Taxi wars – Uber and mobile app new entrants Theory and Practice - case study series Oxford, March 2015 Reflections on strategies of mobile app-led and incumbents in the regulated taxi industry www.justinjenk.com www.raktas.ee © Justin Jenk.com. Unauthorised reproduction and use prohibited

Justin jenk theory and practice taxi wars uber_ raktas_case study_march 2015

Jul 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Taxi wars – Uber and mobile app new entrants

Theory and Practice - case study series Oxford, March 2015

Reflections on strategies of mobile app-led and incumbents in the regulated taxi industry

www.justinjenk.com www.raktas.ee

© Justin Jenk.com.

Unauthorised reproduction and use prohibited

1 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Summary: taxi app wars ongoing, but at least one leader - Uber

This document provides a synthetic assessment of the strategies and action of the leading players in the mobile app taxi/rideshare/hailing segment, part of the larger taxi industry – city based and regulated. The contents of this thought paper reflect the work Raktas has provided to relevant decision-makers in the industry.

• The actions of the ‘new entrants’ based on a mobile app business system is a text book example of applying disruption to create value in a regulated and ossified industry (such as with airlines, utilities, telecoms/mobile phones, etc).

• Successful entrants have completed redesigned the whole business system from a user’s perspective to improve cost - quality-time aspects by using technology and digital practices to challenge entrenched regulated behaviors

• The regulated taxi markets are being forced to change as a result.

• With regard to performance. Historically incumbents have generated viable returns but with no growth. New entrants bring the promise of increased volumes and revenues for their businesses; but as yet have not recorded sustainable margins nor returns. Valuations for the successful players are “rich”.

• The process (“war”) is ongoing and while there are some clear winners amongst the new entrants (eg Uber, Lyft) a sustainable industry position has not been reached as yet.

• This development in the taxi industry provides some excellent examples of:

– Interaction of Innovation and Regulation

– Disruptive strategies

– Digital best practice

– Base for proving Nobel Laureate Coase’s social utility at minimal transaction costs (“the Coase Theorem”)

Table of Contents:

p2: Industry setting

pp3-6: Demand aspects and Key Buying Factors (KBFs)

pp7-12: Comparison of strategies and Best practice

pp13-14: Implications & Conclusions

2 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Setting: the industry for taxi services- ripe for change • The mobile app for taxi booking or ridesharing is an emerging, disruptive approach in the highly regulated and entrenched

taxi industry, resistant to change. Through management of the taxi value chain (improved booking, responsiveness, availability and payment) these mobile app companies manage virtual fleets.

• The taxi industry is a monopolistic, highly regulated and ossified one. Licensed taxis (operated by owner-operators) provide metered fares at set rates. Regulations are organized around individual urban markets and subject to local ordinances, practices and politics.

• Current practice being challenged. Often licensed taxis are hailed from the street and fares paid in cash (ie London has 23,000 licensed black cabs, New York City 40,000 medallion yellow cabs.) These fleets are a supplement by radio-taxis and chauffered services (allowing for increased capacity, but requiring booking). Payment methods and fares remain confused.

• The taxi industry is characterized by poor behaviours. Entrenched players provide: poor infrastructure, inefficient booking, pre/post journey delays, poor capacity-supply/demand management, poor service & fulfillment, questionable vehicle quality, (in)experienced drivers, poor CX , high/monopolistic fares, payment confusion, in difficult working conditions.

• To date changes by incumbents have been bolt-ons to existing analogue businesses (eg credit card payments, telephone and computer bookings) but in a haphazard manner.

• Some cities have tried to manage the capacity imbalances (eg: Stockholm with unrestricted pricing; London by increasing the min-cab/radio fleets and seeking to coordinate fleet capacity within its overall public transport authority-TfL; Washington DC with temporary ordinance changes).

• While journey times are invariably similar passenger KBFs are clear: the ability to secure a taxi, waiting times for pickup, journey quality, fares and payment add important quality and time improvement aspects.

