AKD Research [email protected] Weekly Review Connuing its volale trend, the benchmark KSE-100 Index stayed in the red territory this week as well aſter further declining by 2,044pts or -4.68%WoW to close the current week at 41,637 points (lowest level of ongoing calendar year). Rising concerns regarding global growth amid ongoing trade war (US and China) and domesc macroeconomic headwinds were major reasons behind the overall poor performance of the market during the week. However, with the conclusion of Ramadan, average daily traded volumes the at bourse in- creased encouragingly by 29%WoW to 170.07mn shares with 1) KEL (77.01mn shares), 2) POWER (41.48mn shares), 3) TRG (40.12mn shares), 4) LOTCHEM (31.73mn shares) and 5) SMBL (31.31mn shares) leading the board. Major news highlights during the week included: 1) the caretaker FM commented that the amnesty scheme for declaraon of assets will not be extended beyond the Jun 30’18 deadline, 2) country’s current account deficit rising to US$15.961bn in 11MFY18, an increase of 43%YoY, 3) Moody’s Investors Service downgrad- ing Pakistan’s rang outlook to negave from stable, 4) SECP nofying new An- Money Laundering and Countering Financing of Terrorism Regulaons 2018 to sasfy the upcoming FATF meeng and 5) local urea prices posng a sharp increase toward PkR1,600/bag in the last few week amid looming urea shortage in upcoming months. Performance leaders from our AKD universe during the week were: 1) FATIMA (+4.69%WoW), 2) FFC (+2.84%WoW), and 3) EFERT (+1.59%WoW); while laggards included: 1) MLCF (-12.50%WoW), 2) ASTL (- 10.53%WoW), 3) HASCOL (-9.72%WoW), 4) HBL (-9.59%WoW) and 5) LUCK (-7.70%WoW). On the other hand, foreign parcipaon have gone from bad to worse this week with US$24.53mn oulows compared to US$4.45mn oulows in the preceding week. StockSmart AKD Equity Research / Pakistan Pakistan Weekly Update Important disclosures including investment banking relationships and analyst certification at end of this report. AKD Securities does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision. Important disclosures Copyright©2018 AKD Securities Limited. All rights reserved. The information provided on this document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject AKD Securities or its affiliates to any registration requirement within such jurisdiction or country. Neither the information, nor any opinion contained in this document constitutes a solicitation or offer by AKD Securities or its affiliates to buy or sell any securities or provide any investment advice or service. AKD Securities does not warrant the accuracy of the information provided herein. www.akdsecurities.net AKD Securities TREC Holder & Registered Broker Pakistan Stock Exchange REP-108 Find AKD research on Bloomberg (AKDS<GO>), firstcall.com and Reuters Knowledge The eagerly ancipated decision regarding raising oil supply in the OPEC biannual meeng in Vienna happening on Friday (today) will be a key event for the market next week where in- vestors will likely to take direcon from movements in Crude Oil. Moreover, any decision with regards to the review of Pakistan’s acon plan by the FATF in its plenary meeng (scheduled next week from Jun 24-29) can connue to weigh on market senment. Howev- er, value investors can be expected to deploy liquidity to take advantage of aracve valua- ons aſter the sizable decline in share prices witnessed this week. 22 June 2018 Outlook Index & Volume Chart Source: PSX & AKD Research Universe Gainers & Losers 43,683 43,003 42,359 41,637 40,500 41,000 41,500 42,000 42,500 43,000 43,500 44,000 - 50,000 100,000 150,000 200,000 250,000 300,000 19-Jun 20-Jun 21-Jun 22-Jun (Index) (Shrs'000) Ready Volume (LHS) KSE100 Index (RHS) Top- 5 Volume Leaders Symbol Volume (mn) KEL : 77.01 POWER : 41.48 TRG : 40.12 LOTCHEM : 31.73 SMBL : 31.31 Source: PSX & AKD Research Indices KSE-100 KSE-30 This w eek 41,637 20,490 Last w eek 43,681 21,566 Change -4.68% -4.99% Indices KMI-30 Allshare This w eek 70,649 30,152 Last w eek 74,060 31,691 Change -4.60% -4.86% Mkt Cap. PkRbn US$bn This w eek 8,539 70.28 Last w eek 8,978 74.57 Change -4.88% -5.75% Avg. Daily Turnover ('mn shares) This w eek 170.07 Last w eek 131.84 Change 29.00% -14.0% -12.0% -10.0% -8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% FATIMA FFC EFERT APL FFBL LUCK HBL HASCOL ASTL MLCF 37,000 39,000 41,000 43,000 45,000 47,000 0 55 110 165 220 275 330 385 440 495 Jun-17 Aug-17 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Mar-18 May-18 Jun-18 (Index) (share mn) Volume (LHS) KSE-100 Index

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AKD Research [email protected]

Weekly Review

Continuing its volatile trend, the benchmark KSE-100 Index stayed in the red territory this

week as well after further declining by 2,044pts or -4.68%WoW to close the current week at

41,637 points (lowest level of ongoing calendar year). Rising concerns regarding global

growth amid ongoing trade war (US and China) and domestic macroeconomic headwinds

were major reasons behind the overall poor performance of the market during the week.

However, with the conclusion of Ramadan, average daily traded volumes the at bourse in-

creased encouragingly by 29%WoW to 170.07mn shares with 1) KEL (77.01mn shares), 2)

POWER (41.48mn shares), 3) TRG (40.12mn shares), 4) LOTCHEM (31.73mn shares) and 5)

SMBL (31.31mn shares) leading the board. Major news highlights during the week included:

1) the caretaker FM commented that the amnesty scheme for declaration of assets will not

be extended beyond the Jun 30’18 deadline, 2) country’s current account deficit rising to

US$15.961bn in 11MFY18, an increase of 43%YoY, 3) Moody’s Investors Service downgrad-

ing Pakistan’s rating outlook to negative from stable, 4) SECP notifying new Anti- Money

Laundering and Countering Financing of Terrorism Regulations 2018 to satisfy the upcoming

FATF meeting and 5) local urea prices posting a sharp increase toward PkR1,600/bag in the

last few week amid looming urea shortage in upcoming months. Performance leaders from

our AKD universe during the week were: 1) FATIMA (+4.69%WoW), 2) FFC (+2.84%WoW),

and 3) EFERT (+1.59%WoW); while laggards included: 1) MLCF (-12.50%WoW), 2) ASTL (-

10.53%WoW), 3) HASCOL (-9.72%WoW), 4) HBL (-9.59%WoW) and 5) LUCK (-7.70%WoW).

