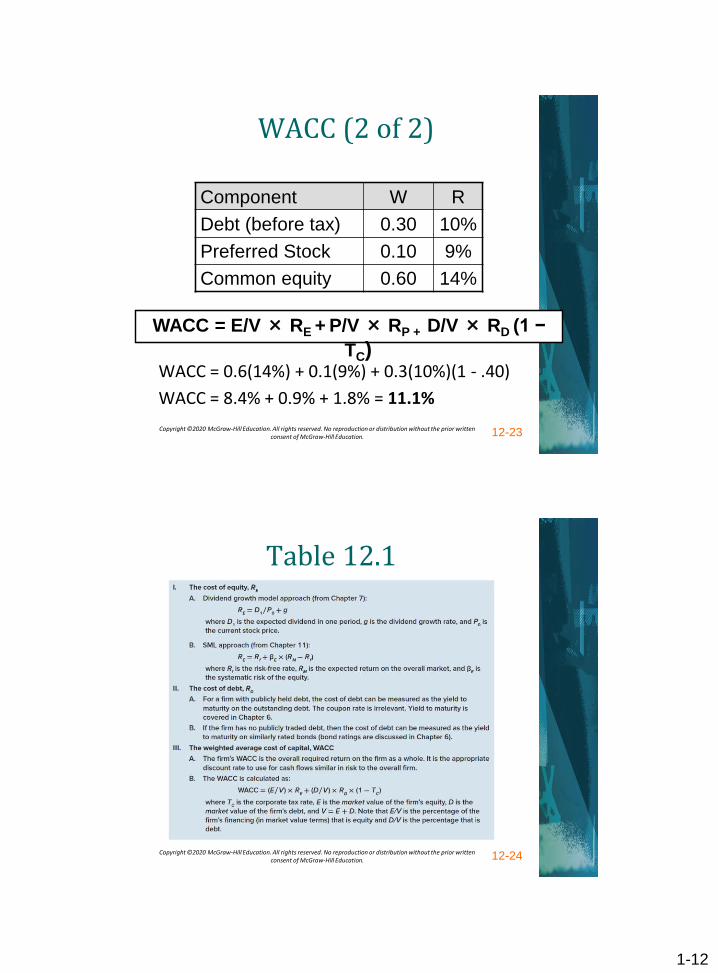

WACC (1 of 2)

WACC = (E/V) x RE + (P/V) x RP + (D/V) x RD x (1- TC)

Where:

(E/V) = % of common equity in capital structure

(P/V) = % of preferred stock in capital structure

(D/V) = % of debt in capital structure

RE = firm’s cost of equity

RP = firm’s cost of preferred stock

RD = firm’s cost of debt

TC = firm’s corporate tax rate

Weights

Component

costs

12-21Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Estimating Weights Given:

• Stock price = $50

• 3m shares common stock

• $25m preferred stock

• $75m debt

• 40% Tax rate

Weights:

E/V = $150/$250 = 0.6 (60%)

P/V = $25/$250 = 0.1 (10%)

D/V = $75/$250 = 0.3 (30%)

Component Values:

• VE = $50 × (3 m) = $150m

• VP = $25m

• VD = $75m

• VF = $150+$25+$75=$250m

12-22Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-12

WACC (2 of 2)

WACC = 0.6(14%) + 0.1(9%) + 0.3(10%)(1 - .40)

WACC = 8.4% + 0.9% + 1.8% = 11.1%

Component W R

Debt (before tax) 0.30 10%

Preferred Stock 0.10 9%

Common equity 0.60 14%

WACC = E/V × RE + P/V × RP + D/V × RD (1 −

TC)