• Mobile app-led new entrants have used disruptive strategies are based on challenging established regulations and practices, through redesign of the value offering to enhance consumer utility and value, by applying technology and digital communication practices to improved service levels, margins and engage consumer support to force changes to regulation and industry behaviors. Incumbents have largely relied on legal redress rather than change.

• The two mobile app leaders are: Uber (rapidly scaling an productive commercial model) and; Lyft (leveraging the emerging trend of open-source and sharing to provide a rideshare). Other new entrants are challenged with incumbents are struggling to redesign existing pre-digital businesses.

3 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Demand: travel time is better with taxis/ridesharing

Source: App-based on-demand ride servoices- L Reyle, ”Washington Post”

4 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Demand/Supply: waiting time, a critical KBF that mobile apps meet

Source: App-based on-demand ride servoices- L Reyle, ”Washington Post”

5 © Justin Jenk.com. Unauthorised reproduction and use prohibited

KBFs: mobile taxi/hailing/rideshare apps meet these better

Source: ”Washington Post”, Respsodent survey (n=313) ”What 2 factors are most importnat to you when choosing a taxi or public transport alternative”

6 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Comparison of players: strategy & hard elements

Me-toos

Incumbents

Strategy Lifestyle: Stylish and Improved taxi experience through quality assured process and independent drivers Selected cities (130) Targets aspirant sector

Trade: Facilitates finding a licensed taxi and paying the licensed fare 10 cities

Social: Open source/Sharing through cooperating drivers 60 cities

Serve neighbour-hood/local market

Serve defined local market

Structure Centralized core Service company connecting riders and drivers and facilitating payment Franchised local operations

Centralized core Local partnerships

Centralized core Central admin to coordinate network

Small local/micro companies

Owner operators and small local/micro companies

Systems App based redesign & management of the taxi experience at variable fares taking the rider’s perspective and KBF with pull through communications

App that facilitates participating licensed drivers to connect drivers & riders at standard metered fares

App based rideshare through us e of network of drivers willing to carry passengers at pre-agreed fares

Availability through a phone call and lower price point than licensed/metered cabs

Licensed under current regulations. Set industry prices and base practices

Mobile app taxis meet and exceed clearly defined KBFs for taxi consumers • Key segments • Productive