On the other hand, foreign participation have gone from bad to worse this week with

US$24.53mn outflows compared to US$4.45mn outflows in the preceding week.

StockSmart

AKD Equity Research / Pakistan

Pakistan Weekly Update

Important disclosures including investment banking relationships and analyst certification at end of this report. AKD Securities does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Important disclosures

Copyright©2018 AKD Securities Limited. All rights reserved. The information provided on this document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject AKD Securities or its affiliates to any registration requirement within such jurisdiction or country. Neither the information, nor any opinion contained in this document constitutes a solicitation or offer by AKD Securities or its affiliates to buy or sell any securities or provide any investment advice or service. AKD Securities does not warrant the accuracy of the information provided herein.

www.akdsecurities.net

AKD Securities

TREC Holder & Registered Broker

Pakistan Stock Exchange

REP-108

Find AKD research on Bloomberg

(AKDS<GO>), firstcall.com and Reuters Knowledge

The eagerly anticipated decision regarding raising oil supply in the OPEC biannual meeting in Vienna happening on Friday (today) will be a key event for the market next week where in-vestors will likely to take direction from movements in Crude Oil. Moreover, any decision with regards to the review of Pakistan’s action plan by the FATF in its plenary meeting (scheduled next week from Jun 24-29) can continue to weigh on market sentiment. Howev-er, value investors can be expected to deploy liquidity to take advantage of attractive valua-tions after the sizable decline in share prices witnessed this week.

22 June 2018

Outlook

Index & Volume Chart

Source: PSX & AKD Research

Universe Gainers & Losers

43,683

43,003 42,359

41,637

40,500

41,000

41,500

42,000

42,500

43,000

43,500

44,000

-

50,000

100,000

150,000

200,000

250,000

300,000

19-Jun 20-Jun 21-Jun 22-Jun

(Index)(Shrs'000)

Ready Volume (LHS) KSE100 Index (RHS)

Top- 5 Volume Leade rs

Symbol Volume (mn)

KEL : 77.01

POWER : 41.48

TRG : 40.12

LOTCHEM : 31.73

SMBL : 31.31

Source: PSX & AKD Research

Indices KSE-100 KSE-30

This w eek 41,637 20,490

Last w eek 43,681 21,566

Change -4.68% -4.99%

Indices KMI-30 Allshare

This w eek 70,649 30,152

Last w eek 74,060 31,691

Change -4.60% -4.86%

Mkt Cap. PkRbn US$bn

This w eek 8,539 70.28

Last w eek 8,978 74.57

Change -4.88% -5.75%

Avg. Daily Turnover ('mn shares)

This w eek 170.07

Last w eek 131.84

Change 29.00%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

FATI

MA

FFC

EFER

T

AP

L

FFB

L

LUC

K

HBL

HA

SCO

L

AST

L

MLC

F

37,000

39,000

41,000

43,000

45,000

47,000

0

55

110

165

220

275

330

385

440

495

Jun-

17

Au

g-17

Sep

-17

Oct

-17

No

v-1

7

Jan

-18

Feb

-18

Mar

-18

May

-18

Jun-

18

(Index)(share mn)

Volume (LHS) KSE-100 Index

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

This Week’s Daily Reports

2

Jun 21, 2018

Pakistan Economy: CAD remains elevated for May'18, (AKD Daily, Jun 22, 2018)

Current account deficit for May'18 clocked in at US$1.93bn (marginally down 0.7%MoM) vs.

US$1.95bn in the previous month. Rise in trade deficit to US$2.9bn (up 6.7%MoM) for the

month was offset by a rebound in current transfer (up by US$337mn) and uptick in remit-

tance inflows, recorded at US$1.77bn (reflecting growth of 7.3%MoM). Consequently, cur-

rent account for 11MFY18 surged to US$15.96bn (vs. US$11.14bn in comparable period last

year), surpassing the GoP target of US$15.3bn for full year FY18. The rise in CAD is primarily

a function of growing trade deficit recording at US$27.94 (highest ever recorded), as import

growth (+16.4%YoY) outpaced the growth in exports (13.2%YoY) while remittance showed

marginal recovery (up 3.0%YoY). Consequently, SBP's FX reserves sharply fell to US$10.03bn

by May-end (cumulative drawdown of US$6.1bn in 11MFY18) in the absence of any material

inflows. Going forward, external account imbalance is likely to remain persistent in FY19F

with CAD likely to record at 4.95% of GDP (US$16.3bn) considering higher oil imports

(+16.8%YoY in FY19F). This together with chunky debt repayments (FY19F: US$7.5bn) during

the year is expected to push gross external financing gap to US$20.7bn, according to our

estimates.

Pakistan Fertilizers: From export to import, (AKD Daily, Jun 21, 2018)

After exporting more than 500k tons of Urea last year on account of all-time high inventory

levels, the fertilizer sector dynamics are likley to take another turn this year with the indus-

try expecting acute shortage of urea during the later part of CY18. Currently standing at

436k tons in Apr'18 (significantly lower than last 2yr average of 1.5mn tons - equivalent to

just 0.9x of one month's average production), we expect urea inventory to further go down

to extreme levels in the upcoming months owing to: 1) continued high demand in the ongo-

ing kharif season, followed by Rabi season later in Oct-Dec, and 2) lower industry produc-

tion due to closure of LNG based plants (economically infeasible LNG cost) and limited gas

supply. In this regard, MoI is already considering NFML's proposal of importing 0.6mn tons

urea in the current calendar year to meet the expected demand-supply gap. In our view,

this highly probable import scenario presents a lucrative opportunity to local manufacturers

to further increase local urea price which is currently available at ~12-15% discount to pre-

vailing elevated cost of imported fertilizers (higher int'l prices coupled amid sharp currency

depreciation). Having posted a strong recovery (market capitalization is up 13.8% CYTD) on

improving fundamentals, we expect sector to remain in limelight where EFERT (TP of

PkR87.8/sh) remains our top pick on the basis of an attractive dividend yield of ~11%, fol-

lowed by FATIMA (TP of PkR45.1/sh).