12-23Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Table 12.1

12-24Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-13

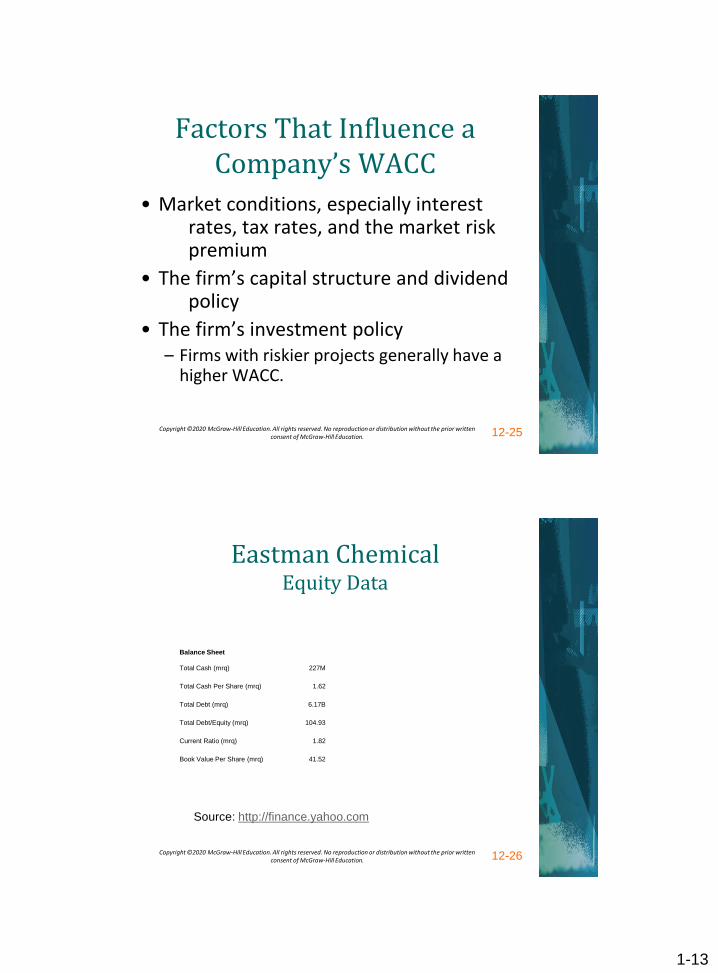

Factors That Influence a Company’s WACC

• Market conditions, especially interest rates, tax rates, and the market risk premium

• The firm’s capital structure and dividend policy

• The firm’s investment policy – Firms with riskier projects generally have a

higher WACC.

12-25Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Eastman ChemicalEquity Data

Source: http://finance.yahoo.com

Balance Sheet

Total Cash (mrq) 227M

Total Cash Per Share (mrq) 1.62

Total Debt (mrq) 6.17B

Total Debt/Equity (mrq) 104.93

Current Ratio (mrq) 1.82

Book Value Per Share (mrq) 41.52

12-26Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-14

Source: http://finance.yahoo.com

12-27Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Eastman ChemicalDividend Growth

Eastman Chemical

Beta and Shares

Outstanding

Source: http://finance.yahoo.com12-28Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

1-15

Eastman ChemicalDividends

Source: http://finance.yahoo.com

Growth Estimates EMN Industry Sector S&P 500Current Qtr. -14.30% N/A N/A -0.01Next Qtr. 7.70% N/A N/A 0.05Current Year 7.00% N/A N/A 0.05Next Year 10.00% N/A N/A 0.11Next 5 Years (per annum) 9.84% N/A N/A 0.10Past 5 Years (per annum) 3.53% N/A N/A N/A

12-29Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Eastman ChemicalCost of Equity—SML

• Beta: Yahoo Finance 0.98

Value Line 1.20

Reuters 1.37

Average of the three is about 1.20

• T-Bill rate = 1.98% (Yahoo Finance bonds section)

• Market Risk Premium = 7% (assumed)

• Cost of Equity (SML) = 1.98% + (7%)(1.20) = 10.38%

)R)R(E(RR fMEfE

12-30Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-16

Eastman Chemical Cost of Equity—DCF

• Growth rate 6.5%

• Last dividend 2.00

• Stock price $98.53

• Cost of Equity (DCF) =

%77.8

065.53.98

)065.1(00.2$

0

1

E

E

E

R

R

gP

DR

12-31Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Eastman Chemical Cost of Equity

Cost of Equity Method Estimated Value

SML 9.69%

DCF 10.17%

Average 9.93%

12-32Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-17

Eastman Chemical Bond Data

Source: http://www.sec.gov

12-33Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Eastman ChemicalCost of Debt

• For Eastman, the cost of debt is similar when using

either book values or market values.

CouponRate

Book Value(in millions)

Percentage of Total

Market Value(in millions)

Percentageof Total

Yield toMaturity Book Values

MarketValues

5.50% $250 .05 $258.39 .05 2.97% .14% .14%2.70 798 .15 793.00 .15 3.12 .46 .464.50 192 .04 192.26 .04 3.49 .12 .133.60 753 .14 750.67 .14 3.68 .51 .511.25 920 .17 817.38 .15 3.72 .63 .577.25 197 .04 230.50 .04 3.85 .14 .177.625 43 .01 50.11 .01 4.45 .04 .043.80 689 .13 682.10 .13 3.97 .51 .507.60 195 .04 242.81 .05 4.20 .15 .194.80 493 .09 490.53 .09 4.84 .44 .444.65 871 .16 853.84 .16 4.78 .77 .76

12-34Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-18

Eastman ChemicalWACC

Capital structure weights (market values):

E = $14.066 billion

D =$5.366 billion

V = $14.066 + 5.366 = 19.432 billion

E/V = 14.066 / 19.432 = .72

D/V = 5.366 / 19.432 = .28

Tax rate (assumed) = 21%

WACC = .72(9.58%) + .28(3.92%)(1 - .21)

= 7.79%

12-35Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Risk-Adjusted WACC

• A firm’s WACC reflects the risk of an

average project undertaken by the firm.