processes and structure

• Proactive in service provision and pricing

Clear winner

7 © Justin Jenk.com. Unauthorised reproduction and use prohibited

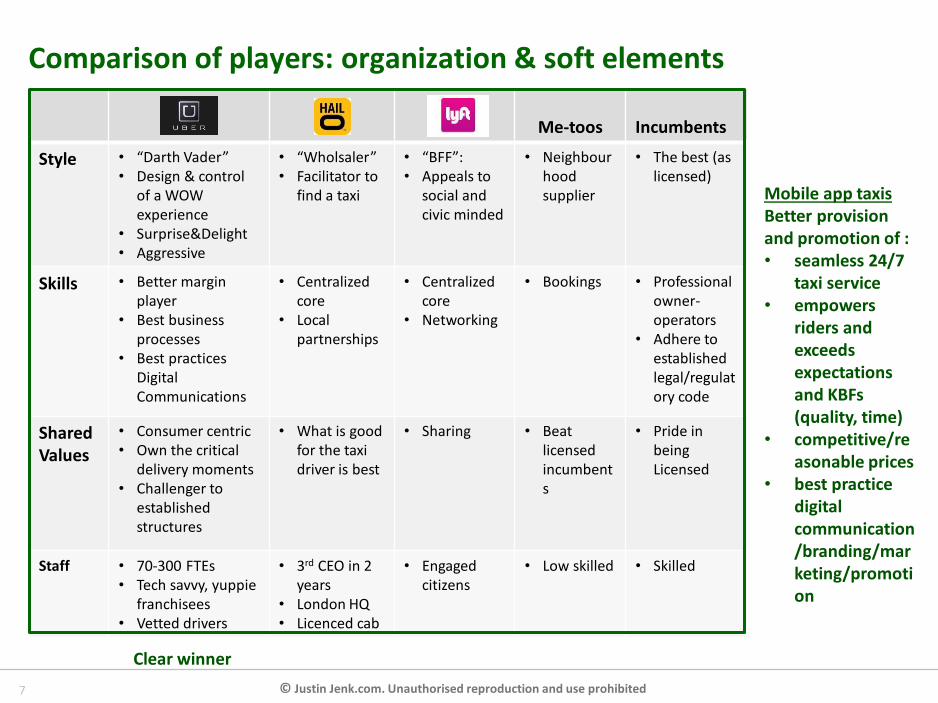

Comparison of players: organization & soft elements

Me-toos

Incumbents

Style • “Darth Vader” • Design & control

of a WOW experience

• Surprise&Delight • Aggressive

• “Wholsaler” • Facilitator to

find a taxi

• “BFF”: • Appeals to

social and civic minded

• Neighbourhood supplier

• The best (as licensed)

Skills • Better margin player

• Best business processes

• Best practices Digital Communications

• Centralized core

• Local partnerships

• Centralized core

• Networking

• Bookings • Professional owner- operators

• Adhere to established legal/regulatory code

Shared Values

• Consumer centric • Own the critical

delivery moments • Challenger to

established structures

• What is good for the taxi driver is best

• Sharing

• Beat licensed incumbents

• Pride in being Licensed

Staff • 70-300 FTEs • Tech savvy, yuppie

franchisees • Vetted drivers

• 3rd CEO in 2 years

• London HQ • Licenced cab

• Engaged citizens

• Low skilled • Skilled

Mobile app taxis Better provision and promotion of : • seamless 24/7

taxi service • empowers

riders and exceeds expectations and KBFs (quality, time)

• competitive/reasonable prices

• best practice digital communication/branding/marketing/promotion

Clear winner

8 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Comparison of players: performance – growth and potential

Me-toos

Incumbents

Metrics • Started 2010 • Fasted growing digital

company (ever) • Largest volume and

revenues increases • 5 cities established,

125 being entered • Off the self systems

• Started 2012 • 10 cities • Change in

systems (Sage to NetSuite)

• Started 2011 • 60 cities • Fast growing

volume and revenues

• Developed with regulated umbrella

• May seek value-add service as upscale chauffeured services (Addison-Lee

• Long established in each city

• Owner-operators

• No growth • Fares set by

regulators

P&L • 80:20 rule • Gross revenues on

target for US$10bn • Targeted net revenues

US$2bn • Strong revenues

growth, negative margins

• Better position for margins

• Centralized core • Local

partnerships • Gross revenues

UK£81m • Net revenues ,

UK£7m ,loss UK£21.5m

• Share of gross revenue

• Net revenues US$2.7m

• Small fleets • Annual

revenues vary US$300k+

• Return>Cost of capital

• US$500 per day revenues

• Annual revenues of US$80-130K

• Returns provide above average income

Funding • Multiple series funding • US$ last round

US$3.7bn • Google Ventures • Post Money US$ 40 bn

valuation

• Multiple series funding

• US$120mn

• Sharing

• Cash flow • Bank loans

• Cash flow • Bank loans

9 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Comparison of US taxi fares: Uber, even with its surge, is cheaper

(Uber’s surges have seen its rates climb to 8x advertised levels during peak demand periods. However even when factored in, Uber remains

cheaper on a motion and time basis)

Source: www..BusinessInsider.com; S. Silverstein

10 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Revenues US$ 27.4 m US$ 2.2m

Users-Riders 1,200,000 170,000

‘Margin’ 4.76% 0.45%

New Riders a month 6,700 1,200

(User behaviour based on 3.8 m credit card holders in the US of which 96,000 have used either Uber of Lyft services, May 2013-April 2014)