BAFL: Valuations catching up, (AKD Daily, Jun 20, 2018)

Despite all the negativity surrounding the banking space in Pakistan, BAFL prominently re-

mains the only bank under our coverage to stand its ground. Depicting consistent funda-

mental improvement, the bank under its new management continues to focus on: 1) im-

proving credit quality, 2) enhancing its non-interest income base and 3) managing its cost

base. More importantly, steps to address the bank's inadequacy on the CAR front, a long

standing concern, have started bearing fruit resulting in CAR enhancement of 1.4ppts in

1QCY18 to 15.1% (Tier-1 capital issue of PkR7bn completed by Mar'18). We feel this move

should allow the bank enough space to maintain its focus on growing its core revenue

stream by tapping into high-yielding segments (ADR in excess of 60% - the highest amongst

peer group) while also being able to maintain dividends particularly when it has not been

designated for additional capital surcharge levy under the new SBP framework. While

BAFL's recent price performance against the sector has narrowed down its valuation dis-

count to B-4 (standing at a negligible 2%/9% on PB/PER levels ex-NBP), its relative immunity

to issues faced by peer banks (limited foreign operations, no pension related expense, high-Source: PSX & AKD Research

Jun 20, 2018

Jun 22, 2018

Jun 19, 2018

41,950

42,005

42,060

42,115

42,170

42,225

42,280

42,335

42,390

42,445

42,500

9:1

5

9:3

8

10:0

2

10:2

5

10:4

9

11:1

2

11:3

6

11:5

9

42,200

42,300

42,400

42,500

42,600

42,700

42,800

42,900

43,000

9:3

0

9:5

3

10:1

7

10:4

0

11:0

4

11:2

7

11:5

1

12:1

4

12:3

8

13:0

1

13:2

5

13:4

8

14:1

2

14:3

5

14:5

9

15:2

3

42,850

42,950

43,050

43,150

43,250

43,350

43,450

43,550

43,650

43,750

9:3

0

9:5

4

10:1

9

10:4

4

11:0

9

11:3

3

11:5

8

12:2

3

12:4

7

13:1

2

13:3

7

14:0

1

14:2

6

14:5

1

15:1

6

43,500

43,533

43,566

43,599

43,632

43,665

43,698

43,731

43,764

43,797

43,830

43,863

9:3

0

9:5

4

10:1

9

10:4

4

11:0

9

11:3

3

11:5

8

12:2

3

12:4

7

13:1

2

13:3

7

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

This Week’s Daily Reports

3

er sensitivity to interest rates) alongwith consistent earnings growth should keep the stock

in limelight. While price performance can take a breather (2QCY18 results to remain subpar

on account of super tax), we advise building positions on dips (TP: PkR52.7/sh).

Pakistan Commodities_May’18 Review, (AKD Daily, Jun 19, 2018)

Pushed up by increasing energy prices, the TRJ commodity index ended 0.43%MoM higher

during May’18. In this regard, major oil benchmarks, WTI/Brent/Arab Lite were up

5.47/7.36/8.19%MoM on Trump renouncing from Iran’s nuclear pact, geopolitical instability

and declining US inventories. The price trend in other major commodities also followed an

upward trend with coal (+9%MoM on strong demand across North Asia and China in partic-

ular with an early summer heatwave driving up electricity demand), urea (+8%MoM on

higher demand commitments from Brazil and Asia) and cotton (+2.2%MoM on account of

renewed buying by China) leading the price chart. Undeterred by the protectionist

measures taken across the world, steel prices have so far remained firm on account of ro-

bust Chinese demand. Going into Jun'18, oil producers meeting (scheduled on Friday, June

22’18) regarding extension of the agreed supply cut holds significant importance with impli-

cations spilling on to overall commodity price trend.

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

4

Commodities

International Major Currencies

Source: Bloomberg

Source: Bloomberg

Major World Indices’ Performance

Source: Bloomberg

TRJ-CRB Index

Source: Bloomberg

PkR/US$ Trend

Source: Bloomberg

Regional Valuations (2018)