– “Average” risk = the firm’s current

operations

• Different divisions/projects may have

different risks.

– The division’s or project’s WACC should be

adjusted to reflect the appropriate risk and

capital structure. Return to

Quick Quiz

12-36Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-19

Using WACC for All Projects(1 of 2)

• What would happen if we use the WACC for all projects regardless of risk?

• Assume the WACC = 15%

Project

A

B

IRR Project Beta

14% 0.60

16% 1.20

WACC=15%

Reject

Accept

12-37Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Using WACC for All Projects(2 of 2)

• Assume the WACC = 15%

• A project’s required return is calculated using the SML and the project’s Beta.

• Adjusting for risk changes the decisions.

Required

Project IRR Return WACC=15% Risk Adj

A 14% 11.8% Reject Accept

B 16% 16.6% Accept Reject

Decision

12-38Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-20

Divisional Risk & the Cost of Capital

12-39Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Pure Play Approach

• Find one or more companies that specialize in the product or service being considered.

• Compute the beta for each company.

• Take an average.

• Use that beta along with the CAPM to find the appropriate return for a project of that risk.

• Pure play companies can be difficult to find.

Return to

Quick Quiz

12-40Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-21

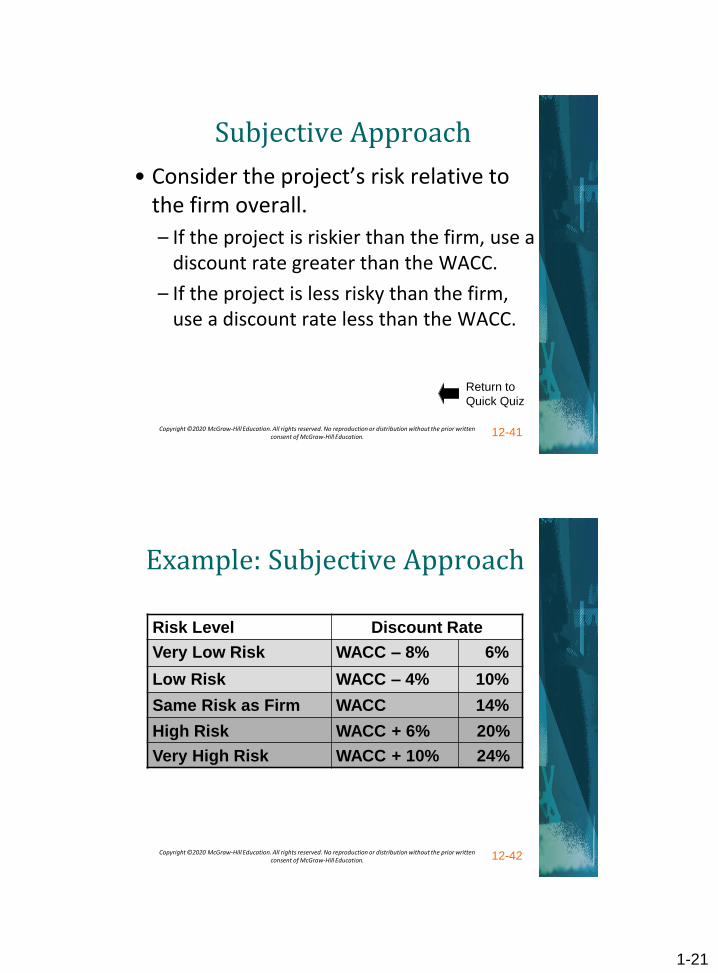

Subjective Approach

• Consider the project’s risk relative to the firm overall.

– If the project is riskier than the firm, use a discount rate greater than the WACC.

– If the project is less risky than the firm, use a discount rate less than the WACC.

Return to

Quick Quiz

12-41Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Example: Subjective Approach

Risk Level Discount Rate

Very Low Risk WACC – 8% 6%

Low Risk WACC – 4% 10%

Same Risk as Firm WACC 14%

High Risk WACC + 6% 20%

Very High Risk WACC + 10% 24%

12-42Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

1-22

Quick Quiz

• What are the two approaches for computing the cost of equity? (Slide 12.5)

• How do you compute the cost of debt and the after tax cost of debt? (Slide 12.16)

• How do you compute the capital structure weights required for the WACC? (Slide 12.20)

• What is the WACC? (Slide 12.18)

• What happens if we use the WACC as the discount rate for all projects? (Slide 12.36)

• What are two methods that can be used to compute the appropriate discount rate when WACC isn’t appropriate? (Slide 12.40 and Slide 12.41)

12-43Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

END

Chapter 12

Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Related Documents