Comparison of mobile app taxi players in US: Uber dominates

Source: www.fortune.com, www.futureadvisor.com

11 © Justin Jenk.com. Unauthorised reproduction and use prohibited

TLC cabs

Number of taxis 14,088 13,587

Implied share (40,000 total registered taxis)

35% 34%

Daily rides 29,333 440,000

Rides/taxi/day 2 32

Driver hours/week 40 140

(Uber in just 4 years now has an equal share of market with important implications for future market dynamics (pricing) and its business model of connected single, owner-

operators contrasts vs the Medallion owning taxi companies with multiple drivers with implications to costs, investments and returns)

Local taxi market analysis – NYC: Uber well established

Source: Taxi and Limousine Commission, http://www.telegraph.co.uk/technology/news/11485026/Uber-overtakes-New-Yorks-iconic-yellow-cabs.html

12 © Justin Jenk.com. Unauthorised reproduction and use prohibited

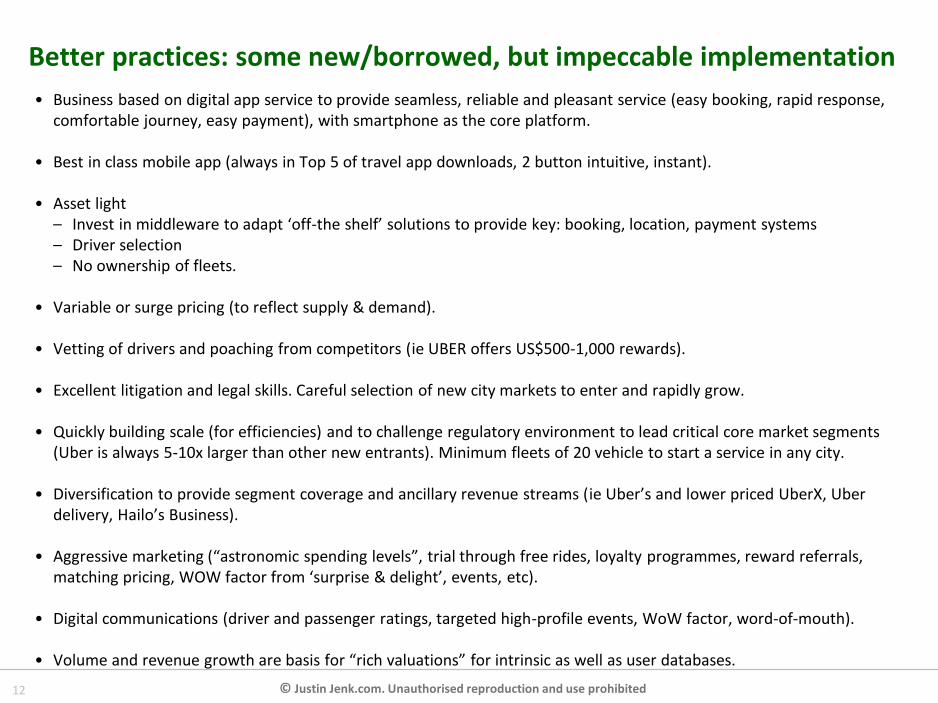

Better practices: some new/borrowed, but impeccable implementation

• Business based on digital app service to provide seamless, reliable and pleasant service (easy booking, rapid response, comfortable journey, easy payment), with smartphone as the core platform.

• Best in class mobile app (always in Top 5 of travel app downloads, 2 button intuitive, instant). • Asset light

– Invest in middleware to adapt ‘off-the shelf’ solutions to provide key: booking, location, payment systems – Driver selection – No ownership of fleets.

• Variable or surge pricing (to reflect supply & demand).

• Vetting of drivers and poaching from competitors (ie UBER offers US$500-1,000 rewards).

• Excellent litigation and legal skills. Careful selection of new city markets to enter and rapidly grow.