Source: Bloomberg & AKD Universe

103.0

104.4

105.8

107.2

108.6

110.0

111.4

112.8

114.2

115.6

117.0

118.4

119.8

121.2

122.6

124.0

Jun-1

7

Jul-17

Aug-1

7

Sep-1

7

Oct-17

Nov-

17

Dec-

17

Jan-1

8

Feb

-18

Mar-

18

Apr-

18

May-

18

SPOT Units 22-Jun-18 14-Jun-18 WoW CYTD

TRJ-CRB Points 195.621 199.0083 -1.70% 0.91%

Nymex (WTI) US$/bbl. 66.5 66.89 -0.58% 10.06%

ICE Brent US$/bbl. 73.93 75.21 -1.70% 10.64%

N. Gas Henry Hub US$/Mmbtu 2.9978 2.9554 1.43% -15.31%

Cotton USd/Pound 93.4 101.45 -7.93% 4.24%

Gold US$/Tr.Oz 1269.62 1302.3 -2.51% -2.57%

Sliver US$/Tr.Oz 16.4175 17.175 -4.41% -3.08%

Copper US$/MT 6788.75 7173 -5.36% -5.80%

Platinum US$/Oz 868.12 904.86 -4.06% -6.70%

Coal US$/MT 104.25 105.9 -1.56% 9.51%

SPOT 22-Jun-18 14-Jun-18 Chg +/- WoW CYTD

Dollar Index 94.595 94.879 -0.284 -0.30% 2.68%

USD/PkR 121.450 121.396 0.054 0.04% 9.96%

USD/JPY 110.160 110.630 -0.470 -0.42% -2.25%

EUR/USD 1.164 1.157 0.007 0.62% -3.04%

GBP/USD 1.328 1.326 0.002 0.13% -1.73%

AUD/USD 0.743 0.748 -0.005 -0.68% -4.89%

NZD/USD 0.690 0.698 -0.007 -1.07% -2.76%

CHF/USD 0.990 0.997 -0.007 -0.69% 1.62%

CAD/USD 1.328 1.311 0.018 1.34% 5.65%

USD/KRW 1,108 1,083 24.500 2.26% 3.45%

CNY/USD 6.498 6.402 0.096 1.50% -0.14%

Country Bloomberg Code 22-Jun-18 14-Jun-18 WoW CYTD

Pakistan KSE100 Index 41,637 43,681 -4.68% 2.9%

Srilanka CSEALL Index 6,228 6,331 -1.63% -2.2%

Thailand SET Index 1,635 1,710 -4.38% -6.8%

Indonesia JCI Index 5,822 5,994 -2.87% -8.4%

Malaysia FBMKLCI Index 1,694 1,762 -3.84% -5.7%

Philippines PCOMP Index 7,063 7,530 -6.19% -17.5%

Vietnam VNINDEX Index 983 1,016 -3.20% -0.1%

Hong Kong HSI Index 29,339 30,440 -3.62% -1.9%

Singapore FSSTI Index 3,287 3,357 -2.07% -3.4%

Brazil IBX Index 28,900 29,457 -1.89% -8.6%

Russia RTSSTD Index 14,902 14,864 0.25% 9.0%

India SENSEX Index 35,690 35,600 0.25% 4.8%

S&P SPX Index 2,750 2,782 -1.18% 2.8%

DJIA INDU Index 24,462 25,175 -2.83% -1.0%

UK UKX Index 7,626 7,766 -1.80% -0.8%

Germany DAX Index 12,564 13,107 -4.15% -2.7%

Qatar DSM Index 8,923 9,098 -1.93% 4.7%

Abu Dhabi ADSMI Index 4,535 4,715 -3.81% 3.1%

Dubai DFMGI Index 2,928 3,038 -3.62% -13.1%

Kuwait KWSEIDX Index 6,633 6,633 0.00% 3.5%

Oman MSM30 Index 4,610 4,596 0.30% -8.7%

Saudi Arabia SASEIDX Index 8,206 8,270 -0.77% 13.5%

MSCI EM MXEF Index 1,080 1,126 -4.04% -6.8%

MSCI FM MXFM Index 573 581 -1.23% -10.1%

EPS Growth PE(x)

Pakistan 16.19% 7.99

Indonesia 9.57% 13.60

Malaysia 11.69% 13.26

Philippines 6.81% 15.27

Vitenam 12.15% 14.41

India 21.00% 15.26

China 13.54% 10.11

% ROE Divd Yld

Pakistan 15.9% 6.43

Indonesia 15.28 2.57

Malaysia 10.44 3.51

Philippines 11.80 1.96

Vitenam 19.07 1.46

India 15.67 1.65

China 12.24 2.92

165

168

171

174

177

180

183

186

189

192

195

198

201

204

207

210

Jun-1

7

Jul-17

Aug-1

7

Sep-1

7

Oct-17

Nov-

17

Dec-

17

Jan-1

8

Feb

-18

Mar-

18

Apr-

18

May-

18

Jun-1

8

5

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

Chart Bank

FIPI Flows for the week

Advance to Decline Ratio

AKD Universe vs. KSE-100 Index

LIPI Flows for the week

Earnings Yield vs. T-Bill (12M) Differential

KSE-100 vs. MSCI-EM & MSCI-FM

-25%-20%-15%-10%

-5%0%5%

10%15%20%25%30%

Jun

-17

Jul-

17

Au

g-17

Sep

-17

No

v-17

Dec

-17

Jan-

18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

KSE100 MSCI EM

MSCI FM

(454)

(2,653)

(11,466)

(9,961)

(14,000)

(12,000)

(10,000)

(8,000)

(6,000)

(4,000)

(2,000)

-

19-Jun-18 20-Jun-18 21-Jun-18 22-Jun-18

(US$'000)

-1.70

-1.30

-0.90

-0.50

-0.10

0.30

0.70

1.10

Jun

-17

Jul-

17

Au

g-17

Au

g-17

Sep

-17

Oct

-17

No

v-17

Dec

-17

Jan-

18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

(%)

Ind., (5.64)

Co., 14.60

Bank/DFI, 1.59 NBFC, 0.10

M.Funds, (5.96)

Ins, 15.21

Others, (0.24)

Prop. Trading , 4.87

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

Jun-1

7

Jul-1

7

Jul-1

7

Aug-1

7

Sep-1

7

Sep-1

7

Oct

-17

Oct

-17

Nov-1

7

Dec-1

7

Dec-1

7

Jan-1

8

Feb

-18

Feb

-18

Ma

r-1

8

Ma

r-1

8

Apr-

18

Ma

y-18

Ma

y-18

Jun-1

8

-32%

-27%

-22%

-17%

-12%

-7%

-2%

3%

8%

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

De

c-1

7

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

KSE-All Share Index AKD Universe

6

AKD Securities Limited StockSmart

Pakistan Weekly Update

Market PER Chart 2018

Source: AKD Research

Market P/BVS Chart 2018

Source: AKD Research

Source: AKD Research

22 June 2018

Jul-0

7

Apr

-08

Jan-

09

Nov

-09

Aug

-10

May

-11

Mar

-12

Dec

-12

Sep-

13

Jul-1

4

Apr

-15

Jan-

16

Nov

-16

Aug

-17

Jun-

18

14.0

10.5

7.0

3.5

(x)

Jul-0

7

Apr

-08

Jan-

09

Nov

-09

Aug

-10

May

-11

Mar

-12

Dec

-12

Sep-

13

Jul-1

4

Apr

-15

Jan-

16

Nov

-16

Aug

-17

Jun-

18

2.5

2.0

1.5

1.0

(x)

AKD Universe Valuations

22-Jun-18 2015 2016 2017 2018F 2019F 2020F

EPS (PkR) 7.15 7.27 6.69 7.56 8.48 10.41

EPS chg (%) (0.88) 1.78 (7.98) 12.98 12.16 22.73

EPS chg (%) ex-E&P 19.34 18.73 (16.62) 10.03 13.67 32.03

Book Value per Share (PkR) 37.20 40.90 44.51 48.33 52.68 58.27

Payout (%) 51.63 49.86 50.21 53.10 51.07 44.44

Valuations

Price to Earnings (x) 8.74 8.58 9.33 8.26 7.36 6.00

PER (ex-E&P) (x) 8.50 7.16 8.58 7.80 6.86 5.20

Price to Book (x) 1.68 1.53 1.40 1.29 1.19 1.07

Price to CF (x) 12.54 9.97 12.13 8.42 8.73 7.47

Earnings Yield (%) 11.45 11.65 10.72 12.11 13.58 16.67

Dividend Yield (%) 5.91 5.81 5.38 6.43 6.94 7.41

EV / EBITDA (x) 6.06 6.45 6.58 6.40 5.69 5.43

Profitability

Return on Equity (%) 19.21 17.79 15.04 15.65 16.10 17.87

Return on Assets (%) 3.96 3.66 2.96 3.10 3.21 3.63

Chg in Sales (%) (8.10) (13.51) 17.47 10.25 11.83 8.59

Gross Margin (%) 28.71 33.02 35.31 35.73 35.52 35.28

Operating Margin (%) 19.51 21.84 25.10 25.73 25.81 25.56

Net Margin (%) 13.47 15.85 12.42 12.73 12.76 14.43

7

AKD Securities Limited StockSmart

Pakistan Weekly Update

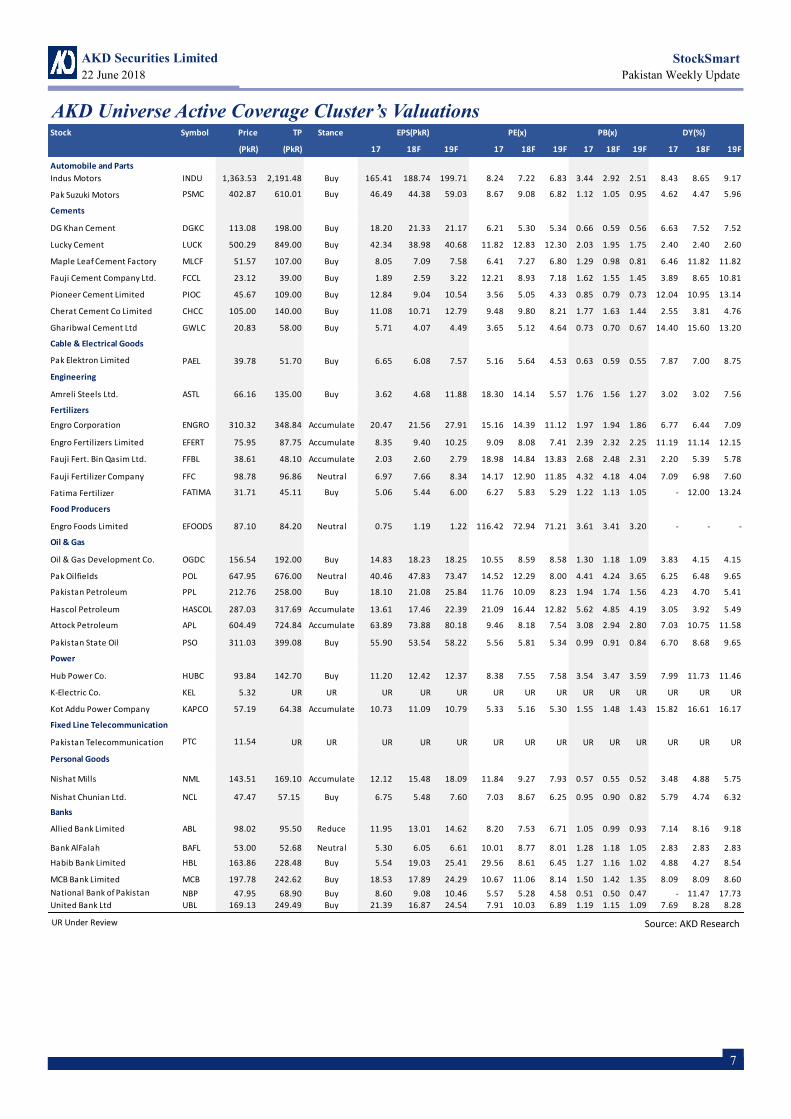

AKD Universe Active Coverage Cluster’s Valuations

22 June 2018

Source: AKD Research UR Under Review

Stock Symbol Price TP Stance EPS(PkR) PE(x) PB(x) DY(%)

(PkR) (PkR) 17 18F 19F 17 18F 19F 17 18F 19F 17 18F 19F

Automobile and Parts

Indus Motors INDU 1,363.53 2,191.48 Buy 165.41 188.74 199.71 8.24 7.22 6.83 3.44 2.92 2.51 8.43 8.65 9.17

Pak Suzuki Motors PSMC 402.87 610.01 Buy 46.49 44.38 59.03 8.67 9.08 6.82 1.12 1.05 0.95 4.62 4.47 5.96

Cements

DG Khan Cement DGKC 113.08 198.00 Buy 18.20 21.33 21.17 6.21 5.30 5.34 0.66 0.59 0.56 6.63 7.52 7.52

Lucky Cement LUCK 500.29 849.00 Buy 42.34 38.98 40.68 11.82 12.83 12.30 2.03 1.95 1.75 2.40 2.40 2.60

Maple Leaf Cement Factory MLCF 51.57 107.00 Buy 8.05 7.09 7.58 6.41 7.27 6.80 1.29 0.98 0.81 6.46 11.82 11.82

Fauji Cement Company Ltd. FCCL 23.12 39.00 Buy 1.89 2.59 3.22 12.21 8.93 7.18 1.62 1.55 1.45 3.89 8.65 10.81

Pioneer Cement Limited PIOC 45.67 109.00 Buy 12.84 9.04 10.54 3.56 5.05 4.33 0.85 0.79 0.73 12.04 10.95 13.14

Cherat Cement Co Limited CHCC 105.00 140.00 Buy 11.08 10.71 12.79 9.48 9.80 8.21 1.77 1.63 1.44 2.55 3.81 4.76

Gharibwal Cement Ltd GWLC 20.83 58.00 Buy 5.71 4.07 4.49 3.65 5.12 4.64 0.73 0.70 0.67 14.40 15.60 13.20

Cable & Electrical Goods

Pak Elektron Limited PAEL 39.78 51.70 Buy 6.65 6.08 7.57 5.16 5.64 4.53 0.63 0.59 0.55 7.87 7.00 8.75

Engineering

Amreli Steels Ltd. ASTL 66.16 135.00 Buy 3.62 4.68 11.88 18.30 14.14 5.57 1.76 1.56 1.27 3.02 3.02 7.56

Fertilizers

Engro Corporation ENGRO 310.32 348.84 Accumulate 20.47 21.56 27.91 15.16 14.39 11.12 1.97 1.94 1.86 6.77 6.44 7.09

Engro Fertilizers Limited EFERT 75.95 87.75 Accumulate 8.35 9.40 10.25 9.09 8.08 7.41 2.39 2.32 2.25 11.19 11.14 12.15

Fauji Fert. Bin Qasim Ltd. FFBL 38.61 48.10 Accumulate 2.03 2.60 2.79 18.98 14.84 13.83 2.68 2.48 2.31 2.20 5.39 5.78

Fauji Fertilizer Company FFC 98.78 96.86 Neutral 6.97 7.66 8.34 14.17 12.90 11.85 4.32 4.18 4.04 7.09 6.98 7.60

Fatima Fertilizer FATIMA 31.71 45.11 Buy 5.06 5.44 6.00 6.27 5.83 5.29 1.22 1.13 1.05 - 12.00 13.24

Food Producers

Engro Foods Limited EFOODS 87.10 84.20 Neutral 0.75 1.19 1.22 116.42 72.94 71.21 3.61 3.41 3.20 - - -

Oil & Gas

Oil & Gas Development Co. OGDC 156.54 192.00 Buy 14.83 18.23 18.25 10.55 8.59 8.58 1.30 1.18 1.09 3.83 4.15 4.15