• Quickly building scale (for efficiencies) and to challenge regulatory environment to lead critical core market segments (Uber is always 5-10x larger than other new entrants). Minimum fleets of 20 vehicle to start a service in any city.

• Diversification to provide segment coverage and ancillary revenue streams (ie Uber’s and lower priced UberX, Uber

delivery, Hailo’s Business).

• Aggressive marketing (“astronomic spending levels”, trial through free rides, loyalty programmes, reward referrals, matching pricing, WOW factor from ‘surprise & delight’, events, etc).

• Digital communications (driver and passenger ratings, targeted high-profile events, WoW factor, word-of-mouth).

• Volume and revenue growth are basis for “rich valuations” for intrinsic as well as user databases.

13 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Implications: value to being created through successful change • Precedent examples of regulated inefficiencies (ie, airlines, public utilities, telecommunications, etc) provide the opportunity

for commercial change in the taxi industry through disruptive strategies. • Uber is winning the war, but it is not over. • Best practice characterized my using technology and digital methods to create and communicate a business that netter meets

user-KBFs: – Total redesign of user experience based on technology to reduce time-lags and payment frictions – Use UX/CX to pull through demand, challenging existing monopolies and forcing change – Use off the shelf systems but link to create seamless CX – Target and key user occasion/benefits-KBFs – Variable pricing – Use of best practice digital communications and marketing techniques – Scale proven system in supportive city markets

• Legal challenges remain at several levels: – Passengers/Riders/Users are legally exposed to safety and insurance issues (as subject to the driver’s coverage) – Incumbents may win legal cases to enforce existing regulatory framework (London, Toronto, Miami) – Municipalities may change regulations that remove disruptors advantage (Cleveland),

• Prices falling: fares for consumers are lower; medallions/permits for licensed are falling • Competitive intensity will leave any future market with a combination of: a clear mobile app as well as for rideshare providers,

reduced number of regulated incumbents, niche positions for cost-driven, me-too fleets. • Key Success factors for Disruptive strategies are met on at least 2 (of 3) points:

1. Clear margin advantage (combination of growth in revenues and containment of costs & investment) – Uber? 2. Sustainable business and operations advantage – Uber, Lyft 3. Asymmetry of exit decision: will exits occur to allow for industry consolidation? – Uncertain as yet

• As a business model longer-term rideshare (Lyft), as a concept, may pose real challenge to classical commercial operations (eg Uber).

• On current trajectories valuations for Uber and Lyft seem “rich” but may not be extreme. • This industry provides an excellent example of Nobel Prize Laureate Coase’s “Theorem” providing social utility with minimal

transaction cost. Source: http://mpra.ub.uni-muenchen.de/id/eprint/63206:

14 © Justin Jenk.com. Unauthorised reproduction and use prohibited

Conclusions:

• The “war” is ongoing. • Currently, Uber is best placed to win. • Regulators’ actions can accelerate/decelerate the pace as well as scope of change, which will affect

the prospects of the mobile app-based new entrants. • Taxi industry consolidation is underway (licensed fleets will be trimmed, current incumbents and

‘me-too’s will be most adversely affected, some mobile app companies will gain relevant share of target segments/markets.

• Any new entrant must match Uber/Lyft standards and should only enter in new markets • Incumbents need to overhaul their complete system to compete. • There are many lessons to be derived for companies from the: ongoing development of the taxi

industry, digital business development and precedent deregulated industry examples (eg airlines, public utilities, telecommunications).

about

Raktas: www.raktas.ee

Raktas is a specialist firm that offers growth and restructuring solutions to build businesses as well as transform companies and financial institutions; usually with an implementation component. Services are directed at decision-makers that believe their organizations are facing complex situations and resource constrained.

Justin Jenk: www.justinjenk.com

Justin Jenk is a business professional with extensive, practical experience from a successful career as a manager, advisor, investor and board member. He has an established track-record of delivering value-added solutions. He is a graduate of Oxford and Harvard.

Related Documents