Pak Oilfields POL 647.95 676.00 Neutral 40.46 47.83 73.47 14.52 12.29 8.00 4.41 4.24 3.65 6.25 6.48 9.65

Pakistan Petroleum PPL 212.76 258.00 Buy 18.10 21.08 25.84 11.76 10.09 8.23 1.94 1.74 1.56 4.23 4.70 5.41

Hascol Petroleum HASCOL 287.03 317.69 Accumulate 13.61 17.46 22.39 21.09 16.44 12.82 5.62 4.85 4.19 3.05 3.92 5.49

Attock Petroleum APL 604.49 724.84 Accumulate 63.89 73.88 80.18 9.46 8.18 7.54 3.08 2.94 2.80 7.03 10.75 11.58

Pakistan State Oil PSO 311.03 399.08 Buy 55.90 53.54 58.22 5.56 5.81 5.34 0.99 0.91 0.84 6.70 8.68 9.65

Power

Hub Power Co. HUBC 93.84 142.70 Buy 11.20 12.42 12.37 8.38 7.55 7.58 3.54 3.47 3.59 7.99 11.73 11.46

K-Electric Co. KEL 5.32 UR UR UR UR UR UR UR UR UR UR UR UR UR UR

Kot Addu Power Company KAPCO 57.19 64.38 Accumulate 10.73 11.09 10.79 5.33 5.16 5.30 1.55 1.48 1.43 15.82 16.61 16.17

Fixed Line Telecommunication

Pakistan Telecommunication PTC 11.54 UR UR UR UR UR UR UR UR UR UR UR UR UR UR

Personal Goods

Nishat Mills NML 143.51 169.10 Accumulate 12.12 15.48 18.09 11.84 9.27 7.93 0.57 0.55 0.52 3.48 4.88 5.75

Nishat Chunian Ltd. NCL 47.47 57.15 Buy 6.75 5.48 7.60 7.03 8.67 6.25 0.95 0.90 0.82 5.79 4.74 6.32

Banks

Allied Bank Limited ABL 98.02 95.50 Reduce 11.95 13.01 14.62 8.20 7.53 6.71 1.05 0.99 0.93 7.14 8.16 9.18

Bank AlFalah BAFL 53.00 52.68 Neutral 5.30 6.05 6.61 10.01 8.77 8.01 1.28 1.18 1.05 2.83 2.83 2.83

Habib Bank Limited HBL 163.86 228.48 Buy 5.54 19.03 25.41 29.56 8.61 6.45 1.27 1.16 1.02 4.88 4.27 8.54

MCB Bank Limited MCB 197.78 242.62 Buy 18.53 17.89 24.29 10.67 11.06 8.14 1.50 1.42 1.35 8.09 8.09 8.60

National Bank of Pakistan NBP 47.95 68.90 Buy 8.60 9.08 10.46 5.57 5.28 4.58 0.51 0.50 0.47 - 11.47 17.73

United Bank Ltd UBL 169.13 249.49 Buy 21.39 16.87 24.54 7.91 10.03 6.89 1.19 1.15 1.09 7.69 8.28 8.28

8

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

AKD Universe Coverage Cluster’s Performance

Source: PSX & AKD Research

Stoc ks Symbol Pric e 1 Ye a r 1 Ye a r

2 2 - Jun- 18 1M 3 M 6 M 12 M CYTD High Low

KSE- 10 0 Inde x 4 1,6 3 7 .3 8 - 2 .6 - 7 .5 2 .6 - 10 .1 2 .9 4 7 ,0 8 4 .3 3 7 ,9 19 .4

Automobile a nd Pa rts

Indus Motors INDU 1363.53 - 16.1 - 22.0 - 22.0 - 25.3 - 18.8 1941.95 1363.53

Pak Suzuki Motors PSMC 402.87 - 12.1 - 16.8 - 20.9 - 48.1 - 19.1 790.43 400.15

Ce me nts

DG Khan Cement DGKC 113.08 - 13.9 - 27.6 - 16.9 - 47.4 - 15.4 215.23 112.74

Lucky Cement LUCK 500.29 - 12.2 - 24.4 - 1.8 - 39.9 - 3.3 844.43 445.80

Maple Leaf Cement Factory MLCF 51.57 - 23.1 - 28.2 - 29.0 - 53.8 - 24.6 118.53 51.57

Fauji Cement Company Ltd. FCCL 23.12 - 10.1 - 18.2 - 16.7 - 45.1 - 7.6 42.14 21.00

Pioneer Cement Limited PIOC 45.67 - 16.5 - 34.8 - 27.1 - 65.1 - 27.6 133.36 45.67

Cherat Cement Limited CHCC 105.00 - 10.6 - 21.6 5.0 - 39.4 - 5.3 178.78 88.50

Gharibwal Cement Limited GWLC 20.83 - 11.1 - 21.8 - 11.8 - 56.8 - 13.6 48.19 19.79

Engine e ring

Amreli Steel Ltd ASTL 66.16 - 15.4 - 29.6 - 31.0 - 48.2 - 28.6 127.69 66.16

Fe rtilize rs

Dawood Hercules DAWH 116.52 - 6.7 - 10.7 - 2.0 - 12.8 4.1 140.30 105.45

Engro Fertilizers Ltd. EFERT 75.95 1.4 11.4 13.8 40.9 12.2 76.73 51.90

Engro Chemical ENGRO 310.32 2.6 1.6 18.8 - 8.1 12.9 339.88 253.43

Fatima Fertilizer FATIMA 31.71 11.2 - 0.2 2.3 - 3.1 2.7 34.05 26.83

Fauji Fert. Bin Qasim Ltd. FFBL 38.61 - 1.0 - 6.1 9.1 - 1.7 8.6 44.81 32.17

Fauji Fertilizer Company FFC 98.78 0.4 11.9 18.6 17.9 24.9 102.02 70.07

Food Produc e rs

Engro Foods Limited EFOODS 87.10 - 9.1 - 10.5 5.6 - 32.1 8.5 134.23 70.19

Ca ble & Ele c tric a l Goods

Pak Elektron Limited PAEL 34.02 - 9.1 - 25.1 - 39.3 - 69.4 - 28.4 111.48 34.02

Oil & Ga s

Oil & Gas Development Co. OGDC 156.54 - 3.6 - 9.1 - 0.8 12.0 - 3.8 177.31 133.69

Pak Oilfields POL 647.95 - 4.0 1.4 4.3 44.1 9.0 707.34 429.75

Pakistan Petroleum Ltd. PPL 212.76 - 0.9 - 0.1 7.6 45.3 3.3 222.96 144.71

Pakistan State Oil PSO 311.03 - 1.6 0.1 - 2.5 - 21.1 6.1 466.59 265.17

Attock Petroleum Ltd. APL 604.49 0.7 5.0 1.8 - 4.6 15.6 703.86 490.02

Hascol Petroleum HASCOL 287.03 - 5.7 6.8 5.1 - 13.3 16.2 348.42 211.63

Powe r

Hub Power Co. HUBC 93.84 - 3.6 - 6.8 - 8.4 - 22.3 3.1 125.88 89.90

K- Electric Limited KEL 5.32 - 13.1 - 15.7 - 9.5 - 24.0 - 15.7 7.46 5.32

Kot Addu Power Company KAPCO 57.19 0.9 - 10.4 - 9.4 - 20.6 6.1 77.44 49.39

Fixe d Line Te le c ommunic a tion

Pakistan Telecommunication PTC 11.54 - 1.6 - 6.7 - 8.1 - 23.6 - 11.6 15.66 11.53

Pe rsona l Goods

Nisaht (Chunian) Ltd. NCL 47.47 - 4.1 - 2.9 2.0 - 4.9 3.7 62.35 44.03

Nishat Mills NML 143.51 6.2 - 11.4 0.3 - 9.1 - 4.0 171.56 130.03

Ba nks

Allied Bank Limited ABL 98.02 1.7 - 0.5 21.6 10.8 15.3 104.31 76.72

Bank AlFalah BAFL 53.00 8.9 2.9 30.9 35.4 24.7 56.61 37.77

Habib Bank Limited HBL 163.86 - 6.5 - 23.7 - 1.3 - 35.3 - 1.9 269.14 152.41

MCB Bank Limited MCB 197.78 - 1.0 - 11.7 - 3.3 - 5.6 - 6.8 236.56 190.43

National Bank of Pakistan NBP 47.95 - 1.7 - 4.5 8.3 - 21.0 - 1.3 62.31 43.01

United Bank Ltd UBL 169.13 - 2.1 - 14.7 - 1.3 - 25.3 - 10.0 235.75 163.40

Absolute Pe rforma nc e (%)

9

AKD Securities Limited

22 June 2018

StockSmart

Pakistan Weekly Update

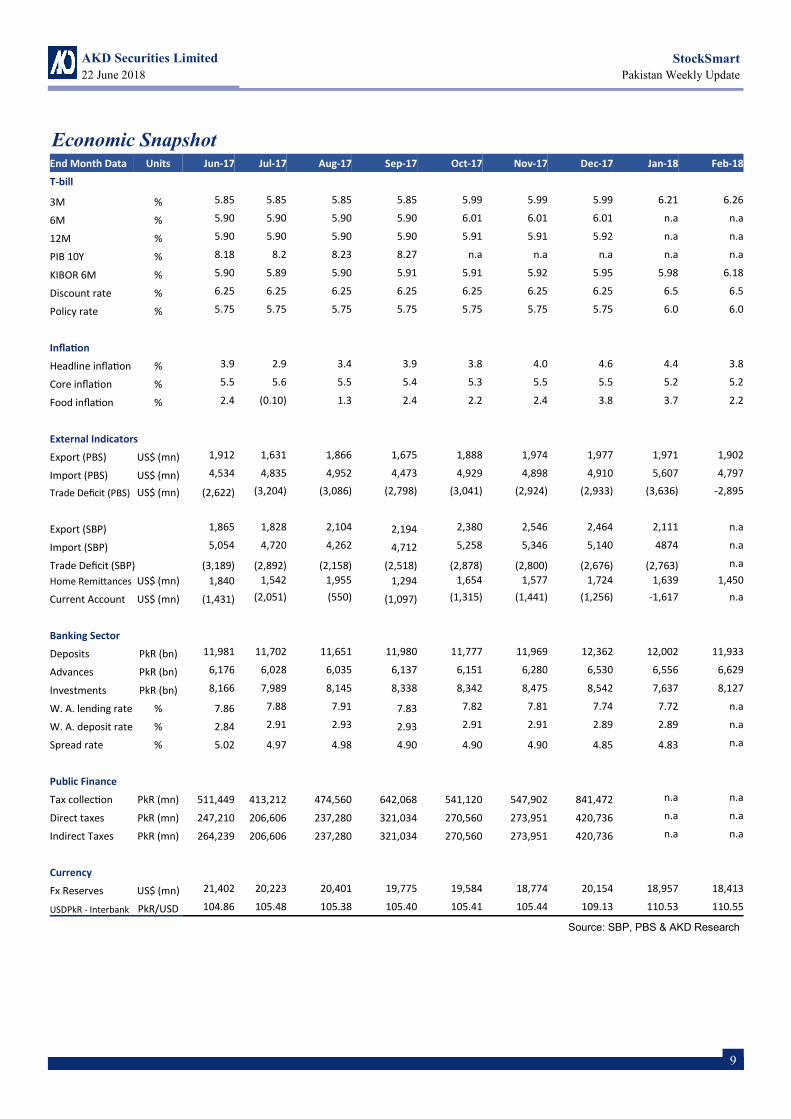

Economic Snapshot

Source: SBP, PBS & AKD Research

End Month Data Units Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18

T-bill

3M % 5.85 5.85 5.85 5.85 5.99 5.99 5.99 6.21 6.26

6M % 5.90 5.90 5.90 5.90 6.01 6.01 6.01 n.a n.a

12M % 5.90 5.90 5.90 5.90 5.91 5.91 5.92 n.a n.a

PIB 10Y % 8.18 8.2 8.23 8.27 n.a n.a n.a n.a n.a

KIBOR 6M % 5.90 5.89 5.90 5.91 5.91 5.92 5.95 5.98 6.18

Discount rate % 6.25 6.25 6.25 6.25 6.25 6.25 6.25 6.5 6.5

Policy rate % 5.75 5.75 5.75 5.75 5.75 5.75 5.75 6.0 6.0

Inflation

Headline inflation % 3.9 2.9 3.4 3.9 3.8 4.0 4.6 4.4 3.8

Core inflation % 5.5 5.6 5.5 5.4 5.3 5.5 5.5 5.2 5.2

Food inflation % 2.4 (0.10) 1.3 2.4 2.2 2.4 3.8 3.7 2.2

External Indicators

Export (PBS) US$ (mn) 1,912 1,631 1,866 1,675 1,888 1,974 1,977 1,971 1,902

Import (PBS) US$ (mn) 4,534 4,835 4,952 4,473 4,929 4,898 4,910 5,607 4,797

Trade Deficit (PBS) US$ (mn) (2,622) (3,204) (3,086) (2,798) (3,041) (2,924) (2,933) (3,636) -2,895

Export (SBP) 1,865 1,828 2,104 2,194 2,380 2,546 2,464 2,111 n.a

Import (SBP) 5,054 4,720 4,262 4,712 5,258 5,346 5,140 4874 n.a

Trade Deficit (SBP) (3,189) (2,892) (2,158) (2,518) (2,878) (2,800) (2,676) (2,763) n.a

Home Remittances US$ (mn) 1,840 1,542 1,955 1,294 1,654 1,577 1,724 1,639 1,450

Current Account US$ (mn) (1,431) (2,051) (550) (1,097) (1,315) (1,441) (1,256) -1,617 n.a

Banking Sector

Deposits PkR (bn) 11,981 11,702 11,651 11,980 11,777 11,969 12,362 12,002 11,933

Advances PkR (bn) 6,176 6,028 6,035 6,137 6,151 6,280 6,530 6,556 6,629

Investments PkR (bn) 8,166 7,989 8,145 8,338 8,342 8,475 8,542 7,637 8,127

W. A. lending rate % 7.86 7.88 7.91 7.83 7.82 7.81 7.74 7.72 n.a

W. A. deposit rate % 2.84 2.91 2.93 2.93 2.91 2.91 2.89 2.89 n.a

Spread rate % 5.02 4.97 4.98 4.90 4.90 4.90 4.85 4.83 n.a

Public Finance

Tax collection PkR (mn) 511,449 413,212 474,560 642,068 541,120 547,902 841,472 n.a n.a

Direct taxes PkR (mn) 247,210 206,606 237,280 321,034 270,560 273,951 420,736 n.a n.a

Indirect Taxes PkR (mn) 264,239 206,606 237,280 321,034 270,560 273,951 420,736 n.a n.a

Currency

Fx Reserves US$ (mn) 21,402 20,223 20,401 19,775 19,584 18,774 20,154 18,957 18,413

USDPkR - Interbank PkR/USD 104.86 105.48 105.38 105.40 105.41 105.44 109.13 110.53 110.55

10

AKD Securities Limited StockSmart

Pakistan Weekly Update

DISCLOSURES & DISCLAIMERS

This publication/communication or any portion hereof may not be reprinted, sold or redistributed without the written consent of AKD Securities Limited. AKD Securities Limited has produced this report for private circulation to professional and institutional clients only. The information, opinions and estimates herein are not directed at, or intended for distribution to or use by, any person or entity in any jurisdiction where doing so would be contrary to law or regulation or which would subject AKD Securities Limited to any additional registration or licensing requirement within such jurisdiction. The information and statistical data herein have been obtained from sources we believe to be reliable and complied by our research department in good faith. Such information has not been independently verified and we make no representation or warranty as to its accuracy, completeness or correctness. Any opinions or estimates herein reflect the judgment of AKD Securities Limited at the date of this publication/ communication and are subject to change at any time without notice.

This report is not a solicitation or any offer to buy or sell any of the securities mentioned herein. It is for information purposes only and is not intended to provide professional, investment or any other type of advice or recommendation and does not take into account the particular invest-ment objectives, financial situation or needs of individual recipients. Before acting on any information in this publication/communication, you should consider whether it is suitable for your particular circumstances and, if appropriate, seek professional advice. Neither AKD Securities Limited nor any of its affiliates or any other person connected with the company accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained therein.

Subject to any applicable laws and regulations, AKD Securities Limited, its affiliates or group companies or individuals connected with AKD Securities Limited may have used the information contained herein before publication and may have positions in, may from time to time pur-chase or sell or have a material interest in any of the securities mentioned or related securities or may currently or in future have or have had a relationship with, or may provide or have provided investment banking, capital markets and/or other services to, the entities referred to herein, their advisors and/or any other connected parties.

AKD Securities Limited (the company) or persons connected with it may from time to time have an investment banking or other relationship, including but not limited to, the participation or investment in commercial banking transaction (including loans) with some or all of the issuers mentioned therein, either for their own account or the account of their customers. Persons connected with the company may provide corporate finance and other services to the issuer of the securities mentioned herein, including the issuance of options on securities mentioned herein or any related investment and may make a purchase and/or sale of the securities or any related investment from time to time in the open market or otherwise, in each case either as principal or agent.

This document is being distributed in the United State solely to "major institutional investors" as defined in Rule 15a-6 under the U.S. Securities Exchange Act of 1934, and may not be furnished to any other person in the United States. Each U.S. person that receives this document by its acceptance hereof represents and agrees that it: is a "major institutional investor", as so defined; and understands the whole document. Any such person wishing to follow-up any of the information should do so by contacting a registered representative of AKD Securities Limited.

The securities discussed in this report may not be eligible for sale in some states in the U.S. or in some countries.

Any recipient, other than a U.S. recipient that wishes further information should contact the company.

This report may not be reproduced, distributed or published, in whole or in part, by any recipient hereof for any purpose.

Analyst Certification We, the AKD Research Team, hereby individually & jointly certify that the views expressed in this research report accurately reflect our personal views about the subject securities and issuers. We also certify that no part of our compensation was, is,or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report. We further certify that we do not have any beneficial holding of the specific securities that we have recommendations on in this report.

AKD Research Team

Analyst Tel no. E-mail Coverage

Umer Pervez +92 111 253 111 (693) [email protected] Executive Director Research & Business Development

Zoya Ahmed +92 111 253 111 (603) [email protected] Banks, Telecoms & Consumers

Haris Imtiaz +92 111 253 111 (639) [email protected] Economy

Ali Asghar Poonawala +92 111 253 111 (646) [email protected] OMCs & Automobiles

Waqas Imdad Ali +92 111 253 111 (634) [email protected] Cements & Fertilizer

M.Daniyal Kanani +92 111 253 111 (602) [email protected] Oil & Gas & Power

Umer Farooq +92 111 253 111 (637) [email protected] Textiles & Steel

Bilal Ahsan Elahi +92 111 253 111 (685) [email protected] Automobiles

Qasim Anwar +92 111 253 111 (680) [email protected] Technical Analysis

Nasir Khan +92 111 253 111 (639) [email protected] Research Production

Tariq Mehmood +92 111 253 111 (643) [email protected] Library Operations

22 June 2018

Related Documents